Metallica Minerals (MLM.AX) - noch unbekannter Bauxite Explorer - Akt. 3,8 audcent - Ziel kurzf. 10, - 500 Beiträge pro Seite

eröffnet am 30.08.16 14:55:34 von

neuester Beitrag 09.08.17 09:30:35 von

neuester Beitrag 09.08.17 09:30:35 von

Beiträge: 50

ID: 1.237.608

ID: 1.237.608

Aufrufe heute: 0

Gesamt: 3.166

Gesamt: 3.166

Aktive User: 0

ISIN: AU000000MLM0 · WKN: 591060

0,0165

EUR

+13,79 %

+0,0020 EUR

Letzter Kurs 10:09:41 Lang & Schwarz

Neuigkeiten

06.09.23 · Stephan Bogner Anzeige |

13.06.23 · Stephan Bogner Anzeige |

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 45,20 | +14,14 | |

| 76,28 | +10,47 | |

| 4,9300 | +10,04 | |

| 17.600,00 | +10,00 | |

| 204,50 | +9,98 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,5460 | -6,83 | |

| 2,1800 | -9,17 | |

| 0,5850 | -10,00 | |

| 4,2300 | -17,86 | |

| 47,85 | -97,99 |

Entwicklung / Historie

Warum ein neuer Thread, gibt doch schon einen?

Ich denke wir haben hier eine gute kurzfristige Investmentchance, auf die ich hinweisen will.

Ich habe mich die letzten Jahre sehr intensiv mit dem Bauxite Markt (Verkauf Richtung China) beschäftigt und hier insbesondere mit Metro Mining (MMI.AX). Siehe auch den Metro Haupt Thread.

Metallica war übrigens die ursprüngliche Mutter von Metro, hat aber soweit die letzten Jahre diverse Explorer-Beteiligungen verkauft, sowie in letzter Zeit auch eigene Non-Core Assets versilbert.

Im Rahmen des Peer Group Vergleiches der australischen Bauxite Explorer wurde Metallica natürlich die letzten Jahre immer etwas von mir mit analysiert.

Die letzten Jahre war der Wert eher uninteressant. Man hat sich mit zu vielen Projekten verzettelt und nix wirklich vorangebracht. Zum Beispiel: Nickel-Cobalt-Scandium, Graphite und Heavy Mineral Sands Projekte.

Nun scheint man sich seit einigen Monaten wohl wirklich auf das 50% Bauxite Projekt zu konzentrieren, was meiner Ansicht auch Sinn macht.

Highlights des Bauxite Projektes sind:

Well funded through to grant of Urquhart Bauxite mining lease

On track to commence bauxite production in H1 2017 with minimal capex

Commonwealth Government confirms no requirement for EIS

Heads of Agreement for access and logistics through Hey Point significantly de-risks delivery

Ramp up to 1.5 – 2mtpa to deliver sustainable free cash flow

Positiv finde ich:

A) Es wird nur die kleine Umweltstudie gebraucht.(Man sieht wie Gulf und Metro immer wieder mehr Zeit mit der großen Umweltstudie verschwenden)

B) Nutzung der vorhandenen Verladestation Hey Point angedacht (nur ca. 10 Km entfernt)

C) Bauxite von Metallica hat eine gute Qualität (Besser als alle anderen Explorer Konkurrenten) mit 40.6% available Al and 4.9% RSi

D) Noch sehr günstige Bewertung mit knapp 9 Mio. aud Börsenwert

E) Produktionsstart schon in Q2/2017 angedacht

F) Sehr geringe CAPEX zu erwarten

G) Geringe OPEX wahrscheinlich und damit eine gute Marge auch bei dem nur Zeit eher niedrigen Bauxite Preis

H) Ausreichend Cash bis zur Genehmigung

Negativ:

A) Resource mit 7,5 mio /t doch recht klein. Würde also beim einem 1,5 Mio/t Szenario 5 Jahre Minenleben bedeuten. Aber weiteres large (42 Mt – 128 Mt) bauxite Exploration Target vorhanden (wenn auch eine Kilometer entfernt)

B) Management im Vergleich zu Metro eher mittelmäßig.

C) Kommunikation zu den Shareholder verbesserungswürdig

D) Zeitplan realistisch ?

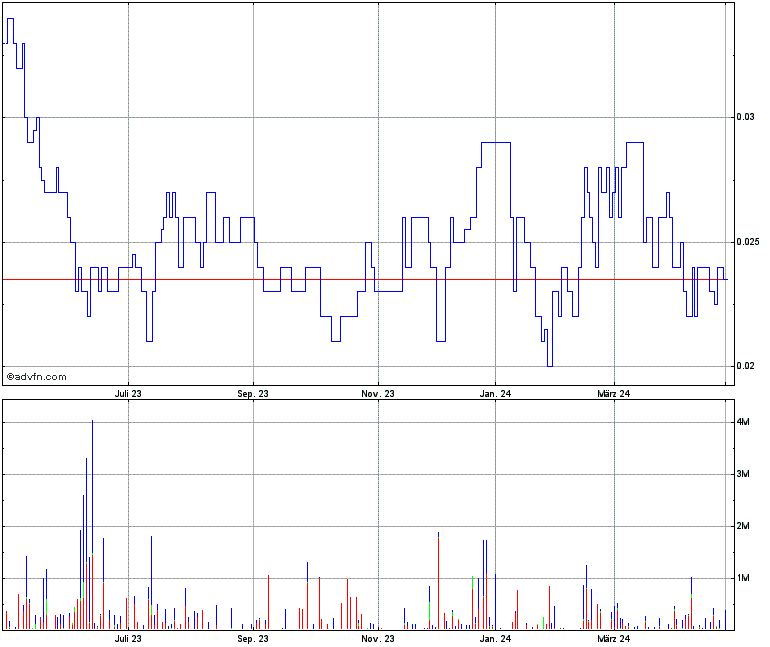

Hier die Chartentwicklung:

Mehrjahreschart:

Jahreschart:

Monatschart:

Orderbuch:

Sollte der Eisberg (aktuell ca. 5 mio Shares) bis 4 audcent fallen, würde es auch charttechnisch ein Ausbruchssignal bedeuten

Aktuelle Präsi:

http://hotcopper.com.au/documentdownload?id=uOMxKKzFkiWRTLKh…

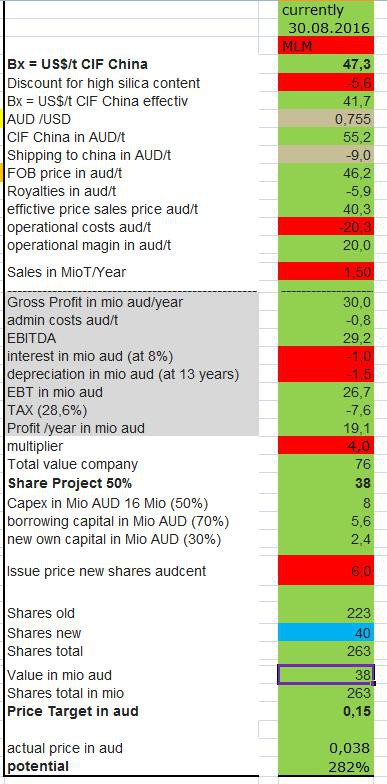

Kurszielkalkulation:

Meine Kurszielkalkulation kommt auf 15 audcent. Nehmen wir einen Sicherheitsabschlag reden wir von 10 audcent. Hohes Kurspotential von aktuell 3,8 audcent wäre also gegeben.

Ich bin dabei vom kleineren 1,5 Mio/t Szenario (nicht 2 Mio/t) ausgegangen und mit dem aktuell historisch gesehen niedrigen Bauxite Referenzpreis von 47,3 USD/T gerechnet, Verlustvorträge nicht berücksichtigt, KGV Multiplikator von 4 wegen der kurzen Minendauer, auch wenn 42 Mt – 128 Mt bauxite Exploration Target da sind. Auch die anderen Projekt mit null bewertet.

Katalysator:

Warum denke ich das hier kurstechnisch kurzfristig (1-6 Monate) was passieren könnte ?

Stutzig wurde ich über folgende Aussage im ASX Release vom 11 August 2016:

• Key drill program commences at Urquhart Bauxite project near Weipa in north

Queensland to assist final planning for 2017 mine start

• Results to be used as part of the Urquhart Bauxite Pre-Feasibility Study (PFS)

which is planned to be completed in 8-10 weeks

• PFS outcomes expected to confirm result of Metallica‘s internal Options Study

completed on Urquhart early in 2016

Metallica CEO, Mr Simon Slesarewich:

“The new drill program will deliver closed spaced drilling results to assist detailed mine

planning at Urquhart Bauxite project for the planned commencement of operations in

the first half of 2017. Metallica remains bullish that this project will deliver significant

shareholder value and is looking forward to sharing the results of the Pre-Feasibility

Study as soon as they are available.”

11 August und dann 8-10 Wochen weiter ist irgendwann im Oktober 2016. Dann sollte die interne vielversprechende Study vom Jahresanfang bestätigt werden und was noch wichtiger ist, der Markt erfährt erstmalig vom dieses kleinen aber feinen Bauxite Projekt (inklusive Wirtschaftlichkeitszahlen).

Ich rechne daher spätestens im Oktober mit stärkeren Kursanstiegen. Der Wert ist noch überhaupt nicht gelaufen und im Oktober sollte der Wert vom Markt entdeckt werden.

Meinungen ?

Warum ein neuer Thread, gibt doch schon einen?

Ich denke wir haben hier eine gute kurzfristige Investmentchance, auf die ich hinweisen will.

Ich habe mich die letzten Jahre sehr intensiv mit dem Bauxite Markt (Verkauf Richtung China) beschäftigt und hier insbesondere mit Metro Mining (MMI.AX). Siehe auch den Metro Haupt Thread.

Metallica war übrigens die ursprüngliche Mutter von Metro, hat aber soweit die letzten Jahre diverse Explorer-Beteiligungen verkauft, sowie in letzter Zeit auch eigene Non-Core Assets versilbert.

Im Rahmen des Peer Group Vergleiches der australischen Bauxite Explorer wurde Metallica natürlich die letzten Jahre immer etwas von mir mit analysiert.

Die letzten Jahre war der Wert eher uninteressant. Man hat sich mit zu vielen Projekten verzettelt und nix wirklich vorangebracht. Zum Beispiel: Nickel-Cobalt-Scandium, Graphite und Heavy Mineral Sands Projekte.

Nun scheint man sich seit einigen Monaten wohl wirklich auf das 50% Bauxite Projekt zu konzentrieren, was meiner Ansicht auch Sinn macht.

Highlights des Bauxite Projektes sind:

Well funded through to grant of Urquhart Bauxite mining lease

On track to commence bauxite production in H1 2017 with minimal capex

Commonwealth Government confirms no requirement for EIS

Heads of Agreement for access and logistics through Hey Point significantly de-risks delivery

Ramp up to 1.5 – 2mtpa to deliver sustainable free cash flow

Positiv finde ich:

A) Es wird nur die kleine Umweltstudie gebraucht.(Man sieht wie Gulf und Metro immer wieder mehr Zeit mit der großen Umweltstudie verschwenden)

B) Nutzung der vorhandenen Verladestation Hey Point angedacht (nur ca. 10 Km entfernt)

C) Bauxite von Metallica hat eine gute Qualität (Besser als alle anderen Explorer Konkurrenten) mit 40.6% available Al and 4.9% RSi

D) Noch sehr günstige Bewertung mit knapp 9 Mio. aud Börsenwert

E) Produktionsstart schon in Q2/2017 angedacht

F) Sehr geringe CAPEX zu erwarten

G) Geringe OPEX wahrscheinlich und damit eine gute Marge auch bei dem nur Zeit eher niedrigen Bauxite Preis

H) Ausreichend Cash bis zur Genehmigung

Negativ:

A) Resource mit 7,5 mio /t doch recht klein. Würde also beim einem 1,5 Mio/t Szenario 5 Jahre Minenleben bedeuten. Aber weiteres large (42 Mt – 128 Mt) bauxite Exploration Target vorhanden (wenn auch eine Kilometer entfernt)

B) Management im Vergleich zu Metro eher mittelmäßig.

C) Kommunikation zu den Shareholder verbesserungswürdig

D) Zeitplan realistisch ?

Hier die Chartentwicklung:

Mehrjahreschart:

Jahreschart:

Monatschart:

Orderbuch:

Sollte der Eisberg (aktuell ca. 5 mio Shares) bis 4 audcent fallen, würde es auch charttechnisch ein Ausbruchssignal bedeuten

Aktuelle Präsi:

http://hotcopper.com.au/documentdownload?id=uOMxKKzFkiWRTLKh…

Kurszielkalkulation:

Meine Kurszielkalkulation kommt auf 15 audcent. Nehmen wir einen Sicherheitsabschlag reden wir von 10 audcent. Hohes Kurspotential von aktuell 3,8 audcent wäre also gegeben.

Ich bin dabei vom kleineren 1,5 Mio/t Szenario (nicht 2 Mio/t) ausgegangen und mit dem aktuell historisch gesehen niedrigen Bauxite Referenzpreis von 47,3 USD/T gerechnet, Verlustvorträge nicht berücksichtigt, KGV Multiplikator von 4 wegen der kurzen Minendauer, auch wenn 42 Mt – 128 Mt bauxite Exploration Target da sind. Auch die anderen Projekt mit null bewertet.

Katalysator:

Warum denke ich das hier kurstechnisch kurzfristig (1-6 Monate) was passieren könnte ?

Stutzig wurde ich über folgende Aussage im ASX Release vom 11 August 2016:

• Key drill program commences at Urquhart Bauxite project near Weipa in north

Queensland to assist final planning for 2017 mine start

• Results to be used as part of the Urquhart Bauxite Pre-Feasibility Study (PFS)

which is planned to be completed in 8-10 weeks

• PFS outcomes expected to confirm result of Metallica‘s internal Options Study

completed on Urquhart early in 2016

Metallica CEO, Mr Simon Slesarewich:

“The new drill program will deliver closed spaced drilling results to assist detailed mine

planning at Urquhart Bauxite project for the planned commencement of operations in

the first half of 2017. Metallica remains bullish that this project will deliver significant

shareholder value and is looking forward to sharing the results of the Pre-Feasibility

Study as soon as they are available.”

11 August und dann 8-10 Wochen weiter ist irgendwann im Oktober 2016. Dann sollte die interne vielversprechende Study vom Jahresanfang bestätigt werden und was noch wichtiger ist, der Markt erfährt erstmalig vom dieses kleinen aber feinen Bauxite Projekt (inklusive Wirtschaftlichkeitszahlen).

Ich rechne daher spätestens im Oktober mit stärkeren Kursanstiegen. Der Wert ist noch überhaupt nicht gelaufen und im Oktober sollte der Wert vom Markt entdeckt werden.

Meinungen ?

Achso eins noch:

Falls jedem Interesse hat, bitte nur in Australien unter dem Symbol MLM kaufen. In Deutschland werden unverschämte BID / ASK Taxen gestellt.

-------------------

zu oben noch

(wenn auch eine Kilometer entfernt)

Soll natürlich "einige" heißen

Falls jedem Interesse hat, bitte nur in Australien unter dem Symbol MLM kaufen. In Deutschland werden unverschämte BID / ASK Taxen gestellt.

-------------------

zu oben noch

(wenn auch eine Kilometer entfernt)

Soll natürlich "einige" heißen

alles drin was rein gehört!

danke für deine mühe und den tip!

klingt recht verlockend.

werde mich heute abend mal einlesen um eventuell das verschlafen des einstiegs wie bei metro dieses mal vermeiden

danke für deine mühe und den tip!

klingt recht verlockend.

werde mich heute abend mal einlesen um eventuell das verschlafen des einstiegs wie bei metro dieses mal vermeiden

Manchmal kommen sie wieder.....war MLM nicht auch mal die Mutter von Metrocoal? Die hat mir vor x Jahren mal ne fette Rendite gebracht und ist deswegen immer noch unter meinen favourites bei W:o gewesen....

Danke für den neuen Hinweis und die Threaderöffnung. Werde mich mal einlesen und ggfls handeln.

Danke für den neuen Hinweis und die Threaderöffnung. Werde mich mal einlesen und ggfls handeln.

Antwort auf Beitrag Nr.: 53.166.603 von Reiners am 30.08.16 14:55:34

Hallo,

Danke auf jeden Fall für Das drauf aufmerksam machen.

Mir wäre Das Minenleben einfach zu klein(auch wenn ja noch ein, weitaus, größeres Resourcenziel aussteht),

da hab ich Unterkante schon gern 10ys zu stehen,

lieber 20, aufwärts

Hallo,

Danke auf jeden Fall für Das drauf aufmerksam machen.

Mir wäre Das Minenleben einfach zu klein(auch wenn ja noch ein, weitaus, größeres Resourcenziel aussteht),

da hab ich Unterkante schon gern 10ys zu stehen,

lieber 20, aufwärts

Trading Spotlight

Antwort auf Beitrag Nr.: 53.167.491 von Popeye82 am 30.08.16 16:23:54@ Reiners ,

deine Beiträge sind einfach klasse,

du versuchst immer sehr objektiv zu bleiben und Chancen und Risiken richtig einzuschätzen und stellst Deine Recherchen auch immer allen zur Verfügung.

Ich wollte Dich eigentlich schon mal fragen ob du dich auch für andere Explorer interessierst derzeit, insofern interessant, aber auch für mich etwas klein der Wert.

Werde aber die Verfügbaren Daten mir mal genau ansehen und dann entscheiden.

deine Beiträge sind einfach klasse,

du versuchst immer sehr objektiv zu bleiben und Chancen und Risiken richtig einzuschätzen und stellst Deine Recherchen auch immer allen zur Verfügung.

Ich wollte Dich eigentlich schon mal fragen ob du dich auch für andere Explorer interessierst derzeit, insofern interessant, aber auch für mich etwas klein der Wert.

Werde aber die Verfügbaren Daten mir mal genau ansehen und dann entscheiden.

Klar wäre eine längere Minenlebensdauer wünschenswert, nur dann wäre der Kurs wohl auch nicht da, wo er jetzt ist und in meiner Berechnung ist es ja auch berücksichtigt.

Minendauer sollte vorallem dann lang sein, wenn es um eine nicht so einfache Operation geht mit hoher Capex und Aufbau von einer gewissen Infrastruktur, die sich über die Jahre bezahlt machen muss.

Ist hier aber nicht der Fall. Das Zeug liegt einen Meter unter der Erde, muss nicht groß aufbereitet werden und "nur" kurz zur 10 Km entfernten vorhandenen Verladestation gefahren werden.

In 5 Jahren würde man "einfach" zum nächsten Gebiet mit seinen Baggern und LKW weiterziehen.

Weil es so einfach ist, kam die unbekannten neuen Produzenten in Malaysia auch so schnell auf den Markt. Metallica hat halt noch den Vorteil, dass das Bauxite ein bessere Qualität hat.

-----------

Mir ist aber auch klar das Metallica noch eine Menge Milesstones bis dahin erledigen muss.

Mir ist etwas anderes wichtiger:

Nochmal:

Der Markt kennt noch überhaupt keine Wirtschalftlichkeitszahlen vom Projekt. Diese sind jetzt für Oktober angekündigt. Das die vielversprechend sein können / sollten habe ich in meiner Berechnung simulieret. Klar hat mir dabei mein Wissen zu Metro / Gulf und dem Bauxitemarkt geholfen.

Spricht doch nix dagegen jetzt rein und von mir aus Ende Oktober nach den Zahlen zur PFS mit 7,5 audcent und 100% Gain wieder raus zu gehen. Man muss hier nicht 10 Jahre investiert bleiben.

Wichtig für mich, Metallica wie auch der Bauxite Markt im Allgemeinen ist im Moment weder von den Anlegern noch den Anaysten in irgendeiner Weise gehypt worden. Kurstechnisch befinden wir uns immer noch nahe dem All Time Low.

Minendauer sollte vorallem dann lang sein, wenn es um eine nicht so einfache Operation geht mit hoher Capex und Aufbau von einer gewissen Infrastruktur, die sich über die Jahre bezahlt machen muss.

Ist hier aber nicht der Fall. Das Zeug liegt einen Meter unter der Erde, muss nicht groß aufbereitet werden und "nur" kurz zur 10 Km entfernten vorhandenen Verladestation gefahren werden.

In 5 Jahren würde man "einfach" zum nächsten Gebiet mit seinen Baggern und LKW weiterziehen.

Weil es so einfach ist, kam die unbekannten neuen Produzenten in Malaysia auch so schnell auf den Markt. Metallica hat halt noch den Vorteil, dass das Bauxite ein bessere Qualität hat.

-----------

Mir ist aber auch klar das Metallica noch eine Menge Milesstones bis dahin erledigen muss.

Mir ist etwas anderes wichtiger:

Nochmal:

Der Markt kennt noch überhaupt keine Wirtschalftlichkeitszahlen vom Projekt. Diese sind jetzt für Oktober angekündigt. Das die vielversprechend sein können / sollten habe ich in meiner Berechnung simulieret. Klar hat mir dabei mein Wissen zu Metro / Gulf und dem Bauxitemarkt geholfen.

Spricht doch nix dagegen jetzt rein und von mir aus Ende Oktober nach den Zahlen zur PFS mit 7,5 audcent und 100% Gain wieder raus zu gehen. Man muss hier nicht 10 Jahre investiert bleiben.

Wichtig für mich, Metallica wie auch der Bauxite Markt im Allgemeinen ist im Moment weder von den Anlegern noch den Anaysten in irgendeiner Weise gehypt worden. Kurstechnisch befinden wir uns immer noch nahe dem All Time Low.

Antwort auf Beitrag Nr.: 53.168.478 von Lenardo am 30.08.16 18:20:18" aber auch für mich etwas klein der Wert."

Dazu sage ich nur:

Was hast Du gegen klein aber fein?

-------------

Wie gesagt, ich spekuliere auf die PFS im Oktober. Dann entscheide ich ob ich drin bleibe, teilweise rausgehe oder komplett.

Für mich die die Minendauer oder die Größe des Wertes alleine noch kein K.O Kriterium.

Wenn es für euch so ist, dann ist es halt so.

------------------

Man kann es auch noch anders sehen. Ich denke, mal dass der Kurs durch die PFS Zahlen nicht unbedingt sinken wird.

Dazu sage ich nur:

Was hast Du gegen klein aber fein?

-------------

Wie gesagt, ich spekuliere auf die PFS im Oktober. Dann entscheide ich ob ich drin bleibe, teilweise rausgehe oder komplett.

Für mich die die Minendauer oder die Größe des Wertes alleine noch kein K.O Kriterium.

Wenn es für euch so ist, dann ist es halt so.

------------------

Man kann es auch noch anders sehen. Ich denke, mal dass der Kurs durch die PFS Zahlen nicht unbedingt sinken wird.

sau angenehm hier mitzulesen.

ich fühl mich nach dem lesen deiner prima darstellung, als ob ich das teil schon 5 jahre kennen würde. werde mich jetzt mal bisl einlesen.

ich fühl mich nach dem lesen deiner prima darstellung, als ob ich das teil schon 5 jahre kennen würde. werde mich jetzt mal bisl einlesen.

Anscheinend ist heute Nacht keiner von euch eingestiegen, zumindest kaum Volumen heute.

Sei's drum

----------------------------

Hier noch mal ein Inverview mit dem CEO aus Mai 2016, ganz interessant

Metallica Minerals (ASX:MLM) talks resource development and exploration

May 20, 2016 11:20 AM

Transcription of Finance News Network Interview with Metallica Minerals Limited (ASX:MLM) CEO, Simon Siesarewich

Clive Tompkins: Hello I’m Clive Tompkins for the Finance News Network. Joining me from Metallica Minerals Limited (ASX:MLM) is CEO, Simon Siesarewich. Simon, welcome to FNN.

Simon Siesarewich: Thanks for having me.

Clive Tompkins: First up, can you start with an introduction to Metallica Minerals?

Simon Siesarewich: Metallica’s an ASX listed junior resource company. We’ve got a market cap of about $7 million or $8 million; we’ve been listed for about 11 years. And we’re very much focused on our direct shipping bauxite project called Urquhart Point, which is up near Weipa in northern Queensland.

Clive Tompkins: Now to your Cape York heavy mineral sand and bauxite project, where the Urquhart bauxite project seems to be the priority. What does it contain?

Simon Siesarewich: Urquhart bauxite’s got about 7.5/8 million tonnes in direct shipping bauxite. It’s located directly opposite Weipa, so it’s on deep water. We’re very much focused on bringing that into production. The benefit that project has is twofold. Firstly, it’s a low temperature bauxite, which is sought after in the world market and secondly, it’s on deep water. So the capital to bring that on is extremely low and we can bring that into production very very quickly, with minimal requirements on capital and also on approvals.

Clive Tompkins: What’s been taking place?

Simon Siesarewich: We’ve been busy, very very busy on approvals, which isn’t all that sexy unfortunately. But it’s a lot of the grunt work that we need to do, to make sure we have all our approvals in place that’ll make this happen. Critically, what we’ve done is de-risk the project by delivering a logistic solution. So 15 kilometres away from Urquhart Point is another small bauxite mine, called Hey Point. We’ve executed heads of agreement with Hey Point to do the logistic services, to get our bauxite from land and onto export ships, which will be able to go into the open market. That mine is now in production, i.e. Hey Point’s in production. And we expect to piggyback off the back of their infrastructure, which means again, it’s about low capital and bringing this into market as quickly as possible.

Clive Tompkins: When do you see bauxite production commencing?

Simon Siesarewich: We’re confident that we’ll be producing bauxite, by the first half of 2017. We think we’ll have the approvals in place over the wet season 2016/17. Obviously that’s not the best time up around Weipa to be producing a new mine, so we’ll wait for that wet season to stop and then go into production. The benefit that Urquhart bauxite has is it doesn’t require any infrastructure. So therefore, the construction timetable for this is a couple of months and then we’re into cash flow, which is an absolute benefit for any project anywhere, but particularly for this one.

Clive Tompkins: You have an exploration program planned for the coming months. What do you hope to find?

Simon Siesarewich: So knowing that program is twofold, firstly we will increase the resource category and the confidence in that resource category. So we’ll have one to two years worth of production measured, then an indicated tale and then inferred thereafter. We’ll also be getting bulk samples; we’ll be going out and testing the market and talking to buyers, and putting things in place. And when we do come into production in 2017, we have a ready market ready to go.

Clive Tompkins: Now to your other project the Esmeralda graphite project. Where is it located and what does it contain?

Simon Siesarewich: Esmeralda graphite project’s located in north Queensland, around Croydon. It’s a unique graphite project in that it’s hosted in granite. Most other graphite projects globally are metamorphic. Why this is unique is that usually hydrothermal projects like this have very high quality graphite. We put two holes into the project in late 2015 and got significant intercepts. We’ve since then done some metallurgical test work on those two holes and have got graphite purity of over 91 per cent, and with over a 90 per cent recovery. We’ve since gone and done some caustic bake work on that and got purities in the concentrate of over 97 per cent, which means a very high purity concentrate, which should be valuable in the market.

Clive Tompkins: What’s the priority for the next six months?

Simon Siesarewich: Priority there is to understand the market for where this could sit, because it is a unique style of mineralisation. Therefore, the graphite that comes from Esmeralda will have to find a niche, but it’s likely to have a high market value in that niche. So we’ll do some market studies and we also understand it’s a very large tenement portfolio there, so over 1,000 square kilometres. So we’ll go and find where the graphite’s concentrated and where it’s closest to surface.

Clive Tompkins: A more general question Simon. What has the price of graphite flake been doing over the last year?

Simon Siesarewich: Graphite flake I guess depends on the type of graphite; it’s an opaque market. But my reading of it is that graphite flake has probably gone up a little and that’s really on the back of the tech sector. But again, it comes back to the type of graphite you have and who you’re selling it to. So if you have an everyday run of the mill graphite, you’re probably getting less than what you would have a year ago, whereas that higher graphite going into the tech sector, is probably increasing in value.

Clive Tompkins: Now to financials and strategy. What’s your cash position and how much are you budgeting for exploration over the next six months?

Simon Siesarewich: So Metallica’s just recently completed a capital raise, where we raised $1.8 million; we’re well supported by existing shareholders. We’ve also just converted an option on the sale of a non-core limestone asset, which will deliver another $900,000 in cash. So when that’s completed, we’ll have $2.2 million to $2.3 million in cash, which means the company’s well funded well into next year. And to the grant of the mining lease at Urquhart Point, and that’s what we’re very much focused on. The exploration program that we’re doing in the coming quarter is nominal, it’s sort of $300,000 to $400,000, but there’ll be a lot of work being put into the marketing and pushing that project forward, into production.

Clive Tompkins: What is the company’s long-term strategy?

Simon Siesarewich: Metallica’s very much focused on becoming cash flow positive, it’s as simple as that. We will be focused on Urquhart bauxite to produce that cash flow. That will be a game changer for our company. And hopefully we will see a rerating off the back of that, once people understand that we are able to bring a project into market. From that it gives us a great platform to grow on. Both organically, there’s a large portfolio of bauxite and mineral sands projects within the joint venture, but also we’ll also be looking outside our normal home, which has been Queensland. We’ll look globally for other projects that add value to shareholders, and take advantage of where the cycle’s at right now.

Clive Tompkins: Last question Simon. Where would you like to see Metallica Minerals by year’s end?

Simon Siesarewich: By year’s end, we’d love to have the mining lease in our hot little hands and pushing towards production. And de-risk that project and bring cash flow in as soon as we can.

Clive Tompkins: Simon Siesarewich thanks for the update.

Simon Siesarewich: Thank you.

Sei's drum

----------------------------

Hier noch mal ein Inverview mit dem CEO aus Mai 2016, ganz interessant

Metallica Minerals (ASX:MLM) talks resource development and exploration

May 20, 2016 11:20 AM

Transcription of Finance News Network Interview with Metallica Minerals Limited (ASX:MLM) CEO, Simon Siesarewich

Clive Tompkins: Hello I’m Clive Tompkins for the Finance News Network. Joining me from Metallica Minerals Limited (ASX:MLM) is CEO, Simon Siesarewich. Simon, welcome to FNN.

Simon Siesarewich: Thanks for having me.

Clive Tompkins: First up, can you start with an introduction to Metallica Minerals?

Simon Siesarewich: Metallica’s an ASX listed junior resource company. We’ve got a market cap of about $7 million or $8 million; we’ve been listed for about 11 years. And we’re very much focused on our direct shipping bauxite project called Urquhart Point, which is up near Weipa in northern Queensland.

Clive Tompkins: Now to your Cape York heavy mineral sand and bauxite project, where the Urquhart bauxite project seems to be the priority. What does it contain?

Simon Siesarewich: Urquhart bauxite’s got about 7.5/8 million tonnes in direct shipping bauxite. It’s located directly opposite Weipa, so it’s on deep water. We’re very much focused on bringing that into production. The benefit that project has is twofold. Firstly, it’s a low temperature bauxite, which is sought after in the world market and secondly, it’s on deep water. So the capital to bring that on is extremely low and we can bring that into production very very quickly, with minimal requirements on capital and also on approvals.

Clive Tompkins: What’s been taking place?

Simon Siesarewich: We’ve been busy, very very busy on approvals, which isn’t all that sexy unfortunately. But it’s a lot of the grunt work that we need to do, to make sure we have all our approvals in place that’ll make this happen. Critically, what we’ve done is de-risk the project by delivering a logistic solution. So 15 kilometres away from Urquhart Point is another small bauxite mine, called Hey Point. We’ve executed heads of agreement with Hey Point to do the logistic services, to get our bauxite from land and onto export ships, which will be able to go into the open market. That mine is now in production, i.e. Hey Point’s in production. And we expect to piggyback off the back of their infrastructure, which means again, it’s about low capital and bringing this into market as quickly as possible.

Clive Tompkins: When do you see bauxite production commencing?

Simon Siesarewich: We’re confident that we’ll be producing bauxite, by the first half of 2017. We think we’ll have the approvals in place over the wet season 2016/17. Obviously that’s not the best time up around Weipa to be producing a new mine, so we’ll wait for that wet season to stop and then go into production. The benefit that Urquhart bauxite has is it doesn’t require any infrastructure. So therefore, the construction timetable for this is a couple of months and then we’re into cash flow, which is an absolute benefit for any project anywhere, but particularly for this one.

Clive Tompkins: You have an exploration program planned for the coming months. What do you hope to find?

Simon Siesarewich: So knowing that program is twofold, firstly we will increase the resource category and the confidence in that resource category. So we’ll have one to two years worth of production measured, then an indicated tale and then inferred thereafter. We’ll also be getting bulk samples; we’ll be going out and testing the market and talking to buyers, and putting things in place. And when we do come into production in 2017, we have a ready market ready to go.

Clive Tompkins: Now to your other project the Esmeralda graphite project. Where is it located and what does it contain?

Simon Siesarewich: Esmeralda graphite project’s located in north Queensland, around Croydon. It’s a unique graphite project in that it’s hosted in granite. Most other graphite projects globally are metamorphic. Why this is unique is that usually hydrothermal projects like this have very high quality graphite. We put two holes into the project in late 2015 and got significant intercepts. We’ve since then done some metallurgical test work on those two holes and have got graphite purity of over 91 per cent, and with over a 90 per cent recovery. We’ve since gone and done some caustic bake work on that and got purities in the concentrate of over 97 per cent, which means a very high purity concentrate, which should be valuable in the market.

Clive Tompkins: What’s the priority for the next six months?

Simon Siesarewich: Priority there is to understand the market for where this could sit, because it is a unique style of mineralisation. Therefore, the graphite that comes from Esmeralda will have to find a niche, but it’s likely to have a high market value in that niche. So we’ll do some market studies and we also understand it’s a very large tenement portfolio there, so over 1,000 square kilometres. So we’ll go and find where the graphite’s concentrated and where it’s closest to surface.

Clive Tompkins: A more general question Simon. What has the price of graphite flake been doing over the last year?

Simon Siesarewich: Graphite flake I guess depends on the type of graphite; it’s an opaque market. But my reading of it is that graphite flake has probably gone up a little and that’s really on the back of the tech sector. But again, it comes back to the type of graphite you have and who you’re selling it to. So if you have an everyday run of the mill graphite, you’re probably getting less than what you would have a year ago, whereas that higher graphite going into the tech sector, is probably increasing in value.

Clive Tompkins: Now to financials and strategy. What’s your cash position and how much are you budgeting for exploration over the next six months?

Simon Siesarewich: So Metallica’s just recently completed a capital raise, where we raised $1.8 million; we’re well supported by existing shareholders. We’ve also just converted an option on the sale of a non-core limestone asset, which will deliver another $900,000 in cash. So when that’s completed, we’ll have $2.2 million to $2.3 million in cash, which means the company’s well funded well into next year. And to the grant of the mining lease at Urquhart Point, and that’s what we’re very much focused on. The exploration program that we’re doing in the coming quarter is nominal, it’s sort of $300,000 to $400,000, but there’ll be a lot of work being put into the marketing and pushing that project forward, into production.

Clive Tompkins: What is the company’s long-term strategy?

Simon Siesarewich: Metallica’s very much focused on becoming cash flow positive, it’s as simple as that. We will be focused on Urquhart bauxite to produce that cash flow. That will be a game changer for our company. And hopefully we will see a rerating off the back of that, once people understand that we are able to bring a project into market. From that it gives us a great platform to grow on. Both organically, there’s a large portfolio of bauxite and mineral sands projects within the joint venture, but also we’ll also be looking outside our normal home, which has been Queensland. We’ll look globally for other projects that add value to shareholders, and take advantage of where the cycle’s at right now.

Clive Tompkins: Last question Simon. Where would you like to see Metallica Minerals by year’s end?

Simon Siesarewich: By year’s end, we’d love to have the mining lease in our hot little hands and pushing towards production. And de-risk that project and bring cash flow in as soon as we can.

Clive Tompkins: Simon Siesarewich thanks for the update.

Simon Siesarewich: Thank you.

ne noch nicht. will erstmal nix überstürzen. habe jetzt mal die liegenschaft und die letzte resourcenschätzung untersucht. ist halt alles inferred und erstreckt sich über einen weiten korridor. abstand der löcher waren bisher 320 m. schon recht großer abstand. als blockmodell wurde das übliche 100x100 model angesetzt. jedenfalls wurden die bereich zwischen den löchern dennoch als durchgängige erzschicht gewertet und die unbebohrten zwischenräume hochgerechnet.

mein problem damit ist lediglich jenes, wenn nun die infill-drills diesen durchgängigen körper nicht überall bestätigen fällt die aktuelle resource fix in sich zusammen. und da die 7,5 mio tonnen schon nicht so der absolute berg sind und wie ihr schon festgestellt habt ein überschaubares minenleben bietet könnte sich das dann eben unangenehm weiter verringern.

reiners, welche liegenschaft meinst du die 1 km weg sein soll? kann da gerade nix finden.

meinst du es könnte eher von vorteil oder nachteil sein, dass sich die liegenschaft neben derer von rio befindet?

mein problem damit ist lediglich jenes, wenn nun die infill-drills diesen durchgängigen körper nicht überall bestätigen fällt die aktuelle resource fix in sich zusammen. und da die 7,5 mio tonnen schon nicht so der absolute berg sind und wie ihr schon festgestellt habt ein überschaubares minenleben bietet könnte sich das dann eben unangenehm weiter verringern.

reiners, welche liegenschaft meinst du die 1 km weg sein soll? kann da gerade nix finden.

meinst du es könnte eher von vorteil oder nachteil sein, dass sich die liegenschaft neben derer von rio befindet?

Antwort auf Beitrag Nr.: 53.173.911 von sir_krisowaritschko am 31.08.16 11:58:40Ja das Upgrade der Resource (Bohrprogramm) läüft gerade, bzw. ist fertig und soll die Basis der PFS werden.

reiners, welche liegenschaft meinst du die 1 km weg sein soll?

Ich habe im Posting 2 meinen Fehler korrigiert und aus "eine" "einige" gemacht.

Um mit "einige" meine ich ca. 250 Km. Das weitere Explorergebiet liegt ca. 50 km nördlich von Metro/Gulf.

Siehe auch Karte in der Präsi

kann da gerade nix finden. meinst du es könnte eher von vorteil oder nachteil sein, dass sich die liegenschaft neben derer von rio befindet?

Weiss nicht ob Vor- oder Nachteil. Meinst Du mit Nachteil das Rio sicht bedrengt fühlt und dagegen wettert ? Ich denke MLM ist für RIO kein wirklicher Konkurrent. Vorteil könnte sein, das vielleicht die Qualität ähnlich gut ist wie die Spitzenqualität vom Branchenführer Rio.

reiners, welche liegenschaft meinst du die 1 km weg sein soll?

Ich habe im Posting 2 meinen Fehler korrigiert und aus "eine" "einige" gemacht.

Um mit "einige" meine ich ca. 250 Km. Das weitere Explorergebiet liegt ca. 50 km nördlich von Metro/Gulf.

Siehe auch Karte in der Präsi

kann da gerade nix finden. meinst du es könnte eher von vorteil oder nachteil sein, dass sich die liegenschaft neben derer von rio befindet?

Weiss nicht ob Vor- oder Nachteil. Meinst Du mit Nachteil das Rio sicht bedrengt fühlt und dagegen wettert ? Ich denke MLM ist für RIO kein wirklicher Konkurrent. Vorteil könnte sein, das vielleicht die Qualität ähnlich gut ist wie die Spitzenqualität vom Branchenführer Rio.

Mal sehen ob "die News" morgen etwas im Shareprice bewegt

Das gute vielleicht, es gibt nur 6 Australische Bauxite Juniors. Und da ABX, QBL und BAU aus verschiedenen Gründen rausfallen bleiben eigentlich nur MLM, MMI (und Gulf die man aber nicht kaufen kann.)

-------------------------------------------------------------

MLM is in the news of Mining News:

Bauxite plays for juniors

BAUXITE is looking like an interesting little niche play in the ASX resource sector with a number of juniors moving into position to hopefully prosper.

• Michael Quinn

• 31 Aug 2016

• 8:26

• Feature

Two such juniors, Metallica Minerals and Iron Mountain Mining were out on the promotion hustings last week when they presented at the Mining 2016 Resources Convention in Brisbane.

Iron Mountain has re-emerged out of iron ore-induced hibernation and headed to the Solomon Islands where it’s completing due diligence on the scrip-based acquisition of the Nendo bauxite project.

Non-exec director Brett Smith told the Mining 2016 Resources Convention in Brisbane that the prospects for bauxite were looking promising, with alumina refineries reportedly becoming concerned about bauxite supplies and major producer Rio said to have referred to it as ‘the new iron ore’.

Coincidentally Nendo was found by Rio forerunner CRA back in 1969.

While it is early days for Iron Mountain, the signs seem positive from what Smith says.

The bauxite found at Nendo was indicated to be of very good quality (including low silica) with testwork continuing.

The locals are also said to be very much behind a mining development, and given some of the history of the Solomon Islands, this is critical.

More advanced is Metallica Minerals and its Urquhart bauxite project over the road (or more accurately over the river), from Weipa in north Queensland.

Regarding the macro outlook, Metallica’s CEO Simon Slesarewich pointed to China’s largest alumina refineries being designed to accept low temp bauxite – versus China predominantly producing high temperature bauxite.

“Bauxite has decoupled from the alumina and aluminium pricing as new refining and smelting capacity is not integrated with dedicated mining operations,” Slesarewich said.

“Low temperature bauxite market undersupplied in the short, medium and long term.”

Slesarewich sees Urquhart as a dead simple mining opportunity that should come into production in the first half of 2017, with modest capital needed given the ideal logistics.

A mining lease has been applied for and the Commonwealth government has confirmed no requirement for a full scale environmental impact statement because of its modest scale.

An earlier mooted development in the neck of the woods by Metro Mining (called Bauxite Hills) is understood to have stalled when authorities informed Metro such a full-scale environmental process was required given the size of the resource and hence timeframe of possible operations.

Metro is now working on its EIS for Bauxite Hills and is aiming to be in production in the second half of 2018.

While that is some way off, Metro’s Bauxite Hills’ numbers probably illustrate why other companies have entered the space.

That because after spending about $40 million in capex, Bauxite Hills could generate earnings of about $133 million per annum for 13 years.

Metro was capitalised this week at over $A60 million, while Metallica was at about $A8 million and early stage Iron Mountain was valued at about $5.4 million – though the latter’s stock price is up 400% since the start of April!

Das gute vielleicht, es gibt nur 6 Australische Bauxite Juniors. Und da ABX, QBL und BAU aus verschiedenen Gründen rausfallen bleiben eigentlich nur MLM, MMI (und Gulf die man aber nicht kaufen kann.)

-------------------------------------------------------------

MLM is in the news of Mining News:

Bauxite plays for juniors

BAUXITE is looking like an interesting little niche play in the ASX resource sector with a number of juniors moving into position to hopefully prosper.

• Michael Quinn

• 31 Aug 2016

• 8:26

• Feature

Two such juniors, Metallica Minerals and Iron Mountain Mining were out on the promotion hustings last week when they presented at the Mining 2016 Resources Convention in Brisbane.

Iron Mountain has re-emerged out of iron ore-induced hibernation and headed to the Solomon Islands where it’s completing due diligence on the scrip-based acquisition of the Nendo bauxite project.

Non-exec director Brett Smith told the Mining 2016 Resources Convention in Brisbane that the prospects for bauxite were looking promising, with alumina refineries reportedly becoming concerned about bauxite supplies and major producer Rio said to have referred to it as ‘the new iron ore’.

Coincidentally Nendo was found by Rio forerunner CRA back in 1969.

While it is early days for Iron Mountain, the signs seem positive from what Smith says.

The bauxite found at Nendo was indicated to be of very good quality (including low silica) with testwork continuing.

The locals are also said to be very much behind a mining development, and given some of the history of the Solomon Islands, this is critical.

More advanced is Metallica Minerals and its Urquhart bauxite project over the road (or more accurately over the river), from Weipa in north Queensland.

Regarding the macro outlook, Metallica’s CEO Simon Slesarewich pointed to China’s largest alumina refineries being designed to accept low temp bauxite – versus China predominantly producing high temperature bauxite.

“Bauxite has decoupled from the alumina and aluminium pricing as new refining and smelting capacity is not integrated with dedicated mining operations,” Slesarewich said.

“Low temperature bauxite market undersupplied in the short, medium and long term.”

Slesarewich sees Urquhart as a dead simple mining opportunity that should come into production in the first half of 2017, with modest capital needed given the ideal logistics.

A mining lease has been applied for and the Commonwealth government has confirmed no requirement for a full scale environmental impact statement because of its modest scale.

An earlier mooted development in the neck of the woods by Metro Mining (called Bauxite Hills) is understood to have stalled when authorities informed Metro such a full-scale environmental process was required given the size of the resource and hence timeframe of possible operations.

Metro is now working on its EIS for Bauxite Hills and is aiming to be in production in the second half of 2018.

While that is some way off, Metro’s Bauxite Hills’ numbers probably illustrate why other companies have entered the space.

That because after spending about $40 million in capex, Bauxite Hills could generate earnings of about $133 million per annum for 13 years.

Metro was capitalised this week at over $A60 million, while Metallica was at about $A8 million and early stage Iron Mountain was valued at about $5.4 million – though the latter’s stock price is up 400% since the start of April!

Orderbuch:

Naja, der Eisberg (ca. 5 mio Shares) war dann doch schneller weg als gedacht.

An ASK und CHI-X Börsen zusammen heute 7,7 Mio

Aktien gehandelt worden.

Aktien gehandelt worden.Orderbuch jetzt sauber.

Charttechnisch sollte / könnte es jetzt schnell zum Ausbruch kommen. (Siehe Chart unten)

Jahreschart:

Ausbruch gescheitert. Aktuell 3,4 audcent

Fehlen die Anschlusskäufer.

Warten wir mal auf die PFS im Oktober.

Fehlen die Anschlusskäufer.

Warten wir mal auf die PFS im Oktober.

Malaysia extends bauxite mining ban until year-end

By Reuters

Published: 05:40 GMT, 7 September 2016 | Updated: 05:40 GMT, 7 September 2016

KUALA LUMPUR, Sept 7 (Reuters) - Malaysia extended a moratorium on bauxite mining activities by more than three months to Dec. 31, the environment minister said at a press conference on Wednesday.

The previous moratorium was set to expire on Sept. 14.

Malaysia's largely unregulated bauxite mining industry has boomed in the past two years to meet demand from China, filling in a supply gap after Indonesia banned exports, but the frenetic pace of digging has led to a public outcry with many complaining of water contamination and destruction of the environment.

Late last year, bauxite mining was blamed for turning the waters and seas red near Kuantan, the capital of Malaysia's third-largest state and key bauxite producer Pahang, following which, in January, the government imposed its first three-month ban on mining the commodity. (Reporting by Liz Lee, Writing by Emily Chow; Editing by Himani Sarkar)

Read more: http://www.dailymail.co.uk/wires/reuters/article-3777251/Mal…

By Reuters

Published: 05:40 GMT, 7 September 2016 | Updated: 05:40 GMT, 7 September 2016

KUALA LUMPUR, Sept 7 (Reuters) - Malaysia extended a moratorium on bauxite mining activities by more than three months to Dec. 31, the environment minister said at a press conference on Wednesday.

The previous moratorium was set to expire on Sept. 14.

Malaysia's largely unregulated bauxite mining industry has boomed in the past two years to meet demand from China, filling in a supply gap after Indonesia banned exports, but the frenetic pace of digging has led to a public outcry with many complaining of water contamination and destruction of the environment.

Late last year, bauxite mining was blamed for turning the waters and seas red near Kuantan, the capital of Malaysia's third-largest state and key bauxite producer Pahang, following which, in January, the government imposed its first three-month ban on mining the commodity. (Reporting by Liz Lee, Writing by Emily Chow; Editing by Himani Sarkar)

Read more: http://www.dailymail.co.uk/wires/reuters/article-3777251/Mal…

http://www.metallicaminerals.com.au/

Homepage im neuen Design.

------

Hier noch mal das letzte Video

Homepage im neuen Design.

------

Hier noch mal das letzte Video

http://www.stocknessmonster.com/news-item?S=MLM&E=ASX&N=9760…

Man scheint bei der Logistiklösung weiter zu kommen.

Ziel weiter bestätigt. Produktion 1 Halbjahr 2017 (also bis 30.6.2017). Halte ich weiterhin als zu optimistisch. Lasse mich gerne überraschen, aber Produktionsstart noch Ende 2017 wäre schon sehr gut. Ich hoffe wir sehen demnächst (Ende Oktober ?) erstmal gute PFS Zahlen.

-----------------------------------

ASX RELEASE

4 OCTO BER 2016

COMPANY UPDATE AND LOAN TO GREEN COAST RESOURCES

Highlights

Short Term Loan to Green Coast Resources to facilitate its maiden bauxite exports from its Hey Point Bauxite Project

Approved and operational logistics solution locked in for Urquhart Bauxite

Environmental Authority for Urquhart Bauxite Project lodged with the Queensland government

Urquhart detailed drill program completed on time and on budget

JORC Resource and Pre-Feasibility Study underway

-----------------------------------

Metallica CEO, Mr Simon Slesarewich:

“Metallica is delighted to be able to assist GCR in the realization of exports from the Hey Point Bauxite Project - the first new independent bauxite mine on Cape York since 1963.

The agreement with GCR and the commencement of bauxite shipments from Hey Point is another positive step for the planned commencement of bauxite exports from the neighboring Urquhart Bauxite Project in the first half of 2017, with minimal capital expenditure.

Metallica remains confidentthat the project will deliver significant shareholder value and is looking forward to sharing the results of a Pre-Feasibility Study as soon as they are available.”

Man scheint bei der Logistiklösung weiter zu kommen.

Ziel weiter bestätigt. Produktion 1 Halbjahr 2017 (also bis 30.6.2017). Halte ich weiterhin als zu optimistisch. Lasse mich gerne überraschen, aber Produktionsstart noch Ende 2017 wäre schon sehr gut. Ich hoffe wir sehen demnächst (Ende Oktober ?) erstmal gute PFS Zahlen.

-----------------------------------

ASX RELEASE

4 OCTO BER 2016

COMPANY UPDATE AND LOAN TO GREEN COAST RESOURCES

Highlights

Short Term Loan to Green Coast Resources to facilitate its maiden bauxite exports from its Hey Point Bauxite Project

Approved and operational logistics solution locked in for Urquhart Bauxite

Environmental Authority for Urquhart Bauxite Project lodged with the Queensland government

Urquhart detailed drill program completed on time and on budget

JORC Resource and Pre-Feasibility Study underway

-----------------------------------

Metallica CEO, Mr Simon Slesarewich:

“Metallica is delighted to be able to assist GCR in the realization of exports from the Hey Point Bauxite Project - the first new independent bauxite mine on Cape York since 1963.

The agreement with GCR and the commencement of bauxite shipments from Hey Point is another positive step for the planned commencement of bauxite exports from the neighboring Urquhart Bauxite Project in the first half of 2017

, with minimal capital expenditure. Metallica remains confidentthat the project will deliver significant shareholder value and is looking forward to sharing the results of a Pre-Feasibility Study as soon as they are available.”

Ich will mich mall wieder etwas aus dem Fenster lehnen.

Was erwarte ich von der PFS?

NPV sollte so ca. bei 80 Mio AUD liegen. Davon 50% Anteil wären 40 Mio für Metallica. Hört sich erstmal nicht viel an, muss man aber im Verhältnis zu dem sehr niedrigen Börsenwert von kanpp 9 Mio setzen. Dann passt das aber schon wieder.

Was ich aber auch erwarte ist, dass wir hier einen sehr hohen IRR erwarten können. Ich rede hier von vielleicht sogar über 200%.

Warten wir mal noch ein paar Woche ab.

Was erwarte ich von der PFS?

NPV sollte so ca. bei 80 Mio AUD liegen. Davon 50% Anteil wären 40 Mio für Metallica. Hört sich erstmal nicht viel an, muss man aber im Verhältnis zu dem sehr niedrigen Börsenwert von kanpp 9 Mio setzen. Dann passt das aber schon wieder.

Was ich aber auch erwarte ist, dass wir hier einen sehr hohen IRR erwarten können. Ich rede hier von vielleicht sogar über 200%.

Warten wir mal noch ein paar Woche ab.

schöne kerze und mit tageshoch geschlossen

gutes händchen du hast!!!

gutes händchen du hast!!!

Ja der Zug scheint langsam den Bahnhof zu verlassen. Bitte jetzt zügig alle einsteigen.

Der charttechnische Ausbruch könnte jetzt im zweiten Anlauf wirklich mal klappen. Die größeren Verkäufer scheinen jetzt endlich "fertig zu haben".

-----------------------------------------------------

Oderbuch recht leer, zur Zeit 650k bis 5 audcent. Wenn man bedenkt das heute über 2 Mio Stücke gehandelt wurden nicht viel.

Der charttechnische Ausbruch könnte jetzt im zweiten Anlauf wirklich mal klappen. Die größeren Verkäufer scheinen jetzt endlich "fertig zu haben".

-----------------------------------------------------

Oderbuch recht leer, zur Zeit 650k bis 5 audcent. Wenn man bedenkt das heute über 2 Mio Stücke gehandelt wurden nicht viel.

Ausbruch 2. Versuch erstmal gescheitert.

Sind noch zuviele Verkäufer da, die auch keine Gewinne realisieren.

Denke für eine Move auf 5 cent brauchen wir jetzt eine gute PFS

Sind noch zuviele Verkäufer da, die auch keine Gewinne realisieren.

Denke für eine Move auf 5 cent brauchen wir jetzt eine gute PFS

"Kleine" Gewinne

Logistics provider ships maiden bauxite cargo

http://www.stocknessmonster.com/news-item?S=MLM&E=ASX&N=9798…

Die Verlandelogistik scheint jetzt "eingetütet" zu sein.

http://www.stocknessmonster.com/news-item?S=MLM&E=ASX&N=9798…

Die Verlandelogistik scheint jetzt "eingetütet" zu sein.

Genehmigung in Q1/ 2017 sollte jetzt nur noch Formsache sein.

Was ich immer noch bemerkenswert finde ist, dass man immer noch davon ausgeht bereits in Q2/ 2017 zu produzieren, wir reden hier von in 6-8 Monaten

Ich hätte nix dagegen, aber wo soll die Finanzierung der CAPEX herkommen und an wen soll das Bauxite verkauft werden? Hier fehlen komplett noch die Infos.

Die Wirtschaftlichkeitsrechnung PFS sollte bald kommen, dann sehen wir über welche Zahlen wir hier überhaupt reden.

A successful shipment of bauxite using a barge loading facility at Weipa in Cape York Peninsula has been a cause of excitement in the far northern mining town.

Green Coast Resources (GCR) is the first company not aligned with Rio Tinto or Comalco to export bauxite from Cape York Peninsula for more than 50 years.

Media player: "Space" to play, "M" to mute, "left" and "right" to seek.

Audio: Metallica Minerals chief executive Simon Slesarewich says it is an exciting time for new bauxite miners in Cape York (ABC Rural)

GCR purchased a tenement several years ago from Cape Alumina Limited, and gained approval to extract and export bauxite from the new mine.

But its maiden shipment also was seen as a major step forward for developmental company Metallica Minerals, which provided working capital to assist with the first shipment.

According to its statement to the Australian Stock Exchange, Metallica Minerals provided a short-term loan to GCR and in return, will receive transhipping services when production from its nearby Urquhart project starts next year.

Metallica Minerals chief executive Simon Slesarewich said the new mine had the potential to export 1.6 million tonnes of bauxite annually.

He said the successful transhipping operation, from a self-propelled barge into ocean-going export vessels, had vindicated the company's decision to use the existing Hey Point barge loading facility as a low capital cost logistics option.

"I have no doubt that all the locals up there in their tinnies and their boats would have gone to have a look at the transhipping because it's something they haven't seen before," Mr Slesarewich said.

"But I think very soon it'll just become very run-of-the-mill, and those guys are over there mining bauxite and shipping it, just like Rio do.

"Obviously we won't be anywhere near the same volumes, but it offers new opportunities for smaller contractors and suppliers and just another boost for the local economy."

Bauxite has been mined at Weipa on western Cape York Peninsula in Queensland since 1963 by Rio Tinto (and formerly Comalco).

The mine produces 26 million tonnes of bauxite annually.

Mr Slesarewich said two new, small bauxite operations in Weipa would complement, not compete with, the mining giant.

"We're running our own race and looking to build a sustainable bauxite mine and business off the back of that," he said.

Green Coast Resources (GCR) is the first company not aligned with Rio Tinto or Comalco to export bauxite from Cape York Peninsula for more than 50 years.

Media player: "Space" to play, "M" to mute, "left" and "right" to seek.

Audio: Metallica Minerals chief executive Simon Slesarewich says it is an exciting time for new bauxite miners in Cape York (ABC Rural)

GCR purchased a tenement several years ago from Cape Alumina Limited, and gained approval to extract and export bauxite from the new mine.

But its maiden shipment also was seen as a major step forward for developmental company Metallica Minerals, which provided working capital to assist with the first shipment.

According to its statement to the Australian Stock Exchange, Metallica Minerals provided a short-term loan to GCR and in return, will receive transhipping services when production from its nearby Urquhart project starts next year.

Metallica Minerals chief executive Simon Slesarewich said the new mine had the potential to export 1.6 million tonnes of bauxite annually.

He said the successful transhipping operation, from a self-propelled barge into ocean-going export vessels, had vindicated the company's decision to use the existing Hey Point barge loading facility as a low capital cost logistics option.

"I have no doubt that all the locals up there in their tinnies and their boats would have gone to have a look at the transhipping because it's something they haven't seen before," Mr Slesarewich said.

"But I think very soon it'll just become very run-of-the-mill, and those guys are over there mining bauxite and shipping it, just like Rio do.

"Obviously we won't be anywhere near the same volumes, but it offers new opportunities for smaller contractors and suppliers and just another boost for the local economy."

Bauxite has been mined at Weipa on western Cape York Peninsula in Queensland since 1963 by Rio Tinto (and formerly Comalco).

The mine produces 26 million tonnes of bauxite annually.

Mr Slesarewich said two new, small bauxite operations in Weipa would complement, not compete with, the mining giant.

"We're running our own race and looking to build a sustainable bauxite mine and business off the back of that," he said.

http://www.abc.net.au/news/2016-10-25/metallica-minerals-sim…

Netter 4:41 Minuten Broadcast mit dem CEO

Netter 4:41 Minuten Broadcast mit dem CEO

Wenn nur ein Fünkchen Wahrheit an dem Statment ist, könnte das kurzfristig eine richtige Kursrakete werden.

Marktkapitialisierung 9,3 Mio AUD

---------------------------------------------------------------------

Von Heute:

Dear Metallica shareholders,

The 12 months under review has been a period primarily

focused on ensuring your Company is better positioned to

now make a sustainable transition from minerals explorer

and developer to a successful and profitable bauxite miner.

This period of review has also been the first full year under the

leadership of Simon Slesarewich as Chief Executive Officer and

a smaller non–executive Board of three led by Barry Casson

as Non–Executive Chairman. This has placed additional

emphasis on streamlined management and experience in

development, preparing for operations going forward.

That prospect – of first production from our Urquhart

Bauxite project in far north Queensland – is becoming

a reality. Your Board and Management team remain

confident that we will see first exports of bauxite and

positive cash flow in the first half of calendar year 2017.

The preparedness for this step–change was underpinned

by the prioritised delivery over 2015–2016 of

successful outcomes against four key objectives:

•

Firstly, a realistic assessment and review of our then held

assets and business strategies against the most likely

outcomes for them, if any, over the immediate period ahead

•

Secondly, recognition that on current assets and market

outlook, Metallica had to be preferentially positioned as an

emerging bauxite producer, not a mixed commodity player

•

Thirdly, the immediate continuation and associated

expenditure of evolving (initially) as a heavy mineral sands

miner, was not justifiable on current market conditions, and

•

Fourthly, Metallica had to enhance its cash strength

via a combination of timely sales of non–core assets,

minimising shareholder dilution, and appropriate

levels of capital raisings that were clearly understood

and appreciated by the broader equities market.

As a result, the majority of the Company’s limestone assets

in Queensland were sold during the period, for total net

proceeds of just under $2 Million. The Joint Venture with

Australian Mines over the SCONI project delivers on the

Company’s promise to create value from non–core assets,

as well as preserving Metallica’s significant past investment,

whilst maintaining an exposure to the continued upside

from the development of SCONI. Further non–equity

funding for the Company was recently successful in terms

of a Research and Development refund of $316,000.

Our core assets remain Metallica’s significant portfolio

of bauxite and zircon–rutile heavy mineral sands (HMS)

resources and exploration interests on Cape York

Peninsula, and the unique Esmeralda graphite exploration

project near Croydon, also in north Queensland. These

projects will underpin our forward business activity in

the near–term and be supplemented as appropriate with

opportunities that are expected to arise going forward.

A more detailed explanation of your Company’s aspirations

around its current projects is contained elswhere in this report.

The transition to a successful bauxite producer

The decision to prioritise Metallica as an emerging bauxite

producer is that we control substantial bauxite resources

of sufficient grade and quality to underpin our growing

Company. Bauxite as a commodity also includes pricing

upside, and our bauxite resources are located adjacent

to an ideal deep water export gateway on Cape York,

with direct sea routes to key Asian markets at favourable

shipping rates, relative to many other exporting nations.

In addition, the global bauxite sector is widely tipped

to entertain a supply shortfall in the coming 12 months.

This window of opportunity continues to deepen due to

mining and export restrictions imposed during the year

by some of our regional overseas bauxite competitors.

Indeed, the global shortfall of low temperature bauxite (the

type we will expect to produce at Urquhart) is tipped to rise

to 68 million tonnes per annum (Mtpa) by just 2040.

As such, the decisions of your Board and Management

in the past year have been to maximise this window

and ready Metallica to grow production towards a

target of 5–7 Mtpaof bauxite over the coming 3 to 5

years. This production journey is now very close.

No other recently owned or currently owned

Metallica assets offer such immediate maiden

mining and maiden revenue pathways.

Within this push to first mining, your Board acknowledges the

valuable and ongoing partnership with our Cape York Bauxite

and HMS Project Joint Venture partner, Ozore Resources

Pty Ltd. We publicly congratulate Ozore on successfully

moving to a 50% interest in the JV during the year.

Particularly pleasing within our bauxite pursuit was the

decision during the review period by the Commonwealth

Department of the Environment to determine that the

Urquhart Bauxite Project is a “Controlled Action”.

Put simply, this means the regulatory approval process for

our proposed bauxite mine will be less onerous, meaning

an Environmental Impact Statement (EIS) will not be

required, and issues can be addressed in our preliminary

documentation covering management plans and how

we plan to mitigate the potential impacts of the mine.

This “determination” is a key positive for the project and

is a direct result of the significant work and consultation

undertaken by the Joint Venture team and its consultants

to deliver sustainability for our new mine.

We further added to our progress with the signing of the Heads

of Agreement to utilise the nearby and recently completed

Hey Point bulk storage, loading and barging infrastructure

(just 15 km from our mine site and owned by another bauxite

miner). This transhipping solution eliminates the need

to build our own costly infrastructure to move Urquhart

bauxite onto waiting bulk vessels, moored only 3.5 km from

the already installed barge loading facility at Hey Point.

This was a major achievement in substantially de–risking

our pursuit to sustainable cash flow. It means Metallica is

assured of much lower start–up costs for our own mine

and we are able to compress the start–up schedule.

Hey Point was the most viable solution from three logistics

and transhipping options considered for Urquhart bauxite and

presents your company with a low risk start–up operation.

With a mining lease application lodged, we will continue to

work closely with the Queensland Government and other

stakeholders, including Traditional Land Owners, to secure

all approvals allowing a mining start in the first half of 2017.

As a consequence of our focus on delivering Urquhart

bauxite, the purpose built processing plant for our co–

located and planned Heavy Mineral Sands mining project

at Urquhart Point, just south of Weipa, has been put on

hold for the time being, pending improvement in the

mineral sands commodity prices. Your Company continues

to monitor the mineral sands market and is encouraged

by recent price increases for those commodities contained

at Urquhart Point that may deliver value in the future.

Promising graphite play

Progress on our wholly–owned Esmeralda graphite project

(graphite–in–granite, a unique style of mineralisation

because of its rarity and general high purity in either

flake or crystalline form) was encouraging.

The positive drill and metallurgical outcomes from our late in

2015 drill campaign included intersections of significant broad

graphite mineralisation. The forward program for this project

includes further exploration planned in 2016 and potentially

a follow up drill program in 2017. However our priority will

continue to be sustainable cash flow from Urquhart bauxite.

Robust capital outcomes

Your Company’s capital raising initiatives included a

renounceable rights issue that was closed early, with just under

$1.8 Million raised. We sincerely thank Metallica shareholders

for your loyalty and support for this raising as the proceeds are

sufficient to materially advance the Urquhart bauxite project.

These capital initiatives saw the Company close out the

2015–2016 full year with a robust $2.3 Million cash at bank.

Importantly, Metallica remains a company with a tight capital

structure and no debt after 12 years as an ASX listed entity.

One negative for Metallica during the year, as confronts most

of the junior resources space, is the lack–lustre share price

performance. After a flat two to three year period, equities market

sentiment towards junior explorers and developers only recently

commenced showing signs of genuine renewed buoyancy.

Your Board believes achieving the transition next year to bauxite

miner, will attract a positive re–rating of the Company.

In closing, the current 2016–2017 financial year should prove

the most important in Metallica’s history and elevate the

Company from developer to the milestone of producer. While

there is still work to be done, your Board and Management

team are confident that the correct stepping stones

for realisable growth are in place – and we invite you to

continue to share this exciting time ahead for Metallica.

SIMON SLESAREWICH

Chief Executive Officer

BARRY CASSON

Non–Executive Chairman

Marktkapitialisierung 9,3 Mio AUD

---------------------------------------------------------------------

Von Heute:

Dear Metallica shareholders,

The 12 months under review has been a period primarily

focused on ensuring your Company is better positioned to

now make a sustainable transition from minerals explorer

and developer to a successful and profitable bauxite miner.

This period of review has also been the first full year under the

leadership of Simon Slesarewich as Chief Executive Officer and

a smaller non–executive Board of three led by Barry Casson

as Non–Executive Chairman. This has placed additional

emphasis on streamlined management and experience in

development, preparing for operations going forward.

That prospect – of first production from our Urquhart

Bauxite project in far north Queensland – is becoming

a reality. Your Board and Management team remain

confident that we will see first exports of bauxite and

positive cash flow in the first half of calendar year 2017.

The preparedness for this step–change was underpinned

by the prioritised delivery over 2015–2016 of

successful outcomes against four key objectives:

•

Firstly, a realistic assessment and review of our then held

assets and business strategies against the most likely

outcomes for them, if any, over the immediate period ahead

•

Secondly, recognition that on current assets and market

outlook, Metallica had to be preferentially positioned as an

emerging bauxite producer, not a mixed commodity player

•

Thirdly, the immediate continuation and associated

expenditure of evolving (initially) as a heavy mineral sands

miner, was not justifiable on current market conditions, and

•

Fourthly, Metallica had to enhance its cash strength

via a combination of timely sales of non–core assets,

minimising shareholder dilution, and appropriate

levels of capital raisings that were clearly understood

and appreciated by the broader equities market.

As a result, the majority of the Company’s limestone assets

in Queensland were sold during the period, for total net

proceeds of just under $2 Million. The Joint Venture with

Australian Mines over the SCONI project delivers on the

Company’s promise to create value from non–core assets,

as well as preserving Metallica’s significant past investment,

whilst maintaining an exposure to the continued upside

from the development of SCONI. Further non–equity

funding for the Company was recently successful in terms

of a Research and Development refund of $316,000.

Our core assets remain Metallica’s significant portfolio

of bauxite and zircon–rutile heavy mineral sands (HMS)

resources and exploration interests on Cape York

Peninsula, and the unique Esmeralda graphite exploration

project near Croydon, also in north Queensland. These

projects will underpin our forward business activity in

the near–term and be supplemented as appropriate with

opportunities that are expected to arise going forward.

A more detailed explanation of your Company’s aspirations

around its current projects is contained elswhere in this report.

The transition to a successful bauxite producer

The decision to prioritise Metallica as an emerging bauxite

producer is that we control substantial bauxite resources

of sufficient grade and quality to underpin our growing

Company. Bauxite as a commodity also includes pricing

upside, and our bauxite resources are located adjacent

to an ideal deep water export gateway on Cape York,

with direct sea routes to key Asian markets at favourable

shipping rates, relative to many other exporting nations.

In addition, the global bauxite sector is widely tipped

to entertain a supply shortfall in the coming 12 months.

This window of opportunity continues to deepen due to

mining and export restrictions imposed during the year

by some of our regional overseas bauxite competitors.

Indeed, the global shortfall of low temperature bauxite (the

type we will expect to produce at Urquhart) is tipped to rise

to 68 million tonnes per annum (Mtpa) by just 2040.

As such, the decisions of your Board and Management

in the past year have been to maximise this window

and ready Metallica to grow production towards a

target of 5–7 Mtpa

of bauxite over the coming 3 to 5 years. This production journey is now very close.

No other recently owned or currently owned

Metallica assets offer such immediate maiden

mining and maiden revenue pathways.

Within this push to first mining, your Board acknowledges the

valuable and ongoing partnership with our Cape York Bauxite

and HMS Project Joint Venture partner, Ozore Resources

Pty Ltd. We publicly congratulate Ozore on successfully

moving to a 50% interest in the JV during the year.

Particularly pleasing within our bauxite pursuit was the

decision during the review period by the Commonwealth

Department of the Environment to determine that the

Urquhart Bauxite Project is a “Controlled Action”.

Put simply, this means the regulatory approval process for

our proposed bauxite mine will be less onerous, meaning

an Environmental Impact Statement (EIS) will not be

required, and issues can be addressed in our preliminary

documentation covering management plans and how

we plan to mitigate the potential impacts of the mine.

This “determination” is a key positive for the project and

is a direct result of the significant work and consultation

undertaken by the Joint Venture team and its consultants

to deliver sustainability for our new mine.

We further added to our progress with the signing of the Heads

of Agreement to utilise the nearby and recently completed

Hey Point bulk storage, loading and barging infrastructure

(just 15 km from our mine site and owned by another bauxite

miner). This transhipping solution eliminates the need

to build our own costly infrastructure to move Urquhart

bauxite onto waiting bulk vessels, moored only 3.5 km from

the already installed barge loading facility at Hey Point.

This was a major achievement in substantially de–risking

our pursuit to sustainable cash flow. It means Metallica is

assured of much lower start–up costs for our own mine

and we are able to compress the start–up schedule.

Hey Point was the most viable solution from three logistics

and transhipping options considered for Urquhart bauxite and

presents your company with a low risk start–up operation.

With a mining lease application lodged, we will continue to

work closely with the Queensland Government and other

stakeholders, including Traditional Land Owners, to secure

all approvals allowing a mining start in the first half of 2017.

As a consequence of our focus on delivering Urquhart

bauxite, the purpose built processing plant for our co–

located and planned Heavy Mineral Sands mining project

at Urquhart Point, just south of Weipa, has been put on

hold for the time being, pending improvement in the

mineral sands commodity prices. Your Company continues

to monitor the mineral sands market and is encouraged

by recent price increases for those commodities contained

at Urquhart Point that may deliver value in the future.

Promising graphite play

Progress on our wholly–owned Esmeralda graphite project

(graphite–in–granite, a unique style of mineralisation

because of its rarity and general high purity in either

flake or crystalline form) was encouraging.

The positive drill and metallurgical outcomes from our late in

2015 drill campaign included intersections of significant broad

graphite mineralisation. The forward program for this project

includes further exploration planned in 2016 and potentially

a follow up drill program in 2017. However our priority will

continue to be sustainable cash flow from Urquhart bauxite.

Robust capital outcomes

Your Company’s capital raising initiatives included a

renounceable rights issue that was closed early, with just under

$1.8 Million raised. We sincerely thank Metallica shareholders

for your loyalty and support for this raising as the proceeds are

sufficient to materially advance the Urquhart bauxite project.

These capital initiatives saw the Company close out the

2015–2016 full year with a robust $2.3 Million cash at bank.

Importantly, Metallica remains a company with a tight capital

structure and no debt after 12 years as an ASX listed entity.

One negative for Metallica during the year, as confronts most

of the junior resources space, is the lack–lustre share price

performance. After a flat two to three year period, equities market

sentiment towards junior explorers and developers only recently

commenced showing signs of genuine renewed buoyancy.

Your Board believes achieving the transition next year to bauxite

miner, will attract a positive re–rating of the Company.