Tassal - australischer Lachswert (Seite 3)

eröffnet am 15.08.12 13:37:56 von

neuester Beitrag 19.07.22 12:41:39 von

neuester Beitrag 19.07.22 12:41:39 von

Beiträge: 59

ID: 1.176.177

ID: 1.176.177

Aufrufe heute: 0

Gesamt: 6.828

Gesamt: 6.828

Aktive User: 0

ISIN: AU000000TGR4 · WKN: 548233

3,2600

EUR

-1,81 %

-0,0600 EUR

Letzter Kurs 09.11.22 Tradegate

Neuigkeiten

Werte aus der Branche Nahrungsmittel

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 86.500,00 | +408,82 | |

| 5,3354 | +165,44 | |

| 5,9400 | +46,31 | |

| 0,9221 | +30,78 | |

| 71,75 | +26,43 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 10,050 | -17,54 | |

| 1,1500 | -50,00 | |

| 2,6600 | -60,88 | |

| 30,00 | -61,54 | |

| 2,8000 | -70,21 |

Beitrag zu dieser Diskussion schreiben

Antwort auf Beitrag Nr.: 52.808.920 von Lwymi am 11.07.16 19:07:40Thread: Scottish Salmon

Thread: Megatrend Aquakultur - META-Thread

Thread: Megatrend Aquakultur - META-Thread

Sehr starke Zahlen wurden heute bekannt gegeben

http://finance.nine.com.au/2017/02/22/13/29/tassal-shares-ju…

http://finance.nine.com.au/2017/02/22/13/29/tassal-shares-ju…

Antwort auf Beitrag Nr.: 53.181.936 von R-BgO am 01.09.16 11:04:10Gutes Händchen !

Antwort auf Beitrag Nr.: 52.813.372 von R-BgO am 12.07.16 10:44:52

Bei sowas nicht ungewöhnlich.

Divi minimal rauf.

Überlege, Nachzukaufen.

Zahlen kamen vor 2 Wochen,

Umsatz aufgrund der Akquisition deutlich gewachsen, Nettoergebnis minimal runter.Bei sowas nicht ungewöhnlich.

Divi minimal rauf.

Überlege, Nachzukaufen.

Antwort auf Beitrag Nr.: 52.813.372 von R-BgO am 12.07.16 10:44:52Hi R-BgO!

Danke für die Info, dann habe ich wohl keine spektakulär unterbewerteten Unternehmen aus der Peergroup übersehen.

Tassal werde ich aber weiter im Auge behalten.

Bei Scottish Salmon gibt es vermutlich auch nichts Besonderes. Meine damaligen Gründe waren die Hoffung auf eine (baldige) Übernahme und das gute Kurs/Buchwert Verhältnis. Jetzt habe ich eben doch nicht bis zur (möglichen) Übernahme ausgehalten.

Danke für die Info, dann habe ich wohl keine spektakulär unterbewerteten Unternehmen aus der Peergroup übersehen.

Tassal werde ich aber weiter im Auge behalten.

Bei Scottish Salmon gibt es vermutlich auch nichts Besonderes. Meine damaligen Gründe waren die Hoffung auf eine (baldige) Übernahme und das gute Kurs/Buchwert Verhältnis. Jetzt habe ich eben doch nicht bis zur (möglichen) Übernahme ausgehalten.

Trading Spotlight

Antwort auf Beitrag Nr.: 52.808.920 von Lwymi am 11.07.16 19:07:40

insbesondere finde ich keinerlei News zu den zugegebenermaßen spektakulären jüngsten Kurszuwächsen.

re-Seafood allgemein:

mein gewichtetes Portfolio (mit den Werten aus #31) hat -auf Basis der Zahlen des jeweils letzten abgeschlossenen Geschäftsjahres-

-ein KGV von 20,9

-ein KBV von 2,9

-eine EK-Rendite von 16,3%

der größte Einzelwert bei mir ist MH, knapp vor Oceana.

Tassal ist von den Kennzahlen her mit 12,1/1,6/15% definitiv der günstigste Wert, allerdings steht die Bekanntgabe der Zahlen per 30.6.2016 noch aus.

Und außer bei MH habe ich mir noch keinen Q1-2016 Bericht angesehen.

wie vor 2 Jahren,

verstehe ich (immer noch) nicht, was das Besondere an Scottish Salmon ist;insbesondere finde ich keinerlei News zu den zugegebenermaßen spektakulären jüngsten Kurszuwächsen.

re-Seafood allgemein:

mein gewichtetes Portfolio (mit den Werten aus #31) hat -auf Basis der Zahlen des jeweils letzten abgeschlossenen Geschäftsjahres-

-ein KGV von 20,9

-ein KBV von 2,9

-eine EK-Rendite von 16,3%

der größte Einzelwert bei mir ist MH, knapp vor Oceana.

Tassal ist von den Kennzahlen her mit 12,1/1,6/15% definitiv der günstigste Wert, allerdings steht die Bekanntgabe der Zahlen per 30.6.2016 noch aus.

Und außer bei MH habe ich mir noch keinen Q1-2016 Bericht angesehen.

Antwort auf Beitrag Nr.: 52.499.104 von R-BgO am 29.05.16 23:23:20Nachdem ich bei Tassal, Cermaq und Marine Harvest vollständig ausgestiegen war, schrieb ich am 18.07.2014 "Den Bereich Fisch decke ich derzeit [nur noch] über Scottish Salmon ab."

Aus gegebenem Anlass und da im Link von Fostr auch die Scottish Salmon erwähnt wird nutze ich dies für ein Update meiner Positionen.

Am Freitag wurde mir der steile Kursanstieg bei Scottish Salmon zu unheimlich und ich habe nun auch diese Position vollständig verkauft ... leider zu früh, wie sich heute zeigt.

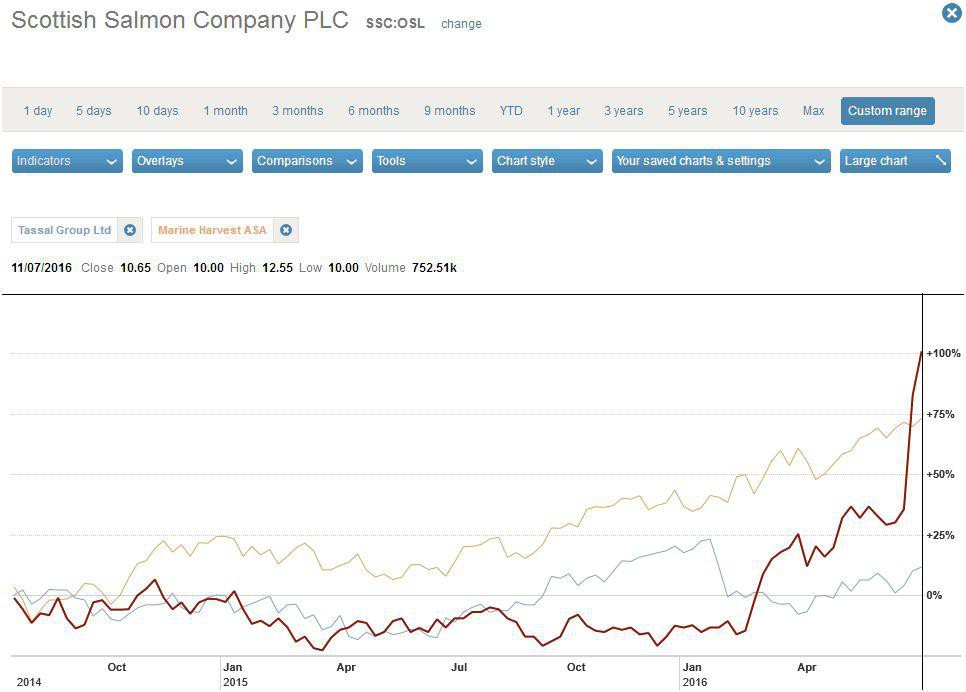

Rückblickend fällt auch auf, dass man beispielsweise mit Marine Harvest über den o.g. Zeitraum ab 18.07.2014 in etwa die gleiche Performance erzielt hätte (siehe Chart mit SSC, MHG und Tassal).

Mein "Seafood-Portfolios" ist jetzt also leer und ich bin nicht sicher, ob es sinnvoll ist nach den jahrelangen Anstiegen in der Branche länger dabei zu bleiben. Tassal scheint mir jetzt eventuell wieder der interessanteste Wert zu sein, aber ich habe mir die Zahlen in der Peergroup schon länger nicht mehr näher angesehen.

@R-BgO (und alle die sich noch angesprochen fühlen), welcher Wert aus der Peergroup erscheint derzeit am günstigsten und warum? Oder ist die gesamte Branche aktuell doch zu sportlich bewertet?

Aus gegebenem Anlass und da im Link von Fostr auch die Scottish Salmon erwähnt wird nutze ich dies für ein Update meiner Positionen.

Am Freitag wurde mir der steile Kursanstieg bei Scottish Salmon zu unheimlich und ich habe nun auch diese Position vollständig verkauft ... leider zu früh, wie sich heute zeigt.

Rückblickend fällt auch auf, dass man beispielsweise mit Marine Harvest über den o.g. Zeitraum ab 18.07.2014 in etwa die gleiche Performance erzielt hätte (siehe Chart mit SSC, MHG und Tassal).

Mein "Seafood-Portfolios" ist jetzt also leer und ich bin nicht sicher, ob es sinnvoll ist nach den jahrelangen Anstiegen in der Branche länger dabei zu bleiben. Tassal scheint mir jetzt eventuell wieder der interessanteste Wert zu sein, aber ich habe mir die Zahlen in der Peergroup schon länger nicht mehr näher angesehen.

@R-BgO (und alle die sich noch angesprochen fühlen), welcher Wert aus der Peergroup erscheint derzeit am günstigsten und warum? Oder ist die gesamte Branche aktuell doch zu sportlich bewertet?

https://www.tradingfloor.com/posts/fishing-for-returns-in-ta…

Summary

Tassal (TGR:xasx), is a class one stock and the company has a competitive edge, high barriers to entry and is a leader in the aquaculture (fisheries) industry. It delivers above average returns in a low growth global macro environment. We regard it as a hidden gem, waiting to be found with an opportunity of a 75% return in three years.

Background

Tassal (TGR) is Australia’s largest salmon producer which listed on the Australian stock exchange in 2003. Tassal Group was born from the collapse of Tassal Limited, following a restructure from the receivers, KordaMentha. After a number of successful strategic takeovers, TGR operations have grown to include hatching, farming, processing and selling Atlantic salmon.

The recent acquisition of De Costa has now expanded their market to include the seafood industry. The company share price has been growing in strength from 2012 once finishing significant capital expansion. Tassal now holds a competitive edge through economies of scale and brand recognition. At the age of 34, CEO Mark Ryan, a specialist in restructuring, corporate recovery and turnaround management, came from KordaMentha in 2003 to lead TGR. Since then, he has generated a compound share price return for shareholders of 16% + dividends per annum. With revenue and a market capitalisation over twice that of its nearest competitor, TGR is in a class of its own in the Australian market.

Industry Overview

Globally, more than 2 million tonnes of salmon are farmed annually. The industry worldwide has experienced strong growth in the last decade with CAGR of 6% from 2004–2013, while Australia at the same time grew at 10% CAGR. Norway and Chile are the world’s two largest producers, accounting for 56% and 38% of the world’s production respectively, where Australia contributes just 2%. There are three main reasons for the rise in demand for salmon in Australia. The first is increased awareness of healthy eating, the second is convenience and a preference for food that is faster and simpler to cook, and finally, the influence of Asian cuisine on Australian dining. Over the past seven years salmon consumption has almost doubled in Australia with a third of all consumers buying it weekly.

Australian salmon may look like a small fish in a big pond when compared to international producers. And it is. But it is in no way under threat from a larger player of losing market share. Australia, known for its wildlife diversity, fiercely protects its boarders from pests and disease. Quarantine and biodiversity laws do not allow the importation of live brood stock, live eggs or salmon milt. This makes competing in the fresh HOG space very restrictive and costly for international competitors.

Locally, Tasmania is the only state that is suitable for farming salmon as other state waters are too warm. Marine leases and hatchery licences are issued to industry incumbents by the state government. So not only is it financially costly to compete in the Australian salmon territory, but the high barriers to entry makes it very difficult to start a new enterprise. In such an environment, an intending player would find it easier to enter the market via a merger or acquisition than by attempting to start from scratch.

On a relative basis TGR is looking well priced. Its P/E is trading above that of other industry players. This higher P/E we believe is on a lower forecasted EPS and not over pricing the stock. We believe the market is underestimating the takeover of De Costa and that EPS will beat expectations. In addition, TGR's protected market place and growth opportunities warrants a higher P/E. Australian produce is highly regarded by our Australasia neighbours and it should not be overlooked at a large player looking to strategically partner up or buy into this world leader.

Competetive Strategy

Of the 55,000 tonnes of salmon farmed in Australia, Tassel accounts for 49% of the volume. The other major competitors being Huon (38%) and Petuna (13%). Tassal’s capital investment at the turn of the decade focused on three key areas: First was infrastructure of farming waters and in bio-assets; the second avenue has come through developing their product range to include fresh, frozen, canned and packaged salmon and; lastly the distribution network. The outcome of this investment resulted in a slew of awards being won for innovation, employer of choice and lastly, most remarkably, being named # 1 seafood provider in an international report on the world’s top 100 companies for sustainability, transparency and social responsibility. This adds to brand awareness and trust.

As the largest farmer of Atlantic salmon in Australia Tassal has economy of scale but still chooses to be selective in who it does business with. As recently as last month, the company chose to walk away from a distribution contract with Australia’s second largest supermarket chain, Coles, citing, inter alia, a need to ensure the sustainability of its stock in the long term.

Importantly, we see this move as strategic in allowing the company to not be reliant on a few large buyers . Any fish not sold can easily be exported and absorbed by the export market, admittedly at a higher cost. Supply shortages are expected in the international market over the next two years, driving prices higher. Developing a new supply chain into Asian emerging markets is a focus and growth opportunity as well.

The acquisition of De Costa Seafood has opened the company’s total target market from $700 million in salmon to now include $4.3 billion in seafood. This led to a rise in revenue of 50% in the second half of 2015. Leveraging existing operations and channels as well as stripping costs from the business, TGR is looking to increase margins on De Costa's current thinner margins. Synergies have already been recognised and we expect there are more to come as the business integration gains more traction. The company also continually invests in maximising salmon growth efficiencies, utilising selective breeding for size and reducing feed conversion ratios and bathing.

Current Situation

Tassal sold off ahead of its first half reporting on a "buy the rumour, sell the fact", following its recent acquisition. We believe the market was shortsighted in expecting business operations and synergies to be integrated within six months. We anticipate second half results to show margin improvement with further economies of scale and efficiencies to continue through to 2017. We believe management's track record of adding shareholder value affords them the trust to make good on the De Costa Seafood takeover. A discount needs to be recognised for the risks unique to farming.

TGR currently has a market capitalisation of $620m with a P/E of 11.11 and a P/B of 1.53. Its debt structure is conservative at 14% and gross dividend yield of 4.40%. According to these figures TGR is being priced as a value stock following its 2015 financial report that showed figures more closely related to a growth company:

Revenue up 50% to $226.8m

Operational EBITA up 11.2% to $41.3m

Operating cashflow up 34.9% to $25.5m

Operational NPAT up 4.7% to $19.3

Interim Dividend up 7.1% to 7.5%

Valuation

TGR will have plenty of cash to pay out to shareholders in the next few years. In addition it is key to capture the pricing of growth opportunities the company offers. Therefore we feel pricing TGR using a dividend discount model would be most appropriate.

Dividend growth in the past 3 years has been: 19%, 21% and 21%. This may very well continue at this trajectory given the protected market it operates in and the above average growth within the industry. But let’s clip the fins a little to offer room for accommodative pricing.

Anticipated dividends we’ve put forward in 2016 – 2018 are: $0.16, $0.18, and $0.20. From there an expected growth will flatten out to 5%. Given a required return of 8% the discounted cash flow model gives us a price of $7.46 in three years.

Summary

Tassal (TGR:xasx), is a class one stock and the company has a competitive edge, high barriers to entry and is a leader in the aquaculture (fisheries) industry. It delivers above average returns in a low growth global macro environment. We regard it as a hidden gem, waiting to be found with an opportunity of a 75% return in three years.

Background

Tassal (TGR) is Australia’s largest salmon producer which listed on the Australian stock exchange in 2003. Tassal Group was born from the collapse of Tassal Limited, following a restructure from the receivers, KordaMentha. After a number of successful strategic takeovers, TGR operations have grown to include hatching, farming, processing and selling Atlantic salmon.

The recent acquisition of De Costa has now expanded their market to include the seafood industry. The company share price has been growing in strength from 2012 once finishing significant capital expansion. Tassal now holds a competitive edge through economies of scale and brand recognition. At the age of 34, CEO Mark Ryan, a specialist in restructuring, corporate recovery and turnaround management, came from KordaMentha in 2003 to lead TGR. Since then, he has generated a compound share price return for shareholders of 16% + dividends per annum. With revenue and a market capitalisation over twice that of its nearest competitor, TGR is in a class of its own in the Australian market.

Industry Overview

Globally, more than 2 million tonnes of salmon are farmed annually. The industry worldwide has experienced strong growth in the last decade with CAGR of 6% from 2004–2013, while Australia at the same time grew at 10% CAGR. Norway and Chile are the world’s two largest producers, accounting for 56% and 38% of the world’s production respectively, where Australia contributes just 2%. There are three main reasons for the rise in demand for salmon in Australia. The first is increased awareness of healthy eating, the second is convenience and a preference for food that is faster and simpler to cook, and finally, the influence of Asian cuisine on Australian dining. Over the past seven years salmon consumption has almost doubled in Australia with a third of all consumers buying it weekly.

Australian salmon may look like a small fish in a big pond when compared to international producers. And it is. But it is in no way under threat from a larger player of losing market share. Australia, known for its wildlife diversity, fiercely protects its boarders from pests and disease. Quarantine and biodiversity laws do not allow the importation of live brood stock, live eggs or salmon milt. This makes competing in the fresh HOG space very restrictive and costly for international competitors.

Locally, Tasmania is the only state that is suitable for farming salmon as other state waters are too warm. Marine leases and hatchery licences are issued to industry incumbents by the state government. So not only is it financially costly to compete in the Australian salmon territory, but the high barriers to entry makes it very difficult to start a new enterprise. In such an environment, an intending player would find it easier to enter the market via a merger or acquisition than by attempting to start from scratch.

On a relative basis TGR is looking well priced. Its P/E is trading above that of other industry players. This higher P/E we believe is on a lower forecasted EPS and not over pricing the stock. We believe the market is underestimating the takeover of De Costa and that EPS will beat expectations. In addition, TGR's protected market place and growth opportunities warrants a higher P/E. Australian produce is highly regarded by our Australasia neighbours and it should not be overlooked at a large player looking to strategically partner up or buy into this world leader.

Competetive Strategy

Of the 55,000 tonnes of salmon farmed in Australia, Tassel accounts for 49% of the volume. The other major competitors being Huon (38%) and Petuna (13%). Tassal’s capital investment at the turn of the decade focused on three key areas: First was infrastructure of farming waters and in bio-assets; the second avenue has come through developing their product range to include fresh, frozen, canned and packaged salmon and; lastly the distribution network. The outcome of this investment resulted in a slew of awards being won for innovation, employer of choice and lastly, most remarkably, being named # 1 seafood provider in an international report on the world’s top 100 companies for sustainability, transparency and social responsibility. This adds to brand awareness and trust.

As the largest farmer of Atlantic salmon in Australia Tassal has economy of scale but still chooses to be selective in who it does business with. As recently as last month, the company chose to walk away from a distribution contract with Australia’s second largest supermarket chain, Coles, citing, inter alia, a need to ensure the sustainability of its stock in the long term.

Importantly, we see this move as strategic in allowing the company to not be reliant on a few large buyers . Any fish not sold can easily be exported and absorbed by the export market, admittedly at a higher cost. Supply shortages are expected in the international market over the next two years, driving prices higher. Developing a new supply chain into Asian emerging markets is a focus and growth opportunity as well.

The acquisition of De Costa Seafood has opened the company’s total target market from $700 million in salmon to now include $4.3 billion in seafood. This led to a rise in revenue of 50% in the second half of 2015. Leveraging existing operations and channels as well as stripping costs from the business, TGR is looking to increase margins on De Costa's current thinner margins. Synergies have already been recognised and we expect there are more to come as the business integration gains more traction. The company also continually invests in maximising salmon growth efficiencies, utilising selective breeding for size and reducing feed conversion ratios and bathing.

Current Situation

Tassal sold off ahead of its first half reporting on a "buy the rumour, sell the fact", following its recent acquisition. We believe the market was shortsighted in expecting business operations and synergies to be integrated within six months. We anticipate second half results to show margin improvement with further economies of scale and efficiencies to continue through to 2017. We believe management's track record of adding shareholder value affords them the trust to make good on the De Costa Seafood takeover. A discount needs to be recognised for the risks unique to farming.

TGR currently has a market capitalisation of $620m with a P/E of 11.11 and a P/B of 1.53. Its debt structure is conservative at 14% and gross dividend yield of 4.40%. According to these figures TGR is being priced as a value stock following its 2015 financial report that showed figures more closely related to a growth company:

Revenue up 50% to $226.8m

Operational EBITA up 11.2% to $41.3m

Operating cashflow up 34.9% to $25.5m

Operational NPAT up 4.7% to $19.3

Interim Dividend up 7.1% to 7.5%

Valuation

TGR will have plenty of cash to pay out to shareholders in the next few years. In addition it is key to capture the pricing of growth opportunities the company offers. Therefore we feel pricing TGR using a dividend discount model would be most appropriate.

Dividend growth in the past 3 years has been: 19%, 21% and 21%. This may very well continue at this trajectory given the protected market it operates in and the above average growth within the industry. But let’s clip the fins a little to offer room for accommodative pricing.

Anticipated dividends we’ve put forward in 2016 – 2018 are: $0.16, $0.18, and $0.20. From there an expected growth will flatten out to 5%. Given a required return of 8% the discounted cash flow model gives us a price of $7.46 in three years.

Antwort auf Beitrag Nr.: 52.499.077 von R-BgO am 29.05.16 23:17:35

halte Tassal als Teil meines Seafood-Portfolios mit den Werten

Marine Harvest

Bakkafrost

Salmar

Grieg Seafood

Austevoll

Thai Union Frozen

Ocean Group

Leroy Seafood

und Akva Group

PS:

hatte seit Threaderöffnung eine Position, zwischenzeitliche Ein- und Ausstiege sind alle gepostet;halte Tassal als Teil meines Seafood-Portfolios mit den Werten

Marine Harvest

Bakkafrost

Salmar

Grieg Seafood

Austevoll

Thai Union Frozen

Ocean Group

Leroy Seafood

und Akva Group

Antwort auf Beitrag Nr.: 52.498.483 von BuettnerIngo am 29.05.16 20:26:19

Welche Aussagen hat Fostr getroffen?

1) FK-Quote niedriger als dänische Fischfarmen

2) MarketCap <1/10 von MH

3) Kennzahlen (KGV, Divi, etc.) gut

4) Direkte Verarbeitung und Verkauf der Fische

5) Konkurrenz (Huon) schwächelt, was Tassal beflügeln sollte

6) Tassal soll "anziehen" und sich "vervielfachen"

7) bei MH ist das MK schon relativ hoch

8) Lt. CEO wird Tassal expandieren

9) "Was ich als großes Kurspotential zusätzlich sehe ist die Lage unter Japan."

10) "Mein Kursziel nächstes Jahr ist auf 10 Dollar gesetzt."

11) "Die 1 Milliarde Marktkapitalisierung sollte kein Problem sein."

12) "Tassal hat eine Marktkapitalisierung von 380 Millionen und Harvest von 6,7 Milliarden."

Dazu folgende Kommentare:

zu 1):

Tassal hatte am 31.12.2015 eine EK-Quote von 52,9%, MH eine von 45,2%; beides ist solide, aus dem Unterschied würde ich ohne weitere Analyse (=oberflächlich) erst mal nicht viel ableiten.

ABER:

*MH ist nicht etwa dänisch, sondern norwegisch (=oberflächlich)

*Bakkafrost hingegen ist dänisch, hat aber eine deutlich höhere EK-Quote von 65,8% zum gleichen Stichtag (=oberflächlich)

zu 2) & 12):

stimmt; zumindest wenn von Euro die Rede ist

zu 3):

finde den Begriff "gut" jetzt nicht gerade finanzwissenschaftlich definiert, kann mich aber insoweit anschließen, dass ich ein KGV von 12 und eine Dividendenrendite von 3,5% ok finde; MH hat übrigens 4,9% Dividende

zu 4):

bedeutet WAS genau? Alle mir bekannten Lachszüchter verarbeiten ihre Fische selbst "direkt", von Lebendverschiffung wüßte ich nix; was ich tatsächlich als Plus sehe, ist dass Tassal unter eigener Marke in den australische Supermarktregalen zu finden ist. Vergleichbares habe ich noch von keinem MH, SalMar, Austevoll, Grieg, oder Bakkafrost gefunden

zu 5):

nur vom "Schwächeln" der Konkurrenz ist noch keine Aktie beflügelt worden; und das Schwächeln wird ja vorsichtshalber auch nicht näher definiert...

was eine gewisse Wettbewerbsrelevanz haben könnte, ist das Volumen - und das hat im 2 HJ. 2015 um 57% angezogen! Wenn überhaupt, dürfte das auf die Preise drücken und schlecht für den Tassal-Kurs sein (=oberflächlich)

zu 6):

eine Behauptung im vollkommen luftleeren Raum; kein Zielkurs, keine fundamentale Begründung, kein Ziel-KGV, kein Catalyst, kein Nix (=OBERFLÄCHLICH!)

zu 7):

die "Begründung" einer relativen "Unterbewertung" im Vergleich zu MH geht so voll ins Leere; wenn schon, dann müssten Wege pro Aktie verglichen werden, MH ist nun mal auch deutlich größer;

mit dieser "Logik" könnte ich auch sagen, dass Ferrari steigen muss, weil die MK ja kleiner als bei Toyota wäre (nicht geprüft, keine Ahnung, ob das stimmt) - ohne nähere Erläuterung ausgemachter Schwachsinn

zu 8):

maybe; expandieren WIE? neue Standorte? mehr Volumen aus bestehenden Standorten? downstream? neue Produkte? ...??? (=oberflächlich)

zu 9):

keine Ahnung, was Frost "unter" Japan vermutet, meine Vermutung ist, dass sich da Lava befindet und der Zusammenhang mit Tassal erschließt sich mir nicht...

zu 10):

ENDLICH mal was Konkretes! Allerdings: das Kursziel 10 Dollar -USD? oder AUD? (=oberflächlich)- ist im ersten Falle sehr ambitioniert (x3,4) und als reine Bewertungserhöhung extrem unwahrscheinlich (steigende Gewinne werden ja nicht argumentiert) oder im zweiten Fall (x2,4) immer noch unwahrscheinlich und definitiv kein "Vervielfacher" mehr (=oberflächlich)

zu 11):

passend dazu wird das eben genannte Kursziel gleich wieder einkassiert: bei 147,2 Mio. ausstehenden Aktien komme ich auf einen Kurs von etwa 6,8 - natürlich wieder unbekannter Währung - vielleicht hat er hier ja britische Pfund gemeint.. (=oberflächlich)

reicht das?

Wenn Du wirklich neu an der Börse bist,

dann will ich mal das Offensichtliche wiederholen:Welche Aussagen hat Fostr getroffen?

1) FK-Quote niedriger als dänische Fischfarmen

2) MarketCap <1/10 von MH

3) Kennzahlen (KGV, Divi, etc.) gut

4) Direkte Verarbeitung und Verkauf der Fische

5) Konkurrenz (Huon) schwächelt, was Tassal beflügeln sollte

6) Tassal soll "anziehen" und sich "vervielfachen"

7) bei MH ist das MK schon relativ hoch

8) Lt. CEO wird Tassal expandieren

9) "Was ich als großes Kurspotential zusätzlich sehe ist die Lage unter Japan."

10) "Mein Kursziel nächstes Jahr ist auf 10 Dollar gesetzt."

11) "Die 1 Milliarde Marktkapitalisierung sollte kein Problem sein."

12) "Tassal hat eine Marktkapitalisierung von 380 Millionen und Harvest von 6,7 Milliarden."

Dazu folgende Kommentare:

zu 1):

Tassal hatte am 31.12.2015 eine EK-Quote von 52,9%, MH eine von 45,2%; beides ist solide, aus dem Unterschied würde ich ohne weitere Analyse (=oberflächlich) erst mal nicht viel ableiten.

ABER:

*MH ist nicht etwa dänisch, sondern norwegisch (=oberflächlich)

*Bakkafrost hingegen ist dänisch, hat aber eine deutlich höhere EK-Quote von 65,8% zum gleichen Stichtag (=oberflächlich)

zu 2) & 12):

stimmt; zumindest wenn von Euro die Rede ist

zu 3):

finde den Begriff "gut" jetzt nicht gerade finanzwissenschaftlich definiert, kann mich aber insoweit anschließen, dass ich ein KGV von 12 und eine Dividendenrendite von 3,5% ok finde; MH hat übrigens 4,9% Dividende

zu 4):

bedeutet WAS genau? Alle mir bekannten Lachszüchter verarbeiten ihre Fische selbst "direkt", von Lebendverschiffung wüßte ich nix; was ich tatsächlich als Plus sehe, ist dass Tassal unter eigener Marke in den australische Supermarktregalen zu finden ist. Vergleichbares habe ich noch von keinem MH, SalMar, Austevoll, Grieg, oder Bakkafrost gefunden

zu 5):

nur vom "Schwächeln" der Konkurrenz ist noch keine Aktie beflügelt worden; und das Schwächeln wird ja vorsichtshalber auch nicht näher definiert...

was eine gewisse Wettbewerbsrelevanz haben könnte, ist das Volumen - und das hat im 2 HJ. 2015 um 57% angezogen! Wenn überhaupt, dürfte das auf die Preise drücken und schlecht für den Tassal-Kurs sein (=oberflächlich)

zu 6):

eine Behauptung im vollkommen luftleeren Raum; kein Zielkurs, keine fundamentale Begründung, kein Ziel-KGV, kein Catalyst, kein Nix (=OBERFLÄCHLICH!)

zu 7):

die "Begründung" einer relativen "Unterbewertung" im Vergleich zu MH geht so voll ins Leere; wenn schon, dann müssten Wege pro Aktie verglichen werden, MH ist nun mal auch deutlich größer;

mit dieser "Logik" könnte ich auch sagen, dass Ferrari steigen muss, weil die MK ja kleiner als bei Toyota wäre (nicht geprüft, keine Ahnung, ob das stimmt) - ohne nähere Erläuterung ausgemachter Schwachsinn

zu 8):

maybe; expandieren WIE? neue Standorte? mehr Volumen aus bestehenden Standorten? downstream? neue Produkte? ...??? (=oberflächlich)

zu 9):

keine Ahnung, was Frost "unter" Japan vermutet, meine Vermutung ist, dass sich da Lava befindet und der Zusammenhang mit Tassal erschließt sich mir nicht...

zu 10):

ENDLICH mal was Konkretes! Allerdings: das Kursziel 10 Dollar -USD? oder AUD? (=oberflächlich)- ist im ersten Falle sehr ambitioniert (x3,4) und als reine Bewertungserhöhung extrem unwahrscheinlich (steigende Gewinne werden ja nicht argumentiert) oder im zweiten Fall (x2,4) immer noch unwahrscheinlich und definitiv kein "Vervielfacher" mehr (=oberflächlich)

zu 11):

passend dazu wird das eben genannte Kursziel gleich wieder einkassiert: bei 147,2 Mio. ausstehenden Aktien komme ich auf einen Kurs von etwa 6,8 - natürlich wieder unbekannter Währung - vielleicht hat er hier ja britische Pfund gemeint.. (=oberflächlich)

reicht das?