Die beste Moly-Aktie der Welt - Kobex Resources hebt gerade ab! - 500 Beiträge pro Seite (Seite 2)

eröffnet am 07.03.07 17:11:51 von

neuester Beitrag 24.11.09 16:08:38 von

neuester Beitrag 24.11.09 16:08:38 von

Beiträge: 8.529

ID: 1.117.046

ID: 1.117.046

Aufrufe heute: 0

Gesamt: 665.727

Gesamt: 665.727

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| vor 29 Minuten | 3864 | |

| vor 1 Stunde | 2327 | |

| 08.05.24, 11:56 | 1266 | |

| vor 21 Minuten | 1224 | |

| vor 10 Minuten | 883 | |

| vor 20 Minuten | 871 | |

| vor 9 Minuten | 765 | |

| vor 40 Minuten | 725 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 2. | 18.742,03 | -0,17 | 137 | |||

| 2. | 1. | 0,1965 | -9,45 | 56 | |||

| 3. | 8. | 10,900 | +5,42 | 37 | |||

| 4. | 3. | 156,86 | +0,26 | 24 | |||

| 5. | 5. | 2,3750 | +0,13 | 23 | |||

| 6. | 6. | 0,2880 | -3,36 | 20 | |||

| 7. | 4. | 0,1601 | -3,61 | 20 | |||

| 8. | 11. | 6,8140 | +0,21 | 16 |

Hab bereits 2mal Kobex gekauft, aber der Chef (Neono) schrieb - warten - vielleicht kommt Kobex bis auf 2 oder 2.10 zurück.

Ob ich das noch erwarten kann? Oder meinte der Chef Euro?

Schönen Abend

Antea

Ob ich das noch erwarten kann? Oder meinte der Chef Euro?

Schönen Abend

Antea

Antwort auf Beitrag Nr.: 28.640.417 von Neono am 03.04.07 15:24:26wieso ist denn Tenajon Resources nicht auf dieser Grafik? Sind die wohl noch genauso unbekannt und unterbewertet wie kobex das sie hier noch nichtmal auftauchen?

Haben immerhin auch ein riesiges Moly-Vorkommen mit hohen Graden

und sind von der Market-Cap her sogar noch kleiner wie kobex.

Tenajon Announces 2007 Ajax Molybdenum Drill Plans

Near Surface Higher Grade Zones to be Targeted

VANCOUVER, BRITISH COLUMBIA--(CCNMatthews - April 3, 2007) - Tenajon Resources Corp. (TSX VENTURE:TJS) (the "Company") is pleased to announce the first phase drill program has been formulated for its 100% owned Ajax Molybdenum Deposit. The program, consisting of 3,500 metres of diamond drilling, is expected to commence in June. The purpose of the program is to further define near surface high-grade mineralized zones within a potential starter pit.

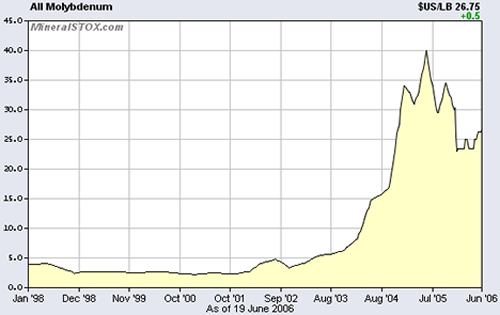

Ajax, one of North America\'s largest undeveloped molybdenum deposits, is located 14 km north of Alice Arm in northwestern British Columbia. Infrastructure in the area is very good with both tidewater access and hydro electric power situated at Kitsault 16km to the south. At a 0.040% Mo cut-off, the Ajax Deposit hosts an inferred mineral resource of 448.8 million tonnes grading 0.063% Mo (623.4 million pounds) and an indicated mineral resource of 38.8 million tonnes grading 0.064% Mo (56.4 million pounds). This resource estimate was prepared by Giroux Consultants Ltd., an independent consulting firm (released March 5, 2007). The current price for molybdenum is approximately US$30.25/lb.

Haben immerhin auch ein riesiges Moly-Vorkommen mit hohen Graden

und sind von der Market-Cap her sogar noch kleiner wie kobex.

Tenajon Announces 2007 Ajax Molybdenum Drill Plans

Near Surface Higher Grade Zones to be Targeted

VANCOUVER, BRITISH COLUMBIA--(CCNMatthews - April 3, 2007) - Tenajon Resources Corp. (TSX VENTURE:TJS) (the "Company") is pleased to announce the first phase drill program has been formulated for its 100% owned Ajax Molybdenum Deposit. The program, consisting of 3,500 metres of diamond drilling, is expected to commence in June. The purpose of the program is to further define near surface high-grade mineralized zones within a potential starter pit.

Ajax, one of North America\'s largest undeveloped molybdenum deposits, is located 14 km north of Alice Arm in northwestern British Columbia. Infrastructure in the area is very good with both tidewater access and hydro electric power situated at Kitsault 16km to the south. At a 0.040% Mo cut-off, the Ajax Deposit hosts an inferred mineral resource of 448.8 million tonnes grading 0.063% Mo (623.4 million pounds) and an indicated mineral resource of 38.8 million tonnes grading 0.064% Mo (56.4 million pounds). This resource estimate was prepared by Giroux Consultants Ltd., an independent consulting firm (released March 5, 2007). The current price for molybdenum is approximately US$30.25/lb.

Antwort auf Beitrag Nr.: 28.640.417 von Neono am 03.04.07 15:24:26....die drei von dir geposteten Grafiken lassen nur einen Schluss zu:

Kobex ist unterbewertet und Kobex sollte in keinem Molybdenum-Portfolio fehlen!

(Mist, sind 2 "Schlüsse" geworden )

)

Kobex ist unterbewertet und Kobex sollte in keinem Molybdenum-Portfolio fehlen!

(Mist, sind 2 "Schlüsse" geworden

)

)

Antwort auf Beitrag Nr.: 28.641.447 von silbernd am 03.04.07 15:58:58das kann wohl wirklich niemand ernsthat bestreiten!

Antwort auf Beitrag Nr.: 28.641.255 von nosabotas am 03.04.07 15:53:12tenajon kanst du schlecht mit kobex vergleichen.

TJS hatt ein moly gehalt von 0,04 bis 0,064% was ja lichtjahre weit weg von kobex liegt, kobex hatt 0,366% bis up to 0,7%, höher geht nimmer. TJS hatt niemals die chance im gleichen zeitrahmen wie kbx die produktion aufzunehmen und wen müsste TJS 10x soviel gestein verarbeiten um die gleiche menge moyl zu erhalten.

Da bringt auch kleinere mcap wenig, was natürlich nicht heisst das nicht auch tjs im moly hype sehr gut laufen könnte.

-------

@stompi

Das kbx noch nicht längst bei 10$ ist könnte mit dem zusammenhängen wo wir einige seiten weiter vorn schon diskutiert haben.

TJS hatt ein moly gehalt von 0,04 bis 0,064% was ja lichtjahre weit weg von kobex liegt, kobex hatt 0,366% bis up to 0,7%, höher geht nimmer. TJS hatt niemals die chance im gleichen zeitrahmen wie kbx die produktion aufzunehmen und wen müsste TJS 10x soviel gestein verarbeiten um die gleiche menge moyl zu erhalten.

Da bringt auch kleinere mcap wenig, was natürlich nicht heisst das nicht auch tjs im moly hype sehr gut laufen könnte.

-------

@stompi

Das kbx noch nicht längst bei 10$ ist könnte mit dem zusammenhängen wo wir einige seiten weiter vorn schon diskutiert haben.

Trading Spotlight

Antwort auf Beitrag Nr.: 28.641.447 von silbernd am 03.04.07 15:58:58Diese Grafiken könnten in der Tat nicht aussagekräftiger sein

Thanx Neono

darcon

Thanx Neono

darcon

Antwort auf Beitrag Nr.: 28.641.189 von Antea600 am 03.04.07 15:50:27Der Chef schreibst meistens von CAD

Ich liege selbst bei 2,02 im Bid. Sollte das 43-101 kommen, werde ich ganz schnell dort weg sein und am Ask kaufen

Neono

Ich liege selbst bei 2,02 im Bid. Sollte das 43-101 kommen, werde ich ganz schnell dort weg sein und am Ask kaufen

Neono

Antwort auf Beitrag Nr.: 28.650.342 von Neono am 03.04.07 23:26:52finde die studie leider nicht von jennings, gibts zwar viele for free dort aber nichts allegmeines zu moly gefunden.

hast du evt ein link für uns? oder falls die nicht gratis ist, was ist das fazit für kbx von jennings? gibts kursziel oder ratings?

jennings sind ja eher konservativ, für mercator haben sie erst vor tagen ein 1jahres kurziel von 5$ angegeben.

hast du evt ein link für uns? oder falls die nicht gratis ist, was ist das fazit für kbx von jennings? gibts kursziel oder ratings?

jennings sind ja eher konservativ, für mercator haben sie erst vor tagen ein 1jahres kurziel von 5$ angegeben.

habe mich mal schlau gemacht über rick rule, es gibt leider nur spärlich infos über ihn im www, doch alle bekannteren BB schreiber aus übersee reden in höchsten tönen über rick rule!

schönen dank für die info neono!

freut mich grad doppelt es dürften inzwischen gleich 2 meiner depot werte von der rick rule/casey promo maschinerie profitieren.

die uranium stock summit von d. casey, da ist auch rick rule als moderator für den uran explorer bereich, und da steht meine centram ganz oben

neono gehst du an die uranium stock summit ?

http://www.caseyresearch.com/pdfs/crLvConf.pdf

das ist übrigens die seite von rick rule: http://www.gril.net/

schönen dank für die info neono!

freut mich grad doppelt es dürften inzwischen gleich 2 meiner depot werte von der rick rule/casey promo maschinerie profitieren.

die uranium stock summit von d. casey, da ist auch rick rule als moderator für den uran explorer bereich, und da steht meine centram ganz oben

neono gehst du an die uranium stock summit ?

http://www.caseyresearch.com/pdfs/crLvConf.pdf

das ist übrigens die seite von rick rule: http://www.gril.net/

Guten Morgen!

FCB!

Wednesday, April 4, 2007

2.5 Canadian Dollar = 1.61776 Euro

FCB!

Wednesday, April 4, 2007

2.5 Canadian Dollar = 1.61776 Euro

Sprott legt los:

Blue Pearl arranges $36-million private placement

2007-04-03 20:23 ET - News Release

Mr. Wayne Cheveldayoff reports

BLUE PEARL ANNOUNCES $36 MILLION FINANCING

Blue Pearl Mining Ltd. has arranged a private placement of three million common shares at a price of $12.00 per common share to Sprott Molybdenum Participation Corp. for total proceeds of $36-million. The private placement is expected to close on April 19, 2007. Subsequent to the closing, Blue Pearl will reduce its debt (first lien credit facility) by $36-million. The private placement is subject to definitive documentation, completion of Sprott Molybdenum Participation's proposed initial public offering, and receipt of all required regulatory approvals and consents, including the approval of the Toronto Stock Exchange.

Kobex wird folgen. Vor Sprott einsteigen spart Rennerei

Neono

Blue Pearl arranges $36-million private placement

2007-04-03 20:23 ET - News Release

Mr. Wayne Cheveldayoff reports

BLUE PEARL ANNOUNCES $36 MILLION FINANCING

Blue Pearl Mining Ltd. has arranged a private placement of three million common shares at a price of $12.00 per common share to Sprott Molybdenum Participation Corp. for total proceeds of $36-million. The private placement is expected to close on April 19, 2007. Subsequent to the closing, Blue Pearl will reduce its debt (first lien credit facility) by $36-million. The private placement is subject to definitive documentation, completion of Sprott Molybdenum Participation's proposed initial public offering, and receipt of all required regulatory approvals and consents, including the approval of the Toronto Stock Exchange.

Kobex wird folgen. Vor Sprott einsteigen spart Rennerei

Neono

Antwort auf Beitrag Nr.: 28.651.980 von Neono am 04.04.07 09:03:54bei PBX auch

man beachte den preis den sie zahlen

2007-04-03 16:22 ET - Private Placement

The TSX Venture Exchange has accepted for filing documentation with respect to the first tranche of a non-brokered private placement announced March 16, 2007.

Number of shares: 13.5 million

Purchase price: 75 cents per share

Warrants: 13.5 million share purchase warrants to purchase 13.5 million shares

Warrant exercise price: 75 cents for a two-year period

Hidden placee: One

Pro group participation: Sprott Asset Management Inc., 12 million

das gab nen schub

man beachte den preis den sie zahlen

2007-04-03 16:22 ET - Private Placement

The TSX Venture Exchange has accepted for filing documentation with respect to the first tranche of a non-brokered private placement announced March 16, 2007.

Number of shares: 13.5 million

Purchase price: 75 cents per share

Warrants: 13.5 million share purchase warrants to purchase 13.5 million shares

Warrant exercise price: 75 cents for a two-year period

Hidden placee: One

Pro group participation: Sprott Asset Management Inc., 12 million

das gab nen schub

Ich habe gestern gehört, dass Sprott 500mio Dollar hätte kriegen können

Neono

Neono

Antwort auf Beitrag Nr.: 28.654.903 von Neono am 04.04.07 11:32:09

der wird uns up to da moon schicken

der wird uns up to da moon schicken

Und Sprott ist ein verdammt sicherer

Indikator für unmittelbar steigende Kurse.

Tasche

Indikator für unmittelbar steigende Kurse.

Tasche

Antwort auf Beitrag Nr.: 28.649.683 von snowflyer1 am 03.04.07 22:20:34danke snowflyer1 für deine Einschätzung!

es war aber auch garnicht meine Absicht tenajon mit kobex zu vergleichen. Mich hätte lediglich ein Vergleich mit den anderen Companys auf neonos Liste interessiert.

Denn dabei wäre herausgekommen das tenajon nach kobex mit Abstand der billigste Moly-Play ist was $Mark. Cap/lb Mo. angeht und somit auch sehr gute Chancen bietet zumal sie auch noch andere Projekte vorantreiben. Zur Diversifizierung im Moly-Bereich also hervorragend geeignet. Habe hier auch mal ein paar andere Moly-Explorer herausgesucht die sich der geneigte Moly-Investor einmal anschauen kann um sich ein eigenes Urteil zu bilden.

GVI, WRY, CYU, ROK, PBX(dürfte vielen ein Begriff sein), TCR

nun aber zurück zu unserer Perle kobex!

es war aber auch garnicht meine Absicht tenajon mit kobex zu vergleichen. Mich hätte lediglich ein Vergleich mit den anderen Companys auf neonos Liste interessiert.

Denn dabei wäre herausgekommen das tenajon nach kobex mit Abstand der billigste Moly-Play ist was $Mark. Cap/lb Mo. angeht und somit auch sehr gute Chancen bietet zumal sie auch noch andere Projekte vorantreiben. Zur Diversifizierung im Moly-Bereich also hervorragend geeignet. Habe hier auch mal ein paar andere Moly-Explorer herausgesucht die sich der geneigte Moly-Investor einmal anschauen kann um sich ein eigenes Urteil zu bilden.

GVI, WRY, CYU, ROK, PBX(dürfte vielen ein Begriff sein), TCR

nun aber zurück zu unserer Perle kobex!

gibt es irgendwo belegte direkte Kontakte von Kobex mit Sprott ??

Antwort auf Beitrag Nr.: 28.656.266 von hacho18 am 04.04.07 12:36:11sollte man warten bis es diese gibt?

Antwort auf Beitrag Nr.: 28.656.622 von e_type1 am 04.04.07 12:49:09wieso wird bei kobex soviel über Pari Kurs bezahlt, gibt's

irgendetwas besonderes seit gestern abend für ne Antwort wäre ich dankbar

irgendetwas besonderes seit gestern abend für ne Antwort wäre ich dankbar

Antwort auf Beitrag Nr.: 28.657.267 von bergsteigen am 04.04.07 13:12:57ich weiss nicht

das ask drüben ist auch sehr dünn .

das ask drüben ist auch sehr dünn .

Antwort auf Beitrag Nr.: 28.657.448 von e_type1 am 04.04.07 13:19:27danke für die antwort, kriegt man bestimmt noch viel billiger heute

Antwort auf Beitrag Nr.: 28.657.576 von bergsteigen am 04.04.07 13:24:16einige geben lieber 80 € mehr aus um sicher zu gehen nix zu verpassen .

Antwort auf Beitrag Nr.: 28.657.576 von bergsteigen am 04.04.07 13:24:16man könnte auch sagen:

man hat sie (vor Tagen ) schon viel billiger bekommen; aber es ist bestimmt noch nicht zu spät, um hier einzusteigen.

) schon viel billiger bekommen; aber es ist bestimmt noch nicht zu spät, um hier einzusteigen.

man hat sie (vor Tagen

) schon viel billiger bekommen; aber es ist bestimmt noch nicht zu spät, um hier einzusteigen.

) schon viel billiger bekommen; aber es ist bestimmt noch nicht zu spät, um hier einzusteigen.

komisch , jitney liegt drüben im bid bei 2,60....

der wird doch nicht über pari kaufen

der wird doch nicht über pari kaufen

Antwort auf Beitrag Nr.: 28.658.635 von e_type1 am 04.04.07 14:11:44kannst du das OB mal reinstellen - meins zeigt 2.46 als höchstes Gebot, muss aber nicht zwingend stimmen..

Antwort auf Beitrag Nr.: 28.659.106 von e39 am 04.04.07 14:35:24stimmt auch nicht .

12,5 k bei 2,60 im bid

12,5 k bei 2,60 im bid

weiss jemand in welchem quartal 07 ungefähr die 43-101 resourcenschätzung kommen wird ???

weiss jemand in welchem quartal 07 ungefähr die 43-101 resourcenschätzung kommen wird ???

Antwort auf Beitrag Nr.: 28.659.207 von hacho18 am 04.04.07 14:39:39Frag' nach Tagen. Das passt eher.

Antwort auf Beitrag Nr.: 28.659.200 von e_type1 am 04.04.07 14:39:18Danke, sehe aber immer noch 2.46/2.50 - nevermind, wenn's mehr ist ist mir auch recht

Antwort auf Beitrag Nr.: 28.659.517 von e39 am 04.04.07 14:52:56oh, jetzt kann ich's auch sehen 2.6/2.6...nett

Antwort auf Beitrag Nr.: 28.659.932 von e39 am 04.04.07 15:11:01Bid füllt sich nett

2,60 12500

2,51 5000

2,50 20000

2,60 9500

2,70 5100

2,75 2500

Neono

2,60 12500

2,51 5000

2,50 20000

2,60 9500

2,70 5100

2,75 2500

Neono

Antwort auf Beitrag Nr.: 28.660.018 von Neono am 04.04.07 15:14:10 Sprotti beam me up..

Sprotti beam me up..

Antwort auf Beitrag Nr.: 28.660.058 von e39 am 04.04.07 15:16:23seh ich jetzt wieder mehr Nullen als effektiv oder sind das wirklich 180000 zu 1.61 auf 1.61 95000?

Antwort auf Beitrag Nr.: 28.660.207 von e39 am 04.04.07 15:22:00korrigiere, 1.65

Antwort auf Beitrag Nr.: 28.660.207 von e39 am 04.04.07 15:22:00 1,61 ?

1,61 ?

es sind 18k 2,65 zu 9,5k 2,65

1,61 ?es sind 18k 2,65 zu 9,5k 2,65

Antwort auf Beitrag Nr.: 28.660.239 von e_type1 am 04.04.07 15:23:04ok, danke - somit wieder mein Broker Problem, eine Null zuviel..

Antwort auf Beitrag Nr.: 28.660.220 von e39 am 04.04.07 15:22:27korrigiere, 1.65

Antwort auf Beitrag Nr.: 28.659.468 von Neono am 04.04.07 14:50:25Kann man die vorhandenen Bohrkerne und die nach ursprünglichem US-Standard vorhandenen Ressourcenschätzung zu einer NI 43-101 konformen Schätzung nutzen, ohne zusätzlich zu bohren?

Gruss, Arts

Gruss, Arts

09:30:12 V 2.65 +0.15 2,500 79 CIBC 33 Canaccord K

09:30:12 V 2.65 +0.15 1,500 99 Jitney 33 Canaccord K

09:30:12 V 2.65 +0.15 10,000 99 Jitney 89 Raymond James K

09:30:12 V 2.65 +0.15 500 99 Jitney 2 RBC K

09:30:12 V 2.65 +0.15 1,500 99 Jitney 2 RBC K

09:30:12 V 2.65 +0.15 3,500 99 Jitney 15 UBS K

09:30:12 V 2.65 +0.15 1,200 99 Jitney 15 UBS K

09:30:12 V 2.65 +0.15 300 99 Jitney 1 Anonymous K

09:30:12 V 2.65 +0.15 1,200 99 Jitney 1 Anonymous K

09:30:12 V 2.65 +0.15 1,000 99 Jitney 85 Scotia K

09:30:12 V 2.65 +0.15 1,500 99 Jitney 33 Canaccord K

09:30:12 V 2.65 +0.15 10,000 99 Jitney 89 Raymond James K

09:30:12 V 2.65 +0.15 500 99 Jitney 2 RBC K

09:30:12 V 2.65 +0.15 1,500 99 Jitney 2 RBC K

09:30:12 V 2.65 +0.15 3,500 99 Jitney 15 UBS K

09:30:12 V 2.65 +0.15 1,200 99 Jitney 15 UBS K

09:30:12 V 2.65 +0.15 300 99 Jitney 1 Anonymous K

09:30:12 V 2.65 +0.15 1,200 99 Jitney 1 Anonymous K

09:30:12 V 2.65 +0.15 1,000 99 Jitney 85 Scotia K

Antwort auf Beitrag Nr.: 28.660.435 von e_type1 am 04.04.07 15:30:532.7

Antwort auf Beitrag Nr.: 28.660.435 von e_type1 am 04.04.07 15:30:53so viel zu über pari

V 2007-04-04 09:31:05 2.70 0.20 5,000 1 Anonymous 7 TD Sec K

V 2007-04-04 09:31:05 2.70 0.20 5,000 1 Anonymous 7 TD Sec K

Antwort auf Beitrag Nr.: 28.660.265 von Arts am 04.04.07 15:24:16Das glaube ich schon. Es sind 157,036 Fuss (30 Meilen) Bohrkerne aus 168 Löchern. Insdgesamt wurden schon 150mio Dollar in die Entwicklung des Projekts reingesteckt. Das hat Kobex allen anderen voraus und sollte genug Indikation für andere sein. Viel weniger werden die auch nicht brauchen, um eine Mine zu etablieren.

Neono

Neono

Antwort auf Beitrag Nr.: 28.660.458 von e_type1 am 04.04.07 15:31:51Nice, nach weniger als einem Monat sind die ersten 100% geschafft

Und sie ist immer noch ein potentieller Tenbagger

Neono

Und sie ist immer noch ein potentieller Tenbagger

Neono

Antwort auf Beitrag Nr.: 28.660.762 von Neono am 04.04.07 15:43:57auch meine 100% sind knapp voll..

Antwort auf Beitrag Nr.: 28.660.814 von e39 am 04.04.07 15:45:55ups, Danke Neono, einmal mehr..wirklich ein Prophet..(im kapitalistischen Sinne meine ich)..

bid 11k 2,71

so viel zu über pari

so viel zu über pari

Gestern noch eingestiegen.

Thanx für die zahlreichen fundierten Info’s hier im Thread

Maigret

RT 2.85

Thanx für die zahlreichen fundierten Info’s hier im Thread

Maigret

RT 2.85

Antwort auf Beitrag Nr.: 28.661.131 von Maigret am 04.04.07 15:58:43Und das Ask ist leer

2,85 1500

2,90 4500

2,97 2500

3,00 2000

3,07 2500

3,10 1500

9,00 2000

LEER

Hier kann noch jeder mit

Neono

2,85 1500

2,90 4500

2,97 2500

3,00 2000

3,07 2500

3,10 1500

9,00 2000

LEER

Hier kann noch jeder mit

Neono

2,90

Antwort auf Beitrag Nr.: 28.661.309 von Neono am 04.04.07 16:04:50Und noch hat das Rindvieh (der Markt) nichts mitbekommen

Antwort auf Beitrag Nr.: 28.661.309 von Neono am 04.04.07 16:04:50Mein erster Verdoppler seit 1998 und mein schnellster überhaupt.

Thx Neono

Thx Neono

bid jetzt 10k bei 2,90

und starke auflösungserscheinungen im ask

2.97 2,500 54 Global

3.00 2,000 89 Raymond James

3.07 2,500 54 Global

3.10 1,500 7 TD Sec

3.15 2,500 80 National Bank

9.00 2,000 6 Union

Antwort auf Beitrag Nr.: 28.661.460 von pisco am 04.04.07 16:10:25Ask bricht zusammen

10:09:36 5000 2.90 + VAN 079/074

10:08:42 2800 2.90 + VAN 059/074

10:08:42 2000 2.90 + VAN 059/006

10:08:42 1200 2.90 + VAN 059/002

10:08:42 4000 2.89 - VAN 059/007

10:04:27 1300 2.90 + VAN 033/002

2,97 2500

3,00 2000

3,07 2500

3,10 1500

9,00 2000

LEER

Neono

10:09:36 5000 2.90 + VAN 079/074

10:08:42 2800 2.90 + VAN 059/074

10:08:42 2000 2.90 + VAN 059/006

10:08:42 1200 2.90 + VAN 059/002

10:08:42 4000 2.89 - VAN 059/007

10:04:27 1300 2.90 + VAN 033/002

2,97 2500

3,00 2000

3,07 2500

3,10 1500

9,00 2000

LEER

Neono

Antwort auf Beitrag Nr.: 28.661.548 von Neono am 04.04.07 16:13:32mach du mal weiter

dann steht hier nich alles doppelt

dann steht hier nich alles doppelt

dat is ja der Hammer :O

Antwort auf Beitrag Nr.: 28.661.583 von e_type1 am 04.04.07 16:15:08Mir geht's a bisserl zu schnell. Nicht das es mich nicht erheitern würde, was heute nicht schwer ist, aber.... ich wollte selbst noch 58k haben

Neono

Neono

Antwort auf Beitrag Nr.: 28.661.685 von Neono am 04.04.07 16:19:01ja , es geht flott .

aber es steht ja auch einiges an ...viele wollen nicht mehr warten bis es "raus" ist .

aber es steht ja auch einiges an ...viele wollen nicht mehr warten bis es "raus" ist .

Antwort auf Beitrag Nr.: 28.661.733 von e_type1 am 04.04.07 16:20:41Vor allem füllt sich das Bid immer wieder

wer sind denn heute die hauptkäufer???

Antwort auf Beitrag Nr.: 28.664.432 von hacho18 am 04.04.07 18:16:54Natürlich der deutsche Makler (über house 99), um seine shorts zu covern. Alles andere ist recht gemischt. Ein bisschen GMP, PI, Canaccord, TD, BMO, CIBC, Questrade, Instinet und Anonymus.

12:15:30 500 2.70 + VAN 007/009

12:14:54 400 2.70 + VAN 007/033

12:09:33 1200 2.70 + VAN 099/033

12:09:27 1300 2.69 - VAN 079/002

12:03:00 2500 2.69 - VAN 124/001

12:02:39 1000 2.70 - VAN 007/033

12:02:39 2500 2.70 - VAN 001/033

12:02:39 900 2.71 - VAN 099/033

11:35:33 1100 2.71 - VAN 099/033

11:35:33 1600 2.74 - VAN 007/033

11:35:33 1300 2.75 + VAN 099/033

11:33:33 3700 2.75 + VAN 099/033

11:17:57 1000 2.74 - VAN 007/081

11:13:24 7400 2.74 - VAN 007/001

11:13:24 600 2.80 - VAN 079/001

11:12:57 2000 2.80 - VAN 079/085

11:03:54 1000 2.85 + VAN 007/089

11:01:09 1600 2.85 + VAN 099/089

11:01:06 300 2.85 + VAN 099/089

11:00:57 4900 2.80 + VAN 099/062

11:00:45 3000 2.79 + VAN 099/098

10:57:03 3000 2.73 - VAN 099/033

10:54:03 7000 2.73 - VAN 099/033

10:42:33 100 2.80 - VAN 013/062

10:40:03 1000 2.80 - VAN 013/033

10:38:12 1500 2.80 - VAN 013/027

10:38:00 4000 2.83 - VAN 009/033

10:35:33 1000 2.83 - VAN 009/099

10:35:12 5000 2.84 - VAN 099/098

10:30:51 2000 2.84 - VAN 099/098

10:23:45 1000 2.85 - VAN 099/062

10:16:21 5000 2.90 - VAN 074/033

10:16:21 3000 2.90 - VAN 074/007

10:13:51 7000 2.90 - VAN 074/007

10:13:18 3000 2.90 - VAN 074/001

10:13:18 5000 2.91 + VAN 009/001

10:09:36 5000 2.90 + VAN 079/074

10:08:42 2800 2.90 + VAN 059/074

10:08:42 2000 2.90 + VAN 059/006

10:08:42 1200 2.90 + VAN 059/002

10:08:42 4000 2.89 - VAN 059/007

10:04:27 1300 2.90 + VAN 033/002

10:04:03 1500 2.85 + VAN 033/005

09:55:36 5000 2.85 + VAN 001/033

09:55:12 100 2.75 + VAN 033/002

09:55:12 2400 2.75 + VAN 079/002

09:53:09 2000 2.70 + VAN 033/005

09:53:09 100 2.70 + VAN 033/007

09:42:54 100 2.65 - VAN 079/007

09:31:03 5000 2.70 + VAN 001/007

09:30:12 2500 2.65 + VAN 079/033

09:30:12 1500 2.65 + VAN 099/033

09:30:12 10000 2.65 + VAN 099/089

09:30:12 500 2.65 + VAN 099/002

09:30:12 1500 2.65 + VAN 099/002

09:30:12 3500 2.65 + VAN 099/015

09:30:12 1200 2.65 + VAN 099/015

09:30:12 300 2.65 + VAN 099/001

09:30:12 1200 2.65 + VAN 099/001

09:30:12 1000 2.65 + VAN 099/085

09:30:12 800 2.65 + VAN 099/007

09:30:12 1500 2.65 VAN 099/002

Neono

12:15:30 500 2.70 + VAN 007/009

12:14:54 400 2.70 + VAN 007/033

12:09:33 1200 2.70 + VAN 099/033

12:09:27 1300 2.69 - VAN 079/002

12:03:00 2500 2.69 - VAN 124/001

12:02:39 1000 2.70 - VAN 007/033

12:02:39 2500 2.70 - VAN 001/033

12:02:39 900 2.71 - VAN 099/033

11:35:33 1100 2.71 - VAN 099/033

11:35:33 1600 2.74 - VAN 007/033

11:35:33 1300 2.75 + VAN 099/033

11:33:33 3700 2.75 + VAN 099/033

11:17:57 1000 2.74 - VAN 007/081

11:13:24 7400 2.74 - VAN 007/001

11:13:24 600 2.80 - VAN 079/001

11:12:57 2000 2.80 - VAN 079/085

11:03:54 1000 2.85 + VAN 007/089

11:01:09 1600 2.85 + VAN 099/089

11:01:06 300 2.85 + VAN 099/089

11:00:57 4900 2.80 + VAN 099/062

11:00:45 3000 2.79 + VAN 099/098

10:57:03 3000 2.73 - VAN 099/033

10:54:03 7000 2.73 - VAN 099/033

10:42:33 100 2.80 - VAN 013/062

10:40:03 1000 2.80 - VAN 013/033

10:38:12 1500 2.80 - VAN 013/027

10:38:00 4000 2.83 - VAN 009/033

10:35:33 1000 2.83 - VAN 009/099

10:35:12 5000 2.84 - VAN 099/098

10:30:51 2000 2.84 - VAN 099/098

10:23:45 1000 2.85 - VAN 099/062

10:16:21 5000 2.90 - VAN 074/033

10:16:21 3000 2.90 - VAN 074/007

10:13:51 7000 2.90 - VAN 074/007

10:13:18 3000 2.90 - VAN 074/001

10:13:18 5000 2.91 + VAN 009/001

10:09:36 5000 2.90 + VAN 079/074

10:08:42 2800 2.90 + VAN 059/074

10:08:42 2000 2.90 + VAN 059/006

10:08:42 1200 2.90 + VAN 059/002

10:08:42 4000 2.89 - VAN 059/007

10:04:27 1300 2.90 + VAN 033/002

10:04:03 1500 2.85 + VAN 033/005

09:55:36 5000 2.85 + VAN 001/033

09:55:12 100 2.75 + VAN 033/002

09:55:12 2400 2.75 + VAN 079/002

09:53:09 2000 2.70 + VAN 033/005

09:53:09 100 2.70 + VAN 033/007

09:42:54 100 2.65 - VAN 079/007

09:31:03 5000 2.70 + VAN 001/007

09:30:12 2500 2.65 + VAN 079/033

09:30:12 1500 2.65 + VAN 099/033

09:30:12 10000 2.65 + VAN 099/089

09:30:12 500 2.65 + VAN 099/002

09:30:12 1500 2.65 + VAN 099/002

09:30:12 3500 2.65 + VAN 099/015

09:30:12 1200 2.65 + VAN 099/015

09:30:12 300 2.65 + VAN 099/001

09:30:12 1200 2.65 + VAN 099/001

09:30:12 1000 2.65 + VAN 099/085

09:30:12 800 2.65 + VAN 099/007

09:30:12 1500 2.65 VAN 099/002

Neono

Sie nimmt wieder Schung auf

12:39:12 1000 2.71 + VAN 001/007

12:39:12 1000 2.71 + VAN 001/033

12:38:54 16400 2.70 + VAN 033/001

12:33:06 5000 2.70 + VAN 033/001

12:32:21 3000 2.70 + VAN 033/001

Neono

12:39:12 1000 2.71 + VAN 001/007

12:39:12 1000 2.71 + VAN 001/033

12:38:54 16400 2.70 + VAN 033/001

12:33:06 5000 2.70 + VAN 033/001

12:32:21 3000 2.70 + VAN 033/001

Neono

Antwort auf Beitrag Nr.: 28.664.547 von Neono am 04.04.07 18:22:45danke für die info neono... - hab dir gerade ne BM gesendet

Nun gut, Geiz ist zwar geil, aber er hemmt auch manchmal.

8000 von Research Capital (083) zu 2,70

Neono

8000 von Research Capital (083) zu 2,70

Neono

Antwort auf Beitrag Nr.: 28.667.819 von Neono am 04.04.07 21:27:0615:28:06 6600 2.70 + VAN 083/001

15:27:57 1400 2.70 + VAN 083/033

15:27:57 1400 2.70 + VAN 083/033

Oder wie einfach nur der Unterschied in der Bewertung aufgeholt wird

Neono

Antwort auf Beitrag Nr.: 28.668.546 von Neono am 04.04.07 22:08:01

Antwort auf Beitrag Nr.: 28.668.546 von Neono am 04.04.07 22:08:01

Das ist eine extreme Aktie. (Bin zwar

erst dieser Tage zu 1,55 rein, aber

einen solchen run sieht man auch bei

Explorern äußerst selten nur, wobei hier

gar nichts mehr zu explorieren ist ...

Tasche

Das ist eine extreme Aktie. (Bin zwar

erst dieser Tage zu 1,55 rein, aber

einen solchen run sieht man auch bei

Explorern äußerst selten nur, wobei hier

gar nichts mehr zu explorieren ist ...

Tasche

Antwort auf Beitrag Nr.: 28.668.949 von Taschenrechner am 04.04.07 22:35:20Ich habe mir gerade mal die ersten Postings durchgelesen. Warum kommt keiner von denen und entschuldigt sich?

Kobex - die beste Molyaktie der Welt - BASTA

Neono

Kobex - die beste Molyaktie der Welt - BASTA

Neono

Antwort auf Beitrag Nr.: 28.669.317 von Neono am 04.04.07 23:05:07Gratulation Neono zu dieser Aktie wie immer du sie auch gefunden hast! Ehre wem Ehre gebührt!

Ich hoffe du entwickelst jetzt keine Star-Allüren oder hast bald deine eigene Sendung auf n-tv...

Ehre wem Ehre gebührt!Ich hoffe du entwickelst jetzt keine Star-Allüren oder hast bald deine eigene Sendung auf n-tv...

Antwort auf Beitrag Nr.: 28.669.317 von Neono am 04.04.07 23:05:07ja zur zeit machts freude stimmt!

Neono du hast die am besten funktionierende glaskugel, wie siehst du das allgemein für den rest vom 2007. (nicht speziell kobex bezogen)

Zur zeit steigen sehr viele bessere explorer auf breiter front, aktuell ist geld verdienen wieder leichter, aber solche zeiten dauern leider meist nicht ewig.

Was meinst du, kommt es im 2007 wieder so wie 2006 konso technisch?

Ich würde mal tippen die fette konso für den gesamten explorer markt kommt wieder, nur etwas zeitverzögert, sprich später als im 2006.

Wie siehst du das mit deiner doch auch schon langjährigen erfahrung?

thx

Neono du hast die am besten funktionierende glaskugel, wie siehst du das allgemein für den rest vom 2007. (nicht speziell kobex bezogen)

Zur zeit steigen sehr viele bessere explorer auf breiter front, aktuell ist geld verdienen wieder leichter, aber solche zeiten dauern leider meist nicht ewig.

Was meinst du, kommt es im 2007 wieder so wie 2006 konso technisch?

Ich würde mal tippen die fette konso für den gesamten explorer markt kommt wieder, nur etwas zeitverzögert, sprich später als im 2006.

Wie siehst du das mit deiner doch auch schon langjährigen erfahrung?

thx

Guten Morgen!

Thursday, April 5, 2007

2.75 Canadian Dollar = 1.77978 Euro

Thursday, April 5, 2007

2.75 Canadian Dollar = 1.77978 Euro

Antwort auf Beitrag Nr.: 28.669.611 von nosabotas am 04.04.07 23:39:05Ich dachte an eine Sendung auf dem Discovery Channel

snowflyer

"Stocks go up and stocks go down", sagt mein Freund Bob immer. Ich habe mit meiner langfristig angelegten Strategie die besten Erfahrungen gemacht, handle nie auf Wertpapierkredit und denke nicht kurzfristig. Von daher ist es mit egal, ob und wann ein Markt korrigiert.

Er wird korrigieren, weil es einfach nur normal ist. Bis Mitte April müssen die Amis ihre Steuern bezahlen und viele haben fette Gewinne im letzten Jahr in diesem Markt eingefahren. Bis Ende April sind die Kanadier fällig. Danach kommt das Sommerloch und die beste Zeit, um satt aufz… Da eine Korrektur nicht jede Aktie erwischt sichert man sich mit entsprechenden Derivaten ab und verkauft keine Aktien, zumal wir hier ja noch den grossen Vorteil der Spekulationsfrist haben.

Marktkorrekturen spiegeln nicht die fundamentale Situation von Unternehmen wieder.

Aber um Deine Frage zu beantworten.... spätestens Mitte Mai rumpelts wieder weltweit.

In den Links findet ihr nützliches zu diesem Thema.

Neono

snowflyer

"Stocks go up and stocks go down", sagt mein Freund Bob immer. Ich habe mit meiner langfristig angelegten Strategie die besten Erfahrungen gemacht, handle nie auf Wertpapierkredit und denke nicht kurzfristig. Von daher ist es mit egal, ob und wann ein Markt korrigiert.

Er wird korrigieren, weil es einfach nur normal ist. Bis Mitte April müssen die Amis ihre Steuern bezahlen und viele haben fette Gewinne im letzten Jahr in diesem Markt eingefahren. Bis Ende April sind die Kanadier fällig. Danach kommt das Sommerloch und die beste Zeit, um satt aufz… Da eine Korrektur nicht jede Aktie erwischt sichert man sich mit entsprechenden Derivaten ab und verkauft keine Aktien, zumal wir hier ja noch den grossen Vorteil der Spekulationsfrist haben.

Marktkorrekturen spiegeln nicht die fundamentale Situation von Unternehmen wieder.

Aber um Deine Frage zu beantworten.... spätestens Mitte Mai rumpelts wieder weltweit.

In den Links findet ihr nützliches zu diesem Thema.

Neono

Antwort auf Beitrag Nr.: 28.670.565 von Neono am 05.04.07 08:20:24Was würdest du denn zur Absicherung nehmen?

Habe mir schon ein Dax-Short-knock-out-endlos ausgesucht. Ich weiß nur noch nicht, mit welcher k.o.-Schwelle.

Oder direkt ein Put auf die Rohstoffbranche?

Habe mir schon ein Dax-Short-knock-out-endlos ausgesucht. Ich weiß nur noch nicht, mit welcher k.o.-Schwelle.

Oder direkt ein Put auf die Rohstoffbranche?

Antwort auf Beitrag Nr.: 28.670.677 von GulOcram am 05.04.07 08:35:14Dafür halte ich mir einen Broker. Der kann das besser

Antwort auf Beitrag Nr.: 28.670.565 von Neono am 05.04.07 08:20:24thanks für die ausführliche antwort!

denke auch das dein muster in etwa eintreffen wird, mit glück läufts ja noch ein bisschen länger gut, evt zieht ja der gold/uran/moly preis die nächste zeit noch schön hoch das der kurzzfristige trend noch einwenig länger so läuft wie jetzt.

wens dan rumpelt dan müssten wohl viele "unserer lieblinge" bis zu 50% einbüssen, grad auch bei uran hatts massig mikro plays mit fahnenstangenchart.

denke auch das dein muster in etwa eintreffen wird, mit glück läufts ja noch ein bisschen länger gut, evt zieht ja der gold/uran/moly preis die nächste zeit noch schön hoch das der kurzzfristige trend noch einwenig länger so läuft wie jetzt.

wens dan rumpelt dan müssten wohl viele "unserer lieblinge" bis zu 50% einbüssen, grad auch bei uran hatts massig mikro plays mit fahnenstangenchart.

Hallo Mannen!

Bin heute auch noch auf den Zug aufgesprungen..

Der Chart macht mich fertig, ich trau ihn mir gar nicht anschaun..

Ich denke die Konsolidierung bei Kobex ist unausweichlich,

es sei denn, diese Aktie setzt wirklich die physikalischen Gesetze

außer Kraft und macht einfach so noch mal 100%..

Kann ich mir nicht wirklich vorstellen,aber mal schaun..

Ich hoffe, der Markt hat erbarmen mit mir..

Viel Erfolg uns allen und schöne Ostereiertage!

Bin heute auch noch auf den Zug aufgesprungen..

Der Chart macht mich fertig, ich trau ihn mir gar nicht anschaun..

Ich denke die Konsolidierung bei Kobex ist unausweichlich,

es sei denn, diese Aktie setzt wirklich die physikalischen Gesetze

außer Kraft und macht einfach so noch mal 100%..

Kann ich mir nicht wirklich vorstellen,aber mal schaun..

Ich hoffe, der Markt hat erbarmen mit mir..

Viel Erfolg uns allen und schöne Ostereiertage!

Antwort auf Beitrag Nr.: 28.675.731 von vis-major am 05.04.07 13:13:41Wenn du so fest mit einer baldigen Konsolidierung rechnest, dann ist dein Einstiegszeitpunkt natürlich geschickt gewählt.

Antwort auf Beitrag Nr.: 28.675.890 von knisterfink am 05.04.07 13:24:35Wollte gerade genau das selbe schreiben

Antwort auf Beitrag Nr.: 28.675.890 von knisterfink am 05.04.07 13:24:35

Ich habe vor, diese Aktie 1-2 Jahre zu halten.

Auf diesen zeitlichen Horizont gesehen gehören Konsolidierungen

zum gesunden Chartbild..

Die Vergangenheit hat mich gelehrt, dass es immer einen besseren

Einstiegs-Ausstiegszeitpunkt gibt..das mag auch hier der Fall sein..

Ich stell mir diese was/wäre/wenn-Fragen nicht mehr..

so wies kommt, so kommts...

aber wenn ich nicht an dieses Unternehmen glauben würde, wäre

ich hier fehl am Platz..

Ich habe vor, diese Aktie 1-2 Jahre zu halten.

Auf diesen zeitlichen Horizont gesehen gehören Konsolidierungen

zum gesunden Chartbild..

Die Vergangenheit hat mich gelehrt, dass es immer einen besseren

Einstiegs-Ausstiegszeitpunkt gibt..das mag auch hier der Fall sein..

Ich stell mir diese was/wäre/wenn-Fragen nicht mehr..

so wies kommt, so kommts...

aber wenn ich nicht an dieses Unternehmen glauben würde, wäre

ich hier fehl am Platz..

Here we go

U.S. Energy Corp., Crested Corp. and U.S. Moly Corp. Sign Exploration, Development and Mine Operating Agreement With Kobex Resources Ltd.

2007-04-05 14:07 ET - News Release

Also News Release (U-CBAG) CRESTED CP

RIVERTON, Wyo., April 5 /PRNewswire-FirstCall/ -- U.S. Energy Corp. and Crested Corp. , natural resource exploration and development companies, are pleased to announce the signing of a definitive Exploration, Development and Mine Operating Agreement with Kobex Resources Ltd. ("Kobex"). The agreement outlines the terms under which Kobex will operate the project and earn up to a 65% interest in the project if certain terms and conditions are met.

Upon receiving TSX Venture Exchange approval of the transaction, U.S. Energy Corp. and Kobex plan to issue a comprehensive project update.

"We are pleased to have signed an operating agreement that will govern the further exploration, development and ultimate operations of the Lucky Jack molybdenum property with Kobex," stated Mark Larsen, President of U.S. Energy Corp. He added, "Kobex has been a tremendous partner to work with since signing our Amended Letter Agreement in December 2006. We look forward to continuing our work hand in hand with them and the local communities well into the future and to providing the market with a comprehensive update on the project in the near future."

Disclosure Regarding Mineral Resources

Under SEC and Canadian Regulations;

and Forward-Looking Statements

USE and Crested (the "Company") own or may come to own stock in companies which are traded on foreign exchanges, and may have agreements with some of these companies to acquire and/or develop the Company's mineral properties. Examples of these other companies are Sutter Gold Mining Inc., Uranium Power Corp., sxr Uranium One, and Kobex Resources Ltd. These other companies are subject to the reporting requirements of other jurisdictions.

United States residents are cautioned that some of the information available about our mineral properties, which is reported by the other companies in foreign jurisdictions, may be materially different from what the Company is permitted to disclose in the United States.

This news release includes statements which may constitute "forward- looking" statements, usually containing the words "believe," "estimate," "project," "expect," or similar expressions. These statements are made pursuant to the safe harbor provision of the Private Securities Litigation Reform Act of 1995. Forward-looking statements inherently involve risks and uncertainties that could cause actual results to differ materially from the forward-looking statements. Factors that would cause or contribute to such differences include, but are not limited to, future trends in mineral prices, the availability of capital, competitive factors, and other risks. By making these forward-looking statements, the Company undertakes no obligation to update these statements for revision or changes after the date of this release.

For further information on the differences between the reporting limitations of the United States, compared to reports filed in foreign jurisdictions, and also concerning forward-looking statements, please see the Company's Form 10-K ("Disclosure Regarding Forward-Looking Statements"; "Disclosure Regarding Mineral Resources under SEC and Canadian Regulation,"; and "Risk Factors"); and similar disclosures in the Company's Forms 10-Q.

Neono

U.S. Energy Corp., Crested Corp. and U.S. Moly Corp. Sign Exploration, Development and Mine Operating Agreement With Kobex Resources Ltd.

2007-04-05 14:07 ET - News Release

Also News Release (U-CBAG) CRESTED CP

RIVERTON, Wyo., April 5 /PRNewswire-FirstCall/ -- U.S. Energy Corp. and Crested Corp. , natural resource exploration and development companies, are pleased to announce the signing of a definitive Exploration, Development and Mine Operating Agreement with Kobex Resources Ltd. ("Kobex"). The agreement outlines the terms under which Kobex will operate the project and earn up to a 65% interest in the project if certain terms and conditions are met.

Upon receiving TSX Venture Exchange approval of the transaction, U.S. Energy Corp. and Kobex plan to issue a comprehensive project update.

"We are pleased to have signed an operating agreement that will govern the further exploration, development and ultimate operations of the Lucky Jack molybdenum property with Kobex," stated Mark Larsen, President of U.S. Energy Corp. He added, "Kobex has been a tremendous partner to work with since signing our Amended Letter Agreement in December 2006. We look forward to continuing our work hand in hand with them and the local communities well into the future and to providing the market with a comprehensive update on the project in the near future."

Disclosure Regarding Mineral Resources

Under SEC and Canadian Regulations;

and Forward-Looking Statements

USE and Crested (the "Company") own or may come to own stock in companies which are traded on foreign exchanges, and may have agreements with some of these companies to acquire and/or develop the Company's mineral properties. Examples of these other companies are Sutter Gold Mining Inc., Uranium Power Corp., sxr Uranium One, and Kobex Resources Ltd. These other companies are subject to the reporting requirements of other jurisdictions.

United States residents are cautioned that some of the information available about our mineral properties, which is reported by the other companies in foreign jurisdictions, may be materially different from what the Company is permitted to disclose in the United States.

This news release includes statements which may constitute "forward- looking" statements, usually containing the words "believe," "estimate," "project," "expect," or similar expressions. These statements are made pursuant to the safe harbor provision of the Private Securities Litigation Reform Act of 1995. Forward-looking statements inherently involve risks and uncertainties that could cause actual results to differ materially from the forward-looking statements. Factors that would cause or contribute to such differences include, but are not limited to, future trends in mineral prices, the availability of capital, competitive factors, and other risks. By making these forward-looking statements, the Company undertakes no obligation to update these statements for revision or changes after the date of this release.

For further information on the differences between the reporting limitations of the United States, compared to reports filed in foreign jurisdictions, and also concerning forward-looking statements, please see the Company's Form 10-K ("Disclosure Regarding Forward-Looking Statements"; "Disclosure Regarding Mineral Resources under SEC and Canadian Regulation,"; and "Risk Factors"); and similar disclosures in the Company's Forms 10-Q.

Neono

lecker und nett

Aba nicht grad der passende tag für sone News oda?

Die meisten sind doch schon im langem Osterwochenende!

Die meisten sind doch schon im langem Osterwochenende!

Damit dürfte das 43-101 nicht weit sein

Neono

Neono

Antwort auf Beitrag Nr.: 28.683.401 von Teffie am 05.04.07 20:39:48Das Rindvieh lebt und scheint die News zu mögen

14:41:27 10000 2.85 + VAN 033/089

14:37:54 2500 2.80 + VAN 074/001

14:34:33 7000 2.80 + VAN 074/081

14:34:33 5000 2.80 + VAN 074/001

14:34:33 3000 2.80 + VAN 074/001

14:34:33 1000 2.80 + VAN 074/033

14:34:33 700 2.80 + VAN 074/080

14:34:33 1000 2.80 + VAN 074/088

14:34:09 4500 2.78 + VAN 074/007

14:31:30 500 2.78 + VAN 005/007

Neono

14:41:27 10000 2.85 + VAN 033/089

14:37:54 2500 2.80 + VAN 074/001

14:34:33 7000 2.80 + VAN 074/081

14:34:33 5000 2.80 + VAN 074/001

14:34:33 3000 2.80 + VAN 074/001

14:34:33 1000 2.80 + VAN 074/033

14:34:33 700 2.80 + VAN 074/080

14:34:33 1000 2.80 + VAN 074/088

14:34:09 4500 2.78 + VAN 074/007

14:31:30 500 2.78 + VAN 005/007

Neono

Antwort auf Beitrag Nr.: 28.683.429 von Neono am 05.04.07 20:42:29Neono

07.03.07 17:11:51 opened

Neono

05.04.07 20:42:29 last post

Mein lieber Scholli, äh, Neono, das ist aber ne Ereigniskette für nen knappen Monat

07.03.07 17:11:51 opened

Neono

05.04.07 20:42:29 last post

Mein lieber Scholli, äh, Neono, das ist aber ne Ereigniskette für nen knappen Monat

Hi Neono,

wollte heute eigentlich zugreifen, habe es aber nicht durchgezogen...

Frage an Dich: Fundamental, welche Kursziele siehst Du 2007 - 2010. Vielelciht dann eben nach den Feiertagen...also auch leider nach diesen News....

Eine Antwort wäre toll!

Grüße

wollte heute eigentlich zugreifen, habe es aber nicht durchgezogen...

Frage an Dich: Fundamental, welche Kursziele siehst Du 2007 - 2010. Vielelciht dann eben nach den Feiertagen...also auch leider nach diesen News....

Eine Antwort wäre toll!

Grüße

Das sind die News von Kobex dazu....

Kobex Executes Definitive Agreement With U.S. Energy Corp., Crested Corp. and U.S. Moly Corp. For the Lucky Jack (Mt. Emmons) Project

Apr 5, 2007 2:52:00 PM

VANCOUVER, BRITISH COLUMBIA--(CCNMatthews - April 5, 2007) - Kobex Resources Ltd. ("Kobex") (TSX VENTURE:KBX) is pleased to announce the signing of a definitive Exploration, Development and Mine Operating Agreement with U.S. Energy Corp., Crested Corp. and U.S. Moly Corp. on April 3, 2007 in respect of the Lucky Jack Molybdenum Project (previously known as the Mt. Emmons Project) located near Crested Butte, Colorado, USA (the "Project"). The agreement sets out the terms that were previously announced on October 10 and December 7, 2006, with some minor amendments, whereby Kobex will operate the Project, and Kobex has the option to earn from U.S. Energy and Crested Corp., up to a 65% interest in the Project. In addition, Kobex may be required to purchase, through the issuance of up to 50% (but not 50% or greater) of the issued share capital of Kobex, 100% of the Project through a newly formed wholly owned subsidiary of U.S. Energy Corp., all upon certain terms and conditions being met.

The agreement is subject to TSX Venture Exchange approval, and upon such approval, U.S. Energy Corp. and Kobex plan to issue a comprehensive project update.

In addition Kobex has received a National Instrument 43-101 ("NI 43-101") compliant technical report dated March 23, 2007 on the Lucky Jack Project prepared by Robert Cameron, Mark A. Anderson, Ralph W. Crosser and John Reis of Behre Dolbear & Company, Inc. Dr. Cameron and Mr. Anderson are "qualified persons" as defined under NI 43-101 and independent to Kobex. Kobex plans to file this report on SEDAR upon finalizing the report with Behre Dolbear. Kobex has also retained Greenspirit Strategies Ltd. to assist in providing environmental and community relations advice in respect of the Project.

Roman Shklanka, Kobex's Chairman, commented that, "The definitive agreement and the receipt of the 43-101 report, will allow filing for Exchange approval to permit the project to move forward aggressively. We also welcome having Patrick Moore, a cofounder and former leader of Greenpeace, together with his Greenspirit team help us in our efforts to present a balanced approach of our endeavors to the local community."

"We are pleased to have signed an operating agreement that will govern the further exploration, development and ultimate operations of the Lucky Jack molybdenum property with Kobex," stated Mark Larsen, President of U.S. Energy Corp. He added, "Kobex has been a tremendous partner to work with since signing our Amended Letter Agreement in December 2006. We look forward to continuing our work hand in hand with them and the local communities well into the future and to providing the market with a comprehensive update on the project in the near future."

This news release includes certain statements that express management's expectation or estimates of future performance and may be deemed "forward-looking statements". These forward-looking statements include plans, estimates, forecasts and statements as to management's expectations concerning Kobex and its proposed acquisition of an interest in the Lucky Jack Project, including, among other things, Kobex's plans to earn a 65% interest in the Project, the requirement to purchase 100% of the Project and Kobex's plans to finalize the Behre Dolbear technical report and file it on SEDAR. These forward-looking statements involve assumptions, risks and uncertainties and actual results may vary materially. For these reasons shareholders should not place undue reliance on such forward-looking information.

United States residents are cautioned that some of the information that may be published by Kobex may not be consistent with United States Securities and Exchange Commission disclosure rules and may be materially different from what the Company is permitted to disclose in the United States and therefore United States residents should not rely on such information.

The TSX Venture Exchange has not reviewed and does not accept responsibility for the adequacy or accuracy of this News Release.

FOR FURTHER INFORMATION PLEASE CONTACT:

Kobex Resources Ltd.

Leo King

President

(604) 484-6228

Kobex Resources Ltd.

Ivan Bebek

Manager of Investor Relations

(604) 484-6228

Fax: (604) 688-9336 (FAX)

Email: investor@kobexresources.com

Website: www.kobexresources.com

Source: Kobex Resources Ltd.

Neono

Kobex Executes Definitive Agreement With U.S. Energy Corp., Crested Corp. and U.S. Moly Corp. For the Lucky Jack (Mt. Emmons) Project

Apr 5, 2007 2:52:00 PM

VANCOUVER, BRITISH COLUMBIA--(CCNMatthews - April 5, 2007) - Kobex Resources Ltd. ("Kobex") (TSX VENTURE:KBX) is pleased to announce the signing of a definitive Exploration, Development and Mine Operating Agreement with U.S. Energy Corp., Crested Corp. and U.S. Moly Corp. on April 3, 2007 in respect of the Lucky Jack Molybdenum Project (previously known as the Mt. Emmons Project) located near Crested Butte, Colorado, USA (the "Project"). The agreement sets out the terms that were previously announced on October 10 and December 7, 2006, with some minor amendments, whereby Kobex will operate the Project, and Kobex has the option to earn from U.S. Energy and Crested Corp., up to a 65% interest in the Project. In addition, Kobex may be required to purchase, through the issuance of up to 50% (but not 50% or greater) of the issued share capital of Kobex, 100% of the Project through a newly formed wholly owned subsidiary of U.S. Energy Corp., all upon certain terms and conditions being met.

The agreement is subject to TSX Venture Exchange approval, and upon such approval, U.S. Energy Corp. and Kobex plan to issue a comprehensive project update.

In addition Kobex has received a National Instrument 43-101 ("NI 43-101") compliant technical report dated March 23, 2007 on the Lucky Jack Project prepared by Robert Cameron, Mark A. Anderson, Ralph W. Crosser and John Reis of Behre Dolbear & Company, Inc. Dr. Cameron and Mr. Anderson are "qualified persons" as defined under NI 43-101 and independent to Kobex. Kobex plans to file this report on SEDAR upon finalizing the report with Behre Dolbear. Kobex has also retained Greenspirit Strategies Ltd. to assist in providing environmental and community relations advice in respect of the Project.

Roman Shklanka, Kobex's Chairman, commented that, "The definitive agreement and the receipt of the 43-101 report, will allow filing for Exchange approval to permit the project to move forward aggressively. We also welcome having Patrick Moore, a cofounder and former leader of Greenpeace, together with his Greenspirit team help us in our efforts to present a balanced approach of our endeavors to the local community."

"We are pleased to have signed an operating agreement that will govern the further exploration, development and ultimate operations of the Lucky Jack molybdenum property with Kobex," stated Mark Larsen, President of U.S. Energy Corp. He added, "Kobex has been a tremendous partner to work with since signing our Amended Letter Agreement in December 2006. We look forward to continuing our work hand in hand with them and the local communities well into the future and to providing the market with a comprehensive update on the project in the near future."

This news release includes certain statements that express management's expectation or estimates of future performance and may be deemed "forward-looking statements". These forward-looking statements include plans, estimates, forecasts and statements as to management's expectations concerning Kobex and its proposed acquisition of an interest in the Lucky Jack Project, including, among other things, Kobex's plans to earn a 65% interest in the Project, the requirement to purchase 100% of the Project and Kobex's plans to finalize the Behre Dolbear technical report and file it on SEDAR. These forward-looking statements involve assumptions, risks and uncertainties and actual results may vary materially. For these reasons shareholders should not place undue reliance on such forward-looking information.

United States residents are cautioned that some of the information that may be published by Kobex may not be consistent with United States Securities and Exchange Commission disclosure rules and may be materially different from what the Company is permitted to disclose in the United States and therefore United States residents should not rely on such information.

The TSX Venture Exchange has not reviewed and does not accept responsibility for the adequacy or accuracy of this News Release.

FOR FURTHER INFORMATION PLEASE CONTACT:

Kobex Resources Ltd.

Leo King

President

(604) 484-6228

Kobex Resources Ltd.

Ivan Bebek

Manager of Investor Relations

(604) 484-6228

Fax: (604) 688-9336 (FAX)

Email: investor@kobexresources.com

Website: www.kobexresources.com

Source: Kobex Resources Ltd.

Neono

We also welcome having Patrick Moore, a cofounder and former leader of Greenpeace, together with his Greenspirit team help us in our efforts to present a balanced approach of our endeavors to the local community."

Wink mit der Zaunlattenfabrik!

Wink mit der Zaunlattenfabrik!

Antwort auf Beitrag Nr.: 28.683.667 von Teffie am 05.04.07 21:02:44

Antwort auf Beitrag Nr.: 28.683.502 von steinbock1969 am 05.04.07 20:48:03Die Frage kann Dir so niemand beantworten, da die Antwort von zu vielen Faktoren abhängt.

Ich kann Dir aber sagen, dass Kobex meiner Ansicht nach speilend eine Marketcap von 200 - 300mio erreichen wird und, sofern es halbwegs normal läuft, noch einmal 500mio draufpacken wird. Wieviele Shares sie dann outstanding haben und was der Gesamtmarkt und/ oder der Molymarkt machen.... das weiss heute niemand.

Aktuell sind 200mio Marketcap rund 8 Dollar.

Neono

Ich kann Dir aber sagen, dass Kobex meiner Ansicht nach speilend eine Marketcap von 200 - 300mio erreichen wird und, sofern es halbwegs normal läuft, noch einmal 500mio draufpacken wird. Wieviele Shares sie dann outstanding haben und was der Gesamtmarkt und/ oder der Molymarkt machen.... das weiss heute niemand.

Aktuell sind 200mio Marketcap rund 8 Dollar.

Neono

Antwort auf Beitrag Nr.: 28.683.667 von Teffie am 05.04.07 21:02:44jetzt noch Bode Miller ins Team, dann passt das.....

Antwort auf Beitrag Nr.: 28.684.102 von Neono am 05.04.07 21:39:23BTW

Der Hauptpunkt ist aber, dass Kobex erstmal das Gap in der Bewertung zu anderen schliesst und das wird die Aktie treiben, mit steigender Bekanntheit und da sind wir gerade erst am Anfang, wenn überhaupt.

Neono

Der Hauptpunkt ist aber, dass Kobex erstmal das Gap in der Bewertung zu anderen schliesst und das wird die Aktie treiben, mit steigender Bekanntheit und da sind wir gerade erst am Anfang, wenn überhaupt.

Neono

Schöne Ostern!

Antwort auf Beitrag Nr.: 28.684.229 von Kauf am 05.04.07 21:49:32Hallo Neono,

Danke Dir!

Grüße und schöne Ostern

André

Danke Dir!

Grüße und schöne Ostern

André

Bin sprachlos was ein schönes ostergeschenk.

Schöne Ostern alle!

BinBush

Schöne Ostern alle!

BinBush

Die News von heute = `Schach`

Antwort auf Beitrag Nr.: 28.684.717 von KKCS am 05.04.07 22:27:45absolut geil

Antwort auf Beitrag Nr.: 28.684.727 von gsx1100e am 05.04.07 22:28:16...und das nur mit 180K shares. Wow..

Antwort auf Beitrag Nr.: 28.684.789 von Rastaone am 05.04.07 22:31:35das unglaubliche an kobex ist, dass es heute wieder nur höchstens ein paar "Rinder" waren (um neonos Worte aufzugreifen), die Herde scheint kobex immernoch nicht entdeckt zu haben

Thursday, April 5, 2007

3.05 Canadian Dollar = 1.97394 Euro

3.05 Canadian Dollar = 1.97394 Euro

Antwort auf Beitrag Nr.: 28.683.667 von Teffie am 05.04.07 21:02:44Perfekt!!

Wenn mir irgend etwas Kopfzerbrechen machte, dann waren es die noch einzuholenden, umweltbedingten Genehmigungen zum Betrieb der Mine.

It's all about people:

http://de.wikipedia.org/wiki/Patrick_Moore_(Umweltsch%C3%BCt…

Der schaukelt das Ding..

Frohe Ostern

Arts

Wenn mir irgend etwas Kopfzerbrechen machte, dann waren es die noch einzuholenden, umweltbedingten Genehmigungen zum Betrieb der Mine.

It's all about people:

http://de.wikipedia.org/wiki/Patrick_Moore_(Umweltsch%C3%BCt…

Der schaukelt das Ding..

Frohe Ostern

Arts

Kobex Resources Ltd. (KBX)

As of April 4th, 2007

Filing Date Transaction Date Insider Name Nature of transaction Securities # or value acquired or disposed of Unit Price

Mar 27/07 Mar 22/07 King, Herman Leo 10 - Acquisition in the public market Common Shares 5,000 $1.760

Mar 27/07 Mar 23/07 King, Herman Leo 10 - Acquisition in the public market Common Shares 25,000 $0.250

Mar 27/07 Mar 23/07 King, Herman Leo 51 - Exercise of options Options -25,000 $0.250

Mar 23/07 Mar 22/07 Shklanka, Roman 10 - Acquisition in the public market Common Shares 10,000 $1.770

Mar 23/07 Mar 22/07 Bird, Geoffrey 50 - Grant of options Common Shares 25,000 $0.250

Mar 23/07 Nov 07/97 Bird, Geoffrey 00 - Opening Balance-Initial SEDI Report Common Shares

Mar 23/07 Mar 22/07 Bird, Geoffrey 51 - Exercise of options Options -25,000

Mar 23/07 Mar 16/07 Bird, Geoffrey 50 - Grant of options Options 25,000

Mar 22/07 Mar 16/07 King, Herman Leo 50 - Grant of options Options 25,000 $1.870

Mar 21/07 Mar 16/07 Koblanski, Evan 50 - Grant of options Options 50,000 $1.870

As of April 4th, 2007

Filing Date Transaction Date Insider Name Nature of transaction Securities # or value acquired or disposed of Unit Price

Mar 27/07 Mar 22/07 King, Herman Leo 10 - Acquisition in the public market Common Shares 5,000 $1.760

Mar 27/07 Mar 23/07 King, Herman Leo 10 - Acquisition in the public market Common Shares 25,000 $0.250

Mar 27/07 Mar 23/07 King, Herman Leo 51 - Exercise of options Options -25,000 $0.250

Mar 23/07 Mar 22/07 Shklanka, Roman 10 - Acquisition in the public market Common Shares 10,000 $1.770

Mar 23/07 Mar 22/07 Bird, Geoffrey 50 - Grant of options Common Shares 25,000 $0.250

Mar 23/07 Nov 07/97 Bird, Geoffrey 00 - Opening Balance-Initial SEDI Report Common Shares

Mar 23/07 Mar 22/07 Bird, Geoffrey 51 - Exercise of options Options -25,000

Mar 23/07 Mar 16/07 Bird, Geoffrey 50 - Grant of options Options 25,000

Mar 22/07 Mar 16/07 King, Herman Leo 50 - Grant of options Options 25,000 $1.870

Mar 21/07 Mar 16/07 Koblanski, Evan 50 - Grant of options Options 50,000 $1.870

Antwort auf Beitrag Nr.: 28.685.302 von Arts am 05.04.07 23:11:36Wenn mir irgend etwas Kopfzerbrechen machte, dann waren es die noch einzuholenden, umweltbedingten Genehmigungen zum Betrieb der Mine.

Bis das überhaupt eine Rolle spielt, ist sie ein vielfaches vom heutigen Kurs wert

Neono

Bis das überhaupt eine Rolle spielt, ist sie ein vielfaches vom heutigen Kurs wert

Neono

Sehr clever uns sehr zeitig in

die richtigen Bahnhen gebracht;

der Kursverlauf: sie bleibt eine

wirklich extreme Aktie.

Tasche

die richtigen Bahnhen gebracht;

der Kursverlauf: sie bleibt eine

wirklich extreme Aktie.

Tasche

Antwort auf Beitrag Nr.: 28.685.302 von Arts am 05.04.07 23:11:36das sie moore ins boot holen zeigt das sie das diese problematik sehr ernst nehmen, man darf sich schonmal auf das umfangreiche update das angekündet wurde freuen.

Kobex wird in einigen jahren eine mcap von 1milliarde oder sonst halt 10mio haben, es gibt kein dazwischen.

1 milliarde wäre nicht soo abwegig wies ertmal klingt, den 400-500mio$ pro jahr könnte man locker mit ner 8000t mill einnehmen bei diesen moly gehalten.

Kobex wird in einigen jahren eine mcap von 1milliarde oder sonst halt 10mio haben, es gibt kein dazwischen.

1 milliarde wäre nicht soo abwegig wies ertmal klingt, den 400-500mio$ pro jahr könnte man locker mit ner 8000t mill einnehmen bei diesen moly gehalten.

Guten Morgen

Vor den News:

Nach den News:

Frohe Ostern meine Lieben!

Neono

Vor den News:

Nach den News:

Frohe Ostern meine Lieben!

Neono

Short History

Symbol Report Date Volume Change

KBX - V 2007-03-31 20,000 -45,000

Symbol Report Date Volume Change

KBX - V 2007-03-31 20,000 -45,000

sind die börsen in kanada am montag geöffnet?

ich wünsche auch allen frohe ostern

mit kobex haben wir uns ja schon ein dickes ei ins nest gelegt

Antwort auf Beitrag Nr.: 28.686.579 von e_type1 am 06.04.07 11:05:54Yep, ich nenne sie ein extremes

(goldenes sowieso) "Ei".

Tasche

(goldenes sowieso) "Ei".

Tasche

Aging Energy Infrastructure Could Drive Molybdenum Demand Hi…

March 4, 2007

By James Finch

Corrosion Factor to Keep Molybdenum Price High

Corrosion’s impact on a gas pipeline. Courtesy of CC Technologies

As long as air conditioners keep us cool in the summer and central heating warms us in the winter, all is well in the world. In order to keep this gas and electricity continuously flowing into our homes, molybdenum has emerged as an essential metal to help preserve a challenging energy transportation network. The anti-corrosive qualities found in molybdenum could also help prevent the collapse of the U.S. energy infrastructure.

Tucked beneath our streets, farms, deserts and forests lays a multi-million mile network of mostly aging pipelines supplying our energy needs. Meanwhile, hydrogen sulphide, carbon dioxide and common oxygen corrode the energy transportation system we rely upon to fuel our cars and power our computers. Corrosion annually costs the U.S. economy about $276 billion, more than three percent of the GDP, according to Technology Today (Spring 2005).

Unacceptably high percentages of two key energy-providing vehicles, such as nuclear power plants and the U.S. pipeline network, have begun aging beyond their original design life. About half of the nation’s 2.4 million miles of oil and gas pipelines were built in the 1950s and 1960s. And the composition of the liquids flowing through those pipelines has deteriorated over the past half century.

According the U.S. Department of Transportation’s Pipeline and Hazardous Materials Safety Administration (PHMSA) website, “Corrosion is one of the most prevalent causes of pipeline spills or failures. For the period 2002 through 2003, incidents attributable to corrosion have represented 25 percent of the incidents reported to the Office of Pipeline Safety for both Natural Gas Transmission Pipelines and Hazardous Liquid Transmission Pipelines.” Industry sources note corrosion is also a leading cause of pipeline leaks and ruptures.

Corroded Prudhoe Bay Pipeline Rupture

Arctic Temperatures can help accelerate pipeline corrosion. Courtesy of BP.

Corrosion makes each of us vulnerable to price shocks. On August 7th, public awareness about the impact of corroded pipelines in the energy infrastructure registered when prices shot up at the gasoline pump. BP shut down about eight percent of U.S. oil production. The international oil company cited ‘unexpectedly severe corrosion’ in its Alaska oil pipelines. This was the first shutdown ever in America’s biggest oil fields. According to BP, sixteen anomalies were discovered in twelve separate locations on the eastern side of the oil field. Earlier in the year, a pipeline spill was reported from the western side of the field.

Immediately following the corroded pipeline rupture, the industry introduced legislation, hoping to prevent a recurrence. Signed into law in December, the Pipeline, Inspection, Protection and Enforcement and Safety Act, affected low-stress crude oil pipelines, and included provisions for the improved controls and detection of pipeline corrosion. During Senate committee hearings, trade representatives pointed to the Department of Transportation’s Integrity Management program, implemented in 2001 and which was reported to have demonstrated a reduction of leaks and releases resulting from corrosion from high-stress inter-state gas pipelines in ‘high consequence areas.’

Natural Gas Market Centers – U.S. trading and transshipment points. Courtesy of EIA.

Official statistics published by the PHMSA Office of Pipeline Safety disagree. In the twenty-year period of 1986 to 2006, 2883 incidents resulting in 1467 injuries, 349 fatalities and nearly $860 million of property damage were reported by distribution operators at U.S. natural gas pipelines. In the five-year period ending in 2006, 25 percent of the incidents, about 20 percent of the fatalities, nearly 19 percent of the injuries and more than 69 percent of the property damage occurred compared to the previous fifteen years, before legislation was enacted. Similar percentages were reported by natural gas transmission operators.

Faced with aging, out-dated infrastructure, the pipeline industry aimed legislation toward the lowest-cost solution – detection of corrosion and piecemeal pipeline replacement – rather than addressing the separate issues which led to the problem.

Older Pipeline Steels Vulnerable to Corrosion

Pipeline corrosion and pitting are one of the greatest dangers to the U.S. energy infrastructure. Courtesy of CC Technologies.

During its massive build up phase, U.S. pipeline infrastructure relied upon carbon and low-alloy steels for natural gas and petroleum transportation. As oil fields have aged, the risk of pipeline corrosion and pitting has increased. The Prudhoe Bay oilfield now produces more water than oil. This is a common occurrence in numerous U.S. oil fields and around the globe.

In the absence of water, hydrogen sulphide is non-corrosive to pipelines. However, increased moisture in pipelines is problematic, because it activates the corrosive capabilities of hydrogen sulphide. A combination of tensile stress, susceptibility of low-alloy steels and chemical corrosion will lead to sulfide stress cracking. Hydrogen ions weaken the steel. Over time, pressure causes the embrittled steel in the pipeline to rupture.

Similar problems have emerged in the natural gas sector. As deeper wells are drilled in hot, high-pressure gas deposits, the probability of hydrogen sulphide in gas can increase. An entire industry has sprung up around decontaminating sour gas. U.S. sulfur production from gas processing plants accounts for about 15 percent of the total U.S. production of sulfur.

Sour gas is a naturally occurring gas containing more than one per cent hydrogen sulphide (H2S) and sometimes above 25 percent. It is typically identifiable by a strong ‘rotten eggs’ smell. Commonly found in the foothills of western Canada’s Rocky Mountain region, sour gas comprises more than one-third of the gas produced in Alberta. It is ‘sweetened’ at more than 200 plants in this province to bring the gas up to pipeline quality.

The one-to-two percent of the H2S remaining in the gas is considered pipeline quality. But the interaction of the hydrogen sulphide with water can accelerate the pipeline corrosion process. Potentially, the combination of the old gas pipeline material and the rise of sour gas could pose the greatest risk to gas pipeline safety. Molybdenum is crucial in defending against hydrogen sulfide environments as reported in a metallurgical journal study and published by the Defense Technical Information Center.

High Strength Low Alloy Steels

Large diameter pipelines transporting natural gas require high strength low alloy steels with substantial quantities of molybdenum. Courtesy of International Molybdenum Association (IMOA).

Long running cracks, some stretching more than six miles, first began fracturing gas pipelines in the 1960s. The industry’s solution was the development of, and encouragement to use, High Strength Low Alloy (HSLA) steels. Older pipelines, built in the 1920s (or earlier), of 500mm or less, could only handle an operating pressure of about 20 bar. Annual capacity of gas transportation for those pipelines stood at about 650 million or less. Because of today’s high energy content of compressed gas at 80 to 100 bar and an annual transportation capacity of 26,000 million or more, pipelines require modern HSLA steel to prevent brittle fracture behavior or ductile cracks.

HSLA steels capable of building large diameter pipes came about from the introduction of the thermomechanical rolling process in the 1970s, which maximized grain refinement. By increasing the strength of the steels, one could sustain the high operating pressure and reduce the wall thickness of the pipe. Steel manufacturers could use less steel, reduce the pipe weight and double the yield strength. Transportation costs from plate and pipe mills to construction sites were also reduced. Delivering a lighter-weight pipe to remote or arctic areas became more economical.

Steel is vulnerable to acids and is generally stable with pH values above 7. Acidity-causing corrosion comes about when magnesium and calcium are hydrolytically converted to form hydrochloric acid. Hydrogen sulphide and carbon dioxide are also acid-forming gases corroding steel. Molybdenum’s corrosive-resistant properties has grown beyond its original scope in manufacturing modern steel, which was to harden steel.

Initially, molybdenum was included to harden steel and increase weldability, while reducing the carbon content previously utilized. Higher toughness, but lower tensile strength, was required. By adding molybdenum in the range of 0.15 to 0.30 percent, depending upon the pipe wall’s thickness, carbon content in the steel could be reduced to 0.07 percent. The metal has played a key factor in oil and gas development projects as pipes continue being used in arctic, sour and sub-sea environments. Apparently, the more rugged the climate, the better the more recent gas projects have panned out. One example would be the Sakhalin oil and gas project in Russia’s Far East, where on- and off-shore pipelines in excess of 1,000 miles would transport some of the world’s largest natural gas reserves.

Steels for natural gas pipelines require higher standards than those used for oil. These pipelines must carry compressed gas at minus 25 degrees centigrade to minus 4 degrees centigrade. Crack growth and brittleness intensify in the severe arctic environment. Achieving low-temperature notch toughness, grain size control, and low sulfur content were some of the problems solved while developing this modern steel.

Since the 1970s, more than two million tons of molybdenum-containing HSLA steels for pipelines were manufactured. We checked with the world’s largest pipeline manufacturer Tenaris (NYSE: TS), which offers steel with high resistance to Sulphide Stress Corrosion Cracking (SSCC), to confirm continued interest in molybdenum. In a phone call to the company’s Houston office, we discovered the company had purchased $65 million of ferromolybdenum in the six-month period ending January 31, 2007 for use in its new pipeline steels. As an aside, the company representative, having checked with company’s central purchasing ‘sister company’ in Argentina, pointed to the rising cost of ferromolybdenum and anticipated paying $80 kg in the coming year. (This could help explain why the moly price has remained high through 2006 and could rise higher in 2007.)

Pipeline Projects on the Horizon Confirm Moly Demand

We talked with Rita Tubbs, managing editor of Pipeline and Gas Journal (P&GJ), about molybdenum content to be used in the construction of gas pipelines outside of the United States. “Most will adhere to the standards used in North America,” she told us. According to Adanac Molybdenum Corp consultant, Ken Reser, the new standard has grown to 0.5 percent moly content.

In a December 2006 worldwide pipeline construction survey, compiled by Rita Tubbs, she observed “81,593 miles of new and planned oil and gas pipelines under construction and planned.” She pointed out North American pipeline construction plans nearly doubled to 28,314 miles. In these figures, Tubbs spotlighted Canadian activity, which is expected to increase overall North American pipeline construction mileage. She wrote, “By 2008, contractors expect to see a workload that has not been seen in Canada for nearly three decades.”

Tubbs explained in her report, “Much of the activity will be generated by the massive oil production that will come from the oil sands in northern Alberta which contain the largest deposits of hydrocarbons on earth. Terasen and Enbridge plan to move oil sands by pipeline.” Molybdenum is likely to play a vital role in pipelines carrying the material, which is a mixture of sand bitumen and water – with high sulphur content.

An unexpected addition to the P&GJ report came on February 26th. Shanghai Daily newspaper reported a boom for China’s energy pipelines. The world’s most populous country plans to add another 15,000 miles of oil and gas pipelines to its existing infrastructure of 24,000 miles by 2010. In three years, the country hopes to extend its mileage by nearly 63 percent as China races to raise its energy mix for gas to 10 percent.

Perhaps the greatest number of new pipeline growth will occur in the United States – the world’s largest energy consumer. By 2025 EIA expects the US will need 47 percent more oil and 54 percent more natural gas. To transport this energy, transmission and distribution line mileage is expect to increase by approximately 30 percent. This implies pipeline projects on the order of some 600,000 miles.

Whether this would include the nearly one million pipeline miles sorely in need of replacement since the introduction of molybdenum in the 1970s to the steel in pipes is not known. However, whether one calculates the number of new pipeline miles potentially constructed or the number of replacement pipeline miles, one arrives at a staggering quantity of molybdenum required to more strongly protect the steel from future corrosion.

Depending upon the diameter of the pipe, wall thickness and environment, each pipeline mile could require between 600 and 1000 pounds of molybdenum. About one-half of the U.S. oil and gas pipeline network could call for replacement. In the United States alone, and solely to upgrade the out-dated portion of America’s pipelines, more than 300 million and as many as one billion pounds of molybdenum could potentially be required. While this should be considered a speculative extrapolation, based upon available data, it may not be that far off the mark. Pipelines aged more than thirty or forty years could very well be replaced before 2020. Chemical changes in the material passing through U.S. pipelines could accelerate pipeline corrosion. Based upon future natural gas incidents, future legislation could hasten the remediation process of America’s energy transportation infrastructure.

By comparison, the number of new pipeline constructions now on the books might require between 50 and 100 million pounds. This could be upwardly revised as the rest of the world, especially Russia and Europe, suffer from the similar aging pipeline problems found in the United States.

Molybdenum: Old and New Infrastructure

Type 316L piping at the Minneapolis Water Works membrane filtration plant. Courtesy of Dale A. Folen, City of Minneapolis and the International Molybdenum Association.