Rohstoff-Explorer: Research oder Neuvorstellung (Seite 2151)

eröffnet am 13.03.08 13:14:32 von

neuester Beitrag 13.05.24 13:54:35 von

neuester Beitrag 13.05.24 13:54:35 von

Beiträge: 29.541

ID: 1.139.490

ID: 1.139.490

Aufrufe heute: 94

Gesamt: 2.701.902

Gesamt: 2.701.902

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| vor 55 Minuten | 9359 | |

| vor 1 Stunde | 5590 | |

| vor 39 Minuten | 4907 | |

| vor 1 Stunde | 2960 | |

| heute 17:14 | 2839 | |

| vor 40 Minuten | 2529 | |

| 08.05.24, 11:56 | 2071 | |

| vor 1 Stunde | 2023 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 2. | 18.722,67 | -0,27 | 154 | |||

| 2. | 8. | 10,480 | +1,35 | 92 | |||

| 3. | 3. | 158,78 | +1,48 | 71 | |||

| 4. | 1. | 0,1960 | -9,68 | 67 | |||

| 5. | 26. | 4,0335 | +49,06 | 47 | |||

| 6. | 18. | 12,384 | +49,98 | 44 | |||

| 7. | 9. | 26,54 | +63,75 | 39 | |||

| 8. | Neu! | 0,0900 | -36,17 | 38 |

Beitrag zu dieser Diskussion schreiben

Antwort auf Beitrag Nr.: 44.352.447 von IllePille am 03.04.13 11:15:59die rede war von mid-tier produzenten.

hast du andere erkenntnisse? wo liegt denn d.m.n. der break-even für fe-produzenten, und um wen handelt es sich dabei?

hast du andere erkenntnisse? wo liegt denn d.m.n. der break-even für fe-produzenten, und um wen handelt es sich dabei?

Antwort auf Beitrag Nr.: 44.352.615 von Stefan0310 am 03.04.13 11:35:38Ein Blick auf die GS Analysen der letzten Jahre reicht, um den Gehalt dieser Zahlen zu deuten.

Ob wir in 2015 einen Durchschnittspreis von 80$/t sehen oder nicht ist für GS und die anderen Brokerhäuser auch gar nicht so entscheidend. Das dient einzig der (versuchten) Beeinflussung des Marktgeschehens, sprich da ist viel Psychologie im Spiel.

80$/t im Jahresschnitt kann bedeuten, dass man sogar Preise von 50$-60$/t erwartet. Spätestens dann sollte man sich nicht nur Gedanken um den Eisenerzpreis und die Erzproduzenten machen, sondern um viel weitreichendere Dinge.

Und wie man in den nächsten Jahren entscheidend an der Kostenschraube drehen kann? In meinen Augen gibt es da kaum Spielraum.

Die Ressourcen liegen gerade in Zukunft nun mal nicht mehr in Hafennähe, sondern in Gebieten ohne bzw. ohne nennenswerter Infrastruktur. Hinzu kommen immer strengere Umweltauflagen und höhere Steuerabgaben. Die Produzenten haben zudem endliche Ressourcen, sprich sie haben langfristig ebenfalls mit den o.g. höheren Kosten zu rechnen.

Den größten Faktor stellen aber sicherlich die weiter steigenden Energiekosten dar, die sich über Produktion und Transport bis hin zur letzten Schraube bemerkbar machen.

Ob wir in 2015 einen Durchschnittspreis von 80$/t sehen oder nicht ist für GS und die anderen Brokerhäuser auch gar nicht so entscheidend. Das dient einzig der (versuchten) Beeinflussung des Marktgeschehens, sprich da ist viel Psychologie im Spiel.

80$/t im Jahresschnitt kann bedeuten, dass man sogar Preise von 50$-60$/t erwartet. Spätestens dann sollte man sich nicht nur Gedanken um den Eisenerzpreis und die Erzproduzenten machen, sondern um viel weitreichendere Dinge.

Und wie man in den nächsten Jahren entscheidend an der Kostenschraube drehen kann? In meinen Augen gibt es da kaum Spielraum.

Die Ressourcen liegen gerade in Zukunft nun mal nicht mehr in Hafennähe, sondern in Gebieten ohne bzw. ohne nennenswerter Infrastruktur. Hinzu kommen immer strengere Umweltauflagen und höhere Steuerabgaben. Die Produzenten haben zudem endliche Ressourcen, sprich sie haben langfristig ebenfalls mit den o.g. höheren Kosten zu rechnen.

Den größten Faktor stellen aber sicherlich die weiter steigenden Energiekosten dar, die sich über Produktion und Transport bis hin zur letzten Schraube bemerkbar machen.

Naja, man kann von Goldman Sachs halten was man will. Für mich sind das die größten Verbrecher überhaupt, da sind selbst Putin und Assad Waisenknaben dagegen. Es gibt durchaus auch positivere Einschätzungen zum Fe-Sektor:

http://www.carbonpositive.net/media-centre/industry-updates/…

http://online.wsj.com/article/SB1000142412788732468510457838…

Stefan

http://www.carbonpositive.net/media-centre/industry-updates/…

http://online.wsj.com/article/SB1000142412788732468510457838…

Stefan

Das break-even liegt nach meiner Berechnung bei durchschnittlich 130 $/t auf Vollkosten-Basis. Unter 130 sind keine Gewinne möglich, es sei denn die Produzenten drehen an der Kostenschraube.

für wen soll das gelten? Ich kenne einige Fe-Produzenten, aber mir ist keiner bekannt, der bei diesem Preisszenario keine Gewinne erzielen würde.

Im Übrigen gilt es zu unterscheiden zwischen Cahsflow- und Ergebnisrechnung. Hier liegt dein Denkfehler. Innerhalb der CF-Betrachtung gilt es zudem zu unterscheiden zwischen CAPEX für neue Minen (z.B. Atlas Iron) und sustaining capital costs. Sonst wird´s endgültig eine Milchmädchenrechnung.

für wen soll das gelten? Ich kenne einige Fe-Produzenten, aber mir ist keiner bekannt, der bei diesem Preisszenario keine Gewinne erzielen würde.

Im Übrigen gilt es zu unterscheiden zwischen Cahsflow- und Ergebnisrechnung. Hier liegt dein Denkfehler. Innerhalb der CF-Betrachtung gilt es zudem zu unterscheiden zwischen CAPEX für neue Minen (z.B. Atlas Iron) und sustaining capital costs. Sonst wird´s endgültig eine Milchmädchenrechnung.

Eisenerz

Die "Goldmänner" hatten Ende März den Fe-Sektor abgestuft und speziell mittelgroße Produzenten heruntergestuft.

Kursziele nach unten revidiert:

Atlas Iron um 23% runter auf A$ 1,15

Mt. Gibson um 14% runter auf A$ 0,60

GS prognostiziert folgende Durchschnittspreise für 62% Eisenerz je Tonne:

2013: $ 139,-

2014: $ 115,-

2015: $ 80,-

Das break-even liegt nach meiner Berechnung bei durchschnittlich 130 $/t auf Vollkosten-Basis. Unter 130 sind keine Gewinne möglich, es sei denn die Produzenten drehen an der Kostenschraube.

Der Fe-Preis steht bei 136 $/t - also knapp über der kritischen 130 $-Marke:

spot price chart:

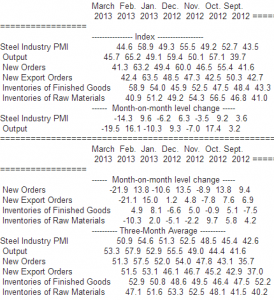

Einkaufsmanager-Index

Der PMI für den chin. Stahlsektor ist unter die "50" auf 44,6 gefallen, womit eine negative Erwartung ausgedrückt wird:

Fazit:

Momentan sieht es nicht rosig aus für den Fe-Sektor. Mid-tier Produzenten, wie Atlas, Northern, Grange und kleine Produz. wie Bellzone oder Northland sollte man m.M.n. zurzeit meiden! Es wird schwer, damit Geld zu verdienen. Maßgebend ist die Entwicklung des Fe-Preises!

MARKETS SPECTATOR: Goldman delivers an iron fist

Ben Potter 26 Mar, 10:59 AM

Goldman Sachs recently lowered its iron ore price forecasts for calendar years 2013-15 as it sees a period of oversupply arriving sooner than initially predicted. For each year, it cut its forecasts by 3 per cent, 11 per cent, and 9 per cent to $US139 per tonne, $US115/t, and $US80/t, respectively.

The key drivers of this downgrade were:

1) The increasing scrap usage within China.

2) Chinese iron ore production to surprise on the upside.

3) Lower total steel production.

This results in a market surplus from 2014 onwards, which Goldman believes will weigh on prices and, in particular, the mid-cap iron ore miners.

Consequently, it has downgraded the earnings for mid-tier producers given they operate at much tighter margins than the big producers; and as such the iron ore price downgrades have had a much bigger impact on future earnings.

“We have downgraded fiscal years 2013, 2014 and 2015 by -16 per cent, -33 per cent and -145 per cent for Atlas Iron, and -5 per cent, -12 per cent and -114 per cent for Mount Gibson Iron Ore," the broker said in a note to clients. "While the mid-term outlook (fiscal years 2015-16) appears particularly grim based on a straight pass through of these new commodity forecasts, we highlight that these companies, one, are highly sensitive to small commodity and currency changes, and outcomes could be vastly different from those forecast; two, are cash flow positive at our long term forecasts and at present have sufficient liquidity to withstand sustained dips in pricing; and three, are likely to take more decisive action if such dips occur."

Nonetheless, the above downgrades have not had an effect on the stocks’ neutral ratings as the broker believes current prices appropriately reflect the near term earnings. However, target prices have been ratcheted down by 23 per cent to $1.15 for Atlas Iron and 14 per cent to $0.60 for Mount Gibson Iron Ore.

Chart Atlas Iron:

Chart Grange Res:

Chart Fortescus Metals:

Chart Bellzone:

Die "Goldmänner" hatten Ende März den Fe-Sektor abgestuft und speziell mittelgroße Produzenten heruntergestuft.

Kursziele nach unten revidiert:

Atlas Iron um 23% runter auf A$ 1,15

Mt. Gibson um 14% runter auf A$ 0,60

GS prognostiziert folgende Durchschnittspreise für 62% Eisenerz je Tonne:

2013: $ 139,-

2014: $ 115,-

2015: $ 80,-

Das break-even liegt nach meiner Berechnung bei durchschnittlich 130 $/t auf Vollkosten-Basis. Unter 130 sind keine Gewinne möglich, es sei denn die Produzenten drehen an der Kostenschraube.

Der Fe-Preis steht bei 136 $/t - also knapp über der kritischen 130 $-Marke:

spot price chart:

Einkaufsmanager-Index

Der PMI für den chin. Stahlsektor ist unter die "50" auf 44,6 gefallen, womit eine negative Erwartung ausgedrückt wird:

Fazit:

Momentan sieht es nicht rosig aus für den Fe-Sektor. Mid-tier Produzenten, wie Atlas, Northern, Grange und kleine Produz. wie Bellzone oder Northland sollte man m.M.n. zurzeit meiden! Es wird schwer, damit Geld zu verdienen. Maßgebend ist die Entwicklung des Fe-Preises!

MARKETS SPECTATOR: Goldman delivers an iron fist

Ben Potter 26 Mar, 10:59 AM

Goldman Sachs recently lowered its iron ore price forecasts for calendar years 2013-15 as it sees a period of oversupply arriving sooner than initially predicted. For each year, it cut its forecasts by 3 per cent, 11 per cent, and 9 per cent to $US139 per tonne, $US115/t, and $US80/t, respectively.

The key drivers of this downgrade were:

1) The increasing scrap usage within China.

2) Chinese iron ore production to surprise on the upside.

3) Lower total steel production.

This results in a market surplus from 2014 onwards, which Goldman believes will weigh on prices and, in particular, the mid-cap iron ore miners.

Consequently, it has downgraded the earnings for mid-tier producers given they operate at much tighter margins than the big producers; and as such the iron ore price downgrades have had a much bigger impact on future earnings.

“We have downgraded fiscal years 2013, 2014 and 2015 by -16 per cent, -33 per cent and -145 per cent for Atlas Iron, and -5 per cent, -12 per cent and -114 per cent for Mount Gibson Iron Ore," the broker said in a note to clients. "While the mid-term outlook (fiscal years 2015-16) appears particularly grim based on a straight pass through of these new commodity forecasts, we highlight that these companies, one, are highly sensitive to small commodity and currency changes, and outcomes could be vastly different from those forecast; two, are cash flow positive at our long term forecasts and at present have sufficient liquidity to withstand sustained dips in pricing; and three, are likely to take more decisive action if such dips occur."

Nonetheless, the above downgrades have not had an effect on the stocks’ neutral ratings as the broker believes current prices appropriately reflect the near term earnings. However, target prices have been ratcheted down by 23 per cent to $1.15 for Atlas Iron and 14 per cent to $0.60 for Mount Gibson Iron Ore.

Chart Atlas Iron:

Chart Grange Res:

Chart Fortescus Metals:

Chart Bellzone:

Trading Spotlight

Zitat von Fantomas96: Insider buying of gold stocks surges to multi-year highs

“Such extreme situations usually do not last for long,” notes Mr. Dixon. “With both fundamental and technical conditions supporting recent heavy insider buying, it looks like a significant bottom in precious metals mining shares may be in the process of forming now.”

GOLD/Aktien

Meist sind die gestiegenen Insiderkäufe dem Tief ein paar Monate voraus. Ich gehe davon aus, dass wir das Jahrestief bei Gold noch nicht gesehen haben. Ich rechne damit, dass wir noch Preise in Richtung $1.500 sehen werden. Bis etwa zur Jahresmitte. Von dort an rechne ich wieder mit steigenden Notierungen, auch für Goldaktien.

Antwort auf Beitrag Nr.: 44.342.313 von tommy-hl am 02.04.13 08:20:39An Update on the Silver Stocks

http://thedailygold.com/an-update-on-the-silver-stocks/

When we discuss gold stocks we often refer to gold and silver stocks. Today we take a look at the silver stocks specifically.

Below is a chart of our partially weighted producers index which contains 14 of the largest silver producers. We didn’t cherry pick the 14. We went down the list and that includes a handful of companies which have really struggled in recent years. Anyway, the 56% in the current cyclical bear is well in line with history. Previous downturns have been 51% and 49% and then 85% from 2007-2008.

Only time will tell but there is a chance that this evolving spring bottom could be the right side of a major long-term double bottom. Keep an eye on the trendline above. A break above that and the multi-year outlook becomes all the more bullish given the lack of overhead resistance.

Zooming in (see below) we find that the market is holding slightly above its 2012 double bottom. The silver stocks put in a strong bullish reversal with volume four weeks ago. The market has yet to confirm the bottom but it could if it closes next week or the following week at five or six week high. Once that happens, the downtrend line becomes the next important resistance.

The silver stock ETF, SIL has also failed to close below the 2012 double bottom. It closed at $18.15 and faces key resistance at both $19 and $20.

There are a few other observations to note. First, note that SIL is showing relative strength against Silver. For whatever reason, the silver stocks in comparison to the gold stocks have fared better. The gold stocks (GDX, HUI) have broken below their 2012 lows while the silver stocks have not. Also, note the average volume in SIL. The 20-day average volume is roughly 100K shares. At its peak two years ago it was about 1.5 Million shares. That is 15 times higher!

Relative to gold stocks we were super bullish on silver stocks in 2010 but less so in 2011 and 2012. Gold leads Silver but once Gold finds its stride Silver heats up. If the precious metals bull market has another leg higher in it then we’ll move to an overweight position in the silver stocks at somepoint. The silver stocks as a group haven’t experienced a sustained breakout to new highs since 2007. If Silver is to advance to $40, $50 and beyond then that has incredibly bullish implications for the chart of our Silver Producers Index. The silver producers could be poised for leadership and incredible performance in 2014 and 2015. If you’d be interested in professional guidance in uncovering the producers and explorers poised for big gains in the next few years then we invite you to learn more about our service.

Good Luck!

Jordan Roy-Byrne, CMT

Jordan@TheDailyGold.com

http://thedailygold.com/an-update-on-the-silver-stocks/

When we discuss gold stocks we often refer to gold and silver stocks. Today we take a look at the silver stocks specifically.

Below is a chart of our partially weighted producers index which contains 14 of the largest silver producers. We didn’t cherry pick the 14. We went down the list and that includes a handful of companies which have really struggled in recent years. Anyway, the 56% in the current cyclical bear is well in line with history. Previous downturns have been 51% and 49% and then 85% from 2007-2008.

Only time will tell but there is a chance that this evolving spring bottom could be the right side of a major long-term double bottom. Keep an eye on the trendline above. A break above that and the multi-year outlook becomes all the more bullish given the lack of overhead resistance.

Zooming in (see below) we find that the market is holding slightly above its 2012 double bottom. The silver stocks put in a strong bullish reversal with volume four weeks ago. The market has yet to confirm the bottom but it could if it closes next week or the following week at five or six week high. Once that happens, the downtrend line becomes the next important resistance.

The silver stock ETF, SIL has also failed to close below the 2012 double bottom. It closed at $18.15 and faces key resistance at both $19 and $20.

There are a few other observations to note. First, note that SIL is showing relative strength against Silver. For whatever reason, the silver stocks in comparison to the gold stocks have fared better. The gold stocks (GDX, HUI) have broken below their 2012 lows while the silver stocks have not. Also, note the average volume in SIL. The 20-day average volume is roughly 100K shares. At its peak two years ago it was about 1.5 Million shares. That is 15 times higher!

Relative to gold stocks we were super bullish on silver stocks in 2010 but less so in 2011 and 2012. Gold leads Silver but once Gold finds its stride Silver heats up. If the precious metals bull market has another leg higher in it then we’ll move to an overweight position in the silver stocks at somepoint. The silver stocks as a group haven’t experienced a sustained breakout to new highs since 2007. If Silver is to advance to $40, $50 and beyond then that has incredibly bullish implications for the chart of our Silver Producers Index. The silver producers could be poised for leadership and incredible performance in 2014 and 2015. If you’d be interested in professional guidance in uncovering the producers and explorers poised for big gains in the next few years then we invite you to learn more about our service.

Good Luck!

Jordan Roy-Byrne, CMT

Jordan@TheDailyGold.com

Antwort auf Beitrag Nr.: 44.342.313 von tommy-hl am 02.04.13 08:20:39Insider buying of gold stocks surges to multi-year highs

http://www.theglobeandmail.com/globe-investor/inside-the-mar…

The TSX global gold index has lost about a third of its value over the past two years. The S&P/TSX Venture Exchange, stock full of gold mining juniors, hit a multi-year low this month.

Yet, executives and officers who work within those businesses are showing remarkable confidence that the sector is poised for better times.

According to INK Research, there are now seven precious metals stocks on the TSX with insider buying for every one with selling. That’s a near doubling of the ratio since mid-January – and represents a level of lopsided transactions that is usually only seen during major market peaks or valleys.

“That is the type of insider buying we saw in the broad market during the height of the great financial crisis in late 2008 and early 2009,” points out Ted Dixon, CEO of INK Research. “A similar situation now seems to be in place among gold and silver miners.”

Insiders are typically contrarian investors – buying shares when they perceive them to be undervalued. Right now, it appears many think the stocks are going for fire-sale prices.

They are usually early, too. Historically, insider transactions often foreshadow market moves six- to 36-months in advance.

While that may be quite a wait, it’s interesting to see insiders display this level of confidence in a sector that the broader investment community has been fleeing.

Mr. Dixon points out that while gold is well off highs near $1,900 (U.S.) an ounce in 2011, the macro backdrop hasn’t radically changed. Central banks are working hard to keep real interest rates in negative territory, and the threat that bond-buying measures will eventually lead to inflation – gold’s best friend – remains intact.

There are no shortages of forecasts calling for gold’s demise, or at least losing some of its lustre. Last week, for instance, Société Générale predicted gold would pull back to below $1,400 (U.S.) an ounce by the end of this year as the U.S. economy improves and the need for quantitative easing is scaled back.

But there are plenty of others that are more optimistic. John Hathaway, manager of the $1.8-billion Tocqueville Gold Fund, who has one of the best long-term track records in the sector, thinks gold could easily vault 25 per cent from current levels to $2,000 an ounce. The recent events in Cyprus have highlighted the continued risks to the global economy arising from the European debt crisis, and gold could continue to benefit from haven flows into hard assets.

While gold stocks have significantly underperformed the bullion market recently for various reasons, including rising production costs, Mr. Dixon thinks miners have a lot of emerging factors working in their favour.

Several CEOs have recently been fired for investing in projects that ultimately hurt shareholder value, suggesting they'll be more prudent going forward. And technicals suggest gold stocks are cheap in relation to gold; last week, the NYSE Arch Gold Bugs index, made up of U.S.-listed gold companies, hit the lowest levels versus the SPDR Gold ETF – an investment in physical metal – since the Lehman Brothers collapse.

“Such extreme situations usually do not last for long,” notes Mr. Dixon. “With both fundamental and technical conditions supporting recent heavy insider buying, it looks like a significant bottom in precious metals mining shares may be in the process of forming now.”

FANTOMAS

http://www.theglobeandmail.com/globe-investor/inside-the-mar…

The TSX global gold index has lost about a third of its value over the past two years. The S&P/TSX Venture Exchange, stock full of gold mining juniors, hit a multi-year low this month.

Yet, executives and officers who work within those businesses are showing remarkable confidence that the sector is poised for better times.

According to INK Research, there are now seven precious metals stocks on the TSX with insider buying for every one with selling. That’s a near doubling of the ratio since mid-January – and represents a level of lopsided transactions that is usually only seen during major market peaks or valleys.

“That is the type of insider buying we saw in the broad market during the height of the great financial crisis in late 2008 and early 2009,” points out Ted Dixon, CEO of INK Research. “A similar situation now seems to be in place among gold and silver miners.”

Insiders are typically contrarian investors – buying shares when they perceive them to be undervalued. Right now, it appears many think the stocks are going for fire-sale prices.

They are usually early, too. Historically, insider transactions often foreshadow market moves six- to 36-months in advance.

While that may be quite a wait, it’s interesting to see insiders display this level of confidence in a sector that the broader investment community has been fleeing.

Mr. Dixon points out that while gold is well off highs near $1,900 (U.S.) an ounce in 2011, the macro backdrop hasn’t radically changed. Central banks are working hard to keep real interest rates in negative territory, and the threat that bond-buying measures will eventually lead to inflation – gold’s best friend – remains intact.

There are no shortages of forecasts calling for gold’s demise, or at least losing some of its lustre. Last week, for instance, Société Générale predicted gold would pull back to below $1,400 (U.S.) an ounce by the end of this year as the U.S. economy improves and the need for quantitative easing is scaled back.

But there are plenty of others that are more optimistic. John Hathaway, manager of the $1.8-billion Tocqueville Gold Fund, who has one of the best long-term track records in the sector, thinks gold could easily vault 25 per cent from current levels to $2,000 an ounce. The recent events in Cyprus have highlighted the continued risks to the global economy arising from the European debt crisis, and gold could continue to benefit from haven flows into hard assets.

While gold stocks have significantly underperformed the bullion market recently for various reasons, including rising production costs, Mr. Dixon thinks miners have a lot of emerging factors working in their favour.

Several CEOs have recently been fired for investing in projects that ultimately hurt shareholder value, suggesting they'll be more prudent going forward. And technicals suggest gold stocks are cheap in relation to gold; last week, the NYSE Arch Gold Bugs index, made up of U.S.-listed gold companies, hit the lowest levels versus the SPDR Gold ETF – an investment in physical metal – since the Lehman Brothers collapse.

“Such extreme situations usually do not last for long,” notes Mr. Dixon. “With both fundamental and technical conditions supporting recent heavy insider buying, it looks like a significant bottom in precious metals mining shares may be in the process of forming now.”

FANTOMAS

Zitat von tpnl: Hallo tommy-hl,

habe nun seit längerem nichts mehr von dir gelesen (gefühlt seit drei-vier Wochen). Auch ein Wettbüroupdate wäre sehr interessant. Welche Aktien zeigen ein erstes Aufbäumen gegen den Abwärtstrend...?

Ich hoffe sehr, dir geht es gut, du genießt irgendwo einen ausgedehnten Urlaub und lässt Börse Börse sein.

Mit den besten Wünschen

tpnl

Hallo tpnl,

danke für die lieben Wünsche. Ich hatte beruflich viel um die Ohren, war viel unterwegs und hatte zuletzt eine Woche Urlaub (muss auch mal sein und die Familie darf auch nicht vernachlässigt werden). Somit hatte ich keine Zeit, bei w-o aktiv zu sein.

Ich hatte in der Zwischenzeit aber Gelegenheit ein bisschen zu recherchieren, um neue Anregungen zu bekommen. So konnte ich z. B. die Vision/Strategie des CEO von XBR erfahren. Für diejenigen, die in XBR investiert sind: Wir stehen erst an Anfang einer großartigen Entwicklung. Mein Eindruck ist, dass hier noch sehr viel kommen wird, was geduldigen Anlegern mit einem mittleren bis langfristigen Zeithorizont außerordentliche Gewinne bescheren wird.

Des weiteren konnte ich für einen Rohstoff Erkenntnisse erlangen, der hier m. W. noch nicht besprochen worden ist. Es geht darum die zeitweiligen Überkapazitäten von Erneuerbaren Energien zu "lagern" und dann zu nutzen, wenn die Erneuerbaren Energien keine oder zu geringe Leistung abgeben (z. B. bei Windstille oder wenn die Sonne nicht scheint). Läuft unter "P2G".

Jedenfalls muss ich mich bei div. Aktien/Rohstoffen erst mal einlesen.

Diverse Eisenerz-Aktien wurden "geschlachtet". Bin bei Atlas Iron kurz über meinem Kaufpreis ausgestoppt worden. Bei Bellzone und Rogue Iron gab es wahre Blutbäder ... Ich meine mich noch zu erinnern darauf hingewiesen zu haben, bei BZM auf die 17p zu achten und bei Unterschreiten auszusteigen. War wohl keine schlechte Idee ...

Ansonsten scheint die Stimmung bei Rohstoff/Aktien ziemlich düster zu sein. Vielleicht ein Kontraindikator?

Guten Morgen,

das überfällige Update fürs Wettbüro:

das überfällige Update fürs Wettbüro: