Gulf Keystone - 500 Beiträge pro Seite

eröffnet am 19.12.11 09:44:04 von

neuester Beitrag 09.02.12 11:46:06 von

neuester Beitrag 09.02.12 11:46:06 von

Beiträge: 240

ID: 1.171.135

ID: 1.171.135

Aufrufe heute: 1

Gesamt: 15.393

Gesamt: 15.393

Aktive User: 0

ISIN: BMG4209G2077 · WKN: A2DGZ5 · Symbol: GVP1

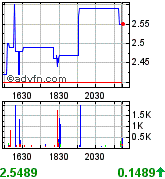

1,3260

EUR

+0,76 %

+0,0100 EUR

Letzter Kurs 18:32:35 Tradegate

Neuigkeiten

22.04.24 · EQS Group AG |

18.04.24 · EQS Group AG |

28.02.24 · EQS Group AG |

Werte aus der Branche Öl/Gas

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,7000 | +53,15 | |

| 6,0800 | +43,06 | |

| 12,990 | +38,93 | |

| 0,5070 | +31,52 | |

| 1,0200 | +24,39 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 5,0300 | -7,71 | |

| 6,7200 | -8,82 | |

| 0,6500 | -12,16 | |

| 13,420 | -21,98 | |

| 20,000 | -33,33 |

Hier bahnt sich eine Riesebuebernahme durch Exxon an

Seht mal unter Oel und Gaswerte

Achtung!

Nur mit Limit kaufen

Heute frueh sind die ersten mit Kursen ueber 6 Euro abgezogen worden

Wenn es aufgeht stehen die bei 8

Aber trotzdem

Nur kontrolliert rein

Seht mal unter Oel und Gaswerte

Achtung!

Nur mit Limit kaufen

Heute frueh sind die ersten mit Kursen ueber 6 Euro abgezogen worden

Wenn es aufgeht stehen die bei 8

Aber trotzdem

Nur kontrolliert rein

WKN ISIN ??

Oder hast du nur grosse Töne ?

Oder hast du nur grosse Töne ?

Antwort auf Beitrag Nr.: 42.497.481 von Loserin am 19.12.11 09:48:51A0B72B

schau mal auf www.reuters.de

unter exxon.....

schau mal auf www.reuters.de

unter exxon.....

Gulf Keystone Petroleum Aktie (WKN A0B72B / ISIN BMG4209G1087)

Antwort auf Beitrag Nr.: 42.497.489 von Loserin am 19.12.11 09:50:42aus dem handelsblatt

Exxon plant offenbar Milliardenübernahme

18.12.2011, 18:34 Uhr

Der Ölmulti Exxon bemüht sich einem Zeitungsbericht zufolge um eine Milliardenübernahme in Großbritannien. Der US-Ölriese wolle für sieben Milliarden Pfund Gulf Keystone Petroleum kaufen, berichtet der „Independent“.

Exxon plant offenbar Milliardenübernahme

18.12.2011, 18:34 Uhr

Der Ölmulti Exxon bemüht sich einem Zeitungsbericht zufolge um eine Milliardenübernahme in Großbritannien. Der US-Ölriese wolle für sieben Milliarden Pfund Gulf Keystone Petroleum kaufen, berichtet der „Independent“.

Trading Spotlight

Zeitung: Exxon strebt Milliardenübernahme in Großbritannien an

Montag, 19. Dezember 2011, 07:55 Uhr

London (Reuters) - Exxon bemüht sich einem Zeitungsbericht zufolge um eine Milliardenübernahme in Großbritannien.

Der US-Ölriese wolle für sieben Milliarden Pfund Gulf Keystone Petroleum kaufen, berichtete der "Independent" am Sonntag. Exxon erwäge, 800 Pence je Aktie für den Öl-Förderer zu zahlen. Gulf Keystone hat zuletzt große Vorkommen in der semi-autonomen kurdischen Region im Irak entdeckt. Exxon wie auch Gulf Keystone wollten sich zu dem Bericht nicht äußern.

Am Freitag waren die Anteilsscheine von Gulf Keystone bei 165,5 Pence aus dem Handel gegangen. Damit wurde die Firma mit 1,4 Milliarden Pfund bewertet. Exxon ist bereits im Norden Kurdistans und damit auch auf irakischem Gebiet aktiv. Mitte Oktober unterzeichnete der Konzern einen entsprechenden Vertrag mit der Regionalregierung. Dieser Schritt erzürnte den Irak. Die Regierung in Bagdad hält die Vereinbarungen für illegal.

http://de.reuters.com/article/companiesNews/idDEBEE7BI00Y201…

Montag, 19. Dezember 2011, 07:55 Uhr

London (Reuters) - Exxon bemüht sich einem Zeitungsbericht zufolge um eine Milliardenübernahme in Großbritannien.

Der US-Ölriese wolle für sieben Milliarden Pfund Gulf Keystone Petroleum kaufen, berichtete der "Independent" am Sonntag. Exxon erwäge, 800 Pence je Aktie für den Öl-Förderer zu zahlen. Gulf Keystone hat zuletzt große Vorkommen in der semi-autonomen kurdischen Region im Irak entdeckt. Exxon wie auch Gulf Keystone wollten sich zu dem Bericht nicht äußern.

Am Freitag waren die Anteilsscheine von Gulf Keystone bei 165,5 Pence aus dem Handel gegangen. Damit wurde die Firma mit 1,4 Milliarden Pfund bewertet. Exxon ist bereits im Norden Kurdistans und damit auch auf irakischem Gebiet aktiv. Mitte Oktober unterzeichnete der Konzern einen entsprechenden Vertrag mit der Regionalregierung. Dieser Schritt erzürnte den Irak. Die Regierung in Bagdad hält die Vereinbarungen für illegal.

http://de.reuters.com/article/companiesNews/idDEBEE7BI00Y201…

wenn irgendwas an diesen gerüchten wahr wäre.....würde der kurs nicht bei 195pb stehen

Mag sein, dass es nur ein Gerücht ist. Aber wenn überhaupt nichts dran sein sollte, warum dementieren die Firmen die Nachricht nicht, sondern schweigen sich auf Nachfrage lieber aus?

Gruß hergis

Gruß hergis

aus dem independent

US oil supermajor Exxon Mobil is understood to have sounded out London-listed Gulf Keystone Petroleum (GKP) over a possible deal that could value the Kurdistan-focused group at around £7bn.

GKP has a market capitalisation of around £1.5bn and is listed on the junior Aim market, but its chief executive, Todd Kozel, believes the group could eventually go for double-figure billions. GKP is sitting on what is considered to be one of the world's great recent oil finds – Shaikan, about 50 miles north-west of Kurdistan's capital, Erbil – but the regional government is known to want a supermajor on board to properly fund and develop the field.

It is thought that the board would not accept the estimated £8-a-share that Exxon is considering and that a number of other companies, perhaps including China's Sinopec and Californian giant Chevron, are monitoring the situation. There is even some speculation that an informal four-way auction for GKP might be under way, while it is also believed that the company has spoken to at least two smaller businesses about potentially developing its assets in a joint venture.

Last month, it emerged that Exxon was the first of the oil industry's giants to enter Kurdistan, taking six licences. However, this has angered the government in Baghdad because there are old territorial disputes between Iraq and Kurdistan.

Baghdad had threatened to terminate Exxon's existing deal in southern Iraq and it had been reported that the US giant might reconsider its licences in Kurdistan. However, the lucrative potential of the Kurdistan fields means that analysts expect Exxon will pursue opportunities in the semi-autonomous region and may already have taken additional positions to those licences previously revealed.

There are suggestions that Exxon's interest in GKP was discussed at a board meeting 10 days ago and that initial soundings may have been taken at least six weeks ago. Last month, much of the oil world descended on Erbil for a conference that highlighted the extraordinary oil opportunities in Kurdistan, with Mr Kozel one of the key speakers.

It is believed that Mr Kozel would be happy to sell up soon and has even started mulling over his next venture. The American businessman is one of the most colourful figures in the City and has a base of devoted retail investors who are waiting for a takeover of GKP to make them rich.

GKP declined to comment. Exxon did not return calls.

inShare

US oil supermajor Exxon Mobil is understood to have sounded out London-listed Gulf Keystone Petroleum (GKP) over a possible deal that could value the Kurdistan-focused group at around £7bn.

GKP has a market capitalisation of around £1.5bn and is listed on the junior Aim market, but its chief executive, Todd Kozel, believes the group could eventually go for double-figure billions. GKP is sitting on what is considered to be one of the world's great recent oil finds – Shaikan, about 50 miles north-west of Kurdistan's capital, Erbil – but the regional government is known to want a supermajor on board to properly fund and develop the field.

It is thought that the board would not accept the estimated £8-a-share that Exxon is considering and that a number of other companies, perhaps including China's Sinopec and Californian giant Chevron, are monitoring the situation. There is even some speculation that an informal four-way auction for GKP might be under way, while it is also believed that the company has spoken to at least two smaller businesses about potentially developing its assets in a joint venture.

Last month, it emerged that Exxon was the first of the oil industry's giants to enter Kurdistan, taking six licences. However, this has angered the government in Baghdad because there are old territorial disputes between Iraq and Kurdistan.

Baghdad had threatened to terminate Exxon's existing deal in southern Iraq and it had been reported that the US giant might reconsider its licences in Kurdistan. However, the lucrative potential of the Kurdistan fields means that analysts expect Exxon will pursue opportunities in the semi-autonomous region and may already have taken additional positions to those licences previously revealed.

There are suggestions that Exxon's interest in GKP was discussed at a board meeting 10 days ago and that initial soundings may have been taken at least six weeks ago. Last month, much of the oil world descended on Erbil for a conference that highlighted the extraordinary oil opportunities in Kurdistan, with Mr Kozel one of the key speakers.

It is believed that Mr Kozel would be happy to sell up soon and has even started mulling over his next venture. The American businessman is one of the most colourful figures in the City and has a base of devoted retail investors who are waiting for a takeover of GKP to make them rich.

GKP declined to comment. Exxon did not return calls.

inShare

punkt für dich

wie siehst du den weiteren verlauf....?

wie siehst du den weiteren verlauf....?

aus der ftd

GKP kommt dem Bericht zufolge derzeit lediglich auf eine Marktkapitalisierung von 1,5 Milliarden Pfund. GKP-Chef Todd Kozel sehe den Unternehmenswert aber bei einer möglicherweise zweistelligen Milliardensumme. GKP lehnte eine Stellungnahme auf Nachfrage der Zeitung ab. Exxon rief nicht zurück.

GKP kommt dem Bericht zufolge derzeit lediglich auf eine Marktkapitalisierung von 1,5 Milliarden Pfund. GKP-Chef Todd Kozel sehe den Unternehmenswert aber bei einer möglicherweise zweistelligen Milliardensumme. GKP lehnte eine Stellungnahme auf Nachfrage der Zeitung ab. Exxon rief nicht zurück.

für ein abverkauf fehlt mir das volumen..... bleibe mal mit meiner posi dabei.

Zitat von ikarusfly: wie siehst du den weiteren verlauf....?

schwer zu sagen - im Moment ist das Ganze ja sehr spekulativ. Wenn die Nachricht sich erhärtet, geht's natürlich schnell nach oben. Und solange nicht ausdrücklich dementiert wird, glaube ich auch nicht, dass die Kurse allzu stark abbröckeln.

Ich bleibe auf jeden Fall mit einer kleinen Position drin.

mich würde interessieren, wie der independent auf die 8 pfund kommt

zieht jetzt aber mächtig an.....

aus cnbc

U.S. oil major Exxon Mobil Corp is mulling a 7 billion pound ($10.9 billion) takeover of Kurdistan-focused explorer Gulf Keystone Petroleum, the Independent on Sunday reported.

Exxon Mobile

Robert F. Bukaty / AP

Gulf Keystone Petroleum [GFKSY 0.00 --- UNCH ] shares opened up 21 percent on Monday following the report. Gulf Keystone declined to comment.

The newspaper said that Exxon [XOM 80.16 0.13 (+0.16%) ] is considering making an estimated 800 pence per share bid for Britain's Gulf Keystone, which has made huge oil finds in the semi-autonomous Kurdistan region of Iraq.

"It's not our practice to comment on media reports, rumors or speculation," an Exxon spokesman told Reuters in an emailed statement.

Exxon has "sounded out" Gulf Keystone about the possible deal, said the report without citing its sources, adding that it is thought that the company would not accept an offer at the 800 pence per share level.

Shares in Gulf Keystone closed at 165.5 pence on Friday, valuing the firm at 1.4 billion pounds.

Exxon became the first major to move into the northern Kurdish region in mid-October when it signed with the Kurdistan Regional Government (KRG) for six exploration blocks, a move which has angered the Baghdad government. Baghdad has said any oil deals signed with the KRG are illegal.

U.S. oil major Exxon Mobil Corp is mulling a 7 billion pound ($10.9 billion) takeover of Kurdistan-focused explorer Gulf Keystone Petroleum, the Independent on Sunday reported.

Exxon Mobile

Robert F. Bukaty / AP

Gulf Keystone Petroleum [GFKSY 0.00 --- UNCH ] shares opened up 21 percent on Monday following the report. Gulf Keystone declined to comment.

The newspaper said that Exxon [XOM 80.16 0.13 (+0.16%) ] is considering making an estimated 800 pence per share bid for Britain's Gulf Keystone, which has made huge oil finds in the semi-autonomous Kurdistan region of Iraq.

"It's not our practice to comment on media reports, rumors or speculation," an Exxon spokesman told Reuters in an emailed statement.

Exxon has "sounded out" Gulf Keystone about the possible deal, said the report without citing its sources, adding that it is thought that the company would not accept an offer at the 800 pence per share level.

Shares in Gulf Keystone closed at 165.5 pence on Friday, valuing the firm at 1.4 billion pounds.

Exxon became the first major to move into the northern Kurdish region in mid-October when it signed with the Kurdistan Regional Government (KRG) for six exploration blocks, a move which has angered the Baghdad government. Baghdad has said any oil deals signed with the KRG are illegal.

Mir sind in STU folgende Umsätze aufgefallen , heute morgen

09:00:54

5,00 400 2.000 14.400 96.350

08:57:09

7,25 1.000 7.250 14.000 94.350

08:36:32

6,70 13.000 87.100 13.000 87.100

Handelsplatz:

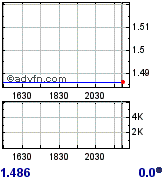

2,45

€

+0,548 €

+28,81 %

11:27:44 18.382 107.581,599 €

Kurs Zeit Aktienkurs

Schluss 16.12. 1,902

Eröffnung 6,70

Tageshoch 7,25

Tagestief 2,364

52-Wochen-Hoch 08:57 7,25

52-Wochen-Tief 09.08. 1,039

Times & Sales | Historische Kurse »

wer hat den da so teuer gekauft ?

09:00:54

5,00 400 2.000 14.400 96.350

08:57:09

7,25 1.000 7.250 14.000 94.350

08:36:32

6,70 13.000 87.100 13.000 87.100

Handelsplatz:

2,45

€

+0,548 €

+28,81 %

11:27:44 18.382 107.581,599 €

Kurs Zeit Aktienkurs

Schluss 16.12. 1,902

Eröffnung 6,70

Tageshoch 7,25

Tagestief 2,364

52-Wochen-Hoch 08:57 7,25

52-Wochen-Tief 09.08. 1,039

Times & Sales | Historische Kurse »

wer hat den da so teuer gekauft ?

Antwort auf Beitrag Nr.: 42.498.205 von Loserin am 19.12.11 12:18:03ich denke da haben einige die 800 pence erhofft

wer unlimitiert kauft wird abgezockt

kann noch gutgehen,mal schauen

wer unlimitiert kauft wird abgezockt

kann noch gutgehen,mal schauen

Man munkelt von 800 Pence

Das wären 8 GBP = 9,52903 EURO

Das wären 8 GBP = 9,52903 EURO

bin mal eine posi long

bisher keine dementis

.....mal sehen ob noch was kommt

bisher keine dementis

.....mal sehen ob noch was kommt

soeben auf finanznachrichten

Exxon Mobil steht vor Milliardenübernahme in Großbritannien

Nach Medienberichten steht das größte an der Börse notierte Unternehmen vor einer Milliardenübernahme in Großbritannien. Das Ziel der Übernahme soll Gulf Keystone Petroleum sein.

7 Milliarden Pfund für Gulf Keystone Petroleum

Das Ölförderunternehmen Gulf Keystone Petroleum wird an der Londoner Börse im "Alternative Investment Market" gehandelt und hat sich auf die Förderung aus unterentwickelten Öl- und Gasfeldern spezialisiert. Zuletzt machte das Unternehmen durch die Entdeckung eines großen Ölvorkommens in einem Ölfeld in der halbautonomischen, kurdischen Nordregion des Iraks auf sich aufmerksam.

Zum Wochenschluss am Freitag wurden die Aktien von Gulf Keystone Petroleum mit 165,5 Pence bewertet. Exxon Mobil ist laut eines Berichts von "The Independent" bereit bis zu 800 Pence für die Anteile des Unternehmens zu bezahlen. Insgesamt wird Gulf Keystone Petroleum dadurch mit 7 Milliarden britische Pfund bewertet.

Positive Quartalszahlen bei Exxon Mobil

Im dritten Quartal konnte Exxon Mobil den Gewinn um 41 Prozent auf 10,33 Milliarden Dollar (2,13 USD pro Aktie) steigern. Besonders gut liefen die Raffinerie-Sparte, die international zulegen konnte und die Exploration und Förderung außerhalb der USA.

Exxon Mobil ist derzeit nach der Marktkapitalisierung das wertvollste an der Börse gehandelte Unternehmen der Welt und ging im Jahr 1999 aus dem Zusammenschluss von Exxon und Mobil Oil hervor.

Exxon Mobil steht vor Milliardenübernahme in Großbritannien

Nach Medienberichten steht das größte an der Börse notierte Unternehmen vor einer Milliardenübernahme in Großbritannien. Das Ziel der Übernahme soll Gulf Keystone Petroleum sein.

7 Milliarden Pfund für Gulf Keystone Petroleum

Das Ölförderunternehmen Gulf Keystone Petroleum wird an der Londoner Börse im "Alternative Investment Market" gehandelt und hat sich auf die Förderung aus unterentwickelten Öl- und Gasfeldern spezialisiert. Zuletzt machte das Unternehmen durch die Entdeckung eines großen Ölvorkommens in einem Ölfeld in der halbautonomischen, kurdischen Nordregion des Iraks auf sich aufmerksam.

Zum Wochenschluss am Freitag wurden die Aktien von Gulf Keystone Petroleum mit 165,5 Pence bewertet. Exxon Mobil ist laut eines Berichts von "The Independent" bereit bis zu 800 Pence für die Anteile des Unternehmens zu bezahlen. Insgesamt wird Gulf Keystone Petroleum dadurch mit 7 Milliarden britische Pfund bewertet.

Positive Quartalszahlen bei Exxon Mobil

Im dritten Quartal konnte Exxon Mobil den Gewinn um 41 Prozent auf 10,33 Milliarden Dollar (2,13 USD pro Aktie) steigern. Besonders gut liefen die Raffinerie-Sparte, die international zulegen konnte und die Exploration und Förderung außerhalb der USA.

Exxon Mobil ist derzeit nach der Marktkapitalisierung das wertvollste an der Börse gehandelte Unternehmen der Welt und ging im Jahr 1999 aus dem Zusammenschluss von Exxon und Mobil Oil hervor.

aber wie kommen die auf 800 pence

hab ich mich auch schon gefragt

ich hab ne mail an den redakteur vom indpendent geschrieben

wahrscheinlich bekomm ich keine antwort

vielleicht ist das der wert der felder im irak

oder der gesamten öl/gasreserven des unternehmens

ich kauf noch mal nach....

ich hab ne mail an den redakteur vom indpendent geschrieben

wahrscheinlich bekomm ich keine antwort

vielleicht ist das der wert der felder im irak

oder der gesamten öl/gasreserven des unternehmens

ich kauf noch mal nach....

nochmal ne schippe zu 205 geladen

Antwort auf Beitrag Nr.: 42.498.361 von ikarusfly am 19.12.11 12:52:55interesse in london ist enorm

Antwort auf Beitrag Nr.: 42.498.364 von Frhstck am 19.12.11 12:54:02aber der markt reagiert noch nicht auf die gerüchte

Antwort auf Beitrag Nr.: 42.498.364 von Frhstck am 19.12.11 12:54:02bei solchen news ist dir aufmerksamkeit garantiert........mir fehlt dennoch das volumen, viele trauen dem braten nicht. für heute dürfte es gewesen sein. wenn eine offerte gemacht wird, dann außerhalb der börsenzeit.

Antwort auf Beitrag Nr.: 42.498.387 von ikarusfly am 19.12.11 12:59:18und das kann sich natürlich wochen und monate hinziehen

Antwort auf Beitrag Nr.: 42.498.405 von Frhstck am 19.12.11 13:01:50oder ruck zuck gehen

laut den berichten sind die 800 pence dem gulf chef zuwenig....

laut den berichten sind die 800 pence dem gulf chef zuwenig....

Antwort auf Beitrag Nr.: 42.498.409 von gnuldi am 19.12.11 13:03:12welchen berichten??

also ich hab noch nicht gefunden wo geschrieben steht das dem gulf ceo

die 800 pence zu wenig sind

also ich hab noch nicht gefunden wo geschrieben steht das dem gulf ceo

die 800 pence zu wenig sind

Antwort auf Beitrag Nr.: 42.498.409 von gnuldi am 19.12.11 13:03:12laut seiner aussage liegt fair value im 2 stelligen milliardenbeireich.....differenz über 30%...ist ne menge holz

Antwort auf Beitrag Nr.: 42.498.427 von Frhstck am 19.12.11 13:07:21WDH/Presse: Exxon Mobil arbeitet an Übernahme des Ölförderers GKP

(Wiederholung vom Wochenende)

LONDON (dpa-AFX) - Der US-Ölkonzern Exxon Mobil arbeitet laut einem Pressebericht an der milliardenschweren Übernahme des Ölförderers Gulf Keystone Petroleum (GKP). Die Amerikaner bewerteten das Unternehmen mit rund sieben Milliarden britischen Pfund (8,3 Mrd Euro), berichtet der 'Independent' am Sonntag in seiner Online-Ausgabe. Das Gebot solle sich auf etwa acht Pfund je Aktie belaufen. Exxon Mobil soll bei GKP bereits angeklopft haben. Das Unternehmen ist im kurdischen Nordirak aktiv.

GKP kommt dem Bericht zufolge derzeit lediglich auf eine Marktkapitalisierung von 1,5 Milliarden Pfund. GKP-Chef Todd Kozel sehe den Unternehmenswert aber bei einer möglicherweise zweistelligen Milliardensumme. GKP lehnte eine Stellungnahme auf Nachfrage der Zeitung ab. Exxon rief nicht zurück./stw

(Wiederholung vom Wochenende)

LONDON (dpa-AFX) - Der US-Ölkonzern Exxon Mobil arbeitet laut einem Pressebericht an der milliardenschweren Übernahme des Ölförderers Gulf Keystone Petroleum (GKP). Die Amerikaner bewerteten das Unternehmen mit rund sieben Milliarden britischen Pfund (8,3 Mrd Euro), berichtet der 'Independent' am Sonntag in seiner Online-Ausgabe. Das Gebot solle sich auf etwa acht Pfund je Aktie belaufen. Exxon Mobil soll bei GKP bereits angeklopft haben. Das Unternehmen ist im kurdischen Nordirak aktiv.

GKP kommt dem Bericht zufolge derzeit lediglich auf eine Marktkapitalisierung von 1,5 Milliarden Pfund. GKP-Chef Todd Kozel sehe den Unternehmenswert aber bei einer möglicherweise zweistelligen Milliardensumme. GKP lehnte eine Stellungnahme auf Nachfrage der Zeitung ab. Exxon rief nicht zurück./stw

Antwort auf Beitrag Nr.: 42.498.439 von ikarusfly am 19.12.11 13:09:59na ja, fair value - also mir wärs recht die würden 800 penc zahlen und gut ist

Antwort auf Beitrag Nr.: 42.498.487 von Frhstck am 19.12.11 13:19:40meine erfahrungen mit übernahmen......wenn was durchgesickert ist, wird meist dementiert oder einfach das gebot erhöht. rechne hier mit vers. 2. exxon op/gewinn bei 44% zum vorjahr. für die ist gpv ein kleiner snack

Antwort auf Beitrag Nr.: 42.498.507 von ikarusfly am 19.12.11 13:22:20jetzt gab es wohl das dementi?

Antwort auf Beitrag Nr.: 42.498.487 von Frhstck am 19.12.11 13:19:40wars das nun erst mal oder geht da bis zu neuen Veröffentlichungen erst mal nichts mehr?

Antwort auf Beitrag Nr.: 42.498.296 von Frhstck am 19.12.11 12:34:09aus der ftd

GKP kommt dem Bericht zufolge derzeit lediglich auf eine Marktkapitalisierung von 1,5 Milliarden Pfund. GKP-Chef Todd Kozel sehe den Unternehmenswert aber bei einer möglicherweise zweistelligen Milliardensumme. GKP lehnte eine Stellungnahme auf Nachfrage der Zeitung ab. Exxon rief nicht zurück.

GKP kommt dem Bericht zufolge derzeit lediglich auf eine Marktkapitalisierung von 1,5 Milliarden Pfund. GKP-Chef Todd Kozel sehe den Unternehmenswert aber bei einer möglicherweise zweistelligen Milliardensumme. GKP lehnte eine Stellungnahme auf Nachfrage der Zeitung ab. Exxon rief nicht zurück.

hast du einen link?

Antwort auf Beitrag Nr.: 42.498.594 von ikarusfly am 19.12.11 13:40:57du hattest die meldung doch schon

resse-exxon-mobil-arbeitet-an-uebernahme-des-oelfoerderers-gkp/60144342.html" target="_blank" rel="nofollow ugc noopener">http://www.ftd.de/unternehmen/industrie/ resse-exxon-mobil-arbeitet-an-uebernahme-des-oelfoerderers-gkp/60144342.html

resse-exxon-mobil-arbeitet-an-uebernahme-des-oelfoerderers-gkp/60144342.html

jetzt gehts wieder runter

manchmal ist boerse nicht begreifbar

resse-exxon-mobil-arbeitet-an-uebernahme-des-oelfoerderers-gkp/60144342.html" target="_blank" rel="nofollow ugc noopener">http://www.ftd.de/unternehmen/industrie/

resse-exxon-mobil-arbeitet-an-uebernahme-des-oelfoerderers-gkp/60144342.html

resse-exxon-mobil-arbeitet-an-uebernahme-des-oelfoerderers-gkp/60144342.htmljetzt gehts wieder runter

manchmal ist boerse nicht begreifbar

Antwort auf Beitrag Nr.: 42.498.637 von gnuldi am 19.12.11 13:50:18nein!!! meinte frhstck´s aussage betreffend dementie...

Antwort auf Beitrag Nr.: 42.498.654 von ikarusfly am 19.12.11 13:56:31nö, das war nur vermutung weil der kurs wieder gegen süden geht

Frag mich wer die arme Sau ist, die heute vorbörslich 13K zu 6,70 für insgesamt € 87.000,- gekauft hat. Do leggst di nieder. Ich hoffe, der kommt wieder auf seinen Einstand.

Drück dir wirklich die Daumen. Mir auch, bin zu 2,30 auch dabei.

Drück dir wirklich die Daumen. Mir auch, bin zu 2,30 auch dabei.

Letztes Jahr wollte Exxon doch BP übernehmen.

Ist auch nix geworden

Ist auch nix geworden

Antwort auf Beitrag Nr.: 42.498.718 von Loserin am 19.12.11 14:11:12nein-ich wars nicht mit den 6 euro

aber ich frag mich warum ihr immer so negativ drauf seid

bei 10 euro ist auch der mit 6 noch dick im gewinn

warten muss man koennen

bp ist ja auch ein anderes kaliber als gulf

werdet ihr fuers kurs runterreden eigentlich mit heizoel von esso bezahlt?

aber ich frag mich warum ihr immer so negativ drauf seid

bei 10 euro ist auch der mit 6 noch dick im gewinn

warten muss man koennen

bp ist ja auch ein anderes kaliber als gulf

werdet ihr fuers kurs runterreden eigentlich mit heizoel von esso bezahlt?

Antwort auf Beitrag Nr.: 42.498.707 von moneyscheffler am 19.12.11 14:08:51höchstbietender lag bei 7,25 ich hoffe er hat nicht verkauft......70%verlust auf intradaybasis. mußt du inv. bleiben, die nächste offerte wird wohl nicht lange auf sich warten lassen.....wünsch dieser person gute nerven

ich hoffe er hat nicht verkauft......70%verlust auf intradaybasis. mußt du inv. bleiben, die nächste offerte wird wohl nicht lange auf sich warten lassen.....wünsch dieser person gute nerven

ich hoffe er hat nicht verkauft......70%verlust auf intradaybasis. mußt du inv. bleiben, die nächste offerte wird wohl nicht lange auf sich warten lassen.....wünsch dieser person gute nerven

ich hoffe er hat nicht verkauft......70%verlust auf intradaybasis. mußt du inv. bleiben, die nächste offerte wird wohl nicht lange auf sich warten lassen.....wünsch dieser person gute nerven

Antwort auf Beitrag Nr.: 42.498.718 von Loserin am 19.12.11 14:11:12Aha, du vergleichst Gulf Keystone mit BP.

Hm, was soll man da sagen/schreiben ?!

Hm, was soll man da sagen/schreiben ?!

Antwort auf Beitrag Nr.: 42.498.718 von Loserin am 19.12.11 14:11:12also das kann man wohl nicht vergleichen

Zitat von gnuldi: nein-ich wars nicht mit den 6 euro

aber ich frag mich warum ihr immer so negativ drauf seid

bei 10 euro ist auch der mit 6 noch dick im gewinn

warten muss man koennen

bp ist ja auch ein anderes kaliber als gulf

werdet ihr fuers kurs runterreden eigentlich mit heizoel von esso bezahlt?

Deine Reaktion auf meine Frage ist nicht korrekt.

Nervös ?

Zitat von ikarusfly: höchstbietender lag bei 7,25

Denke nicht das er verkauft hat, kommt ja fast einem Totalverlust gleich.

Der arme Kerl hat nur zu schnell den Kaufbutton gedrückt.

Die Intradyschwankungen halte ich in dieser spekulativen Phase für völlig normal.........

Sollte der Deal wirklich zustande kommen, dann kommt dies einem Wheinachtsgeschenk gleich...

Antwort auf Beitrag Nr.: 42.498.753 von Earthfire am 19.12.11 14:19:06das kommt vom kaufen ohne limit

er kann ja wieder raus und dann wieder kaufen

so hat er moeglichkeiten seine abgeltungssteuer zu druecken

er kann ja wieder raus und dann wieder kaufen

so hat er moeglichkeiten seine abgeltungssteuer zu druecken

Bin mal gespannt, wie wir in London schliessen.

Oft genug kommt die entscheidende News nach Handelsschluss .

Oft genug kommt die entscheidende News nach Handelsschluss .

Antwort auf Beitrag Nr.: 42.498.917 von Earthfire am 19.12.11 14:55:00dann würde es längst schon insider geben die den kurs weiter richtung norden tragen. so schnell geht das alles nicht.

solche deals werden nicht immer an der boerse gemacht

grosse pakete werden ausserboerslich umplatziert

grosse pakete werden ausserboerslich umplatziert

Antwort auf Beitrag Nr.: 42.498.954 von gnuldi am 19.12.11 15:04:26ich bin mir dennoch sicher das dies noch sehr lang dauern wird

Antwort auf Beitrag Nr.: 42.499.023 von Frhstck am 19.12.11 15:17:43bisher keine dementi

Tippe auf TH als SK in London.

Antwort auf Beitrag Nr.: 42.499.123 von Frhstck am 19.12.11 15:42:09denke da geht es heiß her hinter den kulissen......kann mir nicht vorstellen, daß sich die ganze sache lange hinauszögern wird. je besser sich gkp entwickelt ,desto teuerer wirds für exxon......und die konkurrenz nicht vergessen. kann mir gut ein bieterverfahren vorstellen

Deutschland (Kurs) Chart:

USA OTC CHART:

London:

http://www.shareprice.co.uk/GKP/GULF-KEYSTONE-PETROLEUM-LD-C…

USA OTC CHART:

London:

http://www.shareprice.co.uk/GKP/GULF-KEYSTONE-PETROLEUM-LD-C…

Acquirers rarely make offers at more than a 50 percent premium to a target's pre-bid share price.

Nonetheless, Gulf Keystone shares opened 24 percent higher before giving up some of the gains to trade up 17.5 percent at 194.5 pence at 1526 GMT.

One dealer said they were especially surprised by the report's claim that Gulf Keystone's board would not accept the estimated 800 pence/share bid that Exxon was considering and instead the Chief Executive, Todd Kozel, wanted a price tag over 10 billion pounds in total.

"I bet the shareholders would jump for anything over 250 pence a share," the dealer said.

The Kurdistan Regional Government (KRG) said last month that Exxon had signed contracts for six exploration blocks, prompting criticism from the Baghdad government, which has challenged the regional government's right to issue licenses.

The deal would make Exxon the first company in the top tier of the industry to move into the Kurdish region but Exxon has not confirmed it and declines all comment on the matter.

Industry sources said that many big western oil companies have been mulling an entry into Kurdistan, by either buying existing players in the region, many of whom are small independents, or by buying new licensing blocks.

Gulf Keystone said in September it was seeking a buyer for its 20 percent interest in the Akri-Bijeel block in Kurdistan in order to help finance ongoing development of other assets.

Industry sources said the company has mulled a possible sale of others parts, or all, of its interests in Kurdistan.

(Additional reporting by Sarah Young; Editing by Jon Loades-Carter and Mike Nesbit)

Nonetheless, Gulf Keystone shares opened 24 percent higher before giving up some of the gains to trade up 17.5 percent at 194.5 pence at 1526 GMT.

One dealer said they were especially surprised by the report's claim that Gulf Keystone's board would not accept the estimated 800 pence/share bid that Exxon was considering and instead the Chief Executive, Todd Kozel, wanted a price tag over 10 billion pounds in total.

"I bet the shareholders would jump for anything over 250 pence a share," the dealer said.

The Kurdistan Regional Government (KRG) said last month that Exxon had signed contracts for six exploration blocks, prompting criticism from the Baghdad government, which has challenged the regional government's right to issue licenses.

The deal would make Exxon the first company in the top tier of the industry to move into the Kurdish region but Exxon has not confirmed it and declines all comment on the matter.

Industry sources said that many big western oil companies have been mulling an entry into Kurdistan, by either buying existing players in the region, many of whom are small independents, or by buying new licensing blocks.

Gulf Keystone said in September it was seeking a buyer for its 20 percent interest in the Akri-Bijeel block in Kurdistan in order to help finance ongoing development of other assets.

Industry sources said the company has mulled a possible sale of others parts, or all, of its interests in Kurdistan.

(Additional reporting by Sarah Young; Editing by Jon Loades-Carter and Mike Nesbit)

Antwort auf Beitrag Nr.: 42.499.445 von ikarusfly am 19.12.11 16:51:16http://de.reuters.com/article/companyNews/idUKTRE7BI13320111…

Antwort auf Beitrag Nr.: 42.499.448 von ikarusfly am 19.12.11 16:52:02was soll uns die news sagen?

Antwort auf Beitrag Nr.: 42.499.487 von Frhstck am 19.12.11 16:57:00laut diesem bericht gab es keine gespräche.......ein analyst wundert sich auch über die aussage des ceo`s von gkp das sie ein angebot von 800bp/share ablehnen würden....er meint das bei einem angebot von über 200bp allse verkaufen würden. bla bla bla bla

aber von der firma direkt gab es noch kein dementie.......wait and see

aber von der firma direkt gab es noch kein dementie.......wait and see

so wie es aussieht schließen wir noch im minus.......unglaublich was sich auf den märkten abspielt.

http://de.reuters.com/article/pressRelease/idUS155632+19-Dec…

wäre auch zu schön gewesen....

allen noch einen schönen abend

wäre auch zu schön gewesen....

allen noch einen schönen abend

Antwort auf Beitrag Nr.: 42.499.739 von ikarusfly am 19.12.11 17:47:03hinter den Kulissen wird sich schon was abspielen, ist doch klar das keiner

zugibt, in Verhandlungen zu stehen.

Am Gerücht wird schon was dran sein.

zugibt, in Verhandlungen zu stehen.

Am Gerücht wird schon was dran sein.

Also Amerika steht schon wieder bei umgerechnet 2,21 Euro

aktuell !!!

...Wo Rauch ist auch Feuer...

aktuell !!!

...Wo Rauch ist auch Feuer...

Antwort auf Beitrag Nr.: 42.499.848 von JimmySpoon am 19.12.11 18:07:02die morgenpost berichtet ueber weitere interessenten

Irving, TX (aktiencheck.de AG) - Der amerikanische Ölgigant Exxon Mobil Corp. (ISIN US30231G1022/ WKN 852549) ist einem Medienbericht zufolge an einer Übernahme der in London notierten Gulf Keystone Petroleum plc (ISIN BMG4209G1087/ WKN A0B72B) interessiert.

Wie die britische Zeitung "The Independent" am Sonntag unter Berufung auf informierte Kreise berichtet, zieht der US-Ölmulti eine Übernahme des operativ in Kurdistan tätigen Ölkonzerns in Betracht. Laut dem Bericht werde die Aktie von Gulf Keystone Petroleum derzeit an der Londoner Börse lediglich mit 1,5 Mrd. Britischen Pfund (GBP) bewertet. Angesichts des zuletzt in Kasachstan gemachten Ölfundes gilt der Konzern laut dem Bericht als attraktives Übernahmeziel. Nach Informationen der Tageszeitung will Exxon Mobile rund 7 Mrd. GBP bzw. 8 GBP je Aktie für Gulf Keystone Petroleum bieten. Dies könnte jedoch zu wenig sein, um die Zustimmung des CEO Todd Koze erhalten, zumal es sich nach Meinung von Experten bei dem jüngsten Ölfundnordwestlich der kurdischen Hauptstadt Erbil um eine der größten Öllagerstätten handeln könnte, die zuletzt weltweit entdeckt wurden.

Als mögliche weitere Interessenten für Gulf Keystone Petroleum wurden in dem Bericht auch der chinesische Öl- und Raffineriekonzern China Petroleum & Chemical Corp. (Sinopec) (ISIN CNE1000002Q2/ WKN A0M4XN) sowie der US-Konzern Chevron Corp. (ISIN US1667641005/ WKN 852552) genannt.

Die Aktie von Gulf Keystone Petroleum gewinnt derzeit in London 16, 92 Prozent auf 193,50 Pence

Irving, TX (aktiencheck.de AG) - Der amerikanische Ölgigant Exxon Mobil Corp. (ISIN US30231G1022/ WKN 852549) ist einem Medienbericht zufolge an einer Übernahme der in London notierten Gulf Keystone Petroleum plc (ISIN BMG4209G1087/ WKN A0B72B) interessiert.

Wie die britische Zeitung "The Independent" am Sonntag unter Berufung auf informierte Kreise berichtet, zieht der US-Ölmulti eine Übernahme des operativ in Kurdistan tätigen Ölkonzerns in Betracht. Laut dem Bericht werde die Aktie von Gulf Keystone Petroleum derzeit an der Londoner Börse lediglich mit 1,5 Mrd. Britischen Pfund (GBP) bewertet. Angesichts des zuletzt in Kasachstan gemachten Ölfundes gilt der Konzern laut dem Bericht als attraktives Übernahmeziel. Nach Informationen der Tageszeitung will Exxon Mobile rund 7 Mrd. GBP bzw. 8 GBP je Aktie für Gulf Keystone Petroleum bieten. Dies könnte jedoch zu wenig sein, um die Zustimmung des CEO Todd Koze erhalten, zumal es sich nach Meinung von Experten bei dem jüngsten Ölfundnordwestlich der kurdischen Hauptstadt Erbil um eine der größten Öllagerstätten handeln könnte, die zuletzt weltweit entdeckt wurden.

Als mögliche weitere Interessenten für Gulf Keystone Petroleum wurden in dem Bericht auch der chinesische Öl- und Raffineriekonzern China Petroleum & Chemical Corp. (Sinopec) (ISIN CNE1000002Q2/ WKN A0M4XN) sowie der US-Konzern Chevron Corp. (ISIN US1667641005/ WKN 852552) genannt.

Die Aktie von Gulf Keystone Petroleum gewinnt derzeit in London 16, 92 Prozent auf 193,50 Pence

die news ist klasse

Antwort auf Beitrag Nr.: 42.501.624 von ikarusfly am 20.12.11 08:17:44kein wunder das alle heiß auf gvp sind

das wird hier noch richtig lustig werden.

20 December 2011

Gulf Keystone Petroleum Ltd. (AIM: GKP)

("Gulf Keystone" or "the Company")

Kurdistan Operational Update

Spudding of Shaikan-6 Appraisal Well

Gulf Keystone is pleased to announce that the Shaikan-6 appraisal well has spudded on the Shaikan block in the Kurdistan Region of Iraq on 16th December 2011.

Shaikan-6 is the fourth deep appraisal well to be drilled on the Company's major oil discovery with independently audited gross oil-in-place volumes of between 8 billion barrels and 13.4 billion barrels calculated on the P90 to P10 basis with a mean value of 10.5 billion barrels.

Shaikan-6 is being drilled 9 km to the east of the Shaikan-2 appraisal well to an estimated total depth of 3,800 metres subject to technical conditions. Shaikan-6, the last appraisal well to be drilled as part of the Shaikan appraisal programme, will target prospective intervals in the Jurassic and Triassic

Shaikan-6 will be followed by the Shaikan-7 exploration well in 2012, which will target potential untapped resources in the lower Triassic and the Permian, the Company's deepest undrilled horizon to date.

Gulf Keystone is the Operator of the Shaikan block with a working interest of 75 per cent and is partnered with Kalegran Ltd. (a 100 per cent subsidiary of MOL Hungarian Oil and Gas Plc.) and Texas Keystone Inc., which have working interests of 20 per cent and 5 per cent respectively.

John Gerstenlauer, Gulf Keystone's Chief Operating Officer commented:

"Shaikan-6 is the tenth well to be drilled across the Company's four adjacent blocks and the seventh well to be drilled on the blocks which Gulf Keystone operates in the Kurdistan Region of Iraq. This number of completed and current exploration and appraisal wells comfortably places Gulf Keystone among top three operators in the region. As part of our high impact drilling campaign, planned and funded through 2012, the Shaikan-5 and Shaikan-6 appraisal wells will provide us with better understanding of the flanks of the massive Shaikan structure and its yet untapped resources."

Enquiries:

Gulf Keystone Petroleum:

+44 (0) 20 7514 1400

Todd Kozel, Executive Chairman and

Chief Executive Officer

Ewen Ainsworth, Finance Director

Strand Hanson Limited

+44 (0) 20 7409 3494

Simon Raggett / Rory Murphy / James Harris

Mirabaud Securities LLP

+44 (0) 20 7878 3362

Peter Krens

Pelham Bell Pottinger

+44 (0) 20 7861 3232

Mark Antelme

or visit: www.gulfkeystone.com

das wird hier noch richtig lustig werden.

20 December 2011

Gulf Keystone Petroleum Ltd. (AIM: GKP)

("Gulf Keystone" or "the Company")

Kurdistan Operational Update

Spudding of Shaikan-6 Appraisal Well

Gulf Keystone is pleased to announce that the Shaikan-6 appraisal well has spudded on the Shaikan block in the Kurdistan Region of Iraq on 16th December 2011.

Shaikan-6 is the fourth deep appraisal well to be drilled on the Company's major oil discovery with independently audited gross oil-in-place volumes of between 8 billion barrels and 13.4 billion barrels calculated on the P90 to P10 basis with a mean value of 10.5 billion barrels.

Shaikan-6 is being drilled 9 km to the east of the Shaikan-2 appraisal well to an estimated total depth of 3,800 metres subject to technical conditions. Shaikan-6, the last appraisal well to be drilled as part of the Shaikan appraisal programme, will target prospective intervals in the Jurassic and Triassic

Shaikan-6 will be followed by the Shaikan-7 exploration well in 2012, which will target potential untapped resources in the lower Triassic and the Permian, the Company's deepest undrilled horizon to date.

Gulf Keystone is the Operator of the Shaikan block with a working interest of 75 per cent and is partnered with Kalegran Ltd. (a 100 per cent subsidiary of MOL Hungarian Oil and Gas Plc.) and Texas Keystone Inc., which have working interests of 20 per cent and 5 per cent respectively.

John Gerstenlauer, Gulf Keystone's Chief Operating Officer commented:

"Shaikan-6 is the tenth well to be drilled across the Company's four adjacent blocks and the seventh well to be drilled on the blocks which Gulf Keystone operates in the Kurdistan Region of Iraq. This number of completed and current exploration and appraisal wells comfortably places Gulf Keystone among top three operators in the region. As part of our high impact drilling campaign, planned and funded through 2012, the Shaikan-5 and Shaikan-6 appraisal wells will provide us with better understanding of the flanks of the massive Shaikan structure and its yet untapped resources."

Enquiries:

Gulf Keystone Petroleum:

+44 (0) 20 7514 1400

Todd Kozel, Executive Chairman and

Chief Executive Officer

Ewen Ainsworth, Finance Director

Strand Hanson Limited

+44 (0) 20 7409 3494

Simon Raggett / Rory Murphy / James Harris

Mirabaud Securities LLP

+44 (0) 20 7878 3362

Peter Krens

Pelham Bell Pottinger

+44 (0) 20 7861 3232

Mark Antelme

or visit: www.gulfkeystone.com

Antwort auf Beitrag Nr.: 42.501.728 von Earthfire am 20.12.11 08:47:45vorher wird die übernommen

von mir aus kann der bieterkamp beginnen

von mir aus kann der bieterkamp beginnen

Antwort auf Beitrag Nr.: 42.501.756 von ikarusfly am 20.12.11 08:52:46die news ist echt hammer

das teil ist sowas von unterbewertet

das teil ist sowas von unterbewertet

Antwort auf Beitrag Nr.: 42.501.685 von ikarusfly am 20.12.11 08:38:58die news kam doch heute oder?

der kurs reagiert ziemlich verhalten auf diese top news

der kurs reagiert ziemlich verhalten auf diese top news

Antwort auf Beitrag Nr.: 42.501.847 von Frhstck am 20.12.11 09:11:31preis muß doch optisch niedrig gehalten werden.....sonst wird die übernahmeofferte richtig teuer

.....sonst wird die übernahmeofferte richtig teuer

Antwort auf Beitrag Nr.: 42.501.893 von ikarusfly am 20.12.11 09:21:30die bewertung müsste trotzdem viel höher sein

und weiter gehts

Nach Informationen der Tageszeitung will Exxon Mobile rund 7 Mrd. GBP bzw. 8 GBP je Aktie für Gulf Keystone Petroleum bieten. Dies könnte jedoch zu wenig sein, um die Zustimmung des CEO Todd Koze erhalten, zumal es sich nach Meinung von Experten bei dem jüngsten Ölfundnordwestlich der kurdischen Hauptstadt Erbil um eine der größten Öllagerstätten handeln könnte, die zuletzt weltweit entdeckt wurden.

Hatte mich beim ersten Überfliegen nur auf die weiteren Interessenten konzentriert!

Nach Informationen der Tageszeitung will Exxon Mobile rund 7 Mrd. GBP bzw. 8 GBP je Aktie für Gulf Keystone Petroleum bieten. Dies könnte jedoch zu wenig sein, um die Zustimmung des CEO Todd Koze erhalten, zumal es sich nach Meinung von Experten bei dem jüngsten Ölfundnordwestlich der kurdischen Hauptstadt Erbil um eine der größten Öllagerstätten

handeln könnte, die zuletzt weltweit entdeckt wurden.Hatte mich beim ersten Überfliegen nur auf die weiteren Interessenten konzentriert!

Zitat von ikarusfly: und weiter gehts

Nach Informationen der Tageszeitung will Exxon Mobile rund 7 Mrd. GBP bzw. 8 GBP je Aktie für Gulf Keystone Petroleum bieten. Dies könnte jedoch zu wenig sein, um die Zustimmung des CEO Todd Koze erhalten, zumal es sich nach Meinung von Experten bei dem jüngsten Ölfundnordwestlich der kurdischen Hauptstadt Erbil um eine der größten Öllagerstätten

Hatte mich beim ersten Überfliegen nur auf die weiteren Interessenten konzentriert!

Ich bleibe hier erstmal investiert, und kaufe evtl. bei einem tieferen Rücksetzer nochmal nach !

an jedem Gerücht ist fast "immer" ein Stück Wahrheit vorhanden.

Fakt ist, die Jungs von GKP sind gut aufgestellt, und bei ihren Explorationen erfolgreich....die Trefferquoten bei Öl u. Gasexplorer sollten ja hinlänglich bekannt sein...1 zu 10 !

Das gestrige Dementi von GKP würde ich auch eher als normal ansehen....passiert ja des öfteren das vor einer Übernahme dementiert wird.

Und sollte es bei einer Übernahme zu einem Bieterkampf kommen....dann sehen wir hier schnell den gestrigen TAX von über 7 € wieder.

Mein Bauch ( was nicht heisst) sagt mir, das es hier bald zu weiteren Gerüchten bzw. Fakten im Hinblick auf eine Übernahme kommen könnte.

http://www.iii.co.uk/investment/detail?code=cotn:GKP.L&displ…

GKP has to be the biggest TO target out there .. blimey it is written all over GKP !!!

it is apparent that even STM got caught out wrongly with his analysis for yesterday and he is trying to put a positive spin on it today!!!

einer der wenigen user der vom fach ist

GKP has to be the biggest TO target

out there .. blimey it is written all over GKP !!! it is apparent that even STM got caught out wrongly with his analysis for yesterday and he is trying to put a positive spin on it today!!!

einer der wenigen user der vom fach ist

Antwort auf Beitrag Nr.: 42.502.899 von ikarusfly am 20.12.11 12:59:27inter. gedanke

So we still don't know for sure from where the initial rumour emanated. It doesn't appear to be in Exxon's interest to have instigated it and the comments from GKP such as 'baseless' 'stupid' etc wouldn't sit too well with the Independant if they were indeed the initial source.

Maybe, just maybe, the answer is closer to home. If you refer back to GRH1's 'In Shock,,,Awe' post recently he was extremenly passionate about getting the word out that we were about to be stitched up. Picketing embassies, lobbying the KRG, in fact any legal means possible were suggested if I remember correctly to get this in the public domain and force a rethink by TK and the KRG.

Could it be that therin lies the source of the rumour? Maybe not GRH1 himself, but some investor who has the ear of the BOD and also has contacts within the media and took up the suggestion and acted upon it?

Just a thought. Maybe one day we will find out! GLA

So we still don't know for sure from where the initial rumour emanated. It doesn't appear to be in Exxon's interest to have instigated it and the comments from GKP such as 'baseless' 'stupid' etc wouldn't sit too well with the Independant if they were indeed the initial source.

Maybe, just maybe, the answer is closer to home. If you refer back to GRH1's 'In Shock,,,Awe' post recently he was extremenly passionate about getting the word out that we were about to be stitched up. Picketing embassies, lobbying the KRG, in fact any legal means possible were suggested if I remember correctly to get this in the public domain and force a rethink by TK and the KRG.

Could it be that therin lies the source of the rumour? Maybe not GRH1 himself, but some investor who has the ear of the BOD and also has contacts within the media and took up the suggestion and acted upon it?

Just a thought. Maybe one day we will find out! GLA

Zitat von ikarusfly: inter. gedanke

So we still don't know for sure from where the initial rumour emanated. It doesn't appear to be in Exxon's interest to have instigated it and the comments from GKP such as 'baseless' 'stupid' etc wouldn't sit too well with the Independant if they were indeed the initial source.

Maybe, just maybe, the answer is closer to home. If you refer back to GRH1's 'In Shock,,,Awe' post recently he was extremenly passionate about getting the word out that we were about to be stitched up. Picketing embassies, lobbying the KRG, in fact any legal means possible were suggested if I remember correctly to get this in the public domain and force a rethink by TK and the KRG.

Could it be that therin lies the source of the rumour? Maybe not GRH1 himself, but some investor who has the ear of the BOD and also has contacts within the media and took up the suggestion and acted upon it?

Just a thought. Maybe one day we will find out! GLA

Ja interessant !

So ein Gerücht ruft nach meiner Auffassung mit Sicherheit auch andere Interessenten auf den Plan, die jetzt mit dem Taschenrechner schon fleißig rechnen......was unterm Strich da an Recourcen so liegt und vermarktbar wäre.

Über den Kurs bei der heutigen News würde ich mir nicht all zu große Gedanken machen d.h. bei Drillbeginn kann alle passieren Süden od. Norden...aber je tiefer der Bohrer eindringt, bzw. wenn es heißt Oil shows...dann geht die Geschichte meist richtig los.

Und was die Seismik bzw. Schätzung von GKP betrifft.....die Menge ist ja wohl gigantisch.....ich rechne die mal auf den Kurs um , wenn ich ewas mehr Zeit habe.

Antwort auf Beitrag Nr.: 42.503.000 von Earthfire am 20.12.11 13:21:1412+ billion barrels

11 $bn tabled

10 billion of P50

9 bag Chinese offer

8 billion of P90

7 £bn knocked back

6 Shaikan spudded

5 bag by Jan?

4 way t/o auction

3D caught short

2 Shaikans

and still no sign of OWC.

11 $bn tabled

10 billion of P50

9 bag Chinese offer

8 billion of P90

7 £bn knocked back

6 Shaikan spudded

5 bag by Jan?

4 way t/o auction

3D caught short

2 Shaikans

and still no sign of OWC.

Zitat von ikarusfly: 12+ billion barrels

11 $bn tabled

10 billion of P50

9 bag Chinese offer

8 billion of P90

7 £bn knocked back

6 Shaikan spudded

5 bag by Jan?

4 way t/o auction

3D caught short

2 Shaikans

and still no sign of OWC.

ich mach gleich mal eine Berechnung für P90 Szenario auf....

GKP hält 75 % ...richtig ?

I have a VERY well informed hunch that GKP wants to keep quiet on who it was who spoke to Dow Jones purportedly on GKP's behalf. Why are they protecting his identity?

In a conversation with me yesterday, however, the newswire spoke very highly of this person and indeed used his quote again in its closing update.

I find it totally incredible that they would authorise an intraday comment comprehensively trashing the Indie story and then issue a 'non-denial denial' RNS.

Putting the whole thing together, I think they needed to get authorisation from 'higher authority' and, in the meantime, bombared by a welter of enquiries, allowed someone to speak off the record in a bid to calm things down.

GKP has not reacted to the Dow Jones story so that further suggests this guy was a genuine executive at GKP in London.

The whole affair suggests enormous sensitivity and I personally think any statement needed a US party to approve it. Who is that, I wonder.

In a conversation with me yesterday, however, the newswire spoke very highly of this person and indeed used his quote again in its closing update.

I find it totally incredible that they would authorise an intraday comment comprehensively trashing the Indie story and then issue a 'non-denial denial' RNS.

Putting the whole thing together, I think they needed to get authorisation from 'higher authority' and, in the meantime, bombared by a welter of enquiries, allowed someone to speak off the record in a bid to calm things down.

GKP has not reacted to the Dow Jones story so that further suggests this guy was a genuine executive at GKP in London.

The whole affair suggests enormous sensitivity and I personally think any statement needed a US party to approve it. Who is that, I wonder.

Sieht so aus , als würde sich an der LSE etwas tun...

Antwort auf Beitrag Nr.: 42.503.838 von Earthfire am 20.12.11 15:58:16.....wenn da mal nicht noch eine meldung kommt

Zitat von Frhstck: .....wenn da mal nicht noch eine meldung kommt

auf jeden Fall tut sich was, da ja keine direkte Reaktion auf die heutige News erfolgte ( Was nicht viel zu bedeuten hat ! )

ASK wird auf jeden Fall so weg geknabbert

Hier kann jederzeit eine Hammernews eintrudeln....

Mal schauen wo London heute schließt ?

Antwort auf Beitrag Nr.: 42.503.678 von Earthfire am 20.12.11 15:35:34Sieht so aus , als würde sich an der LSE etwas tun...

Ja, ein Stuhl ist umgefallen. Ein Händler musste dringend aufs Klo.

Er hat heute angeblich den ganzen Tag auf die finale Meldung gewartet.

Jetzt konnte er nicht mehr anders.

Ja, ein Stuhl ist umgefallen. Ein Händler musste dringend aufs Klo.

Er hat heute angeblich den ganzen Tag auf die finale Meldung gewartet.

Jetzt konnte er nicht mehr anders.

Antwort auf Beitrag Nr.: 42.503.929 von Earthfire am 20.12.11 16:13:42charttechnischer ausbruch eben erfolgt

aber ich freu mich mal nicht zu früh

aber ich freu mich mal nicht zu früh

Zitat von moneyscheffler: Sieht so aus , als würde sich an der LSE etwas tun...

Ja, ein Stuhl ist umgefallen. Ein Händler musste dringend aufs Klo.

Er hat heute angeblich den ganzen Tag auf die finale Meldung gewartet.

Jetzt konnte er nicht mehr anders.

Ich bezog mich eher auf das Volumen und den Kurs............aber schön einen Witzbold ( und das meine ich ernst) an Bord zu haben.

Antwort auf Beitrag Nr.: 42.504.056 von Earthfire am 20.12.11 16:35:02hab keine taxen mehr

Antwort auf Beitrag Nr.: 42.504.077 von Frhstck am 20.12.11 16:37:34hab keine taxen mehr

und ich hab keine Kohle mehr um nachzuladen.

Ich glaube dennoch nicht an eine kurzfristige Übernahme.

Da wurde m. E. zuviel dementiert.

Von beiden Seiten.

Die Berichte, Nachrichten und sonstigen Statements stimmen mich nicht sonderlich zuversichtlich, dass da eine Übernahme kommt.

Hätte sicherlich nichts einzuwenden.

Aber überlegt bzw. rechnet mal nach. Von unter 200 auf 800 Pence....

Das wäre einfach zu schön um wahr zu sein.

und ich hab keine Kohle mehr um nachzuladen.

Ich glaube dennoch nicht an eine kurzfristige Übernahme.

Da wurde m. E. zuviel dementiert.

Von beiden Seiten.

Die Berichte, Nachrichten und sonstigen Statements stimmen mich nicht sonderlich zuversichtlich, dass da eine Übernahme kommt.

Hätte sicherlich nichts einzuwenden.

Aber überlegt bzw. rechnet mal nach. Von unter 200 auf 800 Pence....

Das wäre einfach zu schön um wahr zu sein.

Antwort auf Beitrag Nr.: 42.504.151 von moneyscheffler am 20.12.11 16:47:59also exxon hat garnicht dementiert

Antwort auf Beitrag Nr.: 42.504.175 von Frhstck am 20.12.11 16:51:25Soll ich´s dir suchen ?

Zitat von moneyscheffler: hab keine taxen mehr

und ich hab keine Kohle mehr um nachzuladen.

Ich glaube dennoch nicht an eine kurzfristige Übernahme.

Da wurde m. E. zuviel dementiert.

Von beiden Seiten.

Die Berichte, Nachrichten und sonstigen Statements stimmen mich nicht sonderlich zuversichtlich, dass da eine Übernahme kommt.

Hätte sicherlich nichts einzuwenden.

Aber überlegt bzw. rechnet mal nach. Von unter 200 auf 800 Pence....

Das wäre einfach zu schön um wahr zu sein.

Dann rechne mal die Recourcen aus der heutigen News aus.....und dann durch die Sharezahl teilen.....schau doch mal was da dann raus kommen könnte.

Für den " Verkauf" des Brunnens, kannst du dann mal "nur" 10 US $ / Barrel ansetzen, falls es zu einer Übernahme kommt, liegt der Preis / Barrel entsprechend höher.

Leider hatte ich so einen Fall noch nicht bzw. müsste ich recherchieren.

Ich habe aber schon eine Anfrage gestartet um diesen in Erfahrung zu bringen.

Ich meine man könnte 15- 20 US $ / Barrel für den Fall ansetzen....immer vorrausgesetzt, die finden auch diese Größenordnung wie durch die 3D Seismik vermutet, und es handelt sich beim Fund um " leichtes ÖL " mit guter Qualität ( AFI )

Antwort auf Beitrag Nr.: 42.504.243 von moneyscheffler am 20.12.11 17:01:33ja,bitte - hab nur ein dementi von ceo der gvp gelesen

http://www.rigzone.com/news/article.asp?a_id=113471&rss=true

ist das für die Herren deutlich genug ?

ist das für die Herren deutlich genug ?

Antwort auf Beitrag Nr.: 42.504.295 von moneyscheffler am 20.12.11 17:09:01wir reden hier von exxon mobile.....die haben noch nicht dementiert

Antwort auf Beitrag Nr.: 42.504.295 von moneyscheffler am 20.12.11 17:09:01danke dir

Zitat von moneyscheffler: http://www.rigzone.com/news/article.asp?a_id=113471&rss=true

ist das für die Herren deutlich genug ?

Ohne Worte !

Antwort auf Beitrag Nr.: 42.504.324 von Earthfire am 20.12.11 17:14:09Warum, wieso ?

Kannst kein Englisch ?

Sorry, hab denk ich den falschen Artikel rein gestellt.

Bin mir ziemlich sicher, dass ich auf finanznachrichten oder UPI.com was gelesen habe.

Suche weiter.

Wär mir ja lieber, ich würd mich täuschen und kein Dementi finden.

Kannst kein Englisch ?

Sorry, hab denk ich den falschen Artikel rein gestellt.

Bin mir ziemlich sicher, dass ich auf finanznachrichten oder UPI.com was gelesen habe.

Suche weiter.

Wär mir ja lieber, ich würd mich täuschen und kein Dementi finden.

bis morgen früh männers......

Antwort auf Beitrag Nr.: 42.504.365 von moneyscheffler am 20.12.11 17:24:15

von Exxon wirste keine Dementi finden, da die sich noch nicht geäußert haben.

schätze mal die arbeiten an einer Übernahme und kaufen Aktien, vermutlich

kauft Exxon still und heimlich jetzt Aktien, denn ab Handelsstart in USA

gings auch in England höher mit dem Kurs.

Vielleicht wirds hier ähnlich wie bei VW und Porsche, und der Kurs wird

jeden Tag hochgetrieben

von Exxon wirste keine Dementi finden, da die sich noch nicht geäußert haben.

schätze mal die arbeiten an einer Übernahme und kaufen Aktien, vermutlich

kauft Exxon still und heimlich jetzt Aktien, denn ab Handelsstart in USA

gings auch in England höher mit dem Kurs.

Vielleicht wirds hier ähnlich wie bei VW und Porsche, und der Kurs wird

jeden Tag hochgetrieben

Antwort auf Beitrag Nr.: 42.504.585 von i2fan am 20.12.11 18:00:22charttechnisch heute auf sk basis auf ath geschlossen

us boys 3,19$ pari währe 205,7bp

Antwort auf Beitrag Nr.: 42.504.585 von i2fan am 20.12.11 18:00:22@i2fan....

dieser user vertritt genau die gleiche these......

Many of the posts from a few weeks ago are starting to make sense as they were implying a stitch up.

My guess is the KRG want Exxon to have us. The talk has been of Sinopec offering more and the BoD would clearly be obliged to try and achieve that. The way to circumvent all of this is for Exxon to go hostile with a large premium and as long as Sinopec doesn't go public we will never know. Sinopec have blocks in Kurdistan so If the KRG want Exxon it would be difficult to Sinopec to go against them.

That kind of confirms my suspicions, all of the stories appear to be coming from Exxons direction and he did kind of say GKP had indicated they wouldn't accept £8 which may have been the informal approach in Erbil in November. Perhaps GKPs BoD learnt Sinopec would offer more.

I am increasingly wondering whether Exxon have decided that a 400% premium will almost certainly succeed irrespective of what the BoD thinks. The RNS makes sense if a TO is not actually being discussed by Exxon with GKPs BoD and Exxon think they will have more success going straight to shareholders.

It might also explain why yesterdays RNS seemed very reluctant. If they issue a denial the SP drops, if they say there have been talks the SP rises but there would be huge pressure to accept the deal.

dieser user vertritt genau die gleiche these......

Many of the posts from a few weeks ago are starting to make sense as they were implying a stitch up.

My guess is the KRG want Exxon to have us. The talk has been of Sinopec offering more and the BoD would clearly be obliged to try and achieve that. The way to circumvent all of this is for Exxon to go hostile with a large premium and as long as Sinopec doesn't go public we will never know. Sinopec have blocks in Kurdistan so If the KRG want Exxon it would be difficult to Sinopec to go against them.

That kind of confirms my suspicions, all of the stories appear to be coming from Exxons direction and he did kind of say GKP had indicated they wouldn't accept £8 which may have been the informal approach in Erbil in November. Perhaps GKPs BoD learnt Sinopec would offer more.

I am increasingly wondering whether Exxon have decided that a 400% premium will almost certainly succeed irrespective of what the BoD thinks. The RNS makes sense if a TO is not actually being discussed by Exxon with GKPs BoD and Exxon think they will have more success going straight to shareholders.

It might also explain why yesterdays RNS seemed very reluctant. If they issue a denial the SP drops, if they say there have been talks the SP rises but there would be huge pressure to accept the deal.

ONE of the most controversial oil companies in the City yesterday insisted it was NOT in talks to sell.

http://www.thesun.co.uk/sol/homepage/news/money/4009008/UK-e…

GULF KEYSTONE — whose boss Todd Kozel is in the middle of a $100million divorce battle with his wife — was forced to act after rumours US giant EXXON was on the verge of a £7billion bid. It claimed the rumours were "unfounded". Experts believe Gulf will eventually be taken over, given its prized Shaikan oil field in Kurdistan, northern Iraq, which it discovered in 2009.

The field is thought to hold 10billion barrels of oil, making it one of the world's best recent finds.

Insiders claim America's CHEVRON is among those interested.

http://www.thesun.co.uk/sol/homepage/news/money/4009008/UK-e…

GULF KEYSTONE — whose boss Todd Kozel is in the middle of a $100million divorce battle with his wife — was forced to act after rumours US giant EXXON was on the verge of a £7billion bid. It claimed the rumours were "unfounded". Experts believe Gulf will eventually be taken over, given its prized Shaikan oil field in Kurdistan, northern Iraq, which it discovered in 2009.

The field is thought to hold 10billion barrels of oil, making it one of the world's best recent finds.

Insiders claim America's CHEVRON is among those interested.

pari zu us sk wären 2,45€

Antwort auf Beitrag Nr.: 42.506.601 von moneyscheffler am 21.12.11 08:46:47News kam getern schon über reuters

Antwort auf Beitrag Nr.: 42.506.624 von Frhstck am 21.12.11 08:54:27ok, habs erst heute Morgen auf finanznachrichtn (7.27 Uhr) gelesen.

Übernahme hin oder her. Das Teil kann nur nach oben gehen.

Normalerweise.

Aber was ist an der Börse schon normal ?

Übernahme hin oder her. Das Teil kann nur nach oben gehen.

Normalerweise.

Aber was ist an der Börse schon normal ?

würde gerne nochmal nachlegen, aber ein Spread von 6 - 8 % ist wohl etwas unverschämt, oder ?

Warten wir mal, bis sich das Teil wieder beruhigt hat.

Warten wir mal, bis sich das Teil wieder beruhigt hat.

scheint so das unser direkter nachbar, gekauft wird......

ist nur noch eine frage der zeit, bis sich einer der großen sich unser animmt

21 Dec 2011 - 08:05

LONDON, Dec 21 (Reuters) - Genel Energy PLC <GENL.L>:

* notes the press speculation with regard to the possible acquisition of an additional 40% stake in the Chia Surkh oilfield in the Kurdistan Region of Iraq

* Confirm that we are in negotiations with Longford Energy

* There can be no certainty these discussions will result in a transaction

((London Equities Newsroom; +44 20 7542 7717))

((For more news, please click here [GENL.L]))

ist nur noch eine frage der zeit, bis sich einer der großen sich unser animmt

21 Dec 2011 - 08:05

LONDON, Dec 21 (Reuters) - Genel Energy PLC <GENL.L>:

* notes the press speculation with regard to the possible acquisition of an additional 40% stake in the Chia Surkh oilfield in the Kurdistan Region of Iraq

* Confirm that we are in negotiations with Longford Energy

* There can be no certainty these discussions will result in a transaction

((London Equities Newsroom; +44 20 7542 7717))

((For more news, please click here [GENL.L]))

drill ergebnisse sollen noch dieses jahr veröffentlicht werden.......rumors nachbarboard

Antwort auf Beitrag Nr.: 42.506.904 von ikarusfly am 21.12.11 09:41:17geht das so schnell??

Antwort auf Beitrag Nr.: 42.506.915 von Frhstck am 21.12.11 09:43:13Bekhme results in December..... es wurde zu verschiedenen zeiten in vers. gebieten gebohrt. und für den bereich bekhme sollen in dec. ergebnisse kommen.

und wenn die gut ausfallen sollten

und wenn die gut ausfallen sollten

I wouldn't be surprised to hear a few more rumours as Mark Leftly certainly kicked the hornets nest.

If Chevron were not privy to any Exxon/KRG talks etc then they are now! £8 has been laid down as a marker which has been rumoured by the independent as being likely to be rejected.

If an auction is underway - it will be underway as of now if not although sounds like it is in full swing over the last few weeks.

The hungry buyers need to woo TK, GKP and the KRG with many different fruits. The KRG will want guarantees on infrastructure and cap ex spend etc.

We know Sinopec could blow them all away - and I think Mark Hanson will certainly in demand both from his old chinese contacts but also from the GKP board.

If Chevron were not privy to any Exxon/KRG talks etc then they are now! £8 has been laid down as a marker which has been rumoured by the independent as being likely to be rejected.

If an auction is underway - it will be underway as of now if not although sounds like it is in full swing over the last few weeks.

The hungry buyers need to woo TK, GKP and the KRG with many different fruits. The KRG will want guarantees on infrastructure and cap ex spend etc.

We know Sinopec could blow them all away - and I think Mark Hanson will certainly in demand both from his old chinese contacts but also from the GKP board.

Geile Übersetzung:

Golf Keystone sagte, dass es seine Anstrengungen auf die Entwicklung Ölfelder in den kurdischen Regionen des Irak konzentrieren wollte. Diese Bewegung folgt Anweisungen von Golf Keystone, dass es in Übernahme Gespräche mit U.S. Supermajor Exxon Mobil einbezogen war nicht.

Read more: http://www.upi.com/Business_News/Energy-Resources/2011/12/21…

Golf Keystone sagte, dass es seine Anstrengungen auf die Entwicklung Ölfelder in den kurdischen Regionen des Irak konzentrieren wollte. Diese Bewegung folgt Anweisungen von Golf Keystone, dass es in Übernahme Gespräche mit U.S. Supermajor Exxon Mobil einbezogen war nicht.

Read more: http://www.upi.com/Business_News/Energy-Resources/2011/12/21…

As Exxon continue to 'sound out' (yeah, right) GKP for a full t/o, they are certainly being reminded at every turn by both GKP and the KRG that others are waiting to pounce:

13th November – The Independent

According to sources, Chevron has "run the slide rule" over the Shaikan onshore block, which is majority owned by London-listed group Gulf Keystone Petroleum.

18th November

We are told in the press that, following Exxon’s entry to Kurdistan, ‘Chevron, Italy's Eni and Total are thought to be negotiating deals with the KRG, but none will comment.’

2nd December

In an article in which Todd Kozel publicised target production of 400k-500k barrels from Shaikan, an asset he described as ‘quickly becoming another Kirkuk’, the French major Total is cited as having ‘the expertise and the required technology that can benefit Gulf Keystone.’ And Adnan Samrrai adds: ‘that Chevron may be more interested in farming into Shaikan.’

14th December

Kurdish delegation, including the prime minister, visits Paris. Salih ‘Declined to comment on whether there were talks with the oil company, Total, or if the company have shown interest in exploration agreements. There was no immediate comment from the French company.’

Yesterday – This Is Money

‘Dealers heard revived whispers that several major oil companies are running the slide rule over Afren, including Italy’s ENI, Total of France and America’s Chevron. Chevron has made no secret of its desire to get into Kurdistan.’

13th November – The Independent

According to sources, Chevron has "run the slide rule" over the Shaikan onshore block, which is majority owned by London-listed group Gulf Keystone Petroleum.

18th November

We are told in the press that, following Exxon’s entry to Kurdistan, ‘Chevron, Italy's Eni and Total are thought to be negotiating deals with the KRG, but none will comment.’

2nd December

In an article in which Todd Kozel publicised target production of 400k-500k barrels from Shaikan, an asset he described as ‘quickly becoming another Kirkuk’, the French major Total is cited as having ‘the expertise and the required technology that can benefit Gulf Keystone.’ And Adnan Samrrai adds: ‘that Chevron may be more interested in farming into Shaikan.’

14th December

Kurdish delegation, including the prime minister, visits Paris. Salih ‘Declined to comment on whether there were talks with the oil company, Total, or if the company have shown interest in exploration agreements. There was no immediate comment from the French company.’

Yesterday – This Is Money

‘Dealers heard revived whispers that several major oil companies are running the slide rule over Afren, including Italy’s ENI, Total of France and America’s Chevron. Chevron has made no secret of its desire to get into Kurdistan.’

bin gespannt ob die cowboys.....

hoffe auf den gleichen verlauf wie die letzten 2 tage......zuerst down und dann stück für stück rauf

hoffe auf den gleichen verlauf wie die letzten 2 tage......zuerst down und dann stück für stück rauf

there is no link because it has not made the news 'yet'. This BB has proven to be around 12 hrs ahead minimum (sometimes days) when it comes to the breaking news. Astonishing resource and I imagine all the city analysts and press are logging in daily.

When Exxon made their move to embarrass Maliki by signing oil contracts with the Kurds and defying his pet dog Sharistani - that was the game changer. Everything that has happened since has been down hill for Maliki.

It's clear as day to me that there is a concerted effort to get him out and he's not going down without a fight.

Note Sharistani is 'quiet' these days and I would expect him to try and hang on by his toe nails when it comes to the oil ministry. But I doubt it's going to happen.

Maliki biggest mistake was going back on his word. When you can't trust a man's word - he's as good as dead in terms of politics.

All he had to do was sign the O&G and he could have been a hero. Instead he's mr zero and going down faster than a Genel drill bit.

The Kurds rule and it looks like Exxon are relocating for good.

I expect a few more super majors to follow as it looks like 'regional' powers will lead the way from here on and ironically - Baghdad's contracts probably are not worth squat when Maliki goes. Whereas, the kurds contracts will remain constitutional for decades to come.

Exxon can make the leap to the north knowing with confidence that they have one of the biggest oil reserve opportunities in the world - should they JV or buy out GKP.

I can't believe we are sub 200p - infact I can't believe we are sub 400p - but then Mr Market has been dire in valuing anything properly in 2011.

HUB

When Exxon made their move to embarrass Maliki by signing oil contracts with the Kurds and defying his pet dog Sharistani - that was the game changer. Everything that has happened since has been down hill for Maliki.

It's clear as day to me that there is a concerted effort to get him out and he's not going down without a fight.

Note Sharistani is 'quiet' these days and I would expect him to try and hang on by his toe nails when it comes to the oil ministry. But I doubt it's going to happen.

Maliki biggest mistake was going back on his word. When you can't trust a man's word - he's as good as dead in terms of politics.

All he had to do was sign the O&G and he could have been a hero. Instead he's mr zero and going down faster than a Genel drill bit.

The Kurds rule and it looks like Exxon are relocating for good.

I expect a few more super majors to follow as it looks like 'regional' powers will lead the way from here on and ironically - Baghdad's contracts probably are not worth squat when Maliki goes. Whereas, the kurds contracts will remain constitutional for decades to come.

Exxon can make the leap to the north knowing with confidence that they have one of the biggest oil reserve opportunities in the world - should they JV or buy out GKP.

I can't believe we are sub 200p - infact I can't believe we are sub 400p - but then Mr Market has been dire in valuing anything properly in 2011.

HUB

Zitat von ikarusfly: http://www.forbes.com/sites/greatspeculations/2011/12/21/exx…

Moin Ikarus, wollte mal Danke sagen. fürs recherchieren der Infos.

Erfolgreichen Handelstag wünscht :

Earthfire

http://www.microsofttranslator.com/BV.aspx?ref=IE8Activity&a…

Vielleicht für den einen oder anderen hier interessant.

Vielleicht für den einen oder anderen hier interessant.

morgen

Antwort auf Beitrag Nr.: 42.512.095 von Earthfire am 22.12.11 07:49:54@earth danke

With only 2 trading days left in the year (plus a half day) MOL are really are stringing out BEK-1 results.

Surely the press department have the RNS all typed up and ready to go or do management plan to come in to work next week just to answer press enquiries etc etc.

Get the news out today and then you can trolly off to the supermarkets for the turkey and start xmas hols.

HUB

Surely the press department have the RNS all typed up and ready to go or do management plan to come in to work next week just to answer press enquiries etc etc.

Get the news out today and then you can trolly off to the supermarkets for the turkey and start xmas hols.

HUB

hoffe das ihr alle schöne feiertage hattet...

The pace that the Kurdistan oil play has advanced in 2011 is an example of the excitement that can be created by new and emerging oil frontiers.

The semi-autonomous region of northern Iraq is one of the world’s last great oil frontiers, according to former BP boss Tony Hayward.

This widely cited comment was made amid the summer’s frenzied land grab in Kurdistan when in a few short weeks most of the region’s prospective land was snapped up by mid-tier oil companies.

The period also saw Vallares, then a £2 billion vehicle for Hayward and City financier Nat Rothschild, merge with Turkish firm Genel, one of the leading players in Kurdistan. Afren (LON:AFR) and Petroceltic (LON:PCI) also inked deals in the region.

In fact, barely a week goes by without further deals being agreed. So far the majors are yet to show their hands, though there are reports, still not confirmed, that ExxonMobil (NYSE:XOM) is ready to plant its flag in Kurdistan.

The experience of Gulf Keystone Petroleum (LON:GKP) is an interesting case study of how success with the drill bit in a newly emerging sphere of interest can utterly transform a company’s fortunes.

Borrowing parlance used by gold prospectors of old, GKP has hit the mother lode with its Shaikan discovery in Kurdistan, which is estimated to contain between 8 and 13.4 billion barrels of oil

Prior to striking first oil in August 2009, shares in the explorer were changing hands at just 13p. Now, nearly two years on, they are worth just under 200p a share, which values the company at £1.6 billion.

It is a vivid illustration of what can happen to a junior explorer when it strikes big in an up-and-coming oil frontier.

Another potentially world-class oil frontier is found in the harsh environment of the south Atlantic, in the waters off the Falkland Islands.

http://www.proactiveinvestors.co.uk/companies/news/37295/eme…

The semi-autonomous region of northern Iraq is one of the world’s last great oil frontiers, according to former BP boss Tony Hayward.

This widely cited comment was made amid the summer’s frenzied land grab in Kurdistan when in a few short weeks most of the region’s prospective land was snapped up by mid-tier oil companies.

The period also saw Vallares, then a £2 billion vehicle for Hayward and City financier Nat Rothschild, merge with Turkish firm Genel, one of the leading players in Kurdistan. Afren (LON:AFR) and Petroceltic (LON:PCI) also inked deals in the region.

In fact, barely a week goes by without further deals being agreed. So far the majors are yet to show their hands, though there are reports, still not confirmed, that ExxonMobil (NYSE:XOM) is ready to plant its flag in Kurdistan.

The experience of Gulf Keystone Petroleum (LON:GKP) is an interesting case study of how success with the drill bit in a newly emerging sphere of interest can utterly transform a company’s fortunes.