Nzuri Copper -Kupfer & Kobalt im Kongo- - 500 Beiträge pro Seite

eröffnet am 24.09.17 15:00:30 von

neuester Beitrag 27.02.19 07:45:14 von

neuester Beitrag 27.02.19 07:45:14 von

Beiträge: 158

ID: 1.262.580

ID: 1.262.580

Aufrufe heute: 0

Gesamt: 10.880

Gesamt: 10.880

Aktive User: 0

ISIN: AU000000NZC9 · WKN: A2DLR2

0,2200

EUR

0,00 %

0,0000 EUR

Letzter Kurs 28.02.20 Tradegate

Neuigkeiten

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7950 | +30,33 | |

| 55,80 | +15,41 | |

| 0,7999 | +14,27 | |

| 11,250 | +12,73 | |

| 1,6500 | +11,79 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 4,8400 | -9,67 | |

| 17,310 | -9,98 | |

| 186,20 | -10,48 | |

| 4,2300 | -17,86 | |

| 0,5550 | -29,30 |

- highgrade

- 15 km weg von Ivanhoe´s projekt

- bzgl Exloration JV mit Ivanhoe

- FS sollte in den nächsten Wochen kommen, evtl. früher

Präsi (Stand September 2017):

http://nzuricopper.com.au/wp-content/uploads/2017/09/170918-…

Artikel (5.9.2017):

https://thewest.com.au/business/public-companies/nzuri-in-da…

- 15 km weg von Ivanhoe´s projekt

- bzgl Exloration JV mit Ivanhoe

- FS sollte in den nächsten Wochen kommen, evtl. früher

Präsi (Stand September 2017):

http://nzuricopper.com.au/wp-content/uploads/2017/09/170918-…

Artikel (5.9.2017):

https://thewest.com.au/business/public-companies/nzuri-in-da…

Link zum Quarterly: http://www.asx.com.au/asxpdf/20171031/pdf/43ntflmc25ytzb.pdf

Zusammenfassung der FS:

Co-Grade (0,36%) halbiert gegenüber September-Präsentation.

Das Explorationspotential könnte hier der GameChanger sein.

Ist hier jemand drin?

Zusammenfassung der FS:

Co-Grade (0,36%) halbiert gegenüber September-Präsentation.

Das Explorationspotential könnte hier der GameChanger sein.

Ist hier jemand drin?

Antwort auf Beitrag Nr.: 56.082.035 von mge am 02.11.17 13:49:01habs gelassen... dachte unter 100 mios USD

marktkap soweit ok. hab erstmal das große dingens nicht gesehen.

aber ok exploration usw...

kein uninteressanter wert.

hab vor 3 tagen die wesentlich riskantere Celsius Res.

reingenommen (namibia)

marktkap soweit ok. hab erstmal das große dingens nicht gesehen.

aber ok exploration usw...

kein uninteressanter wert.

hab vor 3 tagen die wesentlich riskantere Celsius Res.

reingenommen (namibia)

Bin heute Nacht zu 22 audcent einstiegen.

Antwort auf Beitrag Nr.: 56.311.304 von Reiners am 29.11.17 14:52:28

achso ich hab ja sogar nen thread aufgemacht zu denen

sorry für die 3 bm´s

vom projekt her im gegensatz zu den aussies und can´s in bezug auf wirtschaftlichkeit und hohen margen natürlich bombensicher

Zitat von Reiners: Bin heute Nacht zu 22 audcent einstiegen.

achso ich hab ja sogar nen thread aufgemacht zu denen

sorry für die 3 bm´s

vom projekt her im gegensatz zu den aussies und can´s in bezug auf wirtschaftlichkeit und hohen margen natürlich bombensicher

Trading Spotlight

hab noch en paar "stehlen" können zu 0,235 AUD

Willkommen an Board

Man(n) trifft doch überall die Gleichen .... ;---)))) .. scheinbar ticken wir irgendwie ähnlich? Good luck!

Jeder der sich für den Wert interessiert, sollte sich Beitrag von Thunder54 (Profi User auf Hotcopper) mal unbedingt durchlesen.

Hier der Link

https://www.getrevue.co/profile/Thunder54/issues/asx-just-th…

Wie er mir gerade bestätigt hat, ist es seine größte Position, und das soll schon was heißen.

Wer keine Berührungsängste mit der Demokratische Republik Kongo hat, der sollte sich den Wert ins Depot legen.

Hier der Link

https://www.getrevue.co/profile/Thunder54/issues/asx-just-th…

Wie er mir gerade bestätigt hat, ist es seine größte Position, und das soll schon was heißen.

Wer keine Berührungsängste mit der Demokratische Republik Kongo hat, der sollte sich den Wert ins Depot legen.

https://m.investing.com/commodities/cobalt-streaming-chart

Cobalt steigt weiter, jetzt schon 68.694 USD/T

Cobalt steigt weiter, jetzt schon 68.694 USD/T

von tommy-hl geklaut:

-----------------------------

Prognosen für Kobaltpreise werden erhöht

BMO Capital Markets ... sees the annual average cobalt price peaking at $40.50/lb ($89,290 mt) in 2019

Citi also made a price forecast for cobalt on Monday of $75,000/mt ($34.01/lb) in 2018 and $80,000/mt in 2019 and 2020.

https://www.platts.com/latest-news/metals/newyork/cobalt-pri…

-----------------------------

Prognosen für Kobaltpreise werden erhöht

BMO Capital Markets ... sees the annual average cobalt price peaking at $40.50/lb ($89,290 mt) in 2019

Citi also made a price forecast for cobalt on Monday of $75,000/mt ($34.01/lb) in 2018 and $80,000/mt in 2019 and 2020.

https://www.platts.com/latest-news/metals/newyork/cobalt-pri…

http://www.republicofmining.com/2017/12/05/electric-charge-g…

@Boerseback

ich möchte anfügen meine(Nzuri) Meinung(Die Die "feasibility" "nicht so dolle" fand(was sich an sichh nicht geändert hat, aber ein paar Andere Faktoren hinzugekommen sind)-auf Reiners hin- geändert zu haben.

@Boerseback

ich möchte anfügen meine(Nzuri) Meinung(Die Die "feasibility" "nicht so dolle" fand(was sich an sichh nicht geändert hat, aber ein paar Andere Faktoren hinzugekommen sind)-auf Reiners hin- geändert zu haben.

Antwort auf Beitrag Nr.: 56.377.585 von Popeye82 am 06.12.17 15:32:17ja, ging mir auch so... Reiners hat den wert ganz gut beleuchtet.

mir war das verhältnis marketcap vs NPV damals irgendwie nicht so dass ich rein wollte.

natürlich stieg jetzt auch kobalt stärker.

ich glaub auch weniger dass es hier in die extreme geht in bälde... ich halte die nur im esktor für vergleichsweise (vom land abgesehen) als ziemlich sicher im sinne dass das eine profitable mine werden wird.

bei den aussies bin ich mir da teils nicht so ganz sicher wie AUZ und so.

mir war das verhältnis marketcap vs NPV damals irgendwie nicht so dass ich rein wollte.

natürlich stieg jetzt auch kobalt stärker.

ich glaub auch weniger dass es hier in die extreme geht in bälde... ich halte die nur im esktor für vergleichsweise (vom land abgesehen) als ziemlich sicher im sinne dass das eine profitable mine werden wird.

bei den aussies bin ich mir da teils nicht so ganz sicher wie AUZ und so.

nzuri-value-considerations

I have four basic areas I look at when considering value of Nzuri:

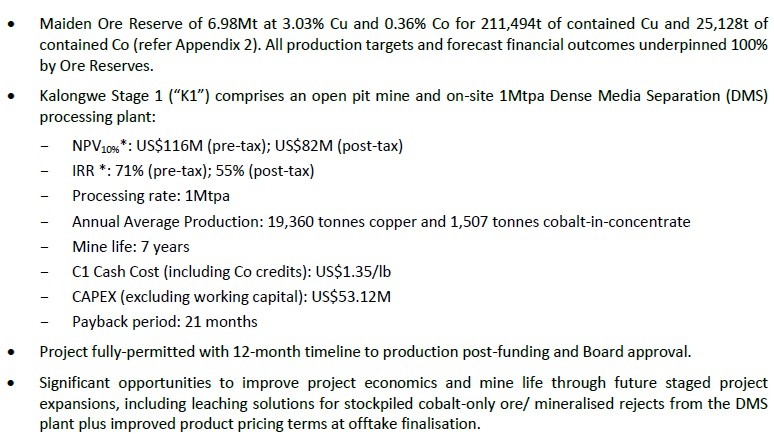

1 - Kalongwe Stage 1, 7 year LOM, Ore Reserve of 6.98Mt at 3.03% Cu and 0.36% Co.

2 - Kalongwe Stage 2, 6-7 year LOM, Leach of tailings/stockpiles, combined resources of 6.1MT at 0.98% Cu and 0.29% Co

3 - Kalongwe Stage 3, LOM extension using satellite deposits from Monwezi cluster (19m at 0.48% Co, 8m at 2.53% Cu), Kambudji (4m at 3.87% Cu)

4 - Exploration program (2018), Kasangasi kamoa/kakula target, Mukansa cobalt target, new aeromag targets

Now start at just looking at part 1, Kalongwe Stage 1, a feasibility level project.

Feasibility Study gave us an NPV of $116M USD and about US$33m in annual cashflow for 7 years. With a capex of just US$52M this feasibility study more than justifies our current market cap. Just one year of the projected annual cashflow in AUD is 82% of our current enterprise.

Now if you just upgrade this FS to LME spot prices you get an NPV of US$142M and US$39.13M in annual cashflow for 7 years.

Now change the transportation costs to reflect a probable off-take with one of the new Kolwezi based SXEW plants, and you get an NPV of US$180M and annual cashflow of US$47M for 7 years.

Now improve payability of that offtake modestly to 55% of LME for copper and 20% of LME for cobalt (very realistic given what we are hearing about cobalt and I'm hearing about severe on the ground on ore shortages in the DRC due to bad mine planning and legal disputes) and you get NPV of US$280M and annual cashflow of US$67M for 7 years.

This final iteration is my personal baseline expectation for Kalongwe Stage 1, using spot commodity prices, around US$280M NPV or A$370M. This compared to a present day EV of $52m (using 22.5c as last close price for NZC).

And if you like to use the oft quoted $4 copper and $55 cobalt for 2019, you get US$596M NPV.

All Nzuri management have to do now is close off the offtake/financing and built it as is, and its a very straightforward build and mine plan.

So what we already have is very exciting.

Then on top of this we have points 1 - 3 as described above. Or if you can't bother scrolling, almost double the mine life with much more cobalt revenue thanks to leaching, more oxide ore from satellite deposits, and then the exploration program might deliver an elephant, who cares.

In 2017 I largely held for the risk free exposure to exploration (which worked out but would have been nice to jag something), in 2018/2019 I hold for the cobalt/copper concentrate market, Kalongwe financing/offtake and to finally be able to say I was right, I have a large ego and its bruised for holding so long with no reward. Fingers crossed.

* Note all NPV are pre-tax and on 100% project basis, CBF trimming it, but its on 10% discount rate, all the spruikers use 8%

https://hotcopper.com.au/threads/nzuri-value-considerations.…

I have four basic areas I look at when considering value of Nzuri:

1 - Kalongwe Stage 1, 7 year LOM, Ore Reserve of 6.98Mt at 3.03% Cu and 0.36% Co.

2 - Kalongwe Stage 2, 6-7 year LOM, Leach of tailings/stockpiles, combined resources of 6.1MT at 0.98% Cu and 0.29% Co

3 - Kalongwe Stage 3, LOM extension using satellite deposits from Monwezi cluster (19m at 0.48% Co, 8m at 2.53% Cu), Kambudji (4m at 3.87% Cu)

4 - Exploration program (2018), Kasangasi kamoa/kakula target, Mukansa cobalt target, new aeromag targets

Now start at just looking at part 1, Kalongwe Stage 1, a feasibility level project.

Feasibility Study gave us an NPV of $116M USD and about US$33m in annual cashflow for 7 years. With a capex of just US$52M this feasibility study more than justifies our current market cap. Just one year of the projected annual cashflow in AUD is 82% of our current enterprise.

Now if you just upgrade this FS to LME spot prices you get an NPV of US$142M and US$39.13M in annual cashflow for 7 years.

Now change the transportation costs to reflect a probable off-take with one of the new Kolwezi based SXEW plants, and you get an NPV of US$180M and annual cashflow of US$47M for 7 years.

Now improve payability of that offtake modestly to 55% of LME for copper and 20% of LME for cobalt (very realistic given what we are hearing about cobalt and I'm hearing about severe on the ground on ore shortages in the DRC due to bad mine planning and legal disputes) and you get NPV of US$280M and annual cashflow of US$67M for 7 years.

This final iteration is my personal baseline expectation for Kalongwe Stage 1, using spot commodity prices, around US$280M NPV or A$370M. This compared to a present day EV of $52m (using 22.5c as last close price for NZC).

And if you like to use the oft quoted $4 copper and $55 cobalt for 2019, you get US$596M NPV.

All Nzuri management have to do now is close off the offtake/financing and built it as is, and its a very straightforward build and mine plan.

So what we already have is very exciting.

Then on top of this we have points 1 - 3 as described above. Or if you can't bother scrolling, almost double the mine life with much more cobalt revenue thanks to leaching, more oxide ore from satellite deposits, and then the exploration program might deliver an elephant, who cares.

In 2017 I largely held for the risk free exposure to exploration (which worked out but would have been nice to jag something), in 2018/2019 I hold for the cobalt/copper concentrate market, Kalongwe financing/offtake and to finally be able to say I was right, I have a large ego and its bruised for holding so long with no reward. Fingers crossed.

* Note all NPV are pre-tax and on 100% project basis, CBF trimming it, but its on 10% discount rate, all the spruikers use 8%

https://hotcopper.com.au/threads/nzuri-value-considerations.…

Klingt realistisch und vielversprechend ... bleibt nur zu hoffen, dass die ganze Story mit der Elektromobilität nicht wie eine heiße Blase platzt - Gründe dafür gäb's genug. Und wenn auch nur

HALWEGS der Crash kommt, mit dem über kurz oder lang zu rechnen ist, sieht's auch bei den

modischsten Rohstoffen düster aus. Ich selbst bin breitgefächert dabei, zieh aber sauber meine SL's nach ...

HALWEGS der Crash kommt, mit dem über kurz oder lang zu rechnen ist, sieht's auch bei den

modischsten Rohstoffen düster aus. Ich selbst bin breitgefächert dabei, zieh aber sauber meine SL's nach ...

Antwort auf Beitrag Nr.: 56.383.693 von bmann025 am 07.12.17 00:03:38"four basic areas" ist denk ich ganz gut.

lieber ein bisschen vorsichtig mit dem "überüberoptimistischem case" sein,

aber in dem artikel sind eine ganze Reihe der "paar Anderen Faktoren" aufgeführt.

lieber ein bisschen vorsichtig mit dem "überüberoptimistischem case" sein,

aber in dem artikel sind eine ganze Reihe der "paar Anderen Faktoren" aufgeführt.

Antwort auf Beitrag Nr.: 56.383.693 von bmann025 am 07.12.17 00:03:38p.S.

du scheinst auch ein "ganz Vernünftiger" zu sein.

(ich hatte, bei Diesem Namen, -duuunkel-"so einen Chaoten" in Erinnerung)

du scheinst auch ein "ganz Vernünftiger" zu sein.

(ich hatte, bei Diesem Namen, -duuunkel-"so einen Chaoten" in Erinnerung)

Antwort auf Beitrag Nr.: 56.383.738 von Popeye82 am 07.12.17 00:24:26Von der Vernunftshöhe herunter sieht das ganze Leben wie eine böse Krankheit und die Welt einem Tollhaus gleich. (Johann Wolfgang von Goethe)

bmann025 bekommt DAUSEND Punkte

für dieses weise Zitat ... ;--))))))

für dieses weise Zitat ... ;--))))))

Hier noch 3 Postings von hotcopper

Angeblicher Anstieg von Cobalt auf USD 75.000 / t (Quelle nicht verifiziert)

Cobalt27 sammelt USD 85 Mio um bis zu 720 Tonnen physisches Kobalt zu kaufen. Kaufpreis 10% ueber (!) dem Ask Kurs vom 6. Dezember.

https://hotcopper.com.au/threads/ann-company-presentation-fo…

Nic French: we are approaching the Cobalt Cliff

https://www.youtube.com/watch?time_continue=985&v=eooo8yezOF…

und vielleicht am Interessantesten, Interview mit Mark Arnesen (veroeffentlicht am 9.11.2017):

'There is lot of room in respect to what happens with our off-take. We'd like to think we would be announcing results on our work on the off-take side shortly. ... We got a project that we can bring to production extremley, extremely quickly."

Angeblicher Anstieg von Cobalt auf USD 75.000 / t (Quelle nicht verifiziert)

Cobalt27 sammelt USD 85 Mio um bis zu 720 Tonnen physisches Kobalt zu kaufen. Kaufpreis 10% ueber (!) dem Ask Kurs vom 6. Dezember.

https://hotcopper.com.au/threads/ann-company-presentation-fo…

Nic French: we are approaching the Cobalt Cliff

https://www.youtube.com/watch?time_continue=985&v=eooo8yezOF…

und vielleicht am Interessantesten, Interview mit Mark Arnesen (veroeffentlicht am 9.11.2017):

'There is lot of room in respect to what happens with our off-take. We'd like to think we would be announcing results on our work on the off-take side shortly. ... We got a project that we can bring to production extremley, extremely quickly."

Antwort auf Beitrag Nr.: 56.409.700 von bmann025 am 08.12.17 22:45:43Die laut erstem HC Post bezahlten USD 36.39/pound entsprechen (0.454 Pound/kg) USD 80.15/kg bzw. USD 80150/t.

Von einem HC User. Lesenswert

-----------------------------------------------------

I wanted to try and explain things around “payability” in laymans terms, and I by no means claim to be an expert, just piecing things together as I’ve been learning about this industry myself. Payability is simply what you will be paid for metal contained as a % of the metal contained.

So if you’ve got 1 tonne of dirt which has 10kg (1% grade) of a metal called X, and you go to a smelter, they may offer you terms that only means you get paid for 1kg of metal, even if you have 10kg in the dirt. Why - because they have costs involved in upgrading that 1% dirt to a saleable product and a sale price determined by the rest of market.

Now go back to the FS. As of the FS Nzuri are putting out a Copper/Cobalt concentrate with 19,360t of Copper and 1507t of Cobalt annually for 7 years.

Now using one indicative quote from an off-taker, given/tendered when cobalt was $15/lb, Nzuri are expecting to be paid for around 50% of the copper in the concentrate and a range of 7-15% of the cobalt.

Using last LME prices this gives us a pre-tax NPV of ~A$180M or A$47M in avg. annual profits.

Now for arguments sake, what if hypothetically Nzuri was paid 60% for contained copper and 40% for contained cobalt?

Using last LME price this gives us a pre-tax NPV of ~A$520M or $112m in avg. annual profits.

(Note this is all relating to the FS which is stage 1 only, no cobalt stockpiles or tailings or satellite deposits)

So a simple thing like the terms of the offtake contract have a very large impact on the Stage 1 project. Not that my personal expectation is quite that high but just showing why its important.

To understand what conditions could occur to allow such an uplift in value, I am going to look at oranges and orange juice, this is how I have to explain things to myself, with things you can eat.

Say there is an orange farmer and an orange juice producer. (note this is all a a vast simplification of the juice supply chain). Now normally the orange farmer sells his oranges to the juicer for a price related to the yield of his fellow farmers and the demand for oranges as a whole. This price is not so volatile.

Say for arguments sake this price is ~ $2/kg.

Now picture a situation where for some reason only the farmers in one particular valley, lets call this valley “Katanga” can produce enough oranges consistently enough to satisfy a big orange juice maker.

In this valley you have different kinds of orange production, some of them use immigrant labour to harvest, some use pesticides, some are completely automated, sustainable and organic.

It so happens that a new fad diet emerges called the “OJ cleanse” and the proponents of this diet insist that only sustainable, organic oranges can make the right orange juice, and you need to drink copious amounts of juice to be awesome.

The juice makers immediately secure supply with the organic farmers and start charging more for the organic juice.

The fad is wildly successful. The juice maker is able to charge over triple the amount they could have normally, but are still paying the farmer around $2/kg.

Now something interesting happens, other entrepreneurs notice the ridiculous margins the organic juice has and new juice makers start being established.

Now there’s only one valley, the Katanga valley, that has the consistent and scalable production. To make matters worse, they can only use farmers who are sustainable, organic, which is again a subset of the Katanga subset. To make matters even worse there are market speculators stockpiling organic oranges understanding that juice makers can afford to pay much more.

Now the organic, sustainable juice farmer in the Katanga valley has multiple parties knocking on his door asking for organic oranges. He only has a certain sized orchard but now far more customers than he has oranges, so he tries asking for a higher price - $4/kg, the bidders are all still keen. Then he tries something interesting. He asks them to give him a 50% share of the margin on the fad orange juice, because without him, they don’t have a market.

One of the juice makers agrees and offers to buy a years production upfront, deal done. and farmer is now getting paid multiples of the $2/kg. The other parties will have to start with planting new trees or try experiment in an unproven valley that takes years to prove up with no guarantee of success.

So coming back to the cobalt and the battery market.

The katanga valley is the DRC.

The orange farmers are the mines producing copper/cobalt concentrate.

The orange juice makers are the cobalt chemical producers/ cathode material producers.

Organic, sustainable juice is the equivalent to traceable, mechanically/heavy equipment mining (non-artisinal as Glencore operates)

The fad is the battery boom and the margins are disgustingly high for the chemical producers at $35/lb for cobalt and paying just 7-15% for contained cobalt in concentrate.

The competition has arrived, two SXEW plants looking to start pumping out juice, with no sources of “Organic, sustainable” oranges or mechanically mined copper/cobalt concentrate. To make matters more urgent, one major juice operation that had its own farms, Metorex has actually screwed up their mine plan and are buying their organic oranges on market (at coles) at a huge cost premium, still making bucket loads but needing to lock away feed.

The customers are insisting on organic, the options are limited, the margins are skewed towards juice makers and the competition is coming very very fast.

There will be some creative deals done by Farmer Arnesen to capture this value currently being locked away by the juice maker. Last I spoke to Farmer Arnesen he said that there is a lot of interest and desperation to secure offtake now, but in his experience the best way is to leave it to the last possible stage. The binding offtake is the prize and the suitors need to compete. You meet the suitors, you are polite, you discuss the product and the market and if they look like they can afford it you put them on the shortlist.

This waiting game raises in my mind the possibility of a takeover, at some stage it will be simply a matter of - “these Nzuri guys are holding out, there’s more and more competition coming, lets just take them out and start making juice!! there’s plenty more oranges coming in the 2nd orchard (stage 2 kalongwe), and the ground is fertile (ripe for more cobalt discoveries), and the price of “Juice” is only getting higher, lets pay what we need to pay to put this away”.

Now some smart Bob will inject their 2c and say Nzuri is too small. That's actually wrong, Nzuri already has defined 40,000 tonnes of contained cobalt, that is roughly 2.5 - 3M electric vehicles worth. That is extremely significant and there is more to come from the ground we hold, see for example the 7m at 1% cobalt intercept from a few weeks ago that all the canadian and european cobalt explorer's would have loved to report.

We are also fortunate enough to have greedy private equity holding a controlling stake in the company and they will want to have their cake and eat it, and have some cake for later too. So they could not care less what Bob has to say, Bob should go back to speculating on bitcoin.

Our job is to simply hold onto our shares and tune out the anti DRC melancholics.

The top 20 hold 90% of this company. How often do you hear “tightly held” but this is the real thing.

We barely need a handful of HNW to recognise the speculation here and it will rip upwards with every move in cobalt price, every development in the DRC market, exploration result or similar positive catalyst.

What are the risks - wholesale collapse of govt and society in DRC and Katanga.

The DRC can make you feel hope and despair at times in equal measure. It is a young country in age and in demographics and I believe the best years are ahead and the long term trend has been upward since the conflicts post Mobutu / Rwandan genocide.

It was encouraging to see that Alphamin have secured 80% of the $200M they need to finance a world class tin mine at the epicentre of conflicts in Kivu region.

There is tragedy and progress. I believe Kabila plans to remain in his position for many years to come but at the same time he will have to make improvements to security, transparency, food, water availability and power infrastructure for all citizens if he hopes to actually stick around. If he doesn’t, the most popular alternative figure to lead the country seems like he will.

My personal view is to think positively. We have recently opened an office in Lubumbashi looking at investing and starting up mineral and agriculture projects because we prefer to engage and reap the benefits of understanding the risks while operating ethically to sustainably build a business.

The way I see it, without the DRC all the EV bets are completely off. China wants to breathe clean air and I think they will have some pretty strong influence on ensuring stability.

Why is the EV market toast without the DRC share of production? All the other non-battery customers for cobalt can afford to pay much more than battery makers.

Battery makers will have to switch to less marketable, less energy dense and not as safe chemistries with zero cobalt as they wouldn’t be able to pay for cobalt and compete with ICE. LFP (Iron Phosphate chemistry with no Cobalt) has been proven to be most successful in commercial applications but not really mass market.

Should Katanga prove unable to continue supply, IMO TSLA, Panasonic stock would take a massive hit and that would be the first of many dominos. The EV and battery metals market at large has a lot of future growth already priced in and this would be cause a correction. Luckily Nzuri as of today still does not even have the base case at low payables and $18/lb priced in.

Re Substitution - Will cobalt be the best speculation in the electrification theme forever? I don’t know, but the next 5 years is a safe bet. The NMC chemistry still has a fair few years of improvements on the roadmap thanks to Panasonic. This period happens to cover the juiciest parts of our stage 1 project, which is light on CAPEX $50m and very quick to get online.

Bottom line - I’m not telling you to buy shares in Nzuri. Its not for everyone, I grew up in Africa and understand the landscape.

If you don’t have the conviction, don’t come near Nzuri. It is hard to build a position and you drag us all down if you chicken out and leave.

If you have the conviction and understand the risks, please hold strong, we don’t want to sell our oranges for $2/kg and let the juice makers make all the profits.

I’m saying, if you plan to buy, buy and hold because just like the cobalt market at large, there are not many shares available and through simple supply and demand dynamic we can get a much better price, this is a very exciting possibility for me, two choke points with many catalysts ahead to create pressure.

The main catalysts are simply: Exploration, Off6take and Financing. Of these three there will be joy from one or all avenues.

My guess is that this will all be finally topped up by a bid at a significant premium to market to end the misery off a lucky orange customer / juice maker.

Ok enough waffling, this cafe is closing

-----------------------------------------------------

I wanted to try and explain things around “payability” in laymans terms, and I by no means claim to be an expert, just piecing things together as I’ve been learning about this industry myself. Payability is simply what you will be paid for metal contained as a % of the metal contained.

So if you’ve got 1 tonne of dirt which has 10kg (1% grade) of a metal called X, and you go to a smelter, they may offer you terms that only means you get paid for 1kg of metal, even if you have 10kg in the dirt. Why - because they have costs involved in upgrading that 1% dirt to a saleable product and a sale price determined by the rest of market.

Now go back to the FS. As of the FS Nzuri are putting out a Copper/Cobalt concentrate with 19,360t of Copper and 1507t of Cobalt annually for 7 years.

Now using one indicative quote from an off-taker, given/tendered when cobalt was $15/lb, Nzuri are expecting to be paid for around 50% of the copper in the concentrate and a range of 7-15% of the cobalt.

Using last LME prices this gives us a pre-tax NPV of ~A$180M or A$47M in avg. annual profits.

Now for arguments sake, what if hypothetically Nzuri was paid 60% for contained copper and 40% for contained cobalt?

Using last LME price this gives us a pre-tax NPV of ~A$520M or $112m in avg. annual profits.

(Note this is all relating to the FS which is stage 1 only, no cobalt stockpiles or tailings or satellite deposits)

So a simple thing like the terms of the offtake contract have a very large impact on the Stage 1 project. Not that my personal expectation is quite that high but just showing why its important.

To understand what conditions could occur to allow such an uplift in value, I am going to look at oranges and orange juice, this is how I have to explain things to myself, with things you can eat.

Say there is an orange farmer and an orange juice producer. (note this is all a a vast simplification of the juice supply chain). Now normally the orange farmer sells his oranges to the juicer for a price related to the yield of his fellow farmers and the demand for oranges as a whole. This price is not so volatile.

Say for arguments sake this price is ~ $2/kg.

Now picture a situation where for some reason only the farmers in one particular valley, lets call this valley “Katanga” can produce enough oranges consistently enough to satisfy a big orange juice maker.

In this valley you have different kinds of orange production, some of them use immigrant labour to harvest, some use pesticides, some are completely automated, sustainable and organic.

It so happens that a new fad diet emerges called the “OJ cleanse” and the proponents of this diet insist that only sustainable, organic oranges can make the right orange juice, and you need to drink copious amounts of juice to be awesome.

The juice makers immediately secure supply with the organic farmers and start charging more for the organic juice.

The fad is wildly successful. The juice maker is able to charge over triple the amount they could have normally, but are still paying the farmer around $2/kg.

Now something interesting happens, other entrepreneurs notice the ridiculous margins the organic juice has and new juice makers start being established.

Now there’s only one valley, the Katanga valley, that has the consistent and scalable production. To make matters worse, they can only use farmers who are sustainable, organic, which is again a subset of the Katanga subset. To make matters even worse there are market speculators stockpiling organic oranges understanding that juice makers can afford to pay much more.

Now the organic, sustainable juice farmer in the Katanga valley has multiple parties knocking on his door asking for organic oranges. He only has a certain sized orchard but now far more customers than he has oranges, so he tries asking for a higher price - $4/kg, the bidders are all still keen. Then he tries something interesting. He asks them to give him a 50% share of the margin on the fad orange juice, because without him, they don’t have a market.

One of the juice makers agrees and offers to buy a years production upfront, deal done. and farmer is now getting paid multiples of the $2/kg. The other parties will have to start with planting new trees or try experiment in an unproven valley that takes years to prove up with no guarantee of success.

So coming back to the cobalt and the battery market.

The katanga valley is the DRC.

The orange farmers are the mines producing copper/cobalt concentrate.

The orange juice makers are the cobalt chemical producers/ cathode material producers.

Organic, sustainable juice is the equivalent to traceable, mechanically/heavy equipment mining (non-artisinal as Glencore operates)

The fad is the battery boom and the margins are disgustingly high for the chemical producers at $35/lb for cobalt and paying just 7-15% for contained cobalt in concentrate.

The competition has arrived, two SXEW plants looking to start pumping out juice, with no sources of “Organic, sustainable” oranges or mechanically mined copper/cobalt concentrate. To make matters more urgent, one major juice operation that had its own farms, Metorex has actually screwed up their mine plan and are buying their organic oranges on market (at coles) at a huge cost premium, still making bucket loads but needing to lock away feed.

The customers are insisting on organic, the options are limited, the margins are skewed towards juice makers and the competition is coming very very fast.

There will be some creative deals done by Farmer Arnesen to capture this value currently being locked away by the juice maker. Last I spoke to Farmer Arnesen he said that there is a lot of interest and desperation to secure offtake now, but in his experience the best way is to leave it to the last possible stage. The binding offtake is the prize and the suitors need to compete. You meet the suitors, you are polite, you discuss the product and the market and if they look like they can afford it you put them on the shortlist.

This waiting game raises in my mind the possibility of a takeover, at some stage it will be simply a matter of - “these Nzuri guys are holding out, there’s more and more competition coming, lets just take them out and start making juice!! there’s plenty more oranges coming in the 2nd orchard (stage 2 kalongwe), and the ground is fertile (ripe for more cobalt discoveries), and the price of “Juice” is only getting higher, lets pay what we need to pay to put this away”.

Now some smart Bob will inject their 2c and say Nzuri is too small. That's actually wrong, Nzuri already has defined 40,000 tonnes of contained cobalt, that is roughly 2.5 - 3M electric vehicles worth. That is extremely significant and there is more to come from the ground we hold, see for example the 7m at 1% cobalt intercept from a few weeks ago that all the canadian and european cobalt explorer's would have loved to report.

We are also fortunate enough to have greedy private equity holding a controlling stake in the company and they will want to have their cake and eat it, and have some cake for later too. So they could not care less what Bob has to say, Bob should go back to speculating on bitcoin.

Our job is to simply hold onto our shares and tune out the anti DRC melancholics.

The top 20 hold 90% of this company. How often do you hear “tightly held” but this is the real thing.

We barely need a handful of HNW to recognise the speculation here and it will rip upwards with every move in cobalt price, every development in the DRC market, exploration result or similar positive catalyst.

What are the risks - wholesale collapse of govt and society in DRC and Katanga.

The DRC can make you feel hope and despair at times in equal measure. It is a young country in age and in demographics and I believe the best years are ahead and the long term trend has been upward since the conflicts post Mobutu / Rwandan genocide.

It was encouraging to see that Alphamin have secured 80% of the $200M they need to finance a world class tin mine at the epicentre of conflicts in Kivu region.

There is tragedy and progress. I believe Kabila plans to remain in his position for many years to come but at the same time he will have to make improvements to security, transparency, food, water availability and power infrastructure for all citizens if he hopes to actually stick around. If he doesn’t, the most popular alternative figure to lead the country seems like he will.

My personal view is to think positively. We have recently opened an office in Lubumbashi looking at investing and starting up mineral and agriculture projects because we prefer to engage and reap the benefits of understanding the risks while operating ethically to sustainably build a business.

The way I see it, without the DRC all the EV bets are completely off. China wants to breathe clean air and I think they will have some pretty strong influence on ensuring stability.

Why is the EV market toast without the DRC share of production? All the other non-battery customers for cobalt can afford to pay much more than battery makers.

Battery makers will have to switch to less marketable, less energy dense and not as safe chemistries with zero cobalt as they wouldn’t be able to pay for cobalt and compete with ICE. LFP (Iron Phosphate chemistry with no Cobalt) has been proven to be most successful in commercial applications but not really mass market.

Should Katanga prove unable to continue supply, IMO TSLA, Panasonic stock would take a massive hit and that would be the first of many dominos. The EV and battery metals market at large has a lot of future growth already priced in and this would be cause a correction. Luckily Nzuri as of today still does not even have the base case at low payables and $18/lb priced in.

Re Substitution - Will cobalt be the best speculation in the electrification theme forever? I don’t know, but the next 5 years is a safe bet. The NMC chemistry still has a fair few years of improvements on the roadmap thanks to Panasonic. This period happens to cover the juiciest parts of our stage 1 project, which is light on CAPEX $50m and very quick to get online.

Bottom line - I’m not telling you to buy shares in Nzuri. Its not for everyone, I grew up in Africa and understand the landscape.

If you don’t have the conviction, don’t come near Nzuri. It is hard to build a position and you drag us all down if you chicken out and leave.

If you have the conviction and understand the risks, please hold strong, we don’t want to sell our oranges for $2/kg and let the juice makers make all the profits.

I’m saying, if you plan to buy, buy and hold because just like the cobalt market at large, there are not many shares available and through simple supply and demand dynamic we can get a much better price, this is a very exciting possibility for me, two choke points with many catalysts ahead to create pressure.

The main catalysts are simply: Exploration, Off6take and Financing. Of these three there will be joy from one or all avenues.

My guess is that this will all be finally topped up by a bid at a significant premium to market to end the misery off a lucky orange customer / juice maker.

Ok enough waffling, this cafe is closing

Macht einfach nur Spaß der Wert, schon 37 audcent

Capital Raise

Ich hoffe sie bekommen es besser hin als WKT.

Ich hoffe sie bekommen es besser hin als WKT.

Antwort auf Beitrag Nr.: 56.435.529 von Reiners am 12.12.17 23:40:42ja, jetzt erst gesehen...

anstieg war steil... befürchte da auch dass es etwas niedrig sein könnte.

0,25 AUD oder sowas in der art

anstieg war steil... befürchte da auch dass es etwas niedrig sein könnte.

0,25 AUD oder sowas in der art

Starker "strategischer" Investor aus China steigt ein.

Huayou cobalt invests in Nzuri for A$10m.

NZC totaling 10M at price of 0.2507 per share. after allotment, they become the second share holder with proportion of14.7%

---------------------

Hier eine Präsi von Ihm

http://en.huayou.com/downloadRepository/cfd6baf6-6aba-4846-9…

-----------------------

Würde sagen, hätte und schlechter treffen können.

Huayou cobalt invests in Nzuri for A$10m.

NZC totaling 10M at price of 0.2507 per share. after allotment, they become the second share holder with proportion of14.7%

---------------------

Hier eine Präsi von Ihm

http://en.huayou.com/downloadRepository/cfd6baf6-6aba-4846-9…

-----------------------

Würde sagen, hätte und schlechter treffen können.

Antwort auf Beitrag Nr.: 56.439.867 von Reiners am 13.12.17 16:26:10naja hab ja auf 0,25 AUD getippt... von daher sag ich mal: den erwartungen entsprechend

Antwort auf Beitrag Nr.: 56.439.887 von Boersiback am 13.12.17 16:28:23Es geht nicht nur um den Price, sondern auch um die Adresse.

Pricing - If I recall, AVZ was close to 9c when Huayou came in at 7c with a free 10c option. It went to the moon shortly after.

Aktueller Price von AVZ ist 21c

Pricing - If I recall, AVZ was close to 9c when Huayou came in at 7c with a free 10c option. It went to the moon shortly after.

Aktueller Price von AVZ ist 21c

Antwort auf Beitrag Nr.: 56.439.959 von Reiners am 13.12.17 16:34:31Die unmittelbare Reaktion nach Wiederaufnahme des Handels bei AVZ sah so aus:

(laut IB Broker Chart)

letzter Kurs vor Trading Halt: 8.8 cents

Schlusskurs naechster Handelstag 9.2 cents (Tief: 8.6 cents, Hoch 10.0 cents).

(laut IB Broker Chart)

letzter Kurs vor Trading Halt: 8.8 cents

Schlusskurs naechster Handelstag 9.2 cents (Tief: 8.6 cents, Hoch 10.0 cents).

So News ist da.

Liest sich extrem gut.

Liest sich extrem gut.

Antwort auf Beitrag Nr.: 56.443.273 von Reiners am 13.12.17 23:58:35http://www.asx.com.au/asxpdf/20171214/pdf/43q5601k40f78n.pdf

ja, liest sich seh schön...

auch bzgl des JV mit ivanhoe kann man also was erwarten evtl.

ja, liest sich seh schön...

auch bzgl des JV mit ivanhoe kann man also was erwarten evtl.

Antwort auf Beitrag Nr.: 56.443.424 von Boersiback am 14.12.17 01:08:50Dafür ist der Capital Raise bei WKT aber sowas von in die Hose gegangen.

Antwort auf Beitrag Nr.: 56.443.427 von Reiners am 14.12.17 01:11:11ui bei WKT schepperts aber grad

The Rights Issue is to be underwritten by Patersons up to $6.2 million.

Es wird vermutet das Patersons dahintersteckt und den Kurs unter 10 c drückt, damit keiner zeichnet und sie den shortfall bis zu ca. 62 Mio Akien absahnen können.

Es wird vermutet das Patersons dahintersteckt und den Kurs unter 10 c drückt, damit keiner zeichnet und sie den shortfall bis zu ca. 62 Mio Akien absahnen können.

Antwort auf Beitrag Nr.: 56.443.427 von Reiners am 14.12.17 01:11:11eine "OT" Frage:

hast Du Was für "PGMs" übrig?

ich hatte Dir eine eigentlich ein sehr lange BM

-mit, zur Abwechslung - mal richtig Viel Mühe(geht echt auch, Schaltjahr)- geschrieben,

dann ging Irgendwas mit kopieren/einfügen schief, weg.( )

)

wenn Ja würde ich Dich mal auf Ein Projekt verweisen,

mich reizt Das Ding ziemlich muss ich sagen, aber habe Diese Aktie nicht.

der BBack ist schon Anteilshaber.

also ich finde Das hat schon "richtig, richtig Viele interessante Punkte".

abseits davon: Gratulation NZC.

mir sieht Die Wahrscheinlichkeit Hier über Einen künftigen Producer zu reden ziemlich, ziemlich hoch aus.

(und Kinder wollnse ja glaube ich nicht anstellen)

hast Du Was für "PGMs" übrig?

ich hatte Dir eine eigentlich ein sehr lange BM

-mit, zur Abwechslung

- mal richtig Viel Mühe(geht echt auch, Schaltjahr)- geschrieben,dann ging Irgendwas mit kopieren/einfügen schief, weg.(

)

)wenn Ja würde ich Dich mal auf Ein Projekt verweisen,

mich reizt Das Ding ziemlich muss ich sagen, aber habe Diese Aktie nicht.

der BBack ist schon Anteilshaber.

also ich finde Das hat schon "richtig, richtig Viele interessante Punkte".

abseits davon: Gratulation NZC.

mir sieht Die Wahrscheinlichkeit Hier über Einen künftigen Producer zu reden ziemlich, ziemlich hoch aus.

(und Kinder wollnse ja glaube ich nicht anstellen)

Was sind PGMs?

"Tembo Capital" ist Übrigens m.W.('s) "viel in Afrika unterwegs".

Antwort auf Beitrag Nr.: 56.443.454 von Reiners am 14.12.17 01:34:15Platin Group Metals(/Elements)

Antwort auf Beitrag Nr.: 56.443.463 von Popeye82 am 14.12.17 01:41:05Keine Ahnung,

Mach dir nicht so viel Arbeit.

Aktuell habe ich genug anderes um die Ohren.

Meine Pferde, bis auf Nzuri, laufen aktuell nicht so gut. Muss ich mich erstmal drum kümmern

Mach dir nicht so viel Arbeit.

Aktuell habe ich genug anderes um die Ohren.

Meine Pferde, bis auf Nzuri, laufen aktuell nicht so gut. Muss ich mich erstmal drum kümmern

Antwort auf Beitrag Nr.: 56.443.463 von Popeye82 am 14.12.17 01:41:05meinst du den wert den ich habe ?

Antwort auf Beitrag Nr.: 56.443.472 von Reiners am 14.12.17 01:46:23Popeye macht sich immer viel arbeit.

der fleissigste bei ganz WO

der fleissigste bei ganz WO

Boersiback hast du noch was rausgefunden über den Grund des Kursverfalls bei WKT?

Popeye hat den Wert ja glaube ich nicht

Popeye hat den Wert ja glaube ich nicht

Antwort auf Beitrag Nr.: 56.443.496 von Reiners am 14.12.17 01:57:12nö, ist mir ein rätsel... wobei nach der KE dachte ich schon könnt auf 0,10 zurückgehen.

aber weshalb heute auch noch darunter bei 18% down...

kann nix finden.

aber weshalb heute auch noch darunter bei 18% down...

kann nix finden.

Antwort auf Beitrag Nr.: 56.443.472 von Reiners am 14.12.17 01:46:23ich denke anhand Der Kurzumschreibung kannst Du schon ganz schnell sagen wenn es Dich NICHT interessiert:

"Jangada Mines plc IS focused, on developing, the Pedra Branca PGM Project ('the Project'), one of the largest undeveloped PGM projects outside of Africa, with the potential to supply a market in long-term deficit. The Company is aiming to establish a low cost, low capex open pit mine, with a target to produce 30,000 oz/annum by the end of 2018 from three existing mining licences with mineralisation commencing at surface. The Project has a JORC (2012) Compliant Resource of approximately 1 million ounces of PGM+Au at a grade of 1.3 g/t, 109Mlbs of Ni, 23Mlbs of Cu, 6.4Mlbs of Co and 670kt of Cr. Circa 52% of this is contained within current mining licences and is considered a low development risk due to previous exploration work totalling + US$35 million. Additionally, the Company owns a further 44 exploration licences spanning 55,000 hectares, which have significant upside potential for PGM, nickel, copper, chrome, rhodium, gold, and vanadium. The team has a wealth of experience, not only of the Project but of mining in South America across a range of commodities."

wenn doch......................................

guck mal Hier:

(relevanteste "bulk"informationen link1-3)

https://polaris.brighterir.com/public/jangada_mines/news/rns…

http://www.jangadamines.com/docs/Jangada%20Mines%20plc%20-%2…

http://www.beaufortsecurities.com/shp/research.php?vid=415

http://www.sharepickers.com/3-reasons-add-jangada-mines-jan-…

die Herleitung/history Des Projektes macht für mich schon Sinn(für einen "major nicht groß genug", usw).

was mir auch noch nicht so ganz einleuchtet ist Was Sie in der Vielen Zeit-"zwischen" Kauf und Börsengang(s. Interview)- gemacht haben.

also es hört sich für Mich-jedenfalls- so ann dass Sie Diese Zeit "speziell" "penibel und sensibel" genutzt haben(weiss nur nicht wirklich mit Was. Konkret.).

also ich kann bis dato sagen dass mir Viele, Viele Punkte schon richtig, richtig gut gefallen,

aber mir Die knicki"knack"punkte noch nicht so richtig klar sind.

wenn uninteressant: no prob,

wenn doch wäre es aber schade nicht darauf hingewiesen zu haben.

p.S.

die Websitebenutzung ist bei den Briten Irgendwie unter Aller ********************** (.)

pp.S.

wenn es bei Dir wohl "gerade nicht so gut läuft":

stecke nicht da drin, keine Ahnung.

aber Wenn Der Letzte Monat Dein Bester Monat Aller Zeiten war,

und Es Jetzt von Einer, extremer, "Spitze" mal deutlicher runtergeht

muss man Das "vielleicht auch nicht überbewerten".

"bmann" kannst auch Was sagen, Wenn Du willst.

"Jangada Mines plc IS focused, on developing, the Pedra Branca PGM Project ('the Project'), one of the largest undeveloped PGM projects outside of Africa, with the potential to supply a market in long-term deficit. The Company is aiming to establish a low cost, low capex open pit mine, with a target to produce 30,000 oz/annum by the end of 2018 from three existing mining licences with mineralisation commencing at surface. The Project has a JORC (2012) Compliant Resource of approximately 1 million ounces of PGM+Au at a grade of 1.3 g/t, 109Mlbs of Ni, 23Mlbs of Cu, 6.4Mlbs of Co and 670kt of Cr. Circa 52% of this is contained within current mining licences and is considered a low development risk due to previous exploration work totalling + US$35 million. Additionally, the Company owns a further 44 exploration licences spanning 55,000 hectares, which have significant upside potential for PGM, nickel, copper, chrome, rhodium, gold, and vanadium. The team has a wealth of experience, not only of the Project but of mining in South America across a range of commodities."

wenn doch......................................

guck mal Hier:

(relevanteste "bulk"informationen link1-3)

https://polaris.brighterir.com/public/jangada_mines/news/rns…

http://www.jangadamines.com/docs/Jangada%20Mines%20plc%20-%2…

http://www.beaufortsecurities.com/shp/research.php?vid=415

http://www.sharepickers.com/3-reasons-add-jangada-mines-jan-…

die Herleitung/history Des Projektes macht für mich schon Sinn(für einen "major nicht groß genug", usw).

was mir auch noch nicht so ganz einleuchtet ist Was Sie in der Vielen Zeit-"zwischen" Kauf und Börsengang(s. Interview)- gemacht haben.

also es hört sich für Mich-jedenfalls- so ann dass Sie Diese Zeit "speziell" "penibel und sensibel" genutzt haben(weiss nur nicht wirklich mit Was. Konkret.).

also ich kann bis dato sagen dass mir Viele, Viele Punkte schon richtig, richtig gut gefallen,

aber mir Die knicki"knack"punkte noch nicht so richtig klar sind.

wenn uninteressant: no prob,

wenn doch wäre es aber schade nicht darauf hingewiesen zu haben.

p.S.

die Websitebenutzung ist bei den Briten Irgendwie unter Aller ********************** (.)

pp.S.

wenn es bei Dir wohl "gerade nicht so gut läuft":

stecke nicht da drin, keine Ahnung.

aber Wenn Der Letzte Monat Dein Bester Monat Aller Zeiten war,

und Es Jetzt von Einer, extremer, "Spitze" mal deutlicher runtergeht

muss man Das "vielleicht auch nicht überbewerten".

"bmann" kannst auch Was sagen, Wenn Du willst.

closed on the 200MA, 36c as seen below strong resistance. Break above and we should go back into the 50-60c channel.

1. Nzuri brings Chinese cobalt giant to its register

https://thewest.com.au/business/nzuri-brings-chinese-cobalt-…

2.

https://thewest.com.au/business/nzuri-brings-chinese-cobalt-…

2.

Der Riese, Nachbar und Partner Ivanhoe Mines

100 mal mehr Kupfer, groesste High-Grade Ressource der Welt

Untertagemine geplant/im Bau

https://www.ivanhoemines.com/site/assets/files/3608/ivanhoe_…

(kein Hinweis auf Kobalt)

Vorsicht gebietet das politische Umfeld

https://www.bloomberg.com/news/articles/2017-07-17/ivanhoe-s…

100 mal mehr Kupfer, groesste High-Grade Ressource der Welt

Untertagemine geplant/im Bau

https://www.ivanhoemines.com/site/assets/files/3608/ivanhoe_…

(kein Hinweis auf Kobalt)

Vorsicht gebietet das politische Umfeld

https://www.bloomberg.com/news/articles/2017-07-17/ivanhoe-s…

Antwort auf Beitrag Nr.: 56.461.277 von Reiners am 15.12.17 16:15:30und Reiners,

2fragen:

du scheinst ja schon ganz schön an den E-metals "dran"zuhängen:

1) hast Du eigentlich eine Meinung zu "Tesla", der Ganzen (R)E-volution?

2) hast Du Eine Meinung zu den Celsius Schreiben? -25.398, Bezugsff:

https://www.wallstreet-online.de/diskussion/1139490-25391-25…

eigener Hintergrund: bin Dir bei CLA und NZC ge"folgt",

nach aktuellem Stand sind auf "Sicht" noch 2 Transaktionen-inkl. wahrscheinlich Deiner "LIN"- geplant,

dann abgeschlossen(Was sich "vielleicht noch ergibt", umjustiert werden muss usw, hat man aber eh immer noch keine Ahnung, also da: 0plan(erfahrungsgemäss wird dann da sicher auch noch "Einiges" passieren).

und wäre vielleicht nicht schlecht da noch 1,2 rauszu"schmeissen".

bei Celsius bin ich, da, jetzt am überlegen.

2fragen:

du scheinst ja schon ganz schön an den E-metals "dran"zuhängen:

1) hast Du eigentlich eine Meinung zu "Tesla", der Ganzen (R)E-volution?

2) hast Du Eine Meinung zu den Celsius Schreiben? -25.398, Bezugsff:

https://www.wallstreet-online.de/diskussion/1139490-25391-25…

eigener Hintergrund: bin Dir bei CLA und NZC ge"folgt",

nach aktuellem Stand sind auf "Sicht" noch 2 Transaktionen-inkl. wahrscheinlich Deiner "LIN"- geplant,

dann abgeschlossen(Was sich "vielleicht noch ergibt", umjustiert werden muss usw, hat man aber eh immer noch keine Ahnung, also da: 0plan(erfahrungsgemäss wird dann da sicher auch noch "Einiges" passieren).

und wäre vielleicht nicht schlecht da noch 1,2 rauszu"schmeissen".

bei Celsius bin ich, da, jetzt am überlegen.

Antwort auf Beitrag Nr.: 56.465.402 von bmann025 am 16.12.17 02:09:45Der Riese, Nachbar und Partner Ivanhoe Mines 100 mal mehr Kupfer, groesste High-Grade Ressource der Welt Untertagemine geplant/im Bau https://www.ivanhoemines.com/site/assets/files/3608/ivanhoe_… (kein Hinweis auf Kobalt) Vorsicht gebietet das politische Umfeld https://www.bloomberg.com/news/articles/2017-07-17/ivanhoe-s…

____________________________________________________________________________

Meinung zu dem Teil???

____________________________________________________________________________

Meinung zu dem Teil???

Antwort auf Beitrag Nr.: 56.471.717 von Popeye82 am 17.12.17 13:23:42

1) hast Du eigentlich eine Meinung zu "Tesla", der Ganzen (R)E-volution?

Tesla ist nix für mich, auch Du teuer.

Der Ganzen (R)E-volution werde ich langsam immer positiver gestimmt, hielt das bis vor kurzem für einen Medien Hype. Denke jetzt eher in den benötigenden Rohsoffen.

Lithium : der alte Star, könnte noch ein Jahr laufen

Cobalt: der Star 2018 und wahrscheinlich bis 2020

Grafite: Ein weiterer Star ab 2019

Für Lithium habe ich einen near term producer Tawana und early stage noch WKT

Für Cobalt Nzuri und noch CLA als Zweitwert

Für Grafit WKT und an zweiter Stelle BKT

2) hast Du Eine Meinung zu den Celsius Schreiben? -25.398, Bezugsff:

Bin auch etwas skeptischer geworden aber ich kann nicht nur auf Nzuri setzten und als Zweitwert taugt CLA. Im anstehenden Cobalt Hype wird CLA schon mitgezogen

1) hast Du eigentlich eine Meinung zu "Tesla", der Ganzen (R)E-volution?

Tesla ist nix für mich, auch Du teuer.

Der Ganzen (R)E-volution werde ich langsam immer positiver gestimmt, hielt das bis vor kurzem für einen Medien Hype. Denke jetzt eher in den benötigenden Rohsoffen.

Lithium : der alte Star, könnte noch ein Jahr laufen

Cobalt: der Star 2018 und wahrscheinlich bis 2020

Grafite: Ein weiterer Star ab 2019

Für Lithium habe ich einen near term producer Tawana und early stage noch WKT

Für Cobalt Nzuri und noch CLA als Zweitwert

Für Grafit WKT und an zweiter Stelle BKT

2) hast Du Eine Meinung zu den Celsius Schreiben? -25.398, Bezugsff:

Bin auch etwas skeptischer geworden aber ich kann nicht nur auf Nzuri setzten und als Zweitwert taugt CLA. Im anstehenden Cobalt Hype wird CLA schon mitgezogen

Danke,

ich meinte Tesla allerdings nicht als "Aktie"(lohnt "sich zu kaufenn, oder nicht...??"),

sondern als "Industry player".

bei Celsius mal noch überlegen,

aber 1,2noch raus wäre schon gut.

ich meinte Tesla allerdings nicht als "Aktie"(lohnt "sich zu kaufenn, oder nicht...??"),

sondern als "Industry player".

bei Celsius mal noch überlegen,

aber 1,2noch raus wäre schon gut.

Ich behalte meine CLA

würde gerne rein. habe aber eine order unter 0,3 aud und würde hoffen dass der kurs noch etwas nachgibt in Richtung placement preis

Ja aber doch nicht mit den Modellen die sie aktuell im Angebot haben. Kenne niemanden der sich den i3 freiwillig zulegen würde. Der i8 ist doch fern von jeglichem Mainstream. Welcher Normalo soll sich den denn leisten? Und ob die so einfach in ihre anderen Modelle ein e-modul einbauen können bleibt abzuwarten.

Also BMW kann ich noch nicht ganz ernst nehmen.

Also BMW kann ich noch nicht ganz ernst nehmen.

na Das ist ja total peinlich dass ich Dies behauptete.

ich gehe mich nun auspeitschen.

ich gehe mich nun auspeitschen.

Antwort auf Beitrag Nr.: 56.522.435 von Popeye82 am 21.12.17 21:14:30ja, züchtige dich und lerne disziplin

Antwort auf Beitrag Nr.: 56.522.435 von Popeye82 am 21.12.17 21:14:30Ne wollte ich auch gar nicht weiter unterstellen.

Auspeitschen klingt trotzdem gut!

Ging mir nur um die Witznummer BMW. Ob wer das genau so sieht wie ich ist eine andere Geschichte.

Auspeitschen klingt trotzdem gut!

Ging mir nur um die Witznummer BMW. Ob wer das genau so sieht wie ich ist eine andere Geschichte.

von Donnerpowers Geteilten Links, Weiterführung.

Kobaltfreaks sollten mal ansehen:

http://www.deutsche-rohstoffagentur.de/DE/Gemeinsames/Produk…

Kobaltfreaks sollten mal ansehen:

http://www.deutsche-rohstoffagentur.de/DE/Gemeinsames/Produk…

Glencore and other miners entreat Congo to rethink damaging new laws

https://www.businesslive.co.za/bd/companies/mining/2017-12-2…

https://www.businesslive.co.za/bd/companies/mining/2017-12-2…

Problem is we can't fix the problem

http://www.mining-journal.com/politics/news/1310295/-fix-don…

http://www.mining-journal.com/politics/news/1310295/-fix-don…

Antwort auf Beitrag Nr.: 56.630.981 von Popeye82 am 05.01.18 17:41:20und mal wieder die Sensation

im übrigen nix neues mit Lithium und Eisen:

Lithium iron oxide as alternative anode for li-ion batteries

https://www.sciencedirect.com/science/article/pii/S146660490…

....aus dem jahre 2000

das problem sind immer die absoluten durchbrüche andauernd seit vielen jahren in dem sektor.

und wenn man dann mal neutrale und zugleich wissenschaftliche artikel findet, werden solche neugikeiten oft komplett vernichtend erklärt.

das machts halt schwierig... kobalt an für sich ist im sektor "gefährdet". lithium weniger.

dafür gitbs lithium in massen. wenn chile und bolivien hochfahren ist die welt mit lowcost-lithium auf 5.000 jahre versorgt.

von daher immer aufpassen... kupfer bleibt mein lieblingsmetall, gefolgt von gold, silber, nickel...

bei kobalt und lithium muss man die zeitfenster besonders gut treffen.

im übrigen nix neues mit Lithium und Eisen:

Lithium iron oxide as alternative anode for li-ion batteries

https://www.sciencedirect.com/science/article/pii/S146660490…

....aus dem jahre 2000

das problem sind immer die absoluten durchbrüche andauernd seit vielen jahren in dem sektor.

und wenn man dann mal neutrale und zugleich wissenschaftliche artikel findet, werden solche neugikeiten oft komplett vernichtend erklärt.

das machts halt schwierig... kobalt an für sich ist im sektor "gefährdet". lithium weniger.

dafür gitbs lithium in massen. wenn chile und bolivien hochfahren ist die welt mit lowcost-lithium auf 5.000 jahre versorgt.

von daher immer aufpassen... kupfer bleibt mein lieblingsmetall, gefolgt von gold, silber, nickel...

bei kobalt und lithium muss man die zeitfenster besonders gut treffen.

Antwort auf Beitrag Nr.: 56.638.751 von Boersiback am 06.01.18 19:18:21Schwierig zu sagen,

aber prinzipiell ist es eben oft in Diesen Bereichen,

bei Vielen(technischen) DIngen, Die sich(mit "Wehen"(Letztlich(Irgendwann))) durchsetzen nach Dem Prinzip:

"1.000 versuchens, 999 rennen gegen Die Wand, und 1ner schaffts. Irgendwann".

(und wenns EIner ge"packt" hat wird, natürlich, oft Irgendwann Die "Burg gestürmt")

So auf Die Aaaaart ist Es schon bei Vielen Unserer "(technischen) Errungenschaften" gewesen.

Also prinzipiell sind Das ganz, gaaaanz Normale Entwicklungs"cycles".

aber prinzipiell ist es eben oft in Diesen Bereichen,

bei Vielen(technischen) DIngen, Die sich(mit "Wehen"(Letztlich(Irgendwann))) durchsetzen nach Dem Prinzip:

"1.000 versuchens, 999 rennen gegen Die Wand, und 1ner schaffts. Irgendwann".

(und wenns EIner ge"packt" hat wird, natürlich, oft Irgendwann Die "Burg gestürmt")

So auf Die Aaaaart ist Es schon bei Vielen Unserer "(technischen) Errungenschaften" gewesen.

Also prinzipiell sind Das ganz, gaaaanz Normale Entwicklungs"cycles".

Antwort auf Beitrag Nr.: 56.639.627 von Popeye82 am 06.01.18 22:42:58Also prinzipiell sind Das ganz, gaaaanz Normale Entwicklungs"cycles".

_____________________________________________________

nur halt wharpspeed, mittlerweile.

_____________________________________________________

nur halt wharpspeed, mittlerweile.

Nzuri Copper bags funds from US$8 billion Chinese cobalt player

http://www.proactiveinvestors.com.au/companies/news/189748/n…

http://www.proactiveinvestors.com.au/companies/news/189748/n…

http://www.reuters.com/article/us-autoshow-detroit-electric/global-carmakers-to-invest-at-least-90-billion-in-electric-vehicles-idUSKBN1F42NW

Nzuri Copper – Management Interview

Management Profile

Adam Smits (COO & Executive Director)

Mechanical Engineer with 20 year's experience in Australia and West Africa & lived in francophone West Africa for 8 years. Past senior positions with Perseus Mining, TiZir Ltd, Mineral Deposits Ltd, Placer Dome Asia Pacific and Lycopodium Engineering

Mark Arnesen (CEO & Executive Director)

Mark is a Chartered Accountant with extensive expertise in structuring and negotiating finance for major resource projects. Mark Has strong DRC experience with Moto Goldmines along with prior senior positions with Billiton, Ashanti Goldfields, Equinox Minerals; non-executive Director of Centamin PLC

What is your rationale for attending 121 Mining Investment?

Raising awareness of Nzrui copper/ Cobalt an the quality of the copper/ Cobalt asset and its stage in the development curve

What recent news would you like to highlight to investors attending?

Recent ASX release dated 13/12/17 - A$10M Strategic investment by Huayou Cobalt

What are your key goals for the next 3, 6 and 12 months?

3 Months:

Successful Leaching/ SXEW testwork program & scoping study

Ongoing Off-take discussions

6 Months:

Completion of Pre-feasibility on Leaching/ SXEW options

Commenced early-works site program

12 Months:

Successful exploration on the FBTJV with additional resource added to the Kalongwe project

What do you see as the key risks and challenges facing your company at the moment and how are you overcoming these?

Key risk:- Funding of project development

How do we overcome:- Strategic Investors Tembo/ Huayou

In a sentence, what do you think makes your company such a compelling investment?

Near term exposure to Cobalt/ Copper production

Management Profile

Adam Smits (COO & Executive Director)

Mechanical Engineer with 20 year's experience in Australia and West Africa & lived in francophone West Africa for 8 years. Past senior positions with Perseus Mining, TiZir Ltd, Mineral Deposits Ltd, Placer Dome Asia Pacific and Lycopodium Engineering

Mark Arnesen (CEO & Executive Director)

Mark is a Chartered Accountant with extensive expertise in structuring and negotiating finance for major resource projects. Mark Has strong DRC experience with Moto Goldmines along with prior senior positions with Billiton, Ashanti Goldfields, Equinox Minerals; non-executive Director of Centamin PLC

What is your rationale for attending 121 Mining Investment?

Raising awareness of Nzrui copper/ Cobalt an the quality of the copper/ Cobalt asset and its stage in the development curve

What recent news would you like to highlight to investors attending?

Recent ASX release dated 13/12/17 - A$10M Strategic investment by Huayou Cobalt

What are your key goals for the next 3, 6 and 12 months?

3 Months:

Successful Leaching/ SXEW testwork program & scoping study

Ongoing Off-take discussions

6 Months:

Completion of Pre-feasibility on Leaching/ SXEW options

Commenced early-works site program

12 Months:

Successful exploration on the FBTJV with additional resource added to the Kalongwe project

What do you see as the key risks and challenges facing your company at the moment and how are you overcoming these?

Key risk:- Funding of project development

How do we overcome:- Strategic Investors Tembo/ Huayou

In a sentence, what do you think makes your company such a compelling investment?

Near term exposure to Cobalt/ Copper production

http://www.mining.com/web/congo-seeks-cobalt-market-control-…

"(Bloomberg) — The Democratic Republic of Congo will seek greater control of the global cobalt market by engaging directly with car and battery manufacturers, according to its largest state-owned mining company.

"I find it scandalous that when cobalt is discussed, and the explosion of electric vehicles, only the traders and consumers are referenced and Congo and Gecamines are not cited," Gecamines Chairman Albert Yuma said in an interview in Cape Town.

The market seems to think that "the future of cobalt is in the hands of Glencore, Trafigura and CMOC but not the Congo or Gecamines," Yuma said. "We legitimately want to control the cobalt market because it is ours."

Congo accounts for about two-thirds of global cobalt supply. The country isn’t benefiting from rallying copper and cobalt prices and plans to renegotiate partnerships with international mining companies, Yuma said earlier Monday.

Read more: Congo’s Gecamines Plans to Renegotiate Mining Agreements

Gecamines has already held discussion with one large Chinese battery producer about establishing a joint venture to develop the state-owned miner’s cobalt concessions, Yuma said. It is also planning discussions with a Chinese car manufacturer, he added, declining to identify either company.

Consumers want to secure, stable, long-term supply and, unlike traders, don’t speculate on price, he said.

(Written by Tom Wilson)"

Antwort auf Beitrag Nr.: 56.948.585 von Popeye82 am 06.02.18 13:41:59was macht mister popeye eigentlich bei solchen marktphasen die nicht mehr vom newsflow geprägt sind ?

ich lass bisher noch munter laufen... so wie ich dich kenne, ist das unsere gemeinsamkeit

ich lass bisher noch munter laufen... so wie ich dich kenne, ist das unsere gemeinsamkeit

Antwort auf Beitrag Nr.: 56.953.070 von Boersiback am 06.02.18 19:12:35Also ich halte.

Ob Das richtig ist, wird sich zeigen.

Wer von Nzuri Was hält, Der hat vermutlich gerade Jetzt eher Chancen.

Ob Das richtig ist, wird sich zeigen.

Wer von Nzuri Was hält, Der hat vermutlich gerade Jetzt eher Chancen.

Antwort auf Beitrag Nr.: 56.956.676 von Popeye82 am 07.02.18 07:25:33würd ich auch so sehen...

im allgemeinen waren die anstieg ab mitte dezember extrem steil. sowas wird dann meistens ein stück weit abverkauft. bei so zeugs kann man dann durchaus einfache charttechnik nehmen wie 61,8 Fibo. den anstieg berechnen und eben diese 61,8% davon abziehen. dann hat man den zu erwartenden konsokurs. ist doch recht beliebt diese zahl

15 cents auf 48 cents... 0,27x naja war en bischen drunter... aber die richtung stimmt sehr oft... vorausgesetzt die hausse geht dann weiter...

ich hab nur die sorge 2008 reloaded nur viel schlimmer...

das system macht mir immer mehr angst... schulden, billigkredite. blasen aller art...

dann können wir hier komplett einpacken

im allgemeinen waren die anstieg ab mitte dezember extrem steil. sowas wird dann meistens ein stück weit abverkauft. bei so zeugs kann man dann durchaus einfache charttechnik nehmen wie 61,8 Fibo. den anstieg berechnen und eben diese 61,8% davon abziehen. dann hat man den zu erwartenden konsokurs. ist doch recht beliebt diese zahl

15 cents auf 48 cents... 0,27x naja war en bischen drunter... aber die richtung stimmt sehr oft... vorausgesetzt die hausse geht dann weiter...

ich hab nur die sorge 2008 reloaded nur viel schlimmer...

das system macht mir immer mehr angst... schulden, billigkredite. blasen aller art...

dann können wir hier komplett einpacken

Antwort auf Beitrag Nr.: 56.964.749 von Boersiback am 07.02.18 19:07:02Nun mal nicht verzagen....Du bist doch auch einer derjenigen, die mehr als andere vom Börsengeschäft verstehen.

Klar, der Supercrash kann schon vor der Türe stehen, ich glaube aber nicht, daß es schon so weit ist. Die Manipulationsmechanismen funktionieren schon soooo lange soooo gut. Warum sollte sich das nicht noch einige Zeit in die Länge ziehen ? Aber wer weiß.

Was Nzuri anbelangt, sitze ich auch tief in den Miesen, bleibe aber trotzdem dabei und verkaufe kein einziges Stück.

Klar, der Supercrash kann schon vor der Türe stehen, ich glaube aber nicht, daß es schon so weit ist. Die Manipulationsmechanismen funktionieren schon soooo lange soooo gut. Warum sollte sich das nicht noch einige Zeit in die Länge ziehen ? Aber wer weiß.

Was Nzuri anbelangt, sitze ich auch tief in den Miesen, bleibe aber trotzdem dabei und verkaufe kein einziges Stück.

Antwort auf Beitrag Nr.: 56.966.336 von pmodds am 07.02.18 21:22:18Nzuri bin ich noch ganz gut grün. tja supercrash... bringt nix dauernd daran zu denken natürlich.

man muss halt wachsam sein auch wenns noch jahre geht.

was dann genau in welcher reihenfolge abläuft muss man sehen.

gerade bei gold z.b. recht schwierig vorhersehbar

us-aktien kommen mir jedenfalls keine mehr ins depot, deutsche auch nicht.

versorger oder nahrung behalt ich aber.

der anstieg war auch extrem heftig bei den aussies vor allem... man ist etwas verwöhnt worden

die zeit davor. von daher schon ok so.

der ASX Metals hat praktisch von anfang dezember bis anfang januar 0 konsolidiert. ich glaub kein tag im minus. das ist auch selten und "rächt" sich dann etwas

man muss halt wachsam sein auch wenns noch jahre geht.

was dann genau in welcher reihenfolge abläuft muss man sehen.

gerade bei gold z.b. recht schwierig vorhersehbar

us-aktien kommen mir jedenfalls keine mehr ins depot, deutsche auch nicht.

versorger oder nahrung behalt ich aber.

der anstieg war auch extrem heftig bei den aussies vor allem... man ist etwas verwöhnt worden

die zeit davor. von daher schon ok so.

der ASX Metals hat praktisch von anfang dezember bis anfang januar 0 konsolidiert. ich glaub kein tag im minus. das ist auch selten und "rächt" sich dann etwas

Antwort auf Beitrag Nr.: 56.889.464 von Popeye82 am 31.01.18 17:32:52http://www.spiegel.de/auto/aktuell/elektroautos-absatz-in-eu…

"Verkauf von E-Autos steigt enorm

Der Absatz von Elektroautos, Pkw mit Hybridantrieb oder Gasfahrzeugen ist in Europa im vergangenen Jahr gestiegen, allein in Deutschland um 80 Prozent. Der Gesamtanteil der umweltfreundlichen Autos ist aber immer noch gering.

Elektroauto BMW i3s

BMW

Elektroauto BMW i3s

Donnerstag, 01.02.2018 11:18 Uhr

Drucken

Nutzungsrechte

Feedback

Kommentieren

Knapp 853.000 der im vergangenen Jahr in der EU zugelassenen Neuwagen waren Elektroautos, Pkw mit Hybridantrieb oder Gasfahrzeuge, wie der Branchenverband Acea am Donnerstag in Brüssel mitteilte. Das war ein Plus von rund 40 Prozent.

WERBUNG

inRead invented by Teads

Am stärksten griffen die Italiener bei Wagen mit alternativen Antrieben zu. Dort wuchs der Absatz um knapp ein Viertel auf 230.000 Fahrzeuge. Dahinter folgte Großbritannien mit einem Wachstum um rund 35 Prozent auf knapp 120.000 Fahrzeuge. Deutschland als größter Pkw-Markt Europas hängt mit etwa 118.000 Zulassungen hinterher - das war allerdings immer noch ein Plus von rund 80 Prozent zum Vorjahr.

Die Zahlen zeigen, dass Autos mit alternativen Antrieben trotz der aktuellen Debatten um Feinstaub und Abgaswerte in Europa nur schwer Käufer finden. Denn gemessen an 15,1 Millionen Neuzulassungen ist der Marktanteil mit sechs Prozent noch gering. Gerade 1,4 Prozent der Neuwagen waren reine E-Fahrzeuge.

Video-Autogramm: Der BMW i3 S

Video abspielen... Video

SPIEGEL ONLINE

In Deutschland gibt es seit mehr als anderthalb Jahren eine Kaufprämie für Elektroautos. Dieser aus Steuermitteln finanzierte Bonus stößt bislang nur auf geringes Interesse. Rund 51.000 Anträge wurden beim zuständigen Bundesamt für Wirtschaft und Ausfuhrkontrolle gestellt.

Besonders Hybridfahrzeuge werden nachgefragt

Das Wachstum bei den alternativen Antrieben geht vor allem auf Hybridfahrzeuge zurück, die einen Elektro- mit einem Verbrennungsmotor kombinieren. Dieses Segment wuchs um rund 55 Prozent von 279.700 Fahrzeugen auf 431.500.

mhu/dpa"

"Verkauf von E-Autos steigt enorm

Der Absatz von Elektroautos, Pkw mit Hybridantrieb oder Gasfahrzeugen ist in Europa im vergangenen Jahr gestiegen, allein in Deutschland um 80 Prozent. Der Gesamtanteil der umweltfreundlichen Autos ist aber immer noch gering.

Elektroauto BMW i3s

BMW

Elektroauto BMW i3s

Donnerstag, 01.02.2018 11:18 Uhr

Nutzungsrechte

Feedback

Kommentieren

Knapp 853.000 der im vergangenen Jahr in der EU zugelassenen Neuwagen waren Elektroautos, Pkw mit Hybridantrieb oder Gasfahrzeuge, wie der Branchenverband Acea am Donnerstag in Brüssel mitteilte. Das war ein Plus von rund 40 Prozent.

WERBUNG

inRead invented by Teads

Am stärksten griffen die Italiener bei Wagen mit alternativen Antrieben zu. Dort wuchs der Absatz um knapp ein Viertel auf 230.000 Fahrzeuge. Dahinter folgte Großbritannien mit einem Wachstum um rund 35 Prozent auf knapp 120.000 Fahrzeuge. Deutschland als größter Pkw-Markt Europas hängt mit etwa 118.000 Zulassungen hinterher - das war allerdings immer noch ein Plus von rund 80 Prozent zum Vorjahr.

Die Zahlen zeigen, dass Autos mit alternativen Antrieben trotz der aktuellen Debatten um Feinstaub und Abgaswerte in Europa nur schwer Käufer finden. Denn gemessen an 15,1 Millionen Neuzulassungen ist der Marktanteil mit sechs Prozent noch gering. Gerade 1,4 Prozent der Neuwagen waren reine E-Fahrzeuge.

Video-Autogramm: Der BMW i3 S

Video abspielen... Video

SPIEGEL ONLINE

In Deutschland gibt es seit mehr als anderthalb Jahren eine Kaufprämie für Elektroautos. Dieser aus Steuermitteln finanzierte Bonus stößt bislang nur auf geringes Interesse. Rund 51.000 Anträge wurden beim zuständigen Bundesamt für Wirtschaft und Ausfuhrkontrolle gestellt.

Besonders Hybridfahrzeuge werden nachgefragt

Das Wachstum bei den alternativen Antrieben geht vor allem auf Hybridfahrzeuge zurück, die einen Elektro- mit einem Verbrennungsmotor kombinieren. Dieses Segment wuchs um rund 55 Prozent von 279.700 Fahrzeugen auf 431.500.

mhu/dpa"

Antwort auf Beitrag Nr.: 57.079.869 von Popeye82 am 21.02.18 13:34:34

Das Gesicht mit dem Bart

Zitat von Popeye82:![]()

http://www.mining.com/web/congos-kabila-yet-sign-new-mining-…

Das Gesicht mit dem Bart

Kasangasi muss ich mir Jetzt erstmal noch genauer ansehen.

http://www.mining.com/web/taxes-arent-real-problem-mining-co…

"There's a strange thing about the fear going through the global mining industry after the Democratic Republic of Congo signed an order to lift royalties last week: Compared with most other countries, these levies are still relatively low.

The existing 2 percent rate on copper extraction compares with royalties five times that level in Chile and Peru, the two biggest producers.

Even at the new 3.5 percent rate proposed by the country's national assembly, charges will still be lower than those paid in Australia and the U.S., according to a PricewaterhouseCoopers database of copper royalties. (There'll be an additional levy on windfall profits, too — but the history of those taxes suggests little money will be raised, anyway.)

So what's the fuss about?

For one thing, royalties are only part of the cost mix for a mine. Congo's southeastern copper belt is isolated and infrastructure-poor even by the standards of major mining regions. Electricity is brought by powerlines from near the mouth of the Congo River on the opposite side of the continent, and the region has invested heavily in diesel back-up generators and upgrades to the dams and transmission lines to gain a measure of stability. Exports are mostly along a snaking roadway via Zambia and Botswana to South Africa's Durban port.

That raises costs substantially. Despite some of the highest ore grades in the world and a rich endowment of the currently red-hot battery element cobalt, operating cash costs at Katanga Mining Ltd., controlled by Glencore Plc, came to $2.17 per pound of copper in 2014. That's more than double the 93 cents per pound at BHP Billiton Ltd.'s Escondida, in Chile, in its most recent fiscal year.

On top of that, there's an informal Congo dividend to be paid. Israeli billionaire Dan Gertler, a former shareholder in Katanga, had his U.S. assets frozen in December after the Treasury alleged he'd forced multinational companies to use him as a middleman to do business in Congo. The Guardian reported the previous month that the Paradise Papers leak showed Glencore loaning $45 million to Gertler in exchange for assistance securing a mining agreement for Katanga. (Both sides have said there was nothing unusual or improper about the arrangement.)

There are other problems. Katanga had to restate two years of its accounts last November after Canadian securities regulators started questioning some of its practices. The review found the company claimed to have made about 8,000 tons of copper that was never produced, and said that about $108 million of metal concentrates had gone missing from the plant, while Katanga hadn't known about $5.5 million in undisclosed payments that Glencore had made to 12 of its managers.