Spectrum Pharmaceuticals - Chancen und Risiken? - 500 Beiträge pro Seite (Seite 9)

eröffnet am 31.08.08 11:55:05 von

neuester Beitrag 10.08.23 11:06:43 von

neuester Beitrag 10.08.23 11:06:43 von

Beiträge: 4.229

ID: 1.143.896

ID: 1.143.896

Aufrufe heute: 0

Gesamt: 285.526

Gesamt: 285.526

Aktive User: 0

ISIN: US84763A1088 · WKN: 164623 · Symbol: NTR

0,8910

EUR

+4,97 %

+0,0450 EUR

Letzter Kurs 31.07.23 Tradegate

Neuigkeiten

20.07.23 · Business Wire (engl.) |

30.06.23 · Business Wire (engl.) |

17.05.23 · Business Wire (engl.) |

09.05.23 · Business Wire (engl.) |

Werte aus der Branche Pharmaindustrie

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,2000 | +471,16 | |

| 13,110 | +38,44 | |

| 1,2100 | +21,00 | |

| 27,50 | +19,57 | |

| 4,4900 | +19,10 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,6400 | -18,81 | |

| 1,4500 | -20,55 | |

| 36,70 | -22,87 | |

| 2,3450 | -25,32 | |

| 15,600 | -31,64 |

hörst du die konferenz?

2012 war ganz gut, melphalan ist wieder ein inder....

scheint jedenfalls auch nix zu bewirken, die kommen nicht ausm Start...

2012 war ganz gut, melphalan ist wieder ein inder....

scheint jedenfalls auch nix zu bewirken, die kommen nicht ausm Start...

immerhin läuft danz gute mucke am schluss....

and wie immer: Stay tuned, the best is yet to come.....

and wie immer: Stay tuned, the best is yet to come.....

Antwort auf Beitrag Nr.: 47.256.688 von Ville7 am 03.07.14 18:12:35

Hi Ville,

Last Exit Brooklyn?

Ich meine vielleicht sollte man Spectrum jetzt einfach verkaufen und vergessen? Sind immerhin fast bei 7 + Dollargewinn....

Vanville

Zitat von Ville7: Belinostat Zulassung kostet Spectrum erst mal 25Mio USD. Deswegen feiert die Börse die Zulassung auch nicht. Auch Melphalan würde mit 30Mio USD und sehr sehr hohen Royalties erst mal sehr teuer bis es etwas abwirft.

Warten wir jetzt auf Melphalan. Sicherheitsdaten wollte man hierzu aus irgendwelchen Gründen ja noch nicht veröffentlichen.

Hi Ville,

Last Exit Brooklyn?

Ich meine vielleicht sollte man Spectrum jetzt einfach verkaufen und vergessen? Sind immerhin fast bei 7 + Dollargewinn....

Vanville

Antwort auf Beitrag Nr.: 49.791.003 von vanville am 16.05.15 20:07:25PS.: der Übernahme Müll geht nie auf. Niemand will sicherlich diese Firma kaufen.

Trading Spotlight

hallo,

mal eine vollaive frage in die runde

vermarktet Spectrum Zevalin im moment in den USA?

und wenn -wie läuft das, mit welchem erfolg?

Danke.

P.

mal eine vollaive frage in die runde

vermarktet Spectrum Zevalin im moment in den USA?

und wenn -wie läuft das, mit welchem erfolg?

Danke.

P.

Hilft dir das weiter? Kommt aus dem letzten Q-Bericht -> http://investor.sppirx.com/secfiling.cfm?filingID=831547-15-…

Antwort auf Beitrag Nr.: 49.924.077 von Tommi33 am 06.06.15 15:06:44Pledge to reduce training from 700 to 80hrs for zevalin administration:

http://pbadupws.nrc.gov/docs/ML1514/ML15149A509.pdf

http://pbadupws.nrc.gov/docs/ML1514/ML15149A509.pdf

Antwort auf Beitrag Nr.: 49.990.110 von vanville am 17.06.15 10:25:34Alle raus?

Antwort auf Beitrag Nr.: 49.322.486 von VaJo am 13.03.15 15:42:11Man könnte wieder einsteigen, was meinst?

bin wieder drin, lass mich von raj überraschen.

Ich habe noch welche von 4,80 EUR/Stück. Rest ist weg. Sind nur wenige, aber ganz ohne SPPI gehts bei mir auch nicht

Antwort auf Beitrag Nr.: 51.372.609 von VaJo am 28.12.15 09:23:31Habs aufegeben. Steuerfrei hin oder her. Vermutlich irgendwann wieder für 90 cents zu haben.

Vanville

Vanville

Warum hast du aufgegeben wenn man fragen darf?

Langjährig dahindümpelnd. Nun 52Wochenhoch und es scheint big money sich mehr und mehr zu positionieren. Kein Wunder, denn es stehen 2018 mit eflapegrastim ( Rolontis) und poziotinib in exon20 NSCLC zwei möglicherweise transformierende Ereignisse an. Da kann selbst das gierige und inkompetente Management möglicherweise höhere Kurse nicht verhindern. Dennoch hohes Risiko, denn die Studien werden von SPPI oftmals underpowered gefahren. Zudem wird vom Management ständig ein viel zu rosiges Bild gezeichnet, daher eine Historie von shareholder lawsuits, und nebenbei unverschämt sich selbst Optionen zugeteilt...

Zu ESMO 2017 gibt es die Ergebnisse zu der koreanischen Phase 2 Studie von poziotinib in HER-2 positive breast cancer.

Breast cancer, metastatic

Proffered Paper session

ESMO 2017 Congress, 09.09.2017, 11:00 - 12:30, Madrid Auditorium

237O - A phase II trial of pan-HER inhibitor Poziotinib, in patients with HER2-positive metastatic breast cancer who have received at least two prior HER2-directed regimens: The results of NOV120101-203 trial.

Um diesen trial geht es:

https://clinicaltrials.gov/ct2/show/NCT02418689?term=NOV1201…

Man darf gespannt sein, wie sehr Raj mal wieder seine Klappe gestopft bekommt nach all der Pusherei von poziotinib in dieser Indikation ("60% response rate" auf Basis von nur 10 Patienten)....

Breast cancer, metastatic

Proffered Paper session

ESMO 2017 Congress, 09.09.2017, 11:00 - 12:30, Madrid Auditorium

237O - A phase II trial of pan-HER inhibitor Poziotinib, in patients with HER2-positive metastatic breast cancer who have received at least two prior HER2-directed regimens: The results of NOV120101-203 trial.

Um diesen trial geht es:

https://clinicaltrials.gov/ct2/show/NCT02418689?term=NOV1201…

Man darf gespannt sein, wie sehr Raj mal wieder seine Klappe gestopft bekommt nach all der Pusherei von poziotinib in dieser Indikation ("60% response rate" auf Basis von nur 10 Patienten)....

Allzu schlecht können die Daten aber nicht sein... aus der ESMO Defintion der Präsentationskategorien:

Proffered Paper – Oral presentations by authors presenting original data of superior quality, followed by expert discussion and perspectives.

-----

Also SPPI Aktien mal festhalten und nicht verkaufen. 2018f könnte payday (bzgl. Kursen) sein...

Proffered Paper – Oral presentations by authors presenting original data of superior quality, followed by expert discussion and perspectives.

-----

Also SPPI Aktien mal festhalten und nicht verkaufen. 2018f könnte payday (bzgl. Kursen) sein...

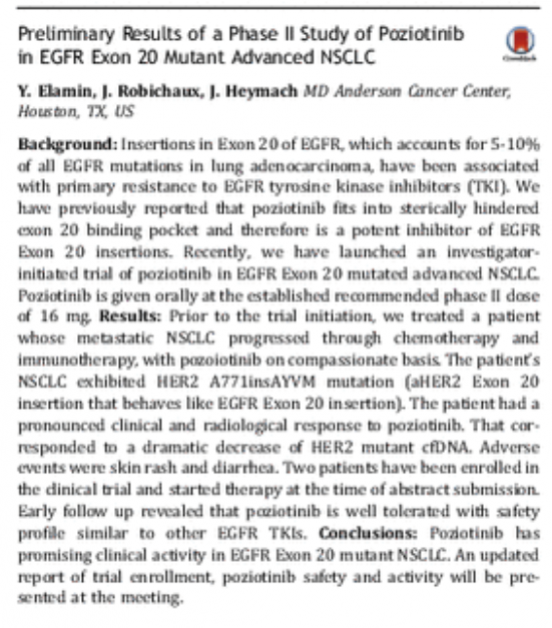

Journal of Thoracic Oncology - August 2017Volume 12, Issue 8, Supplement, Page S1536

Preliminary Results of a Phase II Study of Poziotinib in EGFR Exon 20 Mutant Advanced NSCLC

SPPI Announces Completion of Enrollment in the Phase 3 Pivotal Study (ADVANCE) of ROLONTIS™ (eflapegrastim)

Nachrichtenquelle: Business Wire (engl.) | 01.08.2017, 13:00 Spectrum Pharmaceuticals, Inc. (NasdaqGS: SPPI), a biotechnology company with fully integrated commercial and drug development operations with a primary focus in Hematology and Oncology, announced today the Company has completed enrollment with 405 patients randomized in the ROLONTIS Phase 3 ADVANCE pivotal study under a Special Protocol Assessment (SPA) with the Food and Drug Administration. The study is evaluating the safety and efficacy of ROLONTIS in the management of chemotherapy-induced neutropenia in patients with breast cancer.

“I am pleased to report that we have been able to complete enrollment in the ADVANCE study ahead of schedule,” said Rajesh C. Shrotriya, MD, Chairman and Chief Executive Officer of Spectrum Pharmaceuticals. “We plan to announce topline data early next year and expect to file a BLA in 2018. RECOVER, the second Phase 3 study for ROLONTIS, is a smaller study that will include sites in the U.S. and Europe, and is currently enrolling patients. RECOVER will leverage established relationships with U.S. sites from the ADVANCE study to help expedite enrollment. We believe ROLONTIS, if approved by the FDA, has the opportunity to change the growth trajectory of our Company because it targets a multi-billion dollar market and our team has a deep knowledge and understanding of the space. We are excited to be in the final stages of what could be a transformational development for the Company.”

Spectrum is conducting a second Phase 3 study, RECOVER, which is a multicenter, randomized, active-controlled study similar in design to the ADVANCE study that is currently enrolling in the U.S. and Europe. This study will enroll approximately 218 early-stage breast cancer patients, who will receive adjuvant or neoadjuvant TC (docetaxel and cyclophosphamide) chemotherapy every 21 days for up to 4 cycles. Adjuvant chemotherapy is treatment given after primary surgical therapy to kill any remaining cancer cells and increase the chance of long-term, disease-free survival; neoadjuvant chemotherapy is the administration of cytotoxic agents before surgical resection in early-stage breast cancer to help shrink the tumor and potentially allow for breast-conserving surgery. The primary study endpoint is the Duration of Severe Neutropenia (Absolute Neutrophil Counts [ANC] <0.5×109/L) in Cycle 1 of chemotherapy, based on central laboratory assessment of ANC over the 21 day cycle. Secondary endpoints include the incidence of neutropenic complications, incidence of febrile neutropenia, relative dose intensity, and safety.

Spectrum Pharmaceuticals Announces Completion of Enrollment in the Phase 3 Pivotal Study (ADVANCE) of ROLONTIS™ (eflapegrastim), a Novel Long-Acting GCSF | wallstreet-online.de -

Vollständiger Artikel unter:

https://www.wallstreet-online.de/nachricht/9786714-spectrum-…

Erste Daten ("initital clinical data") zum NSCLC exon 20 (HER/EGRF) Trial in mit poziotinib sind in 71 Tagen hier zu erwarten ("oral presetantion"):

http://wclc2017.iaslc.org/

findet vom 15.-18.Oktober 2017 in Yokohama statt.

June 21, 2017

Abstract Submission Deadline

July 26, 2017

Abstract Notifications

August 4, 2017

Early Registration Deadline

August 31, 2017

Regular Registration & Housing Deadline

August 31, 2017

Late Breaking Abstract Submission Deadline

http://wclc2017.iaslc.org/

findet vom 15.-18.Oktober 2017 in Yokohama statt.

June 21, 2017

Abstract Submission Deadline

July 26, 2017

Abstract Notifications

August 4, 2017

Early Registration Deadline

August 31, 2017

Regular Registration & Housing Deadline

August 31, 2017

Late Breaking Abstract Submission Deadline

August 3, 2017

Spectrum Pharmaceuticals Reports Second Quarter 2017 Financial Results and Pipeline Update

ROLONTIS™ (eflapegrastim):

BLA filing expected next year.

Enrollment completed in registrational ADVANCE Study under a Special Protocol Assessment (SPA) with the FDA. Topline results expected in Q1 2018.

A second smaller study RECOVER is enrolling patients in EU and U.S. Enrollment completion expected in Q1 2018.

Poziotinib:

Interim results are expected before year end from an ongoing Phase 2 study in non-small cell lung cancer patients with exon 20 insertion mutations in EGFR or HER2. This study is being conducted at The University of Texas MD Anderson Cancer Center.

Following discussions with the FDA, the Company is initiating an additional multicenter clinical trial to expedite the development of poziotinib in this patient population.

Financials:

Q2 revenues were $34.3 million, including $31.2 million in product sales.

FOLOTYN® (pralatrexate injection) was recently approved in Japan and the Company expects multiple related milestone payments totaling approximately $5 million from Mundipharma in the second half of the year.

HENDERSON, Nev.--(BUSINESS WIRE)-- Spectrum Pharmaceuticals, Inc. (NasdaqGS: SPPI), a biotechnology company with fully integrated commercial and drug development operations with a primary focus in Hematology and Oncology, announced today financial results for the three-month period ended June 30, 2017.

"During the second quarter we made significant progress in our highest priority clinical programs and achieved solid performance across our commercial business," said Rajesh C. Shrotriya, MD, Chairman and Chief Executive Officer of Spectrum Pharmaceuticals. "We completed enrollment in ROLONTIS's ADVANCE registrational Phase 3 study ahead of schedule and enrollment in a second international study RECOVER is well under way in Europe and U.S. We are also very excited about the prospects of poziotinib in cancer patients with exon 20 insertion mutations and expect interim results from the Phase 2 lung cancer study before the end of the year. We are driven to bring our novel drugs to patients with unmet medical needs and look forward to multiple near-term development catalysts that could shape the Company's future."

Pipeline Update:

ROLONTIS (eflapegrastim), a novel long-acting GCSF: A registrational Phase 3 study ADVANCE was initiated under an SPA with the FDA last year to evaluate ROLONTIS in the management of chemotherapy-induced neutropenia. The Company has completed enrollment in the ADVANCE study with 405 patients randomized and expects to report topline data in Q1 2018. To strengthen the regulatory package in the Europe and U.S., the Company is currently enrolling the 218-patient international RECOVER study. The Company continues to expect to file the BLA next year.

Poziotinib, a potential best-in-class, novel, pan-HER inhibitor: An investigator sponsored trial is currently enrolling at the University of Texas MD Anderson Cancer Center in non-small cell lung cancer patients with exon 20 insertion mutations in EGFR or HER2. The study is expected to yield interim results before year end. Following discussions with the FDA, the Company is initiating an additional multicenter study in a similar patient population. Spectrum is also conducting a Phase 2 breast cancer study in the third-line setting in the U.S., based on promising Phase 1 study efficacy data in breast cancer patients who had failed multiple HER2-directed therapies. The Company is in discussions with the FDA about a combination trial of poziotinib and standard of care therapy in HER2+ breast cancer patients in the second-line setting.

QAPZOLA™, a potent tumor-activated drug for bladder cancer is being investigated for low and intermediate risk non-muscle invasive bladder cancer: The Company has an SPA from the FDA for a new Phase 3 study incorporating learnings from the previous studies, as well as recommendations from the FDA. Compared to the previous program, this new Phase 3 study will include fewer evaluable patients (n=425 versus 1,557 patients), use a higher dosage of QAPZOLA (8 mg versus 4 mg), and will evaluate time-to-recurrence as the primary endpoint. Approximately 50 sites have been selected thus far for enrolling patients in the Phase 3 study and patients are currently being screened.

Three-Month Period Ended June 30, 2017 (All numbers are approximate)

GAAP Results

Total product sales were $31.2 million in the second quarter of 2017. Product sales in the second quarter included: FUSILEV® (levoleucovorin) net sales of $2.1 million, FOLOTYN® (pralatrexate injection) net sales of $11.2 million, ZEVALIN® (ibritumomab tiuxetan) net sales of $2.3 million, MARQIBO® (vinCRIStine sulfate LIPOSOME injection) net sales of $2.2 million, BELEODAQ® (belinostat) for injection net sales of $3.4 million, and EVOMELA® (melphalan) for injection net sales of $10.1 million.

Spectrum recorded a net loss of $20.5 million, or $0.26 per basic and diluted share in the three-month period ended June 30, 2017, compared to a net loss of $24.3 million, or $0.35 per basic and diluted share in the comparable period in 2016. Total research and development expenses were $15.1 million in the quarter, as compared to $14.3 million in the same period in 2016. Selling, general and administrative expenses were $17.1 million in the quarter, compared to $27.6 million in the same period in 2016.

Our June 30, 2017 cash and equivalents balance is $138.6 million. In July 2017, we sold and issued 3.2 million shares of our common stock for net proceeds of $23.7 million under our ATM. These shares and proceeds are not included in our June 30, 2017 financial statements. We have now fully utilized the ATM facility.

Non-GAAP Results

Spectrum recorded non-GAAP net loss of $8.6 million, or $0.11 per basic and diluted share in the three-month period ended June 30, 2017, compared to non-GAAP net loss of $3.7 million, or $0.05 per basic share and diluted share in the comparable period in 2016. Non-GAAP research and development expenses were $14.6 million, as compared to $12.9 million in the same period of 2016. Non-GAAP selling, general and administrative expenses were $14.5 million, as compared to $16.1 million in the same period in 2016

Spectrum Pharmaceuticals Reports Second Quarter 2017 Financial Results and Pipeline Update

ROLONTIS™ (eflapegrastim):

BLA filing expected next year.

Enrollment completed in registrational ADVANCE Study under a Special Protocol Assessment (SPA) with the FDA. Topline results expected in Q1 2018.

A second smaller study RECOVER is enrolling patients in EU and U.S. Enrollment completion expected in Q1 2018.

Poziotinib:

Interim results are expected before year end from an ongoing Phase 2 study in non-small cell lung cancer patients with exon 20 insertion mutations in EGFR or HER2. This study is being conducted at The University of Texas MD Anderson Cancer Center.

Following discussions with the FDA, the Company is initiating an additional multicenter clinical trial to expedite the development of poziotinib in this patient population.

Financials:

Q2 revenues were $34.3 million, including $31.2 million in product sales.

FOLOTYN® (pralatrexate injection) was recently approved in Japan and the Company expects multiple related milestone payments totaling approximately $5 million from Mundipharma in the second half of the year.

HENDERSON, Nev.--(BUSINESS WIRE)-- Spectrum Pharmaceuticals, Inc. (NasdaqGS: SPPI), a biotechnology company with fully integrated commercial and drug development operations with a primary focus in Hematology and Oncology, announced today financial results for the three-month period ended June 30, 2017.

"During the second quarter we made significant progress in our highest priority clinical programs and achieved solid performance across our commercial business," said Rajesh C. Shrotriya, MD, Chairman and Chief Executive Officer of Spectrum Pharmaceuticals. "We completed enrollment in ROLONTIS's ADVANCE registrational Phase 3 study ahead of schedule and enrollment in a second international study RECOVER is well under way in Europe and U.S. We are also very excited about the prospects of poziotinib in cancer patients with exon 20 insertion mutations and expect interim results from the Phase 2 lung cancer study before the end of the year. We are driven to bring our novel drugs to patients with unmet medical needs and look forward to multiple near-term development catalysts that could shape the Company's future."

Pipeline Update:

ROLONTIS (eflapegrastim), a novel long-acting GCSF: A registrational Phase 3 study ADVANCE was initiated under an SPA with the FDA last year to evaluate ROLONTIS in the management of chemotherapy-induced neutropenia. The Company has completed enrollment in the ADVANCE study with 405 patients randomized and expects to report topline data in Q1 2018. To strengthen the regulatory package in the Europe and U.S., the Company is currently enrolling the 218-patient international RECOVER study. The Company continues to expect to file the BLA next year.

Poziotinib, a potential best-in-class, novel, pan-HER inhibitor: An investigator sponsored trial is currently enrolling at the University of Texas MD Anderson Cancer Center in non-small cell lung cancer patients with exon 20 insertion mutations in EGFR or HER2. The study is expected to yield interim results before year end. Following discussions with the FDA, the Company is initiating an additional multicenter study in a similar patient population. Spectrum is also conducting a Phase 2 breast cancer study in the third-line setting in the U.S., based on promising Phase 1 study efficacy data in breast cancer patients who had failed multiple HER2-directed therapies. The Company is in discussions with the FDA about a combination trial of poziotinib and standard of care therapy in HER2+ breast cancer patients in the second-line setting.

QAPZOLA™, a potent tumor-activated drug for bladder cancer is being investigated for low and intermediate risk non-muscle invasive bladder cancer: The Company has an SPA from the FDA for a new Phase 3 study incorporating learnings from the previous studies, as well as recommendations from the FDA. Compared to the previous program, this new Phase 3 study will include fewer evaluable patients (n=425 versus 1,557 patients), use a higher dosage of QAPZOLA (8 mg versus 4 mg), and will evaluate time-to-recurrence as the primary endpoint. Approximately 50 sites have been selected thus far for enrolling patients in the Phase 3 study and patients are currently being screened.

Three-Month Period Ended June 30, 2017 (All numbers are approximate)

GAAP Results

Total product sales were $31.2 million in the second quarter of 2017. Product sales in the second quarter included: FUSILEV® (levoleucovorin) net sales of $2.1 million, FOLOTYN® (pralatrexate injection) net sales of $11.2 million, ZEVALIN® (ibritumomab tiuxetan) net sales of $2.3 million, MARQIBO® (vinCRIStine sulfate LIPOSOME injection) net sales of $2.2 million, BELEODAQ® (belinostat) for injection net sales of $3.4 million, and EVOMELA® (melphalan) for injection net sales of $10.1 million.

Spectrum recorded a net loss of $20.5 million, or $0.26 per basic and diluted share in the three-month period ended June 30, 2017, compared to a net loss of $24.3 million, or $0.35 per basic and diluted share in the comparable period in 2016. Total research and development expenses were $15.1 million in the quarter, as compared to $14.3 million in the same period in 2016. Selling, general and administrative expenses were $17.1 million in the quarter, compared to $27.6 million in the same period in 2016.

Our June 30, 2017 cash and equivalents balance is $138.6 million. In July 2017, we sold and issued 3.2 million shares of our common stock for net proceeds of $23.7 million under our ATM. These shares and proceeds are not included in our June 30, 2017 financial statements. We have now fully utilized the ATM facility.

Non-GAAP Results

Spectrum recorded non-GAAP net loss of $8.6 million, or $0.11 per basic and diluted share in the three-month period ended June 30, 2017, compared to non-GAAP net loss of $3.7 million, or $0.05 per basic share and diluted share in the comparable period in 2016. Non-GAAP research and development expenses were $14.6 million, as compared to $12.9 million in the same period of 2016. Non-GAAP selling, general and administrative expenses were $14.5 million, as compared to $16.1 million in the same period in 2016

Cash-Situation: Ende Q2 2017: $138.6 million + Verwässerung $23.7 million im Juli 2017 = ca. $160 million

Cashburn je Quartal ca. $20 million

Firma wird versuchen Cashbestand stets über $100-$120 million zu belassen (wegen debt, das 2018 fällig ist). D.h. weitere Verwässerungen absehbar.

Cashburn je Quartal ca. $20 million

Firma wird versuchen Cashbestand stets über $100-$120 million zu belassen (wegen debt, das 2018 fällig ist). D.h. weitere Verwässerungen absehbar.

expected newsflow ( (c) Ville ):

2017-09-09 11:00 - 12:30: poziotinib Hanmi Her2 BC trial "proffered paper" presentation at http://www.esmo.org/Conferences/ESMO-2017-Congress in Madrid2017-10-15 - 2017-10-18: pozitinib EGFR/HER exon20 single agent "initial clinical data" from MD Anderson trial at http://wclc2017.iaslc.org/ in Yokohama

Q3 2017: Start ROLONTIS RECOVER trial (218 patients)

Q3 2017: Start QAPZOLA trial 8mg 2:1 (425 patients)

Q3 2017: Start SPPI sponsored multicenter trial pozitinib EGFR/HER exon20 single agent

Q1 2018: Enrollment completion for ROLONTIS RECOVER trial

Q1 2018: Topline Data for ROLONTIS ADVANCE trial (405 patients)

Q1 2018: Try to get "breakthrough designation" for pozitinib in EGFR/HER exon20 NSCLC on basis of MD Anderson trial

Q2 2018: Data for ROLONTIS ADVANCE trial at ASCO

Q3 2018: Topline Data for ROLONTIS RECOVER trial

Q4 2018: File BLA for ROLONTIS on basis of ADVANCE and RECOVER

> +20% heute, wahrscheinlich eine Menge Momentum ab jetzt bis in 2018 rein und keiner dabei

...so gefällt mir das.

Antwort auf Beitrag Nr.: 55.458.294 von Ville7 am 04.08.17 12:27:01Meine älteste Depotleiche erwacht zu neuen Leben, nach Jahren steh ich sogar wieder im Plus

Daran hätte ich ja selber kaum mehr gedcht

Was genau steht im Bericht, dass wir so steigen? Hab irgendwie nicht mal mehr Lust das selber zu lesen, die Aktie war mir so egal. Vielleicht ändert sich das ja bald.

Daran hätte ich ja selber kaum mehr gedcht

Was genau steht im Bericht, dass wir so steigen? Hab irgendwie nicht mal mehr Lust das selber zu lesen, die Aktie war mir so egal. Vielleicht ändert sich das ja bald.

123fly, es wird sich ändern...tut es ja auch schon seit Monaten. big money positioniert sich hier bereits, da es vielleicht hier was zu holen gibt...

Im September ist m.E. bereits zweistellig möglich - Stichwort ESMO 2017. Wenn alles gut geht nächstes Jahr noch weit höher.

Spectrum hat mit poziotinib einen potentiellen Winner im Depot, der nächstes Jahr breakthrough therapy status bekommen könnte - für exon 20 Mutationen in Lungenkrebs. Zudem wird Hamni auf ESMO 2017 Anfang September wahrscheinlich hervorragende Daten von poziotinib in Brustkrebs präsentieren - die Präsentationskategorie ist mit "proffered paper" die zweithöchst mögliche und die gibts nur bei hervoragenden Daten. Dazu noch Rolontis. Also in 2019 könnte Spectrum zwei Medikamente auf den Markt bringen, jedes davon mit Pontential von mehreren 100 Millionen USD im Peak. Wenn das so kommt ist eine Bewertung der Börse wie aktuell natürlich viel zu niedrig.

Kann mich aber wie immer auch irren. Wir werden sehen...

Im September ist m.E. bereits zweistellig möglich - Stichwort ESMO 2017. Wenn alles gut geht nächstes Jahr noch weit höher.

Spectrum hat mit poziotinib einen potentiellen Winner im Depot, der nächstes Jahr breakthrough therapy status bekommen könnte - für exon 20 Mutationen in Lungenkrebs. Zudem wird Hamni auf ESMO 2017 Anfang September wahrscheinlich hervorragende Daten von poziotinib in Brustkrebs präsentieren - die Präsentationskategorie ist mit "proffered paper" die zweithöchst mögliche und die gibts nur bei hervoragenden Daten. Dazu noch Rolontis. Also in 2019 könnte Spectrum zwei Medikamente auf den Markt bringen, jedes davon mit Pontential von mehreren 100 Millionen USD im Peak. Wenn das so kommt ist eine Bewertung der Börse wie aktuell natürlich viel zu niedrig.

Kann mich aber wie immer auch irren. Wir werden sehen...

Antwort auf Beitrag Nr.: 55.460.226 von Ville7 am 04.08.17 16:23:46Hallo Ville7

Danke für die hilfreiche Antwort. Bin auch überhaupt noch dabei, weil ich bei Kauf die Pipeline vielversprechend fand. In erster Linie SPPI2012. Bin aber im Nachhinein zu früh eingestiegen. Habe aber die Firma gar nicht mehr aktiv verfolgt, da beim Tiefpunkt um die 3 Dollar ich faktisch nur noch mit relativ wenig drin war.

Ist denn poziotinib der vermarktete Name von SPPI2012?

Danke für die hilfreiche Antwort. Bin auch überhaupt noch dabei, weil ich bei Kauf die Pipeline vielversprechend fand. In erster Linie SPPI2012. Bin aber im Nachhinein zu früh eingestiegen. Habe aber die Firma gar nicht mehr aktiv verfolgt, da beim Tiefpunkt um die 3 Dollar ich faktisch nur noch mit relativ wenig drin war.

Ist denn poziotinib der vermarktete Name von SPPI2012?

Antwort auf Beitrag Nr.: 55.460.322 von 123fly am 04.08.17 16:31:37Nein, SPI-2012 heißt inzwischen ROLONTIS.

Kann man hier noch einsteigen? Was meint ihr?

Antwort auf Beitrag Nr.: 55.472.496 von abgemeldet-577022 am 07.08.17 13:04:52Wenn du an die Pipeline glaubst und vorallem Rolontis das in naher Zukunft Daten liefern wird dann schon. Das Risiko besteht natürlich immer ich bin seit 2013 dabei und nun zum ersten Mal leicht im Plus.

Geduld bringt oft Rosen doch nicht immer das Risiko ist hier höher als mit einem Pharma Multi doch die Chancen auch viel grösser.

Falls es in dein Depot passt und du das Geld nicht zwingend brauchst kannst ja mit einer kleinen Posi rein.

Versteht sich nicht als Kaufempfehlung

Viel Erfolg

Geduld bringt oft Rosen doch nicht immer das Risiko ist hier höher als mit einem Pharma Multi doch die Chancen auch viel grösser.

Falls es in dein Depot passt und du das Geld nicht zwingend brauchst kannst ja mit einer kleinen Posi rein.

Versteht sich nicht als Kaufempfehlung

Viel Erfolg

Poziotinib Non Small Cell Lung Cancer exon 20 Mutationen: 9 Patienten sind im MD Anderson Trial inzwischen behandelt, zwei wurden zusätzlich über "compassionate use" behandelt (weil sie nicht in die Inklusionsbedingungen der Studie gepasst hätten). Beide "compassionate use" Patienten haben scheinbar angesprochen. Das wissen wir erstens aus den SPPI Calls (der erste Patient nun bereits 9 Monate stable disease, die zweite Patientin ist die Frau des Threaderöffners des nachfolgenden Patiententreads - dort sind ihre Berichte nachlesbar, id Anne121259):

https://www.inspire.com/groups/american-lung-association-lun…

Nun hat sich eine weitere Patientin zu Wort gemeldet (sie ist im trial) - sehr ermutigend:

Lili123

yesterday at 6:07 pm

Hello everybody, I am on Poziotinib in clinical trial at MD Anderson. sharing my expirience there:

It's my third week on this drug. NSCLC, exon 20 in EGFR, stage 4, no distant mets. I am 54 years old. Had chemo Carboplatin and Alimta in 2015, stable disease, then slow grow on Ct scans.

Had a lot of congestion in my chest, coughing out foam sputum. After day 2 my chest congestion has gone completely! I couldn't believe it .... so fast. My oxygen numbers went from 86 (I was on home oxygen) to 89-90, and one week later to 92-94!

I can breath now... Doctor wanted to do CT scan right away but we decided to wait until the one on schedule.

My side effects are nasty, however: rash on my face, itching scalp . My face is all red, and itching and burning.

Never mind, I can breath!!!

I will keep you posted,

Best of luck to everybody.

https://www.inspire.com/groups/american-lung-association-lun…

Nun hat sich eine weitere Patientin zu Wort gemeldet (sie ist im trial) - sehr ermutigend:

Lili123

yesterday at 6:07 pm

Hello everybody, I am on Poziotinib in clinical trial at MD Anderson. sharing my expirience there:

It's my third week on this drug. NSCLC, exon 20 in EGFR, stage 4, no distant mets. I am 54 years old. Had chemo Carboplatin and Alimta in 2015, stable disease, then slow grow on Ct scans.

Had a lot of congestion in my chest, coughing out foam sputum. After day 2 my chest congestion has gone completely! I couldn't believe it .... so fast. My oxygen numbers went from 86 (I was on home oxygen) to 89-90, and one week later to 92-94!

I can breath now... Doctor wanted to do CT scan right away but we decided to wait until the one on schedule.

My side effects are nasty, however: rash on my face, itching scalp . My face is all red, and itching and burning.

Never mind, I can breath!!!

I will keep you posted,

Best of luck to everybody.

Antwort auf Beitrag Nr.: 55.460.226 von Ville7 am 04.08.17 16:23:46

Es ist September und wir sind zweistellig. Ich spekuliere auf die USD20 nächstes Jahr, falls sowohl poziotinib in exon-20 NSCLC als auch Rolontis gute Topline Daten liefern. Fundamental wäre das dann gerechtfertigt...

Zitat von Ville7: Im September ist m.E. bereits zweistellig möglich - Stichwort ESMO 2017. Wenn alles gut geht nächstes Jahr noch weit höher.

Es ist September und wir sind zweistellig. Ich spekuliere auf die USD20 nächstes Jahr, falls sowohl poziotinib in exon-20 NSCLC als auch Rolontis gute Topline Daten liefern. Fundamental wäre das dann gerechtfertigt...

Hi ville,

Sollen das die neuen Ergebnisse vom ESMO sein?:

http://www.esmo.org/content/download/117241/2057634/file/ESM…

hört sich nicht gerade spektakulär an oder?

Background:

Although the introduction of HER2 directed therapy including trastuzu-

mab, pertuzumab, lapatinib, and TDM-1 in the treatment of HER2-positive metastatic

breast cancer (mBC) patients favorably changed the natural history of this disease,

HER2-positive mBC will eventually progress in most patients. Poziotinib is a novel,

oral pan-HER kinase inhibitor which showed potent anti-tumor activities through irre-

versible inhibition of HER family tyrosine kinases.

Methods:

This open-label, multicenter phase 2 study was designed to evaluate the effi-

cacy and safety of poziotinib monotherapy in patients with HER2-positive mBC who

have progressed from more than 2 HER2-directed therapies. Patients received pozioti-

nib 12 mg once daily on a 14-day on/7-day off schedule. Dose escalation up to 16 mg

was allowed at appropriate time point and dose reduction to 8-10 mg were performed

according to toxicities. Progression-free survival (PFS) as the primary endpoint and ob-

jective response rate (ORR), overall survival (OS), and safety were evaluated.

Results:

From Apr 2015 to Feb 2016, 106 patients were enrolled in the trial from 7 insti-

tutes in Korea. The patients were median age of 50 (range: 30

76) who had received median 4 prior anti-cancer therapies including median 2 HER2-directed therapies in the advanced or metastatic setting. Median follow up duration was 12 months. The me- dian PFS was 4.04 months (95% CI, 2.94 - 4.40 months), and median overall survival

has not been reached. The disease control rate was 75.49% (77/102) including 20 pa-

tients with confirmed partial response. The most common treatment-related AEs were

(total/grade 3) diarrhea (96.23%/14.15%), stomatitis (92.45%/12.26%), and rash

(63.21%/3.77%).

Conclusions:

Poziotinib showed meaningful clinical activity in heavily-treated HER2-

positive mBCs. Diarrhea and stomatitis were the major toxicities leading to dose modi-

fication. Biomarker study being analyzed from pre- and on-treatment biopsies is war-

ranted to support further on the meaningful clinical outcomes of poziotinib in HER2-

positive mBC

Sollen das die neuen Ergebnisse vom ESMO sein?:

http://www.esmo.org/content/download/117241/2057634/file/ESM…

hört sich nicht gerade spektakulär an oder?

Background:

Although the introduction of HER2 directed therapy including trastuzu-

mab, pertuzumab, lapatinib, and TDM-1 in the treatment of HER2-positive metastatic

breast cancer (mBC) patients favorably changed the natural history of this disease,

HER2-positive mBC will eventually progress in most patients. Poziotinib is a novel,

oral pan-HER kinase inhibitor which showed potent anti-tumor activities through irre-

versible inhibition of HER family tyrosine kinases.

Methods:

This open-label, multicenter phase 2 study was designed to evaluate the effi-

cacy and safety of poziotinib monotherapy in patients with HER2-positive mBC who

have progressed from more than 2 HER2-directed therapies. Patients received pozioti-

nib 12 mg once daily on a 14-day on/7-day off schedule. Dose escalation up to 16 mg

was allowed at appropriate time point and dose reduction to 8-10 mg were performed

according to toxicities. Progression-free survival (PFS) as the primary endpoint and ob-

jective response rate (ORR), overall survival (OS), and safety were evaluated.

Results:

From Apr 2015 to Feb 2016, 106 patients were enrolled in the trial from 7 insti-

tutes in Korea. The patients were median age of 50 (range: 30

76) who had received median 4 prior anti-cancer therapies including median 2 HER2-directed therapies in the advanced or metastatic setting. Median follow up duration was 12 months. The me- dian PFS was 4.04 months (95% CI, 2.94 - 4.40 months), and median overall survival

has not been reached. The disease control rate was 75.49% (77/102) including 20 pa-

tients with confirmed partial response. The most common treatment-related AEs were

(total/grade 3) diarrhea (96.23%/14.15%), stomatitis (92.45%/12.26%), and rash

(63.21%/3.77%).

Conclusions:

Poziotinib showed meaningful clinical activity in heavily-treated HER2-

positive mBCs. Diarrhea and stomatitis were the major toxicities leading to dose modi-

fication. Biomarker study being analyzed from pre- and on-treatment biopsies is war-

ranted to support further on the meaningful clinical outcomes of poziotinib in HER2-

positive mBC

Vielleicht ist das besser:

CR: 0%

PR: 20%

SD: 51%

PD: 24%

Würde 71% Partial response oder Stable disease machen.(fast 75% im 95% confidenve interval)

siehe 3tes slide von Dr Sunil Verma auf https://twitter.com/cancermd?lang=de

Was sagen die Kurse am Montag dazu?

CR: 0%

PR: 20%

SD: 51%

PD: 24%

Würde 71% Partial response oder Stable disease machen.(fast 75% im 95% confidenve interval)

siehe 3tes slide von Dr Sunil Verma auf https://twitter.com/cancermd?lang=de

Was sagen die Kurse am Montag dazu?

Antwort auf Beitrag Nr.: 55.707.423 von vanville am 10.09.17 12:32:37Hey vanville,

RR von 20% ist gar nicht schlecht bei medium 4 Vorbehandlungen und medium + mind. zwei vorige HER2 Therapien. Die Patienten sind eigentlich weitgehend austherapiert. Daher ist das schon ein bedeutendes Ergebnis, wenn auch nicht überragend.

RR von 20% ist gar nicht schlecht bei medium 4 Vorbehandlungen und medium + mind. zwei vorige HER2 Therapien. Die Patienten sind eigentlich weitgehend austherapiert. Daher ist das schon ein bedeutendes Ergebnis, wenn auch nicht überragend.

medium = median (Vertipper)

Hi Ville,

Und wenn ich es richtig verstehe war die Studie unabhängig vom exon20 status? D.h. bei den anderen mit egfr und her2 ex20 muation selection könnten die reponses besser sein... ??

Danke, für die Antwort. Grüße

Und wenn ich es richtig verstehe war die Studie unabhängig vom exon20 status? D.h. bei den anderen mit egfr und her2 ex20 muation selection könnten die reponses besser sein... ??

Danke, für die Antwort. Grüße

Antwort auf Beitrag Nr.: 55.708.077 von Ville7 am 10.09.17 15:41:53

MD Anderson - clinical trial exon-20 poziotinib - analysis ( (c) Ville) from inspire.com patient postings and SPPI CCs:

Number of patient - Username in inspire.com / mutation / posted personal results by patient

1. ??? - first compassionate use patient / exon-20 HER2 / stable 9 months now

2. Anne121259 - second compassionate use patient / exon-20 EGFR / mixed (better in bone and pain, but growing lung tumor)

3. Lili123 - NCT03066206 trial / exon-20 EGFR / patient can breath again after 3 weeks

4. 20165 - NCT03066206 trial, start: Jun 26 / exon-20 ??? / shrinking in brain, mets, lung

5. Gardengal1565 - NCT03066206 trial / exon-20 EGFR / pain reduced, needs rarely pain meds now

6. janet129 - NCT03066206 trial start: 8/18/17 / exon-20 EGFR / no results feedback yet

Number of patient - Username in inspire.com / mutation / posted personal results by patient

1. ??? - first compassionate use patient / exon-20 HER2 / stable 9 months now

2. Anne121259 - second compassionate use patient / exon-20 EGFR / mixed (better in bone and pain, but growing lung tumor)

3. Lili123 - NCT03066206 trial / exon-20 EGFR / patient can breath again after 3 weeks

4. 20165 - NCT03066206 trial, start: Jun 26 / exon-20 ??? / shrinking in brain, mets, lung

5. Gardengal1565 - NCT03066206 trial / exon-20 EGFR / pain reduced, needs rarely pain meds now

6. janet129 - NCT03066206 trial start: 8/18/17 / exon-20 EGFR / no results feedback yet

Ich bin vor einiger Zeit mit 500 St. zu 6,30 EUR rein. Jetzt habe ich natürlich ein bisschen Gewinn. Was meint ihr laufen lassen? Wie hoch könnte es gehen?

Spectrum hing ja mal eine zeit lang recht durch aber jetzt schaut es ganz gut aus.

Spectrum hing ja mal eine zeit lang recht durch aber jetzt schaut es ganz gut aus.

Antwort auf Beitrag Nr.: 55.708.212 von vanville am 10.09.17 16:10:54Das war in HER2 positive Brustkrebs. Das hat mit NSCLC (non small cell lung cancer, also Lungenkrebs) exon20 mutations, die es u.a. in Variante EGRF und HER2 gibt nichts zu tun. Die ersten Daten dazu gibt es im Oktober. Mehr relevant für den Kurs..

Antwort auf Beitrag Nr.: 55.709.889 von Ville7 am 11.09.17 06:42:12Hier gibt's dann die ersten Daten mit Hinweisen, ob poziotinib ein "breakthrough" in NCSCL exon-20 EGFR mutations werden könnte oder eher nicht:

Antwort auf Beitrag Nr.: 55.709.889 von Ville7 am 11.09.17 06:42:12ja klar danke.... Wer lesen kann hat mehr vom Leben....

Erste Daten zu poziotinib in EGFR exon20 NSCLC via IASLC 2017 abstract

Background: Approximately 10% of EGFR mutant NSCLCs have an insertion/mutation in exon 20 of EGFR resulting in primary resistance to currently available tyrosine kinase inhibitors (TKIs). We previously reported that the structural features of poziotinib could potentially enable it to circumvent the steric hindrance induced by exon 20 mutations. Here we further characterize the preclinical activity of poziotinib and report on initial clinical activity of poziotinib in patients with EGFR exon 20 mutations from an ongoing phase II study.

Method:

We evaluated poziotinib activity in vitro using human NSCLC cell lines and the BAF3 model as well as several patient-derived xenograft (PDX) models and genetically engineered mouse models (GEMMs) of exon 20 insertion. We launched a phase 2 investigator-initiated trial of poziotinib in patients with metastatic NSCLC with EGFR exon 20 insertions (NCT03066206).

Result:

In vitro poziotinib was approximately 100x more potent than osimertinib and 40x more potent than afatinib against a common panel of EGFR exon 20 insertions. Furthermore, it had ~65-fold greater potency against common exon 20 insertions compared with EGFR T790M mutations; 3[rd] generation inhibitors osimertinib, EGF816, and rociletinib were all significantly less potent for exon 20 mutations/insertions compared with T790M. in vivo poziotinib led to >85% reduction in tumor burden in GEM models of EGFR exon 20 insertion (D770insNPG) NSCLC and the PDX model LU0387 (H773insNPH). To date, 8 platinum-refractory patients with EGFR exon 20 insertion mutation metastatic NSCLC have been enrolled in the clinical trial and treated with poziotinib at a dose of 16 mg PO daily. Two patients have reached the first interval-imaging time point (at 8 weeks of therapy per protocol). Both patients exhibited dramatic partial response, with one patient reporting improvement in dyspnea and cough at one week of therapy. In this early stage of the study, one case of grade 3 paronchycia was observed. One additional platinum- and erlotinib-refractory patient with EGFR exon 20 insertion was treated with poziotinib on compassionate basis. The patient achieved partial response after three weeks of treatment.

Conclusion:

Poziotinib has selective activity against EGFR exon 20 mutations and potent activity in cell lines, PDX, and GEM models. Three platinum-refractory patients with EGFR exon 20 mutations have been treated thus far and are evaluable for response; all three had partial responses at the time of the initial scan. Updated data from the ongoing phase 2 clinical trial of poziotinib will be presented at the meeting.

8+1 Patienten, 3 Patienten auswertbar => Objective Response Rate (ORR): 3 Patienten mit Partial Response (PR)

ORR = 100% (bezogen auf die bisher auswertbaren Patienten)

ORR = 33% (bis jetzt - bezogen auf alle Patienten)

Mit >= 30% können sie zur Zulassungsbehörde gehen und haben eine gute Chance "breakthrough designation" zu bekommen.

Ich kann es kaum erwarten, die upgedateten Daten am 18. Oktober zu sehen.

Ich erwarte eine ORR von gleich oder mehr als 50%.

ORR = 100% (bezogen auf die bisher auswertbaren Patienten)

ORR = 33% (bis jetzt - bezogen auf alle Patienten)

Mit >= 30% können sie zur Zulassungsbehörde gehen und haben eine gute Chance "breakthrough designation" zu bekommen.

Ich kann es kaum erwarten, die upgedateten Daten am 18. Oktober zu sehen.

Ich erwarte eine ORR von gleich oder mehr als 50%.

Heute die Pressemeldung von SPPI mit der Abstract-Information. Kurs zieht 20% an. Eine Neubewertung ist im Gange.

Bisher:

Compassionate Use NSCLC exon 20 HER: 2 Patienten mit PR (laut SPPI Präsentationsfolien der Präsentation vom 12.9.)

Compassionate Use NSCLC exon 20 EGFR: 1 Patient mit PR (laut gestrigem Abstract)

NCT03066206 trial NSCLC exon 20 EGFR: 2 Patienten mit "dramatic" PR (laut gestrigem Abstract)

Bilanz (bisher): 5 von 5 Patienten mit PR = 100% ORR

Man kann also gespannt auf den 18. Oktober sein. Alles weniger als 50% ORR wäre dann wahrscheinlich eine Enttäuschung für den Markt.

Mehr als 50% ORR wäre gigantisch für diese Indikation. Selbst wenn es später dann in einem pivotal trial nur zwischen 30-40% wären. Klar auf "breakthrough" Kurs bisher.

Compassionate Use NSCLC exon 20 HER: 2 Patienten mit PR (laut SPPI Präsentationsfolien der Präsentation vom 12.9.)

Compassionate Use NSCLC exon 20 EGFR: 1 Patient mit PR (laut gestrigem Abstract)

NCT03066206 trial NSCLC exon 20 EGFR: 2 Patienten mit "dramatic" PR (laut gestrigem Abstract)

Bilanz (bisher): 5 von 5 Patienten mit PR = 100% ORR

Man kann also gespannt auf den 18. Oktober sein. Alles weniger als 50% ORR wäre dann wahrscheinlich eine Enttäuschung für den Markt.

Mehr als 50% ORR wäre gigantisch für diese Indikation. Selbst wenn es später dann in einem pivotal trial nur zwischen 30-40% wären. Klar auf "breakthrough" Kurs bisher.

https://www.fool.com/investing/2017/09/28/heres-why-spectrum…

Ergänzung zu dem Inhalt des Artikels: Der Autor hat wohl noch nicht mitbekommen, dass poziotinib potentiell nicht nur bei NSCLC exon-20 EGFR Mutationen wirkt (um die es im abstract ging), sondern höchstwahrscheinlich auch bei der HER Variante - auch das wird durch die präklinischen Daten und durch zwei Responses in "Compassionate Use" Patienten gestützt. Das verdoppelt das Potential potentiell.

Ich sehe SPPI nächstes Jahr über USD 20, wenn die Erwartungen an die Wirksamkeit sich erfüllen.

Ergänzung zu dem Inhalt des Artikels: Der Autor hat wohl noch nicht mitbekommen, dass poziotinib potentiell nicht nur bei NSCLC exon-20 EGFR Mutationen wirkt (um die es im abstract ging), sondern höchstwahrscheinlich auch bei der HER Variante - auch das wird durch die präklinischen Daten und durch zwei Responses in "Compassionate Use" Patienten gestützt. Das verdoppelt das Potential potentiell.

Ich sehe SPPI nächstes Jahr über USD 20, wenn die Erwartungen an die Wirksamkeit sich erfüllen.

Kapitalerhöhung (wieder mal) durch die Hintertüre:

Spectrum Pharmaceuticals Provides Update on At-The-Market Facility

HENDERSON, Nev.--(BUSINESS WIRE)-- Spectrum Pharmaceuticals, Inc. (NasdaqGS: SPPI), a biotechnology company with fully integrated commercial and drug development operations with a primary focus in Hematology and Oncology, announced that between August 11, 2017 and September 29, 2017, it issued an aggregate of approximately 9.3 million shares of its common stock under its previously announced "at-the-market" offering program, resulting in aggregate net proceeds to the company of approximately $90.2 million. The company expects to use the proceeds from this financing to continue to develop its pipeline and to provide additional flexibility to its capital structure.

This press release does not constitute an offer to sell or the solicitation of an offer to buy the securities, nor shall there by any sale of the securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of such state or jurisdiction.

Spectrum Pharmaceuticals Provides Update on At-The-Market Facility

HENDERSON, Nev.--(BUSINESS WIRE)-- Spectrum Pharmaceuticals, Inc. (NasdaqGS: SPPI), a biotechnology company with fully integrated commercial and drug development operations with a primary focus in Hematology and Oncology, announced that between August 11, 2017 and September 29, 2017, it issued an aggregate of approximately 9.3 million shares of its common stock under its previously announced "at-the-market" offering program, resulting in aggregate net proceeds to the company of approximately $90.2 million. The company expects to use the proceeds from this financing to continue to develop its pipeline and to provide additional flexibility to its capital structure.

This press release does not constitute an offer to sell or the solicitation of an offer to buy the securities, nor shall there by any sale of the securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of such state or jurisdiction.

Antwort auf Beitrag Nr.: 55.850.619 von Ville7 am 29.09.17 13:18:21Leider eine Verwässerung von 9 Mio Aktien jedoch war einer bereit 90 Mio Dollar zu investieren und das sehe ich eher positiv.

Die Daten mitte Oktober falls positiv werden den Kurs noch mehr steigen lassen.

Je nach dem bin ich vor den Daten raus, noch 10% und mein Verkaufskurs ist erreicht.

Allen viel Erfolg

Die Daten mitte Oktober falls positiv werden den Kurs noch mehr steigen lassen.

Je nach dem bin ich vor den Daten raus, noch 10% und mein Verkaufskurs ist erreicht.

Allen viel Erfolg

Der Analyst H.C. Wainwright & Co. hat das Kursziel für Spectrum Pharmaceuticals IncShs von 14 auf 20 USD angehoben, aber die Einstufung auf "Buy" belassen.

Quelle: http://www.finanzen.net

Quelle: http://www.finanzen.net

Vorsicht!

Aktuelle Kurse sind schon recht weit gelaufen. Es stellt sich die Frage, ob der 18.Okt. nicht dann als Grund für "Sell the news" genommen wird.

Längerfristig (nächstes Jahr) sehe ich bei Erfolg von poziotinib in exon 20 insertions (EGFR + HER2) und positiven Rolontis Daten Kurse von > 20 USD.

Aktuelle Kurse sind schon recht weit gelaufen. Es stellt sich die Frage, ob der 18.Okt. nicht dann als Grund für "Sell the news" genommen wird.

Längerfristig (nächstes Jahr) sehe ich bei Erfolg von poziotinib in exon 20 insertions (EGFR + HER2) und positiven Rolontis Daten Kurse von > 20 USD.

Antwort auf Beitrag Nr.: 49.251.605 von Ville7 am 05.03.15 17:29:58Hi ville,

Und jetzt? Kann mir kaum vorstellen dass Pozi jetzt das Allheilmittel werden soll.

Vanville

Und jetzt? Kann mir kaum vorstellen dass Pozi jetzt das Allheilmittel werden soll.

Vanville

Antwort auf Beitrag Nr.: 55.879.645 von vanville am 04.10.17 17:40:26oder es ist es doch.

Antwort auf Beitrag Nr.: 55.879.576 von Ville7 am 04.10.17 17:34:14Also Abstossen?

Scheint sich weltweit eh keiner mehr für sppi zu interessieren. Ausser antihama dass ist vajo? Hast immer noch kein endrglwish gelernt....

Vanville

Scheint sich weltweit eh keiner mehr für sppi zu interessieren. Ausser antihama dass ist vajo? Hast immer noch kein endrglwish gelernt....

Vanville

Antwort auf Beitrag Nr.: 55.879.699 von vanville am 04.10.17 17:47:59Vajo ist nicht mehr aktiv. Ob er noch Stücke hat weiss man nicht. Antihama ist nicht Vajo.

Wer glaubt den Markt timen zu können kann gerne verkaufen und tiefer wieder kaufen. Kann aber auch sein man kommt nicht tiefer wieder rein.. Keiner weiss das.

Keiner weiss auch wie die Daten am 18.10. sein werden und wie der Markt kurz- und mittelfristig reagiert.

Keiner weiss zudem ob und wann der Gesamtmarkt ne Korrektur einlegt....

Wer glaubt den Markt timen zu können kann gerne verkaufen und tiefer wieder kaufen. Kann aber auch sein man kommt nicht tiefer wieder rein.. Keiner weiss das.

Keiner weiss auch wie die Daten am 18.10. sein werden und wie der Markt kurz- und mittelfristig reagiert.

Keiner weiss zudem ob und wann der Gesamtmarkt ne Korrektur einlegt....

Antwort auf Beitrag Nr.: 55.882.390 von Ville7 am 05.10.17 02:45:49Also was bis heute ja bekannt ist gehe ich von guten bis sehr guten Daten aus.

Auch eine KE bei Kursen von ca. 10 Dollar und total 90 Mio lässt erahnen wies kommt.

Ein sell on good News kann sein kann aber auch gegen 20 laufen und nicht mehr markant zurück kommt.

Viel Erfolg

Auch eine KE bei Kursen von ca. 10 Dollar und total 90 Mio lässt erahnen wies kommt.

Ein sell on good News kann sein kann aber auch gegen 20 laufen und nicht mehr markant zurück kommt.

Viel Erfolg

Noch 10 Stunden ...

... bis zu den upgedateten poziotinib Phase 1 Daten in NSCLC exon 20 EGFR insertion mutations.11:00 bis 11:10 in Yokohama Japan

Spannend auch wie der Kurs auf hervorragende oder enttäuschende Daten reagiert... man sollte sich auf beide Richtungen einstellen.

73% ORR (unconfirmed)

Drug yields high response rates for lung cancer patients with harsh mutation

https://www.mdanderson.org/newsroom/2017/10/drug-yields-high…MD Anderson Moon Shots Program finds poziotinib strikes EGFR exon 20 insertion

MD Anderson News Release 10/17/2017

A targeted therapy resurrected by the Moon Shots Program™ at The University of Texas MD Anderson Cancer Center has produced unprecedented response rates among patients with metastatic non-small cell lung cancer that carries a highly treatment-resistant mutation.

In a phase 2 clinical trial, the drug poziotinib has shrunk tumors by at least 30 percent in eight of 11 (73 percent) non-small cell lung cancer patients whose cancer includes an epidermal growth factor receptor (EGFR) mutation called an exon 20 insertion. Shrinkage ranged from 30 percent to 50 percent among the eight patients reaching partial response. One patient has progressed on the clinical trial, which began in March. All patients experienced some tumor shrinkage.

“We’ve had no effective drugs for these patients, who historically have progression free survival of about two months, and a response rate of less than 20 percent for other therapies,” said clinical trial leader John Heymach, M.D., Ph.D., chair of Thoracic/Head and Neck Medical Oncology at MD Anderson and holder of the David Bruton Junior Chair in Cancer Research.

“These early results are highly encouraging, and our research shows that poziotinib’s structure makes it a great potential fit for attacking this mutation,” Heymach said. Preliminary results were presented at the International Association for the Study of Lung Cancer 18th World Conference on Lung Cancer in Yokohama, Japan, by Yasir Elamin, M.D., assistant professor of Thoracic/Head and Neck Medical Oncology.

The investigator-initiated clinical trial marks the latest progress in the identification and development of poziotinib for this group of patients conducted by MD Anderson’s Lung Cancer Moon Shot™, which is co-led by Heymach as part of the institution’s Moon Shots Program™. The program was launched in 2012 to accelerate the development of new approaches to cancer based on scientific discoveries.

About 2 percent of non-small cell lung cancer patients (about 3,500 annually in the United States) have an EGFR exon 20 insertion. The trial has enrolled 27 patients and is expected to enroll up to 50. Other tyrosine kinase inhibitors against EGFR have been approved by the U.S. Food and Drug Administration, but none have proved effective against the exon 20 insertion.

Six of 11 patients have had their dose reduced due to side effects, mainly due to rash but also diarrhea, mucositis and paronychia – inflammation of the tissue around finger nails and toenails.

Preclinical research points to poziotinib vs. exon 20

Poziotinib had been tried and abandoned as a general EGFR inhibitor against lung cancer when Heymach’s team turned up evidence of its potential against exon 20 through a drug screening program that’s part of the moon shot.

Postdoctoral fellow Jacqulyne Robichaux, Ph.D., tapped the Genomic Marker-Guided Therapy Initiative (GEMINI), which includes tumor samples and detailed clinical information on more than 4,000 lung cancer patients treated at MD Anderson since 2012.

Robichaux developed EGFR exon 20 NSCLC cell lines as well as patient-derived xenograft models, and tested a variety of EGFR inhibitors against them under the Lung Moon Shot’s drug repurposing program.

“Poziotinib is the only drug we’ve ever found that was dramatically better for exon 20 than it was for the classical EGFR mutation, T790M, that everyone tests,” Heymach said.

Working with Shuxing Zhang, PHARMD, Ph.D., associate professor of Experimental Therapeutics, the multidisciplinary team identified structural aspects of the drug that explain that divergent impact.

Heymach and colleagues then contacted Spectrum Pharmaceuticals, a Nevada-based biotechnology company that initially developed poziotinib. Subsequent collaboration included compassionate use of poziotinib for some patients with advanced disease and rapid development of the phase 2 clinical trial.

The Lung Moon Shot has funded the effort from the beginning, from preclinical identification and confirmation through the clinical trial. A scientific paper describing the group’s preclinical research is pending with a major journal. Spectrum has provided poziotinib and also partially funds the trial.

Based on the MD Anderson team’s discoveries, the institution is developing intellectual property related to the use of poziotinib for the treatment of these mutant cancers.

Co-authors with Heymach, Elamin, Robichaux and Zhang are Vincent Lam, M.D., Anne Tsao, M.D., Charles Lu, M.D., George Blumenschein, M.D., Jonathan Kurie, M.D., and Monique Nilsson, Ph.D., of Thoracic/Head and Neck Medical Oncology; Zhi Tan of Experimental Therapeutics; Julie Brahmer, M.D., of the Bloomberg-Kimmel Institute for Cancer Immunotherapy at Johns Hopkins, Baltimore; Anna Truini, Ph.D., and Katerina Politi, Ph.D., Yale School of Medicine; Adriana Estrada-Bernal and Robert Doebele, M.D., Ph.D., University of Colorado School of Medicine; Shengwu Liu, Ph.D., Ting Chen, Ph.D., Shuai Li, M.D., and Kwok-Kin Wong, M.D., Ph.D., of Perlmutter Cancer Center at New York University Langone Medical School, and Zane Yang, M.D., of Spectrum Pharmaceuticals, Henderson, Nev. Zhi Tan also is a graduate student in the MD Anderson UTHealth Graduate School of Biomedical Sciences.

Spectrum Pharmaceuticals Highlights Poziotinib Data in Non-Small-Cell Lung Cancer (NSCLC)

October 17, 2017Presented at the 18th IASLC World Conference on Lung Cancer in Japan

Poziotinib demonstrates evidence of significant antitumor activity in NSCLC patients with EGFR exon 20 insertion mutations, with interim data showing an Objective Response Rate of 73%.

Evidence of central nervous system (CNS) activity in a patient with CNS metastasis and another with leptomeningeal disease (LMD).

On October 18th at 8:30 a.m. EDT/5:30 a.m. PDT, the Company will hold a conference call with Dr. John Heymach, from The University of Texas MD Anderson Cancer Center to discuss the study results.

HENDERSON, Nev.--(BUSINESS WIRE)-- Spectrum Pharmaceuticals, Inc. (NasdaqGS: SPPI), a biotechnology company with fully integrated commercial and drug development operations with a primary focus in Hematology and Oncology, announced the oral presentation of interim data from a Phase 2 clinical study evaluating poziotinib in EGFR Exon 20 Mutant Non-Small-Cell Lung Cancer (NSCLC) by scientists from the MD Anderson Cancer Center which was presented in Yokohama, Japan, October 15-18, 2017. The Company will hold a conference call tomorrow, October 18th, at 8:30 a.m. EDT/5:30 a.m. PDT with Dr. John Heymach, M.D., Ph.D., Chairman, Professor, and David Bruton Junior Chair in Cancer Research, Department of Thoracic/Head and Neck Medical Oncology, The University of Texas MD Anderson Cancer Center, to discuss his study results.

"These data are remarkable for NSCLC patients with exon 20 insertion mutations," said John Heymach, M.D., Ph.D., The University of Texas MD Anderson Cancer Center. "These patients currently have a poor prognosis, single-digit response rate on first generation tyrosine kinase inhibitors (TKI's), and a PFS of about two months. What is truly noteworthy is that all 11 study patients who received poziotinib at a 16mg daily dose and have reached their first scan, have seen some level of tumor shrinkage. Interestingly, we have also seen evidence of CNS activity. Toxicities have included rash, diarrhea, paronychia, and mucositis consistent with those previously described for poziotinib and other TKI's, which led to dose reduction in 55% of the patients. We believe that poziotinib specifically inhibits EGFR with exon 20 insertion mutations because it overcomes steric hindrance caused by exon 20 insertions, due to its smaller size and flexibility. To date poziotinib has shown promising results in patients with exon 20 insertion mutations and we are fortunate to be leading the efforts in the continuing development of this product."

"We are greatly encouraged with the clinical data emerging from poziotinib and plan to pursue its clinical development expeditiously and aggressively," said Rajesh C. Shrotriya, M.D., Chairman and Chief Executive Officer of Spectrum Pharmaceuticals. "In the near future, we plan to discuss the regulatory pathway for poziotinib with the FDA. At the same time, we are embarking upon an overall strategy for global clinical development and regulatory filings. With three promising drugs in late-stage development, Spectrum's pipeline has never been as exciting and our prospects never as bright."

Conference Call

Wednesday, October 18, 2017 @ 8:30 a.m. Eastern/5:30 a.m. Pacific

Domestic: (877) 837-3910, Conference ID# 86093351

International: (973) 796-5077, Conference ID# 86093351

For interested individuals unable to join the call, a replay will be available from October 18, 2017 @ 11:30 a.m. ET/8:30 a.m. PT through October 28, 2017, until 11:30 a.m. ET/8:30 a.m. PT.

Domestic Replay Dial-In #: (855) 859-2056, Conference ID# 86093351

International Replay Dial-In #: (404) 537-3406, Conference ID# 86093351

This conference call will also be webcast. Listeners may access the webcast, which will be available on the investor relations page of Spectrum Pharmaceuticals' website: www.sppirx.com on October 18, 2017, at 8:30 a.m. Eastern/5:30 a.m. Pacific.

About Poziotinib

Poziotinib is a novel, oral pan-HER inhibitor that irreversibly blocks signaling through the Epidermal Growth Factor Receptor (EGFR, HER) Family of tyrosine-kinase receptors, including HER1 (erbB1; EGFR), HER2 (erbB2), and HER4 (erbB4), and importantly, also HER receptor mutations; this, in turn, leads to the inhibition of the proliferation of tumor cells that overexpress these receptors. Mutations or overexpression/amplification of EGFR family receptors have been associated with a number of different cancers, including non-small-cell lung cancer (NSCLC), breast cancer, and gastric cancer. Spectrum received exclusive license to develop, manufacture, and commercialize worldwide excluding Korea and China from Hanmi Pharmaceuticals. Poziotinib is currently being investigated by Spectrum and Hanmi in several mid-stage trials in multiple solid tumor indications.

About the WCLC

The World Conference on Lung Cancer (WCLC) is the world's largest meeting dedicated to lung cancer and other thoracic malignancies, attracting over 6,000 researchers, physicians, and specialists from more than 100 countries. The goal is to disseminate the latest scientific achievements; increase awareness, collaboration, and understanding of lung cancer; and to help participants implement the latest developments across the globe. Organized under the theme of "Synergy to Conquer Lung Cancer," the conference covers a wide range of disciplines and unveils several research studies and clinical trial results. For more information, visit http://wclc2017.iaslc.org/.

About Spectrum Pharmaceuticals, Inc.

Spectrum Pharmaceuticals is a leading biotechnology company focused on acquiring, developing, and commercializing drug products, with a primary focus in Hematology and Oncology. Spectrum currently markets six hematology/oncology drugs, and has an advanced stage pipeline that has the potential to transform the Company. Spectrum's strong track record for in-licensing and acquiring differentiated drugs, and expertise in clinical development have generated a robust, diversified, and growing pipeline of product candidates in advanced-stage Phase 2 and Phase 3 studies. More information on Spectrum is available at www.sppirx.com.

Hallo Ville wie siehst du die Chancen?

Antwort auf Beitrag Nr.: 55.973.769 von abgemeldet-577022 am 18.10.17 12:47:32Schau dir den Kurs an, war vorbörslich fast schon bei USD 20. Der Markt bewertet es sehr positiv. "Breakthrough designation" sollte drin sein.

Wenn alles gut läuft nächstes Jahr klar > 20 USD. Vielleicht sogar schon früher...

Dennoch habe ich 40% meiner Aktien vorbörslich zu 19-19.30 verkauft. Zu gut ist das hier gelaufen, nachdem ich einen Teil dieser verkauften Aktien erst Anfang August zu um die USD 8 gekauft habe.

Zudem bin ich zwar zufrieden über die 73% (unconfirmed) ORR, aber etwas Wasser im Wein ist, dass es alles nur knappe partial responses sind. Keine complete response. Das schmeckt mir nicht so.

Jetzt aktuell der CC...

Wenn alles gut läuft nächstes Jahr klar > 20 USD. Vielleicht sogar schon früher...

Dennoch habe ich 40% meiner Aktien vorbörslich zu 19-19.30 verkauft. Zu gut ist das hier gelaufen, nachdem ich einen Teil dieser verkauften Aktien erst Anfang August zu um die USD 8 gekauft habe.

Zudem bin ich zwar zufrieden über die 73% (unconfirmed) ORR, aber etwas Wasser im Wein ist, dass es alles nur knappe partial responses sind. Keine complete response. Das schmeckt mir nicht so.

Jetzt aktuell der CC...

Extrem positiver CC und Präsentation von Dr. Heymach. Der Kurs zieht folglicherweise erneut an.

Spannend wie der Kurs sich dann in der Haupttradingsession verhält. Ein Riesen-Gap wird aufgerissen. Neues Mulitjahreshoch.

Spannend wie der Kurs sich dann in der Haupttradingsession verhält. Ein Riesen-Gap wird aufgerissen. Neues Mulitjahreshoch.

SPPI wird versuchen bei der FDA eine Strategie zur schnellen Zulassung in 1st line zu erarbeiten.

Antwort auf Beitrag Nr.: 55.974.954 von Ville7 am 18.10.17 15:14:401st line = erheblich höheres Potential. Erheblich bessere Ergebnisse und längere PFS und OS zu erwarten.

Glückwunsch zum Gewinn Ville.

SPPI und Firstline hat ja Tradition (Zevalin). Die Frage ist halt wie es sich vermarktet. Aber das ist ja noch weit. Wenn man sieht woher SPPI kommt und welchen weiten Weg die Bude gegangen ist, seit 2008 freut mich der Erfolg total. Ich hatte früher schon immer gute Gewinne mit Spectrum. Das ist aber sehr lange her (GPC Biotech läßt grüßen) :-)

Mittlerweile habe ich nur noch einen ganz kleinen Restbestand (Hauptsache ich bin dabei)

SPPI und Firstline hat ja Tradition (Zevalin). Die Frage ist halt wie es sich vermarktet. Aber das ist ja noch weit. Wenn man sieht woher SPPI kommt und welchen weiten Weg die Bude gegangen ist, seit 2008 freut mich der Erfolg total. Ich hatte früher schon immer gute Gewinne mit Spectrum. Das ist aber sehr lange her (GPC Biotech läßt grüßen) :-)

Mittlerweile habe ich nur noch einen ganz kleinen Restbestand (Hauptsache ich bin dabei)

Die USD 21 gab es eben. Jetzt um die 20.

Der Markt sieht das alles was zu sehen und zu hören war noch positiver als ich ... sehr gut. In der Präsentation wurde ja auch angesprochen, dass es sich um sehr kranke, vielmals vorbehandelte Patienten handelt. Poziotinib sollte in first line treatment noch bessere Response Rates liefern und eine ordentliche Duration of Response, sodass hier entgegen meiner jüngsten Annahmen doch ein Blockbusterpotential drin ist.

Ich trauere meinem Verkauf von vorhin nicht hinterher. Das Risiko ist hier bei SPPI nun auch komplett weg, alle meine restlichen Stücke sind hier komplett "for free". Und das sind nicht wenige.

Der Markt sieht das alles was zu sehen und zu hören war noch positiver als ich ... sehr gut. In der Präsentation wurde ja auch angesprochen, dass es sich um sehr kranke, vielmals vorbehandelte Patienten handelt. Poziotinib sollte in first line treatment noch bessere Response Rates liefern und eine ordentliche Duration of Response, sodass hier entgegen meiner jüngsten Annahmen doch ein Blockbusterpotential drin ist.

Ich trauere meinem Verkauf von vorhin nicht hinterher. Das Risiko ist hier bei SPPI nun auch komplett weg, alle meine restlichen Stücke sind hier komplett "for free". Und das sind nicht wenige.

Bin grad raus mit meinen 500 St. mir wird das zu heiß. Guter Gewinn. Mal schauen wenn sich das GAP schließt lege ich mir vielleicht wieder ein paar rein.

Antwort auf Beitrag Nr.: 55.975.428 von abgemeldet-577022 am 18.10.17 15:56:50Das Gap ist riesig. Von 14.47 bis 19.21. Ich glaube nicht, dass es geschlossen wird. Wenn, dann wird es angeknabbert. Vielleicht im Extremfall ein Rückgang bis zum letzten Multiyear-High um die 17-irgendwas. Aber wenn Poziotinib so durchstartet und massive Unterstützung von der FDA bekommt (z.B. "breakthrough" plus aktuelle Phase II Trial zur Zulassungsstudie ausbauen), dann wird selbst das Anknabbern extrem schwierig....

Nachdem ich hier jahrelang "gelitten" habe, möchte ich eigentlich nicht gleich wieder aussteigen, obwohl ich mittlerweile auch schon sehr deutlich im Plus bin.

Nach der Verwässerung der letzten Jahre sind wir aber bei einem Share Preis von 20 Dollar aber andererseits bei der Marketcap ja schon deutlich über 1 Milliarde, was immer das Versprechen von Raj war.

Was ist eine Biotechbude wert mit "nur" einem Blockbluster? 5x der Jahresumsatz des Medikaments? Oder mehr?

Nach der Verwässerung der letzten Jahre sind wir aber bei einem Share Preis von 20 Dollar aber andererseits bei der Marketcap ja schon deutlich über 1 Milliarde, was immer das Versprechen von Raj war.

Was ist eine Biotechbude wert mit "nur" einem Blockbluster? 5x der Jahresumsatz des Medikaments? Oder mehr?

Antwort auf Beitrag Nr.: 55.976.361 von 123fly am 18.10.17 17:21:395x Blockbusterjahresumsatz  ?

?

Nein, das traue ich Rajesh nicht zu. Obwohl der große Teile an meinem Haus gebaut hat. Und Ville hat sicher noch mehr als 10k Stücke

$40 Dollar / Stck wären möglich, aber nicht im Vorfeld. Ich glaube daran das der Kurs vorher nochmal deutlich runter geht um dann je näher der Termin für die Entscheidung rückt extrem anzuziehen. So wie es halt immer war.

SPPI hat jetzt eine riesen Ralley hingelegt. Ich hätte das nie geglaubt. Ich habe 17,50 EUR pro Anteil bekommen. Ich freu mich. Aber mitmachen werde ich das was jetzt kommt erstmal nicht.

Vielleicht hast Du Glück und die Amis treiben den Kurs von heute immer weiter. Das wäre dann der Jackpot für Ville.

?

?Nein, das traue ich Rajesh nicht zu. Obwohl der große Teile an meinem Haus gebaut hat. Und Ville hat sicher noch mehr als 10k Stücke

$40 Dollar / Stck wären möglich, aber nicht im Vorfeld. Ich glaube daran das der Kurs vorher nochmal deutlich runter geht um dann je näher der Termin für die Entscheidung rückt extrem anzuziehen. So wie es halt immer war.

SPPI hat jetzt eine riesen Ralley hingelegt. Ich hätte das nie geglaubt. Ich habe 17,50 EUR pro Anteil bekommen. Ich freu mich. Aber mitmachen werde ich das was jetzt kommt erstmal nicht.

Vielleicht hast Du Glück und die Amis treiben den Kurs von heute immer weiter. Das wäre dann der Jackpot für Ville.

Poziotential?

Hallo Ville,Was ist denn nun eigentlich das Potential von Poziotinib falls es denn wirklich was wird? Ich habe nirgends mal eine Schätzung gesehen.

222.000 neue Lungenkrebsfälle (wieviel davon ist eigentlich NSCLC?) in den USA /Jahr. Davon 2 % EGFR Exon20 insertion= 4440. Wie frequent ist Her2 exon20 ins? Sagen wir mal +1% dazu, sind 6660 Patienten in den USA bei 325 Mio Leuten. In Europa sind 742 Mio. Macht sagen wir mal 20000 potentielle Patienten / Jahr. Lassen wir mal den Rest der Welt weg, Korea und China ist bei Hanmi. Was soll so ein treatment kosten? 100.000 Euro? = 2000000000, also 2 Millarden Euro Umsatz. Wie könnte SPPI dann bewertet sein? 10x? Bei 100 Millionen Aktien sind das ca 200 Euro /per share. Halbieren wir mal das ganze macht immer noch 100/share.

Ist das Käse?

Grüße

vanville

Hi vanville,

wenn du mich so fragst: ja das ist Käse. Das Potential ist wahrscheinlich viel geringer. Ich rechne das Potential nur mal für USA aus. Die verbleibenden Länder interessieren mich gerade nicht.

In USA sind nur ca. 9% von 10-15% EGFR NSCLC Exon 20 insertions. Sagen wir 1,1%.

In USA sind nur 2% von NSCLC Exon 20 insertions. Sagen wir 2%.

Macht 235.000 mal 3,1% = 7285 Patienten.

Sagen wir die Behandlung kostet 100.000 im Jahr, so viel kostet ein typischer neuer TKI. Möglicherweise sind wegen der Einzigartigkeit und dem medical need auch 200.000 im Jahr drin.

Allerdings kommt es darauf an wie lange die durchschnittliche Behandlungszeit sein wird. Die Patienten werden so lange behandelt, bis sie progressive Disease zeigen. Gehen wir hier mal von 6 Monaten aus. Hinweis: ein PFS von 6 Monaten wurde von Heymach als excellentes, eines von 4 Monaten als gut bezeichnet, wenn das rauskommen würde. Hierzu hat man aber noch keine Daten.

Rechnen wir damit, dass 60% der Patienten überhaupt eine Behandlung erhalten. Die anderen 40% nicht, weil sie es sich z.B. nicht leisten können oder nicht ordentlich versichert sind.

Rechnung: 60% * 7285 * 6Monate/12 Monate * 100.000 = 218,55 Mio.

Das restliche Territorium müsste man anders rechnen, da die Mutationen in unterschiedlichen Ethnien unterschiedlich häufig auftreten. Ich würde daher vereinfacht einfach die USA Summe verdoppeln.

Man wäre dann bei potentiell knapp 450 Mio USD weltweit.

Zum Blockbuster könnte es nur werden, wenn SPPI viel höhere Preise nimmt und / oder die Duration of Response und somit das PFS deutlich höher ist als die genannten 4 oder 6 Monate.

Wenn du eine Umsatzmultiple von 4 nimmst, bewertest du schon sehr gut. Und klar, manchmal spinnt der Markt auch Multiplen von 6 oder höher. Das korrigiert aber irgendwann wieder, wenn die Erwartungen nicht erfüllt werden können. Normalerweise nimmt man 2-3 als Umsatzmultiple. D.h. Poziotinib hat im konservativen Ansatz erst mal einen Wert für die Firma von sagen wir mal 1250 bis 1750 Mio USD, wenn beide Mutationen erfolgreich mit hohen Ansprechraten behandelt werden können.

Hinzu gepreist werden muss dann natürlich die bisherige Pipeline mit vielleicht 200 Mio USD. Zudem Rolontis, da wäre ich aktuell noch vorsichtig, das alleine könnte aber auch noch mal 1000 bis 1200 USD Bewertung oder mehr bringen. Quapzola würde ich nicht einpreisen, hier sehe ich wenig Chancen, da der Phase 3 Trial einfach zu wenig Power hat.

Also alles in allem sollte mit guten Rolontis Topline Daten und Erfüllung des Poziotinib Potentials 30 USD Bewertung (3000 Mio USD bei 100 Mio Aktien) in Ordnung sein. Und in der Euphorie kann es auch gut und gerne bis 40 oder höher gehen.

Kommt jetzt auf die weitere Entwicklung an. Unbekannt ist zudem wie viel von den Poziotinib Umsätzen an Hanmi gehen. Da SPPI keinen Upfront gezahlt hat gehe ich davon aus, dass es sehr hohe Tantiemen sein werden...

wenn du mich so fragst: ja das ist Käse.

Das Potential ist wahrscheinlich viel geringer. Ich rechne das Potential nur mal für USA aus. Die verbleibenden Länder interessieren mich gerade nicht.In USA sind nur ca. 9% von 10-15% EGFR NSCLC Exon 20 insertions. Sagen wir 1,1%.

In USA sind nur 2% von NSCLC Exon 20 insertions. Sagen wir 2%.

Macht 235.000 mal 3,1% = 7285 Patienten.

Sagen wir die Behandlung kostet 100.000 im Jahr, so viel kostet ein typischer neuer TKI. Möglicherweise sind wegen der Einzigartigkeit und dem medical need auch 200.000 im Jahr drin.

Allerdings kommt es darauf an wie lange die durchschnittliche Behandlungszeit sein wird. Die Patienten werden so lange behandelt, bis sie progressive Disease zeigen. Gehen wir hier mal von 6 Monaten aus. Hinweis: ein PFS von 6 Monaten wurde von Heymach als excellentes, eines von 4 Monaten als gut bezeichnet, wenn das rauskommen würde. Hierzu hat man aber noch keine Daten.

Rechnen wir damit, dass 60% der Patienten überhaupt eine Behandlung erhalten. Die anderen 40% nicht, weil sie es sich z.B. nicht leisten können oder nicht ordentlich versichert sind.

Rechnung: 60% * 7285 * 6Monate/12 Monate * 100.000 = 218,55 Mio.

Das restliche Territorium müsste man anders rechnen, da die Mutationen in unterschiedlichen Ethnien unterschiedlich häufig auftreten. Ich würde daher vereinfacht einfach die USA Summe verdoppeln.

Man wäre dann bei potentiell knapp 450 Mio USD weltweit.

Zum Blockbuster könnte es nur werden, wenn SPPI viel höhere Preise nimmt und / oder die Duration of Response und somit das PFS deutlich höher ist als die genannten 4 oder 6 Monate.

Wenn du eine Umsatzmultiple von 4 nimmst, bewertest du schon sehr gut. Und klar, manchmal spinnt der Markt auch Multiplen von 6 oder höher. Das korrigiert aber irgendwann wieder, wenn die Erwartungen nicht erfüllt werden können. Normalerweise nimmt man 2-3 als Umsatzmultiple. D.h. Poziotinib hat im konservativen Ansatz erst mal einen Wert für die Firma von sagen wir mal 1250 bis 1750 Mio USD, wenn beide Mutationen erfolgreich mit hohen Ansprechraten behandelt werden können.