Marinus Pharmaceuticals - Attraktiver Risk / Reward in - 500 Beiträge pro Seite

eröffnet am 02.08.17 19:23:35 von

neuester Beitrag 17.07.18 21:06:27 von

neuester Beitrag 17.07.18 21:06:27 von

Beiträge: 37

ID: 1.258.569

ID: 1.258.569

Aufrufe heute: 0

Gesamt: 2.632

Gesamt: 2.632

Aktive User: 0

ISIN: US56854Q1013 · WKN: A12CGZ

2,6800

EUR

-2,19 %

-0,0600 EUR

Letzter Kurs 23.09.20 Tradegate

Werte aus der Branche Pharmaindustrie

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 3,5800 | +922,86 | |

| 0,8800 | +95,56 | |

| 2.000,00 | +71,23 | |

| 29,10 | +21,25 | |

| 0,9650 | +14,88 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 9,7200 | -19,60 | |

| 1,5000 | -24,62 | |

| 14,510 | -32,32 | |

| 3,6400 | -38,62 | |

| 0,7000 | -61,85 |

Das Unternehmen beschäftigt sich mit epileptischen und neuropsychiatrischen Krankheitsbildern.

Kürzlich wurde eine P2 Study in PPD (Postpartum Depression) initiiert, deren Erfolgsaussichten ich als hoch bewerte.

Sollte hier ein Wirksamkeitsnachweis gelingen wäre dies sicherlich ein Multibagger, angesichts der gegenwärtigen Bewertung von einem EV in Höhe von ca. 22 Mio USD.

Auch werden in H2 2017 Ergebnisse von SAGE Therapeutics in deren SRSE-Studie erwartet, welche Einfluss auf den shareprice von MRNS haben könnten.

Ist auf das Unternehmen schon jemand anderes aufmerksam geworden? Sehe hier derzeit eine kleine Perle mit einem sehr guten R/R.

Kürzlich wurde eine P2 Study in PPD (Postpartum Depression) initiiert, deren Erfolgsaussichten ich als hoch bewerte.

Sollte hier ein Wirksamkeitsnachweis gelingen wäre dies sicherlich ein Multibagger, angesichts der gegenwärtigen Bewertung von einem EV in Höhe von ca. 22 Mio USD.

Auch werden in H2 2017 Ergebnisse von SAGE Therapeutics in deren SRSE-Studie erwartet, welche Einfluss auf den shareprice von MRNS haben könnten.

Ist auf das Unternehmen schon jemand anderes aufmerksam geworden? Sehe hier derzeit eine kleine Perle mit einem sehr guten R/R.

Antwort auf Beitrag Nr.: 55.446.018 von biopadawan am 02.08.17 19:23:35Hallo biopadawan,

in der Tat hast du eine vom R/R sehr interessante Aktie aufgetan. Ich wusste noch gar nicht, dass die Studie in PPD schon gestartet ist. Sehr schön!

https://clinicaltrials.gov/ct2/show/NCT03228394?term=ganaxol…

Ich bin hier auch investiert (leider schon länger). Die Story hier ist m.E. die niedrige Bewertung im Vergleich mit SAGE. 40 Mio vs. 3000 Mio.

Im nächsten halben Jahr steht hier einiges an. Besonders auf die Ergebnisse von SAGE in super refractory status epilepticus und postpartum depression bin ich gespannt. In SAGE bin ich übrigens auch investiert.

Ich finde die Ergebnisse von SAGE in PPD sehr gut. Für mich eines der wenigen Medikamente in der Entwicklung, die das Potenzial haben, die Behandlung auf eine völlig neue Stufe zu bringen.

Zu den Aussichten in SRSE/PPD:

MRNS macht m.E. das Richtige. Sie kopieren SAGE. Von daher wird MRNS stark auf die Ergebnisse von SAGE reagieren.

Ob MRNS selber jemals ein Produkt auf den Markt bringt - da bin ich mir nicht so sicher. Bisher waren die Ergebnisse von ganaxolone enttäuschend. Die gestartete P2 in PPD benutzt nun aber die IV Version und nicht mehr die Tablette. Es gab wohl auch Probleme mit der Formulierung der Tablette (Bioverfügbarkeit). Von daher könnte es mit der IV Version eine positive Überraschung geben. Kleiner Insider: Beide IV Versionen SAGE547 und auch ganaxolone IV sind mit Captisol von LGND formuliert. Auch hier hat MRNS im Grunde SAGE kopiert. LGND bekäme von beiden niedrige einstellige Roylties.

in der Tat hast du eine vom R/R sehr interessante Aktie aufgetan. Ich wusste noch gar nicht, dass die Studie in PPD schon gestartet ist. Sehr schön!

https://clinicaltrials.gov/ct2/show/NCT03228394?term=ganaxol…

Ich bin hier auch investiert (leider schon länger). Die Story hier ist m.E. die niedrige Bewertung im Vergleich mit SAGE. 40 Mio vs. 3000 Mio.

Im nächsten halben Jahr steht hier einiges an. Besonders auf die Ergebnisse von SAGE in super refractory status epilepticus und postpartum depression bin ich gespannt. In SAGE bin ich übrigens auch investiert.

Ich finde die Ergebnisse von SAGE in PPD sehr gut. Für mich eines der wenigen Medikamente in der Entwicklung, die das Potenzial haben, die Behandlung auf eine völlig neue Stufe zu bringen.

Zu den Aussichten in SRSE/PPD:

MRNS macht m.E. das Richtige. Sie kopieren SAGE. Von daher wird MRNS stark auf die Ergebnisse von SAGE reagieren.

Ob MRNS selber jemals ein Produkt auf den Markt bringt - da bin ich mir nicht so sicher. Bisher waren die Ergebnisse von ganaxolone enttäuschend. Die gestartete P2 in PPD benutzt nun aber die IV Version und nicht mehr die Tablette. Es gab wohl auch Probleme mit der Formulierung der Tablette (Bioverfügbarkeit). Von daher könnte es mit der IV Version eine positive Überraschung geben. Kleiner Insider: Beide IV Versionen SAGE547 und auch ganaxolone IV sind mit Captisol von LGND formuliert. Auch hier hat MRNS im Grunde SAGE kopiert. LGND bekäme von beiden niedrige einstellige Roylties.

Hallo!

Ich habe auch einige MRNS und bin durch den nachkauf für 1 Euro auch fast wieder im Plus.

Schöne Zusammenfassung von kmastra!

Ich habe auch einige MRNS und bin durch den nachkauf für 1 Euro auch fast wieder im Plus.

Schöne Zusammenfassung von kmastra!

Danke Schnappi!

Nicht vernachlässigen würde ich auch die Ergebnisse von SAGE217 (Tablette) bei major depressive disorder(13 Patienten, open label):

The trial also examined the effect of SAGE-217 on the Hamilton Rating Scale for Depression (HAM-D) total score, in addition to other secondary measures. Patients in the trial had a mean HAM-D total score of 27.2 at baseline. Data demonstrated a mean reduction from baseline in the HAM-D of 19.9 points at Day 15, with 85% (11 of 13) patients showing at least a 50% reduction of their HAM-D and 62% (8 of 13) of patients achieving remission, as determined by a HAM-D ≤7. Statistically significant mean change from baseline was observed by Day 2 of the study, following the first of once-daily, nighttime oral dosing of 30 mg of SAGE-217. A significant mean change from baseline was maintained throughout the treatment period (p < 0.0001 at Day 15).

Die Ergebnisse scheinen vergleichbar mit denen von 547 bei PPD.

Das wäre für SAGE und somit potenziell für MRNS nochmal ein richtig großer Markt. Auch hier soll es noch im 2. HJ Ergebnisse der plazebo kontrollierten Studie geben. Ganz schön was los bei SAGE:

Für MRNS ist es natürlich sehr praktisch, dass SAGE so viele proof of concept Studien macht.

Bei MRNS selber ist ja nicht so viel los. Da hängt erst mal alles von SAGE ab. Von den pediatric orphan Programmen erwarte ich nicht viel. Die P2 Ergebnisse bei PPD kommen sicher nicht vor 2018. Wurde da schon mal was kommuniziert?

Nicht vernachlässigen würde ich auch die Ergebnisse von SAGE217 (Tablette) bei major depressive disorder(13 Patienten, open label):

The trial also examined the effect of SAGE-217 on the Hamilton Rating Scale for Depression (HAM-D) total score, in addition to other secondary measures. Patients in the trial had a mean HAM-D total score of 27.2 at baseline. Data demonstrated a mean reduction from baseline in the HAM-D of 19.9 points at Day 15, with 85% (11 of 13) patients showing at least a 50% reduction of their HAM-D and 62% (8 of 13) of patients achieving remission, as determined by a HAM-D ≤7. Statistically significant mean change from baseline was observed by Day 2 of the study, following the first of once-daily, nighttime oral dosing of 30 mg of SAGE-217. A significant mean change from baseline was maintained throughout the treatment period (p < 0.0001 at Day 15).

Die Ergebnisse scheinen vergleichbar mit denen von 547 bei PPD.

Das wäre für SAGE und somit potenziell für MRNS nochmal ein richtig großer Markt. Auch hier soll es noch im 2. HJ Ergebnisse der plazebo kontrollierten Studie geben. Ganz schön was los bei SAGE:

Für MRNS ist es natürlich sehr praktisch, dass SAGE so viele proof of concept Studien macht.

Bei MRNS selber ist ja nicht so viel los. Da hängt erst mal alles von SAGE ab. Von den pediatric orphan Programmen erwarte ich nicht viel. Die P2 Ergebnisse bei PPD kommen sicher nicht vor 2018. Wurde da schon mal was kommuniziert?

Die Ergebnisse der P3 in SRSE werden demnächst kommen. Die Rekrutierung ist abgeschlossen. Ein schöner Ausblick:

Upcoming events – Sage and Ablynx look to their lead assets

Date August 11, 2017

Welcome to your weekly digest of approaching regulatory and clinical readouts. Sage Therapeutics has a busy year ahead, with three phase III readouts of its lead asset, Sage-547, one of which will be its first placebo-controlled test in a rare form of epilepsy.

Meanwhile, Ablynx is due to report phase III results for caplacizumab in a rare blood-clotting disorder. This is the company’s most advanced project, and has already been filed in the EU on the back of phase II data.

Sage’s catalysts

Sage-547 (brexanolone) is an intravenous formulation of allopregnanolone, a neuroactive steroid that acts as a GABA-A receptor modulator.

Three phase III datasets are due shortly. The first will come from its super-refractory status epilepticus (SRSE) trial, expected within the next two months, while results in severe and moderate postpartum depression are due later in the year.

SRSE consists of persistent, unremitting seizures that do not respond to benzodiazepines or second-line anti-seizure drugs. Patients are typically placed into a medically induced coma and given high-dose general anaesthetics, with an attempt then made every 24-72 hours to wean them off these.

In the Status trial 126 patients were randomised to receive either Sage-547 or placebo in addition to standard-of-care third-line anti-seizure agents for six days. The primary outcome is the number of patients who can be weaned off third-line agents before the end of the Sage-547 or placebo infusion and remain off all third-line agents for over 24 hours thereafter.

In a phase I/II open-label study of 22 evaluable patients, 73% were successfully weaned off anaesthetic agents and Sage-547 within five days of starting treatment, and 82% within six days, without the need to reinstate anaesthetics in the following 24 hours (Upcoming events – Shire in Sanfilippo A while Sage looks to its lead asset, April 26, 2016).

One big unknown is the response rate of the placebo arm; many CNS trials are scuppered by high placebo responses, and Stifel analysts have estimated that a rate of around 35% would only require around 52% in the active treatment arm to reach statistical significance, so a repeat of the earlier trial would be a bonus.

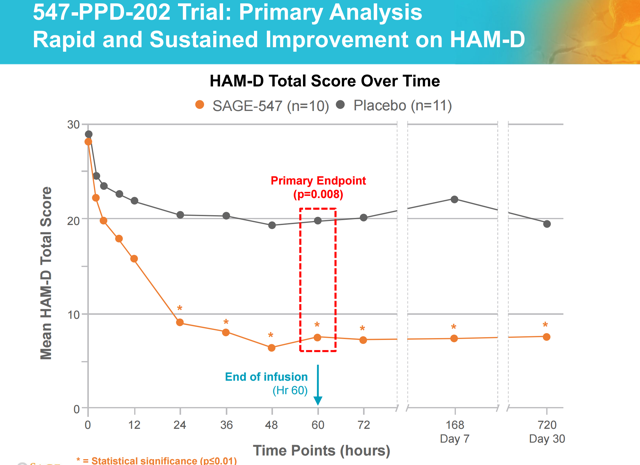

The same project is in two postpartum depression trials, known collectively as Hummingbird. One has recruited 120 patients with severe depression and the other 100 with moderate depression. The primary endpoint is the effect of Sage-547 on depressive symptoms versus placebo as measured on the Hamilton Rating Scale for Depression total score at three days.

Results from a small phase II trial caused shares to jump 35% last July (Post-partum depression data spice Sage trading, July 12, 2016). Revenue forecasts for Sage-457 sit at $962m by 2022, according to sellside consensus from EvaluatePharma, with 83% of sales are assigned to the epilepsy indication. It has an NPV of $2bn, or 66% of the company’s market cap.

Earlier this year the company had to play down rumours of a buyout after its chief executive fuelled speculation in a media interview. Still, this might become reality before the year is out if the data look good.

http://www.epvantage.com/Universal/View.aspx?type=Story&id=7…" target="_blank" rel="nofollow ugc noopener">http://www.epvantage.com/Universal/View.aspx?type=Story&id=7…

Die Bedeutung der Ergebnisse wird hier m.E. aber verzehrt dargestellt. Die Ergebnisse in PPD und auch die P2 in MDD halte ich für wichtiger.

MRNS will tatsächlich auch dieses Jahr noch Ergebnisse in PPD bringen.

Upcoming events – Sage and Ablynx look to their lead assets

Date August 11, 2017

Welcome to your weekly digest of approaching regulatory and clinical readouts. Sage Therapeutics has a busy year ahead, with three phase III readouts of its lead asset, Sage-547, one of which will be its first placebo-controlled test in a rare form of epilepsy.

Meanwhile, Ablynx is due to report phase III results for caplacizumab in a rare blood-clotting disorder. This is the company’s most advanced project, and has already been filed in the EU on the back of phase II data.

Sage’s catalysts

Sage-547 (brexanolone) is an intravenous formulation of allopregnanolone, a neuroactive steroid that acts as a GABA-A receptor modulator.

Three phase III datasets are due shortly. The first will come from its super-refractory status epilepticus (SRSE) trial, expected within the next two months, while results in severe and moderate postpartum depression are due later in the year.

SRSE consists of persistent, unremitting seizures that do not respond to benzodiazepines or second-line anti-seizure drugs. Patients are typically placed into a medically induced coma and given high-dose general anaesthetics, with an attempt then made every 24-72 hours to wean them off these.

In the Status trial 126 patients were randomised to receive either Sage-547 or placebo in addition to standard-of-care third-line anti-seizure agents for six days. The primary outcome is the number of patients who can be weaned off third-line agents before the end of the Sage-547 or placebo infusion and remain off all third-line agents for over 24 hours thereafter.

In a phase I/II open-label study of 22 evaluable patients, 73% were successfully weaned off anaesthetic agents and Sage-547 within five days of starting treatment, and 82% within six days, without the need to reinstate anaesthetics in the following 24 hours (Upcoming events – Shire in Sanfilippo A while Sage looks to its lead asset, April 26, 2016).

One big unknown is the response rate of the placebo arm; many CNS trials are scuppered by high placebo responses, and Stifel analysts have estimated that a rate of around 35% would only require around 52% in the active treatment arm to reach statistical significance, so a repeat of the earlier trial would be a bonus.

The same project is in two postpartum depression trials, known collectively as Hummingbird. One has recruited 120 patients with severe depression and the other 100 with moderate depression. The primary endpoint is the effect of Sage-547 on depressive symptoms versus placebo as measured on the Hamilton Rating Scale for Depression total score at three days.

Results from a small phase II trial caused shares to jump 35% last July (Post-partum depression data spice Sage trading, July 12, 2016). Revenue forecasts for Sage-457 sit at $962m by 2022, according to sellside consensus from EvaluatePharma, with 83% of sales are assigned to the epilepsy indication. It has an NPV of $2bn, or 66% of the company’s market cap.

Earlier this year the company had to play down rumours of a buyout after its chief executive fuelled speculation in a media interview. Still, this might become reality before the year is out if the data look good.

http://www.epvantage.com/Universal/View.aspx?type=Story&id=7…" target="_blank" rel="nofollow ugc noopener">http://www.epvantage.com/Universal/View.aspx?type=Story&id=7…

Die Bedeutung der Ergebnisse wird hier m.E. aber verzehrt dargestellt. Die Ergebnisse in PPD und auch die P2 in MDD halte ich für wichtiger.

MRNS will tatsächlich auch dieses Jahr noch Ergebnisse in PPD bringen.

Trading Spotlight

Charttechnisch wäre ein nachhaltiges Überwinden von 3$ wünschenswert. Dann wären sogar Kurse von 5-6$ drin!

Antwort auf Beitrag Nr.: 55.546.233 von kmastra am 17.08.17 18:52:01Das ging jetzt schnell! Heute in der Spitze +50% nach erfreulichen Studienergebnissen:

https://finance.yahoo.com/news/marinus-announces-successful-…

https://finance.yahoo.com/news/marinus-announces-successful-…

Antwort auf Beitrag Nr.: 55.714.953 von kmastra am 11.09.17 16:44:14Ja sehr schön

Antwort auf Beitrag Nr.: 55.714.953 von kmastra am 11.09.17 16:44:14Hier könnte dann auch die nächste KE anstehen.

Heute die P3 Ergebnisse von SAGE bei SRSE: Ein überraschend deutlicher Flop! Mal sehen was die Märkte heute draus machen...

https://endpts.com/sages-quick-flip-into-phiii-crashes-as-le…

https://endpts.com/sages-quick-flip-into-phiii-crashes-as-le…

Antwort auf Beitrag Nr.: 55.722.303 von kmastra am 12.09.17 13:04:46Habe es gerade auch gesehen habe keine $SAGE Aktien im Depot bin gespannt wie $MRNS darauf reagiert.

$MRNS: Marinus Pharmaceuticals (MRNS) PT Raised to $11 at JMP Securities

Also ich muss schon zugeben, dass ich nach dem SRSE Fail mit einer heftigeren Reaktion sowohl bei SAGE als auch bei MRNS gerechnet hätte.

Für MRNS ist zumindest die angedachte eigene Studie bei SRSE jetzt stark in Frage gestellt.

Für SAGE ist die Studie natürlich ein herber Rückschlag. Die P3 bei PPD muss jetzt zünden. Floppt auch die bricht im Grunde genommen alles zusammen, denn dann wären auch die guten Ergebnisse bei MDD nichts Wert...

Für MRNS ist zumindest die angedachte eigene Studie bei SRSE jetzt stark in Frage gestellt.

Für SAGE ist die Studie natürlich ein herber Rückschlag. Die P3 bei PPD muss jetzt zünden. Floppt auch die bricht im Grunde genommen alles zusammen, denn dann wären auch die guten Ergebnisse bei MDD nichts Wert...

Antwort auf Beitrag Nr.: 55.732.041 von kmastra am 13.09.17 13:36:19MRNS nutzt auf jeden Fall jetzt die Gelegenheit, um sich Geld zu beschaffen:

https://finance.yahoo.com/news/marinus-pharmaceuticals-annou…

https://finance.yahoo.com/news/marinus-pharmaceuticals-annou…

Antwort auf Beitrag Nr.: 55.716.132 von schnappi am 11.09.17 18:32:14RADNOR, Pa., Sept. 15, 2017 (GLOBE NEWSWIRE) -- Marinus Pharmaceuticals, Inc. (Nasdaq:MRNS) (“Marinus” or the “Company”) announced the pricing of an underwritten public offering of 9,333,334 shares of common stock for a public offering price of $3.75 per share. The gross proceeds from the offering are expected to be $35 million, before deducting underwriting discounts and commissions and estimated offering expenses payable by the Company. The Company has granted the underwriter a 30-day option to purchase up to an additional 1,400,000 shares of common stock. The offering is expected to close on or about September 19, 2017, subject to customary closing conditions.

Antwort auf Beitrag Nr.: 55.751.862 von schnappi am 15.09.17 13:39:35Ich finde die 3,75$ sind Okay hätte können schlimmer kommen.

Antwort auf Beitrag Nr.: 55.546.233 von kmastra am 17.08.17 18:52:01Das macht mal Laune die letzten Tage.

Präsentation bei Cantor Fitzgerald wohl auch gut angekommen heute.

Präsentation bei Cantor Fitzgerald wohl auch gut angekommen heute.

Antwort auf Beitrag Nr.: 55.837.140 von schnappi am 27.09.17 20:02:58Ja, Wahnsinn!! MRNS/SAGE ist ein echter Krimi! Wie gesagt hätte ich nach dem srse fail von SAGE mit einer anderen Marktreaktion gerechnet, aber ich will mich da nicht groß beschweren...

Neben der Präsentation könnte MRNS heute auch von einem Analystenkommentar profitieren, der MRNS als Übernahmekandidaten ins Spiel bringt.

Neben der Präsentation könnte MRNS heute auch von einem Analystenkommentar profitieren, der MRNS als Übernahmekandidaten ins Spiel bringt.

Sie rennt und rennt

Die beiden mal im Vergleich

Antwort auf Beitrag Nr.: 55.892.956 von schnappi am 06.10.17 09:52:39Von der Marktkapitalisierung aus gesehen,

liegen noch Welten dazwischen,

ich denke hier dürfte es auch einige neue Kurziele demnächst geben.

liegen noch Welten dazwischen,

ich denke hier dürfte es auch einige neue Kurziele demnächst geben.

Nach oben korrigierte meinst du?

Bei beiden PPD Studien von Sage ist mittlerweile die Rekrutierung abgeschlossen.

https://clinicaltrials.gov/ct2/show/NCT02942017?term=sage&ph…

https://clinicaltrials.gov/ct2/show/NCT02942004?term=sage&ph…

Die Studien müssen jetzt natürlich noch zu Ende geführt und ausgewertet werden. Daten sollten aber definitiv noch in diesem Jahr kommen. Sage hat bisher immer offen gehalten, ob sie erst die eine und dann die andere oder beide gleichzeitig veröffentlichen werden. Ich rechne eher damit, dass sie beide auf einmal veröffentlichen. (Das scheint mir weniger riskant.)

Die erste Studie von MRNS in PPD (severe) soll ja auch noch in diesem Jahr erste Ergebnisse bringen. Hier ist das Timing sehr schwer vorhersehbar, da zunächst nur die Ergebnisse der ersten Gruppe veröffentlicht werden. Theoretisch könnte dies sogar noch vor den SAGE Ergebnissen sein. (Das ist m.E. aber nicht unbedingt wünschenswert.)

Man muss kein Prophet sein, um vorherzusagen, dass die Ergebnisse große Kursbewegungen bei beiden Werten mit sich bringen dürften. Bei MRNS ist die Lage besonders spannend, weil einerseits viele Institutionelle Anleger in den letzten Monaten große Aktienpakete gekauft haben und andererseits doch noch viele short sind. Geht man davon aus, dass die Instis starke Hände haben, wird es ggf. schwer für die Shorts ihre Positionen aufzulösen.

Aber auch bei SAGE ist die Lage spannend, weil die P2 Ergebnisse so gut waren, dass bei einem Scheitern im Grunde alles zusammenbricht (-90% würden mich dann nicht wundern) anderseits bei guten Ergebnissen nacht dem Scheitern in SRSE und dem Rückgang jetzt aber auch viel Potenzial nach Oben wäre (100% würden mich nicht wundern)

In Anbetracht der jüngsten Ereignisse maße ich mir aber nicht an, die Marktreaktion vorherzusehen. Ich habe bei beiden Werten jetzt meine Positionsgröße erreicht, mit der ich in den Readout gehen werde und bin gespannt!

https://clinicaltrials.gov/ct2/show/NCT02942017?term=sage&ph…

https://clinicaltrials.gov/ct2/show/NCT02942004?term=sage&ph…

Die Studien müssen jetzt natürlich noch zu Ende geführt und ausgewertet werden. Daten sollten aber definitiv noch in diesem Jahr kommen. Sage hat bisher immer offen gehalten, ob sie erst die eine und dann die andere oder beide gleichzeitig veröffentlichen werden. Ich rechne eher damit, dass sie beide auf einmal veröffentlichen. (Das scheint mir weniger riskant.)

Die erste Studie von MRNS in PPD (severe) soll ja auch noch in diesem Jahr erste Ergebnisse bringen. Hier ist das Timing sehr schwer vorhersehbar, da zunächst nur die Ergebnisse der ersten Gruppe veröffentlicht werden. Theoretisch könnte dies sogar noch vor den SAGE Ergebnissen sein. (Das ist m.E. aber nicht unbedingt wünschenswert.)

Man muss kein Prophet sein, um vorherzusagen, dass die Ergebnisse große Kursbewegungen bei beiden Werten mit sich bringen dürften. Bei MRNS ist die Lage besonders spannend, weil einerseits viele Institutionelle Anleger in den letzten Monaten große Aktienpakete gekauft haben und andererseits doch noch viele short sind. Geht man davon aus, dass die Instis starke Hände haben, wird es ggf. schwer für die Shorts ihre Positionen aufzulösen.

Aber auch bei SAGE ist die Lage spannend, weil die P2 Ergebnisse so gut waren, dass bei einem Scheitern im Grunde alles zusammenbricht (-90% würden mich dann nicht wundern) anderseits bei guten Ergebnissen nacht dem Scheitern in SRSE und dem Rückgang jetzt aber auch viel Potenzial nach Oben wäre (100% würden mich nicht wundern)

In Anbetracht der jüngsten Ereignisse maße ich mir aber nicht an, die Marktreaktion vorherzusehen. Ich habe bei beiden Werten jetzt meine Positionsgröße erreicht, mit der ich in den Readout gehen werde und bin gespannt!

Antwort auf Beitrag Nr.: 56.000.967 von kmastra am 22.10.17 13:06:53PPD Ergebnisse von MRNS kommen jetzt erst Anfang 2018 also definitiv nach denen von Sage.

https://finance.yahoo.com/news/marinus-pharmaceuticals-provi…

Bei Sage sollen neben den PPD Daten ja zudem noch weitere Ergebnisse kommen. MRNS kann sich das Ganze entspannt von der Seitenlinie anschauen.

https://finance.yahoo.com/news/marinus-pharmaceuticals-provi…

Bei Sage sollen neben den PPD Daten ja zudem noch weitere Ergebnisse kommen. MRNS kann sich das Ganze entspannt von der Seitenlinie anschauen.

Ich bin im Oktober raus und habe die Gewinne mal mitgenommen.

Nun zapfen sie den Markt ja wieder an $200M ich bleib mal an der Seitenlinie.

Nun zapfen sie den Markt ja wieder an $200M ich bleib mal an der Seitenlinie.

Antwort auf Beitrag Nr.: 56.070.680 von schnappi am 01.11.17 10:26:20Ich bin hier noch mit 1/5 meiner ursprünglichen Position dabei. Damit gehe ich dann aber auch in die Readouts. Eine Position wie MRNS möchte ich grundsätzlich nicht zu groß werden lassen...

JPM $SAGE Highlights from Our Management Conference Call

On Thursday, as part of our 2017 Fall Biotech Conference Call Series, we hosted a call with SAGE’s CEO JeffJonas, CMO Steve Kanes, and CFO Kimi Iguchi. The discussions covered all aspects of SAGE’s clinical programs including learnings from SRSE, expectations and available data for PPD/MDD as well as plans for the earlier stage pipeline. Below we provide some highlights from the call (we will also send around the transcript once available). A replay is available through 10/12 with the following dial-in info: 866-442-2107 (US); +1-203-369-1083 (outside US); Passcode: 10517

On SRSE...

Despite the obvious disappointment around the recent failure of the Phase 3 STATUS trial, management believes it was the right study at the right time. They learned quite a bit more about GABA, and importantly, there were no new safety signals in this larger group of patients. SAGE is currently analyzing the data regarding the “biologically relevant subgroup” where there was reportedly activity as discussed on the Sept conf call. Whatever the outcome, it sounds like another trial in SRSE is unlikely. Management stated that the story might be different if they were a one drug one indication company. However with multiple indications and products now in their portfolio, an assessment of feasibility and opportunity would likely place SRSE pretty far down on the ladder. Failure in SRSE further reinforces SAGE’s strategy of proceeding from open label pilot studies to randomized Phase 2s. In fact, STATUS could have probably been a Phase 2 study but was rather granted Phase 3 status. The company feels that this process will allow them to avoid spending undue time and resources on programs that ultimately will not pan out.

Read through from SRSE to PPD should be quite limited in the eyes of management. In fact they view a comparison as apples and oranges. Perhaps most notably, the quality and robustness of the PPD data far outstrips what was available for SRSE given that there is published randomized data (which was also scrutinized by the FDA/EMA for the BTD/PRIME designation) in this indication. Additionally, PPD is thought to be a distinct disease rather than the final common pathway of a series of heterogenous disorders as with SRSE (where pts are extremely ill and on many medications).

On PPD...

SAGE is currently on track to release data for all the PPD trials and the Phase 2 MDD trial this quarter. Management believes that the data so far is compelling not only for the fact that it was randomized and peer reviewed but that the onset/efficacy/duration of the effect seen was extremely different from anything else in the world of psychiatry. To put things into perspective, much smaller deltas than what was seen for 547 have historically led to later stage trials. Recall that a 70% remission rate was seen at 60hrs which was durable out to at least 30 days. The company believes there were no significant imbalances between the experimental and control groups in the PPD Lancet publication. Though the presence or absence of underlying treatments was not actively selected for, this metric was also well balanced between the two groups. The design of the Phase 3 HUMMINGBIRD trials are almost identical to the Phase 2 trial but on a larger scale. The major difference of course is that 202b includes only severe patients while 202c includes moderate patients (as assessed by HAM-D score). 202b also includes two different dose levels as an initial step towards investigating alternative dosing schedules. The primary endpoints for the two trials will be assessed independently, and thus the threshold for statistical significance for both trials is 0.05.

In discussing commercial relevance the company pointed to the 12 point placebo adjusted difference in HAMD seen with brexanolone, which is substantially greater than what is seen with SSRIs. This, in conjunction with the extended duration of effect may potentially allow for a fast acting treatment with sporadic dosing vs chronic therapy with SSRIs (6 months – 1 year). In regards to the separate trials for moderate and severe patients, management believes that a common strategy for obtaining a broad label is to have two trials with slightly different enrollment criteria. The HAM-D cutoffs used are purely for regulatory purposes and have very little bearing on how depression is managed in the clinic. Moreover, there is currently no evidence to suggest that baseline severity should impact treatment effect.

The company currently believes that 10-20% of mothers experience PPD in some form with 70% of them being moderate-severe. This number could be materially higher but due to the stigma of the disease, there may be a negative ascertainment bias and under-diagnosis. SAGE views PPD as a medical condition as much as it is a psychiatric condition (“biologic complication of

pregnancy”) and a leading cause of maternal death. As such, the company believes that there should be a range of physicians who have access to 547 in the course of caring for patients (e.g. ob/gyns and family doctors). The company is therefore engaged in commercial readiness planning and disease awareness programs. The drug itself is a simple IV injection, which can be done through a peripheral IV and does not require special training. In terms of launch preparation, the company is putting together sales forces for both hospitals and specialty pharmacies (though the actual numbers have not yet been disclosed). Manufacturing capacity and supply chain are similarly being prepped for a potential launch.

In regards to pricing, SRSE was the previous anchor (recall the company had guided to a range of $25-75k per patient treated). The company is currently in the process of doing additional work with payers now that the likely first indication will be PPD. How these discussions ultimately shake out will depend on the effect size and flexibility in terms of how the drug is administered. The company continues to believe that they could be viewed as a differentiated therapeutic intervention.

In regards to the Phase 2 SAGE-217 in PPD, the company disclosed that patients were preferentially being placed onto the HUMMINGBIRD trials for obvious reasons. However, the timing for topline data remains intact. The intent for SAGE-547 was always to establish a commercial footprint for 217, which will come several years later. In terms of co-existence, the company believes this commercial footprint and the presence of two potentially complimentary assets in the same space is a good problem to have.

On MDD...

The company concedes that data so far has been open label and thus are subject to the obvious caveats of such studies. Nevertheless, the objective of the Phase 1 was always hypothesis and methodology generation in preparation for randomized trials. With that said the reduction in HAM-D total scores of 20 pts was quite striking when compared with approved treatments (typical range of 5-10 points on the same time scale). Patients included in the open label portion were standard MDD patients who had severe symptoms at the time of enrollment. Concomitant treatment with another drug was allowed (1/3 of patients). The company stressed that these patients would not be considered treatment refractory.

As an aside, management believes that depression trials which choose to specifically target refractory patients are doing so on the premise that those patients who have failed multiple therapies have a distinct subtype of the disease (which is an unproven hypothesis). This attempt to homogenize the patient population may not ultimately be the correct path to take. The company stated the Phase 2 will give greater clarity in regards to endpoints and powering for the potential pivotal trial. For example, with enough remissions the next trial could be powered for an endpoint of remissions rather than HAM-D reduction. Overall the company believes that if the results of the open label can be carried forwards into larger patient populations, this would be a paradigm shifting event in the sense that this would represent the ability to treat a psychiatric disorder in the acute setting without the side effects seen with current standard of care.

Other pipeline programs/updates...

The rationale for pursuing movement disorders is built on the premise that an imbalance of GABAergic tone mediated through various pathways (management emphasized that these diseases are different but share this common feature) result in the neuromuscular manifestations of diseases such as ET and Parkinson’s. For example, known GAGA agonists such as alcohol can transiently cause ET symptoms to abate, though this response rapidly diminishes over time due to, presumably, a down-regulation of synaptic GABA receptors (SAGE acts on extra synaptic receptors which do not down-regulate).

In regards to the recently initiated sleep study for SAGE-217 in healthy volunteers, the company is trying to confirm the sleep signal they saw in their other studies in a systemic fashion. Patients are being looked at in a standard sleep label, potentially at higher doses than the 30mg used in MDD. Metrics such as sleep quality and next morning performance will be evaluated.

The NMDA SAD study in healthy volunteers is on track to read out this quarter as well.

https://www.investorvillage.com/smbd.asp?mb=17990&mn=225&pt=…

Interessant finde ich, dass MRNS laut Quartalsbericht an der P2 zu SRSE festhält. Sie wollen dies ja auch in einem gänzlich anderen Setting tun (bevor Patienten in ein Koma versetzt werden) und könnten zudem von der genaueren Analyse der gescheiterten SAGE Studie profitieren z.B. bei der Teilnehmerauswahl.

On Thursday, as part of our 2017 Fall Biotech Conference Call Series, we hosted a call with SAGE’s CEO JeffJonas, CMO Steve Kanes, and CFO Kimi Iguchi. The discussions covered all aspects of SAGE’s clinical programs including learnings from SRSE, expectations and available data for PPD/MDD as well as plans for the earlier stage pipeline. Below we provide some highlights from the call (we will also send around the transcript once available). A replay is available through 10/12 with the following dial-in info: 866-442-2107 (US); +1-203-369-1083 (outside US); Passcode: 10517

On SRSE...

Despite the obvious disappointment around the recent failure of the Phase 3 STATUS trial, management believes it was the right study at the right time. They learned quite a bit more about GABA, and importantly, there were no new safety signals in this larger group of patients. SAGE is currently analyzing the data regarding the “biologically relevant subgroup” where there was reportedly activity as discussed on the Sept conf call. Whatever the outcome, it sounds like another trial in SRSE is unlikely. Management stated that the story might be different if they were a one drug one indication company. However with multiple indications and products now in their portfolio, an assessment of feasibility and opportunity would likely place SRSE pretty far down on the ladder. Failure in SRSE further reinforces SAGE’s strategy of proceeding from open label pilot studies to randomized Phase 2s. In fact, STATUS could have probably been a Phase 2 study but was rather granted Phase 3 status. The company feels that this process will allow them to avoid spending undue time and resources on programs that ultimately will not pan out.

Read through from SRSE to PPD should be quite limited in the eyes of management. In fact they view a comparison as apples and oranges. Perhaps most notably, the quality and robustness of the PPD data far outstrips what was available for SRSE given that there is published randomized data (which was also scrutinized by the FDA/EMA for the BTD/PRIME designation) in this indication. Additionally, PPD is thought to be a distinct disease rather than the final common pathway of a series of heterogenous disorders as with SRSE (where pts are extremely ill and on many medications).

On PPD...

SAGE is currently on track to release data for all the PPD trials and the Phase 2 MDD trial this quarter. Management believes that the data so far is compelling not only for the fact that it was randomized and peer reviewed but that the onset/efficacy/duration of the effect seen was extremely different from anything else in the world of psychiatry. To put things into perspective, much smaller deltas than what was seen for 547 have historically led to later stage trials. Recall that a 70% remission rate was seen at 60hrs which was durable out to at least 30 days. The company believes there were no significant imbalances between the experimental and control groups in the PPD Lancet publication. Though the presence or absence of underlying treatments was not actively selected for, this metric was also well balanced between the two groups. The design of the Phase 3 HUMMINGBIRD trials are almost identical to the Phase 2 trial but on a larger scale. The major difference of course is that 202b includes only severe patients while 202c includes moderate patients (as assessed by HAM-D score). 202b also includes two different dose levels as an initial step towards investigating alternative dosing schedules. The primary endpoints for the two trials will be assessed independently, and thus the threshold for statistical significance for both trials is 0.05.

In discussing commercial relevance the company pointed to the 12 point placebo adjusted difference in HAMD seen with brexanolone, which is substantially greater than what is seen with SSRIs. This, in conjunction with the extended duration of effect may potentially allow for a fast acting treatment with sporadic dosing vs chronic therapy with SSRIs (6 months – 1 year). In regards to the separate trials for moderate and severe patients, management believes that a common strategy for obtaining a broad label is to have two trials with slightly different enrollment criteria. The HAM-D cutoffs used are purely for regulatory purposes and have very little bearing on how depression is managed in the clinic. Moreover, there is currently no evidence to suggest that baseline severity should impact treatment effect.

The company currently believes that 10-20% of mothers experience PPD in some form with 70% of them being moderate-severe. This number could be materially higher but due to the stigma of the disease, there may be a negative ascertainment bias and under-diagnosis. SAGE views PPD as a medical condition as much as it is a psychiatric condition (“biologic complication of

pregnancy”) and a leading cause of maternal death. As such, the company believes that there should be a range of physicians who have access to 547 in the course of caring for patients (e.g. ob/gyns and family doctors). The company is therefore engaged in commercial readiness planning and disease awareness programs. The drug itself is a simple IV injection, which can be done through a peripheral IV and does not require special training. In terms of launch preparation, the company is putting together sales forces for both hospitals and specialty pharmacies (though the actual numbers have not yet been disclosed). Manufacturing capacity and supply chain are similarly being prepped for a potential launch.

In regards to pricing, SRSE was the previous anchor (recall the company had guided to a range of $25-75k per patient treated). The company is currently in the process of doing additional work with payers now that the likely first indication will be PPD. How these discussions ultimately shake out will depend on the effect size and flexibility in terms of how the drug is administered. The company continues to believe that they could be viewed as a differentiated therapeutic intervention.

In regards to the Phase 2 SAGE-217 in PPD, the company disclosed that patients were preferentially being placed onto the HUMMINGBIRD trials for obvious reasons. However, the timing for topline data remains intact. The intent for SAGE-547 was always to establish a commercial footprint for 217, which will come several years later. In terms of co-existence, the company believes this commercial footprint and the presence of two potentially complimentary assets in the same space is a good problem to have.

On MDD...

The company concedes that data so far has been open label and thus are subject to the obvious caveats of such studies. Nevertheless, the objective of the Phase 1 was always hypothesis and methodology generation in preparation for randomized trials. With that said the reduction in HAM-D total scores of 20 pts was quite striking when compared with approved treatments (typical range of 5-10 points on the same time scale). Patients included in the open label portion were standard MDD patients who had severe symptoms at the time of enrollment. Concomitant treatment with another drug was allowed (1/3 of patients). The company stressed that these patients would not be considered treatment refractory.

As an aside, management believes that depression trials which choose to specifically target refractory patients are doing so on the premise that those patients who have failed multiple therapies have a distinct subtype of the disease (which is an unproven hypothesis). This attempt to homogenize the patient population may not ultimately be the correct path to take. The company stated the Phase 2 will give greater clarity in regards to endpoints and powering for the potential pivotal trial. For example, with enough remissions the next trial could be powered for an endpoint of remissions rather than HAM-D reduction. Overall the company believes that if the results of the open label can be carried forwards into larger patient populations, this would be a paradigm shifting event in the sense that this would represent the ability to treat a psychiatric disorder in the acute setting without the side effects seen with current standard of care.

Other pipeline programs/updates...

The rationale for pursuing movement disorders is built on the premise that an imbalance of GABAergic tone mediated through various pathways (management emphasized that these diseases are different but share this common feature) result in the neuromuscular manifestations of diseases such as ET and Parkinson’s. For example, known GAGA agonists such as alcohol can transiently cause ET symptoms to abate, though this response rapidly diminishes over time due to, presumably, a down-regulation of synaptic GABA receptors (SAGE acts on extra synaptic receptors which do not down-regulate).

In regards to the recently initiated sleep study for SAGE-217 in healthy volunteers, the company is trying to confirm the sleep signal they saw in their other studies in a systemic fashion. Patients are being looked at in a standard sleep label, potentially at higher doses than the 30mg used in MDD. Metrics such as sleep quality and next morning performance will be evaluated.

The NMDA SAD study in healthy volunteers is on track to read out this quarter as well.

https://www.investorvillage.com/smbd.asp?mb=17990&mn=225&pt=…

Interessant finde ich, dass MRNS laut Quartalsbericht an der P2 zu SRSE festhält. Sie wollen dies ja auch in einem gänzlich anderen Setting tun (bevor Patienten in ein Koma versetzt werden) und könnten zudem von der genaueren Analyse der gescheiterten SAGE Studie profitieren z.B. bei der Teilnehmerauswahl.

SAGE schon heute (früher als gedacht) mit den Ergebnissen zu PPD. Und die waren so:

http://www.epvantage.com/Universal/View.aspx?type=Story&id=7…

Habe aber trotz meiner Überzeugung, dass hier noch Potenzial wäre, moderat bei beiden Gewinne realisiert. Jetzt kommt in diesem Jahr noch die P2 in Major Depression. Ein Erfolg hier wäre nochmal ein Quantensprung. Entscheidend wird wohl die Höhe der Placeboresponse sein.

Anfang 2018 dann die Ergebnisse von MRNS in PPD...

http://www.epvantage.com/Universal/View.aspx?type=Story&id=7…

Habe aber trotz meiner Überzeugung, dass hier noch Potenzial wäre, moderat bei beiden Gewinne realisiert. Jetzt kommt in diesem Jahr noch die P2 in Major Depression. Ein Erfolg hier wäre nochmal ein Quantensprung. Entscheidend wird wohl die Höhe der Placeboresponse sein.

Anfang 2018 dann die Ergebnisse von MRNS in PPD...

SAGE hat die bisherigen singlearm Ergebnisse genauer vorgestellt:

https://www.ecnp.eu/presentationpdfs/71/P.2.f.018.pdf

Wenn sich die Ergebnisse in der Placebo kontrollierten Studie ansatzweise halten lassen wäre das natürlich großartig -auch für MRNS!

https://www.ecnp.eu/presentationpdfs/71/P.2.f.018.pdf

Wenn sich die Ergebnisse in der Placebo kontrollierten Studie ansatzweise halten lassen wäre das natürlich großartig -auch für MRNS!

Antwort auf Beitrag Nr.: 56.244.056 von kmastra am 22.11.17 11:13:49Und es ist dann auch großartig! SAGE heute +75% MRNS im Schlepptau bei +30%.

Die Ergebnisse sind wirklich toll und werden wohl die Behandlung von schwer depressiven (evtl. ja auch leicht) Menschen revolutionieren.

http://www.businesswire.com/news/home/20171207005149/en/Sage…

Wichtig auch, dass es sich hier um die orale Version (lange Patentlaufzeit) handelt. Es stehen für dieses Jahr ja auch noch die PPD Ergebnisse von 217 an. Ein Erfolg ist jetzt dann doch wahrscheinlich und würde den Markt auch für leichtere Formen von PPD öffnen...Sehr schön!

Die Ergebnisse sind wirklich toll und werden wohl die Behandlung von schwer depressiven (evtl. ja auch leicht) Menschen revolutionieren.

http://www.businesswire.com/news/home/20171207005149/en/Sage…

Wichtig auch, dass es sich hier um die orale Version (lange Patentlaufzeit) handelt. Es stehen für dieses Jahr ja auch noch die PPD Ergebnisse von 217 an. Ein Erfolg ist jetzt dann doch wahrscheinlich und würde den Markt auch für leichtere Formen von PPD öffnen...Sehr schön!

Antwort auf Beitrag Nr.: 56.396.188 von kmastra am 07.12.17 20:23:54Sehr schön bin ja leider nicht mehr dabei, aber gönne es jedem der dabei ist!

Anmerkungen zum CC von SAGE:

-Man will bei 217 in PPD nun wohl die laufende P2 in eine zulassungsrelevante Studie umbauen. Man ist hier nach den Ergebnissen von 547 und jetzt 217 in MDD einfach so sicher, dass man da jetzt Zeit sparen möchte.

-Man will weiter psychische Erkrankungen im Bereich Mooddisorder testen z.B. Angst oder Bipolare Störung. (Angst ist laut clinicaltrials.gov bereits gestartet)

-Es stehen dieses Jahr noch die Ergebnisse von essential tremor und Parkinson aus sowie erste Ergebnisse von 718. Die Ergebnisse von 217 in PPD werden wohl nicht mehr in diesem Jahr kommen. (s.O.)

Für MRNS ist das nicht ganz unrelevant, da SAGE bei der oralen Version jetzt ziemlich Gas gibt. Zudem kommen die dann ggf. schon zulassungsrelevanten Daten nach den ersten Ergebnissen von MRNS.

-Man will bei 217 in PPD nun wohl die laufende P2 in eine zulassungsrelevante Studie umbauen. Man ist hier nach den Ergebnissen von 547 und jetzt 217 in MDD einfach so sicher, dass man da jetzt Zeit sparen möchte.

-Man will weiter psychische Erkrankungen im Bereich Mooddisorder testen z.B. Angst oder Bipolare Störung. (Angst ist laut clinicaltrials.gov bereits gestartet)

-Es stehen dieses Jahr noch die Ergebnisse von essential tremor und Parkinson aus sowie erste Ergebnisse von 718. Die Ergebnisse von 217 in PPD werden wohl nicht mehr in diesem Jahr kommen. (s.O.)

Für MRNS ist das nicht ganz unrelevant, da SAGE bei der oralen Version jetzt ziemlich Gas gibt. Zudem kommen die dann ggf. schon zulassungsrelevanten Daten nach den ersten Ergebnissen von MRNS.

Die wird noch abgehen 2018. Schöne Bewertung auf:

https://finance.yahoo.com/news/3-best-biotech-stocks-2017-14…

Marinus Pharmaceuticals:

The award for best-performing biotech stock of all in 2017 goes to Marinus Pharmaceuticals. Marinus' stock skyrocketed over 700%, edging out XOMA. Marinus' market cap was below $20 million at the beginning of the year. The biotech's valuation now is close to $330 million.

It's been an eventful year for Marinus. In June, the FDA granted orphan-drug designation to ganaxolone as a treatment for CDKL5 Disorder, a rare genetic type of epilepsy. Marinus announced top-line data from its phase 2 study of the drug in September. Those results were overwhelmingly positive. On Dec. 13, Marinus was added to the Nasdaq Biotechnology Index, which meant that several exchange-traded funds were buying the company's shares.

2018 should be another huge year for Marinus. The biotech expects to begin a pivotal clinical study of ganaxolone in treating CDKL5 Disorder next year. Marinus should also report results from a couple of phase 2 studies of the drug in 2018, one in treating postpartum depression and the other in treating refractory status epilepticus.

Honorable mentions

While Marinus, XOMA, and Sangamo were the best-performing biotech stocks this year, a couple of other biotechs deserve honorable mentions. Alnylam Pharmaceuticals (NASDAQ: ALNY) stock more than tripled in 2017, while Nektar Therapeutics (NASDAQ: NKTR) stock soared more than 350%. In a sense, Alnylam's and Nektar's gains are even more impressive than the top three biotech stocks, since the two companies started out the year with market caps of $1.8 billion and $3.2 billion, respectively.

Alnylam's share price had more than doubled by August, but the really big news for the biotech came in September. On Sept. 20, the company reported positive results from a late-stage study of RNAi drug patisiran in patients with hereditary ATTR amyloidosis with polyneuropathy. Alnylam is now pursuing U.S. and regulatory approval for the drug.

Nektar's story is similar. The stock posted solid gains throughout most of 2017, but really took off in November. Nektar announced positive clinical results in November for two pipeline candidates -- mu-opioid receptor agonist NKTR-181 and cancer drug NKTR-214.

With their relatively large market caps, it will probably be more difficult for Alnylam and Nektar to achieve similar gains in 2018. However, don't be surprised if all of these biotech stocks -- the three winners and the two honorable mentions -- perform well next year.

Im englischsprachigen Forum wird sie mit 50$ in 2018 prognostiziert. Von mir aus gern.

https://finance.yahoo.com/news/3-best-biotech-stocks-2017-14…

Marinus Pharmaceuticals:

The award for best-performing biotech stock of all in 2017 goes to Marinus Pharmaceuticals. Marinus' stock skyrocketed over 700%, edging out XOMA. Marinus' market cap was below $20 million at the beginning of the year. The biotech's valuation now is close to $330 million.

It's been an eventful year for Marinus. In June, the FDA granted orphan-drug designation to ganaxolone as a treatment for CDKL5 Disorder, a rare genetic type of epilepsy. Marinus announced top-line data from its phase 2 study of the drug in September. Those results were overwhelmingly positive. On Dec. 13, Marinus was added to the Nasdaq Biotechnology Index, which meant that several exchange-traded funds were buying the company's shares.

2018 should be another huge year for Marinus. The biotech expects to begin a pivotal clinical study of ganaxolone in treating CDKL5 Disorder next year. Marinus should also report results from a couple of phase 2 studies of the drug in 2018, one in treating postpartum depression and the other in treating refractory status epilepticus.

Honorable mentions

While Marinus, XOMA, and Sangamo were the best-performing biotech stocks this year, a couple of other biotechs deserve honorable mentions. Alnylam Pharmaceuticals (NASDAQ: ALNY) stock more than tripled in 2017, while Nektar Therapeutics (NASDAQ: NKTR) stock soared more than 350%. In a sense, Alnylam's and Nektar's gains are even more impressive than the top three biotech stocks, since the two companies started out the year with market caps of $1.8 billion and $3.2 billion, respectively.

Alnylam's share price had more than doubled by August, but the really big news for the biotech came in September. On Sept. 20, the company reported positive results from a late-stage study of RNAi drug patisiran in patients with hereditary ATTR amyloidosis with polyneuropathy. Alnylam is now pursuing U.S. and regulatory approval for the drug.

Nektar's story is similar. The stock posted solid gains throughout most of 2017, but really took off in November. Nektar announced positive clinical results in November for two pipeline candidates -- mu-opioid receptor agonist NKTR-181 and cancer drug NKTR-214.

With their relatively large market caps, it will probably be more difficult for Alnylam and Nektar to achieve similar gains in 2018. However, don't be surprised if all of these biotech stocks -- the three winners and the two honorable mentions -- perform well next year.

Im englischsprachigen Forum wird sie mit 50$ in 2018 prognostiziert. Von mir aus gern.

Diese oder nächste Woche sollte es Updates zum FDA-Approval geben. Schön, dass die Shorter so fleißig verkaufen. Günstiger wird es wohl nicht mehr. Ich rechne mit einem Anstieg auf 8-9 Euro zu Ende Januar.

Feine Sache! Insiderkäufe vom CEO persönlich gestern. Die News stehen kurz bevor. Und sie dürften sehr positiv ausfallen! Ich gehe davon aus, dass MRNS noch im Februar über die 10 $ Marke klettert.

bin froh, dass ich hier nochmals die Chance für einen Einstieg erhalte, dachte der Zug sei schon abgefahren, der Bewertungsabschlag zu SAGE ist ja riesig

Was ist Eure Meinung zu dieser Aktie. Das Unternehmen klingt spannend, aber ist bei der Performance noch Luft nach oben?

Beitrag zu dieser Diskussion schreiben

Zu dieser Diskussion können keine Beiträge mehr verfasst werden, da der letzte Beitrag vor mehr als zwei Jahren verfasst wurde und die Diskussion daraufhin archiviert wurde.

Bitte wenden Sie sich an feedback@wallstreet-online.de und erfragen Sie die Reaktivierung der Diskussion oder starten Sie eine neue Diskussion.

Investoren beobachten auch:

| Wertpapier | Perf. % |

|---|---|

| -1,76 | |

| +0,54 | |

| -1,91 | |

| +0,67 | |

| +0,07 | |

| +4,44 |

Meistdiskutiert

| Wertpapier | Beiträge | |

|---|---|---|

| 185 | ||

| 126 | ||

| 90 | ||

| 66 | ||

| 65 | ||

| 50 | ||

| 41 | ||

| 32 | ||

| 32 | ||

| 31 |