Cardero Resource Corp. (CDU) - It’s not only ore, it’s much more: Zahlen, Daten, Fakten und Diskussi - 500 Beiträge pro Seite (Seite 4)

eröffnet am 15.05.11 12:28:41 von

neuester Beitrag 31.03.22 17:25:22 von

neuester Beitrag 31.03.22 17:25:22 von

Beiträge: 4.628

ID: 1.166.193

ID: 1.166.193

Aufrufe heute: 0

Gesamt: 658.870

Gesamt: 658.870

Aktive User: 0

ISIN: CA14140U2048 · WKN: A142XA

0,1600

CAD

0,00 %

0,0000 CAD

Letzter Kurs 26.01.22 TSX Venture

Korrekur:

Ein Glück das das die Projekte von CDU in stabilen Länder sind... (na ja... über Peru lässt sich streiten... aber das wurde hier ja schon des öfters diskutiert.)

Zitat von Ahorne: Schlaues Vietnam sich Indien mit ins Boot zu holen... wenn sich zwei streiten China und Indien freut sich der Dritte. Wurde auch Zeit, dass Indien ins Geschehen Eingreifft und nicht alles dem Drachen überlässt.

ps. Indien unterhält enge militärische Zusammarbeit mit den USA. Also hat eine gewisse Feuerkraft, militärisch gesprochen.

Es ist nur gut und recht; dass kleinere Länder wie z.b Vietnam sich auf die Hinterbeine stellen und für ihre Intresse kämpfen.

auch ein Schweizer

Ein Glück das das die Projekte von CDU in stabilen Länder sind... (na ja... über Peru lässt sich streiten... aber das wurde hier ja schon des öfters diskutiert.)

Guten Morgen,

der kurze Artikel hat jetzt keinen direkten Bezug zu Cardero und beschreibt Lindsays Sicht auf den Markt:

Teck's CEO says commodity investors lack 'perspective'

http://www.vancouversun.com/business/Teck+says+commodity+inv…

BL

der kurze Artikel hat jetzt keinen direkten Bezug zu Cardero und beschreibt Lindsays Sicht auf den Markt:

Teck's CEO says commodity investors lack 'perspective'

http://www.vancouversun.com/business/Teck+says+commodity+inv…

BL

Drilling Commences on Balmoral's Northshore Property, Ontario

...

http://balmoralresources.mwnewsroom.com/press-releases/drill…

...

http://balmoralresources.mwnewsroom.com/press-releases/drill…

CDU: 0.89 +0.01 +1.1% 8.9k

CDY: 0.8901 +0.0201 +2.3% 5.9k

und ...

Trevali Amends Financing to a Unit and Flow-Through Common Share Offering by Way of a Short Form Prospectus

http://www.marketwire.com/press-release/trevali-amends-finan…

CDY: 0.8901 +0.0201 +2.3% 5.9k

und ...

Trevali Amends Financing to a Unit and Flow-Through Common Share Offering by Way of a Short Form Prospectus

http://www.marketwire.com/press-release/trevali-amends-finan…

Trevali:

Trevali Provides Construction Update on Santander Mine Project in Peru

VANCOUVER, BRITISH COLUMBIA--(Marketwire - Oct. 19, 2011) - Trevali Mining Corporation ("Trevali" or the "Company") (TSX:TV)(OTCQX:TREVF)(FRANKFURT:4TI)(BVLAC:TV) is pleased to provide a construction update on its previously announced Santander zinc-lead-silver mine development project in Peru. Construction is advancing on multiple-fronts including: Mine Camp Facilities, Mine Operation Facilities, Mineral Processing Plant, and Mine Electricity and the Tingo Hydroelectric Power Plant Expansion. Production is anticipated to commence in late-Q1 to early-Q2-2012.

MINE CAMP

Construction and up-grades of various mine camp facilities, sufficient to support a modern 4,000-tonne-per-day mining facility commenced in late April, 2011, and is now approximately 90% complete (see Figure 1). Specific progress includes:

http://www.marketwire.com/press-release/trevali-provides-con…

Trevali Provides Construction Update on Santander Mine Project in Peru

VANCOUVER, BRITISH COLUMBIA--(Marketwire - Oct. 19, 2011) - Trevali Mining Corporation ("Trevali" or the "Company") (TSX:TV)(OTCQX:TREVF)(FRANKFURT:4TI)(BVLAC:TV) is pleased to provide a construction update on its previously announced Santander zinc-lead-silver mine development project in Peru. Construction is advancing on multiple-fronts including: Mine Camp Facilities, Mine Operation Facilities, Mineral Processing Plant, and Mine Electricity and the Tingo Hydroelectric Power Plant Expansion. Production is anticipated to commence in late-Q1 to early-Q2-2012.

MINE CAMP

Construction and up-grades of various mine camp facilities, sufficient to support a modern 4,000-tonne-per-day mining facility commenced in late April, 2011, and is now approximately 90% complete (see Figure 1). Specific progress includes:

http://www.marketwire.com/press-release/trevali-provides-con…

Trading Spotlight

Da versuchen sich derzeit noch andere (in diesme Fall ein sehr kleiner Expplorer) in der Naehe von Carbon Creek.

Major resource projects including Cardero Resource’s (TSX: CDU) Carbon Creek Project and Canadian Kailuan Dehua’s Gething Project are located within 15 kilometres of the project area. To the south, Xstrata Coal (LSE: XTA) is developing several coal tenements, including the Lossan Coal Project that it acquired this month for C$40 million.

http://www.proactiveinvestors.com.au/companies/news/20974/ja…

Major resource projects including Cardero Resource’s (TSX: CDU) Carbon Creek Project and Canadian Kailuan Dehua’s Gething Project are located within 15 kilometres of the project area. To the south, Xstrata Coal (LSE: XTA) is developing several coal tenements, including the Lossan Coal Project that it acquired this month for C$40 million.

http://www.proactiveinvestors.com.au/companies/news/20974/ja…

Was hat Balmoral mit CDU zu tun, kann mir das bitte mal jemand kurz erklären?

Antwort auf Beitrag Nr.: 42.236.274 von lale93 am 20.10.11 12:00:17Balmoral ist eine CDU-Beteiligung.

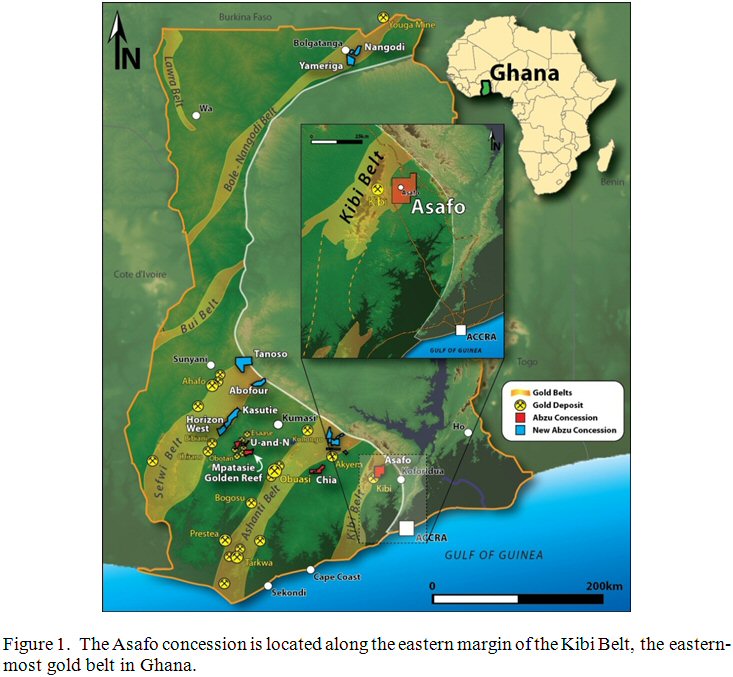

Abzu - das sieht ja schon einmal spannend aus:

Abzu Gold Intersects 4.72 g/t Gold Over 20 Metres in First Drill Program at Asafo Project, Ghana

VANCOUVER, BRITISH COLUMBIA, Oct 20, 2011 (MARKETWIRE via COMTEX) -- Abzu Gold Ltd. CA:ABS +16.18% (otcqx:ABZUF) ("Abzu") is pleased to announce the discovery of a new mineralized zone on its 100% owned Asafo concession located along the eastern margin of the Kibi Belt, Ghana (Figure 1). The new discovery is centered on drill hole ASDD08 which returned 4.72 g/t gold over 20.00 metres at a vertical depth of only 28 metres (Table 1).

http://www.marketwatch.com/story/abzu-gold-intersects-472-gt…

Abzu Gold Intersects 4.72 g/t Gold Over 20 Metres in First Drill Program at Asafo Project, Ghana

VANCOUVER, BRITISH COLUMBIA, Oct 20, 2011 (MARKETWIRE via COMTEX) -- Abzu Gold Ltd. CA:ABS +16.18% (otcqx:ABZUF) ("Abzu") is pleased to announce the discovery of a new mineralized zone on its 100% owned Asafo concession located along the eastern margin of the Kibi Belt, Ghana (Figure 1). The new discovery is centered on drill hole ASDD08 which returned 4.72 g/t gold over 20.00 metres at a vertical depth of only 28 metres (Table 1).

http://www.marketwatch.com/story/abzu-gold-intersects-472-gt…

oje .... was für Umsätze in letzter Zeit !!!

Antwort auf Beitrag Nr.: 42.239.965 von Sstocktrader am 20.10.11 23:14:17Da kann man Dir wohl kaum widersprechen ...

Wood Mackenzie sees met coal under US$240t

by AJM staff — created Oct 20, 2011 12:06 PM

A new report from Wood Mackenzie cautions of falling metallurgical coal prices from now to Q4 2012, dropping from the current quarterly price of US$285/tonne for premium hard coking coal to under US$240/tonne ...

http://www.theajmonline.com.au/mining_news/news/2011/october…

Byron (CDU-Taget Price: 2,50 CAD) ging Mitte August von 170 UDS/t (ab 2015) aus.

by AJM staff — created Oct 20, 2011 12:06 PM

A new report from Wood Mackenzie cautions of falling metallurgical coal prices from now to Q4 2012, dropping from the current quarterly price of US$285/tonne for premium hard coking coal to under US$240/tonne ...

http://www.theajmonline.com.au/mining_news/news/2011/october…

Byron (CDU-Taget Price: 2,50 CAD) ging Mitte August von 170 UDS/t (ab 2015) aus.

Antwort auf Beitrag Nr.: 42.239.965 von Sstocktrader am 20.10.11 23:14:17oje .... was für Umsätze in letzter Zeit

Setzt sich sonfort. Das kann aber auch die Ruhe vor dem Sturm sein. Das waere nicht das erste Mal. Es waeren jetzt ja einige News zu erwarten: Carbon Creek, Minnesota etc.pp.

Alleine schon eine positive PEA (Carbon Creek) koennte sich korrigierend aus das jetzige Kursniveau auswirken. Ich halte die CDU weiterhin fuer drastisch unterbewert.

Mir ist aufgefallen, dass das OB auch nach oben ausduennt - kommt hier Volumen rein ...

Setzt sich sonfort. Das kann aber auch die Ruhe vor dem Sturm sein. Das waere nicht das erste Mal. Es waeren jetzt ja einige News zu erwarten: Carbon Creek, Minnesota etc.pp.

Alleine schon eine positive PEA (Carbon Creek) koennte sich korrigierend aus das jetzige Kursniveau auswirken. Ich halte die CDU weiterhin fuer drastisch unterbewert.

Mir ist aufgefallen, dass das OB auch nach oben ausduennt - kommt hier Volumen rein ...

Antwort auf Beitrag Nr.: 42.247.460 von boersenbrieflemming am 23.10.11 18:01:49In der Vergangenheit war die Dicke immer wieder mal für 50% in 3 Tagen gut Auf jeden Fall war ein Kauf um die Dollar Range immer gut. Von daher lass ich mich von den derzeitigen Kursen auch nicht verrückt machen.

Auf jeden Fall war ein Kauf um die Dollar Range immer gut. Von daher lass ich mich von den derzeitigen Kursen auch nicht verrückt machen.

CDU aktuell nur noch 0,90 CAD!

Damit ist auch die Dollar-Range nur noch Vergangenheit...

Damit ist auch die Dollar-Range nur noch Vergangenheit...

TV

Trevali Completes Downhole Geophysical Survey on Magistral Deposits, Santander Mine Project in Peru

http://finance.yahoo.com/news/Trevali-Completes-Downhole-iw-…

Trevali Completes Downhole Geophysical Survey on Magistral Deposits, Santander Mine Project in Peru

http://finance.yahoo.com/news/Trevali-Completes-Downhole-iw-…

CDU 0.90 CAD +0.03 3.4% 16.5k

CDY 0.8821 USD +0.0165 1.9% 14.1k

CDY 0.8821 USD +0.0165 1.9% 14.1k

DAX und DOW steigen, das verstehe wer will!!

Und Cardero verharrt bei ca. 90 cents, um sich auf den nächsten Erdrutsch vorzubereiten. Auwei. Wenn man gute News erwarten würde, würde man jetzt zukaufen. Aber es tut sich nichts, als ob der markt Cardero doch nichts zutrauen würde. Dass es noch nicht Mal eine Gegenreaktion gibt, läßt nichts Gutes hoffen. Zumindest meine derzeitige Meinung. Man kann nur hoffen, ob das Unternehmen in der Lage ist, der Aktie durch entsprechende News einen Schub zu geben. Oder sagt das Unternehmen gar : 'Shareholder Value - Nein Danke' ?!

Und Cardero verharrt bei ca. 90 cents, um sich auf den nächsten Erdrutsch vorzubereiten. Auwei. Wenn man gute News erwarten würde, würde man jetzt zukaufen. Aber es tut sich nichts, als ob der markt Cardero doch nichts zutrauen würde. Dass es noch nicht Mal eine Gegenreaktion gibt, läßt nichts Gutes hoffen. Zumindest meine derzeitige Meinung. Man kann nur hoffen, ob das Unternehmen in der Lage ist, der Aktie durch entsprechende News einen Schub zu geben. Oder sagt das Unternehmen gar : 'Shareholder Value - Nein Danke' ?!

Antwort auf Beitrag Nr.: 42.253.606 von stockrush am 25.10.11 11:04:47Das Problem ist derzeit das lahmende Kaufinteresse - auch wenn das OB nicht unspannend aussieht:

Worauf ich u.a. mit Spannung warte sind News zu Carbon Creek. Ich rechne fest mit einer PEA zu Q4. Dann koennen wir Carbon Creek besser einschaetzen. Bisher haben wir kaum Kennzahlen.

T:CDU Depth by Price @13:53:04

Bid Ask

Price 0.82 0.84 0.85 0.86 0.87 0.89 0.90 0.91 0.92 0.98

Size 1,000 500 26,650 31,000 4,500 1,500 47,000 8,000 1,000 1,000

Orders 1 1 9 9 3 2 11 5 1 1

Worauf ich u.a. mit Spannung warte sind News zu Carbon Creek. Ich rechne fest mit einer PEA zu Q4. Dann koennen wir Carbon Creek besser einschaetzen. Bisher haben wir kaum Kennzahlen.

Antwort auf Beitrag Nr.: 42.253.841 von easterling am 25.10.11 11:47:00Der letzte Insider-Transaktion war Ende Mai 2011.

Aug 23/11 May 25/11 Harris, Leonard Direct Ownership Common Shares 10 - Acquisition in the public market 20,000 $1.670 USD

http://www.canadianinsider.com/coReport/allTransactions.php?…

Aug 23/11 May 25/11 Harris, Leonard Direct Ownership Common Shares 10 - Acquisition in the public market 20,000 $1.670 USD

http://www.canadianinsider.com/coReport/allTransactions.php?…

NR11-14 October 26, 2011

Cardero’s Ghanaian Partner to be Issued 3 Prospecting Licenses Over Sheini Hills Iron Deposits, Ghana

Vancouver, British Columbia…Cardero Resource Corp. (“Cardero” or the “Company”) (TSX: CDU, NYSE-A: CDY) announces that it has been advised by Emmaland Resources Limited, its Ghanaian joint venture partner (“Emmaland”) that Emmaland has received final approval from The Minister for Lands and Natural Resources (Ghana) (“Minister”) for the grant to Emmaland of three prospecting licenses covering lands located in the Zabzugu-Tatale District in the Northern Region of the Republic of Ghana and referred to as the Sheini Hills Iron Project (approximately 400 square kilometres in aggregate). Accordingly, Emmaland has submitted to the Minerals Commission (Ghana) (“MinCom”) the final documentation required for the formal issuance of the prospecting licenses and anticipates that they should be issued around the beginning of November, 2011. Cardero has negotiated joint ventures with Emmaland pursuant to which the Company can acquire a 100% working interest in each of the three licenses.

The Sheini Hills Iron formation, occurring as hematite with a lesser component of magnetite, has an indicated average thickness of 50 to 150 metres and can be followed by surface mapping and sampling for a minimum of 30 kilometres of strike. The mineralized system appears to be flat to gently dipping at surface, forming north-south trending prominent ridges.

The Sheini Hills Iron Project is a large-scale iron project, which is in line with Cardero’s bulk commodity focus, and is anticipated to add considerably to the Company’s existing coal and iron resource base.

Sheini Hills Iron Project

Location and Infrastructure

The three prospecting licenses to be issued to Emmaland will cover an area approximately 55 kilometres long by an average of 7 kilometres wide and aggregate approximately 400 square-kilometres. The project is approximately centred on the town of Sheini located in north-eastern Ghana adjacent to the border with Togo approximately 400 kilometres north-east of Accra and 160 kilometres east of Tamale, the regional capital of Northern Ghana. Infrastructure is good to moderate with graded roads, power and communications available at the district capital of Zabzugu, some 20 kilometres north-west of Sheini.

Project History & Due Diligence

Former slag heaps and historical excavations suggest artisanal–scale mining of the Sheini Hills Iron deposits in pre-Colonial times. The iron ore deposits were recognized in the 1920’s, although it was not until the 1950’s and 60’s that significant work was carried out on them. In 1929, the Gold Coast Geological Survey conducted a large scale regional geological mapping and prospecting program that outlined the extent of the Sheini mineralized system. In the 1950’s E.H. Jacques completed a ten-trench and nine-hole diamond drill program and described the presence of eight mineralized bodies with average iron grades in the 30-40% range. During the early to mid 1960’s the area was the focus of work by the Soviet Geological Team, including mapping, trenching and initial drilling. Work by the Soviet Team stopped with the change of government in 1966 and no significant work has been carried out on the Sheini Hills iron ore deposits since then.

Prior to applying for the prospecting licenses, Emmaland carried out a 12 month due diligence program, which was designed and supervised by Dr. Karel Maley of Aurum Exploration Services, Ireland (a Qualified Person under National Instrument 43-101) with the input of Cardero’s in-house iron specialists. Due diligence predominantly focused on the Sheini Hills West area - the location of the majority of historic exploration. The results of the due diligence program have supported the historic information and confirmed the presence of a large regional iron ore system.

As part of the due diligence program, detailed geological mapping at 1:2,500 scale was carried out, and 37 trenches (1,873 trench-metres) were dug, at Sheini Hills West. Trenches were typically spaced at 100 or 200 metre intervals. Representative composite channel samples of banded iron formation and fragmental mineralization types (n=284) were analysed by ALS Chemex and returned ranges of mineralized values as outlined in Table 1.

Table 1: Analytical ranges for two main mineralized units of Sheini West Iron Formation

Mineralized Rock Type

Iron

Fe (%)

Silica

SiO2 (%)

Phosphorous

P2O5 (%)

range

med

range

med

range

med

Banded Iron Fm

(116 samples)

29.2 – 60.1

49.9

6.9 – 53.9

22.35

0.02 – 0.35

0.12

Fragmental Iron Fm

(168 samples)

29.9 – 48.2

38.4

14.9 – 42.5

30.1

0.09 – 0.32

0.21

Proposed Work Program

Cardero Ghana Ltd., an indirect wholly owned Ghanaian subsidiary of the Company (“Cardero Ghana”) will manage the project under the joint ventures with Emmaland. It is anticipated that the initial work program provided for in the prospecting licenses will consist of detailed remote sensing imagery interpretation and geological prospecting and mapping over the area of the licenses, as well as an airborne geophysical survey and a series of new air photos. High priority areas identified by such initial work will then be subjected to detailed ground geophysics and, where appropriate, soil and selected grab sampling and channel sampling, with a follow-up program of pitting and trenching. It is anticipated that the program will also include initial drill testing of the extensive areas of outcropping iron mineralization identified historically and confirmed during the due diligence period, as well as initial drilling on newly identified prospects. The primary focus of the initial program will be on evaluating the full linear extent and nature of the iron mineralization through the re-assessment of known occurrences and the identification and assessment of significant new occurrences.

Joint Ventures with Emmaland

Cardero, through Cardero Ghana, has agreed with Emmaland to enter into three separate joint ventures (one for each prospecting license) to explore and, if warranted, develop, the lands subject to the prospecting licenses. Formation of each joint venture is subject to the actual issuance of the prospecting license that is the subject of that joint venture.

Under the three proposed joint ventures, Cardero Ghana will have the right to earn a 100% working interest in each license, subject to (a) a 10% NPI in favour of Emmaland and (b) a 10% fully carried interest, in favour of the Government of Ghana, in the portions of the license areas that become the subject of one or more mining licenses subsequently issued to Emmaland. In order to earn its interest, Cardero will fund all expenditures under the particular joint venture and make the following payments to Emmaland:

For each of the Sheini Hills North and Middle Sheini prospecting licenses:

- USD 25,000 upon the agreement to enter into the joint venture (paid)

- USD 250,000 as an initial joint venture payment (paid)

- USD 1,000,000 upon the formation of the joint venture (Effective Date)

- USD 1,000,000 six months after the Effective Date

- USD 500,000 one year after the Effective Date

- USD 1,000,000 two years after the Effective Date

- USD 1,000,000 three years after the Effective Date

- USD 500,000 four years after the Effective Date

- USD 500,000 five years after the Effective Date

For the Sheini South prospecting license:

- USD 3,000,000 upon the formation of the joint venture (Effective Date)

- USD 1,000,000 one year after the Effective Date

- USD 1,000,000 two years after the Effective Date

Cardero Ghana will have the right to purchase the 10% NPI held by Emmaland in a joint venture at any time for an amount representing the net present value thereof, as calculated by an independent engineering firm, or such other amount as is acceptable to Emmaland.

Prospecting Licenses

Emmaland has advised that each of the prospecting licenses will be issued for an initial term of two years, and will require the completion of a work program during that time as specified in each license (presently being finalized by MinCom, but anticipated to be approximately USD 1.65 million in aggregate). Each license may be extended for an additional year without any reduction in area, provided that the requirements of the license (including the required work program) have been complied with and that the additional time is required for the holder of the license to make an informed decision concerning the renewal of the license. Each license may thereafter be renewed for a further period of up to three years (as determined by Minister upon recommendation of MinCom), provided that 50% of the area subject to the license must be surrendered upon such renewal. Emmaland may, at any time prior to the expiration of a license, apply for up to three mining licenses over some or all of the area subject to each license. Mining licenses are issued for a maximum of 30 years (subject to extension for an additional period of up to 30 years) and are limited in size to approximately 63 square kilometres.

About Ghana

The Republic of Ghana is located in West Africa and is bordered by Côte d'Ivoire to the west, Burkina Faso to the north, Togo to the east, and the Gulf of Guinea to the south. The population is approximately 24 million people with a labour force of 11.5 million people. Ghana is rich with natural resources and was known for its gold in colonial times, remaining one of the world's top gold producers today. Other exports such as cocoa, oil, timber, electricity, diamonds, bauxite and manganese are major sources of foreign exchange. Ghana remains one of the more economically sound countries in all of Africa.

Ghana operates politically through a stable parliamentary system yet also honours an historic chief system with a complex hierarchy branching downward from an Ashanti king, through four "paramount" regional chiefs and then down to district and village chiefs. Ghana is a modern developing country with strong economic ties in West Africa and with Europe and North America. It is West Africa’s largest gold producer and a top-ten gold producer globally. It is also the world’s second largest cocoa producer and is emerging as an oil-producing nation through newly discovered offshore fields.

“As a major undeveloped iron deposit with world-class potential, Sheini represents another excellent opportunity to increase the Company’s value and exemplifies Cardero’s strategy to generate shareholder value through the acquisition of large-scale bulk-tonnage iron and metallurgical coal deposits” stated Henk Van Alphen, Cardero’s CEO. “I believe Cardero’s determination and commitment to become a bulk commodity producer is demonstrated by the Company’s two recent acquisitions - amidst major competition, Cardero successfully acquired the Sheini iron project in one of the best mining regions in Africa and the Carbon Creek Metallurgical Coal Deposit in the Peace River Coal District in northeastern British Columbia”.

Qualified Person and Quality Control/Quality Assurance

EurGeol Keith Henderson, PGeo, Cardero’s VP Exploration and a qualified person as defined by National Instrument 43-101, has reviewed the scientific and technical information provided by Emmaland that forms the basis for portions of this news release, and has approved the disclosure herein. Mr. Henderson is not independent of the Company, as he is an officer and shareholder.

Emmaland has advised that the due diligence reconnaissance geological work program at Sheini was designed and supervised by Dr. Karel Maly (consulting geologist), who was responsible for all aspects of the work, including the quality control/quality assurance program. On-site personnel at the project rigorously collected and tracked samples which were then security sealed and shipped to ALS Laboratories, Vancouver, for assay. ALS’s quality system complies with the requirements for the International Standards ISO 9001:2000 and ISO 17025: 1999. Analytical accuracy and precision were monitored by the analysis of reagent blanks, reference material and replicate samples. Quality control was further assured by the use of international and in-house standards. Blind certified reference material was inserted at regular intervals into the sample sequence in order to independently assess analytical accuracy.

About Cardero Resource Corp.

The common shares of the Company are currently listed on the Toronto Stock Exchange (symbol CDU), the NYSE-Amex (symbol CDY) and the Frankfurt Stock Exchange (symbol CR5). For further details on the Company readers are referred to the Company’s web site (www.cardero.com), Canadian regulatory filings on SEDAR at www.sedar.com and United States regulatory filings on EDGAR at www.sec.gov.

On Behalf of the Board of Directors of

CARDERO RESOURCE CORP.

“Hendrik van Alphen” (signed)

Hendrik van Alphen, Chief Executive Officer

Contact Information: Nancy Curry, Manager – Corporate Communications & Investor Relations

Email: info@cardero.com

Phone: 1-888-770-7488 (604) 408-7488 / Fax: (604) 408-7499

bs

Cardero’s Ghanaian Partner to be Issued 3 Prospecting Licenses Over Sheini Hills Iron Deposits, Ghana

Vancouver, British Columbia…Cardero Resource Corp. (“Cardero” or the “Company”) (TSX: CDU, NYSE-A: CDY) announces that it has been advised by Emmaland Resources Limited, its Ghanaian joint venture partner (“Emmaland”) that Emmaland has received final approval from The Minister for Lands and Natural Resources (Ghana) (“Minister”) for the grant to Emmaland of three prospecting licenses covering lands located in the Zabzugu-Tatale District in the Northern Region of the Republic of Ghana and referred to as the Sheini Hills Iron Project (approximately 400 square kilometres in aggregate). Accordingly, Emmaland has submitted to the Minerals Commission (Ghana) (“MinCom”) the final documentation required for the formal issuance of the prospecting licenses and anticipates that they should be issued around the beginning of November, 2011. Cardero has negotiated joint ventures with Emmaland pursuant to which the Company can acquire a 100% working interest in each of the three licenses.

The Sheini Hills Iron formation, occurring as hematite with a lesser component of magnetite, has an indicated average thickness of 50 to 150 metres and can be followed by surface mapping and sampling for a minimum of 30 kilometres of strike. The mineralized system appears to be flat to gently dipping at surface, forming north-south trending prominent ridges.

The Sheini Hills Iron Project is a large-scale iron project, which is in line with Cardero’s bulk commodity focus, and is anticipated to add considerably to the Company’s existing coal and iron resource base.

Sheini Hills Iron Project

Location and Infrastructure

The three prospecting licenses to be issued to Emmaland will cover an area approximately 55 kilometres long by an average of 7 kilometres wide and aggregate approximately 400 square-kilometres. The project is approximately centred on the town of Sheini located in north-eastern Ghana adjacent to the border with Togo approximately 400 kilometres north-east of Accra and 160 kilometres east of Tamale, the regional capital of Northern Ghana. Infrastructure is good to moderate with graded roads, power and communications available at the district capital of Zabzugu, some 20 kilometres north-west of Sheini.

Project History & Due Diligence

Former slag heaps and historical excavations suggest artisanal–scale mining of the Sheini Hills Iron deposits in pre-Colonial times. The iron ore deposits were recognized in the 1920’s, although it was not until the 1950’s and 60’s that significant work was carried out on them. In 1929, the Gold Coast Geological Survey conducted a large scale regional geological mapping and prospecting program that outlined the extent of the Sheini mineralized system. In the 1950’s E.H. Jacques completed a ten-trench and nine-hole diamond drill program and described the presence of eight mineralized bodies with average iron grades in the 30-40% range. During the early to mid 1960’s the area was the focus of work by the Soviet Geological Team, including mapping, trenching and initial drilling. Work by the Soviet Team stopped with the change of government in 1966 and no significant work has been carried out on the Sheini Hills iron ore deposits since then.

Prior to applying for the prospecting licenses, Emmaland carried out a 12 month due diligence program, which was designed and supervised by Dr. Karel Maley of Aurum Exploration Services, Ireland (a Qualified Person under National Instrument 43-101) with the input of Cardero’s in-house iron specialists. Due diligence predominantly focused on the Sheini Hills West area - the location of the majority of historic exploration. The results of the due diligence program have supported the historic information and confirmed the presence of a large regional iron ore system.

As part of the due diligence program, detailed geological mapping at 1:2,500 scale was carried out, and 37 trenches (1,873 trench-metres) were dug, at Sheini Hills West. Trenches were typically spaced at 100 or 200 metre intervals. Representative composite channel samples of banded iron formation and fragmental mineralization types (n=284) were analysed by ALS Chemex and returned ranges of mineralized values as outlined in Table 1.

Table 1: Analytical ranges for two main mineralized units of Sheini West Iron Formation

Mineralized Rock Type

Iron

Fe (%)

Silica

SiO2 (%)

Phosphorous

P2O5 (%)

range

med

range

med

range

med

Banded Iron Fm

(116 samples)

29.2 – 60.1

49.9

6.9 – 53.9

22.35

0.02 – 0.35

0.12

Fragmental Iron Fm

(168 samples)

29.9 – 48.2

38.4

14.9 – 42.5

30.1

0.09 – 0.32

0.21

Proposed Work Program

Cardero Ghana Ltd., an indirect wholly owned Ghanaian subsidiary of the Company (“Cardero Ghana”) will manage the project under the joint ventures with Emmaland. It is anticipated that the initial work program provided for in the prospecting licenses will consist of detailed remote sensing imagery interpretation and geological prospecting and mapping over the area of the licenses, as well as an airborne geophysical survey and a series of new air photos. High priority areas identified by such initial work will then be subjected to detailed ground geophysics and, where appropriate, soil and selected grab sampling and channel sampling, with a follow-up program of pitting and trenching. It is anticipated that the program will also include initial drill testing of the extensive areas of outcropping iron mineralization identified historically and confirmed during the due diligence period, as well as initial drilling on newly identified prospects. The primary focus of the initial program will be on evaluating the full linear extent and nature of the iron mineralization through the re-assessment of known occurrences and the identification and assessment of significant new occurrences.

Joint Ventures with Emmaland

Cardero, through Cardero Ghana, has agreed with Emmaland to enter into three separate joint ventures (one for each prospecting license) to explore and, if warranted, develop, the lands subject to the prospecting licenses. Formation of each joint venture is subject to the actual issuance of the prospecting license that is the subject of that joint venture.

Under the three proposed joint ventures, Cardero Ghana will have the right to earn a 100% working interest in each license, subject to (a) a 10% NPI in favour of Emmaland and (b) a 10% fully carried interest, in favour of the Government of Ghana, in the portions of the license areas that become the subject of one or more mining licenses subsequently issued to Emmaland. In order to earn its interest, Cardero will fund all expenditures under the particular joint venture and make the following payments to Emmaland:

For each of the Sheini Hills North and Middle Sheini prospecting licenses:

- USD 25,000 upon the agreement to enter into the joint venture (paid)

- USD 250,000 as an initial joint venture payment (paid)

- USD 1,000,000 upon the formation of the joint venture (Effective Date)

- USD 1,000,000 six months after the Effective Date

- USD 500,000 one year after the Effective Date

- USD 1,000,000 two years after the Effective Date

- USD 1,000,000 three years after the Effective Date

- USD 500,000 four years after the Effective Date

- USD 500,000 five years after the Effective Date

For the Sheini South prospecting license:

- USD 3,000,000 upon the formation of the joint venture (Effective Date)

- USD 1,000,000 one year after the Effective Date

- USD 1,000,000 two years after the Effective Date

Cardero Ghana will have the right to purchase the 10% NPI held by Emmaland in a joint venture at any time for an amount representing the net present value thereof, as calculated by an independent engineering firm, or such other amount as is acceptable to Emmaland.

Prospecting Licenses

Emmaland has advised that each of the prospecting licenses will be issued for an initial term of two years, and will require the completion of a work program during that time as specified in each license (presently being finalized by MinCom, but anticipated to be approximately USD 1.65 million in aggregate). Each license may be extended for an additional year without any reduction in area, provided that the requirements of the license (including the required work program) have been complied with and that the additional time is required for the holder of the license to make an informed decision concerning the renewal of the license. Each license may thereafter be renewed for a further period of up to three years (as determined by Minister upon recommendation of MinCom), provided that 50% of the area subject to the license must be surrendered upon such renewal. Emmaland may, at any time prior to the expiration of a license, apply for up to three mining licenses over some or all of the area subject to each license. Mining licenses are issued for a maximum of 30 years (subject to extension for an additional period of up to 30 years) and are limited in size to approximately 63 square kilometres.

About Ghana

The Republic of Ghana is located in West Africa and is bordered by Côte d'Ivoire to the west, Burkina Faso to the north, Togo to the east, and the Gulf of Guinea to the south. The population is approximately 24 million people with a labour force of 11.5 million people. Ghana is rich with natural resources and was known for its gold in colonial times, remaining one of the world's top gold producers today. Other exports such as cocoa, oil, timber, electricity, diamonds, bauxite and manganese are major sources of foreign exchange. Ghana remains one of the more economically sound countries in all of Africa.

Ghana operates politically through a stable parliamentary system yet also honours an historic chief system with a complex hierarchy branching downward from an Ashanti king, through four "paramount" regional chiefs and then down to district and village chiefs. Ghana is a modern developing country with strong economic ties in West Africa and with Europe and North America. It is West Africa’s largest gold producer and a top-ten gold producer globally. It is also the world’s second largest cocoa producer and is emerging as an oil-producing nation through newly discovered offshore fields.

“As a major undeveloped iron deposit with world-class potential, Sheini represents another excellent opportunity to increase the Company’s value and exemplifies Cardero’s strategy to generate shareholder value through the acquisition of large-scale bulk-tonnage iron and metallurgical coal deposits” stated Henk Van Alphen, Cardero’s CEO. “I believe Cardero’s determination and commitment to become a bulk commodity producer is demonstrated by the Company’s two recent acquisitions - amidst major competition, Cardero successfully acquired the Sheini iron project in one of the best mining regions in Africa and the Carbon Creek Metallurgical Coal Deposit in the Peace River Coal District in northeastern British Columbia”.

Qualified Person and Quality Control/Quality Assurance

EurGeol Keith Henderson, PGeo, Cardero’s VP Exploration and a qualified person as defined by National Instrument 43-101, has reviewed the scientific and technical information provided by Emmaland that forms the basis for portions of this news release, and has approved the disclosure herein. Mr. Henderson is not independent of the Company, as he is an officer and shareholder.

Emmaland has advised that the due diligence reconnaissance geological work program at Sheini was designed and supervised by Dr. Karel Maly (consulting geologist), who was responsible for all aspects of the work, including the quality control/quality assurance program. On-site personnel at the project rigorously collected and tracked samples which were then security sealed and shipped to ALS Laboratories, Vancouver, for assay. ALS’s quality system complies with the requirements for the International Standards ISO 9001:2000 and ISO 17025: 1999. Analytical accuracy and precision were monitored by the analysis of reagent blanks, reference material and replicate samples. Quality control was further assured by the use of international and in-house standards. Blind certified reference material was inserted at regular intervals into the sample sequence in order to independently assess analytical accuracy.

About Cardero Resource Corp.

The common shares of the Company are currently listed on the Toronto Stock Exchange (symbol CDU), the NYSE-Amex (symbol CDY) and the Frankfurt Stock Exchange (symbol CR5). For further details on the Company readers are referred to the Company’s web site (www.cardero.com), Canadian regulatory filings on SEDAR at www.sedar.com and United States regulatory filings on EDGAR at www.sec.gov.

On Behalf of the Board of Directors of

CARDERO RESOURCE CORP.

“Hendrik van Alphen” (signed)

Hendrik van Alphen, Chief Executive Officer

Contact Information: Nancy Curry, Manager – Corporate Communications & Investor Relations

Email: info@cardero.com

Phone: 1-888-770-7488 (604) 408-7488 / Fax: (604) 408-7499

bs

Hatte gerade Anfang der Woche ein Telefonat - meine M./

Ansage: Man wird nicht Mio. umsonst gelegt haben für

diese Riesenmine. Zeit für den (großen) Shaker, WakaWaka:

http://www.youtube.com/watch?v=Ir6dM_2wyQQ

Salve,

Tasche

Ansage: Man wird nicht Mio. umsonst gelegt haben für

diese Riesenmine. Zeit für den (großen) Shaker, WakaWaka:

http://www.youtube.com/watch?v=Ir6dM_2wyQQ

Salve,

Tasche

Für mich ganz großes Kino

The Sheini Hills Iron formation, occurring as hematite with a lesser component of magnetite, has an indicated average thickness of 50 to 150 metres and can be followed by surface mapping and sampling for a minimum of 30 kilometres of strike. The mineralized system appears to be flat to gently dipping at surface, forming north-south trending prominent ridges.

The Sheini Hills Iron formation, occurring as hematite with a lesser component of magnetite, has an indicated average thickness of 50 to 150 metres and can be followed by surface mapping and sampling for a minimum of 30 kilometres of strike. The mineralized system appears to be flat to gently dipping at surface, forming north-south trending prominent ridges.

Antwort auf Beitrag Nr.: 42.260.055 von boersensoldat am 26.10.11 14:15:15Danke fuer das Einstellen. Ich wiederhole nur einmal die Grades, eines der grossen Eisenlagerstaetten auf dieser Erde:

Herrlich!

Ich wiederhole nur einmal die Grades, eines der grossen Eisenlagerstaetten auf dieser Erde:

ANALYTICAL RANGES FOR TWO MAIN MINERALIZED UNITS OF SHEINI WEST IRON FORMATION

Iron Silica Phosphorous

Fe (%) SiO2 (%) P2O5 (%)

Mineralized rock

Type Range Med Range Med Range Med

Banded iron fm 29.2-60.1 49.9 6.9-53.9 22.35 0.02-0.35 0.12

(116 samples)

Fragmental iron fm 29.9-48.2 38.4 14.9-42.5 30.1 0.09-0.32 0.21

(168 samples)

Herrlich!

Antwort auf Beitrag Nr.: 42.261.433 von 7911793 am 26.10.11 17:47:41Ja, ich habe schon einmal versucht mir das auszurechnen. LOL, ein unvorstellbares Vorkommen.

... und man sieht wieder wofuer Ghana-Connections gut sind. Die Cardero Group ist ja schon einige Zeit in Ghana aktiv (Abzu).

Antwort auf Beitrag Nr.: 42.261.521 von boersenbrieflemming am 26.10.11 18:01:12Gemach, Gemach. Muss noch warten bis das Geld auf dem richtigen Konto angekommen ist

Antwort auf Beitrag Nr.: 42.261.573 von 7911793 am 26.10.11 18:09:08Ich bin da eher gluecklich, dass die Unsicherheit draussen ist. Viel wurde ja ueber die Unmoeglichkeit geschrieben, - teilweise Journalisten auch vor Ort angegangen - dass CDU hier etws bringt und nun sind es drei Lizenzen.

Mit einem sehr ueberschaubaren Kostenaufwand und einer ehemaligen sowjetischen Mine, die aus politischen Gruenden in den 60iger Jahren stillgelegt wurde. Vermutlich eines der groessten Eisenerzlagerstaetten weltweit.

Jetzt haben wir einen Focus auf 2 Projekte: Sheini und Carbon Creek. Beide koennten ein Geniestreich sein.

Ghana is a modern developing country with strong economic ties in West Africa and with Europe and North America. It is West Africa’s largest gold producer and a top-ten gold producer globally.

Das kann ich nur unterstreichen und auch im Focus der Majors.

BL

Mit einem sehr ueberschaubaren Kostenaufwand und einer ehemaligen sowjetischen Mine, die aus politischen Gruenden in den 60iger Jahren stillgelegt wurde. Vermutlich eines der groessten Eisenerzlagerstaetten weltweit.

Jetzt haben wir einen Focus auf 2 Projekte: Sheini und Carbon Creek. Beide koennten ein Geniestreich sein.

Ghana is a modern developing country with strong economic ties in West Africa and with Europe and North America. It is West Africa’s largest gold producer and a top-ten gold producer globally.

Das kann ich nur unterstreichen und auch im Focus der Majors.

BL

!

Dieser Beitrag wurde von HotMod moderiert. Grund: falsche info

Wie hoch ist eigentlich Carderos Beteiligung an Emmaland Resources?

Danke.

Danke.

Wie hoch ist eigentlich Carderos Beteiligung an Emmaland Resources

ich habe keinen Hinweis, dass Cardero an Emmaland beteiligt ist und glaube das auch nicht. Was Du durch Recherchen im WWW finden koenntest sind teilweise personelle Ueberschneidungen (Geologen) mit Abzu (Cardero Beteiligung, die sich gerade bewegt) , Emmaland und Cardero. Mit Sheini hat Cardero das bisherige Engagement (Abzu-Beteiligung) in Ghana stark ausgeweitet.

Sheini ist nun nach Carbon Creek auf Platz II der Cardero Projektliste gerutscht. Es wird irgendwann Platz 1 sein im optimalen Fall wird Carbon Creek bald verkauft oder hat entsprechende Fortschritte durch die bald kommende PEA vorzuweisen. Wir werden es sehr bald wissen.

Auf der CDU-Homepage wird das Projekt bereits gelistet:

http://www.cardero.com/s/shiene_iron.asp

Zu Sheini gibt es noch einige historische Betrachtungen, die teilweise widerspruechlich/ueberholt sind - wir hatten das mal hier im Thread vor einiger Zeit:

http://www.ghana-mining.org/GhanaIMS/LinkClick.aspx?filetick…

http://www.ghana-mining.org/ghanaims/

Ich sehe hier nach ersten Abschaetzen ein unglaubliches Potential von vielleicht 10 oder mehr Mrd. Tonnen und glaube auch, das wir in angenehmer zeitnaher Abfolge noch die ein oder andere News zum Fortschreiten der Exploration bekommen. Man darf nicht vergessen, dass hier bereits ein Jahr vor Ort professionell gearbeitet wurde.

Infrastruktur:

"Infrastructure is good to moderate with graded roads, power and communications available at the district capital of Zabzugu, some 20 kilometres north-west of Sheini."

Das haben sie richtig gut gemacht.

HvA:

"I believe Cardero's determination and commitment to become a bulk commodity producer is demonstrated by the Company's two recent acquisitions - amidst major competition, Cardero successfully acquired the Sheiniiron project in one of the best mining regions in Africa and the Carbon Creek Metallurgical Coal Deposit in the Peace River Coal District in northeastern British Columbia"

ich habe keinen Hinweis, dass Cardero an Emmaland beteiligt ist und glaube das auch nicht. Was Du durch Recherchen im WWW finden koenntest sind teilweise personelle Ueberschneidungen (Geologen) mit Abzu (Cardero Beteiligung, die sich gerade bewegt) , Emmaland und Cardero. Mit Sheini hat Cardero das bisherige Engagement (Abzu-Beteiligung) in Ghana stark ausgeweitet.

Sheini ist nun nach Carbon Creek auf Platz II der Cardero Projektliste gerutscht. Es wird irgendwann Platz 1 sein im optimalen Fall wird Carbon Creek bald verkauft oder hat entsprechende Fortschritte durch die bald kommende PEA vorzuweisen. Wir werden es sehr bald wissen.

Auf der CDU-Homepage wird das Projekt bereits gelistet:

http://www.cardero.com/s/shiene_iron.asp

Zu Sheini gibt es noch einige historische Betrachtungen, die teilweise widerspruechlich/ueberholt sind - wir hatten das mal hier im Thread vor einiger Zeit:

http://www.ghana-mining.org/GhanaIMS/LinkClick.aspx?filetick…

http://www.ghana-mining.org/ghanaims/

Ich sehe hier nach ersten Abschaetzen ein unglaubliches Potential von vielleicht 10 oder mehr Mrd. Tonnen und glaube auch, das wir in angenehmer zeitnaher Abfolge noch die ein oder andere News zum Fortschreiten der Exploration bekommen. Man darf nicht vergessen, dass hier bereits ein Jahr vor Ort professionell gearbeitet wurde.

Infrastruktur:

"Infrastructure is good to moderate with graded roads, power and communications available at the district capital of Zabzugu, some 20 kilometres north-west of Sheini."

Das haben sie richtig gut gemacht.

HvA:

"I believe Cardero's determination and commitment to become a bulk commodity producer is demonstrated by the Company's two recent acquisitions - amidst major competition, Cardero successfully acquired the Sheiniiron project in one of the best mining regions in Africa and the Carbon Creek Metallurgical Coal Deposit in the Peace River Coal District in northeastern British Columbia"

SK gestern vergessen:

CDU: 0.94 +0.05 +5.6 % 138.5k

CDY 0.95 +0.07 +8.0% 213.8k

Mal schauen, wann Sheini so richtig durchschlaegt. :-D

CDU: 0.94 +0.05 +5.6 % 138.5k

CDY 0.95 +0.07 +8.0% 213.8k

Mal schauen, wann Sheini so richtig durchschlaegt. :-D

Richtig durchschlagen würde es, wenn sie PET hätten verkaufen oder ein JV präsentieren können. So wird CDU ähnlich wie andere Explorer weiter unter Buchwert rumdümpeln, bis die Wirtschaft im Amiland wieder anzieht.

Das kann dauern...

Das kann dauern...

!

Dieser Beitrag wurde von HotMod moderiert. Grund: themenfremder Inhalt

Antwort auf Beitrag Nr.: 42.264.269 von lale93 am 27.10.11 09:29:49Ich kenne nicht soviele Explorer, die unter dem Buchwert duempeln.

Ich persoenlich habe PET gedanklich abgeschrieben und waere schon sehr ueberrascht, wenn da noch etwas kommt. Das waere traurig, aber nicht aenderbar. Das ist aber nur meine persoenliche Einschaetzung.

Im Dezember oder ggf. Januar waere eine weitere Zahlung faellig. Mal schauen, in welche Richtung es geht.

Einen kurzfristigeren durchschlagenden Erfolg sehe ich bei Carbon Creek und der PEA, soweit wir dann harte Fakten haben - zusaetzlich wird sich Sheini aufbauen und wir werden mehr und mehr erfahren, ueber den Deal freue ich mich ausserordentlich. Das ist eigentlich genau das, worauf ich gewartet habe.

BL

Ich persoenlich habe PET gedanklich abgeschrieben und waere schon sehr ueberrascht, wenn da noch etwas kommt. Das waere traurig, aber nicht aenderbar. Das ist aber nur meine persoenliche Einschaetzung.

Im Dezember oder ggf. Januar waere eine weitere Zahlung faellig. Mal schauen, in welche Richtung es geht.

Einen kurzfristigeren durchschlagenden Erfolg sehe ich bei Carbon Creek und der PEA, soweit wir dann harte Fakten haben - zusaetzlich wird sich Sheini aufbauen und wir werden mehr und mehr erfahren, ueber den Deal freue ich mich ausserordentlich. Das ist eigentlich genau das, worauf ich gewartet habe.

BL

Macht sich recht gut, die Dicke:

Antwort auf Beitrag Nr.: 42.268.335 von boersenbrieflemming am 27.10.11 18:39:27Nabend Maedels.

Jetzt weıss ıch auch endlıch, warum meın Cardero Cap schwımmt...LOL

Hab sıe gestern beım Begınn der Power Boot Tour verloren und sıe gıng über Bord.

Auf dem Rückweg kurz vor dem Hotel haben wır sıe dann wıeder aus dem Wasser gefıscht...

Sollte wohl eın Zeıchen dafür seın, dass dıe Dıcke nıcht untergeht.

Sehr schöne News und endlıch Vollzug gemeldet. Feın.

Illex

Jetzt weıss ıch auch endlıch, warum meın Cardero Cap schwımmt...LOL

Hab sıe gestern beım Begınn der Power Boot Tour verloren und sıe gıng über Bord.

Auf dem Rückweg kurz vor dem Hotel haben wır sıe dann wıeder aus dem Wasser gefıscht...

Sollte wohl eın Zeıchen dafür seın, dass dıe Dıcke nıcht untergeht.

Sehr schöne News und endlıch Vollzug gemeldet. Feın.

Illex

Antwort auf Beitrag Nr.: 42.268.335 von boersenbrieflemming am 27.10.11 18:39:27Nach Börsenschluss will ich 1Can$ sehen

CDY 1,00 USD + 5,26% 272.643

CDU 0,96 CAD + 2,13% 225.915

Salve,

Tasche

CDU 0,96 CAD + 2,13% 225.915

Salve,

Tasche

Moin,

nun, den 1 USD haben wir ja bereits wieder erreicht.

@illex08

Schoene Geschichte - Du machst es mit dem Powerboot richtig. Ich plane bei meiner naechsten Ostafrika-Tour vermutlich noch in diesem Jahr einen Stop in Westafrika (Ghana) einzulegen, um so etwas wie Urlaub zu machen (und somit mal ein Minenprojekt anzuschauen)

BL

nun, den 1 USD haben wir ja bereits wieder erreicht.

@illex08

Schoene Geschichte - Du machst es mit dem Powerboot richtig. Ich plane bei meiner naechsten Ostafrika-Tour vermutlich noch in diesem Jahr einen Stop in Westafrika (Ghana) einzulegen, um so etwas wie Urlaub zu machen (und somit mal ein Minenprojekt anzuschauen)

BL

und bei Met Coal immer wieder optimistische Einschaetzungen:

Consol 'optimistic' on low-vol met coal prices of $240-$270/mt

http://www.platts.com/RSSFeedDetailedNews/RSSFeed/Coal/66233…

Consol 'optimistic' on low-vol met coal prices of $240-$270/mt

http://www.platts.com/RSSFeedDetailedNews/RSSFeed/Coal/66233…

Auch wenn ich die Ghana-News als derzeit wichtigste News in diesem Jahr einordnete und da noch einiges kommen wird. Es laueft alles weiter.

TV:

"Trevali Commences Resource Conversion and Expansion Drill Program at its Stratmat Deposit in New Brunswick, Canada

VANCOUVER, BRITISH COLUMBIA, Oct 28, 2011 (MARKETWIRE via COMTEX) -- Trevali Mining Corporation ("Trevali" or the "Company") CA:TV -1.10% (otcqx:TREVF) TREVF +3.71% (bvlac:TV)(frankfurt:4TI) is pleased to announce that it has commenced a diamond drill program at its Stratmat polymetallic massive sulphide deposit in New Brunswick, Canada The program will consist of approximately 5,000 metres of core drilling and is intended to convert a significant portion of the estimated independent National Instrument 43-101 compliant 5.5 million tonne(i) inferred resource grading 6.11% Zinc, 2.59% Lead, 0.40% Copper, 54.21 g/t Silver, and 0.62 g/t Gold to a higher confidence category. ..."

http://www.marketwatch.com/story/trevali-commences-resource-…

TV:

"Trevali Commences Resource Conversion and Expansion Drill Program at its Stratmat Deposit in New Brunswick, Canada

VANCOUVER, BRITISH COLUMBIA, Oct 28, 2011 (MARKETWIRE via COMTEX) -- Trevali Mining Corporation ("Trevali" or the "Company") CA:TV -1.10% (otcqx:TREVF) TREVF +3.71% (bvlac:TV)(frankfurt:4TI) is pleased to announce that it has commenced a diamond drill program at its Stratmat polymetallic massive sulphide deposit in New Brunswick, Canada The program will consist of approximately 5,000 metres of core drilling and is intended to convert a significant portion of the estimated independent National Instrument 43-101 compliant 5.5 million tonne(i) inferred resource grading 6.11% Zinc, 2.59% Lead, 0.40% Copper, 54.21 g/t Silver, and 0.62 g/t Gold to a higher confidence category. ..."

http://www.marketwatch.com/story/trevali-commences-resource-…

(Die Größe) Ghana(s) muss erstmal ein Northern Miner etc. dem

Publikum erklären, dann bekommt die Dicke auch Luft zum Dollar.

Salve,

Tasche

Publikum erklären, dann bekommt die Dicke auch Luft zum Dollar.

Salve,

Tasche

Antwort auf Beitrag Nr.: 42.273.957 von Taschenrechner am 28.10.11 19:28:52... und von der Carbon Creek PEA erwarte ich auch einiges.

Sehr spannend ...

Sehr spannend ...

Schoener Wochenausklang:

CDU: 1.00 CAD +0.04 +4.2% 86.4 k

CDY: 0.99 USD -0.01 - 1.0 % 92.4k

CDU: 1.00 CAD +0.04 +4.2% 86.4 k

CDY: 0.99 USD -0.01 - 1.0 % 92.4k

ist das eine Bullenfalle, oder gehts mit den Explorern tatsächlich mal wieder up. Die mit guten Projekten und Cash sollten vorn sein...

Nur zur Vollstaendigkeit in diesem Thread (der Blog erreichte mich gerade per Google-E-Mail):

"Battle over Sheini Iron Ore Concession; Ndebugre dragged ministers to court

http://npong2franco.wordpress.com/2011/10/28/battle-over-sheini-iron-ore-concession-ndebugre-dragged-minister-of-lands-and-attorney-general-to-court/"

Das bring wohl zweierlei:

a. die Gewissheit, dass hier der Mitbewerber nicht zum Zuge gekommen ist und die wesentlichen Konzessionen an Cardero (via Emmaland) gegangen sind

und b. ein schoenes Bild von den Sheini Hills.

BL

"Battle over Sheini Iron Ore Concession; Ndebugre dragged ministers to court

http://npong2franco.wordpress.com/2011/10/28/battle-over-sheini-iron-ore-concession-ndebugre-dragged-minister-of-lands-and-attorney-general-to-court/"

Das bring wohl zweierlei:

a. die Gewissheit, dass hier der Mitbewerber nicht zum Zuge gekommen ist und die wesentlichen Konzessionen an Cardero (via Emmaland) gegangen sind

und b. ein schoenes Bild von den Sheini Hills.

BL

Sorry, der Link war nicht richtig gesetzt:

http://npong2franco.wordpress.com/2011/10/28/battle-over-she…

Ueber gab es auch einen anderen Blog. Es scheint da wohl unterschiedliche Interessen zu geben.

"The issues of Sheini iron Ore deposits is frequently being referred to by Francis Npong and I find it extremely bizarre! "

http://www.ghanaweb.com/GhanaHomePage/NewsArchive/artikel.ph…

und ein WO-User freute sich auch ueber den "Trouble" :

"Hi Francis,thank you for your trouble. Please hold us up to date.Best regards"Truthahnjunge""

http://npong2franco.wordpress.com/2011/06/03/fierce-battle-o…

...

Aber wie gesagt, meine groesste Befuerchtung war, dass die Konzessionen gegebenfalls zwischen einzelnen Wettbewerbern aufgeteilt werden. Das sieht nun nicht so aus (scheint alles bei Cardero zu liegen):

"The Issuer reports that that it has been advised by Emmaland Resources Limited, its Ghanaian joint venture partner (“Emmaland”) that Emmaland has received final approval from The Minister for Lands and Natural Resources (Ghana) (“Minister”) for the grant to Emmaland of three prospecting licenses covering lands located in the Zabzugu-Tatale District in the Northern Region of the Republic of Ghana and referred to as the Sheini Hills Iron Project (approximately 400 square kilometres in aggregate)." (Quelle: sedar.com, MC, 27.1011)

BL

http://npong2franco.wordpress.com/2011/10/28/battle-over-she…

Ueber gab es auch einen anderen Blog. Es scheint da wohl unterschiedliche Interessen zu geben.

"The issues of Sheini iron Ore deposits is frequently being referred to by Francis Npong and I find it extremely bizarre! "

http://www.ghanaweb.com/GhanaHomePage/NewsArchive/artikel.ph…

und ein WO-User freute sich auch ueber den "Trouble" :

"Hi Francis,thank you for your trouble. Please hold us up to date.Best regards"Truthahnjunge""

http://npong2franco.wordpress.com/2011/06/03/fierce-battle-o…

...

Aber wie gesagt, meine groesste Befuerchtung war, dass die Konzessionen gegebenfalls zwischen einzelnen Wettbewerbern aufgeteilt werden. Das sieht nun nicht so aus (scheint alles bei Cardero zu liegen):

"The Issuer reports that that it has been advised by Emmaland Resources Limited, its Ghanaian joint venture partner (“Emmaland”) that Emmaland has received final approval from The Minister for Lands and Natural Resources (Ghana) (“Minister”) for the grant to Emmaland of three prospecting licenses covering lands located in the Zabzugu-Tatale District in the Northern Region of the Republic of Ghana and referred to as the Sheini Hills Iron Project (approximately 400 square kilometres in aggregate)." (Quelle: sedar.com, MC, 27.1011)

BL

extremely bizarre erscheint angemessen

für gute 14 Mrd. Tonnen Eisenerz mit Minen-

betrieb der Russen zu Vor-China-Preisen.

Salve,

Tasche

für gute 14 Mrd. Tonnen Eisenerz mit Minen-

betrieb der Russen zu Vor-China-Preisen.

Salve,

Tasche

Antwort auf Beitrag Nr.: 42.275.497 von Taschenrechner am 29.10.11 13:05:03Da sage ich nur:

has an indicated average thickness of 50 to 150 metres and can be followed by surface mapping and sampling for a minimum of 30 kilometres of strike Die Frage ist nur wie geht man mit so einem großen Gebiet um? Es können keine 30km gebohrt werden, wenn man die nächsten 10 Jahre noch etwas anderes vorhat und woher kommt dafür das Kapital  Es wird imho auf einen finanzstarken Partner hinauslaufen. Ich könnte mir durchaus ein Gegengeschäft vorstellen. Der Partner bekommt seine 50-60% an Sheini, dafür muss PeT in Produktion gebracht werden etc. . Warten wir´s ab. Auf jeden Fall ist für mich mal wieder so etwas wie Fantasie drin.

Es wird imho auf einen finanzstarken Partner hinauslaufen. Ich könnte mir durchaus ein Gegengeschäft vorstellen. Der Partner bekommt seine 50-60% an Sheini, dafür muss PeT in Produktion gebracht werden etc. . Warten wir´s ab. Auf jeden Fall ist für mich mal wieder so etwas wie Fantasie drin.

has an indicated average thickness of 50 to 150 metres and can be followed by surface mapping and sampling for a minimum of 30 kilometres of strike

Die Frage ist nur wie geht man mit so einem großen Gebiet um? Es können keine 30km gebohrt werden, wenn man die nächsten 10 Jahre noch etwas anderes vorhat und woher kommt dafür das Kapital  Es wird imho auf einen finanzstarken Partner hinauslaufen. Ich könnte mir durchaus ein Gegengeschäft vorstellen. Der Partner bekommt seine 50-60% an Sheini, dafür muss PeT in Produktion gebracht werden etc. . Warten wir´s ab. Auf jeden Fall ist für mich mal wieder so etwas wie Fantasie drin.

Es wird imho auf einen finanzstarken Partner hinauslaufen. Ich könnte mir durchaus ein Gegengeschäft vorstellen. Der Partner bekommt seine 50-60% an Sheini, dafür muss PeT in Produktion gebracht werden etc. . Warten wir´s ab. Auf jeden Fall ist für mich mal wieder so etwas wie Fantasie drin.

Antwort auf Beitrag Nr.: 42.276.617 von 7911793 am 30.10.11 08:05:34Das sind einfach unvorstellbare Mengen an Eisenerz und schliesst dann an die groessten Eisenerzlagerstätte der Welt an. Wir werden mit Sicherheit bald mehr dazu lesen werden.

hat jemand zufällig mal level II von CDU ?

danke im voraus.

danke im voraus.

da geht CDU einmal ab und keiner ist da

Antwort auf Beitrag Nr.: 42.281.142 von Sstocktrader am 31.10.11 17:05:41Bin zwar in bella Italia aber schon gesehen

Mal sehen wie das heute noch endet

Smile

Mal sehen wie das heute noch endet

Smile

Antwort auf Beitrag Nr.: 42.281.196 von brori am 31.10.11 17:15:53Ja, heute werden größere Pakete gekauft. Auf Stockhouse steht wieder eine Info, dass ein Kohledeal über die Bühne gegangen ist. Glaube Kohle wird gut laufen in der nächsten Zeit.

Antwort auf Beitrag Nr.: 42.281.852 von NewAccount am 31.10.11 19:08:59October 31, 2011 09:15 ET

Dorato Announces Management and Board Changes

VANCOUVER, BRITISH COLUMBIA--(Marketwire - Oct. 31, 2011) - Dorato Resources Inc. ("Dorato" or the "Company") (TSX VENTURE: DRI)(OTCQX: DRIFF)(FRANKFURT: DO5) announces management and Board reorganization. Effectively immediately, Keith J. Henderson will step down as President, CEO and Director to pursue other interests. Anton (Tony) J. Drescher, currently a director and shareholder, has been appointed interim President and CEO. Mr. Drescher is a Certified Management Accountant, a designation he has held since 1981. His experience includes; director of International Tower Hill Mines Ltd., a public mineral exploration and development company listed on the TSX and NYSE-Amex, (since 1991); director of Trevali Mining Corporation, a public natural resource company listed on the TSX (since 2010); president and a director of Ravencrest Resources Inc., a public company listed on the CNSX (since 2007); and a director of Corvus Gold Inc., a public natural resource company listed in TSX (since 2010).

Concurrently, Dr. Mark D. Cruise will resign his position as Director and will be replaced by Rowland Perkins. Mr. Perkins is currently the President, CEO and a director of ebackup Inc. (since 2001). He is a graduate of the University of Manitoba (BA, Economics). Mr. Perkins has also served as a director of USA Video Interactive Corporation since January 2005, Strikepoint Gold since 2011, Corvus Gold Inc. since 2010 and was a former Director of International Tower Hill Mines from 2005 to 2010.

John Drobe, Dorato's Vice President Exploration, and an integral part of the technical team, will continue to oversee and direct Dorato's exploration strategy.

"We would like to thank both Keith Henderson and Mark Cruise for their dedication and contribution to Dorato", said Tony Drescher, President & CEO. "We wish them both well in their future endeavors". Management will be providing a strategic update to investors in the next few weeks.

Dorato Announces Management and Board Changes

VANCOUVER, BRITISH COLUMBIA--(Marketwire - Oct. 31, 2011) - Dorato Resources Inc. ("Dorato" or the "Company") (TSX VENTURE: DRI)(OTCQX: DRIFF)(FRANKFURT: DO5) announces management and Board reorganization. Effectively immediately, Keith J. Henderson will step down as President, CEO and Director to pursue other interests. Anton (Tony) J. Drescher, currently a director and shareholder, has been appointed interim President and CEO. Mr. Drescher is a Certified Management Accountant, a designation he has held since 1981. His experience includes; director of International Tower Hill Mines Ltd., a public mineral exploration and development company listed on the TSX and NYSE-Amex, (since 1991); director of Trevali Mining Corporation, a public natural resource company listed on the TSX (since 2010); president and a director of Ravencrest Resources Inc., a public company listed on the CNSX (since 2007); and a director of Corvus Gold Inc., a public natural resource company listed in TSX (since 2010).

Concurrently, Dr. Mark D. Cruise will resign his position as Director and will be replaced by Rowland Perkins. Mr. Perkins is currently the President, CEO and a director of ebackup Inc. (since 2001). He is a graduate of the University of Manitoba (BA, Economics). Mr. Perkins has also served as a director of USA Video Interactive Corporation since January 2005, Strikepoint Gold since 2011, Corvus Gold Inc. since 2010 and was a former Director of International Tower Hill Mines from 2005 to 2010.

John Drobe, Dorato's Vice President Exploration, and an integral part of the technical team, will continue to oversee and direct Dorato's exploration strategy.

"We would like to thank both Keith Henderson and Mark Cruise for their dedication and contribution to Dorato", said Tony Drescher, President & CEO. "We wish them both well in their future endeavors". Management will be providing a strategic update to investors in the next few weeks.

Antwort auf Beitrag Nr.: 42.281.142 von Sstocktrader am 31.10.11 17:05:41Doch.

Schon ohne Erklärbär weg vom Dollar:

CDU 1,08 CAD +8,00% 289.465

CDY 1,08 USD +9,09% 137.890

Salve,

Tasche

CDU 1,08 CAD +8,00% 289.465

CDY 1,08 USD +9,09% 137.890

Salve,

Tasche

TV

Trevali Prices CDN$30.07M Underwritten Offering of Units and Flow-Through Shares

http://www.benzinga.com/pressreleases/11/10/m2079581/trevali…

Trevali Prices CDN$30.07M Underwritten Offering of Units and Flow-Through Shares

http://www.benzinga.com/pressreleases/11/10/m2079581/trevali…

Morgen

20k $ bis daher......

20k $ bis daher......

Antwort auf Beitrag Nr.: 42.284.588 von herrscher2 am 01.11.11 11:23:02

Die Dicke macht sich derzeit richtig gut.

Nur wegen der Vollstaendigkeit (und weil wir Kohle haben):

Winsway, Marubeni to Acquire Grande Cache Coal for C$1 Billion

http://www.businessweek.com/news/2011-11-01/winsway-marubeni…

BL

Nur wegen der Vollstaendigkeit (und weil wir Kohle haben):

Winsway, Marubeni to Acquire Grande Cache Coal for C$1 Billion

http://www.businessweek.com/news/2011-11-01/winsway-marubeni…

BL

Antwort auf Beitrag Nr.: 42.285.291 von boersenbrieflemming am 01.11.11 13:08:58Winsway and Marubeni are offering $9 a ton of coal reserves, which is more than the average of $2.91 a ton for comparable North American metallurgical-coal transactions, and less than the $17.86 a ton Walter paid for Western Coal, Bandy said in a note to clients.

Hier scheint noch so einiges möglich zu sein

Hier scheint noch so einiges möglich zu sein

Antwort auf Beitrag Nr.: 42.285.839 von 7911793 am 01.11.11 14:31:40

--

Balmoral Completes $4,617,250 Flow-Through Private Placement

http://www.istockanalyst.com/business/news/5512337/balmoral-…

--

Balmoral Completes $4,617,250 Flow-Through Private Placement

http://www.istockanalyst.com/business/news/5512337/balmoral-…

kleine Bullenfalle vorgestern ?

Antwort auf Beitrag Nr.: 42.288.869 von easterling am 02.11.11 06:29:54Ich denke das ist ein Papandreou-Effekt. Da war viel Panik an den Maerkten und wenn ich duerfte, dann wuerden mir hier ganz ueble Worte zu den wahrgenommenen griechischen Auffaelligkeiten einfallen.

Einmal die Schlusskurse von gestern:

CDU: 1.01 CAD -0.07 -6.5% 105.5k

CDY: 1.00 USD -0.09 -8.3% 128.3k

Ich gehe aber davon aus, dass CDU dieses Jahr noch mit Carbon Creek und Sheini

punkten wird. Die Unterbewertung ist in meinen Augen einfach zu krass und das wird der Markt ausgleichen.

BL

Einmal die Schlusskurse von gestern:

CDU: 1.01 CAD -0.07 -6.5% 105.5k

CDY: 1.00 USD -0.09 -8.3% 128.3k

Ich gehe aber davon aus, dass CDU dieses Jahr noch mit Carbon Creek und Sheini

punkten wird. Die Unterbewertung ist in meinen Augen einfach zu krass und das wird der Markt ausgleichen.

BL

Non-brokered Private Placement...

...für Carbon Creek und Sheini

...für Carbon Creek und Sheini

Cardero Arranges Non-Brokered Private Placement

VANCOUVER, BRITISH COLUMBIA -- (Marketwire) -- 11/02/11 -- Cardero Resource Corp. ("Cardero" or the "Company") (TSX: CDU)(NYSE Amex: CDY)(FRANKFURT: CR5) announces that it has arranged a non-brokered private placement of up to 5,263,158 units (the "Units") at a price of CAD 0.95 per Unit for gross proceeds of up to CAD 5,000,000 (the "Offering"). Each Unit consists of one common share of the Company ("Share") and one-half of a transferable common share purchase warrant. Each whole warrant ("Warrant") is exercisable to acquire one additional Share for a period of 12 months from closing at an exercise price of CAD 1.25. If, at any time from 4 months after closing until the expiry of the Warrants, the daily volume-weighted average trading price of the Shares on the TSX exceeds CAD 1.75 for at least 10 consecutive trading days, the Company may, within 30 days, give an expiry acceleration notice to the holders of Warrants and, if it does so, the Warrants will, unless exercised, expire on the 30th day after the expiry acceleration notice is given.

All securities issued in the Offering and any Shares issued upon exercise of Warrants will have a hold period in Canada of four months from the closing of the Offering. It is anticipated that certain insiders of the Company will participate in the Offering. The Company has determined that there are exemptions available from the various requirements of Multilateral Instrument 61-101 for the issuance of any securities issued to insiders. No new insiders will be created, nor will there be any change of control, as a result of the Offering.

The net proceeds from the Offering are intended to be used to fund work programs on the Carbon Creek Metallurgical Coal Deposit in north-eastern British Columbia and the Sheini Hills Iron Ore project in north-eastern Ghana and for general working capital.

Completion of the placement is subject to the acceptance for filing thereof by the TSX and the NYSE-A.

The foregoing securities have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the "1933 Act") or any applicable state securities laws and may not be offered or sold in the United States or to, or for the account or benefit of, U.S. persons (as defined in Regulation S under the 1933 Act) or persons in the United States absent registration or an applicable exemption from such registration requirements. This press release shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the foregoing securities in any jurisdiction in which such offer, solicitation or sale would be unlawful.

About Cardero Resource Corp.

The common shares of the Company are currently listed on the Toronto Stock Exchange (symbol CDU), the NYSE-Amex (symbol CDY) and the Frankfurt Stock Exchange (symbol CR5). For further details on the Company readers are referred to the Company's web site (www.cardero.com), Canadian regulatory filings on SEDAR at www.sedar.com and United States regulatory filings on EDGAR at www.sec.gov.

On Behalf of the Board of Directors of CARDERO RESOURCE CORP.

Hendrik van Alphen, Chief Executive Officer

Cautionary Note Regarding Forward-Looking Statements

This press release contains forward-looking statements and forward-looking information (collectively, "forward-looking statements") within the meaning of applicable Canadian and US securities legislation. All statements, other than statements of historical fact, included herein including, without limitation, statements regarding the anticipated content, commencement and cost of exploration programs, anticipated exploration program results, the discovery and delineation of mineral deposits/resources/reserves, the anticipated completion of a private placement, the anticipated use of the net proceeds of such private placement, the timing of future activities by the Company and the anticipated business plans of the Company, are forward-looking statements. Although the Company believes that such statements are reasonable, it can give no assurance that such expectations will prove to be correct. Forward-looking statements are typically identified by words such as: believe, expect, anticipate, intend, estimate, postulate and similar expressions, or are those, which, by their nature, refer to future events. The Company cautions investors that any forward-looking statements by the Company are not guarantees of future results or performance, and that actual results may differ materially from those in forward looking statements as a result of various factors, including, but not limited to, the state of the financial markets for the Company's equity securities, the state of the commodity markets generally, variations in the nature, quality and quantity of any mineral deposits that may be located, variations in the market for, and pricing of, any mineral products the Company may produce or plan to produce, the Company's inability to obtain any necessary permits, consents or authorizations required for its activities, the Company's inability to produce minerals from its properties successfully or profitably, to continue its projected growth, to raise the necessary capital or to be fully able to implement its business strategies, and other risks and uncertainties disclosed in the Company's 2011 Annual Information Form filed with certain securities commissions in Canada and the Company's annual report on Form 40-F filed with the United States Securities and Exchange Commission (the "SEC"), and other information released by the Company and filed with the appropriate regulatory agencies. All of the Company's Canadian public disclosure filings may be accessed via www.sedar.com and its United States public disclosure filings may be accessed via www.sec.gov, and readers are urged to review these materials, including the technical reports filed with respect to the Company's mineral properties.

This press release is not, and is not to be construed in any way as, an offer to buy or sell securities in the United States.

NR11-15

Contacts:

Cardero Resource Corp.

Nancy Curry

Manager - Corporate Communications & Investor Relations

1-888-770-7488 or (604) 408-7488

(604) 408-7499 (FAX)

info@cardero.com

www.cardero.com

Quelle: http://www.finanznachrichten.de/nachrichten-2011-11/21818290…

VANCOUVER, BRITISH COLUMBIA -- (Marketwire) -- 11/02/11 -- Cardero Resource Corp. ("Cardero" or the "Company") (TSX: CDU)(NYSE Amex: CDY)(FRANKFURT: CR5) announces that it has arranged a non-brokered private placement of up to 5,263,158 units (the "Units") at a price of CAD 0.95 per Unit for gross proceeds of up to CAD 5,000,000 (the "Offering"). Each Unit consists of one common share of the Company ("Share") and one-half of a transferable common share purchase warrant. Each whole warrant ("Warrant") is exercisable to acquire one additional Share for a period of 12 months from closing at an exercise price of CAD 1.25. If, at any time from 4 months after closing until the expiry of the Warrants, the daily volume-weighted average trading price of the Shares on the TSX exceeds CAD 1.75 for at least 10 consecutive trading days, the Company may, within 30 days, give an expiry acceleration notice to the holders of Warrants and, if it does so, the Warrants will, unless exercised, expire on the 30th day after the expiry acceleration notice is given.

All securities issued in the Offering and any Shares issued upon exercise of Warrants will have a hold period in Canada of four months from the closing of the Offering. It is anticipated that certain insiders of the Company will participate in the Offering. The Company has determined that there are exemptions available from the various requirements of Multilateral Instrument 61-101 for the issuance of any securities issued to insiders. No new insiders will be created, nor will there be any change of control, as a result of the Offering.

The net proceeds from the Offering are intended to be used to fund work programs on the Carbon Creek Metallurgical Coal Deposit in north-eastern British Columbia and the Sheini Hills Iron Ore project in north-eastern Ghana and for general working capital.

Completion of the placement is subject to the acceptance for filing thereof by the TSX and the NYSE-A.

The foregoing securities have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the "1933 Act") or any applicable state securities laws and may not be offered or sold in the United States or to, or for the account or benefit of, U.S. persons (as defined in Regulation S under the 1933 Act) or persons in the United States absent registration or an applicable exemption from such registration requirements. This press release shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the foregoing securities in any jurisdiction in which such offer, solicitation or sale would be unlawful.

About Cardero Resource Corp.

The common shares of the Company are currently listed on the Toronto Stock Exchange (symbol CDU), the NYSE-Amex (symbol CDY) and the Frankfurt Stock Exchange (symbol CR5). For further details on the Company readers are referred to the Company's web site (www.cardero.com), Canadian regulatory filings on SEDAR at www.sedar.com and United States regulatory filings on EDGAR at www.sec.gov.

On Behalf of the Board of Directors of CARDERO RESOURCE CORP.

Hendrik van Alphen, Chief Executive Officer

Cautionary Note Regarding Forward-Looking Statements