SEABRIDGE GOLD INC. - CANADA - 500 Beiträge pro Seite (Seite 14)

eröffnet am 25.05.03 16:11:24 von

neuester Beitrag 22.07.19 10:06:05 von

neuester Beitrag 22.07.19 10:06:05 von

Beiträge: 6.865

ID: 735.946

ID: 735.946

Aufrufe heute: 2

Gesamt: 322.643

Gesamt: 322.643

Aktive User: 0

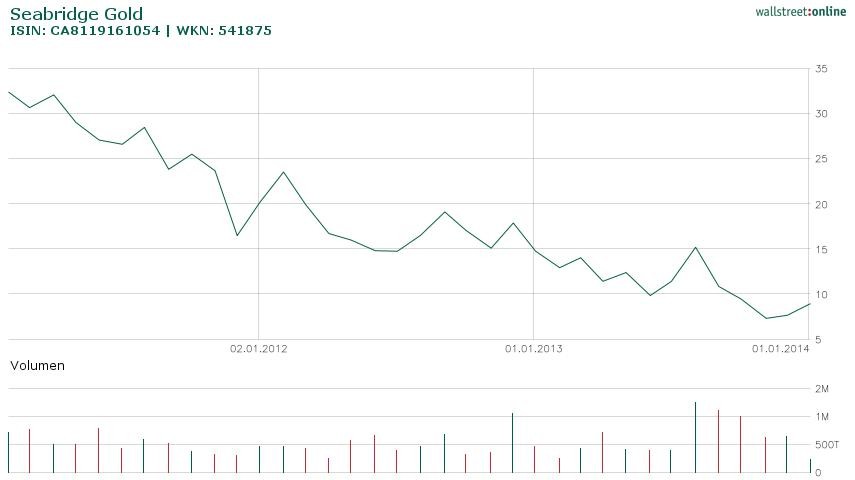

ISIN: CA8119161054 · WKN: 541875 · Symbol: SA

15,160

USD

+3,62 %

+0,530 USD

Letzter Kurs 02:04:00 NYSE

Neuigkeiten

29.02.24 · Swiss Resource Capital AG Anzeige |

24.10.23 · Swiss Resource Capital AG Anzeige |

29.04.23 · Jörg Schulte Anzeige |

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7950 | +30,33 | |

| 55,80 | +15,41 | |

| 0,7999 | +14,27 | |

| 11,250 | +12,73 | |

| 0,5500 | +10,00 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7145 | -8,92 | |

| 2,1800 | -9,17 | |

| 186,20 | -10,48 | |

| 4,2300 | -17,86 | |

| 46,74 | -98,00 |

Antwort auf Beitrag Nr.: 45.326.573 von valueinvestor am 26.08.13 17:06:41Das war wohl eher Mittelmass.

16.31 +0.30 1.9% 799.4k

---

Aber ich bin tatsaechlich etwas überrascht, hatte ich doch Kurse um 15.X fuer SA prognostiziert, nun liegt sie einen schlappen Dollar drüber. Ich sehe aber tatsaechlich die 35 Dollar oder die Kursprognosen (Hausbaufinanzierung) von 90 Dollar gar nicht. Was sagst du zu deinen Kurszielen?

16.31 +0.30 1.9% 799.4k

---

Aber ich bin tatsaechlich etwas überrascht, hatte ich doch Kurse um 15.X fuer SA prognostiziert, nun liegt sie einen schlappen Dollar drüber. Ich sehe aber tatsaechlich die 35 Dollar oder die Kursprognosen (Hausbaufinanzierung) von 90 Dollar gar nicht. Was sagst du zu deinen Kurszielen?

http://www.nasdaq.com/symbol/sa/short-interest

das wird spassig, 6 Millionen Aktien short. Das heißt der jüngste 100% Anstieg lief nicht wegen sich eindeckender Leerverkäufer sondern im Gegenteil gegen zusätzlichen Leerverkaufsdruck.

Syrien, der Schuldendeckel der USA, das ausbleibende Tapering der FED, weitere nervorragend gute Bohrergebnisse, Margin Calls für die shorts - das ist wirklich eine außerordentliche Gemengelage.

Lemming, wie stehst du eigentlich zu den spamartig und unter verschiedensten Nicknames weltweit wiederholt von dir verbreiteten Lügen, es würde kein Abkommen zwischen Pretium und Seabridge bezüglich einer optimalen Nutzung der KSM Lagerstätte geben? Du solltest dich schämen.

SEABRIDGE AND PRETIUM SIGN AGREEMENTS ON COOPERATION

Monday, 9th May 2011

Toronto, Canada - Seabridge Gold announced today it has executed two agreements with Pretium Resources Inc. to: (1) establish the terms under which mining operations at one project can encroach on the other's boundaries;

http://www.seabridgegold.net/News/Article/323/seabridge-and-…

Quellen für die Lügenverbreitung unter verschiedenen Usernamen:

http://finance.yahoo.com/mbview/userview/;_ylt=ArZvtFWKj0A6.…

und hier in den Kommentaren:

http://seekingalpha.com/article/1615372-seabridge-gold-will-…

das wird spassig, 6 Millionen Aktien short. Das heißt der jüngste 100% Anstieg lief nicht wegen sich eindeckender Leerverkäufer sondern im Gegenteil gegen zusätzlichen Leerverkaufsdruck.

Syrien, der Schuldendeckel der USA, das ausbleibende Tapering der FED, weitere nervorragend gute Bohrergebnisse, Margin Calls für die shorts - das ist wirklich eine außerordentliche Gemengelage.

Lemming, wie stehst du eigentlich zu den spamartig und unter verschiedensten Nicknames weltweit wiederholt von dir verbreiteten Lügen, es würde kein Abkommen zwischen Pretium und Seabridge bezüglich einer optimalen Nutzung der KSM Lagerstätte geben? Du solltest dich schämen.

SEABRIDGE AND PRETIUM SIGN AGREEMENTS ON COOPERATION

Monday, 9th May 2011

Toronto, Canada - Seabridge Gold announced today it has executed two agreements with Pretium Resources Inc. to: (1) establish the terms under which mining operations at one project can encroach on the other's boundaries;

http://www.seabridgegold.net/News/Article/323/seabridge-and-…

Quellen für die Lügenverbreitung unter verschiedenen Usernamen:

http://finance.yahoo.com/mbview/userview/;_ylt=ArZvtFWKj0A6.…

und hier in den Kommentaren:

http://seekingalpha.com/article/1615372-seabridge-gold-will-…

vorbörslich wieder bei 17...

Ich sehe da in der Tat keine bindende Vereinbarung - anlässlich einer gemeinsamen Studie im Jahr 2011 wurde ein vertrauliches Agreement getroffen. mehr ist das nicht. Die Joint-Studie wurde nie veroeffentlicht und Quartermain hat daraufhin Snowfield bis 2023 auf Eis gelegt.

Es ist in der Tat so, dass KSM und Snowfield eine gemeinsame Grenze haben und das hier mit Sicherheit ein Major mit Pretium ebenfalls verhandeln muesste. Das ist aber eher eine akademische Frage, da KSM wohl auch bis 2023 keine Mine wird und Snowfield nur sehr langfristig zu betrachten ist.

Bblemming und Boersenbrieflemming wuerde ich nicht als unterschiedliche Nicknames bezeichnen wollen.

Vielen Dank fuer Deine Aufmerksamkeit,

BL

Es ist in der Tat so, dass KSM und Snowfield eine gemeinsame Grenze haben und das hier mit Sicherheit ein Major mit Pretium ebenfalls verhandeln muesste. Das ist aber eher eine akademische Frage, da KSM wohl auch bis 2023 keine Mine wird und Snowfield nur sehr langfristig zu betrachten ist.

Bblemming und Boersenbrieflemming wuerde ich nicht als unterschiedliche Nicknames bezeichnen wollen.

Vielen Dank fuer Deine Aufmerksamkeit,

BL

Antwort auf Beitrag Nr.: 45.333.647 von valueinvestor am 27.08.13 14:36:40Was nicht stimmt ... Zum Zeitpunkt deines Postings 16.50 USD

Trading Spotlight

jetzt wird es albern ...

SA

08:21:32 Z 16.50 0.19 100

Quelle:stockwatch.com

P.S. Kannst du dein Kursziel von 90 USD noch einmal erläutern? Steht das noch?

SA

08:21:32 Z 16.50 0.19 100

Quelle:stockwatch.com

P.S. Kannst du dein Kursziel von 90 USD noch einmal erläutern? Steht das noch?

Die vorbörslichen Marktmanipulationen haben nichts gebracht. Das Ergebnis war ein Absturz der Aktie Seabridge Gold an den Maerkten.

SA 15.02 -1.29 USD -7.9 1,334.8k

Denkt mal darueber nach,

BL

SA 15.02 -1.29 USD -7.9 1,334.8k

Denkt mal darueber nach,

BL

11,548 €

-12,21 %

In Frankfurt geht es auch kraeftig runter - die vorboerslichen Spielereien in Uebersee

mit wenigen Stuecken haben m.M.n. haeufig auch den deutschen Kaeufer im Visier. Hier wird dann abgeladen.

Denkt mal darueber nach,

BL

-12,21 %

In Frankfurt geht es auch kraeftig runter - die vorboerslichen Spielereien in Uebersee

mit wenigen Stuecken haben m.M.n. haeufig auch den deutschen Kaeufer im Visier. Hier wird dann abgeladen.

Denkt mal darueber nach,

BL

vorbörslich bereits wieder 15,70...

Antwort auf Beitrag Nr.: 45.271.193 von valueinvestor am 17.08.13 18:52:08deinem überdimensionierten Geländewagen

Ich hatte das ueberlesen. Es ist unschoen, welches Interesse du an meiner Person zeigst.

Bitte unterlass das kuenftig.

Ich hatte das ueberlesen. Es ist unschoen, welches Interesse du an meiner Person zeigst.

Bitte unterlass das kuenftig.

SELL

Our system’s recommendation today is to SELL. The BEARISH BELT HOLD pattern finally received a confirmation because the prices crossed the confirmation level which was at 15,2900, and our valid average selling price stands now at 15,2700.

Quelle: http://americanbulls.com/SignalPage.aspx?lang=en&Ticker=SA

Our system’s recommendation today is to SELL. The BEARISH BELT HOLD pattern finally received a confirmation because the prices crossed the confirmation level which was at 15,2900, and our valid average selling price stands now at 15,2700.

Quelle: http://americanbulls.com/SignalPage.aspx?lang=en&Ticker=SA

Zitat von boersenbrieflemming: SELL

Our system’s recommendation today is to SELL. The BEARISH BELT HOLD pattern finally received a confirmation because the prices crossed the confirmation level which was at 15,2900, and our valid average selling price stands now at 15,2700.

Quelle: http://americanbulls.com/SignalPage.aspx?lang=en&Ticker=SA

Sehr aussagekräftig ist der direkt an dein Zitat anschließende Text:

The previous BUY recommendation was issued on 22.07.2013, 36 days ago, when the stock price was 10,0000. Since then SA has risen by +52,70%.

Da darf dann schon mal Gewinn mitgenommen werden.

Antwort auf Beitrag Nr.: 45.342.421 von valueinvestor am 28.08.13 15:09:53... und da waren es dann wieder 1,12 USD weniger. Am Vortag waren es knapp 2 USD.

SA: 14.58 USD

Wie hiess es noch gleich am Hoehepunkt: "now this is big fun"

http://finance.yahoo.com/mbview/threadview/?&bn=ae2d8375-038…

Diese vorboerslichen Spielereien, das Hochziehen des Kurses mit gerade einmal 100 Stueck ist sehr bemerkenswert und funktioniert im Moment nicht mehr.

Denkt mal darueber nach,

BL

SA: 14.58 USD

Wie hiess es noch gleich am Hoehepunkt: "now this is big fun"

http://finance.yahoo.com/mbview/threadview/?&bn=ae2d8375-038…

Diese vorboerslichen Spielereien, das Hochziehen des Kurses mit gerade einmal 100 Stueck ist sehr bemerkenswert und funktioniert im Moment nicht mehr.

Denkt mal darueber nach,

BL

Da kann man nun in den naechsten Wochen gespannt sein, wurde doch lautstark von der deutschen PR verkuendet das die First Nations fuer das KSM-Projekt wären.

"Public Notice

Environmental Assessment of the Proposed KSM Project - Public Comment Period and Information Sessions

Seabridge Gold Incorporated proposes to develop a combined open-pit and underground gold, copper, silver, and molybdenum mine in the Kerr, Sulphurets, and Mitchell Creek watersheds located about 65 kilometres northwest of Stewart, British Columbia. The proposed KSM Project is expected to process 130,000 tonnes per day of ore over a mine life of up to 55 years.

The KSM Project is subject to review under both the Canadian Environmental Assessment Act and B.C.'s Environmental Assessment Act and is undergoing a cooperative environmental assessment process. ..."

http://www.ceaa-acee.gc.ca/050/document-eng.cfm?document=939…

"Public Notice

Environmental Assessment of the Proposed KSM Project - Public Comment Period and Information Sessions

Seabridge Gold Incorporated proposes to develop a combined open-pit and underground gold, copper, silver, and molybdenum mine in the Kerr, Sulphurets, and Mitchell Creek watersheds located about 65 kilometres northwest of Stewart, British Columbia. The proposed KSM Project is expected to process 130,000 tonnes per day of ore over a mine life of up to 55 years.

The KSM Project is subject to review under both the Canadian Environmental Assessment Act and B.C.'s Environmental Assessment Act and is undergoing a cooperative environmental assessment process. ..."

http://www.ceaa-acee.gc.ca/050/document-eng.cfm?document=939…

Nach den Kaiftipps von vorbestraften Promotern, dem Hochziehen des vorbörslichen Aktienkurses mit wenigen Stuecken, den üblichen Jubelpersern in den Aktien-Boards, den "Spielereien" mit Calls folgt nun der Insider-Abverkauf. Das ist ein bekanntes Muster und ein schöner 6stelliger Betrag fuer einen Fruehstuecksdirektor.

Aug 27/13 Aug 23/13 Dawson, Thomas C. Direct Ownership Common Shares 10 - Disposition in the public market -15,000 $16.79

Quelle: http://canadianinsider.com/node/7?menu_tickersearch=SEA

Denkt mal darueber nach,

BL

Aug 27/13 Aug 23/13 Dawson, Thomas C. Direct Ownership Common Shares 10 - Disposition in the public market -15,000 $16.79

Quelle: http://canadianinsider.com/node/7?menu_tickersearch=SEA

Denkt mal darueber nach,

BL

fyi, SEA Deletion im GDM wahrscheinlich

bzgl. NYSE Arca Gold Miners Index [GDM] Anpassungen (HUI comp.) - Wichtige, anstehende Änderungen

"Key points:

- Today the NYSE Arca Gold Miners Index (GDM), will provide a mock GDM rebalance. Official changes will be announced after the close on Friday September 13th.

- The ETF is going to conduct the entire rebalance in September, likely at/near the close on Friday September 20th.

- Full methodology changes can be seen here: https://indices.nyx.com/sites/indices.nyx.com/files/gdm_inde…

Likely additions: Alacer, Newcrest, Argonaut, Alamos, Franco Nevada, Osisko and Detour.

Likely deletions: Allied Nevada, Vista Gold, Tanzanian Royalty and Golden Star.

Large reweights: Gold Fields, Harmony, B2Gold, New Gold, Eldorado and IAMGOLD.

A full list of potential changes and scale of demand/supply attached (note the addition of Torex is less likely given it is pre-production):

Quelle: NYSE, https://indices.nyx.com/sites/indices.nyx.com/files/gdm_inde…

bzgl. NYSE Arca Gold Miners Index [GDM] Anpassungen (HUI comp.) - Wichtige, anstehende Änderungen

"Key points:

- Today the NYSE Arca Gold Miners Index (GDM), will provide a mock GDM rebalance. Official changes will be announced after the close on Friday September 13th.

- The ETF is going to conduct the entire rebalance in September, likely at/near the close on Friday September 20th.

- Full methodology changes can be seen here: https://indices.nyx.com/sites/indices.nyx.com/files/gdm_inde…

Likely additions: Alacer, Newcrest, Argonaut, Alamos, Franco Nevada, Osisko and Detour.

Likely deletions: Allied Nevada, Vista Gold, Tanzanian Royalty and Golden Star.

Large reweights: Gold Fields, Harmony, B2Gold, New Gold, Eldorado and IAMGOLD.

A full list of potential changes and scale of demand/supply attached (note the addition of Torex is less likely given it is pre-production):

Quelle: NYSE, https://indices.nyx.com/sites/indices.nyx.com/files/gdm_inde…

Was mich im Moment besonders wundert sind die fehlenden CL(Walsh)-Drillings, hatten sie im Mai 2013 noch Bohrergebnisse veroeffentlicht und damit quasi das CL-Projekt fuer die naechsten 10-15 Jahre mehr oder weniger auf Eis gelegt - jedenfalls kann man das nachfolgende Statement so interpretieren - so kommt nun gar nichts mehr von den verbleibenden 19 Löcher. Sofern ich nichts verpasst habe, stehen in etwa 2/3 der Ergebnisse seit Monaten aus. Warum?

"We now have a green light to consider mining the Walsh Lake deposit prior to constructing the processing plant required for the larger FAT deposit. This order of development could have significant economic benefits for the Courageous Lake project as it would generate cash flow to pay for some of the capital costs."

Quelle: http://www.marketwire.com/press-release/seabridge-reports-ex…

"We now have a green light to consider mining the Walsh Lake deposit prior to constructing the processing plant required for the larger FAT deposit. This order of development could have significant economic benefits for the Courageous Lake project as it would generate cash flow to pay for some of the capital costs."

Quelle: http://www.marketwire.com/press-release/seabridge-reports-ex…

seltsam, und wieder hat SA die bessere Performance, allen wund geschriebenen Fingern zum Trotz...

Antwort auf Beitrag Nr.: 45.357.383 von valueinvestor am 30.08.13 14:31:21Wie schätzt du denn die ausbleibenden Bohrergebnisse von Walsh Lake ein und denkst du das eine Walsh-Mine das CL-Projekt finanzieren koennte? Mit welchem Zeitrahmen waere zu rechnen?

Ich habe gerade einmal kurz einen Faktencheck, zwischen der derzeitigen Praesention auf der Seabridge Website und der IST-Situation gemacht.

Quelle: http://www.seabridgegold.net/pdf/FactSheet-1.pdf

--

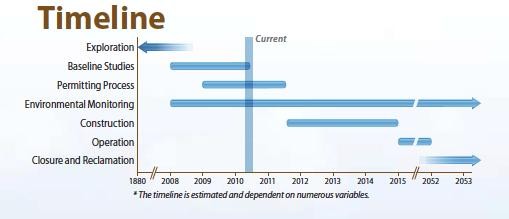

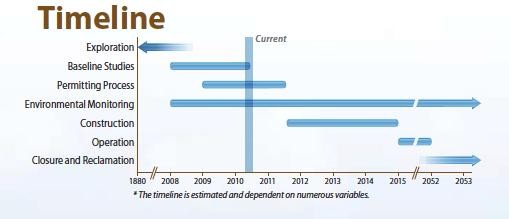

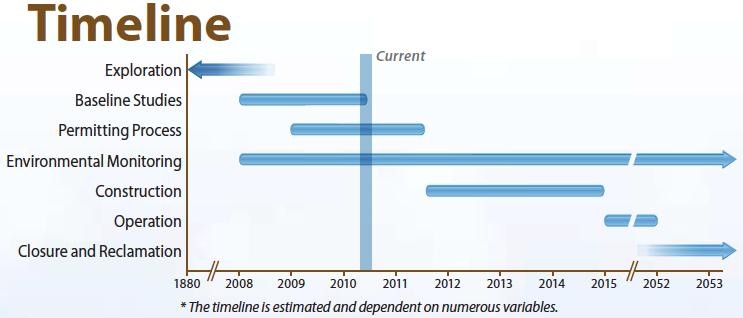

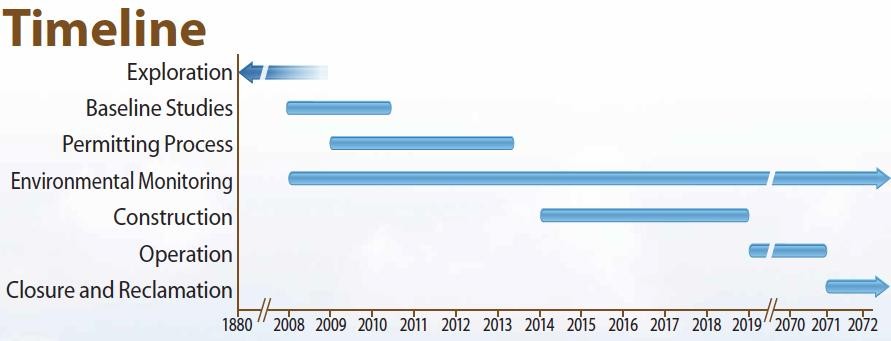

Es ist sehr verwunderlich - sie geben fuer KSM eine wesentlich geringere CAPEX aus (ca. 3 Mrd. Dollar statt ueber 5 Mrd. - vermutlich werden es sogar 7 Mrd. oder mehr) und schreiben" etwas von einer Minenkonstruktion (siehe u.a. Timeline), die 2014 abgeschlossen sein soll.

Alles falsch und ein schoenes Beispiel, wie Explorer Lügen, um unbedarfte Anleger zu ködern. Sehr unschoen ist das.

Quelle: http://www.seabridgegold.net/pdf/FactSheet-1.pdf

--

Es ist sehr verwunderlich - sie geben fuer KSM eine wesentlich geringere CAPEX aus (ca. 3 Mrd. Dollar statt ueber 5 Mrd. - vermutlich werden es sogar 7 Mrd. oder mehr) und schreiben" etwas von einer Minenkonstruktion (siehe u.a. Timeline), die 2014 abgeschlossen sein soll.

Alles falsch und ein schoenes Beispiel, wie Explorer Lügen, um unbedarfte Anleger zu ködern. Sehr unschoen ist das.

!

Dieser Beitrag wurde von m.klemm moderiert. Grund: haltlose Unterstellung

Antwort auf Beitrag Nr.: 45.393.571 von hingucker am 05.09.13 20:00:57Du solltest dich einmal ein wenig entspannen. Ich finde Unternehmenspraesentationen, die mit falschen Zahlen taeuschen, eher unschön. Das ist aber bei Seabridge Gold nicht ungewöhnlich, vor allen Dingen dann nicht, wenn Stockpromoter eingeschaltet werden. Ich erinnere da gerne an die Gletscherluegen der deutschen Promotion Ich sehe da auch weit und breit kein Archiv, die Praesentationen sind u.a. ordentlich durchnummeriert.

Siehe: https://www.google.de/search?q=link:http://www.seabridgegold…

Siehe: https://www.google.de/search?q=link:http://www.seabridgegold…

Antwort auf Beitrag Nr.: 45.395.063 von boersenbrieflemming am 06.09.13 00:39:05Du solltest dich einmal ein wenig entspannen...

Ich bin völlig entspannt und genieße den schönen Spätsommer. Mach dir also keine Gedanken um meinen Gemütszustand. Aber es ist sowieso nur eine deiner üblichen provokativen Floskeln, wenn man dich beim einer Lüge erwischt hat.

Dass du nach wie vor an dieser Lüge festhältst, statt dich wenigstens mit einem Irrtum herauszureden, wundert mich nicht wirklich. Einen Irrtum einzugestehen und um Entschuldigung zu bitten, dass gehört nicht zur Wesensart eines notorischen Lügners.

Nochmal für alle langsam zu mitschreiben.

Du behauptest, die derzeitige (also aktuelle) Präsentation auf der SEA Website enthält als CAPEX für KSM ca. 3 Mrd. Dollar statt der aktuell bereits kommunizierten über 5 Mrd.

Fakt ist:

Auf der HP von Seabridge Gold ist die aktuelle Corporate Presentation unter Investors → Corp. Presentation als PDF abrufbar. Sie wurde und wird ständig aktualisiert. Letztmalig am 1. Sept 2013.

Auf Seite 16 ist die CAPEX mit 5,3 Mrd. US$ ausgewiesen. Dies ist der aktuelle Stand.

Fazit:

Wer seine falschen Behauptungen mit abgelaufenen Dokumenten zu beweisen versucht, die er nur noch mittels Google findet, der lügt ganz bewusst um SEA und seine Investoren zu schädigen.

Ich bin völlig entspannt und genieße den schönen Spätsommer. Mach dir also keine Gedanken um meinen Gemütszustand. Aber es ist sowieso nur eine deiner üblichen provokativen Floskeln, wenn man dich beim einer Lüge erwischt hat.

Dass du nach wie vor an dieser Lüge festhältst, statt dich wenigstens mit einem Irrtum herauszureden, wundert mich nicht wirklich. Einen Irrtum einzugestehen und um Entschuldigung zu bitten, dass gehört nicht zur Wesensart eines notorischen Lügners.

Nochmal für alle langsam zu mitschreiben.

Du behauptest, die derzeitige (also aktuelle) Präsentation auf der SEA Website enthält als CAPEX für KSM ca. 3 Mrd. Dollar statt der aktuell bereits kommunizierten über 5 Mrd.

Fakt ist:

Auf der HP von Seabridge Gold ist die aktuelle Corporate Presentation unter Investors → Corp. Presentation als PDF abrufbar. Sie wurde und wird ständig aktualisiert. Letztmalig am 1. Sept 2013.

Auf Seite 16 ist die CAPEX mit 5,3 Mrd. US$ ausgewiesen. Dies ist der aktuelle Stand.

Fazit:

Wer seine falschen Behauptungen mit abgelaufenen Dokumenten zu beweisen versucht, die er nur noch mittels Google findet, der lügt ganz bewusst um SEA und seine Investoren zu schädigen.

Deine Ausdrucksweise ist zumindest verhaltensoriginell. Ich verorte das einmal in prekäre Lebenssituationen.

Ich möchte an diesem Punkt nicht weiter mit dir diskutieren, dieses Fact Sheet ist nun einmal aktuell online und die Aussagen in dieser Publikation sind grob falsch, sollten diese auf veralteten Daten fussen, dann waere es noch schlimmer, da dann sehr deutlich wird, wie das MM an den eigenen Zielvorgaben vorbeigeschrammt ist und zudem eben noch mit diesen Daten (und optimistischen Annahmen) wirbt.

Denk mal darueber nach,

BL

Ich möchte an diesem Punkt nicht weiter mit dir diskutieren, dieses Fact Sheet ist nun einmal aktuell online und die Aussagen in dieser Publikation sind grob falsch, sollten diese auf veralteten Daten fussen, dann waere es noch schlimmer, da dann sehr deutlich wird, wie das MM an den eigenen Zielvorgaben vorbeigeschrammt ist und zudem eben noch mit diesen Daten (und optimistischen Annahmen) wirbt.

Denk mal darueber nach,

BL

Antwort auf Beitrag Nr.: 45.397.057 von hingucker am 06.09.13 11:19:08Das dieser User hier häufig lügt, ist mittlerweile bekannt, er sollte sich entspannen und wieder einmal Beck anhören.

Themenwechsel:

Die Bürgermeister der umliegenden Gemeinden von KSM sehen immense Vorteile durch einen Bau von KSM:

Seabridge Gold Hosts Tour Of KSM Project For Municipal Officials

Community leaders see benefits for Northwest

Katherine Dow

9/5/2013

Seabridge Gold hosted a tour on Sept.5 of the company's proposed KSM Project for municipal officials from Stewart, Terrace and Smithers. The project, which is still in the environmental assessment faze, would develope a copper-gold mine about 65 kilometers northwest of Stewart.

Elizabeth Miller, the company's environmental affairs manager, says the purpose of the tour was to update community leaders on the project's progress and its promise.

"It really gave us the ability to illustrate the amount of engineering, environmental and technical work that we've been doing on the project site since 2006, and that also gives them the opportunity to communicate to the people within the communities about the work that we've been doing there," she said.

Stewart Mayor Galina Durant says the tour was eye-opening and the project is promising for Stewart residents should it make it through the Environmental Assessment process.

"What it means for us, it means jobs. It means all will ship through our ports, and Seabridge will be looking at Stewart as their shipping destination, which is great," she said via phone from Stewart.

Terrace City Councillor Brian Downie sees similar opportunities not only for his constituents, but for communities throughout the Northwest.

"I expect that residents of Terrace will either be involved in supplying or working in the mining project. I mean, there's a great opportunity there and all of the communities in Northwest BC will see the benefits," he said.

Smithers Mayor Taylor Bachrach echoed Downie's sentiments, saying while the project is relatively far from his municipality, it could still have positive implications for Smithers residents.

"If this project were to go ahead, there would be big employment benefits for Smithers, we would see new residents moving to the area, and all those could be really good things for a community like ours, he said.

Earlier this month, the company signed an agreement in principal with the Nisga'a First Nation, and Miller says they're hoping to form similar relationships with several other First Nations groups that also have traditional land claims. Seabridge will also be visiting individual communities as part of its consultation process.

"There will be open houses in Terrace on October 1st, in Smithers on October 2nd, in Stewart on October 9th and Iskut and Telegraph Creek on September 25 and 26." Miller said.

She added that they expect a decision on the project in about a year's time. Should it be approved, the KSM Project would take about 5 years to construct and have a 52-year minelife expectancy.

http://www.cftktv.com/News/Story.aspx?ID=2036583

Themenwechsel:

Die Bürgermeister der umliegenden Gemeinden von KSM sehen immense Vorteile durch einen Bau von KSM:

Seabridge Gold Hosts Tour Of KSM Project For Municipal Officials

Community leaders see benefits for Northwest

Katherine Dow

9/5/2013

Seabridge Gold hosted a tour on Sept.5 of the company's proposed KSM Project for municipal officials from Stewart, Terrace and Smithers. The project, which is still in the environmental assessment faze, would develope a copper-gold mine about 65 kilometers northwest of Stewart.

Elizabeth Miller, the company's environmental affairs manager, says the purpose of the tour was to update community leaders on the project's progress and its promise.

"It really gave us the ability to illustrate the amount of engineering, environmental and technical work that we've been doing on the project site since 2006, and that also gives them the opportunity to communicate to the people within the communities about the work that we've been doing there," she said.

Stewart Mayor Galina Durant says the tour was eye-opening and the project is promising for Stewart residents should it make it through the Environmental Assessment process.

"What it means for us, it means jobs. It means all will ship through our ports, and Seabridge will be looking at Stewart as their shipping destination, which is great," she said via phone from Stewart.

Terrace City Councillor Brian Downie sees similar opportunities not only for his constituents, but for communities throughout the Northwest.

"I expect that residents of Terrace will either be involved in supplying or working in the mining project. I mean, there's a great opportunity there and all of the communities in Northwest BC will see the benefits," he said.

Smithers Mayor Taylor Bachrach echoed Downie's sentiments, saying while the project is relatively far from his municipality, it could still have positive implications for Smithers residents.

"If this project were to go ahead, there would be big employment benefits for Smithers, we would see new residents moving to the area, and all those could be really good things for a community like ours, he said.

Earlier this month, the company signed an agreement in principal with the Nisga'a First Nation, and Miller says they're hoping to form similar relationships with several other First Nations groups that also have traditional land claims. Seabridge will also be visiting individual communities as part of its consultation process.

"There will be open houses in Terrace on October 1st, in Smithers on October 2nd, in Stewart on October 9th and Iskut and Telegraph Creek on September 25 and 26." Miller said.

She added that they expect a decision on the project in about a year's time. Should it be approved, the KSM Project would take about 5 years to construct and have a 52-year minelife expectancy.

http://www.cftktv.com/News/Story.aspx?ID=2036583

"It means all will ship through our ports, and Seabridge will be looking at Stewart as their shipping destination, which is great," she said via phone from Stewart."

(siehe "Hafen"-Bild)

Das wuerde Investitionen weiterer Dollar-Mrd. bedeuten, in keiner Seabridge PFS ausgewiesen (ebenspowenig wie das partielle Entfernen des Gletschers). Auch Kosten, die in einer Machbarkeitsstudie (FS) ausgewiesen werden müssten, doch die kommt wohl nicht mehr. Ich erhoehe meine CAPEX-Schaetzung nun auf 9-12 Mrd.

Denkt mal darueber nach,

BL

(siehe "Hafen"-Bild)Das wuerde Investitionen weiterer Dollar-Mrd. bedeuten, in keiner Seabridge PFS ausgewiesen (ebenspowenig wie das partielle Entfernen des Gletschers). Auch Kosten, die in einer Machbarkeitsstudie (FS) ausgewiesen werden müssten, doch die kommt wohl nicht mehr. Ich erhoehe meine CAPEX-Schaetzung nun auf 9-12 Mrd.

Denkt mal darueber nach,

BL

signed an agreement in principal with the Nisga'a First Nation

Die Liste der "concerns" ist die laengste Auflistung, die ich je bei einem Projekt gefunden habe. Das Agreement in Principal loest da praktisch gar nichts, sondern sagt mehr oder weniger nur aus, dass hier nun - nach massiven "Spenden" ueberhaupt erst eine gewisse Verhandlungsbereitschaft besteht.

Denk mal darueber nach,

BL

Die Liste der "concerns" ist die laengste Auflistung, die ich je bei einem Projekt gefunden habe. Das Agreement in Principal loest da praktisch gar nichts, sondern sagt mehr oder weniger nur aus, dass hier nun - nach massiven "Spenden" ueberhaupt erst eine gewisse Verhandlungsbereitschaft besteht.

Denk mal darueber nach,

BL

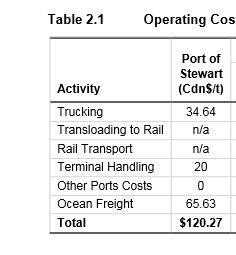

Über den Bulk Terminal wurde schon die Granduc Produktion von Newmont verladen, die Infrastruktur ist da.

Zu CL würde ich jetzt eine Ressourcenschätzung in Q3 oder Q4 erwarten.

Wesentlich war die News vom Mai:

(Seabridge Gold reported today that the first round of metallurgical tests on material from the new Walsh Lake deposit at its 100%-owned Courageous Lake project confirm high gold recoveries from conventional, direct ore cyanidation.)

Das bedeutet, eine Ausbeutung von Walsh Lake könnte vorangeschaltet werden und mit dem Cash Flow das teurere Autoklavverfahren für das Fat Deposit vorfinanzieren helfen.

Zu CL würde ich jetzt eine Ressourcenschätzung in Q3 oder Q4 erwarten.

Wesentlich war die News vom Mai:

(Seabridge Gold reported today that the first round of metallurgical tests on material from the new Walsh Lake deposit at its 100%-owned Courageous Lake project confirm high gold recoveries from conventional, direct ore cyanidation.)

Das bedeutet, eine Ausbeutung von Walsh Lake könnte vorangeschaltet werden und mit dem Cash Flow das teurere Autoklavverfahren für das Fat Deposit vorfinanzieren helfen.

die Infrastruktur ist da

Du hast wirklich Humor.

P.S. Die Projekt-Website wurde schon abgeschaltet.

http://investnorthwestbc.ca/major-projects-and-investment-op…

CL:

Was mich im Moment besonders wundert sind die fehlenden CL(Walsh)-Drillings, hatten sie im Mai 2013 noch Bohrergebnisse veroeffentlicht und damit quasi das CL-Projekt fuer die naechsten 10-15 Jahre mehr oder weniger auf Eis gelegt - jedenfalls kann man das nachfolgende Statement so interpretieren - so kommt nun gar nichts mehr von den verbleibenden 19 Löcher. Sofern ich nichts verpasst habe, stehen in etwa 2/3 der Ergebnisse seit Monaten aus. Warum?

Du hast wirklich Humor.

P.S. Die Projekt-Website wurde schon abgeschaltet.

http://investnorthwestbc.ca/major-projects-and-investment-op…

CL:

Was mich im Moment besonders wundert sind die fehlenden CL(Walsh)-Drillings, hatten sie im Mai 2013 noch Bohrergebnisse veroeffentlicht und damit quasi das CL-Projekt fuer die naechsten 10-15 Jahre mehr oder weniger auf Eis gelegt - jedenfalls kann man das nachfolgende Statement so interpretieren - so kommt nun gar nichts mehr von den verbleibenden 19 Löcher. Sofern ich nichts verpasst habe, stehen in etwa 2/3 der Ergebnisse seit Monaten aus. Warum?

die Infrastruktur ist da

Kleine Ergaenzung, der kleine, alte Terminal ist im Wesentlichen dicht (z.B. durch Vertraege mit Imerial Mineral bis 2021).

Bei der PFS wurde nicht beruecksichtigt das hier sehr hohe Kosten fuer die Ausweitung der Infrastruktur anfallen (falls ueberhaupt moeglich).

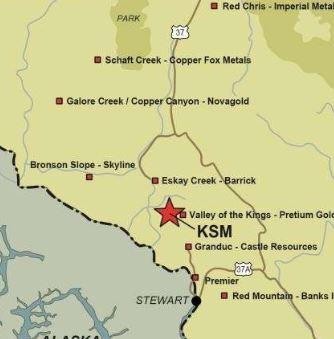

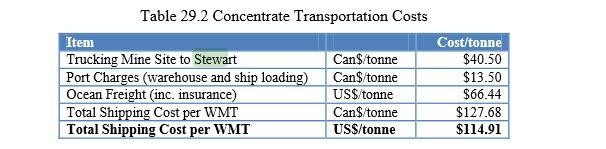

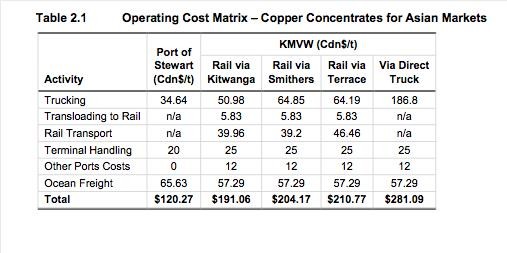

Der Copper-Concentrate Transport fuer den asiatischen Markt duerfte ca. C$300 Dollar/t kosten (ohne Rail, mittels Trucks). Unabhaengig von der fehlenden Metallurgie (handelt es sich ueberhaupt um ein marktfaehiges Produkt?), waeren die Transportkosten immens - man mag das ruhig im Hinblick auf 300.000 t Konzentrat berechnen.

Auch hier fehlt es an Infrastruktur, da die schmale "Nass River Bridge" nicht fuer einen Trucktransport (single lane bridge) ausgelegt ist.

Weitgehend unklar ist es, wie die das Mining -und Konstruktionsequipment ueberhaupt zu den jeweiligen Einsatzgebieten kommt (diese weit entfernten Taeler, Gletscher und Berge)

Quelle: http://www.ceaa-acee.gc.ca/050/documents_staticpost/49262/89…

Kleine Ergaenzung, der kleine, alte Terminal ist im Wesentlichen dicht (z.B. durch Vertraege mit Imerial Mineral bis 2021).

Bei der PFS wurde nicht beruecksichtigt das hier sehr hohe Kosten fuer die Ausweitung der Infrastruktur anfallen (falls ueberhaupt moeglich).

Der Copper-Concentrate Transport fuer den asiatischen Markt duerfte ca. C$300 Dollar/t kosten (ohne Rail, mittels Trucks). Unabhaengig von der fehlenden Metallurgie (handelt es sich ueberhaupt um ein marktfaehiges Produkt?), waeren die Transportkosten immens - man mag das ruhig im Hinblick auf 300.000 t Konzentrat berechnen.

Auch hier fehlt es an Infrastruktur, da die schmale "Nass River Bridge" nicht fuer einen Trucktransport (single lane bridge) ausgelegt ist.

Weitgehend unklar ist es, wie die das Mining -und Konstruktionsequipment ueberhaupt zu den jeweiligen Einsatzgebieten kommt (diese weit entfernten Taeler, Gletscher und Berge)

Quelle: http://www.ceaa-acee.gc.ca/050/documents_staticpost/49262/89…

sehr schön!

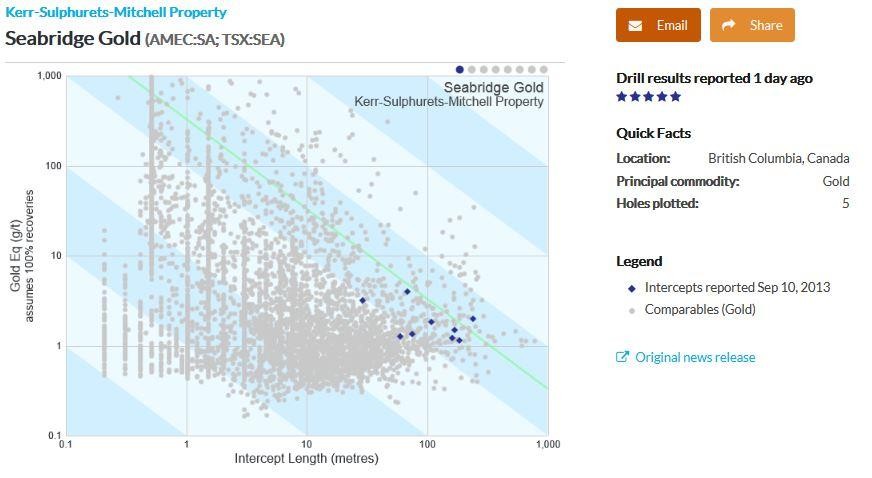

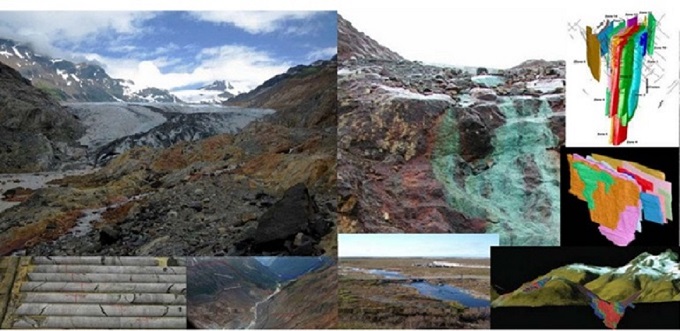

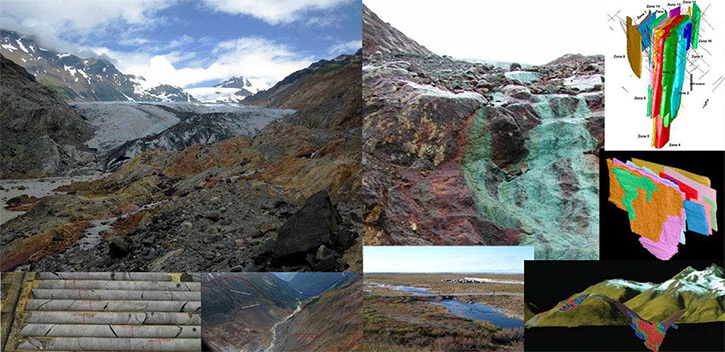

Seabridge Gold Intercepts Rich Bornite Zone at KSM Project

Grade continues to rise as drilling on Deep Kerr Core Zone intersects 69 meters of 1.78% copper and 1.14 g/T gold

TORONTO, CANADA, Sep 10, 2013 (Marketwired via COMTEX) -- Seabridge Gold CA:SEA -2.36% SA -2.24% announced today that new drilling has found an exceptional bornite-rich zone within the higher-grade Deep Kerr core zone on its 100% owned KSM project in north western British Columbia, Canada. Bornite is a copper mineral generally formed at higher temperatures within a core zone and is typically found in larger, higher-grade copper deposits.

As announced on August 12, 2013, Seabridge has discovered a higher-grade copper-gold core zone named Deep Kerr which lies beneath the Kerr porphyry deposit. Wide-spaced drilling has established that Deep Kerr is at least 1600 meters long and remains open to the north and at depth. The mineralized envelope thus far is up to 300 meters in width consisting primarily of chalcopyrite (a copper mineral) and gold. Within this envelope, wide bornite-rich intervals have now been intersected in stockwork veins with abundant chalcopyrite and other minor copper minerals as well as high gold values. The first of these bornite intercepts to be assayed contains the highest grade copper mineralization ever drilled at KSM. Wall rock in these intervals is intensely altered; the style of alteration and mineralization are characteristic of a deep, high temperature core zone targeted by Seabridge in this year's program.

Seabridge Chairman and CEO Rudi Fronk noted that "the discovery of abundant bornite was near the top of this year's exploration wish list because it typically brings higher grades of both copper and gold. We are now focused on expanding the bornite zone and finding where its expression is strongest. We are gratified to see that the bornite zone appears at moderate depths within Deep Kerr, indicating that this material could be accessed from the valley floor," Fronk said.

"Drilling at Deep Kerr is continuing on schedule with five core rigs. This is a very large target. Drill hole locations are therefore being confined to a thousand meters of strike length to facilitate an initial resource estimate later this year. An assessment of the overall size of Deep Kerr will need to wait for next year. A sixth core rig has been added to the current program and is now at Iron Cap where the first three holes that we drilled this year indicate the potential for another high-grade core zone discovery." (See August 20, 2013 news release on Iron Cap).

2013 drilling at Deep Kerr is employing state-of-the-art directional drilling tools that enable a process known as wedging, in which additional holes are started part way down a previously drilled hole. The directional tools ensure that the new hole deviates from the first in a predictable manner so as to provide another intercept of the target at least 75 meters from the original intercept, thereby generating new information to be used in calculating an initial resource estimate for Deep Kerr. This technology significantly reduces the amount of drilling required to achieve a new intercept of the target zone as the top 500 to 800 meters of the hole does not have to be redrilled. The above reported drill holes with a letter designation after the hole number represent wedged drill holes completed from holes that have been previously reported (i.e. K-13-23 and K-13-24). Drill hole K-13-23A wedged from K-13-23 at 547 meters. Hole K-13-24A was wedged at 608 meters and K-24-B at 524 meters from K-13-24.

The above reported drill holes were designed to intersect mineralized zones as close as technically feasible to a perpendicular angle to their strike. Therefore, the true widths of this mineralization are believed to be at least 75% of the reported intercepts. (For a drill location map and cross sections of the Deep Kerr, see www.seabridgegold.net/DKmap2.pdf. For photos of bornite-rich drill core see www.seabridgegold.net/bornitecore.pdf).

http://www.marketwatch.com/story/seabridge-gold-intercepts-r…

Seabridge Gold Intercepts Rich Bornite Zone at KSM Project

Grade continues to rise as drilling on Deep Kerr Core Zone intersects 69 meters of 1.78% copper and 1.14 g/T gold

TORONTO, CANADA, Sep 10, 2013 (Marketwired via COMTEX) -- Seabridge Gold CA:SEA -2.36% SA -2.24% announced today that new drilling has found an exceptional bornite-rich zone within the higher-grade Deep Kerr core zone on its 100% owned KSM project in north western British Columbia, Canada. Bornite is a copper mineral generally formed at higher temperatures within a core zone and is typically found in larger, higher-grade copper deposits.

As announced on August 12, 2013, Seabridge has discovered a higher-grade copper-gold core zone named Deep Kerr which lies beneath the Kerr porphyry deposit. Wide-spaced drilling has established that Deep Kerr is at least 1600 meters long and remains open to the north and at depth. The mineralized envelope thus far is up to 300 meters in width consisting primarily of chalcopyrite (a copper mineral) and gold. Within this envelope, wide bornite-rich intervals have now been intersected in stockwork veins with abundant chalcopyrite and other minor copper minerals as well as high gold values. The first of these bornite intercepts to be assayed contains the highest grade copper mineralization ever drilled at KSM. Wall rock in these intervals is intensely altered; the style of alteration and mineralization are characteristic of a deep, high temperature core zone targeted by Seabridge in this year's program.

Seabridge Chairman and CEO Rudi Fronk noted that "the discovery of abundant bornite was near the top of this year's exploration wish list because it typically brings higher grades of both copper and gold. We are now focused on expanding the bornite zone and finding where its expression is strongest. We are gratified to see that the bornite zone appears at moderate depths within Deep Kerr, indicating that this material could be accessed from the valley floor," Fronk said.

"Drilling at Deep Kerr is continuing on schedule with five core rigs. This is a very large target. Drill hole locations are therefore being confined to a thousand meters of strike length to facilitate an initial resource estimate later this year. An assessment of the overall size of Deep Kerr will need to wait for next year. A sixth core rig has been added to the current program and is now at Iron Cap where the first three holes that we drilled this year indicate the potential for another high-grade core zone discovery." (See August 20, 2013 news release on Iron Cap).

-----------------------------------------------------------------------

-----

Total Gold Copper Silver

Depth From To Thickness Grade Grade Grade

Hole ID (meters) (meters) (meters) (meters) (g/T) (%) (g/T)

----------------------------------------------------------------------------

K-13-23A 1368 823.4 1007.8 184.4 0.21 0.56 2.11

----------------------------------------------------------------------------

K-13-24A 1206 791.0 952.0 161.0 0.38 0.51 1.97

--------------------------------------------------------

1080.4 1139.6 59.2 0.26 0.62 1.26

----------------------------------------------------------------------------

K-13-24B 1155 762.0 931.0 169.0 0.50 0.59 2.34

--------------------------------------------------------

1027 1102 75 0.41 0.57 1.22

----------------------------------------------------------------------------

K-13-28 1340 710.0 739.1 29.1 2.04 0.60 11.63

--------------------------------------------------------

904.0 1012.4 108.4 0.59 0.75 3.23

----------------------------------------------------------------------------

K-13-29 993 572.4 810.4 238.0 0.55 0.89 1.39

--------------------------------------------------------

including 641.7 710.4 68.7 1.14 1.78 2.06

----------------------------------------------------------------------------

2013 drilling at Deep Kerr is employing state-of-the-art directional drilling tools that enable a process known as wedging, in which additional holes are started part way down a previously drilled hole. The directional tools ensure that the new hole deviates from the first in a predictable manner so as to provide another intercept of the target at least 75 meters from the original intercept, thereby generating new information to be used in calculating an initial resource estimate for Deep Kerr. This technology significantly reduces the amount of drilling required to achieve a new intercept of the target zone as the top 500 to 800 meters of the hole does not have to be redrilled. The above reported drill holes with a letter designation after the hole number represent wedged drill holes completed from holes that have been previously reported (i.e. K-13-23 and K-13-24). Drill hole K-13-23A wedged from K-13-23 at 547 meters. Hole K-13-24A was wedged at 608 meters and K-24-B at 524 meters from K-13-24.

The above reported drill holes were designed to intersect mineralized zones as close as technically feasible to a perpendicular angle to their strike. Therefore, the true widths of this mineralization are believed to be at least 75% of the reported intercepts. (For a drill location map and cross sections of the Deep Kerr, see www.seabridgegold.net/DKmap2.pdf. For photos of bornite-rich drill core see www.seabridgegold.net/bornitecore.pdf).

http://www.marketwatch.com/story/seabridge-gold-intercepts-r…

Bohrtiefen.

Antwort auf Beitrag Nr.: 45.418.997 von boersenbrieflemming am 10.09.13 13:54:46Morphologie!

Zugang über den Talboden.

Zugang über den Talboden.

69 meters of 1.78% copper and 1.14 g/T gold

kurze Berechnungen hierzu:

Wert über 180$ je Tonne

Kupferäquivalent: 2,5%

Goldäquivalent 4,09g je Tonne

Within this envelope, wide bornite-rich intervals have now been intersected in stockwork veins with abundant chalcopyrite and other minor copper minerals as well as high gold values. The first of these bornite intercepts to be assayed contains the highest grade copper mineralization ever drilled at KSM.

Man hat also schon jetzt an mehreren Bohrkernen bornitreiche Abschnitte entdeckt und in dieser news von einem ersten die Labordaten erhalten, es werden nun noch weitere Abschnitte folgen.

The bornite was evident in core photos Seabridge released Tuesday morning (example above), showing a mixture of chalcopyrite (bronzish in colour) and the blue-black bornite.

kurze Berechnungen hierzu:

Wert über 180$ je Tonne

Kupferäquivalent: 2,5%

Goldäquivalent 4,09g je Tonne

Within this envelope, wide bornite-rich intervals have now been intersected in stockwork veins with abundant chalcopyrite and other minor copper minerals as well as high gold values. The first of these bornite intercepts to be assayed contains the highest grade copper mineralization ever drilled at KSM.

Man hat also schon jetzt an mehreren Bohrkernen bornitreiche Abschnitte entdeckt und in dieser news von einem ersten die Labordaten erhalten, es werden nun noch weitere Abschnitte folgen.

The bornite was evident in core photos Seabridge released Tuesday morning (example above), showing a mixture of chalcopyrite (bronzish in colour) and the blue-black bornite.

Antwort auf Beitrag Nr.: 45.419.433 von valueinvestor am 10.09.13 14:50:06Die Reaktion des Marktes entspricht meinen Erwartungen: SA 12.9016 -0.6884 -5.1%

Antwort auf Beitrag Nr.: 45.419.815 von valueinvestor am 10.09.13 15:36:14chalcopyrite

Jetzt koimmen sie schon mit Katzengold. Das wird immer bizarrer.

Jetzt koimmen sie schon mit Katzengold. Das wird immer bizarrer.

Zitat von boersenbrieflemming: chalcopyrite

Jetzt koimmen sie schon mit Katzengold. Das wird immer bizarrer.

Die Lügendichte dieses Users steigt gewaltig an:

Chalcopyrit ist mitnichten Katzengold.

Chalkopyrit hat die Formel CuFeS2

Katzengold hingegen ist der volkstümliche Name von Pyrit mit der Formel FeS2.

Antwort auf Beitrag Nr.: 45.420.877 von valueinvestor am 10.09.13 17:28:56Lügendichte dieses Users

Du (seabridgegold@xxx.xx) solltest eher weniger das Wort Luege in den Mund zu nehmen.

Ich bezog mich auf folgenden Artikel:

Chalcopyrit

"Narren- o. Katzengold"

http://www.edelsteine.at/lexikon/chalcopyrit/

Narrengold

Du (seabridgegold@xxx.xx) solltest eher weniger das Wort Luege in den Mund zu nehmen.

Ich bezog mich auf folgenden Artikel:

Chalcopyrit

"Narren- o. Katzengold"

http://www.edelsteine.at/lexikon/chalcopyrit/

Narrengold

auch der Bezug auf irgendwelche albernen Seiten kann dich hier nicht exculpieren. Als vorgeblicher Explorationsexperte ist die mutwillige Verwechslung von Pyrit und Chalkopyrit kein Kavaliersdelikt.

Antwort auf Beitrag Nr.: 45.421.479 von valueinvestor am 10.09.13 18:29:43Nun, jahrelang von HighGrades (wie Brucejack) zu schwadronieren , dann nicht derartiges zu finden und statt sichtbarem Gold nun dem unbearften Anleger Narrengold zu zeigen, dass ist schon witzig.

Fronk:

"...the discovery of abundant bornite was near the top of this year's exploration wish list"

So funktioniert dann das Marketing sie zeigen Narrengold und versuchen es als sichtbares Gold zu verkaufen:

"The article has a link to actual pictures of the rock that was drilled, You can see the gold in the rock."

Quelle: http://finance.yahoo.com/mbview/threadview/;_ylt=AmjQeMMab5w…

"The article has a link to actual pictures of the rock that was drilled, You can see the gold in the rock."

Quelle: http://finance.yahoo.com/mbview/threadview/;_ylt=AmjQeMMab5w…

man sieht hier sehr gut, dass es nur selten Intervalle dieser Grade gibt.

Ich bin wirklich gespamnnt, wie die anderen Bornit-Abschnitte herauskommen.

Ich bin wirklich gespamnnt, wie die anderen Bornit-Abschnitte herauskommen.

Die letzten Ergebnisse wuerden fuer einen Explorer mit einer MK von vielleicht 7-10 Mio. Dollar noch fuer eine Spekulationsmoeglichkeit sorgen und auch nur sehr bedingt, da man die Bohrtiefe im Blick haben sollte.

Seabridge eine MK von rund $600 Mio. und seit Gruendung der Company 1999 bisher keine Aussicht auf einen wirtschaftlichen Abbau, keine Machbarkeitsstudie in Sicht, keine Bulk Samples - hier werden nur bestaendig neue Saeue durch das Dorf gehetzt. Mit immer weniger Erfolg ...

Beim Ressourcenschaetzer Lechner, der als Einzelperson sich fuer die geschätzten Ressourcen (und deren raketenhafte Erweiterung) verantwortlich zeichnet, ist mir zudem aufgefallen das man ihn nach den Schaetzkatastrophen bei keinem groesseren Projekt mehr findet - nur Seabridge Gold.

Ich sehe noch erhebliches Abwaertspotential und sehe in einem Jahr eher 8 als 18 Dollar.

Die letzten Ergebnisse wuerden fuer einen Explorer mit einer MK von vielleicht 7-10 Mio. Dollar noch fuer eine Spekulationsmoeglichkeit sorgen und auch nur sehr bedingt, da man die Bohrtiefe im Blick haben sollte.

Seabridge eine MK von rund $600 Mio. und seit Gruendung der Company 1999 bisher keine Aussicht auf einen wirtschaftlichen Abbau, keine Machbarkeitsstudie in Sicht, keine Bulk Samples - hier werden nur bestaendig neue Saeue durch das Dorf gehetzt. Mit immer weniger Erfolg ...

Beim Ressourcenschaetzer Lechner, der als Einzelperson sich fuer die geschätzten Ressourcen (und deren raketenhafte Erweiterung) verantwortlich zeichnet, ist mir zudem aufgefallen das man ihn nach den Schaetzkatastrophen bei keinem groesseren Projekt mehr findet - nur Seabridge Gold.

Ich sehe noch erhebliches Abwaertspotential und sehe in einem Jahr eher 8 als 18 Dollar.

Kennst du außer Reservoir vielleicht einen Explorer, der jüngst über 70 Meter 2,5% Kupfer oder 4 Gramm Gold nachgewiesen hätte? Dies ist eine beachtliche Entdeckung, zumal jegliche Investition zum Abbau über die bereits vorhandenen Reserven gedeckt ist.

Bei der Bohrtiefe solltest du die Geländemorphologie berücksichtigen sowie die Tatsache, dass die Bohrlöcher nicht senkrecht sondern in dem Winkel niedergebracht werden, der für die Abschätzunmg der Ressourcen am besten geeignet ist. Um die Tiefe unter der Berghöhe von Kerr zu ermitteln, müsstest du Rechnungen mit der Sinusfunktion durchführen - ich weiß nicht, ob du so etwas kannst. Jedoch sind die mieralisierten Abschnitte eindeutig über den Talboden des Sulphurets Tals zu erreichen.

Our first priority is to generate a high quality resource for Deep Kerr which could have a very significant economic impact on the KSM project particularly if it proves to be accessible from the Sulphurets valley floor by way of an inclined tunnel.

http://www.seabridgegold.net/News/Article/406/seabridge-gold…

und:

This is a very large target. Drill hole locations are therefore being confined to a thousand meters of strike length to facilitate an initial resource estimate later this year. An assessment of the overall size of Deep Kerr will need to wait for next year.

1.000 Meter strike length - das wird richtig groß!

Bei der Bohrtiefe solltest du die Geländemorphologie berücksichtigen sowie die Tatsache, dass die Bohrlöcher nicht senkrecht sondern in dem Winkel niedergebracht werden, der für die Abschätzunmg der Ressourcen am besten geeignet ist. Um die Tiefe unter der Berghöhe von Kerr zu ermitteln, müsstest du Rechnungen mit der Sinusfunktion durchführen - ich weiß nicht, ob du so etwas kannst. Jedoch sind die mieralisierten Abschnitte eindeutig über den Talboden des Sulphurets Tals zu erreichen.

Our first priority is to generate a high quality resource for Deep Kerr which could have a very significant economic impact on the KSM project particularly if it proves to be accessible from the Sulphurets valley floor by way of an inclined tunnel.

http://www.seabridgegold.net/News/Article/406/seabridge-gold…

und:

This is a very large target. Drill hole locations are therefore being confined to a thousand meters of strike length to facilitate an initial resource estimate later this year. An assessment of the overall size of Deep Kerr will need to wait for next year.

1.000 Meter strike length - das wird richtig groß!

2,5% Kupfer oder 4 Gramm Gold nachgewiesen hätte

Haben Sie ja auch nicht. Du rechnest vermutlich Aequivalenten schön, das fuehrt zusaetzlich in die Irre. Diese Grade sind bei der schlechten Labor-Metallurgie (das was bisher in rudimentaerer Form vorliegt) ... ein Witz. Ich fand die Ergebnisse fuer die Bohrtiefe (und den damit verbundenen Aufwand) nicht besonders aufregend. Fuer einen minderkapitalisierten Explorer waere das ganz nett - mehr aber auch nicht.

Sie haben ja versucht einem im Rahmen einer PEA einen Produktionsplan zu erstellen, der muesste komplett umgestellt werden. Das wird vermutlich auch geschehen, wenn das Explorationsziel nicht erreicht werden kann. Dargestelltes Katzen, -oder Narrengold ersetzt halt kein sichtbares Gold und sie sind weiter von einer Machbarkeitsstudie entfernt den je.

Wir werden zusehen können, wie jetzt die Marketingtrommel weiter geruehrt wird. Es wird viel Geld benötigt, alleine schon fuer den Erwerb notwendiger Rechte.

Denk mal darueber nach,

BL

Haben Sie ja auch nicht. Du rechnest vermutlich Aequivalenten schön, das fuehrt zusaetzlich in die Irre. Diese Grade sind bei der schlechten Labor-Metallurgie (das was bisher in rudimentaerer Form vorliegt) ... ein Witz. Ich fand die Ergebnisse fuer die Bohrtiefe (und den damit verbundenen Aufwand) nicht besonders aufregend. Fuer einen minderkapitalisierten Explorer waere das ganz nett - mehr aber auch nicht.

Sie haben ja versucht einem im Rahmen einer PEA einen Produktionsplan zu erstellen, der muesste komplett umgestellt werden. Das wird vermutlich auch geschehen, wenn das Explorationsziel nicht erreicht werden kann. Dargestelltes Katzen, -oder Narrengold ersetzt halt kein sichtbares Gold und sie sind weiter von einer Machbarkeitsstudie entfernt den je.

Wir werden zusehen können, wie jetzt die Marketingtrommel weiter geruehrt wird. Es wird viel Geld benötigt, alleine schon fuer den Erwerb notwendiger Rechte.

Denk mal darueber nach,

BL

Seabridge finds high-grade core zones underneath two of KSM's porphyries -

(...)

Those holes returned what Seabridge described as "favorable markers, characteristic of core zones", along with the copper grades that a core zone should carry. Hole 12-21, for example, returned 473 metres grading 0.9% copper, along with 0.31 gram gold per tonne and 3.7 grams silver per tonne. KSM's measured and indicated resources bear an average copper grade of just 0.21%.

With those results Seabridge's primary exploration goal in 2013 became a "core zone discovery at Deep Kerr". To that, the company returned to Kerr with five drill rigs and those rigs have produced several intervals grading better than 1% copper and 1.7 grams gold.

The results confirmed the presence of the sought-after core zone at Deep Kerr. Seabridge has the zone tracked along 1,600 metres strike and across 300 metres width; it remains open to the north and at depth. Mineralization in the core consists primarily of chalcopyrite and gold, but in its latest holes Seabridge has encountered wide intervals of stockwork veining carrying abundant bornite.

Bornite is a copper-iron-sulphide mineral that generally forms at higher temperatures than its counterpart chalcopyrite, the most common copper mineral. Importantly, each bornite molecule has five copper atoms, compared to just one in each chalcopyrite. As a result, bornite-bearing ores carry higher copper grades.

For example, the Deep Kerr intercept from hole 29 carried 0.55 gram gold, 0.89% copper, and 1.39 grams silver over 238 metres, but a bornite-rich segment graded 1.14 grams gold, 1.78% copper, and 2.06 grams silver over 69 metres.

"The first of these bornite intercepts to be assayed contains the highest grade copper mineralization ever drilled at KSM," said Seabridge. "Wall rock in these intervals is intensely altered; the style of alternation and mineralization are characteristic of a deep, high-temperature core zone as targeted by Seabridge in this year's program."

The zone represents a very large target, so Seabridge chairman and CEO Rudy Fronk says they are confining their drills to a 1000-metre section. That will provide drill data of sufficient density to inform an initial resource estimate, due out later this year. Next year Fronk says drills will step out farther and assess the overall size of Deep Kerr.

Nevertheless, Seabridge is already contemplating how Deep Kerr might fit into the KSM mine plan. The bornite zone "…appears at moderate depths within Deep Kerr, indicating that this material could be accessed from the valley floor." That is important, because if high-grade material from Kerr could enhance KSM's economics in the mine's early years Seabridge would likely take its production plan back to the drawing board.

http://www.northernminer.com/news/seabridge-finds-high-grade…

(...)

Those holes returned what Seabridge described as "favorable markers, characteristic of core zones", along with the copper grades that a core zone should carry. Hole 12-21, for example, returned 473 metres grading 0.9% copper, along with 0.31 gram gold per tonne and 3.7 grams silver per tonne. KSM's measured and indicated resources bear an average copper grade of just 0.21%.

With those results Seabridge's primary exploration goal in 2013 became a "core zone discovery at Deep Kerr". To that, the company returned to Kerr with five drill rigs and those rigs have produced several intervals grading better than 1% copper and 1.7 grams gold.

The results confirmed the presence of the sought-after core zone at Deep Kerr. Seabridge has the zone tracked along 1,600 metres strike and across 300 metres width; it remains open to the north and at depth. Mineralization in the core consists primarily of chalcopyrite and gold, but in its latest holes Seabridge has encountered wide intervals of stockwork veining carrying abundant bornite.

Bornite is a copper-iron-sulphide mineral that generally forms at higher temperatures than its counterpart chalcopyrite, the most common copper mineral. Importantly, each bornite molecule has five copper atoms, compared to just one in each chalcopyrite. As a result, bornite-bearing ores carry higher copper grades.

For example, the Deep Kerr intercept from hole 29 carried 0.55 gram gold, 0.89% copper, and 1.39 grams silver over 238 metres, but a bornite-rich segment graded 1.14 grams gold, 1.78% copper, and 2.06 grams silver over 69 metres.

"The first of these bornite intercepts to be assayed contains the highest grade copper mineralization ever drilled at KSM," said Seabridge. "Wall rock in these intervals is intensely altered; the style of alternation and mineralization are characteristic of a deep, high-temperature core zone as targeted by Seabridge in this year's program."

The zone represents a very large target, so Seabridge chairman and CEO Rudy Fronk says they are confining their drills to a 1000-metre section. That will provide drill data of sufficient density to inform an initial resource estimate, due out later this year. Next year Fronk says drills will step out farther and assess the overall size of Deep Kerr.

Nevertheless, Seabridge is already contemplating how Deep Kerr might fit into the KSM mine plan. The bornite zone "…appears at moderate depths within Deep Kerr, indicating that this material could be accessed from the valley floor." That is important, because if high-grade material from Kerr could enhance KSM's economics in the mine's early years Seabridge would likely take its production plan back to the drawing board.

http://www.northernminer.com/news/seabridge-finds-high-grade…

Antwort auf Beitrag Nr.: 45.437.067 von valueinvestor am 12.09.13 16:20:04would likely take its production plan back to the drawing board.

Bei Ressourcen mit Bereichen von 180$ die Tonne machen die das sicher gerne und mich als Aktionär feut das auch.

"mich als Aktionär feut das auch"

Ja, ja .... "now this is big fun" (bei ca. 17 USD) etc.pp- das batten wir alles schon. Vielleicht sollten sie einen Online-Versandhandel fuer Narrengold aufziehen.

Ja, ja .... "now this is big fun" (bei ca. 17 USD) etc.pp- das batten wir alles schon. Vielleicht sollten sie einen Online-Versandhandel fuer Narrengold aufziehen.

Der Markt honoriert die Anstrengungen alles schoen aussehen zu lassen nicht.

12.95 SA -0.56 USD -4.1% 631.1k

12.95 SA -0.56 USD -4.1% 631.1k

Mit dem gelobten Projekt Grassy Mountain konnte beim "Verkauf" kein Geld erzielt werden und nun wird versucht das Schlimmste zu verhindern. Wenn ich daran denke wie Fronk vor noch nicht einmal einem Jahr behauptet hat hier nun mindestens 30 Mio. Dollar zusaetzlich einnehmen zu können ... was fuer eine Anlegerverar******.

Seabridge Gold Acquires an Additional 1,671,000 Common Shares of Calico Resources Corp. Upon Exercise of Special Warrants

The Acquired Shares were issued in a private transaction.

http://www.marketwire.com/press-release/seabridge-gold-acqui…

--

@value du (seabridgegold@xxx.xx) hast doch Calico sehr stark beworben hier bei WO (da stsand die Aktie noch bei ca. 60 Cent, nun sind es 9 Cent), warum machst du dich in dem von dir betreuten Thread so rar?

Seabridge Gold Acquires an Additional 1,671,000 Common Shares of Calico Resources Corp. Upon Exercise of Special Warrants

The Acquired Shares were issued in a private transaction.

http://www.marketwire.com/press-release/seabridge-gold-acqui…

--

@value du (seabridgegold@xxx.xx) hast doch Calico sehr stark beworben hier bei WO (da stsand die Aktie noch bei ca. 60 Cent, nun sind es 9 Cent), warum machst du dich in dem von dir betreuten Thread so rar?

ein paar Charts:

Sea im Verfgleich der letzten drei Monate mit den drei Indices Gold Miners, Goldminer Juniors und Explorer:

Sea in der Erholung deutlich besser

gleiche Vergleichsgruppe mit dem desaströsen letzten Jahr - Sea deutlich besser.

Nun die gleichen Zeiträume mit der Peer Group NG, PVG, ITH und XRA

ein heterogeneres Bild hier - im Jahreschart gibt es einen unsäglichen Ausreisser nach unten - gleichwohl hier prominent protegiert.

hier wird deutlich, wie Sea davon profitiert, zum einen für KSM ein wirtschaftliches Kupfer Gold Vorkommen bereits nachgewiesen zu haben, zum anderen aber dieses Projekt mit signifikanten höhergradigen Explorationserfolgen und weiterem Potential die Wirtschaftlichkeit boosten zu können.

Short interest mittlerweile bei 6,6 Millionen, das wird eine große Party, wenn hier Eindeckungen nötig werden...

Sea im Verfgleich der letzten drei Monate mit den drei Indices Gold Miners, Goldminer Juniors und Explorer:

Sea in der Erholung deutlich besser

gleiche Vergleichsgruppe mit dem desaströsen letzten Jahr - Sea deutlich besser.

Nun die gleichen Zeiträume mit der Peer Group NG, PVG, ITH und XRA

ein heterogeneres Bild hier - im Jahreschart gibt es einen unsäglichen Ausreisser nach unten - gleichwohl hier prominent protegiert.

hier wird deutlich, wie Sea davon profitiert, zum einen für KSM ein wirtschaftliches Kupfer Gold Vorkommen bereits nachgewiesen zu haben, zum anderen aber dieses Projekt mit signifikanten höhergradigen Explorationserfolgen und weiterem Potential die Wirtschaftlichkeit boosten zu können.

Short interest mittlerweile bei 6,6 Millionen, das wird eine große Party, wenn hier Eindeckungen nötig werden...

Antwort auf Beitrag Nr.: 45.450.235 von valueinvestor am 14.09.13 18:33:07Die Chartverläufe zeigen ganz eindeutig, dass SEA sich trotz der anhaltenden Explorerkrise ausgesprochen gut behaupten kann.

Wenn man im Angesicht dieser Fakten die verzweifelten Versuche unseres "beobachtenden Kommentators" gegenüberstellt, KSM und CL für gescheitert bzw. tot zu erklären, dann fragt man sich schon, ob hier jemand noch alle seine Sinne beieinander hat.

Aber es tut natürlich schon weh, wenn die von ihm hier wärmstens anempfohlene Pretium kursmäßig SEA hinterherhinkt.

Wenn man im Angesicht dieser Fakten die verzweifelten Versuche unseres "beobachtenden Kommentators" gegenüberstellt, KSM und CL für gescheitert bzw. tot zu erklären, dann fragt man sich schon, ob hier jemand noch alle seine Sinne beieinander hat.

Aber es tut natürlich schon weh, wenn die von ihm hier wärmstens anempfohlene Pretium kursmäßig SEA hinterherhinkt.

Antwort auf Beitrag Nr.: 45.450.803 von hingucker am 14.09.13 22:41:55Deine Feststellungen sind zweifelsohne richtig. Eine ITH hatte er wiederholt empfohlen und bei 1,44$ gekauft - sauber, sag ich.

Folgendes noch zu den Bornitzonen:

Within this envelope, wide bornite-rich intervals have now been intersected in stockwork veins with abundant chalcopyrite and other minor copper minerals as well as high gold values.

Dies bedeutet meiner Einschätzung nach, dass es bis jetzt mindestens 3 Bornitintervalle gibt.

Aus der news

http://www.seabridgegold.net/News/Article/424/drilling-begin…

mit der Aussage:

"The first phase of exploration at Deep Kerr in 2013 will include drilling multiple intersections 300 to 400 meters down dip of the current resource at approximately 500 meters spacing."

ergibt sich bei drei Fundstellen die Möglichkeit, dass sich Bornitintervalle in einem sehr großen Gebiet finden lassen, entweder auf einer Linie von etwa 800 bis 1000 Metern oder aber die dritte Fundstelle liegt in einer irgend gearteten Dreiecksposition zu den anderen Beiden. Nach der zeitlichen Abfolge der Veröffentlichungen kann man glaube ich vermuten, dass es sich bei den anderen Bornitfunden noch nicht um Wedging handelt.

Folgendes noch zu den Bornitzonen:

Within this envelope, wide bornite-rich intervals have now been intersected in stockwork veins with abundant chalcopyrite and other minor copper minerals as well as high gold values.

Dies bedeutet meiner Einschätzung nach, dass es bis jetzt mindestens 3 Bornitintervalle gibt.

Aus der news

http://www.seabridgegold.net/News/Article/424/drilling-begin…

mit der Aussage:

"The first phase of exploration at Deep Kerr in 2013 will include drilling multiple intersections 300 to 400 meters down dip of the current resource at approximately 500 meters spacing."

ergibt sich bei drei Fundstellen die Möglichkeit, dass sich Bornitintervalle in einem sehr großen Gebiet finden lassen, entweder auf einer Linie von etwa 800 bis 1000 Metern oder aber die dritte Fundstelle liegt in einer irgend gearteten Dreiecksposition zu den anderen Beiden. Nach der zeitlichen Abfolge der Veröffentlichungen kann man glaube ich vermuten, dass es sich bei den anderen Bornitfunden noch nicht um Wedging handelt.

Einfaches Einfügen von wallstreetONLINE Charts: So funktionierts.

Da ist der gemeinsame Haushalt ja wieder zusammen.

Von ehemals exorbitanten Kurszielen (200 Dollar, später dann 80-90 Dollar/Share), die als sicher galten, lese ich hier nun leider nichts mehr, leider auch nicht zu den Empfehlungen bei damaligen Mondpreisen (bei ca. 35Dollar, später erneut bei 29 Dollar). Es geht nur noch um ein Behaupten am Markt. Und wie man oben im Chartbild recht gut sieht ... Ich rechne im naechsten Jahr dann mit Kursen zwischen 6-9 Dollar. Kommt eine DD durch einen Interessenten, kann es noch schneller runter gehen. Ich werde das weiter beobachten.

Bei den ganzen Problemen sehe ich auch 2014 keine Machbarkeitsstudie.

Denkt mal darueber nach,

BL

Antwort auf Beitrag Nr.: 45.452.083 von boersenbrieflemming am 15.09.13 14:55:04...Es geht nur noch um ein Behaupten am Markt...

Na also, geht doch! Genau das wollte Value ja aufzeigen. Und SEA behauptet sich nun mal in diesem katastrophalen Explorermarkt besser als das von dir so hochgelobte Pretium und ITH. Du musst das ja nicht zugeben. Das wäre nun wirklich zuviel verlangt.

Aber es ist nun einmal Fakt.

Denk mal darueber nach.

Na also, geht doch! Genau das wollte Value ja aufzeigen. Und SEA behauptet sich nun mal in diesem katastrophalen Explorermarkt besser als das von dir so hochgelobte Pretium und ITH. Du musst das ja nicht zugeben. Das wäre nun wirklich zuviel verlangt.

Aber es ist nun einmal Fakt.

Denk mal darueber nach.

Antwort auf Beitrag Nr.: 45.452.733 von hingucker am 15.09.13 17:44:33 SEA behauptet sich nun mal in diesem katastrophalen Explorermarkt besser als das von dir so hochgelobte Pretium

Es ist schon ziemlich unglaublich was eure Truppe da so an Luegengebilden ablaesst.

Kurz zu den "Bornitintervallen" - ich will da jetzt nicht darauf rumreiten das das SEA-MM da nun Bilder von Narrengold praesentiert hat, damit das alles etwas nach Gold aussieht. Jeder weiss ja, das hier eine erneute Finanzierung ansteht, nachdem die (auch bei WO) beworbene Projekte so grandios scheiterten.

Aber habt ihr schon einmal die potentiellen Kaeufer darueber informiert was bei einem "Declined Tunnel"system an Resourcen übrig bleiben wird - unabhaengig davon sind die Grade in meinen Augen zu kuemmerlich und hier nun von einem "Boost" zu sprechen ist lächerlich.

Denk mal darueber nach,

BL

Einfaches Einfügen von wallstreetONLINE Charts: So funktionierts.

Es ist schon ziemlich unglaublich was eure Truppe da so an Luegengebilden ablaesst.

Kurz zu den "Bornitintervallen" - ich will da jetzt nicht darauf rumreiten das das SEA-MM da nun Bilder von Narrengold praesentiert hat, damit das alles etwas nach Gold aussieht. Jeder weiss ja, das hier eine erneute Finanzierung ansteht, nachdem die (auch bei WO) beworbene Projekte so grandios scheiterten.

Aber habt ihr schon einmal die potentiellen Kaeufer darueber informiert was bei einem "Declined Tunnel"system an Resourcen übrig bleiben wird - unabhaengig davon sind die Grade in meinen Augen zu kuemmerlich und hier nun von einem "Boost" zu sprechen ist lächerlich.

Denk mal darueber nach,

BL

Antwort auf Beitrag Nr.: 45.453.029 von boersenbrieflemming am 15.09.13 19:08:40...Es ist schon ziemlich unglaublich was eure Truppe da so an Luegengebilden ablaesst...

Jemand wie du, der erst kürzlich die Lüge verbreitet hat, auf der aktuellen HP von SEA würden falsche Daten veröffentlicht, der sollte schon deshalb gewissenhafter prüfen ob er andere der Lüge bezichtigen darf. Denn du schreibst schon wieder die Unwahrheit.

Ich bezog mich mit meinem von dir zitierten Fazit auf die von Value eingestellten Charts. Insofern ist dein Lügenvorwurf nur eine weitere Entgleisung.

Dein 3-Jahres-Chart ist für meine Betrachtung unwichtig. Denn der Tiefpunkt beider Aktien lag in der Mitte diesen Jahres. Die Erholung aus diesem Tief heraus ist SEA besser gelungen als deiner Lieblingsaktie. Und das ist nun mal nur mit einem 3-Monats- oder Jahreschart zu belegen.

Denk mal darueber nach.

Jemand wie du, der erst kürzlich die Lüge verbreitet hat, auf der aktuellen HP von SEA würden falsche Daten veröffentlicht, der sollte schon deshalb gewissenhafter prüfen ob er andere der Lüge bezichtigen darf. Denn du schreibst schon wieder die Unwahrheit.

Ich bezog mich mit meinem von dir zitierten Fazit auf die von Value eingestellten Charts. Insofern ist dein Lügenvorwurf nur eine weitere Entgleisung.

Dein 3-Jahres-Chart ist für meine Betrachtung unwichtig. Denn der Tiefpunkt beider Aktien lag in der Mitte diesen Jahres. Die Erholung aus diesem Tief heraus ist SEA besser gelungen als deiner Lieblingsaktie. Und das ist nun mal nur mit einem 3-Monats- oder Jahreschart zu belegen.

Denk mal darueber nach.

Antwort auf Beitrag Nr.: 45.453.029 von boersenbrieflemming am 15.09.13 19:08:40...Kurz zu den "Bornitintervallen"...

Ich dachte doch glatt jetzt kommt was zum Thema Bornit.

Statt dessen wieder dein platter Narrengold-Humor.

Denk mal darueber nach.

Ich dachte doch glatt jetzt kommt was zum Thema Bornit.

Statt dessen wieder dein platter Narrengold-Humor.

Denk mal darueber nach.

Die Aufregung ist ja wieder gross im Team Seabridge.

" Jemand wie du, der erst kürzlich die Lüge verbreitet hat,auf der aktuellen HP von SEA würden falsche Daten veröffentlicht"

Das sind nun einmal die Fakten. Die Zahlen die Seabridge Gold auf der Homepage bereit hält waren falsch, das Bild zu optimistisch und die Kosten im Wesentlichen zu gering angegeben. Das Projekt KSM braucht nun einen komplett neuen Minenplan und ich sehe weiterhin keine Machbarkeitsstudie.

Man kann aber einmal schauen, wie es bei der letzten Grosspleite von Fron, Anthony und Park zuging.

I spoke to IR today (Anmerkung: gemeint ist Fronk) and I get the impression

that a merger deal is definitely in the

works.

http://www.siliconinvestor.com/readmsg.aspx?msgid=7542043

Schuld am Shareprice waren jedoch immer die anderen.

"They say it's unfortunate there has been some negative rumors about the company going around. They also refer to a company interested in buying Greenstone spreading bad rumors to manipulate the price."

http://www.siliconinvestor.com/readmsg.aspx?msgid=7478008

Eure Art der "Informationsverbreitung" ist also sehr alt, fuer den deutschen Anleger heisst es dann seit 2006: "Die Einschlaege kommen näher", etc.pp. - was damals folgte waren manipulierte Conference Calls (*) und dann eine 300 Mio. Pleite. Die Anleger verloren trotz optimistischer Aeusserungen alles.

(*) http://www.siliconinvestor.com/readmsg.aspx?msgid=7883309

" Jemand wie du, der erst kürzlich die Lüge verbreitet hat,auf der aktuellen HP von SEA würden falsche Daten veröffentlicht"

Das sind nun einmal die Fakten. Die Zahlen die Seabridge Gold auf der Homepage bereit hält waren falsch, das Bild zu optimistisch und die Kosten im Wesentlichen zu gering angegeben. Das Projekt KSM braucht nun einen komplett neuen Minenplan und ich sehe weiterhin keine Machbarkeitsstudie.

Man kann aber einmal schauen, wie es bei der letzten Grosspleite von Fron, Anthony und Park zuging.

I spoke to IR today (Anmerkung: gemeint ist Fronk) and I get the impression

that a merger deal is definitely in the

works.

http://www.siliconinvestor.com/readmsg.aspx?msgid=7542043

Schuld am Shareprice waren jedoch immer die anderen.

"They say it's unfortunate there has been some negative rumors about the company going around. They also refer to a company interested in buying Greenstone spreading bad rumors to manipulate the price."

http://www.siliconinvestor.com/readmsg.aspx?msgid=7478008

Eure Art der "Informationsverbreitung" ist also sehr alt, fuer den deutschen Anleger heisst es dann seit 2006: "Die Einschlaege kommen näher", etc.pp. - was damals folgte waren manipulierte Conference Calls (*) und dann eine 300 Mio. Pleite. Die Anleger verloren trotz optimistischer Aeusserungen alles.

(*) http://www.siliconinvestor.com/readmsg.aspx?msgid=7883309

http://finance.yahoo.com/q/ta?s=SA&t=1y&l=on&z=l&q=b&p=e100%…

technische Analyse, hier könnten bald die drei wichtigsten SMA Linien positive Signale generieren.

Das Auswerteprogram kommt zu folgendem Schluss:

"1y Target Est: 37.70"

einen Chartvergleich mit Pretium, wo die Linien zu unterschiedlichen Zeitpunkten beginnen wirst du wohl kaum als ernsthaft in den Raum stellen wollen. Zudem hat SSRI den Emissionspreis offensichtlich zu niedrig angesetzt, vermutlich haben sich da einige bei der Emission selber die Taschen mit billigen Aktien vollgestopft. Damals habe ich auch gut an dem Papier verdient, das war schnelles Geld. Im Moment wäre mir eine Spekulation auf das bulk sample Programm viel zu riskant, weil die große Gefahr besteht, dass sich die luftig hohen Ressourcenschätzungen nicht realisieren lassen. Zudem ist Pretium eine gigantische Verwässerungsmaschine, in der kurzen Zeit der Börsennotierung haben sie sich schon auf fully diluted 113 Millionen Aktien aufgebläht - allein 4 Kapitalmassnahmen gab es in 2013!

Antwort auf Beitrag Nr.: 45.454.575 von valueinvestor am 16.09.13 08:36:03bulk sample Programm viel zu riskant

... wann wird es denn bei Seabridge Gold deiner Meinung nach zu einer Machbarkeitsstudie und einem Bulk Sample Programm kommen? Das ist besonders spannend, da die Verantwortlichen Seabridgeschaetzer (1-Mann Firmen) ja bisher ueberwiegend durch Fehlschaetzungen international aufgefallen sind. Wann wird es etwas zur Metallurgie geben - hier finden sich nur sehr einfache Tests, waehrend bei der Seabridge Resosurcenschaetzung von einer sehr hohen Recovery Rate ausgegangen wird. Warum werden 2/3 der Bohrergebnisse beim CL-Projekt (Walsh Lake) nicht veröffentlicht.

Das Auswerteprogram kommt zu folgendem Schluss:

... wann wird es denn bei Seabridge Gold deiner Meinung nach zu einer Machbarkeitsstudie und einem Bulk Sample Programm kommen? Das ist besonders spannend, da die Verantwortlichen Seabridgeschaetzer (1-Mann Firmen) ja bisher ueberwiegend durch Fehlschaetzungen international aufgefallen sind. Wann wird es etwas zur Metallurgie geben - hier finden sich nur sehr einfache Tests, waehrend bei der Seabridge Resosurcenschaetzung von einer sehr hohen Recovery Rate ausgegangen wird. Warum werden 2/3 der Bohrergebnisse beim CL-Projekt (Walsh Lake) nicht veröffentlicht.

Das Auswerteprogram kommt zu folgendem Schluss:

Antwort auf Beitrag Nr.: 45.454.421 von boersenbrieflemming am 16.09.13 08:12:08...Die Zahlen die Seabridge Gold auf der Homepage bereit hält waren falsch, das Bild zu optimistisch und die Kosten im Wesentlichen zu gering angegeben...

Ja da schau her. Die Zahlen waren falsch, zu optimistisch, zu gering. Das sind ja ganz neue Töne.

Mit der PFS vom 24.7.2012 wurde in der Tat eine neue, höhere Kostenschätzung veröffentlicht. Nämlich 5,3 Mrd statt bis dahin ca. 3 Mrd US$. Und seit dieser Veröffentlichung steht diese Summe auch so auf der HP von Seabridge. Also auch aktuell heute.

Du allerdings hast behauptet, die derzeitige (also aktuelle) Präsentation auf der SEA Website enthält als CAPEX für KSM ca. 3 Mrd. Dollar statt der aktuell bereits kommunizierten über 5 Mrd.

Ich weiß nicht wie oft ich es hier noch wiederholen muss, dass du hier ganz bewusst gelogen hast. Da hilft dir auch nicht die erfolgreiche Suche über Google nach einem Pdf-Dokument in dem die alten Zahlen noch zu ersehen sind. Der interessierte Anleger informiert sich auf der HP einer Company und sucht nicht per Google nach Dokumenten. Das ist eher die Vorgehensweise von Bashern.

Das du dann auch noch 14 Jahre alte (!) anonyme Beiträge aus irgendwelchen Foren heranführst, die nicht SEA sondern Greenstone betreffen, zeigt deine Hilflosigkeit in der Argumentation. Das ist einfach nur noch als Spamming zu bezeichnen.

Denk mal darueber nach.

Ja da schau her. Die Zahlen waren falsch, zu optimistisch, zu gering. Das sind ja ganz neue Töne.

Mit der PFS vom 24.7.2012 wurde in der Tat eine neue, höhere Kostenschätzung veröffentlicht. Nämlich 5,3 Mrd statt bis dahin ca. 3 Mrd US$. Und seit dieser Veröffentlichung steht diese Summe auch so auf der HP von Seabridge. Also auch aktuell heute.

Du allerdings hast behauptet, die derzeitige (also aktuelle) Präsentation auf der SEA Website enthält als CAPEX für KSM ca. 3 Mrd. Dollar statt der aktuell bereits kommunizierten über 5 Mrd.