Silvercorp Metals - Jetzt geht\'s hier richtig los! (Seite 5)

eröffnet am 11.12.06 17:04:22 von

neuester Beitrag 30.04.24 00:07:09 von

neuester Beitrag 30.04.24 00:07:09 von

Beiträge: 4.810

ID: 1.099.579

ID: 1.099.579

Aufrufe heute: 0

Gesamt: 530.418

Gesamt: 530.418

Aktive User: 0

ISIN: CA82835P1036 · WKN: A0EAS0 · Symbol: SVM

3,1500

EUR

-0,82 %

-0,0260 EUR

Letzter Kurs 08.05.24 Tradegate

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,8100 | +11,11 | |

| 0,8000 | +11,11 | |

| 2,0800 | +10,05 | |

| 10,770 | +9,50 | |

| 16.000,00 | +8,11 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 10,520 | -12,33 | |

| 0,9860 | -12,74 | |

| 0,6000 | -18,37 | |

| 0,6601 | -26,22 | |

| 46,43 | -98,01 |

Beitrag zu dieser Diskussion schreiben

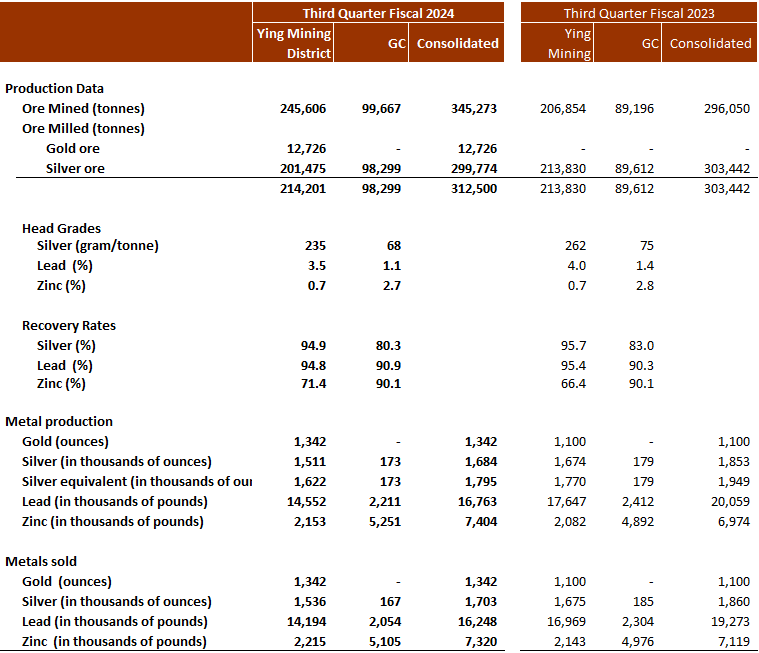

Antwort auf Beitrag Nr.: 75.109.605 von 90BVB09 am 16.01.24 12:06:31Hab da noch mal im Detail drauf geschaut, Vergleich jeweils mit Q3-2023:

Ore Mined gestiegen von 296.050 auf 345.272 Tonnen

Gold hoch: 1.100 oz auf 1.342 oz

Silber runter: 1.853 koz auf 1.511 koz

AgEq auch runter: 1.949 koz auf 1.622 koz

Trotz mehr Mining weniger Erz, Gründe dafür sind:

- erstmal die gesunkenen head grades von 262g/t auf 235g/t

- dann wurden 60,095 Tonnen Erz stockpiled und werden processed während des Chinesichen Neuen Jahr (sind im Mined Ore mit drin!)

- 12,700 tonnes of gold ores were mined and processed with grades of 1.9 g/t gold, 74 g/t silver, 1.0% lead, and 0.1% zinc to produce gravity gold concentrates, silver-gold-lead concentrate, and zinc concentrate

Warum???

Das waren die Gründe für die geringere Produktion, hier die Tabelle in der Übersicht:

Ore Mined gestiegen von 296.050 auf 345.272 Tonnen

Gold hoch: 1.100 oz auf 1.342 oz

Silber runter: 1.853 koz auf 1.511 koz

AgEq auch runter: 1.949 koz auf 1.622 koz

Trotz mehr Mining weniger Erz, Gründe dafür sind:

- erstmal die gesunkenen head grades von 262g/t auf 235g/t

- dann wurden 60,095 Tonnen Erz stockpiled und werden processed während des Chinesichen Neuen Jahr (sind im Mined Ore mit drin!)

- 12,700 tonnes of gold ores were mined and processed with grades of 1.9 g/t gold, 74 g/t silver, 1.0% lead, and 0.1% zinc to produce gravity gold concentrates, silver-gold-lead concentrate, and zinc concentrate

Warum???

Das waren die Gründe für die geringere Produktion, hier die Tabelle in der Übersicht:

übrigens der Kurs von hier ist in einem jämmerlichen Zustand. Beim letzten Fake Bullenmarkt konnte man auch in den Minentitels keinen

Hebel mehr ausmachen. Ich denke die Hebelgeschichte wird beim Silber verschwinden- fade away

Hebel mehr ausmachen. Ich denke die Hebelgeschichte wird beim Silber verschwinden- fade away

Es ist völlig unwichtig was in diesen Särgen liegt. Große Teile sind in London im Privatbesitz und somit gilt das als unberechenbar.

Kein Mensch am Metallmarkt handelt nach Särgen, nach ETFs etc. Der Handel läuft über lieferbare Terminkontrakte der wirklichen

Verarbeiter. Klar spielen ab und zu die Spekulanten eine Rolle, aber halten weder Kontrakte noch füllen die Särge. Die wollen MONEY

Kein Mensch am Metallmarkt handelt nach Särgen, nach ETFs etc. Der Handel läuft über lieferbare Terminkontrakte der wirklichen

Verarbeiter. Klar spielen ab und zu die Spekulanten eine Rolle, aber halten weder Kontrakte noch füllen die Särge. Die wollen MONEY

Was willst du eigentlich irgendwas beweisen was nicht stimmt. Am 27.Nov 2023 waren es 1026 SFE und 1489 SGE (1 Seite zurück). Aktuell SFE 1065 und nun diese Woche 1322 (wobei dieser letzte Woche noch über 1400 lag). Da ist überhaupt kein Rückgang, bzw. mit den Zahlen dieser Woche nur minimal. Also lass doch stecken das Thema.

Antwort auf Beitrag Nr.: 75.043.419 von ohnonotagain am 03.01.24 14:00:54Nochmal zum Posting von ohnonotagain "die Theorie der Knappheit in China ist ad acta" vom 3. Januar 2024 und der Entwicklung über 14 Tage, der Preis dabei in Shanghai konsequent 2 Dollar Premium zur COMEX:

SFE Vaults am 3. Januar: 1.196.881

SFE Vaults heute: 1.065.164

SFE -131.717

SGE Vaults am 3. Januar: 1.445.205

SGE Vaults heute: 1.321.950

SGE -123.255

SFE/SGE Vaults 03.01.2024 zusammen: 2.642.086

SFE/SGE Vaults heute zusammen: 2.387.114

SFE/SGE -254.972 kg

Das sind 10 Prozent MINUS, statt 50 Prozent PLUS...!

Posting: 75.040.074 von ohnonotagain am 02.01.24 19:50:20 im Thread: Silvercorp Metals - Jetzt geht\'s hier richtig los!

SFE Vaults am 3. Januar: 1.196.881

SFE Vaults heute: 1.065.164

SFE -131.717

SGE Vaults am 3. Januar: 1.445.205

SGE Vaults heute: 1.321.950

SGE -123.255

SFE/SGE Vaults 03.01.2024 zusammen: 2.642.086

SFE/SGE Vaults heute zusammen: 2.387.114

SFE/SGE -254.972 kg

Das sind 10 Prozent MINUS, statt 50 Prozent PLUS...!

Posting: 75.040.074 von ohnonotagain am 02.01.24 19:50:20 im Thread: Silvercorp Metals - Jetzt geht\'s hier richtig los!

Trading Spotlight

Silvercorp Reports Operational Results and Financial Results Release Date for Third Quarter, Fiscal 2024

https://ceo.ca/@newswire/silvercorp-reports-operational-resu…"Operative Ergebnisse für das 3. Quartal des Geschäftsjahres 2024

Goldproduktion von 1.342 Unzen, ein Anstieg von 22 % gegenüber dem dritten Quartal des Geschäftsjahres 2023;

Silberäquivalentproduktion (nur Silber und Gold)1 von ungefähr 1,8 Millionen Unzen;

Zinkproduktion von etwa 7,4 Millionen Pfund, ein Anstieg von 6 % gegenüber dem dritten Quartal des Geschäftsjahres 2023; und

Bleiproduktion von ungefähr 16,8 Millionen Pfund, ein Rückgang von 16 % gegenüber dem dritten Quartal des Geschäftsjahres 2023."

Silvercorp Provides Update on OreCorp Transaction

https://ceo.ca/@newswire/silvercorp-provides-update-on-oreco…"VANCOUVER, BC, 16. Januar 2024 /CNW/ - Silvercorp Metals Inc. ("Silvercorp" oder das "Unternehmen") (TSX: SVM) (NYSE American: SVM) meldet, dass das Unternehmen heute mit dem Versand der Angebotsunterlage an die Aktionäre von OreCorp Limited ("OreCorp") beginnen wird, und zwar im Zusammenhang mit dem außerbörslichen Übernahmeangebot von Silvercorp für alle OreCorp-Aktien, die sich nicht bereits im Besitz von Silvercorp befinden, zu einem Preis von 0. 0967 Stammaktien von Silvercorp und 0,19 A$ in bar pro OreCorp-Aktie (die "Transaktion"), wie in der Pressemitteilung des Unternehmens vom 26. Dezember 2023 beschrieben. Das Angebot kann von den OreCorp-Aktionären bis zum 23. Februar 2024 (Ortszeit Sydney) angenommen werden, sofern es nicht verlängert wird. Silvercorp wird zu gegebener Zeit weitere Updates zur Transaktion veröffentlichen."

mhm...

Kapier ich nicht, sofern man das "Problem" mit perseus nicht beseitigt, hat das doch gar keinen Arsch?!

Neuer Research von Benzinga, für uns hier nix Neues und auch ein bisschen PR "contains sponsored content" - trotzdem eine gute Übersicht was Silvercorp Metals und Silber angeht:

Stars Align For A Silver Bull Market? Primary Silver Miners May Be Poised To Shine

by Faith Ashmore, Benzinga Staff Writer

2023 marked another year of a pronounced supply-demand deficit in silver, driven by record industrial demand from robust global investments in the green economy. The most significant increase came from photovoltaics. In a recent revision for 2023, the Silver Institute and Metal Focus group bumped up their estimate of silver uptake in solar panels, indicating usage of approximately 200 million ounces of silver for the year. This represents a substantial increase from the approximately 110 million ounces used in 2021.

Mirroring this growth, BloombergNEF upgraded its global solar build forecast to 413 GW in 2023 – up 125% over two years, with China accounting for nearly 60% of the installed volumes. The acceleration can, in part, be attributed to record-low prices for all types of solar panels, making adoption more affordable.

Meanwhile, solar panel innovation has reached an inflection point. In a recent opinion piece published on Streetwise Reports, market commentator and fund manager Chen Lin pointed out that upcoming generations of solar panels are anticipated to require 25-100% more silver for improved efficiency. Many experts in the field share the same optimism regarding the continued rapid growth of silver uptake in solar panels over the coming years. In particular, ANZ Bank expects photovoltaics to represent more than 50% of silver industrial demand by 2025, compared to about 20% in 2021.

On the supply front, annual mine production has remained rangebound between 800 and 900 million ounces over the last decade. The current structural deficit will likely persist for the foreseeable future unless numerous new primary silver mines are built or marginal mines resume production. Achieving either of these scenarios demands a prolonged period of elevated silver prices.

Light At The End Of The Tunnel? Precious Metals Rally

Throughout 2023, the volatility of silver prices persisted, primarily driven by the dynamic influence of the U.S. Federal Reserve's monetary policy. However, there appears to be light at the end of the tunnel. The start of last December welcomed a more dovish tone from the Fed, which fueled a precious metals rally. Gold broke above $2,100 per ounce (an all-time high), and silver nearly reached $26 per ounce (a multi-month high). By mid-December, the Fed released a more definitive signal for the end of the tightening cycle by keeping key interest rates steady and indicating three cuts in 2024

With this in mind, companies like Silvercorp Metals Inc. (TSX: SVM) could potentially be undervalued relative to peers despite Silvercorp’s performance and growth strategy. Silvercorp is an established Canadian miner that boasts of a strong balance sheet and of combining a track record of profitability along with growth opportunities including fully-funded ‘organic’ growth within its existing low-cost mines, while also engaging in ongoing strategic M&A efforts.

Ying Mining District: Helping To Meet The Global Silver Demand

In 2004, the company began operations in China’s Ying Mining District which is known for its tremendous resource wealth, principally in silver-lead-zinc mineralization. After two years of exploration and development, the company began production in April 2006. The company reports that the operation proved to be extremely profitable, largely in part due to the high grades of the metals found at the site.

Over the next several years, Silvercorp expanded its footprint in the region and increased the production profile of the flagship operation. From 2007 to 2017, Silvercorp roughly tripled Ying’s silver output, delivering 5.9 million ounces in 2017 – solidifying the company’s status as China’s largest primary silver producer. Silvercorp has maintained strong operating margins at Ying while growing its production, with annual all-in sustaining costs remaining below $10/oz over the last seven years despite mounting inflationary pressures affecting miners globally. In fiscal 2023, Ying reported producing 6 million ounces of silver at an all-in sustaining cost of $9.73/oz, generating $63 million in income from mine operations and representing a peer-leading operating margin of 36%. The company is working to further improve the operation’s productivity and efficiency by enhancing mine mechanization and expanding milling capacity.

As silver becomes an increasingly integral component of the green economy, established pure-play producers like Silvercorp could play a more instrumental role in meeting the global industrial demand for silver. Anticipating further positive developments for Silvercorp in 2024, interested investors may want to stay tuned for additional news and analysis on the company. Readers interested in the latest updates on Silvercorp's performance and growth strategies can find additional information at silvercorpmetals.com/welcome.

https://www.benzinga.com/markets/commodities/24/01/36592587/…

Stars Align For A Silver Bull Market? Primary Silver Miners May Be Poised To Shine

by Faith Ashmore, Benzinga Staff Writer

2023 marked another year of a pronounced supply-demand deficit in silver, driven by record industrial demand from robust global investments in the green economy. The most significant increase came from photovoltaics. In a recent revision for 2023, the Silver Institute and Metal Focus group bumped up their estimate of silver uptake in solar panels, indicating usage of approximately 200 million ounces of silver for the year. This represents a substantial increase from the approximately 110 million ounces used in 2021.

Mirroring this growth, BloombergNEF upgraded its global solar build forecast to 413 GW in 2023 – up 125% over two years, with China accounting for nearly 60% of the installed volumes. The acceleration can, in part, be attributed to record-low prices for all types of solar panels, making adoption more affordable.

Meanwhile, solar panel innovation has reached an inflection point. In a recent opinion piece published on Streetwise Reports, market commentator and fund manager Chen Lin pointed out that upcoming generations of solar panels are anticipated to require 25-100% more silver for improved efficiency. Many experts in the field share the same optimism regarding the continued rapid growth of silver uptake in solar panels over the coming years. In particular, ANZ Bank expects photovoltaics to represent more than 50% of silver industrial demand by 2025, compared to about 20% in 2021.

On the supply front, annual mine production has remained rangebound between 800 and 900 million ounces over the last decade. The current structural deficit will likely persist for the foreseeable future unless numerous new primary silver mines are built or marginal mines resume production. Achieving either of these scenarios demands a prolonged period of elevated silver prices.

Light At The End Of The Tunnel? Precious Metals Rally

Throughout 2023, the volatility of silver prices persisted, primarily driven by the dynamic influence of the U.S. Federal Reserve's monetary policy. However, there appears to be light at the end of the tunnel. The start of last December welcomed a more dovish tone from the Fed, which fueled a precious metals rally. Gold broke above $2,100 per ounce (an all-time high), and silver nearly reached $26 per ounce (a multi-month high). By mid-December, the Fed released a more definitive signal for the end of the tightening cycle by keeping key interest rates steady and indicating three cuts in 2024

With this in mind, companies like Silvercorp Metals Inc. (TSX: SVM) could potentially be undervalued relative to peers despite Silvercorp’s performance and growth strategy. Silvercorp is an established Canadian miner that boasts of a strong balance sheet and of combining a track record of profitability along with growth opportunities including fully-funded ‘organic’ growth within its existing low-cost mines, while also engaging in ongoing strategic M&A efforts.

Ying Mining District: Helping To Meet The Global Silver Demand

In 2004, the company began operations in China’s Ying Mining District which is known for its tremendous resource wealth, principally in silver-lead-zinc mineralization. After two years of exploration and development, the company began production in April 2006. The company reports that the operation proved to be extremely profitable, largely in part due to the high grades of the metals found at the site.

Over the next several years, Silvercorp expanded its footprint in the region and increased the production profile of the flagship operation. From 2007 to 2017, Silvercorp roughly tripled Ying’s silver output, delivering 5.9 million ounces in 2017 – solidifying the company’s status as China’s largest primary silver producer. Silvercorp has maintained strong operating margins at Ying while growing its production, with annual all-in sustaining costs remaining below $10/oz over the last seven years despite mounting inflationary pressures affecting miners globally. In fiscal 2023, Ying reported producing 6 million ounces of silver at an all-in sustaining cost of $9.73/oz, generating $63 million in income from mine operations and representing a peer-leading operating margin of 36%. The company is working to further improve the operation’s productivity and efficiency by enhancing mine mechanization and expanding milling capacity.

As silver becomes an increasingly integral component of the green economy, established pure-play producers like Silvercorp could play a more instrumental role in meeting the global industrial demand for silver. Anticipating further positive developments for Silvercorp in 2024, interested investors may want to stay tuned for additional news and analysis on the company. Readers interested in the latest updates on Silvercorp's performance and growth strategies can find additional information at silvercorpmetals.com/welcome.

https://www.benzinga.com/markets/commodities/24/01/36592587/…

Antwort auf Beitrag Nr.: 75.070.626 von ohnonotagain am 08.01.24 23:08:05Wenn es so wäre, könnte die Situation sich nicht schon Jahre hinziehen.

Über Jahre hinziehen? Von welchen Jahren sprichst du? Hast du schon vergessen, dass China drei Jahre lang von 2020 bis 2022 eine strikte zero-COVID Strategie verfolgt hat und dabei mit drakonischen Lockdowns (nicht so ein Pillepalle-Lockdown wie in Deutschland!!!!) die Produktion und Nachfrage nach Rohstoffen vor die Wand gefahren hat?

Sowas löst sich nicht über Nacht auf, und ja, dabei kann sich durchaus über drei Jahre ein Monsterüberangebot aufgebaut haben, das jetzt in den letzten 12 Monaten langsam wieder abgebaut wird.

Und ja, du hast Recht: Der Markt ist völlig intransparent.

Aber Fakt ist doch, dass wir seit langem an der SGE und SFE die Situation haben, dass es ein Premium ggü. der COMES gibt:

- Gold ist ca. 2,5% höher und

- Silver fast 10% höher

Über Jahre hinziehen? Von welchen Jahren sprichst du? Hast du schon vergessen, dass China drei Jahre lang von 2020 bis 2022 eine strikte zero-COVID Strategie verfolgt hat und dabei mit drakonischen Lockdowns (nicht so ein Pillepalle-Lockdown wie in Deutschland!!!!) die Produktion und Nachfrage nach Rohstoffen vor die Wand gefahren hat?

Sowas löst sich nicht über Nacht auf, und ja, dabei kann sich durchaus über drei Jahre ein Monsterüberangebot aufgebaut haben, das jetzt in den letzten 12 Monaten langsam wieder abgebaut wird.

Und ja, du hast Recht: Der Markt ist völlig intransparent.

Aber Fakt ist doch, dass wir seit langem an der SGE und SFE die Situation haben, dass es ein Premium ggü. der COMES gibt:

- Gold ist ca. 2,5% höher und

- Silver fast 10% höher

Dann müsste der Silberbestand an der Comex oder LBMA abnehmen. Sonst können da nicht sovieke Unzen aus dem Nichts auftauchen. Tut er aber nicht. Ich bleibe dabei, wir befinden uns mitnichten in einer Defizitsituation. Wenn es so wäre, könnte die Situation sich nicht schon Jahre hinziehen. Es sei denn es hätte vorher ein Monsterüberangebot gegeben. Was aber auch nicht der Fall war.

Der Markt ist völlig intransparent. Ich halte alle Zahlen für gefälscht bzw. frisiert, weshalb es sich nicht lohnt sie zu beobachten.

Der Markt ist völlig intransparent. Ich halte alle Zahlen für gefälscht bzw. frisiert, weshalb es sich nicht lohnt sie zu beobachten.