Great Panther Mining neuer Edelmetall-Investorenliebling (Seite 202)

eröffnet am 20.01.10 16:10:47 von

neuester Beitrag 02.03.24 12:21:59 von

neuester Beitrag 02.03.24 12:21:59 von

Beiträge: 7.994

ID: 1.155.436

ID: 1.155.436

Aufrufe heute: 0

Gesamt: 977.341

Gesamt: 977.341

Aktive User: 0

ISIN: CA39115V3092 · WKN: A3DMEW · Symbol: GPLDF

0,0000

USD

0,00 %

0,0000 USD

Letzter Kurs 23.04.24 Nasdaq OTC

Neuigkeiten

13.11.23 · GOLDINVEST.de Anzeige |

09.10.23 · GOLDINVEST.de Anzeige |

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7950 | +30,33 | |

| 3,9300 | +15,59 | |

| 1,7500 | +15,13 | |

| 11,180 | +14,08 | |

| 208,00 | +13,60 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 18,550 | -11,03 | |

| 0,7000 | -12,49 | |

| 0,7250 | -14,71 | |

| 4,2300 | -17,86 | |

| 0,9000 | -25,00 |

Beitrag zu dieser Diskussion schreiben

ok, ein Posting geht noch

Warum ich glaube, dass das Mgmt GPL nicht billig nach China verscherbeln wird

Antwort Kurzfassung: Weil es keinerlei Sinn macht und sie sich nur ins eigene Knie schießen würden.

Das Mgmt besitzt:

desweiteren:

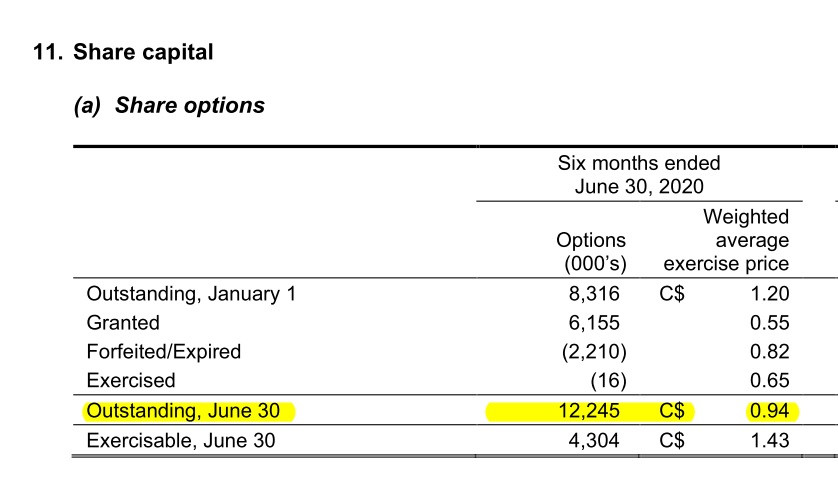

Restricted share units ("RSUs"),

Outstanding at June 30 2,085,395 C$ 0.74

Performance based restricted share unit (“PSUs”)

Outstanding at June 30 1,970,600 C$ 0.70

Deferred share units ("DSUs")

Outstanding at June 30 2,966,350 C$ 0.76

(SECURITIES OUTSTANDING

As of the date of this MD&A, the Company had 353,084,419 common shares issued and outstanding. There were

12,142,633 options, 2,085,395 restricted share units, 1,970,600 performance-based restricted share units,

3,203,750 deferred share units and 9,749,727 share purchase warrants outstanding. )

Das sind 17 Mio. gute Gründe nicht auf den Spatz in der Hand zu setzen sondern den 10$+ homerun anzustreben. Kaum jemand besitzt mehr und hat folglich ein höheres Eigeninteresse die Firma nicht unter Wert zu verschleudern!

GPL wird eher Goldcorp 2.0 als zu 2-3$ nach China zu wandern..... jmho

Warum ich glaube, dass das Mgmt GPL nicht billig nach China verscherbeln wird

Antwort Kurzfassung: Weil es keinerlei Sinn macht und sie sich nur ins eigene Knie schießen würden.

Das Mgmt besitzt:

desweiteren:

Restricted share units ("RSUs"),

Outstanding at June 30 2,085,395 C$ 0.74

Performance based restricted share unit (“PSUs”)

Outstanding at June 30 1,970,600 C$ 0.70

Deferred share units ("DSUs")

Outstanding at June 30 2,966,350 C$ 0.76

(SECURITIES OUTSTANDING

As of the date of this MD&A, the Company had 353,084,419 common shares issued and outstanding. There were

12,142,633 options, 2,085,395 restricted share units, 1,970,600 performance-based restricted share units,

3,203,750 deferred share units and 9,749,727 share purchase warrants outstanding. )

Das sind 17 Mio. gute Gründe nicht auf den Spatz in der Hand zu setzen sondern den 10$+ homerun anzustreben. Kaum jemand besitzt mehr und hat folglich ein höheres Eigeninteresse die Firma nicht unter Wert zu verschleudern!

GPL wird eher Goldcorp 2.0 als zu 2-3$ nach China zu wandern..... jmho

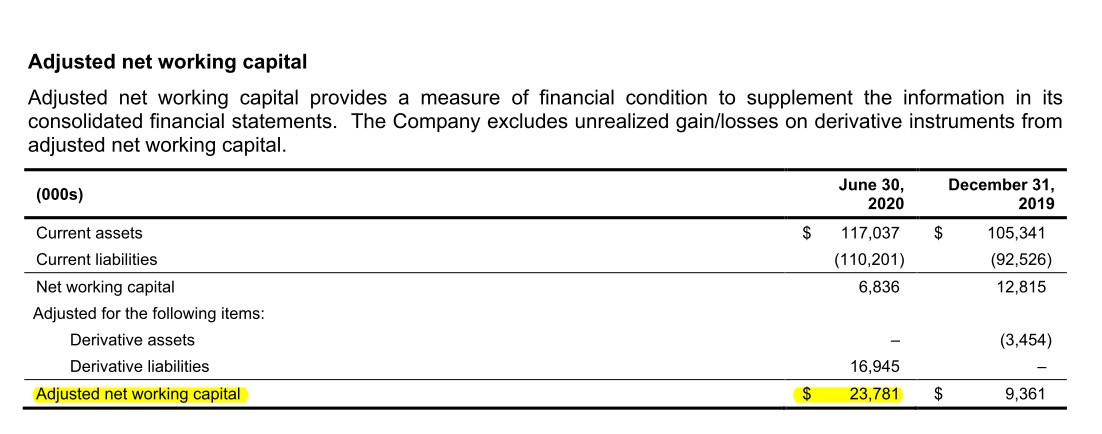

Ach, zwei findings könnte man noch hinterher schieben:

Das net working capital ist ohne Währungs-Buchverluste bereits mit fetten knapp 24m $ positiv, FX eingerechnet immerhin knapp 7m $ per Ende Juni.

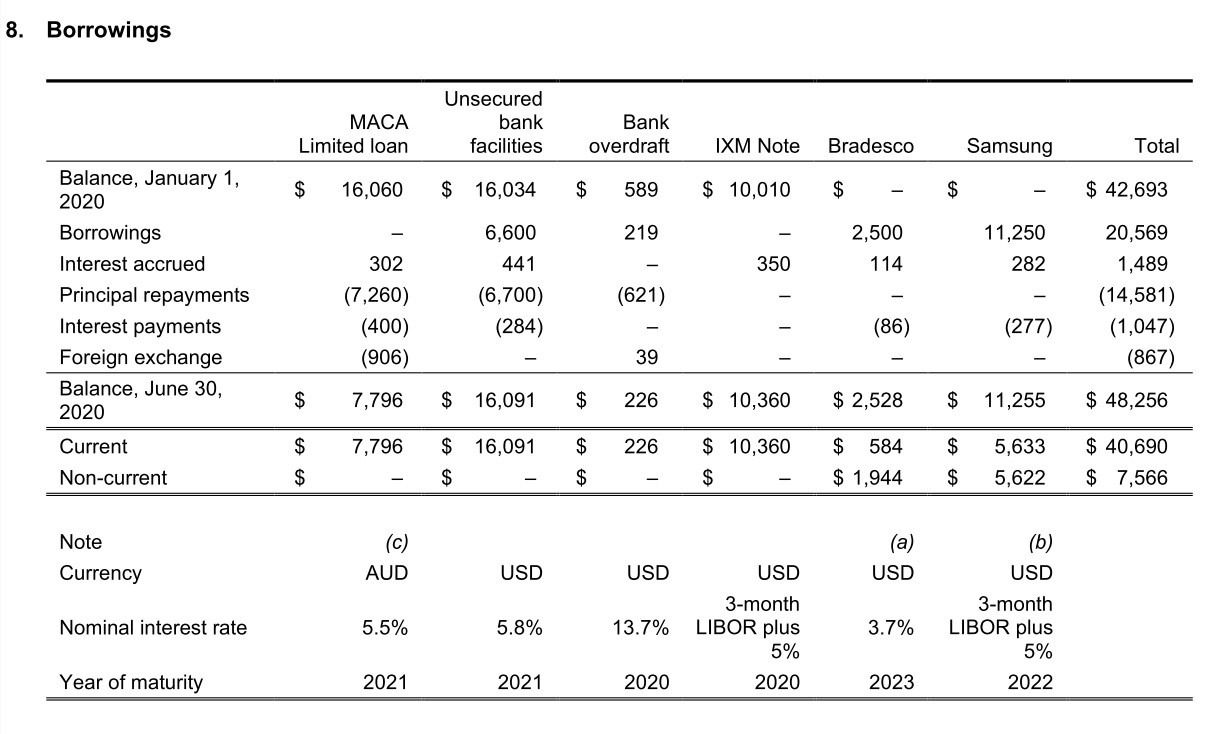

Ein Blick auf die bestehenden Ausleihungen ist auch interessant:

MACA sind keine 8m $ mehr offen... d.h. das Thema ist noch 2020 durch!

Insgesamt gilt:

Of the $40.7 million of current borrowings at June 30, 2020, $2.0 million was repaid subsequent to the end of the

quarter, and there are approximately $28.5 million of remaining repayments due in 2020.

D.h. von den 40.7m verschwinden bereits über 30m bis Jahresende!

Wer jetzt fragt, kann GPL sich das denn leisten? Ja, mit geschätzt 100 Mio. Gewinn im 2. HJ macht das nur 1/3 des incomming cashs aus...

Und dann hat GPL bereits per Jahresende eine fast blitzeblanke Bilanz. Und die Restschulden bestehen dann nur noch, weil sie schlicht nicht fällig sind und GPL keine Kündigungsoption besitzt

Und last but not least, fande ich spannend das hier zu lesen:

Coricancha

Coricancha continues on care and maintenance as the Company evaluates conditions for a restart of the mine.

The evaluation has included a PEA completed in 2018 and the BSP completed in June 2019. In the fourth quarter

of 2019, the Company initiated a limited mining and processing campaign of approximately 25,000 tonnes. These

activities were temporarily suspended in accordance with the Peruvian government-mandated restrictions

associated with the National State of Emergency announced on March 16, 2020 in response to the COVID-19,

which was lifted on May 24, 2020. The Company resumed the processing campaign and continued with its

evaluation activities. There is no assurance that the Company’s evaluation efforts will be sufficient to bring

Coricancha back into production.

There are no established estimates of Mineral Reserves at Coricancha and it is not anticipated that any Mineral

Reserve estimates will be available when the Company expects to make a decision on the potential restart of

operations. If a restart of operations does occur, its production decision will not be based on any feasibility studies

of Mineral Reserves demonstrating economic and technical viability. There may be increased uncertainty and risks

with respect to revenues, cash flows and profitability of such operations, the potential to achieve any particular level

of recovery, the costs of such recovery, the rates of production and costs of production.

Das liest sich für mich so, dass GPL sich vorbehält auch ohne Studien und Co. schlicht die Produktionsentscheidung zu treffen, eben weil man sich sicher ist, dass es funzt. Das ist FR styl, wo man bekanntlich auch regelmäßig auf Studien geschissen hat und einfach angefangen hat zu produzieren. Halt, weil man die Studien einfach nicht braucht. Der Hinweis, das damit höhere Risiken verbunden sind..... ist schlicht obligatorisch

Also: nicht wundern, wenn GPL plötzlich mit der Produktionsentscheidung um die Ecke kommt. Es geht immerhin um 3 Mio. oz Ag eqv oder 80-90 Mio. $ Umsatz bei kosten von unter 30m $......... da legt man los, wenn man sich sicher, ist 10-15m dafür übrig zu haben!

Und das ist aus meiner Sicht bald / jetzt! 30m Schuldenrückzahlungen +15 Peru = alles bis Ende September durchfinanziert aus cash flow. Q4 explodiert dann das Bankkonto

Das net working capital ist ohne Währungs-Buchverluste bereits mit fetten knapp 24m $ positiv, FX eingerechnet immerhin knapp 7m $ per Ende Juni.

Ein Blick auf die bestehenden Ausleihungen ist auch interessant:

MACA sind keine 8m $ mehr offen... d.h. das Thema ist noch 2020 durch!

Insgesamt gilt:

Of the $40.7 million of current borrowings at June 30, 2020, $2.0 million was repaid subsequent to the end of the

quarter, and there are approximately $28.5 million of remaining repayments due in 2020.

D.h. von den 40.7m verschwinden bereits über 30m bis Jahresende!

Wer jetzt fragt, kann GPL sich das denn leisten? Ja, mit geschätzt 100 Mio. Gewinn im 2. HJ macht das nur 1/3 des incomming cashs aus...

Und dann hat GPL bereits per Jahresende eine fast blitzeblanke Bilanz. Und die Restschulden bestehen dann nur noch, weil sie schlicht nicht fällig sind und GPL keine Kündigungsoption besitzt

Und last but not least, fande ich spannend das hier zu lesen:

Coricancha

Coricancha continues on care and maintenance as the Company evaluates conditions for a restart of the mine.

The evaluation has included a PEA completed in 2018 and the BSP completed in June 2019. In the fourth quarter

of 2019, the Company initiated a limited mining and processing campaign of approximately 25,000 tonnes. These

activities were temporarily suspended in accordance with the Peruvian government-mandated restrictions

associated with the National State of Emergency announced on March 16, 2020 in response to the COVID-19,

which was lifted on May 24, 2020. The Company resumed the processing campaign and continued with its

evaluation activities. There is no assurance that the Company’s evaluation efforts will be sufficient to bring

Coricancha back into production.

There are no established estimates of Mineral Reserves at Coricancha and it is not anticipated that any Mineral

Reserve estimates will be available when the Company expects to make a decision on the potential restart of

operations. If a restart of operations does occur, its production decision will not be based on any feasibility studies

of Mineral Reserves demonstrating economic and technical viability. There may be increased uncertainty and risks

with respect to revenues, cash flows and profitability of such operations, the potential to achieve any particular level

of recovery, the costs of such recovery, the rates of production and costs of production.

Das liest sich für mich so, dass GPL sich vorbehält auch ohne Studien und Co. schlicht die Produktionsentscheidung zu treffen, eben weil man sich sicher ist, dass es funzt. Das ist FR styl, wo man bekanntlich auch regelmäßig auf Studien geschissen hat und einfach angefangen hat zu produzieren. Halt, weil man die Studien einfach nicht braucht. Der Hinweis, das damit höhere Risiken verbunden sind..... ist schlicht obligatorisch

Also: nicht wundern, wenn GPL plötzlich mit der Produktionsentscheidung um die Ecke kommt. Es geht immerhin um 3 Mio. oz Ag eqv oder 80-90 Mio. $ Umsatz bei kosten von unter 30m $......... da legt man los, wenn man sich sicher, ist 10-15m dafür übrig zu haben!

Und das ist aus meiner Sicht bald / jetzt! 30m Schuldenrückzahlungen +15 Peru = alles bis Ende September durchfinanziert aus cash flow. Q4 explodiert dann das Bankkonto

Antwort auf Beitrag Nr.: 64.698.508 von dogweiler am 09.08.20 16:20:53Mein Korrekturziel wurde am Freitag erreicht... 2015 USD 😁 Seh jetzt erstmal 2250 USD. Dann sehen wir ma weiter.. 😉

Q2 Bericht

Ich habe mir gestern in Ruhe den Q2 Bericht angeschaut resp. quergelesen. Was soll ich sagen: absolut mind-blowing! Ich kann mich nicht entsinnen, jemals die vergangenen 15 Jahre von einer meinem mining-investments einen inhaltlich stärkeren Report gelesen zu haben!

Jede Seite, jede Tabelle strotzt nur so vor Stärke. Die GUV-Rechnung ist atemberaubend stark - selbst in diesem schwachen Q2.

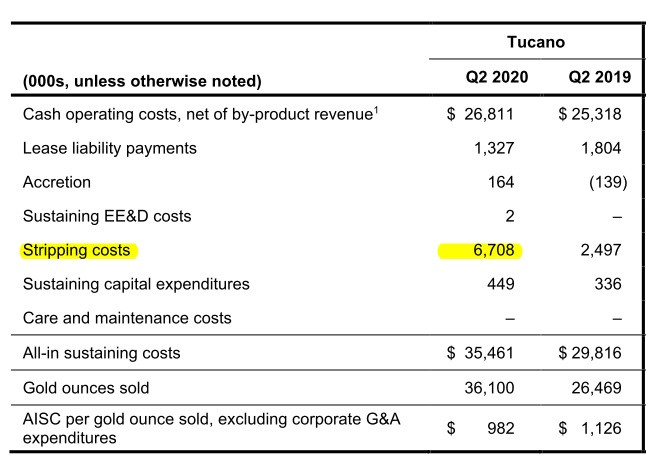

Wie ihr wisst, hatte ich mit Kosten um 29 Mio. $/Quartal gerechnet, der Bericht bestätigt dies voll. Es waren in Q2 sogar weniger als 27 Mio (pre Strpping) um nur eine einzige Tabelle zu zeigen:

Trotz dieser übermässigen stripiing costs hatte GPL bereits AISCs unter 1.000$ je oz! Wie Börsenbriefschreiber jüngst noch auf 1400 $ kamen ist mir schleierhaft. Wo haben die Rechnen gelernt??!??

Die Mexico Minen zu betrachten, macht in einem Quartal, wo für 3 Monate die (Lohn)Kosten liefen, aber nur einen Monat praktisch produziert wurde, keinen Sinn (aber wir wissen, auch Mexico ist in einem "normalen" Quartal um Kosten von 1k Au eqv.).

Im gesamten 1. HJ 2020 hatte GPL übrigens Stripping costs 19,313 Mio USD vs. Vorjahr 5,479 Mio. $. Letzteres ist das "normale Niveau". In 2021 wird GPL also im selben Zeitraum 15 Mio. $ GERINGERE (Gesamt-)KOSTEN haben!

Ausblick auf Q3-2020:

rechne ich mit konservativen 32 Mio. USD Gesamtkosten (inkl. moderatem Resttrpping des kaputten Pits für Q4) komme ich, diese Kosten auf konservative 40.000 Unzen verteilt auf:

AISC per gold oz sold: 800 USD !!!!

Ausblick auf Q4-2020:

rechne ich mit konservativen 31 Mio. USD Gesamtkosten (stärkerer Real unterstellt!) und verteile diese auf 45.000 Unzen Gold erhalte ich:

AISC per gold oz sold: 689 USD !!!!

ergibt im Gesamtjahr 2020

HJ 1 60,263 oz @ 1291 AISC +

HJ 2 85,000 oz @ 741 AISC =

GJ 145,263 oz @ 969 $ AISC

Ausblick auf GJ-2021:

Kostenbasis (-15m; ansonsten Zahlen wie 2020 unterstellt, d.h. höhere Kosten von Q1-2020 übernommen): 125.8m USD

Produktion konservativ geschätzt: 150.000 oz (Tucano only)

AISC Tucano: 839 US$

Nochmal: wo hat GPL ein Profitablitätsproblem, von dem einige phantasierten?

Eine Sache muss natürlich doch noch erwähnt werden. Ich war selbst überrarscht:

Derivative instruments

A significant portion of the Company’s capital, exploration, operating and administrative expenditures are

incurred in Brazilian real (“BRL”) and Mexican peso (“MXN”), while revenues from the sale of refined gold and

metal concentrates are denominated in USD. The fluctuation of the USD in relation to the BRL and MXN,

consequently, impacts the reported financial performance of the Company. To manage the Company’s

exposure to changes in the BRL and MXN exchange rate, the Company has entered into forward contracts to

purchase foreign currencies in exchange for USD at various rates and maturity dates.

As at June 30, 2020, non-deliverable forward foreign exchange contracts for BRL against USD totaling BRL

344.1 million (December 31, 2019 – BRL 418.2 million) at various pre-determined rates ranging from BRL

4.18/USD to BRL 4.45/USD, at various maturity dates until February 2021, were outstanding. The fair value of

these contracts resulted in a liability of $16.9 million at June 30, 2020 (December 31, 2019 – asset of $3.5

million). A non-deliverable forward foreign exchange contract does not require physical delivery of the

designated currencies at maturity.

The objective of the Company’s BRL/USD hedging strategy is to reduce exposure to any appreciation in the

BRL, which was at or near record lows relative to the USD at the time the contracts were entered into, and gain

better certainty with regard to the Company’s projected operating cash-flows and capital expenditures for

Tucano. In addition, the non-deliverable forward contracts were entered into at a time when the gold price was

lower. The Company has not entered any additional forward contracts since January 2020.

A weakening in the BRL such that spot rates were above the contract rates would result in a realized loss to

the Company to settle the foreign exchange contracts that mature or the recognition of an unrealized, mark-to-

market loss on contracts that are still subject to settlement. This result would effectively offset the benefit to

the Company of any decline in Tucano USD operating costs resulting from a weakened BRL in the amount of

the notional value of the contracts. These contracts represent approximately 85% of the Company’s projected

BRL expenditures for Tucano from July 2020 to February 2021 and, accordingly, approximately 15% of the

Company’s BRL expenditures remain unhedged and the Company will realize a net benefit from a weaker BRL

to the extent these unhedged expenditures are incurred.

To the extent that the June 30, 2020 BRL/USD spot market exchange rate was greater than the contract

exchange rates, the Company recorded a liability as of June 30, 2020. This liability represents the payment that

Great Panther would have to pay out under these agreements through to February 2021 assuming the

BRL/USD spot market exchange rate on settlement is the same as that on June 30, 2020 and the assumed

settlement amount is discounted to reflect the time-value-of-money.

To the extent that the BRL strengthens against the USD during this period, the payouts required under these

forward contracts will be reduced, but any reduction will be offset by increases in the USD equivalent of BRL

operating costs.

The forward contracts are settled on each maturity date irrespective of the existence of BRL operating expenses

and, accordingly, in the event that operations at Tucano are curtailed or shutdown during the period to February

2021, the counterparties to the contract will be entitled to receive or will have an obligation to pay the settlement

amount. With respect to the unhedged portion of the Company’s BRL requirements for Tucano, these costs

are fully exposed to fluctuations in the BRL/USD exchange rate, with a weakening in the BRL decreasing USD

operating costs and strengthening in the BRL increasing USD operating costs.

Das Thema ist also in halben Jahren endgültig Geschichte. Im Gegensatz zum Zeitpunkt, wo diese Hedgingpolitik als sinnvoll erachtet wurde, ist das Umfeld jetzt ein gänzlich anderes, dass GPL sich so stark fühlt, das Währungsrisiko künftig sofort voll zu tragen. Also spätestens ab Mitte Q1 profitiert GPL voll vom schwachen Real und die bis dahin anfallenden Derivate-Währungsverluste von einigen wenigen Mio. im Monat fallen dann komplett weg = weiterer Gewinnsprung vorprogrammiert, wenn der Real da bleibt, wo er aktuell ist.

Fazit: ich stelle für mich fest, dass ich viel zu gering in GPL gewichtet bin und muss die jetzt startende Gold/Silberkorrektur dringend dafür nutzen, mehr GPLs einzusammeln. Es ist das beste Goldinvestment, das es am weltweiten Kurszettel gibt. Ich kenne mit weitem Abstand kein besseres!

Meine Korrekturziele für Gold:

1780 - 1850 (1820)

Silber:

21 - 21-50 (21.23)

GDXJ 51 $

GDX 37 $

für GPL gibts keines, da bin ich aus o.g. befangen und pers. restricted

Viel Glück und frohes Shopping 😎

Ich habe mir gestern in Ruhe den Q2 Bericht angeschaut resp. quergelesen. Was soll ich sagen: absolut mind-blowing! Ich kann mich nicht entsinnen, jemals die vergangenen 15 Jahre von einer meinem mining-investments einen inhaltlich stärkeren Report gelesen zu haben!

Jede Seite, jede Tabelle strotzt nur so vor Stärke. Die GUV-Rechnung ist atemberaubend stark - selbst in diesem schwachen Q2.

Wie ihr wisst, hatte ich mit Kosten um 29 Mio. $/Quartal gerechnet, der Bericht bestätigt dies voll. Es waren in Q2 sogar weniger als 27 Mio (pre Strpping) um nur eine einzige Tabelle zu zeigen:

Trotz dieser übermässigen stripiing costs hatte GPL bereits AISCs unter 1.000$ je oz! Wie Börsenbriefschreiber jüngst noch auf 1400 $ kamen ist mir schleierhaft. Wo haben die Rechnen gelernt??!??

Die Mexico Minen zu betrachten, macht in einem Quartal, wo für 3 Monate die (Lohn)Kosten liefen, aber nur einen Monat praktisch produziert wurde, keinen Sinn (aber wir wissen, auch Mexico ist in einem "normalen" Quartal um Kosten von 1k Au eqv.).

Im gesamten 1. HJ 2020 hatte GPL übrigens Stripping costs 19,313 Mio USD vs. Vorjahr 5,479 Mio. $. Letzteres ist das "normale Niveau". In 2021 wird GPL also im selben Zeitraum 15 Mio. $ GERINGERE (Gesamt-)KOSTEN haben!

Ausblick auf Q3-2020:

rechne ich mit konservativen 32 Mio. USD Gesamtkosten (inkl. moderatem Resttrpping des kaputten Pits für Q4) komme ich, diese Kosten auf konservative 40.000 Unzen verteilt auf:

AISC per gold oz sold: 800 USD !!!!

Ausblick auf Q4-2020:

rechne ich mit konservativen 31 Mio. USD Gesamtkosten (stärkerer Real unterstellt!) und verteile diese auf 45.000 Unzen Gold erhalte ich:

AISC per gold oz sold: 689 USD !!!!

ergibt im Gesamtjahr 2020

HJ 1 60,263 oz @ 1291 AISC +

HJ 2 85,000 oz @ 741 AISC =

GJ 145,263 oz @ 969 $ AISC

Ausblick auf GJ-2021:

Kostenbasis (-15m; ansonsten Zahlen wie 2020 unterstellt, d.h. höhere Kosten von Q1-2020 übernommen): 125.8m USD

Produktion konservativ geschätzt: 150.000 oz (Tucano only)

AISC Tucano: 839 US$

Nochmal: wo hat GPL ein Profitablitätsproblem, von dem einige phantasierten?

Eine Sache muss natürlich doch noch erwähnt werden. Ich war selbst überrarscht:

Derivative instruments

A significant portion of the Company’s capital, exploration, operating and administrative expenditures are

incurred in Brazilian real (“BRL”) and Mexican peso (“MXN”), while revenues from the sale of refined gold and

metal concentrates are denominated in USD. The fluctuation of the USD in relation to the BRL and MXN,

consequently, impacts the reported financial performance of the Company. To manage the Company’s

exposure to changes in the BRL and MXN exchange rate, the Company has entered into forward contracts to

purchase foreign currencies in exchange for USD at various rates and maturity dates.

As at June 30, 2020, non-deliverable forward foreign exchange contracts for BRL against USD totaling BRL

344.1 million (December 31, 2019 – BRL 418.2 million) at various pre-determined rates ranging from BRL

4.18/USD to BRL 4.45/USD, at various maturity dates until February 2021, were outstanding. The fair value of

these contracts resulted in a liability of $16.9 million at June 30, 2020 (December 31, 2019 – asset of $3.5

million). A non-deliverable forward foreign exchange contract does not require physical delivery of the

designated currencies at maturity.

The objective of the Company’s BRL/USD hedging strategy is to reduce exposure to any appreciation in the

BRL, which was at or near record lows relative to the USD at the time the contracts were entered into, and gain

better certainty with regard to the Company’s projected operating cash-flows and capital expenditures for

Tucano. In addition, the non-deliverable forward contracts were entered into at a time when the gold price was

lower. The Company has not entered any additional forward contracts since January 2020.

A weakening in the BRL such that spot rates were above the contract rates would result in a realized loss to

the Company to settle the foreign exchange contracts that mature or the recognition of an unrealized, mark-to-

market loss on contracts that are still subject to settlement. This result would effectively offset the benefit to

the Company of any decline in Tucano USD operating costs resulting from a weakened BRL in the amount of

the notional value of the contracts. These contracts represent approximately 85% of the Company’s projected

BRL expenditures for Tucano from July 2020 to February 2021 and, accordingly, approximately 15% of the

Company’s BRL expenditures remain unhedged and the Company will realize a net benefit from a weaker BRL

to the extent these unhedged expenditures are incurred.

To the extent that the June 30, 2020 BRL/USD spot market exchange rate was greater than the contract

exchange rates, the Company recorded a liability as of June 30, 2020. This liability represents the payment that

Great Panther would have to pay out under these agreements through to February 2021 assuming the

BRL/USD spot market exchange rate on settlement is the same as that on June 30, 2020 and the assumed

settlement amount is discounted to reflect the time-value-of-money.

To the extent that the BRL strengthens against the USD during this period, the payouts required under these

forward contracts will be reduced, but any reduction will be offset by increases in the USD equivalent of BRL

operating costs.

The forward contracts are settled on each maturity date irrespective of the existence of BRL operating expenses

and, accordingly, in the event that operations at Tucano are curtailed or shutdown during the period to February

2021, the counterparties to the contract will be entitled to receive or will have an obligation to pay the settlement

amount. With respect to the unhedged portion of the Company’s BRL requirements for Tucano, these costs

are fully exposed to fluctuations in the BRL/USD exchange rate, with a weakening in the BRL decreasing USD

operating costs and strengthening in the BRL increasing USD operating costs.

Das Thema ist also in halben Jahren endgültig Geschichte. Im Gegensatz zum Zeitpunkt, wo diese Hedgingpolitik als sinnvoll erachtet wurde, ist das Umfeld jetzt ein gänzlich anderes, dass GPL sich so stark fühlt, das Währungsrisiko künftig sofort voll zu tragen. Also spätestens ab Mitte Q1 profitiert GPL voll vom schwachen Real und die bis dahin anfallenden Derivate-Währungsverluste von einigen wenigen Mio. im Monat fallen dann komplett weg = weiterer Gewinnsprung vorprogrammiert, wenn der Real da bleibt, wo er aktuell ist.

Fazit: ich stelle für mich fest, dass ich viel zu gering in GPL gewichtet bin und muss die jetzt startende Gold/Silberkorrektur dringend dafür nutzen, mehr GPLs einzusammeln. Es ist das beste Goldinvestment, das es am weltweiten Kurszettel gibt. Ich kenne mit weitem Abstand kein besseres!

Meine Korrekturziele für Gold:

1780 - 1850 (1820)

Silber:

21 - 21-50 (21.23)

GDXJ 51 $

GDX 37 $

für GPL gibts keines, da bin ich aus o.g. befangen und pers. restricted

Viel Glück und frohes Shopping 😎

Trading Spotlight

Ich kam also durch Dich auf dein "LOB" .. 🙃

Antwort auf Beitrag Nr.: 64.688.464 von iam57 am 07.08.20 20:06:15Ich meine mich zu Erinnern, dass Du Gogold mal im Rohstoffforum bei Urpferdchen, dort war ich mit Ausnahme der letzten Woche aber schon ewig nicht mehr, empfohlen hättest. Glaube so war es.

Und wenn man sich den Thread anschaut.. warste dort auch lang allein.

Hellseher sind wir alle nicht.. CT ( Charttechnik ) ist ja nur eine Unterstützung. Gut wenn es klappt und andere auch davon profitieren können. 👍 / Eines sollte man aber immer mitnehmen, bzw im Hinterkopf behalten. Allein CT bei einer Mine ist der sichere Tod. Eine Mine ist ein Loch mit einem Lügner drauf--so das alte Sprichwort. Und oft trifft es das mehr als genau.

Ich bin nur nicht allzu aktiv auf W.O bzw war es noch nie.

Grüße FF

Und wenn man sich den Thread anschaut.. warste dort auch lang allein.

Hellseher sind wir alle nicht.. CT ( Charttechnik ) ist ja nur eine Unterstützung. Gut wenn es klappt und andere auch davon profitieren können. 👍 / Eines sollte man aber immer mitnehmen, bzw im Hinterkopf behalten. Allein CT bei einer Mine ist der sichere Tod. Eine Mine ist ein Loch mit einem Lügner drauf--so das alte Sprichwort. Und oft trifft es das mehr als genau.

Ich bin nur nicht allzu aktiv auf W.O bzw war es noch nie.

Grüße FF

Antwort auf Beitrag Nr.: 64.681.111 von ffeuerstein am 07.08.20 11:23:14..wenn du Gogold im Depot hast, dann ein Lob von mir, da hast du dir ganz edles Besteck hineingelegt. Sagen wir mal so, die haben ihre Hausaufgaben gemacht, auch wenn es heute ein Rücksetzer gibt, wäre das die letzte Position, von meinen 15 Minen, die ich hergeben würde.

Antwort auf Beitrag Nr.: 64.677.367 von ffeuerstein am 07.08.20 07:22:35

..ich habe sie heute Abend, günstiger bekommen. Wie du schon richtig schreibst..man braucht Mut und Erfahrung.😎

Zitat von ffeuerstein: Als ich Saracen damals ausgebuddelt habe stand sie bei 0,4€/ct.

Wahnsinn. Und auch dort habe ich 2-3 Anläufe gebraucht, wenn ich mich recht erinnere.

Gibt es das perfekte Timing. Ja.. aber nur mit wirklich viel Glück und Erfahrung.

Schon wirklich komisch zu sehen wie viel Angst die Newbies haben. Anders kann ich die Kommentare hier nicht mehr einordnen.

https://www.wallstreet-online.de/diskussion/1190973-2751-276…

Wahrscheinlich ist es das was den meisten fehlt. Der Mut und dei Erfahrung. Nun gut. Gestern war noch mal eine gute Kaufgelegenheit und die habe ich genutzt.

..ich habe sie heute Abend, günstiger bekommen. Wie du schon richtig schreibst..man braucht Mut und Erfahrung.😎

Antwort auf Beitrag Nr.: 64.685.590 von Iboss87 am 07.08.20 16:25:45Bei GDXJ -4,5 bis -5% sind sämtliche Indexmitglieder "sichere Bänke" zum shorten.

Gold + Silber im freien Fall (und das ist sehr gesund)

Gold + Silber im freien Fall (und das ist sehr gesund)