Gefahr von scharfen Kursrückgängen bei dt.Nebenwerten im späten Bullenmarkt - Älteste Beiträge zuerst (Seite 6)

eröffnet am 15.07.18 14:10:13 von

neuester Beitrag 08.02.24 14:46:14 von

neuester Beitrag 08.02.24 14:46:14 von

Beiträge: 130

ID: 1.284.525

ID: 1.284.525

Aufrufe heute: 0

Gesamt: 10.857

Gesamt: 10.857

Aktive User: 0

ISIN: DE0007203325 · WKN: 720332 · Symbol: PXAP

7.051,75

PKT

-0,98 %

-70,00 PKT

Letzter Kurs 17:50:00 Xetra

Nemetschek

..

=> ich denke, auf <EUR75 fällt das Teil in jedem Fall, so Richtung ~EUR50, im derzeitigen Bärenmarkt; aber nicht mehr dieses Jahr (>85%)

--> im Grunde gilt für das P/E etc. dasselbe, wie für einige der oben beschriebenen Werte

=> erst bei ~EUR51 ist eine breite Unterstützung

Antwort auf Beitrag Nr.: 58.218.111 von faultcode am 15.07.18 15:50:21

--> abwarten

--> diese Unterstüzung (mittelfristig) bei ~EUR12.5 wurde zuletzt bei bislang geringem Volumen glatt durchschlagen

--> bleibt noch eine (eher kleine) bei ~EUR9.4

=> darunter sieht es zappenduster aus:

=> das ist momentan das Dilemma bei (dt.) Nebenwerten am Ende eines Bullenmarktes:

• oft viel Cash

• aber gedämpfte Wachstumsaussichten in den nächsten 6...24 Monaten

=> was tun??

• eine doofe Übernahme?

• Dividenden erhöhen, nur um sie später ev. wieder zurücknehmen zu müssen?

• Aktienrückkaufprogramm? --> um es gleich zu sagen:

-- ich halte davon gar nichts; es stabilisert (natürlich) zunächst den Kurs; ist aber wie eine Droge für den Vorstand

=> fängst Du einmal damit an, wird es ganz schwer (wenn noch Cash da) damit aufzuhören

--> nach 2..4 Jahren stellt der Buy&Hold-Anleger fest, daß es ihm nichts gebracht hat, aber viel schlimmer: die schöne Kohle ist nun weg!

--> Blue Chips haben es mMn - im Schnitt - bei diesem Dilemma vor vornherein einfacher; können sie doch einfach und relativ sicher die Dividende (maßvoll) erhöhen, da ihnen der Weg zu hohem organischen Wachstum sowieso (idR) versperrt ist

(gut, auch da wird ganz viel Blödsinn mit Aktienrückkäufen gemacht, v.a. in den USA in den letzten Jahren...)

Frage:

• warum werden dann überhaupt Aktienrückkaufprogramme aufgelegt?

--> ganz einfach:

• weil sie dem Vorstand (und der Verwaltung) insgesamt nutzen; Dividenden (trotz idR ESt) würden hingegen mehrheitlich nur dem Anleger nutzen

• ..und: greift diese Unsitte erst einmal um sich, so wie seit 1...2 Jahren auch in Deutschland, sinkt die Hemmschwelle im einzelnen Unternehmen, was bislang davon Abstand nahm: "Die anderen machen das doch auch!"

=> am schlimmsten (nach meiner kl.Umsicht) ist es bei ProSieben:

• Dividendenkürzung und Aktienrückkaufprogramm (um später in 2019e eine Kap.-Erhöhung besser durchführen zu können)

=> das wird sich auch mMn einen Tages böse für den Buy&Hold-Anleger rächen --> einfach mal 2...4 Jahre warten

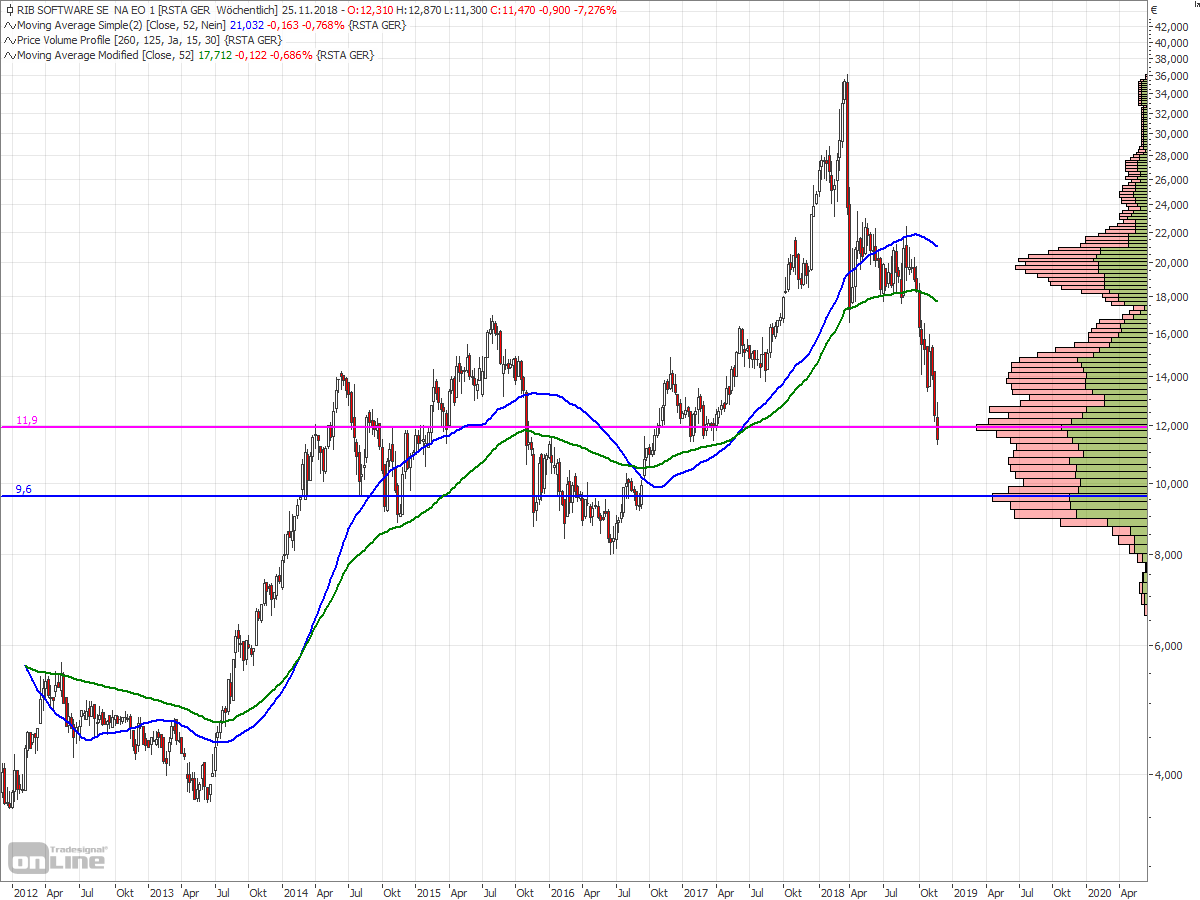

RIB Software

29.03.18 Zitat von faultcode: ...--> das Teil ist auf der Longseite (kurz- und mittelfrsitig) momentan hochgradig toxisch...

--> spätestens bei EUR12 (< 9m) ist aber Schluss mit Kursverfall...

--> abwarten

--> diese Unterstüzung (mittelfristig) bei ~EUR12.5 wurde zuletzt bei bislang geringem Volumen glatt durchschlagen

--> bleibt noch eine (eher kleine) bei ~EUR9.4

=> darunter sieht es zappenduster aus:

=> das ist momentan das Dilemma bei (dt.) Nebenwerten am Ende eines Bullenmarktes:

• oft viel Cash

• aber gedämpfte Wachstumsaussichten in den nächsten 6...24 Monaten

=> was tun??

• eine doofe Übernahme?

• Dividenden erhöhen, nur um sie später ev. wieder zurücknehmen zu müssen?

• Aktienrückkaufprogramm? --> um es gleich zu sagen:

-- ich halte davon gar nichts; es stabilisert (natürlich) zunächst den Kurs; ist aber wie eine Droge für den Vorstand

=> fängst Du einmal damit an, wird es ganz schwer (wenn noch Cash da) damit aufzuhören

--> nach 2..4 Jahren stellt der Buy&Hold-Anleger fest, daß es ihm nichts gebracht hat, aber viel schlimmer: die schöne Kohle ist nun weg!

--> Blue Chips haben es mMn - im Schnitt - bei diesem Dilemma vor vornherein einfacher; können sie doch einfach und relativ sicher die Dividende (maßvoll) erhöhen, da ihnen der Weg zu hohem organischen Wachstum sowieso (idR) versperrt ist

(gut, auch da wird ganz viel Blödsinn mit Aktienrückkäufen gemacht, v.a. in den USA in den letzten Jahren...)

Frage:

• warum werden dann überhaupt Aktienrückkaufprogramme aufgelegt?

--> ganz einfach:

• weil sie dem Vorstand (und der Verwaltung) insgesamt nutzen; Dividenden (trotz idR ESt) würden hingegen mehrheitlich nur dem Anleger nutzen

• ..und: greift diese Unsitte erst einmal um sich, so wie seit 1...2 Jahren auch in Deutschland, sinkt die Hemmschwelle im einzelnen Unternehmen, was bislang davon Abstand nahm: "Die anderen machen das doch auch!"

=> am schlimmsten (nach meiner kl.Umsicht) ist es bei ProSieben:

• Dividendenkürzung und Aktienrückkaufprogramm (um später in 2019e eine Kap.-Erhöhung besser durchführen zu können)

=> das wird sich auch mMn einen Tages böse für den Buy&Hold-Anleger rächen --> einfach mal 2...4 Jahre warten

Antwort auf Beitrag Nr.: 59.259.454 von faultcode am 20.11.18 15:51:57

https://www.marketwatch.com/story/misguided-share-buybacks-a…

=>

...

A year ago, I wrote about the worrying increase in leverage among America’s blue chips caused by share repurchases (“Hollowed-out blue chips are the next subprime”)....

GE was one of Wall Street’s major share buyback operators between 2015 and 2017; it repurchased $40 billion of shares at prices between $20 and $32. The share price is now $8.60, so the company has liquidated between $23 billion and $29 billion of its shareholders’ money on this utterly futile activity alone. Since the highest net income recorded by the company during those years was $8.8 billion in 2016, with 2015 and 2017 recording a loss, it has managed to lose more on its share repurchases during those three years than it made in operations, by a substantial margin.

Even more important, GE has now left itself with minus $48 billion in tangible net worth at Sept. 30, with actual genuine tangible debt of close to $100 billion. As the new CEO Larry Culp told CNBC last Monday: “We have no higher priority right now than bringing those leverage levels down.” The following day, GE announced the sale of 15% of its oil services arm Baker Hughes, for a round $4 billion.

Of course, since that sale values Baker Hughes at $26 billion, and GE paid $32 billion for 62% of Baker Hughes as recently as last year, which looks to me like a valuation for the whole company of $52 billion, GE shareholders appears to have lost half the value of their investment in Baker Hughes in about 18 months.

As I have said several times, GE has been abominably managed since the odious “Neutron Jack” Welch took over in 1981; let us hope that Culp, who had a fine track record at Danaher, can turn it around.

The GE situation reminds me of another overvalued conglomerate, based in the railroad sector, that had been one of the bluest of blue chips and that slithered into bankruptcy over a period of about two years, via a series of divestitures at fire-sale prices, each of which appeared to have enabled the company to “turn the corner.” Its bankruptcy was unthinkable — until it happened, shaking market confidence for the next year, especially in the commercial paper market, and tipping off a considerable recession.

For those of you lucky enough not to have been around that far back (and even I only learned about in business school, a couple of years later), I am referring to the Penn Central Corporation, which bit the dust in 1970. That too, or rather its predecessor New York Central (the two behemoths merged in 1968), had benefited from a managerial wizard, Robert R. Young, whose reputation in the 1950s was almost as overblown as Welch’s. The one way in which GE differs from Penn Central is that it has announced its intention to exit the commercial paper market, so at least that market won’t be spooked if it goes after redeeming most of its outstandings.

Just as Penn Central’s bankruptcy revealed weaknesses in several other major U.S. companies, such as Lockheed, and shook business confidence for several years (President Nixon resorted to bullying the Fed into money printing to try to escape from the resulting recession) so it’s likely that GE, or some other titan of U.S. industry, will go unexpectedly bankrupt in the next year or so and spark off a similar stock market meltdown and period of general gloom.

AT&T with $181 billion of debt and minus $128 billion of tangible net worth, most of it through overpriced acquisitions, is another potential Penn Central lookalike; again its bankruptcy is unthinkable but not by any means impossible.

Share-repurchase shenanigans are not however confined to the dinosaurs of yesteryear. A recent Financial Times article outlined how the five tech companies with the most cash (Apple, Alphabet, Cisco, Microsoft and Oracle) have repurchased an astounding $115 billion of stock in the first three quarters of 2018. By contrast, the total capital spending of the five companies was only $42.6 billion during the same period. The story then congratulated investors for having done so well out of President Trump’s tax reform, which lowered the corporate tax rate, thus encouraging investment in the United States. With share repurchases in these companies being almost three times their actual investment, one must wonder how much actual U.S. economic growth they are expecting.

These share repurchases are misguided in so many ways. First, Apple, Alphabet and Microsoft are valued by the stock market at close to $1 trillion, levels no company has ever reached before (Cisco and Oracle, to be fair, have more reasonable valuations, under $200 billion.) If you ignore the current stock price, a company repurchasing its shares is simply giving away its cash and reducing its share count; it creates no value. If you don’t ignore the share price, share repurchases are highly pro-cyclical, pushing up share prices in a bull market and raising the possibility that the company will be short of cash in the next recession. For $1 trillion companies, share repurchases are almost certainly being done very close to the top.

Either way, the company is not “giving” anything to shareholders (especially not to small shareholders, who generally do not have the possibility of dealing directly with the company Treasurer repurchasing the shares.)

Most likely, the share price rise caused by the heavy repurchases will merely bring a new set of even more ignorant investors into the shares, attracted by their apparent “momentum.” That is what has happened to the shares of the FAANGs in 2018 (until the last month) — share repurchases have pushed up their prices and brought in more suckers who are unlikely to be long-term happy shareholders.

Cash dividends are quite different; they represent a return to the shareholders of the profits legitimately earned by the company. Provided the company does not pay out more than it earns, dividends do not significantly increase the company’s leverage or its risk. However, tech companies are generally loath to pay out substantial cash dividends; they prefer to indulge in vast share repurchases for one very good reason: the share repurchases benefit the value of the employees’ stock options, whereas dividends don’t.

It has always been clear that a decade of negative real interest rates would cause excess investment in some area or other, which would eventually bring the overinflated stock market crashing down. Simple souls have been watching the U.S. housing market intensely, but that was never likely to be the principal cause of collapse again, as it was in 2007-08, because the last housing disaster is so recent. To some extent, the tech sector is headed for disaster; both the private-equity-funded sector, with its “dekacorns,” and the publicly quoted sector with its arrogant leftist FAANGs, are clearly overblown in value, have lost most of the purpose for their existence and are due for a massive cull.

Another sector that looks likely to crash, and has been warned about frequently, is the leveraged loan market. Too much capital has gone into speculative private-equity deals, generally poorly managed, and achieving value only by “financial engineering” in the high-yield debt markets. There is no doubt that this sector is also due for massive cathartic shakeout, causing bankruptcies and dismay but ultimately healthy for the U.S. and global economies as a whole.

However, no bubble is as overblown and as unjustified as share buybacks, which have totaled $350 billion in the first 10 months of 2018 alone. These have run at far more than double the level of any previous economic upsurge, at a time when stock prices are more overvalued than they have ever been before — 1929 was a model of sound valuation and caution by comparison — with the favorite tech stock, Radio Corporation of America, trading at only 28 times trailing earnings. They have de-capitalized blue-chip companies, leaving many of them with negative equity (in last year’s piece I detailed the precise position of several; it need hardly be said that another year of frantic buyback activity has left the balance sheets of most of those companies in even worse shape.)

The crash to come will focus therefore on the major names of corporate America, which have hollowed out their balance sheets to goose the prices of their management’s stock options.

Because corporate America provides far more jobs than the housing sector, or even the tech sector, its collapse will be uniquely painful. But that is only a just recompense for a decade of monetary policy that has been uniquely, criminally foolish...

Misguided share buybacks are hollowing out companies’ balance sheets...

Published: Nov 21, 2018https://www.marketwatch.com/story/misguided-share-buybacks-a…

=>

...

A year ago, I wrote about the worrying increase in leverage among America’s blue chips caused by share repurchases (“Hollowed-out blue chips are the next subprime”)....

GE was one of Wall Street’s major share buyback operators between 2015 and 2017; it repurchased $40 billion of shares at prices between $20 and $32. The share price is now $8.60, so the company has liquidated between $23 billion and $29 billion of its shareholders’ money on this utterly futile activity alone. Since the highest net income recorded by the company during those years was $8.8 billion in 2016, with 2015 and 2017 recording a loss, it has managed to lose more on its share repurchases during those three years than it made in operations, by a substantial margin.

Even more important, GE has now left itself with minus $48 billion in tangible net worth at Sept. 30, with actual genuine tangible debt of close to $100 billion. As the new CEO Larry Culp told CNBC last Monday: “We have no higher priority right now than bringing those leverage levels down.” The following day, GE announced the sale of 15% of its oil services arm Baker Hughes, for a round $4 billion.

Of course, since that sale values Baker Hughes at $26 billion, and GE paid $32 billion for 62% of Baker Hughes as recently as last year, which looks to me like a valuation for the whole company of $52 billion, GE shareholders appears to have lost half the value of their investment in Baker Hughes in about 18 months.

As I have said several times, GE has been abominably managed since the odious “Neutron Jack” Welch took over in 1981; let us hope that Culp, who had a fine track record at Danaher, can turn it around.

The GE situation reminds me of another overvalued conglomerate, based in the railroad sector, that had been one of the bluest of blue chips and that slithered into bankruptcy over a period of about two years, via a series of divestitures at fire-sale prices, each of which appeared to have enabled the company to “turn the corner.” Its bankruptcy was unthinkable — until it happened, shaking market confidence for the next year, especially in the commercial paper market, and tipping off a considerable recession.

For those of you lucky enough not to have been around that far back (and even I only learned about in business school, a couple of years later), I am referring to the Penn Central Corporation, which bit the dust in 1970. That too, or rather its predecessor New York Central (the two behemoths merged in 1968), had benefited from a managerial wizard, Robert R. Young, whose reputation in the 1950s was almost as overblown as Welch’s. The one way in which GE differs from Penn Central is that it has announced its intention to exit the commercial paper market, so at least that market won’t be spooked if it goes after redeeming most of its outstandings.

Just as Penn Central’s bankruptcy revealed weaknesses in several other major U.S. companies, such as Lockheed, and shook business confidence for several years (President Nixon resorted to bullying the Fed into money printing to try to escape from the resulting recession) so it’s likely that GE, or some other titan of U.S. industry, will go unexpectedly bankrupt in the next year or so and spark off a similar stock market meltdown and period of general gloom.

AT&T with $181 billion of debt and minus $128 billion of tangible net worth, most of it through overpriced acquisitions, is another potential Penn Central lookalike; again its bankruptcy is unthinkable but not by any means impossible.

Share-repurchase shenanigans are not however confined to the dinosaurs of yesteryear. A recent Financial Times article outlined how the five tech companies with the most cash (Apple, Alphabet, Cisco, Microsoft and Oracle) have repurchased an astounding $115 billion of stock in the first three quarters of 2018. By contrast, the total capital spending of the five companies was only $42.6 billion during the same period. The story then congratulated investors for having done so well out of President Trump’s tax reform, which lowered the corporate tax rate, thus encouraging investment in the United States. With share repurchases in these companies being almost three times their actual investment, one must wonder how much actual U.S. economic growth they are expecting.

These share repurchases are misguided in so many ways. First, Apple, Alphabet and Microsoft are valued by the stock market at close to $1 trillion, levels no company has ever reached before (Cisco and Oracle, to be fair, have more reasonable valuations, under $200 billion.) If you ignore the current stock price, a company repurchasing its shares is simply giving away its cash and reducing its share count; it creates no value. If you don’t ignore the share price, share repurchases are highly pro-cyclical, pushing up share prices in a bull market and raising the possibility that the company will be short of cash in the next recession. For $1 trillion companies, share repurchases are almost certainly being done very close to the top.

Either way, the company is not “giving” anything to shareholders (especially not to small shareholders, who generally do not have the possibility of dealing directly with the company Treasurer repurchasing the shares.)

Most likely, the share price rise caused by the heavy repurchases will merely bring a new set of even more ignorant investors into the shares, attracted by their apparent “momentum.” That is what has happened to the shares of the FAANGs in 2018 (until the last month) — share repurchases have pushed up their prices and brought in more suckers who are unlikely to be long-term happy shareholders.

Cash dividends are quite different; they represent a return to the shareholders of the profits legitimately earned by the company. Provided the company does not pay out more than it earns, dividends do not significantly increase the company’s leverage or its risk. However, tech companies are generally loath to pay out substantial cash dividends; they prefer to indulge in vast share repurchases for one very good reason: the share repurchases benefit the value of the employees’ stock options, whereas dividends don’t.

It has always been clear that a decade of negative real interest rates would cause excess investment in some area or other, which would eventually bring the overinflated stock market crashing down. Simple souls have been watching the U.S. housing market intensely, but that was never likely to be the principal cause of collapse again, as it was in 2007-08, because the last housing disaster is so recent. To some extent, the tech sector is headed for disaster; both the private-equity-funded sector, with its “dekacorns,” and the publicly quoted sector with its arrogant leftist FAANGs, are clearly overblown in value, have lost most of the purpose for their existence and are due for a massive cull.

Another sector that looks likely to crash, and has been warned about frequently, is the leveraged loan market. Too much capital has gone into speculative private-equity deals, generally poorly managed, and achieving value only by “financial engineering” in the high-yield debt markets. There is no doubt that this sector is also due for massive cathartic shakeout, causing bankruptcies and dismay but ultimately healthy for the U.S. and global economies as a whole.

However, no bubble is as overblown and as unjustified as share buybacks, which have totaled $350 billion in the first 10 months of 2018 alone. These have run at far more than double the level of any previous economic upsurge, at a time when stock prices are more overvalued than they have ever been before — 1929 was a model of sound valuation and caution by comparison — with the favorite tech stock, Radio Corporation of America, trading at only 28 times trailing earnings. They have de-capitalized blue-chip companies, leaving many of them with negative equity (in last year’s piece I detailed the precise position of several; it need hardly be said that another year of frantic buyback activity has left the balance sheets of most of those companies in even worse shape.)

The crash to come will focus therefore on the major names of corporate America, which have hollowed out their balance sheets to goose the prices of their management’s stock options.

Because corporate America provides far more jobs than the housing sector, or even the tech sector, its collapse will be uniquely painful. But that is only a just recompense for a decade of monetary policy that has been uniquely, criminally foolish...

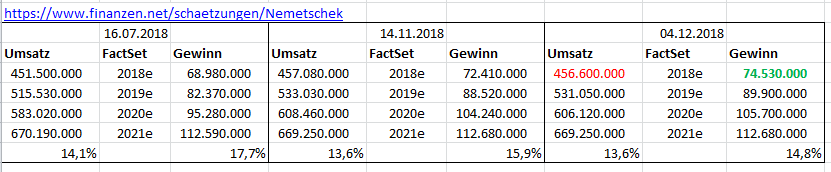

Antwort auf Beitrag Nr.: 59.258.440 von faultcode am 20.11.18 14:16:52

=> nun beim Umsatz etwas weniger (2018e), dafür beim Gewinn mehr

Nemetschek: FactSet-Schätzungen

=> nun beim Umsatz etwas weniger (2018e), dafür beim Gewinn mehr

Stabilus

weiter von hier: https://www.wallstreet-online.de/diskussion/1289357-1-10/cre…=>

...US-Handelsminister Wilbur Ross hat die deutschen Autohersteller zu mehr Produktion in den USA ermahnt. Ziel sei es, das US-Handelsdefizit mit Deutschland bei Autos und Autoteilen zu senken, sagte Ross dem Finanzsender CNBC am Dienstag.

Das gehe hoffentlich mit erhöhter Produktion in den Vereinigten Staaten einher. Wichtig sei es, einen großen Teil der künftigen Elektroautoproduktion in die Staaten zu bekommen, sagte Ross....

aus: https://www.godmode-trader.de/artikel/dax-verschnaufpause-au…

Trading Spotlight

Das ist mal ein wichtiger Punkt, den du da ansprichst. Die ganzen Werte die auf der Aktionär TV hoch und runtergejubelt worden sind und einfach nur ein Traum wahren fallen nun alle in Rekordgeschwindigkeit wieder in sich zusammen.

Gut, dass ich für den Anfang zum Handeln von Nebenwerten erstmal mit einem TEstwikifolio angefangen habe.

Das ist aber auch einer der Gründe, warum ich den Zyklus am Ende sehe. Allgemein die Flucht aus dem Risiko. Bevor ich wieder long gehe möchte ich wieder mehr Risikofreude sehen.

Gut, dass ich für den Anfang zum Handeln von Nebenwerten erstmal mit einem TEstwikifolio angefangen habe.

Das ist aber auch einer der Gründe, warum ich den Zyklus am Ende sehe. Allgemein die Flucht aus dem Risiko. Bevor ich wieder long gehe möchte ich wieder mehr Risikofreude sehen.

Antwort auf Beitrag Nr.: 59.259.454 von faultcode am 20.11.18 15:51:57

=> so ist es

=> auch dieses sehr kräftige Expansion Breakdown wird noch bestätigt werden; die letzten wurden es auch:

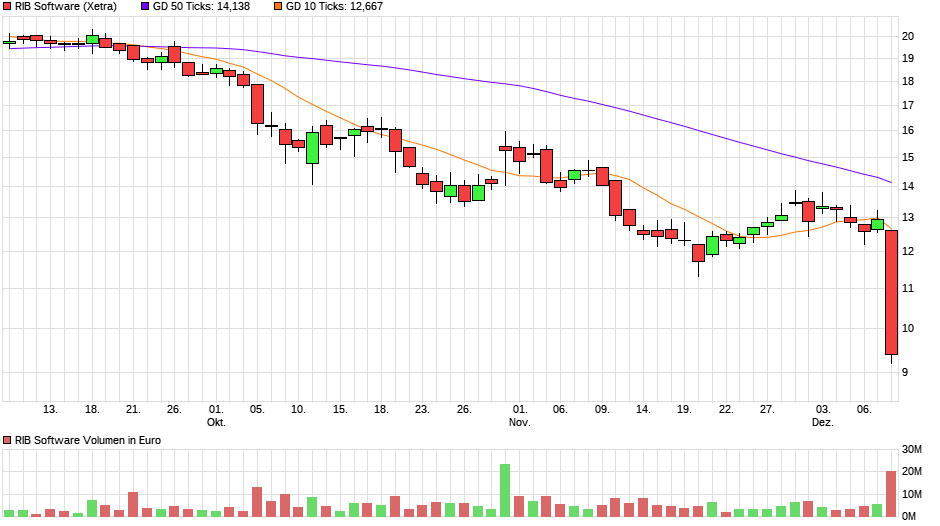

=> nun eben die oben erwähnte "doofe Übernahme":

Rib Software übernimmt US-Gemeinschaftsunternehmen - Aktie stürzt ab

https://www.wallstreet-online.de/nachricht/11075757-roundup-…

=> nachdem das alles hier nun charttechnisch nach unten war und noch immer ist:

• welches Ziel nun?

--> in so einem Fall <EUR10 kann man mittelfristig immer von einer "5-EURO-Aktie" ausgehen

RIB-Crash

20.11.Zitat von faultcode: ...=> darunter sieht es zappenduster aus...

...

=> was tun??

• eine doofe Übernahme?

=> so ist es

=> auch dieses sehr kräftige Expansion Breakdown wird noch bestätigt werden; die letzten wurden es auch:

=> nun eben die oben erwähnte "doofe Übernahme":

Rib Software übernimmt US-Gemeinschaftsunternehmen - Aktie stürzt ab

https://www.wallstreet-online.de/nachricht/11075757-roundup-…

=> nachdem das alles hier nun charttechnisch nach unten war und noch immer ist:

• welches Ziel nun?

--> in so einem Fall <EUR10 kann man mittelfristig immer von einer "5-EURO-Aktie" ausgehen

Antwort auf Beitrag Nr.: 58.637.832 von faultcode am 07.09.18 01:02:31

boiiiiing

so, nun nach unten durchgeknallt nach längerer Zeit mit einem satten Expansion Breakdown diese Woche --> Signal-Bestätigung sollte auch noch kommen:

Antwort auf Beitrag Nr.: 58.218.111 von faultcode am 15.07.18 15:50:21

=> bald ist der TecDAX wieder eingeholt:

...und danach wird Isra unten diesen abtauchen

die Konjunktur!

15.7.18Zitat von faultcode: Beim Thema "Maschinen gucken" scheint die Begeisterung ja keine Grenzen - in Deutschland! - zu kennen:

...

Da das Volumen, auch durch die TecDAX-Mitgliedschaft seit Anfang 2018, z.Z. sehr hoch ist bei Isra Vision, könnte ich mir mittelfristig eine Korrektur so wie zuletzt bei RIB Software vorstellen:

...

=> ...und wie gesagt: der Korrekturgrund wird dann sehr plausibel hinterher geliefert

=> bald ist der TecDAX wieder eingeholt:

...und danach wird Isra unten diesen abtauchen

Antwort auf Beitrag Nr.: 59.433.534 von faultcode am 13.12.18 17:34:12

=> schon auf dem besten Weg dahin - heute mit einem satten Expansion Breakdown, was auch noch demnächst bestätigt werden wird (<2m):

=>

https://www.finanzen.net/nachricht/aktien/rekordgewinn-autom…

=> ...Der Maschinenbauer ISRA VISION hat im vergangenen Geschäftsjahr 2017/18 so viel verdient wie noch nie.

Allerdings wächst das Unternehmen weniger schnell als angekündigt. Die Aktionäre zeigen sich enttäuscht...

=> ja was haben die sich wohl in den letzten 2 Jahren so gedacht? Daß bei einem schnöden Industrie-Zykliker die Bäume in den Himmel wachsen - ganz ohne Wettbewerb quasi?!

=> hinzukommt der seinerzeitige Reverse Split mit den danach vermeintlich "kleinen Zahlen" (bei den Kursen)

=> so was wirkt anschließend in einem Bärenmarkt - obwohl sich "fundamental ja nichts geändert hat" - wie ein Brandbeschleuniger

Isra Vision

Zitat von faultcode: 1...=> bald ist der TecDAX wieder eingeholt:

...

...und danach wird Isra unten diesen abtauchen

=> schon auf dem besten Weg dahin - heute mit einem satten Expansion Breakdown, was auch noch demnächst bestätigt werden wird (<2m):

=>

https://www.finanzen.net/nachricht/aktien/rekordgewinn-autom…

=> ...Der Maschinenbauer ISRA VISION hat im vergangenen Geschäftsjahr 2017/18 so viel verdient wie noch nie.

Allerdings wächst das Unternehmen weniger schnell als angekündigt. Die Aktionäre zeigen sich enttäuscht...

=> ja was haben die sich wohl in den letzten 2 Jahren so gedacht? Daß bei einem schnöden Industrie-Zykliker die Bäume in den Himmel wachsen - ganz ohne Wettbewerb quasi?!

=> hinzukommt der seinerzeitige Reverse Split mit den danach vermeintlich "kleinen Zahlen" (bei den Kursen)

=> so was wirkt anschließend in einem Bärenmarkt - obwohl sich "fundamental ja nichts geändert hat" - wie ein Brandbeschleuniger

Beitrag zu dieser Diskussion schreiben

Investoren beobachten auch:

| Wertpapier | Perf. % |

|---|---|

| +2,55 | |

| +3,22 | |

| +2,48 | |

| +6,97 | |

| -0,80 | |

| -0,87 | |

| +0,08 | |

| -1,07 | |

| -1,34 | |

| -0,98 |

Meistdiskutiert

| Wertpapier | Beiträge | |

|---|---|---|

| 241 | ||

| 93 | ||

| 83 | ||

| 77 | ||

| 73 | ||

| 53 | ||

| 45 | ||

| 38 | ||

| 37 | ||

| 34 |