Ferronordic Machines - 500 Beiträge pro Seite

eröffnet am 13.05.17 14:23:30 von

neuester Beitrag 12.09.18 11:47:11 von

neuester Beitrag 12.09.18 11:47:11 von

Beiträge: 3

ID: 1.252.808

ID: 1.252.808

Aufrufe heute: 0

Gesamt: 651

Gesamt: 651

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| vor 49 Minuten | 2801 | |

| vor 1 Stunde | 1775 | |

| vor 47 Minuten | 1478 | |

| vor 47 Minuten | 985 | |

| heute 08:27 | 980 | |

| vor 41 Minuten | 971 | |

| heute 09:56 | 781 | |

| vor 42 Minuten | 707 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 1. | 17.756,45 | -0,10 | 172 | |||

| 2. | 2. | 143,32 | -1,66 | 131 | |||

| 3. | 3. | 2.378,97 | +0,77 | 69 | |||

| 4. | 5. | 6,6920 | +1,49 | 67 | |||

| 5. | 4. | 7,0000 | -5,41 | 56 | |||

| 6. | 6. | 3,7150 | +3,05 | 38 | |||

| 7. | 7. | 0,4034 | +0,35 | 37 | |||

| 8. | 29. | 22,610 | +5,46 | 32 |

gefunden in einem Letter von Alluvial Capital:

Ferronordic Machines AB Preferred

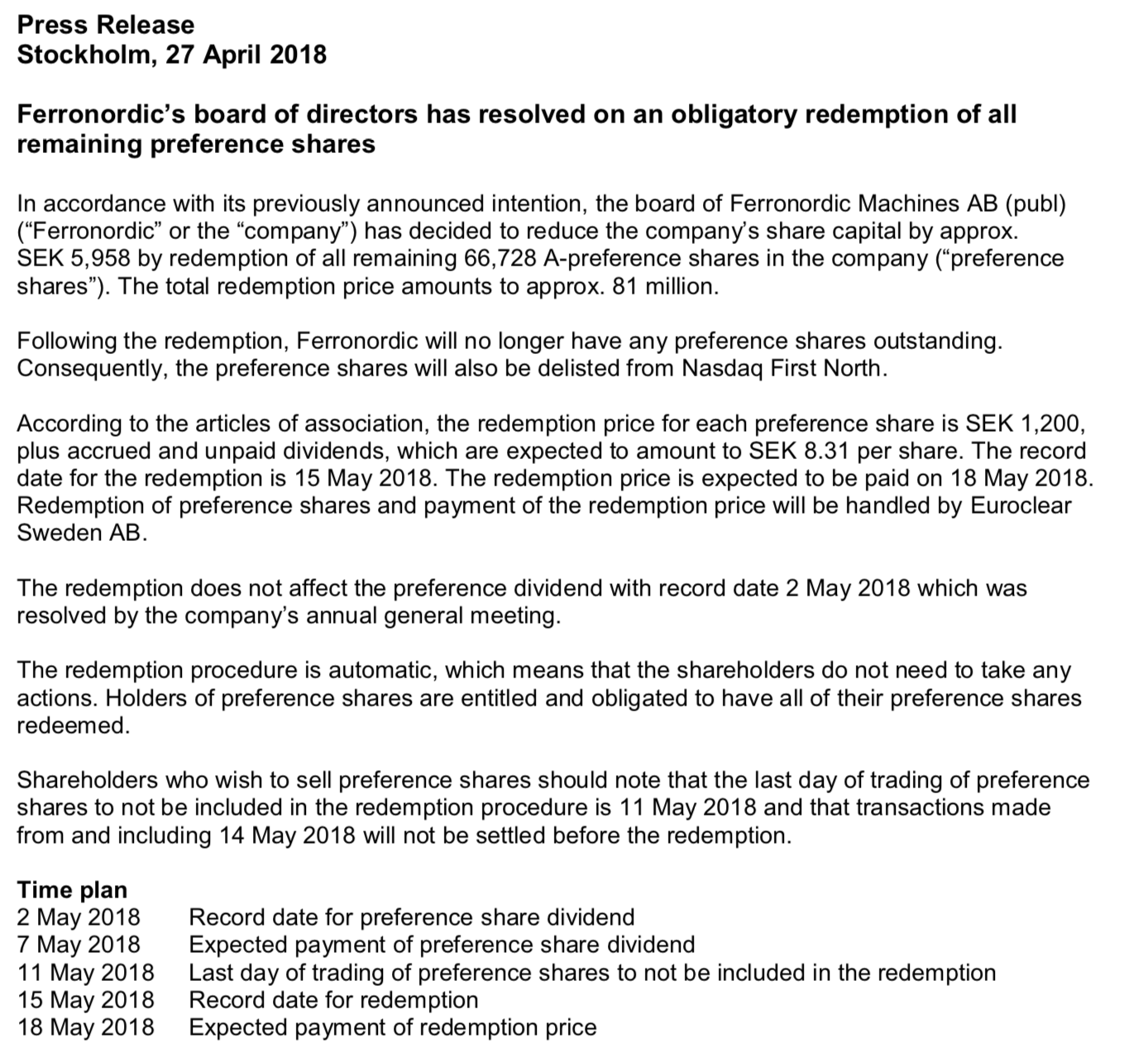

One of the more unusual ideas I have ever come across is preferred shares of Ferronordic Machines AB. (I suspect a few of you have looked at your portfolios only to see the ticker FNMA and wondered if I’ve lost my mind buying Fannie Mae. No, it’s Ferronordic.)

A Swedish company, Ferronordic Machines is the authorized dealer of Volvo construction equipment and Terex trucks in the Russian Federation. The company deals in new and used vehicles and also supplies parts and support services. Ferronordic was founded in 2010 and expanded rapidly.

The company issued a series of preferred stock in 2013 to provide growth capital in anticipation of an eventual IPO of its common shares. The preferred stock would be convertible into common shares in an IPO at a discounted rate. Well, the Russian economy ran into trouble, profits plunged, and no IPO would occur.

Here is where things get interesting!

The preferred stock has some neat features. First, the coupon increases by SEK 10 annually. The annual coupon is now SEK 110 and will top out at SEK 180 in 2023. Second, the delayed IPO has caused the effective value of the preferred stock in a conversion to increase to the maximum SEK 1,300 from the original SEK 1,150. In the event that a holder elects not to convert to common stock in an IPO, the preferred stock is redeemable by the company at a price of SEK 1,200.

Ferronordic Machines AB preferred shares trade at SEK 945. This represents a discount of 21% to liquidation/redemption value and 27% to conversion value, as well as a current dividend yield of 11.6%. Because the annual dividend will only increase, this is a very expensive source of financing for Ferronordic Machines. The company has every incentive to restructure these preferreds via an IPO or share exchange. An IPO is no longer a remote possibility as recovering market conditions have allowed the company to return to profitability.

Ferronordic Machines used the downturn to become as efficient as possible and to pay down debt to a net cash position, so the preferred stock sits in a favorable position in Ferronordic’s capital structure. For the preferred shares to be worth their full 1,200 redemption value, Ferronordic Machines AB must be worth at least 3.4x trailing EBIT. This is a very low hurdle. At the current price, Ferronordic preferred shares offer a potential IRR of 15%+ from rising dividend payments alone, and substantially higher if the company can pull off an IPO at some point in the coming years.

The main risks to the value of Ferronordic Machines AB preferred stock are macroeconomic and political. The Russian economy is ever precarious, heavily exposed to fluctuations in commodities prices and the whims of an autocratic government. While Ferronordic cites gradually improving conditions, a return to recession would impact the company’s financial position and further delay an IPO.

Ferronordic Machines AB Preferred

One of the more unusual ideas I have ever come across is preferred shares of Ferronordic Machines AB. (I suspect a few of you have looked at your portfolios only to see the ticker FNMA and wondered if I’ve lost my mind buying Fannie Mae. No, it’s Ferronordic.)

A Swedish company, Ferronordic Machines is the authorized dealer of Volvo construction equipment and Terex trucks in the Russian Federation. The company deals in new and used vehicles and also supplies parts and support services. Ferronordic was founded in 2010 and expanded rapidly.

The company issued a series of preferred stock in 2013 to provide growth capital in anticipation of an eventual IPO of its common shares. The preferred stock would be convertible into common shares in an IPO at a discounted rate. Well, the Russian economy ran into trouble, profits plunged, and no IPO would occur.

Here is where things get interesting!

The preferred stock has some neat features. First, the coupon increases by SEK 10 annually. The annual coupon is now SEK 110 and will top out at SEK 180 in 2023. Second, the delayed IPO has caused the effective value of the preferred stock in a conversion to increase to the maximum SEK 1,300 from the original SEK 1,150. In the event that a holder elects not to convert to common stock in an IPO, the preferred stock is redeemable by the company at a price of SEK 1,200.

Ferronordic Machines AB preferred shares trade at SEK 945. This represents a discount of 21% to liquidation/redemption value and 27% to conversion value, as well as a current dividend yield of 11.6%. Because the annual dividend will only increase, this is a very expensive source of financing for Ferronordic Machines. The company has every incentive to restructure these preferreds via an IPO or share exchange. An IPO is no longer a remote possibility as recovering market conditions have allowed the company to return to profitability.

Ferronordic Machines used the downturn to become as efficient as possible and to pay down debt to a net cash position, so the preferred stock sits in a favorable position in Ferronordic’s capital structure. For the preferred shares to be worth their full 1,200 redemption value, Ferronordic Machines AB must be worth at least 3.4x trailing EBIT. This is a very low hurdle. At the current price, Ferronordic preferred shares offer a potential IRR of 15%+ from rising dividend payments alone, and substantially higher if the company can pull off an IPO at some point in the coming years.

The main risks to the value of Ferronordic Machines AB preferred stock are macroeconomic and political. The Russian economy is ever precarious, heavily exposed to fluctuations in commodities prices and the whims of an autocratic government. While Ferronordic cites gradually improving conditions, a return to recession would impact the company’s financial position and further delay an IPO.

Antwort auf Beitrag Nr.: 54.937.388 von R-BgO am 13.05.17 14:23:30

kommt mit auf den Friedhof der Übernahmen

Beitrag zu dieser Diskussion schreiben

Zu dieser Diskussion können keine Beiträge mehr verfasst werden, da der letzte Beitrag vor mehr als zwei Jahren verfasst wurde und die Diskussion daraufhin archiviert wurde.

Bitte wenden Sie sich an feedback@wallstreet-online.de und erfragen Sie die Reaktivierung der Diskussion oder starten Sie eine neue Diskussion.

Meistdiskutiert

| Wertpapier | Beiträge | |

|---|---|---|

| 168 | ||

| 122 | ||

| 77 | ||

| 69 | ||

| 68 | ||

| 37 | ||

| 37 | ||

| 32 | ||

| 30 | ||

| 29 |

| Wertpapier | Beiträge | |

|---|---|---|

| 29 | ||

| 28 | ||

| 27 | ||

| 25 | ||

| 24 | ||

| 23 | ||

| 22 | ||

| 19 | ||

| 19 | ||

| 18 |