ALLANA RESOURCES in ALLANA POTASH umfirmiert --- Die Äthiopische Potash-Perle - 500 Beiträge pro Seite (Seite 2)

eröffnet am 14.12.09 18:23:35 von

neuester Beitrag 18.02.19 03:09:49 von

neuester Beitrag 18.02.19 03:09:49 von

Beiträge: 864

ID: 1.154.839

ID: 1.154.839

Aufrufe heute: 1

Gesamt: 46.613

Gesamt: 46.613

Aktive User: 0

ISIN: CA0167351026 · WKN: A0YKGZ

0,3950

USD

-3,19 %

-0,0130 USD

Letzter Kurs 25.06.15 Nasdaq OTC

Neuigkeiten

Werte aus der Branche Stahl und Bergbau

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,7000 | +30,77 | |

| 6,1400 | +19,46 | |

| 0,6000 | +16,05 | |

| 291,97 | +11,87 | |

| 0,6255 | +10,71 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 6,6200 | -10,05 | |

| 475,00 | -13,64 | |

| 2.500,00 | -13,79 | |

| 1,6700 | -15,97 | |

| 2,1400 | -45,41 |

Antwort auf Beitrag Nr.: 45.354.867 von Popeye82 am 30.08.13 10:08:28

Meinem ernsten Eindruck nach, den jetzigen Umständen entsprechend, eine recht gute Vereinbarung. Was sagen die Mitstreiter?

Soviel auch dazu dass sich "wohl" keine Majors für Danakhil interessieren(was ich eh wusste dass es falsch war).

Man zeige mit mal eiiiiinen, weiteren, Potash Junior der (schon)so weit wie Allana ist.

Allana Potash Announces Strategic Alliance With ICL, "one of the world's largest fertilizer producers"; Investor Webcast Planned for Thursday, Feb 13, 2014 @8:30 a.m. EST - Feb 12, 2014

www.allanapotash.com/s/News.asp?ReportID=622885

"Allana Potash Corp. (TSX:AAA) ("Allana" or the "Company") announces that it has secured a strategic alliance with ICL, one of the world's largest fertilizer producers, pursuant to which a wholly-owned subsidiary of ICL has entered into a definitive share purchase agreement (the "SPA") with Allana for an aggregate investment of $25 million in units of the Company ("Units") at a price of $0.47 per unit on a private placement basis (the "Offering") with the potential for a total investment of up to $84 million upon full exercise of the warrants comprising part of the Units. In addition, a wholly-owned subsidiary of ICL has entered into an offtake agreement (the "Offtake Agreement") with respect to the Company's Danakhil potash project in Ethiopia (the "Project"). The terms of the SPA also include the provision of technical assistance resources by ICL for the development and operation of the Project. The Unit issue price of $0.47 was determined at a 35% premium to the five day volume weighted average of Allana's market price on the TSX, and at a 45% premium to Allana's closing market price on the TSX, as of December 3, 2013, the date on which Allana and ICL commenced exclusive negotiations with respect to this transaction.

Farhad Abasov, President and CEO of Allana, commented, "We are pleased about our strategic alliance with ICL. This is a significant and defining milestone in our Company's history, paving the path towards the transformation of Allana into a major, global potash producer. This strategic alliance is comprehensive and encompasses three major aspects that are critical to the success of a new potash project: 1) financial support; 2) a take-or-pay offtake; and 3) technical cooperation."

Mr. Abasov added, "ICL has broad experience in, and knowledge of, the global potash market, and in developing large scale potash projects. With ICL as our partner, Allana will benefit from ICL's proven potash production ability to accelerate our development and operational plans. At the same time, with ICL's purchase of our product, Allana will benefit from ICL's existing global and regional marketing and distribution networks. This wide-ranging alliance is transformative for Ethiopia and for East Africa. Both Allana and ICL are committed to expanding fertilizer supply within Africa in support of the farming renaissance that is occurring on the continent."

Mr. Abasov concluded by saying, "We thank the people and governments of Ethiopia and Djibouti for having the foresight to work tirelessly towards this goal with the Company. As agricultural production and fertilizer utilization are on the rise in Africa, I am pleased to introduce our new corporate vision of 'Potash for Africa First'. It is significant to note that both ICL and Allana share this vision for our planned potash production in Dallol. We look forward to working with ICL and developing a world-class project to supply potash to the fast growing African markets for many years to come. Once in production, Danakhil is expected to be one of the world's lowest cash cost potash projects, and I am confident that the alliance with ICL will allow Allana to successfully achieve the operational and commercial targets of the project."

Stefan Borgas, President and CEO of ICL, said, "We are pleased to enter into a strategic alliance with Allana to develop its Danakhil potash project in Ethiopia which will provide potash for Ethiopia and Africa - the market with the highest growth potential in the fertilizer world. Our cooperation with Allana highlights our previously announced strategy to broaden our sources of raw materials worldwide, as well as our intention to deepen and significantly increase our activities in emerging markets such as the African continent. The Danakhil project will allow ICL to add substantial value to Allana through the deployment of production technologies similar to Dead Sea Works. The location of the Danakhil mine will further enable ICL to even better serve our growing customer base in India and South East Asia."

The Project secured environmental approvals in May 2013 and a Mining License in October 2013 and, having gained the cooperation of several major development financing institutions and export credit agencies in mid-2013, the Company is proceeding with its Project financing activities together with ICL. The Project will also provide numerous opportunities for economic and social development for the Afar Region, Ethiopia and Djibouti and the Company will continue to develop its infrastructure and transportation programs in close cooperation with the respective governments.

The Offering

The SPA provides that the Offering shall be completed in two tranches, with the first tranche having closed on the date hereof (the "First Tranche") and the second tranche being subject to the receipt of approval by Allana's shareholders (the "Second Tranche") and other standard closing conditions. Each Unit issued pursuant to the Offering consists of a common share of the Company (a "Common Share"), one and one half Series A Common Share purchase warrants (the "Series A Warrants") and one half of one Series B Common Share purchase warrant (the "Series B Warrants", and collectively with the Series A Warrants, the "Warrants"). Each whole Warrant will be exercisable for one Common Share for a period of 36 months from issuance of the Warrant. Each whole Series A Warrant will be exercisable for a price of $0.54 per Common Share, and each whole Series B Warrant will be exercisable for a price of $0.60 per Common Share.

Pursuant to the First Tranche, the Company issued to ICL 22,577,001 Units for gross proceeds of approximately $10.6 million, following which ICL holds approximately 7.7% of the issued and outstanding Common Shares of Allana on a non-diluted basis and 19.99% of the issued and outstanding Common Shares of Allana on a partially diluted basis.

Subject to receipt of shareholder and regulatory approvals, 30,614,488 Units at a price of $0.47 per Unit for gross proceeds of approximately $14.4 million, will be issued to ICL pursuant to the Second Tranche. In addition, the Company may issue Units to Liberty Metals and Mining Holdings, LLC and/or IFC, in such amount as is required to be issued upon due exercise of their respective pre-emptive rights with respect to the Second Tranche.

The Company plans to use the proceeds from the Offering exclusively to fund the construction of the Project and for other general corporate and working capital purposes related to the advancement of the Project.

The transactions contemplated by the SPA were approved by the independent directors of Allana. As required by the Toronto Stock Exchange ("TSX"), the Company will call a special meeting of its shareholders to be held on or about March 28, 2014 to authorize the issuance of Units pursuant to the Second Tranche. Subject to the receipt of the required shareholder approval, closing of the Second Tranche is anticipated to occur shortly thereafter. Directors and officers of Allana holding an aggregate of 1.4% of the outstanding Common Shares have agreed to vote in favor of the issuance of the Units pursuant to the Second Tranche to ICL.

Effective today, in connection with the closing of the First Tranche, Mr. Yoram Cohen has been appointed to the Board of Directors of Allana. Mr. Cohen joined ICL in 1998 and has served in several global level positions at ICL. He is currently General Manager of ICL Africa and a member of ICL Fertilizers' management team. Previously, he was Senior VP and CFO of ICL Specialty Fertilizers and VP, Business Development, of ICL's Fertilizers and Chemicals business unit. Mr. Cohen has a BA in Economics and Statistics and a MBA from The Hebrew University in Jerusalem. In addition, subject to ICL's investment of an additional $15 million in Allana (for an aggregate investment of $40 million), ICL shall have the right to nominate a second director to Allana's board.

In addition to these director nomination rights, pursuant to the SPA, Allana has granted ICL additional ancillary rights as a part of the strategic alliance, as follows:

From and after the date hereof, and at any time after the date which is twelve months from the date hereof (the "Grace Period") provided ICL beneficially owns securities acquired from Allana representing 7.5% of the fully diluted Common Shares of Allana, ICL will have a right of first refusal on the direct or indirect disposition of Allana's interest in the Project.

Subject to the same minimum equity ownership condition following the Grace Period, ICL has been granted a pre-emptive right pursuant to which ICL has the right to participate in any equity financings of Allana up to the greater of (i) 30% of the aggregate amount of such equity financing and (ii) its then undiluted ownership of Allana Common Shares acquired from treasury (assuming the issuance of the Second Tranche).

ICL has also been granted prospectus qualification rights pursuant to a prospectus qualification rights agreement entered into in conjunction with the First Tranche.

The SPA also provides for the establishment of a technical committee pursuant to which ICL has agreed to provide technical support to the Project.

The Offering remains subject to final approval of the TSX. Closing of Second Tranche of the Offering is expected to occur on or before March 31, 2014 subject to receipt of shareholder approval. In accordance with the SPA, shareholder approval and closing of the Second Tranche must occur prior to April 14, 2014.

The Offtake

The parties have also entered into the Offtake Agreement pursuant to which ICL has agreed to purchase the entire production of the Project up to 1Mtpa with a take-or-pay commitment of ICL on a minimum of 80% of output from the Project. The Offtake Agreement include typical terms and conditions for product supply agreements for global sales and shipments and also provides allowances in time for production ramp-up while maintaining the minimum 80% take-or-pay commitment.

Credit Suisse Securities (Canada), Inc. acted as sole financial advisor to Allana with respect to the strategic alliance.

Admission on the AIM Market

Further to the Company's December 16, 2013 press release, due to the Company's focus on other corporate initiatives, including the ICL strategic alliance, Allana has elected not to pursue an AIM listing at this time.

Investor Webcast

An Investor webcast to review the ICL strategic alliance will be held at 8:30am EST tomorrow, Thursday, February 13, 2014. To participate in the webcast, please go to our website's homepage (www.allanapotash.com) and register by using the link to the webcast registration page at least 10 minutes in advance of the scheduled start time.

About ICL

ICL, a global manufacturer of products based on unique minerals that fulfill humanity's essential needs, primarily in three markets: agriculture, food and engineered materials. The agricultural products that ICL produce help to feed the world's growing population. The potash and phosphates that it mines and manufactures are used as ingredients in fertilizers and serve as an essential component in the pharmaceutical and food additives industries. The food additives that we produce enable people to have greater access to more varied and higher quality food; ICL's water treatment products supply clean water to millions of people as well as industry around the world; and other substances, based on bromine and phosphates help to create energy that is more efficient and environmentally friendly, prevent the spread of forest fires and allow the safe and widespread use of a variety of products and materials. ICL benefits from a broad presence throughout the world and proximity to large markets, including in developing regions. ICL operates within a strategic framework of sustainability that includes a commitment to the environment, support of communities in which ICL's manufacturing operations are located and where its employees live, and a commitment to all its employees, customers, suppliers and other stakeholders.

ICL is a public company whose shares are traded on the Tel Aviv Stock Exchange (TASE:ICL). The company employs around 12,000 people worldwide, and its sales in 2012 totaled $6.5 billion. For more information, visit the company's website at www.icl-group.com

About Allana Potash Corp.

Allana is a publicly traded corporation with a focus on the acquisition and development of potash assets internationally with its major focus on a previously explored potash property in Ethiopia. Allana has secured financial support from three significant strategic investors: ICL, one of the world's largest potash producers, IFC, a member of World Bank Group, and LMM, a member of Liberty Mutual Group. Allana has estimated measured and indicated Sylvinite mineral resources of 327.4 million tonnes of 28.3% KCl; and an estimated inferred Sylvinite mineral resource of 90.8 million tonnes grading 27.8% KCl, In addition, the Project hosts estimated measured and indicated Kainitite mineral resources of 1,150.5 million tonnes at 19.4% KCl, an estimated inferred Kainitite mineral resource of 481.8 million tonnes of 19.8%KCl; estimated measured and indicated Upper Carnallitite mineral resources of 411.3 million tonnes grading 17.3% KCl, estimated inferred Upper Carnallitite mineral resources of 175.5 million tonnes of 16.5% KCl; estimated measured and indicated Lower Carnallitite mineral resources of 557.2 million tonnes of 9.2%KCl, and estimated inferred Lower Carnallitite mineral resources of 369.3 million tonnes grading 7.7% KCl. The foregoing mineral resource estimates are as at April 17, 2013. For more information with respect to the data verification procedures undertaken and the key assumptions, parameters and risks associated with the foregoing estimates, refer to Allana's Technical Report entitled "Resource Update for the Danakhil Potash Deposit, Danakhil Depression, Afar State, Ethiopia" dated effective April 17, 2013 filed under the Company's SEDAR profile at www.sedar.com on August 7, 2013.Allana has approximately 293,501,018 shares outstanding. Allana trades on the Toronto Stock Exchange under the symbol "AAA".

Dr. Peter J. MacLean, Ph.D., P. Geo., Allana's Senior VP Exploration, is the Company's designated Qualified Person and has reviewed and approved the technical information presented in this release.

Allana Potash Corp.

Richard Kelertas

Senior Vice President, Corporate Development

514 717 6256

rkelertas@allanapotash.com "

Zitat von Popeye82:Zitat von Popeye82: Meiner Einschätzung nach müsste Allana unter technischen, wirtschaftlichen und Resourcengesichtspunkten, sowie dem Stadium(in Verhandlung mit Kreditgebern) eines der besten, wenn nicht das Beste Projekt (zumindest von börsennotierten Gesellschaften)haben. Wenn jemand meint dass das übertrieben ist -bitte bessere Projekte nennen. Was ja aber nicht heisst dass es nicht noch andere Gesichtspunkte gäbe.

... Von der Profitabilität ist AAAs Projekt eben noch mindestens 1 Klasse höher(ich denke eher 2) -und da reden wir nur über den Abbau der 1.(von 4) Layer(basierend auf einer Minireserve)!

Israel Chemicals considering potash mine in Ethiopia; Site is cheaper on balance than other places worldwide, closer to company’s main markets - H - Aug 12, 2013

- Yoram Gabison -

www.haaretz.com/business/.premium-1.541051

"Israel Chemicals has been in talks recently with a Canadian listed company Allana Potash about opening a potash mine in Ethiopia.

Allana Potash CEO Farhad Abasov met with ICL senior management in Tel Aviv three weeks ago to seek ICL's participation in the construction of a mine at the Dallol site in Ethiopia's Danakhil Valley, located in the country's northeast.

Allana has already raised $85 million from investors to build the mine, which is expected to yield a million tons of potash annually. The mine site has 182 million tons of proven potash reserves and potential reserves as high as 438 million tons. The mining project will be based on technology in which ICL has particular expertise from its Dead Sea Works, pumping and evaporating brine to extract potash.

ICL commented it regularly examines opportunities for international projects and was seeking to expand its current potash production capacity. However, it cautioned that recent circumstances in the potash market were making new mining projects challenging.

Allana estimates that investment in the mine will reach $642 million, a figure which includes both the mining operation and building the transportation infrastructure to carry the potash from Dankil to the Indian Ocean port of Tadjoura, located in next-door Djibouti. The production costs including haulage to port, are expected to reach $98 per ton, with annual maintenance costs of $26 per ton. (These costs compare with averaging mining costs of $100-$150 million per ton.)

Acquiring either full or partial ownership of the mine in Ethiopia would present several advantages to ICL, which is looking to expand its production capacity in core areas such as potash. The company will be required to return its Dead Sea potash concession to the state in 2030, which will leave the company scrambling to find a replacement for 4 million tons of production capacity for a mineral that provided 63% of its operating profit in 2012.

ICL already holds a 640 square kilometer potash mining concession in Spain's Catalan region. Currently, the company exploits only 64 square kilometers of that concession, but estimates that the site has reserves that would support production of up to 10 million tons of potash per year. However, Ethiopia is closer to two key markets for ICL, China and India. Moreover, the demand for potash in the local African market, which is currently 1 million tons per year, is expected to reach between 5 million and 7 million tons per year by 2020.

The Dallol project has already completed the prospecting stage and pilot production. It also completed a series of operational tests conducted in February 2013 to determine the cost of establishing and operating the mine and to receive the approval of Ethiopia's environmental ministry. Allana has submitted a formal request to the Ethiopian authorities for a mining permit.

The Ethiopian government has also paved most of the highway leading from the Dallol site to the port in Tadjoura, which although belonging to Djibouti, serves as Ethiopia's main Indian Ocean port. "

Meinem ernsten Eindruck nach, den jetzigen Umständen entsprechend, eine recht gute Vereinbarung. Was sagen die Mitstreiter?

Soviel auch dazu dass sich "wohl" keine Majors für Danakhil interessieren(was ich eh wusste dass es falsch war).

Man zeige mit mal eiiiiinen, weiteren, Potash Junior der (schon)so weit wie Allana ist.

Allana Potash Announces Strategic Alliance With ICL, "one of the world's largest fertilizer producers"; Investor Webcast Planned for Thursday, Feb 13, 2014 @8:30 a.m. EST - Feb 12, 2014

www.allanapotash.com/s/News.asp?ReportID=622885

"Allana Potash Corp. (TSX:AAA) ("Allana" or the "Company") announces that it has secured a strategic alliance with ICL, one of the world's largest fertilizer producers, pursuant to which a wholly-owned subsidiary of ICL has entered into a definitive share purchase agreement (the "SPA") with Allana for an aggregate investment of $25 million in units of the Company ("Units") at a price of $0.47 per unit on a private placement basis (the "Offering") with the potential for a total investment of up to $84 million upon full exercise of the warrants comprising part of the Units. In addition, a wholly-owned subsidiary of ICL has entered into an offtake agreement (the "Offtake Agreement") with respect to the Company's Danakhil potash project in Ethiopia (the "Project"). The terms of the SPA also include the provision of technical assistance resources by ICL for the development and operation of the Project. The Unit issue price of $0.47 was determined at a 35% premium to the five day volume weighted average of Allana's market price on the TSX, and at a 45% premium to Allana's closing market price on the TSX, as of December 3, 2013, the date on which Allana and ICL commenced exclusive negotiations with respect to this transaction.

Farhad Abasov, President and CEO of Allana, commented, "We are pleased about our strategic alliance with ICL. This is a significant and defining milestone in our Company's history, paving the path towards the transformation of Allana into a major, global potash producer. This strategic alliance is comprehensive and encompasses three major aspects that are critical to the success of a new potash project: 1) financial support; 2) a take-or-pay offtake; and 3) technical cooperation."

Mr. Abasov added, "ICL has broad experience in, and knowledge of, the global potash market, and in developing large scale potash projects. With ICL as our partner, Allana will benefit from ICL's proven potash production ability to accelerate our development and operational plans. At the same time, with ICL's purchase of our product, Allana will benefit from ICL's existing global and regional marketing and distribution networks. This wide-ranging alliance is transformative for Ethiopia and for East Africa. Both Allana and ICL are committed to expanding fertilizer supply within Africa in support of the farming renaissance that is occurring on the continent."

Mr. Abasov concluded by saying, "We thank the people and governments of Ethiopia and Djibouti for having the foresight to work tirelessly towards this goal with the Company. As agricultural production and fertilizer utilization are on the rise in Africa, I am pleased to introduce our new corporate vision of 'Potash for Africa First'. It is significant to note that both ICL and Allana share this vision for our planned potash production in Dallol. We look forward to working with ICL and developing a world-class project to supply potash to the fast growing African markets for many years to come. Once in production, Danakhil is expected to be one of the world's lowest cash cost potash projects, and I am confident that the alliance with ICL will allow Allana to successfully achieve the operational and commercial targets of the project."

Stefan Borgas, President and CEO of ICL, said, "We are pleased to enter into a strategic alliance with Allana to develop its Danakhil potash project in Ethiopia which will provide potash for Ethiopia and Africa - the market with the highest growth potential in the fertilizer world. Our cooperation with Allana highlights our previously announced strategy to broaden our sources of raw materials worldwide, as well as our intention to deepen and significantly increase our activities in emerging markets such as the African continent. The Danakhil project will allow ICL to add substantial value to Allana through the deployment of production technologies similar to Dead Sea Works. The location of the Danakhil mine will further enable ICL to even better serve our growing customer base in India and South East Asia."

The Project secured environmental approvals in May 2013 and a Mining License in October 2013 and, having gained the cooperation of several major development financing institutions and export credit agencies in mid-2013, the Company is proceeding with its Project financing activities together with ICL. The Project will also provide numerous opportunities for economic and social development for the Afar Region, Ethiopia and Djibouti and the Company will continue to develop its infrastructure and transportation programs in close cooperation with the respective governments.

The Offering

The SPA provides that the Offering shall be completed in two tranches, with the first tranche having closed on the date hereof (the "First Tranche") and the second tranche being subject to the receipt of approval by Allana's shareholders (the "Second Tranche") and other standard closing conditions. Each Unit issued pursuant to the Offering consists of a common share of the Company (a "Common Share"), one and one half Series A Common Share purchase warrants (the "Series A Warrants") and one half of one Series B Common Share purchase warrant (the "Series B Warrants", and collectively with the Series A Warrants, the "Warrants"). Each whole Warrant will be exercisable for one Common Share for a period of 36 months from issuance of the Warrant. Each whole Series A Warrant will be exercisable for a price of $0.54 per Common Share, and each whole Series B Warrant will be exercisable for a price of $0.60 per Common Share.

Pursuant to the First Tranche, the Company issued to ICL 22,577,001 Units for gross proceeds of approximately $10.6 million, following which ICL holds approximately 7.7% of the issued and outstanding Common Shares of Allana on a non-diluted basis and 19.99% of the issued and outstanding Common Shares of Allana on a partially diluted basis.

Subject to receipt of shareholder and regulatory approvals, 30,614,488 Units at a price of $0.47 per Unit for gross proceeds of approximately $14.4 million, will be issued to ICL pursuant to the Second Tranche. In addition, the Company may issue Units to Liberty Metals and Mining Holdings, LLC and/or IFC, in such amount as is required to be issued upon due exercise of their respective pre-emptive rights with respect to the Second Tranche.

The Company plans to use the proceeds from the Offering exclusively to fund the construction of the Project and for other general corporate and working capital purposes related to the advancement of the Project.

The transactions contemplated by the SPA were approved by the independent directors of Allana. As required by the Toronto Stock Exchange ("TSX"), the Company will call a special meeting of its shareholders to be held on or about March 28, 2014 to authorize the issuance of Units pursuant to the Second Tranche. Subject to the receipt of the required shareholder approval, closing of the Second Tranche is anticipated to occur shortly thereafter. Directors and officers of Allana holding an aggregate of 1.4% of the outstanding Common Shares have agreed to vote in favor of the issuance of the Units pursuant to the Second Tranche to ICL.

Effective today, in connection with the closing of the First Tranche, Mr. Yoram Cohen has been appointed to the Board of Directors of Allana. Mr. Cohen joined ICL in 1998 and has served in several global level positions at ICL. He is currently General Manager of ICL Africa and a member of ICL Fertilizers' management team. Previously, he was Senior VP and CFO of ICL Specialty Fertilizers and VP, Business Development, of ICL's Fertilizers and Chemicals business unit. Mr. Cohen has a BA in Economics and Statistics and a MBA from The Hebrew University in Jerusalem. In addition, subject to ICL's investment of an additional $15 million in Allana (for an aggregate investment of $40 million), ICL shall have the right to nominate a second director to Allana's board.

In addition to these director nomination rights, pursuant to the SPA, Allana has granted ICL additional ancillary rights as a part of the strategic alliance, as follows:

From and after the date hereof, and at any time after the date which is twelve months from the date hereof (the "Grace Period") provided ICL beneficially owns securities acquired from Allana representing 7.5% of the fully diluted Common Shares of Allana, ICL will have a right of first refusal on the direct or indirect disposition of Allana's interest in the Project.

Subject to the same minimum equity ownership condition following the Grace Period, ICL has been granted a pre-emptive right pursuant to which ICL has the right to participate in any equity financings of Allana up to the greater of (i) 30% of the aggregate amount of such equity financing and (ii) its then undiluted ownership of Allana Common Shares acquired from treasury (assuming the issuance of the Second Tranche).

ICL has also been granted prospectus qualification rights pursuant to a prospectus qualification rights agreement entered into in conjunction with the First Tranche.

The SPA also provides for the establishment of a technical committee pursuant to which ICL has agreed to provide technical support to the Project.

The Offering remains subject to final approval of the TSX. Closing of Second Tranche of the Offering is expected to occur on or before March 31, 2014 subject to receipt of shareholder approval. In accordance with the SPA, shareholder approval and closing of the Second Tranche must occur prior to April 14, 2014.

The Offtake

The parties have also entered into the Offtake Agreement pursuant to which ICL has agreed to purchase the entire production of the Project up to 1Mtpa with a take-or-pay commitment of ICL on a minimum of 80% of output from the Project. The Offtake Agreement include typical terms and conditions for product supply agreements for global sales and shipments and also provides allowances in time for production ramp-up while maintaining the minimum 80% take-or-pay commitment.

Credit Suisse Securities (Canada), Inc. acted as sole financial advisor to Allana with respect to the strategic alliance.

Admission on the AIM Market

Further to the Company's December 16, 2013 press release, due to the Company's focus on other corporate initiatives, including the ICL strategic alliance, Allana has elected not to pursue an AIM listing at this time.

Investor Webcast

An Investor webcast to review the ICL strategic alliance will be held at 8:30am EST tomorrow, Thursday, February 13, 2014. To participate in the webcast, please go to our website's homepage (www.allanapotash.com) and register by using the link to the webcast registration page at least 10 minutes in advance of the scheduled start time.

About ICL

ICL, a global manufacturer of products based on unique minerals that fulfill humanity's essential needs, primarily in three markets: agriculture, food and engineered materials. The agricultural products that ICL produce help to feed the world's growing population. The potash and phosphates that it mines and manufactures are used as ingredients in fertilizers and serve as an essential component in the pharmaceutical and food additives industries. The food additives that we produce enable people to have greater access to more varied and higher quality food; ICL's water treatment products supply clean water to millions of people as well as industry around the world; and other substances, based on bromine and phosphates help to create energy that is more efficient and environmentally friendly, prevent the spread of forest fires and allow the safe and widespread use of a variety of products and materials. ICL benefits from a broad presence throughout the world and proximity to large markets, including in developing regions. ICL operates within a strategic framework of sustainability that includes a commitment to the environment, support of communities in which ICL's manufacturing operations are located and where its employees live, and a commitment to all its employees, customers, suppliers and other stakeholders.

ICL is a public company whose shares are traded on the Tel Aviv Stock Exchange (TASE:ICL). The company employs around 12,000 people worldwide, and its sales in 2012 totaled $6.5 billion. For more information, visit the company's website at www.icl-group.com

About Allana Potash Corp.

Allana is a publicly traded corporation with a focus on the acquisition and development of potash assets internationally with its major focus on a previously explored potash property in Ethiopia. Allana has secured financial support from three significant strategic investors: ICL, one of the world's largest potash producers, IFC, a member of World Bank Group, and LMM, a member of Liberty Mutual Group. Allana has estimated measured and indicated Sylvinite mineral resources of 327.4 million tonnes of 28.3% KCl; and an estimated inferred Sylvinite mineral resource of 90.8 million tonnes grading 27.8% KCl, In addition, the Project hosts estimated measured and indicated Kainitite mineral resources of 1,150.5 million tonnes at 19.4% KCl, an estimated inferred Kainitite mineral resource of 481.8 million tonnes of 19.8%KCl; estimated measured and indicated Upper Carnallitite mineral resources of 411.3 million tonnes grading 17.3% KCl, estimated inferred Upper Carnallitite mineral resources of 175.5 million tonnes of 16.5% KCl; estimated measured and indicated Lower Carnallitite mineral resources of 557.2 million tonnes of 9.2%KCl, and estimated inferred Lower Carnallitite mineral resources of 369.3 million tonnes grading 7.7% KCl. The foregoing mineral resource estimates are as at April 17, 2013. For more information with respect to the data verification procedures undertaken and the key assumptions, parameters and risks associated with the foregoing estimates, refer to Allana's Technical Report entitled "Resource Update for the Danakhil Potash Deposit, Danakhil Depression, Afar State, Ethiopia" dated effective April 17, 2013 filed under the Company's SEDAR profile at www.sedar.com on August 7, 2013.Allana has approximately 293,501,018 shares outstanding. Allana trades on the Toronto Stock Exchange under the symbol "AAA".

Dr. Peter J. MacLean, Ph.D., P. Geo., Allana's Senior VP Exploration, is the Company's designated Qualified Person and has reviewed and approved the technical information presented in this release.

Allana Potash Corp.

Richard Kelertas

Senior Vice President, Corporate Development

514 717 6256

rkelertas@allanapotash.com "

Die sich abzeichnende Zusammenarbeit mit ICL war einer der Gründe (u.a. auch neben der günstigen Lage und dem erwarteten low cost-Abbau) für meinen Einstieg.

Jetzt haben wir einen umfangreichen financial support, ein take-or-pay offtake und eine technical cooperation.

Der Abschluss dieser Verhandlungen dürften den Kursanstieg der letzten Wochen begründet haben (ärgerlich nur, dass mal wieder einige mehr wussten als die Masse der Privatanleger...).

Grundsätzlich wirkt der Abschluss auf mich positiv. ICL hat ernsthaftes Interesse an uns und haben sich nach meinem Eindruck günstig aber fair eingekauft.

Bin sehr gespannt wie der Markt in den nächsten Wochen reagieren wird.

Jetzt haben wir einen umfangreichen financial support, ein take-or-pay offtake und eine technical cooperation.

Der Abschluss dieser Verhandlungen dürften den Kursanstieg der letzten Wochen begründet haben (ärgerlich nur, dass mal wieder einige mehr wussten als die Masse der Privatanleger...).

Grundsätzlich wirkt der Abschluss auf mich positiv. ICL hat ernsthaftes Interesse an uns und haben sich nach meinem Eindruck günstig aber fair eingekauft.

Bin sehr gespannt wie der Markt in den nächsten Wochen reagieren wird.

Antwort auf Beitrag Nr.: 46.438.667 von tpnl am 13.02.14 07:22:09

Da würde ich mir, fürs erste, nicht zuviel versprechen.

Ich könnte mir sogar vooorstellen dass er "negativ reagiert".

Ich muss zugeben dass ich als es immer mehr Richtung C$0.30 ging die Hosen voll hatte.

Meine (ursprüngliche)Hoooffnung war eigentlich dass eine Finanzierung vielleicht "irgendwo in der Nähe von" C$0.50 durchgeführt werden könnte, Als es dann abwärts ging naja.

(Selbst)verstärkende Abwärtsspiralen(vor aaalem in solch entscheidenden Zeiten) das kann sich ooordentlich "selbst befeuern". Als es (dann)wirklich (wieder)so hoch ging, hatte ich komplett nicht mehr damit gerechnet. Der Grund ist ja jetzt klar. Rückwirkend betrachtet "hätte" ICL aber wohl auch noch Ecke höher zeichnen können.

Ich bin mir nicht sicher wieviel IFC, die anderen (N)GOs, und ähnliche, beisteuern werden, aber eventuell könnte gar nicht mehr soviel Geld benötigt werden. Fürs erste bin ich sehr zufrieden, auuuch dass sie keinen (direkten)Projektanteil abgegeben haben.

Noch ist die Katze nicht im Sack, aber das erste ("nennenswerte")Pottascheprojekt eines Juniors/nicht in der Hand eines Majors seit Ewigkeiten dürfte wesentlich wahrscheinlicher geworden sein.

Gruß

P.

Zitat von tpnl: Bin sehr gespannt wie der Markt in den nächsten Wochen reagieren wird.

Da würde ich mir, fürs erste, nicht zuviel versprechen.

Ich könnte mir sogar vooorstellen dass er "negativ reagiert".

Ich muss zugeben dass ich als es immer mehr Richtung C$0.30 ging die Hosen voll hatte.

Meine (ursprüngliche)Hoooffnung war eigentlich dass eine Finanzierung vielleicht "irgendwo in der Nähe von" C$0.50 durchgeführt werden könnte, Als es dann abwärts ging naja.

(Selbst)verstärkende Abwärtsspiralen(vor aaalem in solch entscheidenden Zeiten) das kann sich ooordentlich "selbst befeuern". Als es (dann)wirklich (wieder)so hoch ging, hatte ich komplett nicht mehr damit gerechnet. Der Grund ist ja jetzt klar. Rückwirkend betrachtet "hätte" ICL aber wohl auch noch Ecke höher zeichnen können.

Ich bin mir nicht sicher wieviel IFC, die anderen (N)GOs, und ähnliche, beisteuern werden, aber eventuell könnte gar nicht mehr soviel Geld benötigt werden. Fürs erste bin ich sehr zufrieden, auuuch dass sie keinen (direkten)Projektanteil abgegeben haben.

Noch ist die Katze nicht im Sack, aber das erste ("nennenswerte")Pottascheprojekt eines Juniors/nicht in der Hand eines Majors seit Ewigkeiten dürfte wesentlich wahrscheinlicher geworden sein.

Gruß

P.

ich teile nicht alles, aber ich denke so schlecht sind seine "Konjunktiv Überlegungen" nicht:

ICL and ALLANA - Ethanbrodie - SH - Feb 13, 2014

www.stockhouse.com/companies/bullboard/t.aaa/allana-potash-c…

"At first, it seemed dissapointing that it was not over the psychological .50c marker. And second, it seemed like not that big of a deal. I was expecting more like 150 mil investment, because we do need as they said 35% equity. I do find it interesting that ICL decided to go into "exclusive talks" when the shareprice was quite low, so now we should be "happy" because of this "premium"

NOW, the more I think of it, the more important tomorows webcast will be. Maybe because we have ICL as a partner, we won't need as much equity, as they can be "collateral" not only that, but because we have most of our offtakes accounted for (80%) garantee by ICL, we may not need to raise much more. Maybe just the portion of liberty and IFC. If that is the case, this would be a great deal for the both of us. I mean better than what most people are thinking of the deal. It would also seem as though we would get better terms. Also, we may be able to reduce our Capex further after ICL takes a look at the operations. Also, since we have this partner, and yara in the region, there will be much much more pressure for the government to build a railroad to ours and Yara's encampment. Now that we have ICL, we also can go to yara with a much better negotiating leverage if they want our water and/or sharing ports.

If the webcast goes well, and Farhad can explain why this is great for allana's long term shareholders I think retail investors will be satisfied. especially if the above is true.

I think now, institutional investors will take a much closer look at allana and I do believe they will be buying tomorow. I think it will be a green day tomorow, but not a huge pop or anything, unless something comes out of the webcast that is a big surprise....

Just my thoughts. "

ICL and ALLANA - Ethanbrodie - SH - Feb 13, 2014

www.stockhouse.com/companies/bullboard/t.aaa/allana-potash-c…

"At first, it seemed dissapointing that it was not over the psychological .50c marker. And second, it seemed like not that big of a deal. I was expecting more like 150 mil investment, because we do need as they said 35% equity. I do find it interesting that ICL decided to go into "exclusive talks" when the shareprice was quite low, so now we should be "happy" because of this "premium"

NOW, the more I think of it, the more important tomorows webcast will be. Maybe because we have ICL as a partner, we won't need as much equity, as they can be "collateral" not only that, but because we have most of our offtakes accounted for (80%) garantee by ICL, we may not need to raise much more. Maybe just the portion of liberty and IFC. If that is the case, this would be a great deal for the both of us. I mean better than what most people are thinking of the deal. It would also seem as though we would get better terms. Also, we may be able to reduce our Capex further after ICL takes a look at the operations. Also, since we have this partner, and yara in the region, there will be much much more pressure for the government to build a railroad to ours and Yara's encampment. Now that we have ICL, we also can go to yara with a much better negotiating leverage if they want our water and/or sharing ports.

If the webcast goes well, and Farhad can explain why this is great for allana's long term shareholders I think retail investors will be satisfied. especially if the above is true.

I think now, institutional investors will take a much closer look at allana and I do believe they will be buying tomorow. I think it will be a green day tomorow, but not a huge pop or anything, unless something comes out of the webcast that is a big surprise....

Just my thoughts. "

ICL bringt zunächst einmal Sicherheit. Der Prozess hin zum Explorer wird weiter gehen, das Geld reicht für die nächsten Aufgaben. Oder mit dir Popeye: Das erste ("nennenswerte") Pottascheprojekt eines Juniors wird wahrscheinlicher.

Auf kurze Sicht bedeutet dies vermutlich: Schnelle Tradinggewinne sind erst einmal unwahrscheinlicher, da "die sensationelle" Nachricht nun nicht kommt, sondern wir eine gute und solide Nachricht haben. Vielleicht steigen sogar einige Zocker aus und wenden sich Aktien zu, die einen schnelleren Gewinn ermöglichen.

Mittelfristig haben wir jetzt eine Ausgangslage, die auch für ein breiteres Spektrum an Fonds interessant sein könnte. Sollte sich hier etwas bewegen, könnte der Kurs in den nächsten Monaten deutlich nach oben gehen.

Auf kurze Sicht bedeutet dies vermutlich: Schnelle Tradinggewinne sind erst einmal unwahrscheinlicher, da "die sensationelle" Nachricht nun nicht kommt, sondern wir eine gute und solide Nachricht haben. Vielleicht steigen sogar einige Zocker aus und wenden sich Aktien zu, die einen schnelleren Gewinn ermöglichen.

Mittelfristig haben wir jetzt eine Ausgangslage, die auch für ein breiteres Spektrum an Fonds interessant sein könnte. Sollte sich hier etwas bewegen, könnte der Kurs in den nächsten Monaten deutlich nach oben gehen.

Trading Spotlight

Antwort auf Beitrag Nr.: 46.438.751 von Popeye82 am 13.02.14 07:43:51Ich könnte mir sogar vooorstellen dass er "negativ reagiert".

Treffer, kompliment

Treffer, kompliment

Antwort auf Beitrag Nr.: 46.438.355 von Popeye82 am 13.02.14 00:48:27

Investor Webcast - Feb 8, 2014

www.gowebcasting.com/events/allana-potash-inc/2014/02/13/all…

Investor Webcast - Feb 8, 2014

www.gowebcasting.com/events/allana-potash-inc/2014/02/13/all…

Antwort auf Beitrag Nr.: 46.438.355 von Popeye82 am 13.02.14 00:48:27

This might explain - SH - bob_ten1 - Feb 13, 2014

www.stockhouse.com/companies/bullboard/t.aaa/allana-potash-c…

" ...why ICL wants to take so much production . Do you think they will want to fast tract this project .

ICL REPORTS EARLY PUBLICATION OF ITS Q4 AND 2013 RESULTS

Developments

ICL is currently at a crossroads with respect to its phosphate activities. Its Rotem Amfert Negev subsidiary is experiencing one of its most difficult periods in recent memory. Rotem’s production costs are substantially higher than its international competitors. In addition, phosphate reserves at its active mines in Israel will be depleted within a period of only seven to nine years. The only possible additional reserves in Israel are located at the Sde Barir field in the Negev, and ICL’s plan to mine phosphate in this field awaits governmental parties that have yet to conclude their investigation and render a decision regarding the matter. At the end of November, Israel’s Health Ministry requested the professional opinion of an objective, industry expert regarding phosphate mining at Sde Barir, which opinion is expected to be submitted to the Health Ministry soon.

To remain competitive in the current intensively competitive phosphate market environment, the Company must reduce costs at its facilities, invest hundreds of millions of dollars in advanced technology and R&D, as well as increase its production activities. ICL is prepared to undertake these activities assuming the government approves its request to mine the Sde Barir field. However, as a result of the uncertainty regarding Sde Barir, the Company has intensified its activities to increase and diversify its mining sources outside of Israel, as well as to broaden its global activities in the phosphate sector. "

This might explain - SH - bob_ten1 - Feb 13, 2014

www.stockhouse.com/companies/bullboard/t.aaa/allana-potash-c…

" ...why ICL wants to take so much production . Do you think they will want to fast tract this project .

ICL REPORTS EARLY PUBLICATION OF ITS Q4 AND 2013 RESULTS

Developments

ICL is currently at a crossroads with respect to its phosphate activities. Its Rotem Amfert Negev subsidiary is experiencing one of its most difficult periods in recent memory. Rotem’s production costs are substantially higher than its international competitors. In addition, phosphate reserves at its active mines in Israel will be depleted within a period of only seven to nine years. The only possible additional reserves in Israel are located at the Sde Barir field in the Negev, and ICL’s plan to mine phosphate in this field awaits governmental parties that have yet to conclude their investigation and render a decision regarding the matter. At the end of November, Israel’s Health Ministry requested the professional opinion of an objective, industry expert regarding phosphate mining at Sde Barir, which opinion is expected to be submitted to the Health Ministry soon.

To remain competitive in the current intensively competitive phosphate market environment, the Company must reduce costs at its facilities, invest hundreds of millions of dollars in advanced technology and R&D, as well as increase its production activities. ICL is prepared to undertake these activities assuming the government approves its request to mine the Sde Barir field. However, as a result of the uncertainty regarding Sde Barir, the Company has intensified its activities to increase and diversify its mining sources outside of Israel, as well as to broaden its global activities in the phosphate sector. "

Antwort auf Beitrag Nr.: 45.144.683 von DJHLS am 30.07.13 18:34:10

Das sieht im übrigen mehr und mehr danach aus, dass das eine Fehleinschätzung ist(worauf ich nicht gewettet, aber noch weniger dagegen gewettet hätte).

Gruß

P.

Zitat von DJHLS: Sollte der Preis tatsächlich auf 300 USD/t runtergehen, wird niemand das Risiko eingehen, in Äthiopien eine neue Mine zu bauen

Das sieht im übrigen mehr und mehr danach aus, dass das eine Fehleinschätzung ist(worauf ich nicht gewettet, aber noch weniger dagegen gewettet hätte).

Gruß

P.

Antwort auf Beitrag Nr.: 45.711.637 von DJHLS am 28.10.13 23:48:00

Auf SH hat jemand geschrieben 21%, zu $300, NPV10, after Tax.

Ich weiss nicht ob es stimmt.

Gruß

P.

Zitat von DJHLS: Wenn ja, wo liegt die IRR bei einer Discountrate von 10% und einem Kalipreis von 325 USD?

Auf SH hat jemand geschrieben 21%, zu $300, NPV10, after Tax.

Ich weiss nicht ob es stimmt.

Gruß

P.

so kann man es auch sehen. Ich tue es nicht:

reality check - SH - Ethanbrodie - Feb 14, 2014

www.stockhouse.com/companies/bullboard/t.aaa/allana-potash-c…

"In the past, I was very very bullish on this stock. I thought management has been doing everything right. It is unfortunate that we have been dealt the cards we have like belaruskali and uralkali breaking and the potash prices tumbling. Right now, I think we all need to look at this as a reality check. The "pumpers" of this board say how transformational this news is. They are right. It is transformational to ICL, and Ethiopia. It is NOT however transformational to existing shareholders. The people who pay management's salaries. The proof is in the pudding. If it was so transformational for shareholders, then why did the stock price dive? Institutions would jump all over this if it was a great deal at these levels. Something of this news, the stock price should have jumped to 70 or 80 cents. The reason why it did not and it went down is because it is NOT a good deal even at these levels because there still is MUCH UNCERTAINTY to how much return our shares can have. How much more dillution? what is the discount on the price of potash that ICL will get for free? (courtesy of us giving it to them). Also, this is the first time that management has dissapointed me. WHAT WOULD HAVE BEEN A GOOD DEAL FOR BOTH? I understand that when you start "exclusive" negotiations, you can use around that shareprice as your base. I am fine with the .47 pp. Keep in mind that the shareprice was over .50 and they claimed a large premium and it still did not get to our current trading price. I feel as though they could have went to .50 or .51. It would have been psycologically more sound as we all know the markets are that way, and it would not have been much more for ICL. Historically, still a great deal for them. Also, I would have the offtake at a small to medium discount, with after 5 years of full production, the discount gets reduced. I don't think people realise this as well be WE ALSO helped ICL. If this is a "partnership" why did we essentially give half our company away when we took all of the risk. AND we are still not done dillution. We will be lucky to get 20% by the time this is done. You think that is fair for the existing shareholders who have took on all of the risk to get this company to where it is now? I find it funny when Farhad talked about the shareholders how it will bring good value to existing shareholders.. so we get 20%? This is why the stock did not go up. Its reality. They are trying to spin this all as a positive when it is actually a fairly big negative for people who have been in this, keeping the shareprice as high as it has been. If existing shareholders would have all sold, farhad and team would be out of jobs. This is where it gets frustrating to me because I just see this announcement as a huge lie and a farce, just waiting for the next big dillution to come and management will say " oh look we did get the financing and we will be building a mine!" Wow great! but at what cost to the people who have believed in them and held onto their shares and helped boost the shareprice and gave them their jobs and took virtually all of the risk.. 20%. WOW. I find it also funny that analysts have all said on the cc wow great job etc.. this is transformational.. but yet that was just to their face. Now, I will say something positive about this stock.. It still has potential, but not nearly as much as before this deal. What would help the stock price the most is "hopefully" not much more dillution and the potash price going back up to 400 by next year. I just have lost alot of faith in management, they are working more on their resume of accomplishments of building this mine than shareholders. I still own a bunch of shares of allana, but from now on, its going to be much more day trading than holding long. If I would have had that strategy before, I would have made alot of money on this stock. Sorry to all of the longs as I used to be one, and may switch back, but management has alot of proving to do that they can bring value to EXISTING shareholders.

have a great weekend everyone! "

reality check - SH - Ethanbrodie - Feb 14, 2014

www.stockhouse.com/companies/bullboard/t.aaa/allana-potash-c…

"In the past, I was very very bullish on this stock. I thought management has been doing everything right. It is unfortunate that we have been dealt the cards we have like belaruskali and uralkali breaking and the potash prices tumbling. Right now, I think we all need to look at this as a reality check. The "pumpers" of this board say how transformational this news is. They are right. It is transformational to ICL, and Ethiopia. It is NOT however transformational to existing shareholders. The people who pay management's salaries. The proof is in the pudding. If it was so transformational for shareholders, then why did the stock price dive? Institutions would jump all over this if it was a great deal at these levels. Something of this news, the stock price should have jumped to 70 or 80 cents. The reason why it did not and it went down is because it is NOT a good deal even at these levels because there still is MUCH UNCERTAINTY to how much return our shares can have. How much more dillution? what is the discount on the price of potash that ICL will get for free? (courtesy of us giving it to them). Also, this is the first time that management has dissapointed me. WHAT WOULD HAVE BEEN A GOOD DEAL FOR BOTH? I understand that when you start "exclusive" negotiations, you can use around that shareprice as your base. I am fine with the .47 pp. Keep in mind that the shareprice was over .50 and they claimed a large premium and it still did not get to our current trading price. I feel as though they could have went to .50 or .51. It would have been psycologically more sound as we all know the markets are that way, and it would not have been much more for ICL. Historically, still a great deal for them. Also, I would have the offtake at a small to medium discount, with after 5 years of full production, the discount gets reduced. I don't think people realise this as well be WE ALSO helped ICL. If this is a "partnership" why did we essentially give half our company away when we took all of the risk. AND we are still not done dillution. We will be lucky to get 20% by the time this is done. You think that is fair for the existing shareholders who have took on all of the risk to get this company to where it is now? I find it funny when Farhad talked about the shareholders how it will bring good value to existing shareholders.. so we get 20%? This is why the stock did not go up. Its reality. They are trying to spin this all as a positive when it is actually a fairly big negative for people who have been in this, keeping the shareprice as high as it has been. If existing shareholders would have all sold, farhad and team would be out of jobs. This is where it gets frustrating to me because I just see this announcement as a huge lie and a farce, just waiting for the next big dillution to come and management will say " oh look we did get the financing and we will be building a mine!" Wow great! but at what cost to the people who have believed in them and held onto their shares and helped boost the shareprice and gave them their jobs and took virtually all of the risk.. 20%. WOW. I find it also funny that analysts have all said on the cc wow great job etc.. this is transformational.. but yet that was just to their face. Now, I will say something positive about this stock.. It still has potential, but not nearly as much as before this deal. What would help the stock price the most is "hopefully" not much more dillution and the potash price going back up to 400 by next year. I just have lost alot of faith in management, they are working more on their resume of accomplishments of building this mine than shareholders. I still own a bunch of shares of allana, but from now on, its going to be much more day trading than holding long. If I would have had that strategy before, I would have made alot of money on this stock. Sorry to all of the longs as I used to be one, and may switch back, but management has alot of proving to do that they can bring value to EXISTING shareholders.

have a great weekend everyone! "

Antwort auf Beitrag Nr.: 46.428.940 von Boersiback am 12.02.14 00:27:18

ANO fände ich auch interessant wenn wir die hier mal bisschen unter die Lupe nehmen, zu AAA vergleichen würden.

Die könnten ein "relativ(verblüffend??) ähnlicher Parallelprofiteur" sein.

Gruß

P.

ANO fände ich auch interessant wenn wir die hier mal bisschen unter die Lupe nehmen, zu AAA vergleichen würden.

Die könnten

ein "relativ(verblüffend??) ähnlicher Parallelprofiteur" sein.

ein "relativ(verblüffend??) ähnlicher Parallelprofiteur" sein.Gruß

P.

Antwort auf Beitrag Nr.: 46.461.409 von Popeye82 am 15.02.14 19:29:52

ANO hat auf den allerersten Blick durchaus Charme

ANO hat auf den allerersten Blick durchaus Charme

Antwort auf Beitrag Nr.: 46.462.221 von Boersiback am 16.02.14 03:03:05

Herr _______________________________________________________________________ ,

Ich hätte mal eine Frage -haben sie zufällig auf SH meine Schreiben durchgeguckt?

Mit ergebendsten Grüßen

Herr Popeye

Herr _______________________________________________________________________ ,

Ich hätte mal eine Frage -haben sie zufällig auf SH meine Schreiben durchgeguckt?

Mit ergebendsten Grüßen

Herr Popeye

Antwort auf Beitrag Nr.: 46.465.257 von Popeye82 am 16.02.14 22:39:48nein.... danke für den hinweis

Antwort auf Beitrag Nr.: 46.465.303 von Boersiback am 16.02.14 22:56:17

Nein, es ist nur irgendwie komisch.

Nicht wirklich wichtig, und eigentlich sch....egal, aber mir sticht das einfach so ins Auge.

Meistens bekomm ich keine Bewertungen, und wenn dann eher volles Rohr.

Jetzt sind aber die ungefähr letzten Fuffzehn alle mit einem solchem Sternchen bewertet.

Ich könnte schwören dass das 1 Person, oder maximal 2, waren.

Ist wie gesagt eigentlich .......egal, aber jetzt täte mich auch mal interessieren wer das war. Ob ich den kenn.

Gruß

P.

Nein, es ist nur irgendwie komisch.

Nicht wirklich wichtig, und eigentlich sch....egal, aber mir sticht das einfach so ins Auge.

Meistens bekomm ich keine Bewertungen, und wenn dann eher volles Rohr.

Jetzt sind aber die ungefähr letzten Fuffzehn alle mit einem solchem Sternchen bewertet.

Ich könnte schwören dass das 1 Person, oder maximal 2, waren.

Ist wie gesagt eigentlich .......egal, aber jetzt täte mich auch mal interessieren wer das war. Ob ich den kenn.

Gruß

P.

ja wer weiss... ich war´s nicht. ich lese zwar öfters mal bei SH bin aber nicht angemeldet.

ansonsten hätt´s vermutlich ein sternchen gegeben... ANO entspricht von der Idee her absolut meinem geschmack.

vielleicht auch erfahrungswerte bzgl otc und sideplays im rohstoffsegment. letztere hatten einfach sehr oft perfekt funktioniert wie bei FIS, TAS oder CPY

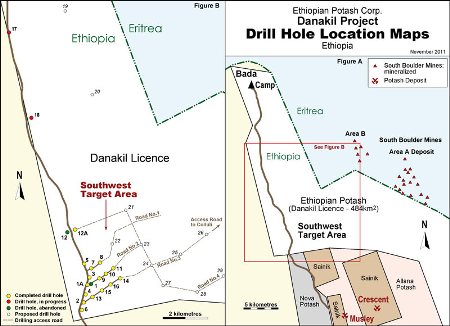

wie weit ist Danakil entfernt von allanas projekt ?

ansonsten hätt´s vermutlich ein sternchen gegeben... ANO entspricht von der Idee her absolut meinem geschmack.

vielleicht auch erfahrungswerte bzgl otc und sideplays im rohstoffsegment. letztere hatten einfach sehr oft perfekt funktioniert wie bei FIS, TAS oder CPY

wie weit ist Danakil entfernt von allanas projekt ?

Antwort auf Beitrag Nr.: 46.465.385 von Boersiback am 16.02.14 23:45:33

Jo, seh ich ähnlich. Abgesehen davon dass das schon so eine halbe "Allana 2" sein könnte, sie denke ich sehr viel Gemeinsamkeiten haben dürften(aber auch einige, signifikante, Unterschiede) könnten sie auch (stark?)von Allanas (Vor)Arbeit profitieren.

Aber so oder so, ganz so leicht dürfte es für sie auch nicht werden. Kann ich bis jetzt nicht richtig beurteilen, aber zeichnet sich in einigen Sachen doch schon ab.

Wenn ein Kommentar im alten ANO Stockhouseboard richtig ist, dann wurde das Projekt wohl auch schon Abasov angeboten. Oder er hatte zumindest die Gelegenheit dazu. Aber er wollte, wohl, nicht.

Gruß

P.

Jo, seh ich ähnlich. Abgesehen davon dass das schon so eine halbe "Allana 2" sein könnte, sie denke ich sehr viel Gemeinsamkeiten haben dürften(aber auch einige, signifikante, Unterschiede) könnten sie auch (stark?)von Allanas (Vor)Arbeit profitieren.

Aber so oder so, ganz so leicht dürfte es für sie auch nicht werden. Kann ich bis jetzt nicht richtig beurteilen, aber zeichnet sich in einigen Sachen doch schon ab.

Wenn ein Kommentar im alten ANO Stockhouseboard richtig ist, dann wurde das Projekt wohl auch schon Abasov angeboten. Oder er hatte zumindest die Gelegenheit dazu. Aber er wollte, wohl, nicht.

Gruß

P.

Antwort auf Beitrag Nr.: 46.465.453 von Popeye82 am 17.02.14 00:22:48hat natürlich immer einen reiz in einer solchen frühphase dabeizusein.

wenn allana mal loslegt dürften andere gebiete in äthopien interessanter werden für den markt.

scheint ja teils so als wolle man in äthopien hier und da weiter erschließen. "meine" centamin ist da jetzt auch aktiv bzgl gold.

wenn man sieht was nevsun für margen erreicht im nachbarland....

wenn allana mal loslegt dürften andere gebiete in äthopien interessanter werden für den markt.

scheint ja teils so als wolle man in äthopien hier und da weiter erschließen. "meine" centamin ist da jetzt auch aktiv bzgl gold.

wenn man sieht was nevsun für margen erreicht im nachbarland....

Antwort auf Beitrag Nr.: 46.465.463 von Boersiback am 17.02.14 00:28:16

Ja, mag prinzipiell stimmen, oder kann man zumindest so sehen.

Aber 2, 3 Gedanken mal dazu:

Ich weiss nicht wer TAS und CPY sind, aber Fission war ja ein Area Play. Da gin es also um Exploration und(ob) was finden. Das ist bei AgriMinco an sich gar nicht mehr das Thema.

Und von wegen 'Early Bird', falls Du auf einen "Bewertungsunterschied" schielst, dann beachte mal mindestens 2 Sachen dabei dazu: AGriMinco gehören 30% an dem Projekt. Und dann schau ma was Allana bisher ausgegeben hat, um bis hierher zu kommen. Dann mal überlegen wieviel das bei AgriMinco, bis dahin, vielleicht noch werden könnten.

Dann dürfte das, diiieser Hintergedanke, bisschen anders aussehen.

Vielleicht wären sie dann sogar 'teurer', keine Ahnung.

Ich wills Dir auch nicht ausreden, sowas kann schon seine Berechtigung haben, aber (mindestens)der 2 Punkte solltest Du Dir bewusst sein.

Gruß

P.

Ja, mag prinzipiell stimmen, oder kann man zumindest so sehen.

Aber 2, 3 Gedanken mal dazu:

Ich weiss nicht wer TAS und CPY sind, aber Fission war ja ein Area Play. Da gin es also um Exploration und(ob) was finden. Das ist bei AgriMinco an sich gar nicht mehr das Thema.

Und von wegen 'Early Bird', falls Du auf einen "Bewertungsunterschied" schielst, dann beachte mal mindestens 2 Sachen dabei dazu: AGriMinco gehören 30% an dem Projekt. Und dann schau ma was Allana bisher ausgegeben hat, um bis hierher zu kommen. Dann mal überlegen wieviel das bei AgriMinco, bis dahin, vielleicht noch werden könnten.

Dann dürfte das, diiieser Hintergedanke, bisschen anders aussehen.

Vielleicht wären sie dann sogar 'teurer', keine Ahnung.

Ich wills Dir auch nicht ausreden, sowas kann schon seine Berechtigung haben, aber (mindestens)der 2 Punkte solltest Du Dir bewusst sein.

Gruß

P.

Antwort auf Beitrag Nr.: 46.465.517 von Popeye82 am 17.02.14 01:32:17

hier nochmal besser, aber auch klein. RIchtig gute habe ich noch nicht gefunden, aber so müsste man sich das (4 bis 5er Gespann)erstmal zusammenreimen können:

hier nochmal besser, aber auch klein. RIchtig gute habe ich noch nicht gefunden, aber so müsste man sich das (4 bis 5er Gespann)erstmal zusammenreimen können:

zwei Artikel, zum Deal:

http://origin.library.constantcontact.com/download/get/file/…

http://origin.library.constantcontact.com/download/get/file/…

Gruß

P.

http://origin.library.constantcontact.com/download/get/file/…

http://origin.library.constantcontact.com/download/get/file/…

Gruß

P.

Danke Popeye,

beide Artikel decken sich mit meiner Einschätzung, dass der ICL-Deal langfristig gut für Allana ist.

ICL als Teilhaber, der mit Warrants 37% von Allana besitzen wird, ist für mich durch das Offtakeagreement vor allem ein beständiger Teilhaber. Die werden nicht bei der ersten Verzögerung das Handtuch schmeißen. Sondern sind bei dieser Größenordnung auch zu einem gewissen Teil von einem Gelingen des Projekts abhängig. Den einzigen Nachteil sehe ich in einer ungewollten Übernahme. Bis dahin sollten aber 60 - 80% Kurssteigerung drin sein.

Kurzfristig hat immerhin die Charttechnische Unterstützung gehalten. Auch nicht schlecht...

beide Artikel decken sich mit meiner Einschätzung, dass der ICL-Deal langfristig gut für Allana ist.

ICL als Teilhaber, der mit Warrants 37% von Allana besitzen wird, ist für mich durch das Offtakeagreement vor allem ein beständiger Teilhaber. Die werden nicht bei der ersten Verzögerung das Handtuch schmeißen. Sondern sind bei dieser Größenordnung auch zu einem gewissen Teil von einem Gelingen des Projekts abhängig. Den einzigen Nachteil sehe ich in einer ungewollten Übernahme. Bis dahin sollten aber 60 - 80% Kurssteigerung drin sein.

Kurzfristig hat immerhin die Charttechnische Unterstützung gehalten. Auch nicht schlecht...

Antwort auf Beitrag Nr.: 46.479.163 von tpnl am 18.02.14 18:36:02

Sehe ich insgesamt recht ähnlich. Ich denke dass eine 'Menge des Wertes', davon, gar nicht in den finanziellen Vereinbarungen zu suchen(finden) ist. Das ist aber eben auch oft seeehr schwierig einzuschätzen, bzw. was der Börsianer nicht in 2 Minuten mit seinem Taschenrechner ausrechnen kann auch oft nicht gemocht.

Ich möchte mal anfügen, wie gesagt, auf Stockhouse sind wirklich viiiele maaasslos enttäuscht, über (das konkrete ausfallen der)die Partnerschaft.

Ich möchte das hier nicht unter dem Teppich verschwinden lassen.

Eine Frage, zu den vorhergehenden Schreiben hier: Hast Du vielleicht so bisschen Meinung ob das mit AgriMinco Sinn machen könnte?

Die eine wirkliche Chance haben könnten, irgendwann auch mal wirklich 'Pottasche rauszuhauen', "AAA nachzueifern"?

(Wenn)Nur eigene EIndrücke, ich bin über die Bude, bisher, auch nur flüchtig drübergehuscht. Wobei sie mir unter 'Etiopian Potash', relativ früh, schon etwas sagten.

Die täten mich einfach auch nochma reizen, zumindest erstmal 'bisschen mehr gucken'.

Gruß

P.

Sehe ich insgesamt recht ähnlich. Ich denke dass eine 'Menge des Wertes', davon, gar nicht in den finanziellen Vereinbarungen zu suchen(finden) ist. Das ist aber eben auch oft seeehr schwierig einzuschätzen, bzw. was der Börsianer nicht in 2 Minuten mit seinem Taschenrechner ausrechnen kann auch oft nicht gemocht.

Ich möchte mal anfügen, wie gesagt, auf Stockhouse sind wirklich viiiele maaasslos enttäuscht, über (das konkrete ausfallen der)die Partnerschaft.

Ich möchte das hier nicht unter dem Teppich verschwinden lassen.

Eine Frage, zu den vorhergehenden Schreiben hier: Hast Du vielleicht so bisschen Meinung ob das mit AgriMinco Sinn machen könnte?

Die eine wirkliche Chance haben könnten, irgendwann auch mal wirklich 'Pottasche rauszuhauen', "AAA nachzueifern"?

(Wenn)Nur eigene EIndrücke, ich bin über die Bude, bisher, auch nur flüchtig drübergehuscht. Wobei sie mir unter 'Etiopian Potash', relativ früh, schon etwas sagten.

Die täten mich einfach auch nochma reizen, zumindest erstmal 'bisschen mehr gucken'.

Gruß

P.

Antwort auf Beitrag Nr.: 46.480.337 von Popeye82 am 18.02.14 20:43:46ja würde mich auch interessieren...

AAA ist ja nun irgendwo sicherer und irgendwo unspektakulärer geworden.

den riesensatz werden wir hier nicht mehr machen, denke ich.

ein hold aber allemal. 100% sind vielleicht drin.

aber das ganze ist doch etwas konservativer geworden und ja, aus der sicht kann man von dem deal enttäuscht sein.

der markt sollte sich nur nicht wundern. wenn er meint er müsse gute rohstoffewerte entsprechend tief bewerten und twitter ins weltall schiessen, dann kommt sowas eben zustande.

AAA ist ja nun irgendwo sicherer und irgendwo unspektakulärer geworden.

den riesensatz werden wir hier nicht mehr machen, denke ich.

ein hold aber allemal. 100% sind vielleicht drin.

aber das ganze ist doch etwas konservativer geworden und ja, aus der sicht kann man von dem deal enttäuscht sein.

der markt sollte sich nur nicht wundern. wenn er meint er müsse gute rohstoffewerte entsprechend tief bewerten und twitter ins weltall schiessen, dann kommt sowas eben zustande.

grundätzlich tendier ich immer noch zu Highfield.

auch recht oberflächennah wie bei allana.

was interssanters in dem sektor kenne ich nicht.

AgriMinco ist natürlich in einer sehr frühen phase. der haken ist eben an geldzu kommen.

klar, awenn man allana und die aufgebrachten gelder grob einschätzt ist agriminco deswegen aktuell auch nicht unbedingt billig.

gibt´s immer noch die chance dass sich der markt bessert und kurse solcher werte "einfach mal so" 200% steigen.

die ganzen kanadier können mit allanas kosten überhaupt nicht mithalten. es bleibt von daher nicht viel und der sektor liegt am boden aufgrund der stimmung.

eigentlich muss man fast irgendwie dort mehr investieren... nachdem die zerhauenen EM-werte ja auch wieder beachtlichst durchgestartet sind bleiben nicht viele sektoren mit negativstimmung... und die reizt mich nunmal sowieso am meisten

auch recht oberflächennah wie bei allana.

was interssanters in dem sektor kenne ich nicht.

AgriMinco ist natürlich in einer sehr frühen phase. der haken ist eben an geldzu kommen.

klar, awenn man allana und die aufgebrachten gelder grob einschätzt ist agriminco deswegen aktuell auch nicht unbedingt billig.

gibt´s immer noch die chance dass sich der markt bessert und kurse solcher werte "einfach mal so" 200% steigen.

die ganzen kanadier können mit allanas kosten überhaupt nicht mithalten. es bleibt von daher nicht viel und der sektor liegt am boden aufgrund der stimmung.

eigentlich muss man fast irgendwie dort mehr investieren... nachdem die zerhauenen EM-werte ja auch wieder beachtlichst durchgestartet sind bleiben nicht viele sektoren mit negativstimmung... und die reizt mich nunmal sowieso am meisten

Antwort auf Beitrag Nr.: 46.481.647 von Boersiback am 18.02.14 22:59:21

Also ich spekuliere bei Allana nicht auf 100%. Von hier an.

Die Möglichkeiten, für den AKtienkurs, im Vergleich zu vorherigen Zeiten, sind schon deutlich bis sehr viel kleiner geworden, aber, meiner Meinung nach, weiterhin nicht klein(nicht nur, aber auch vor aaallem wenn man auf AAA "weitergehende "Möglichkeiten" " schaut).

Da ist noch seeehr viel vorhanden, aber bis dato, für mich jedenfalls, schwer/im Endeffekt nicht festzumachen.

Und zu den 2 anderen Werten, wie gesagt wären, momentan, auch die einzigen (Potash)Werte die mich wirklich interessieren.

Ob die aber nun Geld haben, wie hoch die (jetzt)bewertet sind, in welchem ENtwicklungsstadium die sich befinden und so weiter ist (mir jedenfalls(erstmal)) scheiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiissegal.

Da geht es um gaaaaaaaaaaaaaaaaaanz andere Dinge.

Gruß

P.

Zitat von __________: ein hold aber allemal. 100% sind vielleicht drin.

Also ich spekuliere bei Allana nicht auf 100%. Von hier an.

Die Möglichkeiten, für den AKtienkurs, im Vergleich zu vorherigen Zeiten, sind schon deutlich bis sehr viel kleiner geworden, aber, meiner Meinung nach, weiterhin nicht klein(nicht nur, aber auch vor aaallem wenn man auf AAA "weitergehende "Möglichkeiten" " schaut).

Da ist noch seeehr viel vorhanden, aber bis dato, für mich jedenfalls, schwer/im Endeffekt nicht festzumachen.

Zitat von __________: grundätzlich tendier ich immer noch zu Highfield.

auch recht oberflächennah wie bei allana.

was interssanters in dem sektor kenne ich nicht.

AgriMinco ist natürlich in einer sehr frühen phase. der haken ist eben an geldzu kommen.

Und zu den 2 anderen Werten, wie gesagt wären, momentan, auch die einzigen (Potash)Werte die mich wirklich interessieren.

Ob die aber nun Geld haben, wie hoch die (jetzt)bewertet sind, in welchem ENtwicklungsstadium die sich befinden und so weiter ist (mir jedenfalls(erstmal)) scheiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiissegal.

Da geht es um gaaaaaaaaaaaaaaaaaanz andere Dinge.

Gruß

P.

Guten Morgen,

habe einen kurzen Blick (für mehr reicht die Zeit gerade nicht) auf AgriMinco geworfen. Die Danakil-Liegenschaft halte ich für sehr vielversprechend. Die Lage ist ähnlichh wie die von Allana zukunftsweisend, dann gibt es ein sehr hochgradiges Eck, dass bei Produktionsbeginn schnell Geld in die Kassen spülen könnte.

Die anderen Liegenschaften von Agri schrecken mich eher ab. Der Verdacht kommt auf, dass sie überall ein bisschen tätig sind und nicht wirklich das Ziel haben, selbst zum Produzenten aufzusteigen. Heißt das, dass Sie von keinem ihrem Liegenschaften wirklich überzeugt sind. Weniger ist für mich oft mehr!

Anscheinend ist bei der Danakil-Liegenschaft Circum Minerals zu 70% beteiligt. Es könnte interessant sein, über die etwas herauszufinden. Ist mir aber noch nicht gelungen.

habe einen kurzen Blick (für mehr reicht die Zeit gerade nicht) auf AgriMinco geworfen. Die Danakil-Liegenschaft halte ich für sehr vielversprechend. Die Lage ist ähnlichh wie die von Allana zukunftsweisend, dann gibt es ein sehr hochgradiges Eck, dass bei Produktionsbeginn schnell Geld in die Kassen spülen könnte.

Die anderen Liegenschaften von Agri schrecken mich eher ab. Der Verdacht kommt auf, dass sie überall ein bisschen tätig sind und nicht wirklich das Ziel haben, selbst zum Produzenten aufzusteigen. Heißt das, dass Sie von keinem ihrem Liegenschaften wirklich überzeugt sind. Weniger ist für mich oft mehr!

Anscheinend ist bei der Danakil-Liegenschaft Circum Minerals zu 70% beteiligt. Es könnte interessant sein, über die etwas herauszufinden. Ist mir aber noch nicht gelungen.

Antwort auf Beitrag Nr.: 46.307.159 von Boersiback am 26.01.14 01:50:55

FLUX, 07:11:09, in meinem perma-Spamm-Thread. Sowas auch.

Gruß

P.

FLUX, 07:11:09, in meinem perma-Spamm-Thread. Sowas auch.

Gruß

P.

Antwort auf Beitrag Nr.: 46.482.295 von tpnl am 19.02.14 07:14:53

letzte Diskussionsanalyse, noch Pre-Resource(nbekanntgabe). Hab's ma durch, "bewegte Geschichte", sag ich mal als -eben gewordener

- Weltmeister des Understatements, bisher. Thematik "Restprojekte" könnte sich vielleicht auch (teilweise)von selbst erledigen. 31.03.2014(+/-(?)7 Tage) sollte man sich mal vormerken, davor lieber (noch)nix reinstecken:

- Weltmeister des Understatements, bisher. Thematik "Restprojekte" könnte sich vielleicht auch (teilweise)von selbst erledigen. 31.03.2014(+/-(?)7 Tage) sollte man sich mal vormerken, davor lieber (noch)nix reinstecken:

http://sedar.com/CheckCode.do

Gruß

P.

letzte Diskussionsanalyse, noch Pre-Resource(nbekanntgabe). Hab's ma durch, "bewegte Geschichte", sag ich mal als -eben gewordener

- Weltmeister des Understatements, bisher. Thematik "Restprojekte" könnte sich vielleicht auch (teilweise)von selbst erledigen. 31.03.2014(+/-(?)7 Tage) sollte man sich mal vormerken, davor lieber (noch)nix reinstecken:

- Weltmeister des Understatements, bisher. Thematik "Restprojekte" könnte sich vielleicht auch (teilweise)von selbst erledigen. 31.03.2014(+/-(?)7 Tage) sollte man sich mal vormerken, davor lieber (noch)nix reinstecken:http://sedar.com/CheckCode.do

Gruß

P.

Antwort auf Beitrag Nr.: 46.481.647 von Boersiback am 18.02.14 22:59:21

Waissscht Börsi was ich bei Dir immer bisschen doof finde??

Du weisst immer ganz akkurat dass ein Stock 'paar' 100% Potenzial hat, teilweise größer '10bagger'. Kein Ding.

-99% oder, eben, auch 10.000% Plus alles 'voll normal' sind.

Aber weeenn man mal eine Diskussion anstösst -interpretiere hier mal den Versuch, großzügigerweise, als die Tat- dann kommt von Dir (fast)000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000,0.

Das ist Scheisse.

EIN Grund warum ich in eure Clubs nicht nicht die Gold Card beantrage.

Gruß

P.

Waissscht Börsi was ich bei Dir immer bisschen doof finde??

Du weisst immer ganz akkurat dass ein Stock 'paar' 100% Potenzial hat, teilweise größer '10bagger'. Kein Ding.

-99% oder, eben, auch 10.000% Plus alles 'voll normal' sind.

Aber weeenn man mal eine Diskussion anstösst -interpretiere hier mal den Versuch, großzügigerweise, als die Tat- dann kommt von Dir (fast)000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000000,0.

Das ist Scheisse.

EIN Grund warum ich in eure Clubs nicht nicht die Gold Card beantrage.

Gruß

P.