Globex Mining- Startschuss ??? - Älteste Beiträge zuerst (Seite 2361)

eröffnet am 15.11.05 13:07:13 von

neuester Beitrag 22.04.24 09:18:55 von

neuester Beitrag 22.04.24 09:18:55 von

Beiträge: 32.766

ID: 1.020.143

ID: 1.020.143

Aufrufe heute: 4

Gesamt: 2.343.709

Gesamt: 2.343.709

Aktive User: 0

ISIN: CA3799005093 · WKN: A1H735 · Symbol: GMX

1,0000

CAD

0,00 %

0,0000 CAD

Letzter Kurs 23.04.24 Toronto

Neuigkeiten

22.04.24 · kapitalerhoehungen.de |

18.04.24 · globenewswire |

17.04.24 · inv3st.de Anzeige |

16.04.24 · IR-News |

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7950 | +30,33 | |

| 3,9300 | +15,59 | |

| 1,7500 | +15,13 | |

| 11,180 | +14,08 | |

| 208,00 | +13,60 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 18,550 | -11,03 | |

| 0,7000 | -12,49 | |

| 0,7250 | -14,71 | |

| 4,2300 | -17,86 | |

| 0,9000 | -25,00 |

Antwort auf Beitrag Nr.: 54.410.083 von elmago am 25.02.17 12:43:18Ja, vorläufig kommen von den Nafta-Staaten für mich nur nur die südlich und nördlich von Trump-Land infrage

Auch von mir viel Spaß in Mexiko und einen erholsamen Urlaub.

Ich sehe dieses Trump-Bashing allerdings etwas anders.

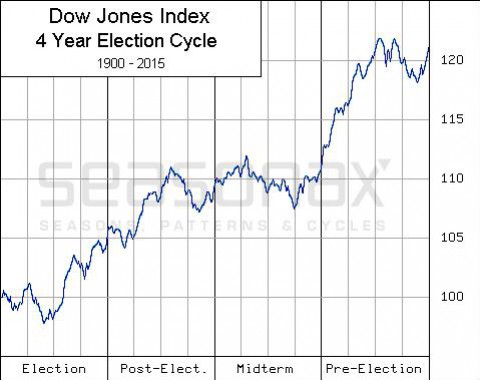

Der DOW JONES ist seit Amtsantritt von Trump über 10% gestiegen. Die Börse lügt bekanntermaßen nie. Weshalb steigt sie also?

Weil Trump ein Geschäftsmann ist und kein wirklicher Politiker. Er setzt um, was er vor der Wahl versprochen hatte. Was ist daran so verwerflich?

Auch von mir viel Spaß in Mexiko und einen erholsamen Urlaub.

Ich sehe dieses Trump-Bashing allerdings etwas anders.

Der DOW JONES ist seit Amtsantritt von Trump über 10% gestiegen. Die Börse lügt bekanntermaßen nie. Weshalb steigt sie also?

Weil Trump ein Geschäftsmann ist und kein wirklicher Politiker. Er setzt um, was er vor der Wahl versprochen hatte. Was ist daran so verwerflich?

Antwort auf Beitrag Nr.: 54.414.127 von Pieselwitz am 26.02.17 11:49:08

Der Anstieg der Börsen ist vermutlich zyklisch begünstigt und dürfte sich bis etwa August noch fortsetzen.

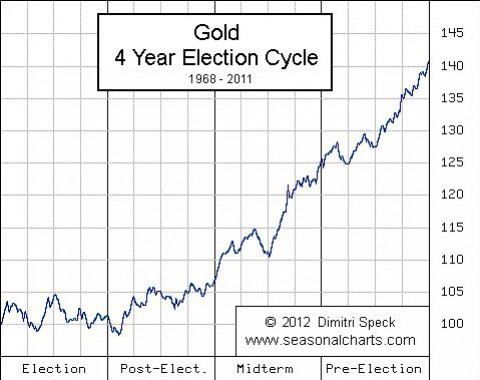

Bei Gold gibt es übrigens auch einen 4-Jährigen US-Wahltrend, was unserer Globex in den nächsten 2-3 Jahren schönen Rückenwind bescheren sollte:

(Quellen: http://www.seasonalcharts.de)

Zitat von Pieselwitz: Ja, vorläufig kommen von den Nafta-Staaten für mich nur nur die südlich und nördlich von Trump-Land infrage

Auch von mir viel Spaß in Mexiko und einen erholsamen Urlaub.

Ich sehe dieses Trump-Bashing allerdings etwas anders.

Der DOW JONES ist seit Amtsantritt von Trump über 10% gestiegen. Die Börse lügt bekanntermaßen nie. Weshalb steigt sie also?

Weil Trump ein Geschäftsmann ist und kein wirklicher Politiker. Er setzt um, was er vor der Wahl versprochen hatte. Was ist daran so verwerflich?

Der Anstieg der Börsen ist vermutlich zyklisch begünstigt und dürfte sich bis etwa August noch fortsetzen.

Bei Gold gibt es übrigens auch einen 4-Jährigen US-Wahltrend, was unserer Globex in den nächsten 2-3 Jahren schönen Rückenwind bescheren sollte:

(Quellen: http://www.seasonalcharts.de)

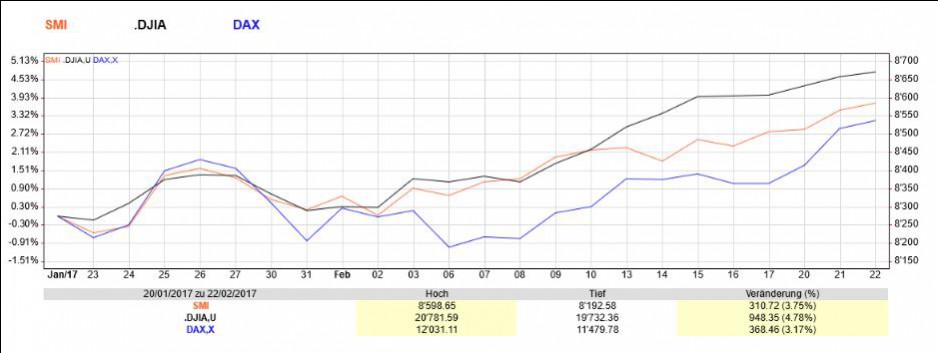

Antwort auf Beitrag Nr.: 54.414.667 von elmago am 26.02.17 14:16:49Bin auch der Meinung, dass der Anstieg des DJ nur am Rande von den Märchen des Lügenbarons beeinflusst wurde. Zudem beträgt der Anstieg nicht 10% sondern nur etwa die Hälfte wie man aus untenstehendem Chart entnehmen kann. Auch der DAX und der SMI haben zugelegt, allerdings leicht weniger als der Dow Jones.

Zudem ist auch unbestritten, dass die Börse auch korrigiert, wenn sich die Annahmen verändern. Im Moment herrscht in den USA noch Optimismus. Allerdings wird sich dies ziemlich rasch ändern, wenn Trump seine Pläne "America First" umsetzen will und Amerika von entsprechenden Gegenmassnahmen der übrigen Welt betroffen sein wird. Ein solcher Handelskrieg wird hüben und drüben schaden und vor allem den Amis nichts Nachhaltiges bringen.

Gruss William

Zudem ist auch unbestritten, dass die Börse auch korrigiert, wenn sich die Annahmen verändern. Im Moment herrscht in den USA noch Optimismus. Allerdings wird sich dies ziemlich rasch ändern, wenn Trump seine Pläne "America First" umsetzen will und Amerika von entsprechenden Gegenmassnahmen der übrigen Welt betroffen sein wird. Ein solcher Handelskrieg wird hüben und drüben schaden und vor allem den Amis nichts Nachhaltiges bringen.

Gruss William

Antwort auf Beitrag Nr.: 54.421.531 von WilliamTell am 27.02.17 17:02:35Setz mal Globex dazu, dann werden die 3 Kurven gaaanz flach

Antwort auf Beitrag Nr.: 54.421.693 von elmago am 27.02.17 17:20:51

Gruss William

Globex First - Trump Second - Merkel Third

Kann leider nur 3 Werte vergleichen.....habe also den SMI weggelassen......Die Indizes haben sich, wie von elmago prognotiziert, stark abgeflacht....

Gruss William

Trading Spotlight

Tages-Chart vom 27.2.2017

Eröffnung bei 0.62 CAD......wieder eine grosse Transaktion zu 0.59 CAD. Wir liegen in Lauerstellung für den Angriff auf die von Sonic prognostizierten 0.70 CAD.....

Gruss William

Einfaches Einfügen von wallstreetONLINE Charts: So funktionierts.

Antwort auf Beitrag Nr.: 54.422.182 von WilliamTell am 27.02.17 18:04:06MNXF) ("Sayona" or the "Company") is pleased provide shareholders with a progress update on exploration and development activities.

Authier Lithium Project

The Company recently announced its maiden Ore Reserve and Pre-Feasibility Study ("PFS") summary for the Authier project. Key findings of the PFS, include:

- Pre-tax NPV of C$140 million and pre-tax IRR 39% (real terms at 8% discount rate);

- Annual average concentrate production of 99,000 tonnes at 5.75% Li20;

- Average annual revenue of C$67 million and EBITDA of C$31 million;

- Life of mine strip ratio of 6:1 (waste to ore) and cash costs of C$367 (US $280) FOB Montreal Port;

- Development capital expenditure of C$66 million; and

- Maiden Ore Reserve of 10.2 Mt @ 1.02% Li20 (Proven Reserve 4.9Mt @ 0.97% Li20 and Probable Reserve 5.3Mt @ 1.06% Li20) delivers a mine life of 13 years.

The Company is now looking at a number of options to significantly enhance the value of the project, including drilling to expand the Mineral Resource and Ore Reserves, further metallurgical and geotechnical test-work, and other downstream value-adding opportunities.

The 4,000 metre resource expansion drilling program is progressing well with 1,857 metres in 7 holes completed. The drilling is demonstrating the extensions of the mineralisation at depth in the western sector. The first drill cores were sent to the laboratory this week for analysis. On-going drilling is planned in the eastern sector, the new pegmatite area in the north, and infill within the existing Inferred Resource areas.

Western Australian Lithium

Recent mapping and sampling programs at the Mallina project has identified five new pegmatite areas with rock chips up to 3.47% Li20. Planning is underway for another phase of exploration including, mapping, rock sampling, and auger drilling. This work will be complemented by systematic soil geochemistry, to be carried out with the aim of identifying targets for RC drilling under shallow cover. The primary focus is the area of newly discovered spodumene pegmatites as well as traversing the unexplored remainder of the tenement area. Whilst the area remains wet from recent rain, a geophysics program is being planned to assist with identifying structures under cover that may be blind on surface.

Future Funding Options

The Company currently has cash resources of $1.3 million which will fund its development activities in the short term. The Company has commenced some preliminary discussions with prospective financiers about options for funding future exploration and development activities with minimal dilution to shareholders. The Company is encouraged by the response regarding the level and types of funding that could be available.

Lithium Industry Pricing Update

The pricing of lithium concentrates being sold from Australia to China continue to surprise on the upside. Two new Australian producers have recently announced settlements for 2017 contract pricing, including:

- Neometals has entered into contracts for 6% Li20 concentrates at US$750 per tonne CFR China for shipments departing Australia before 30 June 2017. Pricing of subsequent shipments is to be set on a 6-month basis by a formula based on a weighted average price of Chinese imports of Lithium Carbonate and Lithium Hydroxide plus a floor price consistent with the original off-take agreement; and

- Galaxy has entered into contracts for all of 2017 production of 120,000 tonnes at a base price of US$830 per tonne FOB for 5.5% Li20 concentrate. The contract terms provided a payment bonus of US$15 per tonne for every 0.1% improvement in the concentrate grade above the 5.5% Li20 base rate or US$905 per tonne FOB for a 6% Li20 concentrate.

The new pricing regime reflects the much tighter market for concentrates as new projects commission slower than forecast and financing constraints slow the planned development timetables for other advanced projects.

The Company notes that its benchmark pricing assumptions for the recently completed PFS of US$515/tonne FOB (5.75% Li20 concentrate) are well below the current prices of lithium concentrate contracts for 2017.

Strategic Intent

The Company remains focused on rapidly developing its spodumene projects and capitalising on the strong pricing window available for new project entrants in the short to medium term. Authier is an advanced development project and cash flow generation opportunity with positive attributes, including:

- Extensively drilled and well understood geology;

- Well studied with the completion of a Pre-Feasibility study (February 2017);

- Maiden JORC Ore Reserves - 10.2 Mt @ 1.02% Li20 (Proven Reserve 4.9Mt @ 0.97% Li20 and Probable Reserve 5.3Mt @ 1.06% Li20);

- Simple open-cut, truck and shovel mining operation;

- Proven process for recovery of spodumene into a saleable concentrate - low technology risk;

- World-class infrastructure and Quebec Government support;

- Low capital hurdle and attractive operating costs; and

- Potential to expand the size of the Mineral Resource through further optimisation and enhance the value of the project through further optimisation studies.

Despite the solid progress achieved at Authier since the acquisition in August 2016, the Company still trades on one of the lowest enterprise value per tonne of Measured and Indicated Resource multiples in the global sector - $176 per tonne. This is more in line with lithium explorers than an advanced project.

The Company believes it will create significant share value-uplift for shareholders as the project resource base is expanded, optimisation activities are completed, and it's advanced towards development.

To view tables and figures, please visit:

http://abnnewswire.net/lnk/09BIEJ26

About Sayona Mining Ltd

Sayona Authier Entwicklungs NR

Brisbane, Feb 27, 2017 AEST (ABN Newswire) - Sayona Mining Limited (ASX:SYA) (OTCMKTSMNXF) ("Sayona" or the "Company") is pleased provide shareholders with a progress update on exploration and development activities. Authier Lithium Project

The Company recently announced its maiden Ore Reserve and Pre-Feasibility Study ("PFS") summary for the Authier project. Key findings of the PFS, include:

- Pre-tax NPV of C$140 million and pre-tax IRR 39% (real terms at 8% discount rate);

- Annual average concentrate production of 99,000 tonnes at 5.75% Li20;

- Average annual revenue of C$67 million and EBITDA of C$31 million;

- Life of mine strip ratio of 6:1 (waste to ore) and cash costs of C$367 (US $280) FOB Montreal Port;

- Development capital expenditure of C$66 million; and

- Maiden Ore Reserve of 10.2 Mt @ 1.02% Li20 (Proven Reserve 4.9Mt @ 0.97% Li20 and Probable Reserve 5.3Mt @ 1.06% Li20) delivers a mine life of 13 years.

The Company is now looking at a number of options to significantly enhance the value of the project, including drilling to expand the Mineral Resource and Ore Reserves, further metallurgical and geotechnical test-work, and other downstream value-adding opportunities.

The 4,000 metre resource expansion drilling program is progressing well with 1,857 metres in 7 holes completed. The drilling is demonstrating the extensions of the mineralisation at depth in the western sector. The first drill cores were sent to the laboratory this week for analysis. On-going drilling is planned in the eastern sector, the new pegmatite area in the north, and infill within the existing Inferred Resource areas.

Western Australian Lithium

Recent mapping and sampling programs at the Mallina project has identified five new pegmatite areas with rock chips up to 3.47% Li20. Planning is underway for another phase of exploration including, mapping, rock sampling, and auger drilling. This work will be complemented by systematic soil geochemistry, to be carried out with the aim of identifying targets for RC drilling under shallow cover. The primary focus is the area of newly discovered spodumene pegmatites as well as traversing the unexplored remainder of the tenement area. Whilst the area remains wet from recent rain, a geophysics program is being planned to assist with identifying structures under cover that may be blind on surface.

Future Funding Options

The Company currently has cash resources of $1.3 million which will fund its development activities in the short term. The Company has commenced some preliminary discussions with prospective financiers about options for funding future exploration and development activities with minimal dilution to shareholders. The Company is encouraged by the response regarding the level and types of funding that could be available.

Lithium Industry Pricing Update

The pricing of lithium concentrates being sold from Australia to China continue to surprise on the upside. Two new Australian producers have recently announced settlements for 2017 contract pricing, including:

- Neometals has entered into contracts for 6% Li20 concentrates at US$750 per tonne CFR China for shipments departing Australia before 30 June 2017. Pricing of subsequent shipments is to be set on a 6-month basis by a formula based on a weighted average price of Chinese imports of Lithium Carbonate and Lithium Hydroxide plus a floor price consistent with the original off-take agreement; and

- Galaxy has entered into contracts for all of 2017 production of 120,000 tonnes at a base price of US$830 per tonne FOB for 5.5% Li20 concentrate. The contract terms provided a payment bonus of US$15 per tonne for every 0.1% improvement in the concentrate grade above the 5.5% Li20 base rate or US$905 per tonne FOB for a 6% Li20 concentrate.

The new pricing regime reflects the much tighter market for concentrates as new projects commission slower than forecast and financing constraints slow the planned development timetables for other advanced projects.

The Company notes that its benchmark pricing assumptions for the recently completed PFS of US$515/tonne FOB (5.75% Li20 concentrate) are well below the current prices of lithium concentrate contracts for 2017.

Strategic Intent

The Company remains focused on rapidly developing its spodumene projects and capitalising on the strong pricing window available for new project entrants in the short to medium term. Authier is an advanced development project and cash flow generation opportunity with positive attributes, including:

- Extensively drilled and well understood geology;

- Well studied with the completion of a Pre-Feasibility study (February 2017);

- Maiden JORC Ore Reserves - 10.2 Mt @ 1.02% Li20 (Proven Reserve 4.9Mt @ 0.97% Li20 and Probable Reserve 5.3Mt @ 1.06% Li20);

- Simple open-cut, truck and shovel mining operation;

- Proven process for recovery of spodumene into a saleable concentrate - low technology risk;

- World-class infrastructure and Quebec Government support;

- Low capital hurdle and attractive operating costs; and

- Potential to expand the size of the Mineral Resource through further optimisation and enhance the value of the project through further optimisation studies.

Despite the solid progress achieved at Authier since the acquisition in August 2016, the Company still trades on one of the lowest enterprise value per tonne of Measured and Indicated Resource multiples in the global sector - $176 per tonne. This is more in line with lithium explorers than an advanced project.

The Company believes it will create significant share value-uplift for shareholders as the project resource base is expanded, optimisation activities are completed, and it's advanced towards development.

To view tables and figures, please visit:

http://abnnewswire.net/lnk/09BIEJ26

About Sayona Mining Ltd

Antwort auf Beitrag Nr.: 54.422.461 von crystalsonic am 27.02.17 18:33:03Lithium ist ei gutes Beispiel für Gegenmassnahmen an die Adresse von Trump. Die USA haben - Irrtum vorbehalten - noch keine produzierende Lithium-Mine. Wenn die kein Lithium mehr kaufen können, dann steht in den USA einiges still.

Gruss William

Gruss William

Antwort auf Beitrag Nr.: 54.421.531 von WilliamTell am 27.02.17 17:02:35

Auszug der Annual Statements:

Development Pipeline Expected to Provide Further Production Growth in 2021 and Beyond

Agnico Eagle has a strong pipeline of development projects that could provide further production growth in 2021 and beyond. These opportunities are typically at an earlier stage than those outlined above. A summary of the longer term opportunities are presented in the following table.

Minesite/Region

Opportunity

LaRonde Complex

Potential development of LaRonde 3 (located below a depth of 3.1 kilometres) where recent drilling has encountered high grade gold intersections

Goldex

Evaluation of the South Zone, G Zone and Deep 3 Zone and the neighboring Joubi Mine École properties

Canadian Malartic (50%)

Evaluation of the potential for production from Odyssey North underground

Kittila

Further optimization of underground mine and development of the lower mine with shaft access

Meadowbank

Evaluation of the potential to carry out underground mining at the Amaruq deposit and the potential to expand the higher grade V Zone

Meliadine

Further drill testing of known zones and gold occurrences on the 80-kilometre-long greenstone belt

Barsele

Testing additional mineralized zones and evaluation of production potential

El Barqueno

Evaluation of several potential production scenarios

Hammond Reef (50%)

Potential for production in a higher margin environment

Kirkland Lake (50%)

Potential production scenario at Upper Beaver and potential synergies from development of other properties in the region

Four-Year Guidance Plan Outlines a Growing Production Profile with Stable Costs

Mine by mine production and cost guidance for 2017, mine by mine production forecasts for 2018 and 2019 and a consolidated production forecast for 2020 are presented below. Opportunities to improve these forecasts are ongoing.

Estimated Payable Gold Production

2016

2017

2018

2019

Actual

Forecast

Forecast

Forecast

Northern Business

LaRonde

305,788

315,000

360,000

365,000

LaRonde Zone 5

-

-

20,000

35,000

Canadian Malartic (50%)

292,514

300,000

325,000

320,000

Lapa

73,930

15,000

-

-

Ich lehne mich mal ganz weit aus dem Fenster :-)

In den Annual Statements von Agnico Eagle ist im Forecast zur Lapa Mine nur noch 15k Unzen in Q1-2017 drin also sind die jetzt platt dort. Ergänzend ist in deren Wachstumsplan der Werttreiber keine Lapa Mine mehr aufgeführt. Von Wood Pandora hören wir nicht viel und alles ist geheimnisvolles Schweigen. Ich tippe wir kaufen das Ding von AEM!!! Wir haben geschätztes Cash von 3m dazu kommt ja Natan, Chalice etc unsere Nyratar royalty das könnte passen. Lapa ist eine alte Mine und wir hätten keine Abschreibungen darauf das könnte ... Naja nur mal so als Diskussion

Auszug der Annual Statements:

Development Pipeline Expected to Provide Further Production Growth in 2021 and Beyond

Agnico Eagle has a strong pipeline of development projects that could provide further production growth in 2021 and beyond. These opportunities are typically at an earlier stage than those outlined above. A summary of the longer term opportunities are presented in the following table.

Minesite/Region

Opportunity

LaRonde Complex

Potential development of LaRonde 3 (located below a depth of 3.1 kilometres) where recent drilling has encountered high grade gold intersections

Goldex

Evaluation of the South Zone, G Zone and Deep 3 Zone and the neighboring Joubi Mine École properties

Canadian Malartic (50%)

Evaluation of the potential for production from Odyssey North underground

Kittila

Further optimization of underground mine and development of the lower mine with shaft access

Meadowbank

Evaluation of the potential to carry out underground mining at the Amaruq deposit and the potential to expand the higher grade V Zone

Meliadine

Further drill testing of known zones and gold occurrences on the 80-kilometre-long greenstone belt

Barsele

Testing additional mineralized zones and evaluation of production potential

El Barqueno

Evaluation of several potential production scenarios

Hammond Reef (50%)

Potential for production in a higher margin environment

Kirkland Lake (50%)

Potential production scenario at Upper Beaver and potential synergies from development of other properties in the region

Four-Year Guidance Plan Outlines a Growing Production Profile with Stable Costs

Mine by mine production and cost guidance for 2017, mine by mine production forecasts for 2018 and 2019 and a consolidated production forecast for 2020 are presented below. Opportunities to improve these forecasts are ongoing.

Estimated Payable Gold Production

2016

2017

2018

2019

Actual

Forecast

Forecast

Forecast

Northern Business

LaRonde

305,788

315,000

360,000

365,000

LaRonde Zone 5

-

-

20,000

35,000

Canadian Malartic (50%)

292,514

300,000

325,000

320,000

Lapa

73,930

15,000

-

-

Antwort auf Beitrag Nr.: 54.424.387 von crystalsonic am 27.02.17 21:49:35Könnte durchaus zutreffen. Ich meine im November 2016 einen Zeitungsartikel gelesen zu haben wonach die Produktion der Lapa-Mine ursprünglich noch bis Ende Dezember 2016 dauern sollte. Zwischenzeitlich sei aber Agnico daran mehrere Targets in die Tiefe sowie Zonen mit niedrigerem Goldgehalt zu untersuchen um die Lebensdauer zu verlängern.

Die Produktionskosten im 3. Quartal 2016 seien viel höher ausgefallen als in der gleichen Periode 2015 wegen niedrigeren Goldgehalten und tieferem Recovery-Anteil.

Deshalb könnte es bei Agnico zu einer ähnlichen Entscheidung kommen wie seinerzeit bei Richmont und der Francoeur Mine.

Deshalb ist die These von Sonic nicht von der Hand zu weisen und durchaus realistisch.

Gruss William

Die Produktionskosten im 3. Quartal 2016 seien viel höher ausgefallen als in der gleichen Periode 2015 wegen niedrigeren Goldgehalten und tieferem Recovery-Anteil.

Deshalb könnte es bei Agnico zu einer ähnlichen Entscheidung kommen wie seinerzeit bei Richmont und der Francoeur Mine.

Deshalb ist die These von Sonic nicht von der Hand zu weisen und durchaus realistisch.

Gruss William

Beitrag zu dieser Diskussion schreiben

Investoren beobachten auch:

| Wertpapier | Perf. % |

|---|---|

| +1,29 | |

| +6,25 | |

| -0,47 | |

| +4,12 | |

| -4,20 | |

| +1,63 | |

| +4,55 | |

| -0,49 | |

| +2,80 | |

| +2,45 |

Meistdiskutiert

| Wertpapier | Beiträge | |

|---|---|---|

| 219 | ||

| 155 | ||

| 75 | ||

| 57 | ||

| 49 | ||

| 45 | ||

| 44 | ||

| 41 | ||

| 36 | ||

| 30 |

22.04.24 · kapitalerhoehungen.de · Rheinmetall |

16.04.24 · IR-News · Almonty Industries |

09.04.24 · kapitalerhoehungen.de · Bayer |

04.04.24 · Der Finanzinvestor · Barrick Gold Corporation |