Orbite - Diskussion zum Rohstoffwert - 500 Beiträge pro Seite

eröffnet am 20.10.11 08:38:55 von

neuester Beitrag 31.03.20 15:24:51 von

neuester Beitrag 31.03.20 15:24:51 von

Beiträge: 513

ID: 1.169.755

ID: 1.169.755

Aufrufe heute: 0

Gesamt: 24.924

Gesamt: 24.924

Aktive User: 0

ISIN: CA68558W1023 · WKN: A14U8Q

0,0700

EUR

-57,32 %

-0,0940 EUR

Letzter Kurs 04.04.17 Tradegate

Neuigkeiten

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7850 | +38,94 | |

| 0,7950 | +30,33 | |

| 55,80 | +15,41 | |

| 0,7999 | +14,27 | |

| 11,250 | +12,73 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7122 | -9,53 | |

| 4,8400 | -9,67 | |

| 17,310 | -9,98 | |

| 186,20 | -10,48 | |

| 4,2300 | -17,86 |

Mich hat es überrascht dass Orbite noch keinen Thread hat. Gut, WKN hat sich geändert, habe aber weder bei der alten noch bei der neuen WKN ein Thema entdeckt.

Meine kurze Synopsis, Orbite hat 3 Standbeine, einmal das Tonerde Projekt , mit dem sie den regionalen Aluminium-Markt versorgen wollen. Ggü. Bauxit hat es Kostenvorteile , die sich v.a. auch durch den schnelleren u. günstigeren Transportwege bemerkbar machen. Denn die lokalen Alu-Schmelzen in Quebec haben einen Marktanteil v. 12 % weltweit ! u. sie müssen bisher das Bauxit aus Übersee beziehen (Brasilien, AUS).

Möglich wird dies durch ein eigens entwickeltes Verfahren (Patent besteht), das die gesamte Alu-Bauxit-Welt ziemlich aufmischen könnte bzw. wird.

Ein ganz wichtiger Grund ist auch die Umweltverträglichkeit, bei dem Verfahren fallen keine giftigen Metallstäube an (siehe Unfall in Ungarn letztes Jahr. Man nennt ihn "roter Staub" , er enthält giftige Schwermetalle u. fällt aber bei Orbite gar nicht an.

Als 3.Standbein wäre zu nennen, dass Orbite in den hochlukrativen Markt v. Rein-Alu (High-Purity Alu) eindringt , das u.a. bei soviel ich weiß allen Arten v. Leuchtdioden gebraucht wird.

Auch Gallium u. Scandium kann Orbite in signifikaten MEngen produzieren.

Ich habe das jetzt aus dem Gedächtnis wiedergegeben, sollten FEhler enthalten sein, so möchte ich mich vorab entschuldigen u. bitten diese rückzumelden.

Hier noch eine Zs.fassung von der Webseite:

1. Technology

2. Resource

3. Markets

4. Management

“Game-changing” technologies

Orbite owns a proprietary and potentially “game-changing” process to extract alumina from aluminous clay deposits that is significantly more economical compared to conventional methods. Separate processes also extract high-purity alumina and a range of high-value elements, including rare earths. The company’s intellectual property is well protected for 20 years in Canada, the United States and around the world by a robust portfolio of patents and patents pending. As “game changers,” these technologies also offer significant licensing potential internationally. Orbite’s alumina extraction technology has been proven in the lab and pilot plant, and is now ready for commercial roll-out.

Strategic resource

An independent geologist, Jean-Guy Levaque, B.Sc.A., P.Eng., has surveyed Orbite’s Grande-Vallée property in Gaspé, Québec. A conservative estimate based on his findings indicates 1 billion tonnes of “indicated mineral resources” in the first 100 metres depth of one sector of the property alone. The property is strategically located near a road and close to a year-round deepwater seaport, giving access to domestic and export markets. The wealth stored on this property could provide much-needed jobs and investment to the economically depressed Gaspé region, and aligns well with the Québec government’s priorities for job creation and value-added processing in the strategic aluminum sector.

Growing markets

Orbite’s key products—metallurgical grade alumina, high-purity alumina and various high-value elements, including rare earths—are in growing demand around the world.

Experienced management

The Orbite executive team and Board of Directors are primarily made up of achievers with a known capacity to deliver. They are repeat entrepreneurs who have long track records of success in bringing new technologies to market, launching start-ups, and managing large and complex enterprises. They also have hands-on, long-standing experience in the mining, environment, government and community relations, and aluminum sectors.

Meine kurze Synopsis, Orbite hat 3 Standbeine, einmal das Tonerde Projekt , mit dem sie den regionalen Aluminium-Markt versorgen wollen. Ggü. Bauxit hat es Kostenvorteile , die sich v.a. auch durch den schnelleren u. günstigeren Transportwege bemerkbar machen. Denn die lokalen Alu-Schmelzen in Quebec haben einen Marktanteil v. 12 % weltweit ! u. sie müssen bisher das Bauxit aus Übersee beziehen (Brasilien, AUS).

Möglich wird dies durch ein eigens entwickeltes Verfahren (Patent besteht), das die gesamte Alu-Bauxit-Welt ziemlich aufmischen könnte bzw. wird.

Ein ganz wichtiger Grund ist auch die Umweltverträglichkeit, bei dem Verfahren fallen keine giftigen Metallstäube an (siehe Unfall in Ungarn letztes Jahr. Man nennt ihn "roter Staub" , er enthält giftige Schwermetalle u. fällt aber bei Orbite gar nicht an.

Als 3.Standbein wäre zu nennen, dass Orbite in den hochlukrativen Markt v. Rein-Alu (High-Purity Alu) eindringt , das u.a. bei soviel ich weiß allen Arten v. Leuchtdioden gebraucht wird.

Auch Gallium u. Scandium kann Orbite in signifikaten MEngen produzieren.

Ich habe das jetzt aus dem Gedächtnis wiedergegeben, sollten FEhler enthalten sein, so möchte ich mich vorab entschuldigen u. bitten diese rückzumelden.

Hier noch eine Zs.fassung von der Webseite:

1. Technology

2. Resource

3. Markets

4. Management

“Game-changing” technologies

Orbite owns a proprietary and potentially “game-changing” process to extract alumina from aluminous clay deposits that is significantly more economical compared to conventional methods. Separate processes also extract high-purity alumina and a range of high-value elements, including rare earths. The company’s intellectual property is well protected for 20 years in Canada, the United States and around the world by a robust portfolio of patents and patents pending. As “game changers,” these technologies also offer significant licensing potential internationally. Orbite’s alumina extraction technology has been proven in the lab and pilot plant, and is now ready for commercial roll-out.

Strategic resource

An independent geologist, Jean-Guy Levaque, B.Sc.A., P.Eng., has surveyed Orbite’s Grande-Vallée property in Gaspé, Québec. A conservative estimate based on his findings indicates 1 billion tonnes of “indicated mineral resources” in the first 100 metres depth of one sector of the property alone. The property is strategically located near a road and close to a year-round deepwater seaport, giving access to domestic and export markets. The wealth stored on this property could provide much-needed jobs and investment to the economically depressed Gaspé region, and aligns well with the Québec government’s priorities for job creation and value-added processing in the strategic aluminum sector.

Growing markets

Orbite’s key products—metallurgical grade alumina, high-purity alumina and various high-value elements, including rare earths—are in growing demand around the world.

Experienced management

The Orbite executive team and Board of Directors are primarily made up of achievers with a known capacity to deliver. They are repeat entrepreneurs who have long track records of success in bringing new technologies to market, launching start-ups, and managing large and complex enterprises. They also have hands-on, long-standing experience in the mining, environment, government and community relations, and aluminum sectors.

!

Dieser Beitrag wurde von akummermehr moderiert. Grund: auf eigenen Wunsch des Users

November 25, 2011 - 3:59 PM EST

Print Email Article Font Down Font Up Charts

T.ORT 2.52 -0.09

Today 5d 1m 3m 1y 5y 10y

Orbite to Announce Preliminary Economic Assessment for the Planned Metallurgical Alumina Plant in Gaspesian Region of Quebec

MONTREAL, QUEBEC--(Marketwire - Nov. 25, 2011) - Orbite Aluminae Inc. (TSX:ORT) ("Orbite" or the "Company") will announce the results of the preliminary economic assessment (PEA) prepared by Genivar Inc. for its planned metallurgical grade alumina plant, on Tuesday morning November 29, 2011.

The Company will host a webcast conference call on Tuesday, November 29, 2011 at 10:30 AM EST where senior management will discuss the results of the PEA. The details of the conference call are as follows:

By phone toll free in Canada and the United states 1-800-892-9785

By phone International 416-981-9000

To listen online, go to www.orbitealuminae.com and click on the link on home page

About Orbite

Orbite owns 100% of the mining rights on approximately 6,400 hectares of a Grande-Vallée property, the site of an aluminous clay deposit located 23 km to the south of Grande-Vallée, and a 2 600 sq. m. full scale pilot plant in Cap Chat, in the Gaspé region. The NI 43-101 report issued in August 2011 has identified an Indicated Resource of about 1 billion tonnes of aluminous clay in part of the deposit. The Company also owns the intellectual property rights to a unique Canada and U.S.-patented process for extracting alumina from aluminous ores and for which patents are also pending in other countries. www.orbitealuminae.com

Source: Marketwire Canada (November 25, 2011 - 3:59 PM EST)

News by QuoteMedia

www.quotemedia.com

Print Email Article Font Down Font Up Charts

T.ORT 2.52 -0.09

Today 5d 1m 3m 1y 5y 10y

Orbite to Announce Preliminary Economic Assessment for the Planned Metallurgical Alumina Plant in Gaspesian Region of Quebec

MONTREAL, QUEBEC--(Marketwire - Nov. 25, 2011) - Orbite Aluminae Inc. (TSX:ORT) ("Orbite" or the "Company") will announce the results of the preliminary economic assessment (PEA) prepared by Genivar Inc. for its planned metallurgical grade alumina plant, on Tuesday morning November 29, 2011.

The Company will host a webcast conference call on Tuesday, November 29, 2011 at 10:30 AM EST where senior management will discuss the results of the PEA. The details of the conference call are as follows:

By phone toll free in Canada and the United states 1-800-892-9785

By phone International 416-981-9000

To listen online, go to www.orbitealuminae.com and click on the link on home page

About Orbite

Orbite owns 100% of the mining rights on approximately 6,400 hectares of a Grande-Vallée property, the site of an aluminous clay deposit located 23 km to the south of Grande-Vallée, and a 2 600 sq. m. full scale pilot plant in Cap Chat, in the Gaspé region. The NI 43-101 report issued in August 2011 has identified an Indicated Resource of about 1 billion tonnes of aluminous clay in part of the deposit. The Company also owns the intellectual property rights to a unique Canada and U.S.-patented process for extracting alumina from aluminous ores and for which patents are also pending in other countries. www.orbitealuminae.com

Source: Marketwire Canada (November 25, 2011 - 3:59 PM EST)

News by QuoteMedia

www.quotemedia.com

unglaubliche Breite an Rohstoffen....

November 29, 2011 - 7:00 AM EST

Print Email Article Font Down Font Up Charts

T.ORT 2.95 0.00

Today 5d 1m 3m 1y 5y 10y

Orbite Releases Positive Preliminary Economic Assessment for Its Planned Metallurgical Grade Alumina Plant With the Capacity to Extract Value-Added Oxides, Rare Metals and Rare Earth Oxides

http://at.marketwire.com/accesstracking/AccessTrackingLogSer…

MONTREAL, QUEBEC -- (Marketwire) -- 11/29/11 -- Orbite Aluminae Inc. (TSX:ORT) ("Orbite") is pleased to announce the results of the Preliminary Economic Assessment ("PEA") prepared by Genivar Inc. on its planned commercial metallurgical grade alumina (SGA) production plant (the "Plant"). Orbite plans to produce an estimated 539,700 tonnes per year of alumina, 189,000 tonnes of pure hematite, 1.2 million tonnes of high purity silica, 28,000 tonnes of magnesium oxides, 104,000 tonnes of other value-added oxides, and 820 tonnes of rare metal and rare earth oxides, including, among others, dysprosium, erbium, europium, yttrium, cerium, neodymium, praseodymium, and terbium, and rare metals such as gallium and scandium.

All figures are in Canadian dollars except where noted.

Highlights

-- Indicated resource of approximately 1 billion metric tonnes of

homogeneous aluminous clay (23.13% average concentration alumina) as per

NI 43-101.

-- Based on conservative metal oxides selling prices (August 2011) and a 5%

discount rate, the PEA reveals a pre-tax net present value (NPV) of $7.7

billion, generating an internal rate of return ("IRR") of 114% and a

payback of under one year.

-- Average production cost:

-- $44.53 / tonne of clay for all foreseen products;

-- $42.71 / tonne of clay for alumina and hematite alone.

-- Feasibility Study underway with contract awarded to Genivar Inc. and

expected to be completed during the first half of 2012, with planned

commissioning in late 2013.

"The operations outlined in this PEA for Orbite's metallurgical grade alumina plant forecasted for initial production through the end of 2013 confirms the potential for high-value, low net production cost alumina and other value-added products. The projected high NPV, net cash flows, and relatively low unit cost compared to standard existing alumina processes provide strategic positioning for Orbite and its planned SGA production plant," said Richard Boudreault, Orbite's President and CEO. "Aluminum is the second most used metal after iron. We are therefore establishing the basis of our unique alumina extraction process and paving the way for the production of metallurgical alumina to meet growing demand from the global aluminium industry. This PEA also explains the net advantages of using an eco-friendly process while extracting high purity value-added products.

"We are pleased with the level of expertise and rigor of all of the parties involved in the Preliminary Economic Assessment of the planned metallurgical alumina production plant," continued Mr. Boudreault. "The exercise has also provided us with considerable insight into potential opportunities for further improvement of the already attractive economics. These include adapting existing technologies (i.e. calcination and acid recovery) and finding new ways to extract high purity products in addition to the alumina, while gaining considerable energy efficiency and thus greatly simplifying the process flow sheet. These opportunities will be validated during the Feasibility Study phase, which is ongoing at Genivar. The relatively low operating unit cost of production coupled with a much lower capital cost requirement than standard alumina greenfield projects using existing processes mean that this operation has the potential to be highly profitable in rapid time due to our unique alumina extraction process."

The table below summarizes the highlights of the PEA (all currency is CAN$, pre-tax):

------------------------------------------------------------------------

NPV at 5% discount rate $7.7 billion

------------------------------------------------------------------------

IRR 114%

------------------------------------------------------------------------

Total Estimated CAPEX $498.5 million

------------------------------------------------------------------------

Estimated OPEX

(All products): $44.53/t of clay

(Alumina and hematite): $42.71/t of clay

------------------------------------------------------------------------

Average annual EBITDA $571.7 million

------------------------------------------------------------------------

Estimated open pit mine life at

present estimated production rate greater than

(Reference for one plant) 100 years

------------------------------------------------------------------------

In-pit indicated resources greater than

(at 23.13% Al2O3): 800 M - 1 billion tonnes

------------------------------------------------------------------------

Revenues to be generated by 2013-2014

------------------------------------------------------------------------

Payback 11.0 months

------------------------------------------------------------------------

"We are impressed by Orbite's visionary process, which is capable of refining alumina while at the same time extracting other high purity oxides, silica and hematite as well as certain high-value rare elements and metals from a local Gaspesian source of clay," said Andre-Martin Bouchard, Eng., Vice President at Genivar. "In addition, the process deploys technologies that will ensure that the local environment will be preserved, compared to current alumina refining processes, thus ensuring the sustainable development of the Gaspe region. We have also looked at the economics of producing and marketing only alumina and hematite, to validate the robustness of the project. In this case, the IRR was 33%, with an NPV of 1.7 B$ and a payback of 3.1 years at a 5% discount rate, demonstrating a strong business case."

NPV sensitivities at various discount rates (25 years)

Pre-Tax NPV Payback

Discount Rate (Million) (Months)

----------------------------------------------------------------------------

5% $7,730 11.0

----------------------------------------------------------------------------

7.5% $5,998 11.3

----------------------------------------------------------------------------

10% $4,783 11.5

----------------------------------------------------------------------------

The project shows favourable economic potential across a range of discount rates. The operations outlined in this PEA are projected to generate average annual revenue of more than $702 million over the first 25 years of mine life, with yearly EBITDA of approximately $571.7 million.

Revenue:

Alumina $ 229,377,175

----------------------------------------------------------------------------

Fe2O3 (Hematite) $ 37,859,680

----------------------------------------------------------------------------

SiO2 (High purity silica) $ 30,715,708

----------------------------------------------------------------------------

MgO $ 11,126,400

----------------------------------------------------------------------------

Mixed oxides $ 520,443

----------------------------------------------------------------------------

Rare earth elements $ 392,868,097

----------------------------------------------------------------------------

TOTAL $ 702,467,503

----------------------------------------------------------------------------

Costs:

Mining $ 11,747,706

----------------------------------------------------------------------------

Processing $ 100,246,505

----------------------------------------------------------------------------

Marketing $ 1,122,500

----------------------------------------------------------------------------

TOTAL COSTS $ 113,116,711

----------------------------------------------------------------------------

Profit before royalty $ 589,350,792

----------------------------------------------------------------------------

3% net operating profit royalty(i) $ 17,680,524

(First 5 years only)

----------------------------------------------------------------------------

EBITDA $ 571,670,269

----------------------------------------------------------------------------

(i) Applies for the first 5 years of operations, subject to a buyout at end

of year 5.

Patented technology

Orbite owns the intellectual property rights to a unique Canada and U.S. patented process, a radical innovation aimed at extracting alumina from aluminous ores and for which international patents are also pending in many other countries, such as Brazil, Russia, Australia and Japan as well as in Europe. The patented Orbite process has the potential to become a viable alternative to the industry standard Bayer and other alumina processes, resulting in significant revenues when the technology is licensed to qualified alumina producers. Orbite is planning on marketing smelter grade alumina (SGA), high purity hematite, magnesium oxide, and silica, as well as producing rare earths oxides. Orbite also has several other patents pending related to various processes for producing such products.

Based on the chemical and metallurgical work completed at Orbite's production pilot plant facility and taking advantage of adaptable technologies for the acid recovery systems, the PEA estimated that the process is expected to yield an average of 93% weight recovery of Al2O3, higher than 90% on hematite, magnesium oxides, and high purity silica, and a conservative 75% for the extraction of rare earths, namely dysprosium, erbium, europium, yttrium, cerium, neodymium, praseodymium, and terbium, and rare metals such as gallium and scandium.

Details and assumptions

Total initial capital expenditures (including contingency) are estimated at $498.5 million to produce alumina and other value-added products. The initial capital cost estimate excludes mine closure costs and sustaining capital. Costs for mining equipment and all required infrastructures are included in the capital expenditure costs. The initial assessment of the preferred port facility suggests that sufficient capacity currently exists for the planned initial production. Energy supply represents one of the key elements of the Orbite project, as with all mining, chemical and hydrometallurgical projects. For the purpose of this study, electrical power and natural gas, which is known to be present but not readily available in the mining site vicinity, have been used as the reference energy source. The Henry Hub Index (September 2011) is used as the reference for natural gas prices. A $4.00/GJ has been used for the PEA evaluation.

CAPEX preliminary evaluation:

Summary of estimated initial capital costs Million $

----------------------------------------------------------------------------

Mining, environmental, tailings 33.8

----------------------------------------------------------------------------

Major buildings and process equipment 335.0

----------------------------------------------------------------------------

Plant infrastructure 24.2

----------------------------------------------------------------------------

Other infrastructures 45.0

----------------------------------------------------------------------------

Contingency 60.5

----------------------------------------------------------------------------

TOTAL 498.5

----------------------------------------------------------------------------

Consistent with industry practices, this PEA has been prepared with an accuracy of +/-30%. As the project progresses through the ongoing feasibility stage, advancement in the basic engineering will improve the accuracy to approximately +/-15%.

The Feasibility Study scope of work involves a comprehensive review of all project characteristics-from process validation to capital costs, operational costs, and basic engineering leading to the detailed engineering, marketing, environmental, health & safety, and other considerations-in order to further validate and integrate the various technical aspects of the project. The Feasibility Study report is expected to be published during the first half of 2012.

Qualified persons

The preliminary economic assessment was prepared by leading independent industry consultants, all Qualified Persons (QP) under National Instrument 43-101. The QPs have reviewed and approved the content of this news release. The following consultants participated in the study:

-- Genivar Inc. a leading independent and top ranking engineering firm

-- The geological model and resources estimate were provided to Genivar by

Jean-Guy Levaque, Eng., QP, and responsible for Orbite's NI 43-101

compliant mineral resources estimate. The PEA was prepared by Rod Doran,

P. Eng. (30 years' experience as a mining/metallurgical engineer) under

the supervision of Andre-Martin Bouchard, Eng. with Genivar. Both Mr.

Doran and Mr. Bouchard are independent Qualified Persons as defined by

NI 43-101, are independent of Orbite, and have reviewed the technical

information contained in this news release. Many other third party

specialists also contributed to the PEA.

The complete PEA report will be filed on SEDAR and Orbite's Web site within 45 days of this news release.

CONFERENCE CALL

Orbite will hold a conference call on Tuesday, November 29, 2011, at 10:30 AM (EST) to discuss the results of the PEA and respond to questions from interested parties.

The conference call can be accessed by dialling: 416-981-9000 or toll free in North America: 1-800-892-9785 or by going to the Company's Web site at www.orbitealuminae.com.

An instant replay of the conference call will be available until December 15, 2011, at the following numbers: 1-416-626-4100 or toll free 800-558-5253, code# 21548806

About Genivar Inc.

Genivar is a leading Canadian engineering services company providing private and public-sector clients with a full range of professional consulting services through all project phases, including planning, design, construction and maintenance. Ranging in size, its clients operate in various market segments, including the building, industrial, power, municipal infrastructure, mining, transportation and environmental sectors. Genivar is one of the largest engineering services companies in Canada by number of employees, with more than 4,700 managers, professionals, technicians, technologists and support staff in over 100 cities in Canada and internationally. Genivar received the 2011 Schreyer Award, presented to the designers of the project with the highest technical merit. www.genivar.com

About Orbite

Orbite owns 100% of the mining rights on approximately 6,441 hectares of a Grande-Vallee property, the site of an aluminous clay deposit located 23 km to the south of Grande-Vallee, and a 2 600 sq. m. full scale pilot plant in Cap Chat, in the Gaspe region. The NI 43-101 report issued in August 2011 has identified an Indicated Resource of about 1 Billion tonnes of aluminous clay in part of the deposit. The Company also owns the intellectual property rights to a unique Canada and U.S.-patented process for extracting alumina from aluminous ores and for which patents are also pending in other countries. www.orbitealuminae.com

The PEA is preliminary in nature and it includes Indicated mineral resources of aluminous clay that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the conclusions reached in the PEA will be realized. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

Regulation 43-101 and forward-looking statements

The Preliminary Economic Assessment ('PEA') referred to herein constitutes a "preliminary economic assessment" within the meaning of Regulation 43-101 respecting standards of disclosure for mineral projects (Quebec) ("Regulation 43-101"). All references contained in this PEA pertains only to the production of smelter grade alumina (SGA) (including projected daily production levels) and the production of other resources, including rare earths, and have been made by assuming that the technical, financial and economic feasibility of such operations will be further demonstrated. No preliminary feasibility study, pre-feasibility study, nor a feasibility study pursuant to the requirements of Regulation 43-101 has been completed to date.

Certain information contained in this document may include "forward-looking information", particularly regarding the daily production of the projected plant described in this PEA, the anticipated cost of the construction of such plant producing SGA and other resources including rare earths. Without limiting the foregoing, the information and any forward-looking information may include statements regarding projects, costs, objectives and future returns of the Company or hypotheses underlying these items. In this document, words such as "may", "would", "could", "will", "likely", "believe", "expect", "anticipate", "intend", "plan", "estimate" and similar words and the negative form thereof are used to identify forward-looking statements. Forward-looking statements should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether, or the times at or by which, such future performance will be achieved. Forward-looking statements and information are based on information available at the time and/or the Company management's good-faith beliefs with respect to future events and are subject to known or unknown risks, uncertainties, assumptions and other unpredictable factors, many of which are beyond the Company's control. These risks uncertainties and assumptions include, but are not limited to, those described in the section of the Management's Discussion and Analysis ( MD&A) entitled "Risk and Uncertainties" as filed on November 14, 2011 on SEDAR, and could cause actual events or results to differ materially from those projected in any forward-looking statements. The Company does not intend, nor does it undertake, any obligation to update or revise any forward-looking information or statements contained in this document to reflect subsequent information, events or circumstances or otherwise, except as required by applicable laws. As for projected dates of beginning of operations, namely the year 2013 for the SGA production plant projected to be put into service, this date is an objective and that many steps (feasibility study, financing, environmental and government authorizations and other important an usual conditions) remain before confirming any particular schedule. Notwithstanding the PEA, no independent study has confirmed the feasibility of putting the production plant described herein into service according to the projected dates and its projected financial and economic performance.

Readers are invited to consult the Report on the Geological Study prepared in conformity with Regulation 43-101 and the Annual Information Form of the Corporation, both amended and restated and respectively filed on August 21 and 25, 2011 and the Management's Discussion and Analysis filed on November 14, 2011 which are available at www.sedar.com or on the Corporation's website at www.orbitealuminae.com.

Contacts:

MEDIA

Frederic Berard

Vice-President

HKDP Communications and public affairs

514-395-0375, ext. 259

Jacques Bedard

Vice-President Finance and Chief Financial

Orbite Aluminae Inc.

514-744-6264

INVESTOR RELATIONS

Louis Morin

Investor Relations

514-591-3988

Jason Monaco

Managing Partner

First Canadian Capital Corp.

416-742-5600

Nicole Blanchard

Investor Relations

Sun International Communications

450-973-6600

Source: Marketwire (November 29, 2011 - 7:00 AM EST)

News by QuoteMedia

www.quotemedia.com

November 29, 2011 - 7:00 AM EST

Print Email Article Font Down Font Up Charts

T.ORT 2.95 0.00

Today 5d 1m 3m 1y 5y 10y

Orbite Releases Positive Preliminary Economic Assessment for Its Planned Metallurgical Grade Alumina Plant With the Capacity to Extract Value-Added Oxides, Rare Metals and Rare Earth Oxides

http://at.marketwire.com/accesstracking/AccessTrackingLogSer…

MONTREAL, QUEBEC -- (Marketwire) -- 11/29/11 -- Orbite Aluminae Inc. (TSX:ORT) ("Orbite") is pleased to announce the results of the Preliminary Economic Assessment ("PEA") prepared by Genivar Inc. on its planned commercial metallurgical grade alumina (SGA) production plant (the "Plant"). Orbite plans to produce an estimated 539,700 tonnes per year of alumina, 189,000 tonnes of pure hematite, 1.2 million tonnes of high purity silica, 28,000 tonnes of magnesium oxides, 104,000 tonnes of other value-added oxides, and 820 tonnes of rare metal and rare earth oxides, including, among others, dysprosium, erbium, europium, yttrium, cerium, neodymium, praseodymium, and terbium, and rare metals such as gallium and scandium.

All figures are in Canadian dollars except where noted.

Highlights

-- Indicated resource of approximately 1 billion metric tonnes of

homogeneous aluminous clay (23.13% average concentration alumina) as per

NI 43-101.

-- Based on conservative metal oxides selling prices (August 2011) and a 5%

discount rate, the PEA reveals a pre-tax net present value (NPV) of $7.7

billion, generating an internal rate of return ("IRR") of 114% and a

payback of under one year.

-- Average production cost:

-- $44.53 / tonne of clay for all foreseen products;

-- $42.71 / tonne of clay for alumina and hematite alone.

-- Feasibility Study underway with contract awarded to Genivar Inc. and

expected to be completed during the first half of 2012, with planned

commissioning in late 2013.

"The operations outlined in this PEA for Orbite's metallurgical grade alumina plant forecasted for initial production through the end of 2013 confirms the potential for high-value, low net production cost alumina and other value-added products. The projected high NPV, net cash flows, and relatively low unit cost compared to standard existing alumina processes provide strategic positioning for Orbite and its planned SGA production plant," said Richard Boudreault, Orbite's President and CEO. "Aluminum is the second most used metal after iron. We are therefore establishing the basis of our unique alumina extraction process and paving the way for the production of metallurgical alumina to meet growing demand from the global aluminium industry. This PEA also explains the net advantages of using an eco-friendly process while extracting high purity value-added products.

"We are pleased with the level of expertise and rigor of all of the parties involved in the Preliminary Economic Assessment of the planned metallurgical alumina production plant," continued Mr. Boudreault. "The exercise has also provided us with considerable insight into potential opportunities for further improvement of the already attractive economics. These include adapting existing technologies (i.e. calcination and acid recovery) and finding new ways to extract high purity products in addition to the alumina, while gaining considerable energy efficiency and thus greatly simplifying the process flow sheet. These opportunities will be validated during the Feasibility Study phase, which is ongoing at Genivar. The relatively low operating unit cost of production coupled with a much lower capital cost requirement than standard alumina greenfield projects using existing processes mean that this operation has the potential to be highly profitable in rapid time due to our unique alumina extraction process."

The table below summarizes the highlights of the PEA (all currency is CAN$, pre-tax):

------------------------------------------------------------------------

NPV at 5% discount rate $7.7 billion

------------------------------------------------------------------------

IRR 114%

------------------------------------------------------------------------

Total Estimated CAPEX $498.5 million

------------------------------------------------------------------------

Estimated OPEX

(All products): $44.53/t of clay

(Alumina and hematite): $42.71/t of clay

------------------------------------------------------------------------

Average annual EBITDA $571.7 million

------------------------------------------------------------------------

Estimated open pit mine life at

present estimated production rate greater than

(Reference for one plant) 100 years

------------------------------------------------------------------------

In-pit indicated resources greater than

(at 23.13% Al2O3): 800 M - 1 billion tonnes

------------------------------------------------------------------------

Revenues to be generated by 2013-2014

------------------------------------------------------------------------

Payback 11.0 months

------------------------------------------------------------------------

"We are impressed by Orbite's visionary process, which is capable of refining alumina while at the same time extracting other high purity oxides, silica and hematite as well as certain high-value rare elements and metals from a local Gaspesian source of clay," said Andre-Martin Bouchard, Eng., Vice President at Genivar. "In addition, the process deploys technologies that will ensure that the local environment will be preserved, compared to current alumina refining processes, thus ensuring the sustainable development of the Gaspe region. We have also looked at the economics of producing and marketing only alumina and hematite, to validate the robustness of the project. In this case, the IRR was 33%, with an NPV of 1.7 B$ and a payback of 3.1 years at a 5% discount rate, demonstrating a strong business case."

NPV sensitivities at various discount rates (25 years)

Pre-Tax NPV Payback

Discount Rate (Million) (Months)

----------------------------------------------------------------------------

5% $7,730 11.0

----------------------------------------------------------------------------

7.5% $5,998 11.3

----------------------------------------------------------------------------

10% $4,783 11.5

----------------------------------------------------------------------------

The project shows favourable economic potential across a range of discount rates. The operations outlined in this PEA are projected to generate average annual revenue of more than $702 million over the first 25 years of mine life, with yearly EBITDA of approximately $571.7 million.

Revenue:

Alumina $ 229,377,175

----------------------------------------------------------------------------

Fe2O3 (Hematite) $ 37,859,680

----------------------------------------------------------------------------

SiO2 (High purity silica) $ 30,715,708

----------------------------------------------------------------------------

MgO $ 11,126,400

----------------------------------------------------------------------------

Mixed oxides $ 520,443

----------------------------------------------------------------------------

Rare earth elements $ 392,868,097

----------------------------------------------------------------------------

TOTAL $ 702,467,503

----------------------------------------------------------------------------

Costs:

Mining $ 11,747,706

----------------------------------------------------------------------------

Processing $ 100,246,505

----------------------------------------------------------------------------

Marketing $ 1,122,500

----------------------------------------------------------------------------

TOTAL COSTS $ 113,116,711

----------------------------------------------------------------------------

Profit before royalty $ 589,350,792

----------------------------------------------------------------------------

3% net operating profit royalty(i) $ 17,680,524

(First 5 years only)

----------------------------------------------------------------------------

EBITDA $ 571,670,269

----------------------------------------------------------------------------

(i) Applies for the first 5 years of operations, subject to a buyout at end

of year 5.

Patented technology

Orbite owns the intellectual property rights to a unique Canada and U.S. patented process, a radical innovation aimed at extracting alumina from aluminous ores and for which international patents are also pending in many other countries, such as Brazil, Russia, Australia and Japan as well as in Europe. The patented Orbite process has the potential to become a viable alternative to the industry standard Bayer and other alumina processes, resulting in significant revenues when the technology is licensed to qualified alumina producers. Orbite is planning on marketing smelter grade alumina (SGA), high purity hematite, magnesium oxide, and silica, as well as producing rare earths oxides. Orbite also has several other patents pending related to various processes for producing such products.

Based on the chemical and metallurgical work completed at Orbite's production pilot plant facility and taking advantage of adaptable technologies for the acid recovery systems, the PEA estimated that the process is expected to yield an average of 93% weight recovery of Al2O3, higher than 90% on hematite, magnesium oxides, and high purity silica, and a conservative 75% for the extraction of rare earths, namely dysprosium, erbium, europium, yttrium, cerium, neodymium, praseodymium, and terbium, and rare metals such as gallium and scandium.

Details and assumptions

Total initial capital expenditures (including contingency) are estimated at $498.5 million to produce alumina and other value-added products. The initial capital cost estimate excludes mine closure costs and sustaining capital. Costs for mining equipment and all required infrastructures are included in the capital expenditure costs. The initial assessment of the preferred port facility suggests that sufficient capacity currently exists for the planned initial production. Energy supply represents one of the key elements of the Orbite project, as with all mining, chemical and hydrometallurgical projects. For the purpose of this study, electrical power and natural gas, which is known to be present but not readily available in the mining site vicinity, have been used as the reference energy source. The Henry Hub Index (September 2011) is used as the reference for natural gas prices. A $4.00/GJ has been used for the PEA evaluation.

CAPEX preliminary evaluation:

Summary of estimated initial capital costs Million $

----------------------------------------------------------------------------

Mining, environmental, tailings 33.8

----------------------------------------------------------------------------

Major buildings and process equipment 335.0

----------------------------------------------------------------------------

Plant infrastructure 24.2

----------------------------------------------------------------------------

Other infrastructures 45.0

----------------------------------------------------------------------------

Contingency 60.5

----------------------------------------------------------------------------

TOTAL 498.5

----------------------------------------------------------------------------

Consistent with industry practices, this PEA has been prepared with an accuracy of +/-30%. As the project progresses through the ongoing feasibility stage, advancement in the basic engineering will improve the accuracy to approximately +/-15%.

The Feasibility Study scope of work involves a comprehensive review of all project characteristics-from process validation to capital costs, operational costs, and basic engineering leading to the detailed engineering, marketing, environmental, health & safety, and other considerations-in order to further validate and integrate the various technical aspects of the project. The Feasibility Study report is expected to be published during the first half of 2012.

Qualified persons

The preliminary economic assessment was prepared by leading independent industry consultants, all Qualified Persons (QP) under National Instrument 43-101. The QPs have reviewed and approved the content of this news release. The following consultants participated in the study:

-- Genivar Inc. a leading independent and top ranking engineering firm

-- The geological model and resources estimate were provided to Genivar by

Jean-Guy Levaque, Eng., QP, and responsible for Orbite's NI 43-101

compliant mineral resources estimate. The PEA was prepared by Rod Doran,

P. Eng. (30 years' experience as a mining/metallurgical engineer) under

the supervision of Andre-Martin Bouchard, Eng. with Genivar. Both Mr.

Doran and Mr. Bouchard are independent Qualified Persons as defined by

NI 43-101, are independent of Orbite, and have reviewed the technical

information contained in this news release. Many other third party

specialists also contributed to the PEA.

The complete PEA report will be filed on SEDAR and Orbite's Web site within 45 days of this news release.

CONFERENCE CALL

Orbite will hold a conference call on Tuesday, November 29, 2011, at 10:30 AM (EST) to discuss the results of the PEA and respond to questions from interested parties.

The conference call can be accessed by dialling: 416-981-9000 or toll free in North America: 1-800-892-9785 or by going to the Company's Web site at www.orbitealuminae.com.

An instant replay of the conference call will be available until December 15, 2011, at the following numbers: 1-416-626-4100 or toll free 800-558-5253, code# 21548806

About Genivar Inc.

Genivar is a leading Canadian engineering services company providing private and public-sector clients with a full range of professional consulting services through all project phases, including planning, design, construction and maintenance. Ranging in size, its clients operate in various market segments, including the building, industrial, power, municipal infrastructure, mining, transportation and environmental sectors. Genivar is one of the largest engineering services companies in Canada by number of employees, with more than 4,700 managers, professionals, technicians, technologists and support staff in over 100 cities in Canada and internationally. Genivar received the 2011 Schreyer Award, presented to the designers of the project with the highest technical merit. www.genivar.com

About Orbite

Orbite owns 100% of the mining rights on approximately 6,441 hectares of a Grande-Vallee property, the site of an aluminous clay deposit located 23 km to the south of Grande-Vallee, and a 2 600 sq. m. full scale pilot plant in Cap Chat, in the Gaspe region. The NI 43-101 report issued in August 2011 has identified an Indicated Resource of about 1 Billion tonnes of aluminous clay in part of the deposit. The Company also owns the intellectual property rights to a unique Canada and U.S.-patented process for extracting alumina from aluminous ores and for which patents are also pending in other countries. www.orbitealuminae.com

The PEA is preliminary in nature and it includes Indicated mineral resources of aluminous clay that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the conclusions reached in the PEA will be realized. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

Regulation 43-101 and forward-looking statements

The Preliminary Economic Assessment ('PEA') referred to herein constitutes a "preliminary economic assessment" within the meaning of Regulation 43-101 respecting standards of disclosure for mineral projects (Quebec) ("Regulation 43-101"). All references contained in this PEA pertains only to the production of smelter grade alumina (SGA) (including projected daily production levels) and the production of other resources, including rare earths, and have been made by assuming that the technical, financial and economic feasibility of such operations will be further demonstrated. No preliminary feasibility study, pre-feasibility study, nor a feasibility study pursuant to the requirements of Regulation 43-101 has been completed to date.

Certain information contained in this document may include "forward-looking information", particularly regarding the daily production of the projected plant described in this PEA, the anticipated cost of the construction of such plant producing SGA and other resources including rare earths. Without limiting the foregoing, the information and any forward-looking information may include statements regarding projects, costs, objectives and future returns of the Company or hypotheses underlying these items. In this document, words such as "may", "would", "could", "will", "likely", "believe", "expect", "anticipate", "intend", "plan", "estimate" and similar words and the negative form thereof are used to identify forward-looking statements. Forward-looking statements should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether, or the times at or by which, such future performance will be achieved. Forward-looking statements and information are based on information available at the time and/or the Company management's good-faith beliefs with respect to future events and are subject to known or unknown risks, uncertainties, assumptions and other unpredictable factors, many of which are beyond the Company's control. These risks uncertainties and assumptions include, but are not limited to, those described in the section of the Management's Discussion and Analysis ( MD&A) entitled "Risk and Uncertainties" as filed on November 14, 2011 on SEDAR, and could cause actual events or results to differ materially from those projected in any forward-looking statements. The Company does not intend, nor does it undertake, any obligation to update or revise any forward-looking information or statements contained in this document to reflect subsequent information, events or circumstances or otherwise, except as required by applicable laws. As for projected dates of beginning of operations, namely the year 2013 for the SGA production plant projected to be put into service, this date is an objective and that many steps (feasibility study, financing, environmental and government authorizations and other important an usual conditions) remain before confirming any particular schedule. Notwithstanding the PEA, no independent study has confirmed the feasibility of putting the production plant described herein into service according to the projected dates and its projected financial and economic performance.

Readers are invited to consult the Report on the Geological Study prepared in conformity with Regulation 43-101 and the Annual Information Form of the Corporation, both amended and restated and respectively filed on August 21 and 25, 2011 and the Management's Discussion and Analysis filed on November 14, 2011 which are available at www.sedar.com or on the Corporation's website at www.orbitealuminae.com.

Contacts:

MEDIA

Frederic Berard

Vice-President

HKDP Communications and public affairs

514-395-0375, ext. 259

Jacques Bedard

Vice-President Finance and Chief Financial

Orbite Aluminae Inc.

514-744-6264

INVESTOR RELATIONS

Louis Morin

Investor Relations

514-591-3988

Jason Monaco

Managing Partner

First Canadian Capital Corp.

416-742-5600

Nicole Blanchard

Investor Relations

Sun International Communications

450-973-6600

Source: Marketwire (November 29, 2011 - 7:00 AM EST)

News by QuoteMedia

www.quotemedia.com

die PEA liest sich der Wahnsinn - dann sofort TradingHalt, man kann die Zahlen wohl nicht ganz nachvollziehen und das Unternehemen hält heute eine Pressekonferenz dazu

die PEA wurde durch unabhängige Geologen erstellt - man hat die Vorkommen

NPV von 7 Mrd$ bei einer Capex von knapp 500 Mio$ sind gigantisch!

das weckt natürlich sofort Nachfragen.......

man darf gespannt sein!

selbst wenn nur das Aluminuim realisiert würde :

"....We have also looked at the economics of producing and marketing only alumina and hematite, to validate the robustness of the project. In this case, the IRR was 33%, with an NPV of 1.7 B$ and a payback of 3.1 years at a 5% discount rate, demonstrating a strong business case...."

immer noch Top!

die PEA wurde durch unabhängige Geologen erstellt - man hat die Vorkommen

NPV von 7 Mrd$ bei einer Capex von knapp 500 Mio$ sind gigantisch!

das weckt natürlich sofort Nachfragen.......

man darf gespannt sein!

selbst wenn nur das Aluminuim realisiert würde :

"....We have also looked at the economics of producing and marketing only alumina and hematite, to validate the robustness of the project. In this case, the IRR was 33%, with an NPV of 1.7 B$ and a payback of 3.1 years at a 5% discount rate, demonstrating a strong business case...."

immer noch Top!

Trading Spotlight

wenn ORT das alles so umsetzten kann wären sie mit einem Schlag neben dem Aluminium der größte Produzent seltener Erden in Nordamerika!

vorbörslich in Canada 3,50 - 3,50..........entspricht ca. 2,55 Euro!

mal sehen was das wird heute.......

Investment Industry Regulatory Organization of Canada Trade Resumption – ORT

TORONTO, Nov. 30, 2011 /CNW/ - Trading resumes in:

Company: Orbite Aluminae Inc.

TSX Symbol: ORT

Resumption: At Open

mal sehen was das wird heute.......

Investment Industry Regulatory Organization of Canada Trade Resumption – ORT

TORONTO, Nov. 30, 2011 /CNW/ - Trading resumes in:

Company: Orbite Aluminae Inc.

TSX Symbol: ORT

Resumption: At Open

Oh - jetzt wollte ich auch mal einen Thread eröffnen und dann gibts den schon. ORT wurde vor Monaten (Februar oder März) schon mal intensiv im Thread von TimLuca vorgstellt, hat aber niemanden interessiert (ausser mir)

Leider hatte ich da zu früh zugegriffen und war zwischenzeitlich schon 70% im roten Bereich...

So wollte ich den Thread eigentlich eröffnen:

Ich habe vor ein paar Tagen einen Beitrag zur Aluminium-Erzeugung auf Kabel1 oder N24 gesehen (weiß es nicht mehr genau).

Was Euch natürlich schon bekannt ist - Aluminium wird aus Bauxit gewonnen. Der größte Teil wird im Moment (so weit mir bekannt) in China gefördert. In Form von Alumnina (sieht wie grauer "Puderzucker" aus) wird es dann nach Island verschifft (da war es dann 2 Wochen auf der "Reise"), weil die Erzeugung von Aluminum mit einem sehr hohem Energieaufwand einhergeht. In Island dagegen gibt es durch die vielen natürlichen Resourcen (Wasser, Geothermie) "billige" Energie. Hier wird dann recht aufwändig Aluminium produziert (konnte mir leider den Firmannamen nicht merken).

Kurzer Excess:

Bauxit wird in Druckbehältern bei 150 bis 200 °C in Natronlauge erhitzt, wobei Aluminium als Aluminat in Lösung geht und vom eisenreichen Rückstand (Rotschlamm) abfiltriert wird (Bayer-Verfahren). Aus der Aluminatlauge scheidet sich beim Abkühlen und Zufügung von feinem Aluminiumhydroxid als Kristallisationskeim reiner Gibbsit ab, der durch Glühen in Aluminiumoxid Al2O3 umgewandelt wird. Das Aluminiumoxid wird unter Zusatz von Kryolith als Schmelzmittel bei etwa 1000 °C geschmolzen und in Elektrolyse-Zellen bei hohem Energieeinsatz zu metallischem Aluminium reduziert (Hall-Héroult-Prozess, Schmelzflusselektrolyse).

http://de.wikipedia.org/wiki/Bauxit

Der Nebeneffekt beim Abbau von Bauxit soll der so genannte rote Schlamm (red mud) sein, welcher hoch giftig sein soll! Orbite hat....

... den Rest kann ich mir ja jetzt sparen...

Grüße

rolleg

Leider hatte ich da zu früh zugegriffen und war zwischenzeitlich schon 70% im roten Bereich...

So wollte ich den Thread eigentlich eröffnen:

Ich habe vor ein paar Tagen einen Beitrag zur Aluminium-Erzeugung auf Kabel1 oder N24 gesehen (weiß es nicht mehr genau).

Was Euch natürlich schon bekannt ist - Aluminium wird aus Bauxit gewonnen. Der größte Teil wird im Moment (so weit mir bekannt) in China gefördert. In Form von Alumnina (sieht wie grauer "Puderzucker" aus) wird es dann nach Island verschifft (da war es dann 2 Wochen auf der "Reise"), weil die Erzeugung von Aluminum mit einem sehr hohem Energieaufwand einhergeht. In Island dagegen gibt es durch die vielen natürlichen Resourcen (Wasser, Geothermie) "billige" Energie. Hier wird dann recht aufwändig Aluminium produziert (konnte mir leider den Firmannamen nicht merken).

Kurzer Excess:

Bauxit wird in Druckbehältern bei 150 bis 200 °C in Natronlauge erhitzt, wobei Aluminium als Aluminat in Lösung geht und vom eisenreichen Rückstand (Rotschlamm) abfiltriert wird (Bayer-Verfahren). Aus der Aluminatlauge scheidet sich beim Abkühlen und Zufügung von feinem Aluminiumhydroxid als Kristallisationskeim reiner Gibbsit ab, der durch Glühen in Aluminiumoxid Al2O3 umgewandelt wird. Das Aluminiumoxid wird unter Zusatz von Kryolith als Schmelzmittel bei etwa 1000 °C geschmolzen und in Elektrolyse-Zellen bei hohem Energieeinsatz zu metallischem Aluminium reduziert (Hall-Héroult-Prozess, Schmelzflusselektrolyse).

http://de.wikipedia.org/wiki/Bauxit

Der Nebeneffekt beim Abbau von Bauxit soll der so genannte rote Schlamm (red mud) sein, welcher hoch giftig sein soll! Orbite hat....

... den Rest kann ich mir ja jetzt sparen...

Grüße

rolleg

Hi Rolleg,

willkommen hier an Board.

Ich halte Orbite für eine der aussichtsreichsten Werte im Rohstoffsektor, die ich zumindest kenne.

Aus dem neuesten Jennings Report (bitte googeln) :

Rare Earths Drive Exceptional Economics: The rare

metal and rare earth oxides include dysprosium, erbium,

europium, yttrium, cerium, neodymium, praseodymium, and

terbium, as well as rare metals such as gallium and

scandium, and account for approximately 55.9% of the

projected average annual revenues derived from a

539,700 tonne alumina plant. These byproducts can be

produced at minimal incremental cost.

willkommen hier an Board.

Ich halte Orbite für eine der aussichtsreichsten Werte im Rohstoffsektor, die ich zumindest kenne.

Aus dem neuesten Jennings Report (bitte googeln) :

Rare Earths Drive Exceptional Economics: The rare

metal and rare earth oxides include dysprosium, erbium,

europium, yttrium, cerium, neodymium, praseodymium, and

terbium, as well as rare metals such as gallium and

scandium, and account for approximately 55.9% of the

projected average annual revenues derived from a

539,700 tonne alumina plant. These byproducts can be

produced at minimal incremental cost.

in dem JenningsReport wird das Endprodukt HPA gar nicht erwähnt, für mich ein weiteres Zuckerl, also das High-Purity Aluminium, wichtig in der Diodentechnik....

December 07, 2011 08:00 ET

Orbite Awards Alumina Calcination and Its Acid Recovery Basic Engineering Contract to Outotec

Alumina production combined with hydrochloric acid recovery integration will also enable Orbite to recover important quantities of other value added elements from the process

http://www.marketwire.com/press-release/orbite-awards-alumin…

MONTREAL, QUEBEC--(Marketwire - Dec. 7, 2011) - Orbite Aluminae Inc. (TSX:ORT) ("Orbite") announces that it has awarded Outotec, a leading global provider of sustainable process solutions, technologies and services for the minerals and metals industries, a contract to perform the basic engineering of its metallurgical grade alumina calcination process and its associated hydrochloric acid recovery.

Basic engineering will ensure a high level of hydrochloric acid recovery to produce suitable high-quality alumina for aluminum smelters. Additionally, Outotec will provide key elements needed to incorporate the calcination process into the ongoing Feasibility Study (FS) previously announced. The basic engineering report is expected to be completed in the first half of 2012.

"Orbite's unique extraction process is truly revolutionary in that it has the potential to become an economically and ecologically viable substitute to the Bayer process, which has been the main industrial method of refining bauxite for the production of alumina for more than 100 years," said Michael Missalla, Outotec vice-president light metals / fluidized beds. "Outotec has the expertise, experience and cost-effective technologies to perform calcination and acid recovery of alumina from Orbite's process."

"Outotec's proven expertise on calcination processes with demonstrated efficient energy consumption and high heat recovery, combined with the hydrochloric acid recovery, constitutes an excellent asset for Orbite. Outotec is a world leader in calcination processes and has proven its capability to successfully process Orbite's raw material with their circulating fluid bed system," said Richard Boudreault, Orbite president and CEO.

Combined with SMS-Siemag's proven hydrothermal technology for both hematite production and low temperature hydrochloric acid recovery, the calcination of alumina will close the important and essential acid recovery portion of Orbite's process. An ongoing feasibility study will integrate all sub-systems together while further optimization of process parameters is underway in different locations in Europe.

"Outotec's expertise has proven successful worldwide and will allow Orbite to produce high-quality alumina. Outotec's experience will facilitate the integration of circulating fluid bed operational units within Orbite's process on a commercial scale", said Richard Boudreault.

Orbite Awards Alumina Calcination and Its Acid Recovery Basic Engineering Contract to Outotec

Alumina production combined with hydrochloric acid recovery integration will also enable Orbite to recover important quantities of other value added elements from the process

http://www.marketwire.com/press-release/orbite-awards-alumin…

MONTREAL, QUEBEC--(Marketwire - Dec. 7, 2011) - Orbite Aluminae Inc. (TSX:ORT) ("Orbite") announces that it has awarded Outotec, a leading global provider of sustainable process solutions, technologies and services for the minerals and metals industries, a contract to perform the basic engineering of its metallurgical grade alumina calcination process and its associated hydrochloric acid recovery.

Basic engineering will ensure a high level of hydrochloric acid recovery to produce suitable high-quality alumina for aluminum smelters. Additionally, Outotec will provide key elements needed to incorporate the calcination process into the ongoing Feasibility Study (FS) previously announced. The basic engineering report is expected to be completed in the first half of 2012.

"Orbite's unique extraction process is truly revolutionary in that it has the potential to become an economically and ecologically viable substitute to the Bayer process, which has been the main industrial method of refining bauxite for the production of alumina for more than 100 years," said Michael Missalla, Outotec vice-president light metals / fluidized beds. "Outotec has the expertise, experience and cost-effective technologies to perform calcination and acid recovery of alumina from Orbite's process."

"Outotec's proven expertise on calcination processes with demonstrated efficient energy consumption and high heat recovery, combined with the hydrochloric acid recovery, constitutes an excellent asset for Orbite. Outotec is a world leader in calcination processes and has proven its capability to successfully process Orbite's raw material with their circulating fluid bed system," said Richard Boudreault, Orbite president and CEO.

Combined with SMS-Siemag's proven hydrothermal technology for both hematite production and low temperature hydrochloric acid recovery, the calcination of alumina will close the important and essential acid recovery portion of Orbite's process. An ongoing feasibility study will integrate all sub-systems together while further optimization of process parameters is underway in different locations in Europe.

"Outotec's expertise has proven successful worldwide and will allow Orbite to produce high-quality alumina. Outotec's experience will facilitate the integration of circulating fluid bed operational units within Orbite's process on a commercial scale", said Richard Boudreault.

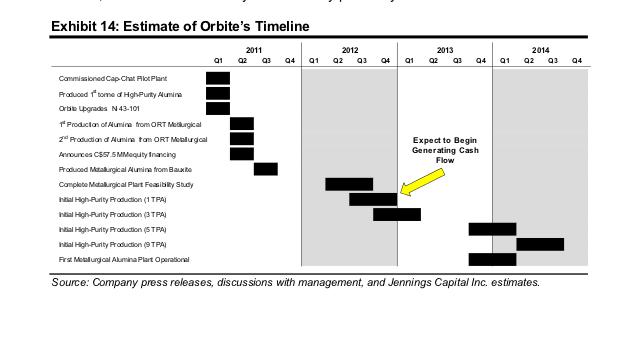

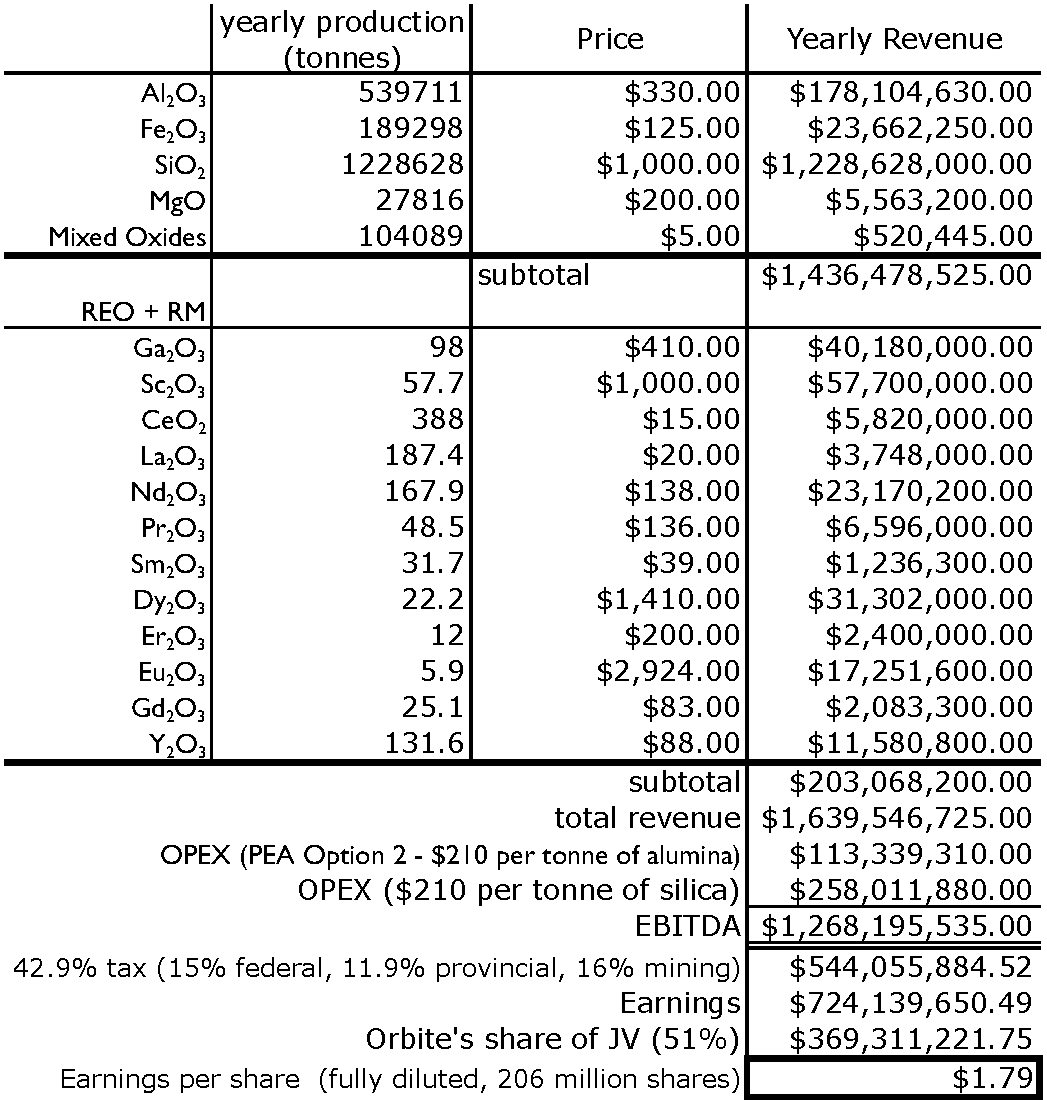

Jennings Top Pick for 2012

Orbite Aluminae is a Québec-based resource / chemical / technology company whose two flagship

assets consist of: (1) patented and patent pending processes to extract metallurgical and high-purity

alumina, as well as other valuable byproducts from aluminous clays, and (2) a 6,441-hectare Grande-

Vallée property situated in Québec’s Gaspe Peninsula, which contains a sizable aluminous clay deposit

(1 Bln tonnes).

We believe that Orbite is poised to revolutionize the aluminum industry with its alumina process patented

technology. The Company has produced both high-purity and metallurgical grade alumina using its

proprietary technology at its 100%-owned industry-scale Cap-Chat facility since February 2011.

Metallurgical Grade Alumina

Metallurgical alumina or smelter grade alumina (SGA) is an essential ingredient in the production of

aluminum; approximately two tonnes of metallurgical alumina is required to produce one tonne of

aluminum. Orbite’s aluminous clay deposit and the planned site location for its first SGA plant are

situated within 20 km of a ship loading facility situated on tidal waters and within a 70 km radius of

10 aluminum smelters in Québec (plus two more in New York State), representing an alumina market of

approximately 5.5 million tonnes, or 12% of global aluminum consumption. These smelters currently

import alumina from such distant countries as Australia, Jamaica and Brazil.

According to a Preliminary Economic Assessment (PEA) prepared by Genivar Inc. and based on the

production of alumina and hematite alone, a single Orbite planned alumina plant is estimated to have an

NPV(5%) of C$1.7 billion (versus capex of C$498.5 million), an IRR of 33%, and a payback of 3.1 years.

This is based on an annual plant capacity of 539,700 tonnes of alumina and an average cash cost of

approximately C$210 per tonne (this would put Orbite’s cash cost in the lowest quartile for global alumina

producers). Furthermore, Orbite’s process appears to be much more environmentally friendly relative to

the Bayer process, which produces a toxic red mud (for example, the failure of a tailings damn at Magyar

Aluminum in Hungary in October 2010 resulted in deaths and considerable damage to surrounding

communities). Orbite’s process does not produce red mud and it is expected that better than 90% of the

acid used in the leaching process will be recovered.

To date, two independent organizations (Norwegian-based leading independent international research

organization SINTEF and the Institute of Scientific Research - Energy, Materials and Communications)

have successfully produced aluminum from Orbite’s alumina, confirming the quality of Orbite’s

metallurgical alumina. Orbite anticipates commencing construction of its first metallurgical plant in 2012

and commencing production in late 2013.

High-Purity Grade Alumina

High-purity alumina is used in applications requiring high ductility or conductivity. These properties are

why high-purity alumina is a key ingredient in sapphire wafers and liquid-crystal polymer, which are key

components used in the production of LEDs. According to the Company, the high-purity alumina

produced from its clay at its pilot plant meets industry standards for LEDs.

24

The information contained in this report was obtained from sources we believe to be reliable. We do not represent that such information is accurate or

complete and it should not be relied on as such. Any opinions expressed herein reflect our judgment at this date and are subject to change. Jennings

Capital Inc. and/or employees from time to time may hold shares, options or warrants on any issue included in this report and may buy or sell such

securities. This report is not to be construed as an offer to sell or solicitation to buy securities. Member – CIPF. Jennings Capital (USA) Inc. is a

member of SIPC.

Orbite expects to have initial production of high-purity alumina of 1 tonne/day in Q3/12, increasing to

3 tonnes/day in Q4/12 – this equates to 350 tonnes of high-purity alumina in 2012. Using a price of

US$250/kg and a production cost of C$1,250/tonne, this production represents revenue of C$87.5 MM

and EBITDA of C$83.1 MM.

In 2010, the global market for LEDs was more than US$10 billion, and it is expected to increase by at

least a 20% CAGR between 2011 and 2015. The high-purity alumina required for the sapphire wafers is

available from only a handful of producers, and it is extremely expensive to produce using

conventional/existing technologies.

More Blue-Sky Potential

According to the PEA, a single Orbite metallurgical plant with the same annual alumina capacity, but

including the recovery of other byproducts including rare earths, is estimated to have an NPV(5%) of

$7.7 billion, an IRR of 114%, and a payback period of 11 months. The incremental cost to produce these

byproducts is estimated to be C$8.43/tonne, which yields an additional C$677/tonne in revenue.

Orbite is also conducting laboratory tests using its proprietary technology to process bauxite, and

according to the Company, the alumina extraction rate compares favourably with that of its Grande-Vallée

aluminous clay. This indicates that Orbite’s process could be used to extract alumina from bauxite and

could possibly be a viable substitute for the 124-year old Bayer process, with significant ecological

advantages.

Our 12-month target price for Orbite of C$11.50 per share is based on a blend of: (1) Our NAV(10%)

estimate of C$46.00 per fully diluted share for high-purity and metallurgical alumina, as well as all other

byproducts used in the PEA, which is risked at 30%; and (2) A 7.5x multiple applied to our FY2013 CFPS

estimate for high-purity alumina alone, which is C$1.25.

Beste Grüsse

Oberkassler

Orbite Aluminae is a Québec-based resource / chemical / technology company whose two flagship

assets consist of: (1) patented and patent pending processes to extract metallurgical and high-purity

alumina, as well as other valuable byproducts from aluminous clays, and (2) a 6,441-hectare Grande-

Vallée property situated in Québec’s Gaspe Peninsula, which contains a sizable aluminous clay deposit

(1 Bln tonnes).

We believe that Orbite is poised to revolutionize the aluminum industry with its alumina process patented

technology. The Company has produced both high-purity and metallurgical grade alumina using its

proprietary technology at its 100%-owned industry-scale Cap-Chat facility since February 2011.

Metallurgical Grade Alumina

Metallurgical alumina or smelter grade alumina (SGA) is an essential ingredient in the production of

aluminum; approximately two tonnes of metallurgical alumina is required to produce one tonne of

aluminum. Orbite’s aluminous clay deposit and the planned site location for its first SGA plant are

situated within 20 km of a ship loading facility situated on tidal waters and within a 70 km radius of

10 aluminum smelters in Québec (plus two more in New York State), representing an alumina market of

approximately 5.5 million tonnes, or 12% of global aluminum consumption. These smelters currently

import alumina from such distant countries as Australia, Jamaica and Brazil.

According to a Preliminary Economic Assessment (PEA) prepared by Genivar Inc. and based on the

production of alumina and hematite alone, a single Orbite planned alumina plant is estimated to have an

NPV(5%) of C$1.7 billion (versus capex of C$498.5 million), an IRR of 33%, and a payback of 3.1 years.

This is based on an annual plant capacity of 539,700 tonnes of alumina and an average cash cost of

approximately C$210 per tonne (this would put Orbite’s cash cost in the lowest quartile for global alumina

producers). Furthermore, Orbite’s process appears to be much more environmentally friendly relative to

the Bayer process, which produces a toxic red mud (for example, the failure of a tailings damn at Magyar

Aluminum in Hungary in October 2010 resulted in deaths and considerable damage to surrounding

communities). Orbite’s process does not produce red mud and it is expected that better than 90% of the

acid used in the leaching process will be recovered.

To date, two independent organizations (Norwegian-based leading independent international research

organization SINTEF and the Institute of Scientific Research - Energy, Materials and Communications)

have successfully produced aluminum from Orbite’s alumina, confirming the quality of Orbite’s

metallurgical alumina. Orbite anticipates commencing construction of its first metallurgical plant in 2012

and commencing production in late 2013.

High-Purity Grade Alumina

High-purity alumina is used in applications requiring high ductility or conductivity. These properties are

why high-purity alumina is a key ingredient in sapphire wafers and liquid-crystal polymer, which are key

components used in the production of LEDs. According to the Company, the high-purity alumina

produced from its clay at its pilot plant meets industry standards for LEDs.

24

The information contained in this report was obtained from sources we believe to be reliable. We do not represent that such information is accurate or

complete and it should not be relied on as such. Any opinions expressed herein reflect our judgment at this date and are subject to change. Jennings

Capital Inc. and/or employees from time to time may hold shares, options or warrants on any issue included in this report and may buy or sell such

securities. This report is not to be construed as an offer to sell or solicitation to buy securities. Member – CIPF. Jennings Capital (USA) Inc. is a

member of SIPC.

Orbite expects to have initial production of high-purity alumina of 1 tonne/day in Q3/12, increasing to

3 tonnes/day in Q4/12 – this equates to 350 tonnes of high-purity alumina in 2012. Using a price of

US$250/kg and a production cost of C$1,250/tonne, this production represents revenue of C$87.5 MM

and EBITDA of C$83.1 MM.

In 2010, the global market for LEDs was more than US$10 billion, and it is expected to increase by at

least a 20% CAGR between 2011 and 2015. The high-purity alumina required for the sapphire wafers is

available from only a handful of producers, and it is extremely expensive to produce using

conventional/existing technologies.

More Blue-Sky Potential

According to the PEA, a single Orbite metallurgical plant with the same annual alumina capacity, but

including the recovery of other byproducts including rare earths, is estimated to have an NPV(5%) of

$7.7 billion, an IRR of 114%, and a payback period of 11 months. The incremental cost to produce these

byproducts is estimated to be C$8.43/tonne, which yields an additional C$677/tonne in revenue.

Orbite is also conducting laboratory tests using its proprietary technology to process bauxite, and

according to the Company, the alumina extraction rate compares favourably with that of its Grande-Vallée

aluminous clay. This indicates that Orbite’s process could be used to extract alumina from bauxite and

could possibly be a viable substitute for the 124-year old Bayer process, with significant ecological

advantages.

Our 12-month target price for Orbite of C$11.50 per share is based on a blend of: (1) Our NAV(10%)

estimate of C$46.00 per fully diluted share for high-purity and metallurgical alumina, as well as all other

byproducts used in the PEA, which is risked at 30%; and (2) A 7.5x multiple applied to our FY2013 CFPS

estimate for high-purity alumina alone, which is C$1.25.

Beste Grüsse

Oberkassler

Na heute (jedenfalls im Moment) gehts ja gut noch oben...

Quote for Orbite Aluminae Inc. (ORT:CA)

$ 2,74 RT 0,24 (+9.60%) Volume: 1,68 m 13:49 EST 05.01.2012

Quote for Orbite Aluminae Inc. (ORT:CA)

$ 2,74 RT 0,24 (+9.60%) Volume: 1,68 m 13:49 EST 05.01.2012

Analysten-Bewertung - 20.12.11

Orbite Alumniae Vervielfachungspotenzial