`Avino Silver´(ASM.V) besser als `Mines Management´(MGN)? - 500 Beiträge pro Seite (Seite 2)

eröffnet am 22.12.04 21:46:10 von

neuester Beitrag 12.04.24 19:17:13 von

neuester Beitrag 12.04.24 19:17:13 von

Beiträge: 1.460

ID: 938.312

ID: 938.312

Aufrufe heute: 0

Gesamt: 133.224

Gesamt: 133.224

Aktive User: 0

ISIN: CA0539061030 · WKN: 862191 · Symbol: ASM

0,7401

USD

-1,84 %

-0,0139 USD

Letzter Kurs 01:54:33 NYSE Arca

Neuigkeiten

08.11.23 · Accesswire |

08.11.23 · Christoph Brüning Anzeige |

03.08.23 · Accesswire |

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7000 | +11,11 | |

| 1,4000 | +10,24 | |

| 37,18 | +10,00 | |

| 17,930 | +10,00 | |

| 6,7700 | +9,90 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,5900 | -8,09 | |

| 2,1800 | -9,17 | |

| 69,05 | -9,48 | |

| 154,95 | -9,76 | |

| 47,99 | -98,00 |

Antwort auf Beitrag Nr.: 43.043.883 von MONSIEURCB am 16.04.12 14:11:58Es läuft alles nach Plan! Denken wie ein Investor!

Spekulieren können andere! Avino macht seinen Weg!Viele Grüße!

Spekulieren können andere! Avino macht seinen Weg!Viele Grüße!

Der März und April sind und waren für den Silbermarkt einfach

zum kotzen. Das hatte ich so nicht erwartet!Die Stimmung ist

völlig am Boden!Und genau das ist es, was man von uns will!

Eines sollte man nicht tun, seine Überzeugung verlieren!

Ein Investor kauft ein, wenn die Masse den Mut verliert!

Also, nicht die Überzeugung verlieren und vergessen warum

sind wir im Silbermarkt! Weil Silber billig wie Dreck ist und

es so nicht bleiben wird!Das ist Fakt!Schönes Wochenende!

zum kotzen. Das hatte ich so nicht erwartet!Die Stimmung ist

völlig am Boden!Und genau das ist es, was man von uns will!

Eines sollte man nicht tun, seine Überzeugung verlieren!

Ein Investor kauft ein, wenn die Masse den Mut verliert!

Also, nicht die Überzeugung verlieren und vergessen warum

sind wir im Silbermarkt! Weil Silber billig wie Dreck ist und

es so nicht bleiben wird!Das ist Fakt!Schönes Wochenende!

Antwort auf Beitrag Nr.: 43.075.277 von MONSIEURCB am 23.04.12 14:10:09Mr. David Wolfin reports

AVINO SILVER & GOLD MINES LTD.: CLARIFICATION AND RETRACTION OF TECHNICAL DISCLOSURES

Avino Silver & Gold Mines Ltd., as a result of a review by the B.C. Securities Commission, has issued this news release to clarify and retract certain disclosures made pertaining to conceptual exploration targets and economic analyses of mineral resources at the company's Avino property in Durango, Mexico.

Certain disclosures relating to the Company's property provided in news releases, on the Company's website and in investor materials, do not comply with National Instrument 43-101 - Standards of Disclosure for Mineral Projects ("NI 43-101"). Also the March 12, 2012 independent NI 43-101 technical report and preliminary economic assessment ("Technical Report") on the tailings resources, prepared by an independent engineering firm, is not complete and contains items not compliant with NI 43-101. There are also compliance issues in Avino's news releases dated February 28, 2012, April 5, 2012 and April 23, 2012, and in its website materials relating to disclosure of the main Avino mine's resources. In addition, the website, fact sheet, and corporate presentation on the website disclosed results of economic analysis of an in-situ inferred resource estimate at San Gonzalo. The Company's technical report on file does not support this estimate and analysis. With respect to the Technical Report, the Company plans to file a restated report that clarifies the status of various in-situ and tailings resource estimates and the economic analysis, once received from the Independent Consultant.

The remainder is available to Stockwatch subscribers. Click the yellow link above for a free trial subscription.

jaja, so ist das, wenn man sich einen in die tasche lügt.

AVINO SILVER & GOLD MINES LTD.: CLARIFICATION AND RETRACTION OF TECHNICAL DISCLOSURES

Avino Silver & Gold Mines Ltd., as a result of a review by the B.C. Securities Commission, has issued this news release to clarify and retract certain disclosures made pertaining to conceptual exploration targets and economic analyses of mineral resources at the company's Avino property in Durango, Mexico.

Certain disclosures relating to the Company's property provided in news releases, on the Company's website and in investor materials, do not comply with National Instrument 43-101 - Standards of Disclosure for Mineral Projects ("NI 43-101"). Also the March 12, 2012 independent NI 43-101 technical report and preliminary economic assessment ("Technical Report") on the tailings resources, prepared by an independent engineering firm, is not complete and contains items not compliant with NI 43-101. There are also compliance issues in Avino's news releases dated February 28, 2012, April 5, 2012 and April 23, 2012, and in its website materials relating to disclosure of the main Avino mine's resources. In addition, the website, fact sheet, and corporate presentation on the website disclosed results of economic analysis of an in-situ inferred resource estimate at San Gonzalo. The Company's technical report on file does not support this estimate and analysis. With respect to the Technical Report, the Company plans to file a restated report that clarifies the status of various in-situ and tailings resource estimates and the economic analysis, once received from the Independent Consultant.

The remainder is available to Stockwatch subscribers. Click the yellow link above for a free trial subscription.

jaja, so ist das, wenn man sich einen in die tasche lügt.

Antwort auf Beitrag Nr.: 43.155.950 von heidiheidi am 12.05.12 01:55:17jaja, so ist das, wenn man sich einen in die tasche lügt.

Wie ist das gemeint?

Wie ist das gemeint?

Trading Spotlight

Dass Avino den Schwanz einziehen muss - hier im Original:

http://finance.yahoo.com/news/avino-silver-gold-mines-ltd-22…

http://finance.yahoo.com/news/avino-silver-gold-mines-ltd-22…

Antwort auf Beitrag Nr.: 43.156.504 von MONSIEURCB am 12.05.12 11:41:19

Avino Silver & Gold Mines Ltd

Symbol C : ASM

Shares Issued 27,071,416

Close 2012-05-11 C$ 1.52

Recent Sedar Documents

View Original Document

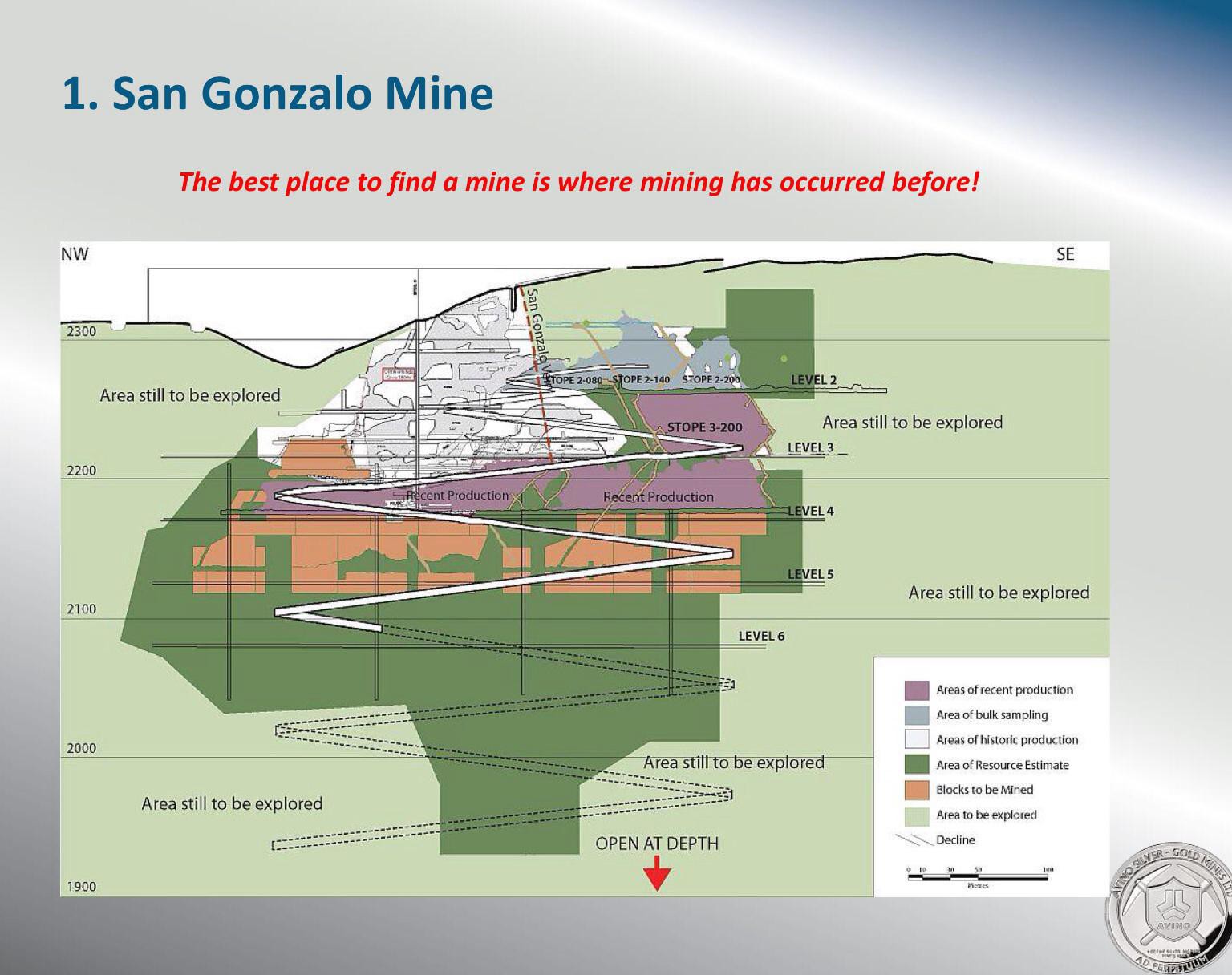

Avino samples 1.2 m of 607.5 g/t Ag at San Gonzalo

2012-05-14 06:49 ET - News Release

Mr. David Wolfin reports

AVINO UPDATES PROGRESS AT SAN GONZALO

Avino Silver & Gold Mines Ltd. has provided the following update on the progress made at its San Gonzalo mine located 82 kilometres northeast of Durango, Mexico.

The decline to the fourth level is nearly complete with only 79 m remaining until level four is reached. A 40 m cross cut will then be driven to access the San Gonzalo vein on the fourth level. Avino will then drift along the vein and collect channel samples. We expect to be in the vein on level 4 by July. Please see the map on Avino's website (http://www.avino.com/i/pdf/PlanoDeMuestreoN-3.pdf) for details.

On the third level, Avino has drifted 94.9 m to the North West and 124.89 m to the South East along the vein; sampling and assay results from along the vein are as follows.

Vein

Strike Average Individual

Length Width Sample Gold Silver Lead Zinc Copper

Area (m) (m) Width (g/t) (g/t) (%) (%) (%)

North

West

of

Cross

Cut 4.33 2.7 0.953 289 0.08 0.23 0.02

Including:

L-60W 1.4 0.990 411.3 0.1043 0.2678 0.0252

L-62W 0.55 1.234 451.4 0.0989 0.2715 0.0425

0.65 0.680 305.3 0.0624 0.4376 0.0471

0.8 0.959 225.3 0.0319 0.2154 0.0148

0.35 0.696 382.3 0. 0556 0.3821 0.0235

13.28 2.77 0.704 146 0.34 0.4 0.03

Including:

L-51W 0.5 1.278 319.9 3.82 3.63 0.147

L-54W 1 2.616 528.7 0.1952 0.2605 0.0446

L-55W 1.2 1.676 607.5 0.318 0.6036 0.0396

L-57W 1.2 2.459 246 0.0549 0.1933 0.0212

L-58W 1.25 0.798 359.9 0.153 0.2937 0.0399

7.5 1.53 0.13 34 0.12 0.6100 0.03

9.01 2.3 0.75 213 0.19 1.15 0.05

Including: 0.9 1.005 225.4 0.2816 3.18 0.0263

L-41W 0.65 1.353 653.2 0.3813 1.54 0.049

L-44W 0.7 1.079 663.8 0.243 0.9504 0.0729

L-45W 0.4 1.015 749.7 0.1511 0.4027 0.0586

15.33 2.02 0.376 42 0.12 0.31 0.02

15.68 2.2 0.508 126 0.027 0.07 0.003

Including:

L-20W 0.55 0.695 339.9 0.1592 0.03491 0.0617

L-22W 0.50 2.955 2684.7 0.4313 0.4481 0.0349

L-24W 0.50 2.507 571.4 0.2481 0.5343 0.0541

L-27W 0.4 1.577 1377 0.2796 1.07 0.047

4.81 1.73 0.139 51 0.007 0.025 0.007

Including:

L-16W 0.50 1.317 706 0.2344 0.34 0.0729

7.97 1.69 0.45 203 0.2426 0.3246 1.469

Including:

L-12W 0.50 1.099 1025.6 0.193 0.2334 0.0765

16.99 1.23 0.37 58 0.3235 0.4224 1.38

Including:

L-6W 0.30 3.074 395.3 3.3 0.5167 2.14

L-7W 0.50 2.451 229.7 0.2991 0.1684 0.9984

94.9 1.99

South

East

of

Cross

Cut 15.08 1.6 0.513 90 0.089 0.38 0.091

Including: 0.9 1.589 215 0.0618 0.2054 0.0166

L-6E 0.9 2.699 445 0.00896 0.2016 0.0135

19.03 2.01 1.06 277 0.829 1.021 0.058

Including:

L-12E 0.7 1.759 4358.8 1.83 1.54 0.1304

L-14E 1.2 1.275 322 0.1359 0.5529 0.025

0.8 3.538 460 0.1884 0.605 0.0479

L-17E 0.4 6.037 219 6.02 12.27 0.3053

0.4 0.872 602 0.4677 0.746 0.0505

L-20E 0.8 1.944 689 0.2844 0.7389 0.1288

L-21E 0.5 2.909 1756.9 0.4395 0.9622 0.1015

L-23E 0.4 3.365 2453.8 0.4767 1.06 0.1171

8.21 1.85 0.21 34 0.253 0.68 0.011

23.14 2.75 0.916 431 0.276 0.657 0.026

Including:

L-31E 0.7 0.908 527 0.1778 0.7445 0.0157

L-32E 0.95 2.061 1233 0.2243 0.6851 0.0394

L-33E 0.65 1.053 603 0.1741 0.591 0.0309

0.55 2.606 2719.3 1.26 1.59 0.1296

L-34E 0.95 2.889 1635 0.7876 1.28 0.041

L-38E 0.6 1.555 1492 0.2565 0.6088 0.0414

L-39E 0.7 0.603 303 0.0975 0.1529 0.0203

1.1 2.29 1770.7 0.2642 0.2195 0.0424

L-41E 1 1.032 589 0.0806 0.165 0.0204

0.2 0.366 676 0.1782 0.4123 0.0281

L-42E 0.6 1.427 1402 0.1562 0.2879 0.0487

0.8 2.111 1851.4 0.7683 0.9447 0.0525

0.9 2.556 1117 0.3795 0.2116 0.0449

0.4 1.923 4894.7 1.2900 0.2659 0.1001

L-43E 1.1 1.347 884 0.1547 0.372 0.0278

0.65 6.397 5348.4 2.53 1.94 0.1204

6 1.96 0.244 72 0.66 0.316 0.036

5.79 1.77 0.169 44 0.083 0.584 0.013

77.25 2.11

Avino Silver & Gold Mines Ltd

Symbol C : ASM

Shares Issued 27,071,416

Close 2012-05-11 C$ 1.52

Recent Sedar Documents

View Original Document

Avino samples 1.2 m of 607.5 g/t Ag at San Gonzalo

2012-05-14 06:49 ET - News Release

Mr. David Wolfin reports

AVINO UPDATES PROGRESS AT SAN GONZALO

Avino Silver & Gold Mines Ltd. has provided the following update on the progress made at its San Gonzalo mine located 82 kilometres northeast of Durango, Mexico.

The decline to the fourth level is nearly complete with only 79 m remaining until level four is reached. A 40 m cross cut will then be driven to access the San Gonzalo vein on the fourth level. Avino will then drift along the vein and collect channel samples. We expect to be in the vein on level 4 by July. Please see the map on Avino's website (http://www.avino.com/i/pdf/PlanoDeMuestreoN-3.pdf) for details.

On the third level, Avino has drifted 94.9 m to the North West and 124.89 m to the South East along the vein; sampling and assay results from along the vein are as follows.

Vein

Strike Average Individual

Length Width Sample Gold Silver Lead Zinc Copper

Area (m) (m) Width (g/t) (g/t) (%) (%) (%)

North

West

of

Cross

Cut 4.33 2.7 0.953 289 0.08 0.23 0.02

Including:

L-60W 1.4 0.990 411.3 0.1043 0.2678 0.0252

L-62W 0.55 1.234 451.4 0.0989 0.2715 0.0425

0.65 0.680 305.3 0.0624 0.4376 0.0471

0.8 0.959 225.3 0.0319 0.2154 0.0148

0.35 0.696 382.3 0. 0556 0.3821 0.0235

13.28 2.77 0.704 146 0.34 0.4 0.03

Including:

L-51W 0.5 1.278 319.9 3.82 3.63 0.147

L-54W 1 2.616 528.7 0.1952 0.2605 0.0446

L-55W 1.2 1.676 607.5 0.318 0.6036 0.0396

L-57W 1.2 2.459 246 0.0549 0.1933 0.0212

L-58W 1.25 0.798 359.9 0.153 0.2937 0.0399

7.5 1.53 0.13 34 0.12 0.6100 0.03

9.01 2.3 0.75 213 0.19 1.15 0.05

Including: 0.9 1.005 225.4 0.2816 3.18 0.0263

L-41W 0.65 1.353 653.2 0.3813 1.54 0.049

L-44W 0.7 1.079 663.8 0.243 0.9504 0.0729

L-45W 0.4 1.015 749.7 0.1511 0.4027 0.0586

15.33 2.02 0.376 42 0.12 0.31 0.02

15.68 2.2 0.508 126 0.027 0.07 0.003

Including:

L-20W 0.55 0.695 339.9 0.1592 0.03491 0.0617

L-22W 0.50 2.955 2684.7 0.4313 0.4481 0.0349

L-24W 0.50 2.507 571.4 0.2481 0.5343 0.0541

L-27W 0.4 1.577 1377 0.2796 1.07 0.047

4.81 1.73 0.139 51 0.007 0.025 0.007

Including:

L-16W 0.50 1.317 706 0.2344 0.34 0.0729

7.97 1.69 0.45 203 0.2426 0.3246 1.469

Including:

L-12W 0.50 1.099 1025.6 0.193 0.2334 0.0765

16.99 1.23 0.37 58 0.3235 0.4224 1.38

Including:

L-6W 0.30 3.074 395.3 3.3 0.5167 2.14

L-7W 0.50 2.451 229.7 0.2991 0.1684 0.9984

94.9 1.99

South

East

of

Cross

Cut 15.08 1.6 0.513 90 0.089 0.38 0.091

Including: 0.9 1.589 215 0.0618 0.2054 0.0166

L-6E 0.9 2.699 445 0.00896 0.2016 0.0135

19.03 2.01 1.06 277 0.829 1.021 0.058

Including:

L-12E 0.7 1.759 4358.8 1.83 1.54 0.1304

L-14E 1.2 1.275 322 0.1359 0.5529 0.025

0.8 3.538 460 0.1884 0.605 0.0479

L-17E 0.4 6.037 219 6.02 12.27 0.3053

0.4 0.872 602 0.4677 0.746 0.0505

L-20E 0.8 1.944 689 0.2844 0.7389 0.1288

L-21E 0.5 2.909 1756.9 0.4395 0.9622 0.1015

L-23E 0.4 3.365 2453.8 0.4767 1.06 0.1171

8.21 1.85 0.21 34 0.253 0.68 0.011

23.14 2.75 0.916 431 0.276 0.657 0.026

Including:

L-31E 0.7 0.908 527 0.1778 0.7445 0.0157

L-32E 0.95 2.061 1233 0.2243 0.6851 0.0394

L-33E 0.65 1.053 603 0.1741 0.591 0.0309

0.55 2.606 2719.3 1.26 1.59 0.1296

L-34E 0.95 2.889 1635 0.7876 1.28 0.041

L-38E 0.6 1.555 1492 0.2565 0.6088 0.0414

L-39E 0.7 0.603 303 0.0975 0.1529 0.0203

1.1 2.29 1770.7 0.2642 0.2195 0.0424

L-41E 1 1.032 589 0.0806 0.165 0.0204

0.2 0.366 676 0.1782 0.4123 0.0281

L-42E 0.6 1.427 1402 0.1562 0.2879 0.0487

0.8 2.111 1851.4 0.7683 0.9447 0.0525

0.9 2.556 1117 0.3795 0.2116 0.0449

0.4 1.923 4894.7 1.2900 0.2659 0.1001

L-43E 1.1 1.347 884 0.1547 0.372 0.0278

0.65 6.397 5348.4 2.53 1.94 0.1204

6 1.96 0.244 72 0.66 0.316 0.036

5.79 1.77 0.169 44 0.083 0.584 0.013

77.25 2.11

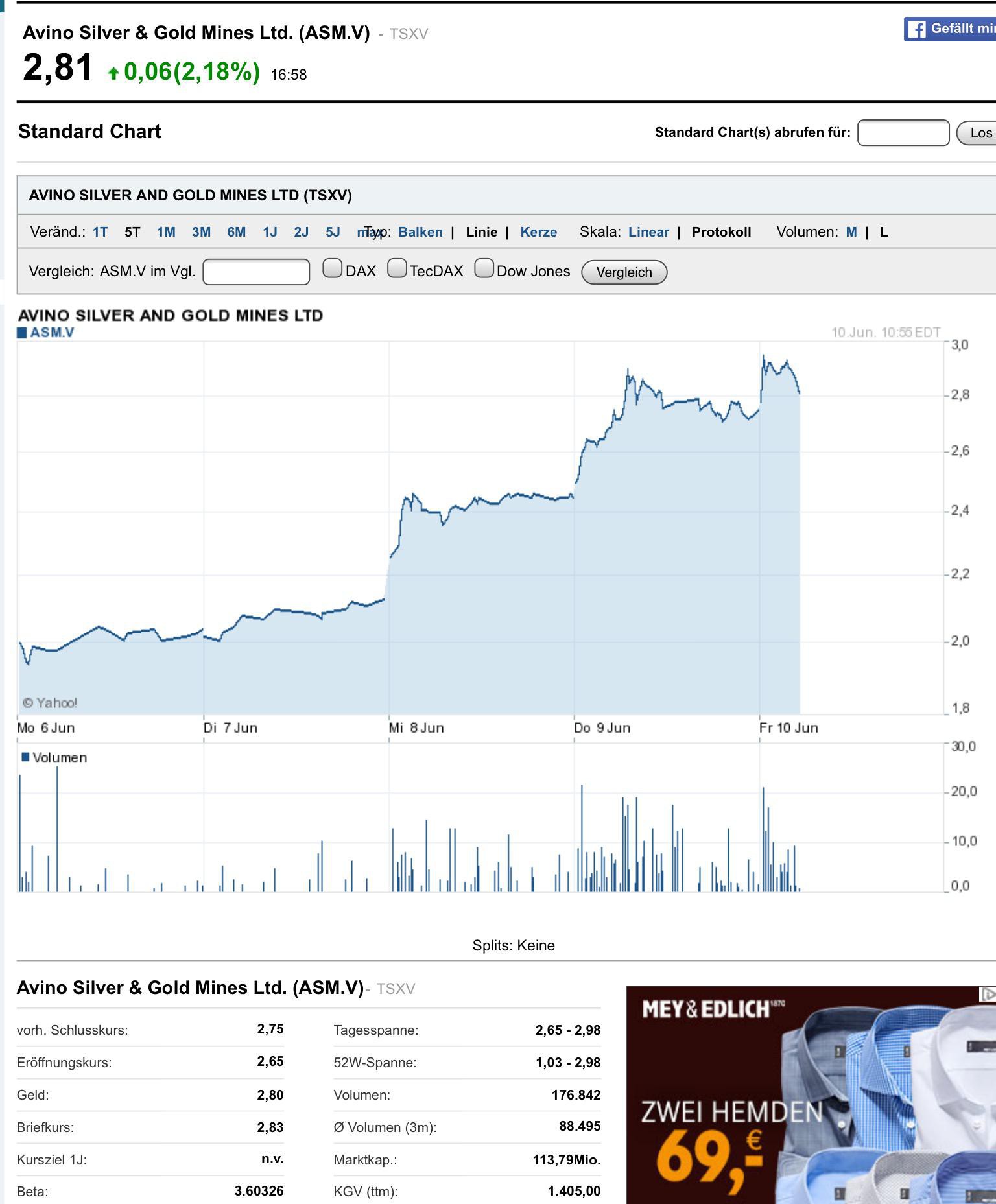

Antwort auf Beitrag Nr.: 43.162.306 von heidiheidi am 14.05.12 15:24:05Oha innerhalb der letzten 2 Monate hat sich der Kurs quasi halbiert

und kein Haltepunkt in Sicht. Ein Trost Avino ist nicht die einzige

Aktie, die total verprügelt wurde...und weiter verprügelt wird ???

und kein Haltepunkt in Sicht. Ein Trost Avino ist nicht die einzige

Aktie, die total verprügelt wurde...und weiter verprügelt wird ???

Hat jemand eine Ahnung, wie lange diese Kursaussetzung noch dauert? Auf der Homepage und im Web ist nichts dazu zu finden ... für den weiteren Kursverlauf ist jeder Tag länger sicher negativ ...

News zur Situation:

http://finance.yahoo.com/news/avino-silver-gold-mines-ltd-19…

...und:

FEATURES

Market Coverage

Market Overview

Market Update

In Play®

Story Stocks

Short Stories

Tech Stocks

Market Events

Earnings Calendar

Economic Calendar

Splits Calendar

Conference Call Calendar

IPO Calendar

Upgrades/Downgrades

Market Statistics

Market Digest

U.S. Market Indices

World Market Indices

Currency Exchange Rates

InPlay

5:34PM CubeSmart has been retained by American Storage to manage 31 self-storage facilities (CUBE) 12.11 -0.05 : CubeSmart will assume management of the portfolio effective August 1, 2012. The facilities will continue to operate under the name American Storage.

5:31PM Alexza Pharma announces submission of responses to the EMA Day 120 List of Questions for the ADASUVE MAA (ALXA) 3.52 -0.06 : Co announced that it has submitted its responses regarding the ADASUVE Marketing Authorization Application (MAA) to the European Medicines Agency (EMA). In March 2012, Alexza received the Committee for Medicinal Products for Human Use Consolidated List of Questions (Day 120 List of Questions) regarding Alexza's ADASUVE MAA. In May 2012, Alexza and its European corporate partner, Grupo Ferrer, met with the Rapporteur, Co-Rapporteur and EMA to further understand specifics of the major objections raised in the Day 120 List of Questions. The submitted responses are intended to address the questions outlined in the Day 120 List of Questions. According to the published EMA timetables, Alexza expects to receive the Day 180 List of Outstanding Issues for the ADASUVE MAA in late September 2012. Alexza also announced today that it has completed the follow-up from the May 2012 EU Pre-Approval Inspection (PAI). This inspection resulted in no findings the EMA classified as Critical or Major deficiencies. The EU PAI resulted in 12 findings classified as Other and 4 recommendations. The EMA has accepted Alexza's final corrective action plan, and proposed timing for the action plan completion and reporting. Alexza expects to receive its EU Good Manufacturing Practices (GMP) Certificate for its Mountain View, California facility as a result of this outcome.

5:27PM DDR announces redemption of 7.5% Class I cumulative redeemable preferred shares (DDR) 14.95 -0.04 : Co announced that it is calling for redemption all outstanding shares of its 7.50% Class I Cumulative Redeemable Preferred Shares, without par value, and the related depositary shares, each representing 1/20th of one share of the Class I Preferred Shares. The Class I Preferred Shares and respective Depositary Shares will be redeemed in whole at a redemption price of $503.75 per Class I Preferred Share or $25.1875 per Depositary Share (the sum of $500.00 per Class I Preferred Share plus accrued and unpaid dividends of $3.75 per Class I Preferred Share to the redemption date or $25.00 per Depositary Share plus accrued and unpaid dividends of $0.1875 per Depositary Share to the redemption date).

5:25PM HNI reports EPS in-line, beats on revs; guides Q3 EPS above consensus, revs above consensus; guides FY12 EPS above consensus (HNI) 27.22 +0.44 : Reports Q2 (Jun) earnings of $0.17 per share, excluding non-recurring items, in-line with the Capital IQ Consensus Estimate consensus of $0.17; revenues rose 11.0% year/year to $480.4 mln vs the $473.04 mln consensus. Co issues upside guidance for Q3, sees EPS of $0.65-0.70, excluding non-recurring items, vs. $0.65 Capital IQ Consensus Estimate; sees Q3 revenue growth of 11-14% (~$559.7-574.8 mln) vs. $555.82 mln Capital IQ Consensus Estimate. Co issues upside guidance for FY12, sees EPS of $1.35-1.45, excluding non-recurring items, vs. $1.34 Capital IQ Consensus Estimate.

5:23PM DDR announces pricing of $200 mln 6.5% cumulative redeemable preferred stock (DDR) 14.95 -0.04 : Co announced that it has priced an underwritten public offering of 8,000,000 depositary shares, each representing a 1/20 fractional interest in a share of its newly designated 6.50% Class J Cumulative Redeemable Preferred Shares at a price of $25.00 per depositary share.

5:06PM IBM conference call summary (call is currently in Q&A) (IBM) 188.20 +4.60 :

Mgmt noted that deadwinds included currency fluctuations and volatility for translation and hedging dynamics. Total operating expense and other income was down 6%. Co is dealing with significant currency dynamics which impacted its revenue lines by ~ $1 bln, or almost 4 points.

Co had $150 mln of workforce balancing in the quarter primarily in Europe.

Co should see ongoing benefits to the GTS portfolio.

GBS returned to a more typical level of profitability.

Co saw strength in Russia and China. China was up over 20% this quarter, gaining share again. Co is continuing to build its capabilities there. They expanded the number of branch offices and now have 68 face-to-face and over 100 virtual branch offices open across all of China.

Europe saw mixed performance as Italy and France were down.

5:06PM J.M. Smucker increases dividend 8.3% to $0.52 from $0.48 per share (SJM) 75.96 -0.02 :

5:04PM Crown Hldgs reports EPS in-line, misses on revs (CCK) 34.20 +0.11 : Reports Q2 (Jun) earnings of $0.84 per share, excluding non-recurring items, in-line with the Capital IQ Consensus Estimate consensus of $0.84; revenues fell 4.3% year/year to $2.18 bln vs the $2.28 bln consensus. "In the Americas and Asia we continued to perform well. Importantly, the results demonstrate the benefit of our product and geographic diversity. Globally, beverage can volumes grew 5%, driven by our emerging market capacity expansion program over the last few years."

5:03PM Noble Corp beats by $0.01, reports revs in-line (NE) 35.40 +0.90 : Reports Q2 (Jun) earnings of $0.59 per share, excluding a non-recurring after tax gain of $0.04, $0.01 better than the Capital IQ Consensus Estimate of $0.58; revenues rose 43.1% year/year to $898.9 mln vs the $897.1 mln consensus. Contract drilling services revenues for Q2 of 2012 were $848 million versus $746 million for Q1 of 2012, an increase of ~14%. For Q2 of 2011, contract drilling services revenues totaled $590 million.

4:46PM Astoria Fincl reports EPS in-line (AF) 9.99 -0.09 : Reports Q2 (Jun) earnings of $0.13 per share, in-line with the Capital IQ Consensus Estimate consensus of $0.13. "I am pleased to report continued growth in both the loan portfolio and balance sheet this quarter, fueled by an increase in the multi-family loan portfolio. In addition, the results of the cost control initiatives undertaken in the first quarter have produced a significant reduction in operating expenses this quarter. I am also pleased with the positive progression in our asset/liability repositioning. Multi-family/commercial real estate loans increased 21% from December 31, 2011, while residential loans remained relatively stable, and low-cost core deposits increased 8%, while high-cost CDs decreased 18%. We expect that together, the growth and repositioning of the balance sheet coupled with improved operating efficiency should benefit the net interest margin and improve profitability throughout the remainder of the year."

4:38PM Financial Stability Oversight Council- designates 8 banks as Systemically important; will face new supervision but that has yet to be determined; Fed Reserve will decide these banks can access borrowing windows (XLF) : Says concerns about growth in emerging markets a concern. Says housing has been a drag on recovery.

4:37PM SLM Corp beats by $0.05 on a GAAP basis (SLM) 16.04 -0.13 : Reports Q2 (Jun) GAAP earnings of $0.59 per share, $0.05 better than the GAAP Capital IQ Consensus Estimate of $0.54; net interest income fell 14.1% year/year to $746 mln, may not compare to the $706.2 mln consensus. Core earnings were $0.49 vs. $0.48 last yr. "We continue to grow our private credit business and find productivity gains in challenging economic conditions. "We head into this academic year with loan products that promote and reward in-school payments. The performance of these loans over recent years foreshadows better credit ratings for our customers and lower defaults for Sallie Mae."

4:34PM Skyworks beats by $0.01, beats on revs; guides Q4 EPS in-line, revs in-line (SWKS) 28.65 +1.12 : Reports Q3 (Jun) earnings of $0.45 per share, excluding non-recurring items, $0.01 better than the Capital IQ Consensus Estimate of $0.44; revenues rose 9.2% year/year to $389 mln vs the $383.02 mln consensus. Co issues in-line guidance for Q4, sees EPS of 0.50-0.51, excluding non-recurring items, vs. $0.51 Capital IQ Consensus Estimate; sees Q4 revs of 415-420 mln vs. $418.03 mln Capital IQ Consensus Estimate. "Our strategic diversification across OEMs and chipset partners is enabling us to produce consistently strong operating results despite the macro economy. Specifically, we are gaining share within adjacent vertical markets including automotive, medical, avionics, military, location services and broadband communications. At the same time, our innovative solutions are powering the world's most popular smartphones, tablets, home automation platforms and network infrastructure systems. In short, we have created a differentiated business model that is delivering demonstrable, best in class mobile internet growth with analog semiconductor shareholder returns."

4:34PM Diana Containerships announces proposed public offering of 8.1 mln shares of common stock (DCIX) 7.20 -0.05 : The net proceeds of the offering are expected to be used by the co for general corporate purposes, including vessel acquisitions and working capital, although no specific vessels have been identified by the Company for acquisition at this time. Wells Fargo Securities, BofA Merrill Lynch and UBS Investment Bank are acting as joint-book runners of the offering. Barclays and RBC Capital Markets are acting as co-managers.

4:33PM Cohen & Steers misses by $0.05, beats on revs (CNS) 36.49 -1.16 : Reports Q2 (Jun) earnings of $0.36 per share, $0.05 worse than the Capital IQ Consensus Estimate of $0.41; revenues rose 9.6% year/year to $67.4 mln vs the $66.63 mln consensus. Assets under management were $44.4 billion as of June 30, 2012, a decrease of 1.1% from $44.9 billion at March 31, 2012 and an increase of 0.2% from $44.3 billion at June 30, 2011.

4:32PM East West Banc beats by $0.02; guides Q4 (Dec) EPS in-line; guides FY12 EPS above consensus (EWBC) 23.74 -0.22 : Reports Q2 (Jun) earnings of $0.47 per share, $0.02 better than the Capital IQ Consensus Estimate of $0.45. Co issues in-line guidance for Q4 (Dec), sees EPS of $0.45-0.47 vs. $0.47 Capital IQ Consensus Estimate. Co issues upside guidance for FY12, sees EPS of $1.84-1.86 vs. $1.84 Capital IQ Consensus Estimate.

The Company is providing guidance for the third quarter and full year of 2012. Management currently estimates that fully diluted earnings per share for the full year of 2012 will range from $1.84 to $1.86, an increase of 15% to 16% from the full year of 2011. Also, this updated guidance for the full year of 2012 is an increase of approximately $0.05 per dilutive share from our previously released guidance. Management currently estimates that fully diluted earnings per share for the third quarter of 2012 will range from $0.45 to $0.47 per dilutive share.

This EPS guidance for the third quarter of 2012 is based on the following assumptions:

-- Stable balance sheet- A stable interest rate environment and an adjusted net interest margin of approximately 4.00%.

-- Provision for loan losses of approximately $12 to $15 million for the quarter

-- Total noninterest expense of approximately $100 million for the quarter, net of amounts to be reimbursed by the FDIC Effective tax rate of approximately 35%

4:31PM Spectra Energy LP increases quarterly cash distribution 1.0% to $0.485 per unit (SEP) 32.35 +0.18 :

4:31PM Peoples Fed Bancshares Inc announces an initial $0.03 dividend payment to stockholders (PEOP) 16.70 +0.04 : Co announced that its Board of Directors has declared a quarterly cash dividend of $0.03 per share on the Company's common stock. The dividend will be payable to stockholders of record as of August 7, 2012, and will be paid on August 17, 2012.

4:31PM State Auto Fin reports estimate of second quarter storm activity impact (STFC) 14.63 -0.13 : Co announces its preliminary estimate of the impact of catastrophe losses on its second quarter results. The company estimates second quarter 2012 results will include between $33 million and $36 million in pre-tax net catastrophe losses. During the quarter ended June 30, 2012, 13 catastrophe events in the United States were identified by Property Claim Service. STFC's catastrophe losses were primarily related to two events: wind and hail activity affecting the Louisville, Ky., and St. Louis, Mo., areas in late April and, to a lesser extent, wind activity from a storm event in the Midwest and Mid-Atlantic states at the end of June.

4:31PM LaCrosse Footwear receives $29 mln order for the United States Marine Corps (BOOT) 19.94 -0.01 : Co announced that it has received a new $29 million delivery order for the United States Marine Corps for Danner's USMC Rugged All-Terrain (RAT) Hot weather and Temperate boots. The Company anticipates fulfilling this order in multiple deliveries over the next several quarters.

4:25PM YUM! Brands misses by $0.03, beats on revs; reaffirms FY12 EPS guidance (YUM) 65.55 +1.14 : Reports Q2 (Jun) earnings of $0.67 per share, $0.03 worse than the Capital IQ Consensus Estimate of $0.70; revenues rose 12.5% year/year to $3.17 bln vs the $3.11 bln consensus. Worldwide restaurant margin declined 0.6 percentage points to 15.2%, including declines of 4.1 percentage points in China and 1.1 percentage points at YRI. Restaurant margin increased 5.8 percentage points in the U.S... Same-store sales grew 10% in China, 4% at YRI and 7% in the U.S.

Co reaffirms guidance for FY12, sees EPS of at least $3.22 vs. $3.31 Capital IQ Consensus Estimate. The Company also raises new-unit forecast to a record 1,700 new international units for the year, including at least 700 new units in China.

"Yum! China, our largest profit-contributing division, reported strong system sales growth of 27%, prior to foreign currency translation. However, operating profit declined 4%, prior to foreign currency translation, as high inflation drove restaurant margins down 4 percentage points versus last year. We expect this to be short-lived, returning to double-digit profit growth in the second half of the year. Our outstanding China team now expects to open a record of at least 700 new units this year."

4:24PM Xilinx beats by $0.02, beats on revs; guides Q2 revs below consensus (XLNX) 32.01 +1.12 : Reports Q1 (Jun) earnings of $0.47 per share, $0.02 better than the Capital IQ Consensus Estimate of $0.45; revenues fell 5.3% year/year to $582.8 mln vs the $574.03 mln consensus. Co says sales for Q2 are expected to be down 4% to 8% sequentially, this calculates to ~$536.17 -559.48 vs. $587.33 mln Capital IQ Consensus Estimate. Co also says Q2 gross margin is expected to be approximately 66%. Operating expenses are expected to be approximately $220 million, including $2 million of amortization of acquisition-related intangibles. Other income and expense is expected to be an expense of approximately $8 million. Fully diluted share count is expected to be approximately 274 million. September quarter tax rate is expected to be approximately 16%.

4:23PM Anthera Pharma announces proposed public offering of common stock, size not disclosed (ANTH) 1.33 -0.27 : Co intends to use the net proceeds from the offering for general corporate purposes. Piper Jaffray & Co. and Leerink Swann LLC are acting as joint book-running managers in the offering.

4:22PM eBay beats by $0.01, beats on revs; guides Q3 EPS in-line, revs just below consensus; reaffirms FY12 EPS, revs guidance (EBAY) 40.46 +1.39 : Reports Q2 (Jun) earnings of $0.56 per share, excluding non-recurring items, $0.01 better than the Capital IQ Consensus Estimate of $0.55; revenues rose 23.1% year/year to $3.4 bln vs the $3.36 bln consensus. Co issues guidance for Q3, sees EPS of $0.53-0.55, excluding non-recurring items, vs. $0.55 Capital IQ Consensus Estimate; sees Q3 revs of $3.3-3.4 bln vs. $3.41 bln Capital IQ Consensus Estimate. Co reaffirms guidance for FY12, sees EPS of $2.30-2.35, excluding non-recurring items, vs. $2.35 Capital IQ Consensus Estimate; sees FY12 revs of $13.8-14.1 bln vs. $14 bln Capital IQ Consensus Estimate. Q2 non-GAAP op margin of 27.3% vs 26.9% last qtr and 27.6% year ago; Q2 active users of 104.8 mln vs 102.4 mln last qtr. PayPal ended the quarter with 113.2 million active registered accounts, a 13% increase over the second quarter of 2011. PayPal revenue increased 26% year over year, driven primarily by increased penetration on eBay as well as continued merchant and consumer adoption and strong growth in Bill Me Later. "Our entire company is strong, but we're particularly pleased with eBay Marketplaces, which delivered its strongest organic growth in gross merchandise volume, excluding vehicles, since 2006. And mobile continues to be a game changer. We now expect eBay and PayPal mobile to each transact $10 billion in volume in 2012 -- that's more than double 2011, a staggering surge in mobile shopping and payments on devices that did not exist just a few years ago. Retail is at an inflection point, and we are helping to reshape how people around the world shop and pay."

4:21PM Werner Enterprises reports EPS in-line, misses on revs (WERN) 23.46 +0.48 : Reports Q2 (Jun) earnings of $0.42 per share, in-line with the Capital IQ Consensus Estimate consensus of $0.42; revenues rose 1.1% year/year to $521.8 mln vs the $537.38 mln consensus. Second quarter 2012 freight demand demonstrated typical seasonal trends and improved into June similar to second quarter 2011. Freight demand to date in July 2012 continues to show typical seasonal trends similar to July 2011. Freight demand trends are being helped both by supply side constraints limiting truckload capacity and demand generated by economic activity from our customers.

4:18PM Titan Intl disclosure requirements for potential offer (TWI) 21.09 -1.26 : Co wishes to draw to the attention of its shareholders certain disclosure requirements applicable to the possible offer by Titan International for Titan Europe Plc which was announced on 17 July 2012. Titan International, Inc.'s common stock is admitted to trading on the New York Stock Exchange. The above requirements are set out in Rule 8 of the UK City Code on Takeovers and Mergers which is published and administered by the Takeover Panel. In particular Rule 8.3 requires that any person who is interested (directly or indirectly) in 1% or more of any class of relevant securities of any party to the offer must make (a) an Opening Position Disclosure and (b) a Dealing Disclosure if he deals in any relevant securities of any party to the offer during an offer period. The Titan International, Inc. shares are relevant securities for the purposes of the possible offer.

4:16PM The Hanover Insurance Grp announced the estimated impact of catastrophe-related activity on Q2 results in domestic business to be in the range of $70 to $77 million before taxes, or $1.00 to $1.10 after tax per share. (THG) 38.87 +0.47 : Catastrophe losses during the quarter were primarily related to severe hail and wind storms from 11 events in the U.S. The largest losses were caused by hailstorms in the Midwest in April and a series of widespread hail and windstorm events in the Midwest and Mid-Atlantic regions in May and June. Second quarter results are also expected to be impacted by additions to reserves in certain domestic lines, primarily in surety and auto. Surety reserve additions are driven by continuing weak economic conditions, while auto reserve re-estimations primarily reflect an increase in severity of losses from the 2011 accident year. Taking this into account, as well as other currently available information, The Hanover expects second quarter segment income after tax per share to be in the range of $0.15 to $0.25.

4:16PM Stryker misses by $0.01, reports revs in-line; guides FY12 revs in-line; project's 2012 adjusted EPS to grow at double-digits YoY (SYK) 53.57 -0.15 : Reports Q2 (Jun) earnings of $0.98 per share, excluding non-recurring items, $0.01 worse than the Capital IQ Consensus Estimate of $0.99; revenues rose 2.9% year/year to $2.11 bln vs the $2.13 bln consensus. Co issues in-line guidance for FY12, sees FY12 revs of $8.47-8.72 bln vs. $8.69 bln Capital IQ Consensus Estimate. Co project's 2012 adjusted diluted net EPS to grow at double-digit levels over 2011.

4:16PM Thor Industries announces Bob Martin will become its President and Chief Operating Officer effective August 1, 2012 (THO) 28.93 +0.11 : Martin currently serves as RV Senior Group President.

4:15PM Transocean provides fleet status report: backlog associated with new contracts or extensions is ~$1.5 bln and 2012 estimated out of service time increased by a net 16 days (RIG) 47.02 +0.65 : Co issued a comprehensive Fleet Status Report which provides current status and contract information for the co's entire fleet of offshore drilling rigs. Since the June update, backlog associated with new contracts or extensions is ~$1.5 bln and 2012 estimated out of service time increased by a net 16 days.

Highlights are as follows: Discoverer Deep Seas - Awarded a three-year contract for work in the U.S. Gulf of Mexico at a dayrate of $595,000 ($652 mln contract backlog). The rig's prior contract dayrate was $450,000. GSF Arctic III - Awarded a 17-well contract for work in the U.K. sector of the North Sea at a dayrate of $313,000 ($205 mln contract backlog), consistent with the rig's recently-signed, three-month prior contract. GSF Jack Ryan - Customer exercised a one-year option for work offshore Nigeria at a dayrate of $425,000 ($155 mln contract backlog). Transocean Marianas - Awarded a 280-day contract for work offshore Namibia at a dayrate of $530,000 ($148 mln contract backlog). The rig's prior dayrate was $450,000. Transocean Searcher - Customer exercised a one-year option in the Norway North Sea at a dayrate of $386,000 ($141 mln contract backlog). Trident 15 - Awarded a two-year contract extension for work offshore Thailand at a dayrate of $139,000 ($101 mln contract backlog). The rig's prior dayrate was $100,000. GSF Rig 103 is currently held for sale. The rig was previously stacked.

This report also contains the co's initial forecast of planned 2013 out of service time. The estimated 2,657 days (impacting 50 rigs) comprises 824 days (31%) for High-Specification Floaters, 872 days (33%) for Midwater Floaters, and 961 days (36%) for Jackups. This compares with estimated 2012 out of service time of 3,931 days (impacting 58 rigs) consisting of 1,212 days (31%) for High-Specification Floaters, 717 days (18%) for Midwater Floaters, and 2,002 days (51%) for Jackups. Included in the 2013 forecast, the company anticipates performing extensive well control equipment work scope on 12 floaters.

4:13PM Pioneer Natural Resources provides production and financial update for second quarter of 2012: production from continuing operations averaged 150,506 barrels oil equivalent per day (PXD) 89.90 +1.54 : Co's production from continuing operations averaged 150,506 barrels oil equivalent per day in the second quarter of 2012. The Company's production guidance for the quarter was 149 thousand barrels oil equivalent per day to 154 MBOEPD. Production from the Spraberry field in West Texas was negatively impacted by ~4,800 BOEPD due to unplanned third-party natural gas liquids fractionation downtime and tight industry NGL fractionation capacity at Mont Belvieu, Texas as described below. Had these third-party processing issues not occurred during the second quarter and all of Pioneer's NGL volumes could have been fractionated and sold, Pioneer's production would have been above the top of the guidance range at ~155 MBOEPD. Pioneer has a strong financial position and is committed to maintaining this position. In June and July 2012, Pioneer liquidated swap, collar and three-way collar derivatives for 250,000 million British thermal units per day of 2014 gas production and 80,000 MMBTUPD of 2015 gas production.

4:12PM Pioneer Southwest Energy reports production averaged 7,103 barrels oil equivalent per day in the second quarter of 2012 (PSE) 26.26 +0.13 : Production from the Spraberry field in West Texas was negatively impacted by ~530 BOEPD due to unplanned third-party natural gas liquids fractionation downtime and tight industry NGL fractionation capacity at Mont Belvieu, Texas, as described below. Had these third-party processing issues not occurred during the second quarter and all of Pioneer Southwest's NGL volumes could have been fractionated and sold, the Partnership's production would have been ~7,630 BOEPD. In the second quarter of 2012, Pioneer Southwest's oil sales averaged 4,874 barrels per day (BPD), NGL sales averaged 1,164 BPD and gas sales averaged 6 mln cubic feet per day. In the second quarter, the NYMEX West Texas Intermediate (WTI) oil price averaged $93.49 per barrel. Pioneer Southwest's second quarter oil average realized price per barrel before derivative transactions was $86.25 per barrel.

4:12PM El Paso Pipeline Partners increases quarterly distribution 15% to $0.55 per unit (EPB) 35.24 -0.01 : As previously announced, EPB expects to grow its distributions per unit at an annual rate of approximately 9 percent from 2011 to 2015. EPB expects to declare cash distributions of $2.25 per unit for 2012, a 17 percent increase over the $1.93 per unit it distributed for 2011.

4:11PM Mellanox Tech beats by $0.27, beats on revs (MLNX) 66.38 +4.14 : Reports Q2 (Jun) earnings of $0.99 per share, excluding non-recurring items, $0.27 better than the Capital IQ Consensus Estimate of $0.72; revenues rose 110.7% year/year to $133.47 mln vs the $127.96 mln consensus. Non-GAAP gross margin was 70.5% vs 70.0% in Q1 and 68.9% a year ago. Note: Co usually guides on the call, at 5pm ET.

4:11PM Kinder Morgan Partners increases quarterly distribution to $1.23 per unit from $1.20 per unit (KMP) 85.26 -0.12 : Co reported second quarter cash available to pay dividends of $307 million, up 83% from $168 million for the comparable 2011 period. Through the first six months, KMI reported cash available to pay dividends of $610 million, 40% higher than $435 million for the first half of 2011. KMI is expected to finish the year significantly ahead of its published annual budget due to its recent acquisition of El Paso Corporation. The board of directors increased the quarterly cash dividend to $0.35 per share ($1.40 annualized), which is payable on Aug.15, 2012, to shareholders of record as of July 31, 2012. This represents a 17 percent increase over the second quarter 2011 cash distribution per unit of $0.30 ($1.20 annualized) and is up 9 percent from the first quarter 2012 dividend of $0.32 ($1.28 annualized) per share. Chairman and CEO Richard D. Kinder said, "KMI had an excellent quarter, benefiting from the strong performance of Kinder Morgan Energy Partners (NYSE: KMP), and realizing partial-quarter contributions from our new publicly traded pipeline partnership - El Paso Pipeline Partners (NYSE: EPB) - and the natural gas assets we obtained from the acquisition of El Paso Corporation, which closed on May 24'.

4:10PM IBM beats by $0.08, misses on revs; raises FY12 EPS above consensus (IBM) 188.25 +4.60 : Reports Q2 (Jun) earnings of $3.51 per share, excluding non-recurring items, $0.08 better than the Capital IQ Consensus Estimate of $3.43; revenues fell 3.3% year/year to $25.78 bln vs the $26.34 bln consensus. Co issues upside guidance for FY12, raises EPS to at least $15.10, excluding non-recurring items, from at least $15.00 vs. $15.05 Capital IQ Consensus Estimate. The Americas' second-quarter revenues were $11.1 billion, a decrease of 1% (up 1%, adjusting for currency) from the 2011 period. Revenues from Europe/Middle East/Africa were $7.9 billion, down 9% (flat, adjusting for currency). Asia-Pacific revenues increased 2% (up 4%, adjusting for currency) to $6.3 billion. OEM revenues were $512 million, down 24% compared with the 2011 second quarter. Software revenue, flat, up 4% adjusting for currency; Services revenue down 3%, up 1% adjusting for currency: Services pre-tax income up 18%; Services backlog of $136 billion, down 6%, flat adjusting for currency; Systems and Technology revenue down 9%, down 7% adjusting for currency; Growth markets revenue up 2%, up 8% adjusting for currency; Business analytics revenue up 13% in the first half; Smarter Planet revenue up more than 20% in the first half; Cloud revenue doubled first-half 2011 revenue.

4:10PM Core Labs reports EPS in-line, misses on revs; guides Q3 EPS in-line, revs below consensus (CLB) 116.45 +1.92 : Reports Q2 (Jun) earnings of $1.16 per share, ex-items, in-line with the Capital IQ Consensus Estimate consensus of $1.16; revenues rose 9.4% year/year to $247 mln vs the $252.52 mln consensus. Co issues in-line guidance for Q3, sees EPS of $1.17-1.25, ex items, vs. $1.25 Capital IQ Consensus Estimate; sees downside Q3 revs of $250-260 mln vs. $264.60 mln Capital IQ Consensus Estimate.

4:10PM American Express beats by $0.05, misses on revs (AXP) 58.29 -0.39 : Reports Q2 (Jun) earnings of $1.15 per share, $0.05 better than the Capital IQ Consensus Estimate of $1.10; revenues rose 4.6% year/year to $7.96 bln vs the $8.08 bln consensus. The increase was driven by continuing growth in cardmember spending, higher other revenues and higher net interest income, which primarily reflected growth in the cardmember loan portfolio. "Consumer, small business and corporate cardmember spending, along with the business volumes generated by our network of bank partners, remained healthy despite a very uneven economy... Overall cardmember spending rose 7 percent, or 9 percent adjusted for foreign currency translations. That's slower than the increases we've seen in the recent quarters, but it comes on top of a very strong performance a year ago, and continues to grow faster than most of our large issuer competitors.... The cardmember loan portfolio grew 4 percent, and credit indicators, which were excellent at the start of the year, improved even further this quarter... Given the uncertain economic outlook, we remained vigilant in managing discretionary expenses but continued to make substantial investments in marketing initiatives and leverage our loyalty programs to connect millions of consumers and businesses around the world. This helped to continue strengthening our relationships with merchants and cardmembers at a time when mobile and digital technologies are opening up a range of new possibilities."

4:09PM HCP prices an offering of $300 mln of 3.15% senior unsecured notes due 2022; price to the investors was 98.888% of the principal amount of the notes for an effective yield of 3.28% (HCP) 46.06 +0.02 :

4:09PM 8x8 beats by $0.01, beats on revs (EGHT) 4.62 +0.19 : Reports Q1 (Jun) earnings of $0.05 per share, excluding non-recurring items, $0.01 better than the Capital IQ Consensus Estimate of $0.04; revenues rose 36.8% year/year to $25.3 mln vs the $25.02 mln consensus. "With the $12 million influx to our balance sheet from our recent patent sale on top of our ongoing cash from operations, the company is experiencing its highest level of liquidity since it began operating as a service provider and remains committed to executing its aggressive growth strategy in fiscal 2013 and beyond."

4:08PM F5 Networks reports EPS in-line, revs in-line; guides Q1 (Dec) EPS below consensus, revs below consensus (FFIV) 98.59 +6.83 : Reports Q3 (Jun) earnings of $1.14 per share, in-line with the Capital IQ Consensus Estimate consensus of $1.14; revenues rose 21.3% year/year to $352.6 mln vs the $353.16 mln consensus. "Overall, revenue growth slowed in Q3, but revenue by region was generally consistent with historical patterns; 57 percent for the Americas (primarily the United States) and 43 percent for EMEA and APJ, with EMEA contributing 21 percent of the total.

Co issues downside guidance for Q1 (Dec), sees EPS of $1.16-1.19, excluding non-recurring items, vs. $1.24 Capital IQ Consensus Estimate; sees Q1 (Dec) revs of $360-370 mln vs. $383.97 mln Capital IQ Consensus Estimate. Lowered guidance is due to 'cautious spending environment'.

4:08PM Kinder Morgan increases quarterly dividend 9% to $0.35 per share from $0.32 per share (KMI) 35.39 +0.35 :

4:06PM Greenhill misses by $0.18, misses on revs (GHL) 37.68 -0.15 : Reports Q2 (Jun) earnings of $0.07 per share, $0.18 worse than the Capital IQ Consensus Estimate of $0.25; revenues fell 47.9% year/year to $47.3 mln vs the $61.96 mln consensus. Advisory revenues for the quarter were $45.1 million compared to $85.6 million in the second quarter of 2011. Investment revenues for the second quarter of 2012 were $2.2 million compared to $5.2 million in the second quarter of 2011.

4:05PM Qualcomm misses by $0.01, misses on revs; guides Q4 EPS below consensus, revs below consensus; guides FY12 EPS below consensus, revs below consensus (QCOM) 56.05 +1.59 : Reports Q3 (Jun) earnings of $0.85 per share, excluding non-recurring items, $0.01 worse than the Capital IQ Consensus Estimate of $0.86; revenues rose 27.8% year/year to $4.63 bln vs the $4.68 bln consensus. Co issues downside guidance for Q4, sees EPS of $0.78-0.84 vs. $0.89 Capital IQ Consensus Estimate; sees Q4 revs of $4.45-4.85 bln vs. $4.9 bln Capital IQ Consensus Estimate. Co issues downside guidance for FY12, sees EPS of $3.61-3.67 vs. $3.74 Capital IQ Consensus Estimate, down from prior guidance of $3.61-3.76; sees FY12 revs of $18.7-19.1 bln vs. $19.21 bln Capital IQ Consensus Estimate, down from prior guidance of $18.7-19.7 bln.

"Looking forward, our growth estimates for 3G/4G device shipments in calendar 2012 have moderated slightly, and we now expect the demand profile of the calendar year to be more back-end loaded as new devices are launched for the holiday season. Although our outlook for semiconductor volumes in the fiscal fourth quarter has been reduced from our prior expectations, we are ramping supply of our 28 nanometer chipsets to help enable what we expect to be a strong December quarter for our semiconductor business."

4:05PM Select Comfort beats by $0.03, beats on revs; guides FY12 EPS in-line (SCSS) 21.77 +0.65 : Reports Q2 (Jun) earnings of $0.30 per share, $0.03 better than the Capital IQ Consensus Estimate of $0.27; revenues rose 27.3% year/year to $205 mln vs the $195.95 mln consensus. Gross-profit margin in the second quarter of 2012 was 64.1 percent of net sales, an increase of 60 basis points versus 63.5 percent in the prior-year period. The year-over-year increase was primarily driven by a variety of pricing increases executed over the past 12 months.

Co issues in-line guidance for FY12, sees EPS of $1.41-1.47, excluding non-recurring items, vs. $1.44 Capital IQ Consensus Estimate. This outlook continues to assume company-controlled comparable sales growth for the remainder of the year of at least 15 percent and a year-over-year increase in full-year operating margin of at least 100 basis points. The company is increasing its estimate for year-end 2012 store count from the previous range of between 400 and 410 stores to a new range of between 408 to 412 stores, a 7 to 8 percent increase from the 381 stores at year-end 2011. Capital expenditures for 2012 are estimated to be approximately $50 million, reflecting new stores, repositioned stores and remodels, along with continued investment in information systems. The company also plans to continue share repurchases in the second half of 2012, with the objective of maintaining share count.

4:05PM Cypress Sharpridge Investments misses by $0.10 (CYS) 13.93 -0.21 : Reports Q2 (Jun) earnings of $0.38 per share, excluding non-recurring items, $0.10 worse than the Capital IQ Consensus Estimate of $0.48.

4:03PM Plexus beats by $0.03, reports revs in-line; guides for Q4 (PLXS) 27.45 +0.76 : Reports Q3 (Jun) earnings of $0.66 per share, $0.03 better than the Capital IQ Consensus Estimate of $0.63; revenues rose 8.9% year/year to $608.81 mln vs the $606.77 mln consensus. Co issues guidance for Q4, sees EPS of $0.60-0.66 vs. $0.66 Capital IQ Consensus Estimate; sees Q4 revs of $590-620 mln vs. $624.29 mln Capital IQ Consensus Estimate. Co says "Looking further ahead, we anticipate that the macro-environment will continue to be challenging, making longer-range growth projections exceptionally difficult. Our optimism about longer-term growth is anchored in our strong new wins performance over the past year that should result in revenue growth strengthening in fiscal 2013. However, with this difficult macro backdrop, we currently anticipate that the end-market environment will continue to be challenging for many of our customers, resulting in muted growth for mature production programs. Optimizing results under our financial model relies on a balanced mix, where growing mature programs yield typically better operating performance, and offset the production startup costs we experience in the earlier phases of new programs. While we believe that our current level of operating margin performance is industry leading, it is below our target, which we believe may be difficult to achieve in an environment where our revenue growth is heavily biased to ramping new program wins versus end-market growth of mature programs."

4:02PM WellCare Group enters into agreement with Humana (HUM) to acquire select assets of Arcadian Health Plan, Inc.'s Desert Canyon Community (WCG) 66.96 +1.44 : Co announced that it has entered into an agreement with Humana (HUM) to acquire select assets of Arcadian Health Plan Desert Canyon Community Care Medicare Advantage plans in Arizona. The plans are part of a previously announced, government-required divestiture for Humana to complete its acquisition of Arcadian Health. Under the agreement, Desert Canyon members in Mohave and Yavapai Counties will become WellCare of Arizona members on January 1, 2013. Currently, the Desert Canyon plans have approximately 5,000 members in these counties. The transaction is expected to close on December 31, 2012, subject to regulatory approvals.

4:02PM Covanta beats by $0.03, misses on revs (CVA) 17.09 -0.01 : Reports Q2 (Jun) earnings of $0.15 per share, excluding non-recurring items, $0.03 better than the Capital IQ Consensus Estimate of $0.12; revenues fell 0.2% year/year to $410 mln vs the $417.5 mln consensus. "Excellent operating performance drove another solid financial quarter and it gives us confidence to reaffirm our full year guidance, which calls for continued earnings growth despite declines in energy and recycled metal markets." "Furthermore, we are effectively executing against our organic growth initiatives, while strengthening our base business by negotiating win-win contract renewals with our clients. The work we are doing now will pay off in the coming years."

4:02PM RLI Corp beats by $0.04, reports revs in-line (RLI) 70.36 +0.76 : Reports Q2 (Jun) earnings of $1.17 per share, excluding non-recurring items, $0.04 better than the Capital IQ Consensus Estimate of $1.13; revenues fell 0.3% year/year to $155.7 mln vs the $156.73 mln consensus.

4:02PM Pain Therapeutics publishes novel approach to Treat Alzheimer's disease (PTIE) 4.52 +0.05 : Co announced the publication of preclinical data that demonstrate a promising new approach to treat Alzheimer's disease. Patients with Alzheimer's disease suffer from progressive and irreversible cognitive impairment that is widely believed to be caused by a protein called beta-amyloid.

4:01PM Nanosphere announces commencement of public offering of common stock; size not disclosed (NSPH) 2.61 -0.16 : Co announced that it intends to offer shares of its common stock in a public offering. Co plans to use the net proceeds from the offering for general corporate purposes and working capital.

4:00PM Prudential to discontinue sales of group long-term care insurance coverage (PRU) 48.66 +0.01 : Prudential Group Insurance, a business of Prudential Financial, announced that it will discontinue sales of new group long-term care insurance policies, effective August 1, 2012, in all states except Indiana, Iowa, Kansas, Louisiana, and South Dakota, where it will continue to offer products for a period of time as required by state law. Prudential will also notify clients of its intent to continue to accept group long-term care enrollments until June 30, 2013. The decision reflects the impact of the continued low interest rate environment, and Group Insurance's desire to achieve appropriate returns, enhance its long-term risk profile, and further its longer-term goal of sustainable, profitable growth in its core group life and disability lines of business. The terms and conditions of coverage provided under existing group long-term care insurance certificates will not change.

4:00PM Tornier appoints new Chief Financial Officer (TRNX) 21.54 +0.35 : Co announced that it has appointed Shawn T McCormick as Chief Financial Officer, effective as of September 4, 2012. Mr. McCormick will succeed Carmen L. Diersen, who will depart as Global Chief Financial Officer of Tornier immediately for personal reasons, but will remain as a consultant to Tornier through July 16, 2013. Douglas W. Kohrs, President and Chief Executive Officer of Tornier, will serve as Interim Chief Financial Officer until Mr. McCormick assumes the position on September 4, 2012. He most recently served as Chief Operating Officer of Lutonix, Inc., a medical device company acquired by C. R. Bard (BCR).

4:00PM Ignite Restaurant announces restatement and accounting review; guided Q2 revs of $119.9 mln vs $120.9 mln consensus (IRG) 19.06 -0.44 : Co announces following an internal assessment of its lease accounting policies, it has determined it necessary to correct non-cash related errors related to its accounting treatment of certain leases. As a follow-up to this review, the Company is also commencing a detailed review of its historical accounting for fixed assets and related depreciation expense in prior periods as a private company. Following the completion of the accounting review, the Company, with the concurrence of its independent registered public accounting firm, PricewaterhouseCoopers LLP, will restate its previously issued financial statements for years 2009 through 2011 and for the first quarter of 2012. The lease accounting errors have been preliminarily quantified by the Company and date back to 2006, the year of the Company's origination. As discussed below, adjustments for these errors will reflect non-cash charges primarily relating to deferred rent. The Company will restate its previously issued financial statements to recognize rent expense on a straight line basis over the effective lease term, including cancelable option periods where failure to exercise such options would result in an economic penalty. The lease term will commence on the date when the Company establishes effective control over the property. Furthermore, straight line rent will be appropriately calculated on properties with CPI adjustments that are subject to a stated minimum required rent increase. The changes to the recognition of rent expense are timing in nature and do not change the total cash payments or aggregate rent expense over the effective life of the lease term. The total amount of the increases to historical deferred rent expense will be offset by the same aggregate amount of the adjustments in the form of lower deferred rent expense in the future years of the effective lives of the impacted leases. The Company estimates that the aggregate pre-tax effect of the lease accounting related restatement items from 2006 through the first quarter of 2012 will range from $3.4 to $3.8 million. The non-cash charges will impact deferred rent expense and pre-opening expense (the deferred rent portion only). The cumulative impact of these expenses in 2006 through 2009 is estimated to be $500 to $600 thousand. The impact is higher from 2010 through the first quarter of 2012 when the Company opened 24 new or converted units. The lease accounting restatement adjustments reduce pre-tax income by an estimated $1.0 to $1.1 million in 2010, $1.3 to $1.5 million in 2011 and $550 to $650 thousand in the first quarter of 2012. The estimated increases in deferred rent expense and preopening expense will result in a corresponding increase in the deferred rent liability. The lease accounting related restatement items will not impact the Company's cash flows, revenues or comparable restaurant sales. Additionally, these restatement items will not impact restaurant-level profit margin or Adjusted EBITDA. The co also reported for the second quarter ended June 18, 2012, the Company estimates revenues to be approximately $119.9 million, an increase of 16.2% compared to revenues of $103.2 million in the prior-year period vs $120.99 mln consensus. The Company estimates that comparable restaurant sales increased 3.0%. This increase marks the Company's 16th consecutive quarter of comparable restaurant sales growth. Restaurant-level profit margin for the second quarter is expected to be between 19.4% and 19.7%. Restaurant-level profit for the second quarter is estimated to be between $23.2 and $23.6 million, an increase of more than 29% compared to the previously reported prior year period. The prior year comparison does not include any potential impact from the fixed asset review work that is currently underway. The five Joe's Crab Shack restaurants developed under our new unit prototype that have been open for more than twelve months have estimated average sales volumes of $5.9 million over the twelve-month period ended June 18, 2012. The co has not yet completed closing procedures for the second quarter ended June 18, 2012 and these preliminary results are subject to change. Due to the scope and timing of the fixed asset accounting review noted above, the Company's second quarter earnings release and quarterly report on Form 10-Q are expected to be delayed.

3:49PM Mizuho Financial subsidiary reaches settlement agreement with SEC (MFG) 3.23 -0.01 : Mizuho Securities USA, the U.S. broker-dealer subsidiary of Mizuho Financial Group, announced that it has entered into a Settlement Agreement with the SEC in relation to the agency's investigation of a collateralized debt obligation ("CDO") transaction in 2007. The agreement is subject to court approval. Under the terms of the settlement, Mizuho was not charged with fraud or intentional misconduct and the firm did not admit wrongdoing. Mizuho has agreed to pay $127.5 mln under the settlement. Resolution of this matter will not have a material adverse effect on the firm's financial statements. Mizuho cooperated fully with the SEC throughout this process. The firm agreed to the settlement to avoid protracted litigation and distraction and believes the settlement is the right outcome for its shareholders, clients and employees.

3:41PM Earnings Calendar (SUMRX) : Today after the close look for the following companies to report:

EWBC, IBM, SYK, AF, AXP, CCK, CLB, CNS, CVA, CVBF, CYS, EBAY, FFIV, GHL, HNI, LHO, MLNX, NE, PLXS, PTP, QCOM, RLI, SCSS, SLM, UFPI, UMPQ, WTFC, YUM, COF, KMP, XLNX, SWKS, NVEC, EPB, and EGHT.

Tomorrow before the open look for the following companies to report:

SCHL, SHF, DGX, HBAN, TXT, VCBI, ADS, ARB, BAX, BBT, BX, CY, DHR, DO, ENTG, FCS, FCX, FITB, GPC, HOMB, HUB.B, IIIN, KEY, LH, LTM, LUV, MS, NOK, NUE, NVR, PM, POOL, PPG, SASR, SHW, SNA, SON, SYNT, TCB, TRV, TZOO, UNH, UNP, USAK, UTEK, VZ, WCC, JCI, ORB, KNL, NVS, VTNC, AN, GMT, GR, NTCT, SWY, TSM, VIVO, NAFC, VFC, YRCW, and CMCO.

3:20PM Avino Silver & Gold: Clarification and retraction of technical disclosures; says 2009 inferred resource estimate prepared on the San Gonzalo vein is no longer considered a current resource (ASM) 1.26 +0.00 : The Company has been fully co-operating with the BCSC in this matter, and with its independent engineering consultants, Tetra Tech Wardrop, has filed with the BCSC an amended technical report to address the BCSC's disclosure concerns. The Company also wants to clarify certain technical disclosures with respect to the San Gonzalo Mine. Due to the development of a ramp, bulk sampling, limited mining depletion and additional delineation drilling, a 2009 inferred resource estimate prepared on the San Gonzalo vein is no longer considered a current resource estimate and should not and cannot be relied upon as such. It should be noted that there are significant risks associated with making a production decision on the San Gonzalo Mine without a current resource estimate. The Company has not altered its plan to move forward with the development of San Gonzalo Mine and intends on processing feed mined from the San Gonzalo Mine later this year. (shares halted since July 2)

http://finance.yahoo.com/news/avino-silver-gold-mines-ltd-19…

...und:

FEATURES

Market Coverage

Market Overview

Market Update

In Play®

Story Stocks

Short Stories

Tech Stocks

Market Events

Earnings Calendar

Economic Calendar

Splits Calendar

Conference Call Calendar

IPO Calendar

Upgrades/Downgrades

Market Statistics

Market Digest

U.S. Market Indices

World Market Indices

Currency Exchange Rates

InPlay

5:34PM CubeSmart has been retained by American Storage to manage 31 self-storage facilities (CUBE) 12.11 -0.05 : CubeSmart will assume management of the portfolio effective August 1, 2012. The facilities will continue to operate under the name American Storage.

5:31PM Alexza Pharma announces submission of responses to the EMA Day 120 List of Questions for the ADASUVE MAA (ALXA) 3.52 -0.06 : Co announced that it has submitted its responses regarding the ADASUVE Marketing Authorization Application (MAA) to the European Medicines Agency (EMA). In March 2012, Alexza received the Committee for Medicinal Products for Human Use Consolidated List of Questions (Day 120 List of Questions) regarding Alexza's ADASUVE MAA. In May 2012, Alexza and its European corporate partner, Grupo Ferrer, met with the Rapporteur, Co-Rapporteur and EMA to further understand specifics of the major objections raised in the Day 120 List of Questions. The submitted responses are intended to address the questions outlined in the Day 120 List of Questions. According to the published EMA timetables, Alexza expects to receive the Day 180 List of Outstanding Issues for the ADASUVE MAA in late September 2012. Alexza also announced today that it has completed the follow-up from the May 2012 EU Pre-Approval Inspection (PAI). This inspection resulted in no findings the EMA classified as Critical or Major deficiencies. The EU PAI resulted in 12 findings classified as Other and 4 recommendations. The EMA has accepted Alexza's final corrective action plan, and proposed timing for the action plan completion and reporting. Alexza expects to receive its EU Good Manufacturing Practices (GMP) Certificate for its Mountain View, California facility as a result of this outcome.

5:27PM DDR announces redemption of 7.5% Class I cumulative redeemable preferred shares (DDR) 14.95 -0.04 : Co announced that it is calling for redemption all outstanding shares of its 7.50% Class I Cumulative Redeemable Preferred Shares, without par value, and the related depositary shares, each representing 1/20th of one share of the Class I Preferred Shares. The Class I Preferred Shares and respective Depositary Shares will be redeemed in whole at a redemption price of $503.75 per Class I Preferred Share or $25.1875 per Depositary Share (the sum of $500.00 per Class I Preferred Share plus accrued and unpaid dividends of $3.75 per Class I Preferred Share to the redemption date or $25.00 per Depositary Share plus accrued and unpaid dividends of $0.1875 per Depositary Share to the redemption date).

5:25PM HNI reports EPS in-line, beats on revs; guides Q3 EPS above consensus, revs above consensus; guides FY12 EPS above consensus (HNI) 27.22 +0.44 : Reports Q2 (Jun) earnings of $0.17 per share, excluding non-recurring items, in-line with the Capital IQ Consensus Estimate consensus of $0.17; revenues rose 11.0% year/year to $480.4 mln vs the $473.04 mln consensus. Co issues upside guidance for Q3, sees EPS of $0.65-0.70, excluding non-recurring items, vs. $0.65 Capital IQ Consensus Estimate; sees Q3 revenue growth of 11-14% (~$559.7-574.8 mln) vs. $555.82 mln Capital IQ Consensus Estimate. Co issues upside guidance for FY12, sees EPS of $1.35-1.45, excluding non-recurring items, vs. $1.34 Capital IQ Consensus Estimate.

5:23PM DDR announces pricing of $200 mln 6.5% cumulative redeemable preferred stock (DDR) 14.95 -0.04 : Co announced that it has priced an underwritten public offering of 8,000,000 depositary shares, each representing a 1/20 fractional interest in a share of its newly designated 6.50% Class J Cumulative Redeemable Preferred Shares at a price of $25.00 per depositary share.

5:06PM IBM conference call summary (call is currently in Q&A) (IBM) 188.20 +4.60 :

Mgmt noted that deadwinds included currency fluctuations and volatility for translation and hedging dynamics. Total operating expense and other income was down 6%. Co is dealing with significant currency dynamics which impacted its revenue lines by ~ $1 bln, or almost 4 points.

Co had $150 mln of workforce balancing in the quarter primarily in Europe.

Co should see ongoing benefits to the GTS portfolio.

GBS returned to a more typical level of profitability.

Co saw strength in Russia and China. China was up over 20% this quarter, gaining share again. Co is continuing to build its capabilities there. They expanded the number of branch offices and now have 68 face-to-face and over 100 virtual branch offices open across all of China.

Europe saw mixed performance as Italy and France were down.

5:06PM J.M. Smucker increases dividend 8.3% to $0.52 from $0.48 per share (SJM) 75.96 -0.02 :

5:04PM Crown Hldgs reports EPS in-line, misses on revs (CCK) 34.20 +0.11 : Reports Q2 (Jun) earnings of $0.84 per share, excluding non-recurring items, in-line with the Capital IQ Consensus Estimate consensus of $0.84; revenues fell 4.3% year/year to $2.18 bln vs the $2.28 bln consensus. "In the Americas and Asia we continued to perform well. Importantly, the results demonstrate the benefit of our product and geographic diversity. Globally, beverage can volumes grew 5%, driven by our emerging market capacity expansion program over the last few years."

5:03PM Noble Corp beats by $0.01, reports revs in-line (NE) 35.40 +0.90 : Reports Q2 (Jun) earnings of $0.59 per share, excluding a non-recurring after tax gain of $0.04, $0.01 better than the Capital IQ Consensus Estimate of $0.58; revenues rose 43.1% year/year to $898.9 mln vs the $897.1 mln consensus. Contract drilling services revenues for Q2 of 2012 were $848 million versus $746 million for Q1 of 2012, an increase of ~14%. For Q2 of 2011, contract drilling services revenues totaled $590 million.

4:46PM Astoria Fincl reports EPS in-line (AF) 9.99 -0.09 : Reports Q2 (Jun) earnings of $0.13 per share, in-line with the Capital IQ Consensus Estimate consensus of $0.13. "I am pleased to report continued growth in both the loan portfolio and balance sheet this quarter, fueled by an increase in the multi-family loan portfolio. In addition, the results of the cost control initiatives undertaken in the first quarter have produced a significant reduction in operating expenses this quarter. I am also pleased with the positive progression in our asset/liability repositioning. Multi-family/commercial real estate loans increased 21% from December 31, 2011, while residential loans remained relatively stable, and low-cost core deposits increased 8%, while high-cost CDs decreased 18%. We expect that together, the growth and repositioning of the balance sheet coupled with improved operating efficiency should benefit the net interest margin and improve profitability throughout the remainder of the year."

4:38PM Financial Stability Oversight Council- designates 8 banks as Systemically important; will face new supervision but that has yet to be determined; Fed Reserve will decide these banks can access borrowing windows (XLF) : Says concerns about growth in emerging markets a concern. Says housing has been a drag on recovery.

4:37PM SLM Corp beats by $0.05 on a GAAP basis (SLM) 16.04 -0.13 : Reports Q2 (Jun) GAAP earnings of $0.59 per share, $0.05 better than the GAAP Capital IQ Consensus Estimate of $0.54; net interest income fell 14.1% year/year to $746 mln, may not compare to the $706.2 mln consensus. Core earnings were $0.49 vs. $0.48 last yr. "We continue to grow our private credit business and find productivity gains in challenging economic conditions. "We head into this academic year with loan products that promote and reward in-school payments. The performance of these loans over recent years foreshadows better credit ratings for our customers and lower defaults for Sallie Mae."

4:34PM Skyworks beats by $0.01, beats on revs; guides Q4 EPS in-line, revs in-line (SWKS) 28.65 +1.12 : Reports Q3 (Jun) earnings of $0.45 per share, excluding non-recurring items, $0.01 better than the Capital IQ Consensus Estimate of $0.44; revenues rose 9.2% year/year to $389 mln vs the $383.02 mln consensus. Co issues in-line guidance for Q4, sees EPS of 0.50-0.51, excluding non-recurring items, vs. $0.51 Capital IQ Consensus Estimate; sees Q4 revs of 415-420 mln vs. $418.03 mln Capital IQ Consensus Estimate. "Our strategic diversification across OEMs and chipset partners is enabling us to produce consistently strong operating results despite the macro economy. Specifically, we are gaining share within adjacent vertical markets including automotive, medical, avionics, military, location services and broadband communications. At the same time, our innovative solutions are powering the world's most popular smartphones, tablets, home automation platforms and network infrastructure systems. In short, we have created a differentiated business model that is delivering demonstrable, best in class mobile internet growth with analog semiconductor shareholder returns."

4:34PM Diana Containerships announces proposed public offering of 8.1 mln shares of common stock (DCIX) 7.20 -0.05 : The net proceeds of the offering are expected to be used by the co for general corporate purposes, including vessel acquisitions and working capital, although no specific vessels have been identified by the Company for acquisition at this time. Wells Fargo Securities, BofA Merrill Lynch and UBS Investment Bank are acting as joint-book runners of the offering. Barclays and RBC Capital Markets are acting as co-managers.

4:33PM Cohen & Steers misses by $0.05, beats on revs (CNS) 36.49 -1.16 : Reports Q2 (Jun) earnings of $0.36 per share, $0.05 worse than the Capital IQ Consensus Estimate of $0.41; revenues rose 9.6% year/year to $67.4 mln vs the $66.63 mln consensus. Assets under management were $44.4 billion as of June 30, 2012, a decrease of 1.1% from $44.9 billion at March 31, 2012 and an increase of 0.2% from $44.3 billion at June 30, 2011.

4:32PM East West Banc beats by $0.02; guides Q4 (Dec) EPS in-line; guides FY12 EPS above consensus (EWBC) 23.74 -0.22 : Reports Q2 (Jun) earnings of $0.47 per share, $0.02 better than the Capital IQ Consensus Estimate of $0.45. Co issues in-line guidance for Q4 (Dec), sees EPS of $0.45-0.47 vs. $0.47 Capital IQ Consensus Estimate. Co issues upside guidance for FY12, sees EPS of $1.84-1.86 vs. $1.84 Capital IQ Consensus Estimate.

The Company is providing guidance for the third quarter and full year of 2012. Management currently estimates that fully diluted earnings per share for the full year of 2012 will range from $1.84 to $1.86, an increase of 15% to 16% from the full year of 2011. Also, this updated guidance for the full year of 2012 is an increase of approximately $0.05 per dilutive share from our previously released guidance. Management currently estimates that fully diluted earnings per share for the third quarter of 2012 will range from $0.45 to $0.47 per dilutive share.

This EPS guidance for the third quarter of 2012 is based on the following assumptions:

-- Stable balance sheet- A stable interest rate environment and an adjusted net interest margin of approximately 4.00%.

-- Provision for loan losses of approximately $12 to $15 million for the quarter

-- Total noninterest expense of approximately $100 million for the quarter, net of amounts to be reimbursed by the FDIC Effective tax rate of approximately 35%

4:31PM Spectra Energy LP increases quarterly cash distribution 1.0% to $0.485 per unit (SEP) 32.35 +0.18 :

4:31PM Peoples Fed Bancshares Inc announces an initial $0.03 dividend payment to stockholders (PEOP) 16.70 +0.04 : Co announced that its Board of Directors has declared a quarterly cash dividend of $0.03 per share on the Company's common stock. The dividend will be payable to stockholders of record as of August 7, 2012, and will be paid on August 17, 2012.

4:31PM State Auto Fin reports estimate of second quarter storm activity impact (STFC) 14.63 -0.13 : Co announces its preliminary estimate of the impact of catastrophe losses on its second quarter results. The company estimates second quarter 2012 results will include between $33 million and $36 million in pre-tax net catastrophe losses. During the quarter ended June 30, 2012, 13 catastrophe events in the United States were identified by Property Claim Service. STFC's catastrophe losses were primarily related to two events: wind and hail activity affecting the Louisville, Ky., and St. Louis, Mo., areas in late April and, to a lesser extent, wind activity from a storm event in the Midwest and Mid-Atlantic states at the end of June.

4:31PM LaCrosse Footwear receives $29 mln order for the United States Marine Corps (BOOT) 19.94 -0.01 : Co announced that it has received a new $29 million delivery order for the United States Marine Corps for Danner's USMC Rugged All-Terrain (RAT) Hot weather and Temperate boots. The Company anticipates fulfilling this order in multiple deliveries over the next several quarters.

4:25PM YUM! Brands misses by $0.03, beats on revs; reaffirms FY12 EPS guidance (YUM) 65.55 +1.14 : Reports Q2 (Jun) earnings of $0.67 per share, $0.03 worse than the Capital IQ Consensus Estimate of $0.70; revenues rose 12.5% year/year to $3.17 bln vs the $3.11 bln consensus. Worldwide restaurant margin declined 0.6 percentage points to 15.2%, including declines of 4.1 percentage points in China and 1.1 percentage points at YRI. Restaurant margin increased 5.8 percentage points in the U.S... Same-store sales grew 10% in China, 4% at YRI and 7% in the U.S.