Aussichtsreiche Lithiumaktie - 500 Beiträge pro Seite (Seite 6)

eröffnet am 09.10.10 18:47:46 von

neuester Beitrag 24.08.20 20:57:30 von

neuester Beitrag 24.08.20 20:57:30 von

Beiträge: 2.532

ID: 1.160.383

ID: 1.160.383

Aufrufe heute: 1

Gesamt: 219.189

Gesamt: 219.189

Aktive User: 0

ISIN: CA64045C1068 · WKN: A1JQUB

0,1072

EUR

-28,77 %

-0,0433 EUR

Letzter Kurs 21.11.19 Quotrix Düsseldorf

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7950 | +30,33 | |

| 55,80 | +15,41 | |

| 0,7999 | +14,27 | |

| 11,250 | +12,73 | |

| 0,5500 | +10,00 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7145 | -8,92 | |

| 2,1800 | -9,17 | |

| 186,20 | -10,48 | |

| 4,2300 | -17,86 | |

| 46,74 | -98,00 |

Antwort auf Beitrag Nr.: 62.009.063 von Atompuls am 25.11.19 18:43:38So siehts aus,kurz nach dem % Jahrestief

Antwort auf Beitrag Nr.: 62.009.207 von bernharde am 25.11.19 18:57:36Da ist wohl mittlerweile hoffentlich jeder längst ausgestiegen. Leider ein Lehrstück, um aufzuzeigen was mit guten Projekten passiert, wenn es schlecht geführt wird.

Antwort auf Beitrag Nr.: 62.012.975 von bcgk am 26.11.19 08:53:43Hast du mal überschlagen mit wie viel Prozent plus minus du raus bist insgesamt über alle Käufe?

Antwort auf Beitrag Nr.: 62.013.896 von bernharde am 26.11.19 10:13:36Ich habe unter dem Strich mit Nemaska exakt 322.000€ versenkt, damit etwas mehr als meine Microsoft-Buchgewinne aus 2019.

Wie gesagt, lehrreiche Erfahrung.

Wie gesagt, lehrreiche Erfahrung.

Antwort auf Beitrag Nr.: 62.014.121 von bcgk am 26.11.19 10:33:59Respekt für deine Offenheit. Eigentlich hätte mich die Angabe in Prozent mehr interessiert, aber die Zahl ist schon grauenhaft. Naja, an der Börse muss man eben auch mal Verluste aushalten können.

Trading Spotlight

Antwort auf Beitrag Nr.: 62.014.823 von bernharde am 26.11.19 11:52:10Prozentual kann ich das schwer beziffern, da ich neben einer festen Position zigmal getradet habe.

Schade aber, dass meine 2019er Gewinne damit aufgezehrt sind, dafür immerhin steuerlich attraktiv.

Schade aber, dass meine 2019er Gewinne damit aufgezehrt sind, dafür immerhin steuerlich attraktiv.

!

Dieser Beitrag wurde von MODelfin moderiert. Grund: Bitte Argumentation statt Provokation, Danke.!

Dieser Beitrag wurde von MODelfin moderiert. Grund: Korrespondierendes Posting wurde entfernt

Antwort auf Beitrag Nr.: 62.015.621 von bcgk am 26.11.19 13:38:45An deiner Stelle hätte ich 1/4 behalten.

Wer weiss- Tot Gesagte leben länger.

Es gibt durchaus noch Hoffnung, dass G.B. endlich zum Teufel gejagt wird und der Saustall aufgeräumt wird.

Wer weiss- Tot Gesagte leben länger.

Es gibt durchaus noch Hoffnung, dass G.B. endlich zum Teufel gejagt wird und der Saustall aufgeräumt wird.

Antwort auf Beitrag Nr.: 62.016.179 von Kaputzenheini am 26.11.19 15:12:50Es gibt durchaus noch Hoffnung, dass G.B. endlich zum Teufel gejagt wird und der Saustall aufgeräumt wird.

Da G.B. immer noch im Amt ist, würde ich darauf nicht wetten. Davon abgesehen müsste auch ein Nachfolger etwaige Investoren angesichts des immensen Kapitalbedarfs erst noch überzeugen. Das erscheint mir, unabhängig von der Person des CEO, ein schwieriges Unterfangen.

Da G.B. immer noch im Amt ist, würde ich darauf nicht wetten. Davon abgesehen müsste auch ein Nachfolger etwaige Investoren angesichts des immensen Kapitalbedarfs erst noch überzeugen. Das erscheint mir, unabhängig von der Person des CEO, ein schwieriges Unterfangen.

Heute herrschen andere Umstände als zu dem Zeitpunkt, an dem Nemaska seine Finanzierung zustande brachte. Preise wie Stimmung sind im Keller. Heute würde schwerlich jemand deutlich über eine Milliarde CAN-Dollar aufbieten, um ein bestenfalls mittelmäßiges Projekt zu finanzieren, das 33ktpa produziert. Die verschiedensten Projekte stehen in Finanzierungskonkurrenz zueinander. LACs 40ktpa Anlage z.B. wird deutlich günstiger (USD565M), nutzt "proven technology" und vermeidet damit das Risiko, dass der gewählte Prozess im Großformat nicht wie geplant funktionieren könnte. Ein erfahrener JV-Partner wie Ganfeng, der sich mit den downstream Prozessen auskennt wie kaum eine zweite Firma, ist ein weiterer Pluspunkt. Nicht zuletzt dürfte den LAC Zahlen mehr Vertrauen entgegengebracht werden als den erwiesenermaßen unverlässlichen NMX-Zahlen. Vielleicht versenkt ja tatsächlich ein unverantwortlicher Politiker eine horrende Summe fremden Geldes in diesem Fass ohne Boden. Oder es kommt ein Investor - eventuell mit einem Industriepartner -, der alle Fäden an sich reißt und NMX noch als Puppe fungieren lässst. Andererseits, der Name "NEMASKA" ist zum Gespött des Sektors geworden und sollte schon aus Marketinggründen eher früher als später in der Versenkung verschwinden. So oder so dürfte keiner der Altaktionäre, die bei der ursprünglichen Finanzierung eingestiegen sind, das Investment wieder heraus bekommen.

Antwort auf Beitrag Nr.: 62.009.063 von Atompuls am 25.11.19 18:43:38Hat kurzfristig funktioniert...

Antwort auf Beitrag Nr.: 59.799.000 von bcgk am 05.02.19 19:51:08

Wer wirklich Recht hatte, wissen nun auch die, die damals Wandas Märchenstunde für Tatsache hielten. Übrigens, gerade einmal 8 Tage nach Wandas Märchenstunde funkte Nemaska seinen "Offenbarungseid" der wiederum mit jeder Menge Märchen aufgehübscht war und nun doch im Antrag auf Gläubigerschutz gipfelte.

Zitat von bcgk: Hatte bzgl. Joe Lowry Kontakt zu Wanda. Anbei ihre Antwort, die durchaus interessant ist.

Hi,

Mr. Lowry frequently voices his own opinions, of which he is known to have many. We have not had a falling out, we have simply chosen not to use his consulting services, for which others have paid and of which he not surprisingly has a favourable opinion. Mr. Lowry has also speculated in the past that we would never make battery grade lithium hydroxide, yet our customer Johnson Matthey is very happy with the product received to date.

The construction update will be timed around the release of our quarterly financials which should be filed mid February 12 to 15th.

Wanda

Wer wirklich Recht hatte, wissen nun auch die, die damals Wandas Märchenstunde für Tatsache hielten. Übrigens, gerade einmal 8 Tage nach Wandas Märchenstunde funkte Nemaska seinen "Offenbarungseid" der wiederum mit jeder Menge Märchen aufgehübscht war und nun doch im Antrag auf Gläubigerschutz gipfelte.

Antwort auf Beitrag Nr.: 62.226.620 von Nuggeteer am 24.12.19 14:16:12Wer wirklich Recht hatte, wissen nun auch die, die damals Wandas Märchenstunde für Tatsache hielten.

exakt. Und

we have simply chosen not to use his consulting services, for which others have paid and of which he not surprisingly has a favourable opinion.

wer seine Beiträge regelmäßig verfolgt, weiß, dass schon diese Behauptung falsch war/ist. Er lobt/würdigt, wo es ihm geboten erscheint, und kritisiert ebenso, unabhängig vom Unternehmen. Zudem begründet er seine Meinungen regelmäßig.

Als Anleger ist man jedenfalls immer gut beraten, unabhängige echte Expertenmeinungen zu verfolgen (damit sind nicht die üblichen Analysten gemeint, die oftmals auch nur rudimentäre Fachkenntnisse mitbringen!) und in Investitionsentscheidungen einfliessen zu lassen.

Die zweite Lektion, die man hier mitnehmen kann, ist die, dass man Informationen zum Stand der Entwicklung eines Unternehmens, die nicht über den Markt, sondern durch direkten Kontakt zum Vorstand oder der IR kommuniziert werden, weitgehend vergessen kann. Was aber auch logisch ist. Oder glaubt jemand ernsthaft, ein Unternehmen würde einem Retailinvestor per mail Probleme wie hier bei Nemaska mitteilen, die Öffentlichkeit aber im Dunkeln lassen? So ein Unternehmensvertreter stünde mit einem Bein im Knast, von Schadenersatzklagen gar nicht zu reden.

exakt. Und

we have simply chosen not to use his consulting services, for which others have paid and of which he not surprisingly has a favourable opinion.

wer seine Beiträge regelmäßig verfolgt, weiß, dass schon diese Behauptung falsch war/ist. Er lobt/würdigt, wo es ihm geboten erscheint, und kritisiert ebenso, unabhängig vom Unternehmen. Zudem begründet er seine Meinungen regelmäßig.

Als Anleger ist man jedenfalls immer gut beraten, unabhängige echte Expertenmeinungen zu verfolgen (damit sind nicht die üblichen Analysten gemeint, die oftmals auch nur rudimentäre Fachkenntnisse mitbringen!) und in Investitionsentscheidungen einfliessen zu lassen.

Die zweite Lektion, die man hier mitnehmen kann, ist die, dass man Informationen zum Stand der Entwicklung eines Unternehmens, die nicht über den Markt, sondern durch direkten Kontakt zum Vorstand oder der IR kommuniziert werden, weitgehend vergessen kann. Was aber auch logisch ist. Oder glaubt jemand ernsthaft, ein Unternehmen würde einem Retailinvestor per mail Probleme wie hier bei Nemaska mitteilen, die Öffentlichkeit aber im Dunkeln lassen? So ein Unternehmensvertreter stünde mit einem Bein im Knast, von Schadenersatzklagen gar nicht zu reden.

Antwort auf Beitrag Nr.: 62.226.773 von IllePille am 24.12.19 15:05:44Perfekt auf den Punkt gebracht! Was mir noch auffällt, ist dreierlei:

1. Erscheint es mir absurd, zur Überprüfung des Wahrheitsgehalts von Kritk an einer Firma, ausgerechnet die PR-Abteilung dieser Firma zu kontaktieren. Das ist in etwa so, als würde man beim Versuch, herauszufinden, wer für die Abstürze der beiden 737-MAX verantwortlich ist, den Boeing-Pressesprecher fragen. Die Wahrheit findet man so garantiert nicht.

2. Scheint es inzwischen absolut übliche Verfahrensweise von sogenannter "PR" zu sein, Kritik nicht sachlich zu entkräften, sondern ohne jegliche Bezugnahme auf den Inhalt der Kritik ausschließlich die Person des Kritikers - oft mit frei Erfundenem, sprich: Lügen - zu diffamieren. Ironischerweise in Umlauf gebracht von Angestellten wie "Wanda", die ganz offiziell dafür bezahlt werden.

3. Das alleine wäre nur halb so schlimm, wäre es nicht von einem gewissen "Erfolg" gekrönt. Man muss sich nur die Antworten auf den Diffamierungspost auf diesem Board anschauen, um festzustellen, dass diese Lügen nur allzu gerne geglaubt, übernommen und fortan als Totschlag-Argument gegen alle Beiträge verwendet werden, die diese Person zukünftig postet.

Wie Pille völlig richtig bemerkt, sind Herr Lowrys Einschätzungen unabhängig und stets wohl begründet. Und ganz selbstverständlich wird auch Lowry seine Einschätzungen ändern, wenn sich das als notwendig erweist. So äußerte er sich z.B. lange optimistisch über SQMs Aussichten und lag damit richtig. Der Kurs der SQM-Aktie stieg in diesem Zeitraum deutlich. Später, insbesondere nach dem Wechsel and der Spitze der Firma, äußerte er sich skeptischer zu den weiteren Aussichten. Und diese nachvollziehbar begründete "Meinungsänderung" erwies sich ebenfalls als richtig: Der Kurs von SQM fiel seitdem um über -50%. In Bezug auf Nemaska hätte es eine Reihe von anderen unabhängigen, langjährig aktiven, anerkannten Experten gegeben, die sich wie Lowry kritisch zu Nemaska äußerten.

Die finale Rechnung für diese Ignoranz wird nun bald beglichen werden.

Manche machen in der ihr eigenen, großspurig zur Schau gestellten Hybris den genau gleichen Fehler sogar noch ein weiteres Mal, wischen wohl begründete Kritik unter Bezugnahme auf Diffamierungspostings lächerlichen Ursprungs einfach beiseite. "Those who cannot learn from history are doomed to repeat it."

1. Erscheint es mir absurd, zur Überprüfung des Wahrheitsgehalts von Kritk an einer Firma, ausgerechnet die PR-Abteilung dieser Firma zu kontaktieren. Das ist in etwa so, als würde man beim Versuch, herauszufinden, wer für die Abstürze der beiden 737-MAX verantwortlich ist, den Boeing-Pressesprecher fragen. Die Wahrheit findet man so garantiert nicht.

2. Scheint es inzwischen absolut übliche Verfahrensweise von sogenannter "PR" zu sein, Kritik nicht sachlich zu entkräften, sondern ohne jegliche Bezugnahme auf den Inhalt der Kritik ausschließlich die Person des Kritikers - oft mit frei Erfundenem, sprich: Lügen - zu diffamieren. Ironischerweise in Umlauf gebracht von Angestellten wie "Wanda", die ganz offiziell dafür bezahlt werden.

3. Das alleine wäre nur halb so schlimm, wäre es nicht von einem gewissen "Erfolg" gekrönt. Man muss sich nur die Antworten auf den Diffamierungspost auf diesem Board anschauen, um festzustellen, dass diese Lügen nur allzu gerne geglaubt, übernommen und fortan als Totschlag-Argument gegen alle Beiträge verwendet werden, die diese Person zukünftig postet.

Wie Pille völlig richtig bemerkt, sind Herr Lowrys Einschätzungen unabhängig und stets wohl begründet. Und ganz selbstverständlich wird auch Lowry seine Einschätzungen ändern, wenn sich das als notwendig erweist. So äußerte er sich z.B. lange optimistisch über SQMs Aussichten und lag damit richtig. Der Kurs der SQM-Aktie stieg in diesem Zeitraum deutlich. Später, insbesondere nach dem Wechsel and der Spitze der Firma, äußerte er sich skeptischer zu den weiteren Aussichten. Und diese nachvollziehbar begründete "Meinungsänderung" erwies sich ebenfalls als richtig: Der Kurs von SQM fiel seitdem um über -50%. In Bezug auf Nemaska hätte es eine Reihe von anderen unabhängigen, langjährig aktiven, anerkannten Experten gegeben, die sich wie Lowry kritisch zu Nemaska äußerten.

Die finale Rechnung für diese Ignoranz wird nun bald beglichen werden.

Manche machen in der ihr eigenen, großspurig zur Schau gestellten Hybris den genau gleichen Fehler sogar noch ein weiteres Mal, wischen wohl begründete Kritik unter Bezugnahme auf Diffamierungspostings lächerlichen Ursprungs einfach beiseite. "Those who cannot learn from history are doomed to repeat it."

Ich werfe mich in den Staub und bekenne mich schuldig der Naivität. Ich bin hier beim Run auf 40c ausgestiegen, habe dennoch viel Geld verloren und ne Menge gelernt. Zu Lowry habe ich dennoch eine differenzierte Meinung.

Euch beiden frohe Weihnachten und ein gutes Jahr 2020.

Euch beiden frohe Weihnachten und ein gutes Jahr 2020.

Antwort auf Beitrag Nr.: 59.967.898 von Schinkenbaron am 26.02.19 16:32:07

Schinkenbaron 29.12.18 12:48:23 Beitrag Nr. 1.462

Welche charttechnischen Signale sollten nun berücksichtigt werden? Ist die dicke, blau markiert und fallende Linie nun im korrekten Bereich.

Zitat von Schinkenbaron: Abwärtstrend noch im Gange. Wer weiß wie weit es fallen kann, deshalb für mich noch kein Kauf.

Schinkenbaron 29.12.18 12:48:23 Beitrag Nr. 1.462

Welche charttechnischen Signale sollten nun berücksichtigt werden? Ist die dicke, blau markiert und fallende Linie nun im korrekten Bereich.

Antwort auf Beitrag Nr.: 62.229.761 von Sylt1204 am 26.12.19 00:00:40Bei Gläubigerschutz kannst du Charttechnik einpacken. Das kannst du jetzt zocken wie Steinhoff oder Thomas Cook.

Chance auf Comeback nach Gläubigerschutz?

Im Gegensatz zu Insolvenzrecht in Deutschland wo ein Pleiteunternehmen abgewickelt wird, hat ein Unternehmen die Chance nach einen chapter 11 Verfahren durch einen Erlass von Schulden an den Markt zurück zu kehren.Zitat aus der Wikipedia:

Gläubigerschutz in den USA und Kanada

Der Begriff Gläubigerschutz beinhaltet im deutschen Recht die Sicherung der Interessen der Gläubiger. Das Gegenteil wird unter dem Begriff Gläubigerschutz in den USA und Kanada verstanden. Hier sollen die in eine Unternehmenskrise geratenen Unternehmen vor ihren Gläubigern geschützt werden. Sowohl das US-amerikanische Insolvenzrecht (Chapter 11 Bankruptcy Code) als auch der kanadische Companies Creditors Arrangement Act (CCAA) verstehen unter Gläubigerschutz den Schutz vor den Forderungen und Aktivitäten der Gläubiger. Der eigentliche Sinn von Chapter 11 ist die Erhaltung der Arbeitsplätze eines in finanzielle Schwierigkeiten geratenen Unternehmens. Unter Umständen werden dazu Schulden erlassen, das Unternehmen kann zwecks Aufrechterhaltung seines Geschäftsbetriebs in das Eigentum der Gläubiger übergehen, um so letztlich die Forderungen der Gläubiger möglichst noch realisieren zu können.

Gut möglich, dass es ein debt to equity swap gibt - in dem Fall dürfte den Gläubigern wohl dann der Großteil der Aktien des Unternehmens gehören und eine massive Verwässerung - auf englisch dilution - die jetzigen Aktionäre mit ein paar Brotkrumen am Unternehmenswert zurücklassen.

Vermutlich wird die Aktie irgendwo bei 5 Cent den Handel aufnehmen, so denn sie noch einmal gehandelt werden sollte. Vielleicht stürzt sie auch gegen Null, sofern es hier überhaupt etwas zu stürzen gibt.

Es kommt darauf an zu welchen Konditionen die Gläubiger ggf. Schulden in Aktien wandeln werden oder sogar Schulden erlassen...

Ohne Blessuren - bis hin zum möglichen Totalverlust der jetzigen Aktionäre wird dies wohl nicht abgehen.

Interessant allemal - ärgerlich für die Aktionäre in Deutschland nur, wenn gar kein Handel mehr stattfinden sollte, weil die wertlose Ausbuchung der Aktien dann nicht einmal mehr steuerlich dank der Sozialistischen Enteignungsparteien in Berlin als Verlustvortrag seit 1.1.2020 genutzt werden kann.

Ist schon echt krass, was in Deutschland passiert und wie deutsche Anleger gegen die Wand gefahren werden.

Wichtiger Hinweis: Dieser Beitrag dient lediglich zu Informationszwecken und ist keine Aufforderung zum Kauf oder Verkauf von Aktien oder Finanzinstrumenten. Märkte können steigen oder fallen und Investments im Totalverlust enden. Jeder Investor und Anleger handelt auf eigenes Risiko.

die Wahrscheinlichkeit, dass diese Aktie je wieder gehandelt wird, siedle ich bei Null an, angesichts der Schulden in Verbindung mit dem massiven zusätzlichen Kapitalbedarf. Hier geht es zudem nicht um ein operativ tätiges Unternehmen, das in irgendwelche Schwierigkeiten geraten ist. Insofern wäre ein "debt to equity swap" weder für die Gläubiger, noch für das Unternehmen selbst, ein Befreiungsschlag. Ohne das Aufbringen der verbleibenden CAPEX säßen die Gläubiger auch nur auf wertlosen Aktien.

Nicht zu vergessen die Rechtsstreitigkeiten, bei denen es um erhebliche Summen geht. Ich kann nicht erkennen, warum sich ein Interessent ausgerechnet mit einem von dermaßen großen Problemen geplagten Hochrisiko-Projekt belasten sollte, wenn gleichzeitig viele bereits produzierende Minen neue Partner willkommen hießen, um die "Dürre" zu überleben.

Antwort auf Beitrag Nr.: 62.016.179 von Kaputzenheini am 26.11.19 15:12:50

Nein, im letzten Hype Richtung $0.40 auszusteigen war goldrichtig. Zum Glück ist dank CYDY meine 2019 mehr als gerettet.

Zitat von Kaputzenheini: An deiner Stelle hätte ich 1/4 behalten

Nein, im letzten Hype Richtung $0.40 auszusteigen war goldrichtig. Zum Glück ist dank CYDY meine 2019 mehr als gerettet.

"My opinion is that the new cost numbers are not achievable in any scenario and the high capital cost required for a commercial plant make the stock a hard sell except to overly optimistic unsophisticated investors and traders relying on the "greater fool" theory for a quick profit. Many who are smart enough to shrewdly trade this stock will make money but those who stay in long term I can only say: "good luck"."

Jow Lowry im Jahr 2015 über über Nemaska.

Jow Lowry im Jahr 2015 über über Nemaska.

Antwort auf Beitrag Nr.: 62.299.430 von Nuggeteer am 07.01.20 07:50:25https://www.linkedin.com/pulse/does-nemaska-matter-joe-lowry

Guten Morgen in die Runde.

Meine Bank teilte mir gerade mit, dass bei Nemaska das Insolvenz erfahren eröffnet wurde.

Meine Bank teilte mir gerade mit, dass bei Nemaska das Insolvenz erfahren eröffnet wurde.

Echt krass,

damit hätte wohl keiner gerechnet.

damit hätte wohl keiner gerechnet.

Antwort auf Beitrag Nr.: 62.310.014 von michii1983 am 08.01.20 07:45:25Echt nicht?

Zitat von Nuggeteer: Die Frage bei Nemaska ist doch, ob das Ding noch vollkommen vor die Wand fährt und der Absturz auf 25c nur eine erste Haltemarke auf dem Weg nach unten war.

Antwort auf Beitrag Nr.: 59.238.898 von bcgk am 17.11.18 09:49:35

Und nun Pleite, hätte ich nie erwartet.

Selbst seriöse Unternehmen in der EU wie Nortvolt hatten schon Abnahmeverträge vereinbart.

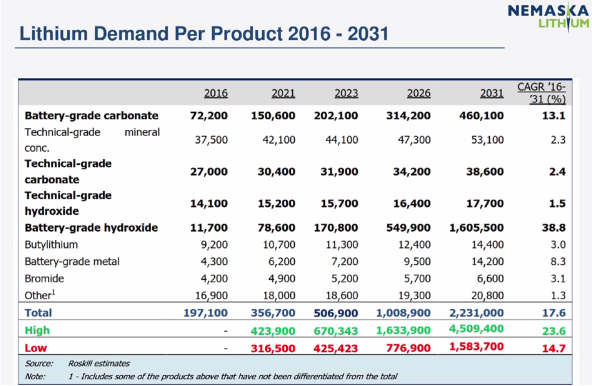

Zitat von bcgk: Hier die wichtigsten Abbildungen aus der aktuellen Präsentation. Wer hier nicht investiert ist, dem ist wahrhaftig nicht zu helfen. As simple as that.

Werde in den mid-70ern (falls wir die nochmal sehen) versuchen nochmal sechsstellig aufzustocken. Der Gesamtmarkt gibt wenig her, daher kann man hier ungeniert zukaufen. Vielleicht schaffe ich die 2*10^6 noch

Und nun Pleite, hätte ich nie erwartet.

Selbst seriöse Unternehmen in der EU wie Nortvolt hatten schon Abnahmeverträge vereinbart.

heute die Meldung, über eine Änderung im Board..ich dachte die sind insolvent und werden abgewickelt.

Hat jemand weitere Infos ?

Hat jemand weitere Infos ?

Antwort auf Beitrag Nr.: 59.938.199 von Nuggeteer am 22.02.19 01:34:52

Heute: "The Board of Directors of Nemaska Lithium is announcing the departure of the President and CEO, Mr. Guy Bourassa, who is leaving the Corporation’s management and his seat on the Board of Directors as of today."

Ein Jahr zu spät!

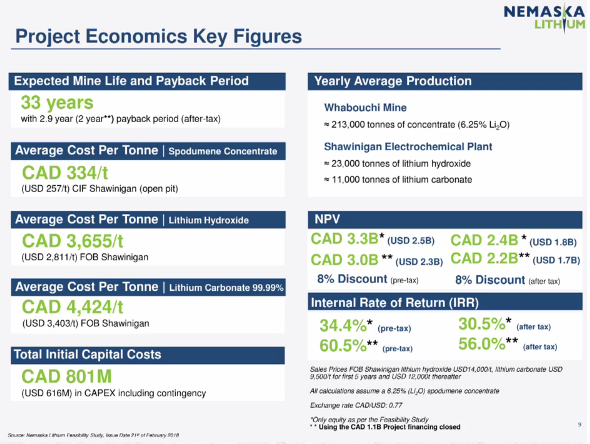

Und alle anderen Befürchtungen aus dem zitierten Beitrag haben sich auch bestätigt. Opex ebenfalls meilenweit daneben, aus angeblich $375M sind über eine Milliarde geworden und letztlich ist die gesamte Finanzierung kollabiert.

Zitat von Nuggeteer: Das bedeute, dass in Wahrheit schon 400 Millionen fehlen. Nach nicht einmal einem Jahr liegt man also schon 1/3 der Gesamtsumme daneben. Und die Kündigung des Abnahmevertrags kostet auch noch einmal 20 Millionen. Dies ist ein dermaßen eklatantes Versagen des Managements, dass es da eigentlich nur eine angemessene Maßnahme geben kann. Es wird kaum jemand noch einmal hunderte Millionen locker machen, ohne dass jemand die Verantwortung für dieses Debakel übernommen hat und entsprechend Konsequenzen gezogen wurden.[...] Es würde mich nicht wundern, wenn es deshalb sehr schwer würde, auf einen Schlag so viel neues Kapital anzulocken. Wer soll diesen Herren glauben, dass es bei 400 Millionen bleiben wird und nicht in weiteren 6-9 Monaten der nächste siebenstellige Nachschlag gefordert wird? Wenn eine Firma bei Capex dermaßen weit daneben liegt, wie steht es dann um die Opex Prognosen? Bevor irgendjemand da nochmal Geld locker macht, wird er viele unangenehme Fragen stellen, jeden Stein umdrehen und alles nochmal ganz genau unter die Lupe nehmen.

Heute: "The Board of Directors of Nemaska Lithium is announcing the departure of the President and CEO, Mr. Guy Bourassa, who is leaving the Corporation’s management and his seat on the Board of Directors as of today."

Ein Jahr zu spät!

Und alle anderen Befürchtungen aus dem zitierten Beitrag haben sich auch bestätigt. Opex ebenfalls meilenweit daneben, aus angeblich $375M sind über eine Milliarde geworden und letztlich ist die gesamte Finanzierung kollabiert.

Wie erwartet: Sollte der "Plan" umgesetzt werden, gehen Altaktionäre komplett leer aus!

"Unfortunately, based on the terms of the Bid and the consideration to be received by Residual Nemaska Lithium, holders of the Corporation’s common shares will not receive any payments for, or distributions on, their common shares in connection with the CCAA proceedings, nor will they hold any interest in New Nemaska Lithium following the completion of the plan of compromise or arrangement."

https://www.nemaskalithium.com/en/investors/press-releases/2…

"Unfortunately, based on the terms of the Bid and the consideration to be received by Residual Nemaska Lithium, holders of the Corporation’s common shares will not receive any payments for, or distributions on, their common shares in connection with the CCAA proceedings, nor will they hold any interest in New Nemaska Lithium following the completion of the plan of compromise or arrangement."

https://www.nemaskalithium.com/en/investors/press-releases/2…

Beitrag zu dieser Diskussion schreiben

Zu dieser Diskussion können keine Beiträge mehr verfasst werden, da der letzte Beitrag vor mehr als zwei Jahren verfasst wurde und die Diskussion daraufhin archiviert wurde.

Bitte wenden Sie sich an feedback@wallstreet-online.de und erfragen Sie die Reaktivierung der Diskussion oder starten Sie eine neue Diskussion.

Investoren beobachten auch:

| Wertpapier | Perf. % |

|---|---|

| +1,27 | |

| -3,39 | |

| -0,22 | |

| +20,00 | |

| -0,89 | |

| -2,43 | |

| 0,00 | |

| 0,00 | |

| +1,00 | |

| -11,83 |

Meistdiskutiert

| Wertpapier | Beiträge | |

|---|---|---|

| 204 | ||

| 190 | ||

| 146 | ||

| 69 | ||

| 32 | ||

| 29 | ||

| 29 | ||

| 26 | ||

| 26 | ||

| 25 |