Tinka resources (Seite 24)

eröffnet am 25.07.14 06:04:06 von

neuester Beitrag 17.06.22 15:52:16 von

neuester Beitrag 17.06.22 15:52:16 von

Beiträge: 541

ID: 1.196.712

ID: 1.196.712

Aufrufe heute: 0

Gesamt: 30.725

Gesamt: 30.725

Aktive User: 0

ISIN: CA8875221001 · WKN: A0B884 · Symbol: TK

0,1300

CAD

-3,70 %

-0,0050 CAD

Letzter Kurs 08.05.24 TSX Venture

Neuigkeiten

15.04.24 · Accesswire |

14.03.24 · Accesswire |

28.02.24 · Accesswire |

14.12.23 · Accesswire |

17.08.23 · Accesswire |

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,5300 | +15,22 | |

| 0,8100 | +11,11 | |

| 0,8000 | +11,11 | |

| 2,3640 | +10,11 | |

| 2,0800 | +10,05 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,5200 | -10,34 | |

| 10,520 | -12,33 | |

| 0,9860 | -12,74 | |

| 0,6000 | -18,37 | |

| 0,6601 | -26,22 |

Beitrag zu dieser Diskussion schreiben

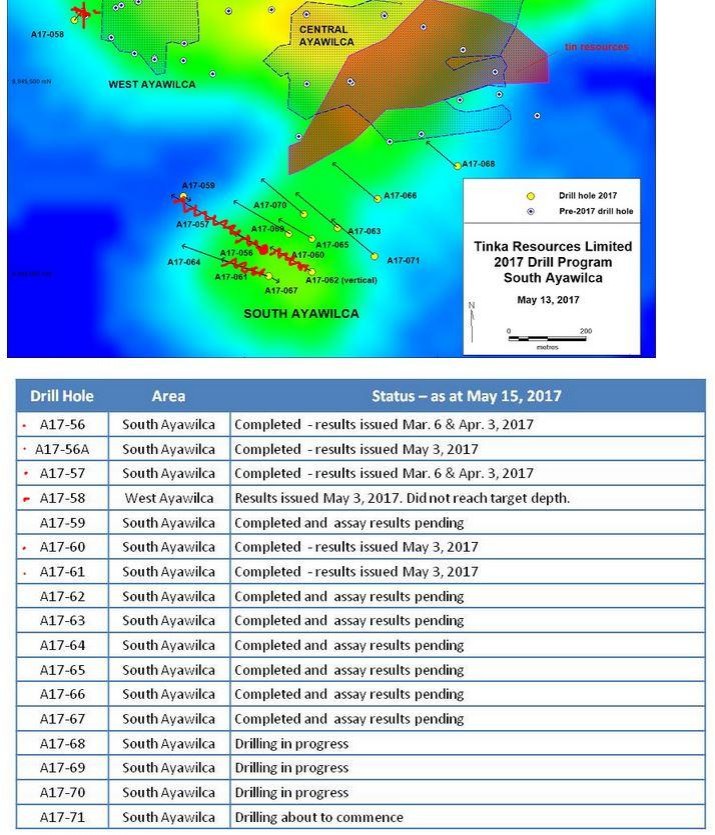

Es gibt eine neue Karte zum Bohrprogramm:

https://www.tinkaresources.com/projects/2017-drill-program

Heute habe ich dann doch noch einmal zugelegt: bei 0,60 zugekauft, nachdem sich wieder alle für Verkaufen entschieden haben... 5 Minuten später ging es dann doch noch weiter runter... kann man nix machen.

https://www.tinkaresources.com/projects/2017-drill-program

Heute habe ich dann doch noch einmal zugelegt: bei 0,60 zugekauft, nachdem sich wieder alle für Verkaufen entschieden haben... 5 Minuten später ging es dann doch noch weiter runter... kann man nix machen.

Antwort auf Beitrag Nr.: 55.036.903 von MaxPower2000 am 29.05.17 18:14:50

1. Die Ressource, die aktuell nachgewiesen ist, ist ungefähr so groß wie Trevali's Santander Projekt, nur mit höheren Gehalten

2. Der nachgewiesene Erzkörper hat hervorragendes Potenzial zum einfachen Abbau großer Tonnagen (ähnlich Cerro Lindo und Santander, die zwei peruanischen Minen mit den niedrigsten Abbaukosten)

3. die bisherigen Bohrergebnisse der South Zone haben die höchsten abbaubaren Gehalte in Peru hervorgebracht

4. die South Zone Entdeckung hat das Potenzial, die bisherige Ressource von Ayawilca zu verdoppeln

5. die Infrastruktur auf und um das Projekt herum ist ist sehr gut: es gibt eine Stromleitung, die direkt über das Projektgebiet läuft, es gibt eine große Mühle in der Nähe, die momentan nicht genutzt wird und es gibt einfachen Zugang zu Bahn und Hafen (Wasserversorgung ist übrigens auch kein Problem, nicht unwichtig für Bohrungen in dem Gebiet, meine Anmerkung)

6. Tinka ist umgeben von mittelgroßen Firmen und Big Playern, ala Volcan (Eigentümer der ungenutzten Mühle) und BHP

https://ceo.ca/tk?8f021abb8145

FAZIT: Habe heute zu 0,65 und 0,66 nochmal nachgelegt !

Gute Zusammenfassung von PamplonaTrader (Übersetzung von mir)

Was wir bis jetzt wissen:1. Die Ressource, die aktuell nachgewiesen ist, ist ungefähr so groß wie Trevali's Santander Projekt, nur mit höheren Gehalten

2. Der nachgewiesene Erzkörper hat hervorragendes Potenzial zum einfachen Abbau großer Tonnagen (ähnlich Cerro Lindo und Santander, die zwei peruanischen Minen mit den niedrigsten Abbaukosten)

3. die bisherigen Bohrergebnisse der South Zone haben die höchsten abbaubaren Gehalte in Peru hervorgebracht

4. die South Zone Entdeckung hat das Potenzial, die bisherige Ressource von Ayawilca zu verdoppeln

5. die Infrastruktur auf und um das Projekt herum ist ist sehr gut: es gibt eine Stromleitung, die direkt über das Projektgebiet läuft, es gibt eine große Mühle in der Nähe, die momentan nicht genutzt wird und es gibt einfachen Zugang zu Bahn und Hafen (Wasserversorgung ist übrigens auch kein Problem, nicht unwichtig für Bohrungen in dem Gebiet, meine Anmerkung)

6. Tinka ist umgeben von mittelgroßen Firmen und Big Playern, ala Volcan (Eigentümer der ungenutzten Mühle) und BHP

https://ceo.ca/tk?8f021abb8145

FAZIT: Habe heute zu 0,65 und 0,66 nochmal nachgelegt !

Scheinbar ist das 4. Bohrgerät wie versprochen in Zone 4 bereits bei der Arbeit:

"@benduck: Received today from IR; I questioned status of Zone 3..."The fourth rig was deployed at Zone 3 last week and is drilling the first hole in that zone as we speak.""

Quelle: Ein User (benduck) hat es auf https://ceo.ca/tk gepostet.

"@benduck: Received today from IR; I questioned status of Zone 3..."The fourth rig was deployed at Zone 3 last week and is drilling the first hole in that zone as we speak.""

Quelle: Ein User (benduck) hat es auf https://ceo.ca/tk gepostet.

Als kleinen Überblick habe ich mir mal die Ergebnisse und Bohrkarte von South Ayawilca vorgenommen und die Bohrungen, von denen wir bereits (hochgradige) Ergebnisse haben, mal kurz rot markiert (Loch -58 mal ausgenommen). Man sieht, dass da noch viel "unentdecktes Land" ist, von dem wir (hoffentlich schnell) Ergebnisse bekommen...

Aus Gründen der Ungedult hoffe ich, dass Teilergebnisse veröffetnlicht werden - und wir uns nicht auf eine große News freuen müssen...

https://www.tinkaresources.com/projects/2017-drill-program

Aus Gründen der Ungedult hoffe ich, dass Teilergebnisse veröffetnlicht werden - und wir uns nicht auf eine große News freuen müssen...

https://www.tinkaresources.com/projects/2017-drill-program

Trading Spotlight

Antwort auf Beitrag Nr.: 54.975.623 von trobs am 19.05.17 06:23:27

These 4 charts will turn you into a (raging) zinc price bull

http://www.mining.com/4-charts-will-turn-raging-zinc-price-b…

Heute nochmal zu 0,64 nachgelegt.

Mon May 15, 2017 | 2:39pm EDT

Zinc miners leverage scarcity to flex muscles over smelters: Andy Home

If there were any doubt that the zinc supply chain is tightening, it should be dispelled by this year's benchmark smelter treatment charge.

The treatment charge is the fee paid by a miner to a smelter for converting mined concentrates into refined metal and it is probably the best indicator of raw material availability; high during times of surplus and low during times of scarcity.

This year's headline fee of $172 per ton is the lowest in a decade, a firm swing of the negotiating pendulum in favor of miners and a tangible sign that the much-anticipated concentrates crunch has arrived.

Indeed, miners have used the squeeze on availability to make what might turn out to be a historic change in how these annual benchmark contracts are structured.

Zinc bulls have been waiting a long time for this supply squeeze and they may have to wait a bit longer before it moves from raw materials to refined metal parts of the chain.

But at a mined concentrates level it has very surely arrived... .

HEADLINE DOWN, PRICE PARTICIPATION OUT

This year's headline treatment charge of $172 per ton was confirmed by Belgium's Nyrstar, a zinc miner itself but a much bigger converter of concentrates into refined metal.

It represented a 15 percent decline from last year's benchmark of $203 per ton and was the lowest outcome since 2006.... .

This zinc supply crunch has been a long time coming and there have been plenty of false starts for over-eager bulls in recent years.

But, to quote Jonathan Leng, principle zinc analyst at Wood Mackenzie, "the record 6.3 percent fall in global mine supply in 2016 transformed the concentrate market."

Concentrate stocks fell to "minimum working levels" in September of last year and smelters, particularly those in China, are having to cut production.

Nor does Woodmac see much change in the zinc concentrates market any time soon. Its view is that it will remain tight for the next couple of years with treatment charges likely to remain at correspondingly low levels over that period.

What does this mean for the refined zinc price?

So far bulls have been frustrated that mine supply crunch hasn't translated into refined metal crunch.

China's imports of refined zinc remain subdued, while metal is still occasionally appearing on LME warrant at New Orleans, albeit not in the sort of volumes as seen in the past.

Woodmac's Leng, however, believes it's only a matter of time. He expects to see acute tightness later this year with stocks "projected to fall to historically low levels and remain so until 2020."

That will translate into a price high next year "comparable to the 2006 price peak".

Not everyone, it's fair to say, is quite so bullish. There are still a good number of known unknowns at work, not least the state of mine supply in China itself.

But this year's benchmark concentrates terms make it hard to argue against the starting proposition of bulls such as Wood Mackenzie.

The concentrates market is as tight as it's been since 2006.

Whether that means a return to the historical peak in zinc prices in that year remains to be seen.

http://www.reuters.com/article/us-zinc-concentrates-ahome-id…

Zinc miners leverage scarcity to flex muscles over smelters: Andy Home

If there were any doubt that the zinc supply chain is tightening, it should be dispelled by this year's benchmark smelter treatment charge.

The treatment charge is the fee paid by a miner to a smelter for converting mined concentrates into refined metal and it is probably the best indicator of raw material availability; high during times of surplus and low during times of scarcity.

This year's headline fee of $172 per ton is the lowest in a decade, a firm swing of the negotiating pendulum in favor of miners and a tangible sign that the much-anticipated concentrates crunch has arrived.

Indeed, miners have used the squeeze on availability to make what might turn out to be a historic change in how these annual benchmark contracts are structured.

Zinc bulls have been waiting a long time for this supply squeeze and they may have to wait a bit longer before it moves from raw materials to refined metal parts of the chain.

But at a mined concentrates level it has very surely arrived... .

HEADLINE DOWN, PRICE PARTICIPATION OUT

This year's headline treatment charge of $172 per ton was confirmed by Belgium's Nyrstar, a zinc miner itself but a much bigger converter of concentrates into refined metal.

It represented a 15 percent decline from last year's benchmark of $203 per ton and was the lowest outcome since 2006.... .

This zinc supply crunch has been a long time coming and there have been plenty of false starts for over-eager bulls in recent years.

But, to quote Jonathan Leng, principle zinc analyst at Wood Mackenzie, "the record 6.3 percent fall in global mine supply in 2016 transformed the concentrate market."

Concentrate stocks fell to "minimum working levels" in September of last year and smelters, particularly those in China, are having to cut production.

Nor does Woodmac see much change in the zinc concentrates market any time soon. Its view is that it will remain tight for the next couple of years with treatment charges likely to remain at correspondingly low levels over that period.

What does this mean for the refined zinc price?

So far bulls have been frustrated that mine supply crunch hasn't translated into refined metal crunch.

China's imports of refined zinc remain subdued, while metal is still occasionally appearing on LME warrant at New Orleans, albeit not in the sort of volumes as seen in the past.

Woodmac's Leng, however, believes it's only a matter of time. He expects to see acute tightness later this year with stocks "projected to fall to historically low levels and remain so until 2020."

That will translate into a price high next year "comparable to the 2006 price peak".

Not everyone, it's fair to say, is quite so bullish. There are still a good number of known unknowns at work, not least the state of mine supply in China itself.

But this year's benchmark concentrates terms make it hard to argue against the starting proposition of bulls such as Wood Mackenzie.

The concentrates market is as tight as it's been since 2006.

Whether that means a return to the historical peak in zinc prices in that year remains to be seen.

http://www.reuters.com/article/us-zinc-concentrates-ahome-id…

Antwort auf Beitrag Nr.: 54.960.107 von MaxPower2000 am 17.05.17 08:59:26A17-068 ist ja noch nicht beendet gewesen (zumindest nicht bis zum 13.Mai), von daher wahrscheinlich auch erst im Mai begonnen und nicht auf der vorherigen Karte eingezeichnet.

Ich denke mir nur, dass ja A17-066 von der Positionierung her eine ganz klare Bohrung ist, um die Verbindung von Ayawilca Central mit South zu prüfen.

Wenn das ein "duster" war, würde ich mir ja eine weitere Prüfung einer möglichen Verbindung (die ja A17-068 offensichtlich darstellt) zwischen den beiden Gebieten sparen können.

Und da Zink in Limestone offensichtlich sehr gut mit dem bloßen Auge erkennbar ist, braucht man auch keine Essays der Bohrkerne abwarten, um weitere Bohrentscheidungen zu treffen.

Ich denke mir nur, dass ja A17-066 von der Positionierung her eine ganz klare Bohrung ist, um die Verbindung von Ayawilca Central mit South zu prüfen.

Wenn das ein "duster" war, würde ich mir ja eine weitere Prüfung einer möglichen Verbindung (die ja A17-068 offensichtlich darstellt) zwischen den beiden Gebieten sparen können.

Und da Zink in Limestone offensichtlich sehr gut mit dem bloßen Auge erkennbar ist, braucht man auch keine Essays der Bohrkerne abwarten, um weitere Bohrentscheidungen zu treffen.