Norske Skog - das Ende und der Neu-Anfang? - 500 Beiträge pro Seite

eröffnet am 12.10.17 21:58:47 von

neuester Beitrag 05.12.19 21:45:36 von

neuester Beitrag 05.12.19 21:45:36 von

Beiträge: 41

ID: 1.264.109

ID: 1.264.109

Aufrufe heute: 0

Gesamt: 16.693

Gesamt: 16.693

Aktive User: 0

ISIN: NO0004135633 · WKN: 879395

0,0250

EUR

-3,85 %

-0,0010 EUR

Letzter Kurs 19.12.17 Tradegate

Werte aus der Branche Holzindustrie

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,5339 | +16,07 | |

| 15,450 | +8,00 | |

| 12,970 | +7,99 | |

| 22,200 | +5,87 | |

| 529,65 | +5,70 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,4600 | -5,19 | |

| 2,7700 | -5,94 | |

| 9,6100 | -6,15 | |

| 0,6100 | -6,15 | |

| 67,00 | -22,09 |

der alter Thread: https://www.wallstreet-online.de/diskussion/500-beitraege/11… hörte schon 2008 auf.

Dabei ging es danach als Investor - nicht als Trader - immer nur bergab.

Die damaligen Übernahmegerüchte müssen heute wie Hohn wirken. Denn: den Laden wollte wirklich niemand mit Verstand und Können.

Auch ist es interessant zu beobachten, warum so etwas überhaupt so schier ewig lange passieren kann. Um es gleich zu sagen: es gab CEO-übergreifend nur einen Grund: Hybris.

Dabei ging es danach als Investor - nicht als Trader - immer nur bergab.

Die damaligen Übernahmegerüchte müssen heute wie Hohn wirken. Denn: den Laden wollte wirklich niemand mit Verstand und Können.

Auch ist es interessant zu beobachten, warum so etwas überhaupt so schier ewig lange passieren kann. Um es gleich zu sagen: es gab CEO-übergreifend nur einen Grund: Hybris.

Antwort auf Beitrag Nr.: 55.942.358 von faultcode am 12.10.17 21:58:47

http://www.hegnar.no/Nyheter/Boers-finans/2017/10/Hauglund-o… (*)

http://www.norskeskog.com/Default.aspx?ID=2890&t=2017-10-11T… (**)

Diesmal wohl vor dem allerletzten Vorschlag vor einer liquidierenden Insolvenz:

=> so sieht es nun aus (**):

After such conversions, the equity ownership of Norske Skogindustrier ASA will be split as follows: a. Secured note holders: 91.0 % b. Unsecured noteholders: 6.3 % c. Existing shareholders: 2.7 %

Der bisherige Streit in 2017 entzündete sich v.a. daran, dass die Halter der ungesicherten Anleihen sich über den Tisch gezogen fühlten.

Die der gesicherten hingegen auf Zeit spielen konnten, da sie - insgesamt - davon ausgehen, im Falle einer Liquidierung durchaus gut aus der Sache herauskommen ("Quote"):

http://e24.no/boers-og-finans/norske-skogindustrier/norske-s… (***)

Wo stehen wir heute? --> The boards' final recapitalization proposal

Aus Aktionärssicht: einen Schritt vor dem Aus:http://www.hegnar.no/Nyheter/Boers-finans/2017/10/Hauglund-o… (*)

http://www.norskeskog.com/Default.aspx?ID=2890&t=2017-10-11T… (**)

Diesmal wohl vor dem allerletzten Vorschlag vor einer liquidierenden Insolvenz:

=> so sieht es nun aus (**):

After such conversions, the equity ownership of Norske Skogindustrier ASA will be split as follows: a. Secured note holders: 91.0 % b. Unsecured noteholders: 6.3 % c. Existing shareholders: 2.7 %

Der bisherige Streit in 2017 entzündete sich v.a. daran, dass die Halter der ungesicherten Anleihen sich über den Tisch gezogen fühlten.

Die der gesicherten hingegen auf Zeit spielen konnten, da sie - insgesamt - davon ausgehen, im Falle einer Liquidierung durchaus gut aus der Sache herauskommen ("Quote"):

http://e24.no/boers-og-finans/norske-skogindustrier/norske-s… (***)

Antwort auf Beitrag Nr.: 55.942.358 von faultcode am 12.10.17 21:58:47

=>

=> das nenn ich hartgesotten:

- man sieht wie die erste Gruppe an Einigungs-Spekulaten im August quasi wieder geschlossen im September ausgestiegen ist.

=> nun sind wohl nur noch die ganz harten hier drin (aber ich nicht - zumindest, wenn ich hier schreibe; so schnell geht's nicht).

=> halten wir mal fest:

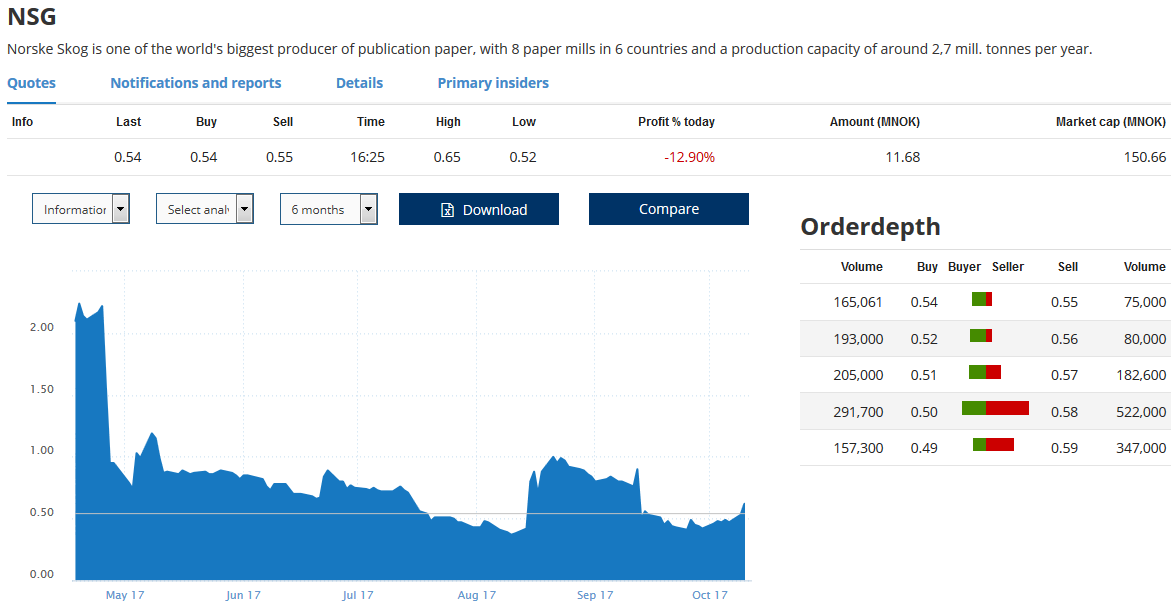

MK = NOK150.66m = EUR16.12m (NOK/EUR = 0.106975624)

Das passt in etwa, wenn ich mit heutigem Oslo-Schlusskurs von NOK0,54 die MK rückrechne.

Der Markt spielt ein bischen auf Annahme des "finalen" Vorschlags

http://oslobors.no/ob_eng/markedsaktivitet/#/details/NSG.OSE…=>

=> das nenn ich hartgesotten:

- man sieht wie die erste Gruppe an Einigungs-Spekulaten im August quasi wieder geschlossen im September ausgestiegen ist.

=> nun sind wohl nur noch die ganz harten hier drin (aber ich nicht - zumindest, wenn ich hier schreibe; so schnell geht's nicht).

=> halten wir mal fest:

MK = NOK150.66m = EUR16.12m (NOK/EUR = 0.106975624)

Das passt in etwa, wenn ich mit heutigem Oslo-Schlusskurs von NOK0,54 die MK rückrechne.

Antwort auf Beitrag Nr.: 55.942.700 von faultcode am 12.10.17 22:41:29

Book value of equity per share: -NOK2.00

=> war in Q1 noch positiv mit NOK0.14

So kommen wir aber nicht weiter, wenn man wissen will, welcher materieller Buchwert einer Aktie bei Annahme des "finalen" Vorschlags zustehen könnte.

=> also schaue ich die mir Tangible assets (TA) an (die intangible assets sind sowieso nur verschwindend gering...)

[mNOK]

2015Q4: 8,585

2016Q2: 6,736

2016Q4: 6,562

2017Q1: 6,601

2017Q2: 6,571

=> d.h. seit 1 Jahr gibt es hier relative Stabilität, was sehr gut ist.

=> pro Aktie:

NOK6,571,000,000 / 278,990,000 = NOK23.55 / share

=> 2.7% von NOK23.55 = NOK0.636 > Schlusskurs 12.10.2017 => P/B|TA = NOK0.54 / NOK0.636 = 0.849

=> also den Dollar für 50 Cent bekäme man nun nicht, aber das wäre schon mal vorläufig akzeptabel - falls komplett schuldenfrei in der "NNS" ("New Norske Skog"/FC), und nicht andere Randbedingungen.

Daher wäre nun zu prüfen, wie es mit Restschulden in der NNS aussehen würde:

If the proposal is successful, the transaction will reduce the group's gross debt from approximately NOK 9 billion to approximately NOK 3 billion (**)

=> macht pro Alt-Aktie: NOK10.753 Schulden / share

=> ich nenne das einfach laienhaft "Net tangible assets per share":

=> (NOK23.55 / share - NOK10.753 / share) * 2.7% = NOK0.346 was schon nicht mehr so gut ist.

...und hinzu kämen diverse Verwässerungen (**) wie:

(4) The board will propose an equity offering by Norske Skogindustrier ASA of up to approximately NOK 500 million with preferential rights for existing unsecured bondholders and shareholders, allocated by approximately NOK 300 million to the unsecured bondholders and approximately NOK 200 million to the shareholders. If fully subscribed, this will entail an increase in their ownership interest from 9 % to approximately 28 %. The subscription price will be set at a valuation of 6x the revised 2017 GOE guidance of EUR 75 million.

(5) Warrants will be issued for up to 10 % of the equity in Norske Skogindustrier ASA to those who have subscribed to the above equity offering. The warrants entitle the holders to subscribe for shares if the sum of the group's average net debt and market value exceeds EUR 525 million in a consecutive period of 6 months prior to 30 June 2019. The subscription rights expire worthless on 30 June 2019 if not exercised.

Obige 9% kommen dadurch zustande: 6.3% (unsecured) + 2.7% (secured) = 9%

=> d.h., man muss eine weitere Verwässerung von grob NOK200m zu NOK150.66m hinnehmen: => d.h., am Ende bliebe für eine Alt-Aktie nur mehr: NOK(150.66m) / (NOK200m + NOK150.66m) = 43.0% übrig

=> also "Net2 tangible assets per share" = NOK0.346 * 43.0% = NOK0.148

=> nun kommen noch die 10% Warrants dazu als weitere Verwässerung (ich rechne auch hier konversativ mit worst case, um das Überleben der NNS anzunehmen - sonst würde diese Rechnung für Alt-Aktionäre ja keinen Sinn machen bei Liquidierung...):

=> also "Net3 tangible assets per share" = NOK0.346 * 100% / (100%+10%) = NOK0.135

=> das ist deutlich unter aktuell NOK0.54 => P/B|TA3 = NOK0.54 / NOK0.135 = 4.0

=> was zahlt man z.Z.?

=> der nächste vergleichbare Competitor wäre Holmen (B), ISIN = SE0000109290: KBV = 1.28

=> massiv weniger => von daher: FINGER WEG falls Buchwert-Spekulation!

Buchwerte --> Finger weg!

Aus dem 2017Q2-Bericht geht hervor:Book value of equity per share: -NOK2.00

=> war in Q1 noch positiv mit NOK0.14

So kommen wir aber nicht weiter, wenn man wissen will, welcher materieller Buchwert einer Aktie bei Annahme des "finalen" Vorschlags zustehen könnte.

=> also schaue ich die mir Tangible assets (TA) an (die intangible assets sind sowieso nur verschwindend gering...)

[mNOK]

2015Q4: 8,585

2016Q2: 6,736

2016Q4: 6,562

2017Q1: 6,601

2017Q2: 6,571

=> d.h. seit 1 Jahr gibt es hier relative Stabilität, was sehr gut ist.

=> pro Aktie:

NOK6,571,000,000 / 278,990,000 = NOK23.55 / share

=> 2.7% von NOK23.55 = NOK0.636 > Schlusskurs 12.10.2017 => P/B|TA = NOK0.54 / NOK0.636 = 0.849

=> also den Dollar für 50 Cent bekäme man nun nicht, aber das wäre schon mal vorläufig akzeptabel - falls komplett schuldenfrei in der "NNS" ("New Norske Skog"/FC), und nicht andere Randbedingungen.

Daher wäre nun zu prüfen, wie es mit Restschulden in der NNS aussehen würde:

If the proposal is successful, the transaction will reduce the group's gross debt from approximately NOK 9 billion to approximately NOK 3 billion (**)

=> macht pro Alt-Aktie: NOK10.753 Schulden / share

=> ich nenne das einfach laienhaft "Net tangible assets per share":

=> (NOK23.55 / share - NOK10.753 / share) * 2.7% = NOK0.346 was schon nicht mehr so gut ist.

...und hinzu kämen diverse Verwässerungen (**) wie:

(4) The board will propose an equity offering by Norske Skogindustrier ASA of up to approximately NOK 500 million with preferential rights for existing unsecured bondholders and shareholders, allocated by approximately NOK 300 million to the unsecured bondholders and approximately NOK 200 million to the shareholders. If fully subscribed, this will entail an increase in their ownership interest from 9 % to approximately 28 %. The subscription price will be set at a valuation of 6x the revised 2017 GOE guidance of EUR 75 million.

(5) Warrants will be issued for up to 10 % of the equity in Norske Skogindustrier ASA to those who have subscribed to the above equity offering. The warrants entitle the holders to subscribe for shares if the sum of the group's average net debt and market value exceeds EUR 525 million in a consecutive period of 6 months prior to 30 June 2019. The subscription rights expire worthless on 30 June 2019 if not exercised.

Obige 9% kommen dadurch zustande: 6.3% (unsecured) + 2.7% (secured) = 9%

=> d.h., man muss eine weitere Verwässerung von grob NOK200m zu NOK150.66m hinnehmen: => d.h., am Ende bliebe für eine Alt-Aktie nur mehr: NOK(150.66m) / (NOK200m + NOK150.66m) = 43.0% übrig

=> also "Net2 tangible assets per share" = NOK0.346 * 43.0% = NOK0.148

=> nun kommen noch die 10% Warrants dazu als weitere Verwässerung (ich rechne auch hier konversativ mit worst case, um das Überleben der NNS anzunehmen - sonst würde diese Rechnung für Alt-Aktionäre ja keinen Sinn machen bei Liquidierung...):

=> also "Net3 tangible assets per share" = NOK0.346 * 100% / (100%+10%) = NOK0.135

=> das ist deutlich unter aktuell NOK0.54 => P/B|TA3 = NOK0.54 / NOK0.135 = 4.0

=> was zahlt man z.Z.?

=> der nächste vergleichbare Competitor wäre Holmen (B), ISIN = SE0000109290: KBV = 1.28

=> massiv weniger => von daher: FINGER WEG falls Buchwert-Spekulation!

Antwort auf Beitrag Nr.: 55.943.051 von faultcode am 12.10.17 23:51:21

Momentan wären das: NOK0.269 per share => P/GOE3 = 5.14 (mit beiden Verwässerungen von oben)

..und das wären nicht die Net earnings im P/E bei der NNS.

Holmen B hat nach FactSet ein KGV für 2017e von relativ hohen 19.68.

Man sieht, 5.14 ist in Nähe der obigen 6 ("The subscription price will be set at a valuation of 6x the revised 2017 GOE guidance of EUR 75 million"), wodurch man von einem Subscription price (SP) in Nähe des aktuellen Aktienkurses ausgehen könnte:

=> SP = 6 / 5.14 * NOK0.54 = NOK0.63

=> auch was wäre alles andere als attraktiv, weil der Abstand beider Ratios einfach nicht gross genug ist für ein Schnäppchen

=> von daher auch: FINGER WEG falls Gewinn-Spekulation!

Operative Gewinnaussicht 2017 --> Finger weg!

Oben ist ja eine GOE guidance von EUR 75 million gemacht worden; mit GOE = Gross operating earnings. Da sind z.Z. auch Währungseinflüsse drin.Momentan wären das: NOK0.269 per share => P/GOE3 = 5.14 (mit beiden Verwässerungen von oben)

..und das wären nicht die Net earnings im P/E bei der NNS.

Holmen B hat nach FactSet ein KGV für 2017e von relativ hohen 19.68.

Man sieht, 5.14 ist in Nähe der obigen 6 ("The subscription price will be set at a valuation of 6x the revised 2017 GOE guidance of EUR 75 million"), wodurch man von einem Subscription price (SP) in Nähe des aktuellen Aktienkurses ausgehen könnte:

=> SP = 6 / 5.14 * NOK0.54 = NOK0.63

=> auch was wäre alles andere als attraktiv, weil der Abstand beider Ratios einfach nicht gross genug ist für ein Schnäppchen

=> von daher auch: FINGER WEG falls Gewinn-Spekulation!

Trading Spotlight

Secured bondholders

Die Secured bondholders sollen also zunächst 91% bekommen, mit beiden (Voll-)Verwässerungen (9% -> 28% + Warrants) ergäben sich dann nur noch, aber immerhin: 65.5%=> also 65.5% von NOK6.571b = NOK4.301b der Tangible assets.

Die Secured bondholders bekämen noch das neue EUR 250 million bond loan carrying 8.5 % interest with a 2022 maturity.

Das betrifft aber ausdrücklich nur diese Gruppe:

- owners of the EUR 290 million bond loan 2019 = senior secured notes (SSN)

- owners of the EUR 100 million NSF-facility 2020 (NSF = Norwegian Securitization Facility)

Ich weiss nun nicht, wieviele Loans die Secured bondholders momentan insgesamt halten. Das geht aus (**) nicht eindeutig hervor.

Denn das wäre zur Beantwortung der Frage, ob die Secured bondholders diesen allerletzten Vorschlag wahrscheinlich wieder ablehnen von allergrösster Bedeutung.

Momentan weiss ich nur, dass die Unsecured bondholders (USBH) mehr bekommen würden als in den vorherigen Vorschlägen.

(**) sagt:

So far, more than 65% of the secured bondholders and major shareholders of the group have indicated their willingness to support the recapitalization proposal upon launch.

...

The bondholders have 7 business days, until Thursday 19 October 2017 (17:00 CET), to accept the proposal.

...

Such schemes of arrangement require the approval of a majority in number and 75 % in value. The transaction will also need the support of existing shareholders of Norske Skogindustrier ASA, with a 2/3 majority in an extraordinary general meeting...as well as the support of the holders of the EUR 100 million NSF facility due in 2020 and the perpetual notes due in 2115.

Weiter als Alternative:

If the recapitalization proposal is not successful, it is likely that the boards of directors of Norske Skogindustrier ASA, Norske Treindustrier AS, and Norske Skog Holding AS will file for voluntary or compulsory debt negotiation proceedings or bankruptcy in Norwegian courts. This will in all likelihood result in the loss of all value for the unsecured bondholders and the existing shareholders.

...

If the proposal is not successful, it is likely that the secured note holders will conclude that the only realistic path open to them will be to enforce upon their security over the shares in Norske Skog AS, which owns all operating units. Consequently, the business operations of the group will be transferred to new owners with little or no recovery for the unsecured bondholders and the existing shareholders.

Unsecured bondholders (USBH's)

Knackpunkt bislang waren ja die Unsecured bondholders.Ich bin nun nahezu (aus dem AR2016) auf die obigen approximately NOK 9 billion debt gekommen (Währungseffekte!):

=> man sieht, dass die Secured bondholders (SBH's) in Summe wieder zustimmen könnten. Allerdings sind deren Sicherheiten im Detail festgelegt, nicht in Summe.

Hingegen hätten die Unsecured bondholders (USBH's) immer noch keine vollständige Deckung durch die restlichen Tangible assets in Summe.

Ich komme auf folgende Grenzen als Richtgrössen (es gibt da einige Unwägbarkeiten, z.B. wie die Equity Subscription ausgehen könnte...):

Net tangible assets available for SBH [NOK]: 4.301.018.182

Net tangible assets available for USBH [NOK]: 2.092.564.818 (maximal), 1.915.147.818 (minimal)

=> tja, so sieht eine vollkommen überschuldete Aktiengesellschaft aus. Zinsen werden sowieso "deferred". Daher nahmen die Schulden in 2017 auch bislang zu, ganz ohne Ausgabe neuer Anleihen oder Aufnahme von weiteren Grundschulden etc.

Ich kann auch nicht sagen, was die Tangible assets im Liquidierungsfall tatsächlich einbringen würden. Die Liquidierung wäre auch ein zeitraubender Vorgang mit Unsicherheiten für den operativen Betrieb, und weitere Spezialisten etc. müssten auch noch vom Erlös bezahlt werden.

Anleihenkurse Norske Skog

Alle nominal 1000?Alles Taxe ohne Volumen:

XS1193909154 -- ungesichert: 12.10.2017: 1.54G, 9.86B

https://www.boerse-stuttgart.de/de/Norske-Skog-Holding-AS-An…

XS1181663292 -- Senior secured notes (SSN) (2019): 12.10.2017: 90.04G, 100.48B

https://www.boerse-stuttgart.de/de/Norske-Skog-AS-Anleihe-XS…

Frf.: 89.850G, 99.220B => hier macht der Briefkurs wenigstens Sinn bei Liquidierung - obwohl vielleicht in so einem Fall eventuell mit Abzügen (extra Gebühren z.B.) zu rechnen wäre...

XS1394812595 -- junior, ungesichert, 2026: 12.10.2017: 1G, 13B

https://www.boerse-stuttgart.de/de/boersenportal/wertpapiere…

XS1394812918 -- perpetual, ungesichert: 12.10.2017: 1G, 10B

http://en.boerse-frankfurt.de/bonds/Norske_Skogindustrier_AS…

USR59730AA00 -- ungesichert: 12.10.2017: 3G, 10B

https://www.boerse-stuttgart.de/de/boersenportal/wertpapiere…

Diese Bonds werden alle ausserhalb der Oslo Exchange gehandelt, z.B. auch in Luxemburg. Obwohl über 2000 Bonds an der Oslo Exchange gehandelt werden; ich habe aber nur NO....-ISIN's dort gefunden.

Antwort auf Beitrag Nr.: 55.942.358 von faultcode am 12.10.17 21:58:47

=> von ehemals 19 Fabriken in 2005 auf nur noch 7 heutzutage:

Das Schulden-Disaster fing bereits 1999 an mit der Übernahme der Fletcher Challenge Paper/NZ (Neuseeland), der grössten Übernahme von Norske Skog und der grössten, die bis dahin im Ausland ein norwegisches Unternehmen tätigte.

Diese Übernahme war quasi als Krönung zum 50-jährigen Bestehen von Norske Skog gedacht. Nebenbei lud man sich NOK21b (EUR2.1b) Schulden auf.

Es gab danach noch weitere Übernahmen im Ausland - natürlich mit neuen Schulden.

2003 war dann aber Schluss damit. Muss sah sich gezwungen Kosten zu sparen - bis zum heutigen Tag!

Nur wurde das dem unbedarften Anleger so nicht verkauft: es folgte eine ganze Reihe von Presseveröffentlichungen mit falschen Versprechungen und Hoffnungen, so am 15.04.2004:

"In the future, Norske Skog will continue to grow and retain its position as one of the world's leading suppliers of newspaper and magazine papers..."

=> so kam es nicht: in 2008 fing man an die asiatischen Papierfabriken zu verkaufen. Dort konnte nie Geld verdient werden. Dabei traten aber wunderliche Aktivitäten zutage: so wurde man 2005 alleinige Eigentümer der Fabriken in Hebei and Shanghai, beide China, also in einer Zeit, als es eigentlich stramm ums Kostensparen gehen sollte.

Bereits 4 Jahre später, 2009, sah man sich gezwungen beide Fabriken wieder (komplett) zu verkaufen:

die Hybris - der historische Abriss (1)

Hier ein guter historischer Abriss vom 26.08.2017: http://e24.no/boers-og-finans/norske-skogindustrier/norske-s…=> von ehemals 19 Fabriken in 2005 auf nur noch 7 heutzutage:

Das Schulden-Disaster fing bereits 1999 an mit der Übernahme der Fletcher Challenge Paper/NZ (Neuseeland), der grössten Übernahme von Norske Skog und der grössten, die bis dahin im Ausland ein norwegisches Unternehmen tätigte.

Diese Übernahme war quasi als Krönung zum 50-jährigen Bestehen von Norske Skog gedacht. Nebenbei lud man sich NOK21b (EUR2.1b) Schulden auf.

Es gab danach noch weitere Übernahmen im Ausland - natürlich mit neuen Schulden.

2003 war dann aber Schluss damit. Muss sah sich gezwungen Kosten zu sparen - bis zum heutigen Tag!

Nur wurde das dem unbedarften Anleger so nicht verkauft: es folgte eine ganze Reihe von Presseveröffentlichungen mit falschen Versprechungen und Hoffnungen, so am 15.04.2004:

"In the future, Norske Skog will continue to grow and retain its position as one of the world's leading suppliers of newspaper and magazine papers..."

=> so kam es nicht: in 2008 fing man an die asiatischen Papierfabriken zu verkaufen. Dort konnte nie Geld verdient werden. Dabei traten aber wunderliche Aktivitäten zutage: so wurde man 2005 alleinige Eigentümer der Fabriken in Hebei and Shanghai, beide China, also in einer Zeit, als es eigentlich stramm ums Kostensparen gehen sollte.

Bereits 4 Jahre später, 2009, sah man sich gezwungen beide Fabriken wieder (komplett) zu verkaufen:

Antwort auf Beitrag Nr.: 55.953.182 von faultcode am 14.10.17 13:11:59

So wurden z.B. (angeblich) USD10m in der damaligen Papierfabrik in Walsum/Duisburg pro Monat Verlust gemacht, bevor sie im Juni 2015 geschlossen wurde. Dort wollen Gläubiger nun EUR40...50m wieder haben, am meisten der dortige Pensionssicherungsfonds.

Dabei brachte der gesamte Werks-Verlauf 2016-09 mit den beiden Papiermaschinen und weiterer Grossanlagen weniger als EUR10m ein: https://www.euwid-papier.de/news/einzelansicht/Artikel/insol…

die Hybris - der historische Abriss (2)

Es gab bei den Fabrik-Verkäufen Anzeichen, dass diese nur zum Buchwert ab 2008/9, also der globalen Finanzkrise, vorgenommen werden konnten, und damit nur zum Bruchteil des ursprünglichen Kaufpreises.So wurden z.B. (angeblich) USD10m in der damaligen Papierfabrik in Walsum/Duisburg pro Monat Verlust gemacht, bevor sie im Juni 2015 geschlossen wurde. Dort wollen Gläubiger nun EUR40...50m wieder haben, am meisten der dortige Pensionssicherungsfonds.

Dabei brachte der gesamte Werks-Verlauf 2016-09 mit den beiden Papiermaschinen und weiterer Grossanlagen weniger als EUR10m ein: https://www.euwid-papier.de/news/einzelansicht/Artikel/insol…

Antwort auf Beitrag Nr.: 55.953.254 von faultcode am 14.10.17 13:26:46

2000: 2.18 billion.

2001: 2.66 billion.

2002: 1.17 billion.

2003: 406 mill.

2004: 629 mill.

2005: minus 848 mill.

2006: minus 3.02 billion.

2007: minus 683 mill.

2008: minus 2.77 billion.

2009: minus 1.40 billion.

2010: minus 2.47 billion.

2011: minus 2.55 billion.

2012: minus 2.78 billion.

2013: minus 1.84 billion.

2014: minus 1.50 billion.

2015: minus 1.53 billion.

2016: 306 mill.

die Hybris - der historische Abriss (2a)

So sehen dann entsprechende Verluste aus: Norske Skog's jährliches Ergebnis nach Steuern [NOK]:2000: 2.18 billion.

2001: 2.66 billion.

2002: 1.17 billion.

2003: 406 mill.

2004: 629 mill.

2005: minus 848 mill.

2006: minus 3.02 billion.

2007: minus 683 mill.

2008: minus 2.77 billion.

2009: minus 1.40 billion.

2010: minus 2.47 billion.

2011: minus 2.55 billion.

2012: minus 2.78 billion.

2013: minus 1.84 billion.

2014: minus 1.50 billion.

2015: minus 1.53 billion.

2016: 306 mill.

Geht es auch anders? - Countercase Holmen B

Nun gut, könnte man sagen, das war eben dem sekularen Abwärtstrend ab 2003 bei Druckpapieren (Zeitungen, Zeitschriften, ...) geschuldet: was hätte man denn überhaupt anders machen können?=> meine fundierte These: BESSER MANAGEN!

Denn: man kann in einer Industrie, deren Produkt-Nachfrage (oder der nach Dienstleistungen) laufend und stetig, aber nicht abrupt zurückgeht, durchaus zu den Gewinnern gehören als Hersteller. Einer, der auch noch relativ gute Gewinne (im Schnitt - nicht jedes Jahr) macht - bei wenig Schulden.

Als ein Königsbeispiel wäre hier sicherlich die globale Zigarettenindustrie zu nennen - zumindest bis zur neuen Nikotin-Diskussion in den USA/FDA ab 2017 (vorerst):

- immer weniger Wettbewerb

- geringste F+E-Kosten

- kaum Investitionen ausserhalb des Marketings

--> ein feuchter Anlegertraum über Jahrzehnte hinweg.

Gut, das ist die Spitze und nicht "normal". Aber es ging nachweislich, siehe den gut vergleichbaren Wettbewerber Holmen B aus Schweden: https://www.wallstreet-online.de/aktien/holmen-b-aktie, ISIN = SE0000109290

Aktienkurs Ende 1993: SEK100

Aktienkurs 2017-10: SEK390 => +5.8% p.a.,

plus Dividende in jedem Jahr seit 1981!,

und Eigenkapitalanteil 2016 von 60.9%

=> Renditen:

5Y: 19.2%

10Y: 7.2%

=> das, was den Aktionären von Norske Skog passiert ist, war kein unabwendbares Schicksal, sondern schnöde Selbstüberschätzung, und das CEO-übergreifend. Erst beim jetzigen änderte sich das, der nun die (Rest-)Suppe auslöffeln oder den Totengräber spielen darf.

Antwort auf Beitrag Nr.: 55.942.436 von faultcode am 12.10.17 22:07:45

Ich gehe fest davon aus, dass der vorliegende Entschuldungs- und Refinanzierungsplan der letzte ist. Es wird keinen anderen mehr geben, da die Schulden von Norske Skog immer weiter anwachsen. Es ist 5 nach 12.

Wie oben beschrieben (Beitrag Nr. 7), haben die Unsecured bondholders mit Sicherheit wieder Bauchschmerzen.

Ich will keine Prognose abgeben, wie am Donnerstag nächster Woche, 19.10.2017, um 17:00h CET die Entscheidungslage sein wird.

Aber ich weiss: wenn es zur Nicht-Annahme kommen sollte, würde wahrscheinlich zunächst doch Chaos ausbrechen und man gewinnt dadurch wenigstens einen Tag Zeit als Spekulant, nämlich den Freitag, 20.10.2017.

Bis dahin würde ich mir dann überlegen eine Portion Holmen B zuzulegen, denn die werden so oder so der schnellste Profiteur der unübersichtlichen Lage sein. Auch vor dem Hintergrund, dass die Aktien schon gut gelaufen sind.

Ob Holmen selber oder andere nun ein paar Fabriken von Norske Skog übernehmen werden, oder ob es wie in Walsum zu Komplett-Schliessungen mit langwierigen Ausrüstungs-Transfers (heutzutage oft nach Indien) kommen sollte: Holmen sollte ein investierbarer Gewinner sein. (Das muss ja nicht gleich sichtbar werden, ob im Aktienkurs oder fundamental...)

Die Uhrzeit in Oslo sollte nächste Woche dieselbe wie z.B. in Berlin/Frankfurt a.M. sein. Zumindest jetzt ist es so (noch) --> also bei 17:00h CET wären das 18:00h CEST in Oslo und Berlin. (Rückstellung auf CET ist am 29. Okt 2017 um 03:00h.)

Idee: Profiteur Holmen bei erneuter Ablehnung nächste Woche

Und damit schliesst sich der Kreis.Ich gehe fest davon aus, dass der vorliegende Entschuldungs- und Refinanzierungsplan der letzte ist. Es wird keinen anderen mehr geben, da die Schulden von Norske Skog immer weiter anwachsen. Es ist 5 nach 12.

Wie oben beschrieben (Beitrag Nr. 7), haben die Unsecured bondholders mit Sicherheit wieder Bauchschmerzen.

Ich will keine Prognose abgeben, wie am Donnerstag nächster Woche, 19.10.2017, um 17:00h CET die Entscheidungslage sein wird.

Aber ich weiss: wenn es zur Nicht-Annahme kommen sollte, würde wahrscheinlich zunächst doch Chaos ausbrechen und man gewinnt dadurch wenigstens einen Tag Zeit als Spekulant, nämlich den Freitag, 20.10.2017.

Bis dahin würde ich mir dann überlegen eine Portion Holmen B zuzulegen, denn die werden so oder so der schnellste Profiteur der unübersichtlichen Lage sein. Auch vor dem Hintergrund, dass die Aktien schon gut gelaufen sind.

Ob Holmen selber oder andere nun ein paar Fabriken von Norske Skog übernehmen werden, oder ob es wie in Walsum zu Komplett-Schliessungen mit langwierigen Ausrüstungs-Transfers (heutzutage oft nach Indien) kommen sollte: Holmen sollte ein investierbarer Gewinner sein. (Das muss ja nicht gleich sichtbar werden, ob im Aktienkurs oder fundamental...)

Die Uhrzeit in Oslo sollte nächste Woche dieselbe wie z.B. in Berlin/Frankfurt a.M. sein. Zumindest jetzt ist es so (noch) --> also bei 17:00h CET wären das 18:00h CEST in Oslo und Berlin. (Rückstellung auf CET ist am 29. Okt 2017 um 03:00h.)

Antwort auf Beitrag Nr.: 55.953.182 von faultcode am 14.10.17 13:11:59

Es war in Wahrheit ein Verkehrs-Mann (Norwegian State Railways, Trondheim Trafikkselskap, Scandinavian Airline Systems) und blieb dem auch treu als Direktror bei Swiss International Air Lines ab 2003.

Dazu auch vom 05.11.2003: http://www.norskeskog.com/files/filer/Arkiv/PR/200311/923698…:

Jan Reinås informed the Board that he wished to retire from his position as CEO latest when he turns 60 years old. The Board carried out an extensive recruitment process to find a successor for Jan Reinås.

=> offenbar sah er selber, in welche Bredouille er das Unternehmen brachte. Interessant auch der zweite Satz: kein Aussenstehender, der als wührdig und fähig befunden wurde, wollte sich den Job antun. Und so griff man zur internen Lösung (Deputy CEO seit 2000), einem Mann der einfach nicht energisch genug gegensteuerte und sogar noch weiter expandierte (in Asien): https://no.wikipedia.org/wiki/Jan_A._Oksum

Es muss ein überdeutliches Warnsignal - auch nach aussen hin - gewesen sein, den Deputy CEO und langjährigen Mitarbeiter (seit 1979) nicht gleich zum CEO zu berufen. Offenbar hatte man bereits Zweifel im Aufsichtsrat. So musste er auch schon ziemlich schnell gehen in 2006-03. Man könnte nun in Nachhinein nach vielen Jahren sagen: es musste ein Sündenbock her. Aber er hätte ja auch nein sagen können und das Unternehmen verlassen.

die Hybris - der historische Abriss (1a)

im obigen Link ist der Name des damaligen CEO's erwähnt, der langjährig im Amt war (1994 - 2003) und die schuldenfinanzierte Grossexpansion einleitete: Jan Reinås (1944 - 2010), der sich aber nun nicht mehr wehren kann: https://en.wikipedia.org/wiki/Jan_Rein%C3%A5sEs war in Wahrheit ein Verkehrs-Mann (Norwegian State Railways, Trondheim Trafikkselskap, Scandinavian Airline Systems) und blieb dem auch treu als Direktror bei Swiss International Air Lines ab 2003.

Dazu auch vom 05.11.2003: http://www.norskeskog.com/files/filer/Arkiv/PR/200311/923698…:

Jan Reinås informed the Board that he wished to retire from his position as CEO latest when he turns 60 years old. The Board carried out an extensive recruitment process to find a successor for Jan Reinås.

=> offenbar sah er selber, in welche Bredouille er das Unternehmen brachte. Interessant auch der zweite Satz: kein Aussenstehender, der als wührdig und fähig befunden wurde, wollte sich den Job antun. Und so griff man zur internen Lösung (Deputy CEO seit 2000), einem Mann der einfach nicht energisch genug gegensteuerte und sogar noch weiter expandierte (in Asien): https://no.wikipedia.org/wiki/Jan_A._Oksum

Es muss ein überdeutliches Warnsignal - auch nach aussen hin - gewesen sein, den Deputy CEO und langjährigen Mitarbeiter (seit 1979) nicht gleich zum CEO zu berufen. Offenbar hatte man bereits Zweifel im Aufsichtsrat. So musste er auch schon ziemlich schnell gehen in 2006-03. Man könnte nun in Nachhinein nach vielen Jahren sagen: es musste ein Sündenbock her. Aber er hätte ja auch nein sagen können und das Unternehmen verlassen.

Antwort auf Beitrag Nr.: 55.955.024 von faultcode am 14.10.17 23:55:56

- und so stellt sich die Frage: was zum Teufel dachte sich der Aufsichtsrat (Board of Directors) von 1994 - 2003?

- wo wurden da die berechtigten Interessen der Aktionäre gewahrt?

Ich lese gerade im Jahresbericht - oder besser gesagt Märchensammlung - von 2004:

One absolute requirement is that all growth must be profitable. Our overriding goal is to deliver the best shareholder value in the paper industry.

=> klingt gut, war aber das exakte Gegenteil der Realität. Niemand traute sich die bereits damals schon prekäre Lage realistisch zu beschreiben. 2004 war noch eine gute Gelegenheit seine Aktien restlos zu verkaufen.

Dieser Jahresbericht liest sich erschreckend "Enron-mässig": http://www.norskeskog.com/Admin/Public/DWSDownload.aspx?File…

Da gab es einmal:

(a) LARS WILHELM GRØHOLT: Chair of the board since 2002, director since 2001.

Forest owner. Chair, Norwegian Forestry Research Institute (NISK) since October 2004, director since 2001. Chair, Norwegian Forest Owners' Association 1998-02. Chair Viken Skog 2000-02, Vest-Viken Forest Owners' Association 1999 and Drammen Forest Owners' Association 1993-99. Board member, Pan European Forest Certification (PEFC) 1999-03.

2006-03 gab es Kritik an ihm: https://www.nrk.no/okonomi/flengende-kritikk-av-groholt-1.56… - da war es aber schon zu spät => 2007 stellte er sich nicht mehr zur Wiederwahl: http://www.nettavisen.no/na24/917563.html

..und zuvor:

(b) Lage Westerbø: Chair of the board: 22 March 1989 – 29 April 2002 => im letzten Viertel seiner langjährigen Amtszeit wurden die fatalen Expansionsentscheidungen auf Pump getroffen. Ein Mann, der sich am Ende, 2002, wortlos vom Acker machte: https://www.nrk.no/okonomi/norske-skog-1-milliard-ned-1.5474… =>

Reinås also announced at the general meeting today that Norske Skog's chairman, Lage Westerbø, is leaving. He did not give any reason for the resignation.

(so lange zurück wird das Internet schon sehr zäh mit brauchbaren Info's...) Ein Überblick über seine Haufen Positionen, früher und heute: https://www.purehelp.no/role/viewManCV/43142511/lagecollingw…

Ich vermute, dass er auch ein Mann aus diesem Umfeld ist: Norske Skog wurde ja im Prinzip 1962 durch Vertreter der Norwegian Forest Owners Association (https://en.wikipedia.org/wiki/Norwegian_Forest_Owners_Associ…) gegründet - zusammen mit anderem Geld, um in Lavanger ihre erste Papierfabrik zu bauen: https://en.wikipedia.org/wiki/Norske_Skog_Skogn

=> d.h., irgendwann haben die Vertreter der privaten Waldbesitzer Norwegen's Norske Skog in Wahrheit für ihre eigenen Zwecke missbraucht - und keiner hielt sie auf.

die Hybris - der historische Abriss (1b)

Aber in einem Konzern gehören immer 2 zum Machen grober Fehler:- und so stellt sich die Frage: was zum Teufel dachte sich der Aufsichtsrat (Board of Directors) von 1994 - 2003?

- wo wurden da die berechtigten Interessen der Aktionäre gewahrt?

Ich lese gerade im Jahresbericht - oder besser gesagt Märchensammlung - von 2004:

One absolute requirement is that all growth must be profitable. Our overriding goal is to deliver the best shareholder value in the paper industry.

=> klingt gut, war aber das exakte Gegenteil der Realität. Niemand traute sich die bereits damals schon prekäre Lage realistisch zu beschreiben. 2004 war noch eine gute Gelegenheit seine Aktien restlos zu verkaufen.

Dieser Jahresbericht liest sich erschreckend "Enron-mässig": http://www.norskeskog.com/Admin/Public/DWSDownload.aspx?File…

Da gab es einmal:

(a) LARS WILHELM GRØHOLT: Chair of the board since 2002, director since 2001.

Forest owner. Chair, Norwegian Forestry Research Institute (NISK) since October 2004, director since 2001. Chair, Norwegian Forest Owners' Association 1998-02. Chair Viken Skog 2000-02, Vest-Viken Forest Owners' Association 1999 and Drammen Forest Owners' Association 1993-99. Board member, Pan European Forest Certification (PEFC) 1999-03.

2006-03 gab es Kritik an ihm: https://www.nrk.no/okonomi/flengende-kritikk-av-groholt-1.56… - da war es aber schon zu spät => 2007 stellte er sich nicht mehr zur Wiederwahl: http://www.nettavisen.no/na24/917563.html

..und zuvor:

(b) Lage Westerbø: Chair of the board: 22 March 1989 – 29 April 2002 => im letzten Viertel seiner langjährigen Amtszeit wurden die fatalen Expansionsentscheidungen auf Pump getroffen. Ein Mann, der sich am Ende, 2002, wortlos vom Acker machte: https://www.nrk.no/okonomi/norske-skog-1-milliard-ned-1.5474… =>

Reinås also announced at the general meeting today that Norske Skog's chairman, Lage Westerbø, is leaving. He did not give any reason for the resignation.

(so lange zurück wird das Internet schon sehr zäh mit brauchbaren Info's...) Ein Überblick über seine Haufen Positionen, früher und heute: https://www.purehelp.no/role/viewManCV/43142511/lagecollingw…

Ich vermute, dass er auch ein Mann aus diesem Umfeld ist: Norske Skog wurde ja im Prinzip 1962 durch Vertreter der Norwegian Forest Owners Association (https://en.wikipedia.org/wiki/Norwegian_Forest_Owners_Associ…) gegründet - zusammen mit anderem Geld, um in Lavanger ihre erste Papierfabrik zu bauen: https://en.wikipedia.org/wiki/Norske_Skog_Skogn

=> d.h., irgendwann haben die Vertreter der privaten Waldbesitzer Norwegen's Norske Skog in Wahrheit für ihre eigenen Zwecke missbraucht - und keiner hielt sie auf.

Antwort auf Beitrag Nr.: 55.955.081 von faultcode am 15.10.17 01:18:01

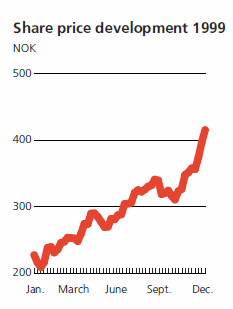

Ende 1999 sollte der Aktienkurs auch sein erstes historische Hoch erreichen; siehe Beitrag Nr. 9.

Aber im Grunde war es schon damals in Wahrheit zu spät für weiter nachhaltig steigende Aktienkurse - ganz unabhängig von der Weltkonjunktur - bedingt durch die Megaschulden der Gross-Übernahme in Neuseeland; siehe auch Beitrag Nr. 9.

=> d.h., 1999 war der Kipppunkt, was aber - fatalerweise - so im Chart nicht sichtbar wird:

=> hier wurde die Zukunft bereits verfrühstückt, dafür einen Aktienkurs mit rund +100% im Jahr der Party.

Das Wort "debt" taucht im Jahresbericht 1999 dutzende Mal auf - aber kein Chart dazu bei so vielen anderen Charts. Stattdessen Aussagen wie z.B.:

The Group’s net interest-bearing debt was NOK 7,618 million as of December 31, 1999 (NOK 7,082 million). Cash flow from operations was to a great extent used to amortise loans. The loan portfolio includes a mix of floating and fixed interest terms. Interest rate risk is hedged by employing securities or off balance sheet hedging instruments.

Average net interest rate on borrowing in 1999 was 6.5%. Of interest-bearing debt, 34% was in NOK and the rest in foreign currency, primarily USD and EUR. The ratio of net interestbearing debt to equity was 0.65. The Group’s target figure is 1.0 or less.

=> dieser letzte Satz aus diesem vollständigen Absatz ist auch bezeichnend, suggeriert er doch, dass alles vollkommen unter Kontrolle und in Ordnung ist. Bei dem oberen, auch rot markierten Satz sollten aber alle Alarmglocken läuten als Aktionär: es zeigt sich wie wichtig es ist, mitunter einen gezielten Blick in der Jahresbericht von Aktiengesellschaften zu werfen. Und man sieht, dass man oft noch genug Zeit hat als Aktionär zu auskömmlichen Preisen zu verkaufen, bevor die Niedergang seinen Lauf nimmt.

=> man sieht an diesem Business Case 18(!) Jahre später:

Schulden sind ein süsses Gift, und zuviele Schulden für ein Privatunternehmen - in Wahrheit - immer ein sehr hohes Risiko. Denn wenn sich das operative Geschäft nicht so entwickelt wie geplant, mitunter nur ein bischen schlechter als geplant, kann man ganz schnell in steile Rückenlage geraten, aus der es jahrelang - und oft bis zum Ende eines Unternehmens - kein Entrinnen mehr gibt.

die Hybris - der historische Abriss (1c) - 1999: das letzte gute Jahr, und Kippunkt

Charts aus obigem Jahresbericht 1999:

Ende 1999 sollte der Aktienkurs auch sein erstes historische Hoch erreichen; siehe Beitrag Nr. 9.

Aber im Grunde war es schon damals in Wahrheit zu spät für weiter nachhaltig steigende Aktienkurse - ganz unabhängig von der Weltkonjunktur - bedingt durch die Megaschulden der Gross-Übernahme in Neuseeland; siehe auch Beitrag Nr. 9.

=> d.h., 1999 war der Kipppunkt, was aber - fatalerweise - so im Chart nicht sichtbar wird:

=> hier wurde die Zukunft bereits verfrühstückt, dafür einen Aktienkurs mit rund +100% im Jahr der Party.

Das Wort "debt" taucht im Jahresbericht 1999 dutzende Mal auf - aber kein Chart dazu bei so vielen anderen Charts. Stattdessen Aussagen wie z.B.:

The Group’s net interest-bearing debt was NOK 7,618 million as of December 31, 1999 (NOK 7,082 million). Cash flow from operations was to a great extent used to amortise loans. The loan portfolio includes a mix of floating and fixed interest terms. Interest rate risk is hedged by employing securities or off balance sheet hedging instruments.

Average net interest rate on borrowing in 1999 was 6.5%. Of interest-bearing debt, 34% was in NOK and the rest in foreign currency, primarily USD and EUR. The ratio of net interestbearing debt to equity was 0.65. The Group’s target figure is 1.0 or less.

=> dieser letzte Satz aus diesem vollständigen Absatz ist auch bezeichnend, suggeriert er doch, dass alles vollkommen unter Kontrolle und in Ordnung ist. Bei dem oberen, auch rot markierten Satz sollten aber alle Alarmglocken läuten als Aktionär: es zeigt sich wie wichtig es ist, mitunter einen gezielten Blick in der Jahresbericht von Aktiengesellschaften zu werfen. Und man sieht, dass man oft noch genug Zeit hat als Aktionär zu auskömmlichen Preisen zu verkaufen, bevor die Niedergang seinen Lauf nimmt.

=> man sieht an diesem Business Case 18(!) Jahre später:

Schulden sind ein süsses Gift, und zuviele Schulden für ein Privatunternehmen - in Wahrheit - immer ein sehr hohes Risiko. Denn wenn sich das operative Geschäft nicht so entwickelt wie geplant, mitunter nur ein bischen schlechter als geplant, kann man ganz schnell in steile Rückenlage geraten, aus der es jahrelang - und oft bis zum Ende eines Unternehmens - kein Entrinnen mehr gibt.

Corporate Governance seit 2017

Nach obigem Abriss hatte ich noch diese Frage:wie sieht es eigentlich heutzutage mit der Corporate Governance bei Norske Skog aus? V.a. im Hinblick auf ein mögliches Weiterbestehen mit Annahme des Refinanzierungsplanes nächste Woche?

CEO und Präsident ist der relativ junge Lars P. S. Sperre (*1976), seit 2006 im Unternehmen und seit Mai 2017 CEO und Präsident. Zwar Jurist und möglichweise nur interimsweise, aber möglicherweise die beste aller Lösungen für den Übergang: http://www.norskeskog.com/Default.aspx?ID=2812

https://www.bloomberg.com/profiles/people/18718884-lars-p-sp…

Und Chair of the board?

Christen Sveeas (*1956), 2017 gewählt ; u.a. Gründer und Eigner der Kistefos AS: http://www.kistefos.no, einer Private Equity Firma mit sehr breit gestreuten Beteiligungen: https://en.wikipedia.org/wiki/Christen_Sveaas

http://www.norskeskog.com/People-and-press/People-and-organi…

https://www.abcnyheter.no/penger/naeringsliv/2017/10/11/1953…

=> kein "Holzfäller" mehr an dieser Stelle! Sondern ein Mann, der (in Norwegen) sicherlich gut bernetzt ist.

Beide keine Papiermacher, aber viel wichtiger als das ist Realismus, auch über die verbliebenen eigenen Möglichkeiten. Das sehe ich als gegeben an.

Weitere Verschiebung auf Mittwoch, 25.10. -- US Hedge Funds

Die Aktie legte bereits seit Mittwoch auf nun NOK0.77 zu - aber eine endgültige Lösung wurde immer noch nicht erreicht:

https://www.oslobors.no/ob_eng/markedsaktivitet/#/details/NS…

http://www.norskeskog.com/Default.aspx?ID=2890&t=2017-10-18T…

http://www.norskeskog.com/Default.aspx?ID=2890&t=2017-10-19T…

=>

...relevant boards in the Norske Skog group have resolved to revise the terms of the ongoing consent solicitation in accordance with the split agreed. The formal consent solicitation deadline is extended until Wednesday 25 October at 17:00 CET to allow adequate time for the group's noteholders to submit their formal consents.

Es liegt momentan nur ca. 50% Unterstützung der Unsecured Bondholders vor, was offenbar zu wenig ist:

...over 80% of the senior secured noteholders and more than 50% of the unsecured noteholders have now indicated their willingness to support such an adjusted recapitalization proposal...

Mein Eindruck: gestern und heute waren die letzten Tage, um alte Schrottaktien vor der völligen Entwertung loszuwerden.

Ein wichtiger Unsecured Bondholder hat ja bereits vor ein paar Tagen erklärt, dass er nicht unterstützen wird:

http://www.finanznachrichten.de/nachrichten-2017-10/41953478…

=>

Restructuring Capital Associates L.P. und seine Partnergesellschaft Bennett Management Corporation ("Bennett") gaben heute bekannt, dass sie den neuesten Rekapitalisierungsvorschlag von Norske Skog ablehnen. Bennet kam nach Überprüfung des gestern veröffentlichen, abgeänderten Rekapitalisierungsvorschlags zu diesem Entschluss. James Bennett, der Gründer von Bennett, erklärte:

"Die von Bennett verwalteten Fonds halten schon seit einigen Jahren unbesicherte Schuldverschreibungen von Norske Skog und besitzen derzeit über 50 % der 2026 Emission und über 40 % der 2033 Emission.

Zusammen sind dies EUR 100 Millionen der von Norske Skogindustrier ASA ausgegebenen vorrangigen unbesicherten Schuldverschreibungen ("SUNs"). Wir unterstützen eine Restrukturierung, welche die Umwandlung aller von uns gehaltenen Titel in Kapital vorsieht, aber wir sind nicht bereit, eine Abschreibung von 98 % zu akzeptieren, während die vorgeblich "besicherten" Schuldverschreibungen (die SSN und NSFs) EUR 421,7 Millionen für EUR 390 Millionen Nennbetrag der Titel erhalten (108 % Rückerstattung)...

=> beide Gesellschaften (US Hedge Funds) haben keine home page:

https://www.bloomberg.com/research/stocks/private/snapshot.a…

https://privatefunddata.com/fund-companies/restructuring-cap…

==> die, d.h. James Donald Bennett, hat sich verzockt - und muss nun seinen Klienten erklären, dass die Kohle so oder so fast weg ist.

=> das erinnert mich an einen alten Sinnspruch, der nun dabei ist, sich hier zu bewahrheiten:

Es ist wichtiger für einen Schuldner einen guten Gläubiger zu haben, als für einen Gläubiger einen guten Schuldner zu haben.

Antwort auf Beitrag Nr.: 55.985.505 von faultcode am 19.10.17 18:48:20

=> zumindest in dieser formellen Verlautbarung werden die US Hedge funds nicht erwähnt, auch nicht indirekt. Die anderen Mitteilungen werde ich später lesen - da gibt's vielleicht noch mehr Hintergründe... bis nächste Woche Dienstag.

Kurs heute: +1.32% => nichts Weltbewegendes.

Zumindest hat sich in meinen Augen verfestigt, dass der bestehende Vorschlag tatsächlich der allerletzte ist.

Take it or leave it.

=> neuer Termin: Tuesday 31 October at 17:00 CET

aus: http://www.norskeskog.com/Default.aspx?ID=2890&t=2017-10-25T…=> zumindest in dieser formellen Verlautbarung werden die US Hedge funds nicht erwähnt, auch nicht indirekt. Die anderen Mitteilungen werde ich später lesen - da gibt's vielleicht noch mehr Hintergründe... bis nächste Woche Dienstag.

Kurs heute: +1.32% => nichts Weltbewegendes.

Zumindest hat sich in meinen Augen verfestigt, dass der bestehende Vorschlag tatsächlich der allerletzte ist.

Take it or leave it.

Holmen B sagt (mir): diese Sache ist gelaufen

aus: http://www.nasdaqomxnordic.com/aktier/microsite?Instrument=S…

Es ist ja auch schwer vorstellbar, dass James Donald Bennett (MBA/Harvard Business School, 1980 (*) ) von seinem "Nein" vom 13.10. wieder zurücktritt, und bis morgen Abend plötzlich mit "Ja" stimmt:

http://www.finanznachrichten.de/nachrichten-2017-10/41953478…

Denn wenn er beim "Nein" bleibt, so bleibt ihm immer noch der Gang durch die Gerichte, um mehr für die ungesicherten Bondholder herauszuschlagen. Sagt er hingegen "ja", bleibt es klar bei den definierten Bedingungen, die er ja offenbar mehrfach ablehnte.

=> wenn ich (noch) länger warte, läuft mir der Holmen-Kurs immer noch weiter nach oben. Am 12.10., Threaderöffnung, standen wir noch bei SEK391 - heute bereits SEK410 (+4.8%).

__

(*) nein, ein MBA der Harvard Business School macht Dich nicht automatisch zu einem guten Investor, auch nicht von distressed assets.

Antwort auf Beitrag Nr.: 56.059.778 von faultcode am 30.10.17 16:01:41

=> jetzt wird's echt albern, weil es keinen neuen Vorschlag mehr geben wird - und Bennett und seine Investoren in den sauren Apfel werden beissen müssen.

Ich muss das auch von Zeit zu Zeit als Kleinanleger. Warum sollen die Grossen davon immer wieder verschont bleiben?

neue Deadline: Friday 3 November at 5 pm

aus: http://e24.no/boers-og-finans/norske-skogindustrier/ny-utset…=> jetzt wird's echt albern, weil es keinen neuen Vorschlag mehr geben wird - und Bennett und seine Investoren in den sauren Apfel werden beissen müssen.

Ich muss das auch von Zeit zu Zeit als Kleinanleger. Warum sollen die Grossen davon immer wieder verschont bleiben?

Antwort auf Beitrag Nr.: 56.067.410 von faultcode am 31.10.17 18:50:28

http://www.newsweb.no/newsweb/search.do?messageId=437919

Klartext hier --> Google Translater:

http://e24.no/boers-og-finans/norske-skogindustrier/sveaas-o…

=>

The board chose earlier today to leave the deadline and announce that they instead have the hope of being able to submit a new proposal that the last creditors can accept.

NSG in Olso heute: +1.37% => Optimismus in einem Pennystock sieht anders aus.

Holmen B (in SEK, SE0000109290) in 1 Monat: +7.16% --> Outperformer

NASDAQ OMX Stockholm All-Share GR SEK: +1.91%

=> ich denke, am Ende wird es doch zu einer Einigung kommen mit genügend Bondholdern. Ich vermute mehrheitlich auf Kosten der Rest-Aktionäre, denn die sind die einzigen auf der schwachen Seite, bei denen (noch) überhaupt was zu holen ist:

=> komplett überteuerte Aktie vor diesem Hintergrund.

doch neuer Vorschlag

kunstvoll verpackt in dieser offiziellen Mitteilung:http://www.newsweb.no/newsweb/search.do?messageId=437919

Klartext hier --> Google Translater:

http://e24.no/boers-og-finans/norske-skogindustrier/sveaas-o…

=>

The board chose earlier today to leave the deadline and announce that they instead have the hope of being able to submit a new proposal that the last creditors can accept.

NSG in Olso heute: +1.37% => Optimismus in einem Pennystock sieht anders aus.

Holmen B (in SEK, SE0000109290) in 1 Monat: +7.16% --> Outperformer

NASDAQ OMX Stockholm All-Share GR SEK: +1.91%

=> ich denke, am Ende wird es doch zu einer Einigung kommen mit genügend Bondholdern. Ich vermute mehrheitlich auf Kosten der Rest-Aktionäre, denn die sind die einzigen auf der schwachen Seite, bei denen (noch) überhaupt was zu holen ist:

=> komplett überteuerte Aktie vor diesem Hintergrund.

Antwort auf Beitrag Nr.: 56.096.120 von faultcode am 03.11.17 20:24:01

Dass kann aber in Norwegen rational niemand wollen. Denn dann hätte man auch noch US-Gläubiger und Eigentümer von norwegischem Grund und Boden für Jahre vor der eigenen Haustür.

Denn womit sonst sollte der (massgeblich norwegische) NSG-Aufsichtsrat den letztendlich erpresst worden sein können?

Interessant ist in diesem Zusammenhang auch, dass die Aktien des konkurrierenden US-Anbieters Verso Corporation (VRS) (der aber nach meinen Info's massgeblich in die USA hineinverkauft) im letzten Monat um +34% zulegten:

https://finance.yahoo.com/quote/VRS?p=VRS

https://www.wallstreet-online.de/aktien/verso-registered-a-a…

Operativ geht es Verso auch nach Chapter 11 (2016) immer noch nicht gut - sieht aber vorsichtig nach Turnaround aus.

Spekulation über Erpressung

Nach endlosen Verhandlungsrunden seit Juni, kann ich mir vorstellen, dass die massgeblichen US Bondholder der Unsecured Bonds mit US-Anwälten hinter den Kulissen gedroht haben - in dem Sinne, dass man den Insolvenz-Prozess so massiv stören und verlängern könnte, dass am Ende Norske Skog auch noch operativ zugrunde geht. Das geht relativ leicht, indem man z.B. US-Kunden von NSG-Papier entsprechend argumentativ bearbeitet.Dass kann aber in Norwegen rational niemand wollen. Denn dann hätte man auch noch US-Gläubiger und Eigentümer von norwegischem Grund und Boden für Jahre vor der eigenen Haustür.

Denn womit sonst sollte der (massgeblich norwegische) NSG-Aufsichtsrat den letztendlich erpresst worden sein können?

Interessant ist in diesem Zusammenhang auch, dass die Aktien des konkurrierenden US-Anbieters Verso Corporation (VRS) (der aber nach meinen Info's massgeblich in die USA hineinverkauft) im letzten Monat um +34% zulegten:

https://finance.yahoo.com/quote/VRS?p=VRS

https://www.wallstreet-online.de/aktien/verso-registered-a-a…

Operativ geht es Verso auch nach Chapter 11 (2016) immer noch nicht gut - sieht aber vorsichtig nach Turnaround aus.

Insolvenz-Vorbereitung

https://www.euwid-paper.com/news/singlenews/Artikel/investme…=>

Oceanwood Capital Management and Aker Capital will form new company which will bid an an auction process to take over Norske Skog. Following the announcement by Oceanwood and Aker, a consensual recapitalisation of the Norske Skog group is unlikely to be achievable, Norske Skog says. The company therefore expects to initiate insolvency proceedings.

According to a Norske Skog release, funds managed by Oceanwood Capital Management and Aker Capital AS, a wholly owned subsidiary of Aker ASA, have issued a joint press release stating the intention to form a new company (Bidco), which will bid in an auction process to ensure that there is a strong new owner of Norske Skog's paper mills.

The board of directors of Norske Skogindustrier stated it is pleased that Aker has taken a role together with Oceanwood in the recapitalization of the Norske Skog group.

The group's seven paper mills are expected to continue as normal without interruption through the remainder of the recapitalization process.

Following the announcement by Oceanwood and Aker, a consensual recapitalisation of the Norske Skog group is unlikely to be achievable, Norske Skog says. Consequently, the company is likely to initiate insolvency proceedings. The board of directors of Norske Skogindustrier said it would continue to assess the situation and the implications of the recent developments.

=> der Markt glaubt es nun auch (endlich):

__

http://e24.no/boers-og-finans/norske-skogindustrier/tror-ake…

=> Skepsis bei Analysten über die längerfristigen Überlebens-Chancen der Fabriken --> die Prozess-Konversion in Kartonage (von Newsprint) z.B., würde wieder viele Investitionen der neuen Eigentümer erfordern...

=> the joint bidders:

http://www.oceanwood.com/

https://www.akerasa.com/ --> 2/3 Oil and gas holdings:

(NO0010234552): https://www.wallstreet-online.de/aktien/aker-asa-a-aktie

--> ein norwegischer, global asset manager; hoch gehebelt; ABER: Trailing P/E (2017-06): 1.69

Antwort auf Beitrag Nr.: 55.953.356 von faultcode am 14.10.17 13:57:38

https://www.wallstreet-online.de/nachricht/10127427-deutschl…

=>

...Auch die SBB ermöglichen seit gut einem Jahr den Bitcoin-Handel an sogenannten Billetautomaten, was schon über 6.000 Kunden genutzt haben, so Cash.ch. Der Automat spuckt nach der Transaktion einen Zettel mit dem Bitcoin-Guthaben aus, der per Handy-App in eine Art elektronisches Portemonnaie eingelesen werden kann...

Bitcoins und das Quittungspapier am ATM

Tja - nun generieren also Strassenverkäufe von Bitcoins und Co. also (kleinste) Nachfrage nach schnödem, grafischen Papier

https://www.wallstreet-online.de/nachricht/10127427-deutschl…

=>

...Auch die SBB ermöglichen seit gut einem Jahr den Bitcoin-Handel an sogenannten Billetautomaten, was schon über 6.000 Kunden genutzt haben, so Cash.ch. Der Automat spuckt nach der Transaktion einen Zettel mit dem Bitcoin-Guthaben aus, der per Handy-App in eine Art elektronisches Portemonnaie eingelesen werden kann...

Launch of sales process for Norske Skog AS

http://www.norskeskog.com/Default.aspx?ID=2890&t=2017-12-13T…=>

Norske Skog AS has appointed Evercore Partners International LLP (Evercore - London/UK) to act as its financial adviser in connection with a sale of Norske Skog AS and its subsidiaries (the Norske Skog group's operating businesses) by way of a competitive sale process which will commence imminently. A range of bidders will be invited to participate in the competitive sale process.

Norske Skog group's seven paper mills will continue as normal, and our customers, suppliers and other business partners will continue to receive high quality products and services from Norske Skog without interruption throughout the competitive sale process.

Any parties, including any existing Norske Skog investors, together with any corporates or financial investors, which are interested in participating in the sale process are invited to contact Evercore as soon as possible to indicate their interest...

=> am Ende kann man vielleicht (irgendwie) sehen, was materielle Buchwerte wirklich wert sind.

OSLO BØRS - SUSPENDED

so, in Oslo ist Schluss mit den Aktien (in Frf. auch):letzte Preisfestellung: 18 Dec -- NOK0.25

Appointment of bankruptcy trustee in Norske Skog companies

20.12.http://www.norskeskog.com/Default.aspx?ID=2890&t=2017-12-20T…

Oslo Byfogdembete (Oslo Bankruptcy Court) has on 19 December and 20 December 2017, appointed lawyer Tom Hugo Ottesen as bankruptcy trustee for the following companies:

- Norske Skogindustrier ASA

- Norske Treindustrier AS

- Norske Skog Holding AS

- Lysaker Invest AS

- Norske Skog Eiendom AS

In addition to the bankruptcy filing of Norske Skogindustrier ASA on 19 December 2017, the board of directors of Norske Treindustrier AS, Lysaker Invest AS, Norske Skog Eiendom AS and Norske Skog Holding AS have filed for bankruptcy at Oslo Byfogdembete (Oslo bankruptcy court) today, Wednesday 20 December 2017.

The deadline for claims to the bankruptcy trustee is set to 23 January 2018.

...

The group's operational activities will continue in Norske Skog AS as normal with as little impact as possible from the bankruptcy proceedings of the above companies.

The non-listed Norske Skog AS will be the new operating parent company of the Norske Skog group, and will continue the head office function that has been performed by Norske Skogindustrier ASA.

Oceanwood Capital Management - Private Equity --> hart bleiben (1)

Oceanwood (London - Malta  ) hat wohl den US Hedge funds, hier zu nennen Restructuring Capital Associates L.P. und Partnergesellschaft Bennett Management Corporation, die ungesicherten Anleihen alle abgenommen:

) hat wohl den US Hedge funds, hier zu nennen Restructuring Capital Associates L.P. und Partnergesellschaft Bennett Management Corporation, die ungesicherten Anleihen alle abgenommen:19.12.

https://www.euwid-papier.de/news/einzelansicht/Artikel/norsk…

=>

Norske Skogindustrier ASA, Oslo, hat heute, Dienstag, den 19. Dezember, beim zuständigen Gericht in Oslo das Insolvenzverfahren beantragt.

„Die Entscheidung des Vorstands war einstimmig und wird damit begründet, dass wir keine realistischen Chancen mehr sehen, eine freiwillige Rekapitalisierung für die Norske Skog Gruppe zu erreichen“, heißt es in einer offiziellen Mitteilung. Oceanwood, der Mehrheitsgläubiger der Gruppe und inzwischen Inhaber aller NSF-Anleihen und einer Mehrzahl der besicherten Anleihen des Unternehmens (Senior Secured Notes), habe Norske Skog darüber informiert, dass er nicht bereit sei, eine solche freiwillige Refinanzierung zu unterstützen, heiß es weiter...

=> da wird es wohl einen Vetrag geben zwischen den James Donald Bennett und Oceanwood - (a) alles Geld jetzt, oder (b) erst einen Teil und den Rest, mit vielen Abhängigkeiten, z.B. von zukünftiger Performance, später.

Ich tippe auf (b).

---> im Dunkeln lässt sich munkeln. Man wird es vermutlich eher nicht erfahren; irgendwo tief drin in zukünftigen "Paradise Papers"

__

hier die Originalmeldung - für alle Fälle: http://ir.asp.manamind.com/products/html/companyDisclosuresA…

=>

Norske Skogindustrier ASA - decision to file for bankruptcy

19.12.2017 08:53

The board of Directors of Norske Skogindustrier ASA has decided to file for bankruptcy at Oslo skifterett (Oslo bankruptcy court) today, Tuesday 19 December 2017. The board's decision is unanimous and is due to the fact that there is no longer a realistic opportunity to achieve a voluntary recapitalization solution for the Norske Skog group.

The group's largest secured creditor, Oceanwood Capital Management Ltd (Oceanwood), has informed the board that it is not willing to support any such solution.

...

The non-listed Norske Skog AS will be the new operating parent company of the Norske Skog

group, and will continue the head office function that has been performed by Norske Skogindustrier ASA.

- The board and management of Norske Skogindustrier ASA have over an extended

period worked hard to achieve a consensual recapitalization of the Norske Skog group and thereby avoid bankruptcy proceedings for the parent company. This work was well advanced and had broad support from the capital structure in October and November 2017. The board's decision to file for bankruptcy is therefore made with great disappointment that this goal was not achieved, said Christen Sveaas, Chairman of the board of Norske Skogindustrier ASA

The recapitalization process has been extremely challenging due to the Group's very complex capital structure. Therefore, a contingency plan has been prepared during the autumn for the event that the consensual recapitalization failed. Consequently, the group's seven paper mills and all key stakeholders as well as employees, customers, suppliers and local authorities are prepared for the process that now must be implemented.

- It is expected that the bankruptcy process of the listed parent company will not have any particular consequences for operations at Norske Skog's seven paper mills. The operations will continue as normal, and all customers will continue to receive quality products from Norske Skog as before, Sveaas said.

The current board of directors was elected on 24 August 2017, and has from that day worked hard and intensively to analyze the group's situation and prepare realistic solutions with management and the company's financial and legal advisors. The new board announced on 12 September 2017 the board's plan to launch an industry-based recapitalization transaction. This proposal was based on the board's view of the level of debt and future interest payments that

Norske Skog's business could sustain. The recapitalized new Norske Skog consequently had significantly less debt than in the proposals announced earlier in 2017 from both the company and the company's creditors. The Board's industrial recapitalization proposal was however never made public as a result of the committee for the secured creditors prior to the announcement made it

clear that they would not support the board's proposal.

Then, the board proceeded with an adjusted recapitalization proposal following extensive dialogue with the committee for the secured creditors, the committee for the unsecured creditors and the company's shareholders. The board launched a proposal for a consensual recapitalization solution on 18 September 2017. In this proposal, the debt level was increased somewhat in line with the view of the secured creditors' committee, and the exchange ratio for equity of the

parent company was adjusted somewhat in line with the views of both the unsecured and secured creditors' committees. While this proposal did not achieve sufficient support from all creditor groups, there was still broad support for a recapitalization transaction in which all unsecured bond debt would be converted into equity and parts of the secured debt would also be converted into equity in order to achieve a sound capitalization of the new Norske Skog group.

After further dialogue among stakeholders, the board on 11 October 2017 announced its third and last recapitalization proposal. This proposal obtained support from both the group's unsecured creditors and among the creditors in the group's secured bond loan. However, the recapitalization proposal did not receive the necessary support from the creditors in the group's EUR 100 million

NSF facility (NSF facility), which is issued by Norske Skog AS.

The subsequent negotiations with the creditors of the NSF facility over a solution in which support for the board's recapitalization proposal could be achieved ended unsuccessfully. However, the process resulted in Oceanwood resolving to buy out the creditors of the NSF facility, so that Oceanwood currently controls 100% of the NSF facility. Oceanwood also purchased additional

significant holdings in the secured bond loan, where they are currently expected to own a stake well above 50%.

Oceanwood then chose to enter into an industrial partnership with Aker Capital AS, and announced on 23 November 2017, through a joint press release, that they had decided not to support further work on implementing a consensual recapitalization solution, despite the fact that the board's third recapitalization proposal at this time seemed to have support both among the

group's secured creditors, the unsecured creditors and the parent company's shareholders.

Following the announcement of 23 November 2017, the board of directors of the parent company has attempted to bring Oceanwood and Aker Capital AS to change their positions in relation to a consensual recapitalization, but this has been unsuccessful. Oceanwood has later, in writing, confirmed to the board its position, namely that it is not willing to support a voluntary recapitalization.

The board has in the dialog with Oceanwood and Aker Capital AS suggested that Oceanwood and Aker Capital AS invite existing shareholders in Norske Skogindustrier ASA as co-investors on the same terms as Oceanwood and Aker Capital AS' joint venture, if it were to become the new owner of Norske Skog AS.

Such a continuation of today's shareholders would in the view of the board ensure a strategic value for the new parent company in having shareholders where a considerable number also are fibre suppliers to the group, and many which are employed by the group. It still remains uncertain if such a co-investment opportunity will be offered to existing shareholders.

In the dialogue with Oceanwood and Aker Capital AS, the Board has expressed the opinion that it believes that a voluntary recapitalization solution would be a adequate way to realize Aker Capital AS's industrially motivated intention to become a new controlling owner of Norske Skog. By a voluntary recapitalization transaction, Oceanwood would through the debt conversion end up as owner of a substantial part of the equity of a recapitalized Norske Skog that could have been offered to Aker Capital AS. The auction process that will now be implemented for Norske Skog AS will be open to all stakeholders, and it is currently unclear who will be the owner of Norske Skog's operational business when the auction process is completed.

In the period following the announcement of 23 November 2017 from Oceanwood and Aker Capital AS, the board has explored whether other realistic solutions could be found in order to avoid bankruptcy of Norske Skogindustrier ASA. For instance, it has been assessed whether it would be possible to convert all unsecured debt to equity while the secured part of the group's debt could be handled by selling the group's operating business through the secured bond

loan's ongoing enforcement process. However, this has also proved to be impossible, partly due to lack of liquidity, remaining pension commitments, and Oceanwood's lack of willingness to convert the parent company's debt to operating subsidiaries and the perpetual bonds to equity.

The board and management have also worked on a contingency plan for the event that the recapitalization process should end with enforcement from the secured creditors, and a subsequent bankruptcy for the listed Norske Skogindustrier ASA. It is therefore a well-prepared process that is now being implemented, in which Norske Skog's operating business is to be valued in accordance with the requirements agreed between the creditors in the inter-creditor agreement to which the group is a party. The board and management have fully cooperated with

both the trustees for the secured bond loan, their financial and legal advisors and the board of Norske Skog AS over the recent period in order to facilitate a smooth process in line with the obligations and provisions that apply to the current situation.

The management and all employees at the headquarter have received binding offers of employment from Norske Skog AS, and the head office function will continue through Norske Skog AS. The operating business will continue with the least disturbances possible, and suppliers and customers of the mills should expect no changes to Norske Skog's ongoing operations as a result of the bankruptcy proceedings of Norske Skogindustrier ASA.

The board wishes to thank all the employees of the Norske Skog group for demonstrating determination and a strong commitment throughout the demanding recapitalization process that has taken place during 2017. The board also wishes to thank the group's customers and suppliers, who have continued to trade with the group's companies in the challenging financial situation that has existed during 2017.

Oslo Stock Exchange has suspended trading of the shares of Norske Skogindustrier ASA.

...

Antwort auf Beitrag Nr.: 56.533.493 von faultcode am 22.12.17 20:27:12

Tja, vorher besser wirtschaften, dann bleibt man auch Herr im eigenen Haus:

=> da sind nun vermutlich nun ein paar Alt-Männerfeindschaften (im kleinen Norwegen --> cf. Aker) entstanden

=> auf der anderen Seite: Oceanwood möchte sicherlich - und von Anfang an - diese ganze norwegische Waldbesitzer-Clique mit einem Schlag loswerden.

Das muss man auch mal von der Seite sehen. Und: einflussreiche Unterstützer in Norwegen selber mit der Aker-Gruppe haben sie ja auch.

Denn wer sitzt denn wieder auf "der anderen Seite"?

-> z.B. ein Alt-CEO Sven Ombudstvedt (CEO 1.1.2010 - 7.5.2017), der ab Mai 2017 als central adviser for secured creditors in Norske Skog, mutmasslich v.a. norwegischen Secured bondholders, unterwegs war -- und der am endgültigen Untergang von Norske Skog auch nicht ganz unschuldig war mit seinen ganzen Diversifizierungs-Ausflügen, die v.a. auch wieder nur (neues) Geld gekostet haben:

- Gesundschrumpfen war ihm, und dem BoD dahinter, mal wieder viel zu schnöde und wenig --> die Hybris ging (mMn) mit ihn in veränderter Form einfach weiter.

Oceanwood Capital Management --> hart bleiben (2)

Ui Ui, da ist wer sauer.Tja, vorher besser wirtschaften, dann bleibt man auch Herr im eigenen Haus:

=> da sind nun vermutlich nun ein paar Alt-Männerfeindschaften (im kleinen Norwegen --> cf. Aker) entstanden

=> auf der anderen Seite: Oceanwood möchte sicherlich - und von Anfang an - diese ganze norwegische Waldbesitzer-Clique mit einem Schlag loswerden.

Das muss man auch mal von der Seite sehen. Und: einflussreiche Unterstützer in Norwegen selber mit der Aker-Gruppe haben sie ja auch.

Denn wer sitzt denn wieder auf "der anderen Seite"?

-> z.B. ein Alt-CEO Sven Ombudstvedt (CEO 1.1.2010 - 7.5.2017), der ab Mai 2017 als central adviser for secured creditors in Norske Skog, mutmasslich v.a. norwegischen Secured bondholders, unterwegs war -- und der am endgültigen Untergang von Norske Skog auch nicht ganz unschuldig war mit seinen ganzen Diversifizierungs-Ausflügen, die v.a. auch wieder nur (neues) Geld gekostet haben:

- Gesundschrumpfen war ihm, und dem BoD dahinter, mal wieder viel zu schnöde und wenig --> die Hybris ging (mMn) mit ihn in veränderter Form einfach weiter.

Antwort auf Beitrag Nr.: 56.533.646 von faultcode am 22.12.17 20:48:25

founded in 2005, is an SEC registered event driven firm with particular expertise in distressed and special situations. Our flagship fund, the Foxhill Opportunity Fund, L.P. was launched January 2006. Our fundamental research process is based on over 25 years experience managing hedge funds.

FCP hält 11.75% der SSN's (2019) (SSN = Senior Secured Notes = besicherten Schuldverschreibungen)

Aber: http://mma.prnewswire.com/media/622422/Foxhill_Capital_Partn…

=>

FCP ist mit dem anvisierten Auktionsprozess gleich in mehrfacher Hinsicht nicht einverstanden (-> 5 Kritikpunkte), und will nun eine eigene Gruppe für Minderheits-Secured Bondholders bilden, sowie unabhängige Berater engagieren.

=> demnach:

1/ monatelange: Unsecured bondholders vs. Secured bondholders

und nun:

2/ Secured bondholders vs Secured bondholders.

=> ist ist aufschlussreich zu sehen, dass solche Distressed Securities nicht beliebig kleinteilig verteilt sind, sondern sich (am Ende) oft in hoch-konzentrierter Form bei wenigen Marktteilnehmern wiederfinden - die sich nun somit mutmasslich zum ersten Mal im Leben gegenüberstehen.

Die neue, non-listed Norske Skog AS wirtschaftet also unter Aufsicht des Insolvenzverwalters in einem halbwegs überlebensfähigen Zustand, da ja schon länger keine Zinsen oder gar Tilgungen bezahlt werden - und man mit dem operativen Geschäft ausreichend Cash generiert (auch wenn sowas nicht beliebig lange funktionieren kann, weil mitunter schon strategisch wichtige Fragen einfach auftauchen werden -> wer soll die zuverlässig, einstimmig und haftbar beantworten können?):

=> und so geht das Ende der alten Norske Skogindustrier ASA auch in 2018 weiter.

__

Der finanzielle Stand lt. Gericht im Überblick:

- total debt: NOK9.24b

- book value: NOK2.87b

aus: https://www.nettavisen.no/na24/norske-skogs-gjeld-9244443378…

neuer Ärger aus USA: Foxhill Capital Partners (FCP)

Das forsche Vorgehen von Oceanwood stösst nun auf US-Widerstand, hier durch FCP, http://www.foxhillcapital.com/:founded in 2005, is an SEC registered event driven firm with particular expertise in distressed and special situations. Our flagship fund, the Foxhill Opportunity Fund, L.P. was launched January 2006. Our fundamental research process is based on over 25 years experience managing hedge funds.

FCP hält 11.75% der SSN's (2019) (SSN = Senior Secured Notes = besicherten Schuldverschreibungen)

Aber: http://mma.prnewswire.com/media/622422/Foxhill_Capital_Partn…

=>

FCP ist mit dem anvisierten Auktionsprozess gleich in mehrfacher Hinsicht nicht einverstanden (-> 5 Kritikpunkte), und will nun eine eigene Gruppe für Minderheits-Secured Bondholders bilden, sowie unabhängige Berater engagieren.

=> demnach:

1/ monatelange: Unsecured bondholders vs. Secured bondholders

und nun:

2/ Secured bondholders vs Secured bondholders.

=> ist ist aufschlussreich zu sehen, dass solche Distressed Securities nicht beliebig kleinteilig verteilt sind, sondern sich (am Ende) oft in hoch-konzentrierter Form bei wenigen Marktteilnehmern wiederfinden - die sich nun somit mutmasslich zum ersten Mal im Leben gegenüberstehen.

Die neue, non-listed Norske Skog AS wirtschaftet also unter Aufsicht des Insolvenzverwalters in einem halbwegs überlebensfähigen Zustand, da ja schon länger keine Zinsen oder gar Tilgungen bezahlt werden - und man mit dem operativen Geschäft ausreichend Cash generiert (auch wenn sowas nicht beliebig lange funktionieren kann, weil mitunter schon strategisch wichtige Fragen einfach auftauchen werden -> wer soll die zuverlässig, einstimmig und haftbar beantworten können?):

=> und so geht das Ende der alten Norske Skogindustrier ASA auch in 2018 weiter.

__

Der finanzielle Stand lt. Gericht im Überblick:

- total debt: NOK9.24b

- book value: NOK2.87b

aus: https://www.nettavisen.no/na24/norske-skogs-gjeld-9244443378…

Antwort auf Beitrag Nr.: 56.096.120 von faultcode am 03.11.17 20:24:01

18.12.: 429.9 SEK (1 Tag vor Insolvenzantrag)

29.12.: 435.9 SEK

=> +1.4% dazugewonnen

=> nicht gerade beeindruckend.

Allerdings hat der Markt die Annahme einer Norske Skog-Insolvenz schon ganz gut vorher (neben anderen Faktoren) eingepreist (meine Unterstellung):

Trailing Returns % (SEK), 28/12/2017 YTD:

Holmen B: +36.38%

NASDAQ OMX Stockholm All-Share GR SEK: +10.35%

aus: http://www.nasdaqomxnordic.com/aktier/microsite?Instrument=S…

(hat den Markt auf 10Y-TR-Sicht aber (noch) nicht geschlagen wie man oben sieht --> Crossover 2018/19 ?)

=> man sieht (mal wieder): die überlebenden (öffentlichen) Unternehmen in schrumpfenden, aber sich konsolidierenden Industrien können auch echte Gewinner sein (v.a. wenn die Notenbanken noch unterstützend wirken...).

Ein einfacher Grund (bei Industrie-Unternehmen):

- der äussere Zwang zu Forschung und Entwicklung lässt nach (research and development, R&D) --> damit kann das Unternehmen hierbei sparen (wenn es opportun erscheint).

R&D-Aufwendungen lt. Annual Reports:

- 2016: SEK95m (bei net sales SEK15.5b == -3.1% YtY; EBITDA SEK2.87b)

...

- 2013: SEK110m (bei net sales SEK16.2b == -9.0% YtY; EBITDA SEK0.429b)

=> man sieht:

1/ Umsatz ging in 3Y um -4.3% zurück

2/ aber R&D-Kosten um -13.6%!

=> OBWOHL sich das EBITDA (was OK ist als KPI, da es eine gewisse Vergleichbarkeit erlaubt) in dieser Zeit deutlich ausweitete => es gäbe eigentlich gar keinen Grund R&D so überproportional herunterzufahren (ausser shareholder value ). Stichwort Inflation auch in diesem Zusammenhang.

). Stichwort Inflation auch in diesem Zusammenhang.

..und natürlich liest man auch im AR2016 solche schönen Sätze wie z.B.:

Holmen creates climate benefit

Carbon dioxide is captured in the growing forests and in the products. The resource-efficient production is predominantly driven by renewable energy. Investments in company-produced energy and the development of today’s products and new products based on forest raw material mean the positive climate effects will be even greater in the future. The Group’s investments in research and development amounted to approximately SEK 95 million in 2016.

=> Heuchelei wo man hinschaut...

Holmen B-Performance

Holmen B (ISIN SE0000109290) seit Insolvenz Norske Skog (immer Close; http://www.nasdaqomxnordic.com/aktier/microsite?Instrument=S…):18.12.: 429.9 SEK (1 Tag vor Insolvenzantrag)

29.12.: 435.9 SEK

=> +1.4% dazugewonnen