Arena....ein schlafender Riese? USD 24.42 am 14.7.2017 - 500 Beiträge pro Seite

eröffnet am 14.07.17 21:27:23 von

neuester Beitrag 13.12.21 16:01:01 von

neuester Beitrag 13.12.21 16:01:01 von

Beiträge: 131

ID: 1.257.250

ID: 1.257.250

Aufrufe heute: 3

Gesamt: 14.489

Gesamt: 14.489

Aktive User: 0

ISIN: US0400476075 · WKN: A2DR4A

91,00

EUR

+0,55 %

+0,50 EUR

Letzter Kurs 10.03.22 Tradegate

Werte aus der Branche Pharmaindustrie

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 3,5800 | +922,86 | |

| 1,0400 | +48,57 | |

| 50,80 | +40,72 | |

| 12,810 | +39,69 | |

| 0,5400 | +38,46 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7500 | -21,05 | |

| 3,2500 | -22,06 | |

| 0,6610 | -24,02 | |

| 28,18 | -32,62 | |

| 0,5660 | -40,42 |

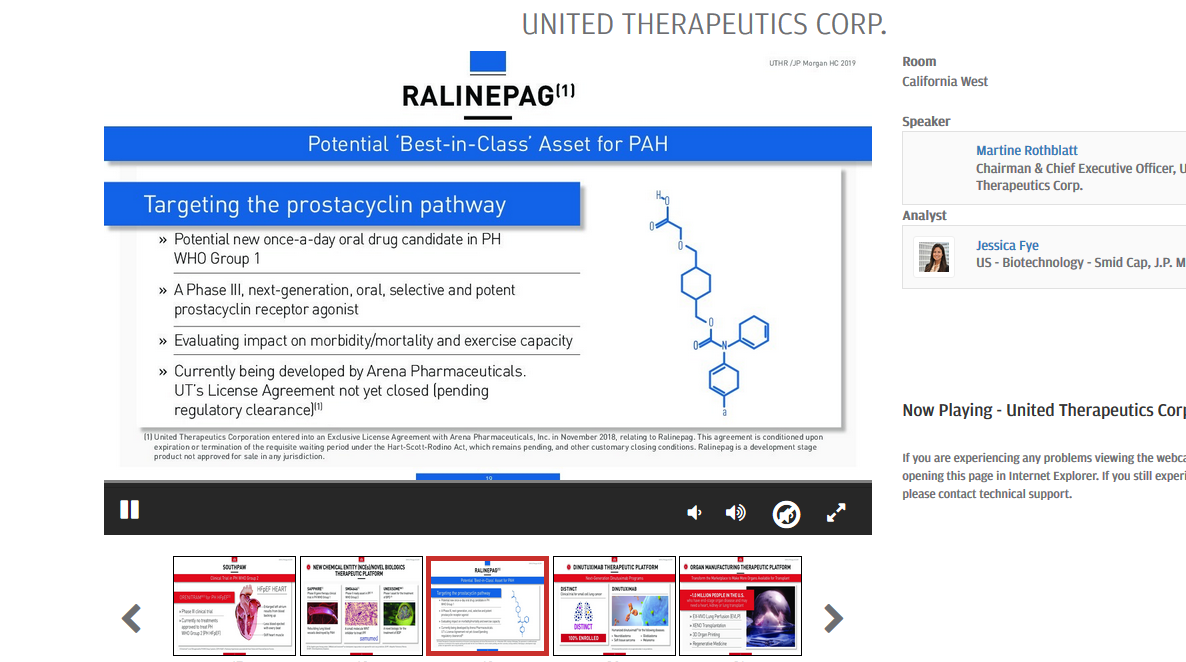

Das Potenzial ist riesig:

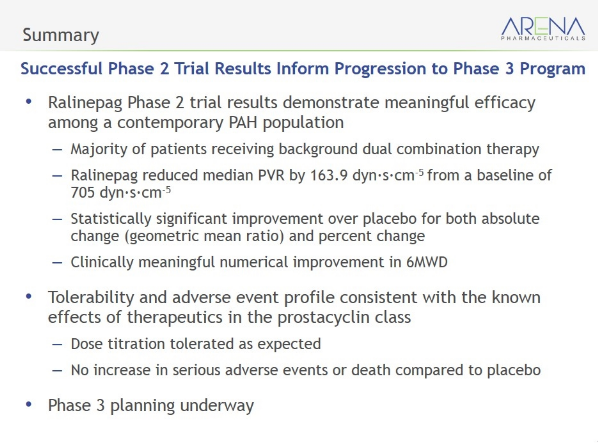

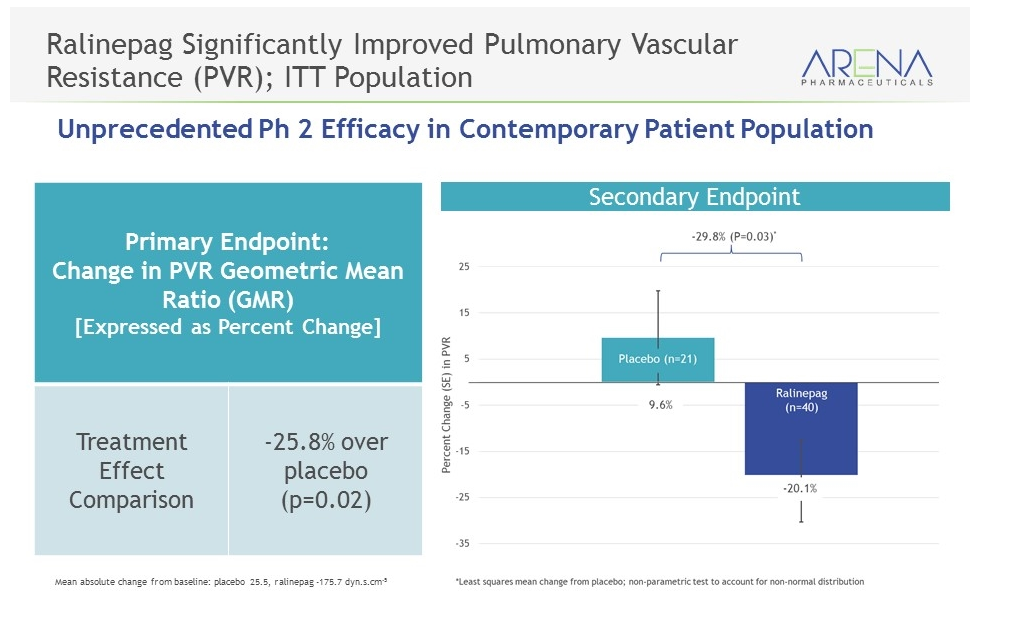

mit der erfolgreichen ph2-Studie bei Ralinepag bei "pulmonary arterial hypertension" (PAH) mit statistisch signifikant erreichtem primären Endpunkt wurde ein erstes dickes Ausrufezeichen gesetzt:

"In this 61-patient study, the primary efficacy analysis demonstrated a statistically significant absolute change from baseline in pulmonary vascular resistance (PVR) compared to placebo."

Seit Bekanntgabe der ph2-Ergebnisse am 10. Juli 2017 habe ich mehrfach gekauft - Tendenz steigend.

http://invest.arenapharm.com/releasedetail.cfm?ReleaseID=103…

mit der erfolgreichen ph2-Studie bei Ralinepag bei "pulmonary arterial hypertension" (PAH) mit statistisch signifikant erreichtem primären Endpunkt wurde ein erstes dickes Ausrufezeichen gesetzt:

"In this 61-patient study, the primary efficacy analysis demonstrated a statistically significant absolute change from baseline in pulmonary vascular resistance (PVR) compared to placebo."

Seit Bekanntgabe der ph2-Ergebnisse am 10. Juli 2017 habe ich mehrfach gekauft - Tendenz steigend.

http://invest.arenapharm.com/releasedetail.cfm?ReleaseID=103…

Antwort auf Beitrag Nr.: 55.328.206 von Cyberhexe am 14.07.17 21:27:23ARENA Pharmaceutical hat unglaubliches Potenzial, weil folgende Entwicklungsmöglichkeiten gegeben sind:

1.) Ralinepag

2.) Etrasimod

3.) APD371

4.) Nelotanserin

sowie das bereits 2012 für Fettleibigkeit zugelassene

5.) Lorcaserin (brand name: BELVIQ) - ja, auch bei diesem Wirkstoff gibt es erstaunliches Entwicklungspotenzial!

Doch der Reihe nach:

zu 1.) Ralinepag

diese Woche wurde zu Ralinepag ein ph2-Studienergebnis veröffentlicht, welches in seiner Eindeutigkeit sicherlich nicht nur mich überrascht hat: ein statistisch erreichter primärer Endpunkt bei der Behandlung von 61 Patienten mit PAH (Pulmonary Arterial Hypertension). Obschon vom Unternehmen aufgrund der präklinischen und pharmakokinetischen Studien schon immer als potenziell "best in class" bezeichnet, konnte diese "Vermutung" für diesen Wirkstoff nun zum ersten Mal mit klinischen Fakten belegt werden, und dies mehr als eindrücklich:

"Ralinepag improved median PVR by 163.9 dyn.s.cm-5 from baseline compared to a 0.7 dyn.s.cm-5 worsening from baseline in the placebo arm (P=0.02). Patients treated with ralinepag had a 29.8% improvement in PVR compared to the placebo arm (P=0.03) and a 20.1% improvement in PVR compared to baseline."

PVR (pulmonary vascular resistance) ist ein Mass, welches das Fortschreiten einer lebensbedrohenden bzw. fatalen Krankheit, nämlich die Pulmonale Hypertonie bzw Pulmonary Arterial Hypertension (PAH), kennzeichnet. Dieser ansteigende Gefässwiderstand in den Lungenarterien führt zu einer stark eingeschränkten Leistungsfähigkeit verbunden mit Kreislaufstörungen und Müdigkeit. Oft führt diese Erkrankung zum Ableben der Betroffenen.

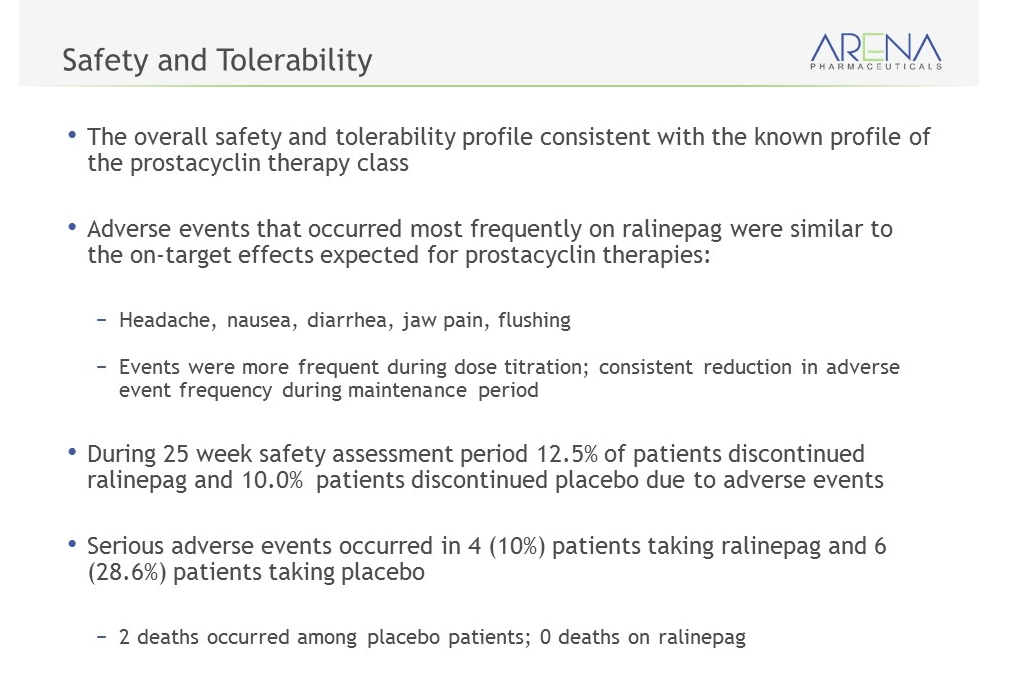

In dieser Phase-2-Studie (n=61) hat Ralinepag nun ein mehr als beachtliches Resultat geliefert, nämlich eine Reduktion des Gefässwiderstand um 30% verglichen mit Placebo, und dies auch noch mit statistischer Signifikanz beim primären Endpunkt. Die Erwartungen im Vorfeld waren weitaus skeptischer, da lediglich eine Senkung um 20 -25% prognostiziert wurde. Allerdings wurde ein sekundärer Endpunkt nicht mit statistischer Signifikanz erreicht, nämlich die Wegstrecke, die ein Patient innerhalb von 6 Minuten zurücklegen kann: Ralinepag-Patienten legten 36m zurück, während Patienten unter Plazebo gerade einmal 30m zurücklegten. Eine statistische signifikante Verbesserung dieser Wegstrecke müsste jedoch bei einer mächtigeren ph3-Studie gelingen.

Folgende Punkte der Studie sind allerdings unausgewogen:

der Umstand, dass Ralinepag-Patienten jünger waren als diejenigen unter Plazebo, könnte zu dessen Vorteil gewesen sein. Hingegen waren die Verum-Patienten in einem schlechteren Zustand als unter Plazebo.

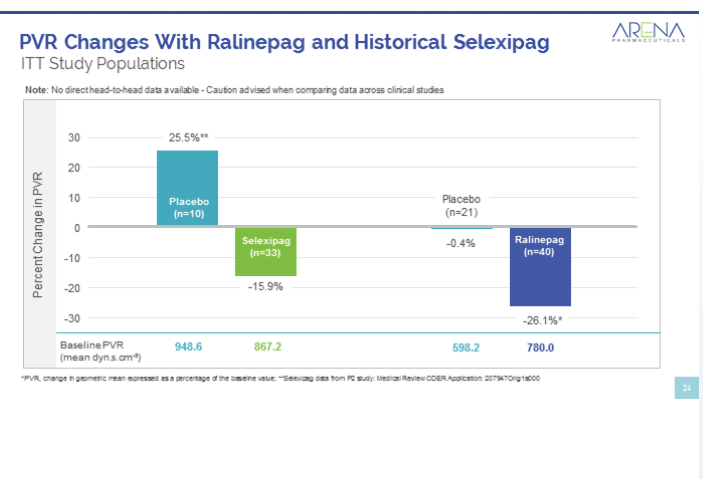

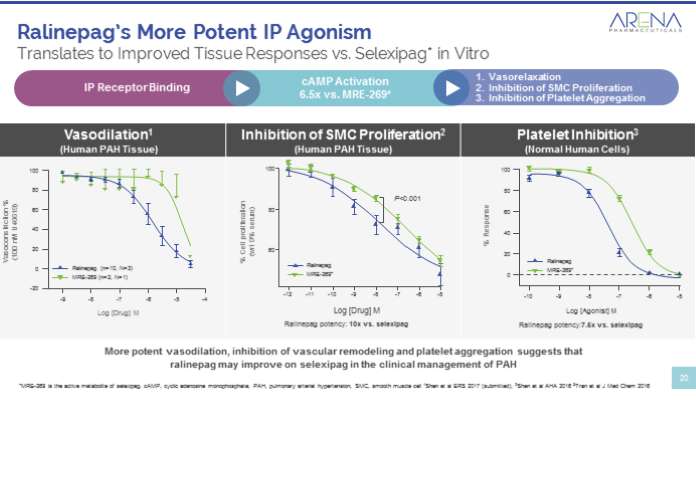

Ralinepag gehört zu einer Klasse von bereits etablierten Wirkstoffen zur Behandlung von PAH (pulmonary arterial hypertension), nämlich den IP Prostacyclin-Rezeptor-Agonisten, die in 2016 insgesamt fast 2 Mrd USD Verkaufserlöse erzielt haben. Einer dieser Wirkstoffe am Markt ist Actelions Uptravi (generic name: Selexipag), mit welchem das CH-Unternehmen in 2016, dem Jahr nach der Zulassung (FDA am 22.12.2015) bereits $240m Umsatz erzielt hat. Das Wachstumspotenzial innerhalb Actelions PAH-Portfolio ist ursächlich dafür verantwortlich, dass JNJ das Unternehmen erst kürzlich für sage und schreibe 30 Milliarden USD übernommen hat.

Ralinepag hat gegenüber Selxipag weitere Vorteile, bspw. die Pharmakokinetik: Ralinepag wird wie Selexipag oral verabreicht, hat jedoch eine viel längere Halbwertszeit als Selxipag, weshalb eine wesentlich feinere Dosierung, ähnlich wie bei intravenöser Applikation, erzielt werden kann.

Fortsetzung folgt!

1.) Ralinepag

2.) Etrasimod

3.) APD371

4.) Nelotanserin

sowie das bereits 2012 für Fettleibigkeit zugelassene

5.) Lorcaserin (brand name: BELVIQ) - ja, auch bei diesem Wirkstoff gibt es erstaunliches Entwicklungspotenzial!

Doch der Reihe nach:

zu 1.) Ralinepag

diese Woche wurde zu Ralinepag ein ph2-Studienergebnis veröffentlicht, welches in seiner Eindeutigkeit sicherlich nicht nur mich überrascht hat: ein statistisch erreichter primärer Endpunkt bei der Behandlung von 61 Patienten mit PAH (Pulmonary Arterial Hypertension). Obschon vom Unternehmen aufgrund der präklinischen und pharmakokinetischen Studien schon immer als potenziell "best in class" bezeichnet, konnte diese "Vermutung" für diesen Wirkstoff nun zum ersten Mal mit klinischen Fakten belegt werden, und dies mehr als eindrücklich:

"Ralinepag improved median PVR by 163.9 dyn.s.cm-5 from baseline compared to a 0.7 dyn.s.cm-5 worsening from baseline in the placebo arm (P=0.02). Patients treated with ralinepag had a 29.8% improvement in PVR compared to the placebo arm (P=0.03) and a 20.1% improvement in PVR compared to baseline."

PVR (pulmonary vascular resistance) ist ein Mass, welches das Fortschreiten einer lebensbedrohenden bzw. fatalen Krankheit, nämlich die Pulmonale Hypertonie bzw Pulmonary Arterial Hypertension (PAH), kennzeichnet. Dieser ansteigende Gefässwiderstand in den Lungenarterien führt zu einer stark eingeschränkten Leistungsfähigkeit verbunden mit Kreislaufstörungen und Müdigkeit. Oft führt diese Erkrankung zum Ableben der Betroffenen.

In dieser Phase-2-Studie (n=61) hat Ralinepag nun ein mehr als beachtliches Resultat geliefert, nämlich eine Reduktion des Gefässwiderstand um 30% verglichen mit Placebo, und dies auch noch mit statistischer Signifikanz beim primären Endpunkt. Die Erwartungen im Vorfeld waren weitaus skeptischer, da lediglich eine Senkung um 20 -25% prognostiziert wurde. Allerdings wurde ein sekundärer Endpunkt nicht mit statistischer Signifikanz erreicht, nämlich die Wegstrecke, die ein Patient innerhalb von 6 Minuten zurücklegen kann: Ralinepag-Patienten legten 36m zurück, während Patienten unter Plazebo gerade einmal 30m zurücklegten. Eine statistische signifikante Verbesserung dieser Wegstrecke müsste jedoch bei einer mächtigeren ph3-Studie gelingen.

Folgende Punkte der Studie sind allerdings unausgewogen:

der Umstand, dass Ralinepag-Patienten jünger waren als diejenigen unter Plazebo, könnte zu dessen Vorteil gewesen sein. Hingegen waren die Verum-Patienten in einem schlechteren Zustand als unter Plazebo.

Ralinepag gehört zu einer Klasse von bereits etablierten Wirkstoffen zur Behandlung von PAH (pulmonary arterial hypertension), nämlich den IP Prostacyclin-Rezeptor-Agonisten, die in 2016 insgesamt fast 2 Mrd USD Verkaufserlöse erzielt haben. Einer dieser Wirkstoffe am Markt ist Actelions Uptravi (generic name: Selexipag), mit welchem das CH-Unternehmen in 2016, dem Jahr nach der Zulassung (FDA am 22.12.2015) bereits $240m Umsatz erzielt hat. Das Wachstumspotenzial innerhalb Actelions PAH-Portfolio ist ursächlich dafür verantwortlich, dass JNJ das Unternehmen erst kürzlich für sage und schreibe 30 Milliarden USD übernommen hat.

Ralinepag hat gegenüber Selxipag weitere Vorteile, bspw. die Pharmakokinetik: Ralinepag wird wie Selexipag oral verabreicht, hat jedoch eine viel längere Halbwertszeit als Selxipag, weshalb eine wesentlich feinere Dosierung, ähnlich wie bei intravenöser Applikation, erzielt werden kann.

Fortsetzung folgt!

Antwort auf Beitrag Nr.: 55.328.206 von Cyberhexe am 14.07.17 21:27:23Schon wieder so ein "toter Hund". Da werden Erinnerungen wach. Ich sage nur "MOLOGEN".

Hab mir einmal die Finger (fast) verbrannt.

Hab mir einmal die Finger (fast) verbrannt.

Antwort auf Beitrag Nr.: 55.330.186 von Inderhals am 15.07.17 11:03:15

...was hat das mit Arena Pharmaceuticals zu tun? Mit Mologen habe ich mich zumindest noch nie beschäftigt! Un weshalb "toter Hund"? Falls es inhaltliche Bedenken gibt, nur zu - eine kontroverse Diskussion kann nur von Vorteil sein.

Zitat von Inderhals: Schon wieder so ein "toter Hund". Da werden Erinnerungen wach. Ich sage nur "MOLOGEN".

Hab mir einmal die Finger (fast) verbrannt.

...was hat das mit Arena Pharmaceuticals zu tun? Mit Mologen habe ich mich zumindest noch nie beschäftigt! Un weshalb "toter Hund"? Falls es inhaltliche Bedenken gibt, nur zu - eine kontroverse Diskussion kann nur von Vorteil sein.

Antwort auf Beitrag Nr.: 55.331.170 von Cyberhexe am 15.07.17 16:32:37ARENA Pharmaceutical hat unglaubliches Potenzial, weil folgende Entwicklungsmöglichkeiten gegeben sind:

1.) Ralinepag

2.) Etrasimod

3.) APD371

4.) Nelotanserin

sowie das bereits 2012 für Fettleibigkeit zugelassene

5.) Lorcaserin (brand name: BELVIQ) - ja, auch bei diesem Wirkstoff gibt es erstaunliches Entwicklungspotenzial!

1.) Ralinepag

2.) Etrasimod

3.) APD371

4.) Nelotanserin

sowie das bereits 2012 für Fettleibigkeit zugelassene

5.) Lorcaserin (brand name: BELVIQ) - ja, auch bei diesem Wirkstoff gibt es erstaunliches Entwicklungspotenzial!

Trading Spotlight

Antwort auf Beitrag Nr.: 55.331.170 von Cyberhexe am 15.07.17 16:32:37Ich meine vom Kursverlauf her. Erinnerungen an 2001 werden da wach.

Antwort auf Beitrag Nr.: 55.331.185 von Cyberhexe am 15.07.17 16:37:02

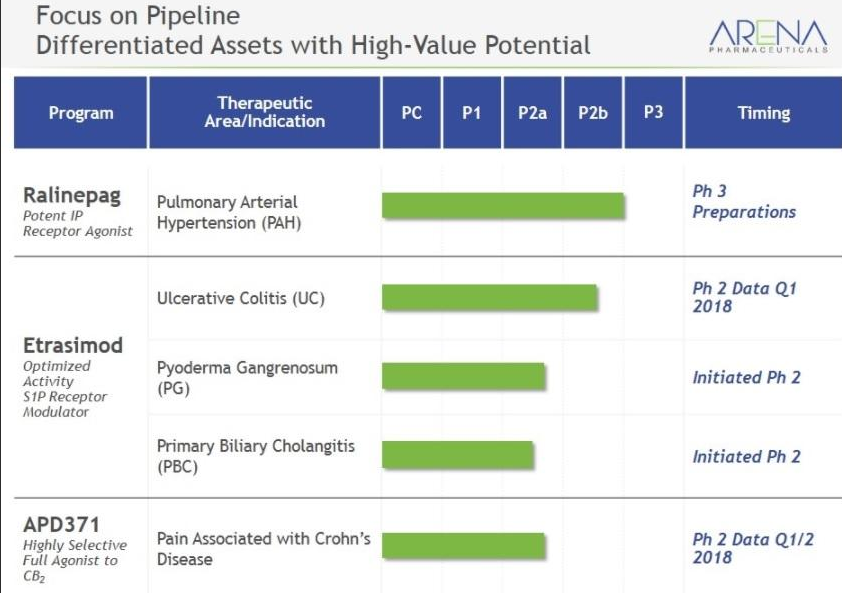

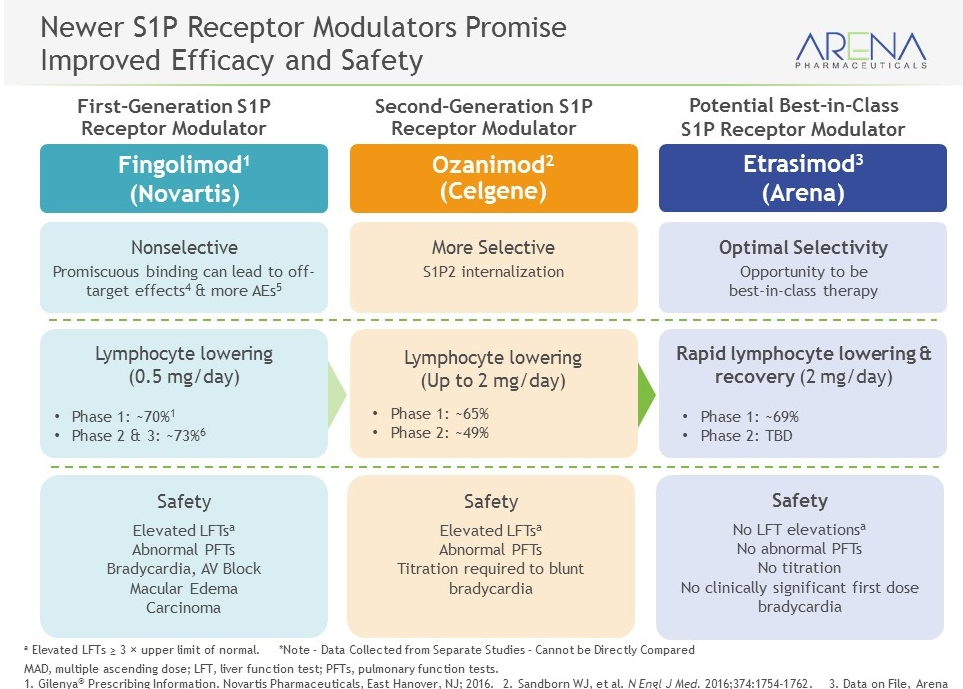

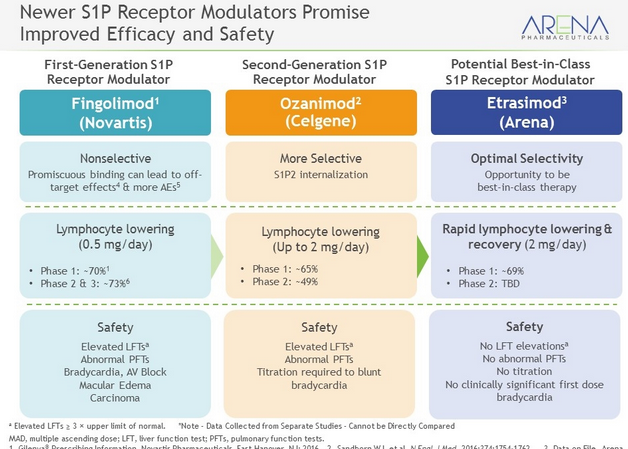

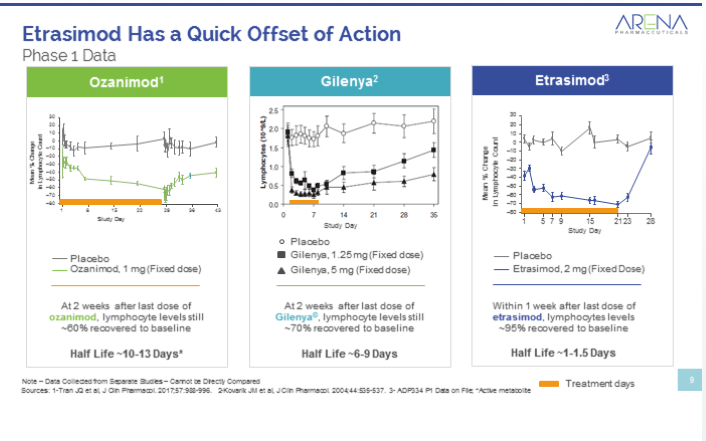

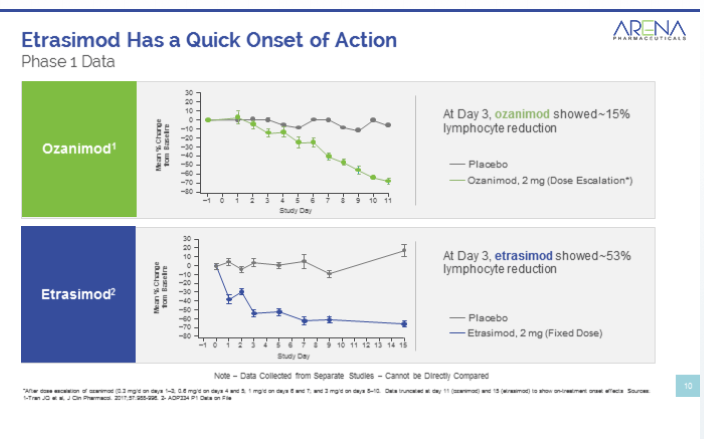

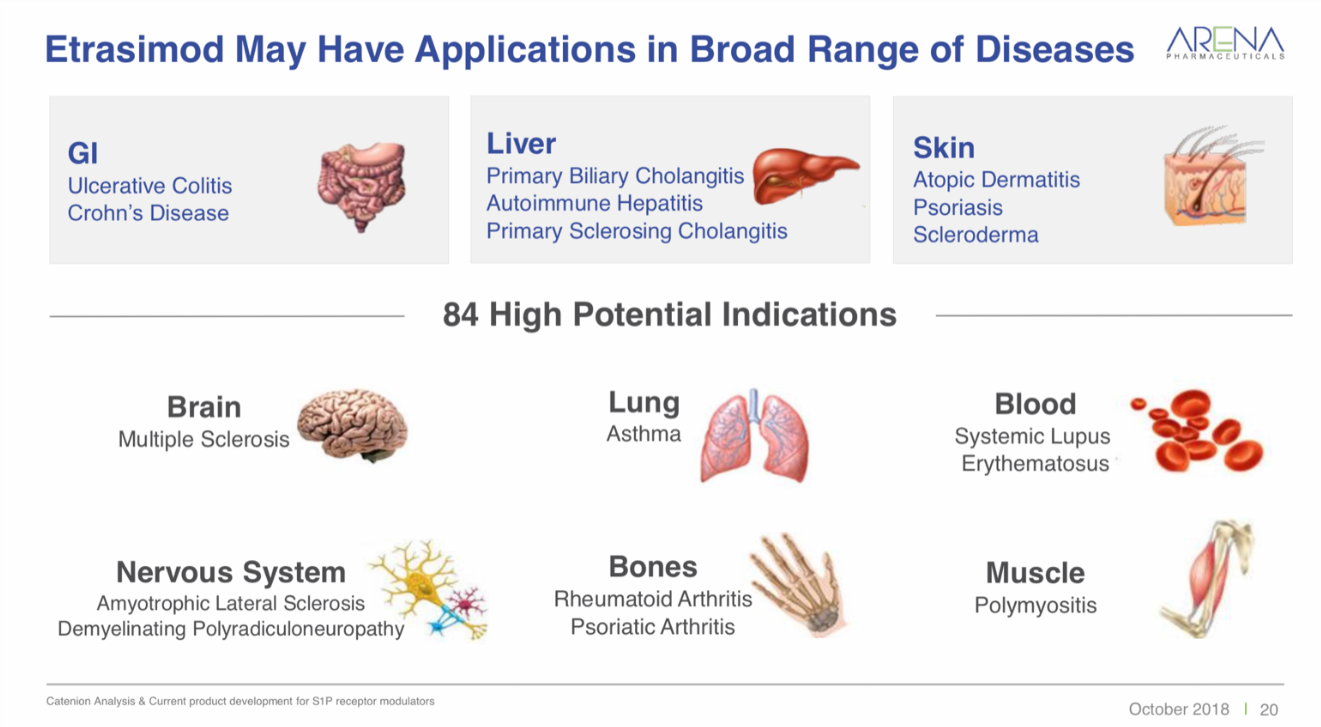

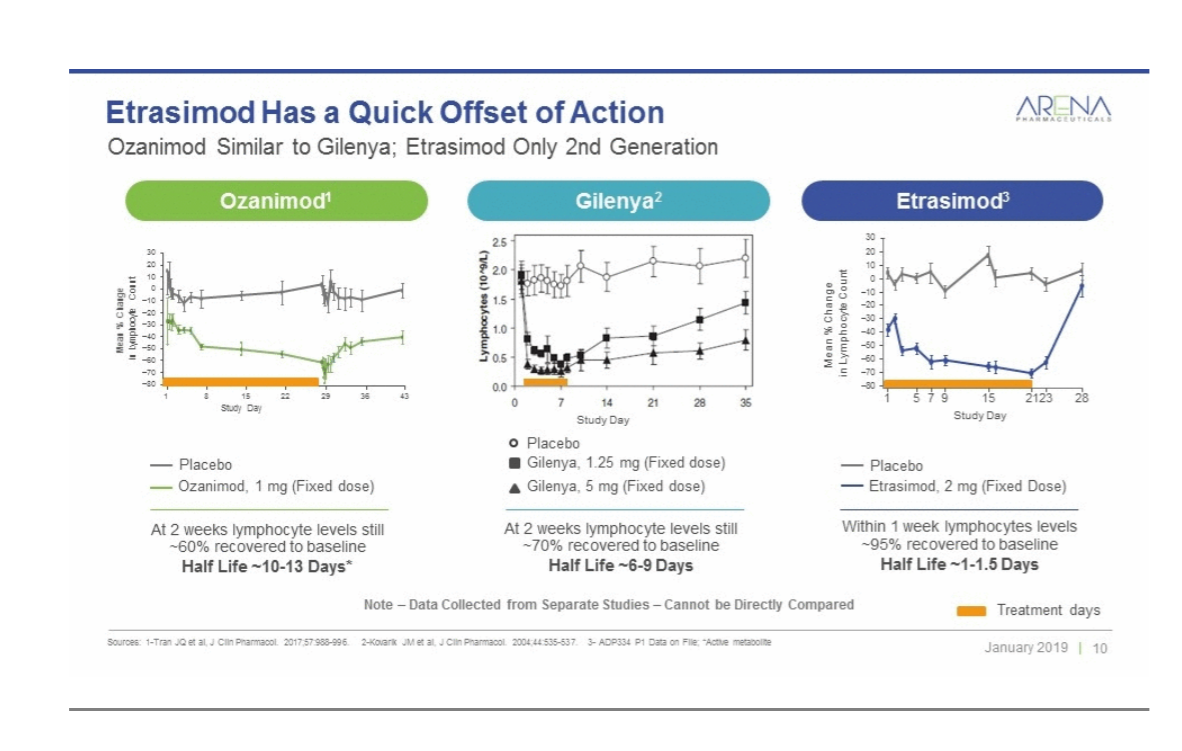

zu 2.) Etrasimod bzw. APD334 ist ein potenzieller best-in class S1P1-Rezeptor-Modulator, der im "grossen Feld" der "Entzündungskrankheiten" aktuell in 4 unterschiedlichen ph2-Studien getestet wird. Der Wirkstoff ist vollständig im Besitz von Arena. Celgene hat kürzlich für die Rechte eines ähnlichen Wirkstoff aus dieser Klasse, Ozanimod, $7.2 Mrd ausgegeben.

Die bisher eingesetzten Wirkstoffe 1. Generation sind sehr unspezifisch und interagieren ebenfalls mit S1P2, S1P3, S1P4 und S1P5- Rezeptoren.

Obwohl ein Wirkstoff der nächsten Generation, ist Oxanimod nicht so spezifisch wie Etrasimod und insbesondere am S1P2-Rezeptor ebenfalls aktiv. Diese Interaktion kann unerwünschte Nebenwirkungen herbei führen.

Etrasimod wird in 4 verschiedenen ph2-Studien in der Klinik getestet, und zwar:

1.) Ulcerative Collitis . Auswertung der Daten soll gegen Ende des Jahres erfolgen

2.) Inflammatory Bowel Disease (IBD)

3.) Pyoderma gangrenosum

4.) Primary biliary cholangitis --> Start im 2HJ2017

(PBC)

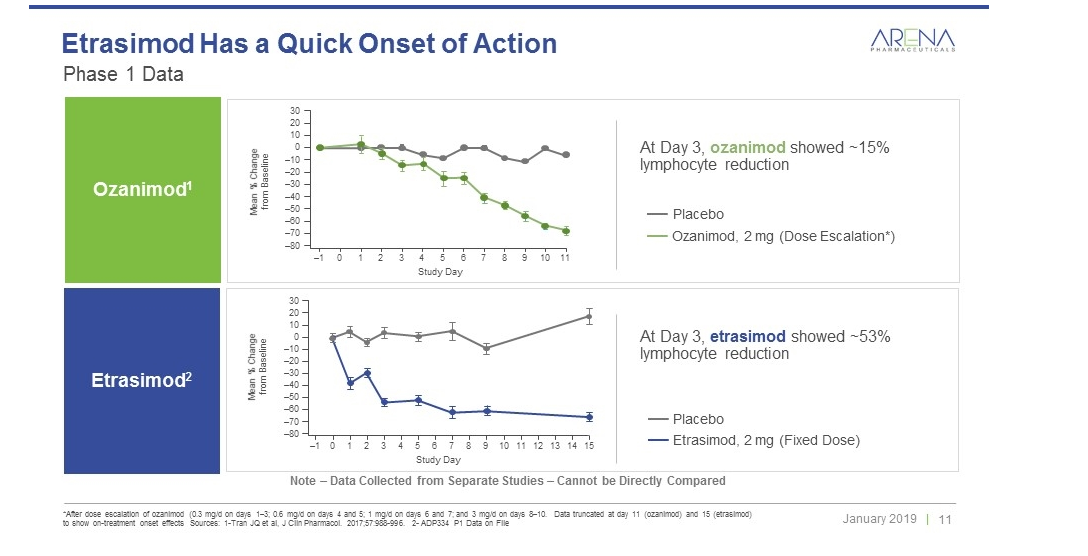

In Phase 1 hat Etrasimod bereits eine Verringerung der Lymphozytenzahl demonstriert.

Sollte das Studienergebnis vorteilhaft ausfallen, dann ist eine ähnliche Bewertung von Etrasimod analog Ozanimod vorstellbar. Und man erinnere sich, dass Celgene insgesamt 7.2 Mrd$ für Ozanimod zu bezahlen hatte.

Aber Vorsicht: bei den autoimunnen Entzündungserkrankungen ist die Zahl der "Durchfaller" beträchtlich.

Zitat von Cyberhexe: ARENA Pharmaceutical hat unglaubliches Potenzial, weil folgende Entwicklungsmöglichkeiten gegeben sind:

1.) Ralinepag

2.) Etrasimod

3.) APD371

4.) Nelotanserin

sowie das bereits 2012 für Fettleibigkeit zugelassene

5.) Lorcaserin (brand name: BELVIQ) - ja, auch bei diesem Wirkstoff gibt es erstaunliches Entwicklungspotenzial!

zu 2.) Etrasimod bzw. APD334 ist ein potenzieller best-in class S1P1-Rezeptor-Modulator, der im "grossen Feld" der "Entzündungskrankheiten" aktuell in 4 unterschiedlichen ph2-Studien getestet wird. Der Wirkstoff ist vollständig im Besitz von Arena. Celgene hat kürzlich für die Rechte eines ähnlichen Wirkstoff aus dieser Klasse, Ozanimod, $7.2 Mrd ausgegeben.

Die bisher eingesetzten Wirkstoffe 1. Generation sind sehr unspezifisch und interagieren ebenfalls mit S1P2, S1P3, S1P4 und S1P5- Rezeptoren.

Obwohl ein Wirkstoff der nächsten Generation, ist Oxanimod nicht so spezifisch wie Etrasimod und insbesondere am S1P2-Rezeptor ebenfalls aktiv. Diese Interaktion kann unerwünschte Nebenwirkungen herbei führen.

Etrasimod wird in 4 verschiedenen ph2-Studien in der Klinik getestet, und zwar:

1.) Ulcerative Collitis . Auswertung der Daten soll gegen Ende des Jahres erfolgen

2.) Inflammatory Bowel Disease (IBD)

3.) Pyoderma gangrenosum

4.) Primary biliary cholangitis --> Start im 2HJ2017

(PBC)

In Phase 1 hat Etrasimod bereits eine Verringerung der Lymphozytenzahl demonstriert.

Sollte das Studienergebnis vorteilhaft ausfallen, dann ist eine ähnliche Bewertung von Etrasimod analog Ozanimod vorstellbar. Und man erinnere sich, dass Celgene insgesamt 7.2 Mrd$ für Ozanimod zu bezahlen hatte.

Aber Vorsicht: bei den autoimunnen Entzündungserkrankungen ist die Zahl der "Durchfaller" beträchtlich.

Antwort auf Beitrag Nr.: 55.331.275 von Cyberhexe am 15.07.17 17:13:28...nun ist sogar Cramer "bullish" - die Daten zu Ralinepag scheinen auch ihn zu überzeugen:

Cramer's lightning round: There are two ways to win with this chipmaker

Elizabeth Gurdus | @elizabethgurdus

Thursday, 13 Jul 2017 | 6:53 PM ET

It's that time again! Jim Cramer rang the lightning round bell, which means he gave his take on caller favorite stocks at rapid speed:

Xilinx: "Two ways to win: I think the earnings are going to be good and I think it could also be taken over. I like the pick."

Arena Pharmaceuticals: "Arena is back from the dead. I can't believe it. They got that positive news about pulmonary and they did a secondary, they raised the money. Pulmonary arterial hypertension, that is a huge market and I've got to tell you – I cannot believe this – it's still a buy."

http://www.cnbc.com/2017/07/13/cramers-lightning-round-there…

Cramer's lightning round: There are two ways to win with this chipmaker

Elizabeth Gurdus | @elizabethgurdus

Thursday, 13 Jul 2017 | 6:53 PM ET

It's that time again! Jim Cramer rang the lightning round bell, which means he gave his take on caller favorite stocks at rapid speed:

Xilinx: "Two ways to win: I think the earnings are going to be good and I think it could also be taken over. I like the pick."

Arena Pharmaceuticals: "Arena is back from the dead. I can't believe it. They got that positive news about pulmonary and they did a secondary, they raised the money. Pulmonary arterial hypertension, that is a huge market and I've got to tell you – I cannot believe this – it's still a buy."

http://www.cnbc.com/2017/07/13/cramers-lightning-round-there…

Antwort auf Beitrag Nr.: 55.333.823 von Cyberhexe am 16.07.17 13:37:14Lisa LaMotta am July 14, 2017

"Elsewhere, Arena Pharmaceuticals may be making a comeback. The once-failing obesity company has switched gears to focus on a hypertension drug that has some recently strong results in Phase 2. If it can reach the market, it won't be as hard a sell as its last attempt."

http://www.biopharmadive.com/news/prescribed-reading-teva-As…

"Elsewhere, Arena Pharmaceuticals may be making a comeback. The once-failing obesity company has switched gears to focus on a hypertension drug that has some recently strong results in Phase 2. If it can reach the market, it won't be as hard a sell as its last attempt."

http://www.biopharmadive.com/news/prescribed-reading-teva-As…

2 neue Patenapplikationen wurden genehmigt:

http://appft.uspto.gov/netacgi/nph-Parser?Sect1=PTO2&Sect2=H…

interessantes Forum:

https://www.investorvillage.com/groups.asp?mb=19370&mn=7206&…

Gruss von Franca_ole

http://appft.uspto.gov/netacgi/nph-Parser?Sect1=PTO2&Sect2=H…

interessantes Forum:

https://www.investorvillage.com/groups.asp?mb=19370&mn=7206&…

Gruss von Franca_ole

Antwort auf Beitrag Nr.: 55.450.260 von Cyberhexe am 03.08.17 12:06:05Arena wird die ph2-Daten zu Ralinepag zur Behandlung von pulmonary arterial hypertension (PAH) in Toronto beim American College of Chest Physicians 2017 (CHEST) Annual Meeting vorstellen und zwar in einem "Late-breaking Abstracts 2": Session 4060

http://chestmeeting.chestnet.org/

http://files.shareholder.com/downloads/ARNA/5444790806x0x960…

http://files.shareholder.com/downloads/ARNA/5444790806x0x948…

http://chestmeeting.chestnet.org/

http://files.shareholder.com/downloads/ARNA/5444790806x0x960…

http://files.shareholder.com/downloads/ARNA/5444790806x0x948…

Antwort auf Beitrag Nr.: 56.011.092 von Cyberhexe am 24.10.17 07:25:27wow....sehr gutes Ergebnis von Etrasimod:

http://invest.arenapharm.com/news-releases/news-release-deta…

http://invest.arenapharm.com/news-releases/news-release-deta…

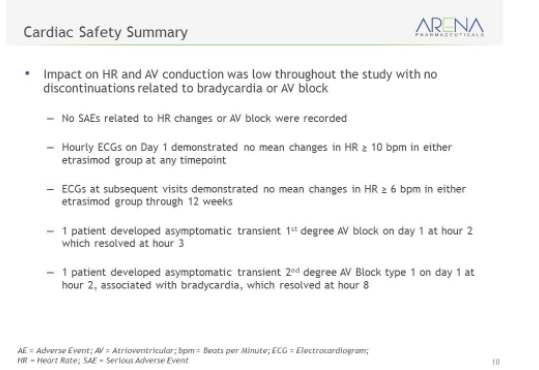

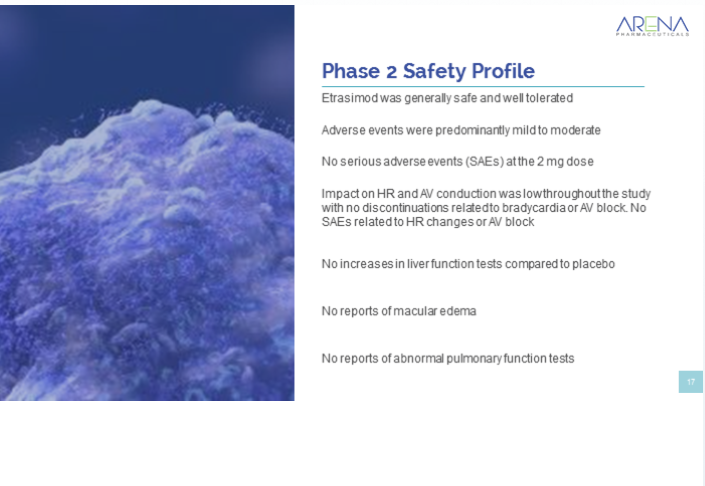

Antwort auf Beitrag Nr.: 57.324.959 von Cyberhexe am 19.03.18 23:38:34Etrasimod bei ulcerative colitis (UC): weniger ernste Nebenwirkungen als unter Plazebo!!!!!!!!!!!!!!!!!!

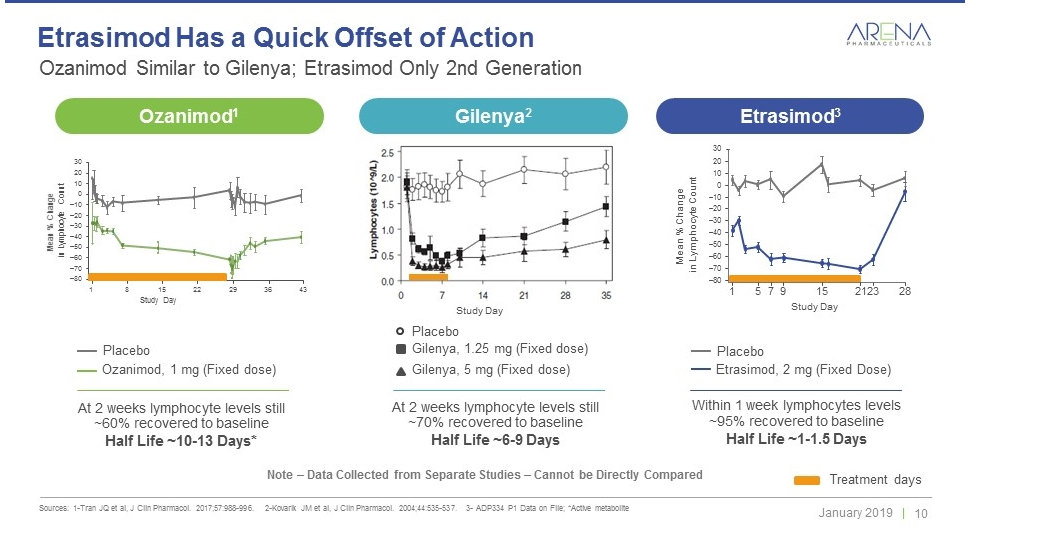

Etrasimod was well tolerated and there were fewer patients with serious adverse events (SAEs) compared to placebo (0% in 2 mg, 5.8% in 1 mg and 11.1% in placebo). Impact on heart rate and atrioventricular (AV) conduction was low throughout the study with no discontinuations from study related to bradycardia or AV block. There were no increases in liver function tests compared to placebo and no reports of macular edema or pulmonary function test abnormalities. The Company plans to present full study results at future medical congresses.

Etrasimod was well tolerated and there were fewer patients with serious adverse events (SAEs) compared to placebo (0% in 2 mg, 5.8% in 1 mg and 11.1% in placebo). Impact on heart rate and atrioventricular (AV) conduction was low throughout the study with no discontinuations from study related to bradycardia or AV block. There were no increases in liver function tests compared to placebo and no reports of macular edema or pulmonary function test abnormalities. The Company plans to present full study results at future medical congresses.

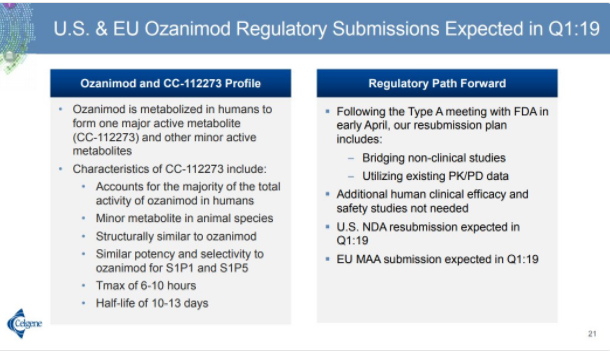

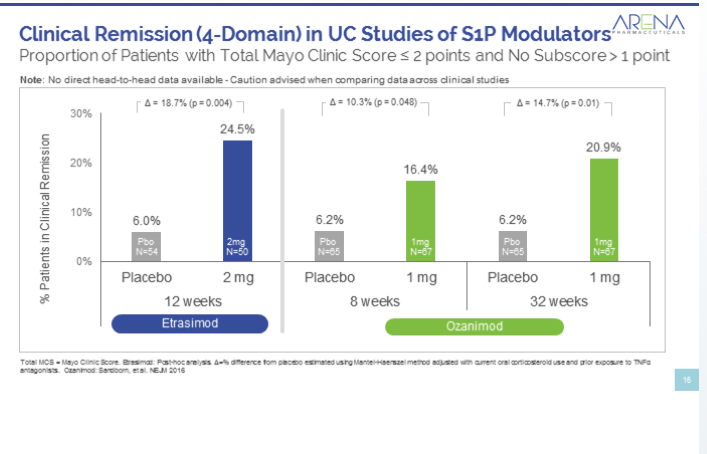

Antwort auf Beitrag Nr.: 57.324.977 von Cyberhexe am 19.03.18 23:42:42man bedenke, dass Receptos im Juli 2015 für 7.2 Milliarden USD von Celgene übernommen wurde, und zwar aufgrund der OZANIMOD-Daten

http://ir.celgene.com/releasedetail.cfm?releaseid=922090

SUMMIT, N.J. & SAN DIEGO--(BUSINESS WIRE)-- Celgene Corporation (NASDAQ: CELG) and Receptos, Inc. (NASDAQ: RCPT) today announced the signing of a definitive agreement in which Celgene has agreed to acquire Receptos. Under the terms of the merger agreement, Celgene will pay $232.00 per share in cash, or a total of approximately $7.2 billion, net of cash acquired.

The acquisition of Receptos significantly enhances Celgene's Inflammation & Immunology (I&I) portfolio, further diversifies the Company's revenue beginning in 2019 and beyond, and builds upon Celgene's growing expertise in inflammatory bowel disease (IBD). The transaction adds Ozanimod, a novel, potential best-in-class, oral, once-daily, selective sphingosine 1-phosphate 1 and 5 receptor modulator (S1P) to Celgene's deep and diverse pipeline of potential disease-altering medicines and investigational compounds.

Based on clinical studies, Ozanimod demonstrated several areas of potential advantage over existing oral therapies for the treatment of ulcerative colitis (UC) and relapsing multiple sclerosis (RMS), including its cardiac, hepatotoxicity and lymphocyte recovery profile. The phase III TRUE NORTH trial in UC is currently underway with data expected in 2018. The phase III RADIANCE and SUNBEAM RMS trials are ongoing and data are expected in the first half of 2017 to support a RMS approval in 2018. Additionally, Ozanimod is positioned to potentially become the first S1P receptor modulator to be approved for IBD.

"The Receptos acquisition provides a transformational opportunity for Celgene to impact multiple therapeutic areas," said Bob Hugin, Chairman and Chief Executive Officer of Celgene. "This acquisition enhances our I&I portfolio and allows us to leverage the investments made in our global organization to accelerate our growth in the medium and long-term."

http://ir.celgene.com/releasedetail.cfm?releaseid=922090

SUMMIT, N.J. & SAN DIEGO--(BUSINESS WIRE)-- Celgene Corporation (NASDAQ: CELG) and Receptos, Inc. (NASDAQ: RCPT) today announced the signing of a definitive agreement in which Celgene has agreed to acquire Receptos. Under the terms of the merger agreement, Celgene will pay $232.00 per share in cash, or a total of approximately $7.2 billion, net of cash acquired.

The acquisition of Receptos significantly enhances Celgene's Inflammation & Immunology (I&I) portfolio, further diversifies the Company's revenue beginning in 2019 and beyond, and builds upon Celgene's growing expertise in inflammatory bowel disease (IBD). The transaction adds Ozanimod, a novel, potential best-in-class, oral, once-daily, selective sphingosine 1-phosphate 1 and 5 receptor modulator (S1P) to Celgene's deep and diverse pipeline of potential disease-altering medicines and investigational compounds.

Based on clinical studies, Ozanimod demonstrated several areas of potential advantage over existing oral therapies for the treatment of ulcerative colitis (UC) and relapsing multiple sclerosis (RMS), including its cardiac, hepatotoxicity and lymphocyte recovery profile. The phase III TRUE NORTH trial in UC is currently underway with data expected in 2018. The phase III RADIANCE and SUNBEAM RMS trials are ongoing and data are expected in the first half of 2017 to support a RMS approval in 2018. Additionally, Ozanimod is positioned to potentially become the first S1P receptor modulator to be approved for IBD.

"The Receptos acquisition provides a transformational opportunity for Celgene to impact multiple therapeutic areas," said Bob Hugin, Chairman and Chief Executive Officer of Celgene. "This acquisition enhances our I&I portfolio and allows us to leverage the investments made in our global organization to accelerate our growth in the medium and long-term."

Antwort auf Beitrag Nr.: 57.324.998 von Cyberhexe am 19.03.18 23:53:41Etrasimod Phase 2 --> kein Signal hinsichtlich Cardiotoxizität:

Antwort auf Beitrag Nr.: 57.330.347 von Cyberhexe am 20.03.18 14:08:26trotz angekündigter Kapitalerhöhung....

Arena Pharmaceuticals Inc. ARNA, +28.68% ticked lower Tuesday after the biotech company announced a secondary offering of shares. Arena shares declined 1.9% after hours, following a surge of 29% to close the regular session at $39.75 on positive clinical results for an ulcerative colitis treatment study. Arena said it will offer 7.5 million shares, with an option to underwriters for 1.1 million more to cover overallotments. Arena has about 39.2 million shares outstanding.

...legt ARENA heute ca. 10% zu - das ist doch sehr ungewöhnlich!

Grosses Tagesvolumen - schon über 6 Mio - und erhöhte Kursziele geben Anlass für weitere Kursphantasie.

Arena Pharmaceuticals Inc. ARNA, +28.68% ticked lower Tuesday after the biotech company announced a secondary offering of shares. Arena shares declined 1.9% after hours, following a surge of 29% to close the regular session at $39.75 on positive clinical results for an ulcerative colitis treatment study. Arena said it will offer 7.5 million shares, with an option to underwriters for 1.1 million more to cover overallotments. Arena has about 39.2 million shares outstanding.

...legt ARENA heute ca. 10% zu - das ist doch sehr ungewöhnlich!

Grosses Tagesvolumen - schon über 6 Mio - und erhöhte Kursziele geben Anlass für weitere Kursphantasie.

Antwort auf Beitrag Nr.: 57.347.147 von Cyberhexe am 21.03.18 20:37:49hab heute unter 40$ eingekauft (1600 Stück), weil die Pipeline von ARENA sehr viel versprechend ist:

Die ph2-Daten zu Etrasimod wurden bereits publiziert und diese sind mindestens genau so gut (eher besser bei Wirkung/Nebenwirkung - allerdings ph2, ist immer mit Vorsicht zu geniessen!) als bei Ozanimod:

und hinsichtlich Nebenwirkungen sehr wahrscheinlich best-in-class:

man beachte Celgene hat 2015 Receptos für 7.2 Milliarden USD nach Bekanntgabe der ph2-Daten von Ozanimod gekauft.

Novartis hat mit Gilenya (generic name: Fingolimod) in 2017 einen Umsatz in Höhe von 3.185 Milliarden USD generiert.

Ausserdem darf man gespannt sein auf die Daten zum CB2 Agonisten APD371, da demnächst die Daten einer ph2-Studie erwartet werden:

https://clinicaltrials.gov/ct2/show/NCT03155945?term=NCT0315…

Die ph2-Daten zu Etrasimod wurden bereits publiziert und diese sind mindestens genau so gut (eher besser bei Wirkung/Nebenwirkung - allerdings ph2, ist immer mit Vorsicht zu geniessen!) als bei Ozanimod:

und hinsichtlich Nebenwirkungen sehr wahrscheinlich best-in-class:

man beachte Celgene hat 2015 Receptos für 7.2 Milliarden USD nach Bekanntgabe der ph2-Daten von Ozanimod gekauft.

Novartis hat mit Gilenya (generic name: Fingolimod) in 2017 einen Umsatz in Höhe von 3.185 Milliarden USD generiert.

Ausserdem darf man gespannt sein auf die Daten zum CB2 Agonisten APD371, da demnächst die Daten einer ph2-Studie erwartet werden:

https://clinicaltrials.gov/ct2/show/NCT03155945?term=NCT0315…

Antwort auf Beitrag Nr.: 55.329.241 von Cyberhexe am 15.07.17 07:25:44

zu Threadbeginn wurden die Hoffnungsträger aus dem Portfolio ausführlich vorgestellt zB Ralinepag:

Zitat von Cyberhexe: ARENA Pharmaceutical hat unglaubliches Potenzial, weil folgende Entwicklungsmöglichkeiten gegeben sind:

1.) Ralinepag

2.) Etrasimod

3.) APD371

4.) Nelotanserin

sowie das bereits 2012 für Fettleibigkeit zugelassene

5.) Lorcaserin (brand name: BELVIQ) - ja, auch bei diesem Wirkstoff gibt es erstaunliches Entwicklungspotenzial!

Doch der Reihe nach:

zu 1.) Ralinepag

diese Woche wurde zu Ralinepag ein ph2-Studienergebnis veröffentlicht, welches in seiner Eindeutigkeit sicherlich nicht nur mich überrascht hat: ein statistisch erreichter primärer Endpunkt bei der Behandlung von 61 Patienten mit PAH (Pulmonary Arterial Hypertension). Obschon vom Unternehmen aufgrund der präklinischen und pharmakokinetischen Studien schon immer als potenziell "best in class" bezeichnet, konnte diese "Vermutung" für diesen Wirkstoff nun zum ersten Mal mit klinischen Fakten belegt werden, und dies mehr als eindrücklich:

"Ralinepag improved median PVR by 163.9 dyn.s.cm-5 from baseline compared to a 0.7 dyn.s.cm-5 worsening from baseline in the placebo arm (P=0.02). Patients treated with ralinepag had a 29.8% improvement in PVR compared to the placebo arm (P=0.03) and a 20.1% improvement in PVR compared to baseline."

PVR (pulmonary vascular resistance) ist ein Mass, welches das Fortschreiten einer lebensbedrohenden bzw. fatalen Krankheit, nämlich die Pulmonale Hypertonie bzw Pulmonary Arterial Hypertension (PAH), kennzeichnet. Dieser ansteigende Gefässwiderstand in den Lungenarterien führt zu einer stark eingeschränkten Leistungsfähigkeit verbunden mit Kreislaufstörungen und Müdigkeit. Oft führt diese Erkrankung zum Ableben der Betroffenen.

In dieser Phase-2-Studie (n=61) hat Ralinepag nun ein mehr als beachtliches Resultat geliefert, nämlich eine Reduktion des Gefässwiderstand um 30% verglichen mit Placebo, und dies auch noch mit statistischer Signifikanz beim primären Endpunkt. Die Erwartungen im Vorfeld waren weitaus skeptischer, da lediglich eine Senkung um 20 -25% prognostiziert wurde. Allerdings wurde ein sekundärer Endpunkt nicht mit statistischer Signifikanz erreicht, nämlich die Wegstrecke, die ein Patient innerhalb von 6 Minuten zurücklegen kann: Ralinepag-Patienten legten 36m zurück, während Patienten unter Plazebo gerade einmal 30m zurücklegten. Eine statistische signifikante Verbesserung dieser Wegstrecke müsste jedoch bei einer mächtigeren ph3-Studie gelingen.

Folgende Punkte der Studie sind allerdings unausgewogen:

der Umstand, dass Ralinepag-Patienten jünger waren als diejenigen unter Plazebo, könnte zu dessen Vorteil gewesen sein. Hingegen waren die Verum-Patienten in einem schlechteren Zustand als unter Plazebo.

Ralinepag gehört zu einer Klasse von bereits etablierten Wirkstoffen zur Behandlung von PAH (pulmonary arterial hypertension), nämlich den IP Prostacyclin-Rezeptor-Agonisten, die in 2016 insgesamt fast 2 Mrd USD Verkaufserlöse erzielt haben. Einer dieser Wirkstoffe am Markt ist Actelions Uptravi (generic name: Selexipag), mit welchem das CH-Unternehmen in 2016, dem Jahr nach der Zulassung (FDA am 22.12.2015) bereits $240m Umsatz erzielt hat. Das Wachstumspotenzial innerhalb Actelions PAH-Portfolio ist ursächlich dafür verantwortlich, dass JNJ das Unternehmen erst kürzlich für sage und schreibe 30 Milliarden USD übernommen hat.

Ralinepag hat gegenüber Selxipag weitere Vorteile, bspw. die Pharmakokinetik: Ralinepag wird wie Selexipag oral verabreicht, hat jedoch eine viel längere Halbwertszeit als Selxipag, weshalb eine wesentlich feinere Dosierung, ähnlich wie bei intravenöser Applikation, erzielt werden kann.

Fortsetzung folgt!

zu Threadbeginn wurden die Hoffnungsträger aus dem Portfolio ausführlich vorgestellt zB Ralinepag:

Antwort auf Beitrag Nr.: 57.391.172 von Cyberhexe am 26.03.18 19:56:01interessantes youTube Video zu Ralinepag:

https://www.youtube.com/watch?v=QOVAgg6OcpA

https://www.youtube.com/watch?v=QOVAgg6OcpA

Antwort auf Beitrag Nr.: 57.395.054 von Cyberhexe am 27.03.18 09:25:56die Kapitalerhöhung einschliesslich "Greenshoe" wurde erfolgreich platziert und bringt dem unternehmen mit ca. USD400m weiteren Spielraum für die Initialisierung der kostenintensiven ph§-Studien zu Ralinepag und Etrasimod. Ausserdem sind auf "demnächst" die ph2-Daten zum CB2-Agonisten APD371 angekündigt, so dass sehr wahrscheinlich ein 3.Kandidat zum Eintritt in die Pivotalstudien zur Verfügung steht.

Arena Pharmaceuticals Announces Completion of Public Offering of Common Stock and Exercise in Full of Underwriters' Option to Purchase Additional Shares

SAN DIEGO, March 26, 2018 /PRNewswire/ -- Arena Pharmaceuticals, Inc. (Nasdaq: ARNA) today announced the completion of its previously announced underwritten public offering of 9,775,000 shares of its common stock at a price to the public of $41.50 per share, including 1,275,000 shares sold pursuant to the exercise in full of the underwriters' option to purchase additional shares. All of the shares were sold by Arena. The gross proceeds from the offering were approximately $405.7 million, before deducting the underwriting discounts and commissions and offering expenses. Arena anticipates using the net proceeds from the offering for the clinical and preclinical development of drug candidates, including its planned Phase 3 programs for etrasimod for the treatment of ulcerative colitis and ralinepag for the treatment of pulmonary arterial hypertension, for general corporate purposes, including working capital and costs associated with manufacturing services, and for capital expenditures.

Ausserdem ist für dieses Jahr noch die BELVIQ-Studie mit 12000 Teilnehmern "fällig".

A Study to Evaluate the Effect of Long-term Treatment With BELVIQ (Lorcaserin HCl) on the Incidence of Major Adverse Cardiovascular Events and Conversion to Type 2 Diabetes Mellitus in Obese and Overweight Subjects With Cardiovascular Disease or Multiple Cardiovascular Risk Factors (CAMELLIA-TIMI)

https://clinicaltrials.gov/ct2/show/NCT02019264?term=Lorcase…

Mit dem Ergebnis dieser Studie könnte sich die Nachfrage nach Lorcaserin sprunghaft vervielfachen - Time will tell!

Arena Pharmaceuticals Announces Completion of Public Offering of Common Stock and Exercise in Full of Underwriters' Option to Purchase Additional Shares

SAN DIEGO, March 26, 2018 /PRNewswire/ -- Arena Pharmaceuticals, Inc. (Nasdaq: ARNA) today announced the completion of its previously announced underwritten public offering of 9,775,000 shares of its common stock at a price to the public of $41.50 per share, including 1,275,000 shares sold pursuant to the exercise in full of the underwriters' option to purchase additional shares. All of the shares were sold by Arena. The gross proceeds from the offering were approximately $405.7 million, before deducting the underwriting discounts and commissions and offering expenses. Arena anticipates using the net proceeds from the offering for the clinical and preclinical development of drug candidates, including its planned Phase 3 programs for etrasimod for the treatment of ulcerative colitis and ralinepag for the treatment of pulmonary arterial hypertension, for general corporate purposes, including working capital and costs associated with manufacturing services, and for capital expenditures.

Ausserdem ist für dieses Jahr noch die BELVIQ-Studie mit 12000 Teilnehmern "fällig".

A Study to Evaluate the Effect of Long-term Treatment With BELVIQ (Lorcaserin HCl) on the Incidence of Major Adverse Cardiovascular Events and Conversion to Type 2 Diabetes Mellitus in Obese and Overweight Subjects With Cardiovascular Disease or Multiple Cardiovascular Risk Factors (CAMELLIA-TIMI)

https://clinicaltrials.gov/ct2/show/NCT02019264?term=Lorcase…

Mit dem Ergebnis dieser Studie könnte sich die Nachfrage nach Lorcaserin sprunghaft vervielfachen - Time will tell!

Antwort auf Beitrag Nr.: 57.395.201 von Cyberhexe am 27.03.18 09:38:22bei den guten ph2-Schlagzeilen zu Ralinepag, Etrasimod und hoffentlich auch zu APD371 sollte man die auslizenzierten Wirkstoffe nicht ganz vergessen, die zukünftig noch für eine grosse Wertschöpfung verantwortlich sein könnten, so zB Lorcaserin (brand: Belviq):

- 5HT2C-Agonist (best in class)

- zugelassen in 2012 zur Behandlung von Fettleibigkeit

- vollständig auslizenziert (Eisai) --> keine Kostenbeteiligung an der Klinik

- Lizenzgebühren vom Umsatz: 9.5% bis 18.5%

bis 175m$/Jahr --> 9.5%

175-500m§/Jahr --> 13.5%

über 500m$/Jahr --> 18.5%

Die ganz grosse Phantasie ergibt sich aus der Tatsache, dass noch in 2018 das Ergebnis einer Phase4-Studie (CAMELLIA) erwartet wird, in welcher 12´000 Teilnehmer mit Lorcaserin behandelt wurden. Nachgewiesen werden soll, dass Lorcaserin sowohl bei der Prävention von Diabetes und cardiovaskulären Erkrankungen einen positiven Effekt hat und nicht, wie viele Vorgängermoleküle (da zu unspezifisch) die Herzklappen schädigt. Sollte diese Studie erfolgreich sein, ist ein starkes Umsatzwachstum bei Belviq sehr wahrscheinlich.

Ebenfalls zu beachten sind die vielen von Eisai initialisierten Studien zur Suchttherapie wie zB

Opioid-Missbrauch --> https://www.upi.com/Health_News/2017/03/24/Prescription-weig…

Update von Eisai zu cardiovaskulären NW (CVOT) in der ph4-Studie:

https://www.eisai.com/news/news201729.html

"...Belviq actually reduced the risk of MACE (e.g 0.8) by 20%"

MACE= Major Adverse Cardiovascular Events

- 5HT2C-Agonist (best in class)

- zugelassen in 2012 zur Behandlung von Fettleibigkeit

- vollständig auslizenziert (Eisai) --> keine Kostenbeteiligung an der Klinik

- Lizenzgebühren vom Umsatz: 9.5% bis 18.5%

bis 175m$/Jahr --> 9.5%

175-500m§/Jahr --> 13.5%

über 500m$/Jahr --> 18.5%

Die ganz grosse Phantasie ergibt sich aus der Tatsache, dass noch in 2018 das Ergebnis einer Phase4-Studie (CAMELLIA) erwartet wird, in welcher 12´000 Teilnehmer mit Lorcaserin behandelt wurden. Nachgewiesen werden soll, dass Lorcaserin sowohl bei der Prävention von Diabetes und cardiovaskulären Erkrankungen einen positiven Effekt hat und nicht, wie viele Vorgängermoleküle (da zu unspezifisch) die Herzklappen schädigt. Sollte diese Studie erfolgreich sein, ist ein starkes Umsatzwachstum bei Belviq sehr wahrscheinlich.

Ebenfalls zu beachten sind die vielen von Eisai initialisierten Studien zur Suchttherapie wie zB

Opioid-Missbrauch --> https://www.upi.com/Health_News/2017/03/24/Prescription-weig…

Update von Eisai zu cardiovaskulären NW (CVOT) in der ph4-Studie:

https://www.eisai.com/news/news201729.html

"...Belviq actually reduced the risk of MACE (e.g 0.8) by 20%"

MACE= Major Adverse Cardiovascular Events

Antwort auf Beitrag Nr.: 55.329.241 von Cyberhexe am 15.07.17 07:25:44

sehr informatives Video zu Ralinepag:

https://www.youtube.com/watch?v=QOVAgg6OcpA

Zitat von Cyberhexe: ARENA Pharmaceutical hat unglaubliches Potenzial, weil folgende Entwicklungsmöglichkeiten gegeben sind:

1.) Ralinepag

2.) Etrasimod

3.) APD371

4.) Nelotanserin

sowie das bereits 2012 für Fettleibigkeit zugelassene

5.) Lorcaserin (brand name: BELVIQ) - ja, auch bei diesem Wirkstoff gibt es erstaunliches Entwicklungspotenzial!

Doch der Reihe nach:

zu 1.) Ralinepag

diese Woche wurde zu Ralinepag ein ph2-Studienergebnis veröffentlicht, welches in seiner Eindeutigkeit sicherlich nicht nur mich überrascht hat: ein statistisch erreichter primärer Endpunkt bei der Behandlung von 61 Patienten mit PAH (Pulmonary Arterial Hypertension). Obschon vom Unternehmen aufgrund der präklinischen und pharmakokinetischen Studien schon immer als potenziell "best in class" bezeichnet, konnte diese "Vermutung" für diesen Wirkstoff nun zum ersten Mal mit klinischen Fakten belegt werden, und dies mehr als eindrücklich:

"Ralinepag improved median PVR by 163.9 dyn.s.cm-5 from baseline compared to a 0.7 dyn.s.cm-5 worsening from baseline in the placebo arm (P=0.02). Patients treated with ralinepag had a 29.8% improvement in PVR compared to the placebo arm (P=0.03) and a 20.1% improvement in PVR compared to baseline."

PVR (pulmonary vascular resistance) ist ein Mass, welches das Fortschreiten einer lebensbedrohenden bzw. fatalen Krankheit, nämlich die Pulmonale Hypertonie bzw Pulmonary Arterial Hypertension (PAH), kennzeichnet. Dieser ansteigende Gefässwiderstand in den Lungenarterien führt zu einer stark eingeschränkten Leistungsfähigkeit verbunden mit Kreislaufstörungen und Müdigkeit. Oft führt diese Erkrankung zum Ableben der Betroffenen.

In dieser Phase-2-Studie (n=61) hat Ralinepag nun ein mehr als beachtliches Resultat geliefert, nämlich eine Reduktion des Gefässwiderstand um 30% verglichen mit Placebo, und dies auch noch mit statistischer Signifikanz beim primären Endpunkt. Die Erwartungen im Vorfeld waren weitaus skeptischer, da lediglich eine Senkung um 20 -25% prognostiziert wurde. Allerdings wurde ein sekundärer Endpunkt nicht mit statistischer Signifikanz erreicht, nämlich die Wegstrecke, die ein Patient innerhalb von 6 Minuten zurücklegen kann: Ralinepag-Patienten legten 36m zurück, während Patienten unter Plazebo gerade einmal 30m zurücklegten. Eine statistische signifikante Verbesserung dieser Wegstrecke müsste jedoch bei einer mächtigeren ph3-Studie gelingen.

Folgende Punkte der Studie sind allerdings unausgewogen:

der Umstand, dass Ralinepag-Patienten jünger waren als diejenigen unter Plazebo, könnte zu dessen Vorteil gewesen sein. Hingegen waren die Verum-Patienten in einem schlechteren Zustand als unter Plazebo.

Ralinepag gehört zu einer Klasse von bereits etablierten Wirkstoffen zur Behandlung von PAH (pulmonary arterial hypertension), nämlich den IP Prostacyclin-Rezeptor-Agonisten, die in 2016 insgesamt fast 2 Mrd USD Verkaufserlöse erzielt haben. Einer dieser Wirkstoffe am Markt ist Actelions Uptravi (generic name: Selexipag), mit welchem das CH-Unternehmen in 2016, dem Jahr nach der Zulassung (FDA am 22.12.2015) bereits $240m Umsatz erzielt hat. Das Wachstumspotenzial innerhalb Actelions PAH-Portfolio ist ursächlich dafür verantwortlich, dass JNJ das Unternehmen erst kürzlich für sage und schreibe 30 Milliarden USD übernommen hat.

Ralinepag hat gegenüber Selxipag weitere Vorteile, bspw. die Pharmakokinetik: Ralinepag wird wie Selexipag oral verabreicht, hat jedoch eine viel längere Halbwertszeit als Selxipag, weshalb eine wesentlich feinere Dosierung, ähnlich wie bei intravenöser Applikation, erzielt werden kann.

Fortsetzung folgt!

sehr informatives Video zu Ralinepag:

https://www.youtube.com/watch?v=QOVAgg6OcpA

Antwort auf Beitrag Nr.: 57.422.510 von Cyberhexe am 29.03.18 13:10:50Ralinepag ph2-Ergebnis:

Nebenwirkungen:

Nebenwirkungen:

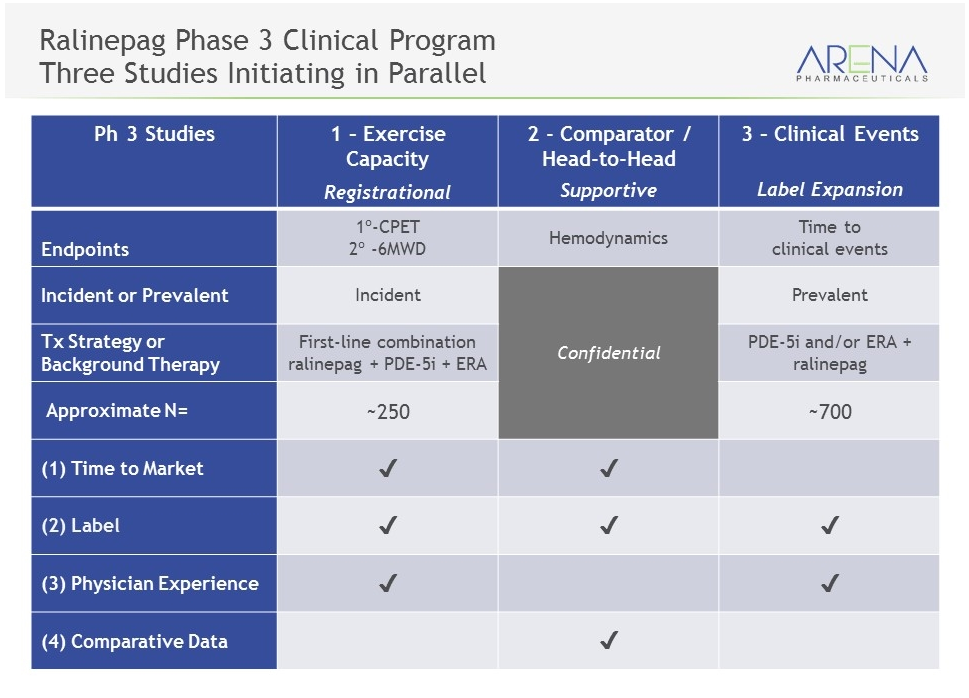

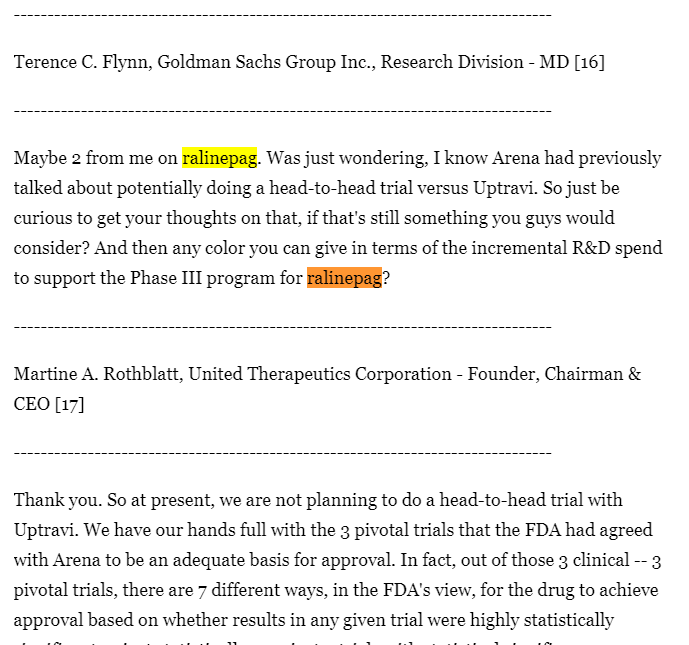

Antwort auf Beitrag Nr.: 57.422.663 von Cyberhexe am 29.03.18 13:22:07es sind 3 ph3-Studien geplant, wobei eine davon eine Head-to-Head-Studie sein wird. Ich würde darauf wetten, dass gegenüber Selexipag verglichen wird:

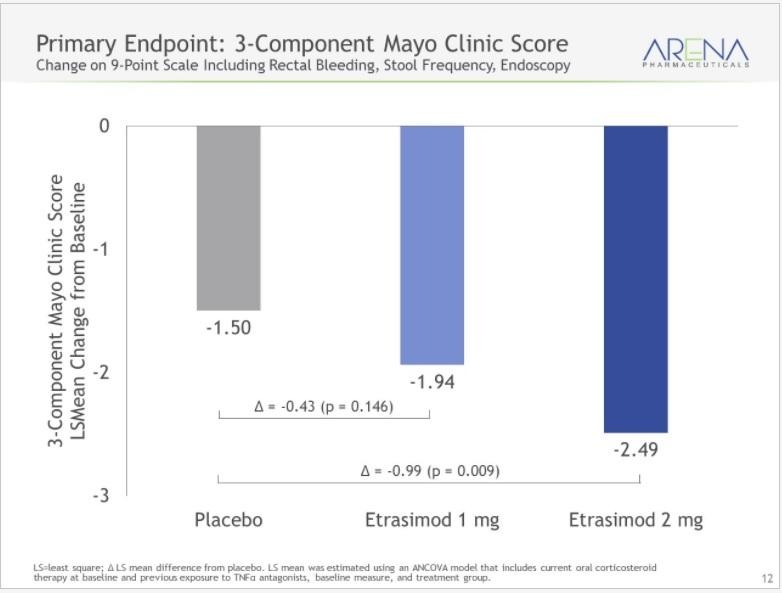

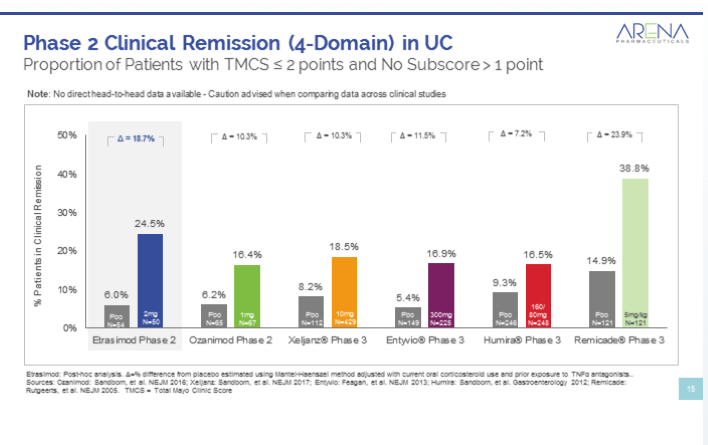

Antwort auf Beitrag Nr.: 57.422.702 von Cyberhexe am 29.03.18 13:24:35Kommentar von Gary R. Lichtenstein, MD über das Ergebnis von OASIS --> ph2-Studie mit Etrasimod zur Behandlung von Ulcerative colitis:

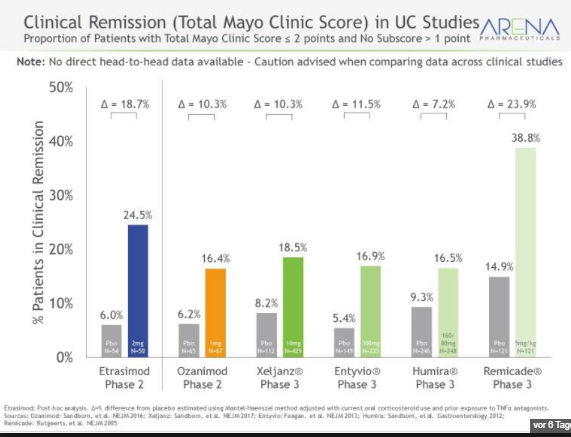

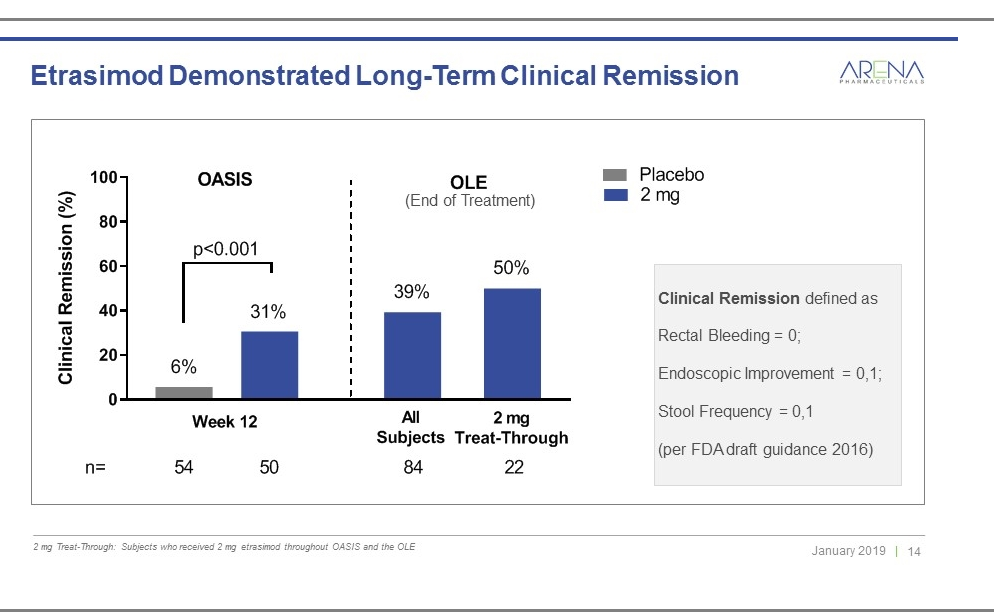

The most recent agent that has been evaluated is etrasimod (APD334, Arena Pharmaceuticals), the next generation S1P agent, which has an increased selectivity of the 1, 4 and 5 receptors. The OASIS trial was a 12-week trial, phase 2 study of patients with UC, which was just completed in December. The data show there was a statistically significant improvement in Mayo scores with the 2-mg dose at week 12. In the 1-mg group there was no benefit, but the 2-mg group had greater endoscopic improvement compared with placebo (41.8% vs. 17.8%; P = .003). Remission was achieved by 33% of the 2-mg group vs. 8% of the placebo group (P = .001), and the four-component total Mayo clinical score remission was achieved by 24.5% vs. 6% (P = .004).

The beauty was it was well-tolerated and resulted in fewer severe adverse events (0% in the 2-mg group vs. 5.8% in the 1-mg group and 11% in the placebo group). So, heart rate and AV conduction defects were low throughout the study with no medication stopped from bradycardia or AV block, no liver test abnormalities compared with placebo, and no macular edema. With this agent there was no observed pulmonary function test abnormalities as had been described with fingolimod.

The results thus far look promising; however, I await the results of the phase 3 studies. This agent has the potential to add another option to our medical arsenal for the treatment of patients with IBD. Thus far, the beauty of this agent is that there is no observed malignancy and no infection. This agent will have significant potential if shown to be efficacious in phase 3 given its safety profile.

Gary R. Lichtenstein, MD

Professor of Medicine

Director, Center for Inflammatory Bowel Disease

University of Pennsylvania Health System, Philadelphia, PA

The most recent agent that has been evaluated is etrasimod (APD334, Arena Pharmaceuticals), the next generation S1P agent, which has an increased selectivity of the 1, 4 and 5 receptors. The OASIS trial was a 12-week trial, phase 2 study of patients with UC, which was just completed in December. The data show there was a statistically significant improvement in Mayo scores with the 2-mg dose at week 12. In the 1-mg group there was no benefit, but the 2-mg group had greater endoscopic improvement compared with placebo (41.8% vs. 17.8%; P = .003). Remission was achieved by 33% of the 2-mg group vs. 8% of the placebo group (P = .001), and the four-component total Mayo clinical score remission was achieved by 24.5% vs. 6% (P = .004).

The beauty was it was well-tolerated and resulted in fewer severe adverse events (0% in the 2-mg group vs. 5.8% in the 1-mg group and 11% in the placebo group). So, heart rate and AV conduction defects were low throughout the study with no medication stopped from bradycardia or AV block, no liver test abnormalities compared with placebo, and no macular edema. With this agent there was no observed pulmonary function test abnormalities as had been described with fingolimod.

The results thus far look promising; however, I await the results of the phase 3 studies. This agent has the potential to add another option to our medical arsenal for the treatment of patients with IBD. Thus far, the beauty of this agent is that there is no observed malignancy and no infection. This agent will have significant potential if shown to be efficacious in phase 3 given its safety profile.

Gary R. Lichtenstein, MD

Professor of Medicine

Director, Center for Inflammatory Bowel Disease

University of Pennsylvania Health System, Philadelphia, PA

Antwort auf Beitrag Nr.: 57.423.692 von Cyberhexe am 29.03.18 14:48:41interessanter Kommentar eines Investment Banker (--> Nathan Sadeghi-Nejad, a partner at Palkon Capital Management) bei einem Forum --> "Biotech Unfiltered" am Wochenende in NYC:

Sadeghi echoed the biotech turnaround theme. Palkon started buying Arena Pharmaceuticals (ARNA) about 16 months ago, he said, because of a disconnect in the market. Most investors still viewed Arena skeptically because its weight-loss drug, Belviq, was a commercial disappointment. But Arena, under new management, had already jettisoned Belviq and started to focus on other drugs that had been sitting on the shelf for a long time.

“Whatever you want to say about Belviq, Arena’s chemists were able to engineer away some well-known cardiac side effects,” said Sadeghi. “That got us thinking that there could be some really good chemistry in Arena’s other, neglected assets. And that prompted us to dig in harder.”

That digging has paid off. Over the past year, Arena shares are up more than 130 percent due to positive mid-stage study results from a pair of the company’s pipeline drugs.

Sadeghi echoed the biotech turnaround theme. Palkon started buying Arena Pharmaceuticals (ARNA) about 16 months ago, he said, because of a disconnect in the market. Most investors still viewed Arena skeptically because its weight-loss drug, Belviq, was a commercial disappointment. But Arena, under new management, had already jettisoned Belviq and started to focus on other drugs that had been sitting on the shelf for a long time.

“Whatever you want to say about Belviq, Arena’s chemists were able to engineer away some well-known cardiac side effects,” said Sadeghi. “That got us thinking that there could be some really good chemistry in Arena’s other, neglected assets. And that prompted us to dig in harder.”

That digging has paid off. Over the past year, Arena shares are up more than 130 percent due to positive mid-stage study results from a pair of the company’s pipeline drugs.

Antwort auf Beitrag Nr.: 57.497.144 von Cyberhexe am 09.04.18 11:56:37Ralinepag war eines der Top-Themen anlässlich des 38. Jahrestreffen der int. Gesellschaft für Herz- und Lungentransplantationen in Nizza:

Improved Pulmonary Arterial Hypertension Mortality Risk Scores

Show Positive Impact of Ralinepag at the ISHLT 38th Annual Meeting

& Scientific Sessions

NICE, FR April 14, 2018 – Today at the International Society for Heart and Lung Transplantation

(ISHLT) 38th Annual Meeting & Scientific Sessions, Raymond Benza, MD, FAAC, shared results of

his team’s phase two study analysis on using Ralinepag—an oral, selective Prostacyclin (IP) receptor

agonist medication—to treat pulmonary arterial hypertension currently in development. During the

presentation, Benza shared that in a 22-week study, 40 patients enrolled who had been prescribed

ralinepag and another 21 patients on placebos. Results showed that after the treatment period,

more patients treated with ralinepag compared with the placebo group stayed or moved into a lowrisk

mortality category significantly improving pulmonary vascular resistance. The study measured

low-risk mortality using three well-established risk scores from three registries.

During the presentation, researchers shared the importance of developing accurate risk scores to

enable identification of patients at highest risk for mortality, and assessment of the impact of

treatments on moving patients into a low-risk category. The team used the following registries to

calculate risk scores:

● REVEAL

● French Pulmonary Hypertension Network

● COMPERA

“It’s exciting to see continued progress with PAH treatment and we’re delighted to have the

ralinepag study results presented here at the ISHLT Annual Meeting,” said Christian Benden, MD,

FCCP, Scientific Program Chair for the ISHLT 38th Annual Meeting and Scientific Sessions.

Benza indicated a ralinepag phase three program in patients with PAH is currently being planned to

evaluate the impact on clinical outcomes and exercise capacity.

http://www.ishlt.org/ContentDocuments/2018PR_4-14-2018_Impro…

Improved Pulmonary Arterial Hypertension Mortality Risk Scores

Show Positive Impact of Ralinepag at the ISHLT 38th Annual Meeting

& Scientific Sessions

NICE, FR April 14, 2018 – Today at the International Society for Heart and Lung Transplantation

(ISHLT) 38th Annual Meeting & Scientific Sessions, Raymond Benza, MD, FAAC, shared results of

his team’s phase two study analysis on using Ralinepag—an oral, selective Prostacyclin (IP) receptor

agonist medication—to treat pulmonary arterial hypertension currently in development. During the

presentation, Benza shared that in a 22-week study, 40 patients enrolled who had been prescribed

ralinepag and another 21 patients on placebos. Results showed that after the treatment period,

more patients treated with ralinepag compared with the placebo group stayed or moved into a lowrisk

mortality category significantly improving pulmonary vascular resistance. The study measured

low-risk mortality using three well-established risk scores from three registries.

During the presentation, researchers shared the importance of developing accurate risk scores to

enable identification of patients at highest risk for mortality, and assessment of the impact of

treatments on moving patients into a low-risk category. The team used the following registries to

calculate risk scores:

● REVEAL

● French Pulmonary Hypertension Network

● COMPERA

“It’s exciting to see continued progress with PAH treatment and we’re delighted to have the

ralinepag study results presented here at the ISHLT Annual Meeting,” said Christian Benden, MD,

FCCP, Scientific Program Chair for the ISHLT 38th Annual Meeting and Scientific Sessions.

Benza indicated a ralinepag phase three program in patients with PAH is currently being planned to

evaluate the impact on clinical outcomes and exercise capacity.

http://www.ishlt.org/ContentDocuments/2018PR_4-14-2018_Impro…

Antwort auf Beitrag Nr.: 57.555.642 von Cyberhexe am 16.04.18 17:40:25es könnte doch noch länger dauern bis Ozanimod den Markt erreicht

https://endpts.com/celgenes-disclosures-about-ozanimod-this-…

Celgene’s disclosures about ozanimod this week spur analysts’ fears of a lengthy delay for a key drug

by john carroll — on April 26, 2018 08:57 AM EDT

Updated: 09:00 AM

Researchers for Celgene $CELG turned up at the American Academy of Neurology meeting this week with some news about the multiple sclerosis drug ozanimod that quickly captured analysts’ attention.

In a presentation on ozanimod Phase III data, an investigator spotlighted an active metabolite produced by the drug, spurring an ah-ha moment for analysts who have been puzzling out why the FDA recently issued a stunning refuse-to-file notice on the drug.

Jefferies’ Michael Yee noted this morning:

We and many observers believe the issue relates to this metabolite that hasn’t been sufficiently characterized by CELG and may not have sufficient information and safety data to permit FDA to fully review the drug for approval which is a problem.

There’s two ways to look at this, he adds, depending on whether you’re a bull or a bear on the suffering stock. The bull argument would pose that a presentation at a conference like this would mean that Celgene couldn’t be all that concerned by the metabolite issue, while the bear view would be:

(I)nsufficient tox coverage for this metabolite which is the actual active moiety, FDA guidance suggests needs 1-2 years more preclinical studies, brings big uncertainty even if NDA filing – whether Ozanimod would actually get approved and/or now has hair on it.

Investors now want to know if the company plans to re-file soon or will look to go back to the drawing board with new, and potentially damaging, delays to disclose. But there’s no sign of an early reaction on the stock price, which is slightly in the green in pre-market trading. The stock is down 18%, though, from the beginning of the year.

The biotech reported at the end of February that the RTF came through because the FDA determined “that the nonclinical and clinical pharmacology sections in the NDA were insufficient to permit a complete review” for multiple sclerosis, leaving plenty of unanswered questions about a drug that Celgene execs had confidently predicted would bring in $4 billion to $6 billion a year. Coming on the heels of the implosion of its $710 million cash roll of the dice on the inflammatory bowel disease drug mongersen (GED-301), investors started wondering why the company was suddenly lurching from disaster to disaster.

CEO Mark Alles followed up with a management shakeup that left him with wider direct control over operations at the company.

I’ve sent out a message to Celgene, but the company isn’t noted for quick transparency.

https://endpts.com/celgenes-disclosures-about-ozanimod-this-…

Celgene’s disclosures about ozanimod this week spur analysts’ fears of a lengthy delay for a key drug

by john carroll — on April 26, 2018 08:57 AM EDT

Updated: 09:00 AM

Researchers for Celgene $CELG turned up at the American Academy of Neurology meeting this week with some news about the multiple sclerosis drug ozanimod that quickly captured analysts’ attention.

In a presentation on ozanimod Phase III data, an investigator spotlighted an active metabolite produced by the drug, spurring an ah-ha moment for analysts who have been puzzling out why the FDA recently issued a stunning refuse-to-file notice on the drug.

Jefferies’ Michael Yee noted this morning:

We and many observers believe the issue relates to this metabolite that hasn’t been sufficiently characterized by CELG and may not have sufficient information and safety data to permit FDA to fully review the drug for approval which is a problem.

There’s two ways to look at this, he adds, depending on whether you’re a bull or a bear on the suffering stock. The bull argument would pose that a presentation at a conference like this would mean that Celgene couldn’t be all that concerned by the metabolite issue, while the bear view would be:

(I)nsufficient tox coverage for this metabolite which is the actual active moiety, FDA guidance suggests needs 1-2 years more preclinical studies, brings big uncertainty even if NDA filing – whether Ozanimod would actually get approved and/or now has hair on it.

Investors now want to know if the company plans to re-file soon or will look to go back to the drawing board with new, and potentially damaging, delays to disclose. But there’s no sign of an early reaction on the stock price, which is slightly in the green in pre-market trading. The stock is down 18%, though, from the beginning of the year.

The biotech reported at the end of February that the RTF came through because the FDA determined “that the nonclinical and clinical pharmacology sections in the NDA were insufficient to permit a complete review” for multiple sclerosis, leaving plenty of unanswered questions about a drug that Celgene execs had confidently predicted would bring in $4 billion to $6 billion a year. Coming on the heels of the implosion of its $710 million cash roll of the dice on the inflammatory bowel disease drug mongersen (GED-301), investors started wondering why the company was suddenly lurching from disaster to disaster.

CEO Mark Alles followed up with a management shakeup that left him with wider direct control over operations at the company.

I’ve sent out a message to Celgene, but the company isn’t noted for quick transparency.

Antwort auf Beitrag Nr.: 57.637.383 von Cyberhexe am 26.04.18 17:45:12APD371 abstract published in The Journal of Pain, March 2018

An abstract summary of the data presented in the March 6 poster by ARNA at the Congress of the American Pain Society. Notice how there were fewer side effects reported in those receiving APD371 vs placebo in the multiple ascending dose (MAD) study.

Safety, Tolerability and Pharmacokinetics of APD371, a Highly Selective CB2 Agonist, in Healthy Adults

C. Jones, S. Turner, J Ruckle, Q Liu, R Christopher, and P Klassen, Arena Pharmaceuticals

Journal of Pain, March 2018, 19:3, S82

Cannabinoids have shown efficacy in the management of chronic pain, but their therapeutic use is limited by the occurrence of psychotropic effects, thought to result from CB1 activation. Most natural or synthetic agents are nonselective for both cannabinoid receptors (CB1 (mainly CNS localized) and CB2 (mainly peripheral). CB2 is an ideal single target to minimize CNS effects, and APD371 is a highly selective, full agonist for the CB2 receptor. Two phase 1, randomized, double-blind, placebo-controlled studies were conducted in healthy subjects aged 18-45 years. Subjects were randomly assigned to receive 1 dose of APD371 (10-400 mg; 6:2 active lacebo per cohort, total 42:14 in a single ascending dose (SAD) study, or to receive APD371 TID for 10 days and once on day 11 (50-200 mg;9:3 activelacebo per cohort, total 27:9) in a multiple ascending dose (MAD) study. Subjects in both studies were monitored for safety, tolerability, and pharmacokinetics. In the SAD study, Tmax was approximately 1.5 hours and mean T ½ was 3.11-4.23 hours across groups. 45.2% of subjects receiving APD371 and 21.4% receiving placebo reported AEs- most were mild, none were serious. Among APD371 subjects, the most common AEs, particularly at the highest dose levels, were dry mouth, somnolence, diarrhea, dizziness and headache. A trend towards dose-related increases in heart rate (asymptomatic) was noted. In the MAD study, plasma steady state was achieved after 4 days of TID dosing. 25.9% of subjects receiving APD371 and 33.3% receiving placebo reported AEs. All were mild, with headache and nausea the most common among APD371 subjects. Asymptomatic decreases in heart rate and BP were observed, which did not preclude dose escalation. APD371 at single and multiple doses was well tolerated, without the CNS/psychotropic effects commonly seen with cannabinoids, and with no clinically significant changes in vital signs, ECGs, or clinical laboratory tests. This study was supported by Arena Pharmaceuticals, Inc.

lacebo per cohort, total 42:14 in a single ascending dose (SAD) study, or to receive APD371 TID for 10 days and once on day 11 (50-200 mg;9:3 activelacebo per cohort, total 27:9) in a multiple ascending dose (MAD) study. Subjects in both studies were monitored for safety, tolerability, and pharmacokinetics. In the SAD study, Tmax was approximately 1.5 hours and mean T ½ was 3.11-4.23 hours across groups. 45.2% of subjects receiving APD371 and 21.4% receiving placebo reported AEs- most were mild, none were serious. Among APD371 subjects, the most common AEs, particularly at the highest dose levels, were dry mouth, somnolence, diarrhea, dizziness and headache. A trend towards dose-related increases in heart rate (asymptomatic) was noted. In the MAD study, plasma steady state was achieved after 4 days of TID dosing. 25.9% of subjects receiving APD371 and 33.3% receiving placebo reported AEs. All were mild, with headache and nausea the most common among APD371 subjects. Asymptomatic decreases in heart rate and BP were observed, which did not preclude dose escalation. APD371 at single and multiple doses was well tolerated, without the CNS/psychotropic effects commonly seen with cannabinoids, and with no clinically significant changes in vital signs, ECGs, or clinical laboratory tests. This study was supported by Arena Pharmaceuticals, Inc.

An abstract summary of the data presented in the March 6 poster by ARNA at the Congress of the American Pain Society. Notice how there were fewer side effects reported in those receiving APD371 vs placebo in the multiple ascending dose (MAD) study.

Safety, Tolerability and Pharmacokinetics of APD371, a Highly Selective CB2 Agonist, in Healthy Adults

C. Jones, S. Turner, J Ruckle, Q Liu, R Christopher, and P Klassen, Arena Pharmaceuticals

Journal of Pain, March 2018, 19:3, S82

Cannabinoids have shown efficacy in the management of chronic pain, but their therapeutic use is limited by the occurrence of psychotropic effects, thought to result from CB1 activation. Most natural or synthetic agents are nonselective for both cannabinoid receptors (CB1 (mainly CNS localized) and CB2 (mainly peripheral). CB2 is an ideal single target to minimize CNS effects, and APD371 is a highly selective, full agonist for the CB2 receptor. Two phase 1, randomized, double-blind, placebo-controlled studies were conducted in healthy subjects aged 18-45 years. Subjects were randomly assigned to receive 1 dose of APD371 (10-400 mg; 6:2 active

lacebo per cohort, total 42:14 in a single ascending dose (SAD) study, or to receive APD371 TID for 10 days and once on day 11 (50-200 mg;9:3 activelacebo per cohort, total 27:9) in a multiple ascending dose (MAD) study. Subjects in both studies were monitored for safety, tolerability, and pharmacokinetics. In the SAD study, Tmax was approximately 1.5 hours and mean T ½ was 3.11-4.23 hours across groups. 45.2% of subjects receiving APD371 and 21.4% receiving placebo reported AEs- most were mild, none were serious. Among APD371 subjects, the most common AEs, particularly at the highest dose levels, were dry mouth, somnolence, diarrhea, dizziness and headache. A trend towards dose-related increases in heart rate (asymptomatic) was noted. In the MAD study, plasma steady state was achieved after 4 days of TID dosing. 25.9% of subjects receiving APD371 and 33.3% receiving placebo reported AEs. All were mild, with headache and nausea the most common among APD371 subjects. Asymptomatic decreases in heart rate and BP were observed, which did not preclude dose escalation. APD371 at single and multiple doses was well tolerated, without the CNS/psychotropic effects commonly seen with cannabinoids, and with no clinically significant changes in vital signs, ECGs, or clinical laboratory tests. This study was supported by Arena Pharmaceuticals, Inc.

lacebo per cohort, total 42:14 in a single ascending dose (SAD) study, or to receive APD371 TID for 10 days and once on day 11 (50-200 mg;9:3 activelacebo per cohort, total 27:9) in a multiple ascending dose (MAD) study. Subjects in both studies were monitored for safety, tolerability, and pharmacokinetics. In the SAD study, Tmax was approximately 1.5 hours and mean T ½ was 3.11-4.23 hours across groups. 45.2% of subjects receiving APD371 and 21.4% receiving placebo reported AEs- most were mild, none were serious. Among APD371 subjects, the most common AEs, particularly at the highest dose levels, were dry mouth, somnolence, diarrhea, dizziness and headache. A trend towards dose-related increases in heart rate (asymptomatic) was noted. In the MAD study, plasma steady state was achieved after 4 days of TID dosing. 25.9% of subjects receiving APD371 and 33.3% receiving placebo reported AEs. All were mild, with headache and nausea the most common among APD371 subjects. Asymptomatic decreases in heart rate and BP were observed, which did not preclude dose escalation. APD371 at single and multiple doses was well tolerated, without the CNS/psychotropic effects commonly seen with cannabinoids, and with no clinically significant changes in vital signs, ECGs, or clinical laboratory tests. This study was supported by Arena Pharmaceuticals, Inc.

Antwort auf Beitrag Nr.: 57.688.824 von Cyberhexe am 03.05.18 18:50:01Daten zur ph2 von Olorinab (APD371) zur Schmerzbehandlung von Crohn-patioenten müssten demnächst publiziert werden:

Antwort auf Beitrag Nr.: 57.693.015 von Cyberhexe am 04.05.18 09:56:41Celgenes Ozanimod hat Schwierigkeiten mit einem Metaboliten, zu welchem kaum Informationen vorliegen. Mit Arenas Etrasimod sind diesbezüglich keine negativen Überraschungen wahrscheinlich:

Antwort auf Beitrag Nr.: 57.390.548 von Cyberhexe am 26.03.18 18:58:10

Ozanimod wurde von Celgene durch den Kauf von Receptos für $7.2 Mrd erworben. Es wird nun mit einer Verzögerung von einem Jahr bei der Zulassung gerechnet, da Abklärungen zu den Nebenwirkungen des aktiven Metaboliten erforderlich sind.

Ich bin mir fast sicher, dass ETRASIMOD (von Arena Pharmaceutical) die bessere Variante darstellt, da sowohl die Spezifität an den Rezeptoren als auch die Entstehung von Metaboliten günstiger erscheint. Allerdings wurde mit Etrasimod erst eine ph2-Studie abgeschlossen, weshalb die Konkurrenz zu Ozanimod noch Jahre von der Marktreife entfernt ist.

https://www.sciencedirect.com/science/article/pii/S156899721…

Adam Feuerstein hat sich zu Celgene geäussert - überwiegend "bullish":

Celgene (CELG) delivered a strong first-quarter earnings report Friday and a regulatory update on its delayed multiple sclerosis drug that took the worst-case scenario off the table. The beleaguered biotech hasn’t fixed all its problems quite yet, but Friday’s business update didn’t give investors another reason to hate them, so it feels like a win. Shares of Celgene were up 3 percent to $87.70 in morning trading. As I pointed out earlier this week, Celgene is growing a lot faster than Amgen or Biogen, yet Celgene’s stock had been trading at a super-depressed seven times 2020 earnings. That makes Celgene’s stock cheap compared to the other big-cap biotechs, but only if investors can trust its financial forecasts. Friday’s update on Celgene’s multiple sclerosis drug candidate ozanimod was reassuring on balance. A resubmission to the Food and Drug Administration will take place in the first half of 2019, so the delay stemming from February’s surprising refuse to file letter will be approximately one year. That’s still costly, but the worst-case scenario feared by some analysts — a filing delay of two to three years — won’t happen. Celgene needs the extra time to gather more information for the FDA about the active metabolite of ozanimod, the company said. This metabolite accounts for about 90 percent of the drug’s activity and lasts a long time in the body. But the FDA’s open questions can be answered with nonclinical studies, meaning no new studies in patients will be required, Celgene said. Ozanomid is an important piece of Celgene’s plan to diversify revenue away from its multiple myeloma drug Revlimid, which accounts for 60 percent of the company’s current sales. Generic versions of Revlimid are expected to reach the market in 2022 and beyond. Many of the analyst questions on Friday morning’s conference call were related to ozanimod and its newly discovered metabolite, reflecting the importance of the clinical program to Celgene’s turnaround. For the first quarter, Celgene beat expectations on the top and bottom lines. There were no surprise blowups. Total revenue increased 19 percent to $3.54 billion from the prior year. Revlimid sales were in-line with expectations at $2.23 billion. Sales of Otezla, which treats psoriasis, totaled $453 million, stronger than expectations and easing concerns due to weak sales reported in prior quarters. On an adjusted basis, Celgene earned $2.05 per share, an increase of 23 percent over the prior year, which also included an adjustment for the acquisition of Juno Therapeutics. Celgene also updated 2018 guidance to fully account for the Juno purchase. The forecast for total revenue is now $14.8 billion, which is basically the high end of the previous range. On an adjusted basis, Celgene now expects to earn $8.45 per share in 2018, which is down from the previous range of $8.70-$.8.80 per share. The company also reiterated financial guidance for 2020 — revenue in the $19-20 billion range and adjusted earnings greater than $12.50 per share.

Ozanimod wurde von Celgene durch den Kauf von Receptos für $7.2 Mrd erworben. Es wird nun mit einer Verzögerung von einem Jahr bei der Zulassung gerechnet, da Abklärungen zu den Nebenwirkungen des aktiven Metaboliten erforderlich sind.

Ich bin mir fast sicher, dass ETRASIMOD (von Arena Pharmaceutical) die bessere Variante darstellt, da sowohl die Spezifität an den Rezeptoren als auch die Entstehung von Metaboliten günstiger erscheint. Allerdings wurde mit Etrasimod erst eine ph2-Studie abgeschlossen, weshalb die Konkurrenz zu Ozanimod noch Jahre von der Marktreife entfernt ist.

https://www.sciencedirect.com/science/article/pii/S156899721…

Adam Feuerstein hat sich zu Celgene geäussert - überwiegend "bullish":

Celgene (CELG) delivered a strong first-quarter earnings report Friday and a regulatory update on its delayed multiple sclerosis drug that took the worst-case scenario off the table. The beleaguered biotech hasn’t fixed all its problems quite yet, but Friday’s business update didn’t give investors another reason to hate them, so it feels like a win. Shares of Celgene were up 3 percent to $87.70 in morning trading. As I pointed out earlier this week, Celgene is growing a lot faster than Amgen or Biogen, yet Celgene’s stock had been trading at a super-depressed seven times 2020 earnings. That makes Celgene’s stock cheap compared to the other big-cap biotechs, but only if investors can trust its financial forecasts. Friday’s update on Celgene’s multiple sclerosis drug candidate ozanimod was reassuring on balance. A resubmission to the Food and Drug Administration will take place in the first half of 2019, so the delay stemming from February’s surprising refuse to file letter will be approximately one year. That’s still costly, but the worst-case scenario feared by some analysts — a filing delay of two to three years — won’t happen. Celgene needs the extra time to gather more information for the FDA about the active metabolite of ozanimod, the company said. This metabolite accounts for about 90 percent of the drug’s activity and lasts a long time in the body. But the FDA’s open questions can be answered with nonclinical studies, meaning no new studies in patients will be required, Celgene said. Ozanomid is an important piece of Celgene’s plan to diversify revenue away from its multiple myeloma drug Revlimid, which accounts for 60 percent of the company’s current sales. Generic versions of Revlimid are expected to reach the market in 2022 and beyond. Many of the analyst questions on Friday morning’s conference call were related to ozanimod and its newly discovered metabolite, reflecting the importance of the clinical program to Celgene’s turnaround. For the first quarter, Celgene beat expectations on the top and bottom lines. There were no surprise blowups. Total revenue increased 19 percent to $3.54 billion from the prior year. Revlimid sales were in-line with expectations at $2.23 billion. Sales of Otezla, which treats psoriasis, totaled $453 million, stronger than expectations and easing concerns due to weak sales reported in prior quarters. On an adjusted basis, Celgene earned $2.05 per share, an increase of 23 percent over the prior year, which also included an adjustment for the acquisition of Juno Therapeutics. Celgene also updated 2018 guidance to fully account for the Juno purchase. The forecast for total revenue is now $14.8 billion, which is basically the high end of the previous range. On an adjusted basis, Celgene now expects to earn $8.45 per share in 2018, which is down from the previous range of $8.70-$.8.80 per share. The company also reiterated financial guidance for 2020 — revenue in the $19-20 billion range and adjusted earnings greater than $12.50 per share.

Antwort auf Beitrag Nr.: 57.699.999 von Cyberhexe am 05.05.18 08:36:40interessant:

By James "Rev Shark" DePorre

| May 11, 2018 | 3:20 PM EDT

Stock quotes in this article: arna

President Trump's speech on drug pricing confirms what had been leaked earlier. The main focus of the plan is on increasing competition, squeezing wholesalers, strong disclosures and adjustments in the insurance system. But there are no overt price controls, which has been the big worry in the pharmaceutical and biotechnology sector.

I like the biotechnology group on this news and have been adding a bit to my positions in various names, such as Arena Pharmaceuticals (ARNA) . Most of the charts aren't particular attractive at this point but they should shape up as this worry about prices is finally put to rest…

By James "Rev Shark" DePorre

| May 11, 2018 | 3:20 PM EDT

Stock quotes in this article: arna

President Trump's speech on drug pricing confirms what had been leaked earlier. The main focus of the plan is on increasing competition, squeezing wholesalers, strong disclosures and adjustments in the insurance system. But there are no overt price controls, which has been the big worry in the pharmaceutical and biotechnology sector.

I like the biotechnology group on this news and have been adding a bit to my positions in various names, such as Arena Pharmaceuticals (ARNA) . Most of the charts aren't particular attractive at this point but they should shape up as this worry about prices is finally put to rest…

Antwort auf Beitrag Nr.: 57.744.736 von Cyberhexe am 12.05.18 08:27:56Arena ist derzeit nach Progenics meine "mächtigste" Position im Portfolio!

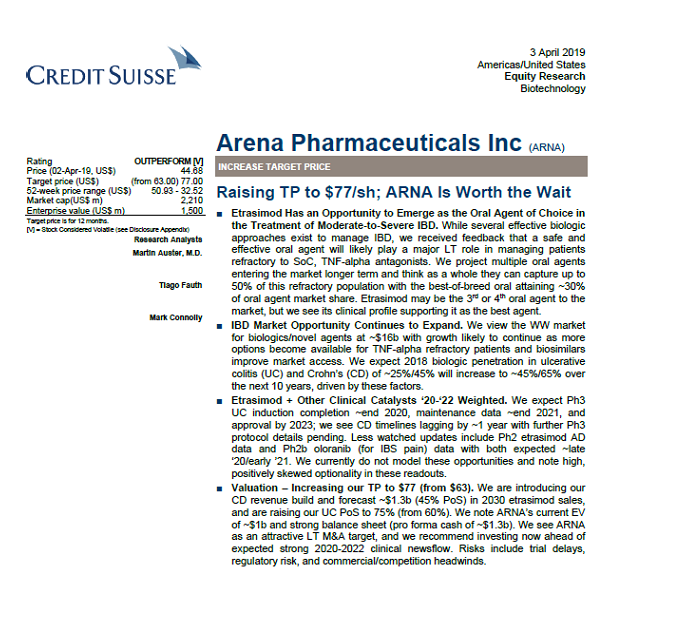

anbei die aktuellen Kursziele der dem Unternehmen folgenden Analysten:

J.P.Morgan Jessica Fye $45

Citi Investment Research Joel Beatty $55

Credit Suisse Martin Auster $58

Needham & Company Alan Carr $60

Wells Fargo Jim Birchenough $60

Leerink Partners Joseph Schwartz $63

Cantor Fitzgerald William Tanner $64

JMP Securities Jason Butler $79

Average Price Target $60.50

anbei die aktuellen Kursziele der dem Unternehmen folgenden Analysten:

J.P.Morgan Jessica Fye $45

Citi Investment Research Joel Beatty $55

Credit Suisse Martin Auster $58

Needham & Company Alan Carr $60

Wells Fargo Jim Birchenough $60

Leerink Partners Joseph Schwartz $63

Cantor Fitzgerald William Tanner $64

JMP Securities Jason Butler $79

Average Price Target $60.50

Antwort auf Beitrag Nr.: 57.744.754 von Cyberhexe am 12.05.18 08:30:47neues bei ETRASIMOD:

Clinical trials update - Extension Study of APD334-003 in Patients With Moderately to Severely Active Ulcerative Colitis

No longer recruiting - Clinical trials update - Extension Study of APD334-003 in Patients With Moderately to Severely Active Ulcerative Colitis

Study Type : Interventional (Clinical Trial)

Actual Enrollment : 118 participants

Allocation: Randomized

Intervention Model: Parallel Assignment

Primary Purpose: Treatment

Official Title: Extension Study of APD334-003 in Patients With Moderately to Severely Active Ulcerative Colitis

Study Start Date : November 2015

Estimated Primary Completion Date : October 12, 2018

Estimated Study Completion Date : October 26, 2018

https://www.clinicaltrials.gov/ct2/show/NCT02536404?term=apd…

Clinical trials update - Extension Study of APD334-003 in Patients With Moderately to Severely Active Ulcerative Colitis

No longer recruiting - Clinical trials update - Extension Study of APD334-003 in Patients With Moderately to Severely Active Ulcerative Colitis

Study Type : Interventional (Clinical Trial)

Actual Enrollment : 118 participants

Allocation: Randomized

Intervention Model: Parallel Assignment

Primary Purpose: Treatment

Official Title: Extension Study of APD334-003 in Patients With Moderately to Severely Active Ulcerative Colitis

Study Start Date : November 2015

Estimated Primary Completion Date : October 12, 2018

Estimated Study Completion Date : October 26, 2018

https://www.clinicaltrials.gov/ct2/show/NCT02536404?term=apd…

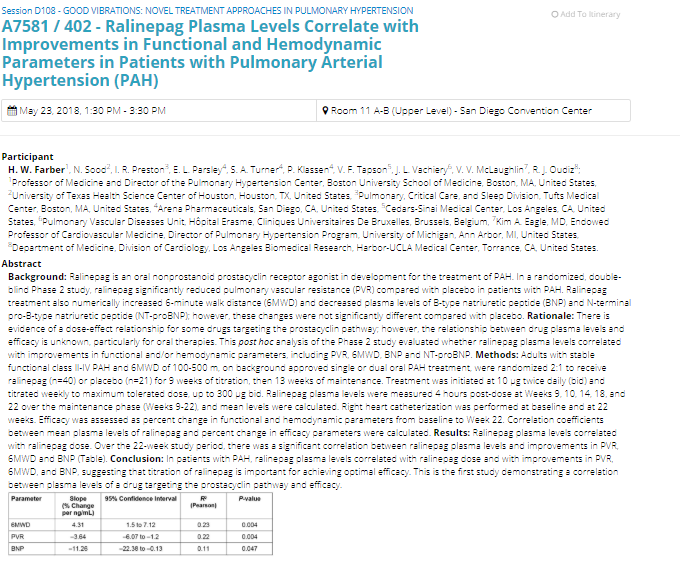

Antwort auf Beitrag Nr.: 57.749.545 von Cyberhexe am 13.05.18 16:28:33Ralinepag Plasma-Level korrelieren mit einer Verbesserung verschiedener Parameter bei PAH - soeben auf ATS2018 in San Diego veröffentlicht:

http://www.abstractsonline.com/pp8/#!/4499/presentation/2059…

http://www.abstractsonline.com/pp8/#!/4499/presentation/2059…

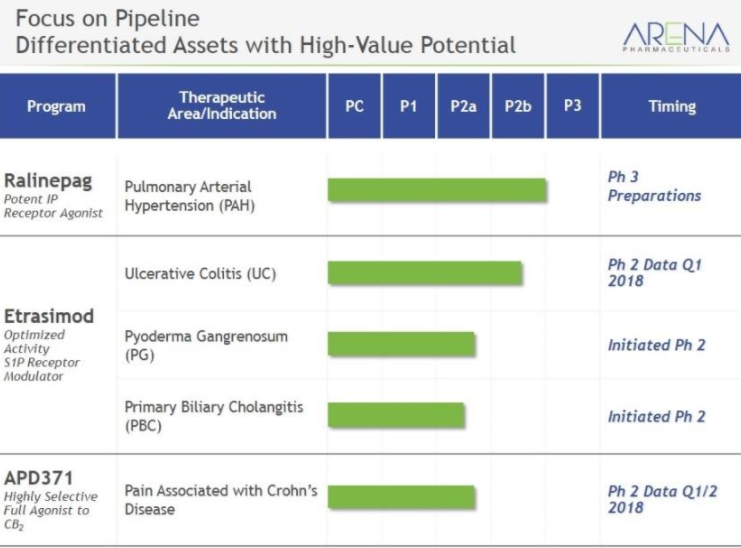

Antwort auf Beitrag Nr.: 57.819.107 von Cyberhexe am 23.05.18 22:41:06diese Pipeline ist ein Versprechen für die Zukunft:

Etrasimod

Ralinepag

Olorinab

Etrasimod

Ralinepag

Olorinab

Antwort auf Beitrag Nr.: 57.823.202 von Cyberhexe am 24.05.18 14:09:26Etrasimod potenter als Ozanimod (CELG hat 7.2 Milliarden$ für die Übernahme von Ozanimod bzw. dessen Lizenzeigner Receptos bezahlt)

Ralinepag potenter als Selexipag (brand: UPTRAVI --> Prognose/Spitzenjahresumsatz > 2Mrd$ )

Ralinepag potenter als Selexipag (brand: UPTRAVI --> Prognose/Spitzenjahresumsatz > 2Mrd$ )

Antwort auf Beitrag Nr.: 57.830.768 von Cyberhexe am 25.05.18 11:11:12Die FDA hat Xeljanz zur Beehandlung von UC zugelassen, allerdings mit einer BlackBox:

WARNING: SERIOUS INFECTIONS AND MALIGNANCY