Aspen Pharmacare - 500 Beiträge pro Seite

eröffnet am 14.03.11 09:28:33 von

neuester Beitrag 09.07.20 23:18:25 von

neuester Beitrag 09.07.20 23:18:25 von

Beiträge: 29

ID: 1.164.587

ID: 1.164.587

Aufrufe heute: 0

Gesamt: 3.190

Gesamt: 3.190

Aktive User: 0

ISIN: ZAE000066692 · WKN: A0ET80 · Symbol: LDZA

10,200

EUR

+0,99 %

+0,100 EUR

Letzter Kurs 14:16:36 Tradegate

Neuigkeiten

Werte aus der Branche Pharmaindustrie

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 3,5800 | +922,86 | |

| 0,8800 | +95,56 | |

| 2.000,00 | +71,23 | |

| 384,00 | +20,00 | |

| 5,9050 | +17,86 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 4,3000 | -21,82 | |

| 14,510 | -32,32 | |

| 71,33 | -33,92 | |

| 3,6400 | -38,62 | |

| 0,7000 | -61,85 |

Aspen increases revenue by 33 percent

03 March 2011

By : Shauneen Beukes

Aspen increases revenue by 33 percent

Johannesburg - JSE Ltd listed Aspen Pharmacare Holdings Limited (Apn), Africa’s largest pharmaceutical manufacturer, has announced pleasing results for the interim period ended 31 December 2010.

Group Performance:

Headline earnings from continuing operations increased by 35 percent to R1.147 billion.

Revenue from continuing operations rose by 33 percent to R5.990 billion (R4.519 billion).

Operating profit from continuing operations improved by 28 percent to R1.614 billion (R1.260 billion).

Headline earnings per share (HEPS) from continuing operations increased by 15 percent to 265.3 cents (230.8 cents).

The rise in headline earnings per share was diluted by an increase in the weighted average number of shares in issue as a consequence of the issue of shares on 1 December 2009 in settlement of the transaction with GlaxoSmithKline (“GSK”) concluded on that date.

Stephen Saad, Aspen Group Chief Executive said, “The South African pharmaceutical division’s consistently good performance ensured that Aspen retained it position as the leader in the South African pharmaceutical market. The successful integration of the GSK business has further contributed and Aspen is now also ranked first in the branded product segment. Aspen’s international and sub-Saharan Africa businesses also performed well, delivering increased revenue and operating profit across the Group”.

South African Business

The South African business increased revenue by 29% to R3.300 billion and improved operating profit by 23% to R0.996 billion. The pharmaceutical division led the growth in revenue raising sales by 36% to R2.682 billion. Consumer division sales were up 8% to R0.618 billion. Profit margins benefited from production efficiencies, procurement savings and the strength of the Rand. The higher insurance compensation received in the prior period inflated the comparative profit margin for that period.

The pharmaceutical business grew ahead of the market in the private sector, increasing Aspen’s share as measured by IMS to 16.7%. Sales of the GSK products for the six months to 31 December 2010 were R463 million against R53 million from one month of sales in the prior period. In the recently adjudicated anti-retroviral (“ARV”) tender, Aspen was awarded 41% by value of the anticipated ARV requirements of the South African government over a two-year period. This validates the cost competitiveness of the Group’s production capabilities.

There has been ongoing investment in the manufacturing capabilities of the Group in South Africa. Most capital projects are well advanced. The focus of these projects has been adding capacity, enhancing technical standards and improving efficiency.

Sub-Saharan Africa Business

Revenue in the sub-Saharan Africa business more than doubled from R279 million to R666 million due to the full period contribution from the GSK Aspen Healthcare for Africa collaboration. Operating profit followed a similar trend, growing from R41 million to R119 million. Performance at Shelys, Aspen’s 60% owned subsidiary in East Africa, improved on the unsatisfactory showing in the second half of the 2010 financial year.

International Business

The international business increased revenue by 39% to R2.423 billion. Revenue benefited by R600 million (2009: R108 million) from the inclusion of the brands and the German-based Bad Oldesloe production facility acquired from GSK in December 2009 for the full period. Asia Pacific revenue was up 28% to R957 million, Latin America revenue increased 20% to R599 million and revenue in the Rest of the World region rose 76% to R867 million. Operating profit before amortisation and once-off items was up 27% to R551 million.

The AUD 900 million (approximately R6.3 billion) acquisition of the pharmaceutical business of Sigma, Australia’s largest listed pharmaceutical company, completed on 31 January 2011. Integration of this business with Aspen Australia is well underway and is progressing to plan.

Prospects

The South African pharmaceutical business has strengthened its position as the market leader over the past period. Performance in the second half of the year will however be affected by the reduced value of the recent ARV tender award. The Minister of Health has announced that no consideration will be given to an increase in the Single Exit Price before the end of 2011.

The South African consumer business will be adversely affected by the ending in April 2011 of the Pfizer infant milk license agreement, which generated annual sales of approximately R250 million. Pfizer has taken the decision to enter the South African market itself following the acquisition of the infant milk franchise as part of its take-over of Wyeth. Aspen has expanded its own infant milk offering with the introduction of the Infacare Gold range in order to replace the Pfizer brands.

The sub-Saharan Africa business is on a firm footing and the positive performance of the first half of the year should be maintained in the second half.

The Asia Pacific region of the International business is set for strong growth as the Sigma pharmaceutical business is integrated into Aspen Australia. The earnings per share impact for this financial year is likely to be close to neutral due to the expensing of transaction fees, stamp duties and restructuring costs expected to exceed R100 million. In years thereafter the transaction is anticipated to be earnings accretive as synergistic benefits are realised.

The International business will continue to transition products acquired from GSK to the Aspen global distribution network. Once complete, the Group will be well positioned to realise procurement and marketing opportunities with these brands.

The Group remains well placed for growth into the medium term. The launch of new products from the extensive product pipeline will provide organic growth across all major markets. The expanded business in the Asia Pacific region is expected to provide further growth momentum. Latin America remains a core focus area for the Group as a region with great potential. Opportunities to add to the portfolio of global brands will be actively pursued.

ends

03 March 2011

By : Shauneen Beukes

Aspen increases revenue by 33 percent

Johannesburg - JSE Ltd listed Aspen Pharmacare Holdings Limited (Apn), Africa’s largest pharmaceutical manufacturer, has announced pleasing results for the interim period ended 31 December 2010.

Group Performance:

Headline earnings from continuing operations increased by 35 percent to R1.147 billion.

Revenue from continuing operations rose by 33 percent to R5.990 billion (R4.519 billion).

Operating profit from continuing operations improved by 28 percent to R1.614 billion (R1.260 billion).

Headline earnings per share (HEPS) from continuing operations increased by 15 percent to 265.3 cents (230.8 cents).

The rise in headline earnings per share was diluted by an increase in the weighted average number of shares in issue as a consequence of the issue of shares on 1 December 2009 in settlement of the transaction with GlaxoSmithKline (“GSK”) concluded on that date.

Stephen Saad, Aspen Group Chief Executive said, “The South African pharmaceutical division’s consistently good performance ensured that Aspen retained it position as the leader in the South African pharmaceutical market. The successful integration of the GSK business has further contributed and Aspen is now also ranked first in the branded product segment. Aspen’s international and sub-Saharan Africa businesses also performed well, delivering increased revenue and operating profit across the Group”.

South African Business

The South African business increased revenue by 29% to R3.300 billion and improved operating profit by 23% to R0.996 billion. The pharmaceutical division led the growth in revenue raising sales by 36% to R2.682 billion. Consumer division sales were up 8% to R0.618 billion. Profit margins benefited from production efficiencies, procurement savings and the strength of the Rand. The higher insurance compensation received in the prior period inflated the comparative profit margin for that period.

The pharmaceutical business grew ahead of the market in the private sector, increasing Aspen’s share as measured by IMS to 16.7%. Sales of the GSK products for the six months to 31 December 2010 were R463 million against R53 million from one month of sales in the prior period. In the recently adjudicated anti-retroviral (“ARV”) tender, Aspen was awarded 41% by value of the anticipated ARV requirements of the South African government over a two-year period. This validates the cost competitiveness of the Group’s production capabilities.

There has been ongoing investment in the manufacturing capabilities of the Group in South Africa. Most capital projects are well advanced. The focus of these projects has been adding capacity, enhancing technical standards and improving efficiency.

Sub-Saharan Africa Business

Revenue in the sub-Saharan Africa business more than doubled from R279 million to R666 million due to the full period contribution from the GSK Aspen Healthcare for Africa collaboration. Operating profit followed a similar trend, growing from R41 million to R119 million. Performance at Shelys, Aspen’s 60% owned subsidiary in East Africa, improved on the unsatisfactory showing in the second half of the 2010 financial year.

International Business

The international business increased revenue by 39% to R2.423 billion. Revenue benefited by R600 million (2009: R108 million) from the inclusion of the brands and the German-based Bad Oldesloe production facility acquired from GSK in December 2009 for the full period. Asia Pacific revenue was up 28% to R957 million, Latin America revenue increased 20% to R599 million and revenue in the Rest of the World region rose 76% to R867 million. Operating profit before amortisation and once-off items was up 27% to R551 million.

The AUD 900 million (approximately R6.3 billion) acquisition of the pharmaceutical business of Sigma, Australia’s largest listed pharmaceutical company, completed on 31 January 2011. Integration of this business with Aspen Australia is well underway and is progressing to plan.

Prospects

The South African pharmaceutical business has strengthened its position as the market leader over the past period. Performance in the second half of the year will however be affected by the reduced value of the recent ARV tender award. The Minister of Health has announced that no consideration will be given to an increase in the Single Exit Price before the end of 2011.

The South African consumer business will be adversely affected by the ending in April 2011 of the Pfizer infant milk license agreement, which generated annual sales of approximately R250 million. Pfizer has taken the decision to enter the South African market itself following the acquisition of the infant milk franchise as part of its take-over of Wyeth. Aspen has expanded its own infant milk offering with the introduction of the Infacare Gold range in order to replace the Pfizer brands.

The sub-Saharan Africa business is on a firm footing and the positive performance of the first half of the year should be maintained in the second half.

The Asia Pacific region of the International business is set for strong growth as the Sigma pharmaceutical business is integrated into Aspen Australia. The earnings per share impact for this financial year is likely to be close to neutral due to the expensing of transaction fees, stamp duties and restructuring costs expected to exceed R100 million. In years thereafter the transaction is anticipated to be earnings accretive as synergistic benefits are realised.

The International business will continue to transition products acquired from GSK to the Aspen global distribution network. Once complete, the Group will be well positioned to realise procurement and marketing opportunities with these brands.

The Group remains well placed for growth into the medium term. The launch of new products from the extensive product pipeline will provide organic growth across all major markets. The expanded business in the Asia Pacific region is expected to provide further growth momentum. Latin America remains a core focus area for the Group as a region with great potential. Opportunities to add to the portfolio of global brands will be actively pursued.

ends

Aspen increases revenue by 29 percent to R12.4 billion

13 September 2011

By : Shauneen Beukes

Johannesburg - JSE Ltd listed Aspen Pharmacare Holdings Limited, the leading pharmaceutical manufacturer in the southern hemisphere, has produced excellent results for the year ended 30 June 2011.

GROUP PERFORMANCE:

Revenue from continuing operations increased by 29% to R12.4 billion (R9,6 billion).

Operating profit from continuing operations improved by 25% to R3.1 billion (R2.5 billion).

Normalised headline earnings from continuing operations rose 29% to R2.4 billion (R1.8 billion).

Diluted normalised headline earnings per share (NHEPS) from continuing operations grew by 20% to 523.3 cents (437.7 cents).

A capital distribution of 105 cents (70 cents) per ordinary share by way of a capital reduction has been declared.

Stephen Saad, Aspen Group Chief Executive said, “The Aspen results are a reflection of the Group’s efforts across all of our key geographies. We had stellar performances in Asia Pacific, Sub-Saharan Africa, Latin America and South Africa. The South African performance was particularly pleasing given the headwinds in the market, namely a 0% increase in selling prices, but cost increases in salaries, wages and electricity. This vindicates our strategic investment in manufacturing infrastructure. The acquisition of the Sigma pharmaceutical business has performed ahead of plan and has contributed to the improved performance in the second half of the year. Next year this impact will be for the entire period.”

SOUTH AFRICA:

Revenue from the South African business increased by 13% to R6.3 billion and operating profit grew 17% to R1.9 billion. The Pharmaceutical division led growth, increasing revenue by 15% to R5.2 billion. This was achieved despite its two biggest brands, Seretide and Truvada, coming under generic competition for the first time, as well as reduced pricing and lower than expected off takes in the new anti-retroviral (ARV) tender which commenced in January 2011. ARV tender volumes have been well below expected levels as Government has used substitute donor funded product. Aspen’s successful strategy to defend the Seretide molecule by launching its own generic, Foxair, has more than compensated for volume declines in Seretide. The Pharmaceutical division is fundamentally in good shape with a strong underlying growth rate. In particular, the Generic division continues to perform, fuelled by the industry’s strongest organic pipeline. This is further validated by Aspen retaining its 2011 Campbell Belman Confidence Predictor Results ranking as the leading pharmaceutical company in South Africa.

Revenue from the Consumer division increased 3% to R1.1 billion in a slow retail market. The division responded to the fourth quarter loss of the Pfizer infant milk formula license, which generated annual sales of approximately R250 million. In response, Aspen launched Infacare Gold as a substitute product range as well as Melegi acidified, a specialist infant formula brand. Aspen participated in the Government tender for infant nutritionals for the first time and was awarded the vast majority of the volume of the products for which it competed. This three-year tender covers eight of South Africa’s nine provinces and will assist in closing the gap left by the Pfizer brands.

The Group has continued to invest in its manufacturing capabilities in South Africa in order to increase capacity, enhance technical standards and improve efficiency. Projects are underway at the Port Elizabeth, East London and Cape Town production sites. Aspen’s production competitiveness continues to be validated by the successes achieved in recent tender awards by the Government for ARVs, tuberculosis, anti-biotics and infant nutritionals where the Group competed with manufacturers from across the world.

SUB-SAHARAN AFRICA:

The Group’s gross revenue in Sub-Saharan Africa advanced by 43% to R1.3 billion and operating profits almost tripled from R66 million to R182 million. A full year’s contribution (prior year 7 months) from the GSK Aspen Healthcare for Africa collaboration assisted in this substantial step-up in results. Wider margins have contributed toward improved performance of East African-based Shelys.

INTERNATIONAL:

The International business increased revenue by 56% to R5.6 billion. Operating profit before amortisation, adjusted for one-off non-trading items, grew 35% to R1.4 billion.

The acquisition of the Australian-based Sigma business was completed with effect from 31 January 2011 for a purchase consideration of AUD 863 million. The addition of the Sigma business was the primary driver in the Asia Pacific region increasing revenue by 122% to R3.1 billion. The original Aspen Australia business also performed strongly, raising revenue by 33% to R1.7 billion. Synergies between the Sigma business and the Aspen Australia business are expected to yield cost of goods reductions from improved procurement and lower manufacturing costs achieved through the Aspen global network.

Aspen’s Latin American businesses generated a 19% increase in revenue to R0.9 billion. Revenue from the Group’s businesses in the rest of the world was up 12% to R1.6 billion.

The disposal of Onco Laboratories was completed in February 2011, realising a profit on disposal of R368 million. This was the largest contributor to profits from discontinued operations.

FUNDING:

Borrowings net of cash were R6.3 billion despite the R5.9 billion investment in the Sigma business, with gearing at 34%.

PROSPECTS:

During the forthcoming year, revenue and profit contributions from the Group’s International businesses are expected to exceed that of the South African business for the first time.

It is anticipated that the Sigma business will lead growth in the Asia Pacific region. The Group’s pipeline for Australia has been further augmented by the conclusion of an agreement with Cipla, the leading Indian generic company, to work together for Aspen to launch Cipla developed products in Australia. Aspen’s representation in the region has taken a further step forward with the commencement of the process to incorporate a subsidiary in the Philippines.

Demographics in South Africa continue to support growth in the utilisation of medicines that could be further accelerated by the introduction of the Government’s National Health Insurance programme.

The South African Department of Health (“DoH”) is presently considering the promulgation of new regulations to implement a process of international benchmarking of originator pharmaceutical products and to cap the logistics fees paid in the distribution of pharmaceuticals. Aspen has been an active participant in the formulation of industry submissions on these proposals. Both proposals are with the DoH for reconsideration. Revised proposals can be anticipated in the year ahead.

The Sub-Saharan African business is well placed to extend its position as the leading supplier of quality pharmaceuticals in that region.

Leadership structures have been strengthened in Latin America and improved focus has been achieved in Brazil with the disposal of non-core products. Aspen continues to regard this region as having significant potential and opportunities are being sought to improve the critical mass of the product offering.

13 September 2011

By : Shauneen Beukes

Johannesburg - JSE Ltd listed Aspen Pharmacare Holdings Limited, the leading pharmaceutical manufacturer in the southern hemisphere, has produced excellent results for the year ended 30 June 2011.

GROUP PERFORMANCE:

Revenue from continuing operations increased by 29% to R12.4 billion (R9,6 billion).

Operating profit from continuing operations improved by 25% to R3.1 billion (R2.5 billion).

Normalised headline earnings from continuing operations rose 29% to R2.4 billion (R1.8 billion).

Diluted normalised headline earnings per share (NHEPS) from continuing operations grew by 20% to 523.3 cents (437.7 cents).

A capital distribution of 105 cents (70 cents) per ordinary share by way of a capital reduction has been declared.

Stephen Saad, Aspen Group Chief Executive said, “The Aspen results are a reflection of the Group’s efforts across all of our key geographies. We had stellar performances in Asia Pacific, Sub-Saharan Africa, Latin America and South Africa. The South African performance was particularly pleasing given the headwinds in the market, namely a 0% increase in selling prices, but cost increases in salaries, wages and electricity. This vindicates our strategic investment in manufacturing infrastructure. The acquisition of the Sigma pharmaceutical business has performed ahead of plan and has contributed to the improved performance in the second half of the year. Next year this impact will be for the entire period.”

SOUTH AFRICA:

Revenue from the South African business increased by 13% to R6.3 billion and operating profit grew 17% to R1.9 billion. The Pharmaceutical division led growth, increasing revenue by 15% to R5.2 billion. This was achieved despite its two biggest brands, Seretide and Truvada, coming under generic competition for the first time, as well as reduced pricing and lower than expected off takes in the new anti-retroviral (ARV) tender which commenced in January 2011. ARV tender volumes have been well below expected levels as Government has used substitute donor funded product. Aspen’s successful strategy to defend the Seretide molecule by launching its own generic, Foxair, has more than compensated for volume declines in Seretide. The Pharmaceutical division is fundamentally in good shape with a strong underlying growth rate. In particular, the Generic division continues to perform, fuelled by the industry’s strongest organic pipeline. This is further validated by Aspen retaining its 2011 Campbell Belman Confidence Predictor Results ranking as the leading pharmaceutical company in South Africa.

Revenue from the Consumer division increased 3% to R1.1 billion in a slow retail market. The division responded to the fourth quarter loss of the Pfizer infant milk formula license, which generated annual sales of approximately R250 million. In response, Aspen launched Infacare Gold as a substitute product range as well as Melegi acidified, a specialist infant formula brand. Aspen participated in the Government tender for infant nutritionals for the first time and was awarded the vast majority of the volume of the products for which it competed. This three-year tender covers eight of South Africa’s nine provinces and will assist in closing the gap left by the Pfizer brands.

The Group has continued to invest in its manufacturing capabilities in South Africa in order to increase capacity, enhance technical standards and improve efficiency. Projects are underway at the Port Elizabeth, East London and Cape Town production sites. Aspen’s production competitiveness continues to be validated by the successes achieved in recent tender awards by the Government for ARVs, tuberculosis, anti-biotics and infant nutritionals where the Group competed with manufacturers from across the world.

SUB-SAHARAN AFRICA:

The Group’s gross revenue in Sub-Saharan Africa advanced by 43% to R1.3 billion and operating profits almost tripled from R66 million to R182 million. A full year’s contribution (prior year 7 months) from the GSK Aspen Healthcare for Africa collaboration assisted in this substantial step-up in results. Wider margins have contributed toward improved performance of East African-based Shelys.

INTERNATIONAL:

The International business increased revenue by 56% to R5.6 billion. Operating profit before amortisation, adjusted for one-off non-trading items, grew 35% to R1.4 billion.

The acquisition of the Australian-based Sigma business was completed with effect from 31 January 2011 for a purchase consideration of AUD 863 million. The addition of the Sigma business was the primary driver in the Asia Pacific region increasing revenue by 122% to R3.1 billion. The original Aspen Australia business also performed strongly, raising revenue by 33% to R1.7 billion. Synergies between the Sigma business and the Aspen Australia business are expected to yield cost of goods reductions from improved procurement and lower manufacturing costs achieved through the Aspen global network.

Aspen’s Latin American businesses generated a 19% increase in revenue to R0.9 billion. Revenue from the Group’s businesses in the rest of the world was up 12% to R1.6 billion.

The disposal of Onco Laboratories was completed in February 2011, realising a profit on disposal of R368 million. This was the largest contributor to profits from discontinued operations.

FUNDING:

Borrowings net of cash were R6.3 billion despite the R5.9 billion investment in the Sigma business, with gearing at 34%.

PROSPECTS:

During the forthcoming year, revenue and profit contributions from the Group’s International businesses are expected to exceed that of the South African business for the first time.

It is anticipated that the Sigma business will lead growth in the Asia Pacific region. The Group’s pipeline for Australia has been further augmented by the conclusion of an agreement with Cipla, the leading Indian generic company, to work together for Aspen to launch Cipla developed products in Australia. Aspen’s representation in the region has taken a further step forward with the commencement of the process to incorporate a subsidiary in the Philippines.

Demographics in South Africa continue to support growth in the utilisation of medicines that could be further accelerated by the introduction of the Government’s National Health Insurance programme.

The South African Department of Health (“DoH”) is presently considering the promulgation of new regulations to implement a process of international benchmarking of originator pharmaceutical products and to cap the logistics fees paid in the distribution of pharmaceuticals. Aspen has been an active participant in the formulation of industry submissions on these proposals. Both proposals are with the DoH for reconsideration. Revised proposals can be anticipated in the year ahead.

The Sub-Saharan African business is well placed to extend its position as the leading supplier of quality pharmaceuticals in that region.

Leadership structures have been strengthened in Latin America and improved focus has been achieved in Brazil with the disposal of non-core products. Aspen continues to regard this region as having significant potential and opportunities are being sought to improve the critical mass of the product offering.

Aspen increases revenue by 29 percent to R12.4 billion

13 September 2011

By : Shauneen Beukes

Johannesburg - JSE Ltd listed Aspen Pharmacare Holdings Limited, the leading pharmaceutical manufacturer in the southern hemisphere, has produced excellent results for the year ended 30 June 2011.

GROUP PERFORMANCE:

Revenue from continuing operations increased by 29% to R12.4 billion (R9,6 billion).

Operating profit from continuing operations improved by 25% to R3.1 billion (R2.5 billion).

Normalised headline earnings from continuing operations rose 29% to R2.4 billion (R1.8 billion).

Diluted normalised headline earnings per share (NHEPS) from continuing operations grew by 20% to 523.3 cents (437.7 cents).

A capital distribution of 105 cents (70 cents) per ordinary share by way of a capital reduction has been declared.

Stephen Saad, Aspen Group Chief Executive said, “The Aspen results are a reflection of the Group’s efforts across all of our key geographies. We had stellar performances in Asia Pacific, Sub-Saharan Africa, Latin America and South Africa. The South African performance was particularly pleasing given the headwinds in the market, namely a 0% increase in selling prices, but cost increases in salaries, wages and electricity. This vindicates our strategic investment in manufacturing infrastructure. The acquisition of the Sigma pharmaceutical business has performed ahead of plan and has contributed to the improved performance in the second half of the year. Next year this impact will be for the entire period.”

SOUTH AFRICA:

Revenue from the South African business increased by 13% to R6.3 billion and operating profit grew 17% to R1.9 billion. The Pharmaceutical division led growth, increasing revenue by 15% to R5.2 billion. This was achieved despite its two biggest brands, Seretide and Truvada, coming under generic competition for the first time, as well as reduced pricing and lower than expected off takes in the new anti-retroviral (ARV) tender which commenced in January 2011. ARV tender volumes have been well below expected levels as Government has used substitute donor funded product. Aspen’s successful strategy to defend the Seretide molecule by launching its own generic, Foxair, has more than compensated for volume declines in Seretide. The Pharmaceutical division is fundamentally in good shape with a strong underlying growth rate. In particular, the Generic division continues to perform, fuelled by the industry’s strongest organic pipeline. This is further validated by Aspen retaining its 2011 Campbell Belman Confidence Predictor Results ranking as the leading pharmaceutical company in South Africa.

Revenue from the Consumer division increased 3% to R1.1 billion in a slow retail market. The division responded to the fourth quarter loss of the Pfizer infant milk formula license, which generated annual sales of approximately R250 million. In response, Aspen launched Infacare Gold as a substitute product range as well as Melegi acidified, a specialist infant formula brand. Aspen participated in the Government tender for infant nutritionals for the first time and was awarded the vast majority of the volume of the products for which it competed. This three-year tender covers eight of South Africa’s nine provinces and will assist in closing the gap left by the Pfizer brands.

The Group has continued to invest in its manufacturing capabilities in South Africa in order to increase capacity, enhance technical standards and improve efficiency. Projects are underway at the Port Elizabeth, East London and Cape Town production sites. Aspen’s production competitiveness continues to be validated by the successes achieved in recent tender awards by the Government for ARVs, tuberculosis, anti-biotics and infant nutritionals where the Group competed with manufacturers from across the world.

SUB-SAHARAN AFRICA:

The Group’s gross revenue in Sub-Saharan Africa advanced by 43% to R1.3 billion and operating profits almost tripled from R66 million to R182 million. A full year’s contribution (prior year 7 months) from the GSK Aspen Healthcare for Africa collaboration assisted in this substantial step-up in results. Wider margins have contributed toward improved performance of East African-based Shelys.

INTERNATIONAL:

The International business increased revenue by 56% to R5.6 billion. Operating profit before amortisation, adjusted for one-off non-trading items, grew 35% to R1.4 billion.

The acquisition of the Australian-based Sigma business was completed with effect from 31 January 2011 for a purchase consideration of AUD 863 million. The addition of the Sigma business was the primary driver in the Asia Pacific region increasing revenue by 122% to R3.1 billion. The original Aspen Australia business also performed strongly, raising revenue by 33% to R1.7 billion. Synergies between the Sigma business and the Aspen Australia business are expected to yield cost of goods reductions from improved procurement and lower manufacturing costs achieved through the Aspen global network.

Aspen’s Latin American businesses generated a 19% increase in revenue to R0.9 billion. Revenue from the Group’s businesses in the rest of the world was up 12% to R1.6 billion.

The disposal of Onco Laboratories was completed in February 2011, realising a profit on disposal of R368 million. This was the largest contributor to profits from discontinued operations.

FUNDING:

Borrowings net of cash were R6.3 billion despite the R5.9 billion investment in the Sigma business, with gearing at 34%.

PROSPECTS:

During the forthcoming year, revenue and profit contributions from the Group’s International businesses are expected to exceed that of the South African business for the first time.

It is anticipated that the Sigma business will lead growth in the Asia Pacific region. The Group’s pipeline for Australia has been further augmented by the conclusion of an agreement with Cipla, the leading Indian generic company, to work together for Aspen to launch Cipla developed products in Australia. Aspen’s representation in the region has taken a further step forward with the commencement of the process to incorporate a subsidiary in the Philippines.

Demographics in South Africa continue to support growth in the utilisation of medicines that could be further accelerated by the introduction of the Government’s National Health Insurance programme.

The South African Department of Health (“DoH”) is presently considering the promulgation of new regulations to implement a process of international benchmarking of originator pharmaceutical products and to cap the logistics fees paid in the distribution of pharmaceuticals. Aspen has been an active participant in the formulation of industry submissions on these proposals. Both proposals are with the DoH for reconsideration. Revised proposals can be anticipated in the year ahead.

The Sub-Saharan African business is well placed to extend its position as the leading supplier of quality pharmaceuticals in that region.

Leadership structures have been strengthened in Latin America and improved focus has been achieved in Brazil with the disposal of non-core products. Aspen continues to regard this region as having significant potential and opportunities are being sought to improve the critical mass of the product offering.

13 September 2011

By : Shauneen Beukes

Johannesburg - JSE Ltd listed Aspen Pharmacare Holdings Limited, the leading pharmaceutical manufacturer in the southern hemisphere, has produced excellent results for the year ended 30 June 2011.

GROUP PERFORMANCE:

Revenue from continuing operations increased by 29% to R12.4 billion (R9,6 billion).

Operating profit from continuing operations improved by 25% to R3.1 billion (R2.5 billion).

Normalised headline earnings from continuing operations rose 29% to R2.4 billion (R1.8 billion).

Diluted normalised headline earnings per share (NHEPS) from continuing operations grew by 20% to 523.3 cents (437.7 cents).

A capital distribution of 105 cents (70 cents) per ordinary share by way of a capital reduction has been declared.

Stephen Saad, Aspen Group Chief Executive said, “The Aspen results are a reflection of the Group’s efforts across all of our key geographies. We had stellar performances in Asia Pacific, Sub-Saharan Africa, Latin America and South Africa. The South African performance was particularly pleasing given the headwinds in the market, namely a 0% increase in selling prices, but cost increases in salaries, wages and electricity. This vindicates our strategic investment in manufacturing infrastructure. The acquisition of the Sigma pharmaceutical business has performed ahead of plan and has contributed to the improved performance in the second half of the year. Next year this impact will be for the entire period.”

SOUTH AFRICA:

Revenue from the South African business increased by 13% to R6.3 billion and operating profit grew 17% to R1.9 billion. The Pharmaceutical division led growth, increasing revenue by 15% to R5.2 billion. This was achieved despite its two biggest brands, Seretide and Truvada, coming under generic competition for the first time, as well as reduced pricing and lower than expected off takes in the new anti-retroviral (ARV) tender which commenced in January 2011. ARV tender volumes have been well below expected levels as Government has used substitute donor funded product. Aspen’s successful strategy to defend the Seretide molecule by launching its own generic, Foxair, has more than compensated for volume declines in Seretide. The Pharmaceutical division is fundamentally in good shape with a strong underlying growth rate. In particular, the Generic division continues to perform, fuelled by the industry’s strongest organic pipeline. This is further validated by Aspen retaining its 2011 Campbell Belman Confidence Predictor Results ranking as the leading pharmaceutical company in South Africa.

Revenue from the Consumer division increased 3% to R1.1 billion in a slow retail market. The division responded to the fourth quarter loss of the Pfizer infant milk formula license, which generated annual sales of approximately R250 million. In response, Aspen launched Infacare Gold as a substitute product range as well as Melegi acidified, a specialist infant formula brand. Aspen participated in the Government tender for infant nutritionals for the first time and was awarded the vast majority of the volume of the products for which it competed. This three-year tender covers eight of South Africa’s nine provinces and will assist in closing the gap left by the Pfizer brands.

The Group has continued to invest in its manufacturing capabilities in South Africa in order to increase capacity, enhance technical standards and improve efficiency. Projects are underway at the Port Elizabeth, East London and Cape Town production sites. Aspen’s production competitiveness continues to be validated by the successes achieved in recent tender awards by the Government for ARVs, tuberculosis, anti-biotics and infant nutritionals where the Group competed with manufacturers from across the world.

SUB-SAHARAN AFRICA:

The Group’s gross revenue in Sub-Saharan Africa advanced by 43% to R1.3 billion and operating profits almost tripled from R66 million to R182 million. A full year’s contribution (prior year 7 months) from the GSK Aspen Healthcare for Africa collaboration assisted in this substantial step-up in results. Wider margins have contributed toward improved performance of East African-based Shelys.

INTERNATIONAL:

The International business increased revenue by 56% to R5.6 billion. Operating profit before amortisation, adjusted for one-off non-trading items, grew 35% to R1.4 billion.

The acquisition of the Australian-based Sigma business was completed with effect from 31 January 2011 for a purchase consideration of AUD 863 million. The addition of the Sigma business was the primary driver in the Asia Pacific region increasing revenue by 122% to R3.1 billion. The original Aspen Australia business also performed strongly, raising revenue by 33% to R1.7 billion. Synergies between the Sigma business and the Aspen Australia business are expected to yield cost of goods reductions from improved procurement and lower manufacturing costs achieved through the Aspen global network.

Aspen’s Latin American businesses generated a 19% increase in revenue to R0.9 billion. Revenue from the Group’s businesses in the rest of the world was up 12% to R1.6 billion.

The disposal of Onco Laboratories was completed in February 2011, realising a profit on disposal of R368 million. This was the largest contributor to profits from discontinued operations.

FUNDING:

Borrowings net of cash were R6.3 billion despite the R5.9 billion investment in the Sigma business, with gearing at 34%.

PROSPECTS:

During the forthcoming year, revenue and profit contributions from the Group’s International businesses are expected to exceed that of the South African business for the first time.

It is anticipated that the Sigma business will lead growth in the Asia Pacific region. The Group’s pipeline for Australia has been further augmented by the conclusion of an agreement with Cipla, the leading Indian generic company, to work together for Aspen to launch Cipla developed products in Australia. Aspen’s representation in the region has taken a further step forward with the commencement of the process to incorporate a subsidiary in the Philippines.

Demographics in South Africa continue to support growth in the utilisation of medicines that could be further accelerated by the introduction of the Government’s National Health Insurance programme.

The South African Department of Health (“DoH”) is presently considering the promulgation of new regulations to implement a process of international benchmarking of originator pharmaceutical products and to cap the logistics fees paid in the distribution of pharmaceuticals. Aspen has been an active participant in the formulation of industry submissions on these proposals. Both proposals are with the DoH for reconsideration. Revised proposals can be anticipated in the year ahead.

The Sub-Saharan African business is well placed to extend its position as the leading supplier of quality pharmaceuticals in that region.

Leadership structures have been strengthened in Latin America and improved focus has been achieved in Brazil with the disposal of non-core products. Aspen continues to regard this region as having significant potential and opportunities are being sought to improve the critical mass of the product offering.

Aspen increases revenue by 31 percent

07 March 2012

By : Shauneen Beukes

Johannesburg - JSE Ltd listed Aspen Pharmacare Holdings Limited (Apn), Africa’s largest pharmaceutical manufacturer, has announced pleasing results for the interim period ended 31 December 2011, once again proving Aspen’s resilience across its global businesses.

Group Performance

Revenue from continuing operations rose by 31 percent to R7.5 billion (R5.7 billion).

Operating profit before amortisation from continuing operations adjusted for specific non-trading items (“EBITA”), improved by 32 percent to R2.2 billion (R1.6 billion)

Diluted normalised headline earnings per share (DNHEPS) from continuing operations increased by 22 percent to 308.1 cents (253.3 cents).

Growth in earnings was affected by higher funding costs on the debt raised to acquire the pharmaceutical division of Sigma Pharmaceuticals Limited in Australia (“the Sigma business”) in January 2011.

Stephen Saad, Aspen Group Chief Executive said, “The Group’s strong showing for the period was the result of excellent performances across the offshore territories with Asia Pacific leading the way. The Asia Pacific region increased its contribution to Group EBITA from 8% to 34% in the current period.”

(detailliertere Infos auf www.aspenpharma.com)

07 March 2012

By : Shauneen Beukes

Johannesburg - JSE Ltd listed Aspen Pharmacare Holdings Limited (Apn), Africa’s largest pharmaceutical manufacturer, has announced pleasing results for the interim period ended 31 December 2011, once again proving Aspen’s resilience across its global businesses.

Group Performance

Revenue from continuing operations rose by 31 percent to R7.5 billion (R5.7 billion).

Operating profit before amortisation from continuing operations adjusted for specific non-trading items (“EBITA”), improved by 32 percent to R2.2 billion (R1.6 billion)

Diluted normalised headline earnings per share (DNHEPS) from continuing operations increased by 22 percent to 308.1 cents (253.3 cents).

Growth in earnings was affected by higher funding costs on the debt raised to acquire the pharmaceutical division of Sigma Pharmaceuticals Limited in Australia (“the Sigma business”) in January 2011.

Stephen Saad, Aspen Group Chief Executive said, “The Group’s strong showing for the period was the result of excellent performances across the offshore territories with Asia Pacific leading the way. The Asia Pacific region increased its contribution to Group EBITA from 8% to 34% in the current period.”

(detailliertere Infos auf www.aspenpharma.com)

12 September 2012

By : Shauneen Beukes

JSE Ltd listed Aspen Pharmacare Holdings Limited (APN), Africa’s largest pharmaceutical manufacturer, has announced pleasing results for the year ended 30 June 2012, extending its record of growth for a fourteenth consecutive year.

Group Performance

Revenue from continuing operations rose by 23 percent to R15.3 billion.

Operating profit from continuing operations increased by 25 percent to R3.9 billion.

Normalised headline earnings from continuing operations, being headline earnings from continuing operations adjusted for restructuring costs, transaction costs and a foreign exchange gain on transaction funding, increased by 22% to R2.9 billion.

Normalised diluted headline earnings per share from continuing operations rose 22 percent to 636.2 cents.

A capital distribution of 157 cents per ordinary share (2011: 105 cents) by way of a capital reduction payable out of share premium.

Stephen Saad, Aspen Group Chief Executive said, “During the year Aspen increased its diversity in product offerings and geographic exposure. The Group’s positive performance was led by exceptional growth in the Asia Pacific business, while the International business and the Sub-Saharan Africa business also achieved strong gains. The South African business had a positive second half, but consistent with previously communicated expectations, showed negative growth for the year as a whole.”

South African Business

The South African business returned to growth in the second half, as projected. A number of well-documented once-off factors unfavourably influenced results, particularly in the first six months of the year. The effect of the difficult first half is evident in full year revenue being 2% lower at R6.2 billion and operating profit before amortisation, adjusted for specific non-trading items (“EBITA”), being down 9% at R1.8 billion.

Revenue in the Pharmaceutical division was up 9% in the second half resulting in the full year revenue coming in flat at R5.2 billion. This creditable result was achieved against a backdrop of a strike, government procurement of anti-retrovirals (“ARVs”) from donors in preference to accessing the awarded tender and the two biggest products in the Pharmaceutical division, Seretide and Truvada, facing generic competition for the first time. These set-backs were mitigated over the course of the year through Aspen’s success with Foxair, the generic of Seretide and by the launch of Tribuss, the first generic once-a-day triple combination ARV in South Africa. Furthermore, with the depletion of the donor funds, the tender offtake regularised in the second half of the year. Profit margin percentages were reduced for the year, affected by energy costs and wage inflation rising considerably more rapidly than the 2.14% increase in the single exit price granted by the Department of Health. Lower pricing in the ARV tender also contributed to the margin squeeze. Fortunately Aspen managed to offset most of the margin pressure through efficiency gains in production.

The Consumer division suffered a contraction in revenue of 11% to R1.0 billion. The major factor was the expiry towards the end of the 2011 financial year of the license with Pfizer for a range of infant milk products, which contributed approximately R250 million to revenue on an annual basis. Growth of over 20% in Aspen’s infant milk brand, Infacare, has been effective in reducing the impact of the reversal.

The Group has continued to invest in capital projects to upgrade and expand production capabilities in Port Elizabeth and in East London. A major refurbishment of the active pharmaceutical ingredient facility at the Fine Chemicals business in Cape Town is also underway.

Asia Pacific business

The Asia Pacific business, bolstered by the acquisition of the Sigma pharmaceutical business in Australia in the second half of the 2011 financial year, delivered exceptional results. This region has increased its contribution to Group revenue from 23% to 37%. Revenue doubled to R6.0 billion and EBITA grew by 128% to R1.5 billion.

The business acquired from Sigma has been fully integrated with Aspen’s pre-existing business in Australia. Synergies have been gained in the establishment of a single business platform. Further benefits have come through reduced cost of goods which have been realised by taking advantage of Aspen’s competitive manufacturing and procurement competencies.

Aspen Philippines commenced trade during the year and has approximately 100 sales personnel actively deployed.

International Business

The International business recorded a 3% reduction in revenue to R2.5 billion, but nevertheless raised EBITA by 28% to R0.9 billion. Customer sales in Latin America increased 11% to R1.0 billion buoyed by strong performances in Brazil and Venezuela. In Mexico sales were flat, but revenue was sacrificed to third party distributors of global brands in the balance of the territory. The overall reduction in revenue in the International business was as a consequence of the transitioning of certain global brands to third party distributors and the elimination of low margin sales to third parties. Profit margins benefitted from the ongoing projects to reduce the cost of goods of global brands.

Sub-Saharan Africa business

In Sub-Saharan Africa, gross revenue increased by 27% to R1.7 billion and EBITA improved 40% to R248 million. Growth in profit was achieved by each of the three elements of the business. The GSK Aspen Healthcare for Africa collaboration advanced revenue strongly with increased representation and new product launches. The Shelys operation, based in East Africa, achieved excellent margin gains through improved business efficiency. Exports into the region also increased.

Prospects

Aspen has withstood the challenges of the last year and has remained the top supplier of medicines in South Africa. One in four prescriptions dispensed in the country in the private sector is for an Aspen product. The Group’s leadership position in the public sector was endorsed with the recent award of the oral solid dose tender with Aspen once again receiving the largest allocation of 25%. The benefits of a strong product pipeline will see increased growth momentum in the 2013 financial year. A number of legislative changes remain under consideration by the regulator, including international benchmarking and the capping of logistics fees. The timing and consequences of the resolution of these matters remain uncertain. The South African government’s policy decision to support domestic manufacturers in future public sector tenders is welcomed and will be of assistance to Aspen in the upcoming ARV tender due for award in December 2012. The Consumer division is targeting an improved performance supported by innovation in the infant nutritionals range.

The Asia Pacific business is destined to become Aspen’s biggest contributor to revenue once it commences distribution of the portfolio of 25 established pharmaceutical brands which the Group has agreed to acquire from GlaxoSmithKline. Completion of this transaction is conditional upon the approval of the Australian competition authorities which is expected in the last quarter of 2012. Aspen is uniquely positioned in the Australian market with the most extensive product offering which spans branded, generic, over-the-counter and consumer products.

Prospects for future growth from South East Asian markets is being actively explored. Trade has commenced in Aspen’s newly established subsidiary in the Philippines and the feasibility of expansion into Thailand, Taiwan and Malaysia is presently under investigation.

The Group continues to see Latin America as the area of greatest growth potential within the International business. Aspen will seek opportunities to establish a presence in further Latin American territories in addition to the existing operations in Brazil, Venezuela and Mexico. Expansion of its portfolio of global brands remains a focus area for the Group in the year ahead.

There are a number of new product launches planned in Sub-Saharan Africa over the next year to support growth initiatives. The region does however remain vulnerable to political instability.

The Group will continue to focus on strengthening existing businesses, extending territorial coverage and increasing the product offering in areas which offer good future growth potential.

By : Shauneen Beukes

JSE Ltd listed Aspen Pharmacare Holdings Limited (APN), Africa’s largest pharmaceutical manufacturer, has announced pleasing results for the year ended 30 June 2012, extending its record of growth for a fourteenth consecutive year.

Group Performance

Revenue from continuing operations rose by 23 percent to R15.3 billion.

Operating profit from continuing operations increased by 25 percent to R3.9 billion.

Normalised headline earnings from continuing operations, being headline earnings from continuing operations adjusted for restructuring costs, transaction costs and a foreign exchange gain on transaction funding, increased by 22% to R2.9 billion.

Normalised diluted headline earnings per share from continuing operations rose 22 percent to 636.2 cents.

A capital distribution of 157 cents per ordinary share (2011: 105 cents) by way of a capital reduction payable out of share premium.

Stephen Saad, Aspen Group Chief Executive said, “During the year Aspen increased its diversity in product offerings and geographic exposure. The Group’s positive performance was led by exceptional growth in the Asia Pacific business, while the International business and the Sub-Saharan Africa business also achieved strong gains. The South African business had a positive second half, but consistent with previously communicated expectations, showed negative growth for the year as a whole.”

South African Business

The South African business returned to growth in the second half, as projected. A number of well-documented once-off factors unfavourably influenced results, particularly in the first six months of the year. The effect of the difficult first half is evident in full year revenue being 2% lower at R6.2 billion and operating profit before amortisation, adjusted for specific non-trading items (“EBITA”), being down 9% at R1.8 billion.

Revenue in the Pharmaceutical division was up 9% in the second half resulting in the full year revenue coming in flat at R5.2 billion. This creditable result was achieved against a backdrop of a strike, government procurement of anti-retrovirals (“ARVs”) from donors in preference to accessing the awarded tender and the two biggest products in the Pharmaceutical division, Seretide and Truvada, facing generic competition for the first time. These set-backs were mitigated over the course of the year through Aspen’s success with Foxair, the generic of Seretide and by the launch of Tribuss, the first generic once-a-day triple combination ARV in South Africa. Furthermore, with the depletion of the donor funds, the tender offtake regularised in the second half of the year. Profit margin percentages were reduced for the year, affected by energy costs and wage inflation rising considerably more rapidly than the 2.14% increase in the single exit price granted by the Department of Health. Lower pricing in the ARV tender also contributed to the margin squeeze. Fortunately Aspen managed to offset most of the margin pressure through efficiency gains in production.

The Consumer division suffered a contraction in revenue of 11% to R1.0 billion. The major factor was the expiry towards the end of the 2011 financial year of the license with Pfizer for a range of infant milk products, which contributed approximately R250 million to revenue on an annual basis. Growth of over 20% in Aspen’s infant milk brand, Infacare, has been effective in reducing the impact of the reversal.

The Group has continued to invest in capital projects to upgrade and expand production capabilities in Port Elizabeth and in East London. A major refurbishment of the active pharmaceutical ingredient facility at the Fine Chemicals business in Cape Town is also underway.

Asia Pacific business

The Asia Pacific business, bolstered by the acquisition of the Sigma pharmaceutical business in Australia in the second half of the 2011 financial year, delivered exceptional results. This region has increased its contribution to Group revenue from 23% to 37%. Revenue doubled to R6.0 billion and EBITA grew by 128% to R1.5 billion.

The business acquired from Sigma has been fully integrated with Aspen’s pre-existing business in Australia. Synergies have been gained in the establishment of a single business platform. Further benefits have come through reduced cost of goods which have been realised by taking advantage of Aspen’s competitive manufacturing and procurement competencies.

Aspen Philippines commenced trade during the year and has approximately 100 sales personnel actively deployed.

International Business

The International business recorded a 3% reduction in revenue to R2.5 billion, but nevertheless raised EBITA by 28% to R0.9 billion. Customer sales in Latin America increased 11% to R1.0 billion buoyed by strong performances in Brazil and Venezuela. In Mexico sales were flat, but revenue was sacrificed to third party distributors of global brands in the balance of the territory. The overall reduction in revenue in the International business was as a consequence of the transitioning of certain global brands to third party distributors and the elimination of low margin sales to third parties. Profit margins benefitted from the ongoing projects to reduce the cost of goods of global brands.

Sub-Saharan Africa business

In Sub-Saharan Africa, gross revenue increased by 27% to R1.7 billion and EBITA improved 40% to R248 million. Growth in profit was achieved by each of the three elements of the business. The GSK Aspen Healthcare for Africa collaboration advanced revenue strongly with increased representation and new product launches. The Shelys operation, based in East Africa, achieved excellent margin gains through improved business efficiency. Exports into the region also increased.

Prospects

Aspen has withstood the challenges of the last year and has remained the top supplier of medicines in South Africa. One in four prescriptions dispensed in the country in the private sector is for an Aspen product. The Group’s leadership position in the public sector was endorsed with the recent award of the oral solid dose tender with Aspen once again receiving the largest allocation of 25%. The benefits of a strong product pipeline will see increased growth momentum in the 2013 financial year. A number of legislative changes remain under consideration by the regulator, including international benchmarking and the capping of logistics fees. The timing and consequences of the resolution of these matters remain uncertain. The South African government’s policy decision to support domestic manufacturers in future public sector tenders is welcomed and will be of assistance to Aspen in the upcoming ARV tender due for award in December 2012. The Consumer division is targeting an improved performance supported by innovation in the infant nutritionals range.

The Asia Pacific business is destined to become Aspen’s biggest contributor to revenue once it commences distribution of the portfolio of 25 established pharmaceutical brands which the Group has agreed to acquire from GlaxoSmithKline. Completion of this transaction is conditional upon the approval of the Australian competition authorities which is expected in the last quarter of 2012. Aspen is uniquely positioned in the Australian market with the most extensive product offering which spans branded, generic, over-the-counter and consumer products.

Prospects for future growth from South East Asian markets is being actively explored. Trade has commenced in Aspen’s newly established subsidiary in the Philippines and the feasibility of expansion into Thailand, Taiwan and Malaysia is presently under investigation.

The Group continues to see Latin America as the area of greatest growth potential within the International business. Aspen will seek opportunities to establish a presence in further Latin American territories in addition to the existing operations in Brazil, Venezuela and Mexico. Expansion of its portfolio of global brands remains a focus area for the Group in the year ahead.

There are a number of new product launches planned in Sub-Saharan Africa over the next year to support growth initiatives. The region does however remain vulnerable to political instability.

The Group will continue to focus on strengthening existing businesses, extending territorial coverage and increasing the product offering in areas which offer good future growth potential.

Trading Spotlight

Bombenzahlen für 2013/14:

Reviewed provisional Group financial results for the year ended 30 June 2014

- Normalised headline earnings per share increased 27% to 1 064,2 cents

- Earnings per share increased 42% to 1 097,9 cents

- Headline earnings per share increased 29% to 1 016,3 cents

- Distribution to shareholders per share increased 20% to 188 cents

- Operating profit increased 47% to R7,4 billion

- Revenue increased 53% to R29,5 billion

- Significant acquisitions amounting to R19,8 billion concluded during the year

- Offshore contribution increased to 78% of Group operating profit

Reviewed provisional Group financial results for the year ended 30 June 2014

- Normalised headline earnings per share increased 27% to 1 064,2 cents

- Earnings per share increased 42% to 1 097,9 cents

- Headline earnings per share increased 29% to 1 016,3 cents

- Distribution to shareholders per share increased 20% to 188 cents

- Operating profit increased 47% to R7,4 billion

- Revenue increased 53% to R29,5 billion

- Significant acquisitions amounting to R19,8 billion concluded during the year

- Offshore contribution increased to 78% of Group operating profit

... und sie steigt, als gäbe es kein Morgen!

verkauft bis auf ein Erinnerungsstück;

durch Schulden finanzierter goodwill ist mir ein bisschen zuviel geworden

durch Schulden finanzierter goodwill ist mir ein bisschen zuviel geworden

Kommt auf meine Watchlist.

1. Halbjahr 2015:

http://3u8n9x34n0y14cxsva1mzqsa.wpengine.netdna-cdn.com/wp-c…

1. Halbjahr 2015:

http://3u8n9x34n0y14cxsva1mzqsa.wpengine.netdna-cdn.com/wp-c…

Antwort auf Beitrag Nr.: 48.275.287 von R-BgO am 10.11.14 16:20:00

vielleicht doch wieder einsteigen?

Kurs hat sich ja etwas beruhigt

und das letzte GJ gab es "nur" EPS +4%;vielleicht doch wieder einsteigen?

Antwort auf Beitrag Nr.: 48.275.287 von R-BgO am 10.11.14 16:20:00

jetzt doch wieder zurückgekauft

ungefähr ein Viertel günstiger

Kennt jemand eine Seite, wo man ein paar Fundamentaldaten zu diesem Wert sieht (KBV, KGV etc.)? Mein Online-Broker schafft es gerade mal die market cap anzuzeigen... ^^

Antwort auf Beitrag Nr.: 51.616.027 von cash_is_king am 30.01.16 03:48:30Hi,

ich schaue oft hier nach, um mir einen Überblick zu verschaffen.

Ich weiß allerdings nicht genau, ob die Zahlen so korrekt sind, wie sie da stehen.

http://de.4-traders.com/ASPEN-PHARMACARE-HOLDINGS-1413350/?t…

ich schaue oft hier nach, um mir einen Überblick zu verschaffen.

Ich weiß allerdings nicht genau, ob die Zahlen so korrekt sind, wie sie da stehen.

http://de.4-traders.com/ASPEN-PHARMACARE-HOLDINGS-1413350/?t…

sie haben die

anästetikasparte von astra zeneca gekauft

Antwort auf Beitrag Nr.: 51.616.027 von cash_is_king am 30.01.16 03:48:30

bei mir kam raus:

KGV 34

KBV 3,5

EKR 11%

Divi 0,8%

Gestern kamen die Zahlen fürs per 30.6. beendete Geschäftsjahr,

am besten selbst reingucken und rechnen;bei mir kam raus:

KGV 34

KBV 3,5

EKR 11%

Divi 0,8%

Zahlen schienen gut anzukommen, aber

sie fahren unverändert einen SEHR heißen Reifen...

Zahlen sind für den 13.9. angekündigt;

HJ war gut

HJ war gut

Antwort auf Beitrag Nr.: 58.611.282 von R-BgO am 04.09.18 15:17:41

Gesamtjahr ebenfalls;

und sie machen auch mal ein bisschen deleveraging:

Antwort auf Beitrag Nr.: 50.984.406 von R-BgO am 02.11.15 12:53:30

und jetzt ver-5-facht

zu EUR 14,31

Antwort auf Beitrag Nr.: 58.689.306 von R-BgO am 13.09.18 11:14:13

wie so oft bei mir:

rauscht gleich weiter nach unten durch...

Antwort auf Beitrag Nr.: 58.689.408 von R-BgO am 13.09.18 11:22:23

VOLUNTARY ANNOUNCEMENT: PROVISION OF SUPPLEMENTARY INFORMATION IN RESPECT OF THE 2018

FINANCIAL YEAR RESULTS

On 13 September 2018, Aspen released its results for the 2018 financial year which reported that Aspen

had improved revenue by 3% to R42.6 billion and had grown normalised headline earnings per share

(“NHEPS”) by 10% to 1 605 cents in the year ended 30 June 2018. Following the release of these results,

trading volumes in Aspen shares increased with the share price declining significantly. We have received a

number of enquiries in respect of certain aspects of our business and for the benefit of our shareholders

the following supplementary information is provided.

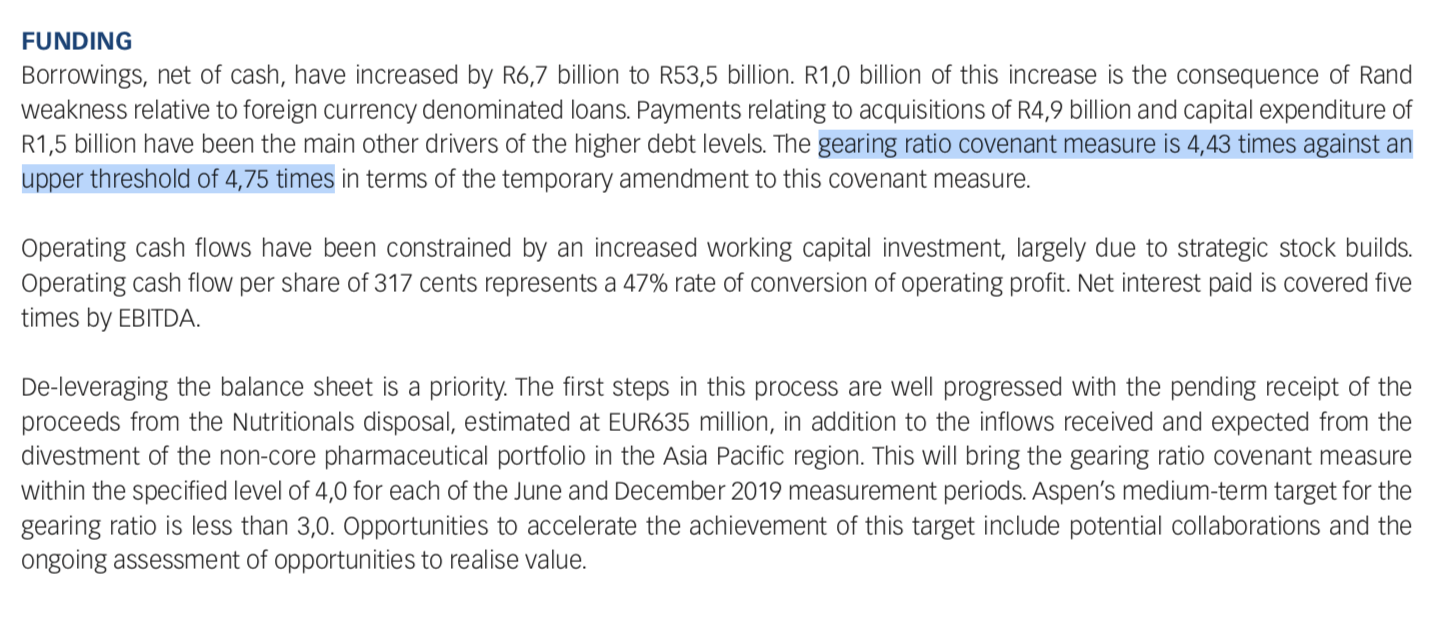

Guarantees to financial institutions relative to net debt levels

Aspen has no off-balance sheet funding and all guarantees to financial institutions apply only to wholly

owned Aspen subsidiaries.

In the announcement of 13 September 2018, Aspen reported guarantees to financial institutions of R73,5

billion and in the accompanying commentary, reported borrowings, net of cash, of R46,8 billion. The

explanation for the difference between these two values is as follows:

- The guarantees are for the maximum value of all available facilities and credit lines, and not only

for the drawn down portion thereof;

- Cash balances are offset against borrowings while the guarantees are on the full available debt

facilities, drawn and undrawn; and

- The guarantees also cover the gross value of the South Africa cash pooling system, and certain lines

which are linked to non-vanilla debt facilities, i.e. derivative lines, guarantee lines and other lines of

credit.

Revenue growth prospects in Commercial Pharmaceuticals

Aspen is targeting organic revenue growth of between 1% and 4% in its Commercial Pharmaceuticals

business for the 2019 financial year.

Sale of Nutritionals business

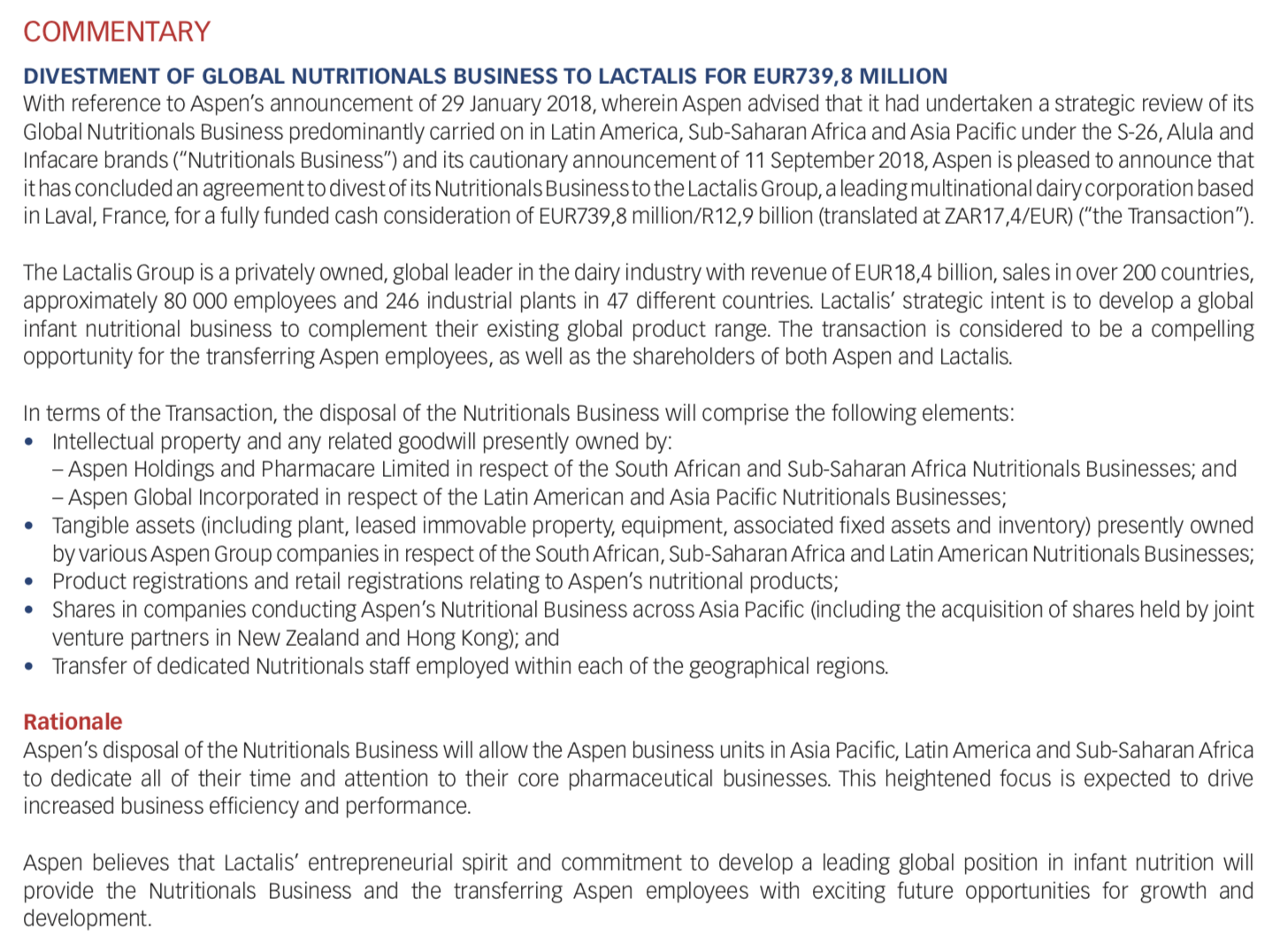

As also announced on 13 September 2018, Aspen has concluded an agreement to divest of its global

nutritionals business (“Nutritionals business”) to the Lactalis Group, a leading multinational dairy

corporation, for a fully funded cash consideration of EUR 739,8 million which includes approximately EUR

62 million to be paid to Aspen’s joint venture partners in Asia Pacific.

The net proceeds to Aspen from completion of the divestment of the Nutritionals business, after

transaction costs and related taxes, is expected to be approximately EUR 644 million (R11,2 billion at EUR

17,44/ZAR). These net proceeds will be utilised to reduce Aspen’s gearing, creating greater headroom and

capacity.

Influence of relative exchange rates

Relative exchange rate movements can have a significant impact on Aspen’s Rand-reported results.

Approximately 20% of the Group’s revenue and less than 20% of the Group’s profit after tax was earned in

Rand in the year ended 30 June 2018, with the balance of revenue and profits earned in a wide spread of

global currencies, the most material of which being the EUR, AUD, USD, CNY and JPN. Should present

exchange rates persist for the remainder of the 2019 financial year this would have a positive impact on

Rand-reported earnings.

Any reference to future financial or forecast information included in this announcement has not been

reviewed or reported on by the auditors.

Durban

19 September 2018

da ist echt der Boden rausgefallen...

und hat offenbar die company zu weiterer disclosure veranlaßt:VOLUNTARY ANNOUNCEMENT: PROVISION OF SUPPLEMENTARY INFORMATION IN RESPECT OF THE 2018

FINANCIAL YEAR RESULTS

On 13 September 2018, Aspen released its results for the 2018 financial year which reported that Aspen

had improved revenue by 3% to R42.6 billion and had grown normalised headline earnings per share

(“NHEPS”) by 10% to 1 605 cents in the year ended 30 June 2018. Following the release of these results,

trading volumes in Aspen shares increased with the share price declining significantly. We have received a

number of enquiries in respect of certain aspects of our business and for the benefit of our shareholders

the following supplementary information is provided.

Guarantees to financial institutions relative to net debt levels

Aspen has no off-balance sheet funding and all guarantees to financial institutions apply only to wholly

owned Aspen subsidiaries.

In the announcement of 13 September 2018, Aspen reported guarantees to financial institutions of R73,5

billion and in the accompanying commentary, reported borrowings, net of cash, of R46,8 billion. The

explanation for the difference between these two values is as follows:

- The guarantees are for the maximum value of all available facilities and credit lines, and not only

for the drawn down portion thereof;

- Cash balances are offset against borrowings while the guarantees are on the full available debt

facilities, drawn and undrawn; and

- The guarantees also cover the gross value of the South Africa cash pooling system, and certain lines

which are linked to non-vanilla debt facilities, i.e. derivative lines, guarantee lines and other lines of

credit.

Revenue growth prospects in Commercial Pharmaceuticals

Aspen is targeting organic revenue growth of between 1% and 4% in its Commercial Pharmaceuticals

business for the 2019 financial year.

Sale of Nutritionals business

As also announced on 13 September 2018, Aspen has concluded an agreement to divest of its global

nutritionals business (“Nutritionals business”) to the Lactalis Group, a leading multinational dairy

corporation, for a fully funded cash consideration of EUR 739,8 million which includes approximately EUR

62 million to be paid to Aspen’s joint venture partners in Asia Pacific.

The net proceeds to Aspen from completion of the divestment of the Nutritionals business, after

transaction costs and related taxes, is expected to be approximately EUR 644 million (R11,2 billion at EUR

17,44/ZAR). These net proceeds will be utilised to reduce Aspen’s gearing, creating greater headroom and

capacity.

Influence of relative exchange rates

Relative exchange rate movements can have a significant impact on Aspen’s Rand-reported results.

Approximately 20% of the Group’s revenue and less than 20% of the Group’s profit after tax was earned in

Rand in the year ended 30 June 2018, with the balance of revenue and profits earned in a wide spread of

global currencies, the most material of which being the EUR, AUD, USD, CNY and JPN. Should present

exchange rates persist for the remainder of the 2019 financial year this would have a positive impact on

Rand-reported earnings.

Any reference to future financial or forecast information included in this announcement has not been

reviewed or reported on by the auditors.

Durban

19 September 2018

Antwort auf Beitrag Nr.: 58.927.452 von R-BgO am 11.10.18 10:44:07

jetzt ist es eine echte Position für mich

nochmal verdoppelt,

trotz: https://www.moneyweb.co.za/news/companies-and-deals/where-to…jetzt ist es eine echte Position für mich

Was ist hier los? Schon wieder auf der Rutsche?

Antwort auf Beitrag Nr.: 59.438.712 von Steigerwälder am 14.12.18 10:59:46

die richtige Rutsche gab es nach dem H1-Bericht:

Antwort auf Beitrag Nr.: 60.148.371 von R-BgO am 20.03.19 10:08:36

den Kurs

hätte ich gerne wieder

Wirklich krass, bin froh, dass ich bislang an der Seitenlinie stehe.

Antwort auf Beitrag Nr.: 61.292.128 von R-BgO am 19.08.19 16:44:17

irgendwie bin ich ein Timing-Wunder:

mit dem letzten Posting genau den Tiefpunkt erwischt und seitdem Erholung um grob 50%

Aspen says it has capacity to meet demand for dexamethasone

www.moneyweb.co.za/news/companies-and-deals/aspen-says-it-ha…

www.moneyweb.co.za/news/companies-and-deals/aspen-says-it-ha…

Beitrag zu dieser Diskussion schreiben

Zu dieser Diskussion können keine Beiträge mehr verfasst werden, da der letzte Beitrag vor mehr als zwei Jahren verfasst wurde und die Diskussion daraufhin archiviert wurde.

Bitte wenden Sie sich an feedback@wallstreet-online.de und erfragen Sie die Reaktivierung der Diskussion oder starten Sie eine neue Diskussion.

Investoren beobachten auch:

| Wertpapier | Perf. % |

|---|---|

| +0,42 | |

| +2,86 | |

| -0,11 | |

| +1,16 | |

| +1,81 | |

| -1,50 | |

| -0,80 | |

| +0,94 | |

| -100,00 | |

| +0,15 |

Meistdiskutiert

| Wertpapier | Beiträge | |

|---|---|---|

| 210 | ||

| 94 | ||

| 82 | ||

| 62 | ||

| 53 | ||

| 49 | ||

| 41 | ||

| 34 | ||

| 29 | ||

| 28 |