Greencore - irische Nahrungsmittelaktie - 500 Beiträge pro Seite

eröffnet am 07.12.10 20:59:35 von

neuester Beitrag 25.10.19 21:02:52 von

neuester Beitrag 25.10.19 21:02:52 von

Beiträge: 21

ID: 1.161.799

ID: 1.161.799

Aufrufe heute: 0

Gesamt: 1.590

Gesamt: 1.590

Aktive User: 0

ISIN: IE0003864109 · WKN: 881630

1,5150

EUR

-0,98 %

-0,0150 EUR

Letzter Kurs 19:21:03 Lang & Schwarz

Neuigkeiten

Werte aus der Branche Nahrungsmittel

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 63,50 | +71,62 | |

| 1,0800 | +35,00 | |

| 1,4750 | +34,09 | |

| 11,500 | +21,05 | |

| 20,500 | +16,48 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,1400 | -17,39 | |

| 1,5409 | -22,18 | |

| 11,840 | -23,42 | |

| 0,6830 | -24,32 | |

| 1,0500 | -50,24 |

mit derzeit gut 5% Dividendenrendite...

und plant mit Northern Foods zu Essent Foods zu fusionieren.

SUZANNE LYNCH

The proposed merger between Greencore and Northern Foods has been thrown into question, following confirmation by Northern Foods that it has received an approach from Boparan Holdings Limited.

Acknowledging the request for information by Boparan, Northern Foods reiterated its support for the Greencore merger, which would create Essenta Foods.

Boparan, an investment vehicle for British chilled-food manufacturer Ranjit Singh Boparan, has a 6.6 per cent stake in Northern Foods.

Mr Boparan is the owner of the 2 Sisters Food Group, a supplier of chicken and prepared chicken products to retailers including Marks Spencer and Tesco. He is also behind the Harry Ramsden chip shop business.

Mr Boparan had been building his stake in Northern Foods since the announcement of the proposed Greencore merger from less than 3 per cent to 6.6 per cent.

In a statement to the Irish Stock Exchange this morning, Greencore said that the company “notes” the announcement, but that the board of Greencore continues to believe that the merger announced on November 17th 2010 “represents a compelling opportunity for value creation for both Greencore and Northern Foods shareholders, through the creation of a business with real scale in the industry and substantial synergies“.

According to British media reports, Mr Boparan is mounting a £300 million bid for Northern Foods.

This morning Northern Foods share price jumped 7 per cent to 65p. Having dropped by more than 10 per cent this morning in Dublin, Greencore’s shares were trading just over 4 per cent lower at 10.15 am at €1.275.

The proposed merger between Greencore and Northern Foods has been thrown into question, following confirmation by Northern Foods that it has received an approach from Boparan Holdings Limited.

Acknowledging the request for information by Boparan, Northern Foods reiterated its support for the Greencore merger, which would create Essenta Foods.

Boparan, an investment vehicle for British chilled-food manufacturer Ranjit Singh Boparan, has a 6.6 per cent stake in Northern Foods.

Mr Boparan is the owner of the 2 Sisters Food Group, a supplier of chicken and prepared chicken products to retailers including Marks Spencer and Tesco. He is also behind the Harry Ramsden chip shop business.

Mr Boparan had been building his stake in Northern Foods since the announcement of the proposed Greencore merger from less than 3 per cent to 6.6 per cent.

In a statement to the Irish Stock Exchange this morning, Greencore said that the company “notes” the announcement, but that the board of Greencore continues to believe that the merger announced on November 17th 2010 “represents a compelling opportunity for value creation for both Greencore and Northern Foods shareholders, through the creation of a business with real scale in the industry and substantial synergies“.

According to British media reports, Mr Boparan is mounting a £300 million bid for Northern Foods.

This morning Northern Foods share price jumped 7 per cent to 65p. Having dropped by more than 10 per cent this morning in Dublin, Greencore’s shares were trading just over 4 per cent lower at 10.15 am at €1.275.

GREENCORE GROUP PLC - INTERIM MANAGEMENT STATEMENT

14 January 2011

Greencore Group plc ('Greencore' or the 'Group'), today issues the following Interim Management Statement in accordance with the reporting requirements of the Transparency Regulations, 2007.

Trading Performance

Convenience Foods division

Following on from a strong performance in FY10, the underlying performance of our Convenience Foods division has remained good in the first three months of FY11, being the period ended 24 December 2010. The division recorded continuing* business revenue of €208.7m in the period, an increase of 7.6% on the comparable period in FY10 (an increase of 3.0% on a constant currency basis) despite severe adverse weather in the UK in December.

In particular, the operating performance in our two key categories of Food to Go and Prepared Meals remained strong with a continuation of the favourable underlying market trends seen in FY10. Value remains a key consumer theme and the Group's portfolio meets this need. As expected, ingredient and packaging inflation is more pronounced than in FY10; the Group is effectively managing this through a combination of selling price increases and cost reduction initiatives. Our US business traded in line with our expectations in the quarter as we completed the re-fit of the Newburyport facility and acquired a fresh sandwich business, On a Roll Inc. (announced on 7 December, 2010).

Ingredients & Property division

Following the disposal of our Malt business in FY10, we expect the contribution from the Ingredients & Property division to represent a much more modest part of the overall Group result. On a continuing basis*, trading in the three months ended 24 December 2010 was down on the same period last year, principally due to the timing of small property disposals.

Financial Position

The Group has a strong balance sheet and is well capitalised to meet the operational and development needs of the business. As previously outlined, the Group's interest expense is expected to be significantly lower in FY11, reflecting the full year impact of prior year disposals and the related debt restructuring.

Outlook

While we are at an early point in our financial year, assuming an average EUR/GBP exchange rate in FY11 in the range of 0.85 to 0.88 and based on our expectation of continued strong performance in Convenience Foods, the Board continues to expect to deliver strong growth on a continuing basis in FY11.

Next Trading Announcement

The next update on Greencore trading is expected to be issued alongside the issue of the prospectus relating to the Merger with Northern Foods Plc.

Merger with Northern Foods Plc

The board of Greencore continues to believe that the recommended all share merger of Greencore and Northern Foods to form Essenta Foods (the 'Merger'), announced on 17 November 2010, represents a compelling opportunity for value creation for both Greencore and Northern Foods shareholders, through the creation of a business with real scale in the industry and substantial synergies.

In common with the board of Northern Foods Plc, the board of Greencore continues unanimously to recommend shareholders to vote in favour of the Merger at the shareholder meeting on 31 January 2011.

14 January 2011

Greencore Group plc ('Greencore' or the 'Group'), today issues the following Interim Management Statement in accordance with the reporting requirements of the Transparency Regulations, 2007.

Trading Performance

Convenience Foods division

Following on from a strong performance in FY10, the underlying performance of our Convenience Foods division has remained good in the first three months of FY11, being the period ended 24 December 2010. The division recorded continuing* business revenue of €208.7m in the period, an increase of 7.6% on the comparable period in FY10 (an increase of 3.0% on a constant currency basis) despite severe adverse weather in the UK in December.

In particular, the operating performance in our two key categories of Food to Go and Prepared Meals remained strong with a continuation of the favourable underlying market trends seen in FY10. Value remains a key consumer theme and the Group's portfolio meets this need. As expected, ingredient and packaging inflation is more pronounced than in FY10; the Group is effectively managing this through a combination of selling price increases and cost reduction initiatives. Our US business traded in line with our expectations in the quarter as we completed the re-fit of the Newburyport facility and acquired a fresh sandwich business, On a Roll Inc. (announced on 7 December, 2010).

Ingredients & Property division

Following the disposal of our Malt business in FY10, we expect the contribution from the Ingredients & Property division to represent a much more modest part of the overall Group result. On a continuing basis*, trading in the three months ended 24 December 2010 was down on the same period last year, principally due to the timing of small property disposals.

Financial Position

The Group has a strong balance sheet and is well capitalised to meet the operational and development needs of the business. As previously outlined, the Group's interest expense is expected to be significantly lower in FY11, reflecting the full year impact of prior year disposals and the related debt restructuring.

Outlook

While we are at an early point in our financial year, assuming an average EUR/GBP exchange rate in FY11 in the range of 0.85 to 0.88 and based on our expectation of continued strong performance in Convenience Foods, the Board continues to expect to deliver strong growth on a continuing basis in FY11.

Next Trading Announcement

The next update on Greencore trading is expected to be issued alongside the issue of the prospectus relating to the Merger with Northern Foods Plc.

Merger with Northern Foods Plc

The board of Greencore continues to believe that the recommended all share merger of Greencore and Northern Foods to form Essenta Foods (the 'Merger'), announced on 17 November 2010, represents a compelling opportunity for value creation for both Greencore and Northern Foods shareholders, through the creation of a business with real scale in the industry and substantial synergies.

In common with the board of Northern Foods Plc, the board of Greencore continues unanimously to recommend shareholders to vote in favour of the Merger at the shareholder meeting on 31 January 2011.

Sunday March 13 2011

LAST week Greencore chief executive Patrick Coveney, brother of new Agriculture Minister Simon, finally bowed to the inevitable and walked away from his company's proposed merger with UK own-label food producer Northern Foods.

Ever since Ranjit Boparan gatecrashed the Greencore/ Northern Foods merger last January with a blockbuster £342m all-cash bid, it has been clear that Coveney's plan to merge the firms was hanging by a thread. Last week's announcement was merely acknowledgement of what most observers had concluded -- that Greencore couldn't afford to match the price Boparan was offering.

So where does Greencore go from here? With the company capitalised at a mere €243m at the current share price and its debts having been reduced to €193m following last year's disposal of its malting business, Greencore, the largest sandwich producer in the UK, is starting to look like an acquisition target itself.

With its Freshways subsidiary already the largest producer of sandwiches in Ireland, the acquisition of Greencore would give the Kerry Group top slot in the UK sandwich market also. Maybe Coveney should give Kerry boss Stan McCarthy a call.

LAST week Greencore chief executive Patrick Coveney, brother of new Agriculture Minister Simon, finally bowed to the inevitable and walked away from his company's proposed merger with UK own-label food producer Northern Foods.

Ever since Ranjit Boparan gatecrashed the Greencore/ Northern Foods merger last January with a blockbuster £342m all-cash bid, it has been clear that Coveney's plan to merge the firms was hanging by a thread. Last week's announcement was merely acknowledgement of what most observers had concluded -- that Greencore couldn't afford to match the price Boparan was offering.

So where does Greencore go from here? With the company capitalised at a mere €243m at the current share price and its debts having been reduced to €193m following last year's disposal of its malting business, Greencore, the largest sandwich producer in the UK, is starting to look like an acquisition target itself.

With its Freshways subsidiary already the largest producer of sandwiches in Ireland, the acquisition of Greencore would give the Kerry Group top slot in the UK sandwich market also. Maybe Coveney should give Kerry boss Stan McCarthy a call.

Trading Spotlight

By Laura Noonan

Monday May 02 2011

GREENCORE has asked advisers Barclays Capital to run the rule over Uniq but is "weeks away" from making a decision on a bid, sources said last night.

Greencore, which recently failed to clinch a €2bn merger with Northern Foods, sees Uniq as its next consolidation target.

UK-based Uniq has effectively put itself on the market after ceding a 90pc stake in its equity-to-pension holders to repair a massive pensions deficit.

With a portfolio including prepared sandwiches, salads and deserts, its business is seen as complementary to Greencore's food-to-go proposition.

Sources last night confirmed Barclays was looking over Uniq on behalf of Greencore, but stressed there was no imminent bid or deal.

Greencore is mulling over a number of deals.

"Uniq is just one thing that's being looked at," a source added. Greencore declined to comment on any possible deal with Uniq.

While significantly smaller than Northern Foods, Uniq's annual revenues of £312m (€352m) would be a significant addition to Greencore's sales of €856m.

Monday May 02 2011

GREENCORE has asked advisers Barclays Capital to run the rule over Uniq but is "weeks away" from making a decision on a bid, sources said last night.

Greencore, which recently failed to clinch a €2bn merger with Northern Foods, sees Uniq as its next consolidation target.

UK-based Uniq has effectively put itself on the market after ceding a 90pc stake in its equity-to-pension holders to repair a massive pensions deficit.

With a portfolio including prepared sandwiches, salads and deserts, its business is seen as complementary to Greencore's food-to-go proposition.

Sources last night confirmed Barclays was looking over Uniq on behalf of Greencore, but stressed there was no imminent bid or deal.

Greencore is mulling over a number of deals.

"Uniq is just one thing that's being looked at," a source added. Greencore declined to comment on any possible deal with Uniq.

While significantly smaller than Northern Foods, Uniq's annual revenues of £312m (€352m) would be a significant addition to Greencore's sales of €856m.

danke fuer all die infos habe mir den wert auf die watchlist gesetzt, wobei ich eigentlich nicht mehr in fallende Messer greifen wollte. Was meinen den die Chartis wann hier ein Boden gefunden ist ?

habe mir erst jetzt den report vom 6.12. angesehen;

trotz reduziertem Divi-Vorschlag immer noch >8% Rendite, allerdings weiterhin extrem wacklige bilanz

trotz reduziertem Divi-Vorschlag immer noch >8% Rendite, allerdings weiterhin extrem wacklige bilanz

Rendite inzwischen fast geviertelt durch Kursanstieg

Bilanz besser, aber immer noch nicht solide

Bilanz besser, aber immer noch nicht solide

Antwort auf Beitrag Nr.: 46.072.524 von R-BgO am 18.12.13 13:03:14und deswegen jetzt bis auf ein Erinnerungsstück verkauft

inzwischen

wenigstens rund 30% EK-Quote

Antwort auf Beitrag Nr.: 51.562.509 von R-BgO am 23.01.16 11:25:40

irgendwie mögen sie keine soliden Bilanzen,

per 30.9.2016 wieder nur 22%

Antwort auf Beitrag Nr.: 51.562.509 von R-BgO am 23.01.16 11:25:40http://seekingalpha.com/article/3098626-greencore-group-is-r…

Antwort auf Beitrag Nr.: 53.955.275 von R-BgO am 26.12.16 11:57:43

mal sehen, ob das Jahresergebnis rot oder schwarz wird...

und um ganz sicher zu gehen,

haben sie in H1 mal wieder einen dicken Zukauf gemacht;mal sehen, ob das Jahresergebnis rot oder schwarz wird...

ich mag "Fress-"Aktien (*), auch diese -- und stosse bei Gelegenheit meine restlichen Agrar-Aktien vollständig ab.

Manche Erkenntnisse dauern etwas länger...

(*) "Restaurant-"Aktien hingegen nicht. Ist ein Spezial-, "Mode-" und machmal auch noch "Immo-"Geschäft --> anderes Börsensegment (ohne Expertise meinerseits...).

Manche Erkenntnisse dauern etwas länger...

(*) "Restaurant-"Aktien hingegen nicht. Ist ein Spezial-, "Mode-" und machmal auch noch "Immo-"Geschäft --> anderes Börsensegment (ohne Expertise meinerseits...).

ummmmmff

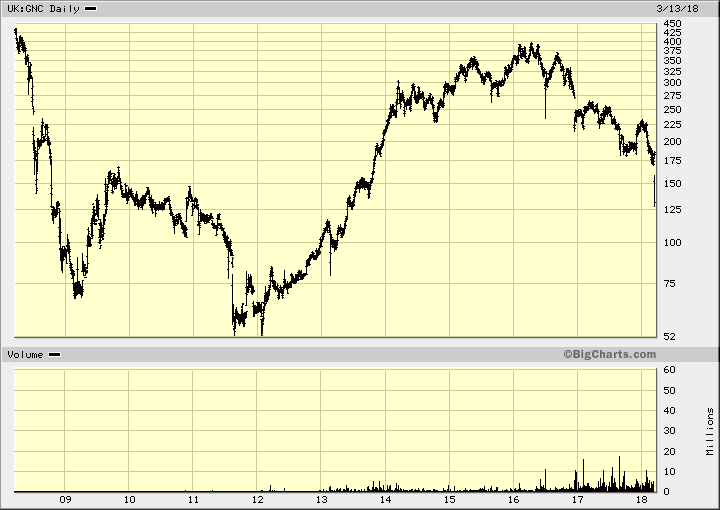

https://www.bloomberg.com/news/articles/2018-03-13/greencore…=>

...The shares tumbled as much as 30 percent in London, the most on record, after the Irish food company forecast earnings for this year below analysts’ expectations as Chief Executive Officer Patrick Coveney seeks to tackle persistent problems in its U.S. business.

Greencore will also be halting fresh production at its Rhode Island facility from March 25...

=> soviel zum Thema - mal wieder: Sell-side-Analysten (aufgrund derer Analysen ich auch nicht handel; aber in Einzelfälle die Marktreaktion darauf beobachte...)

Wobei: wie kann man sich mit Fressaktien so vertun???

=> dieses Teil muss - mMn - erst so konsolidieren wie seinerzeit 2011/12, bevor man über Nachkäufe auch nur nachdenkt...

Antwort auf Beitrag Nr.: 57.265.138 von faultcode am 13.03.18 16:20:52

https://www.finanzen.net/nachricht/aktien/maerkte-europa-erh…

=>

Sodexo hatte am 31.12.2017 427.268 Mitarbeiter!

--> ich denke, da kommt ein Umbau mit Konzentration auf Wachstum und Profit...

zuletzt, 2015 - 2017, nur noch marginal gewachsen...

nun auch Sodexo

An der Pariser Börse brechen Sodexo um 12,5 Prozent ein. Der Caterer hat nach einer schwachen Entwicklung im zweiten Geschäftsquartal den Ausblick gesenkt. Den organischen Umsatzzuwachs sieht Sodexo 2017/18 nur noch bei 1 bis 1,5 Prozent. Bisher wurde ein Plus von 2 bis 4 Prozent in Aussicht gestellt. Bei der bereinigten Gewinnmarge erwartet die Sodexo SA nur noch 5,7 Prozent nach bisher 6,5 Prozent. https://www.finanzen.net/nachricht/aktien/maerkte-europa-erh…

=>

Sodexo hatte am 31.12.2017 427.268 Mitarbeiter!

--> ich denke, da kommt ein Umbau mit Konzentration auf Wachstum und Profit...

zuletzt, 2015 - 2017, nur noch marginal gewachsen...

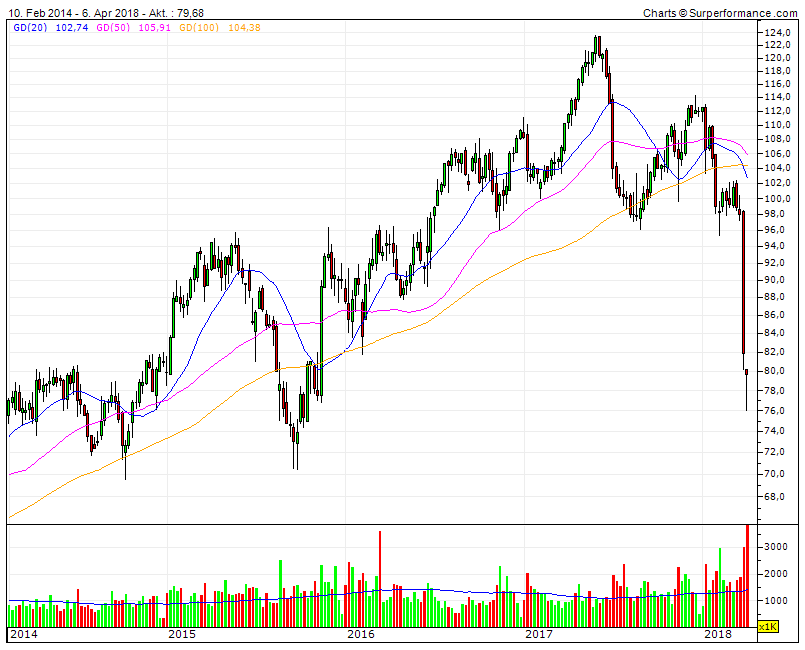

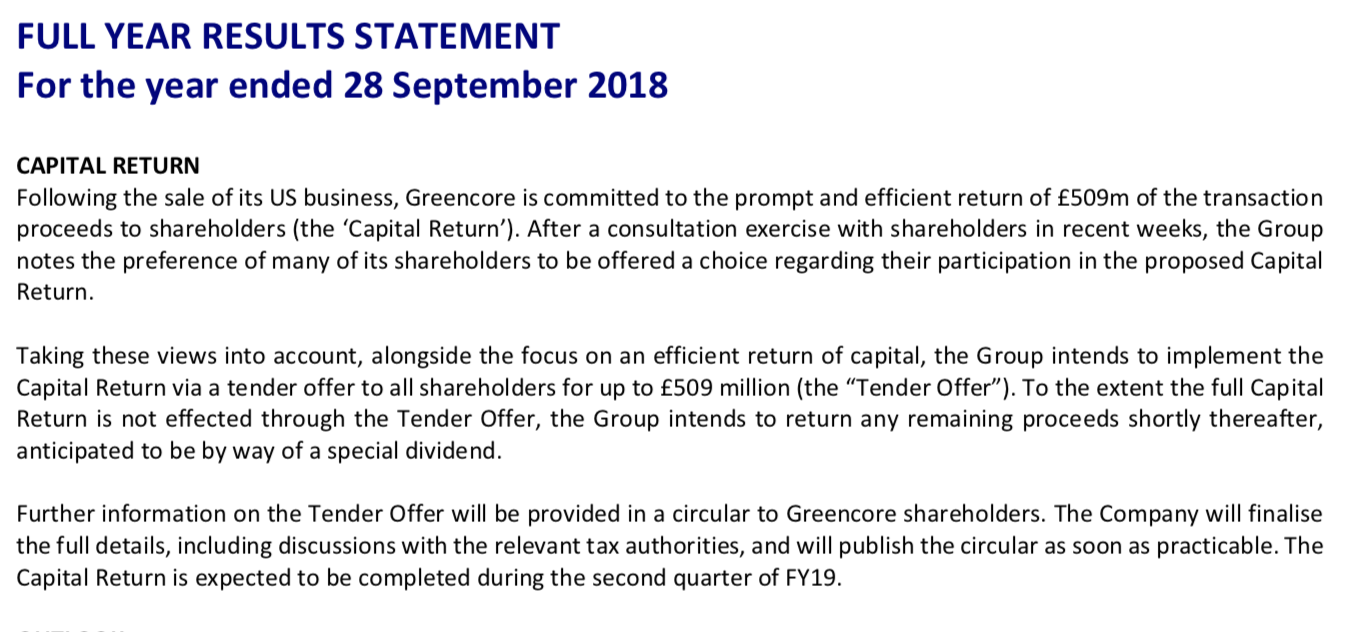

sie verkaufen gerade ihre US-Sparte...

Antwort auf Beitrag Nr.: 59.134.085 von R-BgO am 04.11.18 13:12:31

Antwort auf Beitrag Nr.: 59.357.192 von R-BgO am 04.12.18 10:28:30

Antwort auf Beitrag Nr.: 57.265.138 von faultcode am 13.03.18 16:20:52ich hab meine Position verkauft, und nur aus einem Grund:

• illiquider Handel im ADR. Und das obwohl er sponsored ist - und ich daher verkaufen konnte (zu einem Preis der mMn OK war: USD12)

--> dieser illiquider Handel betrifft nicht nur Greencore, sondern z.Z. auch andere Nebenwerte fernab der Heimatbörse; und ist kein gutes Zeichen mMn für die Verfassung des globalen Aktienmarktes im Allgemeinen

• illiquider Handel im ADR. Und das obwohl er sponsored ist - und ich daher verkaufen konnte (zu einem Preis der mMn OK war: USD12)

--> dieser illiquider Handel betrifft nicht nur Greencore, sondern z.Z. auch andere Nebenwerte fernab der Heimatbörse; und ist kein gutes Zeichen mMn für die Verfassung des globalen Aktienmarktes im Allgemeinen

Beitrag zu dieser Diskussion schreiben

Zu dieser Diskussion können keine Beiträge mehr verfasst werden, da der letzte Beitrag vor mehr als zwei Jahren verfasst wurde und die Diskussion daraufhin archiviert wurde.

Bitte wenden Sie sich an feedback@wallstreet-online.de und erfragen Sie die Reaktivierung der Diskussion oder starten Sie eine neue Diskussion.

Investoren beobachten auch:

| Wertpapier | Perf. % |

|---|---|

| +0,74 | |

| +0,43 | |

| -11,11 | |

| 0,00 | |

| +2,51 | |

| -0,71 | |

| +1,09 | |

| +1,88 | |

| -0,87 | |

| -3,70 |

Meistdiskutiert

| Wertpapier | Beiträge | |

|---|---|---|

| 237 | ||

| 87 | ||

| 85 | ||

| 83 | ||

| 62 | ||

| 59 | ||

| 56 | ||

| 47 | ||

| 34 | ||

| 34 |