Outokumpu - jetzt kommt der Turnaround (Seite 3)

eröffnet am 26.10.11 13:49:30 von

neuester Beitrag 15.12.23 20:24:33 von

neuester Beitrag 15.12.23 20:24:33 von

Beiträge: 136

ID: 1.169.891

ID: 1.169.891

Aufrufe heute: 0

Gesamt: 29.867

Gesamt: 29.867

Aktive User: 0

ISIN: FI0009002422 · WKN: 885421 · Symbol: OUTA

3,7930

EUR

+0,08 %

+0,0030 EUR

Letzter Kurs 08:00:15 Tradegate

Neuigkeiten

04.04.24 · wallstreetONLINE Redaktion |

03.04.24 · BörsenNEWS.de |

28.03.24 · BörsenNEWS.de |

07.11.23 · dpa-AFX |

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 2,5950 | +15,33 | |

| 0,8947 | +11,85 | |

| 205,00 | +10,81 | |

| 1,5750 | +10,68 | |

| 0,9495 | +8,83 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 183,20 | -19,30 | |

| 0,7500 | -21,05 | |

| 1,1367 | -22,67 | |

| 12,000 | -25,00 | |

| 8,3600 | -39,81 |

Beitrag zu dieser Diskussion schreiben

Antwort auf Beitrag Nr.: 57.698.346 von faultcode am 04.05.18 20:21:04

https://globenewswire.com/news-release/2018/07/24/1541023/0/…

=>

Highlights in the second quarter of 2018

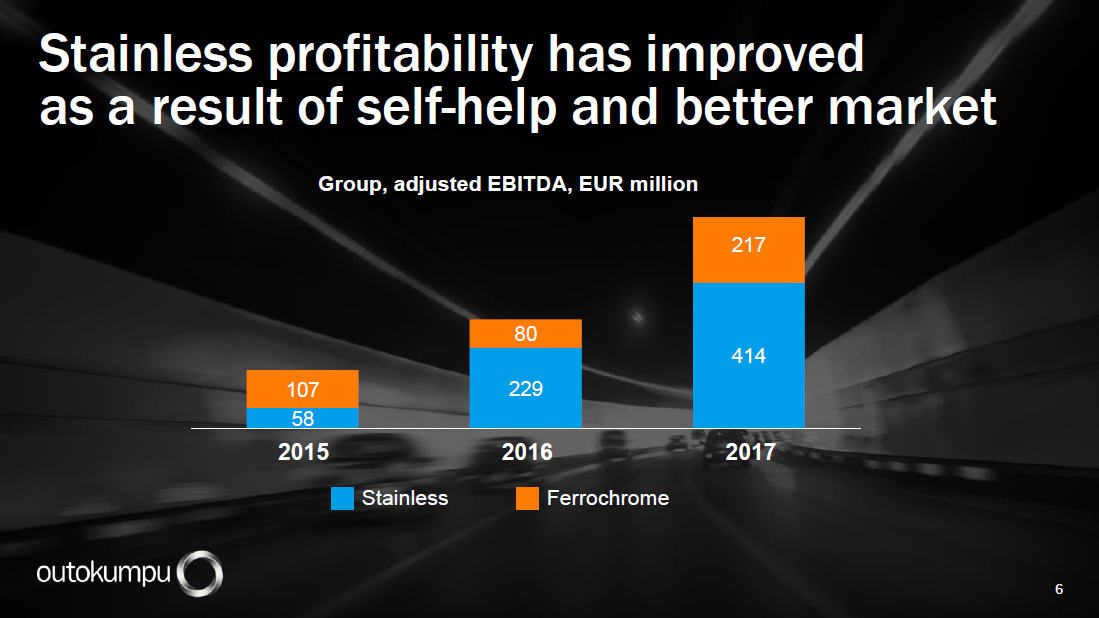

• Stainless steel deliveries were 668,000 tonnes (625,000 tonnes)1.

• Adjusted EBITDA was EUR 136 million (EUR 199 million).

• EBITDA was EUR 136 million (EUR 209 million).

• Operating cash flow was EUR 71 million (EUR 150 million).

• Net debt increased to EUR 1,211 million (March 31, 2018: EUR 1,086 million).

• Gearing was 45.1% (March 31, 2018: 40.9%).

• Return on capital employed (ROCE) was 5.5% (March 31, 2018: 7.2%).

Highlights in the first half of 2018

• Stainless steel deliveries were 1,312,000 tonnes (1,264,000 tonnes).

• Adjusted EBITDA was EUR 269 million (EUR 493 million).

• EBITDA was EUR 276 million (EUR 518 million).

• Operating cash flow was EUR 110 million (EUR 97 million).

• Net result was EUR 74 million (EUR 291 million).

=> daran sieht man - trotz allem - wie da immer noch "so" gedacht wird in der Stahlindustrie (und ähnlichen Industrien):

in Volumen

nach dem alten Motto: "Alles was ich liefern kann, kann der Wettbewerb nicht mehr liefern!"

=>

...

President & CEO Roeland Baan:

“Despite market volatility and the global uncertainty created by the US steel tariffs, we maintained our market position and financial performance during the second quarter. Our adjusted EBITDA amounted to EUR 136 million supported by record-high stainless steel deliveries. Business area Americas’ result improved as expected, and business area Europe was able to maintain its good performance in a challenging market environment with unprecedented price pressure.

The impacts of the US steel tariffs implemented in early May have been two-fold:

(a) on the downside, we have witnessed surging imports to Europe resulting in heavy price pressure while in the Americas, base prices have risen throughout the spring benefiting local manufacturers including us.

(b) the provisional safeguard measures imposed by the European Commission as of July 19 are a logical reaction to restore balance in the European steel markets and stem the flow of low-priced steel imports. We expect the provisional safeguards to be commuted into permanent safeguards within the next 200 days.

We are halfway through our journey to become the best value creator in stainless steel. Despite substantial market headwinds during the past months, we delivered one of our strongest quarters in our history. This development highlights the significant progress we have made to achieve our 2020 targets.”

Outlook for Q3/2018

In line with the market, third-quarter stainless steel deliveries are expected to be seasonally lower in business area Europe and to remain stable in the Americas. Base price pressure continues in Europe but the negative impact of this is partly offset by higher base prices in the US supported by steel import tariffs.

After the successful planned maintenance shutdown of a ferrochrome furnace, Outokumpu expects to achieve normalized ferrochrome production in the third quarter.

Outokumpu expects its third-quarter adjusted EBITDA to be lower than in the second quarter (Q2/18: EUR 136 million) but significantly higher than in the third quarter of 2017 (Q3/17: EUR 56 million).

Good performance in adverse environment, Grp.adj.EBITDA @EUR136m by record-high stainless steel deliv.

July 24, 2018 at 12.00 pm EESThttps://globenewswire.com/news-release/2018/07/24/1541023/0/…

=>

Highlights in the second quarter of 2018

• Stainless steel deliveries were 668,000 tonnes (625,000 tonnes)1.

• Adjusted EBITDA was EUR 136 million (EUR 199 million).

• EBITDA was EUR 136 million (EUR 209 million).

• Operating cash flow was EUR 71 million (EUR 150 million).

• Net debt increased to EUR 1,211 million (March 31, 2018: EUR 1,086 million).

• Gearing was 45.1% (March 31, 2018: 40.9%).

• Return on capital employed (ROCE) was 5.5% (March 31, 2018: 7.2%).

Highlights in the first half of 2018

• Stainless steel deliveries were 1,312,000 tonnes (1,264,000 tonnes).

• Adjusted EBITDA was EUR 269 million (EUR 493 million).

• EBITDA was EUR 276 million (EUR 518 million).

• Operating cash flow was EUR 110 million (EUR 97 million).

• Net result was EUR 74 million (EUR 291 million).

=> daran sieht man - trotz allem - wie da immer noch "so" gedacht wird in der Stahlindustrie (und ähnlichen Industrien):

in Volumen

nach dem alten Motto: "Alles was ich liefern kann, kann der Wettbewerb nicht mehr liefern!"

=>

...

President & CEO Roeland Baan:

“Despite market volatility and the global uncertainty created by the US steel tariffs, we maintained our market position and financial performance during the second quarter. Our adjusted EBITDA amounted to EUR 136 million supported by record-high stainless steel deliveries. Business area Americas’ result improved as expected, and business area Europe was able to maintain its good performance in a challenging market environment with unprecedented price pressure.

The impacts of the US steel tariffs implemented in early May have been two-fold:

(a) on the downside, we have witnessed surging imports to Europe resulting in heavy price pressure while in the Americas, base prices have risen throughout the spring benefiting local manufacturers including us.

(b) the provisional safeguard measures imposed by the European Commission as of July 19 are a logical reaction to restore balance in the European steel markets and stem the flow of low-priced steel imports. We expect the provisional safeguards to be commuted into permanent safeguards within the next 200 days.

We are halfway through our journey to become the best value creator in stainless steel. Despite substantial market headwinds during the past months, we delivered one of our strongest quarters in our history. This development highlights the significant progress we have made to achieve our 2020 targets.”

Outlook for Q3/2018

In line with the market, third-quarter stainless steel deliveries are expected to be seasonally lower in business area Europe and to remain stable in the Americas. Base price pressure continues in Europe but the negative impact of this is partly offset by higher base prices in the US supported by steel import tariffs.

After the successful planned maintenance shutdown of a ferrochrome furnace, Outokumpu expects to achieve normalized ferrochrome production in the third quarter.

Outokumpu expects its third-quarter adjusted EBITDA to be lower than in the second quarter (Q2/18: EUR 136 million) but significantly higher than in the third quarter of 2017 (Q3/17: EUR 56 million).

2018Q1 - und U.S. tariffs

dazu aus dem 2018Q1-Bericht (26.4.2018):The US steel tariffs are expected to come into force in the beginning of May. As negotiations around the effective implementation are still underway, markets have been roiled by the uncertainty this brings.

One of the tangible effects has been an 8% increase of steel imports into Europe year on year.

Antwort auf Beitrag Nr.: 57.107.487 von faultcode am 24.02.18 00:15:17

=>

=> Div.-Rendite so um die 3.8% z.Z. (thyssenkrupp AG < 2% bis auf Weiteres )

)

warum dann der Kurs-Rückgang?

Na altes Spiel: steigt die Konjunktur im Stahl, steigen auch die Kosten:

=>

=> Div.-Rendite so um die 3.8% z.Z. (thyssenkrupp AG < 2% bis auf Weiteres

)

)

Antwort auf Beitrag Nr.: 56.171.484 von faultcode am 13.11.17 16:45:01

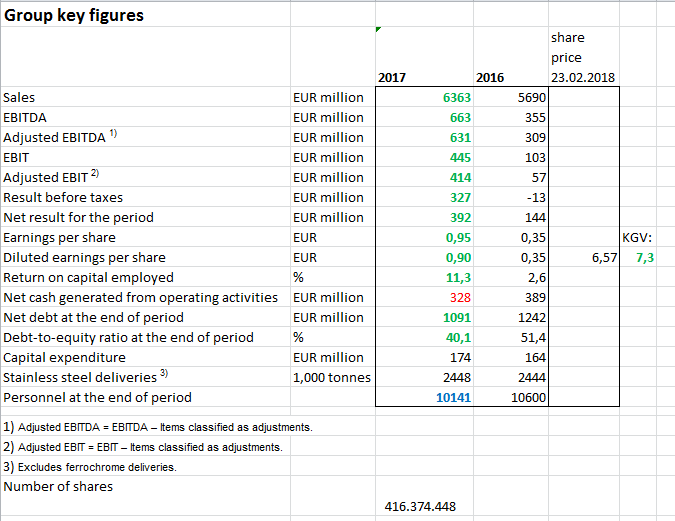

thyssenkrupp AG lt. FactSet heute: KGV 2018e 15,88

KGV 7.3

thyssenkrupp AG lt. FactSet heute: KGV 2018e 15,88

Trading Spotlight

Moody’s upgrades Outokumpu’s issuer corporate family rating to B1

..einfach mal ein Update:http://www.outokumpu.com/en/news-events/press-release/Pages/…

=>

Moody’s has upgraded Outokumpu’s issuer corporate family rating to B1 from the previous rating of B2 and probability default rating to B1-PD from the previous B2-PD. Moody’s has also upgraded the ratings for Outokumpu’s senior secured notes to Ba3 from the previous rating of B1. The outlook of all ratings is stable.

Says CFO Chris de la Camp: “We are pleased that Moody’s has noted our improved operational performance and balance sheet and has consequently upgraded our ratings. Further reduction of net debt and improving of our credit metrics remain key objectives for Outokumpu.”

Outokumpu first obtained Moody’s ratings in March 2016, which were previously upgraded in May 2017.

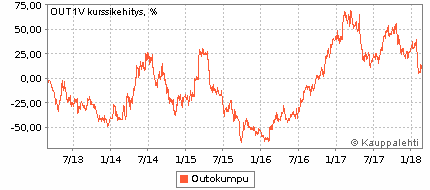

3-Jahreshoch in dieser Woche...

geht doch. Geht doch... - Glück und/oder der Finnische Staat

Ich habe immer noch seit 2012 Stücke hier (in eher bescheidenem Umfang). Seit November 2016 liege ich nun erstmals überhaupt und möglicherweise nachhaltig(?) über Wasser. (Es gibt sogar wieder Dividende nach 6 Jahren: €0.1 am 30.3.2017)Und das nur, weil ich bei der KE vom April 2014 Stücke (ohne Überbezug in meinem Fall) zu €0.08 bezog, also zu €2.0 nach dem 25:1 Reverse Split vom Juni 2014.

Allerdings konnte man Ende 2015 bis Frühjahr 2016 - an ausgewählten Tagen! - auch Stücke für um die €2.0 bekommen. Ich tat einfach gar nichts seit der KE.

Ehrlicherweise muss man auch den Aktionären von Thyssen danken für die freundliche Rücknahme der Inoxum 2013/14 (oder was davon noch übrig blieb).

Dass das im Stahlbereich auch voll daneben gehen kann, hat mir die Australische Arrium (vormals One Steel) gezeigt, die seit letztem Jahr von extrem gewieften Insolvenzverwaltern filetiert wird und diese Einzelstücke nun in der derzeitigen Stahlkonjunktur (ausserhalb Chinas) zu Bestpreisen verhökern kann.

Ich behalte Outokumpu einfach weiter aus drei Gründen:

(a) mein Arrium-Disaster (welches sich schlagartig innerhalb weniger Wochen 2015 von rettbar zu kein Geld mehr da vollzog...) muss irgendwie kompensiert werden ("fight fire with fire")

(b) der seit 2016 begonnene und ernsthafte Kapazitätsabbau in China

(c) die rigorosen Zölle in den USA (siehe US Steel-Erholung nach einer fulminanten Achterbahnfahrt), die der (Rest-)EU als mögliches, weiteres Feigenblatt dienen könnte (die EU fing ja damit an...) mit den Strafzöllen einfach weiterzumachen, auch im Hinblick auf alle möglichen Populisten in der EU...

Ich habe hier keine langfristige Exit-Strategie ausser Halten (die Positionsgrösse und das Money Management sollte bei sowas auch eine angemessene Rolle spielen...); die "neue" OUT ist mit der alten irgendwie nicht so gut vergleichbar; das ist nun alles "unbekanntes Terrain".

Hier weitere Hintergründe vom Februar:

https://www.ft.com/content/7494dfd8-f768-11e6-9516-2d969e0d3…

Antwort auf Beitrag Nr.: 52.016.549 von E.S.T. am 19.03.16 09:50:11

e.s.t.

Aktienkurs in Kürze bei 6 € ?

....dieser volatile Wert, der offensichtlich von den Zollbeschränkungen mit angeschoben wird, ist mittlerweile mit seinem Aktienkurs über den 5 € und sieht gegenüber dem letzten Tiefstand praktisch eine Verdopplung.e.s.t.

Eigenkapital > 5 € / Aktie

Nach dem Geschäftsbericht 2015 ist das Eigenkapital von Outo merklich über 5 € !!e.s.t.

04.04.24 · wallstreetONLINE Redaktion · GRENKE |

03.04.24 · BörsenNEWS.de · GRENKE |

28.03.24 · BörsenNEWS.de · Telefon L.M.Ericsson (B) |

07.11.23 · dpa-AFX · Outokumpu |