Alkane Resources - Seltene Erden, Gold, Nickel - 500 Beiträge pro Seite

eröffnet am 12.04.10 10:17:23 von

neuester Beitrag 25.10.23 16:43:51 von

neuester Beitrag 25.10.23 16:43:51 von

Beiträge: 1.530

ID: 1.157.088

ID: 1.157.088

Aufrufe heute: 0

Gesamt: 205.505

Gesamt: 205.505

Aktive User: 0

ISIN: AU000000ALK9 · WKN: 863617 · Symbol: AK7

0,3980

EUR

-3,40 %

-0,0140 EUR

Letzter Kurs 19.04.24 Tradegate

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 31,90 | +18,10 | |

| 0,8000 | +17,65 | |

| 0,5500 | +14,61 | |

| 0,8200 | +12,33 | |

| 11,420 | +11,41 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,2100 | -7,63 | |

| 2,1800 | -9,17 | |

| 69,01 | -9,53 | |

| 4,2300 | -17,86 | |

| 47,85 | -97,99 |

In den letzten Monaten wurde viel über die marktbeherrschende Rolle Chinas hinsichtlich REE berichtet. Mittlerweile gibt es auch aussichtsreiche Vorkommen in der westl. Hemisphäre (Aru, Avl , GGG, Lyc etc.), jedoch sollte man diese Vorkommen differenziert betrachten.

Ree`s sind immer ein Warenkorb verschiedener Metalle, die zu höchst unterschiedlichen Preisen gehandelt werden. Die wertvollsten Metalle sind hier die sog. schweren REE !

Der folgende Link führt zwar zu einer Präsentation von Greenland Minerals, auf Seite 15 ist jedoch eindrucksvoll zu sehen, wer von den REE-Explorern hinsichtlich schwerer REE die Nase vorn hat …

http://www.ggg.gl/userfiles/GGG_website-%20Presentation_2010…

Dieser Artikel (auszugsweise) mag die hervorragende Position von Alkane (DUBBO ZIRCONIA PROJECT) unterstreichen:

RARE earths were apparently the hot topic at the recent Prospectors & Developers Association of Canada shindig in Toronto, where 21,600 resources types schmoozed one another.

• Robin Bromby

• From: The Australian

• April 12, 2010 12:00AM

… One of the highlights, according to our reliable informant, was a presentation by geologists David Lentz of the University of New Brunswick and Boston-based Anthony Mariano. (Incidentally, Mariano will be in Australia next week, his first visit since 1983, giving several investor briefings on rare earths. We expect brokers and high-net-worth types to be very interested in what he has to say.)

The presentation was highly technical, but it seems to us that the bottom line was that considerable caution needs to be applied to assessing rare earths projects. As Lentz and Mariano point out, even the rarest of rare earth elements are more than 200 times more abundant than gold, they occur mostly as impurities in rock minerals and only a few of such deposits are worth a cracker.

They also made another good point: that projects are more attractive if they contain the heavy rare earths.

You can see this from the prices fetched. These minerals are not openly traded, but the most recent Chinese figures show the difference. Among the "heavy" rare earths, europium (which gives you red on your TV or computer screen) was bringing over $US475/kg; terbium (used in magnets) was worth at least $US340/kg; and dysprosium (magnets and lasers) could bring upwards of $US107/kg.

By contrast, the "light" rare earths are in a different price bracket. Lanthanum (used in re-chargeable batteries) brought under $US6/kg, cerium (used in glass) under $US4/kg, with neodymium (magnets, lasers, glass) fetching around $US14/kg…

Zur Homepage von Alkane Resources geht es hier:

http://www.alkane.com.au/

Und hier findet ihr die letzte Präsentation vom 30.03.2010:

http://www.alkane.com.au/presentations/

Ich habe mir heute eine Kaufempfehlung gegeben

Ree`s sind immer ein Warenkorb verschiedener Metalle, die zu höchst unterschiedlichen Preisen gehandelt werden. Die wertvollsten Metalle sind hier die sog. schweren REE !

Der folgende Link führt zwar zu einer Präsentation von Greenland Minerals, auf Seite 15 ist jedoch eindrucksvoll zu sehen, wer von den REE-Explorern hinsichtlich schwerer REE die Nase vorn hat …

http://www.ggg.gl/userfiles/GGG_website-%20Presentation_2010…

Dieser Artikel (auszugsweise) mag die hervorragende Position von Alkane (DUBBO ZIRCONIA PROJECT) unterstreichen:

RARE earths were apparently the hot topic at the recent Prospectors & Developers Association of Canada shindig in Toronto, where 21,600 resources types schmoozed one another.

• Robin Bromby

• From: The Australian

• April 12, 2010 12:00AM

… One of the highlights, according to our reliable informant, was a presentation by geologists David Lentz of the University of New Brunswick and Boston-based Anthony Mariano. (Incidentally, Mariano will be in Australia next week, his first visit since 1983, giving several investor briefings on rare earths. We expect brokers and high-net-worth types to be very interested in what he has to say.)

The presentation was highly technical, but it seems to us that the bottom line was that considerable caution needs to be applied to assessing rare earths projects. As Lentz and Mariano point out, even the rarest of rare earth elements are more than 200 times more abundant than gold, they occur mostly as impurities in rock minerals and only a few of such deposits are worth a cracker.

They also made another good point: that projects are more attractive if they contain the heavy rare earths.

You can see this from the prices fetched. These minerals are not openly traded, but the most recent Chinese figures show the difference. Among the "heavy" rare earths, europium (which gives you red on your TV or computer screen) was bringing over $US475/kg; terbium (used in magnets) was worth at least $US340/kg; and dysprosium (magnets and lasers) could bring upwards of $US107/kg.

By contrast, the "light" rare earths are in a different price bracket. Lanthanum (used in re-chargeable batteries) brought under $US6/kg, cerium (used in glass) under $US4/kg, with neodymium (magnets, lasers, glass) fetching around $US14/kg…

Zur Homepage von Alkane Resources geht es hier:

http://www.alkane.com.au/

Und hier findet ihr die letzte Präsentation vom 30.03.2010:

http://www.alkane.com.au/presentations/

Ich habe mir heute eine Kaufempfehlung gegeben

Das Unternehmen hat eine MK von ca. 60 mio. €, einen cash-Bestand von ca. 3. mio, einen cashBedarf von ca. 100 mio. in den nächsten 3 Jahren und erwartet einen Umsatz von ca. 70 mio. € nach 2013.

Es dürften also demnächst kräftige Kapitalerhöhungen anstehen.

Es dürften also demnächst kräftige Kapitalerhöhungen anstehen.

Der REO-grade ist bei Lynas 14 %, bei Alkane 0,75 %.

Lynas rechnet mit Produktionskosten von ca. 6 USD/kg.

Keine Ahnung, was das bei 0,75 % kostet.

Lynas rechnet mit Produktionskosten von ca. 6 USD/kg.

Keine Ahnung, was das bei 0,75 % kostet.

D.h. Lynas holt aus 1 t Erz 140 kg REO. mit 15 USD/kg sind das 2100 USD/t.

Alkane will mit 400000 t/a 100 mio USD Umsatz generieren, d.h. 250 USD/t incl. Zirkon, Hf, Nb etc.

Alkane will mit 400000 t/a 100 mio USD Umsatz generieren, d.h. 250 USD/t incl. Zirkon, Hf, Nb etc.

Aus ähnlichen Überlegungen bin auch ich nach über einem jahrvor kurzem wieder aus Alkane rausgegangen: Ich denke, hier hat man noch viiieeeel Zeit, um von der Seitenlinie aus zuzusehen .. und währenddessen mit den anderen RE-Explorern/Produzenten schon echtes Geld zu verdienen. Merke: Sich nie in einen Wert verlieben .. und ihn sich nie schönrechnen!

Trading Spotlight

Antwort auf Beitrag Nr.: 39.313.485 von sailor888 am 12.04.10 11:15:47Kann Deine Berechnung nicht nachvollziehen.

Woher hast Du die Zahlen (14 % : 0,75 %) ?

Verwechselst Du möglicherweise Umsatz mit Ertrag ?

Fakt ist doch, dass schwere REE vergleichsweise selten sind und somit stabilere Erträge (revenues) zu erwarten sind.

Woher hast Du die Zahlen (14 % : 0,75 %) ?

Verwechselst Du möglicherweise Umsatz mit Ertrag ?

Fakt ist doch, dass schwere REE vergleichsweise selten sind und somit stabilere Erträge (revenues) zu erwarten sind.

Antwort auf Beitrag Nr.: 39.320.103 von zopa am 13.04.10 01:00:47Lynas Presentation 3/10, S. 22:

Current mine plan(within Central Zone Pit)

4.47 Mt @ 13.6% REO for 608kt REO

Alkane Pres., S.4:

35.7 million tonnes grading

0 - 55 metres 1.96% Zr02, 0.04%HfO2, 0.46% Nb2O5 ,

0.03% Ta2O5 , 0.14% Y2O3, 0.75% REO

and 0.014% U3O8

auf S. 11 steht dort, dass sie aus 400000 t Erz 2 t Europium

gewinnen. Das sind 5 g pro Tonne Erz!

Lynas hat (S. 23) 0,44 % Eu, also 0,44 % * 14 % = 0,06 % im Erz,

das sind 600 g pro Tonne Erz.

Current mine plan(within Central Zone Pit)

4.47 Mt @ 13.6% REO for 608kt REO

Alkane Pres., S.4:

35.7 million tonnes grading

0 - 55 metres 1.96% Zr02, 0.04%HfO2, 0.46% Nb2O5 ,

0.03% Ta2O5 , 0.14% Y2O3, 0.75% REO

and 0.014% U3O8

auf S. 11 steht dort, dass sie aus 400000 t Erz 2 t Europium

gewinnen. Das sind 5 g pro Tonne Erz!

Lynas hat (S. 23) 0,44 % Eu, also 0,44 % * 14 % = 0,06 % im Erz,

das sind 600 g pro Tonne Erz.

Antwort auf Beitrag Nr.: 39.320.103 von zopa am 13.04.10 01:00:47Verwechselst Du möglicherweise Umsatz mit Ertrag ?

Das ist so ziemlich dasselbe, Du meinst wahrscheinlich Gewinn und Umsatz...

aus wiki:

Erlös im Rechnungswesen

Im Handelsunternehmen sind Erlös und Leistung (betrieblicher Ertrag) identisch, weil es keine Bestandsänderungen an Halb- und Fertigfabrikaten und keine Eigenleistungen gibt. Im Industriebetrieb kommt zum Erlös aus verkauften Fertigprodukten der betriebliche Ertrag aus hergestellten Produkten hinzu. Der Unterschied entsteht durch die Bestandsänderungen an Halb- und Fertigfabrikaten sowie aus der Aktivierung von Eigenleistungen:

Erlös (Umsatz)

± Bestandsänderung Halb- und Fertigfabrikate

+ Aktivierungsfähige Eigenleistungen

-------------------------------------------------

= Leistung (Betriebsertrag, betrieblicher Ertrag)

Das ist so ziemlich dasselbe, Du meinst wahrscheinlich Gewinn und Umsatz...

aus wiki:

Erlös im Rechnungswesen

Im Handelsunternehmen sind Erlös und Leistung (betrieblicher Ertrag) identisch, weil es keine Bestandsänderungen an Halb- und Fertigfabrikaten und keine Eigenleistungen gibt. Im Industriebetrieb kommt zum Erlös aus verkauften Fertigprodukten der betriebliche Ertrag aus hergestellten Produkten hinzu. Der Unterschied entsteht durch die Bestandsänderungen an Halb- und Fertigfabrikaten sowie aus der Aktivierung von Eigenleistungen:

Erlös (Umsatz)

± Bestandsänderung Halb- und Fertigfabrikate

+ Aktivierungsfähige Eigenleistungen

-------------------------------------------------

= Leistung (Betriebsertrag, betrieblicher Ertrag)

Antwort auf Beitrag Nr.: 39.322.314 von sailor888 am 13.04.10 11:48:32Alkane will mit 400000 t/a 100 mio USD Umsatz generieren, d.h. 250 USD/t incl. Zirkon, Hf, Nb etc.

Das bedeutete ja, Alkane würde 1 Kilo REE für ca. USD 0,25 verkaufen ($ 250 : 1000 kg = 0,25 $).

Warum sollten sie dies tun, wenn der REE-Preis derzeit bei über $ 15,00 liegt ? Der Markt-Preis für schwere REE liegt z.Zt. sogar im 3-stelligen $-Bereich (siehe mein Eröffnungsposting vom 12.04.)...

Wo liegt mein Denkfehler ?

turnover = Umsatz = die wertmäßige Erfassung des Absatzes einer Unternehmung

Profit = Gewinn; Der Begriff des Gewinns, auch Nettogewinn, auf einen Zeitraum bezogen Periodenüberschuss, bezeichnet in seiner allgemeinen Verwendung den Erfolg autonomer einzelwirtschaftlicher Tätigkeit. Der Gewinn ist das positive Betriebsergebnis. Er ergibt sich als Unterschied zwischen Aufwand und Ertrag und zwar entweder als Periodengewinn (Gewinn in einer bestimmten Rechnungsperiode) oder als Stückgewinn, d.h. als Gewinn je Leistungseinheit.

Revenue = Ertrag = das Ergebnis der wirtschaftlichen Leistung bezeichnet; betriebswirtschaftlich bezeichnet der Ertrag eine Mehrung des Unternehmenserfolges durch einen Wertezugang,der durch die Erstellung (z. B. von Erzeugnissen oder innerbetrieblichen Leistungen), die Bereitstellung (z. B. von Kapital durch eine Bank) oder den Absatz (z. B. von Waren durch ein Handelsunternehmen) von Gütern entsteht.

Turnover bezieht sich also auf das, was ein Unternehmen gegen Entgelt verkauft.

Gewinn ist das, was am Ende übrig bleibt, wenn man den Aufwand abgezogen hat.

Ertrag ist das was ein Unternehmen erwirtschaftet, aber (!) noch nicht unbedingt verkauft haben muss.

Oder versuchen wir's mal praktisch (und lassen mal Kleinigkeiten wie Steuern, Personalkosten etc. außen vor)

Du kaufst von einem Kumpel 10 Handys für je 60 Euro/Stück

Du verkaufst alle 10 Handys für je 100 Euro pro Stück

Also Du setzt 600 Euro ein und erzielst damit 1000 Euro Umsatz, aber nur 400 Euro Ertrag

(1000 € Umsatz - 600 € Einsatz = 400 € Ertrag).

Übrigens: Mir liegt absolut nichts an der Deutungshoheit über die Begriffe

Ich hoffe,dass bereits Investierte sich an unserem Dialog beteiligen (oder bin ich etwa der einzige ??), die sich schon länger mit dem Wert beschäftigt haben und hier zur Aufklärung beitragen können.

Das bedeutete ja, Alkane würde 1 Kilo REE für ca. USD 0,25 verkaufen ($ 250 : 1000 kg = 0,25 $).

Warum sollten sie dies tun, wenn der REE-Preis derzeit bei über $ 15,00 liegt ? Der Markt-Preis für schwere REE liegt z.Zt. sogar im 3-stelligen $-Bereich (siehe mein Eröffnungsposting vom 12.04.)...

Wo liegt mein Denkfehler ?

turnover = Umsatz = die wertmäßige Erfassung des Absatzes einer Unternehmung

Profit = Gewinn; Der Begriff des Gewinns, auch Nettogewinn, auf einen Zeitraum bezogen Periodenüberschuss, bezeichnet in seiner allgemeinen Verwendung den Erfolg autonomer einzelwirtschaftlicher Tätigkeit. Der Gewinn ist das positive Betriebsergebnis. Er ergibt sich als Unterschied zwischen Aufwand und Ertrag und zwar entweder als Periodengewinn (Gewinn in einer bestimmten Rechnungsperiode) oder als Stückgewinn, d.h. als Gewinn je Leistungseinheit.

Revenue = Ertrag = das Ergebnis der wirtschaftlichen Leistung bezeichnet; betriebswirtschaftlich bezeichnet der Ertrag eine Mehrung des Unternehmenserfolges durch einen Wertezugang,der durch die Erstellung (z. B. von Erzeugnissen oder innerbetrieblichen Leistungen), die Bereitstellung (z. B. von Kapital durch eine Bank) oder den Absatz (z. B. von Waren durch ein Handelsunternehmen) von Gütern entsteht.

Turnover bezieht sich also auf das, was ein Unternehmen gegen Entgelt verkauft.

Gewinn ist das, was am Ende übrig bleibt, wenn man den Aufwand abgezogen hat.

Ertrag ist das was ein Unternehmen erwirtschaftet, aber (!) noch nicht unbedingt verkauft haben muss.

Oder versuchen wir's mal praktisch (und lassen mal Kleinigkeiten wie Steuern, Personalkosten etc. außen vor)

Du kaufst von einem Kumpel 10 Handys für je 60 Euro/Stück

Du verkaufst alle 10 Handys für je 100 Euro pro Stück

Also Du setzt 600 Euro ein und erzielst damit 1000 Euro Umsatz, aber nur 400 Euro Ertrag

(1000 € Umsatz - 600 € Einsatz = 400 € Ertrag).

Übrigens: Mir liegt absolut nichts an der Deutungshoheit über die Begriffe

Ich hoffe,dass bereits Investierte sich an unserem Dialog beteiligen (oder bin ich etwa der einzige ??), die sich schon länger mit dem Wert beschäftigt haben und hier zur Aufklärung beitragen können.

Antwort auf Beitrag Nr.: 39.322.784 von zopa am 13.04.10 12:49:11250 USD / t Erz(!)

in einer t Erz sind u.a. 7,5 kg REO (weil 0,75 %).

Mir scheint, die REOs sind eher Beiprodukt, und es geht mehr um Zirkon etc.

Die Frage ist doch immer, was kostet es, die niedrig konzentrierten Rohstoffe aus dem Erz zu gewinnen (Stichwort: cut off).

Z.B. ist in 1 Kubikkilometer Meerwasser im Schnitt 4 kg Gold im Wert von ca. 100000 €. Trotzdem holt das da keiner raus....

in einer t Erz sind u.a. 7,5 kg REO (weil 0,75 %).

Mir scheint, die REOs sind eher Beiprodukt, und es geht mehr um Zirkon etc.

Die Frage ist doch immer, was kostet es, die niedrig konzentrierten Rohstoffe aus dem Erz zu gewinnen (Stichwort: cut off).

Z.B. ist in 1 Kubikkilometer Meerwasser im Schnitt 4 kg Gold im Wert von ca. 100000 €. Trotzdem holt das da keiner raus....

und die 100 mio USD in der Alkana Pres sind revenue, das Wort profit taucht gar nicht auf.

Antwort auf Beitrag Nr.: 39.322.928 von sailor888 am 13.04.10 13:06:02Achtung

Die Produkte von Alkane sind:

- Zr

- Nb und

- REE

Die Umsatzschätzung beinhaltet alle Produkte.

Wieso halte ich ALKANE? ALKANE ist eines der wenigen Unternehmen weltweit, welches auch Ha-freies Zirkon herstellen kann. Wichtig für Atomreaktoren. Man benötigt 45 t alle 5 bis 6 Jahre. Bei der wachsenden Anzahl an Reaktoren sieht man heute schon einen Engpaß in naher Zukunft bei diesem Material.

lg

Die Produkte von Alkane sind:

- Zr

- Nb und

- REE

Die Umsatzschätzung beinhaltet alle Produkte.

Wieso halte ich ALKANE? ALKANE ist eines der wenigen Unternehmen weltweit, welches auch Ha-freies Zirkon herstellen kann. Wichtig für Atomreaktoren. Man benötigt 45 t alle 5 bis 6 Jahre. Bei der wachsenden Anzahl an Reaktoren sieht man heute schon einen Engpaß in naher Zukunft bei diesem Material.

lg

Antwort auf Beitrag Nr.: 39.322.987 von boehchris am 13.04.10 13:12:48Ha-freies Zirkon

http://www.chemieunterricht.de/dc2/lanthan/kontrakt.htm

...z. B. ist es sehr schwierig die Elementpaare Zirkonium und Hafnium oder Niob und Tantal zu trennen, die Auftrennung von Silber und Gold hingegen gelingt relativ einfach.

Die Tatsache, dass das Zirkonium wegen seiner geringen Tendenz zur Neutronenabsorption beim Bau von Atomreaktoren und Brennelementummantelungen verwendet wird, das Hafnium wegen seines ca. 600mal höheren Neutroneneinfangquerschnitts bei dieser Anwendung jedoch äußerst unerwünscht ist, zeigt die Bedeutung geeigneter Trennverfahren.

Kleiner Service vón einem stillen Mitleser

Freundliche Grüße

supernova

http://www.chemieunterricht.de/dc2/lanthan/kontrakt.htm

...z. B. ist es sehr schwierig die Elementpaare Zirkonium und Hafnium oder Niob und Tantal zu trennen, die Auftrennung von Silber und Gold hingegen gelingt relativ einfach.

Die Tatsache, dass das Zirkonium wegen seiner geringen Tendenz zur Neutronenabsorption beim Bau von Atomreaktoren und Brennelementummantelungen verwendet wird, das Hafnium wegen seines ca. 600mal höheren Neutroneneinfangquerschnitts bei dieser Anwendung jedoch äußerst unerwünscht ist, zeigt die Bedeutung geeigneter Trennverfahren.

Kleiner Service vón einem stillen Mitleser

Freundliche Grüße

supernova

Antwort auf Beitrag Nr.: 39.322.987 von boehchris am 13.04.10 13:12:48Liegt das an der Geologie der Lagerstätte? Oder beherrscht Alkane das Trennverfahren besser?

Antwort auf Beitrag Nr.: 39.324.600 von sailor888 am 13.04.10 15:57:12Hallo SupernovaDanke!

Hallo Sailor888

Ursache - ??? - bin "nur" Metallurge - kenne mich beim Eisen/Stahl sehr gut aus - muß mich mal vertiefen.

lg

Hallo Sailor888

Ursache - ??? - bin "nur" Metallurge - kenne mich beim Eisen/Stahl sehr gut aus - muß mich mal vertiefen.

lg

Aus HC:

...it provides the first estimate of the running costs of the DZP I have seen.

"processing the planned 400,000 metric tons of ore per year will generate A$92-112 million per year at current mineral prices employing a high-end operational cost estimate of A$65 million per year."

This gives a margin of A$27-47M per year. Given the company's history of conservative estimates I doubt that the final margin will be less than A$60M per year.

With the construction costs of $150M it could be debt free in 5 years with 150 years mine life left. Contrast this with the current company capitalisation of below A$90M

Cash costs will be spread over four key commodity groups including the high value YHREE products. Add into the mix the advanced stage of the DZP, including negotiation of non-dilutive off-take agreements with commercial refiners to develop the mine, and the investment picture looks rosy.

Vorausgesetzt die Verhandlungen zwischen Alkane und "commercial refiners" verlaufen erfolgreich, würden diese also Erzlieferungen erhalten, mit deren Erlös Alkane den Minenausbau ohne weitere Verwässerung finanzieren könnte.

Hoffentlich liegen die "Experten" in Oz richtig.

...it provides the first estimate of the running costs of the DZP I have seen.

"processing the planned 400,000 metric tons of ore per year will generate A$92-112 million per year at current mineral prices employing a high-end operational cost estimate of A$65 million per year."

This gives a margin of A$27-47M per year. Given the company's history of conservative estimates I doubt that the final margin will be less than A$60M per year.

With the construction costs of $150M it could be debt free in 5 years with 150 years mine life left. Contrast this with the current company capitalisation of below A$90M

Cash costs will be spread over four key commodity groups including the high value YHREE products. Add into the mix the advanced stage of the DZP, including negotiation of non-dilutive off-take agreements with commercial refiners to develop the mine, and the investment picture looks rosy.

Vorausgesetzt die Verhandlungen zwischen Alkane und "commercial refiners" verlaufen erfolgreich, würden diese also Erzlieferungen erhalten, mit deren Erlös Alkane den Minenausbau ohne weitere Verwässerung finanzieren könnte.

Hoffentlich liegen die "Experten" in Oz richtig.

DZB = Dubbo Zirconia Projekt von Alkane

Antwort auf Beitrag Nr.: 39.329.797 von zopa am 14.04.10 09:31:06Die Erze machen den kleisten Teil der Wertschöpfungskette aus, zumal wenn sie einfach im Tagebau gewonnen werden.

Die geplanten Umsatzzahlen beziehen sich auf die Endprodukte, also reine Oxide.

Dafür braucht man ne teure Fabrik, knowhow, viel Säure, Energie usw.

Es wäre besser, den schweren Weg zu gehen als die Erze zu verhökern.

Dafür muss man aber u.a. nen 3stelligen MillionenBetrag auftreiben.

Die geplanten Umsatzzahlen beziehen sich auf die Endprodukte, also reine Oxide.

Dafür braucht man ne teure Fabrik, knowhow, viel Säure, Energie usw.

Es wäre besser, den schweren Weg zu gehen als die Erze zu verhökern.

Dafür muss man aber u.a. nen 3stelligen MillionenBetrag auftreiben.

Das nennt man ja wohl Konzentration aufs Kerngeschäft. Damit dürfte die company über mehr als 10 Mio AUD cash verfügen !

The directors of Alkane Resources Ltd are pleased to advise that the Company has raised

approximately $9.7m (less costs) by the sale of its remaining investment in BC Iron Ltd. The funds

raised will augment the Company's existing cash balances and will be used to progress its core

activities (being the Tomingley Gold Project, the Dubbo Zirconia Project and other New South Wales

exploration projects).

Alkane was instrumental in the formation of BCI and has been a strong supporter of their rapid

progress towards production. The Company wishes BCI all success in the future.

The directors of Alkane Resources Ltd are pleased to advise that the Company has raised

approximately $9.7m (less costs) by the sale of its remaining investment in BC Iron Ltd. The funds

raised will augment the Company's existing cash balances and will be used to progress its core

activities (being the Tomingley Gold Project, the Dubbo Zirconia Project and other New South Wales

exploration projects).

Alkane was instrumental in the formation of BCI and has been a strong supporter of their rapid

progress towards production. The Company wishes BCI all success in the future.

US auditor warns of China's hold on rare earth supply

* Ian Talley

* From: The Wall Street Journal

* April 15, 2010 12:10PM

AMERICA'S federal auditor today warned of China's power over the supply of rare earth materials vital to the military, mobile phone and clean energy sectors.

The Government Accountability Office said China processes almost 97 per cent of the world's supply of these elements, which have special electromagnetic properties, and although the US has deposits of rare earth ore, it won't likely be produced until 2012.

Furthermore, the US has lost the necessary capacity to refine rare earth material, and rebuilding the supply chain may take up to 15 years.

“China's dominant position in the rare earths market gives it market power, which could affect global rare earth supply and prices,” the GAO said.

While the military needs the rare earth materials for many of its defence systems -including missiles, satellites and radar systems - commercial use includes hybrid electric motors and batteries, wind power turbines, computer hard drives, mobile phones, cameras, energy-efficiency light bulbs and fibre optics.

Start of sidebar. Skip to end of sidebar.

Related Coverage

* Rare earths, it seems, are not so rare The Australian, 4 days ago

* Renaissance or retread? The Australian, 27 Jan 2010

* Lynas rare earths contract extended The Australian, 20 Jan 2010

* ASX speeding ticket for Arafura Resources Adelaide Now, 15 Jan 2010

* Stocks to watch in 2010 The Australian, 27 Dec 2009

End of sidebar. Return to start of sidebar.

Availability of these elements will largely be controlled by Chinese suppliers for at least the next several years.

The auditor said government and industry officials believe China was planning to increase export taxes on the materials to15-20 per cent, and that the country was also using production quotas to limit supply.

“While China is currently exporting rare earth oxides and metals, some rare earth industry officials believe that in the future China will only export finished rare earth material products with higher value,” the GAO said.

A company called Molycorp Minerals, owned by Chevron, has a large deposit of rare earth elements at its Mountain Pass Mine in California. But the mine lacks manufacturing assets to process the ore into finished components. Also, it doesn't have “heavy” rare earth elements necessary for industry and military hardware. Other deposits exist in the US and elsewhere, but it could take nearly a decade just to get production online.

* Ian Talley

* From: The Wall Street Journal

* April 15, 2010 12:10PM

AMERICA'S federal auditor today warned of China's power over the supply of rare earth materials vital to the military, mobile phone and clean energy sectors.

The Government Accountability Office said China processes almost 97 per cent of the world's supply of these elements, which have special electromagnetic properties, and although the US has deposits of rare earth ore, it won't likely be produced until 2012.

Furthermore, the US has lost the necessary capacity to refine rare earth material, and rebuilding the supply chain may take up to 15 years.

“China's dominant position in the rare earths market gives it market power, which could affect global rare earth supply and prices,” the GAO said.

While the military needs the rare earth materials for many of its defence systems -including missiles, satellites and radar systems - commercial use includes hybrid electric motors and batteries, wind power turbines, computer hard drives, mobile phones, cameras, energy-efficiency light bulbs and fibre optics.

Start of sidebar. Skip to end of sidebar.

Related Coverage

* Rare earths, it seems, are not so rare The Australian, 4 days ago

* Renaissance or retread? The Australian, 27 Jan 2010

* Lynas rare earths contract extended The Australian, 20 Jan 2010

* ASX speeding ticket for Arafura Resources Adelaide Now, 15 Jan 2010

* Stocks to watch in 2010 The Australian, 27 Dec 2009

End of sidebar. Return to start of sidebar.

Availability of these elements will largely be controlled by Chinese suppliers for at least the next several years.

The auditor said government and industry officials believe China was planning to increase export taxes on the materials to15-20 per cent, and that the country was also using production quotas to limit supply.

“While China is currently exporting rare earth oxides and metals, some rare earth industry officials believe that in the future China will only export finished rare earth material products with higher value,” the GAO said.

A company called Molycorp Minerals, owned by Chevron, has a large deposit of rare earth elements at its Mountain Pass Mine in California. But the mine lacks manufacturing assets to process the ore into finished components. Also, it doesn't have “heavy” rare earth elements necessary for industry and military hardware. Other deposits exist in the US and elsewhere, but it could take nearly a decade just to get production online.

Caution, rare earths ahead

“The potential shortages are all medium and heavy rare earths, a reflection of the fact that the major non-Chinese projects (Mt Weld and Mountain Pass) likely to be in production by 2015 will predominantly produce light rare earths, with some medium rare earths, but with neodymium contents that are likely to be less than demand,” he writes. The Dubbo project, owned by Alkane Resources, could provide some relief as it has a relatively large proportion of medium and heavy rare earths, but output at this project would be low.

Den ganzen Artikel findet ihr hier:

http://www.theaustralian.com.au/business/mining-energy/cauti…

“The potential shortages are all medium and heavy rare earths, a reflection of the fact that the major non-Chinese projects (Mt Weld and Mountain Pass) likely to be in production by 2015 will predominantly produce light rare earths, with some medium rare earths, but with neodymium contents that are likely to be less than demand,” he writes. The Dubbo project, owned by Alkane Resources, could provide some relief as it has a relatively large proportion of medium and heavy rare earths, but output at this project would be low.

Den ganzen Artikel findet ihr hier:

http://www.theaustralian.com.au/business/mining-energy/cauti…

FOCUS-Money-Titelgeschichte vom 28.04. (heft Nr. 18):

Die Börsenchance des Jahres

Kennen Sie Yttrium, Palladium, Lithium & Co.?

Es geht um die neuen Super-Rohstoffe des E-Zeitalters, wobei aussichtreiche Aktien benannt werden.

Ich nenne hierbei bewusst diejenigen mit einer MK < 1 Milliarde €:

- Orocobre

- Western Lithium

- Lynas

- Arafura

- Neo Material tech.

- Platinum Australia

- Commerce Res.

- Alkane Res.

Ferner wird auf Kobalt als weiteren wichtigen Grundstoff hingewiesen.

Die Börsenchance des Jahres

Kennen Sie Yttrium, Palladium, Lithium & Co.?

Es geht um die neuen Super-Rohstoffe des E-Zeitalters, wobei aussichtreiche Aktien benannt werden.

Ich nenne hierbei bewusst diejenigen mit einer MK < 1 Milliarde €:

- Orocobre

- Western Lithium

- Lynas

- Arafura

- Neo Material tech.

- Platinum Australia

- Commerce Res.

- Alkane Res.

Ferner wird auf Kobalt als weiteren wichtigen Grundstoff hingewiesen.

Antwort auf Beitrag Nr.: 39.419.678 von zopa am 28.04.10 18:06:27unter 0,20€ wäre ein ganz guter Einstieg

Was mich allerdings stört ist die doch größere Differenz zw. Geld- und Briefkurs. Kann jmd. sagen woran das eigentlich liegt (hab ich mich schon öfter gefragt)

Dies müßte die Erklärung sein:

http://www.godmode-trader.de/nachricht/Learning-Der-Spread,a…

...freue mich aber über Euer Feedback!

Was mich allerdings stört ist die doch größere Differenz zw. Geld- und Briefkurs. Kann jmd. sagen woran das eigentlich liegt (hab ich mich schon öfter gefragt)

Dies müßte die Erklärung sein:

http://www.godmode-trader.de/nachricht/Learning-Der-Spread,a…

...freue mich aber über Euer Feedback!

Antwort auf Beitrag Nr.: 39.441.276 von websin am 02.05.10 18:24:55Ich vermute, die meisten haben nur Lynas + Arafura auf dem Radar.

In Downunder wird Alkane m.M.nach wesentlich positiver eingeschätzt. Bei uns sind die Umsätze eher mau. Je geringer das Handelsvolumen, desto größer ist das Risiko, einen ungünstigen Preis zu bekommen.

Nur wenn viele Aktien gehandelt werden, schrumpft der so genannte Spread, der Unterschied zwischen Angebots- und Nachfragekurs.

An einen nahezu 20%igen Abschlag auf 20 ct glaube ich nicht, es sei denn, die Börsen brechen insgesamt ein (Stichwort: US Gewerbeimmobilien).

Bei Lyc/Aru sind die meisten doch deswegen investiert, weil sie von dem Wert überzeugt sind und eine Vervielfachung erhoffen/erwarten.

Und weil das manchmal sehr schnell gehen kann, kann der Pennschieter (Pfennigfuchser) wegen 5 ct zu spät kommen und sich kräftig in den Mors beißen. Der Satz: Im Einkauf liegt der Gewinn ist eben relativ.

Und „hätte“ ist sowieso die beste Aktie.

In Downunder wird Alkane m.M.nach wesentlich positiver eingeschätzt. Bei uns sind die Umsätze eher mau. Je geringer das Handelsvolumen, desto größer ist das Risiko, einen ungünstigen Preis zu bekommen.

Nur wenn viele Aktien gehandelt werden, schrumpft der so genannte Spread, der Unterschied zwischen Angebots- und Nachfragekurs.

An einen nahezu 20%igen Abschlag auf 20 ct glaube ich nicht, es sei denn, die Börsen brechen insgesamt ein (Stichwort: US Gewerbeimmobilien).

Bei Lyc/Aru sind die meisten doch deswegen investiert, weil sie von dem Wert überzeugt sind und eine Vervielfachung erhoffen/erwarten.

Und weil das manchmal sehr schnell gehen kann, kann der Pennschieter (Pfennigfuchser) wegen 5 ct zu spät kommen und sich kräftig in den Mors beißen. Der Satz: Im Einkauf liegt der Gewinn ist eben relativ.

Und „hätte“ ist sowieso die beste Aktie.

Antwort auf Beitrag Nr.: 39.442.040 von zopa am 03.05.10 00:10:12Bisher ist LYC auch mein Hauptinteresse aus den von Dir genannten Gründen. Moly ist denke ich auch ein sicheres Schiff.

Nebenher habe ich neu QRE auf dem Radar, is aber schon etwas zu fix abgegangen, Einstieg verpasst.

Ein Witz ist/ war Tantalus Rare Earth

Schau mal Feb-April 2010 an, da gab es immer wieder gute Alkane EK's - also einfach abwarten.

Aber vorher muss ich mal meine BESCH%$%ENEN Solaries abstoßen.

Danke für Deine Spread-Erklärung

MFG, WEBSIN

aus den von Dir genannten Gründen. Moly ist denke ich auch ein sicheres Schiff.Nebenher habe ich neu QRE auf dem Radar, is aber schon etwas zu fix abgegangen, Einstieg verpasst.

Ein Witz ist/ war Tantalus Rare Earth

Schau mal Feb-April 2010 an, da gab es immer wieder gute Alkane EK's - also einfach abwarten.

Aber vorher muss ich mal meine BESCH%$%ENEN Solaries abstoßen.

Danke für Deine Spread-Erklärung

MFG, WEBSIN

Antwort auf Beitrag Nr.: 39.444.419 von websin am 03.05.10 13:27:56Tja, was ist der richtige Zeitpunkt ? Wenn Du bei € 0,20 Brief `reinkämest, wäre dies ein Einstieg zum 52-Wochen-Tief.

Vorausgesetzt, Du bist bereit, den Wert mind. 3 Jahre zu halten und bist ähnlich optimistisch gestimmt wie bei Mol + Lyc, dann sollten die popeligen 5 ct keine Rolle spielen.

Wie bei vielen Explorer-Werten kann eine richtig gute Nachricht den Kurs anschieben und Du guckst in die Röhre.

Da sag ich mir, lieber jetzt einsteigen und zurücklehnen. Wenn`s losgeht bin ich auf jeden Fall dabei.

Moly + Lyc laufen seit Monaten seitwärts, auch hier kommts doch auf ein paar Cent +- nicht an.

Ich glaube an den Wert, weil Alkane mit ANSTO (Australian Nuclear Science and Technology Organisation) eine Pilot-Anlage betreibt.

Zuvor hat ANSTO u.a. auch beim Mt. Weld mitgemischt ...

http://www.theanchorsite.com/2010/02/09/what-is-ansto-why-do…

Vorausgesetzt, Du bist bereit, den Wert mind. 3 Jahre zu halten und bist ähnlich optimistisch gestimmt wie bei Mol + Lyc, dann sollten die popeligen 5 ct keine Rolle spielen.

Wie bei vielen Explorer-Werten kann eine richtig gute Nachricht den Kurs anschieben und Du guckst in die Röhre.

Da sag ich mir, lieber jetzt einsteigen und zurücklehnen. Wenn`s losgeht bin ich auf jeden Fall dabei.

Moly + Lyc laufen seit Monaten seitwärts, auch hier kommts doch auf ein paar Cent +- nicht an.

Ich glaube an den Wert, weil Alkane mit ANSTO (Australian Nuclear Science and Technology Organisation) eine Pilot-Anlage betreibt.

Zuvor hat ANSTO u.a. auch beim Mt. Weld mitgemischt ...

http://www.theanchorsite.com/2010/02/09/what-is-ansto-why-do…

Antwort auf Beitrag Nr.: 39.444.950 von zopa am 03.05.10 14:41:59Dass es so schnell geht hätten wir beide nicht gedacht, oder?

Hab nur gerade kein Geld frei!

Hab nur gerade kein Geld frei!

Antwort auf Beitrag Nr.: 39.451.609 von websin am 04.05.10 13:14:16Toujours avec la rue - Immer mit der Ruhe

Bis 0,20 € Brief ist noch ein Stück (rd. 25 %).

Ich hoffe, dass sich der Markt trotz der austral. "Super-Tax" bald wieder fängt.

Bis 0,20 € Brief ist noch ein Stück (rd. 25 %).

Ich hoffe, dass sich der Markt trotz der austral. "Super-Tax" bald wieder fängt.

Antwort auf Beitrag Nr.: 39.451.707 von zopa am 04.05.10 13:25:58na aber immerhin  , ist aber nur ein sprungfixer Fall, ich denke kurzweilig.

, ist aber nur ein sprungfixer Fall, ich denke kurzweilig.

Das hoffe ich für meine LYC auch... Vorher könnte meine Solaraktie steigen damit ich in ALKANE einsteigen kann ;-)

, ist aber nur ein sprungfixer Fall, ich denke kurzweilig.

, ist aber nur ein sprungfixer Fall, ich denke kurzweilig. Das hoffe ich für meine LYC auch... Vorher könnte meine Solaraktie steigen damit ich in ALKANE einsteigen kann ;-)

Alkane Resources Ltd has today released an announcement to the Australian Stock Exchange.

The announcement entitled "Alkane AGM Presentation"

can be accessed through the following link to the Company's website:

http://www.alkane.com.au/presentations/

The announcement entitled "Alkane AGM Presentation"

can be accessed through the following link to the Company's website:

http://www.alkane.com.au/presentations/

Viel fehlen nun zu den 0,20€ nicht mehr

Thursday, June 17, 2010

Alkane Resources' rare earths valuation leaves plenty of upside

As the sole owner of a substantial rare earth deposit and two gold properties in central New South Wales, Alkane Resources (ASX:ALK) looks set to play a significant role as a miner of “strategic” rare earth minerals in the near future, while it also develops two gold projects.

The Chinese Government recently announced that they are considering stricter limits on the exports of rare earth minerals despite already accounting for 90% of worldwide production.

On the flip side, worldwide consumption for rare earths is forecast to rise as demand for new technology products such as hybrid cars, wind turbines, cell phones and laptops which contain significant quantities of these “high tech metals” including magnets, batteries, auto catalysts, refining catalysts, polishing powders, glass additives, phosphors and alloys.

Demand is expected to hit 185,000 tonnes by 2014 with mine production only reaching 135,000 tonnes -and that includes substantial new production from Western Australia’s Mount Weld mine - according to Lynas Corporation (ASX:LYC).

There are only four worldwide projects outside of China capable of supplying rare earths that can be in production before 2015. Three are in Australia, including Alkane’s Dubbo Zirconia Project and one in the USA run by MolyCorp at Mountain Pass which plans to ramp annual production to 20,000 tons by 2012. The U.S. government is so concerned that it discussing legislation to provide loan guarantees for the mining and refining of rare earths for industry and defense.

Chinese interests recently attempted to corner the market for foreign rare earths by purchasing a 51.5% interest in LYC for A$500 million / US$425 million, but were rebuffed by Australian Regulators at the Foreign Investment Review Board. Other Chinese interests snagged 25% of Arafura Resources (ASX:ARU) which is establishing a mine at Nolan’s in the Northern Territory. These two miners will represent about 25% of the world supply of rare earths when on stream by 2013.

Dubbo Zirconia Project

The Dubbo Zirconia Project contains a measured and inferred resource of 73.2 million tonnes at a combined grade of 3.38% of zirconium, hafnium, niobium, tantalum, yttrium and rare earths. The deposit also contains uranium at a grade of .014% for a total resource of 23 million lbs which represents over a billion dollars in revenues over the life of the mine.

Uranium mining is currently banned in New South Wales but this could be challenged in Federal Court or a deal worked out, as Australia is a major exporter of uranium. ALK says that the market for zircon and nobium will go into shortfall by 2013 and is looking at prefeasibility studies for annual production rates between 400,000 - 1,000,000 tonnes of ore to produce between 15,000 - 37,000 tonnes of zircon and 2,000 - 5,000 tonnes of nobium plus associated rare earths for annual revenues of US$100 - $250 million.

Capital cost of the mine is estimated at A$150 million and production will continue for 80 - 200 years.

The government run research facilities of ANSTO at Lucas Heights (near Sydney) is running pilot plant studies and specializes in uranium ore processing and removal of radioactivity. So far the plant has produced 1,300 kg of zirconium chemicals, nearly 300 kg of nobium concentrate, yttrium and rare earth products. No indication of costs is available but the pilot plant can model various process flow sheets that will define capital and cash operating costs. Potential clients are now evaluating the substantial amount of refined and concentrated products for suitability, pricing and potential sales contracts that will support financing proposals for the mine.

Infrastructure costs will be low as the project is located 12 miles from Dubbo in Central New South Wales. The area has main roads, railway, water, electricity, gas, substantial population and many small industries that can support the mine. A timeline to get the project into production by 2013 is being pursued.

The current market capitalization of ALK is measured at 5-10% of Molycorp’s Mountain Pass Mine and LYC’s Mount Weld Project which attests to the great value in this little company before we even look at its near term gold production and exploration potential. The ALK market price has fallen in line with the recent mini GFC fallout and for longer term investors, must represent some value at current prices.

Tomingley Gold Project

Tomingley is 24 miles from the Dubbo Zirconia Project. Three open pittable resources called Caloma, Wyoming One and Wyoming Three, were drilled to a shallow depth for a resource of 850,000 ounces of gold which includes an underground component for Wyoming One. Prefeasibility studies indicated a cash operating cost of A$800 per ounce at a rate of 50,000 ounces per year. The study also found that substantial infrastructure costs to bring in water and power and build an underpass under a major road that cuts between the pits indicated more ore was required to justify capital costs.

This led to the search for more resources with positive drilling results from beneath the floor of the proposed Caloma pit where a conceptual target of one million tonnes at 3.5 grams per ton for 120,000 ounces was indicated.

A new ore zone was also uncovered by recent drilling 250 meters south of Caloma which assayed several +3 gram per tonne intersects where the orientation of this east west trending porphyry over 300 meters looks similar to the high grade zones in Wyoming One and Three.

Detailed geological assessment indicates that Caloma may consist of several ore blocks separated by faults. A 3,500 meter rotary core drilling program to scope this zone starts this month. Positive results will lead to more drilling to prove up a resource which may lead to a mine decision before the year is out.

Orange District Joint Venture with Newmont may herald major Australian gold find

Gold mining heavyweight Newmont (NYSE:NEM) has earned 75% of the Molong and Moorilda Prospects from ALK. This ground partially surrounds the Newcrest Mines at Cadia that host massive resources of 44 million ounces of gold and 7.98 million tonnes of copper.

Prior drilling by NEM outlined a conceptual target of 2-4 million ounces of gold and 50-100,000 tonnes of copper at McPhillamy’s within the Moorilda Prospect. The exploration program for this year will be A$2.3 million and includes 4 holes for 3,500 meters to test for depth and continuity of mineralization, and potentially may render this one of Australia’s largest recent gold finds.

Quelle: http://www.proactiveinvestors.com.au/companies/news/7932/alk…

Alkane Resources' rare earths valuation leaves plenty of upside

As the sole owner of a substantial rare earth deposit and two gold properties in central New South Wales, Alkane Resources (ASX:ALK) looks set to play a significant role as a miner of “strategic” rare earth minerals in the near future, while it also develops two gold projects.

The Chinese Government recently announced that they are considering stricter limits on the exports of rare earth minerals despite already accounting for 90% of worldwide production.

On the flip side, worldwide consumption for rare earths is forecast to rise as demand for new technology products such as hybrid cars, wind turbines, cell phones and laptops which contain significant quantities of these “high tech metals” including magnets, batteries, auto catalysts, refining catalysts, polishing powders, glass additives, phosphors and alloys.

Demand is expected to hit 185,000 tonnes by 2014 with mine production only reaching 135,000 tonnes -and that includes substantial new production from Western Australia’s Mount Weld mine - according to Lynas Corporation (ASX:LYC).

There are only four worldwide projects outside of China capable of supplying rare earths that can be in production before 2015. Three are in Australia, including Alkane’s Dubbo Zirconia Project and one in the USA run by MolyCorp at Mountain Pass which plans to ramp annual production to 20,000 tons by 2012. The U.S. government is so concerned that it discussing legislation to provide loan guarantees for the mining and refining of rare earths for industry and defense.

Chinese interests recently attempted to corner the market for foreign rare earths by purchasing a 51.5% interest in LYC for A$500 million / US$425 million, but were rebuffed by Australian Regulators at the Foreign Investment Review Board. Other Chinese interests snagged 25% of Arafura Resources (ASX:ARU) which is establishing a mine at Nolan’s in the Northern Territory. These two miners will represent about 25% of the world supply of rare earths when on stream by 2013.

Dubbo Zirconia Project

The Dubbo Zirconia Project contains a measured and inferred resource of 73.2 million tonnes at a combined grade of 3.38% of zirconium, hafnium, niobium, tantalum, yttrium and rare earths. The deposit also contains uranium at a grade of .014% for a total resource of 23 million lbs which represents over a billion dollars in revenues over the life of the mine.

Uranium mining is currently banned in New South Wales but this could be challenged in Federal Court or a deal worked out, as Australia is a major exporter of uranium. ALK says that the market for zircon and nobium will go into shortfall by 2013 and is looking at prefeasibility studies for annual production rates between 400,000 - 1,000,000 tonnes of ore to produce between 15,000 - 37,000 tonnes of zircon and 2,000 - 5,000 tonnes of nobium plus associated rare earths for annual revenues of US$100 - $250 million.

Capital cost of the mine is estimated at A$150 million and production will continue for 80 - 200 years.

The government run research facilities of ANSTO at Lucas Heights (near Sydney) is running pilot plant studies and specializes in uranium ore processing and removal of radioactivity. So far the plant has produced 1,300 kg of zirconium chemicals, nearly 300 kg of nobium concentrate, yttrium and rare earth products. No indication of costs is available but the pilot plant can model various process flow sheets that will define capital and cash operating costs. Potential clients are now evaluating the substantial amount of refined and concentrated products for suitability, pricing and potential sales contracts that will support financing proposals for the mine.

Infrastructure costs will be low as the project is located 12 miles from Dubbo in Central New South Wales. The area has main roads, railway, water, electricity, gas, substantial population and many small industries that can support the mine. A timeline to get the project into production by 2013 is being pursued.

The current market capitalization of ALK is measured at 5-10% of Molycorp’s Mountain Pass Mine and LYC’s Mount Weld Project which attests to the great value in this little company before we even look at its near term gold production and exploration potential. The ALK market price has fallen in line with the recent mini GFC fallout and for longer term investors, must represent some value at current prices.

Tomingley Gold Project

Tomingley is 24 miles from the Dubbo Zirconia Project. Three open pittable resources called Caloma, Wyoming One and Wyoming Three, were drilled to a shallow depth for a resource of 850,000 ounces of gold which includes an underground component for Wyoming One. Prefeasibility studies indicated a cash operating cost of A$800 per ounce at a rate of 50,000 ounces per year. The study also found that substantial infrastructure costs to bring in water and power and build an underpass under a major road that cuts between the pits indicated more ore was required to justify capital costs.

This led to the search for more resources with positive drilling results from beneath the floor of the proposed Caloma pit where a conceptual target of one million tonnes at 3.5 grams per ton for 120,000 ounces was indicated.

A new ore zone was also uncovered by recent drilling 250 meters south of Caloma which assayed several +3 gram per tonne intersects where the orientation of this east west trending porphyry over 300 meters looks similar to the high grade zones in Wyoming One and Three.

Detailed geological assessment indicates that Caloma may consist of several ore blocks separated by faults. A 3,500 meter rotary core drilling program to scope this zone starts this month. Positive results will lead to more drilling to prove up a resource which may lead to a mine decision before the year is out.

Orange District Joint Venture with Newmont may herald major Australian gold find

Gold mining heavyweight Newmont (NYSE:NEM) has earned 75% of the Molong and Moorilda Prospects from ALK. This ground partially surrounds the Newcrest Mines at Cadia that host massive resources of 44 million ounces of gold and 7.98 million tonnes of copper.

Prior drilling by NEM outlined a conceptual target of 2-4 million ounces of gold and 50-100,000 tonnes of copper at McPhillamy’s within the Moorilda Prospect. The exploration program for this year will be A$2.3 million and includes 4 holes for 3,500 meters to test for depth and continuity of mineralization, and potentially may render this one of Australia’s largest recent gold finds.

Quelle: http://www.proactiveinvestors.com.au/companies/news/7932/alk…

Monday, July 05, 2010

Alkane Resources defines gold resource of 3m ounces at McPhillamys in New South Wales

Alkane Resources (ASX: ALK) has inked a maiden resource estimate of 2.96 million ounces of gold for the McPhillamys gold discovery, located within the Orange District Exploration Joint Venture with Newmont.

An independent resource assessment by Richard Lewis of Lewis Mineral Resource Consulting Pty Ltd in Sydney. defined an initial Indicated and Inferred Resource at a 0.3g/t gold cut-off of 91.94 million tonnes grading 1.00g/t Au and 0.07% Cu for a cumulative total of 2.96 million ounces of gold and 60,000 tonnes of copper.

Alkane is in a joint venture with Newmont Australia Limited, a subsidiary of the US based Newmont Mining Corporation (NYSE: NEM) over the Orange District Exploration Joint Venture, 400km northwest of Sydney, which includes Alkane’s Molong and Moorilda tenements located near the city of Orange in the Central West of New South Wales, adjacent to Newcrest Mining Ltd’s Cadia Valley Operations.

The bulk of the Resource is located within an Inner Ore Zone with dimensions of 600 metres by 200 metres.

Further drilling is likely to significantly expand the resource.

Potential development models include open pit and block caving underground mining concepts.

Currently the JV is drilling four deep core holes to specifically test the potential for the block caving concept.

Regional exploration has defined several targets with McPhillamys type stratigraphy and mineralisation over a strike length of at least 6 kilometres. Aircore test drilling is in progress.

Newmont Australia Limited earned a 51% interest in the JV in August 2009. In March 2010 NAL elected to proceed to 75% by completing a Bankable Feasibility Study on the McPhillamys Project.

Alkane is cashed up with $8.7 million with no debt.

Alkane Resources defines gold resource of 3m ounces at McPhillamys in New South Wales

Alkane Resources (ASX: ALK) has inked a maiden resource estimate of 2.96 million ounces of gold for the McPhillamys gold discovery, located within the Orange District Exploration Joint Venture with Newmont.

An independent resource assessment by Richard Lewis of Lewis Mineral Resource Consulting Pty Ltd in Sydney. defined an initial Indicated and Inferred Resource at a 0.3g/t gold cut-off of 91.94 million tonnes grading 1.00g/t Au and 0.07% Cu for a cumulative total of 2.96 million ounces of gold and 60,000 tonnes of copper.

Alkane is in a joint venture with Newmont Australia Limited, a subsidiary of the US based Newmont Mining Corporation (NYSE: NEM) over the Orange District Exploration Joint Venture, 400km northwest of Sydney, which includes Alkane’s Molong and Moorilda tenements located near the city of Orange in the Central West of New South Wales, adjacent to Newcrest Mining Ltd’s Cadia Valley Operations.

The bulk of the Resource is located within an Inner Ore Zone with dimensions of 600 metres by 200 metres.

Further drilling is likely to significantly expand the resource.

Potential development models include open pit and block caving underground mining concepts.

Currently the JV is drilling four deep core holes to specifically test the potential for the block caving concept.

Regional exploration has defined several targets with McPhillamys type stratigraphy and mineralisation over a strike length of at least 6 kilometres. Aircore test drilling is in progress.

Newmont Australia Limited earned a 51% interest in the JV in August 2009. In March 2010 NAL elected to proceed to 75% by completing a Bankable Feasibility Study on the McPhillamys Project.

Alkane is cashed up with $8.7 million with no debt.

Neue Präsentation:

http://www.alkane.com.au/presentations/pdf/20100714.pdf

http://www.alkane.com.au/presentations/pdf/20100714.pdf

Alkane Resources shares jump on Edison Investment note

SHARES in Alkane Resources received a boost today after a London-based broker valued the company at almost three times its market cap.

London-based Edison Investment Research has given the junior a value of 91 cents a share, which saw Alkane stock trade 4.5 per cent higher today at 35c.

“With exposure to both near-term gold production and an advanced rare earths project, Alkane is unique among its peers,” the broker’s client report said.

Mining at Alkane’s Tomingley gold project in NSW is planned for 2012, while the Dubbo rare metal and rare earth project is expected to come online by 2013.

The report also highlighted a key aspect about Alkane's Dubbo zirconia project.

“Crucially, Alkane has advanced the process routes for separating many of the valuable zirconium, niobium and rare earth products beyond that of many of its peers' rare earths projects around the world,” the report said.

Möge die Kursverdoppelung beginnen

SHARES in Alkane Resources received a boost today after a London-based broker valued the company at almost three times its market cap.

London-based Edison Investment Research has given the junior a value of 91 cents a share, which saw Alkane stock trade 4.5 per cent higher today at 35c.

“With exposure to both near-term gold production and an advanced rare earths project, Alkane is unique among its peers,” the broker’s client report said.

Mining at Alkane’s Tomingley gold project in NSW is planned for 2012, while the Dubbo rare metal and rare earth project is expected to come online by 2013.

The report also highlighted a key aspect about Alkane's Dubbo zirconia project.

“Crucially, Alkane has advanced the process routes for separating many of the valuable zirconium, niobium and rare earth products beyond that of many of its peers' rare earths projects around the world,” the report said.

Möge die Kursverdoppelung beginnen

Alkane Resources (ASX: ALK) is a multi commodity mining and exploration company focused on the Central West of New South Wales, Australia. The Company has built a gold resource inventory of over 1 million ounces and plans recommence operations in 2010 through a new development at Tomingley. Alkane, in partnership with Newmont, has also made another significant gold discovery at McPhillamys near Orange.

The company has an advanced feasibility study in progress for the development of the Dubbo Zirconia Project which is based upon a very large in-ground resource of the metals zirconium, hafnium, niobium, tantalum, yttrium and rare earth elements.

Monday, August 16, 2010

Alkane Resources confirms more gold resource potential at Tomingley

http://www.proactiveinvestors.com.au/companies/news/9366/alk…

The company has an advanced feasibility study in progress for the development of the Dubbo Zirconia Project which is based upon a very large in-ground resource of the metals zirconium, hafnium, niobium, tantalum, yttrium and rare earth elements.

Monday, August 16, 2010

Alkane Resources confirms more gold resource potential at Tomingley

http://www.proactiveinvestors.com.au/companies/news/9366/alk…

Friday, August 27, 2010

Rare Earth Metals to continue to shine after China reduces export quotas

...

Alkane Resources (ASX: ALK) has started larger scale production of an yttrium heavy rare earth concentrate from the new rare earth circuit at its Demonstration Pilot Plant (DPP) at ANSTO as part of the Dubbo Zirconia Project (DZP) in New South Wales.

The yttrium and heavy rare earth distribution in the ore body is unusual with 25% in the heavy category (standard distribution 95% light and 5% heavy) with this generating a higher than average return for the rare earth product.

Data from the DPP and Letters of Intent from future customers will be incorporated in the current DFS which should be completed early 2011. Depending upon financing and Development Consent from the New South Wales state government, Alkane's DZP could be in production late 2012 or early 2013.

...

http://www.proactiveinvestors.com.au/companies/news/9634/rar…

Rare Earth Metals to continue to shine after China reduces export quotas

...

Alkane Resources (ASX: ALK) has started larger scale production of an yttrium heavy rare earth concentrate from the new rare earth circuit at its Demonstration Pilot Plant (DPP) at ANSTO as part of the Dubbo Zirconia Project (DZP) in New South Wales.

The yttrium and heavy rare earth distribution in the ore body is unusual with 25% in the heavy category (standard distribution 95% light and 5% heavy) with this generating a higher than average return for the rare earth product.

Data from the DPP and Letters of Intent from future customers will be incorporated in the current DFS which should be completed early 2011. Depending upon financing and Development Consent from the New South Wales state government, Alkane's DZP could be in production late 2012 or early 2013.

...

http://www.proactiveinvestors.com.au/companies/news/9634/rar…

Wednesday, August 25, 2010

The London HREE Report: The Premier Leag

If China is going to start building and selling a million electric vehicles a year, as has been reported as part of their latest economic plan, in a command economy when the top says build them and sell them, they get built and sold no matter what, then it’s pretty obvious that China is going to implement its rare metals export ban in 2015. We have just 4 1/3rd years to be ready elsewhere to meet the rest of the world’s demand. As I have been trying to show last week and this, new technology breakthroughs are about to double, triple, the double again, demand for these rare metals by the time of the Chinese export ban.

To this old trader that means front weighting investment into those who can meet a 2015 deadline, by that I mean, actually have their resource in production and refined into the product that manufacturers need, and at a sales cost that makes the company a profit. The sole purpose of any investment is to buy low and sell high, since it is highly unlikely that any of the rare earth firms will be paying out dividends in the next few years, if at all. As such that time compression, for me, rules out most firms in the remote wilderness, seeking to get into the game late. The exceptions are perhaps Ucore Rare Metals, Hudson Resources, and Quest which has picked up interest and help from SIDEX in Quebec.

My market experience suggests that we will quickly form a Premier League and a Division Two, where the companies are possible later takeover targets by the companies in the Premier League and possibly China, if China’s companies decide to take that route and are permitted into the game. I know, it’s not a level playing field world. So who get into Graeme’s Premier League?

Great Western Minerals Group, Lynas Corporation, Tasman Metals Ltd, Avalon Rare Metals, Molycorp Minerals, Alkane Resources are the only true Premier League candidates, though I will allow in Ucore, Hudson and Quest. To be sure all have some pluses and minuses. For example, will the Aussie candidates have a disadvantage due to a mining tax and a hung Parliament unable to function well? Will California’s politicians really keep out of Molycorp’s way, as the state goes from broke to ruined? Can Quest and Hudson really catch up with the others by 2015? There is one other company I think ought to be in. Stans Energy Corp is my final pick for the starting Premier 10. The positive is that their mine and region produced and refined once before for the old unloved Soviet Union. The negative is that is in the Kyrgyz Republic, better known to us as Krygyzstan. How will Graeme’s Premier 10 do? Maybe some kind soul will post a table, and start them all off using Friday’s settlement price. Suggestions please on whether it should be equal share weighted, or equal cost weighted. Suggestions please on additions or for filling up the other divisions.

More tomorrow, after I take an evening libation and a nap.

Graeme Irvine. London.

The London HREE Report: The Premier Leag

If China is going to start building and selling a million electric vehicles a year, as has been reported as part of their latest economic plan, in a command economy when the top says build them and sell them, they get built and sold no matter what, then it’s pretty obvious that China is going to implement its rare metals export ban in 2015. We have just 4 1/3rd years to be ready elsewhere to meet the rest of the world’s demand. As I have been trying to show last week and this, new technology breakthroughs are about to double, triple, the double again, demand for these rare metals by the time of the Chinese export ban.

To this old trader that means front weighting investment into those who can meet a 2015 deadline, by that I mean, actually have their resource in production and refined into the product that manufacturers need, and at a sales cost that makes the company a profit. The sole purpose of any investment is to buy low and sell high, since it is highly unlikely that any of the rare earth firms will be paying out dividends in the next few years, if at all. As such that time compression, for me, rules out most firms in the remote wilderness, seeking to get into the game late. The exceptions are perhaps Ucore Rare Metals, Hudson Resources, and Quest which has picked up interest and help from SIDEX in Quebec.

My market experience suggests that we will quickly form a Premier League and a Division Two, where the companies are possible later takeover targets by the companies in the Premier League and possibly China, if China’s companies decide to take that route and are permitted into the game. I know, it’s not a level playing field world. So who get into Graeme’s Premier League?

Great Western Minerals Group, Lynas Corporation, Tasman Metals Ltd, Avalon Rare Metals, Molycorp Minerals, Alkane Resources are the only true Premier League candidates, though I will allow in Ucore, Hudson and Quest. To be sure all have some pluses and minuses. For example, will the Aussie candidates have a disadvantage due to a mining tax and a hung Parliament unable to function well? Will California’s politicians really keep out of Molycorp’s way, as the state goes from broke to ruined? Can Quest and Hudson really catch up with the others by 2015? There is one other company I think ought to be in. Stans Energy Corp is my final pick for the starting Premier 10. The positive is that their mine and region produced and refined once before for the old unloved Soviet Union. The negative is that is in the Kyrgyz Republic, better known to us as Krygyzstan. How will Graeme’s Premier 10 do? Maybe some kind soul will post a table, and start them all off using Friday’s settlement price. Suggestions please on whether it should be equal share weighted, or equal cost weighted. Suggestions please on additions or for filling up the other divisions.

More tomorrow, after I take an evening libation and a nap.

Graeme Irvine. London.

Rare Metal Blog

Thursday, August 26, 2010

The London REE Report: Inelastic Demand

http://www.raremetalblog.com/2010/08/london-august-26-2010-i…

Thursday, August 26, 2010

The London REE Report: Inelastic Demand

http://www.raremetalblog.com/2010/08/london-august-26-2010-i…

China Backs Rare Earth Controls as Environmental Step

August 28, 2010, 11:59 PM EDT

http://www.businessweek.com/news/2010-08-28/china-backs-rare…

August 28, 2010, 11:59 PM EDT

http://www.businessweek.com/news/2010-08-28/china-backs-rare…

Alkane Resources Ltd has today released a presentation to the Australian Stock Exchange.

The presentation entitled “Mining NSW Conference”

can be accessed through the following link to the Company's website:

http://www.alkane.com.au/presentations/" target="_blank" rel="nofollow ugc noopener">

http://www.alkane.com.au/presentations/

ASX: z.Zt. + 10 %

The presentation entitled “Mining NSW Conference”

can be accessed through the following link to the Company's website:

http://www.alkane.com.au/presentations/" target="_blank" rel="nofollow ugc noopener">

http://www.alkane.com.au/presentations/

ASX: z.Zt. + 10 %

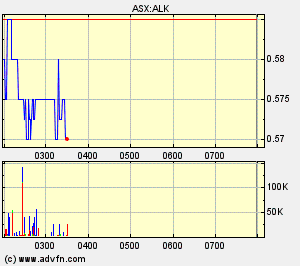

Alkane heute: + 18 % auf AUD 0,59 bei deutlich gestiegenem Volumen die letzten Tage !

Ja aber warum ist das so, ich will schon die ganze Zeit einsteigen. Warum geht das gerade jetzt so Aufwerts?

Die Aktie ist auf all-time-high !

Antwort auf Beitrag Nr.: 40.094.487 von GAGFAHmann am 03.09.10 11:42:10Alkane hat hauptsächlich Vorkommen mit schweren Seltenen Erden. Diese sind im REE-Basket besonders teuer ...

Zirkon ist z. B. beim Reaktorbau unverzichtbar !

So wie es derzeit aussieht, wird ALKANE vor Arafura der nächste Produzent !

http://www.stocks.ch/print_ausgaben/_Himmlische_Renditen_mit…

Zirkon ist z. B. beim Reaktorbau unverzichtbar !

So wie es derzeit aussieht, wird ALKANE vor Arafura der nächste Produzent !

http://www.stocks.ch/print_ausgaben/_Himmlische_Renditen_mit…

Antwort auf Beitrag Nr.: 40.094.614 von zopa am 03.09.10 12:00:57trotz des kräftigen Anstiegs und alltimehigh scheint sich (noch) kaum jemand für die aktie zu interessieren. da kann es eigentlich nur weiter aufwärts gehen

Das ist mein momentaner stand in RRE und drum herum.( Kaufe immer gerne den Kompletten Zyklus) Lohnt sich der Einstig bei Alkane noch schnelle Antwort wäre gut.

.

CHINA RARE EARTH HD-,10

ARAFURA RESOURCES LTD.

LYNAS CORP. LTD

GR.WEST.MIN.

NEO MATERIAL TECHNOL.

BYD CO. LTD H YC 1

UMICORE S.A. NEW

AVALON RARE METALS INC.

MOLYCORP INC.(DEL) DL-001

QUANTUM RARE EARTH DEVEL.

Schnelle Antwort wäre gut schonmal Danke

.

CHINA RARE EARTH HD-,10

ARAFURA RESOURCES LTD.

LYNAS CORP. LTD

GR.WEST.MIN.

NEO MATERIAL TECHNOL.

BYD CO. LTD H YC 1

UMICORE S.A. NEW

AVALON RARE METALS INC.

MOLYCORP INC.(DEL) DL-001

QUANTUM RARE EARTH DEVEL.

Schnelle Antwort wäre gut schonmal Danke

Antwort auf Beitrag Nr.: 40.095.412 von GAGFAHmann am 03.09.10 13:49:08Sieh Dir die Präsentationen von LYNAS, Alkane und anderen an.

Auf jeden Fall frieren sich die Aussies nicht 6 Monate lang den Mors ab, wie manche Kanadier...

Deinen Lolly darfst Du Dir dann selber kaufen

Auf jeden Fall frieren sich die Aussies nicht 6 Monate lang den Mors ab, wie manche Kanadier...

Deinen Lolly darfst Du Dir dann selber kaufen

Es ging mir lediglich darum ob sich der Einstieg noch lohnen würde? Und ob du denkst das es zu den restlichen passen würde.

Wenn du dazusagen würdest. Ja wäre es gut wenn nicht auch nicht schlim

Wenn du dazusagen würdest. Ja wäre es gut wenn nicht auch nicht schlim

Antwort auf Beitrag Nr.: 40.095.715 von GAGFAHmann am 03.09.10 14:35:24#7107 von GAGFAHmann 02.08.10 14:27:15 Beitrag Nr.: 39.912.731

Da ich Depos betreue würde mich mal interessieren ob ich nochmal nachkaufen soll und die Shares verdoppeln soll.

Positiv:Aktie sieht gut aus. Wachstumsmarkt.usw

Negativ: Chart für mich nahezu Überkauft

MFG Nils [/i]

Du betreust Depots ? Von Deiner Oma ??

Aber wie sagte schon A. Einstein: „Fantasie ist wichtiger als Wissen!“

Wenn Du schon o stark auf REE setzt, warum sollte ausgerechnet bei Alkane die Story zu Ende sein ?

Da ich Depos betreue würde mich mal interessieren ob ich nochmal nachkaufen soll und die Shares verdoppeln soll.

Positiv:Aktie sieht gut aus. Wachstumsmarkt.usw

Negativ: Chart für mich nahezu Überkauft

MFG Nils [/i]

Du betreust Depots ? Von Deiner Oma ??

Aber wie sagte schon A. Einstein: „Fantasie ist wichtiger als Wissen!“

Wenn Du schon o stark auf REE setzt, warum sollte ausgerechnet bei Alkane die Story zu Ende sein ?

Tja jeder soll das Glauben was er will^^ Ich zu meinem Teil kann fröhlich sagen das ich die nach besten Wissen und Gewissen die Wahrheit sage.

Und nein nicht von meiner Oma, wobei das schlichtweg Egal ist. Geld ist Geld und solange ich mir damit mein Lebensunterhalt gut verdiene, sehe ich darin kein Manko.

LG

Schade das du lieber an Leuten, die du nicht kennst, rum kritisierst und immer OffTopic bist.

LG

Antwort auf Beitrag Nr.: 40.096.401 von GAGFAHmann am 03.09.10 15:38:36Schade das du lieber an Leuten, die du nicht kennst, rum kritisierst und immer OffTopic bist.

Ich bin kein Dauerposter, zumal sich die Qualität der postings sich meist reziprok zur Häufigkeit - bezogen auf den jewiligen Poster - verhält.

Aber ich bin gerne bereit mich zu bessern. Bitte mal 2 - 3 Beispiele wg. off topic.

Ich habe Deinen Eintritt (der wars doch, oder ?) in den LYC- Thread so verstanden, dass Du Vermögen Dritter betreust. Insofern habe ich Dich zunächst für einen alten Hasen gehalten und mich über Deine Fragen schlichtweg gewundert.

Nach Deiner jüngsten Reaktion erkenne ich, dass ich mich getäuscht habe.

Ich bin kein Dauerposter, zumal sich die Qualität der postings sich meist reziprok zur Häufigkeit - bezogen auf den jewiligen Poster - verhält.

Aber ich bin gerne bereit mich zu bessern. Bitte mal 2 - 3 Beispiele wg. off topic.

Ich habe Deinen Eintritt (der wars doch, oder ?) in den LYC- Thread so verstanden, dass Du Vermögen Dritter betreust. Insofern habe ich Dich zunächst für einen alten Hasen gehalten und mich über Deine Fragen schlichtweg gewundert.

Nach Deiner jüngsten Reaktion erkenne ich, dass ich mich getäuscht habe.

Also ich denke wohl kaum das man, wenn man jemanden eine Anfrage stellt, ob man das Depot seiner Oma betreut, eine gewisse Wertschätzung erbringt.

Aus meiner Sicht habe ich deine Antworten als Feindselig empfunden, ich entschuldige mich gerne bei dir, wenn ich bei diesem Punkt, nicht richtig gelegen habe.

Meine Frage war nur die: Warum wird ein Unternehmen ohne erkennbare News ca. 40% mehr wert?

Das Unternehmen war schon vorher auf der Buyliste bloss war es mir immer (fälschliche Annahme )zu teuer.

Wenn du nun also weißt warum dieser Kurssprung zustande gekommen ist, würde eich mich über dein Wissen freuen, alles andere ist vertane Zeit die ich nicht habe.

LG

Aus meiner Sicht habe ich deine Antworten als Feindselig empfunden, ich entschuldige mich gerne bei dir, wenn ich bei diesem Punkt, nicht richtig gelegen habe.

Meine Frage war nur die: Warum wird ein Unternehmen ohne erkennbare News ca. 40% mehr wert?

Das Unternehmen war schon vorher auf der Buyliste bloss war es mir immer (fälschliche Annahme )zu teuer.

Wenn du nun also weißt warum dieser Kurssprung zustande gekommen ist, würde eich mich über dein Wissen freuen, alles andere ist vertane Zeit die ich nicht habe.

LG

Antwort auf Beitrag Nr.: 40.097.783 von GAGFAHmann am 03.09.10 18:33:00Ich halte unser aller Wissen ohnehin für begrenzt. Deswegen geht mir auch dieses pupertäre geposte so auf den Zeiger.

Wer in Explorer investiert, investiert IMHO auch nach dem Prinzip Hoffnung.

Hoffnung auf sensationell Resourcen, Hoffung auf evtl. Übernahme, Hoffnung auf Entwicklung bis zur Produktionsreife etc.

Und da es in D nun einmal nicht so viele Bergbauexperten gibt, die Ergebnisse entsprechend interpretieren/kommentieren können (anders als bei HotCopper), wird hier einfach zuviel gelabert.Hinzukommen die Wasserstandsmeldungen nach Bauchgefühl. Niveau scheint hier leider doch zu oft für eine Handcreme gehalten zu werden. Und manchmal wird man davon angesteckt.

Immer wenns up geht, kommen sie aus ihren Löchern und schreiben Kommentare (z.B. bei LYC), die einem das Interesse an einem thread schon verleiden können.

Erst sind sie billig drin, dann kräftig nachgelegt (was heißt das in € ?) dann wieder raus und meistens alles richtig gemacht. Nachprüfen kann es sowieso keiner - wenn interessiert es.

So und nun zum Kurssprung.

Ich habe keine Ahnung !

Ich vermute,

1. auch ALKANE kann sich der REE-Hype nicht entziehen

2. die Kooperation mit staatl. Institutionen (Versuchsfabrik) schafft Vertrauen

3. zukünftiger cashflow wg. Goldminen ebenfalls

4. die Vorkommen schwerer REE

5. der derzeitige Entwicklungsstand

Die Reihenfolge ist frei sortierbar

Vielleicht gibt jemand von den übrigen, wenigen Investierten seine Einschätzung ab ...

Wer in Explorer investiert, investiert IMHO auch nach dem Prinzip Hoffnung.

Hoffnung auf sensationell Resourcen, Hoffung auf evtl. Übernahme, Hoffnung auf Entwicklung bis zur Produktionsreife etc.

Und da es in D nun einmal nicht so viele Bergbauexperten gibt, die Ergebnisse entsprechend interpretieren/kommentieren können (anders als bei HotCopper), wird hier einfach zuviel gelabert.Hinzukommen die Wasserstandsmeldungen nach Bauchgefühl. Niveau scheint hier leider doch zu oft für eine Handcreme gehalten zu werden. Und manchmal wird man davon angesteckt.

Immer wenns up geht, kommen sie aus ihren Löchern und schreiben Kommentare (z.B. bei LYC), die einem das Interesse an einem thread schon verleiden können.

Erst sind sie billig drin, dann kräftig nachgelegt (was heißt das in € ?) dann wieder raus und meistens alles richtig gemacht. Nachprüfen kann es sowieso keiner - wenn interessiert es.

So und nun zum Kurssprung.

Ich habe keine Ahnung !

Ich vermute,

1. auch ALKANE kann sich der REE-Hype nicht entziehen

2. die Kooperation mit staatl. Institutionen (Versuchsfabrik) schafft Vertrauen

3. zukünftiger cashflow wg. Goldminen ebenfalls

4. die Vorkommen schwerer REE

5. der derzeitige Entwicklungsstand

Die Reihenfolge ist frei sortierbar

Vielleicht gibt jemand von den übrigen, wenigen Investierten seine Einschätzung ab ...

Eigentlich ist die DFS für Tomingly fällig - vielleicht kommt daher der Sprung.

Antwort auf Beitrag Nr.: 40.096.993 von zopa am 03.09.10 16:41:55Ich weiß, dass ich nicht weiß.

Dieser einfache Satz ist für die meisten Leute schwer zu begreifen, besser gesagt, zu akzeptieren. Ein bisschen gesunder Menschenverstand kann helfen, klar, beim nächsten Rohstoff-Hype (der ja längst läuft bzw. weiterläuft) könnten die ree-minen vorn mit dabei sein. Und dann versucht man eben sein glück. Wie immer wichtig: MM und Risikostreuung, nicht zuviel auf einen Wert, lieber 3 oder 5 verschiedene, und natürlich nur ein kleiner Teil des Gesamtdepots, vielleicht 5%, max 10% insg., dann wird man nicht so schnell nervös, wenn's (zunächst) nicht so gut läuft.