Canadian Solar - wo geht die Reise hin? (Seite 164)

eröffnet am 16.04.07 19:42:54 von

neuester Beitrag 29.04.24 22:19:41 von

neuester Beitrag 29.04.24 22:19:41 von

Beiträge: 1.967

ID: 1.124.883

ID: 1.124.883

Aufrufe heute: 4

Gesamt: 257.341

Gesamt: 257.341

Aktive User: 0

ISIN: CA1366351098 · WKN: A0LCUY · Symbol: L5A

15,610

EUR

+1,17 %

+0,180 EUR

Letzter Kurs 03.05.24 Tradegate

Neuigkeiten

16.11.23 · Shareribs Anzeige |

23.05.23 · BNP Paribas Anzeige |

Werte aus der Branche Erneuerbare Energien

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,9250 | +34,53 | |

| 1,7400 | +33,84 | |

| 0,5770 | +29,66 | |

| 0,5070 | +17,06 | |

| 2,5410 | +11,01 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 5,8000 | -5,69 | |

| 0,8000 | -5,88 | |

| 6,1500 | -6,11 | |

| 12,700 | -8,63 | |

| 1,9200 | -13,12 |

Beitrag zu dieser Diskussion schreiben

Antwort auf Beitrag Nr.: 34.008.034 von Dere am 01.05.08 09:24:27jau, KGV von unter 11 = spottbillig für eine Wachstumsaktie

bald wird charttechnisches Neuland betreten, the sky is the limit ..

Glück auf

U.

bald wird charttechnisches Neuland betreten, the sky is the limit ..

Glück auf

U.

Antwort auf Beitrag Nr.: 34.007.687 von Unkenhorst1 am 01.05.08 01:48:11Willst du uns damit etwas bestimmtes sagen?

Canadian Solar Reports Fourth Quarter 2007 and Year End Results and 2008 Outlook

2007 Results

-- Q4 net revenues of $127.5 million, a 31% increase over Q3 net revenues

of $97.4 million

-- Q4 net income per diluted share of $0.20 compared to Q3 net income per

diluted share of $0.02

-- Full year 2007 net revenues of $302.8 million, a 344% increase over

full year 2006 net revenues of $68.2 million

-- Q4 shipments of 37.8MW, bringing full year 2007 shipments to 83.5MW, a

542% increase over full year 2006 shipments of 15.4MW

2008 Outlook and Developments

-- Reiterates full year 2008 net revenue guidance of $650-$750 million on

shipments of 200-220MW

-- Over 90% of projected 2008 module sales secured by firm contracts

-- Almost all projected 2008 silicon, wafer and cell requirements secured

by firm contracts

-- 100MW of new solar cell production capacity installed in November 2007

and expected to reach full capacity in Q1 2008

-- New Changshu solar module facility completed on schedule in February

2008, bringing total annual solar module production capacity to 400MW

hier ist Musik drin, und das bei einem KGV von unter 11

2007 Results

-- Q4 net revenues of $127.5 million, a 31% increase over Q3 net revenues

of $97.4 million

-- Q4 net income per diluted share of $0.20 compared to Q3 net income per

diluted share of $0.02

-- Full year 2007 net revenues of $302.8 million, a 344% increase over

full year 2006 net revenues of $68.2 million

-- Q4 shipments of 37.8MW, bringing full year 2007 shipments to 83.5MW, a

542% increase over full year 2006 shipments of 15.4MW

2008 Outlook and Developments

-- Reiterates full year 2008 net revenue guidance of $650-$750 million on

shipments of 200-220MW

-- Over 90% of projected 2008 module sales secured by firm contracts

-- Almost all projected 2008 silicon, wafer and cell requirements secured

by firm contracts

-- 100MW of new solar cell production capacity installed in November 2007

and expected to reach full capacity in Q1 2008

-- New Changshu solar module facility completed on schedule in February

2008, bringing total annual solar module production capacity to 400MW

hier ist Musik drin, und das bei einem KGV von unter 11

Antwort auf Beitrag Nr.: 33.981.821 von Dere am 28.04.08 07:16:58Nasdaq 27,37 USD +2,29 +9,13%

ein sehr grüner Tag, die lächerlich niedrige KGV wächst, hat jedoch noch reichlich Raum nach oben,

die Reise geht gen Norden.

Glück auf

U.

ein sehr grüner Tag, die lächerlich niedrige KGV wächst, hat jedoch noch reichlich Raum nach oben,

die Reise geht gen Norden.

Glück auf

U.

27.04.2008 17:03

Union will weniger Solarförderung

Die Unionsfraktion im Bundestag will die Förderung von Solarenergie massiv eindämmen. Der wirtschaftspolitische Sprecher, Laurenz Meyer (CDU), kritisierte im Nachrichtenmagazin "Der Spiegel", dass die Belastung über den Strompreis eine Dimension erreiche, die durch keine Steuererleichterung kompensiert werden könne. Der Solarboom und die hohen Einspeisevergütungen führen nach den Angaben dazu, dass die Verbraucher die bis 2015 installierten Anlagen wohl mit mehr als 100 Milliarden Euro subventionieren werden.

Meyer bezeichnete die Förderung als unsozial. Schließlich müssten die Bezieher kleiner Einkommen für Strom im Verhältnis zu ihrem Gesamtverdienst mehr zahlen als Besserverdiener. Wer hingegen ein eigenes Haus besitze und eine Solaranlage installiere, könne eine vergleichsweise sichere Rendite von rund sieben Prozent einstreichen und so von der bisherigen Regelung profitieren.

Die bayerische Wirtschaftsministerin Emilia Müller (CSU) sprach sich für eine steuerliche Umverteilung zugunsten der erneuerbaren Energien aus. "Ich kann mir vorstellen, dass die Steuern auf Energie ausschließlich für die Förderung erneuerbarer Energien verwendet werden", sagte sie der "Welt am Sonntag". Die Steuerlast für Treibstoffe müsse gesenkt werden. "Wenn die Preisentwicklung so weitergeht, muss man auf jeden Fall über eine Steuerreduzierung reden, weil sonst die Lebenshaltungskosten viel zu hoch werden. Man muss dem Bürger so schnell wie möglich entgegenkommen", sagte Müller. Die volle Pendlerpauschale wieder einzuführen sei ein erster Schritt zur steuerlichen Entlastung./sl/DP/he

Union will weniger Solarförderung

Die Unionsfraktion im Bundestag will die Förderung von Solarenergie massiv eindämmen. Der wirtschaftspolitische Sprecher, Laurenz Meyer (CDU), kritisierte im Nachrichtenmagazin "Der Spiegel", dass die Belastung über den Strompreis eine Dimension erreiche, die durch keine Steuererleichterung kompensiert werden könne. Der Solarboom und die hohen Einspeisevergütungen führen nach den Angaben dazu, dass die Verbraucher die bis 2015 installierten Anlagen wohl mit mehr als 100 Milliarden Euro subventionieren werden.

Meyer bezeichnete die Förderung als unsozial. Schließlich müssten die Bezieher kleiner Einkommen für Strom im Verhältnis zu ihrem Gesamtverdienst mehr zahlen als Besserverdiener. Wer hingegen ein eigenes Haus besitze und eine Solaranlage installiere, könne eine vergleichsweise sichere Rendite von rund sieben Prozent einstreichen und so von der bisherigen Regelung profitieren.

Die bayerische Wirtschaftsministerin Emilia Müller (CSU) sprach sich für eine steuerliche Umverteilung zugunsten der erneuerbaren Energien aus. "Ich kann mir vorstellen, dass die Steuern auf Energie ausschließlich für die Förderung erneuerbarer Energien verwendet werden", sagte sie der "Welt am Sonntag". Die Steuerlast für Treibstoffe müsse gesenkt werden. "Wenn die Preisentwicklung so weitergeht, muss man auf jeden Fall über eine Steuerreduzierung reden, weil sonst die Lebenshaltungskosten viel zu hoch werden. Man muss dem Bürger so schnell wie möglich entgegenkommen", sagte Müller. Die volle Pendlerpauschale wieder einzuführen sei ein erster Schritt zur steuerlichen Entlastung./sl/DP/he

Trading Spotlight

Es wird den PV-Anlagen Käufern immer einfacher gemacht....

Start-up nutzt Google Earth für Solarverkäufe

Software errechnet aus Satellitenbildern die individuellen Anforderungen

http://www.pressetext.de/pte.mc?pte=080422004

Start-up nutzt Google Earth für Solarverkäufe

Software errechnet aus Satellitenbildern die individuellen Anforderungen

http://www.pressetext.de/pte.mc?pte=080422004

Antwort auf Beitrag Nr.: 33.911.207 von Dere am 17.04.08 18:46:20Solar Stocks: Nine That Will Shine in a Bull Market

by: Rick Shea posted on: April 21, 2008 | about stocks: CREE / CSIQ / ESLR / FSLR / LDK / SPWR / STP / TSL / ZOLT

As the market rebounds, investors continue to reward the large cap growth leaders, and alternative energy led by solar has been one of the prime beneficiaries. The need for alternative energy continues to be a main focus for all governments as oil continues it's climb to over $110 a barrel. Solar stocks are getting the most headlines because they are farther along the commercialization continuum and they are more prevalent than their wind and alternative fuel counterparts.

Any discussion about solar companies must start with First Solar (FSLR). Clearly, the leader in the sector according to Wall Street based on its thin film technology, First Solar's stock price has resumed its climb to near record levels as investors await its Q1 earnings report.

Suntech (STP) and SunPower (SPWR) are the next two leading players based on market cap, but they primarily use silicon-based technology for their products. SunPower just released strong first quarter 2008 numbers but some analysts had some concerns about slowing sales growth for the next quarter based on a single comment during its conference call.

Additional players include LDK Solar (LDK), Trina Solar (TSL), Evergreen Solar (ESLR) and Canadian Solar (CSIQ).

There are two main questions when investing in solar stocks:

# First, which technology (thin film vs. silicon) is likely to offer the best long term business model for cost and efficiency. Again, based on market cap and relative performance the market is betting that customers will prefer thin film technology led by First Solar. While I tend to agree I am certain that the market will be large enough for both technology forms to compete and provide strong sales and profits.

# Second, which stocks offer the best values and are likely to maintain the growth rates that investors need to drive higher market capitalizations.

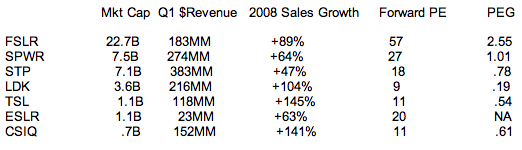

The following chart analyzes the top players with the key growth rates and relative value.

You can see that Wall Street believes that First Solar will prevail based on a market cap that is three times the next largest competitor. You can also see its stock is priced for perfection. First Solar has a history of trouncing estimates and will likely do so again this quarter.

SWPR and STP are the next largest competitors with STP actually showing the largest sales estimate for Q1 2008. Both are well-positioned to lead the silicon based technology and sport reasonable valuations with forward P/E's of 27 and 18 respectively. Their PEG's (price to earnings growth) is actually very attractive and lower than most slower growing companies.

Both Canadian Solar (CSIQ) a Chinese company and LDK are interesting plays. Both are showing strong growth with below average valuations. LDK's PEG is ridiculously low vs. the other solar companies and vs. the overall market. So what's this all mean for the average investor looking to buy alternative energy and solar stocks. I believe FSLR will deliver on Q1 earnings and lead the group to new highs.

I will continue to maintain my long positions in FSLR, SPWR and STP until their valuations get too high. At that point it may be worthwhile to switch into some of the smaller names particularly LDK and CSIQ. The leaders will lead the sector up until valuations get out of hand and then others will play catch up shortly after.

FYI: I also like Cree Inc. (CREE) and Zoltek Companies Inc. (ZOLT) as additional long-term plays in the alternative energy sector.

by: Rick Shea posted on: April 21, 2008 | about stocks: CREE / CSIQ / ESLR / FSLR / LDK / SPWR / STP / TSL / ZOLT

As the market rebounds, investors continue to reward the large cap growth leaders, and alternative energy led by solar has been one of the prime beneficiaries. The need for alternative energy continues to be a main focus for all governments as oil continues it's climb to over $110 a barrel. Solar stocks are getting the most headlines because they are farther along the commercialization continuum and they are more prevalent than their wind and alternative fuel counterparts.

Any discussion about solar companies must start with First Solar (FSLR). Clearly, the leader in the sector according to Wall Street based on its thin film technology, First Solar's stock price has resumed its climb to near record levels as investors await its Q1 earnings report.

Suntech (STP) and SunPower (SPWR) are the next two leading players based on market cap, but they primarily use silicon-based technology for their products. SunPower just released strong first quarter 2008 numbers but some analysts had some concerns about slowing sales growth for the next quarter based on a single comment during its conference call.

Additional players include LDK Solar (LDK), Trina Solar (TSL), Evergreen Solar (ESLR) and Canadian Solar (CSIQ).

There are two main questions when investing in solar stocks:

# First, which technology (thin film vs. silicon) is likely to offer the best long term business model for cost and efficiency. Again, based on market cap and relative performance the market is betting that customers will prefer thin film technology led by First Solar. While I tend to agree I am certain that the market will be large enough for both technology forms to compete and provide strong sales and profits.

# Second, which stocks offer the best values and are likely to maintain the growth rates that investors need to drive higher market capitalizations.

The following chart analyzes the top players with the key growth rates and relative value.

You can see that Wall Street believes that First Solar will prevail based on a market cap that is three times the next largest competitor. You can also see its stock is priced for perfection. First Solar has a history of trouncing estimates and will likely do so again this quarter.

SWPR and STP are the next largest competitors with STP actually showing the largest sales estimate for Q1 2008. Both are well-positioned to lead the silicon based technology and sport reasonable valuations with forward P/E's of 27 and 18 respectively. Their PEG's (price to earnings growth) is actually very attractive and lower than most slower growing companies.

Both Canadian Solar (CSIQ) a Chinese company and LDK are interesting plays. Both are showing strong growth with below average valuations. LDK's PEG is ridiculously low vs. the other solar companies and vs. the overall market. So what's this all mean for the average investor looking to buy alternative energy and solar stocks. I believe FSLR will deliver on Q1 earnings and lead the group to new highs.

I will continue to maintain my long positions in FSLR, SPWR and STP until their valuations get too high. At that point it may be worthwhile to switch into some of the smaller names particularly LDK and CSIQ. The leaders will lead the sector up until valuations get out of hand and then others will play catch up shortly after.

FYI: I also like Cree Inc. (CREE) and Zoltek Companies Inc. (ZOLT) as additional long-term plays in the alternative energy sector.

alles richtig, jedoch ist nach meiner Meinung ein Umsatzmultiple von 3,75 doch schon sehr heftig und als Nummer 3 mit einem Umsatz von 2 Milliarden wird es mit den erwarteten Steigerungsraten auch schwierig,

weil nicht alle Menschen alles Geld für Solarzellen ausgeben wollen.

Glück auf

U.

weil nicht alle Menschen alles Geld für Solarzellen ausgeben wollen.

Glück auf

U.

Antwort auf Beitrag Nr.: 33.910.744 von Unkenhorst1 am 17.04.08 18:00:04Ja nur ganz so einfach ist es dann doch nicht...

STP ist unter den TOP drei der Zellhersteller und Numero uno bei

den Modulhersteller... (auch die Qualität muß man eingestehen ist

sehr gut - besser noch als die von CSIQ)

CSIQ liegt irgendwo zwischen Rang 12-15 in 2007. OK wir wachsen schneller

als manch ein Konkurrent und darum könnte es gut sein das wir in 12

Monaten unter den Top 10 sind. Dann würde der Markt auch genauer auf

CSIQ schauen.

Genauso müßte die Marge noch während 2008 weiterhin steigen um für

den Markt interessanter zu werden. Piper schätzt bis ins Jahr 2009 eine

Netto-Marge von ca. 15 %. Damit stiegen wir auf alle Fälle eine Liga

rauf.

Trotzdem sehe ich für CSIQ noch eine goldige Zukunft auf uns zukommen. EPS für 2009 schätze ich auf 5-6 USD... Kursziel 2009

zwischen 75-100 USD. (wenn der USD dann noch was wert ist

Gruß

Dere

STP ist unter den TOP drei der Zellhersteller und Numero uno bei

den Modulhersteller... (auch die Qualität muß man eingestehen ist

sehr gut - besser noch als die von CSIQ)

CSIQ liegt irgendwo zwischen Rang 12-15 in 2007. OK wir wachsen schneller

als manch ein Konkurrent und darum könnte es gut sein das wir in 12

Monaten unter den Top 10 sind. Dann würde der Markt auch genauer auf

CSIQ schauen.

Genauso müßte die Marge noch während 2008 weiterhin steigen um für

den Markt interessanter zu werden. Piper schätzt bis ins Jahr 2009 eine

Netto-Marge von ca. 15 %. Damit stiegen wir auf alle Fälle eine Liga

rauf.

Trotzdem sehe ich für CSIQ noch eine goldige Zukunft auf uns zukommen. EPS für 2009 schätze ich auf 5-6 USD... Kursziel 2009

zwischen 75-100 USD. (wenn der USD dann noch was wert ist

Gruß

Dere