Meine kleine Sammlung an Börsenstatistiken (Seite 15)

eröffnet am 02.08.17 21:51:33 von

neuester Beitrag 03.01.24 14:57:17 von

neuester Beitrag 03.01.24 14:57:17 von

Beiträge: 204

ID: 1.258.587

ID: 1.258.587

Aufrufe heute: 2

Gesamt: 23.445

Gesamt: 23.445

Aktive User: 0

ISIN: US78378X1072 · WKN: CG3AA5

5.065,04

PKT

+0,19 %

+9,80 PKT

Letzter Kurs 17.04.24 Citigroup

Neuigkeiten

07:28 Uhr · wallstreetONLINE Redaktion |

24.04.24 · dpa-AFX |

24.04.24 · dpa-AFX |

24.04.24 · dpa-AFX |

24.04.24 · BNP Paribas Anzeige |

Schwacher Ausblick: Nach 1.300-Prozent-Rallye: Software-Perle ServiceNow legt den Rückwärtsgang ein

Schwacher Ausblick: Nach 1.300-Prozent-Rallye: Software-Perle ServiceNow legt den Rückwärtsgang einBeitrag zu dieser Diskussion schreiben

Antwort auf Beitrag Nr.: 57.270.442 von faultcode am 14.03.18 01:52:47

=> Definitionen:

* -10% drop from a peak = correction

* -20% drop from a peak = bear market

statistische Grundlagen für S&P500-Marktkorrekturen: (ohne Bärenmärkte!)

- going back to the inception of the S&P500 index ("Composite Index" since 1923/FC), the average correction lasts 51 trading sessions

- the last five corrections have only lasted an average of 37 trading days

- while going back to 1980, the average length has been 44 sessions

- since 1950, the average lasted for 61 trading days

=> heute, 15.3., sind 25 Handelstage (lt. oben) durch seit laufender Korrektur seit 26.01.2018 (Top)

The average S&P 500 correction lasts 51 trading days

https://www.marketwatch.com/story/the-stock-market-correctio…=> Definitionen:

* -10% drop from a peak = correction

* -20% drop from a peak = bear market

statistische Grundlagen für S&P500-Marktkorrekturen: (ohne Bärenmärkte!)

- going back to the inception of the S&P500 index ("Composite Index" since 1923/FC), the average correction lasts 51 trading sessions

- the last five corrections have only lasted an average of 37 trading days

- while going back to 1980, the average length has been 44 sessions

- since 1950, the average lasted for 61 trading days

=> heute, 15.3., sind 25 Handelstage (lt. oben) durch seit laufender Korrektur seit 26.01.2018 (Top)

Antwort auf Beitrag Nr.: 57.246.748 von faultcode am 11.03.18 15:50:47

Hier gesehen: https://www.trading-treff.de/wissen/trading-setup-turn-of-th… --> https://epub.uni-regensburg.de/8314/1/roeder2.pdf

=>

Fazit:

...

=> nochmal -- nach oben:

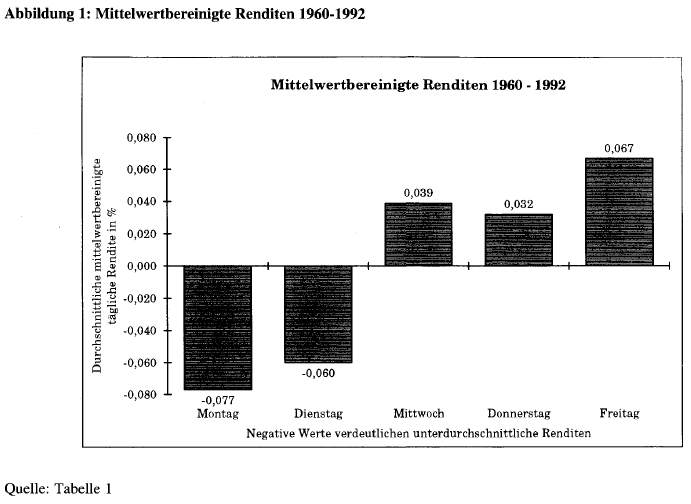

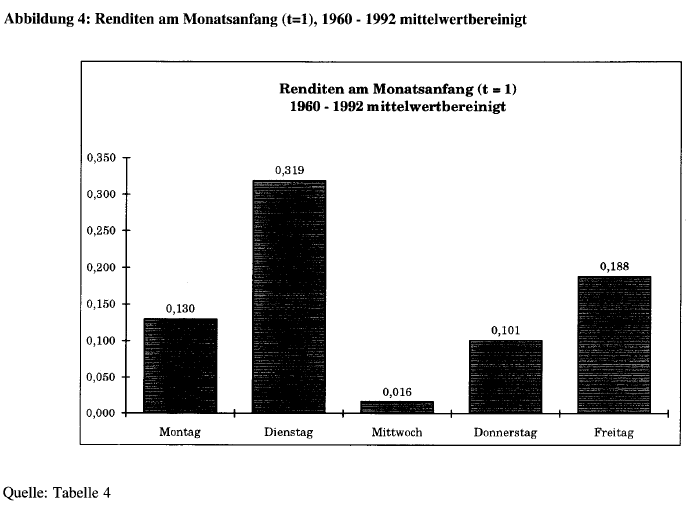

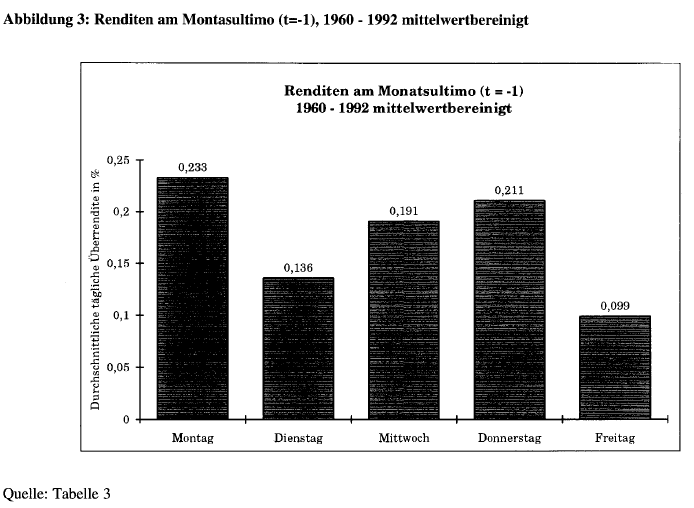

* Aktienkäufe eher vor Monatsende

* Aktienverkäufe eher am oder nach Monatsanfang

durchführen

sehr historische DAX Wochen- und Monatstage

..wobei nicht dieselbe Rechnung benutzt wird (also wie oben tägliche Open-to-Close-Performance), sondern R|t = ln(S|t / S|t-1).Hier gesehen: https://www.trading-treff.de/wissen/trading-setup-turn-of-th… --> https://epub.uni-regensburg.de/8314/1/roeder2.pdf

=>

Fazit:

...

=> nochmal -- nach oben:

* Aktienkäufe eher vor Monatsende

* Aktienverkäufe eher am oder nach Monatsanfang

durchführen

The U.S. health care business

..und nicht "The U.S. health care system" - so wie im auch nicht ganz billigen Deutschland:

2017: > USD10,000.00 pro Kopf und Jahr!

aus: https://www.statista.com/statistics/184955/us-national-healt…

=> damit die deutschen Kleinanleger in Evotec, Morphosys, Biofrontera und Co. mal wissen (wissen die meisten eh nicht, weil nicht davon betroffen in ihrer Komfortzone (*) ), woher ihre tollen Kursgewinne der letzten Jahre kommen

(*) "Unwissenheit ist die höchste Form des Glücks."; chinesisches Sprichwort

Antwort auf Beitrag Nr.: 57.244.711 von faultcode am 11.03.18 02:24:30

DAX 2018: auch hier der Donnerstag der weiche Tag

--> https://www.wallstreet-online.de/diskussion/1131140-260881-2…

Antwort auf Beitrag Nr.: 55.447.173 von faultcode am 02.08.17 22:26:22

Freitags kein Crash zur Zeit (2018Q1) am US-Aktienmarkt,..

https://www.wallstreet-online.de/diskussion/1131140-260841-2… Trading Spotlight

Pump-and-dump in Germany: the modern retiree

https://www.marketwatch.com/story/meet-the-perfect-mark-for-…=>...

That’s because new research shows that many retiree investors could hardly be more different than the stereotype of a naïve and gullible elderly widow. On the contrary, the study found, a good number of retirees turn out to be thrill seekers or gamblers who are attracted to penny-stock pump and dump schemes not out of ignorance but because of their huge risk.

The study, which the National Bureau of Economic Research recently began circulating, was conducted by Christian Leuz, a finance professor at the University of Chicago’s Booth School of Business, Leibniz University of Hanover’s Steffen Meyer, Humboldt University of Berlin’s Maximilian Muhn, Harvard’s Eugene Soltes and Goethe University of Frankfurt’s Andreas Hackethal.

It focused on individual investors who are drawn to pump-and-dump schemes. In such a scheme, of course, an unscrupulous operator will, after quietly acquiring a large position in a penny stock, circulate false stories about how the stock will soon skyrocket. The ensuing investor interest pushes the stock price much higher, allowing the perpetrator to unload his stock at a handsome profit.

The researchers studied more than 400 such schemes in Germany between 2002 and 2015.

Upon analyzing the trading records of over 110,000 individual investors from a major German bank, many of whom were retirees, the researchers found that a surprising number of these individuals—6% in fact—invested in a least one of these schemes. And they invested more than just a little amount, furthermore: Their average investment in the penny stocks was 11% of their account values, in fact. And even more surprising, given that the average investment in a scheme lost 28%, the researchers found that many individuals had invested in more than one of them.

Though the researchers didn’t focus solely on the retirees in their sample, Leuz in an interview said that they found no evidence that retirees’ propensity to invest in pump-and-dump schemes was appreciably different than it was for the non-retirees.

Most of us will be astonished by these findings, since most of us consider pump-and-dump schemes as morally, if not criminally, fraudulent. At the very least, we consider the unsolicited emails and phone calls as serious annoyances. It would never occur to us that anyone who knew better would actually want to invest in one of them.

And yet, believe it or not, they do. The researchers found evidence that many of the investors in these schemes seemed to be aware of the risks involved and proceeded anyway. The researchers speculate that these investors were being seduced by the promise of option-like payoffs of these investments, in which the odds of winning are very small but with big-enough gains when they do win to make the gamble attractive.

To be sure, Luez hastened to add, very few of the investors in their study achieved even a small profit when investing in the penny stocks at the heart of these pump-and-dump schemes—much less the huge returns that would make it even potentially attractive to incur the much-more-probable losses. Still, hope springs eternal.

An analogy to an old joke

These investors’ thought process reminds me of the old joke about an oil man who dies and approaches the Pearly Gates. St. Peter tells him that while he deserves to get into heaven, there is no more room since there are already too many oil men there. So the only way he can get in is by persuading one of the oil men already there to go to hell.

The oil man took the challenge, and pretty soon there was a steady stream of oil men headed straight to hell. St. Peter was amazed, and asked the oil man how he did it. “Easy,” he replied. “I just spread the rumor that oil had been discovered in hell.”

Just as St. Peter was opening the gates so our new oil man could go into heaven, however, he instead joined the procession of oil men to hell. Why ever why, St. Peter asked? Because, the oil man replied, you just never know; it might actually be true that oil had been discovered in hell.

If you doubt the joke’s analogy to pump-and-dump schemes, just consider an email promotion from September 2007 that the researchers refer to in their study: “We are glad to inform you of a CANCER CURE invented by [company name omitted] that will take the world by storm. This new medicine is above all other [sic] and boosts [sic] a 80% success rate during clinical trials. Over the next few days you will hear about this in the PAPERS and on TV. So buy shares now, while the price is low, before the news hits.” The misspellings and grammatical errors were in the original, so even if the content didn’t strain credulity you would have thought these other errors would have been warning enough.

Investment implications

In addition to painting a more nuanced picture of retirees and other investors, this new research points to one reason why regulators have had such difficulty putting pump-and-dump schemes out of business. The presumption has been that no one would invest in them if they knew the risks involved. At least for that subset of retirees and other investors who are thrill seekers, however, such efforts are pointless, since these investors are attracted to the schemes not out of ignorance about the risks but precisely because of them.

In an interview, Leuz said that one focus of his and his co-authors’ subsequent research will be what other possible actions regulators could take to persuade retirees and others not to be seduced by pump-and-dump schemes. But he acknowledged that it will be difficult to put those schemes out of business so long as demand for them remains widespread. After all, pumping and dumping is already questionable legally, and that has not put an end to the phenomenon.

The investment implication for each of us individually, however, is clear. If you want a thrill, buy a lottery ticket. But don’t invest your hard-earned retirement portfolio in a pump-and-dump scheme.

You’ve heard it a thousand times before, but it nevertheless remains true: If something seems too good to be true, it probably is.

=> na dann, willkommen bei WO

Alleine schon daran gut zu erkennen, wie verwaist viele DAX30-Foren sind:

Alleine schon daran gut zu erkennen, wie verwaist viele DAX30-Foren sind:

Hingegen "Alles unter 1€":

Antwort auf Beitrag Nr.: 57.036.162 von faultcode am 15.02.18 18:30:57

VDAX nach Explosion wieder halbiert. Was nun?

https://www.godmode-trader.de/analyse/volatilitaet-vdax-nach…

=> dieser Satz ist unvollständig und damit unklar:

Das Vega liegt aktuell bei 0,2. Das bedeutet, dass ein Anstieg der impliziten Vola - unter sonst gleichen Bedingungen, also isoliert betrachtet - zu einem Kursgewinn von 20 Cent im Optionsschein führen würde.

(Begriff "Vega" erscheint einmal im Artikel).

=> es muss z.B. richtig so lauten:

Das Vega liegt aktuell bei 0,2. Das bedeutet, dass ein Anstieg der impliziten Vola um einen Prozentpunkt - unter sonst gleichen Bedingungen, also isoliert betrachtet - zu einem Kursgewinn von 20 Cent im Optionsschein mit einem Bezugsverhältnis von 1:1 führen würde.

siehe z.B. aus:

https://www.boerse-stuttgart.de/de/boersenportal/boersenwiss…

=>

Neben den Kursveränderungen des Basiswertes hat meist die Veränderung der impliziten Volatilität einen großen Einfluss auf den Wert eines Optionsscheins.

...

Das Vega gibt an, um welchen Betrag ein Optionsschein sich im Wert verändert, wenn die implizite Volatilität um einen Prozentpunkt steigt. Ein Optionsschein mit einem Bezugsverhältnis von 1:1 und einem Vega von 0,5 steigt bzw. fällt um 0,50 Euro im Wert, wenn die implizite Volatilität um einen Prozentpunkt steigt oder fällt.

Volatilität in der dt. Finanzmarkt-Folklore: das Vega -- Veränderungen der Volatilität

Z.B. gerade gesehen:VDAX nach Explosion wieder halbiert. Was nun?

https://www.godmode-trader.de/analyse/volatilitaet-vdax-nach…

=> dieser Satz ist unvollständig und damit unklar:

Das Vega liegt aktuell bei 0,2. Das bedeutet, dass ein Anstieg der impliziten Vola - unter sonst gleichen Bedingungen, also isoliert betrachtet - zu einem Kursgewinn von 20 Cent im Optionsschein führen würde.

(Begriff "Vega" erscheint einmal im Artikel).

=> es muss z.B. richtig so lauten:

Das Vega liegt aktuell bei 0,2. Das bedeutet, dass ein Anstieg der impliziten Vola um einen Prozentpunkt - unter sonst gleichen Bedingungen, also isoliert betrachtet - zu einem Kursgewinn von 20 Cent im Optionsschein mit einem Bezugsverhältnis von 1:1 führen würde.

siehe z.B. aus:

https://www.boerse-stuttgart.de/de/boersenportal/boersenwiss…

=>

Neben den Kursveränderungen des Basiswertes hat meist die Veränderung der impliziten Volatilität einen großen Einfluss auf den Wert eines Optionsscheins.

...

Das Vega gibt an, um welchen Betrag ein Optionsschein sich im Wert verändert, wenn die implizite Volatilität um einen Prozentpunkt steigt. Ein Optionsschein mit einem Bezugsverhältnis von 1:1 und einem Vega von 0,5 steigt bzw. fällt um 0,50 Euro im Wert, wenn die implizite Volatilität um einen Prozentpunkt steigt oder fällt.

Volatility (0)

(wenn ich mehr Zeit habe, versuche ich den VIX- und XIV-Sachverhalt von Anfang Februar irgendwie zu einfachen Erkenntnissen zusammenzufassen. Weil halt doch ein alter Klassiker an einem Finanzmarkt:- ein theoretisch Einmal-in-10.000-Jahren-Ereignis stellte sich im realen Leben dann doch eher als ein alle 10-Jahre-Ereignis heraus --> das produziert sehr schnell, binnen 48h, einige - oft zufällige - Gewinner und viele, systematische Verlierer.)

Aber zur Definition und Sprache, die oft im Zusammenhang mit Volatilität irreführenderweise verwendet wrd:

Volatility is not about "fear" nor is it about "uncertainty." Volatility occurs when options change quickly.

(gemeint ist die implizite Volatilität, die eben aus Preisen von bestimmten Optionen auf einen Aktienindex gebildet wird...)

aus: 7.2.2018:

Stock Gyrations

https://johnhcochrane.blogspot.de/2018/02/stock-gyrations.ht…

Antwort auf Beitrag Nr.: 56.998.380 von faultcode am 11.02.18 16:51:20

aus: https://www.bloomberg.com/news/articles/2017-05-12/there-are…

=> nichts da mit: "What drove the jump? Demand"!

=> auf diese Weise kann nämlich ein Vertreter der Sell side immer einen Index als Benchmark finden, der in der Vergangenheit sehr gut performte

=> wobei wir denn wieder beim Thema "Fooled by randomness" gemäss Nassim N. Taleb wären; cf. https://www.wallstreet-online.de/diskussion/1258587-31-40/me…

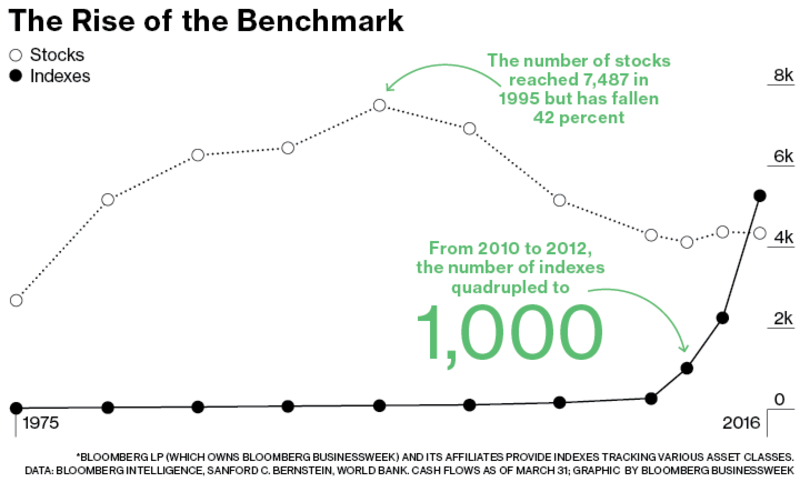

Die Index-Flut als Lösung für ein (vordergründiges) Diversifikationsproblem? (3)

Abgesehen davon: die Finanzindustrie tut sich langfristig keinen Gefallen damit, immer mehr Indizes zu kreieren:

aus: https://www.bloomberg.com/news/articles/2017-05-12/there-are…

=> nichts da mit: "What drove the jump? Demand"!

=> auf diese Weise kann nämlich ein Vertreter der Sell side immer einen Index als Benchmark finden, der in der Vergangenheit sehr gut performte

=> wobei wir denn wieder beim Thema "Fooled by randomness" gemäss Nassim N. Taleb wären; cf. https://www.wallstreet-online.de/diskussion/1258587-31-40/me…

Antwort auf Beitrag Nr.: 56.998.257 von faultcode am 11.02.18 16:27:49

=> interessant: der REIT-Index nahm den DAX-Absturz offensichtlich vorweg.

Dieser Autor, Holger Grethe, meint am 20. Dez 2017 doch allen Ernstes:

Was spricht für die Anlageklasse Immobilienaktien?

...

2. Niedrige Korrelation mit dem Aktiengesamtmarkt

Eine niedrige Korrelation bedeutet: Die einzelnen Jahresrenditen zweier Anlageklassen weichen in einem bestimmten Zeitraum voneinander ab, entwickeln sich also nicht im Gleichlauf.

...

In den letzten 30 Jahren bewegte sich die Korrelation zwischen US-amerikanischen Aktien und REITs in einem weiten Bereich zwischen 0 und 0.85 (+).

...

aus: https://zendepot.de/immobilien-aktien-und-reits/

=> also genau dann, wenn ein Anleger einen positiven Diversifikations-Effekt mit der Anlageklasse REIT haben möchte (bzgl. seines sonstigen Aktienportfolios) bekommt er sie nicht!

=> d.h., auch die sehr hohe Korrelation von oben (+) mit 0.85, kommt mutmasslich genau in einer Krisensituation zum Tragen!

=> es bleibt dabei:

"Chasing the same signals. How black box trading influences stock markets from Wall Street to Shanghai"

von Brian R. Brown, 2010

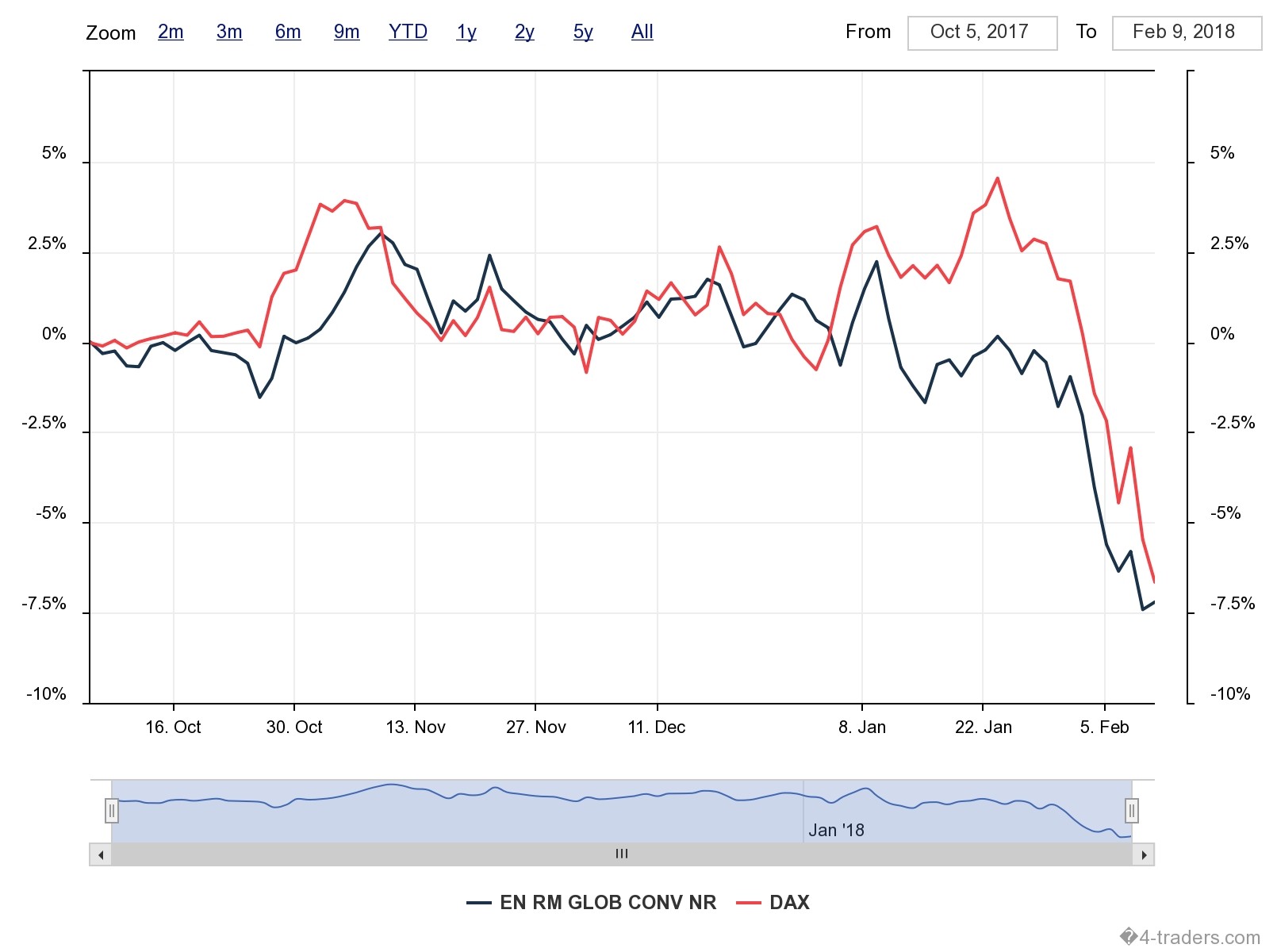

internationale REIT's als Lösung für ein (vordergründiges) Diversifikationsproblem? (2)

Schaut man sich die jüngste Entwicklung mal an (hier der NL0012645212 -- Euronext Reitsmarket Global Conviction NR vs. DAX als Performance-Index), also mit allen Daten, die z.Z. zur Verfügung stehen, dann war's das mit der Diversifikation - weil eindeutig sehr stark korreliert:

=> interessant: der REIT-Index nahm den DAX-Absturz offensichtlich vorweg.

Dieser Autor, Holger Grethe, meint am 20. Dez 2017 doch allen Ernstes:

Was spricht für die Anlageklasse Immobilienaktien?

...

2. Niedrige Korrelation mit dem Aktiengesamtmarkt

Eine niedrige Korrelation bedeutet: Die einzelnen Jahresrenditen zweier Anlageklassen weichen in einem bestimmten Zeitraum voneinander ab, entwickeln sich also nicht im Gleichlauf.

...

In den letzten 30 Jahren bewegte sich die Korrelation zwischen US-amerikanischen Aktien und REITs in einem weiten Bereich zwischen 0 und 0.85 (+).

...

aus: https://zendepot.de/immobilien-aktien-und-reits/

=> also genau dann, wenn ein Anleger einen positiven Diversifikations-Effekt mit der Anlageklasse REIT haben möchte (bzgl. seines sonstigen Aktienportfolios) bekommt er sie nicht!

=> d.h., auch die sehr hohe Korrelation von oben (+) mit 0.85, kommt mutmasslich genau in einer Krisensituation zum Tragen!

=> es bleibt dabei:

"Chasing the same signals. How black box trading influences stock markets from Wall Street to Shanghai"

von Brian R. Brown, 2010

07:28 Uhr · wallstreetONLINE Redaktion · SAP |

24.04.24 · dpa-AFX · Boeing |

24.04.24 · dpa-AFX · Boeing |

24.04.24 · dpa-AFX · ASM International |

24.04.24 · wallstreetONLINE Redaktion · DAX |

24.04.24 · wallstreetONLINE Redaktion · Dow Jones |

24.04.24 · dpa-AFX · Advanced Micro Devices |

23.04.24 · dpa-AFX · Danaher |

23.04.24 · dpa-AFX · Dow Jones |

| Zeit | Titel |

|---|---|

| 23.04.24 | |

| 21.04.24 | |

| 26.03.24 | |

| 14.03.24 | |

| 22.02.24 | |

| 13.02.24 | |

| 13.02.24 | |

| 30.01.24 | |

| 26.01.24 | |

| 22.01.24 |