A0HGAU | Amarillo Gold (Aktie) vor Neubewertung --- Minenbau genehmigt - 500 Beiträge pro Seite

eröffnet am 16.08.16 17:09:58 von

neuester Beitrag 20.08.20 18:04:09 von

neuester Beitrag 20.08.20 18:04:09 von

Beiträge: 114

ID: 1.236.876

ID: 1.236.876

Aufrufe heute: 0

Gesamt: 7.428

Gesamt: 7.428

Aktive User: 0

ISIN: CA02301T1084 · WKN: A0HGAU

0,4350

CAD

+2,35 %

+0,0100 CAD

Letzter Kurs 29.03.22 TSX Venture

http://www.stockhouse.com/news/newswire/2016/08/09/why-amari…

However, Amarillo Gold Corp. (TSX.V: AGC) is an obvious exception.

This low-profile, thinly-traded company was recently issued a preliminary permit to build a gold mine in Brazil. And not a moment too soon. After all, it endured a four-year wait before getting this crucial nod of approval from government regulators.

But timing is everything in the business world.

So Amarillo is finally poised to capitalize on a resurgent gold market in the most meaningful way—by inexpensively mining and selling upwards of 1.2 million ounces of gold.

Read more at http://www.stockhouse.com/news/newswire/2016/08/09/why-amari…

However, Amarillo Gold Corp. (TSX.V: AGC) is an obvious exception.

This low-profile, thinly-traded company was recently issued a preliminary permit to build a gold mine in Brazil. And not a moment too soon. After all, it endured a four-year wait before getting this crucial nod of approval from government regulators.

But timing is everything in the business world.

So Amarillo is finally poised to capitalize on a resurgent gold market in the most meaningful way—by inexpensively mining and selling upwards of 1.2 million ounces of gold.

Read more at http://www.stockhouse.com/news/newswire/2016/08/09/why-amari…

Jul 21, 2016 (TheNewswire.ca via COMTEX) -- (via Thenewswire.ca)

TheNewswire / July 21, 2016 - Amarillo Gold Corp. (AGC) ("Amarillo") is pleased to announce that it has received a new resource model for the Posse deposit, Mara Rosa project, Goias, Brazil. Keith Whitehouse, the principal of Australian Exploration Field Services Ltd, ("AEFS") calculated the new resource estimate at a 0.5 g/t cutoff as listed below in Table 1. Table 2 lists the previous estimate (2011), also at a 0.5 g/t cutoff. A positive Preliminary Feasibility Study ("PFS", Jan 2012), was based on the 2011 resource. This gave reasonable expectations the deposit could be economically mined using an open pit based on a $US1100 per ounce gold price. Since this time, the resource has improved (reported here), as has the gold price. Exchange rates are more favorable, and the company has recently obtained the LP (Preliminary License, conditional acceptance of the project by the state environmental authority, see NR dated May 9th).

http://www.marketwatch.com/story/amarillo-gold-provides-new-…

TheNewswire / July 21, 2016 - Amarillo Gold Corp. (AGC) ("Amarillo") is pleased to announce that it has received a new resource model for the Posse deposit, Mara Rosa project, Goias, Brazil. Keith Whitehouse, the principal of Australian Exploration Field Services Ltd, ("AEFS") calculated the new resource estimate at a 0.5 g/t cutoff as listed below in Table 1. Table 2 lists the previous estimate (2011), also at a 0.5 g/t cutoff. A positive Preliminary Feasibility Study ("PFS", Jan 2012), was based on the 2011 resource. This gave reasonable expectations the deposit could be economically mined using an open pit based on a $US1100 per ounce gold price. Since this time, the resource has improved (reported here), as has the gold price. Exchange rates are more favorable, and the company has recently obtained the LP (Preliminary License, conditional acceptance of the project by the state environmental authority, see NR dated May 9th).

http://www.marketwatch.com/story/amarillo-gold-provides-new-…

Keiner mehr dabei? Bin heute eingestiegen - wie wär's,

wenn wir den thread reaktivieren?

wenn wir den thread reaktivieren?

lesezeichen

Bin auch hier seit gestern dabei: Einstiegskurs C$ 0,39

Trading Spotlight

aha ein thread...

denke an einen einstieg.

was ich nicht ganz gecheckt hab bei der PFS:

"Total gold recovered over LOM is 892,000 ounces- after considering dilution 3% and plant recovery 92%;"

P&P reserven

997,563 ozs

M&I resourcen

1,210,100 ozs

die P&P´s genommen 92% recovery und 3% dilution.

dann käme ich auf grob 891,000 unzen als grob auf das entnommene gold was angegeben wird.

heisst das, daß die M&I unzen noch gar nicht enthalten sind ?

(oder sind bzgl M&I davon inzwischen in die kategorie P&P gehoben worden ?)

also 2,1 Mios unzen summe in der studie nur der P&P-anteil ?

irgendwie peil ich´s grad nicht so ganz.

denke an einen einstieg.

was ich nicht ganz gecheckt hab bei der PFS:

"Total gold recovered over LOM is 892,000 ounces- after considering dilution 3% and plant recovery 92%;"

P&P reserven

997,563 ozs

M&I resourcen

1,210,100 ozs

die P&P´s genommen 92% recovery und 3% dilution.

dann käme ich auf grob 891,000 unzen als grob auf das entnommene gold was angegeben wird.

heisst das, daß die M&I unzen noch gar nicht enthalten sind ?

(oder sind bzgl M&I davon inzwischen in die kategorie P&P gehoben worden ?)

also 2,1 Mios unzen summe in der studie nur der P&P-anteil ?

irgendwie peil ich´s grad nicht so ganz.

Antwort auf Beitrag Nr.: 54.563.365 von Boersiback am 18.03.17 20:27:04Ne also ich bin bisher davon ausgegangen das p&p NUR ins Spiel kommt sobald eine pfs oder fs vorliegt.

P&p ist stets der Teil von m&i der wirtschaftlich abbaubar ist.

Ja irgendwie sind die Zahlen sonderbar. Wie man da auf die 982k kommt ist mir auch bisl schleierhaft.

P&p ist stets der Teil von m&i der wirtschaftlich abbaubar ist.

Ja irgendwie sind die Zahlen sonderbar. Wie man da auf die 982k kommt ist mir auch bisl schleierhaft.

Antwort auf Beitrag Nr.: 54.563.515 von sir_krisowaritschko am 18.03.17 21:09:02eben ist ja eine PFS und auch ok:

passt schon mit den 892K wenn ich die PP nehme in etwa:

997,563 ozs * 0,92 (recovered gold) = 917,758 ozs

917,758 ozs * 0,03 (dilution) = 890,225 ozs

sie schreiben 892,000 ozs (bei dilution 2,8% statt 3% käm ich auf 892,061)

also das passt schon so... auf die 2000 oder ob sie mit 2,8% rechnen und 3% gerundet sind ist dann auch schnurz

ich bin es eigentlich sogewohnt dass P&P und M&I und inferred als summe

die reserven und resourcen angeben.

die frage ist wirklich nur eine eigentlich:

ist P&P ein anteil aus M&I oder wirklich separat ?

dann wärens ja üer 2 Mios unzen

oder ist das einfach die M&I angabe aus denen inzwischen einiges in P&P

upgegradet wurde... also was haben sie ohne inferred ?

1,2 Mios unzen von denen knapp 1 Mio P&P ist

oder

1 Mio P&P PLUS 1,2 Mios M&I

passt schon mit den 892K wenn ich die PP nehme in etwa:

997,563 ozs * 0,92 (recovered gold) = 917,758 ozs

917,758 ozs * 0,03 (dilution) = 890,225 ozs

sie schreiben 892,000 ozs (bei dilution 2,8% statt 3% käm ich auf 892,061)

also das passt schon so... auf die 2000 oder ob sie mit 2,8% rechnen und 3% gerundet sind ist dann auch schnurz

ich bin es eigentlich sogewohnt dass P&P und M&I und inferred als summe

die reserven und resourcen angeben.

die frage ist wirklich nur eine eigentlich:

ist P&P ein anteil aus M&I oder wirklich separat ?

dann wärens ja üer 2 Mios unzen

oder ist das einfach die M&I angabe aus denen inzwischen einiges in P&P

upgegradet wurde... also was haben sie ohne inferred ?

1,2 Mios unzen von denen knapp 1 Mio P&P ist

oder

1 Mio P&P PLUS 1,2 Mios M&I

Antwort auf Beitrag Nr.: 54.563.560 von Boersiback am 18.03.17 21:26:061,2 Mios unzen von denen knapp 1 Mio P&P ist

___________________________________________________

Exakt!

___________________________________________________

Exakt!

Antwort auf Beitrag Nr.: 54.563.596 von sir_krisowaritschko am 18.03.17 21:38:29ja, so ist es wohl frag mich warum sie die P&P noch in den M&I mitdrin haben

im sinne von M&I und davon P&P... naja P&P sind ja nicht mehr M&I

dachte anfangs M&I noch komplett dazu... naja das wär en ding gewesen..

im sinne von M&I und davon P&P... naja P&P sind ja nicht mehr M&I

dachte anfangs M&I noch komplett dazu... naja das wär en ding gewesen..

Antwort auf Beitrag Nr.: 54.563.653 von Boersiback am 18.03.17 22:06:02Naja weil für die p&p-Berechnung stets ein losgelöstes Modell erstellt wird was nix mit dem ökonomischen Modell zu tun hat.

Für die Berechnung der Reserven wird ein Preis x angesetzt unter derem dann die ökonomische grubenform errechnet wird. Je geringer der Goldpreis desto geringer fällt dann die Reserve aus. Umgekehrt bei steigendem pog.

Die m&i stellt in diesem Kontext die absolute Obergrenze dar die innerhalb der Studie rein theoretisch technisch abbaubar ist. Also faktisch könnte agc bei entsprechend hohem pog 1,2mio Oz fördern. Wobei dann immer noch der relativ hohe Unsicherheitsfaktor der Kategorie indicated mit hineinspielt.

Sorry besser kann ich es nicht erklären. Hoffe es ist verständlich?

Für die Berechnung der Reserven wird ein Preis x angesetzt unter derem dann die ökonomische grubenform errechnet wird. Je geringer der Goldpreis desto geringer fällt dann die Reserve aus. Umgekehrt bei steigendem pog.

Die m&i stellt in diesem Kontext die absolute Obergrenze dar die innerhalb der Studie rein theoretisch technisch abbaubar ist. Also faktisch könnte agc bei entsprechend hohem pog 1,2mio Oz fördern. Wobei dann immer noch der relativ hohe Unsicherheitsfaktor der Kategorie indicated mit hineinspielt.

Sorry besser kann ich es nicht erklären. Hoffe es ist verständlich?

Antwort auf Beitrag Nr.: 54.563.758 von sir_krisowaritschko am 18.03.17 22:38:03ja ist eigentlich schon üblich... weiss nicht was mich da geritten hat.

die M&I angaben sind doch meistens komplett und davon entnommen P&P dann eben ja nach cut-off-grade was dann wirklich brauchbar ist.

man kann natürlich den P&P-anteil aus den M&I angaben abziehen besipielsweise M&I 5 Mios unzen davon 2 Mios P&P mit cut-off dass es nur noch 1,7 sind und M&I mit 3 mios übrigem material angeben.

aber normalerweise ist´s schon wie du schreibst... steht nur oft dabei als vermerk dass diese enthalten sind.

die M&I angaben sind doch meistens komplett und davon entnommen P&P dann eben ja nach cut-off-grade was dann wirklich brauchbar ist.

man kann natürlich den P&P-anteil aus den M&I angaben abziehen besipielsweise M&I 5 Mios unzen davon 2 Mios P&P mit cut-off dass es nur noch 1,7 sind und M&I mit 3 mios übrigem material angeben.

aber normalerweise ist´s schon wie du schreibst... steht nur oft dabei als vermerk dass diese enthalten sind.

Updated PFS Released, Amarillo’s Mara Rosa Is Now A Top Acquisition Target – (CVE:AGC, FRA:72A, OTCMKTS:AGCBF)

Amarillo’s updated PFS propels its flagship project, Mara Rosa, into the top percentile in terms of IRR in its comp group.

The PFS indicates that the Mara Rosa project will be a single open-pit mining operation with a rapid payback of 2 years, and robust economics, many of which were improved upon since the 2011 PFS. Some key economic metrics improve include: currency devaluation from 1.9 to 3.2 USD/BRL; reduced strip ratios from 8.2:1 to 4.5:1; low-grade stockpiling; optimized pit scheduling, and increased gold reserves from 945,000 to 997,563 ounces.

http://palisade-research.com/want-exposure-to-gold-robust-ec…

http://palisade-research.com/want-exposure-to-gold-robust-economics-near-term-production-an-acquisition-target-and-exploration-upside-and-cheap-amarillo-gold-corp-cveagc-fra72a-otcmktsagcbf/

DISCLAIMER!!!

Palisade Global Investments Limited holds shares of Amarillo Gold. We receive either monetary or securities compensation for our services. We stand to benefit from any volume this write-up may generate. The information contained in such write-ups is not intended as individual investment advice and is not designed to meet your personal financial situation. Information contained in this report is obtained from sources we believe to be reliable, but its accuracy cannot be guaranteed. The opinions expressed in this report are those of Palisade Global Investments and are subject to change without notice. The information in this report may become outdated and there is no obligation to update any such information. Do your own due diligence.

Hm... sind die Schreiberlinge von Palisade gut oder schlecht? Da scheiden sich die Geister!

Für mich stets erstmal indiz dafür, dass man eventuell Volumen erzeugt um sich von einigen Aktien trennen zu können. Mal abwarten was das für den Kurs in den nächsten Tagen bedeutet.

Amarillo’s updated PFS propels its flagship project, Mara Rosa, into the top percentile in terms of IRR in its comp group.

The PFS indicates that the Mara Rosa project will be a single open-pit mining operation with a rapid payback of 2 years, and robust economics, many of which were improved upon since the 2011 PFS. Some key economic metrics improve include: currency devaluation from 1.9 to 3.2 USD/BRL; reduced strip ratios from 8.2:1 to 4.5:1; low-grade stockpiling; optimized pit scheduling, and increased gold reserves from 945,000 to 997,563 ounces.

Dieses Bild ist nicht SSL-verschlüsselt: [url]http://palisade-research.com/wp-content/uploads/2017/03/1-2.png

[/url]http://palisade-research.com/want-exposure-to-gold-robust-ec…

http://palisade-research.com/want-exposure-to-gold-robust-economics-near-term-production-an-acquisition-target-and-exploration-upside-and-cheap-amarillo-gold-corp-cveagc-fra72a-otcmktsagcbf/

DISCLAIMER!!!

Palisade Global Investments Limited holds shares of Amarillo Gold. We receive either monetary or securities compensation for our services. We stand to benefit from any volume this write-up may generate. The information contained in such write-ups is not intended as individual investment advice and is not designed to meet your personal financial situation. Information contained in this report is obtained from sources we believe to be reliable, but its accuracy cannot be guaranteed. The opinions expressed in this report are those of Palisade Global Investments and are subject to change without notice. The information in this report may become outdated and there is no obligation to update any such information. Do your own due diligence.

Hm... sind die Schreiberlinge von Palisade gut oder schlecht? Da scheiden sich die Geister!

Für mich stets erstmal indiz dafür, dass man eventuell Volumen erzeugt um sich von einigen Aktien trennen zu können. Mal abwarten was das für den Kurs in den nächsten Tagen bedeutet.

Antwort auf Beitrag Nr.: 54.570.645 von sir_krisowaritschko am 20.03.17 13:52:28hab sie noch nicht... aber eigentlich schreiben sie auch nur was ersichtlich ist.

Amarillo müßte eigentlich vergleichsweise eher bei 60-70 Mios CAD stehen als bei 30 Mios.

woran liegts ? brasilienabschlag ? kein großes explorationspotenzial bei dieser mine ?

(dafür bei einem zweiten projekt)

Amarillo müßte eigentlich vergleichsweise eher bei 60-70 Mios CAD stehen als bei 30 Mios.

woran liegts ? brasilienabschlag ? kein großes explorationspotenzial bei dieser mine ?

(dafür bei einem zweiten projekt)

Antwort auf Beitrag Nr.: 54.574.794 von Boersiback am 20.03.17 22:06:11tja, weiß ich eherlich gesagt auch nicht. hätte mir jetzt auch mehr versprochen.

manch eine bude zuckt halt irgendwann verzögert. ATM hatte auch einen krassen sprung hingelegt. da war ich, genau wie hier, zu früh beim kaufen

naja mal abwarten. bei solitario wars auch ein ewiges hin und hergekrebse. wollte da schon die tage den sell button drücken. hab es dann doch gelassen weil ich die kohle nich zwangsläufig gebraucht hätte. heute sind se mal nach oben hin bisl weggekommen. ich gebe agc auch ne kleine chance.

manch eine bude zuckt halt irgendwann verzögert. ATM hatte auch einen krassen sprung hingelegt. da war ich, genau wie hier, zu früh beim kaufen

naja mal abwarten. bei solitario wars auch ein ewiges hin und hergekrebse. wollte da schon die tage den sell button drücken. hab es dann doch gelassen weil ich die kohle nich zwangsläufig gebraucht hätte. heute sind se mal nach oben hin bisl weggekommen. ich gebe agc auch ne kleine chance.

Antwort auf Beitrag Nr.: 54.574.839 von sir_krisowaritschko am 20.03.17 22:12:58passt doch, chart ist ok.. dass die studie nicht mehr beachtung fand ist schade.

naja ok sie ist halt so wie damals im groben (was ich recht gut finde, fand sie schon damals sehr gut).

währung kosten ua sind ja deutlich anders. das eine gleicht das andere dann wieder aus und zeigt eigentlich ein recht solides und robustes projekt.

denke viel schiefgehen wird da nicht mit dem kurs. schlimmstenfalls tut sich nicht viel.

naja ok sie ist halt so wie damals im groben (was ich recht gut finde, fand sie schon damals sehr gut).

währung kosten ua sind ja deutlich anders. das eine gleicht das andere dann wieder aus und zeigt eigentlich ein recht solides und robustes projekt.

denke viel schiefgehen wird da nicht mit dem kurs. schlimmstenfalls tut sich nicht viel.

Antwort auf Beitrag Nr.: 54.574.794 von Boersiback am 20.03.17 22:06:11

doch doch... explopotenzial gibts en mass. mal gucken ob se doch nochmal nen dickes programm aufsetzen um die resource zu erweitern.

Exploration Plans and Rationale

The Company believes that there is good potential for the discovery of additional mineralization within the Mara Rosa project. Such discovery can come from two possible sources: Posse Deposit look-alikes along the same structure, and new gold mineralization away from Posse.

The Posse Deposit is remarkable in that it occurs within a 50 km regional structure that can be traced in the airborne geophysical data (radiometric K channel). This structure has also been mapped by soil sampling for over 10 km as demonstrated by the coincident >0.2 g/t Au anomaly. Mapping along this structure suggests that a friable quartz mica (muscovite and sericite) schist is the likely source of the radiometric anomaly. However, the Posse Deposit is an unremarkable feature along this structure; there are few clues in the geochemical and geophysical data set that would highlight it.

http://www.amarillogold.com/projects/mara-rosa

http://www.amarillogold.com/projects/mara-rosa

Zitat von Boersiback: kein großes explorationspotenzial bei dieser mine ?

(dafür bei einem zweiten projekt)

doch doch... explopotenzial gibts en mass. mal gucken ob se doch nochmal nen dickes programm aufsetzen um die resource zu erweitern.

Exploration Plans and Rationale

The Company believes that there is good potential for the discovery of additional mineralization within the Mara Rosa project. Such discovery can come from two possible sources: Posse Deposit look-alikes along the same structure, and new gold mineralization away from Posse.

The Posse Deposit is remarkable in that it occurs within a 50 km regional structure that can be traced in the airborne geophysical data (radiometric K channel). This structure has also been mapped by soil sampling for over 10 km as demonstrated by the coincident >0.2 g/t Au anomaly. Mapping along this structure suggests that a friable quartz mica (muscovite and sericite) schist is the likely source of the radiometric anomaly. However, the Posse Deposit is an unremarkable feature along this structure; there are few clues in the geochemical and geophysical data set that would highlight it.

Dieses Bild ist nicht SSL-verschlüsselt: [url]http://www.amarillogold.com/sites/default/files/projects/mararosa-fig3colouredgridsoildata.jpg

[/url]http://www.amarillogold.com/projects/mara-rosa

http://www.amarillogold.com/projects/mara-rosa

Antwort auf Beitrag Nr.: 54.575.088 von sir_krisowaritschko am 20.03.17 22:59:27ach ok, da sogar auch...

dachte nur an Lavras (120 meter 3,23 g/t)

sieht ja auch vielversprechend aus..

also schon extrem billig der wert.

stört den markt die starke abwertung des Real die er nicht für nachhaltig hält ?

dann wären die kosten aber dafür geringer, wenn´s anders wäre

die eckdaten sind sehr verschieden gegenüber der alten PFS.

das ergebnis ist aber sehr ähnlich und macht auch sinn so...

durchaus unter verschiedenen szenarien als robust zu sehen

also weiss nicht warum die nicht bei etwa 60-70 Mios CAD liegen.

ABER !!!

was gibts zu meckern ???

alle goldindizes abgehängt deutlich

von daher durchaus perfekt:

billig und klarer outperformer

...oder was wünscht man sich.... genau das !

dachte nur an Lavras (120 meter 3,23 g/t)

sieht ja auch vielversprechend aus..

also schon extrem billig der wert.

stört den markt die starke abwertung des Real die er nicht für nachhaltig hält ?

dann wären die kosten aber dafür geringer, wenn´s anders wäre

die eckdaten sind sehr verschieden gegenüber der alten PFS.

das ergebnis ist aber sehr ähnlich und macht auch sinn so...

durchaus unter verschiedenen szenarien als robust zu sehen

also weiss nicht warum die nicht bei etwa 60-70 Mios CAD liegen.

ABER !!!

Dieses Bild ist nicht SSL-verschlüsselt: [url]http://bigcharts.marketwatch.com/kaavio.Webhost/charts/big.chart?nosettings=1&symb=ca%3aagc&uf=0&type=2&size=2&sid=8110381&style=320&freq=1&entitlementtoken=0c33378313484ba9b46b8e24ded87dd6&time=10&rand=1321310322&compidx=aaaaa%3a0&comp=GDX%2c+GDXJ%2c+HUI%2c+XAU&ma=0&maval=9&lf=1&lf2=0&lf3=0&height=335&width=579&mocktick=1

[/url]was gibts zu meckern ???

alle goldindizes abgehängt deutlich

von daher durchaus perfekt:

billig und klarer outperformer

...oder was wünscht man sich.... genau das !

Antwort auf Beitrag Nr.: 54.575.187 von Boersiback am 20.03.17 23:30:13Ja denke auch das der Real nicht nachhaltig auf dem Niveau verharren wird.

Aber hattest ja fein aufgezeigt dass bei einer Abwertung dementsprechend die Kostenseite profitiert.

Charttechnisch bilde ich mir da schon einen Seitwärtskanal ein. In meiner Vorstellung vielleicht ein möhliches Sprungbrett nach oben.

Aber hattest ja fein aufgezeigt dass bei einer Abwertung dementsprechend die Kostenseite profitiert.

Charttechnisch bilde ich mir da schon einen Seitwärtskanal ein. In meiner Vorstellung vielleicht ein möhliches Sprungbrett nach oben.

Antwort auf Beitrag Nr.: 54.575.220 von sir_krisowaritschko am 20.03.17 23:40:36sieht recht bullish aus vom chart her... recht neutral aber in richtung der spitze früher oder später.

noch ist er ruhig...

noch ist er ruhig...

...bin seit eben auch stolzer besitzer dies kostbaren papiere nun...

0,39 CAD

0,39 CAD

Antwort auf Beitrag Nr.: 54.570.645 von sir_krisowaritschko am 20.03.17 13:52:28

Meine Befürchtung scheint sich zu bestätigen.

Hätte ich mal bisl intensiver die Pushberichte gelesen.

Auch in diesem Fall ein klarer Kontraindikator. Tja selber schuld.

Hinzukommt der POG. Der scheint erneut an der 1250 zu scheitern.

Zitat von sir_krisowaritschko:[/url]Dieses Bild ist nicht SSL-verschlüsselt: [url]http://palisade-research.com/wp-content/uploads/2017/03/1-2.png

http://palisade-research.com/want-exposure-to-gold-robust-ec…

http://palisade-research.com/want-exposure-to-gold-robust-economics-near-term-production-an-acquisition-target-and-exploration-upside-and-cheap-amarillo-gold-corp-cveagc-fra72a-otcmktsagcbf/

DISCLAIMER!!!

Palisade Global Investments Limited holds shares of Amarillo Gold. We receive either monetary or securities compensation for our services. We stand to benefit from any volume this write-up may generate. The information contained in such write-ups is not intended as individual investment advice and is not designed to meet your personal financial situation. Information contained in this report is obtained from sources we believe to be reliable, but its accuracy cannot be guaranteed. The opinions expressed in this report are those of Palisade Global Investments and are subject to change without notice. The information in this report may become outdated and there is no obligation to update any such information. Do your own due diligence.

Hm... sind die Schreiberlinge von Palisade gut oder schlecht? Da scheiden sich die Geister!

Für mich stets erstmal indiz dafür, dass man eventuell Volumen erzeugt um sich von einigen Aktien trennen zu können. Mal abwarten was das für den Kurs in den nächsten Tagen bedeutet.

Meine Befürchtung scheint sich zu bestätigen.

Hätte ich mal bisl intensiver die Pushberichte gelesen.

Auch in diesem Fall ein klarer Kontraindikator. Tja selber schuld.

Hinzukommt der POG. Der scheint erneut an der 1250 zu scheitern.

Dieses Bild ist nicht SSL-verschlüsselt: [url]http://palisade-research.com/wp-content/uploads/2017/03/1-2.png

[/url]

Antwort auf Beitrag Nr.: 54.601.176 von sir_krisowaritschko am 23.03.17 21:09:56wir sind halt im dreieck beim gold....

Amarillo hat eigentlich nen guten chart aber mag sein dass nachdem die katze aus dem sack ist, der wert langweilig wird für den markt.

der haken ist natürlich dass sie die grob 200 Mios CAD für die mine nicht stemmen können.

im vergleich dazu ist Treasury mit einer marktkap von 80 Mios CAD bei benötigten 130 Mios CAD glaub absolut eher in der lage. die bewertung bei amarillo ist eklatant tief. ich glaube nicht dass sie stark fällt. evtl. aber auch so gut wie gar nicht performt auf längere sicht.

naja war halt mal ein valuekauf ohne jegliches momentum.

Amarillo hat eigentlich nen guten chart aber mag sein dass nachdem die katze aus dem sack ist, der wert langweilig wird für den markt.

der haken ist natürlich dass sie die grob 200 Mios CAD für die mine nicht stemmen können.

im vergleich dazu ist Treasury mit einer marktkap von 80 Mios CAD bei benötigten 130 Mios CAD glaub absolut eher in der lage. die bewertung bei amarillo ist eklatant tief. ich glaube nicht dass sie stark fällt. evtl. aber auch so gut wie gar nicht performt auf längere sicht.

naja war halt mal ein valuekauf ohne jegliches momentum.

Lesezeichen

She's alive

Da muß wohl irgendjemand eine Empfehlung ausgesprochen haben.

Antwort auf Beitrag Nr.: 54.621.338 von Fantomas96 am 27.03.17 17:24:07kann natürlich sein dass es nur ein pusch war...

ich les ja sowas nicht mehr und kriegs auch nicht mit.

trotzdem lief sie ja gut über die letzten jahre und ist extrem billig vergleichsweise.

ich les ja sowas nicht mehr und kriegs auch nicht mit.

trotzdem lief sie ja gut über die letzten jahre und ist extrem billig vergleichsweise.

Antwort auf Beitrag Nr.: 54.621.338 von Fantomas96 am 27.03.17 17:24:07Vielleicht lag es auch einfach nur am starken PoG beim Handelsstart?

Der gibt nun nach und AGC offenbar dementsprechend auch.

Der gibt nun nach und AGC offenbar dementsprechend auch.

dank palisade darf man sich hier getrost mit großem abstand ins stinky bid legen.

naja kann auch gaanz wer anderes sein, aber wundern würde es mich nich.

naja kann auch gaanz wer anderes sein, aber wundern würde es mich nich.

Amarillo Files Updated Pre-Feasibility Report, Mara Rosa Project

Amarillo Gold Corp.

VANCOUVER, BRITISH COLUMBIA--(Marketwired - April 28, 2017) - Amarillo Gold Corp. (TSX VENTURE:AGC) ("Amarillo" or the "Company"), is pleased to announce that it has filed the updated Pre-feasibility ("PFS" or "Study") report for the Posse gold deposit within its 100% owned Mara Rosa project (the "Project"), Goias, Brazil on SEDAR.

Highlights:

Post-tax internal rate of return (IRR) of 35.2%, post-tax net present value (NPV5) of US$178M, and post-tax project payback of 2.2 years based on a gold price of US$1,200 per troy ounce and a USD/BRL exchange rate of 3.20

Average annual gold production estimated at 140,000 ounces over first 4 years, average life of mine (LOM) production 112,000 ounces per year over 8 years, and total production of 892,000 ounces

LOM cash operating cost of US$545/oz Au, and all-in sustaining costs (AISC) of US$627/oz Au*

The updated PFS provides an ore reserves statement of 9.27MT Proven, @ 1.81 g/t Au, 540,567 troy ounces and 9.74MT Probable @ 1.46 g/t Au, 456,968 troy ounces at a 0.38 g/t cut-off, for total reserves of 19.01 MT @ 1.63 g/t Au, 997,536 troy ounces of Proven plus Probable that fall within the open pit design based on $US1200/ounce gold price

http://www.minenportal.de/artikel.php?sid=199345&lang=en#Ama…

Amarillo Gold Corp.

VANCOUVER, BRITISH COLUMBIA--(Marketwired - April 28, 2017) - Amarillo Gold Corp. (TSX VENTURE:AGC) ("Amarillo" or the "Company"), is pleased to announce that it has filed the updated Pre-feasibility ("PFS" or "Study") report for the Posse gold deposit within its 100% owned Mara Rosa project (the "Project"), Goias, Brazil on SEDAR.

Highlights:

Post-tax internal rate of return (IRR) of 35.2%, post-tax net present value (NPV5) of US$178M, and post-tax project payback of 2.2 years based on a gold price of US$1,200 per troy ounce and a USD/BRL exchange rate of 3.20

Average annual gold production estimated at 140,000 ounces over first 4 years, average life of mine (LOM) production 112,000 ounces per year over 8 years, and total production of 892,000 ounces

LOM cash operating cost of US$545/oz Au, and all-in sustaining costs (AISC) of US$627/oz Au*

The updated PFS provides an ore reserves statement of 9.27MT Proven, @ 1.81 g/t Au, 540,567 troy ounces and 9.74MT Probable @ 1.46 g/t Au, 456,968 troy ounces at a 0.38 g/t cut-off, for total reserves of 19.01 MT @ 1.63 g/t Au, 997,536 troy ounces of Proven plus Probable that fall within the open pit design based on $US1200/ounce gold price

http://www.minenportal.de/artikel.php?sid=199345&lang=en#Ama…

HAMMERARTIKEL über Amarillo !!!!!

!!!!!

Amarillo Gold flexes — and becomes an M&A target

Marc Davis 4 days ago @SH

It promises to be one of the world’s lowest-cost gold mines.

So suggests an updated pre-feasibility study (an initial blueprint for a mine) for the Mara Rosa gold deposit in Goias State in central Brazil.

The study’s findings were just announced by the deposit’s owner, Amarillo Gold Corp. (TSX.V: AGC) with its filing of the pre-feasibilty report on SEDAR.

All told, the production profile metrics suggest that Mara Rosa has what it takes to be a profitable mine that is inexpensive to build and relatively cheap to run.

Most notably, the one-million-ounce, near-surface deposit is shown to be capable of yielding around 112,000 ounces per annum for at least eight years. And it can be mined by open-pit extraction (a simple, quarry-like operation).

Accordingly, all of this can be done for as little as US $627/oz in “All-in sustaining costs” (total production costs).

By comparison, most of the world’s gold mines cost upwards of $870 oz/ton to operate in 2016, according to RBC Capital Markets. Such a scenario can make for perilously thin profit margins.

In comparison, Mara Rosa promises to be one of the world’s lowest-cost gold mining operations. And this promises to buffer the company’s profits from fluctuations in the price of bullion. It also represents a major differentiator for Amarillo Gold.

It also virtually assures Amarillo a fast payback on invested capital (only 2.2 years based on $1,200 oz/gold), as well as the prospect of a steady stream of robust earnings.

M&A activity in the sector is heating up. And the low cost metrics at Mara Rosa establishes establish Amarillo as a likely takeover candidate for several well-established, supply-hungry gold producers that are active in the same region of Brazil.... .

Why Mara Rosa is Low-Hanging Fruit for M&A Suitors

With the likelihood of becoming Brazil’s next gold mine, Amarillo represents one of the ripest plums among the ranks of aspiring gold miners.

In fact, the Mara Rosa deposit has all the right characteristics and operational logistics to become a lucrative gold mine, which is a considerable rarity these days.

The story gets better. The deposit is located in a mining-friendly jurisdiction where there's plenty of other regional infrastructure in place to support a new mine.

This includes a hydroelectric power grid, a railway within 1.5 km of the deposit, a national highway only 11 kilometres away and a town of 12,000 people (which is also called Mara Rosa) about 5 kilometres away.

All of this promises to minimize projected “Capex” (mine construction) costs, as well as operational expenditures.

Mara Rosa's appeal to prospective suitors is further sweetened by the fact that it is located in a well-established mining district. In fact, there are several proximal mines, including Yamana Gold Inc.'s Chapada mine (35 kilometers away).

By way of explanation, the world’s dominant gold miners are doing all they can to significantly reduce their capital and operating costs just to stay in business. And the key to doing this is to acquire new gold assets that are complementary to their existing mines.

In other words, any proximal gold assets worth acquiring need to be both cheap and relatively fast to commercialize.

Mara Rosa measures up nicely in this regard.

It would therefore make economic sense for one of the region's big gold producers – namely Kinross Gold Corp., AngloGold Ashanti Ltd. or Yamana Gold – to eventually gobble up Amarillo. At least, this is the buzz among some of the industry experts who are following Amarillo’s emerging story.

In fact, the prospect of a rapid after-tax payback period of only 2.2 years should make Mara Rosa all the more appealing. This is because today’s gold miners are keener than ever to quickly recover any outlays of Capex expenditures.

It also bears mentioning that the up-front Capex costs of building a mine at Mara Rosa are relatively cheap by industry standards. At only around US $148 million, this adds to Mara Rosa’s appeal as a low-risk acquisition target.

Furthermore, the presence of shallow mineralization at Mara Rosa offers a favourably very low stripping ratio (the ratio of waste rock to ore), which makes for significant operational cost savings, too.

Other Key Value Drivers

Here’s something that’s been mostly overlooked by the investment community in the wake of this updated pre-feasibility study: Amarillo has made significant headway in recent months with its mine permitting process.

More specifically, the company has been issued a preliminary permit to build a gold mine -- something that represents another major de-risking event. This permit essentially represents both social and environmental acceptance of the mine proposal in Goias State, and also outlines a clear road map for obtaining final approval to commercialize Mara Rosa.

In other words, the company just has to complete the milestones laid out in the preliminary permit to receive this permission. Key components of this work will be the completion of the full feasibility study, detailed plans for the tailings facility, and the finalization of agreements to acquire surface rights. This is all expected to be achieved within the next 12 months

The company now has to demonstrate to the state government that it can operate a successful mining operation, without posing any threat to the local environment. This is expected to be achieved by way of the company completing a full bankable feasibility study (a final blueprint for a mine) within the next 12 months.

Assuming it gets the final go-ahead, the mine promises to generate in excess of US $1 billion in gross revenues, of which about $300 million will be paid directly in federal and state taxes, with further taxes to be paid in payroll and value added tax (VAT). There will also be a 1% production royalty to be paid to the government.

The benefits to the community in the town of Mara Rosa and the surrounding district should be numerous and would include approximately 300 permanent jobs in the local community, as well as many more spin-off employment opportunities.

Investment Summary

On a technical note, the company has about 80.25 million shares outstanding (86.98 million fully diluted) of which about 40% is institutionally held and around 15% is owned by management and the board of directors.

The company recently completed a $3.3 million private placement by issuing 1.3 million shares at $0.32 per share without a warrant.

At under $0.50 a share, the company is trading at a discount to its peers -- companies with comparably-sized projects, and at a similar stages of development. In this regard, Amarillo is trading at around 0.16 X net asset value (NAV) versus a peer average of 0.4 X NAV.

The granting of a preliminary mining license, as well as the demonstration of very robust project logistics at Mara Rosa, are crucial value drivers that have set Amarillo on course for a very bright future.

Ultimately, Amarillo is well-positioned to capitalize on a resurgent gold market in the most meaningful way -- by inexpensively mining up to one million ounces of gold over a mine life of at least eight years.

With such low Capex and production costs, Mara Rosa promises to be one of the world’s most lucrative modestly-sized gold mines. This competitive advantage will therefore make Amarillo an attractive takeover candidate during the balance of 2017 and beyond.

In closing, the company’s enterprise value is well deserving of a positive re-rating by the investment industry. In turn, this should help power an ascendant share price that is destined to go from strength to strength.

!!!!!

!!!!! Amarillo Gold flexes — and becomes an M&A target

Marc Davis 4 days ago @SH

It promises to be one of the world’s lowest-cost gold mines.

So suggests an updated pre-feasibility study (an initial blueprint for a mine) for the Mara Rosa gold deposit in Goias State in central Brazil.

The study’s findings were just announced by the deposit’s owner, Amarillo Gold Corp. (TSX.V: AGC) with its filing of the pre-feasibilty report on SEDAR.

All told, the production profile metrics suggest that Mara Rosa has what it takes to be a profitable mine that is inexpensive to build and relatively cheap to run.

Most notably, the one-million-ounce, near-surface deposit is shown to be capable of yielding around 112,000 ounces per annum for at least eight years. And it can be mined by open-pit extraction (a simple, quarry-like operation).

Accordingly, all of this can be done for as little as US $627/oz in “All-in sustaining costs” (total production costs).

By comparison, most of the world’s gold mines cost upwards of $870 oz/ton to operate in 2016, according to RBC Capital Markets. Such a scenario can make for perilously thin profit margins.

In comparison, Mara Rosa promises to be one of the world’s lowest-cost gold mining operations. And this promises to buffer the company’s profits from fluctuations in the price of bullion. It also represents a major differentiator for Amarillo Gold.

It also virtually assures Amarillo a fast payback on invested capital (only 2.2 years based on $1,200 oz/gold), as well as the prospect of a steady stream of robust earnings.

M&A activity in the sector is heating up. And the low cost metrics at Mara Rosa establishes establish Amarillo as a likely takeover candidate for several well-established, supply-hungry gold producers that are active in the same region of Brazil.... .

Why Mara Rosa is Low-Hanging Fruit for M&A Suitors

With the likelihood of becoming Brazil’s next gold mine, Amarillo represents one of the ripest plums among the ranks of aspiring gold miners.

In fact, the Mara Rosa deposit has all the right characteristics and operational logistics to become a lucrative gold mine, which is a considerable rarity these days.

The story gets better. The deposit is located in a mining-friendly jurisdiction where there's plenty of other regional infrastructure in place to support a new mine.

This includes a hydroelectric power grid, a railway within 1.5 km of the deposit, a national highway only 11 kilometres away and a town of 12,000 people (which is also called Mara Rosa) about 5 kilometres away.

All of this promises to minimize projected “Capex” (mine construction) costs, as well as operational expenditures.

Mara Rosa's appeal to prospective suitors is further sweetened by the fact that it is located in a well-established mining district. In fact, there are several proximal mines, including Yamana Gold Inc.'s Chapada mine (35 kilometers away).

By way of explanation, the world’s dominant gold miners are doing all they can to significantly reduce their capital and operating costs just to stay in business. And the key to doing this is to acquire new gold assets that are complementary to their existing mines.

In other words, any proximal gold assets worth acquiring need to be both cheap and relatively fast to commercialize.

Mara Rosa measures up nicely in this regard.

It would therefore make economic sense for one of the region's big gold producers – namely Kinross Gold Corp., AngloGold Ashanti Ltd. or Yamana Gold – to eventually gobble up Amarillo. At least, this is the buzz among some of the industry experts who are following Amarillo’s emerging story.

In fact, the prospect of a rapid after-tax payback period of only 2.2 years should make Mara Rosa all the more appealing. This is because today’s gold miners are keener than ever to quickly recover any outlays of Capex expenditures.

It also bears mentioning that the up-front Capex costs of building a mine at Mara Rosa are relatively cheap by industry standards. At only around US $148 million, this adds to Mara Rosa’s appeal as a low-risk acquisition target.

Furthermore, the presence of shallow mineralization at Mara Rosa offers a favourably very low stripping ratio (the ratio of waste rock to ore), which makes for significant operational cost savings, too.

Other Key Value Drivers

Here’s something that’s been mostly overlooked by the investment community in the wake of this updated pre-feasibility study: Amarillo has made significant headway in recent months with its mine permitting process.

More specifically, the company has been issued a preliminary permit to build a gold mine -- something that represents another major de-risking event. This permit essentially represents both social and environmental acceptance of the mine proposal in Goias State, and also outlines a clear road map for obtaining final approval to commercialize Mara Rosa.

In other words, the company just has to complete the milestones laid out in the preliminary permit to receive this permission. Key components of this work will be the completion of the full feasibility study, detailed plans for the tailings facility, and the finalization of agreements to acquire surface rights. This is all expected to be achieved within the next 12 months

The company now has to demonstrate to the state government that it can operate a successful mining operation, without posing any threat to the local environment. This is expected to be achieved by way of the company completing a full bankable feasibility study (a final blueprint for a mine) within the next 12 months.

Assuming it gets the final go-ahead, the mine promises to generate in excess of US $1 billion in gross revenues, of which about $300 million will be paid directly in federal and state taxes, with further taxes to be paid in payroll and value added tax (VAT). There will also be a 1% production royalty to be paid to the government.

The benefits to the community in the town of Mara Rosa and the surrounding district should be numerous and would include approximately 300 permanent jobs in the local community, as well as many more spin-off employment opportunities.

Investment Summary

On a technical note, the company has about 80.25 million shares outstanding (86.98 million fully diluted) of which about 40% is institutionally held and around 15% is owned by management and the board of directors.

The company recently completed a $3.3 million private placement by issuing 1.3 million shares at $0.32 per share without a warrant.

At under $0.50 a share, the company is trading at a discount to its peers -- companies with comparably-sized projects, and at a similar stages of development. In this regard, Amarillo is trading at around 0.16 X net asset value (NAV) versus a peer average of 0.4 X NAV.

The granting of a preliminary mining license, as well as the demonstration of very robust project logistics at Mara Rosa, are crucial value drivers that have set Amarillo on course for a very bright future.

Ultimately, Amarillo is well-positioned to capitalize on a resurgent gold market in the most meaningful way -- by inexpensively mining up to one million ounces of gold over a mine life of at least eight years.

With such low Capex and production costs, Mara Rosa promises to be one of the world’s most lucrative modestly-sized gold mines. This competitive advantage will therefore make Amarillo an attractive takeover candidate during the balance of 2017 and beyond.

In closing, the company’s enterprise value is well deserving of a positive re-rating by the investment industry. In turn, this should help power an ascendant share price that is destined to go from strength to strength.

Neueinstieg gestern zu 0,335cad

Amarillo schwarz

Gold blau

Amarillo schwarz

Gold blau

hm... war leider nur die erste trench und somit kleiner bestand.

wollte auf dem level eigentlich weiter ausbauen, aber wird wohl eher schwierig.

werde wohl mal paar stinky bids reinstellen.

wollte auf dem level eigentlich weiter ausbauen, aber wird wohl eher schwierig.

werde wohl mal paar stinky bids reinstellen.

Antwort auf Beitrag Nr.: 55.620.365 von sir_krisowaritschko am 29.08.17 15:33:09ja, warte es mal ab... ich bin hier noch im roten bereich... kaufkurs um den dreh rum soweit ich mich erinnere (steht vermutlich im thread ) aber der euro war nicht so heftig damals.

) aber der euro war nicht so heftig damals.

Ja heute bekäme man einige Aktien mehr für das gleiche Geld.

Erstaunlich dass die letzten Tage recht wenig Interesse für ACG vorhanden war. Jemand eine Idee ob es an der Verschuldung und/ oder einer bevorstehenden KE liegen könnte?

Erstaunlich dass die letzten Tage recht wenig Interesse für ACG vorhanden war. Jemand eine Idee ob es an der Verschuldung und/ oder einer bevorstehenden KE liegen könnte?

Antwort auf Beitrag Nr.: 55.654.085 von sir_krisowaritschko am 02.09.17 16:04:45naja bleiben viele mehr oder weniger liegen.

bid ask am ende waren wieder 0,34/0,35

also nix aufregendes

bid ask am ende waren wieder 0,34/0,35

also nix aufregendes

Antwort auf Beitrag Nr.: 55.655.318 von Boersiback am 03.09.17 00:33:48orca hast berstimmt auch noch im depot oder?

hatte die vor einigen monaten eingetauscht. hatte dann vor derem anstieg überlegt ob ich hier oder eben bei orc wieder einsteige. in der retrospektive eher die falsche entscheidung. orca mit ordentlicher überarbeiter studie. im direkten vergleich, also rein von den zahlen, jetzt trotzdem nicht unbedingt so viel besseres projekt als acg. weil ja orc faktisch nur 70% am projekt besitzt. kein plan was der markt gegen acg hat. möglichweise drücken die im juli gewandelten warrants den kurs. wäre mein vermutung, weil halt schon überwiegend aktiv verkauft wird. muss man wohl abwarten bis die jungs fertig haben. kann also nicht schaden sich hier immer noch auf der passiven käuferseite ins orderbuch zu stellen.

dritte tranche zu 0,315cad steht im system.

hatte die vor einigen monaten eingetauscht. hatte dann vor derem anstieg überlegt ob ich hier oder eben bei orc wieder einsteige. in der retrospektive eher die falsche entscheidung. orca mit ordentlicher überarbeiter studie. im direkten vergleich, also rein von den zahlen, jetzt trotzdem nicht unbedingt so viel besseres projekt als acg. weil ja orc faktisch nur 70% am projekt besitzt. kein plan was der markt gegen acg hat. möglichweise drücken die im juli gewandelten warrants den kurs. wäre mein vermutung, weil halt schon überwiegend aktiv verkauft wird. muss man wohl abwarten bis die jungs fertig haben. kann also nicht schaden sich hier immer noch auf der passiven käuferseite ins orderbuch zu stellen.

dritte tranche zu 0,315cad steht im system.

Antwort auf Beitrag Nr.: 55.782.975 von sir_krisowaritschko am 20.09.17 11:26:54nein ich hab orca dummerweise noch gar nie gehabt

wollte immer mal bei 0,35-0,40 cad rum.

ärgert mich natürlich. ich denke unter 0,5 gehts nochmal

die haben ja ausserhalb ihrer studie ne gute highgradezone gefunden

wollte immer mal bei 0,35-0,40 cad rum.

ärgert mich natürlich. ich denke unter 0,5 gehts nochmal

die haben ja ausserhalb ihrer studie ne gute highgradezone gefunden

Denver Gold Forum

immer wieder pflichtprogramm http://www.denvergoldforum.org/xpl17/company-webcast/AGC:CN/

Antwort auf Beitrag Nr.: 55.858.005 von Boersiback am 30.09.17 20:55:42Den Punkt mit dem konvertieren von inferred kann ich akustisch nicht ganz verstehen.

Steht da ein potentielles Bohrprogram bevor?

Steht da ein potentielles Bohrprogram bevor?

Antwort auf Beitrag Nr.: 55.858.080 von sir_krisowaritschko am 30.09.17 21:29:40ich habs nur so verstanden, daß es so kommen sollte (wären ja ausserhalb P&P ca 50% mehr)

resource ja noch nicht ausgereizt.

war eigentlich dann hellhöriger bzgl Permits.. scheint ja da auch in der spur zu sein.

resource ja noch nicht ausgereizt.

war eigentlich dann hellhöriger bzgl Permits.. scheint ja da auch in der spur zu sein.

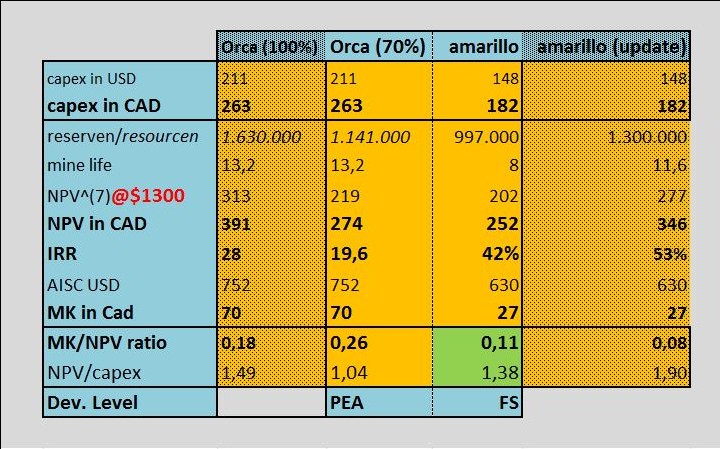

Antwort auf Beitrag Nr.: 55.858.248 von Boersiback am 30.09.17 22:58:57Außerhalb von Proven und Probable sind's über den Daumen gepeilt nochmal 500k oz in Measured, indicated und inferred.

In meinem persönlichen Wunschszenario welches die FS spiegeln werden davon 300k in PP gewandelt.

Das führt dann zu einer Laufzeitverlängerung von 8 auf 11 Jahre. Der NPV würde bei 1300usd je oz von 212 auf knapp 290mio usd ansteigen. Für mich ist AGC unter diesem Aspekt deutlich unterbewertet.

In meinem persönlichen Wunschszenario welches die FS spiegeln werden davon 300k in PP gewandelt.

Das führt dann zu einer Laufzeitverlängerung von 8 auf 11 Jahre. Der NPV würde bei 1300usd je oz von 212 auf knapp 290mio usd ansteigen. Für mich ist AGC unter diesem Aspekt deutlich unterbewertet.

Antwort auf Beitrag Nr.: 55.864.516 von sir_krisowaritschko am 02.10.17 14:06:27so denke ich auch...

klar keine 30 Mios cad.

startkosten sind halt relativ hoch, so dass der markt weiss dass sie da kaum selbst in produktion gehen werden. zudem ist brasilien nicht so beliebt wie kanada.

klar keine 30 Mios cad.

startkosten sind halt relativ hoch, so dass der markt weiss dass sie da kaum selbst in produktion gehen werden. zudem ist brasilien nicht so beliebt wie kanada.

Antwort auf Beitrag Nr.: 55.867.081 von Boersiback am 02.10.17 19:35:37Wobei die Zahlen von ORG wie schon mal angemerkt auch nicht so viel besser aussehen.

Und dort beläuft sich die Bewertung auf schlappe 70 Mio CAD.

Man muss auch einfach sagen, dass AGC projektentwicklungstechnisch eigentlich weiter ist.

Das muss man eben auch nicht wirklich verstehen. Und ob dieser Abschlag dem

Länderrisiko geschuldet ist bleibt fraglich.

Hatte heute nochmal zu 0,315cad nachgelegt.

Und dort beläuft sich die Bewertung auf schlappe 70 Mio CAD.

Man muss auch einfach sagen, dass AGC projektentwicklungstechnisch eigentlich weiter ist.

Das muss man eben auch nicht wirklich verstehen. Und ob dieser Abschlag dem

Länderrisiko geschuldet ist bleibt fraglich.

Hatte heute nochmal zu 0,315cad nachgelegt.

Antwort auf Beitrag Nr.: 55.867.516 von sir_krisowaritschko am 02.10.17 20:47:51das stimmt... bei org ist halt auch noch eingies an explorationspotenzial da. schwer einzuschätzen wie weit das geht. aber über 0,50 CAD sind sie mir zu teuer.

Sudan ist zudem auch nicht kanada

Sudan ist zudem auch nicht kanada

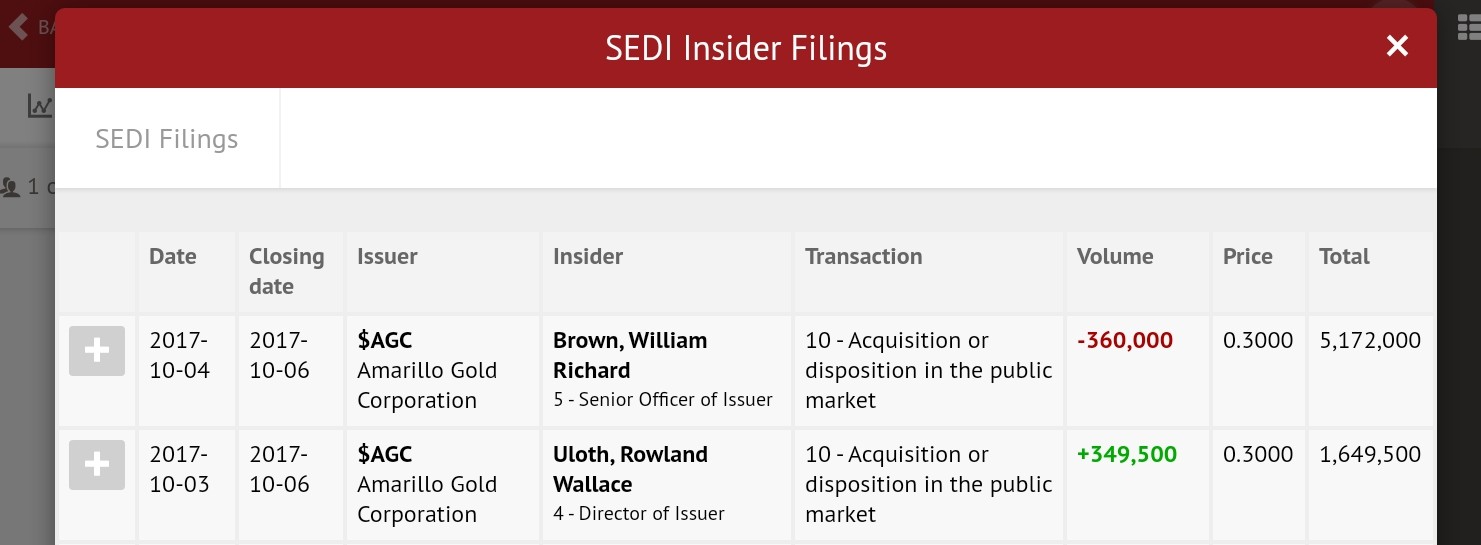

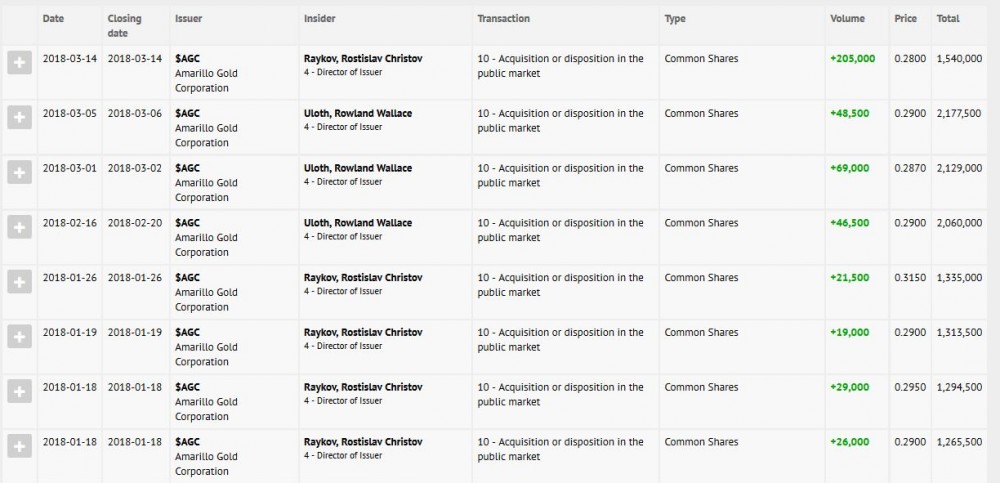

Im Management tauscht man sich untereinander einige Aktien aus.

Wobei das Transaktionsdatum bei Mr.richard nicht stimmt. Es muss dort gewiss ebenfalls der 3.10. stehen! Sieht man mal wie genau da die Geschäfte überwacht werden

Wobei das Transaktionsdatum bei Mr.richard nicht stimmt. Es muss dort gewiss ebenfalls der 3.10. stehen! Sieht man mal wie genau da die Geschäfte überwacht werden

!

Dieser Beitrag wurde von MODelfin moderiert. Grund: auf eigenen Wunsch des Users!

Dieser Beitrag wurde von MODelfin moderiert. Grund: auf eigenen Wunsch des UsersORG vs AGC

Bei ORC spielt natürlich schon der Umstand mächtig mit rein, dass man dort MACHER ins Boot geholt hat.

Ob sich der Buddy mit Rolly Uloth den richtigen Mann ins Unternehmen geholt hat bleibt abzuwarten. Bei Wesdome hat er einige Minen in Betrieb gebracht. Darunter auch die Mishi Mine welche im Tagebau betrieben wird. Unter diesem Aspekt ist schon ein gewisser Erfahrungsschatz vorhanden.

http://www.wesdome.com/corporate/board-of-directors/

http://www.wesdome.com/operations/eagle-river-complex/mishi-…

Antwort auf Beitrag Nr.: 55.913.081 von sir_krisowaritschko am 09.10.17 17:14:28bei Orca haben sie ja noch ausserhalb der schätzung einiges gefunden.

"high-grade

discovered outside of current resource with

grades up to 30.8m at 9.67 g/t (Wadi Doum)

24 m at 3.89 g/t and 10m at 15.32 g/t (Liseiwi)"

-> da ist noch weitaus mehr...

kann man von daher nicht ganz vergleichen

ich glaub bei Orca spielt da mächtig fantasie rein (die evtl berechtigt ist)

hoch aus 2014... abwarten...

ich will die wenigstens bei 0,50 CAD mal noch erwischen.

"high-grade

discovered outside of current resource with

grades up to 30.8m at 9.67 g/t (Wadi Doum)

24 m at 3.89 g/t and 10m at 15.32 g/t (Liseiwi)"

-> da ist noch weitaus mehr...

kann man von daher nicht ganz vergleichen

ich glaub bei Orca spielt da mächtig fantasie rein (die evtl berechtigt ist)

hoch aus 2014... abwarten...

ich will die wenigstens bei 0,50 CAD mal noch erwischen.

Antwort auf Beitrag Nr.: 55.914.296 von Boersiback am 09.10.17 19:36:17Naja deren 27k Drillprogramm läuft aktuell.

Muss man vorerst abwarten was dabei herumkommt.

Sicherlich ist das Potenzial theoretisch größer, keine Rede.

Dennoch sollte man dies bei AGC nicht unterschätzen.

Man muss leider abwarten und gucken was das Management gedenkt weiterhin konkret zu tun.

Dazu brauchen se halt Kohle. Das weiß der Markt. Deshalb wohl auch die Zurückhaltung.

Muss man vorerst abwarten was dabei herumkommt.

Sicherlich ist das Potenzial theoretisch größer, keine Rede.

Dennoch sollte man dies bei AGC nicht unterschätzen.

Man muss leider abwarten und gucken was das Management gedenkt weiterhin konkret zu tun.

Dazu brauchen se halt Kohle. Das weiß der Markt. Deshalb wohl auch die Zurückhaltung.

Antwort auf Beitrag Nr.: 55.915.523 von sir_krisowaritschko am 09.10.17 22:07:47klar, der markt ist nie nett...

wer kohle braucht der wird unten gehalten.

braucht halt immer nen gewissen trigger für nen anstieg.

da ist grad nix in sicht.

wer kohle braucht der wird unten gehalten.

braucht halt immer nen gewissen trigger für nen anstieg.

da ist grad nix in sicht.

witzig: exakt aufs tief vom 12.12.2016 aufgesetzt bei 0,28 CAD und dann gedreht...

wie erwartet (frag mich immer wer so doof ist dann bei dem punkt zu verkaufen)

mal sehen ob´s das jetzt war....

wie erwartet (frag mich immer wer so doof ist dann bei dem punkt zu verkaufen)

mal sehen ob´s das jetzt war....

Antwort auf Beitrag Nr.: 55.943.000 von Boersiback am 12.10.17 23:33:38Hatte es vom Grunde her auch vermutet.

Aber letztlich weist eben nie wie viele Stücke da übern Tisch gehen.

Dass es dann doch so lange im 0,29cad Bereich rumgurkte war bitter da ich kurz vorher zu 0,3cad nachgekauft hatte.

Ich denke für das verkaufen am low wird der marketmaker verantwortlich sein.

Von mir aus kann es jetzt - in Verbindung mit der Finanzierung - nach oben drehen.

Aber letztlich weist eben nie wie viele Stücke da übern Tisch gehen.

Dass es dann doch so lange im 0,29cad Bereich rumgurkte war bitter da ich kurz vorher zu 0,3cad nachgekauft hatte.

Ich denke für das verkaufen am low wird der marketmaker verantwortlich sein.

Von mir aus kann es jetzt - in Verbindung mit der Finanzierung - nach oben drehen.

hm....

Wechsel im Management

https://www.amarillogold.com/news/amarillo-gold-announces-ex…Amarillo Gold Announces Executive Management Change

November 8th, 2017

Amarillo Gold Corp. (TSX-V: AGC) ("Amarillo or the "Company") announced today that Mr. Scott Eldridge, Chief Financial Officer, has departed the Company effectively immediately.

The Company thanks Mr. Eldridge for his contributions to the Company and wishes him all the best in his future endeavors.

Mr. Hemdat Sawh has been appointed Chief Financial Officer, also effective immediately.

Mr. Sawh is a Certified Professional Accountant, and holds an MBA degree in accounting from York University, a BSc degree in geology from Concordia University and a graduate diploma in geology from McGill University. Mr. Sawh has over 16 years of accounting and auditing experience at Grant Thornton LLP, culminating in the position of principal, where he acted as lead supervisor for auditing teams of businesses with a concentration in publicly listed mining companies. Most recently, Mr. Sawh served as Chief Financial Officer for Scorpio Mining Corporation, a TSX listed company with polymetallic operations in Mexico. Mr. Sawh also served as Chief Financial Officer for Goldbelt Resources Ltd. and Crystallex International Corporation, and Wesdome Gold Mines, all TSX listed gold mining companies with assets in South American and Canada.

Mr. Rolly Uloth, President and CEO, commented, "On behalf of the management and board I would like to welcome Hemdat to the team. His extensive experience working for companies with assets in South America will be an excellent asset to us as we advance our Mara Rosa project."

About Amarillo Gold Corporation

Amarillo is developing a highly economic, open pit gold resource at its Mara Rosa deposit in the mining friendly jurisdiction of the Goias State in Brazil. In addition, Amarillo has an advanced exploration project with excellent grades at Lavras do Sul. Both projects have excellent infrastructure. The Mara Rosa project was awarded the main permit last year that gives social and environment permission to mine. This has allowed Amarillo to move forward and work on their construction permit. Construction is expected next year.

Der zweite übrigens in den letzten 10 Tagen

https://www.amarillogold.com/news/amarillo-gold-announces-ma…Amarillo Gold Announces Management Change

October 30th, 2017

Amarillo Gold Corp. (TSX-V: AGC) (“Amarillo or the “Company”) announced today that Mr. Buddy Doyle has tendered his resignation as President & CEO of Amarillo effectively immediately. Mr. Doyle said, “I have spent my career taking projects from discovery to decision to mine and then handing over to a build team. Amarillo’s flagship project, the Mara Rosa project, has reached such a stage that it is now time for Amarillo to assemble the team to commence the build and it is time again for me to pass the baton”.

“On behalf of the Board members, the management team and the staff of Amarillo, I would like to thank Buddy Doyle for his valued contributions and commitment to Amarillo”, said Rolly Uloth, Executive Chairman of the Board of Directors.

Mr. Doyle, has over 35 years of mining industry experience, is a co-founder of the company and has been instrumental over the 12 last years working to advance the Mara Rosa to near the decision to mine stage. We are very pleased that Mr. Doyle has agreed to stay on to assist the Company in taking the projects to the next level in a consulting role. Mr. Doyle also will remain as a director of the company.

The Board has appointed Amarillo’s Executive Chairman Mr. Rolly Uloth as Interim CEO until a suitable replacement can be found. Mr. Uloth has over 20 years as a seasoned mining executive, as well as a business professional with over 45 years of combined experience. This includes being President and Director of River Gold Mines; in 2006, upon the completion of the merger between Wesdome and Eagle River mines, Mr. Uloth became Chairman of the combined company. Mr. Uloth became Chairman, and then CEO of the combined company from 2007 – 2010 where he led Wesdome through several of its most profitable years, and reopened the Kiena Mine. In 2013, Mr. Uloth rejoined Wesdome and successfully restructured the Company. He held this position until last year and still remains on the Board. Mr. Uloth joined as Executive Chairman of Amarillo in June of 2017 with the mandate of optimizing and restructuring Amarillo Gold.

About Amarillo Gold Corporation

Amarillo is developing a highly economic, open pit gold resource at its Mara Rosa deposit in the mining friendly jurisdiction of the Goias State in Brazil. In addition, Amarillo has an advanced exploration project with excellent grades at Lavras do Sol. Both projects have excellent infrastructure. The Mara Rosa project was awarded the main permit last year that gives social and environment permission to mine. This has allowed Amarillo to move forward and work on their construction permit. Construction is expected next year.

For more detail, please refer to our website at: www.amarillogold.com

Antwort auf Beitrag Nr.: 56.139.395 von Marcelarcel am 09.11.17 09:44:15naja doyle ist eben geologe. zumindest bleibt er als direktor im unternehmen.

finde es recht sonderbar, dass man mr. uloth nicht dauerhaft führen lassen will.

erfahrung hat er ja schließlich. jedoch scheint man da andere wege gehen zu wollen.

The Board has appointed Amarillo’s Executive Chairman Mr. Rolly Uloth as Interim CEO until a suitable replacement can be found.

dass der finanzchef abdanken durfte lässt die vermutung zu, dass da irgendwas mit dem geldbeschaffen eventuell nicht ganz nach plan lief. eigentlich hätte hier schon längst zwischenfinanziert werden müssen.

finde es recht sonderbar, dass man mr. uloth nicht dauerhaft führen lassen will.

erfahrung hat er ja schließlich. jedoch scheint man da andere wege gehen zu wollen.

The Board has appointed Amarillo’s Executive Chairman Mr. Rolly Uloth as Interim CEO until a suitable replacement can be found.

dass der finanzchef abdanken durfte lässt die vermutung zu, dass da irgendwas mit dem geldbeschaffen eventuell nicht ganz nach plan lief. eigentlich hätte hier schon längst zwischenfinanziert werden müssen.

Antwort auf Beitrag Nr.: 56.139.935 von sir_krisowaritschko am 09.11.17 10:21:58hmm ist schon sehr naheliegend, dass die Geldbeschaffung nicht so hingehauen hat wie geplant...

Bis die davon was hören lassen wird sich wohl leider auch nichts am Kurs tun.

Bis die davon was hören lassen wird sich wohl leider auch nichts am Kurs tun.

Antwort auf Beitrag Nr.: 56.139.935 von sir_krisowaritschko am 09.11.17 10:21:58Echt krank heute hier. Gestern noch den Einstieg zu 0,29 cad überlegt. Heute jemand 480k shares zu 0,285 aufgesammelt und dann geht der Kurs mit nur 150.000 Shares über 0,40 cad. Selten sowas gesehen

Antwort auf Beitrag Nr.: 56.570.119 von peterhuber91 am 29.12.17 18:57:51Insgesamt konnte AGC nur wenig von den angepeilten Zielen für 2017 in die Tat umsetzen.

Konversion- und Extensiondrilling fielen komplett aus. Finanzierung zu Kursen im 0,3cad Bereich konnte nicht durchgeführt werden. Installation license wurde ebenfalls noch nicht erteilt. Brasilianische Wirtschaft tendenziell noch immer eher Sorgenkind was die Rahmenbedingungen erschwert.

Konversion- und Extensiondrilling fielen komplett aus. Finanzierung zu Kursen im 0,3cad Bereich konnte nicht durchgeführt werden. Installation license wurde ebenfalls noch nicht erteilt. Brasilianische Wirtschaft tendenziell noch immer eher Sorgenkind was die Rahmenbedingungen erschwert.

Sieht nach Turnaround aus.

Now we got apparently a company maker on board!

..

.

Amarillo Appoints Mike Mutchler as President and CEO

TORONTO, Jan. 08, 2018 (GLOBE NEWSWIRE) -- Amarillo Gold Corporation (“Amarillo” or the “Company”) (TSX.V:AGC), is pleased to announce the appointment of Mike Mutchler as President & CEO and Director of the Company effective immediately. Rolly Uloth who has held the position as Interim CEO will continue as Executive Chairman of the Company.

Mr. Mutchler, who is currently a Partner and Advisory Board Member at Whittle Consulting Pty. Ltd., has over 30 years’ experience as a mining engineer in both open-pit and underground mining operations. At Whittle, Mike conducts Enterprise Optimisation using its proprietary software for mining projects worldwide. Prior to Whittle, Mike was COO for Largo Resources where he was responsible for the construction, commissioning, operations and expansion of the Maracas Vanadium Mine and Mill in Bahia, Brazil. Mike’s extensive experience also included the position of COO of Rainy River Resources, Vice President Project Development for Kinross Gold Corporation, Mine & Infrastructure Manager for Kinross’s Cerro Casale project in Chile, Project Director for Kinross’s Paracatu Mine in Brazil, and he held managerial positions at Kinross and ASARCO. Mike holds a BSc (Mining Engineering), South Dakota School of Mines & Technology; MBA, Webster University, Missouri; Executive Juris Doctorate degree, Concord School of Law, Kaplan University; and Chartered Directors Certificate, The Directors College, McMaster University.

Mr. Mutchler commented, “I am very pleased to accept the position of President and CEO at Amarillo. Rolly and the team in Brazil have done a terrific job in advancing the Mara Rosa Project towards the attainment of the Installation Permit (LI) and subsequent construction and operation of this world class deposit in the mining friendly State of Goias, Brazil. I am also excited to apply my experience in the Whittle Optimisation to this project which I believe is a suitable project for optimisation. In addition, the Lavras do Sul properties and in particular the Butia project in the State of Rio Grande do Sul, Brazil offer tremendous opportunities for organic growth within the Company.”

Mr. Uloth commented, “On behalf of the Board of Amarillo, I am very pleased with the appointment of Mike as the President and CEO of Amarillo. Mike’s track record of building major mining projects internationally and in particular his operating experience in Brazil, qualify him as the ideal candidate for Amarrillo. We look forward to his depth of knowledge and skills to take us to the permitting and construction of Mara Rosa, and to lead the efforts in expanding the resources both at Mara Rosa and Butia.”

https://ceo.ca/@nasdaq/amarillo-appoints-mike-mutchler-as-pr…

https://ceo.ca/@nasdaq/amarillo-appoints-mike-mutchler-as-president-and-ceo

Vita Mike Mutchler

http://www.whittleconsulting.com.au/wp-content/uploads/2017/…

http://www.whittleconsulting.com.au/wp-content/uploads/2017/10/WhittleConsulting-StaffProfiles-V3_MMutchler.pdf

Antwort auf Beitrag Nr.: 56.649.590 von sir_krisowaritschko am 08.01.18 13:27:03Hab vergebens versucht die Bilanz von amarillo zu finden? Jedenfalls gut versteckt. Auf den ersten Blick mit deim feinen NPV und im Peersvergleich schon günstig. 33 Millionen assets lt. web, 10 mil. debt ... schon ein high risk play. grundsätzlich mag ich keine firmen die Bilanzen verstecken. sir hast du da irgendwo einen Link?

Antwort auf Beitrag Nr.: 56.719.989 von peterhuber91 am 15.01.18 15:39:13https://sedar.com/DisplayProfile.do?lang=EN&issuerType=03&is…

nach unten scrollen und auf VIEW This company documents klicken!

dann wählst dir den md&a oder financial report aus.

nach unten scrollen und auf VIEW This company documents klicken!

dann wählst dir den md&a oder financial report aus.

Antwort auf Beitrag Nr.: 56.720.037 von sir_krisowaritschko am 15.01.18 15:43:58Also bilanztechnisch mit 21 Mill EK und 25 Mill MK, 11 mil debt und kein Cash für mich auf aktuellem Niveau kein Kauf. Warte jedenfalls mal auf die KE.

Antwort auf Beitrag Nr.: 56.722.824 von peterhuber91 am 15.01.18 20:03:33Der Kredit wird spätestens am 31.07.2019 fällig. 12% Zinsen ist auch eine heftige burnrate. Ich würde sagen Amarillo ist stark in der Zwickmühle. Sehe hier wieder Kurse um die 0,20 cad. Auf jedenfall siehts meiner Meinung nicht gut aus außer man kann jetzt mit einem strategischen Investor bzw. einer Genhmigung punkten.

Antwort auf Beitrag Nr.: 56.723.229 von peterhuber91 am 15.01.18 20:56:23oha... mist da hab ich geschlampt... die schulden war mir nicht bewusst...

bei producern und so mein erster blick. bei explorern die noch keine projektfinanzierung sicherstellen bin ich da manchmal ungenau.

das ist ein großes problem hier !! kein wunder läuft der kurs nicht.

bei producern und so mein erster blick. bei explorern die noch keine projektfinanzierung sicherstellen bin ich da manchmal ungenau.

das ist ein großes problem hier !! kein wunder läuft der kurs nicht.

Antwort auf Beitrag Nr.: 56.724.444 von Boersiback am 15.01.18 23:25:09Oha, Danke für deinen ironischen Beitrag. Lieber wäre mir dein fundamentales Update da ich deine Beiträge schätze.

Antwort auf Beitrag Nr.: 56.724.444 von Boersiback am 15.01.18 23:25:09Gegen Schulden als Developer ist nichts einzuwenden. 11 mil auf 31 Mill Bilanzsumme ist aber schon ein Brett.

sicherlich ein problempunkt, dennoch kein unlösbarer.

guck dir mal an wo AGC im Jahre 2014-15 sharepreistechnisch rumkrepelte als man den gold link abschloss. entweder fiese verwässerung bei 0,10 cad oder vorwärtsverkauf. nachdem der SP wieder anzog konnte man einige gute KEs auf höherem level platzieren. im vergleich zu anderen buden hielt sich die verwässerung der letzten jahre in seeeehr engen grenzen.

ich würde das projekt nicht am schuldenstand messen. entweder es taugt letztlich was, dann wirds in gang kommen oder eben nicht. dass man den mike nun im unternehmen hat sieht schon mal gar nicht so verkehrt aus. alles wartet immer noch auf die zwischenfinanzierung.

daneben ist der markt eben genervt, dass das mit dem bau der anlage in 2018 auch nichts werden wird. darüber hinaus wird nun wohl erst im laufe des jahres wieder gebohrt und wohl ein überarbeitetes minenkonzept erarbeitet was dann hoffentlich direkt in die FS einfließt. noch eine PFS würde ich auch nicht verkraften

wenn ich nicht schon investiert wäre würde ich tatsächlich die finanzierung abwarten.

guck dir mal an wo AGC im Jahre 2014-15 sharepreistechnisch rumkrepelte als man den gold link abschloss. entweder fiese verwässerung bei 0,10 cad oder vorwärtsverkauf. nachdem der SP wieder anzog konnte man einige gute KEs auf höherem level platzieren. im vergleich zu anderen buden hielt sich die verwässerung der letzten jahre in seeeehr engen grenzen.

ich würde das projekt nicht am schuldenstand messen. entweder es taugt letztlich was, dann wirds in gang kommen oder eben nicht. dass man den mike nun im unternehmen hat sieht schon mal gar nicht so verkehrt aus. alles wartet immer noch auf die zwischenfinanzierung.

daneben ist der markt eben genervt, dass das mit dem bau der anlage in 2018 auch nichts werden wird. darüber hinaus wird nun wohl erst im laufe des jahres wieder gebohrt und wohl ein überarbeitetes minenkonzept erarbeitet was dann hoffentlich direkt in die FS einfließt. noch eine PFS würde ich auch nicht verkraften

wenn ich nicht schon investiert wäre würde ich tatsächlich die finanzierung abwarten.

Antwort auf Beitrag Nr.: 56.725.731 von sir_krisowaritschko am 16.01.18 08:39:12Da stimme ich dir absolut zu. Interessantes Projekt aber aktuell eindeutig der falsche Einstiegszeitpunkt. Auf tiefen Stand mit KE - not good

Da tut sich zumindest mal wieder etwas.

TORONTO, Jan. 30, 2018 (GLOBE NEWSWIRE) -- Amarillo Gold Corporation (“Amarillo” or the “Company”) (TSX.V:AGC), is pleased to announce that it has engaged Whittle Consulting (WCPL) to conduct an Enterprise Optimisation study for the Company’s flagship Mara Rosa Gold Project in Brazil.

Read more at http://www.stockhouse.com/news/press-releases/2018/01/31/ama…

TORONTO, Jan. 30, 2018 (GLOBE NEWSWIRE) -- Amarillo Gold Corporation (“Amarillo” or the “Company”) (TSX.V:AGC), is pleased to announce that it has engaged Whittle Consulting (WCPL) to conduct an Enterprise Optimisation study for the Company’s flagship Mara Rosa Gold Project in Brazil.

Read more at http://www.stockhouse.com/news/press-releases/2018/01/31/ama…

Antwort auf Beitrag Nr.: 56.724.996 von peterhuber91 am 16.01.18 06:35:36

war auch ernst gemeint... ich bin daher auch raus hier vorläufig... wegen anderen sachen

Zitat von peterhuber91: Gegen Schulden als Developer ist nichts einzuwenden. 11 mil auf 31 Mill Bilanzsumme ist aber schon ein Brett.

war auch ernst gemeint... ich bin daher auch raus hier vorläufig... wegen anderen sachen

by @nasdaq on February 20, 2018

Amarillo Announces the Extension and Amendment of Its Gold-Linked Credit Facility

Amarillo and its lending group have agreed to extend the maturity of the Facility from July 31, 2019 to June 30, 2022. The other terms and conditions will remain the same.

Mike Mutchler, President & CEO, stated “We are pleased with the extension of this Facility, which will mature at about the time of planned production at Mara Rosa. We are currently pursuing financing alternatives to fund our immediate planned activities to get us to the next step of applying for the Installation Permit (LI). The extension of the maturity date of this Facility has alleviated the uncertainty surrounding its original maturity date and has put us in good stead to move forward with Mara Rosa and Lavras do Sul.”

nasdaq/amarillo-announces-the-extension-and-amendment-of-its" target="_blank" rel="nofollow ugc noopener">https://ceo.ca/@nasdaq/amarillo-announces-the-extension-and-amendment-of-its

https://ceo.ca/@nasdaq/amarillo-announces-the-extension-and-amendment-of-its

na immerhin eine kleine unsicherheit weniger! die konditionen der kommenden KE werden zeigen wer hier was verkaufen kann und zu welchem preis.

Amarillo Announces the Extension and Amendment of Its Gold-Linked Credit Facility

Amarillo and its lending group have agreed to extend the maturity of the Facility from July 31, 2019 to June 30, 2022. The other terms and conditions will remain the same.

Mike Mutchler, President & CEO, stated “We are pleased with the extension of this Facility, which will mature at about the time of planned production at Mara Rosa. We are currently pursuing financing alternatives to fund our immediate planned activities to get us to the next step of applying for the Installation Permit (LI). The extension of the maturity date of this Facility has alleviated the uncertainty surrounding its original maturity date and has put us in good stead to move forward with Mara Rosa and Lavras do Sul.”

nasdaq/amarillo-announces-the-extension-and-amendment-of-its" target="_blank" rel="nofollow ugc noopener">https://ceo.ca/@nasdaq/amarillo-announces-the-extension-and-amendment-of-its

https://ceo.ca/@nasdaq/amarillo-announces-the-extension-and-amendment-of-its

na immerhin eine kleine unsicherheit weniger! die konditionen der kommenden KE werden zeigen wer hier was verkaufen kann und zu welchem preis.

Antwort auf Beitrag Nr.: 57.069.318 von sir_krisowaritschko am 20.02.18 13:30:37

huch... da ist was schief gelaufen!

https://ceo.ca/@nasdaq/amarillo-announces-the-extension-and-… !

Dieser Beitrag wurde von CommunityAssistance moderiert. Grund: auf eigenen Wunsch des Users!

Dieser Beitrag wurde von CloudMOD moderiert. Grund: Löschung auf Wunsch des Users

Antwort auf Beitrag Nr.: 57.214.570 von sir_krisowaritschko am 07.03.18 18:16:27Corp. presentation februar

https://www.amarillogold.com/sites/default/files/attachments…

Third Party Company Review

https://www.amarillogold.com/sites/default/files/attachments…

https://www.amarillogold.com/sites/default/files/attachments…

Third Party Company Review

https://www.amarillogold.com/sites/default/files/attachments…

by the way... nicht verwirren lassen. habe die löschung veranlasst.

Mara Rosa

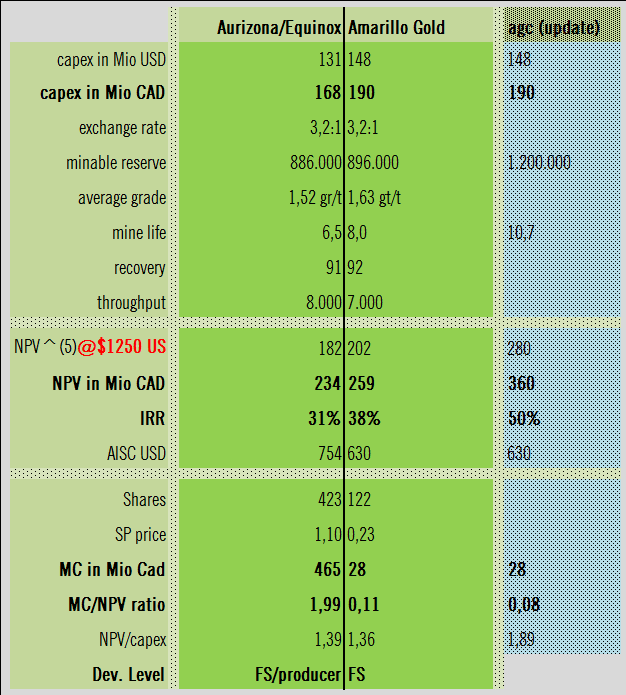

In speaking this past week with the newly appointed

president and CEO of Amarillo, the goal of this year’s

work program will be to do enough drilling to expand the

mine life to a minimum of 10 years. He also believes there are

means of improving the efficiency and cost of production

on this project that can enhance its economics even beyond

an already robust picture. The PFS results displayed

above were based on $1,200 gold. With all-in sustaining

costs of just $630 per ounce, at $1,200 gold that provides a

margin of $570/oz. At the current gold price of $1,350, a

margin of $720 per ounce would be earned. Multiply that

times 140,000 ounces of projected production during the

first four years followed by 112,000 in the following years

and you get a picture of cash flows that can be generated

at a Mara Rosa gold mine.

Lavras do Sol

One note of interest I learned from Mike Mutchler when I

spoke to him this past week was that in the past when the

Lavras do Sul Project was acquired from Rio Tinto, written

into the agreement was a claw back agreement in the

event more than 7 million ounces of gold is outlined on this

project. I believe the claw back allows for Rio Tinto to acquire

a 60% interest in the project by paying Amarillo 3 times the