GURE angeblich steht ein Buyout unmittelbar bevor! - 500 Beiträge pro Seite

eröffnet am 13.03.12 03:57:43 von

neuester Beitrag 09.11.14 22:28:10 von

neuester Beitrag 09.11.14 22:28:10 von

Beiträge: 25

ID: 1.173.005

ID: 1.173.005

Aufrufe heute: 0

Gesamt: 30.544

Gesamt: 30.544

Aktive User: 0

ISIN: US40251W4087 · WKN: A2PY50 · Symbol: R29B

1,3000

EUR

+2,36 %

+0,0300 EUR

Letzter Kurs 18.04.24 Tradegate

Werte aus der Branche Chemie

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1.650,00 | +716,83 | |

| 103,54 | +19,99 | |

| 1,3000 | +18,18 | |

| 1.964,50 | +11,98 | |

| 84,26 | +11,31 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 8.700,00 | -9,37 | |

| 19.600,00 | -9,68 | |

| 37,05 | -12,37 | |

| 5,6900 | -26,68 | |

| 43,02 | -60,46 |

Ticker: GURE

Preis: $2.645

Website: http://www.gulfresourcesinc.com/

http://www.dailyfinance.com/quote/nasdaq/gulf-resources/gure…

Preis: $2.645

Website: http://www.gulfresourcesinc.com/

http://www.dailyfinance.com/quote/nasdaq/gulf-resources/gure…

Gulf Chairman to Consider Privatization Option

http://finance.yahoo.com/news/Gulf-Chairman-Consider-prnews-…

Press Release: Gulf Resources, Inc. – Tue, Feb 21, 2012 9:00 AM EST

SHANDONG, China, Feb. 21, 2012 /PRNewswire-Asia-FirstCall/ -- Gulf Resources, Inc. (Nasdaq: GURE - News) ("Gulf Resources" or the "Company"), a leading manufacturer of bromine, crude salt and specialty chemical products in China, is issuing this press release regarding recent market speculation as to the Company's plans with respect to a potential third-party investment in the Company, or a privatization transaction.

There have been recent market rumors about the implications for the Company of an investment letter of intent ("LOI") between Shandong Ocean Bright Stone Industry Fund Management Co., Ltd., a PRC-based investment fund ("Ocean Bright"), and Shandong Haoyuan Industrial Group Co., Ltd. ("SHIG"). SHIG is an entity controlled by our Chairman and is a record owner of approximately 11.9% of our common stock. SHIG, together with the Chairman and his family, owns in the aggregate approximately 38.5% of our common stock.

We have been informed by Chairman Yang that, on February 20, 2012, SHIG did execute an LOI with Ocean Bright regarding a potential investment program in China's bromine exploitation industry, with the objective of consolidating those investments under SHIG and ultimately seeking a stock exchange listing for SHIG in China. We have been told that the LOI is highly preliminary and conditional, being subject to, among other things, due diligence and the commitment of definitive funding for potential PRC bromine investments. The Company is not a party to the LOI, but the Chairman has informed us that SHIG and Ocean Bright are considering the Company as a potential principal component to their strategy of consolidating the bromine industry in China, and, accordingly, as a potential candidate for a privatization in order to satisfy the listing requirements for SHIG in China.

As of this time, the Company has not received from either SHIG or Ocean Bright any formal or informal offer as to any type of investment or acquisition transaction, or any other inquiry seeking negotiations or due diligence. The Company's Board of Directors will take appropriate steps in the best interests of the Company's shareholders to evaluate fully and independently any such offer or inquiry that may be received from SHIG or Ocean Bright in the future.

"We will continue to focus on our daily operations, exploring strategic alternatives where appropriate, and creating value for our shareholders," said Xiaobin Liu, Chief Executive Officer of Gulf Resources. "If negotiations between the Company and SHIG and Ocean Bright begin and progress to a definitive point meriting shareholder disclosure or consideration, then we will of course update the market at that time. We however cannot give any assurance as to the timing of any of these negotiations, and, if they do begin, whether they will progress to any definitive agreement."

The Company follows a policy of not commenting on market rumors and takeover speculation, but has made an exception in this limited situation. We do not expect to have further comment on this matter at this time.

The reports that, to our knowledge, appeared in the Chinese language press referencing the LOI are set forth below. The Company makes no representation as to the accuracy of these reports or the statements or quotations included therein.

http://news.chemnet.com/item/2012-02-09/1620648.html

http://news.dsqq.cn/ROLLNEWS/2012/02/082232387527.html

About Gulf Resources, Inc.

Gulf Resources, Inc. operates through two wholly-owned subsidiaries, Shouguang City Haoyuan Chemical Company Limited ("SCHC") and Shouguang Yuxin Chemical Industry Co., Limited ("SYCI"). The Company believes that it is one of the largest producers of bromine in China. Elemental Bromine is used to manufacture a wide variety of compounds utilized in industry and agriculture. Through SYCI, the Company manufactures chemical products utilized in a variety of applications, including oil & gas field explorations and as papermaking chemical agents. For more information about the Company, please visit http:// www.gulfresourcesinc.com.

Forward-Looking Statements

Certain statements in this news release contain forward-looking information about Gulf Resources and its subsidiaries business and products within the meaning of Rule 175 under the Securities Act of 1933 and Rule 3b-6 under the Securities Exchange Act of 1934, and are subject to the safe harbor created by those rules. The actual results may differ materially depending on a number of risk factors including, but not limited to, the general economic and business conditions in the PRC, future product development and production capabilities, shipments to end customers, market acceptance of new and existing products, additional competition from existing and new competitors for bromine and other oilfield and power production chemicals, changes in technology, the ability to make future bromine asset purchases, and various other factors beyond its control. All forward-looking statements are expressly qualified in their entirety by this Cautionary Statement and the risks factors detailed in the Company's reports filed with the Securities and Exchange Commission. Gulf Resources undertakes no duty to revise or update any forward-looking statements to reflect events or circumstances after the date of this release.

Gulf Resources, Inc.

CCG Investor Relations Inc.

Helen Xu

David Rudnick, Account Manager

Email: beishengrong@vip.163.com

Phone: +1-646-626-4172

Web: http://www.gulfresourcesinc.com

Email: david.rudnick@ccgir.com

http://finance.yahoo.com/news/Gulf-Chairman-Consider-prnews-…

Press Release: Gulf Resources, Inc. – Tue, Feb 21, 2012 9:00 AM EST

SHANDONG, China, Feb. 21, 2012 /PRNewswire-Asia-FirstCall/ -- Gulf Resources, Inc. (Nasdaq: GURE - News) ("Gulf Resources" or the "Company"), a leading manufacturer of bromine, crude salt and specialty chemical products in China, is issuing this press release regarding recent market speculation as to the Company's plans with respect to a potential third-party investment in the Company, or a privatization transaction.

There have been recent market rumors about the implications for the Company of an investment letter of intent ("LOI") between Shandong Ocean Bright Stone Industry Fund Management Co., Ltd., a PRC-based investment fund ("Ocean Bright"), and Shandong Haoyuan Industrial Group Co., Ltd. ("SHIG"). SHIG is an entity controlled by our Chairman and is a record owner of approximately 11.9% of our common stock. SHIG, together with the Chairman and his family, owns in the aggregate approximately 38.5% of our common stock.

We have been informed by Chairman Yang that, on February 20, 2012, SHIG did execute an LOI with Ocean Bright regarding a potential investment program in China's bromine exploitation industry, with the objective of consolidating those investments under SHIG and ultimately seeking a stock exchange listing for SHIG in China. We have been told that the LOI is highly preliminary and conditional, being subject to, among other things, due diligence and the commitment of definitive funding for potential PRC bromine investments. The Company is not a party to the LOI, but the Chairman has informed us that SHIG and Ocean Bright are considering the Company as a potential principal component to their strategy of consolidating the bromine industry in China, and, accordingly, as a potential candidate for a privatization in order to satisfy the listing requirements for SHIG in China.

As of this time, the Company has not received from either SHIG or Ocean Bright any formal or informal offer as to any type of investment or acquisition transaction, or any other inquiry seeking negotiations or due diligence. The Company's Board of Directors will take appropriate steps in the best interests of the Company's shareholders to evaluate fully and independently any such offer or inquiry that may be received from SHIG or Ocean Bright in the future.

"We will continue to focus on our daily operations, exploring strategic alternatives where appropriate, and creating value for our shareholders," said Xiaobin Liu, Chief Executive Officer of Gulf Resources. "If negotiations between the Company and SHIG and Ocean Bright begin and progress to a definitive point meriting shareholder disclosure or consideration, then we will of course update the market at that time. We however cannot give any assurance as to the timing of any of these negotiations, and, if they do begin, whether they will progress to any definitive agreement."

The Company follows a policy of not commenting on market rumors and takeover speculation, but has made an exception in this limited situation. We do not expect to have further comment on this matter at this time.

The reports that, to our knowledge, appeared in the Chinese language press referencing the LOI are set forth below. The Company makes no representation as to the accuracy of these reports or the statements or quotations included therein.

http://news.chemnet.com/item/2012-02-09/1620648.html

http://news.dsqq.cn/ROLLNEWS/2012/02/082232387527.html

About Gulf Resources, Inc.

Gulf Resources, Inc. operates through two wholly-owned subsidiaries, Shouguang City Haoyuan Chemical Company Limited ("SCHC") and Shouguang Yuxin Chemical Industry Co., Limited ("SYCI"). The Company believes that it is one of the largest producers of bromine in China. Elemental Bromine is used to manufacture a wide variety of compounds utilized in industry and agriculture. Through SYCI, the Company manufactures chemical products utilized in a variety of applications, including oil & gas field explorations and as papermaking chemical agents. For more information about the Company, please visit http:// www.gulfresourcesinc.com.

Forward-Looking Statements

Certain statements in this news release contain forward-looking information about Gulf Resources and its subsidiaries business and products within the meaning of Rule 175 under the Securities Act of 1933 and Rule 3b-6 under the Securities Exchange Act of 1934, and are subject to the safe harbor created by those rules. The actual results may differ materially depending on a number of risk factors including, but not limited to, the general economic and business conditions in the PRC, future product development and production capabilities, shipments to end customers, market acceptance of new and existing products, additional competition from existing and new competitors for bromine and other oilfield and power production chemicals, changes in technology, the ability to make future bromine asset purchases, and various other factors beyond its control. All forward-looking statements are expressly qualified in their entirety by this Cautionary Statement and the risks factors detailed in the Company's reports filed with the Securities and Exchange Commission. Gulf Resources undertakes no duty to revise or update any forward-looking statements to reflect events or circumstances after the date of this release.

Gulf Resources, Inc.

CCG Investor Relations Inc.

Helen Xu

David Rudnick, Account Manager

Email: beishengrong@vip.163.com

Phone: +1-646-626-4172

Web: http://www.gulfresourcesinc.com

Email: david.rudnick@ccgir.com

Sollte ein Buyout erfolgen sollte der Preis meiner Meinung nach bei mindestens $6.00-$8.00 liegen.

Charttechnisch steht die Aktie vor dem Golden Croo (MA50 bricht die MA200)

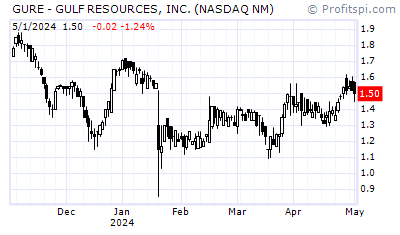

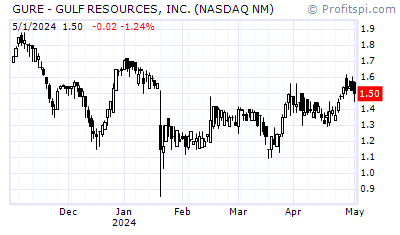

GURE $2.74 new high of day

Trading Spotlight

Noch ist Zeit soviele Aktien wie man will unter $2.80 zu bekommen.

Kommt die Buyoutnews dürfte das der Vergangenheit angehören!

Kommt die Buyoutnews dürfte das der Vergangenheit angehören!

On February 20, 2012, SHIG executed an investment letter of intent (“LOI”) with Shandong Ocean Bright Stone Industry Fund Management Co., Ltd., an investment fund based in the People’s Republic of China, regarding a potential investment program in China’s bromine exploitation industry, with the objective of consolidating those investments under SHIG and ultimately seeking a stock exchange listing for SHIG in China. The LOI is highly preliminary and conditional, being subject to, among other things, due diligence and the commitment of definitive funding for potential bromine investments in China. SHIG and Ocean Bright are considering the Issuer as a potential principal component to their strategy of consolidating the bromine industry in China, and, accordingly, as a potential candidate for privatization in order to satisfy the listing requirements for SHIG in China.

In connection with the foregoing, SHIG may initiate and hold negotiations with the Issuer with respect to a potential transaction; however, SHIG cannot determine at this time the length of any negotiations, when and if begun, and whether any negotiations, if begun, will lead to any definitive agreement or transaction.

http://www.otcmarkets.com/edgar/GetFilingHtml?FilingID=84276…

In connection with the foregoing, SHIG may initiate and hold negotiations with the Issuer with respect to a potential transaction; however, SHIG cannot determine at this time the length of any negotiations, when and if begun, and whether any negotiations, if begun, will lead to any definitive agreement or transaction.

http://www.otcmarkets.com/edgar/GetFilingHtml?FilingID=84276…

GURE selling at the open - bad Conference Call - no buyout details, no real guidance, no buyback..

Während des aktuellen CC für Q1/2012 wurde auch nach dem Buyout gefragt. Es wurden leider vom CEO keine Infos geliefert bzw. es lagen keine vor.

Es gab einige Ideen der Anrufer zur Unterstützung der Shareholder. Der CEO glaubt allerdings, dass er nur durch operative Ergebnisse den Aktienpreis nachhaltig verbessern kann. Ich befürchte, dass er durchaus Recht hat. Diese US-Investoren reagieren nicht auf Aktienrückkäufe oder Dividenden. Sie werden weiter SeekingAlpha lesen, verkaufen und shorten.

Ich werde demnächst hier nachkaufen, aber u.a. auch, um die hohen Gebühren für das Verleihen der Aktie an die US-Shorties zu kassieren.

Es gab einige Ideen der Anrufer zur Unterstützung der Shareholder. Der CEO glaubt allerdings, dass er nur durch operative Ergebnisse den Aktienpreis nachhaltig verbessern kann. Ich befürchte, dass er durchaus Recht hat. Diese US-Investoren reagieren nicht auf Aktienrückkäufe oder Dividenden. Sie werden weiter SeekingAlpha lesen, verkaufen und shorten.

Ich werde demnächst hier nachkaufen, aber u.a. auch, um die hohen Gebühren für das Verleihen der Aktie an die US-Shorties zu kassieren.

Phantasie sollte erstmal raus sein, eher Finger weg

Trotz der schlechten Zahlen für Q3/2012 hat der Kurs die Tiefs um die 1 USD nicht wieder erreicht, was positiv ist:

Die Bilanz ist immer noch stark:

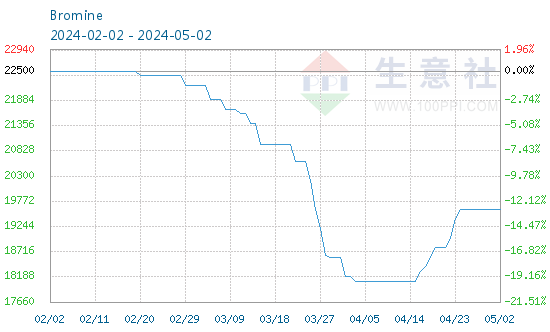

Die heutige Marketcap liegt bei ca. 43 Mio. USD. Das schlechte 3. Quartal lag u.a. an niedrigen Brom-Preisen. Hier siehts aber nun wieder besser aus:

http://sunsirs.com/de/prodetail-643.html

Der Preis liegt also nun wieder fast bei 20.000 RMB/t (3.200 USD).

Umsatz: 24,5 Mio. USD (-35% Y/Y)

Gross Profit: 7,4 Mio. (-46,7%)

Gross-Margin: 30,3% (vs. 36,9%)

op. Gewinn: 5,6 Mio. (8,7 Mio.)

op. Margin: 23% (23,2%)

Gewinn: 4,1 Mio. (5,6)

EPS: 0,12 USD (vs. 0,16)

Die Bilanz ist immer noch stark:

Cash: 58,6 Mio. USD

Forderungen: 41,9 Mio.

Schulden: 14,2 Mio.

EK: 254,9 Mio. USD

Working Capital: 94,7 Mio.

Die heutige Marketcap liegt bei ca. 43 Mio. USD. Das schlechte 3. Quartal lag u.a. an niedrigen Brom-Preisen. Hier siehts aber nun wieder besser aus:

http://sunsirs.com/de/prodetail-643.html

Der Preis liegt also nun wieder fast bei 20.000 RMB/t (3.200 USD).

Antwort auf Beitrag Nr.: 43.959.113 von startvestor am 24.12.12 16:48:31Umsatzmäßig sieht es weiter schlecht aus, durch Einsparungen blieb aber in Q4 zumindest ein Gewinn übrig:

Ausblick 2013:

Bilanz und Marketcap:

Umsatz: 22 Mio. USD (-27,8% Y/Y)

Gross Profit: 4,2 Mio. (-59,5%)

Gross-Margin: 19,1% (vs. 34,1%)

op. Gewinn: 2,6 Mio. (1,9 Mio.)

op. Margin: 12% (6,2%)

Gewinn: 1,9 Mio. (1)

EPS: 0,05 USD (vs. 0,03)

Ausblick 2013:

Umsatz: 122,8 Mio.

Gewinn: 18,7

Bilanz und Marketcap:

Marketcap: 38,5 Mio. USD

Cash: 65,2 Mio. USD (78,6 Y/Y)

Forderungen: 36 Mio.

Schulden: 14 Mio.

EK: 264,2 Mio. USD

Die Lage ist weiter schwierig, bei einem Brompreis von 3.000 USD/t kann Gulf Res. kaum Gewinn machen. Salzsäure und chem. Produkte liefen in Q1/2013 besser:

Der Cash wurde auf 78,5 Mio. ausgebaut, EK beträgt nun 267 Mio. - bei einer Marketcap von 42 Mio. Immerhin gibts nun Aktienrückkäufe für 2 Mio. Der Class Action Suit aus 2011 wurde nun gesettled, Betrag aber noch unbekannt, soll die Versicherung zahlen.

Die Risiken bleiben:

- China- und RTO-Aktie

- schwierige wirtschaft. Lage in China

- keine Dividende

- Misstrauen wg. Class Action aus 2011

etc.

Umsatz: 22,5 Mio. USD (-5% Y/Y)

Gross Profit: 4,5 Mio. (-33%)

Gross-Margin: 20% (vs. 28%)

op. Gewinn: 2,6 Mio. (4,6 Mio.)

op. Margin: 12% (19%)

Gewinn: 1,9 Mio. (3,3 Mio.)

EPS: 0,05 USD (vs. 0,10)

op. Cashflow: 13,3 Mio. USD

inv. Cashflow: -0,3 Mio.

Der Cash wurde auf 78,5 Mio. ausgebaut, EK beträgt nun 267 Mio. - bei einer Marketcap von 42 Mio. Immerhin gibts nun Aktienrückkäufe für 2 Mio. Der Class Action Suit aus 2011 wurde nun gesettled, Betrag aber noch unbekannt, soll die Versicherung zahlen.

Die Risiken bleiben:

- China- und RTO-Aktie

- schwierige wirtschaft. Lage in China

- keine Dividende

- Misstrauen wg. Class Action aus 2011

etc.

Antwort auf Beitrag Nr.: 44.613.995 von startvestor am 11.05.13 23:37:16Gulf Res. ist nun aus der Seitwärtsphase ausgebrochen, Marketcap nun bei 61,6 Mio. USD. Die Klage wird wohl zu 2,1 Mio. USD gesettled. Die Zahlen für Q2/2013 waren besser als erwartet:

Das KGV für 2013 dürfte zwischen 3,5 und 4 liegen.

Umsatz: 32,9 Mio. USD (+5% Y/Y)

Gross Profit: 9,6 Mio. (-3%)

Gross-Margin: 29% (vs. 32%)

op. Gewinn: 7,4 Mio. (7,6 Mio.)

op. Margin: 22% (24%)

Gewinn: 5,4 Mio. (5,7 Mio.)

EPS: 0,14 USD (vs. 0,16)

Das KGV für 2013 dürfte zwischen 3,5 und 4 liegen.

Q3/2013 brachte gute Zahlen:

Der Cash von 97,2 Mio. CAD entspricht in etwa der aktuellen Marketcap.

Umsatz: 32,9 Mio. USD (24,5 Mio. Y/Y)

Gross Profit: 10,9 Mio. (+47%)

Gross-Margin: 33% (vs. 30%)

op. Gewinn: 10,9 Mio. (5,6 Mio.)

op. Margin: 33%

Gewinn: 8,1 Mio. (4,1 Mio.)

EPS: 0,21 USD (vs. 0,12)

Der Cash von 97,2 Mio. CAD entspricht in etwa der aktuellen Marketcap.

Die Zahlen für Q4/2013:

Bilanz:

Marketcap: 105,9 Mio.

Umsatz: 30,1 Mio. USD (+36,5% Y/Y), Q3: 32,9

Gross Profit: 9,1 Mio. (+117%)

Gross-Margin: 30,4% (vs. 19,1%)

op. Gewinn: 7,6 Mio. (+186%)

op. Margin: 25,1% (12%)

Gewinn: 5,6 Mio. (1,9 Mio.), Q3: 8,1

EPS: 0,15 USD (vs. 0,05), Q3: 0,21

Bilanz:

Cash: 107,8 Mio. USD (97,2 Q/Q)

Forderungen: 44,9 Mio. (41,5)

Property etc.: 146,4 Mio.

Verbindl.: 14,2 Mio.

EK: 295 Mio. (286,7 Mio.)

Bilanzsumme: 309,2 Mio

Marketcap: 105,9 Mio.

Zahlen für Q1/14:

Marketcap: 68,5 Mio.

Cash: 119,3 Mio.

Umsatz: 25,6 Mio. USD (+14% Y/Y), 4: 30,1

Gross Profit: 6,9 Mio. (+52%)

Gross-Margin: 27% (vs. 20%)

op. Gewinn: 5,6 Mio. (+115%)

op. Margin: 22% (12%)

Gewinn: 4,3 Mio. (+128%), Q4: 5,6

EPS: 0,11 USD (vs. 0,05), Q4: 0,15

Marketcap: 68,5 Mio.

Cash: 119,3 Mio.

Antwort auf Beitrag Nr.: 46.959.056 von startvestor am 10.05.14 23:47:24ach, danke dir für den hinweis bei cga !!

war mir gar nicht bewusst, daß hier ein thread existiert.

hast ja alels schön übersichtlich reingestellt.

gure ist für mich auch ein klarer longplay.

broom soll ja, wenn man dem ein oder anderen schreiben glauben darf,

an für sich keine schlechte zukunft haben.

mal davon abgesehen dass GURE ein großer hersteller ist und klar unterbewertet ist.

zulassungen zur broomherstellung sind soweit ich weiss auch eher schwer zu bekommen.

war mir gar nicht bewusst, daß hier ein thread existiert.

hast ja alels schön übersichtlich reingestellt.

gure ist für mich auch ein klarer longplay.

broom soll ja, wenn man dem ein oder anderen schreiben glauben darf,

an für sich keine schlechte zukunft haben.

mal davon abgesehen dass GURE ein großer hersteller ist und klar unterbewertet ist.

zulassungen zur broomherstellung sind soweit ich weiss auch eher schwer zu bekommen.

Antwort auf Beitrag Nr.: 47.001.932 von Boersiback am 17.05.14 18:49:32Ganz so abhängig sind sie übrigens nicht mehr von Brom, die Chemiesparte ist zuletzt stark gewachsen. Ansonsten bleibt natürlich das immanente China-Problem, mein Vertrauen in diese Leute ist stark zurückgegangen.

Antwort auf Beitrag Nr.: 47.002.928 von startvestor am 18.05.14 09:54:39stimmt. der chemiesektor bei denen ist ja stark wachsend.

naja das allgemeine vertrauen ist ein problem, klar.

da ja immer wieder neue skandale hochkommen.

scheint da so zu sein wie bei us-otc-werten. man weiss nie so genau, was nicht ausgewiesen wird.

naja das allgemeine vertrauen ist ein problem, klar.

da ja immer wieder neue skandale hochkommen.

scheint da so zu sein wie bei us-otc-werten. man weiss nie so genau, was nicht ausgewiesen wird.

Zahlen für Q2/14:

Bilanz:

Marketcap nun bei ca. 77 Mio. USD, also deutlich unter Cash. Der Conference Call war aber wieder zum Heulen. Letztendlich ist es wohl so, dass der Cash nur den Chinesen, aber nicht den Aktionären gehört - falls er überhaupt da sein sollte. Wenig Chancen auf bessere Kurse.

Umsatz: 31,8 Mio. USD (-3% Y/Y), Q1: 25,6

Gross Profit: 9,2 Mio. (-4%)

Gross-Margin: 29% (vs. 29%)

op. Gewinn: 7,5 Mio. (-2%)

op. Margin: 24% (22%)

Gewinn: 5,7 Mio. (+6%), Q1: 4,3

EPS: 0,15 USD (vs. 0,14), Q1: 0,11

Bilanz:

Cash: 129 Mio. USD (119,3 Q/Q)

Forderungen: 45,3 Mio. (41,3)

Property etc.: 131,5 Mio.

Verbindl.: 14,3 Mio.

EK: 302 Mio. (296,4 Mio.)

Bilanzsumme: 316,3 Mio

Marketcap nun bei ca. 77 Mio. USD, also deutlich unter Cash. Der Conference Call war aber wieder zum Heulen. Letztendlich ist es wohl so, dass der Cash nur den Chinesen, aber nicht den Aktionären gehört - falls er überhaupt da sein sollte. Wenig Chancen auf bessere Kurse.

Antwort auf Beitrag Nr.: 47.494.309 von startvestor am 12.08.14 13:09:52ich hab den wert noch mit ner kleinen 2000 €-pos

vom sektor her mag ich die eigentlich. von den zahlen noch mehr, eben extremer cashanteil auch.

die frage ist nur wie man das da rechnen muss.

cash gehört der firma ist doch klar.

wird ja nicht ausgeschüttet. divis gibt´s keine.

insofern keine relevanten geheimnisvollen nicht ausgewiesenen verbindlichkeiten irgendwo schlummer muss man es mitbewerten.

so gesehen wäre die bude spottbillig... aber chinesen eben... man weiss nie so recht.

vom sektor her mag ich die eigentlich. von den zahlen noch mehr, eben extremer cashanteil auch.

die frage ist nur wie man das da rechnen muss.

cash gehört der firma ist doch klar.

wird ja nicht ausgeschüttet. divis gibt´s keine.

insofern keine relevanten geheimnisvollen nicht ausgewiesenen verbindlichkeiten irgendwo schlummer muss man es mitbewerten.

so gesehen wäre die bude spottbillig... aber chinesen eben... man weiss nie so recht.

Antwort auf Beitrag Nr.: 47.495.683 von Boersiback am 12.08.14 15:32:27Wenn Du den CEO abends in gemütlicher Runde und nach dem 5. Bier fragen würdest, wem der Cash gehört, dann würde er sagen: Mir ganz alleine. Das ist meine Firma und ich mache was ich will.

Und leider hätte er faktisch recht. Wenn er sich den Cash morgen über irgendeinen Trick nehmen würde, er hätte derzeit nichts zu befürchten. Keine chin. Behörde würde ihn anklagen.

Und leider hätte er faktisch recht. Wenn er sich den Cash morgen über irgendeinen Trick nehmen würde, er hätte derzeit nichts zu befürchten. Keine chin. Behörde würde ihn anklagen.

Q3/2014

Zahlen für Q3/14:Umsatz: 31,1 Mio. USD (-6% Y/Y), Q2: 31,8

Gross Profit: 9,2 Mio. (-16%)

Gross-Margin: 30% (vs. 33%)

op. Gewinn: 6,7 Mio. (-39%)

op. Margin: 22% (33%)

Gewinn: 5 Mio. (-38%), Q2: 5,7

EPS: 0,13 USD (vs. 0,21), Q2: 0,15

Bilanz:

Cash: 132 Mio. USD (129 Q/Q)

Forderungen: 48,3 Mio. (45,3)

Property etc.: 130,5 Mio.

Verbindl.: 13,9 Mio.

EK: 307,1 Mio. (302 Mio.)

Bilanzsumme: 321 Mio

In der News zu den Zahlen hat man eine Aquisition angekündigt. Zuletzt ist der Kurs gut gestiegen. Wenn es auch über 1,50 USD geht, könnte es einen neuen Aufwärtstrend geben.

Beitrag zu dieser Diskussion schreiben

Zu dieser Diskussion können keine Beiträge mehr verfasst werden, da der letzte Beitrag vor mehr als zwei Jahren verfasst wurde und die Diskussion daraufhin archiviert wurde.

Bitte wenden Sie sich an feedback@wallstreet-online.de und erfragen Sie die Reaktivierung der Diskussion oder starten Sie eine neue Diskussion.

Investoren beobachten auch:

| Wertpapier | Perf. % |

|---|---|

| +1,24 | |

| -1,06 | |

| 0,00 |

Meistdiskutiert

| Wertpapier | Beiträge | |

|---|---|---|

| 193 | ||

| 109 | ||

| 91 | ||

| 72 | ||

| 68 | ||

| 61 | ||

| 44 | ||

| 42 | ||

| 38 | ||

| 37 |