Apple - unaufhaltsamer Aufstieg - wie lange noch? (Seite 1013)

eröffnet am 18.01.05 13:14:58 von

neuester Beitrag 19.04.24 14:40:49 von

neuester Beitrag 19.04.24 14:40:49 von

Beiträge: 49.510

ID: 944.638

ID: 944.638

Aufrufe heute: 7

Gesamt: 4.619.178

Gesamt: 4.619.178

Aktive User: 0

ISIN: US0378331005 · WKN: 865985 · Symbol: AAPL

165,00

USD

-1,22 %

-2,04 USD

Letzter Kurs 02:00:00 Nasdaq

Neuigkeiten

18.04.24 · wallstreetONLINE Redaktion |

| Apple mit möglichem Doppelboden?Anzeige |

19.04.24 · Roland Jegen Anzeige |

19.04.24 · wO Newsflash |

19.04.24 · dpa-AFX |

KI-Gewinner: Chip-Riese TSMC übertrifft Gewinnerwartungen deutlich

KI-Gewinner: Chip-Riese TSMC übertrifft Gewinnerwartungen deutlich Werte aus der Branche Hardware

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 16,500 | +9,78 | |

| 2,2100 | +4,74 | |

| 3,8400 | +4,35 | |

| 1,1600 | +4,13 | |

| 2,0383 | +2,69 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,8800 | -7,84 | |

| 6,9000 | -8,61 | |

| 1,5300 | -10,00 | |

| 3,9300 | -14,94 | |

| 713,65 | -23,14 |

Beitrag zu dieser Diskussion schreiben

Dann schauen wir mal, ob wir heute > USD 130.- schliessen ....

EUR 114,60 ......also "nur" mehr knapp 10.- Euro fehlen auf´s Euro-ATH

EUR 114,60 ......also "nur" mehr knapp 10.- Euro fehlen auf´s Euro-ATH

Antwort auf Beitrag Nr.: 49.799.796 von auriga am 18.05.15 17:39:38Carl C. Icahn

767 Fifth Avenue, 47th Floor

New York, New York 10153

May 18, 2015

Dear Tim:

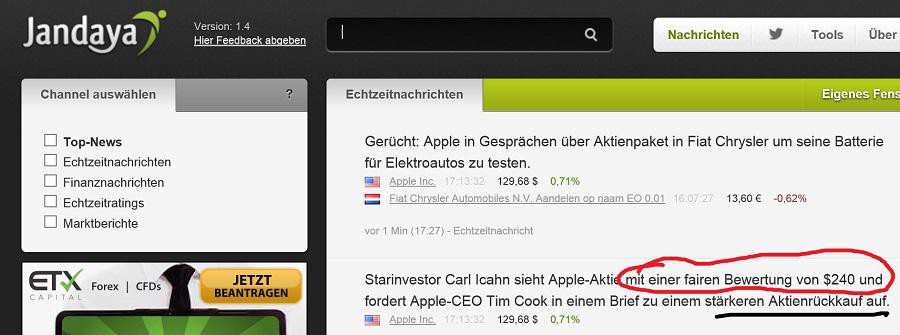

We again applaud you and the rest of management for Apple’s impressive operational performance and growth. It is truly impressive that, despite severe foreign exchange headwinds and massive growth in investment (in both R&D and SG&A), the company will still grow earnings by 40% this year, according to our forecast. After reflecting upon Apple’s tremendous success, we now believe Apple shares are worth $240 today. Apple is poised to enter and in our view dominate two new categories (the television next year and the automobile by 2020) with a combined addressable market of $2.2 trillion, a view investors don’t appear to factor into their valuation at all. We believe this may lead to a de facto short squeeze, as underweight actively managed mutual funds and hedge funds correct their misguided positions. To arrive at the value of $240 per share, we forecast FY2016 EPS of $12.00 (excluding net interest income), apply a P/E multiple of 18x, and then add $24.44 of net cash per share. Considering our forecast for 30% EPS growth in FY 2017 and our belief Apple will soon enter two new markets (Television and the Automobile) with a combined addressable market size of $2.2 trillion, we think a multiple of 18x is a very conservative premium to that of the overall market. Considering the massive scope of its growth opportunities and track record of dominating new categories, we actually think 18x will ultimately prove to be too conservative, especially since we view the market in general as having much lower growth prospects.

We are pleased that Apple has directionally followed our advice and repurchased $80 billion of its shares (yielding the company’s shareholders an excellent return), but the company’s enormous net cash position continues to grow while the company’s shares are still dramatically undervalued. With Apple’s shares trading for just $128.77 per share versus our valuation of $240 per share, now is the time for a much larger buyback. We appreciate that the Board just increased the share repurchase authorization by $50 billion, and that it continues to prioritize share repurchases over dividends (as it should). We again simply ask you to help us convince the board of how these two underlying issues (inefficient net cash growth and share undervaluation) persist and combine to enhance the opportunity for accelerated share repurchases in greater magnitude. We also ask you to help us convince the board that this is not a choice between investing in growth and share repurchases. As our model forecasts, despite more than 30% growth in R&D annually through FY 2017 to $13.5 billion (up from $1.8 billion in FY 2010) and your updated capital return program, Apple’s net cash position (currently the largest of any company in history) will continue to build on the balance sheet.

It is our belief that large institutional investors, Wall Street analysts and the news media alike continue to misunderstand Apple and generally fail to value Apple’s net cash separately from its business, fail to adjust earnings to reflect Apple’s real cash tax rate, fail to recognize the growth prospects of Apple entering new categories, and fail to recognize that Apple will maintain pricing and margins, despite significant evidence to the contrary. Collectively, these failures have caused Apple’s earnings multiple to stay irrationally discounted, in our view.

When we compare Apple’s P/E ratio to that of the S&P 500 index, we find that the market continues to value Apple at a significantly discounted multiple of only 10.9x, compared to 17.4x for the S&P 500, awarding the S&P500 with a 60% premium valuation to Apple:

. . .

http://www.shareholderssquaretable.com/carl-icahn-issues-ope…

767 Fifth Avenue, 47th Floor

New York, New York 10153

May 18, 2015

Dear Tim:

We again applaud you and the rest of management for Apple’s impressive operational performance and growth. It is truly impressive that, despite severe foreign exchange headwinds and massive growth in investment (in both R&D and SG&A), the company will still grow earnings by 40% this year, according to our forecast. After reflecting upon Apple’s tremendous success, we now believe Apple shares are worth $240 today. Apple is poised to enter and in our view dominate two new categories (the television next year and the automobile by 2020) with a combined addressable market of $2.2 trillion, a view investors don’t appear to factor into their valuation at all. We believe this may lead to a de facto short squeeze, as underweight actively managed mutual funds and hedge funds correct their misguided positions. To arrive at the value of $240 per share, we forecast FY2016 EPS of $12.00 (excluding net interest income), apply a P/E multiple of 18x, and then add $24.44 of net cash per share. Considering our forecast for 30% EPS growth in FY 2017 and our belief Apple will soon enter two new markets (Television and the Automobile) with a combined addressable market size of $2.2 trillion, we think a multiple of 18x is a very conservative premium to that of the overall market. Considering the massive scope of its growth opportunities and track record of dominating new categories, we actually think 18x will ultimately prove to be too conservative, especially since we view the market in general as having much lower growth prospects.

We are pleased that Apple has directionally followed our advice and repurchased $80 billion of its shares (yielding the company’s shareholders an excellent return), but the company’s enormous net cash position continues to grow while the company’s shares are still dramatically undervalued. With Apple’s shares trading for just $128.77 per share versus our valuation of $240 per share, now is the time for a much larger buyback. We appreciate that the Board just increased the share repurchase authorization by $50 billion, and that it continues to prioritize share repurchases over dividends (as it should). We again simply ask you to help us convince the board of how these two underlying issues (inefficient net cash growth and share undervaluation) persist and combine to enhance the opportunity for accelerated share repurchases in greater magnitude. We also ask you to help us convince the board that this is not a choice between investing in growth and share repurchases. As our model forecasts, despite more than 30% growth in R&D annually through FY 2017 to $13.5 billion (up from $1.8 billion in FY 2010) and your updated capital return program, Apple’s net cash position (currently the largest of any company in history) will continue to build on the balance sheet.

It is our belief that large institutional investors, Wall Street analysts and the news media alike continue to misunderstand Apple and generally fail to value Apple’s net cash separately from its business, fail to adjust earnings to reflect Apple’s real cash tax rate, fail to recognize the growth prospects of Apple entering new categories, and fail to recognize that Apple will maintain pricing and margins, despite significant evidence to the contrary. Collectively, these failures have caused Apple’s earnings multiple to stay irrationally discounted, in our view.

When we compare Apple’s P/E ratio to that of the S&P 500 index, we find that the market continues to value Apple at a significantly discounted multiple of only 10.9x, compared to 17.4x for the S&P 500, awarding the S&P500 with a 60% premium valuation to Apple:

. . .

http://www.shareholderssquaretable.com/carl-icahn-issues-ope…

Antwort auf Beitrag Nr.: 49.799.796 von auriga am 18.05.15 17:39:38https://twitter.com/Carl_C_Icahn

Think you will find our latest letter to @tim_cook re $AAPL interesting: http://www.shareholderssquaretable.com/carl-icahn-issues-ope…

Think you will find our latest letter to @tim_cook re $AAPL interesting: http://www.shareholderssquaretable.com/carl-icahn-issues-ope…

Antwort auf Beitrag Nr.: 49.799.730 von money84penny85 am 18.05.15 17:32:46the letter

http://www.shareholderssquaretable.com/carl-icahn-issues-ope…

Hab den Brief nur kurz überflogen .....was auch immer davon letztendlich eintrifft - der positive Impuls ist vorerst mal da.

http://www.shareholderssquaretable.com/carl-icahn-issues-ope…

Hab den Brief nur kurz überflogen .....was auch immer davon letztendlich eintrifft - der positive Impuls ist vorerst mal da.

Antwort auf Beitrag Nr.: 49.799.172 von auriga am 18.05.15 16:20:51

http://www.marketwatch.com/investing/Stock/AAPL?CountryCode=…

http://finance.yahoo.com/echarts?s=AAPL+Interactive#%7B%22ra…

http://finance.yahoo.com/q?s=AAPL[/quote]

http://www.marketwatch.com/investing/Stock/AAPL?CountryCode=…

http://finance.yahoo.com/echarts?s=AAPL+Interactive#%7B%22ra…

http://finance.yahoo.com/q?s=AAPL[/quote]

Trading Spotlight

Ok, als ich meinen Post oben abgesetzt habe mit „wir prallen an der 130 USD Marke ab“ wusste ich noch nicht, dass 2 Minuten später die Icaahn News rauskommt…

Aber ich täusche mich hier ja auch gerne

Aber ich täusche mich hier ja auch gerne

Antwort auf Beitrag Nr.: 49.799.664 von money84penny85 am 18.05.15 17:25:38

Gerade bei Icaahn auf Facebook gefunden

http://www.shareholderssquaretable.com/carl-icahn-issues-ope…

http://www.shareholderssquaretable.com/carl-icahn-issues-ope…

Auf Jandaya News ohne Link eben gelesen: Carl Icaahn sieht fairen Wert bei Apple bei 240 USD. Hat schon jemand mehr dazu?

Also ich nutze ab und zu in der Stadt ein Navi, zu Fuß oder im Auto.

Ich nutze ausschließlich die Apple Maps App und bisher bin ich immer angekommen.

Aufgrund des Zeitvorsprungs ist Google hier aber sicher noch etwas weiter vorne.

130.02 USD übrigens eben.

Ich nutze ausschließlich die Apple Maps App und bisher bin ich immer angekommen.

Aufgrund des Zeitvorsprungs ist Google hier aber sicher noch etwas weiter vorne.

130.02 USD übrigens eben.

19.04.24 · wO Newsflash · American Express |

19.04.24 · dpa-AFX · American Express |

19.04.24 · dpa-AFX · Apple |

18.04.24 · Dr. Hamed Esnaashari · Apple |

18.04.24 · dpa-AFX · Apple |

18.04.24 · dpa-AFX · Apple |

| Zeit | Titel |

|---|---|

| 11.02.24 | |

| 18.01.24 | |

| 27.11.23 | |

| 05.11.23 | |

| 22.08.23 | |

| 04.08.23 | |

| 02.07.23 | |

| 24.04.23 |