Focus Minerals, Spekulation der Woche (Seite 63)

eröffnet am 23.01.07 09:45:03 von

neuester Beitrag 27.08.23 12:43:07 von

neuester Beitrag 27.08.23 12:43:07 von

Beiträge: 11.981

ID: 1.106.732

ID: 1.106.732

Aufrufe heute: 1

Gesamt: 1.489.000

Gesamt: 1.489.000

Aktive User: 0

ISIN: AU000000FML4 · WKN: A0F610 · Symbol: FZA

0,1180

EUR

-1,67 %

-0,0020 EUR

Letzter Kurs 26.04.24 Tradegate

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,4700 | +28,95 | |

| 2,6900 | +23,96 | |

| 0,8900 | +17,11 | |

| 0,5800 | +16,00 | |

| 0,5650 | +13,00 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,1500 | -9,45 | |

| 3,3200 | -9,78 | |

| 4,5000 | -12,62 | |

| 3,9600 | -15,74 | |

| 12,000 | -25,00 |

Beitrag zu dieser Diskussion schreiben

um vorzubeugen: hier kann es jederzeit +100% nach oben, aber auch -50% nach unten gehen (in einer Woche oder zwei)

Focus Minerals (FML) - (I)-(II) - Anmerkungen

(0) Zunächst:Da hab ich anscheinend einen empfindlichen Nerv getroffen, mussten meine Beiträge zu Laverton doch unbedingt noch am Samstagvormittag mit (ebenfalls) Monster-Postings, argumentativ nicht bei der Sache und teilweise wieder kindisch personalisiert, nach oben geschoben werden:

=> das an sich spricht schon Bände und lässt nichts Gutes für den zukünftigen Aktienkurs von FML für das restliche Jahr 2017 hoffen.

=> ganz cool bleiben an der Börse

__

Generell gilt:

(A) FML ist insgesamt eine sehr komplexe Operation in Bezug auf die geringe Marktkapitalisierung.

Damit sind notwendigerweise auch nochmals erhöhte Risiken verbunden. Binsenweisheit, sonst wäre der Aktienkurs ja (viel) weiter oben.

=> da würde ich mir einen einfacheren 1-Minen-WA-Goldminer in spe suchen gehen bevor ich hier eine Neuposition eingehen würde.

(WA = Western Australia)

(B) FML hat mit den Laverton-Operations eine schwierige bis unmögliche Lagerstätte am Hals

(ich weiss, ich wiederhole mich hier)

Das eröffnet einem Skeptiker bei näherer Recherche eine weitläufige Spielwiese.

Wer da die Geschichte nicht kennt, hat womöglich die ganz falsche Erwartungshaltung an seine FML-Position.

(C) Der Aktienkurs nach oben ist auch bei Produktionsstart und Ramp-up eher begrenzt. (iSv nachhaltig)

(dazu aus (D) unten im Vorgriff):

Unter Punkt 6. (nur Coolgardie-Plant-Produktion) und später Punkt 8. findet man diese Rechnung:

"...a conservative 40,000 ounces at a conservative $500 per ounce gives a conservative $20 million in the first year of resumed processing."

=> AUD(500 x 40k) / 180m (shares) = AUD0.11/share pre Laverton (pretax)

Nachdem der Autor mit AUD10m an Gesamt-Explorationskosten rechnet (grosszügig; kann aber durchaus notwendig sein), möchte er mit einer Dividende von AUD0.05/share rechnen können ("unfranked", AUS-Steuerkonzept):

=> so einfach ist das nicht:

- man kann zwar zunächst Pretax mit Tax vereinfacht annehmen wg. dem erheblichen Verlustvortrag (aber wer hier ist schon WA+AUS-Corporate-Taxexpert?), aber das (freie) Geld wird auch woanders benötigt als nur für eine mögliche Dividende (was für einen Gerade-Junior-Produzenten schon mal an sich unrealistisch ist), nämlich für die weiter laufenden:

(C1) C+M-Kosten bei Laverton (vielleicht nochmals reduziert 2017 auf grob AUD0.5m)

(C2) sowie alle Nicht-C+M-und-Nicht-Expl.-Kosten bei Laverton (die bislang immer noch nicht hier beziffert wurden)

(C3) sowie - am wichtigsten - die Wiederinstandsetzungkosten für Barnicoat (sonst stimmt Punkt 19., also Mit-Produktion Barnicoat, überhaupt nicht)

__(und Erz-Trucking nach GSM ist ungewiss und mit völlig unbekannten Kosten bislang anzusetzen)

=> nicht vergessen: das jetzige FML-Management hat bzgl. Barnicoat keinerlei Erfahrung, weil diese Anlage bereits 2008 in C+M ging (also weit vor der Crescent Gold-Übernahme)

__

(D) HC:

(Da) zu "Bericht von SNM aus dem HotCopper-Board": Form

Das ist eben der Unterschied. Ich mache wie oben wiederholt "DYOR" gefordert, und andere kopieren als Gegenargument seitenweise und unkommentiert aus anderen Foren. User SNM hat sich erkennbar grosse Mühe gegeben. Man sollte ihm wenigstens eine Dankesmail nach Australien schicken, wenn man sein Posting hier schon ungefragt einstellt.

__

(Db) zu "Bericht von SNM aus dem HotCopper-Board": Inhalt bzgl. Laverton

SNM äussert sich bei 4 Punkten zu Laverton:

Er macht zunächst eine zurückhaltende Äusserung hierzu mit:

"...I note that the Laverton triangle (see page 17 of the AGM presentation) has nothing in the top segment..."

...um dann die Bedeutung von Laverton bei 2 von insgesamt 6 Faktoren für höhere Aktienkurse aufzulisten:

"(3) when (or, for the pessimists, if) they discover more gold in Laverton,..."

(-->

- das deutet mMn auf weitere Probleme bei Laverton hin, auf die ich (noch) nicht eingegangen bin

- und, hier stehe ich also mit einem anderen pessimistischen Faktor bei Laverton nicht alleine da)

"(4) when they resume production in Laverton (in addition to Coolgardie)"

Punkt 19 zieht dann Laverton noch in eine grobe Gesamt-Profitrechnung mit ein (siehe (4) oben),

die bei Einschluss der von ihm angenommenen Laverton-Produktion zu einem P/E (pretax) von 1.0 käme (bei AUD0.50 = P = E). (Da wird - nicht unüblich im Minenbereich - das Bärenfell schon mal verteilt, bevor der überhaupt erlegt ist.)

SNM hat eben eine optimistische Sicht auf Laverton und bezieht folglich am Ende seiner Argumentation Laverton fortlaufend mit ein. Ist prinzipiell OK, und zumindest sehr nett vorgetragen.

=> was soll man daraus schliessen? Ohne Laverton würde die halbe Fantasie fehlen?

hier hängt

shandong drin..was soll hier noch passieren...in dem chinesen seinem kopf..gehört australien eh schon ihm.

Damit die Verbreitung von Unsinn und pseudowissenschaftlien Abhandlungen hier nicht die Überhand gewinnen stelle ich einen Bericht von "SNM" aus dem HotCopper-Board (Australien) hier ein.

Wenn der Thread hier jetzt leider vermüllt/vergiftet wird ist es vielleicht sowieso ratsam zusätzliche Informationen auf HotCopper zu beachten (die Jungs sind auch näher am Geschehen). Jetzt die Jahre 2012 und 2013 oder 2014 zu bewerten ist reine Zeitverschwendung und hat nichts mit der heutigen Realität zu tun!!! Weder hier, noch bei Google und auch nicht beim Bitcoin usw. usw.!

Quelle: https://hotcopper.com.au/threads/the-ugly-duckling-is-becomi…

1 - Apologies, in advance, if this seems more like an essay than a post. You may want to get a cup of coffee so you are still with me at the end! Kindly note that I have used AUD amounts throughout.

2 - Having looked at the PowerPoint presentation to the recent AGM, I note that the Laverton triangle (see page 17 of the AGM presentation) has nothing in the top segment but the Coolgardie triangle (ditto, page 6) does. That suggests the resumption of production will be at Coolgardie first.

3 - The AGM presentations, both last year and this year, referred to Tindalls as the backbone of future, i.e. resumed, production. From the most recent table for reserves, Tindalls has 616,500 ounces at 2.2 grams/tonne in the surface area and a further 234,500 ounces at 3.9 grams/tonne underground. Obviously you have to do the surface first. So the good news is that the surface ore is easy to access but the bad news is that the grade is not as high as most of the other grades.

4 – Simply put, It appears that Tindalls has the reserves needed to create the five-year mine life which is one of their stated criteria for resumed processing.

5 - The Coolgardie plant is said to have a capacity of 1.2 millions tonnes pa. I would have assumed they would use all of that capacity but if they do not expect to use all that capacity then they may do a deal to process the ore of someone else nearby in return for them contributing to the recommissioning cost. It occurs to me that they might not only recommission but also expand the capacity of the plant. Anyway, since I want my analysis to be on the conservative side, I assume they only use half the 1.2 million tonnes per annum capacity of that plant.

6 - 600,000 tonnes pa at a grade of 2 grams per tonne gives 1.2 million grams of gold and that is, roughly, 40,000 ounces. I assume an all up cost of $1,000 per ounce. I pick that figure because FML stopped processing when the price of gold fell to $1,200 but (1) costs should have gone done since then after the mining boom finished, and (2) the Shandong expertise should help to lower costs. I assume a sale price of $1,500 per ounce, again being conservative, allowing for a drop in the price from current price which is close to $1,700 per ounce. Even if FML’s costs end up being $1,100 per ounce and the price drops to $1,600 per ounce, it seems to me they are still going to have a margin of $500 per ounce. So a conservative 40,000 ounces at a conservative $500 per ounce gives a conservative $20 million in the first year of resumed processing.

7 - From the most recent Annual Report, i.e. for the year ended 31 December 2016, FML has Accumulated Losses of $319 million. So the good news is that, for the first few years, there should be no company tax but the bad news is that any dividends will be unfranked.

8 - in the last year (i.e. 2016 calendar year) they spent $9 million on exploration so I assume $10 million of the $20 million profit for exploration which would leave $10 million and that is enough for a dividend of 5 cents per share as that would cost $9.1 million since there are 182 million issued shares.

9 - I note there are no share options on issue or proposed and that there is enough cash to both continue exploration and resume production. Obviously, there is no problem selling the gold because China will take it thanks to the Shandong connection.

10 - If they resume processing by the end of the 2017 calendar year then the first full year of production would be 2018 and the first dividend could be declared after the accounts for the company’s financial year ending 31 December 2018, i.e. in around March 2019, and paid around the time of the AGM in a May 2019, i.e. two years from now.

11 - If my assumption of 5 cents per share dividend is correct then, based on the current price of other ASX listed gold miners that pay dividends, i.e. share price expressed as a multiple of the dividend paid, the FML share price would be at least $1.50 (30 times the dividend) and the good future prospects for FML may reasonably be expected to push the share price higher than that.

12 – Or, in terms of earnings per share, if I stay with 40,000 ounces at a margin of $500 per ounce, giving a profit of $20 million, i.e. earnings of 11 cents per share. At the current share price of around 44 cents, that gives a price-earnings (PE) ratio of only 4 and that suggests a much higher share price. My bank-related stockbroking site suggests a PE for this sector of just over 12 so, on that basis, the shares should be 3 times the current share price of 44 cents (or 12 times earnings of 11 cents per share) which is $1.32, a 200% gain for those buying at 44 cents.

13 - If what appears above is correct then there could be as many as five significant share price increases:

(1) when they resume production in Coolgardie (which may become clearer after the PFS that is due to be received by FML in June),

(2) when they start paying dividends,

(3) when (or, for the pessimists, if) they discover more gold in Laverton,

(4) when they resume production in Laverton (in addition to Coolgardie),

(5) when they increase production levels (I have assumed a low level of initial, resumed production of 40,000 ounces in order to be conservative),

(6) when the price of gold goes up.

14 - With a market capitalisation of around $80 million (182 million shares at 44 cents per share) and cash on hand of around $45 million, shareholders get all those gold reserves and future prospects for $35 million which is just under 20 cents per share.

15 - Even if someone now pays 50 cents per share then, if my figures are correct the even if the share price two years from now is only $1.50 and if the dividend is 5 cents then investors get a capital gain of 200% in two years and then a return of 10% pa on their 50 cents/share investment from the (initially unfranked but later franked) dividends.

16 – For those who think my half the Coolgardie plant's capacity assumption of 600,000 tonnes pa is too low then, as an alternative, I assume 900,000 tonnes pa (being either operating plant with a 1.2 million tonnes pa capacity either (1) at 75% of capacity all the time or (2) at full capacity 75% of the time. Again, assume a measly 2 grams per tonne. That would give 1.8 million grams or about 60,000 ounces and, at a margin of $500 per ounce, the profit is $30 million. Ignoring company tax (due to tax losses of $319 million) and deducting $10 million for continued exploration leaves enough to pay a dividend of 10 cents per share and a likely share price in the region of $3 (30 times the 10 cents dividend) or at least $2 (a PE ratio of 12 and earnings of $30 million which is 16 cents per share). Of course, PE ratio devotees know that share prices tend to be based on forward earnings, i.e. next year’s earnings and not last year’s earnings. Either way, under the assumptions in this paragraph, the share price should be between $2 and $3.

17 - Shandong paid $2.50 for their shares (around 4.5 billion shares at 5 cents each gave the $225 million Shandong paid, then the 1 for 50 conversion means they got roughly 90 million shares for their $225 million which equals $2.50 per share). If the share price got back to $2.50 they would break even. At $3 they would have a 20% capital gain. A sustainable dividend of 5 cents per share dividend would provide a 2% return on their investment and they would have the prospect of further capital gains and dividend growth.

18 - Once dividends commence, the prospect of higher dividends would come from any or all of:

(1) a higher level of processing (I have assumed only 40,000 ounces but they were doing much more than that – I seem to recall, some time ago, seeing a figure of around 170,000 ounces - before they mothballed their plants),

(2) higher grades recovered (I have assumed only 2 grams/tonne and they have higher grades than that in a number of areas),

(3) a higher price for gold.

19 – If you want another basis of calculation then take 170,000 ounces, round it up to 180,000 ounces (to make the maths easier) and assume FML produces that much gold in a year. 180,000 ounces multiplied by an assume margin of $500 an ounce divided by 180 million shares (in round figures) gives 50 cents per share pa which, even allowing for $10 million of that money to be spent on further exploration, gives annual earnings before tax of around the current share price! If you think that figure is too high then I note that to get 180,000 ounces from the current plant capacities (1.2 mtpa at Coolgardie and 1.45 mtpa at Laverton) you would only need a gold grade of 2.7 grams/tonne: 2.65 million tonnes, with plants operating at around 75% capacity, would process 2 mtpa and assuming recovery of 2.7 grams per tonne gives 5.4 million grams or around 180,000 ounces pa.

20 – I note there is a “double whammy” of when processing better grades. For example, if it costs $1,000 an ounce to get 2 grams of gold out of a tonne of ore then if a tonne of ore yields 4 grams for the same outlay then the margin is higher because the same cost is spread over twice the gold. In other words, the better the grade not only provides more ounces of gold but also should result in a greater margin for each of those ounces.

21 - In the case of Tindalls, the underground resource is shown as having 3.9 grams per tonne. While there may be greater costs in extracting ore from what are referred to as the UG reserves than the surface reserves, I would doubt that any additional cost would double the cost per ounce so the progression from Tindalls surface ore to Tindalls UG should result in a greater margin.

22 - I also note that FML:

(1) has gold reserves so it is not one of those pure exploration companies, i.e. cross your fingers and hope they find gold at some time in the future,

(2) has reserves in Australia and not some country with significant sovereign risk,

(3) is not likely to require any capital raising,

(4) has experienced management and directors, and

(5) has links to China which clearly has a strategy for the future which favours gold as revealed by its appetite for gold in recent years, i.e. China would not be accumulating gold if it did not think the price of gold was going to go up.

23 - All that said, I find it hard to see a better investment on the ASX and FML appears to meet my favourite investment criteria of a stock for which it can be said that investment profit, from capital gain and /or dividends, is a question of "when, not if".

24 - I understand that many current shareholders have an average cost above the current spare price. It seems to me there is a need for patience, an often forgotten ingredient in stock exchange investment, which, in order to be successful, needs three ingredients:

(1) buying at the right time,

(2) selling at the right time, and

(3) patience in between those times.

25 - But I do not see FML as a purely speculative stock: it appears to be a good long term investment (i.e. a stock with good growth prospects), especially as a stock that will provide refuge from a financial crisis and as a way to profit from a gold price increase in a leveraged manner, meaning that if the price of gold goes from $1,600 to $2,000 then someone owning gold bars would achieve a 25% increase in value but if the price of gold goes from $1,600 to $2,000 per ounce then that $400 increase in the per ounce price of gold would mean that FML’s margin goes from $500 (assuming 1600-1100) to $900 (i.e. 2000-1100) and an FML shareholder should achieve an 80% increase in value. In other words, buying an FML share is the same as borrowing $1,100 for every ounce of gold you buy at $1,600.

26 – There are three kinds of gold companies:

(1) those who only explore: they risk running out of money;

(2) those who only mine: they risk running out of ore; and

(3) those who mine and explore: funding exploration from mining revenue thus extending mine life.

Happily, it appears it will not be too long before FML is a “category 3 company”.

27 – Further, bear in mind that there are only 182 million shares and, from the list of top twenty shareholders, it would appear that at least 2/3 and probably 3/4 of those shares are tightly held with the result that when FML is discovered by the market, the price may well rise more quickly than a stock with a lot of shares which are not tightly held.

28 – I wonder how long it will be before one of those investment subscription services “discovers” FML and creates a situation that resembles a herd of sheep trying to get through a narrow gate because of the comparatively small number of available shares.

29 – Finally, to give credit where credit is due, the Shandong people are carefully and sensibly turning an ugly duckling into a swan. I shudder to think where FML would be today without them. Over many years, I have noticed a strong correlation between good managers/directors and good performance and FML appears, to me, to support that view.

30 – It seems to me that HC users who follow FML do so for one of a number of reasons:

(1) Their average cost exceeds the current SP who wonder when/if they’ll get their money back,

(2) They are short-term investors who want to make money quickly,

(3) They are long-term investors who want to confirm they have made a good decision, or

(4) They are potential investors who don’t want to make a bad decision.

31 - Regardless of which of those descriptions fits you, the usual two rules apply:

Rule 1 – DYOR

Rule 2 – See Rule 1!

32 – I would welcome any constructive criticism of this analysis from the HC forum and I can only hope that any resulting discussion does not degenerate into comments that require moderation.

Wenn der Thread hier jetzt leider vermüllt/vergiftet wird ist es vielleicht sowieso ratsam zusätzliche Informationen auf HotCopper zu beachten (die Jungs sind auch näher am Geschehen). Jetzt die Jahre 2012 und 2013 oder 2014 zu bewerten ist reine Zeitverschwendung und hat nichts mit der heutigen Realität zu tun!!! Weder hier, noch bei Google und auch nicht beim Bitcoin usw. usw.!

Quelle: https://hotcopper.com.au/threads/the-ugly-duckling-is-becomi…

1 - Apologies, in advance, if this seems more like an essay than a post. You may want to get a cup of coffee so you are still with me at the end! Kindly note that I have used AUD amounts throughout.

2 - Having looked at the PowerPoint presentation to the recent AGM, I note that the Laverton triangle (see page 17 of the AGM presentation) has nothing in the top segment but the Coolgardie triangle (ditto, page 6) does. That suggests the resumption of production will be at Coolgardie first.

3 - The AGM presentations, both last year and this year, referred to Tindalls as the backbone of future, i.e. resumed, production. From the most recent table for reserves, Tindalls has 616,500 ounces at 2.2 grams/tonne in the surface area and a further 234,500 ounces at 3.9 grams/tonne underground. Obviously you have to do the surface first. So the good news is that the surface ore is easy to access but the bad news is that the grade is not as high as most of the other grades.

4 – Simply put, It appears that Tindalls has the reserves needed to create the five-year mine life which is one of their stated criteria for resumed processing.

5 - The Coolgardie plant is said to have a capacity of 1.2 millions tonnes pa. I would have assumed they would use all of that capacity but if they do not expect to use all that capacity then they may do a deal to process the ore of someone else nearby in return for them contributing to the recommissioning cost. It occurs to me that they might not only recommission but also expand the capacity of the plant. Anyway, since I want my analysis to be on the conservative side, I assume they only use half the 1.2 million tonnes per annum capacity of that plant.

6 - 600,000 tonnes pa at a grade of 2 grams per tonne gives 1.2 million grams of gold and that is, roughly, 40,000 ounces. I assume an all up cost of $1,000 per ounce. I pick that figure because FML stopped processing when the price of gold fell to $1,200 but (1) costs should have gone done since then after the mining boom finished, and (2) the Shandong expertise should help to lower costs. I assume a sale price of $1,500 per ounce, again being conservative, allowing for a drop in the price from current price which is close to $1,700 per ounce. Even if FML’s costs end up being $1,100 per ounce and the price drops to $1,600 per ounce, it seems to me they are still going to have a margin of $500 per ounce. So a conservative 40,000 ounces at a conservative $500 per ounce gives a conservative $20 million in the first year of resumed processing.

7 - From the most recent Annual Report, i.e. for the year ended 31 December 2016, FML has Accumulated Losses of $319 million. So the good news is that, for the first few years, there should be no company tax but the bad news is that any dividends will be unfranked.

8 - in the last year (i.e. 2016 calendar year) they spent $9 million on exploration so I assume $10 million of the $20 million profit for exploration which would leave $10 million and that is enough for a dividend of 5 cents per share as that would cost $9.1 million since there are 182 million issued shares.

9 - I note there are no share options on issue or proposed and that there is enough cash to both continue exploration and resume production. Obviously, there is no problem selling the gold because China will take it thanks to the Shandong connection.

10 - If they resume processing by the end of the 2017 calendar year then the first full year of production would be 2018 and the first dividend could be declared after the accounts for the company’s financial year ending 31 December 2018, i.e. in around March 2019, and paid around the time of the AGM in a May 2019, i.e. two years from now.

11 - If my assumption of 5 cents per share dividend is correct then, based on the current price of other ASX listed gold miners that pay dividends, i.e. share price expressed as a multiple of the dividend paid, the FML share price would be at least $1.50 (30 times the dividend) and the good future prospects for FML may reasonably be expected to push the share price higher than that.

12 – Or, in terms of earnings per share, if I stay with 40,000 ounces at a margin of $500 per ounce, giving a profit of $20 million, i.e. earnings of 11 cents per share. At the current share price of around 44 cents, that gives a price-earnings (PE) ratio of only 4 and that suggests a much higher share price. My bank-related stockbroking site suggests a PE for this sector of just over 12 so, on that basis, the shares should be 3 times the current share price of 44 cents (or 12 times earnings of 11 cents per share) which is $1.32, a 200% gain for those buying at 44 cents.

13 - If what appears above is correct then there could be as many as five significant share price increases:

(1) when they resume production in Coolgardie (which may become clearer after the PFS that is due to be received by FML in June),

(2) when they start paying dividends,

(3) when (or, for the pessimists, if) they discover more gold in Laverton,

(4) when they resume production in Laverton (in addition to Coolgardie),

(5) when they increase production levels (I have assumed a low level of initial, resumed production of 40,000 ounces in order to be conservative),

(6) when the price of gold goes up.

14 - With a market capitalisation of around $80 million (182 million shares at 44 cents per share) and cash on hand of around $45 million, shareholders get all those gold reserves and future prospects for $35 million which is just under 20 cents per share.

15 - Even if someone now pays 50 cents per share then, if my figures are correct the even if the share price two years from now is only $1.50 and if the dividend is 5 cents then investors get a capital gain of 200% in two years and then a return of 10% pa on their 50 cents/share investment from the (initially unfranked but later franked) dividends.

16 – For those who think my half the Coolgardie plant's capacity assumption of 600,000 tonnes pa is too low then, as an alternative, I assume 900,000 tonnes pa (being either operating plant with a 1.2 million tonnes pa capacity either (1) at 75% of capacity all the time or (2) at full capacity 75% of the time. Again, assume a measly 2 grams per tonne. That would give 1.8 million grams or about 60,000 ounces and, at a margin of $500 per ounce, the profit is $30 million. Ignoring company tax (due to tax losses of $319 million) and deducting $10 million for continued exploration leaves enough to pay a dividend of 10 cents per share and a likely share price in the region of $3 (30 times the 10 cents dividend) or at least $2 (a PE ratio of 12 and earnings of $30 million which is 16 cents per share). Of course, PE ratio devotees know that share prices tend to be based on forward earnings, i.e. next year’s earnings and not last year’s earnings. Either way, under the assumptions in this paragraph, the share price should be between $2 and $3.

17 - Shandong paid $2.50 for their shares (around 4.5 billion shares at 5 cents each gave the $225 million Shandong paid, then the 1 for 50 conversion means they got roughly 90 million shares for their $225 million which equals $2.50 per share). If the share price got back to $2.50 they would break even. At $3 they would have a 20% capital gain. A sustainable dividend of 5 cents per share dividend would provide a 2% return on their investment and they would have the prospect of further capital gains and dividend growth.

18 - Once dividends commence, the prospect of higher dividends would come from any or all of:

(1) a higher level of processing (I have assumed only 40,000 ounces but they were doing much more than that – I seem to recall, some time ago, seeing a figure of around 170,000 ounces - before they mothballed their plants),

(2) higher grades recovered (I have assumed only 2 grams/tonne and they have higher grades than that in a number of areas),

(3) a higher price for gold.

19 – If you want another basis of calculation then take 170,000 ounces, round it up to 180,000 ounces (to make the maths easier) and assume FML produces that much gold in a year. 180,000 ounces multiplied by an assume margin of $500 an ounce divided by 180 million shares (in round figures) gives 50 cents per share pa which, even allowing for $10 million of that money to be spent on further exploration, gives annual earnings before tax of around the current share price! If you think that figure is too high then I note that to get 180,000 ounces from the current plant capacities (1.2 mtpa at Coolgardie and 1.45 mtpa at Laverton) you would only need a gold grade of 2.7 grams/tonne: 2.65 million tonnes, with plants operating at around 75% capacity, would process 2 mtpa and assuming recovery of 2.7 grams per tonne gives 5.4 million grams or around 180,000 ounces pa.

20 – I note there is a “double whammy” of when processing better grades. For example, if it costs $1,000 an ounce to get 2 grams of gold out of a tonne of ore then if a tonne of ore yields 4 grams for the same outlay then the margin is higher because the same cost is spread over twice the gold. In other words, the better the grade not only provides more ounces of gold but also should result in a greater margin for each of those ounces.

21 - In the case of Tindalls, the underground resource is shown as having 3.9 grams per tonne. While there may be greater costs in extracting ore from what are referred to as the UG reserves than the surface reserves, I would doubt that any additional cost would double the cost per ounce so the progression from Tindalls surface ore to Tindalls UG should result in a greater margin.

22 - I also note that FML:

(1) has gold reserves so it is not one of those pure exploration companies, i.e. cross your fingers and hope they find gold at some time in the future,

(2) has reserves in Australia and not some country with significant sovereign risk,

(3) is not likely to require any capital raising,

(4) has experienced management and directors, and

(5) has links to China which clearly has a strategy for the future which favours gold as revealed by its appetite for gold in recent years, i.e. China would not be accumulating gold if it did not think the price of gold was going to go up.

23 - All that said, I find it hard to see a better investment on the ASX and FML appears to meet my favourite investment criteria of a stock for which it can be said that investment profit, from capital gain and /or dividends, is a question of "when, not if".

24 - I understand that many current shareholders have an average cost above the current spare price. It seems to me there is a need for patience, an often forgotten ingredient in stock exchange investment, which, in order to be successful, needs three ingredients:

(1) buying at the right time,

(2) selling at the right time, and

(3) patience in between those times.

25 - But I do not see FML as a purely speculative stock: it appears to be a good long term investment (i.e. a stock with good growth prospects), especially as a stock that will provide refuge from a financial crisis and as a way to profit from a gold price increase in a leveraged manner, meaning that if the price of gold goes from $1,600 to $2,000 then someone owning gold bars would achieve a 25% increase in value but if the price of gold goes from $1,600 to $2,000 per ounce then that $400 increase in the per ounce price of gold would mean that FML’s margin goes from $500 (assuming 1600-1100) to $900 (i.e. 2000-1100) and an FML shareholder should achieve an 80% increase in value. In other words, buying an FML share is the same as borrowing $1,100 for every ounce of gold you buy at $1,600.

26 – There are three kinds of gold companies:

(1) those who only explore: they risk running out of money;

(2) those who only mine: they risk running out of ore; and

(3) those who mine and explore: funding exploration from mining revenue thus extending mine life.

Happily, it appears it will not be too long before FML is a “category 3 company”.

27 – Further, bear in mind that there are only 182 million shares and, from the list of top twenty shareholders, it would appear that at least 2/3 and probably 3/4 of those shares are tightly held with the result that when FML is discovered by the market, the price may well rise more quickly than a stock with a lot of shares which are not tightly held.

28 – I wonder how long it will be before one of those investment subscription services “discovers” FML and creates a situation that resembles a herd of sheep trying to get through a narrow gate because of the comparatively small number of available shares.

29 – Finally, to give credit where credit is due, the Shandong people are carefully and sensibly turning an ugly duckling into a swan. I shudder to think where FML would be today without them. Over many years, I have noticed a strong correlation between good managers/directors and good performance and FML appears, to me, to support that view.

30 – It seems to me that HC users who follow FML do so for one of a number of reasons:

(1) Their average cost exceeds the current SP who wonder when/if they’ll get their money back,

(2) They are short-term investors who want to make money quickly,

(3) They are long-term investors who want to confirm they have made a good decision, or

(4) They are potential investors who don’t want to make a bad decision.

31 - Regardless of which of those descriptions fits you, the usual two rules apply:

Rule 1 – DYOR

Rule 2 – See Rule 1!

32 – I would welcome any constructive criticism of this analysis from the HC forum and I can only hope that any resulting discussion does not degenerate into comments that require moderation.

viel bla bla mal wieder.

Fakt ist:

Die Chinesen halten 49 % der Aktien.

Die Chinesen haben (so weit ich das noch in Erinnerung habe) knapp 3 AUD pro Aktie vor Jahren gezahlt.

Die Chinesen, haben FML NICHT aufgegeben.

Die Chinesen um Shangdong, werden eines Tages wieder den "alten" Aktienpreis bzw. einen weit aus höheren sehen wollen.

Wenn der F.C so negativ zu FML steht...warum hat er seine Aktien noch nicht verkauft?

Ich bin vor Jahren...als es absehbar war, das Gold weiter abstürzt....aus ALLEN Goldminern ausgestiegen.

Wer der Meinung ist, dass Gold seinen Tiefststand der letzten Jahre noch nicht gesehen hat...der

sollte sowieso aus den Minern aussteigen.

Wer glaubt, dass Gold ein unterbewertetes Asset ist...welches enormes Potential nach OBEN hat, der

sollte sich neben physichem Gold....auch unterbewertete Goldminer...bzw. Developer/Explorer ins

Depot werfen..um den kommenden Goldpreisanstieg zu hebeln.

Manch ein "Gold-Bug" sieht momentan noch die Crypto-Währungen...wie Bitcoin, Ethereum als

"Blase", welche platzen wird.

Ich sehe die Cryptos...als Vorbote eines explosiven Gold/Silber Anstieges.

Die Cryptos laufen dem Edelmetall voraus.

Die Cryptos, sitzen im gleichen Boot....wie Gold/Silber.

Bitcoin, ist auf 21 Mio Coins begrenzt..und nicht wie Fiat-Geld unbegrenzt vermehrbar.

Gold/Silber müssen durch viel Energieaufwand aus der Erde geholt werden.

Weltweit fallen die Gold-Grade rasant.

Gold/Silber sind nicht durch Knopfdruck vermehrbar...wie das weltweite Fiat-Geld.

Mit über 4 Mio Unzen Resource, sitzt FML auf einem gewaltigen Schatz.

Die Chinesen, wissen dieses....deren Zentralbank kauft physisches Gold um den Yuan

teil zu decken.

Die chinesischen Manager, welche unter anderen bei FML im Management sitzen, wissen dieses.

ebenfalls.

Der "Schatz", bei FML wird eines Tages gehoben werden.

Die Chinesen um Shangdong...sind NICHT bei knapp 3 AUD$ vor Jahren bei FML eingestiegen, um

"Peanuts" einzusammeln.

Diese 3 AUD$ können sich jedoch bei einem extremen Goldpreisanstieg als "Peanuts" erweisen.

Für momentan 0,47 AUD$...ist die FML-Aktie als "Geschenk" anzusehen.

0,47 AUD$ für eine FML....das ist m.M. nach, wie Bitcoin auf 3 $

...think about it...Rumpelofen

Fakt ist:

Die Chinesen halten 49 % der Aktien.

Die Chinesen haben (so weit ich das noch in Erinnerung habe) knapp 3 AUD pro Aktie vor Jahren gezahlt.

Die Chinesen, haben FML NICHT aufgegeben.

Die Chinesen um Shangdong, werden eines Tages wieder den "alten" Aktienpreis bzw. einen weit aus höheren sehen wollen.

Wenn der F.C so negativ zu FML steht...warum hat er seine Aktien noch nicht verkauft?

Ich bin vor Jahren...als es absehbar war, das Gold weiter abstürzt....aus ALLEN Goldminern ausgestiegen.

Wer der Meinung ist, dass Gold seinen Tiefststand der letzten Jahre noch nicht gesehen hat...der

sollte sowieso aus den Minern aussteigen.

Wer glaubt, dass Gold ein unterbewertetes Asset ist...welches enormes Potential nach OBEN hat, der

sollte sich neben physichem Gold....auch unterbewertete Goldminer...bzw. Developer/Explorer ins

Depot werfen..um den kommenden Goldpreisanstieg zu hebeln.

Manch ein "Gold-Bug" sieht momentan noch die Crypto-Währungen...wie Bitcoin, Ethereum als

"Blase", welche platzen wird.

Ich sehe die Cryptos...als Vorbote eines explosiven Gold/Silber Anstieges.

Die Cryptos laufen dem Edelmetall voraus.

Die Cryptos, sitzen im gleichen Boot....wie Gold/Silber.

Bitcoin, ist auf 21 Mio Coins begrenzt..und nicht wie Fiat-Geld unbegrenzt vermehrbar.

Gold/Silber müssen durch viel Energieaufwand aus der Erde geholt werden.

Weltweit fallen die Gold-Grade rasant.

Gold/Silber sind nicht durch Knopfdruck vermehrbar...wie das weltweite Fiat-Geld.

Mit über 4 Mio Unzen Resource, sitzt FML auf einem gewaltigen Schatz.

Die Chinesen, wissen dieses....deren Zentralbank kauft physisches Gold um den Yuan

teil zu decken.

Die chinesischen Manager, welche unter anderen bei FML im Management sitzen, wissen dieses.

ebenfalls.

Der "Schatz", bei FML wird eines Tages gehoben werden.

Die Chinesen um Shangdong...sind NICHT bei knapp 3 AUD$ vor Jahren bei FML eingestiegen, um

"Peanuts" einzusammeln.

Diese 3 AUD$ können sich jedoch bei einem extremen Goldpreisanstieg als "Peanuts" erweisen.

Für momentan 0,47 AUD$...ist die FML-Aktie als "Geschenk" anzusehen.

0,47 AUD$ für eine FML....das ist m.M. nach, wie Bitcoin auf 3 $

...think about it...Rumpelofen

Trading Spotlight

wie ich weiß

habe ich einen split mitgemacht....sollte focus in der nähe von barrik liegen..und da liegt auch noch eloro...und sich zusammenschließen..könnten die eine weltparty machen Focus Minerals (FML) - (III) die Laverton-Anlage ist Buchwert-Schrott on C+M

Zunächst:(a) FML ist angemessen bewertet, keineswegs vollkommen unterbewertet

(b) man macht keinen Fehler, wann man die Resourcen und die Verarbeitungsanlage von Laverton komplett zu Null ansetzt, und erst dann versucht FML realistisch zu bewerten (Reserven gibt es noch nicht, sollen aber noch kommen -> da gibt's hier bei W : O einen Beitrag zur "Reserves"-Mentalität in AUS...)

(b1) dabei nicht vergessen die laufenden Kosten von Laverton (wie z.B. C+M) bei der Gesamtbewertung von FML zu berücksichtigen (siehe Jahresbericht 2016)

(Wenn ich nett gefragt werde, probier ich das noch mit den Reourcen, aber nicht hier blöd von der Seite; macht nämlich viel Arbeit.)

Die Realität ist mitunter hart; FML zeigt das sehr deutlich.

__

Ansonsten:

Wer seit 2013-11 auf einen Interim-CEO angewiesen ist, der lässt eine "Lame Duck" an den Schalthebeln, und für alle gut sichtbar. (Als Australier würde ich aber auch ungefragt das chin. Geld ausgeben; macht doch viel mehr Spass als eigenes.)

Schlimmer noch: Interim-CEO Wanghong Yang muss/sollte dann entscheiden, was nach der PFS (Preliminary Feasibility Study, Ende Juni?) bei Coolgardie passieren soll. Der gute Mann hat in seinem ganzen Berufsleben wahrscheinlich noch nicht einmal einen Schraubzieher in der Hand gehabt, um damit für seine Arbeitgeber Geld zu verdienen (plakativ und spekulativ um's mal ganz deutlich zu sagen.)

Mit der PFS wird hier über die Zukunft entschieden, an die dann der potentielle Nachfolger zunächst gebunden ist (iSv Verträgen etc.) => high risk

__

Nicht umsonst ist die Barnicoat processing facility *) (so heisst die Goldmühle bei den Laverton operations) seit 2008 *) bis heute eingemottet. Nicht mal ein Refurbishment 2008 hat da noch geholfen (bei steigenden Goldpreisen wohlgemerkt).

Ich nehme nach über 4 Jahren in C+M auch an, dass die Verarb.-Anlage insgesamt auch prozesstechnisch als "Schrott" bezeichnet werden kann. Solche Art von Übernahmen woanders in Australien zeigen wie schwierig "Brownfield" in diesem Bereich ist. Man kann das hinbekommen, aber oft nur zu sehr hohen Kosten. Die Positivbeispiele sagen nichts über die Gesamtstatistik aus - wie immer eigentlich.

Daher verlängerte es ja das Leben von Crescent Gold (CRE), dass sie das Laverton Erz rüber zur Granny Smith Mill (GSM) von Barrick Gold (ABX) karren durften. Seit 2013 im Übrigen Gold Fields der Hausherr bei GSM.

Da hatten sie Glück; wahrscheinlich half, dass der damalige CRE-CFO Mark Tory mal bei Barrick Gold, damals noch Homestake Gold, zuvor gearbeitet hatte. Ob Gold Fields FML noch mal zu akzeptablen Kosten ranlässt?

Das sind nur 20km Entfernung (von Laverton bis GSM). Das ist nichts im Minenbereich. Andere bauen ein Förderband dafür (wenn Zuversicht in eine Lagerstätte, und nur bei Ehrlichkeit in den Annahmen natürlich).

=> starke Annahme:

in diesem Jahrzehnt geht Barnicoat nicht mehr in Betrieb (bei gleichbleibenden Rahmenbedingungen), wenn überhaupt jemals. (Man darf nicht leichtfertig übersehen, dass der AUD Goldpreis bzgl. Basis 2008 mit AUD1000 auf grob AUD1600 in 2017 gestiegen ist; also wenn das nichts hilft.)

__

Die Frage ist auch: steht Barnicoat überhaupt noch in den Büchern?

Der Jahresbericht 2016 lässt sich dazu nicht im Speziellen aus:

Current assets:

Laverton als solches wird noch mit AUD594k angegeben; Coolgardie nur mit AUD243k. (2015: C: AUD978k und L: AUD586k).

=> es sieht so aus, dass Barnicoat immer noch fahrlässigerweise in den Büchern steht. Klar kann man sagen, muss ja so sein wg.:

- FML hat in 2016 AUD579k für Laverton an C+M-Kosten aufgebracht (und AUD534k für Coolgardie). Und es gibt noch andere erhebliche laufende Kosten für Laverton, schön zusammengefasst in Capital Expenditures mit AUD2.958m (runter von AUD3.267m in 2015). Klar, sind da z.B. die Explorationskosten mit drin, die dann wiederum Assets erzeugen. Ich meine aber die ganzen Nicht-C+M-und-Nicht-Expl.-Kosten.

__

Da nutzt auch der wiederholte Hinweis auf den vermeintlich vielen Cash von FML nicht viel (2017-03-31: AUD46m Cash in Bank). FML hat eben auch eine entsprechende Cash Burn Rate von rund AUD10m p.a. (2015: ca.AUD11m, 2016Q1 - 2017Q1: ca. AUD9.9m; also 46/10 = 4.5a ist OK)

Die ist auch nicht das Problem von FML - denn (weit) bevor es zum Cash Crunch kommen sollte, wird in jedem Fall eine Kapitalerhöhung bei der mittlerweile schön reduzierten Aktienzahl (auf handliche 183m) vorgenommen.

Doch dann ist's ganz schnell vorbei mit Tenbagger - für den hoffenden Aktionär ist es somit schon ein Problem. Und noch was kommt hinzu: es wird automatisch Handlungsdruck - gerade auch bei Laverton - erzeugt. Man muss die anstehende PFS auch mal mit diesen Augen sehen. Muss die Cash burn rate reduziert werden, fällt der Aktienkurs sowieso wieder auf das Niveau von Ende 2015.

Soll man das glauben? --> Aber sicher: einfach mal aktuell die Kollegen bei Rye Patch Gold drüben fragen wie das so ist mit den Überraschungs-KE's bei vermeintlich ausreichend Cash im Goldminenbereich.

__

Es bleibt dabei:

Laverton ist eine massive Weichstelle bei Focus Minerals. Wie ein Mühlstein hängt diese Liegenschaft am Aktienkurs von FML.

(Für heute ist erst mal Schluss. Ich hab ja noch Zeit bis Ende Juni - frühestens

)

)__

*) http://www.focusminerals.com.au/our-projects/lavertongoldpro…

**) http://www.proactiveinvestors.com/companies/news/70471/barri…

Antwort auf Beitrag Nr.: 55.114.897 von rumpelofen am 09.06.17 22:35:06

Das ist nachweislich falsch.

Also "faul" bin ich nun nicht gerade, zumindest nicht lesefaul. Ein Blick in die Focus-Jahresberichte hätte genügt, und man hätte festgestellt, das Laverton unter Focus noch folgendermassen in Produktion war (und das nicht gerade wenig):

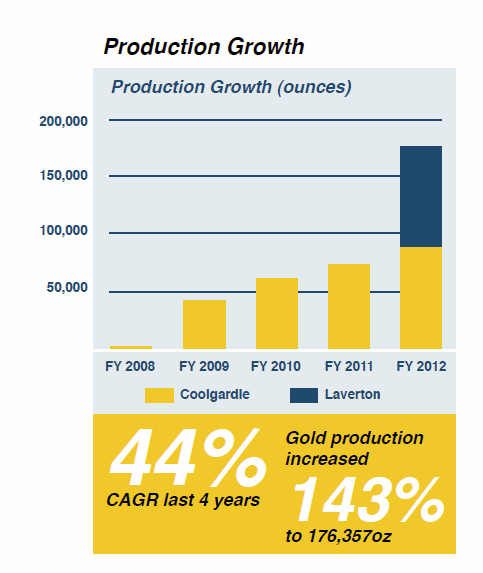

FY 2012: 86.673k oz Au, also bis 30.6.2012

FY 2013: 81.191k oz Au, also bis 30.6.2013; weniger als FY 2012, weil in C+M in 2013-04, da die Verarbeitungskosten bei Granny Smith Mill (GSM), dazu noch mehr, aus dem Ruder liefen:

Das ist aber nicht das Problem mit Laverton. Da gibt es ganz andere.

__

Jahresreporting von FML:

FY 2011-06-30

FY 2012-06-30

__- 2011-10: hier der all-scrip Takeover von Crescent Gold mit Laverton

FY 2013-06-30:

__- 2013-04: C+M von Laverton

FY 2014-06-30

__- 2013-07: C+M von Coolgardie

IFY 2014-12-31

=> Reportung-Umstellung auf Kalenderjahr:

FY 2015-12-31

FY 2016-12-31

Laverton-Betrieb unter Focus Minerals

Zitat von rumpelofen: ...

Leverton war unter Focus niemals in Produktion.

...

Das ist nachweislich falsch.

Also "faul" bin ich nun nicht gerade, zumindest nicht lesefaul. Ein Blick in die Focus-Jahresberichte hätte genügt, und man hätte festgestellt, das Laverton unter Focus noch folgendermassen in Produktion war (und das nicht gerade wenig):

FY 2012: 86.673k oz Au, also bis 30.6.2012

FY 2013: 81.191k oz Au, also bis 30.6.2013; weniger als FY 2012, weil in C+M in 2013-04, da die Verarbeitungskosten bei Granny Smith Mill (GSM), dazu noch mehr, aus dem Ruder liefen:

Das ist aber nicht das Problem mit Laverton. Da gibt es ganz andere.

__

Jahresreporting von FML:

FY 2011-06-30

FY 2012-06-30

__- 2011-10: hier der all-scrip Takeover von Crescent Gold mit Laverton

FY 2013-06-30:

__- 2013-04: C+M von Laverton

FY 2014-06-30

__- 2013-07: C+M von Coolgardie

IFY 2014-12-31

=> Reportung-Umstellung auf Kalenderjahr:

FY 2015-12-31

FY 2016-12-31

völliger unbedeutender Mumpets, was der faule code schon wieder von sich gibt.

Alleine in Kalgoorlie/Coolgardie hat Focus vor Jahren 120k Unzen p.a. produziert.Und war somit einer der grösseren australischen Goldminer.

Leverton war unter Focus niemals in Produktion.

Der Minen betrieb wurde vor Jahren eingestellt, weil der Goldpreis auf 1335 AUD gefallen war.

Da hat das sehr gute Management die Notbremse gezogen...und den Betrieb eingemottet.

Dieses war die Rettung von Focus...man hatte 70 Mio AUD Cash-Reserven (jetzt immer noch über 60 Mio )um den Minenbetrieb bei höheren Goldpreisen wieder aufnehmen zu können.

Andere Ausi-Goldminer, sind damals von der Bildfläche verschwunden...weil sie weiter gemacht haben..

das cash vollkommen verbrannt hatten...und kein neues Kapital am Markt finden konnten.

(z.B. Navigator)

Der faule Code, sollte mal dem Management DANKBAR sein, dass seine "alten Aktien" nicht vollkommen

wertlos geworden sind!

Wie man solch einen Murx, hier im Forum nur schreiben kann?

Muss dazu anmerken, dass dieser User mir ständig Mails schickt...um mir irgendwelchen Quark zu

erzählen. Der hat mich und meine Aktien auf der "watch"...meldet sich meist nur...wenn eine dieser

Aktien am Fallen ist...der sucht Aufmerksamkeit...Zweck?...mir etwas beweisen wollen?

Focus ist ein extrem unterbewerteter ex-Goldproduzent...welcher beinahe so viel Cash (mit den Bonds)

wie Market Cap hat...und über 4 Mio Unzen Goldreserven+keine Schulden....mit 2 funktionstüchtigen

Produktionsanlagen auf C+M.

Focus hat das meiste Cash auf der Bank, von allen Ausi-Explorern/Developern!

...sehr schlechtes Management...klar

Ganz klares 10-Bagger Potential!

DYOR...Rumpelofen

Focus,

Focus Minerals (FML) - (II) Laverton, die Geldvernichtungsmaschine

Jüngere Leser wissen es vielleicht nicht:Crescent Gold (CRE) hat es bis zur Übernahme durch Focus Minerals (FML)..

..bei dramatisch steigenden Goldpreisen und Barrick als Hilfe in der Nachbarschaft

..es nicht fertig gebracht Laverton überhaupt richtig zum Laufen zu bringen (von 2004 bis 2011 *) ).

(Es gab zwar ein Bump nach oben im Goldpreis in 2008/2009 in AUD, den es so in USD nicht annähernd gab, aber das führte zum deutlichen, temporären Rückgang der lokalen Kosten in AUD; auch wenn damals insgesamt im austr. Minenbereich teilweise absurd hohe Löhne gezahlt wurden im allgemeinen Rofstoffpreisrausch...)

Bei der Übernahme durch FML 2011 kamen dann alle "Super-Experten" aus ihren Löchern und laberten was von "beträchtlichen Synergien".

Faktum: die gab es bis heute nicht, und wird es aller Wahrscheinlichkeit auch so nicht geben. Im Gegenteil: das Geld "franzt" hier laufend aus zwischen Coolgardie und Laverton.

Das ist wichtig zu wissen, auch wenn Laverton (noch) keine hohe Bedeutung für FML hat.

Einfach einen Blick in den Jahresbericht 2016 (und auch 2015) werfen:

Net assets (2016):

Coolgardie / Laverton = ca. 29.512k vs 6.554k = 81.8% vs 18.2%

ABER:

Capital Expenditures (2016):

Coolgardie / Laverton = ca. 5.923k vs 2.958k = 66.7% vs 33.3%

=> 18.2% der Net Assets verschlingen 1/3 des Kapitalbedarfs. Eine leichte Unwucht.

2015 war es noch viel ärger. Man erkannte dann wohl, dass man da handeln musste.

(Ich kenne bis heute keine Aufstellung, wieviel Laverton 2017 an Kapitalkosten haben soll; ich habe allerdings auch nicht alle Publikationen zu FML 2017 gelesen. Wäre nett, wann das jemand mal recherchieren könnte.)

__

*)

1998–2006: inactive

2006-07 -- 7,400 ounces

2007-08 -- 56,195 ounces

2008-09 -- inactive

2009-10 -- 73,474 ounces (bei 1.43 g/t)

siehe: https://en.wikipedia.org/wiki/Laverton_Gold_Mine

Focus Minerals, Spekulation der Woche