It's Call on KongZhong (KZ) Time - 500 Beiträge pro Seite

eröffnet am 20.09.14 12:04:38 von

neuester Beitrag 10.06.15 21:23:02 von

neuester Beitrag 10.06.15 21:23:02 von

Beiträge: 86

ID: 1.199.453

ID: 1.199.453

Aufrufe heute: 0

Gesamt: 4.128

Gesamt: 4.128

Aktive User: 0

ISIN: US50047P1049 · WKN: A0B6SL

7,0590

EUR

+0,40 %

+0,0280 EUR

Letzter Kurs 14.04.17 Tradegate

Werte aus der Branche Telekommunikation

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 40,59 | +20,80 | |

| 905,75 | +16,83 | |

| 48,84 | +13,58 | |

| 2,6800 | +11,67 | |

| 2.610,65 | +9,67 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 11,400 | -9,52 | |

| 1,7800 | -11,00 | |

| 2,0100 | -11,06 | |

| 0,7700 | -25,25 | |

| 6,0800 | -39,20 |

Interessante Situation bei Kongzhong (Kürzel KZ an der Nasdaq) – aktuell 6,78 USD

Ergebnis Q2 durch die hohen vorher angekündigten Marketing Kosten nur etwas über break even.

Q3 angekündigt und bei Kong immer auch realistisch / eher leicht konservativ 10 Mio. USD Gewinn. Also ca. 22 Cent Gewinn je Aktie, die zum Cash bzw. cashähnlichen Bestand von 5,10 USD dazu kommen werden.

Keine Schulden.

Hohes Umsatzwachstum. Aktuell ca. 30%

Kein Interesse zur Zeit an Kong, da die guten nächsten Zahlen erst Mitte / Ende November kommen. Zur Zeit nur ein Spielball der Märke und kann auch leicht kurstechnisch weiter gedrückt werden, da Chart auch nicht mehr gut aussieht

Wenn man so wie ich, an gute Zahlen für Q3 und Q4 glaubt kann man mit Hebel die nächsten Monate hier richtig Geld verdienen.

Ich habe dazu meine Kong verkauft und Calls auf Kong gekauft.

Zwei finde ich interessant

Etwas schärfer den KZ141220C00007500

Läuft bis 20.12. (also nach den Zahlen von Q3) Basis 7,50 USD - Kostet aktuell im Kauf 0,40 USD (1 Option immer für 100 Stücke)

Etwas konservativer (da längere Laufzeit) den KZ150320C00007500

Läuft bis 20.03.2015 (also nach den Zahlen von Q4) Basis 7,50 USD - Kostet aktuell im Kauf 0,65 USD

Szenario 1:

Der mögliche Gewinn wenn wir von 10 USD im Dez ausgehen (was ich für nicht unrealistisch halte)

10 / 6,78 = 47,5 % Gewinn wenn man die Aktie jetzt für 6,78 USD kauft

2,50 / 0,40 = 525 % Gewinn wenn man den ersten Call kauft

Szenario 2:

Der mögliche Gewinn wenn wir von 11 USD im März 2015 ausgehen (was ich auch für nicht unrealistisch halte)

11 / 6,78 = 62 % Gewinn wenn man die Aktie jetzt für 6,78 USD kauft

3,50 / 0,65 = 438 % Gewinn wenn man den zweiten Call kauft

Ich habe beide Calls gekauft, vom ersten etwas mehr.

Hier der Jahreschart in USD

Ergebnis Q2 durch die hohen vorher angekündigten Marketing Kosten nur etwas über break even.

Q3 angekündigt und bei Kong immer auch realistisch / eher leicht konservativ 10 Mio. USD Gewinn. Also ca. 22 Cent Gewinn je Aktie, die zum Cash bzw. cashähnlichen Bestand von 5,10 USD dazu kommen werden.

Keine Schulden.

Hohes Umsatzwachstum. Aktuell ca. 30%

Kein Interesse zur Zeit an Kong, da die guten nächsten Zahlen erst Mitte / Ende November kommen. Zur Zeit nur ein Spielball der Märke und kann auch leicht kurstechnisch weiter gedrückt werden, da Chart auch nicht mehr gut aussieht

Wenn man so wie ich, an gute Zahlen für Q3 und Q4 glaubt kann man mit Hebel die nächsten Monate hier richtig Geld verdienen.

Ich habe dazu meine Kong verkauft und Calls auf Kong gekauft.

Zwei finde ich interessant

Etwas schärfer den KZ141220C00007500

Läuft bis 20.12. (also nach den Zahlen von Q3) Basis 7,50 USD - Kostet aktuell im Kauf 0,40 USD (1 Option immer für 100 Stücke)

Etwas konservativer (da längere Laufzeit) den KZ150320C00007500

Läuft bis 20.03.2015 (also nach den Zahlen von Q4) Basis 7,50 USD - Kostet aktuell im Kauf 0,65 USD

Szenario 1:

Der mögliche Gewinn wenn wir von 10 USD im Dez ausgehen (was ich für nicht unrealistisch halte)

10 / 6,78 = 47,5 % Gewinn wenn man die Aktie jetzt für 6,78 USD kauft

2,50 / 0,40 = 525 % Gewinn wenn man den ersten Call kauft

Szenario 2:

Der mögliche Gewinn wenn wir von 11 USD im März 2015 ausgehen (was ich auch für nicht unrealistisch halte)

11 / 6,78 = 62 % Gewinn wenn man die Aktie jetzt für 6,78 USD kauft

3,50 / 0,65 = 438 % Gewinn wenn man den zweiten Call kauft

Ich habe beide Calls gekauft, vom ersten etwas mehr.

Hier der Jahreschart in USD

Übrigens werden die Calls/Puts immer am Börsenanfang (15:30 Uhr) schlecht taxiert.

Ab ca.17:00 bis 17:30 Uhr gibt es dann eine fairere Taxe.

Meine Order hatte ich mit Limit eingegeben und sie wurde (erst) um ca. 18:00 Uhr ausgeführt.

Also geduldig sein, mit Limit arbeiten und realistischen Kauf-Kurs setzen.

Zudem muss ich noch sagen, das z.B. mein Broker Lynx (über Interactive Broker) 7 % Gebühren nimmt, nicht wenig, aber wenn die Wette aufgeht nebensächlich.

Ab ca.17:00 bis 17:30 Uhr gibt es dann eine fairere Taxe.

Meine Order hatte ich mit Limit eingegeben und sie wurde (erst) um ca. 18:00 Uhr ausgeführt.

Also geduldig sein, mit Limit arbeiten und realistischen Kauf-Kurs setzen.

Zudem muss ich noch sagen, das z.B. mein Broker Lynx (über Interactive Broker) 7 % Gebühren nimmt, nicht wenig, aber wenn die Wette aufgeht nebensächlich.

Im übrigen war KONG schon immer eine hervorragende Trading Aktie.

Siehe auch 5 Jahreschart.

Es gab meiner Ansicht nach immer größere Player, die mit Kong Geld verdienen wollten und jetzt auch noch wollen indem sie Trend verstärken und so es immer wieder zu günstigen und hohen Kurse kam /kommt.

Denn Kong hat seit Jahren ein stabliles, profitables Gechäftsmodell, dem

es etwas an Umsatz- und Ertragswachstum /-fantasie mangelte.

Die jetzige Situation ist eigentlich paradox. Wir kommen ab jetzt in ein verstärktes Umsatzwachstum und auch wohl Ertragswachstum was jahrelang bemängelt wurde das es fehlte, haben jetzt mehr Cash je Aktie als je zuvor (ca. 5,30 USD Ende September) , damit hervorragend nach unten abgesichert und der Kurs ist mittlerweile auf 6,78 USD gefallen.

Kann sein das wir noch auf 6,00 USD fallen (was ich nicht glaube, deshalb die Call Käufe jetzt), aber eines sage ich mal mit 15 jähriger Börsenerfahrung und 10 jähriger Erfahrung mit KONG, es wird bald einen kräftigen Rebound geben, spätestens mit den Q3 Zahlen im November.

Siehe auch 5 Jahreschart.

Es gab meiner Ansicht nach immer größere Player, die mit Kong Geld verdienen wollten und jetzt auch noch wollen indem sie Trend verstärken und so es immer wieder zu günstigen und hohen Kurse kam /kommt.

Denn Kong hat seit Jahren ein stabliles, profitables Gechäftsmodell, dem

es etwas an Umsatz- und Ertragswachstum /-fantasie mangelte.

Die jetzige Situation ist eigentlich paradox. Wir kommen ab jetzt in ein verstärktes Umsatzwachstum und auch wohl Ertragswachstum was jahrelang bemängelt wurde das es fehlte, haben jetzt mehr Cash je Aktie als je zuvor (ca. 5,30 USD Ende September) , damit hervorragend nach unten abgesichert und der Kurs ist mittlerweile auf 6,78 USD gefallen.

Kann sein das wir noch auf 6,00 USD fallen (was ich nicht glaube, deshalb die Call Käufe jetzt), aber eines sage ich mal mit 15 jähriger Börsenerfahrung und 10 jähriger Erfahrung mit KONG, es wird bald einen kräftigen Rebound geben, spätestens mit den Q3 Zahlen im November.

... It looks like KZ is cheap, by just about any of the traditional metrics. The problem, therefore is a catalyst to get the market to notice the stock.

Management has hinted about a possible dividend, however it seems relatively unlikely in the near term (based on comments during the Q2 call). The company's business is highly cash generative, and it seems reasonable that after building up the cash cushion somewhat, a divided might be in the cards.

Other possible catalysts could be progress on the share buyback (there are still about 3 million shares eligible for purchase under the FY2012 buyback plan), something which may garner investor attention.

But until the market turns its attention back to KongZhong, patience is investors' only option.

We think that market is currently taking a "show me" approach to many US-listed Chinese companies, something which could provide opportunity for an investor with a longer time horizon.

http://seekingalpha.com/article/2509885-kongzhong-hidden-val…

Management has hinted about a possible dividend, however it seems relatively unlikely in the near term (based on comments during the Q2 call). The company's business is highly cash generative, and it seems reasonable that after building up the cash cushion somewhat, a divided might be in the cards.

Other possible catalysts could be progress on the share buyback (there are still about 3 million shares eligible for purchase under the FY2012 buyback plan), something which may garner investor attention.

But until the market turns its attention back to KongZhong, patience is investors' only option.

We think that market is currently taking a "show me" approach to many US-listed Chinese companies, something which could provide opportunity for an investor with a longer time horizon.

http://seekingalpha.com/article/2509885-kongzhong-hidden-val…

Auf Wunsch des Thread-Erstellers hier der komplette Text des Beitrags aus Seeking-Alpha:

-------------------------------------------------------------------------

Summary

•Not a WVAS company anymore, pushing forward in Internet games.

•Q2 results artificially lower due to new game launch costs.

•New games doing well, could be near-term growth drivers.

KongZhong (KZ, detailed company profile here) is an online game operator in China that has been off investors' radar, but deserves a closer look. The stock has been trading away from the business fundamentals, and taking a longer-term view could offer a rewarding opportunity to a patient investor.

The company is relatively small (market cap of about $300 million), so many investors may not have heard of it before. KongZhong came to the market in 2004 as a provider of SMS and other wireless value added services (WVAS), but adapted to the changing landscape by later expanding into mobile games. After the last of the founders left in FY2009, new management pushed ahead with a growth agenda including entering the online PC games business, acquiring a 3D massively multiplayer online game (MMOG) developer. In addition to developing its own games, KongZhong also began using the licensing model to bring games which were successful abroad into China; its first major title was World of Tanks, developed by Wargaming.net. World of Tanks has become a popular game in its genre, and has been the main driver of KongZhong's success in its Internet Games segment thus far.

Games - KongZhong's New Core

By the end of FY2013, the company's transformation from a "WVAS provider also involved in mobile games" into a company focused on PC gaming was complete. Indeed, non-WVAS revenues comprised the majority of total revenue in FY2013. The shift in focus was a deliberate and timely choice for management. The entire WVAS industry has been dwindling thanks to more powerful smartphones (data messages instead of SMS), and moving into Internet Games has been leading KongZhong's incremental growth.

Up until mid-FY2014, KongZhong's Internet Games business was basically World of Tanks, however the company launched two titles in Q2 that could change that. The first title is Guild Wars 2 (GW2), an innovative MMORPG offering a new type of gameplay beyond the traditional task or quest-based styles. According to disclosures from the company, it has sold over 1 million CD keys for the game through Q2, illustrating gamer demand. The performance of the game since launch appears to be going well (here is a note from VentureBeat). Despite the challenge of adapting to the new style of play GW2 offers and the upfront investment in buying the CD key, it remains a popular title in China. According to 17173.com, a website focusing on online games, GW2 was in the top-5 most popular games when checked in early September 2014. (Guild Wars 2 is "激战2" in Chinese.)

The game's release hasn't gone off without a few hitches, however, with some players finding the adjustment to the licensing model (paying up front for a key), and gameplay challenging. (Aside: some gamers can play other titles for up to a year before paying, so forking over cash before doing anything may have struck a sour note.) KongZhong has taken steps to address the learning curve, dedicating resources to help players transition into the new gameplay style, which could in turn make the payment model less of an issue for hesitant players. As of mid-Q3, KongZhong's management sounded very confident with progress up to that point, and noted that upcoming updates from ArenaNet, the game developer, could also help address some gameplay issues.

KongZhong's second major title released during Q2 was World of Warplanes, also licensed from Wargaming.net. One of the features of the game highlighted during the run-up to its release was how easy it was to play while delivering a realistic gaming experience (vs. real flight physics and hard controls or just the opposite). When discussing the game launch earlier, management sounded confident that it would be able to replicate some of the popularity achieved with World of Tanks. Potential tailwinds for the game include overall popularity with military-themed games in China, as well as crossover players from World of Tanks, due to the unified access afforded by the Wargaming platform.

Mobile Games - Another Avenue of Growth

In addition to the company's progress in PC games, KongZhong has also been pushing into the mobile game space. Its previous mobile game experience was mostly Java-based smartphone games, but a FY2012 acquisition brought smartphone game development expertise in-house. The company launched its first titles based on this technology in FY2013, which helped to later reignite growth in the Mobile games segment.

Success in mobile games is elusive, due in part to the ultra-competitive nature of the market in China, the "flavor of the month" phenomenon that can make-or-break a game's success, and frighteningly short lifespans. KongZhong's approach seems to borrow a page from Wayne Gretzky's playbook, something which could pay off in the long run. Instead of chasing the hot current trends, KongZhong is trying to develop great games that will win based on the game's own merits, not a hot trend. By focusing on where mobile game demand is going to be (not where stands currently), KongZhong trades the risk of chasing current demand for a longer-tail payoff. The company's execution history with smartphone games hasn't all been perfect; after all, not every game is a hit. But instead of abandoning its goal to make truly innovative games, management analyzed what wasn't right, and took the appropriate steps necessary to move forward. (Tiny War, which would later become Pocket Fort, is an example of this "keep after it" attitude.)

Recent Financial Performance

KongZhong's Q2 results weren't that great judging by the P&L: although sales grew YoY and QoQ, it reported an operating loss on higher spending and barely broke even thanks to interest income. Operating metrics also looked tough. Although more gamers were playing KongZhong's games, the key ARPU (average revenue per user) metric tumbled to an anemic 152 RMB.

And anyone stopping there could be forgiven for thinking the company isn't doing well. It's only after a closer look that the story changes.

First, on the operating margin compression: KongZhong launched two major titles during the Q2 (GW2 and World of Warplanes), which meant above-average sales and marketing expenses to support game launches. A successful launch can significantly help a game's chance for a bright future, and in the case of GW2, KongZhong spent the marketing dollars to build buzz in the gamer community. World of Warplanes was the second major launch in Q2, and although it might have seemed like a secondary consideration, it's important to keep in mind that the GW2 launch was a major event. Before the launch of GW2, it was one of the most anticipated titles in China (see this note from back in March 2014), hence the attention on the game. World of Warplanes was also on the list of highly anticipated games (#16 of the top 20), and there appears to be continuing gamer interest, judging by message board activity and news flow on related websites.

The timing of the game launches was also a factor in some of the operating metrics looking softer. Both Guild Wars 2 and World of Warplanes were launched in May 2014 (GW2 May 15, WoWP May 28), contributing to Active Users and Paying Accounts growth, but not ARPU. The calculation for ARPU is the total revenue divided by the number of paying players, so when players increased without a full period of their spending, ARPU was lower.

So on balance, was Q2 a bad quarter? Maybe not, after considering the successful launched of two major game titles, which helped KongZhong expand its Internet game portfolio from one title (World of Tanks), to potentially three major games. If the company can achieve a similar level of success with the new launches, an increase in revenue could follow.

What's Next in Q3?

KongZhong is guiding for revenue growth of about USD 65 million, or about +33% YoY and +7% QoQ, and improving margins (higher gross, operating, and net margins vs. Q2).

A few factors are driving the revenue and margin outlook: a more stable environment in the WVAS segment, incremental revenue contribution from the new Internet games, and also KongZhong's new Mobile games.

GuildWars 2 sounds like it is progressing well, as mentioned earlier, and KongZhong is continuing its promotion efforts to build up the player base. The company mentioned a limited free trial coming up, something which could help attract players who were hesitant to try the game. KongZhong's core title Word of Tanks has been stable, and potential concerns that the game was stagnating may be premature. Wargaming.net recently released a new gameplay mode called Stronghold which could impact player engagement (team members skirmish together to boost team-level battle capabilities and other features).

Management mentioned on the Q2 call that it had a few new Mobile games in the Q3 pipeline, and also planned some releases in Q4 (4-5 total during the second half). Although it's tough to tell if the games will be a hit, none of the titles in the pipeline sounded "risky" in terms of game style, so there could be some upside surprise in the outlook for the segment.

After performing some rough calculations, it seems like revenue could hit the USD 65-66 million level without too much trouble. This is based on flattish revenue contributions from WoT, a full quarter of GW2 and WoWP (averaging just under 8 million of revenue each), slightly lower WVAS revenues, and some degree of success in Mobile games (+5% QoQ). The operating profit margin picture improves assuming a slight rebound at the gross level (flatlined at 50% in our model), and a reduction in sales and marketing expenses (no big Internet game launches were scheduled).

Given the above, operating profit could get close to the USD 8 million mark, reflecting an operating profit margin of about 12% (up vs. 0% last quarter, and similar to levels seen in FY2013). Non-operating items have historically been minimal for KongZhong (non-cash impairment charges aside), so net income could be about USD 9 million. Assuming a moderate increase in shares outstanding, EPADS could be about USD 0.19 (diluted).

We feel this is a conservative estimate for the quarter, particularly when considering management's guidance for net profit of USD 9-10 million (about USD 0.20 per share). The company has recently been delivering results exceeding management's guidance (no surprise there), however we tried to be increasingly conservative to underscore the valuation argument, discussed below.

Applying similar growth and cost estimates to Q4 results in the same EPS (0.19 USD/ADS) and margin picture.

Key assumptions in the scenario above include continued success with GW2 and WoWP (we assume that the two titles combined will break the USD 20 million revenue barrier in Q2 FY2015), stable performance from WoT, and progress in Mobile games.

KongZhong's Mobile game segment passed the USD 10 million revenue hurdle in Q2, and we assumed growth of about 5% QoQ for the next two quarters, and flat afterward. Considering the games in the Mobile game pipeline (4-5 games, both self-developed and licensed), expecting some success from the segment doesn't seem like too much of a stretch.

FY2015

Looking further ahead, FY2015 revenue could approach the USD 300 million mark with Internet games revenue topping USD 200 million; WVAS and Mobile games comprising the remainder. Our Internet game revenue assumptions include flat revenue from WoT (a little over USD 20 million per quarter), but steady growth from GW2 and WoWP. The timing of the third title from Wargaming.net, World of Warships, could be a swing factor in Internet game revenue (margins also, considering pre-launch marketing expense). Assuming cost levels similar to earlier quarters (R&D about 12% of revenues, G&A about 5%, Sales & marketing bouncing around near 17%, etc.), FY2015 net income could reach about USD 39 million, or full-year earnings of about USD 0.80 per ADS.

Such a scenario may seem overly optimistic considering the company's recent performance (FY2013 EPS of USD 0.47), however as noted earlier, performance of GW2 and other Wargaming.net titles is key. We've applied what we consider to be relatively conservative assumptions, which could change based on progress along the way (Q3 results will be key).

Valuation

Assuming KongZhong can reach about USD 0.80 per share in FY2015, the stock currently trading under a 10x forward P/E. But is that cheap?

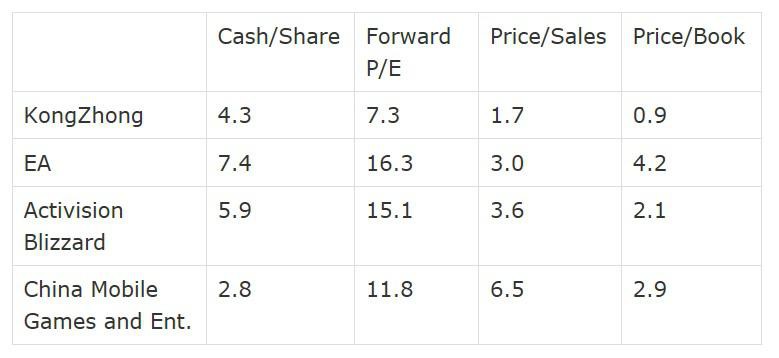

Another gaming company, China Mobile Games and Entertainment (NASDAQ:CMGE) has recently been trading on a forward P/E of about 12, and focuses on a somewhat similar space (mostly mobile games, not large MMO Internet games). Other, larger, game companies trade on more expensive multiples: EA (NASDAQ:EA) is about 16x, Activision Blizzard (NASDAQ:ATVI) is about 15x, so KongZhong trading under 10x may reflect an attractive opportunity. (Note that both EA and ATVI are significantly larger than KZ, so some small firm discount seems reasonable. CMGE, on the other hand, is smaller than KZ, with FY2013 revenue of about USD 58 million, much less than KZ's USD 174 million.)

Judging just "where" KZ should trade depends on how risky investors feel the company's future prospects are, and yes, the "China discount" that the market seems to apply to many smaller Chinese companies.

So retreating to something easier, let's apply CMGE's 12x forward multiple to KongZhong. Doing so results in a stock price close to $9.60, over +35% higher than recent trading levels. Yes, it's cheap, based on our earnings estimates.

As noted earlier, we've applied what we think are relatively conservative assumptions to the KongZhong's near-term outlook (our EPADS was a hair under management's guidance…which it usually beats). So the cheapness argument becomes even more compelling if our EPADS estimates are unfairly handicapping the company.

Risks

KongZhong's business is relatively straightforward, so the main risks are execution. Can the company keep GW2 growing? What about WoT and World of Warplanes, and later World of Warships? So far, it seems that KongZhong is doing reasonably well in its Internet games, however considering the competition in the space, success is anything but guaranteed. Seeing a rebound in operating metrics in Q3 will help provide clarity to the near-term prospects in the segment. But until then, seeing key titles placing highly in popularity ranking supports the idea that gamers are responding well to the titles.

For mobile games, similar questions pop up - creating winners isn't a slam-dunk, and the space is intensely competitive. The company has produced some hit titles this far, so success in mobile wouldn't exactly be unprecedented, giving us confidence in the flat/low-growth scenario discussed above.

KongZhong's WVAS business is another potential risk for the growth scenario. Mobile carriers have been making the business tougher for WVAS companies for the past several years, but the tightening seems to have leveled off recently. In our projections above, we assumed a 2-3% sequential decline in 2H FY2014, accelerating through FY2015, a conservative set of assumptions in our view. WVAS is definitely an industry in decline, and any changes in carrier policy could once again pressure the top line.

China's economic outlook is also a factor for KongZhong, but perhaps not in the obvious way it might seem. Internet and mobile games are a relatively inexpensive form of entertainment (KongZhong's average players spend under 200 RMB/month, slightly over the price of a pair of movie tickets in Beijing or Shanghai). If China's economy continues to weaken, paying to play Internet or mobile games could actually become more attractive (a month's worth of entertainment vs. one evening).

So now what?

The stock is significantly underfollowed and arguably unloved by the market. Turnover in the stock is very thin, with trailing volume under USD 1 million. A strong Q3 could help attract investor interest, particularly when looking at some of the other metrics:

Source: CapitalIQ, provided by Yahoo. KongZhong data is consensus, not figures referenced earlier in this article.

It looks like KZ is cheap, by just about any of the traditional metrics. The problem, therefore is a catalyst to get the market to notice the stock.

Management has hinted about a possible dividend, however it seems relatively unlikely in the near term (based on comments during the Q2 call). The company's business is highly cash generative, and it seems reasonable that after building up the cash cushion somewhat, a divided might be in the cards.

Other possible catalysts could be progress on the share buyback (there are still about 3 million shares eligible for purchase under the FY2012 buyback plan), something which may garner investor attention.

But until the market turns its attention back to KongZhong, patience is investors' only option.

We think that market is currently taking a "show me" approach to many US-listed Chinese companies, something which could provide opportunity for an investor with a longer time horizon.

-------------------------------------------------------------------------

Summary

•Not a WVAS company anymore, pushing forward in Internet games.

•Q2 results artificially lower due to new game launch costs.

•New games doing well, could be near-term growth drivers.

KongZhong (KZ, detailed company profile here) is an online game operator in China that has been off investors' radar, but deserves a closer look. The stock has been trading away from the business fundamentals, and taking a longer-term view could offer a rewarding opportunity to a patient investor.

The company is relatively small (market cap of about $300 million), so many investors may not have heard of it before. KongZhong came to the market in 2004 as a provider of SMS and other wireless value added services (WVAS), but adapted to the changing landscape by later expanding into mobile games. After the last of the founders left in FY2009, new management pushed ahead with a growth agenda including entering the online PC games business, acquiring a 3D massively multiplayer online game (MMOG) developer. In addition to developing its own games, KongZhong also began using the licensing model to bring games which were successful abroad into China; its first major title was World of Tanks, developed by Wargaming.net. World of Tanks has become a popular game in its genre, and has been the main driver of KongZhong's success in its Internet Games segment thus far.

Games - KongZhong's New Core

By the end of FY2013, the company's transformation from a "WVAS provider also involved in mobile games" into a company focused on PC gaming was complete. Indeed, non-WVAS revenues comprised the majority of total revenue in FY2013. The shift in focus was a deliberate and timely choice for management. The entire WVAS industry has been dwindling thanks to more powerful smartphones (data messages instead of SMS), and moving into Internet Games has been leading KongZhong's incremental growth.

Up until mid-FY2014, KongZhong's Internet Games business was basically World of Tanks, however the company launched two titles in Q2 that could change that. The first title is Guild Wars 2 (GW2), an innovative MMORPG offering a new type of gameplay beyond the traditional task or quest-based styles. According to disclosures from the company, it has sold over 1 million CD keys for the game through Q2, illustrating gamer demand. The performance of the game since launch appears to be going well (here is a note from VentureBeat). Despite the challenge of adapting to the new style of play GW2 offers and the upfront investment in buying the CD key, it remains a popular title in China. According to 17173.com, a website focusing on online games, GW2 was in the top-5 most popular games when checked in early September 2014. (Guild Wars 2 is "激战2" in Chinese.)

The game's release hasn't gone off without a few hitches, however, with some players finding the adjustment to the licensing model (paying up front for a key), and gameplay challenging. (Aside: some gamers can play other titles for up to a year before paying, so forking over cash before doing anything may have struck a sour note.) KongZhong has taken steps to address the learning curve, dedicating resources to help players transition into the new gameplay style, which could in turn make the payment model less of an issue for hesitant players. As of mid-Q3, KongZhong's management sounded very confident with progress up to that point, and noted that upcoming updates from ArenaNet, the game developer, could also help address some gameplay issues.

KongZhong's second major title released during Q2 was World of Warplanes, also licensed from Wargaming.net. One of the features of the game highlighted during the run-up to its release was how easy it was to play while delivering a realistic gaming experience (vs. real flight physics and hard controls or just the opposite). When discussing the game launch earlier, management sounded confident that it would be able to replicate some of the popularity achieved with World of Tanks. Potential tailwinds for the game include overall popularity with military-themed games in China, as well as crossover players from World of Tanks, due to the unified access afforded by the Wargaming platform.

Mobile Games - Another Avenue of Growth

In addition to the company's progress in PC games, KongZhong has also been pushing into the mobile game space. Its previous mobile game experience was mostly Java-based smartphone games, but a FY2012 acquisition brought smartphone game development expertise in-house. The company launched its first titles based on this technology in FY2013, which helped to later reignite growth in the Mobile games segment.

Success in mobile games is elusive, due in part to the ultra-competitive nature of the market in China, the "flavor of the month" phenomenon that can make-or-break a game's success, and frighteningly short lifespans. KongZhong's approach seems to borrow a page from Wayne Gretzky's playbook, something which could pay off in the long run. Instead of chasing the hot current trends, KongZhong is trying to develop great games that will win based on the game's own merits, not a hot trend. By focusing on where mobile game demand is going to be (not where stands currently), KongZhong trades the risk of chasing current demand for a longer-tail payoff. The company's execution history with smartphone games hasn't all been perfect; after all, not every game is a hit. But instead of abandoning its goal to make truly innovative games, management analyzed what wasn't right, and took the appropriate steps necessary to move forward. (Tiny War, which would later become Pocket Fort, is an example of this "keep after it" attitude.)

Recent Financial Performance

KongZhong's Q2 results weren't that great judging by the P&L: although sales grew YoY and QoQ, it reported an operating loss on higher spending and barely broke even thanks to interest income. Operating metrics also looked tough. Although more gamers were playing KongZhong's games, the key ARPU (average revenue per user) metric tumbled to an anemic 152 RMB.

And anyone stopping there could be forgiven for thinking the company isn't doing well. It's only after a closer look that the story changes.

First, on the operating margin compression: KongZhong launched two major titles during the Q2 (GW2 and World of Warplanes), which meant above-average sales and marketing expenses to support game launches. A successful launch can significantly help a game's chance for a bright future, and in the case of GW2, KongZhong spent the marketing dollars to build buzz in the gamer community. World of Warplanes was the second major launch in Q2, and although it might have seemed like a secondary consideration, it's important to keep in mind that the GW2 launch was a major event. Before the launch of GW2, it was one of the most anticipated titles in China (see this note from back in March 2014), hence the attention on the game. World of Warplanes was also on the list of highly anticipated games (#16 of the top 20), and there appears to be continuing gamer interest, judging by message board activity and news flow on related websites.

The timing of the game launches was also a factor in some of the operating metrics looking softer. Both Guild Wars 2 and World of Warplanes were launched in May 2014 (GW2 May 15, WoWP May 28), contributing to Active Users and Paying Accounts growth, but not ARPU. The calculation for ARPU is the total revenue divided by the number of paying players, so when players increased without a full period of their spending, ARPU was lower.

So on balance, was Q2 a bad quarter? Maybe not, after considering the successful launched of two major game titles, which helped KongZhong expand its Internet game portfolio from one title (World of Tanks), to potentially three major games. If the company can achieve a similar level of success with the new launches, an increase in revenue could follow.

What's Next in Q3?

KongZhong is guiding for revenue growth of about USD 65 million, or about +33% YoY and +7% QoQ, and improving margins (higher gross, operating, and net margins vs. Q2).

A few factors are driving the revenue and margin outlook: a more stable environment in the WVAS segment, incremental revenue contribution from the new Internet games, and also KongZhong's new Mobile games.

GuildWars 2 sounds like it is progressing well, as mentioned earlier, and KongZhong is continuing its promotion efforts to build up the player base. The company mentioned a limited free trial coming up, something which could help attract players who were hesitant to try the game. KongZhong's core title Word of Tanks has been stable, and potential concerns that the game was stagnating may be premature. Wargaming.net recently released a new gameplay mode called Stronghold which could impact player engagement (team members skirmish together to boost team-level battle capabilities and other features).

Management mentioned on the Q2 call that it had a few new Mobile games in the Q3 pipeline, and also planned some releases in Q4 (4-5 total during the second half). Although it's tough to tell if the games will be a hit, none of the titles in the pipeline sounded "risky" in terms of game style, so there could be some upside surprise in the outlook for the segment.

After performing some rough calculations, it seems like revenue could hit the USD 65-66 million level without too much trouble. This is based on flattish revenue contributions from WoT, a full quarter of GW2 and WoWP (averaging just under 8 million of revenue each), slightly lower WVAS revenues, and some degree of success in Mobile games (+5% QoQ). The operating profit margin picture improves assuming a slight rebound at the gross level (flatlined at 50% in our model), and a reduction in sales and marketing expenses (no big Internet game launches were scheduled).

Given the above, operating profit could get close to the USD 8 million mark, reflecting an operating profit margin of about 12% (up vs. 0% last quarter, and similar to levels seen in FY2013). Non-operating items have historically been minimal for KongZhong (non-cash impairment charges aside), so net income could be about USD 9 million. Assuming a moderate increase in shares outstanding, EPADS could be about USD 0.19 (diluted).

We feel this is a conservative estimate for the quarter, particularly when considering management's guidance for net profit of USD 9-10 million (about USD 0.20 per share). The company has recently been delivering results exceeding management's guidance (no surprise there), however we tried to be increasingly conservative to underscore the valuation argument, discussed below.

Applying similar growth and cost estimates to Q4 results in the same EPS (0.19 USD/ADS) and margin picture.

Key assumptions in the scenario above include continued success with GW2 and WoWP (we assume that the two titles combined will break the USD 20 million revenue barrier in Q2 FY2015), stable performance from WoT, and progress in Mobile games.

KongZhong's Mobile game segment passed the USD 10 million revenue hurdle in Q2, and we assumed growth of about 5% QoQ for the next two quarters, and flat afterward. Considering the games in the Mobile game pipeline (4-5 games, both self-developed and licensed), expecting some success from the segment doesn't seem like too much of a stretch.

FY2015

Looking further ahead, FY2015 revenue could approach the USD 300 million mark with Internet games revenue topping USD 200 million; WVAS and Mobile games comprising the remainder. Our Internet game revenue assumptions include flat revenue from WoT (a little over USD 20 million per quarter), but steady growth from GW2 and WoWP. The timing of the third title from Wargaming.net, World of Warships, could be a swing factor in Internet game revenue (margins also, considering pre-launch marketing expense). Assuming cost levels similar to earlier quarters (R&D about 12% of revenues, G&A about 5%, Sales & marketing bouncing around near 17%, etc.), FY2015 net income could reach about USD 39 million, or full-year earnings of about USD 0.80 per ADS.

Such a scenario may seem overly optimistic considering the company's recent performance (FY2013 EPS of USD 0.47), however as noted earlier, performance of GW2 and other Wargaming.net titles is key. We've applied what we consider to be relatively conservative assumptions, which could change based on progress along the way (Q3 results will be key).

Valuation

Assuming KongZhong can reach about USD 0.80 per share in FY2015, the stock currently trading under a 10x forward P/E. But is that cheap?

Another gaming company, China Mobile Games and Entertainment (NASDAQ:CMGE) has recently been trading on a forward P/E of about 12, and focuses on a somewhat similar space (mostly mobile games, not large MMO Internet games). Other, larger, game companies trade on more expensive multiples: EA (NASDAQ:EA) is about 16x, Activision Blizzard (NASDAQ:ATVI) is about 15x, so KongZhong trading under 10x may reflect an attractive opportunity. (Note that both EA and ATVI are significantly larger than KZ, so some small firm discount seems reasonable. CMGE, on the other hand, is smaller than KZ, with FY2013 revenue of about USD 58 million, much less than KZ's USD 174 million.)

Judging just "where" KZ should trade depends on how risky investors feel the company's future prospects are, and yes, the "China discount" that the market seems to apply to many smaller Chinese companies.

So retreating to something easier, let's apply CMGE's 12x forward multiple to KongZhong. Doing so results in a stock price close to $9.60, over +35% higher than recent trading levels. Yes, it's cheap, based on our earnings estimates.

As noted earlier, we've applied what we think are relatively conservative assumptions to the KongZhong's near-term outlook (our EPADS was a hair under management's guidance…which it usually beats). So the cheapness argument becomes even more compelling if our EPADS estimates are unfairly handicapping the company.

Risks

KongZhong's business is relatively straightforward, so the main risks are execution. Can the company keep GW2 growing? What about WoT and World of Warplanes, and later World of Warships? So far, it seems that KongZhong is doing reasonably well in its Internet games, however considering the competition in the space, success is anything but guaranteed. Seeing a rebound in operating metrics in Q3 will help provide clarity to the near-term prospects in the segment. But until then, seeing key titles placing highly in popularity ranking supports the idea that gamers are responding well to the titles.

For mobile games, similar questions pop up - creating winners isn't a slam-dunk, and the space is intensely competitive. The company has produced some hit titles this far, so success in mobile wouldn't exactly be unprecedented, giving us confidence in the flat/low-growth scenario discussed above.

KongZhong's WVAS business is another potential risk for the growth scenario. Mobile carriers have been making the business tougher for WVAS companies for the past several years, but the tightening seems to have leveled off recently. In our projections above, we assumed a 2-3% sequential decline in 2H FY2014, accelerating through FY2015, a conservative set of assumptions in our view. WVAS is definitely an industry in decline, and any changes in carrier policy could once again pressure the top line.

China's economic outlook is also a factor for KongZhong, but perhaps not in the obvious way it might seem. Internet and mobile games are a relatively inexpensive form of entertainment (KongZhong's average players spend under 200 RMB/month, slightly over the price of a pair of movie tickets in Beijing or Shanghai). If China's economy continues to weaken, paying to play Internet or mobile games could actually become more attractive (a month's worth of entertainment vs. one evening).

So now what?

The stock is significantly underfollowed and arguably unloved by the market. Turnover in the stock is very thin, with trailing volume under USD 1 million. A strong Q3 could help attract investor interest, particularly when looking at some of the other metrics:

Source: CapitalIQ, provided by Yahoo. KongZhong data is consensus, not figures referenced earlier in this article.

It looks like KZ is cheap, by just about any of the traditional metrics. The problem, therefore is a catalyst to get the market to notice the stock.

Management has hinted about a possible dividend, however it seems relatively unlikely in the near term (based on comments during the Q2 call). The company's business is highly cash generative, and it seems reasonable that after building up the cash cushion somewhat, a divided might be in the cards.

Other possible catalysts could be progress on the share buyback (there are still about 3 million shares eligible for purchase under the FY2012 buyback plan), something which may garner investor attention.

But until the market turns its attention back to KongZhong, patience is investors' only option.

We think that market is currently taking a "show me" approach to many US-listed Chinese companies, something which could provide opportunity for an investor with a longer time horizon.

Trading Spotlight

Die Argumentation das kleinere bzw. mittelgroße China Game/Internet Werte an der Nasdaq von den Amis kritisch gesehen werden, kann man auch nicht gelten lassen.

China Mobile Game and Entertaiment (CMGE) ist kleiner als Kong, hat schlechteres KGV (also deutlich höher), Bilanz deutlich schlechter, einzig das Wachstum ist deutlich höher.

Wenn man jetzt bedenkt das KONG jetzt auch in eine Wachstumsphase kommt, kann man nur sagen, das der Kurs von Kong ein Witz ist.

Der Sektor "gets hotter and hotter"

Würde mich auch mittlerweile nicht mehr wundern, wenn demnächst ein Großer versucht, KONG zu übernehmen. Attraktiv bewertet mit einer guten Marktstellung ist KONG ja.

------------------------------------

Mobile Gaming Industry Players Alibaba, Tencent, Tapinator Among Those Attracting Significant Interest Within The Sector

Delray Beach, FL / September 22, 2014 / According to Bloomberg, Alibaba's (BABA) IPO could become the biggest ever (topping Agricultural Bank of China's $22 billion IPO in 2010) if underwriters make use of an option to buy more shares, which market observers expect they will. The event created quite a buzz among both individual and institutional investors, with most asking if Alibaba's stock is a long term buy.

Alibaba certainly has key advantages over its chief rivals, most notably the fact that the company is located in China, where 560 million Internet users spend 20 hours per week online. Additionally, the sheer size of Alibaba allows significant cost savings with its large sales volumes. There are others, but investors must decide if these advantages are sustainable.

Alibaba and Tencent (TCEHY) now boast such a massive share of the Chinese market that they are crossing borders, targeting developing markets and entering the U.S. in search of new sources of growth. In the last two years, Alibaba and Tencent have made major investments in 13 U.S. tech start-ups, mostly in mobile and e-commerce, in addition to smaller investments in numerous companies.

Newly emerging mobile gaming company Tapinator, Inc. (TAPM) continues to quietly locate a wide-ranging customer base with its addicting lineup of games that make the most of their cross-genre and multi-generational appeal. Trading at 1.70 per share, the stock has trended upward the last few weeks, increasing approximately 70% in the past week alone, while its volume has surged; seems Wall St has taken notice of TAPM.

And while investors in another industry giant, China Mobile Games and Entertainment (CMGE) are seeing ups and downs over the past few weeks, they also see that CMGE's very impressive revenue growth greatly exceeded the industry average of 11.6%. Since the same quarter one year prior, revenues leaped by 275.8%. Growth in the company's revenue appears to have helped boost the earnings per share.

About Tapinator:

Tapinator (TAPM) is a developer and publisher of mobile games on the iOS, Google Play, and Amazon platforms. The Company focuses on operating its own titles, publishing properties where it holds substantial ownership positions, and making strategic investments into promising mobile companies. Tapinator's owned and operated portfolio includes over 50 mobile gaming titles that, collectively, have over 26 million users. A number of these titles have risen to the top of the mobile leaderboard charts and have been featured by the Apple, Google, and Amazon App Stores. Founded in 2013, Tapinator is headquartered in New York, with a major office located in Lahore, Pakistan. For a full listing of Tapinator game titles, please go to Tapinator.com. For further financial information on the Company, please go to OTCMarkets.com/stock/TAPM. For live updates, please like us on Facebook at facebook.com/Tapinator or follow us on Twitter at twitter.com/Tapinator.

About Tencent Holdings Ltd

Tencent Holdings Limited, an investment holding company, provides Internet and mobile value-added services (VAS), online advertising services, and e-commerce transactions services to users in the Peoples Republic of China, the United States, Europe, and internationally. The company operates through VAS, Online Advertising, e-Commerce Transactions, and Others segments. It provides online games, community value-added services, and applications across various Internet and mobile platforms; instant messaging services; value added services, such as club membership, avatar, personal spaces and communities, online music, dating services, etc.; and wireless Internet value added services, including short messaging service, multimedia messaging service, interactive voice response services, WAP, mobile IM service, and mobile games. The company also enables third-party game/application developers to host games/applications in its Internet platforms. Its online advertising services consist of display advertising on instant messaging clients, portals, social networks, and other platforms. The companys e-commerce transactions business primarily include the sale of merchandise through its Internet platforms, including QQ Instant Messenger, WeChat, QQ.com, QQ Games, Qzone, 3g.QQ.com, SoSo, PaiPai, and Tenpay. In addition, it provides trademark licensing, software development, and software sale services. Tencent Holdings Limited was founded in 1998 and is headquartered in Shenzhen, the Peoples Republic of China.

About Alibaba Group Holding Ltd

Alibaba Group Holding Limited, through its subsidiaries, operates as an online and mobile commerce company in the Peoples Republic of China and internationally. It operates Taobao Marketplace, an online shopping destination; Tmall, a third-party platform for brands and retailers; Juhuasuan, a group buying marketplace; Alibaba.com, an online business-to-business marketplace that focuses on global trade among businesses; 1688.com, an online wholesale marketplace; and AliExpress, a consumer marketplace. The company also provides pay-for-performance (P4P) and display marketing services through its Alimama marketing technology platform; Taobao Ad Network and Exchange (TANX), a real-time online advertising exchange in China; and data management platform that allows participants on TANX to evaluate and select online advertising inventory using behavioral data, as well as data from browsing behavior and shopping history. In addition, it offers cloud computing services, including elastic computing, database services, and storage and large scale computing services through its Alibaba Cloud Computing platform; payment and escrow services for buyers and sellers; and develops and operates mobile Web browsers. The company provides its solutions primarily for businesses. Alibaba Group Holding Limited was founded in 1999 and is headquartered in Hangzhou, the Peoples Republic of China.

About China Mobile Games and Entertainment Group Limited

China Mobile Games and Entertainment Group Limited, through its subsidiaries, develops and publishes mobile games primarily in the Peoples Republic of China. It provides social games and single-player games for mobiles. The company also offers handset design solutions comprising printed circuit board with operating system software and optional assembly services, and mobile phone contents installation services to mobile phone manufacturers and mobile phone content providers. As of December 31, 2013, its game portfolio consisted of 717 mobile games, including 72 social games and 645 single-player games, of which 196 were developed in-house and 521 were licensed from mobile game developers. The company was incorporated in 2011 and is based in Guangzhou, the Peoples Republic of China. China Mobile Games and Entertainment Group Limited is a subsidiary of VODone Limited.

Würde mich auch mittlerweile nicht mehr wundern, wenn demnächst ein Großer versucht, KONG zu übernehmen. Attraktiv bewertet mit einer guten Marktstellung ist KONG ja.

------------------------------------

Mobile Gaming Industry Players Alibaba, Tencent, Tapinator Among Those Attracting Significant Interest Within The Sector

Delray Beach, FL / September 22, 2014 / According to Bloomberg, Alibaba's (BABA) IPO could become the biggest ever (topping Agricultural Bank of China's $22 billion IPO in 2010) if underwriters make use of an option to buy more shares, which market observers expect they will. The event created quite a buzz among both individual and institutional investors, with most asking if Alibaba's stock is a long term buy.

Alibaba certainly has key advantages over its chief rivals, most notably the fact that the company is located in China, where 560 million Internet users spend 20 hours per week online. Additionally, the sheer size of Alibaba allows significant cost savings with its large sales volumes. There are others, but investors must decide if these advantages are sustainable.

Alibaba and Tencent (TCEHY) now boast such a massive share of the Chinese market that they are crossing borders, targeting developing markets and entering the U.S. in search of new sources of growth. In the last two years, Alibaba and Tencent have made major investments in 13 U.S. tech start-ups, mostly in mobile and e-commerce, in addition to smaller investments in numerous companies.

Newly emerging mobile gaming company Tapinator, Inc. (TAPM) continues to quietly locate a wide-ranging customer base with its addicting lineup of games that make the most of their cross-genre and multi-generational appeal. Trading at 1.70 per share, the stock has trended upward the last few weeks, increasing approximately 70% in the past week alone, while its volume has surged; seems Wall St has taken notice of TAPM.

And while investors in another industry giant, China Mobile Games and Entertainment (CMGE) are seeing ups and downs over the past few weeks, they also see that CMGE's very impressive revenue growth greatly exceeded the industry average of 11.6%. Since the same quarter one year prior, revenues leaped by 275.8%. Growth in the company's revenue appears to have helped boost the earnings per share.

About Tapinator:

Tapinator (TAPM) is a developer and publisher of mobile games on the iOS, Google Play, and Amazon platforms. The Company focuses on operating its own titles, publishing properties where it holds substantial ownership positions, and making strategic investments into promising mobile companies. Tapinator's owned and operated portfolio includes over 50 mobile gaming titles that, collectively, have over 26 million users. A number of these titles have risen to the top of the mobile leaderboard charts and have been featured by the Apple, Google, and Amazon App Stores. Founded in 2013, Tapinator is headquartered in New York, with a major office located in Lahore, Pakistan. For a full listing of Tapinator game titles, please go to Tapinator.com. For further financial information on the Company, please go to OTCMarkets.com/stock/TAPM. For live updates, please like us on Facebook at facebook.com/Tapinator or follow us on Twitter at twitter.com/Tapinator.

About Tencent Holdings Ltd

Tencent Holdings Limited, an investment holding company, provides Internet and mobile value-added services (VAS), online advertising services, and e-commerce transactions services to users in the Peoples Republic of China, the United States, Europe, and internationally. The company operates through VAS, Online Advertising, e-Commerce Transactions, and Others segments. It provides online games, community value-added services, and applications across various Internet and mobile platforms; instant messaging services; value added services, such as club membership, avatar, personal spaces and communities, online music, dating services, etc.; and wireless Internet value added services, including short messaging service, multimedia messaging service, interactive voice response services, WAP, mobile IM service, and mobile games. The company also enables third-party game/application developers to host games/applications in its Internet platforms. Its online advertising services consist of display advertising on instant messaging clients, portals, social networks, and other platforms. The companys e-commerce transactions business primarily include the sale of merchandise through its Internet platforms, including QQ Instant Messenger, WeChat, QQ.com, QQ Games, Qzone, 3g.QQ.com, SoSo, PaiPai, and Tenpay. In addition, it provides trademark licensing, software development, and software sale services. Tencent Holdings Limited was founded in 1998 and is headquartered in Shenzhen, the Peoples Republic of China.

About Alibaba Group Holding Ltd

Alibaba Group Holding Limited, through its subsidiaries, operates as an online and mobile commerce company in the Peoples Republic of China and internationally. It operates Taobao Marketplace, an online shopping destination; Tmall, a third-party platform for brands and retailers; Juhuasuan, a group buying marketplace; Alibaba.com, an online business-to-business marketplace that focuses on global trade among businesses; 1688.com, an online wholesale marketplace; and AliExpress, a consumer marketplace. The company also provides pay-for-performance (P4P) and display marketing services through its Alimama marketing technology platform; Taobao Ad Network and Exchange (TANX), a real-time online advertising exchange in China; and data management platform that allows participants on TANX to evaluate and select online advertising inventory using behavioral data, as well as data from browsing behavior and shopping history. In addition, it offers cloud computing services, including elastic computing, database services, and storage and large scale computing services through its Alibaba Cloud Computing platform; payment and escrow services for buyers and sellers; and develops and operates mobile Web browsers. The company provides its solutions primarily for businesses. Alibaba Group Holding Limited was founded in 1999 and is headquartered in Hangzhou, the Peoples Republic of China.

About China Mobile Games and Entertainment Group Limited

China Mobile Games and Entertainment Group Limited, through its subsidiaries, develops and publishes mobile games primarily in the Peoples Republic of China. It provides social games and single-player games for mobiles. The company also offers handset design solutions comprising printed circuit board with operating system software and optional assembly services, and mobile phone contents installation services to mobile phone manufacturers and mobile phone content providers. As of December 31, 2013, its game portfolio consisted of 717 mobile games, including 72 social games and 645 single-player games, of which 196 were developed in-house and 521 were licensed from mobile game developers. The company was incorporated in 2011 and is based in Guangzhou, the Peoples Republic of China. China Mobile Games and Entertainment Group Limited is a subsidiary of VODone Limited.

Der Call KZ141220C00007500

Läuft bis 20.12. (also nach den Zahlen von Q3) Basis 7,50 USD

Wird gerade gut und günstig gehandelt für 0,30 bis 0,35 USD. (Wer kauft da gerade von euch ? )

)

Die Chance zum Einstieg wäre jetzt da, wer Interesse hat.

Läuft bis 20.12. (also nach den Zahlen von Q3) Basis 7,50 USD

Wird gerade gut und günstig gehandelt für 0,30 bis 0,35 USD. (Wer kauft da gerade von euch ?

)

)Die Chance zum Einstieg wäre jetzt da, wer Interesse hat.

Ein Put hätte bis jetzt mehr gebracht - neues 52 Wochen-Tief heute.

Gibt's Gründe - finde nix.

Gibt's Gründe - finde nix.

Vielleicht deswegen:

KongZhong Corp. Sponsored ADR (KZ) gets weaker ratings this week as last

week’s D drops to an F. The stock also gets an F in Earnings Growth.

Ist aber bereits vom 18.09.

KongZhong Corp. Sponsored ADR (KZ) gets weaker ratings this week as last

week’s D drops to an F. The stock also gets an F in Earnings Growth.

Ist aber bereits vom 18.09.

Allgemeine Marktschwäche heute.

Wichtig sind die Zahlen in 2 Monaten (Ende November).

Dann sollte es spätestens einen kräftigen Rebound geben.

Wichtig sind die Zahlen in 2 Monaten (Ende November).

Dann sollte es spätestens einen kräftigen Rebound geben.

Boden bei 6,50 USD ?????

Mal sehen.

Antwort auf Beitrag Nr.: 47.877.437 von Reiners am 25.09.14 18:53:54

Nur mit Marktschwäche ist der Kursverlauf aber nicht zu erklären.

Heute schon bei 6,15$

Zitat von Reiners: Allgemeine Marktschwäche heute.

Wichtig sind die Zahlen in 2 Monaten (Ende November).

Dann sollte es spätestens einen kräftigen Rebound geben.

Nur mit Marktschwäche ist der Kursverlauf aber nicht zu erklären.

Heute schon bei 6,15$

Marktschwäche / Chartschwäche nenn es wie Du willst.

Entscheidend für mich - es gibt zur Zeit gute Kaufkurse, bei der Aktie wie auch bei meinen beiden favorisierten Optionen.

Deshalb habe ich gerade zugekauft und weitere 480 Optionen zu 0,25 USD erworden (7,5 USD call 19 Dezember)

Der Gewinn soll dann in 2 Monaten erzielt werden, bzw. bei Ausübung der Option am 20 Dez.

Wäre dann doch ein schönen Weihnachtsgeschenk.

------------

Denke auch nicht das es deutlich unter 6 USD geht, weil wir zum 30.9 auf ca 5,30 Cash bzw cashähnlich Wert pro Share sitzen.

------

Habe vor noch weitere Optionen zu kaufen (in den nächsten Tagen / Wochen)

Dann aber den (sichereren) 7,5 call März 2015. Vom 7,5 call Dez 2014 habe ich jetzt genug gekauft.

Entscheidend für mich - es gibt zur Zeit gute Kaufkurse, bei der Aktie wie auch bei meinen beiden favorisierten Optionen.

Deshalb habe ich gerade zugekauft und weitere 480 Optionen zu 0,25 USD erworden (7,5 USD call 19 Dezember)

Der Gewinn soll dann in 2 Monaten erzielt werden, bzw. bei Ausübung der Option am 20 Dez.

Wäre dann doch ein schönen Weihnachtsgeschenk.

------------

Denke auch nicht das es deutlich unter 6 USD geht, weil wir zum 30.9 auf ca 5,30 Cash bzw cashähnlich Wert pro Share sitzen.

------

Habe vor noch weitere Optionen zu kaufen (in den nächsten Tagen / Wochen)

Dann aber den (sichereren) 7,5 call März 2015. Vom 7,5 call Dez 2014 habe ich jetzt genug gekauft.

Mal sehen ob die 6,00 USD halten. Aktuell 6,12 USD

Zudem scheint bei um 6 USD die 2 jährige Unterstützung im Chart zu liegen.

Kongzhong (KZ) provides digital entertainment services in the People's Republic of China. This stock closed up 2.6% to $6.52 in Tuesday’s trading session.

Tuesday's Range: $6.11-$6.57

52-Week Range: $6.11-$13.64

Tuesday's Volume: 325,000

Three-Month Average Volume: 102,739

From a technical perspective, KZ bounced notably higher here right off its new 52-week low of $6.11 with above-average volume. This stock has been downtrending badly for the last five months, with shares falling sharply from its high of $10.61 to its new 52-week low of $6.11. During that downtrend, shares of KZ have been consistently making lower highs and lower lows, which is bearish technical price action. That move has also pushed shares of KZ into extremely oversold territory, since its current relative strength index reading is 25.43. Oversold can always get more oversold, but it's also an area from which a stock can experience a powerful bounce higher if the sellers have become exhausted.

Traders should now look for long-biased trades in KZ as long as it's trending above its new 52-week low of $6.11 and then once it sustains a move or close above Tuesday's intraday high of $6.57 to some more near-term overhead resistance levels at $7.07 to $7.12 with volume that hits near or above 102,739 shares. If that move materializes soon, then KZ will set up to re-test or possibly take out its next major overhead resistance levels at $7.50 to its 50-day moving average at $7.69, or even $8 to $8.50.

Tuesday's Range: $6.11-$6.57

52-Week Range: $6.11-$13.64

Tuesday's Volume: 325,000

Three-Month Average Volume: 102,739

From a technical perspective, KZ bounced notably higher here right off its new 52-week low of $6.11 with above-average volume. This stock has been downtrending badly for the last five months, with shares falling sharply from its high of $10.61 to its new 52-week low of $6.11. During that downtrend, shares of KZ have been consistently making lower highs and lower lows, which is bearish technical price action. That move has also pushed shares of KZ into extremely oversold territory, since its current relative strength index reading is 25.43. Oversold can always get more oversold, but it's also an area from which a stock can experience a powerful bounce higher if the sellers have become exhausted.

Traders should now look for long-biased trades in KZ as long as it's trending above its new 52-week low of $6.11 and then once it sustains a move or close above Tuesday's intraday high of $6.57 to some more near-term overhead resistance levels at $7.07 to $7.12 with volume that hits near or above 102,739 shares. If that move materializes soon, then KZ will set up to re-test or possibly take out its next major overhead resistance levels at $7.50 to its 50-day moving average at $7.69, or even $8 to $8.50.

Das rappelt heute ja ganz schön, auch bei anderen Nasdaq-Werten.

Die erwischts ja gerne überproportional. Außerdem ist in letzter Zeit viel Geld in spekulative Ipos geflossen, das macht sich vermutlich jetzt auch bemerkbar.

Die erwischts ja gerne überproportional. Außerdem ist in letzter Zeit viel Geld in spekulative Ipos geflossen, das macht sich vermutlich jetzt auch bemerkbar.

Middas, schon mal wieder von Dir zu hören.

Ist ja schon fast 10 Jahre, wo wir uns das erste Mal mit KONG beschäftigt haben.

Wie die Zeit vergeht.

Ist ja schon fast 10 Jahre, wo wir uns das erste Mal mit KONG beschäftigt haben.

Wie die Zeit vergeht.

http://chinastockresearch.com/company-profiles/company-summa…

Übrigens ein sehr guter Überblick zu KONG. Die ausführlichste Seite die ich zu Kong kenne.

Wer das Geschäftsmodel von Kong besser verstehen will, sollte diese Seite sich mal anschauen.

Übrigens ein sehr guter Überblick zu KONG. Die ausführlichste Seite die ich zu Kong kenne.

Wer das Geschäftsmodel von Kong besser verstehen will, sollte diese Seite sich mal anschauen.

Antwort auf Beitrag Nr.: 47.924.690 von Midas2000 am 01.10.14 21:06:17Rappelt heute weiter.

Kong hält sich (bis jetzt) ganz gut.

Kong hält sich (bis jetzt) ganz gut.

Future Growth

KongZhong’s CEO Leilei Wang, is aiming for annual game revenues in the 400-500MM USD range by FY2016, which would reflect annual growth of about 200% from FY2013. Along with top-line growth, management also expects to deliver margin expansion, indicating that 20-25% was within the realm of possibility on the Q4 FY2013 conference call.

which would reflect annual growth of about 200% from FY2013. Along with top-line growth, management also expects to deliver margin expansion, indicating that 20-25% was within the realm of possibility on the Q4 FY2013 conference call.

Investors may be skeptical, and have every right to be so. Achieving such stellar results would be a stark contrast from performance in recent years (annual revenue growth of about 15% from FY2007-2013, operating margins about 2% over the same period). Dismissing management’s projections as wishful thinking may unfairly discount the potential of existing, and growing, games as well as those games already announced in the pipeline. World of Tanks has been in operation for only three full years as of early FY2014, and new players were still signing up (WoT revenues grew nearly +25% YoY in FY2013), supporting the continuing growth thesis.

The 400-500 million USD target seems less far-fetched when considering the potential in the development pipeline, namely Guild Wars 2 and other Wargaming.net titles like World of Warplanes. If KongZhong can introduce these titles to Chinese gamers with a degree of success similar to World of Tanks, achieving the total becomes less of a stretch. The gap narrows further when considering the potential contributions from mobile (smartphone) games in the works and possibilities from other MMOs (Blitzkrieg 3, Master of Meteor Blades).

KongZhong’s CEO Leilei Wang, is aiming for annual game revenues in the 400-500MM USD range by FY2016,

which would reflect annual growth of about 200% from FY2013. Along with top-line growth, management also expects to deliver margin expansion, indicating that 20-25% was within the realm of possibility on the Q4 FY2013 conference call.

which would reflect annual growth of about 200% from FY2013. Along with top-line growth, management also expects to deliver margin expansion, indicating that 20-25% was within the realm of possibility on the Q4 FY2013 conference call.Investors may be skeptical, and have every right to be so. Achieving such stellar results would be a stark contrast from performance in recent years (annual revenue growth of about 15% from FY2007-2013, operating margins about 2% over the same period). Dismissing management’s projections as wishful thinking may unfairly discount the potential of existing, and growing, games as well as those games already announced in the pipeline. World of Tanks has been in operation for only three full years as of early FY2014, and new players were still signing up (WoT revenues grew nearly +25% YoY in FY2013), supporting the continuing growth thesis.

The 400-500 million USD target seems less far-fetched when considering the potential in the development pipeline, namely Guild Wars 2 and other Wargaming.net titles like World of Warplanes. If KongZhong can introduce these titles to Chinese gamers with a degree of success similar to World of Tanks, achieving the total becomes less of a stretch. The gap narrows further when considering the potential contributions from mobile (smartphone) games in the works and possibilities from other MMOs (Blitzkrieg 3, Master of Meteor Blades).

Welchen Call ich auch noch empfehlen kann, für die die es sicherer haben wollen und auf ein paar Prozente verzichten können / wollen.

Den Call 5 USD Laufzeit 20 März 2015

Ist 1,40 zu 1,90 gestellt aktuell.

Das heisst man zahlt 1,90 USD je Option. Und der Schein hat jezzt schon einen inneren Wert von 1,30 USD

6,30 USD (Kurs aktuell) - 5 USD Basis = 1,30 USD inner Wert.

Das Schöne, der Schein läuft noch 5,5 Monate.

Den Call 5 USD Laufzeit 20 März 2015

Ist 1,40 zu 1,90 gestellt aktuell.

Das heisst man zahlt 1,90 USD je Option. Und der Schein hat jezzt schon einen inneren Wert von 1,30 USD

6,30 USD (Kurs aktuell) - 5 USD Basis = 1,30 USD inner Wert.

Das Schöne, der Schein läuft noch 5,5 Monate.

Antwort auf Beitrag Nr.: 47.934.028 von Reiners am 02.10.14 17:21:15

Das klingt natürlich sehr vielversprechend, und wenn es so käme hätten wir hier einen Tenbagger.

Aber: Extrem ambitionierte Ziele eines Managements sind nach meiner Erfahrung sehr mit Vorsicht zu genießen.

Insbesondere, wenn dies mit einer verlockend niedrigen Bewertung einhergeht.

Der Markt hat nicht immer recht, aber was allzu attraktiv erscheint hat meist doch einen Haken.

Es ist also zumindest eine heiße Wette, selbst als Aktie. Da ist es vielleicht wirklich besser, einen Call zu nehmen, und dafür - bei ähnlichen Chancen - eine deutlich niedrigere Investitionssumme ins Feuer zu schicken.

Leider gibt es in Deutschland keine Scheine of Kong, und die US-Scheine kann ich bei Comdirect (jedenfalls online) nicht handeln.

Bei welchem Broker kaufst Du die denn?

Zitat von Reiners: Future Growth

KongZhong’s CEO Leilei Wang, is aiming for annual game revenues in the 400-500MM USD range by FY2016,

Das klingt natürlich sehr vielversprechend, und wenn es so käme hätten wir hier einen Tenbagger.

Aber: Extrem ambitionierte Ziele eines Managements sind nach meiner Erfahrung sehr mit Vorsicht zu genießen.

Insbesondere, wenn dies mit einer verlockend niedrigen Bewertung einhergeht.

Der Markt hat nicht immer recht, aber was allzu attraktiv erscheint hat meist doch einen Haken.

Es ist also zumindest eine heiße Wette, selbst als Aktie. Da ist es vielleicht wirklich besser, einen Call zu nehmen, und dafür - bei ähnlichen Chancen - eine deutlich niedrigere Investitionssumme ins Feuer zu schicken.

Leider gibt es in Deutschland keine Scheine of Kong, und die US-Scheine kann ich bei Comdirect (jedenfalls online) nicht handeln.

Bei welchem Broker kaufst Du die denn?

Lynx Broker

Die wiederum handeln über ihren Partner Interaktive Broker der sehr sehr leistungsstark ist

ist einer der größten Broker in der Welt glaube ich

kann ich sehr empfehlen

Die wiederum handeln über ihren Partner Interaktive Broker der sehr sehr leistungsstark ist

ist einer der größten Broker in der Welt glaube ich

kann ich sehr empfehlen

Lynx macht übrigens auch Werbung hier bei WO

kosten sind auch deutlich günstiger als dein Broker

kosten sind auch deutlich günstiger als dein Broker

Antwort auf Beitrag Nr.: 47.964.430 von Reiners am 07.10.14 17:12:41

Übrigens bekommt man den Call aktuell für 1,50 USD.

Ein Schnäppchen aus meiner Sicht.

Zitat von Reiners: Welchen Call ich auch noch empfehlen kann, für die die es sicherer haben wollen und auf ein paar Prozente verzichten können / wollen.

Den Call 5 USD Laufzeit 20 März 2015

Ist 1,40 zu 1,90 gestellt aktuell.

Das heisst man zahlt 1,90 USD je Option. Und der Schein hat jezzt schon einen inneren Wert von 1,30 USD

6,30 USD (Kurs aktuell) - 5 USD Basis = 1,30 USD inner Wert.

Das Schöne, der Schein läuft noch 5,5 Monate.

Übrigens bekommt man den Call aktuell für 1,50 USD.

Ein Schnäppchen aus meiner Sicht.

KongZhong is Now Oversold (KZ)

10/13/14 - 01:18 PM EDT

Legendary investor Warren Buffett advises to be fearful when others are greedy, and be greedy when others are fearful. One way we can try to measure the level of fear in a given stock is through a technical analysis indicator called the Relative Strength Index, or RSI, which measures momentum on a scale of zero to 100. A stock is considered to be oversold if the RSI reading falls below 30.

In trading on Monday, shares of KongZhong Corp (KZ) entered into oversold territory, hitting an RSI reading of 28.6, after changing hands as low as $5.85 per share. By comparison, the current RSI reading of the S&P 500 ETF (SPY) is 32.6. A bullish investor could look at KZ's 28.6 RSI reading today as a sign that the recent heavy selling is in the process of exhausting itself, and begin to look for entry point opportunities on the buy side. The chart below shows the one year performance of KZ shares:

10/13/14 - 01:18 PM EDT

Legendary investor Warren Buffett advises to be fearful when others are greedy, and be greedy when others are fearful. One way we can try to measure the level of fear in a given stock is through a technical analysis indicator called the Relative Strength Index, or RSI, which measures momentum on a scale of zero to 100. A stock is considered to be oversold if the RSI reading falls below 30.

In trading on Monday, shares of KongZhong Corp (KZ) entered into oversold territory, hitting an RSI reading of 28.6, after changing hands as low as $5.85 per share. By comparison, the current RSI reading of the S&P 500 ETF (SPY) is 32.6. A bullish investor could look at KZ's 28.6 RSI reading today as a sign that the recent heavy selling is in the process of exhausting itself, and begin to look for entry point opportunities on the buy side. The chart below shows the one year performance of KZ shares:

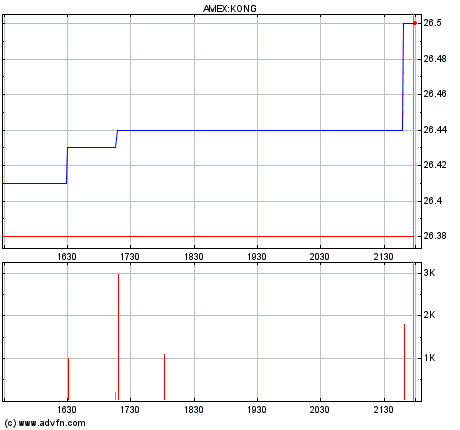

Hier noch der Chart zum Artikel oben

Brutaler Absturz für einen Nasdaq-Wert, der bis auf die mäßigen Q2 Zahlen keine schlechten Nachrichten gebracht hat

Brutaler Absturz für einen Nasdaq-Wert, der bis auf die mäßigen Q2 Zahlen keine schlechten Nachrichten gebracht hat

Das sollte der "kurstechnische" Brustlöser sein.

KongZhong Corporation Announces Special Cash Dividend of USD 0.88 per

43 minutes ago

BEIJING, Oct. 17, 2014 /PRNewswire/ -- KongZhong Corporation (KZ), a leading online games publisher and developer in the PRC, today announced that its Board of Directors has declared a special one-time cash dividend of US$0.022 per ordinary share, or US$0.88 per American Depositary Share ("ADS").

Record holders of the Company's ordinary shares and holders of the Company's ADSs, each representing forty ordinary shares, at the close of business on October 27, 2014 (the "Record Date") will be entitled to receive the special dividend. Citibank, N.A., the depositary bank for the Company's ADS program, expects to pay out dividend to ADS holders on or around November 10, 2014. Dividends to be paid to the Company's ADS holders through the depositary bank will be subject to the terms of the deposit agreement, including the fees and expenses payable thereunder.

The total amount of cash to be distributed for the special dividend is expected to be approximately US$40.1 million.

The Company's Chairman and Chief Executive Officer, Leilei Wang said, "Today's announcement of a US$0.88 per ADS special dividend, is our latest effort in returning capital to our shareholders. Over the past six years, we have undertaken share repurchases with a cumulative value of US$39.3 million. Our strong balance sheet and positive growth opportunities in our Internet and mobile game businesses have allowed us to provide shareholders with this dividend, while preserving financial and operational flexibility to grow our business in the rapidly growing Chinese online game markets. We have strong confidence in our operation cash flow and may consider making further efforts to return capital to our shareholders through dividend distributions. However, the distribution of any dividends will be at the full discretion of the Board of Directors and will be dependent upon our financial position, results of operations, available cash, capital requirements and other factors."

As of June 30, 2014, the Company had US$230.58 million (or US$5.07 per ADS) in cash and cash equivalents, term deposits, held-to-maturity securities, available-for-sale securities and restricted cash. The Company generated US$29.34 million in net cash provided by operating activities for the six months ended June 30, 2014.

KongZhong Corporation Announces Special Cash Dividend of USD 0.88 per

43 minutes ago