South Boulder Mines, Australien, Gold / Nickel / Uran - 500 Beiträge pro Seite (Seite 3)

eröffnet am 22.11.06 15:23:08 von

neuester Beitrag 03.06.15 19:05:21 von

neuester Beitrag 03.06.15 19:05:21 von

Beiträge: 1.611

ID: 1.096.074

ID: 1.096.074

Aufrufe heute: 0

Gesamt: 149.482

Gesamt: 149.482

Aktive User: 0

ISIN: AU000000DNK9 · WKN: A14UCJ · Symbol: SBMSF

0,2095

USD

0,00 %

0,0000 USD

Letzter Kurs 27.04.24 Nasdaq OTC

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 2,6900 | +23,96 | |

| 5,1500 | +21,75 | |

| 15,890 | +21,67 | |

| 0,8900 | +17,11 | |

| 0,9000 | +16,13 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 4,5200 | -6,61 | |

| 1,1200 | -6,67 | |

| 10,040 | -7,89 | |

| 0,5700 | -8,06 | |

| 46,98 | -98,00 |

Neue Ergebnisse !

http://stocknessmonster.com/news-item?S=STB&E=ASX&N=488152

http://stocknessmonster.com/news-item?S=STB&E=ASX&N=488152

Antwort auf Beitrag Nr.: 39.380.047 von ogon am 22.04.10 06:48:39

Thursday, April 22, 2010

South Boulder Mines bullish on gold results from Terminator Prospect

http://www.proactiveinvestors.com.au/companies/news/6633/sou…

Thursday, April 22, 2010

South Boulder Mines bullish on gold results from Terminator Prospect

http://www.proactiveinvestors.com.au/companies/news/6633/sou…

Trend nach unten ist beendet. Wer will sollte jetzt @0.74 AUD einsteigen. Die Party ist noch nicht vorbei.

Antwort auf Beitrag Nr.: 39.409.375 von recession am 27.04.10 16:10:23Also ich sehe als Schlusskurs 0,80 AUD, aber ansonsten sollst du recht haben

STB news 27.04.2010

27/04/2010 Investor Presentation April 2010

http://asx.com.au/asxpdf/20100427/pdf/31pz0720c73p98.pdf

27/04/2010 Investor Presentation April 2010

http://asx.com.au/asxpdf/20100427/pdf/31pz0720c73p98.pdf

Trading Spotlight

Antwort auf Beitrag Nr.: 39.409.719 von Karle45 am 27.04.10 16:38:28Ich habe eher Zukunft gemeint @0.74. Nach der bounce gibt es wieder versuch den tief zu testen. in diesem Fall tief war 0.73 AUD. Wenn wir nicht unter 0.73 AUD gehen dann einsteigen @0.74 wird sich auszahlen.

Wann ist endlich der Boden gefunden und eine Gegenbewegung festzustellen.

Gute Nachrichten scheinen momentan zu verpuffen oder waren die letzten Ergebnisse des Terminator Prospects nicht gut.

Gute Nachrichten scheinen momentan zu verpuffen oder waren die letzten Ergebnisse des Terminator Prospects nicht gut.

Antwort auf Beitrag Nr.: 39.448.817 von Karle45 am 03.05.10 23:25:56

Hallo,

heute bei 0,60 A Cent geschlossen sollte nun aber der Boden gefunden sein.

Jetzt heist es abwarten bis wieder bessere Zeiten kommen.

Auf längere Zeit ( 6-12 Monate ) werden Rohstoffe das Rennen

machen und mit South Boulder hat man keine schlechtes Invest.

Wie heute im Handelsblatt geschrieben beginnt erst jetzt das

Rennen um Rohstoffe und wir in Europa kommen immer zu spät,

China ist oder war schon da.

Die Stunde der Rohstoffe kommt noch.

Montekaolino

Hallo,

heute bei 0,60 A Cent geschlossen sollte nun aber der Boden gefunden sein.

Jetzt heist es abwarten bis wieder bessere Zeiten kommen.

Auf längere Zeit ( 6-12 Monate ) werden Rohstoffe das Rennen

machen und mit South Boulder hat man keine schlechtes Invest.

Wie heute im Handelsblatt geschrieben beginnt erst jetzt das

Rennen um Rohstoffe und wir in Europa kommen immer zu spät,

China ist oder war schon da.

Die Stunde der Rohstoffe kommt noch.

Montekaolino

Antwort auf Beitrag Nr.: 39.449.397 von Montekaolino am 04.05.10 08:32:25Stimmt. Wenn man bedenkt wie wenig cbr index geklettert ist konnte man sagen das war eine Baer rally bis jetzt.

http://index.onvista.de/indizes/crb-index/kurs

http://index.onvista.de/indizes/crb-index/kurs

Der Grund für die Börsen-Abschläge der australischen Minengesellschaften ist die geplante Besteuerung :

Mine stocks plunge as PM defends tax

The Rudd Government's decision to tax mining companies' "super profits" triggered a $6.7 billion plunge in major mining stocks as investors became nervous about the financial impact of the changes.

http://au.news.yahoo.com/thewest/a/-/breaking/7159058/mine-s…

Mine stocks plunge as PM defends tax

The Rudd Government's decision to tax mining companies' "super profits" triggered a $6.7 billion plunge in major mining stocks as investors became nervous about the financial impact of the changes.

http://au.news.yahoo.com/thewest/a/-/breaking/7159058/mine-s…

Habe schlechtes Gefuhl hier, dass wir morgen unter 0.6 gehen. Aber nun wirklich 0.5 AUD sollte doch halten. Insiders haben doch viel hoher gekauft. Muss jetzt zukaufen unter 0.6.

Antwort auf Beitrag Nr.: 39.449.817 von StockExplorer am 04.05.10 09:45:12sollten die wirklich eine zusätzliche Besteuerung von 70% (auf was?) planen ???

Antwort auf Beitrag Nr.: 39.465.907 von prof19 am 06.05.10 07:45:15die geplante Besteuerung ist

1. noch lange nicht beschlossen

2. dürfte South Boulder Mines kaum treffen.

Hier zeigt sich, dass auch die Aussie-Politiker unseren Politikern in nichts nachstehen. Ohne Sachverstand wird erst einmal etwas propagiert und dann darüber nachgedacht. Die Börsenwertverluste der Minengesellschaften BHP und RIO gehen inzwischen in die Milliarden.

Ich gehe davon aus, dass die letzten Worte noch nicht gesprochen sind.

Dazu ein Aussie-Kommentar :

Value Now In BHP And Rio?

BY GREG PEEL - 06/05/2010

Here we are four days on from the government's announcement that it would look to implement the resources super-profits tax (RSPT) recommended in the Henry Tax Review, and still the market is battling to understand the detail. Of most concern is just exactly what impact on discounted valuation the tax will have on Australia's listed resource companies, and in particular on the two biggest players, BHP Billiton (BHP) and Rio Tinto ((RIO)). Said Citi in a report this morning:

“The extent of the impact seems to vary quite markedly across the market, reflecting commodity price assumptions and ambiguity over exactly how the RSPT works”.

The first variance factor is not related to the tax – differing assumptions on longer term commodity prices among analysts have always extrapolated into wildly varying discount valuations and hence target prices and recommendations. However, given profits are based on prices, and the RSPT taxes profits (unlike the existing royalty system which is imposed on production), in fact the new tax adds a new dimension of variance into analysts' valuation models depending on their initial price forecasts.

Throw in the second point of variance – ongoing ambiguity over the RSPT itself – and we have a recipe for simple uncertainty. It is uncertainty more than anything which drives investors to exit stock positions. If the tax is bad but if we know just how bad then prices can adjust accordingly and be done with it. But we just don't quite know yet how bad, or not so bad, the implications of the tax really are.

And, of course, we don't know whether or not the RSPT will be watered down (my assumption is Rudd started from the worst point to leave the door open for concessions) before it becomes legislation, or whether it will ever become legislation, or whether the Rudd government will be around in 2011 anyway. More uncertainty.

Complete commentary :

http://www.sharecafe.com.au/fnarena_news.asp?a=AV&ai=16616

1. noch lange nicht beschlossen

2. dürfte South Boulder Mines kaum treffen.

Hier zeigt sich, dass auch die Aussie-Politiker unseren Politikern in nichts nachstehen. Ohne Sachverstand wird erst einmal etwas propagiert und dann darüber nachgedacht. Die Börsenwertverluste der Minengesellschaften BHP und RIO gehen inzwischen in die Milliarden.

Ich gehe davon aus, dass die letzten Worte noch nicht gesprochen sind.

Dazu ein Aussie-Kommentar :

Value Now In BHP And Rio?

BY GREG PEEL - 06/05/2010

Here we are four days on from the government's announcement that it would look to implement the resources super-profits tax (RSPT) recommended in the Henry Tax Review, and still the market is battling to understand the detail. Of most concern is just exactly what impact on discounted valuation the tax will have on Australia's listed resource companies, and in particular on the two biggest players, BHP Billiton (BHP) and Rio Tinto ((RIO)). Said Citi in a report this morning:

“The extent of the impact seems to vary quite markedly across the market, reflecting commodity price assumptions and ambiguity over exactly how the RSPT works”.

The first variance factor is not related to the tax – differing assumptions on longer term commodity prices among analysts have always extrapolated into wildly varying discount valuations and hence target prices and recommendations. However, given profits are based on prices, and the RSPT taxes profits (unlike the existing royalty system which is imposed on production), in fact the new tax adds a new dimension of variance into analysts' valuation models depending on their initial price forecasts.

Throw in the second point of variance – ongoing ambiguity over the RSPT itself – and we have a recipe for simple uncertainty. It is uncertainty more than anything which drives investors to exit stock positions. If the tax is bad but if we know just how bad then prices can adjust accordingly and be done with it. But we just don't quite know yet how bad, or not so bad, the implications of the tax really are.

And, of course, we don't know whether or not the RSPT will be watered down (my assumption is Rudd started from the worst point to leave the door open for concessions) before it becomes legislation, or whether it will ever become legislation, or whether the Rudd government will be around in 2011 anyway. More uncertainty.

Complete commentary :

http://www.sharecafe.com.au/fnarena_news.asp?a=AV&ai=16616

Exploration News

First Two Holes At Allana’s Ethiopian Potash Project Confirm…

19/05/2010

First Two Holes At Allana's Ethiopian Potash Project Confirm The Presence Of Potash Beds Close To Surface-Positive.

For more information please click the link provided.

http://www.southbouldermines.com.au/images/uploads/05_18_10_…

First Two Holes At Allana’s Ethiopian Potash Project Confirm…

19/05/2010

First Two Holes At Allana's Ethiopian Potash Project Confirm The Presence Of Potash Beds Close To Surface-Positive.

For more information please click the link provided.

http://www.southbouldermines.com.au/images/uploads/05_18_10_…

eine interessante Zusammenfassung über South Boulder Mines von wise-owl.com :

http://www.southbouldermines.com.au/images/uploads/STB_Resea…

----

Das South Boulder Mines Media Center hat jetzt eine deutsche Abteilung :

http://www.southbouldermines.com.au/media/proactive_deutsch/

http://www.southbouldermines.com.au/images/uploads/STB_Resea…

----

Das South Boulder Mines Media Center hat jetzt eine deutsche Abteilung :

http://www.southbouldermines.com.au/media/proactive_deutsch/

STB news 03.06.2010

DUKETON Ni JV EXPLORATION UPDATE

Mining Lease application lodged over the C2 and Rosie Ni-Cu-

PGE Prospects;

Plans for 3-4 drill rig follow-up drill program being finalised.

South Boulder Mines Ltd (ASX: STB) is pleased to announce that together with

JV partner Independence Group NL (ASX: IGO) an application has been made

to the Department of Mines and Petroleum (DMP) for a Mining Lease that

covers the highly significant Ni-Cu-PGE mineralisation discovered at the C2

and Rosie Prospects, within the Duketon Nickel Project (Figure 1).

This is a significant milestone for the Duketon JV partners and is a result of

recent exploration success including the previously announced downhole

massive sulphide drill intercept in hole TBDD098 of:

5.20m @ 9.13% Ni, 1.09% Cu, 0.21% Co and 7.09g/t PGE’s from

599.71m.

complete report :

http://www.southbouldermines.com.au/images/uploads/853296.pd…

DUKETON Ni JV EXPLORATION UPDATE

Mining Lease application lodged over the C2 and Rosie Ni-Cu-

PGE Prospects;

Plans for 3-4 drill rig follow-up drill program being finalised.

South Boulder Mines Ltd (ASX: STB) is pleased to announce that together with

JV partner Independence Group NL (ASX: IGO) an application has been made

to the Department of Mines and Petroleum (DMP) for a Mining Lease that

covers the highly significant Ni-Cu-PGE mineralisation discovered at the C2

and Rosie Prospects, within the Duketon Nickel Project (Figure 1).

This is a significant milestone for the Duketon JV partners and is a result of

recent exploration success including the previously announced downhole

massive sulphide drill intercept in hole TBDD098 of:

5.20m @ 9.13% Ni, 1.09% Cu, 0.21% Co and 7.09g/t PGE’s from

599.71m.

complete report :

http://www.southbouldermines.com.au/images/uploads/853296.pd…

Antwort auf Beitrag Nr.: 39.624.982 von StockExplorer am 03.06.10 09:26:18sehr gut! da gehts bald richtig rund!

Antwort auf Beitrag Nr.: 39.625.127 von IIBI am 03.06.10 09:49:19was erwartest du und in welchem Zeitrahmen?

STB news 15.06.2010

Durch Wandlung von 2,150,000 Optionen in Aktien erhöht Sprott Asset Management LP (Canada) seinen Anteil an STB von 12,1% auf 14,0%.

Dadurch erhält South Boulder Mines 1,075 Mill. AUD Cash

http://asx.com.au/asxpdf/20100615/pdf/31qv91s1wjgsw0.pdf

http://www.asx.com.au/asxpdf/20100615/pdf/31qtrxydp7b6mf.pdf

Durch Wandlung von 2,150,000 Optionen in Aktien erhöht Sprott Asset Management LP (Canada) seinen Anteil an STB von 12,1% auf 14,0%.

Dadurch erhält South Boulder Mines 1,075 Mill. AUD Cash

http://asx.com.au/asxpdf/20100615/pdf/31qv91s1wjgsw0.pdf

http://www.asx.com.au/asxpdf/20100615/pdf/31qtrxydp7b6mf.pdf

Antwort auf Beitrag Nr.: 39.682.218 von StockExplorer am 15.06.10 09:57:02jupp auch gerade gelesen! Sehr gut, wenn Sprott hier weiter mitmischt!

STB news 24.06.2010

Colluli Potash Drilling Commences

South Boulder Mines Ltd (ASX: STB) is pleased to announce that

diamond drilling has commenced at it’s potentially “World Class” 100%

owned Colluli Potash Project in Eritrea.

This is a significant milestone for South Boulder and represents the first

drilling program undertaken on the project in 42 years. The 4-5 hole

program is designed to confirm historic shallow potash drilling intercepts

and provide data to complete an initial JORC resource calculation. The

program is expected to continue for the next 6-8 weeks.

“The Colluli Potash Project exhibits some outstanding potential and we

are looking forward to generating some exciting results,” said South

Boulder Mines Managing Director, Lorry Hughes.

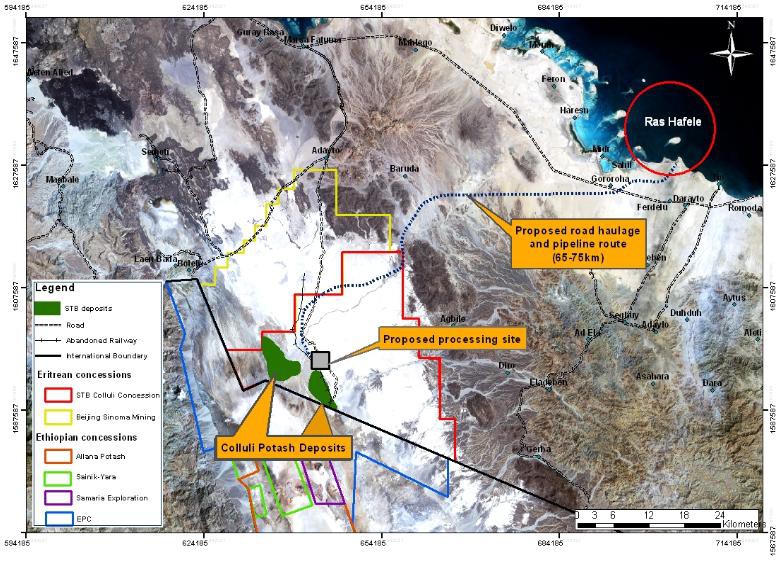

“The key features of the Project are that we are only 70kms from the

coast, there is potential to utilise low cost solution mining and solar

evaporation and the historic mineralisation is shallow. It is hard to find a

potash project across the globe that has these features.”

“High grade ‘Houston Formation’ potash bearing horizons have been

intersected up to 45m thick in drilling only 15kms from Colluli at the

historic and world class ‘Musley Potash Project’.”

“Furthermore Allana Potash Corp. (TSX-V: AAA) at their ‘Ethiopia Potash

Project’ which contains part of the Musley potash mineralisation, have

recently confirmed significant shallow potash mineralisation. In a news

release to the TSX-V on the 15th June 2010, Allana Potash Corp, report

that chemical analyses confirmed 5.5m @ 25.8% KCl including 2.0m @

34.8% KCl in hole DK-10-02.”

“This is a great result for Allana and bodes well for South Boulder also,

as it further confirms the prospectivity of the basin. Importantly buried

potash mineralisation is typically laterally extensive so we are expecting

to confirm extensions to this mineralisation within our project area.”

Further details about the drilling program and the Colluli Potash Project

are detailed in the ASX announcement dated 27th April 2010.

Results from the program as well as progressive updates will be released

as the information come to hand.

http://asx.com.au/asxpdf/20100624/pdf/31qzkynfg1dksb.pdf

Colluli Potash Drilling Commences

South Boulder Mines Ltd (ASX: STB) is pleased to announce that

diamond drilling has commenced at it’s potentially “World Class” 100%

owned Colluli Potash Project in Eritrea.

This is a significant milestone for South Boulder and represents the first

drilling program undertaken on the project in 42 years. The 4-5 hole

program is designed to confirm historic shallow potash drilling intercepts

and provide data to complete an initial JORC resource calculation. The

program is expected to continue for the next 6-8 weeks.

“The Colluli Potash Project exhibits some outstanding potential and we

are looking forward to generating some exciting results,” said South

Boulder Mines Managing Director, Lorry Hughes.

“The key features of the Project are that we are only 70kms from the

coast, there is potential to utilise low cost solution mining and solar

evaporation and the historic mineralisation is shallow. It is hard to find a

potash project across the globe that has these features.”

“High grade ‘Houston Formation’ potash bearing horizons have been

intersected up to 45m thick in drilling only 15kms from Colluli at the

historic and world class ‘Musley Potash Project’.”

“Furthermore Allana Potash Corp. (TSX-V: AAA) at their ‘Ethiopia Potash

Project’ which contains part of the Musley potash mineralisation, have

recently confirmed significant shallow potash mineralisation. In a news

release to the TSX-V on the 15th June 2010, Allana Potash Corp, report

that chemical analyses confirmed 5.5m @ 25.8% KCl including 2.0m @

34.8% KCl in hole DK-10-02.”

“This is a great result for Allana and bodes well for South Boulder also,

as it further confirms the prospectivity of the basin. Importantly buried

potash mineralisation is typically laterally extensive so we are expecting

to confirm extensions to this mineralisation within our project area.”

Further details about the drilling program and the Colluli Potash Project

are detailed in the ASX announcement dated 27th April 2010.

Results from the program as well as progressive updates will be released

as the information come to hand.

http://asx.com.au/asxpdf/20100624/pdf/31qzkynfg1dksb.pdf

Rohstoffe-Go Exklusiv - & Wirtschaftsnews - 25.06.10

Australien: Die Steuer-Wende scheint nun möglich

http://www.rohstoffe-go.de/rohstoff/rohstoffe-go-exklusiv/be…

Shallow Potash Intercepted

South Boulder Mines Ltd (ASX: STB) is very pleased to announce that

diamond drilling has confirmed the presence of potash at the Colluli

Potash Project in Eritrea.

The first hole of a 4-5 hole program has intercepted the upper portion of a

potash layer starting at ~65.00m vertical depth. White carnallite potash

mineralisation has been identified from visual and physical field tests.

The full chemical composition of the mineralised intervals cannot be

determined until laboratory chemical analyses can be performed.

Significant core recovery issues were encountered at a depth of

approximately 70.80m and drilling was temporarily halted in the potash

zone, in order to identify and rectify the problems.

The recovery issues have now been assessed and an updated drilling

mud plan has been implemented in order to maximise core recovery.

Drilling recommenced on the 4th of July.

As at the time of this report a 6.5m interval of potash rich mineralisation

was intercepted from 65.00m which included ~1.50m of core loss at the

base of the interval.

“We are having a few teething problems with our drilling muds as this is

the first hole of the program. It wasn’t unexpected as potash drilling is

technically involved. I am incredibly pleased with the early success of

this first hole though”, commented South Boulder Mines Managing

Director, Lorry Hughes from the Colluli site.

‘We were expecting potash, however, it was a very nice surprise to get it

in our first hole and so shallow. We will continue to drill until we get

conclusive results and confirm the visual identification of the minerals by

chemical analyses.”

Further details about the drilling program and the Colluli Potash Project

are detailed in the recent ASX announcements dated 24th June and 27th

April 2010.

Results from the program as well as progressive updates will be released

as the information come to hand.

http://www.asx.com.au/asxpdf/20100706/pdf/31r5ysb2qz56n8.pdf

South Boulder Mines Ltd (ASX: STB) is very pleased to announce that

diamond drilling has confirmed the presence of potash at the Colluli

Potash Project in Eritrea.

The first hole of a 4-5 hole program has intercepted the upper portion of a

potash layer starting at ~65.00m vertical depth. White carnallite potash

mineralisation has been identified from visual and physical field tests.

The full chemical composition of the mineralised intervals cannot be

determined until laboratory chemical analyses can be performed.

Significant core recovery issues were encountered at a depth of

approximately 70.80m and drilling was temporarily halted in the potash

zone, in order to identify and rectify the problems.

The recovery issues have now been assessed and an updated drilling

mud plan has been implemented in order to maximise core recovery.

Drilling recommenced on the 4th of July.

As at the time of this report a 6.5m interval of potash rich mineralisation

was intercepted from 65.00m which included ~1.50m of core loss at the

base of the interval.

“We are having a few teething problems with our drilling muds as this is

the first hole of the program. It wasn’t unexpected as potash drilling is

technically involved. I am incredibly pleased with the early success of

this first hole though”, commented South Boulder Mines Managing

Director, Lorry Hughes from the Colluli site.

‘We were expecting potash, however, it was a very nice surprise to get it

in our first hole and so shallow. We will continue to drill until we get

conclusive results and confirm the visual identification of the minerals by

chemical analyses.”

Further details about the drilling program and the Colluli Potash Project

are detailed in the recent ASX announcements dated 24th June and 27th

April 2010.

Results from the program as well as progressive updates will be released

as the information come to hand.

http://www.asx.com.au/asxpdf/20100706/pdf/31r5ysb2qz56n8.pdf

STB news 30.07.2010

Quarterly Operations Report

http://www.asx.com.au/asxpdf/20100730/pdf/31rm2gsjdmz9xf.pdf

Appendix 5B

http://www.asx.com.au/asxpdf/20100730/pdf/31rm3dy46fgsdn.pdf

Quarterly Operations Report

http://www.asx.com.au/asxpdf/20100730/pdf/31rm2gsjdmz9xf.pdf

Appendix 5B

http://www.asx.com.au/asxpdf/20100730/pdf/31rm3dy46fgsdn.pdf

Antwort auf Beitrag Nr.: 39.901.503 von StockExplorer am 30.07.10 09:30:44alles im Lot! bin auf die ersten Potash Ergebnisse mal gespannt und natürlich, wenn IGO auf dem Nickelprojekt groß loslegt!

Schöner Anstieg heute in Aussieland, deutlich erhöhtes Volumen.

Scheinbar kommt eine gute Meldung und wie immer wissen einige wieder mehr und früher als andere.

Aber das soll uns wohl recht sein, solange der Kurs steigt.

Scheinbar kommt eine gute Meldung und wie immer wissen einige wieder mehr und früher als andere.

Aber das soll uns wohl recht sein, solange der Kurs steigt.

Antwort auf Beitrag Nr.: 40.002.027 von Karle45 am 18.08.10 05:59:35der Anstieg dürfte an folgendem Bericht liegen :

Aug. 17, 2010, 12:05 p.m. EDT :

Potash Corp. soars as BHP Billiton's $38.6 billion bid rejected

Stock hits highest in two years; shareholder rights plan adopted

By Aude Lagorce and Christopher Hinton, MarketWatch

NEW YORK (MarketWatch) -- Potash Corp. of Saskatchewan Inc. shares hit a two-year high after the fertilizer company said Tuesday it rejected a $38.6 billion takeover bid from BHP Billiton and rebuffed suggestions it enter into formal negotiations with the mining giant.

"This unsolicited proposal we received so grossly undervalues the company -- I mean, it's so far beyond opportunistic, that it really was not a constructive basis for negotiation," said William Doyle, Potash Corp.'s CEO, on a conference call with analysts.

siehe den ganzen Bericht und Kommentare :

http://www.marketwatch.com/story/potash-soars-as-board-rejec…

Aug. 17, 2010, 12:05 p.m. EDT :

Potash Corp. soars as BHP Billiton's $38.6 billion bid rejected

Stock hits highest in two years; shareholder rights plan adopted

By Aude Lagorce and Christopher Hinton, MarketWatch

NEW YORK (MarketWatch) -- Potash Corp. of Saskatchewan Inc. shares hit a two-year high after the fertilizer company said Tuesday it rejected a $38.6 billion takeover bid from BHP Billiton and rebuffed suggestions it enter into formal negotiations with the mining giant.

"This unsolicited proposal we received so grossly undervalues the company -- I mean, it's so far beyond opportunistic, that it really was not a constructive basis for negotiation," said William Doyle, Potash Corp.'s CEO, on a conference call with analysts.

siehe den ganzen Bericht und Kommentare :

http://www.marketwatch.com/story/potash-soars-as-board-rejec…

Tages-Chart STB (aktualisiert sich automatisch - real time)

Antwort auf Beitrag Nr.: 40.002.042 von StockExplorer am 18.08.10 06:41:41sehr schön!!

STB news 19/08/2010

Investor Presentation

http://www.asx.com.au/asxpdf/20100819/pdf/31rzcc20xcgs5q.pdf

Investor Presentation

http://www.asx.com.au/asxpdf/20100819/pdf/31rzcc20xcgs5q.pdf

Antwort auf Beitrag Nr.: 40.009.674 von StockExplorer am 19.08.10 06:22:51Von meinem Informanten in Perth erhielt ich ein Email bzgl. der Potash-Exploration in Eritrea. Ein Auszug aus dem Text :

Have a look at today’s investor update, announced to the ASX, and read by virtually no one. Some key points to look for:

* The Potash drilling has just identified a discovery in what is now 3 holes, over 4.5 sq km’s, at very shallow (ie open pittable, low cost) depths. This is likely to equate to Potash in the 100’s of millions of tonnes.

* BHP (who were obviously very active in Potash yesterday, with their $43 billion bid for Potash Corporation) have tenements just over the border in Ethiopia – refer to the map

* Assay results will be out by the end of the month, whilst we don’t know what they are yet, Allana’s recent results are a good indication as it is likely to be the same stuff – from 12% to 35% Potash.

* The drilling program has been extended from an initial 3 holes to 10 – 12 holes, meaning ongoing news.

* Ercosplan is the consultant geologist, a well known and respected German group

* The shipping advantage they have over others to major markets (particularly India) is very significant – refer to the map, but also to the Potash section of Potash Corporation’s website to see the significance of this.

http://www.potashcorp.com/industry_overview/2009/media/pdf/P…

Have a look at today’s investor update, announced to the ASX, and read by virtually no one. Some key points to look for:

* The Potash drilling has just identified a discovery in what is now 3 holes, over 4.5 sq km’s, at very shallow (ie open pittable, low cost) depths. This is likely to equate to Potash in the 100’s of millions of tonnes.

* BHP (who were obviously very active in Potash yesterday, with their $43 billion bid for Potash Corporation) have tenements just over the border in Ethiopia – refer to the map

* Assay results will be out by the end of the month, whilst we don’t know what they are yet, Allana’s recent results are a good indication as it is likely to be the same stuff – from 12% to 35% Potash.

* The drilling program has been extended from an initial 3 holes to 10 – 12 holes, meaning ongoing news.

* Ercosplan is the consultant geologist, a well known and respected German group

* The shipping advantage they have over others to major markets (particularly India) is very significant – refer to the map, but also to the Potash section of Potash Corporation’s website to see the significance of this.

http://www.potashcorp.com/industry_overview/2009/media/pdf/P…

Antwort auf Beitrag Nr.: 40.012.954 von StockExplorer am 19.08.10 14:19:45

Warten wir mal ab was da ende August kommt.

Bin wirklich gespannt wie die Ergebnisse werden.

Montekaolino

Warten wir mal ab was da ende August kommt.

Bin wirklich gespannt wie die Ergebnisse werden.

Montekaolino

....mit POT- übernahmeangebot von BHP ist der gesamte agri- sektor

wieder im focus der investoren.......

SK heute auf TH...aud 0,70

wieder im focus der investoren.......

SK heute auf TH...aud 0,70

chart sieht super aus!! halte weiter!

Aus "The Australian" vom 23.08.2010

Potash mania fertilises local hopes

NOTHING like a bit of irrational exuberance in the market, and we saw it again last week on the subject of potash.

On the back of the bid by BHP Billiton (BHP) for Canada's Potash Corporation of Saskatchewan, investors dived into local stocks. Reward Minerals (RWD) rose 15.6 per cent, Elemental Minerals (ELM) was up 10.9 per cent, and a further 26.7 per cent the next day, South Boulder Mines (STB) rose by 13.6 per cent, Red Metal (RDM) by 18.2 per cent and Rum Jungle Uranium (RUM) -- which had the presence of mind to put out an ASX announcement doing nothing more than reminding people it had some early stage potash ground -- lifted by 14.3 per cent.

complete report

http://www.theaustralian.com.au/business/potash-mania-fertil…

Potash mania fertilises local hopes

NOTHING like a bit of irrational exuberance in the market, and we saw it again last week on the subject of potash.

On the back of the bid by BHP Billiton (BHP) for Canada's Potash Corporation of Saskatchewan, investors dived into local stocks. Reward Minerals (RWD) rose 15.6 per cent, Elemental Minerals (ELM) was up 10.9 per cent, and a further 26.7 per cent the next day, South Boulder Mines (STB) rose by 13.6 per cent, Red Metal (RDM) by 18.2 per cent and Rum Jungle Uranium (RUM) -- which had the presence of mind to put out an ASX announcement doing nothing more than reminding people it had some early stage potash ground -- lifted by 14.3 per cent.

complete report

http://www.theaustralian.com.au/business/potash-mania-fertil…

vor 5 AUD kein Stück!

...SPROTT erhöht seinen anteil weiter....

http://www.asx.com.au/asxpdf/20100908/pdf/31sd12bn57vwdt.pdf

Antwort auf Beitrag Nr.: 40.116.092 von hbg55 am 08.09.10 10:17:46die wissen schon warum!!!!

Investor Update from South Boulder Mines

Exploration News - Drilling Potash and Nickel -

http://www.southbouldermines.com.au/images/uploads/889177.pd…

Exploration News - Drilling Potash and Nickel -

http://www.southbouldermines.com.au/images/uploads/889177.pd…

1 AUD konnte noch mal kommen. Noch einige ueberraschungen vor uns und auch Potash Preisse sollte anziehen.

Antwort auf Beitrag Nr.: 40.272.865 von recession am 06.10.10 12:06:48Könnte schneller gehen als du denkst. Nach Tagen des stetigen Anstiegs, heute um fast 10 % hoch in Australien.

Was kommt ???

Was kommt ???

Antwort auf Beitrag Nr.: 40.286.189 von Karle45 am 08.10.10 06:29:24Sieht sogar aus, dass es deutlich ueber 1 AUD gehen wird wenn das so mit kleinen volumen nach oben geht. Wa macht denn diese Aktie wenn volume anziehen wird. Bin nicht mehr sicher ob ich jetzt @1 AUD verkaufen soll? Allerdings weiss ich nicht was fuer ueberraschungen kommen. Naja da waere level 2 schon hilfreich.

Tradinghalt in Australien wegen kommender Bohrergebnisse !!!

Schätze sie werden am Montag veröffentlicht. Mal sehen wo wir danach stehen.

Schätze sie werden am Montag veröffentlicht. Mal sehen wo wir danach stehen.

Die Bohrergebnisse aus Eritrea sind wie erwartet da und sehr gut. Es bestätigt sich eines der größten Potash Vorkommen in der Welt, das relativ nah an der Oberfläche liegt.

Handel wurde wieder aufgenommen, Anstieg um ca 10 %.

So kanns weiter gehen.

Handel wurde wieder aufgenommen, Anstieg um ca 10 %.

So kanns weiter gehen.

OUTSTANDING ASSAYS CONFIRM SHALLOW POTASH at the COLLULI POTASH DEPOSIT

• First true width assays from hole Col-004 confirm extensive shallow

potash at Colluli including;

• 7.72m of Sylvinite @ 25% KCl (16% K2O) from 28.68m depth;

• First true width assays from hole Col-004 confirm extensive shallow

potash at Colluli including;

• 7.72m of Sylvinite @ 25% KCl (16% K2O) from 28.68m depth;

Antwort auf Beitrag Nr.: 40.362.693 von StockExplorer am 21.10.10 06:39:59wieder Anstieg unter hohem Volumen in Australien, die Marke von 1 AUD wurde geknackt.

Glückwunsch an alle, die schon länger investiert sind.

Glückwunsch an alle, die schon länger investiert sind.

Antwort auf Beitrag Nr.: 40.362.729 von Karle45 am 21.10.10 06:58:09

Ja so ist das heute hat mein Limit bei 0,98 gegriffen seit drei Jahren dabei

man soll nicht unzufrieden sein.

Gruß

Montekaolino

Ja so ist das heute hat mein Limit bei 0,98 gegriffen seit drei Jahren dabei

man soll nicht unzufrieden sein.

Gruß

Montekaolino

Antwort auf Beitrag Nr.: 40.362.815 von Montekaolino am 21.10.10 07:39:27Endlich mal ein explorer der durchgestartet ist.bin bei 0,15 rein

Antwort auf Beitrag Nr.: 40.367.909 von wucht am 21.10.10 17:53:01hatte um 75 cent einige gegeben, den rest halte ich bis zum bitteren Ende, das hoffentlich bei 2 oder 3$ liegt!

Antwort auf Beitrag Nr.: 40.367.942 von IIBI am 21.10.10 17:56:50Als bitter würde ich das nicht bezeichnen.

Auch heute wieder Anstieg um 10 %, auch das Volumen steigt täglich an

Auch heute wieder Anstieg um 10 %, auch das Volumen steigt täglich an

Antwort auf Beitrag Nr.: 40.370.846 von Karle45 am 22.10.10 07:40:37moin k45/ ALLLLL

jooo, ist für wahr erstaunlich mit welcher dynamik die ONE gekanckt wurde

und ist unter andrem dem umstand geschuldet, daß sich von den 67,6mio shares

eeeeeh nur noch knapp 40% im freien handel befinden.....dazu gehören auch MEINE paaaar

und werde diese keinesfalls vor aud 2,- aus der hand geben - will sagen, der

KAUF- druck nimmt zu und sollte uns noch in schöööööne regionen bringen können

jooo, ist für wahr erstaunlich mit welcher dynamik die ONE gekanckt wurde

und ist unter andrem dem umstand geschuldet, daß sich von den 67,6mio shares

eeeeeh nur noch knapp 40% im freien handel befinden.....dazu gehören auch MEINE paaaar

und werde diese keinesfalls vor aud 2,- aus der hand geben - will sagen, der

KAUF- druck nimmt zu und sollte uns noch in schöööööne regionen bringen können

Aus dem letzten ABID Report :

Due Diligence and Valuation Report

Arrowhead Code: 25-01-01

Coverage initiated: 20 Oct 2010

This document: 20 Oct 2010

Fair share value bracket: AS$1.17 to AS$8.08

Share price on date: AS$ 0.93

Analyst

Thomas Renaud Saravanan Sekar

thomas.renaud@arrowheadbid.com

+1 (212) 619 6889

complete report:

http://www.southbouldermines.com.au/images/uploads/101020_SO…

Due Diligence and Valuation Report

Arrowhead Code: 25-01-01

Coverage initiated: 20 Oct 2010

This document: 20 Oct 2010

Fair share value bracket: AS$1.17 to AS$8.08

Share price on date: AS$ 0.93

Analyst

Thomas Renaud Saravanan Sekar

thomas.renaud@arrowheadbid.com

+1 (212) 619 6889

complete report:

http://www.southbouldermines.com.au/images/uploads/101020_SO…

02.11.2010 STB news

Dear Investor,

Year on year, Mines and Money continues to succeed in providing the best forum for miners and financiers to meet, exchange ideas, learn, debate, make and cement business relationships. Now in its eighth year,2010 promises to deliver another successful event, with a conference programme featuring a broad range of expert speakers covering a wide spectrum of issues concerning the miner and mining financier in today’s business climate.

Lorry Hughes will be speaking on behalf of South Boulder Mines Ltd at this event. To view the full up-to-date brochure please click the link provided.

http://www.southbouldermines.com.au/images/uploads/Mines_and…

Dear Investor,

Year on year, Mines and Money continues to succeed in providing the best forum for miners and financiers to meet, exchange ideas, learn, debate, make and cement business relationships. Now in its eighth year,2010 promises to deliver another successful event, with a conference programme featuring a broad range of expert speakers covering a wide spectrum of issues concerning the miner and mining financier in today’s business climate.

Lorry Hughes will be speaking on behalf of South Boulder Mines Ltd at this event. To view the full up-to-date brochure please click the link provided.

http://www.southbouldermines.com.au/images/uploads/Mines_and…

Bestätigung der guten Ergebnisse in Eritrea.

Handel wieder aufgenommen, Anstieg um 11 %, in der Spitze waren es sogar schon mehr.

Handel wieder aufgenommen, Anstieg um 11 %, in der Spitze waren es sogar schon mehr.

STB news 09.11.2010

FURTHER DRILL RESULTS CONFIRM COLLULI AS WORLD’S SHALLOWEST POTASH DEPOSIT

• Assay results confirm extensive shallow potash over a 4.5km2 area with mineralisation open in all directions;

• Initial exploration target is to define 300mt-500mt of potash ores with average grades from 21 – 25% KCl. The potential quantity and grade is conceptual in nature and there has been insufficient exploration to define a Mineral Resource and that it is uncertain if further exploration will result in the determination of a Mineral Resource.

• Scoping study to evaluate a low cap-ex and op-ex potash from an open pit mine has commenced;

• Hole Col-001 intersected a total thickness of 28.33m of potash including 8.63m of sylvinitite + carnallitite @ 21% KCl from 59.17m which includes higher grade intervals of;

1.96m of sylvinitite @ 26% KCl from 59.17m and;

4.43m of sylvinitite + carnallitite @ 27% KCl from 63.37m and;

1.35m of sylvinitite @ 39% KCl from 63.85m plus;

19.70m of carnallitite + kainitite @ 16% KCl from 83.78m incl;

9.31m of kainitite @ 20% KCl from 94.17m;

• Hole Col-002B intersected a total thickness 24.66m of carnallitite + kainitite @ 16% KCl incl;

4.89m of carnallitite + kainitite @ 20% KCl from 62.71m and;

3.77m of kainitite @ 22% KCl from 76.60m;

• Previously announced hole Col-004 intersected a total thickness of 21.46m of potash including the high grade interval of;

3.44m of sylvinitite @ 44% KCl from 28.68m;

• An initial orientation gravity survey over mineralised extents has been completed with results to be utilised to target further high grade mineralisation;

• Drilling program to resume in approximately 1 week;

• Results to date confirm Colluli as the world’s shallowest buried evaporite deposit.

complete report

http://www.asx.com.au/asxpdf/20101109/pdf/31trqwdb1hvk5v.pdf

FURTHER DRILL RESULTS CONFIRM COLLULI AS WORLD’S SHALLOWEST POTASH DEPOSIT

• Assay results confirm extensive shallow potash over a 4.5km2 area with mineralisation open in all directions;

• Initial exploration target is to define 300mt-500mt of potash ores with average grades from 21 – 25% KCl. The potential quantity and grade is conceptual in nature and there has been insufficient exploration to define a Mineral Resource and that it is uncertain if further exploration will result in the determination of a Mineral Resource.

• Scoping study to evaluate a low cap-ex and op-ex potash from an open pit mine has commenced;

• Hole Col-001 intersected a total thickness of 28.33m of potash including 8.63m of sylvinitite + carnallitite @ 21% KCl from 59.17m which includes higher grade intervals of;

1.96m of sylvinitite @ 26% KCl from 59.17m and;

4.43m of sylvinitite + carnallitite @ 27% KCl from 63.37m and;

1.35m of sylvinitite @ 39% KCl from 63.85m plus;

19.70m of carnallitite + kainitite @ 16% KCl from 83.78m incl;

9.31m of kainitite @ 20% KCl from 94.17m;

• Hole Col-002B intersected a total thickness 24.66m of carnallitite + kainitite @ 16% KCl incl;

4.89m of carnallitite + kainitite @ 20% KCl from 62.71m and;

3.77m of kainitite @ 22% KCl from 76.60m;

• Previously announced hole Col-004 intersected a total thickness of 21.46m of potash including the high grade interval of;

3.44m of sylvinitite @ 44% KCl from 28.68m;

• An initial orientation gravity survey over mineralised extents has been completed with results to be utilised to target further high grade mineralisation;

• Drilling program to resume in approximately 1 week;

• Results to date confirm Colluli as the world’s shallowest buried evaporite deposit.

complete report

http://www.asx.com.au/asxpdf/20101109/pdf/31trqwdb1hvk5v.pdf

STB Kurs ASX 09.11.2010

Code Last % Chg Bid Offer Open High Low Vol

STB 1.170 17% 1.170 1.180 1.170 1.230 1.100 1,740,251

1.17 AUD = 0.8539 Euro

Code Last % Chg Bid Offer Open High Low Vol

STB 1.170 17% 1.170 1.180 1.170 1.230 1.100 1,740,251

1.17 AUD = 0.8539 Euro

Ein neuerer DJ Carmichael Report :

South Boulder Mines (STB)

Eritrea Colluli Potash deposit looks attractive

STB's ASX Release on 9th November 2010 confirmed its Colluli project as the world's

shallowest potash deposit. Assay results from 3 diamond drill holes confirmed medium

grade potassium chloride (KCL) intersections at widths as wide as 19.7m and high grade

intersections around 3.5m thick. It's still early days for STB as work on the Colluli Project's

pre-scoping study has only just begun, but there is little doubt that this potash deposit is

world class and will eventually be mined.

Not withstanding STB's gold and nickel assets we value STB's potash assets at $1.44/sh,

based on EV/Resource multiples for comparable potash companies. We maintain our

Speculative Buy recommendation on STB.

complete report :

http://www.southbouldermines.com.au/images/uploads/101116_DJ…

South Boulder Mines (STB)

Eritrea Colluli Potash deposit looks attractive

STB's ASX Release on 9th November 2010 confirmed its Colluli project as the world's

shallowest potash deposit. Assay results from 3 diamond drill holes confirmed medium

grade potassium chloride (KCL) intersections at widths as wide as 19.7m and high grade

intersections around 3.5m thick. It's still early days for STB as work on the Colluli Project's

pre-scoping study has only just begun, but there is little doubt that this potash deposit is

world class and will eventually be mined.

Not withstanding STB's gold and nickel assets we value STB's potash assets at $1.44/sh,

based on EV/Resource multiples for comparable potash companies. We maintain our

Speculative Buy recommendation on STB.

complete report :

http://www.southbouldermines.com.au/images/uploads/101116_DJ…

Heute geht wieder was in Australien.

Aktuell 1,18 AUD, umgerechnet 0,85 €

Aktuell 1,18 AUD, umgerechnet 0,85 €

STB news 22.11.2010

DRILLING RESUMES AT WORLD’S SHALLOWEST POTASH DEPOSIT

Drilling targeting extensions to high grade potash has re-commenced;

Previously announced hole Col-004 intersected a total thickness of

21.46m of potash including the high grade interval of;

3.44m of sylvinitite @ 44% KCl from 28.68m;

Initial exploration target is to define 300-500mt of potash ores with

average grades from 21 – 25% KCl at less than 100m depth;

Current program is part of a larger 12-15 hole program. The drilling

data will be used to define JORC/43-101 compliant independent

geological resource estimates that will form the basis of a engineering

scoping study;

A ground orientation gravity survey was completed over currently

interpreted extents of shallow potash mineralisation. The current drill

program will test areas defined by the gravity survey as containing

potash bearing evaporites;

Scoping study to evaluate the production of 1.0 – 1.5Mt p.a of low capex

and op-ex potash from an open pit mine has commenced;

Exploration results to date have confirmed Colluli as the world’s

shallowest buried evaporite potash deposit;

New drilling results will be released as the come to hand.

complete report

http://www.asx.com.au/asxpdf/20101122/pdf/31v11rgp5z2475.pdf

DRILLING RESUMES AT WORLD’S SHALLOWEST POTASH DEPOSIT

Drilling targeting extensions to high grade potash has re-commenced;

Previously announced hole Col-004 intersected a total thickness of

21.46m of potash including the high grade interval of;

3.44m of sylvinitite @ 44% KCl from 28.68m;

Initial exploration target is to define 300-500mt of potash ores with

average grades from 21 – 25% KCl at less than 100m depth;

Current program is part of a larger 12-15 hole program. The drilling

data will be used to define JORC/43-101 compliant independent

geological resource estimates that will form the basis of a engineering

scoping study;

A ground orientation gravity survey was completed over currently

interpreted extents of shallow potash mineralisation. The current drill

program will test areas defined by the gravity survey as containing

potash bearing evaporites;

Scoping study to evaluate the production of 1.0 – 1.5Mt p.a of low capex

and op-ex potash from an open pit mine has commenced;

Exploration results to date have confirmed Colluli as the world’s

shallowest buried evaporite potash deposit;

New drilling results will be released as the come to hand.

complete report

http://www.asx.com.au/asxpdf/20101122/pdf/31v11rgp5z2475.pdf

MORE MASSIVE NICKEL SULPHIDES INTERSECTED AT ROSIE AND MINING LEASE GRANTED

Massive sulphides continue to be intersected at depth;

The strike length of the high grade mineralisation zone containing

massive Ni-Cu-PGE sulphides is currently ~ 250m and open;

Mining Lease (M52/1252) over the C2 and Rosie Prospects was

granted on the 19th of November.

South Boulder Mines Ltd (ASX: STB) is pleased to announce that together

with JV partner Independence Group NL (ASX: IGO) drilling at the Rosie Ni-

Cu-PGE Prospect has intersected further highly encouraging massive

sulphides as well as significant zones of brecciated, stringer and

disseminated sulphides.

Two diamond holes have been completed with preliminary assays returned

from TBDD099, and are pending from wedge hole TBDD099W1. The hole

intercepts are located above the position of Hole A and close to the

position of Hole B respectively. These approximate pierce points are

shown in Figure 1.

Hole TBDD099 (Hole A) intersected downhole intervals of;

5.58m @ 1.54% Ni, 0.44% Cu, 0.04% Co and 2.32g/t 6PGE’s from

470.42m including;

4.00m @ 1.80% Ni, 0.51% Cu, 0.05% Co and 2.82g/t 6PGE’s from

471.00m.

In Hole TBDD099W1 (Hole B) initial geological logging has identified that

from approximately 543m, downhole mineralisation includes;

8.00m of ultramafic with up to 5% disseminated/blebby sulphides from

533.00m;

10.20m of ultramafic with up to 10-15% disseminated/blebby sulphides

from 541.00m;

1.60m of structurally disrupted ultramafic with up to 15-20% brecciated

and stringer sulphides from 551.2m;

0.42m of brecciated ultramafic with up to 40-50% massive sulphides

from 552.80m;

0.50m of semi massive sulphides with ultramafic with up to 70%

sulphides from 553.22m;

2.00m of basalt with up to 5% remobilised sulphides.

complete report

http://www.asx.com.au/asxpdf/20101122/pdf/31v11x1y9jbs0n.pdf

Massive sulphides continue to be intersected at depth;

The strike length of the high grade mineralisation zone containing

massive Ni-Cu-PGE sulphides is currently ~ 250m and open;

Mining Lease (M52/1252) over the C2 and Rosie Prospects was

granted on the 19th of November.

South Boulder Mines Ltd (ASX: STB) is pleased to announce that together

with JV partner Independence Group NL (ASX: IGO) drilling at the Rosie Ni-

Cu-PGE Prospect has intersected further highly encouraging massive

sulphides as well as significant zones of brecciated, stringer and

disseminated sulphides.

Two diamond holes have been completed with preliminary assays returned

from TBDD099, and are pending from wedge hole TBDD099W1. The hole

intercepts are located above the position of Hole A and close to the

position of Hole B respectively. These approximate pierce points are

shown in Figure 1.

Hole TBDD099 (Hole A) intersected downhole intervals of;

5.58m @ 1.54% Ni, 0.44% Cu, 0.04% Co and 2.32g/t 6PGE’s from

470.42m including;

4.00m @ 1.80% Ni, 0.51% Cu, 0.05% Co and 2.82g/t 6PGE’s from

471.00m.

In Hole TBDD099W1 (Hole B) initial geological logging has identified that

from approximately 543m, downhole mineralisation includes;

8.00m of ultramafic with up to 5% disseminated/blebby sulphides from

533.00m;

10.20m of ultramafic with up to 10-15% disseminated/blebby sulphides

from 541.00m;

1.60m of structurally disrupted ultramafic with up to 15-20% brecciated

and stringer sulphides from 551.2m;

0.42m of brecciated ultramafic with up to 40-50% massive sulphides

from 552.80m;

0.50m of semi massive sulphides with ultramafic with up to 70%

sulphides from 553.22m;

2.00m of basalt with up to 5% remobilised sulphides.

complete report

http://www.asx.com.au/asxpdf/20101122/pdf/31v11x1y9jbs0n.pdf

die news scheinen nicht so gut aufgenommen zu werden. Der Kurs fällt leicht und das Volumen ist sehr gering. Sell on good news ??

da kauft selbst der Direktor Aktien !

Change of Director’s Interest Notice

Name of Director

David Hughes

Number acquired

30,646 ordinary shares

Number disposed

-

Value/Consideration Note: If consideration is non-cash, provide details and estimated valuation

$36,193

No. of securities held after change

(a) 267,646 ordinary shares 400,000 options, expiry 30 November 2012 (20c) (b) 2,000,000 options, expiry 30 June 2014 (20c) 1,000,000 options, expiry 31 July 2013 (35c)

http://www.asx.com.au/asxpdf/20101123/pdf/31v26yrdkgq2sv.pdf

Change of Director’s Interest Notice

Name of Director

David Hughes

Number acquired

30,646 ordinary shares

Number disposed

-

Value/Consideration Note: If consideration is non-cash, provide details and estimated valuation

$36,193

No. of securities held after change

(a) 267,646 ordinary shares 400,000 options, expiry 30 November 2012 (20c) (b) 2,000,000 options, expiry 30 June 2014 (20c) 1,000,000 options, expiry 31 July 2013 (35c)

http://www.asx.com.au/asxpdf/20101123/pdf/31v26yrdkgq2sv.pdf

November 22, 2010

Potash One Agrees to Friendly Takeover by K+S for CAD $4.50 Per Share in Cash

- 31.3% premium over the 10-day weighted average trading price

- Potash One's Board of Directors unanimously recommends shareholders tender to the offer

- Expected production capacity of up to 2.7 million tonnes would lead to approximately USD 2.5 billion investment in Saskatchewan and the creation of up to 300 highly skilled jobs

complete report

http://view.exacttarget.com/?j=fe5f15717d620d797715&m=feff13…

Potash One Agrees to Friendly Takeover by K+S for CAD $4.50 Per Share in Cash

- 31.3% premium over the 10-day weighted average trading price

- Potash One's Board of Directors unanimously recommends shareholders tender to the offer

- Expected production capacity of up to 2.7 million tonnes would lead to approximately USD 2.5 billion investment in Saskatchewan and the creation of up to 300 highly skilled jobs

complete report

http://view.exacttarget.com/?j=fe5f15717d620d797715&m=feff13…

See the latest Resource Stocks Magazine Article

Potash Win Adds Some International Shine

http://www.southbouldermines.com.au/images/uploads/Resource_…

Potash Win Adds Some International Shine

http://www.southbouldermines.com.au/images/uploads/Resource_…

Antwort auf Beitrag Nr.: 40.572.061 von StockExplorer am 23.11.10 10:22:27Dann sollte man ja nicht verkaufen oder???

Schaut nach mehr aus.

#

Schaut nach mehr aus.

#

Heute schon wieder Anstieg auf umgerechnet 0,91 €.

Kann es sein, dass hier eine Übernahmefantasie ins Spiel kommt.

Das Gebiet in Eritrea muss doch die big player der Branche dazu reizen, zu zuschlagen, bevor der Kurs noch höher steigt. Wie seht ihr das.

Wer ist denn überhaupt noch investiert ?

Nach der Anzahl der postings zu urteilen, können es nicht viele sein.

Kann es sein, dass hier eine Übernahmefantasie ins Spiel kommt.

Das Gebiet in Eritrea muss doch die big player der Branche dazu reizen, zu zuschlagen, bevor der Kurs noch höher steigt. Wie seht ihr das.

Wer ist denn überhaupt noch investiert ?

Nach der Anzahl der postings zu urteilen, können es nicht viele sein.

Antwort auf Beitrag Nr.: 40.578.874 von Karle45 am 24.11.10 05:34:55 Bin noch mit einer kleinen Menge drin und hoffe das es so weiter geht. Glaube da ist noch potential drin , bin bei 0,17 eingestiegen

Bin noch mit einer kleinen Menge drin und hoffe das es so weiter geht. Glaube da ist noch potential drin , bin bei 0,17 eingestiegen

jo neues Hoch! super!

Antwort auf Beitrag Nr.: 40.579.044 von wucht am 24.11.10 07:53:01

Wie schon geschrieben leider nicht mehr dabei bei 0,09 rein bei 0,98 halt dann raus.

Ich bin zufrieden.

Viel Glück noch.

Montekalino

Wie schon geschrieben leider nicht mehr dabei bei 0,09 rein bei 0,98 halt dann raus.

Ich bin zufrieden.

Viel Glück noch.

Montekalino

Antwort auf Beitrag Nr.: 40.580.413 von IIBI am 24.11.10 11:05:56....in der tat, chart schaut prima aus.....

...und auch die news- seite hält kurs !!!

die freude der loooongis dürfte noch andauern..........IMO

...und auch die news- seite hält kurs !!!

die freude der loooongis dürfte noch andauern..........IMO

wenn alles mit dem Potashprojekt klappt, wirds richtig heiß!

....uuuund nen akt. research report gibts ebenfalls - allerdings NUR für die,

die usd 20,- dafür übirg haben..........

http://reports.finance.yahoo.com/w0?r=32032378:1

die usd 20,- dafür übirg haben..........

http://reports.finance.yahoo.com/w0?r=32032378:1

STB updated ABID Report. The fair value bracket has been revised upwards.

Due Diligence and Valuation Report

Arrowhead Code: 25-01-02

Coverage initiated: 15 Sep 2010

This document: 23 Nov 2010

Fair share value bracket: AS$1.61 to AS$9.33

Share price on date: AS$ 1.17

http://www.southbouldermines.com.au/images/uploads/101122_SO…

Due Diligence and Valuation Report

Arrowhead Code: 25-01-02

Coverage initiated: 15 Sep 2010

This document: 23 Nov 2010

Fair share value bracket: AS$1.61 to AS$9.33

Share price on date: AS$ 1.17

http://www.southbouldermines.com.au/images/uploads/101122_SO…

chackalacka booom!

VIDEO BROADCAST WITH PROACTIVE INVESTORS

South Boulder Mines (ASX: STB) provides the opportunity to watch a Video broadcast by Mr Lorry Hughes, Managing Director of South Boulder Mines Limited.

Proactive Investors South Boulder Mines Stock Tube Interview: “Lorry Hughes, CEO of South Boulder Mines Ltd, tells Proactive Investors that his main focus is to getting to potash production in Eritrea. South Boulder Mines is aiming to leapfrog the pack to become a major potash producer. The company has the world’s shallowest potash deposit”

This interview can be viewed on the website in the “media coverage” section by following the link www.southbouldermines.com.au.

http://www.youtube.com/watch?v=FPAYh33DjnM

South Boulder Mines (ASX: STB) provides the opportunity to watch a Video broadcast by Mr Lorry Hughes, Managing Director of South Boulder Mines Limited.

Proactive Investors South Boulder Mines Stock Tube Interview: “Lorry Hughes, CEO of South Boulder Mines Ltd, tells Proactive Investors that his main focus is to getting to potash production in Eritrea. South Boulder Mines is aiming to leapfrog the pack to become a major potash producer. The company has the world’s shallowest potash deposit”

This interview can be viewed on the website in the “media coverage” section by following the link www.southbouldermines.com.au.

http://www.youtube.com/watch?v=FPAYh33DjnM

DRILLING CONTINUES TO INTERSECT SHALLOW POTASH AT COLLULI

• Drill hole Col-006 has intersected a total potash interval of 24.08m starting from 48.32m vertical depth;

• The result further supports the stated initial exploration target of 300-500mt of potash ores with average grades of 21 – 25% KCl;

• Col-006 was drilled approximately half way between previous holes Col-001 and Col-004 and confirms the extensive continuity of mineralisation over at least 4.5km2;

• Hole Col-001 and Col-004 intersected a total thickness of 28.33m and 21.46m of potash respectively;

• Hole Col-006 intersected;

6.29m of sylvinitite from 48.32m;

0.64m of carnallitite from 54.61m;

7.36m of carnallitite from 70.85m;

9.79m of kainitite from 78.21m;

• It is expected that grades similar to that announced from previously released holes will be confirmed with chemical assays;

• Assays up to 44% KCl have been intersected over 3.44m from sylvinitite intercepts;

• The current drilling is part of a JORC/43-101 resource and mining engineering study into the open pit mining and processing operation with an initial starting capacity of 1.5Mt of potash p.a.;

• The study will also examine the viability of additional production of up to 3Mt of potash p.a;

• Exploration results to date have confirmed Colluli as the world’s shallowest buried evaporite potash deposit;

• New drilling and scoping study results will be released as the come to hand.

complete report

http://www.southbouldermines.com.au/images/uploads/101201_Dr…

• Drill hole Col-006 has intersected a total potash interval of 24.08m starting from 48.32m vertical depth;

• The result further supports the stated initial exploration target of 300-500mt of potash ores with average grades of 21 – 25% KCl;

• Col-006 was drilled approximately half way between previous holes Col-001 and Col-004 and confirms the extensive continuity of mineralisation over at least 4.5km2;

• Hole Col-001 and Col-004 intersected a total thickness of 28.33m and 21.46m of potash respectively;

• Hole Col-006 intersected;

6.29m of sylvinitite from 48.32m;

0.64m of carnallitite from 54.61m;

7.36m of carnallitite from 70.85m;

9.79m of kainitite from 78.21m;

• It is expected that grades similar to that announced from previously released holes will be confirmed with chemical assays;

• Assays up to 44% KCl have been intersected over 3.44m from sylvinitite intercepts;

• The current drilling is part of a JORC/43-101 resource and mining engineering study into the open pit mining and processing operation with an initial starting capacity of 1.5Mt of potash p.a.;

• The study will also examine the viability of additional production of up to 3Mt of potash p.a;

• Exploration results to date have confirmed Colluli as the world’s shallowest buried evaporite potash deposit;

• New drilling and scoping study results will be released as the come to hand.

complete report

http://www.southbouldermines.com.au/images/uploads/101201_Dr…

Antwort auf Beitrag Nr.: 40.612.680 von StockExplorer am 30.11.10 05:58:58Wenn South Boulder es wirklich zum Produzenten schafft, würde uns das wohl in andere Kursregionen bringen. Was glaubst du, was dann möglich ist ?

Antwort auf Beitrag Nr.: 40.620.224 von Karle45 am 01.12.10 06:43:43bis zu einer Produktion dürfte es noch einige Zeit dauern.

Eine Vorhersage ist daher kaum möglich, da zu viele

noch unbekannte Faktoren eingerechnet werden müssten.

Aus dem Arrowhead Due Diligence and Valuation Report

vom 23.11.2010 :

Given due diligence and valuation estimations based

on discounted cash flow method and comparables,

Arrowhead believes that South Boulder mines limited

fair share value lies in the AS$1.61 to AS$9.33

bracket. This valuation is based solely on the

Duketon Nickel and Eritrean Potash project and does

not take account of the potential value of the

company’s Terminator Gold prospect. We have

presented a comparable valuation based on

Enterprise Value/resource and Enterprise Value

/proposed capacity to ascertain the value the Nickel

and Potash prospects respectively.

Eine Vorhersage ist daher kaum möglich, da zu viele

noch unbekannte Faktoren eingerechnet werden müssten.

Aus dem Arrowhead Due Diligence and Valuation Report

vom 23.11.2010 :

Given due diligence and valuation estimations based

on discounted cash flow method and comparables,

Arrowhead believes that South Boulder mines limited

fair share value lies in the AS$1.61 to AS$9.33

bracket. This valuation is based solely on the

Duketon Nickel and Eritrean Potash project and does

not take account of the potential value of the

company’s Terminator Gold prospect. We have

presented a comparable valuation based on

Enterprise Value/resource and Enterprise Value

/proposed capacity to ascertain the value the Nickel

and Potash prospects respectively.

02/12/2010 Investor Presentation London

http://www.asx.com.au/asxpdf/20101202/pdf/31vbrn6zlzy4kp.pdf

http://www.asx.com.au/asxpdf/20101202/pdf/31vbrn6zlzy4kp.pdf

aus dem STB HotCopper Forum :

why all the fuss? (josewales)

Post: 6030977 (Start of thread) Views: 120

Posted: 01/12/10 22:55 Stock Price (at time of posting): $1.33 Sentiment: LT Buy Disclosure: Stock Held From: 121.222.xxx.xxx

The big player in the potash industry is Potash

Corp whom BHP recently made a $40bill bid.To quote from their website

"Becoming a player in potash is difficult. With limited viable deposits worldwide, multi-billion-dollar development costs and lead times of seven years or more, barriers to entering the industry are considerable. With recent trends pushing global producers to or near their capacity limits, rising demand is likely to challenge supply over the coming years.

Substantial barriers to entry; economically mineable

deposits are rare, capital costs are high and lead

times are long

Building a conventional 2-million-tonne mine in Saskatchewan would require an estimated CDN $2.8 billion in upfront capital"

Sitting on a potential resourse of 350-500mill tons,worlds shallowest deposit and open pittable,and capex estimates which will be a fraction of the capital costs quoted above,you can begin to see why a rerating is occurring.

This ones a keeper with plenty more upside IMO.

why all the fuss? (josewales)

Post: 6030977 (Start of thread) Views: 120

Posted: 01/12/10 22:55 Stock Price (at time of posting): $1.33 Sentiment: LT Buy Disclosure: Stock Held From: 121.222.xxx.xxx

The big player in the potash industry is Potash

Corp whom BHP recently made a $40bill bid.To quote from their website

"Becoming a player in potash is difficult. With limited viable deposits worldwide, multi-billion-dollar development costs and lead times of seven years or more, barriers to entering the industry are considerable. With recent trends pushing global producers to or near their capacity limits, rising demand is likely to challenge supply over the coming years.

Substantial barriers to entry; economically mineable

deposits are rare, capital costs are high and lead

times are long

Building a conventional 2-million-tonne mine in Saskatchewan would require an estimated CDN $2.8 billion in upfront capital"

Sitting on a potential resourse of 350-500mill tons,worlds shallowest deposit and open pittable,and capex estimates which will be a fraction of the capital costs quoted above,you can begin to see why a rerating is occurring.

This ones a keeper with plenty more upside IMO.

Kurs zieht prompt an, um mehr als 12 % hoch auf umgerechnet 1,09 €.

Glückwunsch an alle Investierten

Glückwunsch an alle Investierten

Antwort auf Beitrag Nr.: 40.628.819 von StockExplorer am 02.12.10 06:09:42moin STB- lers,

denke, dieser HC- user komm. etwas pauschal, OHNE sich intensiv mit

unserm speziellen COLLULI- proj. in eritrea auseinander gesetzt zu haben

ER hätte es sich eigtl. leicht machen können und nur mal die akt. pres.

zu studieren brauchen, wo es auf seite 5 heißt....

....LOW CAP- EX AND OP-EX production........

...erzielt u.a. durch:

1. potential for LOW COST solution to mining

2. energy use - 40 % of opex at other sites

usw........

laaaaanger rede - kurzer sinn.........STB hat glänzende persp., um colluli

in prod. zu bringen...mit kursen, die dann in der oberen range der jüngsten

studie bei aud 9,- angesiedelt sein dürften....IMO

denke, dieser HC- user komm. etwas pauschal, OHNE sich intensiv mit

unserm speziellen COLLULI- proj. in eritrea auseinander gesetzt zu haben

ER hätte es sich eigtl. leicht machen können und nur mal die akt. pres.

zu studieren brauchen, wo es auf seite 5 heißt....

....LOW CAP- EX AND OP-EX production........

...erzielt u.a. durch:

1. potential for LOW COST solution to mining

2. energy use - 40 % of opex at other sites

usw........

laaaaanger rede - kurzer sinn.........STB hat glänzende persp., um colluli

in prod. zu bringen...mit kursen, die dann in der oberen range der jüngsten

studie bei aud 9,- angesiedelt sein dürften....IMO

geilo! fast 1,50 AUD! Hammer

Die Rallye geht weiter. Im Moment bei 1,65 AUD = 1,21 €.

Antwort auf Beitrag Nr.: 40.637.393 von Karle45 am 03.12.10 03:51:00Langsam wird es ein schönes Weihnachtsgeschenk. Da ist noch potenzial nach oben!

Antwort auf Beitrag Nr.: 40.629.784 von hbg55 am 02.12.10 10:14:50Hi Leute,

(Bei hotcopper gibt es den Button, investiert, nicht investiert, um die Postings immer besser zuordnen zu können. Hier bin ich investiert, jedoch sollte man korrekte kritische Fremdmeinungen immer offen besprechen)

So ganz unrecht hat der gute StockExplorer ja nicht. Es dauert, wie bei allen Explorer, 5-7 Jahre bis zur Produktion und das Geld, dass man hier in die Hand nehmen muss ist auch sehr viel.

Es hängt wie immer alles Preis und wie der sich die kommenden 7 Jahre entwickelt.

Alle andere ist mehr als Positiv. Ein oberflächennahes Deposit, weltgrösstes!, ist sicher eine gute Basis für die Zukunft.

Gute Ergebnisse honoriert der Markt und ein Explorer, der so ein Deposit findet und der Preis sich in gute Sphären bewegt, steigt dann nett an.

Bleibt der Preis hoch, muss man sich um die Zukunft von South Boulder keine Sorgen machen.

CAPEX ist für so eine kleine Company zu hoch, daher eher das Schicksal wie bei Potash One, aber bis dahin werden noch ein paar Jahre vergehen.

...aber South Boulder ist ja nicht nur Potash...

Gruss,

Sil

(Bei hotcopper gibt es den Button, investiert, nicht investiert, um die Postings immer besser zuordnen zu können. Hier bin ich investiert, jedoch sollte man korrekte kritische Fremdmeinungen immer offen besprechen)

So ganz unrecht hat der gute StockExplorer ja nicht. Es dauert, wie bei allen Explorer, 5-7 Jahre bis zur Produktion und das Geld, dass man hier in die Hand nehmen muss ist auch sehr viel.

Es hängt wie immer alles Preis und wie der sich die kommenden 7 Jahre entwickelt.

Alle andere ist mehr als Positiv. Ein oberflächennahes Deposit, weltgrösstes!, ist sicher eine gute Basis für die Zukunft.

Gute Ergebnisse honoriert der Markt und ein Explorer, der so ein Deposit findet und der Preis sich in gute Sphären bewegt, steigt dann nett an.

Bleibt der Preis hoch, muss man sich um die Zukunft von South Boulder keine Sorgen machen.

CAPEX ist für so eine kleine Company zu hoch, daher eher das Schicksal wie bei Potash One, aber bis dahin werden noch ein paar Jahre vergehen.

...aber South Boulder ist ja nicht nur Potash...

Gruss,

Sil

Das Ding, das bis jetzt die wenigsten verstehen ist, dass STB meiner Meinung nach eines der genialsten Projekte in dem Sektor hat, da es oberflächennah ist!

in Kanada liegen die Teile 1000 -2000 Meter tief. Jede Bohrung kostet paar Millionen und die Produktionsaufnahme mehrere Milliarden!

STB bohrt derzeit bis max. 100 Meter. Die Kosten für die Produktionsaufnahme liegen vielleicht bei 300-500 Mio AUD. Das ist zwar hoch aber machbar!

Wenn sie das schaffen, dann kann die Aktie auf 10 oder 20 Dollar steigen, das muss einem bewusst sein.

Natürlich kanns auch mal krachen nach dem Anstieg aber wenn die so weiter arbeiten bin ich positiv

in Kanada liegen die Teile 1000 -2000 Meter tief. Jede Bohrung kostet paar Millionen und die Produktionsaufnahme mehrere Milliarden!

STB bohrt derzeit bis max. 100 Meter. Die Kosten für die Produktionsaufnahme liegen vielleicht bei 300-500 Mio AUD. Das ist zwar hoch aber machbar!

Wenn sie das schaffen, dann kann die Aktie auf 10 oder 20 Dollar steigen, das muss einem bewusst sein.

Natürlich kanns auch mal krachen nach dem Anstieg aber wenn die so weiter arbeiten bin ich positiv

Antwort auf Beitrag Nr.: 40.638.237 von IIBI am 03.12.10 09:45:33

Kann Dir nur zustimmen.

Hast Du eine Meinung zu MNB in Australien.

Montekaolino

Kann Dir nur zustimmen.

Hast Du eine Meinung zu MNB in Australien.

Montekaolino

Zur Info aus Hotcopper

December 02, 2010

South Boulder Mines Reckons It Has A Company Maker At The Colluli Potash Deposit in Eritrea

By Charles Wyatt

It is still early days, but it looks as if ASX-listed South Boulder Mines has a world class potash deposit at Colluli in Eritrea. BHP Billton has left the world in no doubt of the value it ascribes to such deposits following the bid it made for Potash Corporation. Certainly, in the case of South Boulder, managing director Lorry Hughes knows he is onto a good thing, and has lately been spinning the story round the world, including at the Mines and Money show which has just ended in London.

The Eritrean government is very supportive of foreign investment in exploration and mining projects, and its mining code is based on that of the Northern Territory of Australia, which helps the boys from South Boulder feel right at home. Thus US$500,000 has to be spent on exploration in the first year, and the government has a free carried interest of 10 per cent. After a bankable feasibility study the government can buy a further 30 per cent at the market rate and will receive up to a 3.5 per cent royalty. The Canadian company Nevsun had a similar deal on its Bisha gold project and the government has duly elected to take up its option ahead of commercial production, which is due to start in the first quarter of 2011 at a rate of 450,000 ounces per year.

South Boulder got its original lead on the Colluli deposit from a reportthat was compiled by the former French state-owned potash company, Entreprises Miniereat Chemique (EMC) back in 1982. EMC specifically took a look at the occurrence of potash in the Danakil Depression, and duly pointed the way to Colluli. This Depression has a history of artisanal salt production, and is in a reaSonably well accessible area. Colluli itself is 100 kilometres south of the shallow-water port of Mersa Fatma on the Red Sea and 200 kilometres south east of the deep water port of Massawa. Cheap transportation is key to the successful exploitation of bulk minerals, as is cheap, shallow mining, which is why the costs of potash produced at depth in central Canada are totally out of sync with the likely costs in Eritrea. Investors therefore welcomed the news on Thursday 2nd December that a new drillhole at Colluli intersected 24.08 metres of potash starting at a vertical depth of only 48.32 metres, which is very much open pit territory. This hole was drilled midway between two previous ones which hit similar intersections, and confirmed continuity of mineralisation over at least 4.5 kilometres.

Drilling by South Boulder indicates that it has two shallow potash seam beds overlying one another. Seam bed 1 is thinner but with a higher grade than the second seam, which lies approximately 20 metres lower. This higher grade seam is around 14.5% K2O, which would equate to an equivalent gold grade of 1.2 gramme per tonne at current prices. Although this isnt a high grade gold equivalent, Lorry Hughes is targeting a huge resource, approaching 500 million tonnes, and is proposing to mine initially at rate of 1.5 million tonnes per year.

The Colluli project is unique because it contains good quality mineralisation which is at a much shallower depth than most known deposits of this type. Mineralisation at depths of only 60 metres is nearly one kilometre above most other deposits, and means that Colluli can be mined by open pit with all the advantages in costs that implies. Another advantage of being in Eritrea is the high evaporation rates, which occur in the arid climate and hot temperatures. High evaporation assists in separating the salt crystals from the potash crystals, following the crushing and grinding process.

On the telephone Lorry Hughes confirms that the priority at the Colluli project is to continue to drill and define resources, which will then be used as the basis for the scoping study. An initial JORC resource estimate should be completed later this month, with an update expected early in 2011. Large diameter drilling, for geotechnical and metallurgical studies, is planned in January 2011.

No doubt that Lorry sees Colluli as a company maker, but the companys Duketon nickel asset also has plenty of potential, and whats more, requires minimal funding from South Boulder as Independence Group is earning a 70 per cent interest. Terry Grammar, the chairman of South Boulder, describes Duketon as one of the most promising and exciting greenfields nickel discovery in Australia. This may be a bit over the top, but there is no doubt that the South Boulder team reckons it has the wind up its tail at the moment.

Lorry Hughes is aware that if the resource estimate confirms that Colluli is on track for 500 million tonnes a number of companies will be casting envious eyes in his direction. He therefore reckons that it is up to him to accelerate towards the feasibility studies in order to maximise value for shareholders. The company is reaSonably well funded with A$6 million in liquid assets and option conversions and this must be put to best use. It should not be difficult to raise more as political risk estimates for Eritrea are dropping, as more Western companies report success there.

Montekaolino

December 02, 2010

South Boulder Mines Reckons It Has A Company Maker At The Colluli Potash Deposit in Eritrea

By Charles Wyatt

It is still early days, but it looks as if ASX-listed South Boulder Mines has a world class potash deposit at Colluli in Eritrea. BHP Billton has left the world in no doubt of the value it ascribes to such deposits following the bid it made for Potash Corporation. Certainly, in the case of South Boulder, managing director Lorry Hughes knows he is onto a good thing, and has lately been spinning the story round the world, including at the Mines and Money show which has just ended in London.

The Eritrean government is very supportive of foreign investment in exploration and mining projects, and its mining code is based on that of the Northern Territory of Australia, which helps the boys from South Boulder feel right at home. Thus US$500,000 has to be spent on exploration in the first year, and the government has a free carried interest of 10 per cent. After a bankable feasibility study the government can buy a further 30 per cent at the market rate and will receive up to a 3.5 per cent royalty. The Canadian company Nevsun had a similar deal on its Bisha gold project and the government has duly elected to take up its option ahead of commercial production, which is due to start in the first quarter of 2011 at a rate of 450,000 ounces per year.