LYNAS - Faktenthread, Analysen, Querverweise u. Meldungen zum Unternehmen - 500 Beiträge pro Seite

eröffnet am 25.04.07 13:15:18 von

neuester Beitrag 31.03.24 09:13:03 von

neuester Beitrag 31.03.24 09:13:03 von

Beiträge: 3.527

ID: 1.126.458

ID: 1.126.458

Aufrufe heute: 2

Gesamt: 784.708

Gesamt: 784.708

Aktive User: 0

ISIN: AU000000LYC6 · WKN: 871899

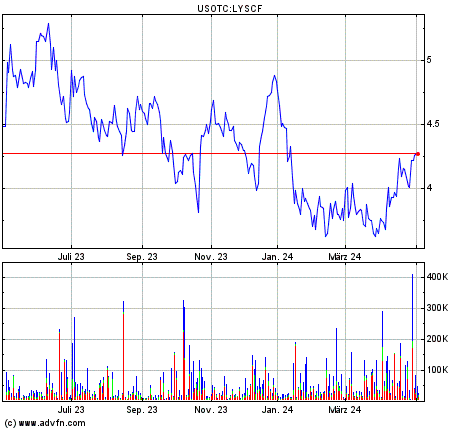

3,8020

EUR

-1,02 %

-0,0390 EUR

Letzter Kurs 25.04.24 Tradegate

Meistbewertete Beiträge

| Datum | Beiträge | Bewertungen |

|---|---|---|

| 31.03.24 |

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7950 | +30,33 | |

| 227,00 | +21,91 | |

| 5,1500 | +21,75 | |

| 29,98 | +18,24 | |

| 16,050 | +17,41 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,6850 | -6,80 | |

| 29,70 | -7,19 | |

| 0,8800 | -7,37 | |

| 0,5400 | -8,47 | |

| 46,59 | -98,01 |

Die Lynas Corp. ist seit 1986 in Australien börsennotiert. Laut eigenen Angaben besitzt Lynas in Mount Weld (West-Australien) die weltweit größte Lagerstätte " seltener Erden"

LYNAS CORP. LTD. REGISTERED SHARES O.N. (871899) AU000000LYC6

Eine besonders ergiebige Lagerstätte, die vom Unternehmen Lynas Corporation erschlossen wird, ist das Mt. Weld-Projekt in West-Australien. Lynas Corporation (Börsenkürzel: LYC.AX) ist in den letzten Zügen der Entwicklung der Mt Weld Mine, wird jedoch die Produktion nach Malaysia verlagern, um die aktuellen chinesischen Exportzölle von 10 % zu vermeiden. Da China mittlerweile die Produktion zurückgefahren hat, sind die durchschnittlichen Preisanstiege von über 60 % bei den "Seltenen Elementen" kein Zufall.

Das Mt Weld-Projekt von Lynas mit nachgewiesenen Reserven von über 2 Millionen Tonnen kann die Lücke zwischen Angebot und Nachfrage in den nächsten Jahren schließen. Geht man von zukünftigen Preisen von etwa 10 bis 15 USD/kg REO aus, so dürften die bisherigen Reserven von Lynas bei einem Reinheitsanteil von konservativ geschätzten 15 bis 20 % alleine 2 Milliarden USD wert sein. Bei noch höheren Reinheitsgraden und Preisen um 20 bis 25 USD könnten die Lynas-Reserven sogar bis zu 5 Milliarden USD wert sein. Dies allein würde Aktienkurse von etwa 3 bis 5 AUD (aktuell 0.6 AUD) in diesem Wert rechtfertigen. Wenn es keine Verzögerungen gibt, sollte Lynas bereits ab dem Jahr 2010 etwa 10.000 Tonnen pro Jahr, d.h. 10 % der weltweiten Nachfrage liefern können. Bis zum Jahr 2015 könnte dieser Anteil auf über 15 % ansteigen.

Die Mt. Weld Lagerstätten (ca 25 % Lanthanoxide, cac. 45 % Ceroxide sowie 20 % Neodymoxide) sind die weltweit größte Fundstätte von "Seltenen Elementen", wobei diese sogar in der Lage wären über einen Zeitraum von 30 Jahren 20 % der weltweiten Nachfrage zu decken. Somit dürfte Lynas in den nächsten Jahren in der Spitze etwa 75 bis 100 Millionen USD pro Jahr verdienen. Aktuell beträgt die Börsenkapitalisierung etwa 190 Millionen USD. Dies entspräche, wenn der heutige Kurs herangezogen wird, in etwa einem Kurs-/-Gewinn-Verhältnis von 1,4 bis 2,7. Besonders interessant an der Strategie von Lynas ist, dass das Unternehmen die vertikale Integration vorantreibt. Es will nicht nur als einer der weltweit größten Lieferanten, sondern auch als Weiterverarbeiter auftreten. Zur Absicherung dieser Strategie hat Lynas einen langfristigen Liefervertrag mit dem französischen Spezialchemieunternehmen Rhodia abgeschlossen.

"Seltene Elemente" werden oft als Nebenprodukt von schweren Sänden gefunden, die Titan beinhalten, was vor allem in Australien der Fall ist. Zusätzliches Potential dürfte Lynas deshalb das Crown Polymetallic Resource-Projekt im Mt. Welt-Abbaugebiet geben, enthält es doch große Ansammlungen von Niob (Legierungszusatz für rostfreie Stähle, Einsatz in der Nukleartechnik), Tantal (Einsatz in Kondensatoren), Zirkonium (Einsatz im Reaktorbau und bei Brennstoffzellen) sowie Titan (Einsatz im Flugzeugbau).

Hightech-Rohstoffe

Im United States Geological Survey (USGS) wird hervorgehoben, dass "Seltene Elemente" einer der kritischen Schlüsselfaktoren für die Hightech-Industrien sind. Wenn die Nachfrage wie erwartet mehr als 10 % steigen sollte, so könnte es eine ernsthafte Knappheit geben, die die Weltmarktpreise für REEs deutlich ansteigen lassen wird.

Abhängigkeit der Hightech-Industrien von "Seltenen Elementen"

Artur P. Schmidt 09.02.2007

Australien greift Chinas heimliches Rohstoff-Monopol an

Auch wenn viele meinen, die Rohstoffhausse sei zu Ende, so lässt sich heute schon prognostizieren, dass die verstärkte Nachfrage aus China und Indien in zahlreichen Commodity-Marktsegmenten zu starken Knappheiten führen wird. Von der Öffentlichkeit kaum wahrgenommen hat China in den letzten beiden Jahrzehnten eine führende Position im Bereich der "Seltenen Elemente", den sogenannten "Rare Earth Elements" (REE), aufgebaut.

Globale Produktion von "Seltenen Element"-Oxiden. Grafik: USGS

"Seltene Elemente", auch Lanthanoide (Lanthanähnliche) genannt, ist eine Gruppenbezeichnung ähnlicher Elemente mit den Atomnummern 57 bis 71, zu denen das Lanthan und die 14 im Periodensystem folgenden Elemente Cer, Praseodym, Neodym, Promethium, Samarium, Europium, Gadolinium, Terbium, Dysprosium, Holmium, Erbium, Thulium, Ytterbium und Lutetium zählen. Obwohl die 15 "Seltenen Elemente" meistens zusammen auftreten, werden diese in zwei Gruppen unterteilt: die leichten und mittelschweren (Atomnummern 57 bis 64) und die schweren (Atomnummern 65 bis 71) Elemente. Zu den Lanthaniden werden auch noch die Atomnummern 21 (Scandium) sowie 39 (Yttrium) gezählt. Der Gehalt an "Seltenen Elemente" wird ausgedrückt durch den Begriff "Rear-Earth-Oxide" (REO) oder "Total Rare Earth Oxide" (TREO).

Die Lanthanoide sind silbrig-glänzende, relativ weiche und reaktionsfreudige Metalle. An der Luft oxidieren sie schnell und werden matt. Im Wasser erfolgt die Zersetzung mehr oder weniger schnell unter Freisetzung von Wasserstoffgas. Wegen ihren ähnlichen physikalischen und chemischen Eigenschaften treten die "Seltenen Elemente" und Yttrium meist gemeinsam in der Natur auf. Der Begriff "Erden" bezieht sich hierbei auf die jeweiligen Oxide. Während das betroffene Element die Endung "-ium" erhielt, wurde für das zugehörige Oxid die Endung "-ia" verwendet (Beispiel: Element "Yttrium", das zugehörige Oxid wurde "Yttria" genannt, zu deutsch "Yttererde"). Die häufigsten und ökonomisch wichtigsten lanthanoidführenden Minerale sind: Monazit, Xenotim, Bastnäsit, Parisit, Allanit, Synchysit, Ancylit sowie Cerianit. Die weltweite Produktion von "Seltenen Elementen" beträgt etwa 100.000 Tonnen Rare Earth Oxyde (REO) pro Jahr. Von Yttrium wird jährlich nur etwa 2,500 Tonnen Yttrium Oxid (Y2O3) produziert.

Hightech-Rohstoffe

Im United States Geological Survey (USGS) wird hervorgehoben, dass "Seltene Elemente" einer der kritischen Schlüsselfaktoren für die Hightech-Industrien sind. Wenn die Nachfrage wie erwartet mehr als 10 % steigen sollte, so könnte es eine ernsthafte Knappheit geben, die die Weltmarktpreise für REEs deutlich ansteigen lassen wird.

"Seltene Elemente" spielen eine Schlüsselrolle für die Elektronikindustrie (Magnetische Kühlung), die Telekommunikation (Glasfaserkabel), die Mikrosystemtechnik (hochfeste Präzisionsbauteile), den Automobilbau (Hybridantriebe), den Umweltschutz (Emissionskontrolle) sowie die Petrochemie (Prozesskatalysatoren). Eine besonders hohe Nachfrage wird nach Cerium in Automobilkatalysatoren und Lathanum in NiMH-Batterien erwartet. Aber auch die Nachfrage von "Seltenen Elementen" beim Einsatz von Phosphor, Glasfasern und Keramiken dürfte die Preise weltweit nach oben treiben. Viele Komponenten wie Batterien, Magneten, Bildschirme werden durch "Seltene Elemente" immer leistungsfähiger und wirken hierbei nachfrageerhöhend.

Was viele "Seltene Elemente" so schwer und teuer abbaubar macht ist, dass diese oftmals zusammen mit strahlendem Material auftreten. Deshalb sind die Preise so verschieden. Während Cerium Oxid etwa 1,6 USD per kg kostet, liegen die Preise für Terbium Oxid bei über 400 USD pro kg.

Seltene Elemente", die sogenannten "Rare Earth Elements" (REE)

Globale Produktion von "Seltenen Element"-Oxiden. Grafik: USGS

Die Abhängigkeit vieler Industrieländer, vor allem den USA, von REEs aus China ist heute nahezu perfekt, insbesondere da die USA nur in Kalifornien (Mountain Pass) und in Wyoming (Bear Lodge) über nennenswerte Reserven verfügen, die dort vom Unternehmen Rare Element Resources (Börsenkürzel: RES.V) abgebaut werden. Während sich die USA im Jahr 1990 noch selbst mit "Seltenen Rohstoffen" versorgen konnte, ist das Land heute zu 90 % von Importen aus China abhängig.

Sich vom chinesischen Quasi-Monopol zu befreien, ist deshalb nur möglich, wenn alternative Anbieter, die über nennenswerte Reserven verfügen, wie Lynas und Arafura, schnellstmöglich in die Abbauphase übergehen. Mit bisher nachgewiesenen Reserven von über 2 Millionen Tonnen kann Lynas zu einer ernsthaften Konkurrenz für die Chinesen avancieren. Wenn es keine Verzögerungen gibt, sollte Lynas Corporation bereits ab dem Jahr 2010 etwa 10.000 Tonnen pro Jahr, d.h. 10 % der weltweiten Nachfrage liefern können. Der andere Key Player Arafura Resources verfügt ebenfalls über erheblichen Reserven an "Seltenen Elementen".

http://www.lynascorp.com/page.asp?category_id=8&page_id=26&q…

http://www.lynascorp.com/

http://www.heise.de/tp/r4/artikel/24/24602/1.html

LYC- Präsentation:

http://sa.iguana2.com/cache/0949095dbdc89bd569294cc1547ca924…

Halbjahresbericht:

http://sa.iguana2.com/cache/daee94345721feced262feb9f050bdcc…

Börsenplatz:

http://www.asx.com.au/asx/research/ChartsSearchAndResults.js…

http://www.rohstoff-spiegel.de/count.php?url=rs_2007-4.pdf&l…

Artikel über die Situation bei REO`s , betrifft auch Lynas:

http://www.goldseiten.de/content/diverses/artikel.php?storyi…

eine Studie die im Auftrag von Lynas angefertigt wurde:

http://www.lynascorp.com/content/upload/files/press_releases…

- Anwendungsbereiche von Rare Earth Produkten, insbesondere Highend-Magnete

- Entwicklungen in der Industrie

- Faktor China (produzieren dort), Exportsteuer für REE

http://www.robtv.com/shows/past_archive.tv

Why Rare Earth Prices are Likely to Continue Their Upward TrendMagnetics2007 ConferenceApril 4-5, 2007Chicago, IllinoisPresented byWalter T. BeneckiConsultant to the Worldwide Magnetics Industry

http://www.waltbenecki.com/uploads/Why_Rare_Earth_Prices_are…

http://www.lynascorp.com/content/upload/files/press_releases…

Bitte zukünftig hier entsprechend dem Threadtitel

"LYNAS - Faktenthread, Analysen, Querverweise u. Meldungen zum Unternehmen"

Posten.

Im Thread: LYNAS - auf dem Weg zu einem Rohstoffproduzent von Hightech-Rohstoffen kann weiterhin nach herzenslust gepostet werden und ich werde dort auch weiterhin posten.

Gruß JoJo

LYNAS CORP. LTD. REGISTERED SHARES O.N. (871899) AU000000LYC6

Eine besonders ergiebige Lagerstätte, die vom Unternehmen Lynas Corporation erschlossen wird, ist das Mt. Weld-Projekt in West-Australien. Lynas Corporation (Börsenkürzel: LYC.AX) ist in den letzten Zügen der Entwicklung der Mt Weld Mine, wird jedoch die Produktion nach Malaysia verlagern, um die aktuellen chinesischen Exportzölle von 10 % zu vermeiden. Da China mittlerweile die Produktion zurückgefahren hat, sind die durchschnittlichen Preisanstiege von über 60 % bei den "Seltenen Elementen" kein Zufall.

Das Mt Weld-Projekt von Lynas mit nachgewiesenen Reserven von über 2 Millionen Tonnen kann die Lücke zwischen Angebot und Nachfrage in den nächsten Jahren schließen. Geht man von zukünftigen Preisen von etwa 10 bis 15 USD/kg REO aus, so dürften die bisherigen Reserven von Lynas bei einem Reinheitsanteil von konservativ geschätzten 15 bis 20 % alleine 2 Milliarden USD wert sein. Bei noch höheren Reinheitsgraden und Preisen um 20 bis 25 USD könnten die Lynas-Reserven sogar bis zu 5 Milliarden USD wert sein. Dies allein würde Aktienkurse von etwa 3 bis 5 AUD (aktuell 0.6 AUD) in diesem Wert rechtfertigen. Wenn es keine Verzögerungen gibt, sollte Lynas bereits ab dem Jahr 2010 etwa 10.000 Tonnen pro Jahr, d.h. 10 % der weltweiten Nachfrage liefern können. Bis zum Jahr 2015 könnte dieser Anteil auf über 15 % ansteigen.

Die Mt. Weld Lagerstätten (ca 25 % Lanthanoxide, cac. 45 % Ceroxide sowie 20 % Neodymoxide) sind die weltweit größte Fundstätte von "Seltenen Elementen", wobei diese sogar in der Lage wären über einen Zeitraum von 30 Jahren 20 % der weltweiten Nachfrage zu decken. Somit dürfte Lynas in den nächsten Jahren in der Spitze etwa 75 bis 100 Millionen USD pro Jahr verdienen. Aktuell beträgt die Börsenkapitalisierung etwa 190 Millionen USD. Dies entspräche, wenn der heutige Kurs herangezogen wird, in etwa einem Kurs-/-Gewinn-Verhältnis von 1,4 bis 2,7. Besonders interessant an der Strategie von Lynas ist, dass das Unternehmen die vertikale Integration vorantreibt. Es will nicht nur als einer der weltweit größten Lieferanten, sondern auch als Weiterverarbeiter auftreten. Zur Absicherung dieser Strategie hat Lynas einen langfristigen Liefervertrag mit dem französischen Spezialchemieunternehmen Rhodia abgeschlossen.

"Seltene Elemente" werden oft als Nebenprodukt von schweren Sänden gefunden, die Titan beinhalten, was vor allem in Australien der Fall ist. Zusätzliches Potential dürfte Lynas deshalb das Crown Polymetallic Resource-Projekt im Mt. Welt-Abbaugebiet geben, enthält es doch große Ansammlungen von Niob (Legierungszusatz für rostfreie Stähle, Einsatz in der Nukleartechnik), Tantal (Einsatz in Kondensatoren), Zirkonium (Einsatz im Reaktorbau und bei Brennstoffzellen) sowie Titan (Einsatz im Flugzeugbau).

Hightech-Rohstoffe

Im United States Geological Survey (USGS) wird hervorgehoben, dass "Seltene Elemente" einer der kritischen Schlüsselfaktoren für die Hightech-Industrien sind. Wenn die Nachfrage wie erwartet mehr als 10 % steigen sollte, so könnte es eine ernsthafte Knappheit geben, die die Weltmarktpreise für REEs deutlich ansteigen lassen wird.

Abhängigkeit der Hightech-Industrien von "Seltenen Elementen"

Artur P. Schmidt 09.02.2007

Australien greift Chinas heimliches Rohstoff-Monopol an

Auch wenn viele meinen, die Rohstoffhausse sei zu Ende, so lässt sich heute schon prognostizieren, dass die verstärkte Nachfrage aus China und Indien in zahlreichen Commodity-Marktsegmenten zu starken Knappheiten führen wird. Von der Öffentlichkeit kaum wahrgenommen hat China in den letzten beiden Jahrzehnten eine führende Position im Bereich der "Seltenen Elemente", den sogenannten "Rare Earth Elements" (REE), aufgebaut.

Globale Produktion von "Seltenen Element"-Oxiden. Grafik: USGS

"Seltene Elemente", auch Lanthanoide (Lanthanähnliche) genannt, ist eine Gruppenbezeichnung ähnlicher Elemente mit den Atomnummern 57 bis 71, zu denen das Lanthan und die 14 im Periodensystem folgenden Elemente Cer, Praseodym, Neodym, Promethium, Samarium, Europium, Gadolinium, Terbium, Dysprosium, Holmium, Erbium, Thulium, Ytterbium und Lutetium zählen. Obwohl die 15 "Seltenen Elemente" meistens zusammen auftreten, werden diese in zwei Gruppen unterteilt: die leichten und mittelschweren (Atomnummern 57 bis 64) und die schweren (Atomnummern 65 bis 71) Elemente. Zu den Lanthaniden werden auch noch die Atomnummern 21 (Scandium) sowie 39 (Yttrium) gezählt. Der Gehalt an "Seltenen Elemente" wird ausgedrückt durch den Begriff "Rear-Earth-Oxide" (REO) oder "Total Rare Earth Oxide" (TREO).

Die Lanthanoide sind silbrig-glänzende, relativ weiche und reaktionsfreudige Metalle. An der Luft oxidieren sie schnell und werden matt. Im Wasser erfolgt die Zersetzung mehr oder weniger schnell unter Freisetzung von Wasserstoffgas. Wegen ihren ähnlichen physikalischen und chemischen Eigenschaften treten die "Seltenen Elemente" und Yttrium meist gemeinsam in der Natur auf. Der Begriff "Erden" bezieht sich hierbei auf die jeweiligen Oxide. Während das betroffene Element die Endung "-ium" erhielt, wurde für das zugehörige Oxid die Endung "-ia" verwendet (Beispiel: Element "Yttrium", das zugehörige Oxid wurde "Yttria" genannt, zu deutsch "Yttererde"). Die häufigsten und ökonomisch wichtigsten lanthanoidführenden Minerale sind: Monazit, Xenotim, Bastnäsit, Parisit, Allanit, Synchysit, Ancylit sowie Cerianit. Die weltweite Produktion von "Seltenen Elementen" beträgt etwa 100.000 Tonnen Rare Earth Oxyde (REO) pro Jahr. Von Yttrium wird jährlich nur etwa 2,500 Tonnen Yttrium Oxid (Y2O3) produziert.

Hightech-Rohstoffe

Im United States Geological Survey (USGS) wird hervorgehoben, dass "Seltene Elemente" einer der kritischen Schlüsselfaktoren für die Hightech-Industrien sind. Wenn die Nachfrage wie erwartet mehr als 10 % steigen sollte, so könnte es eine ernsthafte Knappheit geben, die die Weltmarktpreise für REEs deutlich ansteigen lassen wird.

"Seltene Elemente" spielen eine Schlüsselrolle für die Elektronikindustrie (Magnetische Kühlung), die Telekommunikation (Glasfaserkabel), die Mikrosystemtechnik (hochfeste Präzisionsbauteile), den Automobilbau (Hybridantriebe), den Umweltschutz (Emissionskontrolle) sowie die Petrochemie (Prozesskatalysatoren). Eine besonders hohe Nachfrage wird nach Cerium in Automobilkatalysatoren und Lathanum in NiMH-Batterien erwartet. Aber auch die Nachfrage von "Seltenen Elementen" beim Einsatz von Phosphor, Glasfasern und Keramiken dürfte die Preise weltweit nach oben treiben. Viele Komponenten wie Batterien, Magneten, Bildschirme werden durch "Seltene Elemente" immer leistungsfähiger und wirken hierbei nachfrageerhöhend.

Was viele "Seltene Elemente" so schwer und teuer abbaubar macht ist, dass diese oftmals zusammen mit strahlendem Material auftreten. Deshalb sind die Preise so verschieden. Während Cerium Oxid etwa 1,6 USD per kg kostet, liegen die Preise für Terbium Oxid bei über 400 USD pro kg.

Seltene Elemente", die sogenannten "Rare Earth Elements" (REE)

Globale Produktion von "Seltenen Element"-Oxiden. Grafik: USGS

Die Abhängigkeit vieler Industrieländer, vor allem den USA, von REEs aus China ist heute nahezu perfekt, insbesondere da die USA nur in Kalifornien (Mountain Pass) und in Wyoming (Bear Lodge) über nennenswerte Reserven verfügen, die dort vom Unternehmen Rare Element Resources (Börsenkürzel: RES.V) abgebaut werden. Während sich die USA im Jahr 1990 noch selbst mit "Seltenen Rohstoffen" versorgen konnte, ist das Land heute zu 90 % von Importen aus China abhängig.

Sich vom chinesischen Quasi-Monopol zu befreien, ist deshalb nur möglich, wenn alternative Anbieter, die über nennenswerte Reserven verfügen, wie Lynas und Arafura, schnellstmöglich in die Abbauphase übergehen. Mit bisher nachgewiesenen Reserven von über 2 Millionen Tonnen kann Lynas zu einer ernsthaften Konkurrenz für die Chinesen avancieren. Wenn es keine Verzögerungen gibt, sollte Lynas Corporation bereits ab dem Jahr 2010 etwa 10.000 Tonnen pro Jahr, d.h. 10 % der weltweiten Nachfrage liefern können. Der andere Key Player Arafura Resources verfügt ebenfalls über erheblichen Reserven an "Seltenen Elementen".

http://www.lynascorp.com/page.asp?category_id=8&page_id=26&q…

http://www.lynascorp.com/

http://www.heise.de/tp/r4/artikel/24/24602/1.html

LYC- Präsentation:

http://sa.iguana2.com/cache/0949095dbdc89bd569294cc1547ca924…

Halbjahresbericht:

http://sa.iguana2.com/cache/daee94345721feced262feb9f050bdcc…

Börsenplatz:

http://www.asx.com.au/asx/research/ChartsSearchAndResults.js…

http://www.rohstoff-spiegel.de/count.php?url=rs_2007-4.pdf&l…

Artikel über die Situation bei REO`s , betrifft auch Lynas:

http://www.goldseiten.de/content/diverses/artikel.php?storyi…

eine Studie die im Auftrag von Lynas angefertigt wurde:

http://www.lynascorp.com/content/upload/files/press_releases…

- Anwendungsbereiche von Rare Earth Produkten, insbesondere Highend-Magnete

- Entwicklungen in der Industrie

- Faktor China (produzieren dort), Exportsteuer für REE

http://www.robtv.com/shows/past_archive.tv

Why Rare Earth Prices are Likely to Continue Their Upward TrendMagnetics2007 ConferenceApril 4-5, 2007Chicago, IllinoisPresented byWalter T. BeneckiConsultant to the Worldwide Magnetics Industry

http://www.waltbenecki.com/uploads/Why_Rare_Earth_Prices_are…

http://www.lynascorp.com/content/upload/files/press_releases…

Bitte zukünftig hier entsprechend dem Threadtitel

"LYNAS - Faktenthread, Analysen, Querverweise u. Meldungen zum Unternehmen"

Posten.

Im Thread: LYNAS - auf dem Weg zu einem Rohstoffproduzent von Hightech-Rohstoffen kann weiterhin nach herzenslust gepostet werden und ich werde dort auch weiterhin posten.

Gruß JoJo

http://www.lynascorp.com/

Foundations for the Future

Lynas has a strategy of creating a reliable, fully integrated source of supply from mine through to customers, and to become the benchmark for security of supply and environmental standards in the global Rare Earths industry.

Lynas owns the richest deposit of Rare Earths in the world at Mt Weld, 35km south of Laverton in Western Australia. A feasibility study has been completed on the Rare Earths deposit and all Australian approvals required for project development have been received.

Over the last year Lynas has observed a trend in Chinese Government policy decisions which is leading to an increase in Government control of the Rare Earths industry in China and the tightening of supply due to the imposition of mining production quotas, and the reduction and restrictions on trading of the existing export quota. These policy decisions have followed the removal of VAT rebates for exports of Rare Earths oxides and an increased enforcement of China's stringent environmental standards which resulted in the closure of non-compliant Rare Earths plants.

Shortly after the introduction of production quotas in China the company determined it was prudent to investigate potential sites other than China that would be suitable for the company's proposed processing plant for Mt Weld ore. The drivers for this decision were the:

Increasing Government control of the Rare Earths industry in China, thereby increasing the project risk for our plant

Escalating operating costs in China due to the Government policies noted above, and also inflation affecting cost of reagents, utilities and labour

Favourable tax environments available in alternative countries

Opportunity to reduce cost base denominated in Renminbi, and thereby benefit from a strengthening Chinese currency

Following a detailed evaluation of several possible sites Kemaman, East Coast of Malaysia, was chosen due to the favourable investment climate, the high quality workforce and the excellent infrastructure servicing the proposed site.

Lynas has submitted an application to the Malaysian authorities to locate the plant in the Teluk Kalong Industrial Estate in Kemaman, within the State of Terengganu on the East Coast of Malaysia, and also an application to the Malaysian Industrial Development Association (MIDA) for 'strategic pioneer status', which has a number of associated benefits including a 10 year tax free period.

Kemaman offers a highly skilled, educated, diligent yet competitive labour force. Communication in English is a key benefit and many people in Kemaman's workforce are also fluent in Mandarin, which will make it easy to integrate the company's current engineering staff from China.

The East Coast of Malaysia has a robust and first-class transport network, comprehensive communications networks and reliable supply of natural gas, electricity and water at prices more competitive than China. Kemaman has excellent all weather deep water port facilities for handling bulk shipment of Mt Weld ore and also liquid chemical handling facilities.

Of significant advantage for the Teluk Kalong Industrial Estate site is the fact that manufacturers of key reagents required for the process (lime, sulfuric acid, and hydrochloric acid) are already established in close proximity to the proposed plant site.

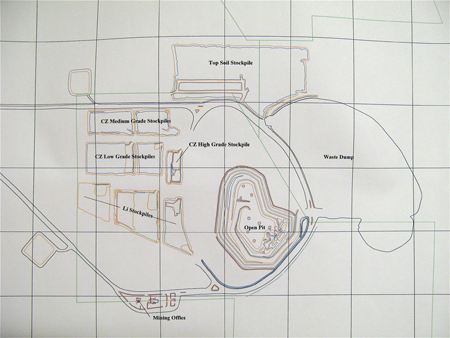

Lynas' Mt Weld tenement also has a JORC compliant polymetallic resource known as the "Crown" deposit. This is a titanium and niobium-rich rare metals resource that is a separate deposit to the Mount Weld Rare Earths deposit

Mt Weld

Mt Weld Rare Earths Oxide (REO) deposit known as the ‘Central Lanthanide Deposit’ (CLD) is without a doubt the world’s richest Rare Earths ore body, easily capable of supplying up to 20% of the global market for 30 years.

In addition to the world class Rare Earths Oxide (REO) deposit, the Mt Weld carbonatite is also host to a JORC compliant polymetallic resources known as the “Crown” deposit. This is a titanium and niobium-rich rare metals resource that is a separate deposit to the Mt Weld Rare Earths deposit.

The main deposits are hosted within the soil / regolith horizon that blankets the entire carbonatite, and form shallow lenses and sheets generally within 60m of the surface. The most important REO deposit defined to date, the Central Lanthanide Deposit (CLD) is located at the centre on the carbonatite, with the polymetallic and other deposits generally located towards the outer fringes.

http://www.rohstoffwelt.de/aktien/snapshot.php?isin=AU000000…

http://www.rohstoffwelt.de/aktien/kursliste.php?klid=19#Selt…

Gruß JoJo

Crown Polymetallic Resource.

As well as Rare Earths, the Mt Weld carbonatite is host to potentially economic deposits of niobium, tantalum, zirconium, and titanium, collectively termed polymetallic by Lynas.

A number of drilling programs have been conducted aimed specifically at the Crown Polymetallic deposit and its niobium and tantalum resource definition. A scoping study has identified an open pit mine followed by a conceptual process route, based on existing technology, located in China to produce the Polymetallic product suite.

Dr Phillip Hellman of Hellman & Schofield Pty Ltd, Sydney, completed the multi-metal geostatistical resource estimation study.

The Indicated and Inferred Resources estimated for the Polymetallic Crown deposit total 37.7 million tonnes with an average ore composition as presented in the table below. The majority of the ore lies between 30m and 60m in depth, suitable for open pit mining.

A large proportion of the value in the resource is in the niobium which has an average grade 1.07% Nb2O5 (niobium oxide). Taking into account the credits for the other Rare Metals and by-products the equivalent niobium oxide mine grade is 2.1%.

Polymetallic mineral Resources for Coors and Crown Sectors, Mt Weld

Mt = million tonnes, other figures are percentages. Ta2O5 tantalum oxide, Nb2O5 niobium oxide, TLnO rare earth oxide, ZrO2 zirconia, Fe2O3 iron oxide, P2O5 phosphate, Y2O3 yttria, Al2O3 alumina, TiO2 titanium oxide

The Mt Weld Resource is potentially the world’s second largest Nb2O5 resource (ranked by contained niobium metal) compared to the resources of existing commercial operations which include:

CBMM’s Araxa deposit in Brazil, with 460 million tonnes grading 2.5% Nb2O5 supplies over 80% of the world niobium market,

Mineracao Catalao de Goias Ltd’s (Anglo American plc) deposit in Brazil totalling approximately 18 million tonnes at an average of 1.34% Nb2O5, and

Niobec Inc’s Canadian underground deposit of 24 million tonnes at 0.65% Nb2O5

Given the size of the resource and the economic and technical strength of the scoping study, the next step for the Polymetallic Crown deposit is commencement of a feasibility study. This will be deferred until after the development of the Rare Earths project.

http://www.lynascorp.com/page.asp?category_id=2&page_id=5

Alle News wie immer sind über australische ASX oder bei LYC direkt abfragbar.

http://www.asx.com.au/asx/research/CompanyInfoSearchResults.…

http://www.lynascorp.com/

http://www.asx.com.au/asx/statistics/showAnnouncementPDF.do?…

http://www.asx.com.au/asx/statistics/showAnnouncementPDF.do?…

http://www.asx.com.au/asx/statistics/showAnnouncementPDF.do?…

usw.

allen Anlegern ein schönen - 1.Mai -

Gru JoJo

Why Rare Earth Prices are Likely to Continue Their Upward Trend

Magnetics2007 ConferenceApril 4-5, 2007Chicago, Illinois

Presented byWalter T. Benecki

Consultant to the Worldwide Magnetics Industry

http://www.waltbenecki.com/uploads/Why_Rare_Earth_Prices_are…

http://www.waltbenecki.com/index.html

http://www.waltbenecki.com/presentations.html

allen Anleger ein chönes Wochenende und weiterhin viel Erfolg

Gruß JoJo

Magnetics2007 ConferenceApril 4-5, 2007Chicago, Illinois

Presented byWalter T. Benecki

Consultant to the Worldwide Magnetics Industry

http://www.waltbenecki.com/uploads/Why_Rare_Earth_Prices_are…

http://www.waltbenecki.com/index.html

http://www.waltbenecki.com/presentations.html

allen Anleger ein chönes Wochenende und weiterhin viel Erfolg

Gruß JoJo

Nun wurde in den letzten Tagen so viel über fallende Kurse spekuliert, und wenn es dann in Australien unerwartet gut aussieht, ist es hier völlig ruhig...

Trading Spotlight

Antwort auf Beitrag Nr.: 29.183.323 von Mhoopisblues am 07.05.07 09:53:21Ach, das tut mir leid - falscher Thread. Kann man das Posting wieder löschen?

Antwort auf Beitrag Nr.: 29.183.384 von Mhoopisblues am 07.05.07 09:56:25Nicht nötig, irren ist menschlich...

Dazu noch ein Bericht zur REO-Verwendung -HANDELSBLATT, Samstag, 5. Mai 2007, 14:28 Uhr - Umfrage -

Titel: Viele wollen Hybridautos kaufen

(gehört auch nicht hierher, aber intereesante Info bis News kommen)

http://www.handelsblatt.com/news/Auto/Auto-News/_pv/_p/20591…

allen Anleger eine erfolgreiche Woche

Gruß JoJo

Dazu noch ein Bericht zur REO-Verwendung -HANDELSBLATT, Samstag, 5. Mai 2007, 14:28 Uhr - Umfrage -

Titel: Viele wollen Hybridautos kaufen

(gehört auch nicht hierher, aber intereesante Info bis News kommen)

http://www.handelsblatt.com/news/Auto/Auto-News/_pv/_p/20591…

allen Anleger eine erfolgreiche Woche

Gruß JoJo

Damit wird LYC weiter kontinuierlich steigen ....

http://www.lynascorp.com/content/upload/files/Announcements/…

Corporate Office Telephone: +61 2 8259 7100

Level 7 Facsimile: +61 2 8259 7199

56 Pitt Street Website: www.lynascorp.com

Sydney NSW 2000 ACN: 009 066 648

AUSTRALIA

15 May 2007

New Price Increases Initiated by Rare Earths Supply Limitations

Highlights

http://www.lynascorp.com/content/upload/files/Announcements/…

Corporate Office Telephone: +61 2 8259 7100

Level 7 Facsimile: +61 2 8259 7199

56 Pitt Street Website: www.lynascorp.com

Sydney NSW 2000 ACN: 009 066 648

AUSTRALIA

15 May 2007

New Price Increases Initiated by Rare Earths Supply Limitations

Highlights

Das neuste Posting aus dem ARU-Thread vom User "sunsuyo"

den ich für so wichtig ud informativ halte, dass ich Ihn hier auch poste.

Danke sunsuyo

Zum Thema Produktionsstopps in China und Preiserhöhungen für REO sowie Wiederaufnahme der Produktionsaufnahme von Mountain Pass erhellt vielleicht ein kleiner Rückblick und Einblick in die Gründe, die zur Wiedereröffnung der Molycorp-Mine führten – die zum Unocal-Konzern gehört.

Der Aspekt „strategische Ressourcen“ ist ja gerade bei REE-Vorkommen in letzter Zeit immer öfters hervorgehoben worden. Auch hier im Thread wurden dazu bereits viele Anmerkungen und Querverweise gepostet.

Auch dass mittlerweile in den USA die Alarmglocken klingeln, wenn es um nationale REE Vorkommen geht, wird dem aufmerksamen Leser unschwer entgangen sein.

Dass dieser Aspekt aber offenbar gerade für US-Militärstrategen einen so herausragenden Stellenwert hat, war mir nicht so deutlich bekannt. Bis ich zufälligerweise auf ein Posting in einem US-Board stieß, das von eher national-konservativen Gesinnungsgenossen frequentiert wird. Doch das ist weniger der Punkt.

Besagtes Posting enthält nämlich den Text eines Vortrags (Testimony), den ein gewisser Frank J. Gaffney, Jr., seines Zeichens President and C.E.O. des Center for Security Policy, Wash. DC, vor dem House Armed Services Committee des US-Kongresses am 13.07.2005 gehalten hat, und zwar anlässlich eines Congressional Hearings zur damals geplanten Übernahme von Unocal durch die Chinesen.

Ich hatte immer angenommen, der Deal sei letztlich gescheitert, weil die Amerikaner um ihre Ölressourcen fürchteten. Doch angesichts des relativ bescheidenen Anteils von Unocal am Gesamtvolumen der Ölreserven aller US-Gesellschaften weltweit war das vielleicht überhaupt nicht der entscheidende Punkt.

Hier das Posting - siehe Absatz im Testimony:

Unocal: The Last American Source of Rare Earth Minerals

http://www.freerepublic.com/focus/f-news/1443737/posts

(sorry, habe leider keine Zeit zu einer Übersetzung.)

Ich möchte mich nicht zu der erschreckend engen Weltsicht äußern, die hier vor immerhin sehr wichtigen Mitgliedern des Kongresses vorgetragen wurde… …nur noch ein paar Gedanken zum angesprochenen Thema hinzufügen.

Bezogen auf die weltweiten REE-Ressourcen ist m.E. gerade dieser Vortrag ein eye-opener. Im Pentagon und sonstwo werden sich längst Expertenteams dieses Themas angenommen haben. China wird die US-Bedenken sehr gut kennen und hat vielleicht sogar aus diesem Grund (militärisch-strategisch) seine begrenzten REE-Ressourcen (vielleicht begrenzter als bisher vom Westen angenommen?) den bekannten Ausfuhreinschränkungen und Produktionsstopps unterworfen (wir wissen, dass die Chinesen den Umfang ihrer eigenen Rohstoffvorkommen bis vor kurzem eher immer großzügig bemessen haben, um das Ausland zu verwirren und so ihre Einkaufspreise niedrig zu halten). Ist bei REE nun aber das Ganze für China womöglich überhaupt gar keine Frage des Preises mehr, sondern längst eine der „nationalen Sicherheit“ geworden?

Auf der einen Seite also die USA mit ihrer knappen, wertvollen (und daher mit allen Mitteln zu schützenden) Mountain Pass Ressource, auf der anderen China, dito mit Batou usw. Russland wird es nicht anders verfahren. Dass die USA jetzt Japan die Offerte machen, an der Ausbeute von Mountain Pass teilzunehmen, hat m.E. ausschließlich besagte strategisch-militärische Gründe (Bündnispolitik). Wahrscheinlich wird man auch nicht auf Teufel komm raus fördern – aus beschriebenen strategischen Gesichtspunkten, zudem dürfte die Umweltthematik dort ebenfalls nicht völlig vom Tisch sein. Insofern kann ich mir nicht vorstellen, dass Mountain Pass eine Bedrohung für zukünftig deutlich höhere REO-Preise darstellen wird.

Wie werden sich aber Australien und Kanada in Bezug auf ihre nationalen Ressourcen verhalten? Bleiben die Ressourcen von Mt. Weld und Nolans Bore auch in Zukunft offen zur kommerziellen Erschließung? Oder werden wir irgendwann auch hier Einschränkungen aus Gründen des „nationalen Sicherheitsinteresses“ erleben?

Letzteres denke ich nicht, da weder Australier noch Kanadier eine nennenswerte eigene High-Tech-Fertigungsindustrie haben, also auf die Länder der „freien Welt“ als Abnehmer setzen müssen. Das stimmt mich eigentlich ungemein positiv im Hinblick auf die Zukunft von ARU.

Wie auch immer, die Sache bleibt spannend in jeder Hinsicht.

sunsuyo

Gruß JoJo

den ich für so wichtig ud informativ halte, dass ich Ihn hier auch poste.

Danke sunsuyo

Zum Thema Produktionsstopps in China und Preiserhöhungen für REO sowie Wiederaufnahme der Produktionsaufnahme von Mountain Pass erhellt vielleicht ein kleiner Rückblick und Einblick in die Gründe, die zur Wiedereröffnung der Molycorp-Mine führten – die zum Unocal-Konzern gehört.

Der Aspekt „strategische Ressourcen“ ist ja gerade bei REE-Vorkommen in letzter Zeit immer öfters hervorgehoben worden. Auch hier im Thread wurden dazu bereits viele Anmerkungen und Querverweise gepostet.

Auch dass mittlerweile in den USA die Alarmglocken klingeln, wenn es um nationale REE Vorkommen geht, wird dem aufmerksamen Leser unschwer entgangen sein.

Dass dieser Aspekt aber offenbar gerade für US-Militärstrategen einen so herausragenden Stellenwert hat, war mir nicht so deutlich bekannt. Bis ich zufälligerweise auf ein Posting in einem US-Board stieß, das von eher national-konservativen Gesinnungsgenossen frequentiert wird. Doch das ist weniger der Punkt.

Besagtes Posting enthält nämlich den Text eines Vortrags (Testimony), den ein gewisser Frank J. Gaffney, Jr., seines Zeichens President and C.E.O. des Center for Security Policy, Wash. DC, vor dem House Armed Services Committee des US-Kongresses am 13.07.2005 gehalten hat, und zwar anlässlich eines Congressional Hearings zur damals geplanten Übernahme von Unocal durch die Chinesen.

Ich hatte immer angenommen, der Deal sei letztlich gescheitert, weil die Amerikaner um ihre Ölressourcen fürchteten. Doch angesichts des relativ bescheidenen Anteils von Unocal am Gesamtvolumen der Ölreserven aller US-Gesellschaften weltweit war das vielleicht überhaupt nicht der entscheidende Punkt.

Hier das Posting - siehe Absatz im Testimony:

Unocal: The Last American Source of Rare Earth Minerals

http://www.freerepublic.com/focus/f-news/1443737/posts

(sorry, habe leider keine Zeit zu einer Übersetzung.)

Ich möchte mich nicht zu der erschreckend engen Weltsicht äußern, die hier vor immerhin sehr wichtigen Mitgliedern des Kongresses vorgetragen wurde… …nur noch ein paar Gedanken zum angesprochenen Thema hinzufügen.

Bezogen auf die weltweiten REE-Ressourcen ist m.E. gerade dieser Vortrag ein eye-opener. Im Pentagon und sonstwo werden sich längst Expertenteams dieses Themas angenommen haben. China wird die US-Bedenken sehr gut kennen und hat vielleicht sogar aus diesem Grund (militärisch-strategisch) seine begrenzten REE-Ressourcen (vielleicht begrenzter als bisher vom Westen angenommen?) den bekannten Ausfuhreinschränkungen und Produktionsstopps unterworfen (wir wissen, dass die Chinesen den Umfang ihrer eigenen Rohstoffvorkommen bis vor kurzem eher immer großzügig bemessen haben, um das Ausland zu verwirren und so ihre Einkaufspreise niedrig zu halten). Ist bei REE nun aber das Ganze für China womöglich überhaupt gar keine Frage des Preises mehr, sondern längst eine der „nationalen Sicherheit“ geworden?

Auf der einen Seite also die USA mit ihrer knappen, wertvollen (und daher mit allen Mitteln zu schützenden) Mountain Pass Ressource, auf der anderen China, dito mit Batou usw. Russland wird es nicht anders verfahren. Dass die USA jetzt Japan die Offerte machen, an der Ausbeute von Mountain Pass teilzunehmen, hat m.E. ausschließlich besagte strategisch-militärische Gründe (Bündnispolitik). Wahrscheinlich wird man auch nicht auf Teufel komm raus fördern – aus beschriebenen strategischen Gesichtspunkten, zudem dürfte die Umweltthematik dort ebenfalls nicht völlig vom Tisch sein. Insofern kann ich mir nicht vorstellen, dass Mountain Pass eine Bedrohung für zukünftig deutlich höhere REO-Preise darstellen wird.

Wie werden sich aber Australien und Kanada in Bezug auf ihre nationalen Ressourcen verhalten? Bleiben die Ressourcen von Mt. Weld und Nolans Bore auch in Zukunft offen zur kommerziellen Erschließung? Oder werden wir irgendwann auch hier Einschränkungen aus Gründen des „nationalen Sicherheitsinteresses“ erleben?

Letzteres denke ich nicht, da weder Australier noch Kanadier eine nennenswerte eigene High-Tech-Fertigungsindustrie haben, also auf die Länder der „freien Welt“ als Abnehmer setzen müssen. Das stimmt mich eigentlich ungemein positiv im Hinblick auf die Zukunft von ARU.

Wie auch immer, die Sache bleibt spannend in jeder Hinsicht.

sunsuyo

Gruß JoJo

Seltenerdmetalle: Nützliche Kobolde der Zukunftstechnologie

23.05.2007 | 10:31 Uhr | Hans Jörg Müllenmeister (Müllenmeister)

über REE/ARU u. LYC und deren Zukunftperspektieven...

u.A. auch:

Auch das beachtenswerte Unternehmen Lynas Corporation Ltd. (WKN: 871 899) in West-Australien ist auf dem Weg zum Großproduzenten. Lynas strebt an, auch der weltgrößte Weiterverarbeiter an SE zu werden. Insgesamt räume ich den Seltenerdmetallen über Jahre eine nachhaltige Performance ein, vielleicht mit dem Überraschungseffekt, daß der Bedarf in dem Maße steigt wie neue High-tech-Anwendungen in Industrie und Forschung erschlossen werden. Nicht auszudenken, wenn die Edelmetalle in einigen Jahren ihren Zenit erreichen und die SE-Perlen in ihrem Depot neuen, strahlenden Glanz verbreiten.

http://www.rohstoffwelt.de/news/artikel.php?sid=776#Seltener…

Zum Thema:

REE spielt eine Hauptrolle bei den Katalysatoren, die in den modernen Erdölraffinerien benutzt werden.

Lanthan und Cer dienen, die Struktur und die Chemie der hohen Flächezeolith zu stabilisieren, die als molekularer Filter benutzt werden.

Refining the Oil Industry (Click here to see flash animation)

Fluid Cracking Catalysts (FCC) are used in the refining operation of crude oil and is the major contributor to “value-add” in the refining process. The process enables the transformation of heavy molecules into lighter compounds that make up gasoline and other fuels such as gas, jet fuel and diesel.

Rare Earths play a major role in the catalysts used in modern petroleum refineries. Lanthanum and cerium serve to stabilise the structure and chemistry of the high surface area zeolites used as a molecular filter.

The market is driven by oil consumption and the quality of oil being refined; heavy oils and tars require an increased amount of rare earths compared to sweet light oils. As crude from oil sands and shale are increasingly used, the amount of FCC used per barrel of oil will increase.

Demand of Rare Earths for Fluid Cracking Catalysts:

Rare Earths used in Fluid Cracking Catalyst:

und weitere Anwendungen ...

http://www.lynascorp.com/application.asp?category_id=1&page_…

allen schöne Pfingstfeiertage und weiterhin viel Erfolg

Gruß JoJo

Neue REE-Preisliste von LYC 28.05.2007

Anmerkung: Millitorr Schweißung Verteilung zählt 98.9%, die Balance besteht Gadolinium, Holmium, Erbium und Yttriumoxide zusammen. Regelmäßige Preiskalkulation Informationen sind nicht für diese Metalle vorhanden.

Der vierteljährliche durchschnittliche Preis für den Millitorr Schweißung Aufbau der seltenen Masse hat 76% von US$5.07/kg für das Periode Ende Q1 2006 auf US$8.93/kg für das Periode Ende Q1 2007 erhöht.

http://translate.google.com/translate?sourceid=navclient&hl=…

Datum Letztes % änderung Hoch Niedrig Vol. *

28. Mai 2007 1.075 5.91% 1.075 1.000 4,258,854

http://translate.google.com/translate?sourceid=navclient&hl=…

Gruß JoJo

Anmerkung: Millitorr Schweißung Verteilung zählt 98.9%, die Balance besteht Gadolinium, Holmium, Erbium und Yttriumoxide zusammen. Regelmäßige Preiskalkulation Informationen sind nicht für diese Metalle vorhanden.

Der vierteljährliche durchschnittliche Preis für den Millitorr Schweißung Aufbau der seltenen Masse hat 76% von US$5.07/kg für das Periode Ende Q1 2006 auf US$8.93/kg für das Periode Ende Q1 2007 erhöht.

http://translate.google.com/translate?sourceid=navclient&hl=…

Datum Letztes % änderung Hoch Niedrig Vol. *

28. Mai 2007 1.075 5.91% 1.075 1.000 4,258,854

http://translate.google.com/translate?sourceid=navclient&hl=…

Gruß JoJo

LYNAS schließt den ersten 5-Jahres-Liefervertrag über 10.500 t REE mit einem Wert von über 90 Mill. $ ab.

Corporate Office Telephone: +61 2 8259 7100

Level 7 Facsimile: +61 2 8259 7199

56 Pitt Street Website: www.lynascorp.com

Sydney NSW 2000 ACN: 009 066 648

AUSTRALIA

30 May 2007

Lynas Signs First Rare Earths Supply Contract

Key Points:

• First supply contract signed for Mt Weld Rare Earths project

• Value of contract is in excess of US$90M

• Five year contract sets new benchmark in Rare Earths industry

• Additional customer negotiations progressing well to migrate Letters of Intent to supply contracts

Lynas Corporation Limited (“Lynas”) (ASX code LYC) is pleased to announce the signing of the first supply contract with a significant Rare Earths customer for the supply of Mt Weld Rare Earths to be produced from the company’s Malaysian processing plant.

The company has been able to offer a long term five year contract as the Mt Weld Rare Earths project and processing plant in Kemaman, Malaysia are not restricted by production or export quotas, which are associated with the present industry supply sources. This represents a new benchmark for the security of supply in the Rare Earths market and is welcomed by customers at a time when demand is increasing strongly but supply is restricted and ever more uncertain.

The contract has a value in excess of US$90M over five years based on current prices. Of the initial 10,500 tonnes production target of Mt Weld Rare Earth Oxides (REO) the contract accounts for, at a minimum, approximately one third of the volume and due to the product mix fifteen percent (15%) of the value.

The contracted sales account for a significant portion of the cerium and heavier Rare Earths, including europium and terbium, as well as other products such as lanthanum from the processing plant’s initial 10,500 tonnes REO capacity. The pricing structure of the contract includes a floor and ceiling price for the cerium and lanthanum sales.

Lynas’ Executive Chairman, Nicholas Curtis, believes that the signing of the contract is a key milestone for the company and the Mt Weld Rare Earths project:

“The market for Rare Earths continues to tighten as existing demand increases, important new applications using Rare Earths are developed and production in China is curtailed due to production quotas and environmental concerns.

“The development of the Mt Weld Rare Earths project has begun and the Board is delighted the company has signed the first long term supply agreement”, Mr Curtis said.

The company is actively engaging potential customers in Europe, Japan and the USA. As announced in the last quarterly report a number of Letters of Intent (LOI) have already been signed with customers and good progress is being made to turn these LOIs into supply contracts.

About Lynas Corporation

Lynas is the world’s only viable producer and processor of Rare Earths outside of China. The company owns the richest deposit of Rare Earths in the world at Mt Weld, near Laverton in Western Australia. The contractor is currently on site and is anticipated to break ground and begin mining on 7 June 2007. Production of Rare Earths from Lynas’ Malaysian processing plant is scheduled to commence in the second half of 2008.

‘Rare Earths’ is the term given to fifteen metallic elements known as the lanthanide series, plus yttrium. They are essential in the development and manufacturing of many modern technological products, from disc drives to flat panel displays, iPods and magnetic resonance imaging (MRI) scans. They also play a key role in green environmental products, from energy efficient compact fluorescent light bulbs (CFLs) to hybrid cars, automotive catalytic converters and wind turbine generators.

Lynas’ strategy is to create a reliable, fully integrated source of Rare Earths supply from the mine through to customers in the global Rare Earths industry. The company plans to become the benchmark for security of supply and a world leader in quality and environmental responsibility to an international customer base.

For further information please contact Nicholas Curtis on +61 (0)2 8259 7100 or visit www.lynascorp.com

http://www.lynascorp.com/content/upload/files/Announcements/…

Gruß JoJo

Corporate Office Telephone: +61 2 8259 7100

Level 7 Facsimile: +61 2 8259 7199

56 Pitt Street Website: www.lynascorp.com

Sydney NSW 2000 ACN: 009 066 648

AUSTRALIA

30 May 2007

Lynas Signs First Rare Earths Supply Contract

Key Points:

• First supply contract signed for Mt Weld Rare Earths project

• Value of contract is in excess of US$90M

• Five year contract sets new benchmark in Rare Earths industry

• Additional customer negotiations progressing well to migrate Letters of Intent to supply contracts

Lynas Corporation Limited (“Lynas”) (ASX code LYC) is pleased to announce the signing of the first supply contract with a significant Rare Earths customer for the supply of Mt Weld Rare Earths to be produced from the company’s Malaysian processing plant.

The company has been able to offer a long term five year contract as the Mt Weld Rare Earths project and processing plant in Kemaman, Malaysia are not restricted by production or export quotas, which are associated with the present industry supply sources. This represents a new benchmark for the security of supply in the Rare Earths market and is welcomed by customers at a time when demand is increasing strongly but supply is restricted and ever more uncertain.

The contract has a value in excess of US$90M over five years based on current prices. Of the initial 10,500 tonnes production target of Mt Weld Rare Earth Oxides (REO) the contract accounts for, at a minimum, approximately one third of the volume and due to the product mix fifteen percent (15%) of the value.

The contracted sales account for a significant portion of the cerium and heavier Rare Earths, including europium and terbium, as well as other products such as lanthanum from the processing plant’s initial 10,500 tonnes REO capacity. The pricing structure of the contract includes a floor and ceiling price for the cerium and lanthanum sales.

Lynas’ Executive Chairman, Nicholas Curtis, believes that the signing of the contract is a key milestone for the company and the Mt Weld Rare Earths project:

“The market for Rare Earths continues to tighten as existing demand increases, important new applications using Rare Earths are developed and production in China is curtailed due to production quotas and environmental concerns.

“The development of the Mt Weld Rare Earths project has begun and the Board is delighted the company has signed the first long term supply agreement”, Mr Curtis said.

The company is actively engaging potential customers in Europe, Japan and the USA. As announced in the last quarterly report a number of Letters of Intent (LOI) have already been signed with customers and good progress is being made to turn these LOIs into supply contracts.

About Lynas Corporation

Lynas is the world’s only viable producer and processor of Rare Earths outside of China. The company owns the richest deposit of Rare Earths in the world at Mt Weld, near Laverton in Western Australia. The contractor is currently on site and is anticipated to break ground and begin mining on 7 June 2007. Production of Rare Earths from Lynas’ Malaysian processing plant is scheduled to commence in the second half of 2008.

‘Rare Earths’ is the term given to fifteen metallic elements known as the lanthanide series, plus yttrium. They are essential in the development and manufacturing of many modern technological products, from disc drives to flat panel displays, iPods and magnetic resonance imaging (MRI) scans. They also play a key role in green environmental products, from energy efficient compact fluorescent light bulbs (CFLs) to hybrid cars, automotive catalytic converters and wind turbine generators.

Lynas’ strategy is to create a reliable, fully integrated source of Rare Earths supply from the mine through to customers in the global Rare Earths industry. The company plans to become the benchmark for security of supply and a world leader in quality and environmental responsibility to an international customer base.

For further information please contact Nicholas Curtis on +61 (0)2 8259 7100 or visit www.lynascorp.com

http://www.lynascorp.com/content/upload/files/Announcements/…

Gruß JoJo

Vom User Big Charly im Hauptthread gepostet und gehört m.E. auch hier gepostet.

Australien greift Chinas heimliches Rohstoff-Monopol an

2007-05-24 09:53:00

Seltene Erdmetalle vor starken Avancen?

Auch wenn viele meinen, die Rohstoffhausse sei zu Ende, so lässt sich heute schon prognostizieren, dass die verstärkte Nachfrage aus China und Indien in zahlreichen Commodity-Marktsegmenten zu starken Knappheiten führen wird. Von der Öffentlichkeit kaum wahrgenommen hat China in den letzten beiden Jahrzehnten eine führende Position im Bereich der “Seltenen Elemente“, den sogenannten “Rare Earth Elements“ (REE) aufgebaut.

- Was sind “Seltene Elemente“?

“Seltene Elemente“, auch Lanthanoide (Lanthanähnliche) genannt, ist eine Gruppenbezeichnung ähnlicher Elemente mit den Atomnummern 57 bis 71, zu denen das Lanthan und die 14 im Periodensystem folgenden Elemente Cer, Praseodym, Neodym, Promethium, Samarium, Europium, Gadolinium, Terbium, Dysprosium, Holmium, Erbium, Thulium, Ytterbium und Lutetium zählen. Obwohl die 15 “Seltenen Elemente“ meistens zusammen auftreten, werden diese in zwei Gruppen unterteilt: die leichten und mittelschweren (Atomnummern 57 bis 64) und die schweren (Atomnummern 65 bis 71) Elemente. Zu den Lanthaniden werden auch noch die Atomnummern 21 (Scandium) sowie 39 (Yttrium) gezählt., Der Gehalt an “Seltenen Elemente“ wird ausgedrückt durch den Begriff „Rear-Earth-Oxyd“ (REO) oder „Total Rare Earth Oxyd“ (TREO). Die Lanthanoide sind silbrig-glänzende, relativ weiche und reaktionsfreudige Metalle. An der Luft oxidieren sie schnell und werden matt. Im Wasser erfolgt die Zersetzung mehr oder weniger schnell unter Freisetzung von Wasserstoffgas. Wegen ihren ähnlichen physikalischen und chemischen Eigenschaften treten die “Seltenen Elemente“ und Yttrium meist gemeinsam in der Natur auf. Der Begriff "Erden" bezieht sich hierbei auf die jeweiligen Oxide. Während das betroffene Element die Endung "-ium" erhielt, wurde für das zugehörige Oxid die Endung "-ia" verwendet (Beispiel: Element "Yttrium", das zugehörige Oxid wurde "Yttria" genannt, zu deutsch "Yttererde"). Die häufigsten und ökonomisch wichtigsten lanthanoidführenden Minerale sind: Monazit Xenotim, Bastnäsit, Parisit, Allanit, Synchysit, Ancylit sowie Cerianit. Die weltweite Produktion von “Seltenen Elementen“ beträgt etwa 100,000 Tonnen Rare Earth Oxyde (REO) pro Jahr. Von Yttrium wird jährlich nur etwa 2,500 Tonnen Yttrium Oxid (Y2O3) produziert.

- Hightech-Rohstoffe

Im United States Geological Survey (USGS) wird hervorgeben, dass “Seltene Elemente“ einer der kritischen Schlüsselfaktoren für die Hightech-Industrien sind. Wenn die Nachfrage wie erwartet mehr als 10 % steigen sollte, so könnte es eine ernsthafte Knappheit geben, die die Weltmarktpreise für REEs deutlich ansteigen lassen wird. “Seltene Elemente“ spielen eine Schlüsselrolle für die Elektronik-industrie (Magnetische Kühlung), die Telekommunikation (Glasfaserkabel) die Mikrosystemtechnik (hochfeste Präzisionsbauteile), den Automobilbau (Hybridantriebe), den Umweltschutz (Emissionskontrolle) sowie in der Petrochemie (Prozesskatalysatoren). Eine besonders hohe Nachfrage wird nach Cerium in Automobilkatalysatoren und Lathanum in NiMH-Batterien erwartet. Aber auch die Nachfrage von “Seltenen Elementen“ beim Einsatz von Phosphor, Glasfasern und Keramiken dürfte die Preise weltweit nach oben treiben. Viele Komponenten wie Batterien, Magneten, Bildschirme werden durch “Seltene Elemente“ immer leistungsfähiger und wirken hierbei nachfrageerhöhend. Was viele “Seltene Elemente“ so schwer abbaubar macht ist, dass diese oftmals zusammen mit strahlendem Material auftreten. Diese treten zwar im Grunde gar nicht so selten auf, jedoch sind diese dadurch oftmals schwer oder nicht ökonomisch abbaubar. Deshalb sind die Preise so verschieden. Während Cerium Oxid etwa 1,6 USD per kg kostet, liegen die Preise für Terbium Oxid bei über 400 USD pro kg.

- China’s marktbeherrschende Rolle

China ist heute der dominante Player für den Abbau von REEs, wobei es 90 % des weltweiten Angebots stellt. Ausserdem ist es der führende Weiterverarbeiter und Nutzer der verfeinerten Elemente. Die Restukturierung des Industriezweiges für “Seltene Elemente“ in China brachte zwei Gruppen von Produzenten hervor, jedoch wurde dies nicht akzeptiert und wieder aufgegeben. Zu den führenden Produzenten in China zählen heute Baotou Steel, Baotou Rare Earth (Group) Co, Gansu Rare Earth Co. Sowie die Sichuan Rare Earth Group. In der Nähe von Baotou, in der inneren Mongolei, ist Bastnaesit ein Nebenprodukt des Eisenabbaus. In Gansu und Sichuan ist Bastnaesit die primäre Mineralie. Der US Geological Survey (USGS) berichtet, dass die Hauptproduktionsgebiete von Scandium ebenfalls in China sowie in Russland und der Ukraine liegen. Die weltweiten Reserven in “Seltenen Elementen“ werden heute auf etwa 100 Millionen Tonnen geschätzt. Zieht man von diesen jedoch die unwirtschaftlich abbaubaren und prozessbedingte Unwägbarkeiten ab, so dürften sich die abbaubaren Nettoreserven auf lediglich 6 bis 10 Millionen Tonnen REO betragen. Die weltweite Produktion von “Seltenen Elementen“ beträgt etwa 100,000 Tonnen Rare Earth Oxide (REO) pro Jahr. Seit den 90er Jahren wurde in Australien verstärkt nach REEs gesucht. Hierbei wurden vor allem die beiden Unternehmen Lynas Corporation und Arafura Resources fündig.

- Lynas ante portas

Eine besonders ergiebige Lagerstätte, welches vom Unternehmen Lynas Corporation (Ticker: LYC.AX) erschlossen wird, ist das Mt. Weld-Projekt in West-Australien. Lynas Corporation (Börsenkürzel: LYC.AX) ist in den letzten Zügen der Entwicklung der Mt Weld Mine, wird jedoch die Produktion nach Malaysien verlagern, um die aktuellen chinesischen Exportzölle von 10 % zu vermeiden. Da China mittlerweile die Produktion zurückgefahren hat, sind die durchschnittlichen Preisanstiege von über 60 % bei den “Seltenen Elementen“ kein Zufall. Das Mt Weld-Projekt von Lynas mit nachgewiesenen Reserven von über 2 Millionen Tonnen kann die Lücke zwischen Angebot und Nachfrage in den nächsten Jahren schliessen. Geht man von zukünftigen Preisen von zukünftig etwa 10 bis 15 USD/kg REO aus, so dürften die bisherigen Reserven von Lynas bei einem Reinheitsanteil von konservativ geschätzten 15 bis 20 % alleine 2 Milliarden USD wert sein. Bei noch höheren Reinheitsgraden und Preisen um 20 bis 25 USD könnten die Lynas-Reserven sogar bis zu 5 Milliarden USD wert sein. Dies allein würde Aktienkurse von etwa 3 bis 5 AUD (aktuell 0.6 AUD) in diesem Wert rechtfertigen. Wenn es keine Verzögerungen gibt, sollte Lynas bereits ab dem Jahr 2010 etwa 10.000 Tonnen pro Jahr, d.h. 10 % der weltweiten Nachfrage liefern können. Bis zum Jahr 2015 könnte diese Anteil auf über 15 % ansteigen. Die Mt. Weld Lagerstätten (ca 25 % Lanthanoxide, cac. 45 % Ceroxide sowie 20 % Neodymoxide) sind die weltweit grösste Fundstätte von “Seltenen Elementen“, wobei diese sogar in der Lage wären über einen Zeitraum von 30 Jahren 20 % der weltweiten Nachfrage zu decken. Somit dürfte Lynas in den nächsten Jahren in der Spitze etwa 75 bis 100 Millionen USD pro Jahr verdienen. Besonders interessant an der Strategie von Lynas ist, dass das Unternehmen die vertikale Integration vorantreibt. Es will nicht nur als einer der weltweit grössten Lieferanten, sondern auch als Weiterverarbeiter auftreten. Zur Absicherung dieser Strategie hat Lynas einen langfristigen Liefervertrag mit dem französischen Spezialchemieunternehmen Rhodia abgeschlossen. “Seltene Elemente“ werden oft als Nebenprodukt von schweren Sänden gefunden, die Titan beinhalten, was vor allem in Australien der Fall ist. Zusätzliches Potential dürfte Lynas deshalb das Crown Polymetallic Resource-Projekt im Mt. Welt-Abbaugebiet geben, enthält es doch grosse Ansammlungen von Niob (Legierungszusatz für rostfreie Stähle, Einsatz in der Nukleartechnik), Tantal (Einsatz in Kondensatoren), Zirkonium (Einsatz im Reaktorbau und bei Brennstoffzellen) sowie Titan (Einsatz im Flugzeugbau).

- Der zweite australische Player

Zu einem weiteren Schlüssel-Player in der australischen Rohstoffszene könnte sich hierbei Arafura Resources (Börsenkürzel: ARU.AX) mausern. Das Unternehmen weist ebenfalls sehr hohe Reserven an “Seltenen Elementen“ auf. So gab Arafura bereits im Jahr 2005 eine Verdreifachung seiner Reserven auf 18.6 Million Tonnen bei 3.1% REO, 14% P2O5 and 0.47 lb/Tonne U3O8 bekannt. Arafura has zahlreiche Abbauprojekte wie das Nolans Bore, das Lagoon Creek, das Lucy Creek-Projekt sowie das Aileron Basins-Projekt. Der Inground Value allein des im Nolans Bore Projekt liegenden Urans und Thoriums dürfte bei mindestens 3 Milliarden USD liegen, der Uranwert der übrigen Projekte bei etwa 1 Milliarde. Hinzu kommen noch einmal etwa 2 Milliarden USD Inground Value der übrigen Projekte im Bereich der “Seltenen Elemente“/Phosphate, dem Gold-Projekt Kurinelli Prospect sowie das Eisen-Projekts Frances Creek. Summa Summarum dürften sich somit die Inground-Resourcen von Arafura auf mindestens 6 Milliarden USD belaufen und dies bei einem Aktienkurs von aktuell etwa 0.9 AUD bzw. einer Börsenkapitalisierung von etwa 85 Millionen USD. Arafura hat den Abbau von Uran ausgegliedert. Der Demerger hat das neue Unternehmen NuPower Resources hervorgebracht. Das Bestreben der Regierungen die Treibhausgase deutlich zu reduzieren, dürfte sowohl Arafuras als auch NuPowers Kursrakete weiter zünden. Insbesondere könnte Thorium zukünftig für den Betrieb von Kernkraftwerken besonders interessant werden, weil dadurch weit weniger Plutonium als Abfallstoff anfällt. Die Abbaugebiete von Arafura sind darüber hinaus in den Northern Territories, welche minenfreundliche Rahmenbedingungen bieten.

- Fazit

Die Abhängigkeit vieler Industrieländer, vor allem den USA, von REEs aus China ist heute nahezu perfekt, insbesondere da die USA nur in Kalifornien (Mountain Pass) und vor allem jedoch in Wyoming (Bear Lodge) über nennenswerte Reserven verfügen, die dort vom Unternehmen Rare Element Resources (Börsenkürzel: RES.V) abgebaut werden. Während im Jahr 1990 die USA sich noch selbst mit “Seltenen Rohstoffen“ versorgen konnten, ist as Land heute zu 90 % von Importen aus China abhängig (Quelle: http://pubs.usgs.gov/fs/2002/fs087-02/). Sich vom chinesischen Quasi-Monopol zu befreien, ist deshalb nur möglich, wenn alternative Anbieter, die über nennenswerte Reserven verfügen, wie Lynas und Arafura, schnellstmöglich in die Abbauphase übergehen. Mit bisher nachgewiesenen Reserven von über 2 Millionen Tonnen kann Lynas zu einer ernsthaften Konkurrenz für die Chinesen avancieren. Wenn es keine Verzögerungen gibt, sollte Lynas Corporation bereits ab dem Jahr 2010 etwa 10.000 Tonnen pro Jahr, d.h. 10 % der weltweiten Nachfrage liefern können. Der andere Key Player Arafura Resources verfügt ebenfalls über erheblichen Reserven an “Seltenen Elementen“. Beide Aktien sind trotz ihres spekulativen Charakters aufgrund ihres zukünftigen Ertragspotentials als “strong buy“ einzustufen und in Schwächephasen zu akkumulieren.

Zur Person: Dr. Artur P. Schmidt ist Fondsmanager des MARIS GLOBAL COCKPIT FUND (www.cockpit.li) und Herausgeber des Finanzportals www.unternehmercockpit.com.

Aktuelle boerse-express.com News

Australien greift Chinas heimliches Rohstoff-Monopol an

2007-05-24 09:53:00

Seltene Erdmetalle vor starken Avancen?

Auch wenn viele meinen, die Rohstoffhausse sei zu Ende, so lässt sich heute schon prognostizieren, dass die verstärkte Nachfrage aus China und Indien in zahlreichen Commodity-Marktsegmenten zu starken Knappheiten führen wird. Von der Öffentlichkeit kaum wahrgenommen hat China in den letzten beiden Jahrzehnten eine führende Position im Bereich der “Seltenen Elemente“, den sogenannten “Rare Earth Elements“ (REE) aufgebaut.

- Was sind “Seltene Elemente“?

“Seltene Elemente“, auch Lanthanoide (Lanthanähnliche) genannt, ist eine Gruppenbezeichnung ähnlicher Elemente mit den Atomnummern 57 bis 71, zu denen das Lanthan und die 14 im Periodensystem folgenden Elemente Cer, Praseodym, Neodym, Promethium, Samarium, Europium, Gadolinium, Terbium, Dysprosium, Holmium, Erbium, Thulium, Ytterbium und Lutetium zählen. Obwohl die 15 “Seltenen Elemente“ meistens zusammen auftreten, werden diese in zwei Gruppen unterteilt: die leichten und mittelschweren (Atomnummern 57 bis 64) und die schweren (Atomnummern 65 bis 71) Elemente. Zu den Lanthaniden werden auch noch die Atomnummern 21 (Scandium) sowie 39 (Yttrium) gezählt., Der Gehalt an “Seltenen Elemente“ wird ausgedrückt durch den Begriff „Rear-Earth-Oxyd“ (REO) oder „Total Rare Earth Oxyd“ (TREO). Die Lanthanoide sind silbrig-glänzende, relativ weiche und reaktionsfreudige Metalle. An der Luft oxidieren sie schnell und werden matt. Im Wasser erfolgt die Zersetzung mehr oder weniger schnell unter Freisetzung von Wasserstoffgas. Wegen ihren ähnlichen physikalischen und chemischen Eigenschaften treten die “Seltenen Elemente“ und Yttrium meist gemeinsam in der Natur auf. Der Begriff "Erden" bezieht sich hierbei auf die jeweiligen Oxide. Während das betroffene Element die Endung "-ium" erhielt, wurde für das zugehörige Oxid die Endung "-ia" verwendet (Beispiel: Element "Yttrium", das zugehörige Oxid wurde "Yttria" genannt, zu deutsch "Yttererde"). Die häufigsten und ökonomisch wichtigsten lanthanoidführenden Minerale sind: Monazit Xenotim, Bastnäsit, Parisit, Allanit, Synchysit, Ancylit sowie Cerianit. Die weltweite Produktion von “Seltenen Elementen“ beträgt etwa 100,000 Tonnen Rare Earth Oxyde (REO) pro Jahr. Von Yttrium wird jährlich nur etwa 2,500 Tonnen Yttrium Oxid (Y2O3) produziert.

- Hightech-Rohstoffe

Im United States Geological Survey (USGS) wird hervorgeben, dass “Seltene Elemente“ einer der kritischen Schlüsselfaktoren für die Hightech-Industrien sind. Wenn die Nachfrage wie erwartet mehr als 10 % steigen sollte, so könnte es eine ernsthafte Knappheit geben, die die Weltmarktpreise für REEs deutlich ansteigen lassen wird. “Seltene Elemente“ spielen eine Schlüsselrolle für die Elektronik-industrie (Magnetische Kühlung), die Telekommunikation (Glasfaserkabel) die Mikrosystemtechnik (hochfeste Präzisionsbauteile), den Automobilbau (Hybridantriebe), den Umweltschutz (Emissionskontrolle) sowie in der Petrochemie (Prozesskatalysatoren). Eine besonders hohe Nachfrage wird nach Cerium in Automobilkatalysatoren und Lathanum in NiMH-Batterien erwartet. Aber auch die Nachfrage von “Seltenen Elementen“ beim Einsatz von Phosphor, Glasfasern und Keramiken dürfte die Preise weltweit nach oben treiben. Viele Komponenten wie Batterien, Magneten, Bildschirme werden durch “Seltene Elemente“ immer leistungsfähiger und wirken hierbei nachfrageerhöhend. Was viele “Seltene Elemente“ so schwer abbaubar macht ist, dass diese oftmals zusammen mit strahlendem Material auftreten. Diese treten zwar im Grunde gar nicht so selten auf, jedoch sind diese dadurch oftmals schwer oder nicht ökonomisch abbaubar. Deshalb sind die Preise so verschieden. Während Cerium Oxid etwa 1,6 USD per kg kostet, liegen die Preise für Terbium Oxid bei über 400 USD pro kg.

- China’s marktbeherrschende Rolle

China ist heute der dominante Player für den Abbau von REEs, wobei es 90 % des weltweiten Angebots stellt. Ausserdem ist es der führende Weiterverarbeiter und Nutzer der verfeinerten Elemente. Die Restukturierung des Industriezweiges für “Seltene Elemente“ in China brachte zwei Gruppen von Produzenten hervor, jedoch wurde dies nicht akzeptiert und wieder aufgegeben. Zu den führenden Produzenten in China zählen heute Baotou Steel, Baotou Rare Earth (Group) Co, Gansu Rare Earth Co. Sowie die Sichuan Rare Earth Group. In der Nähe von Baotou, in der inneren Mongolei, ist Bastnaesit ein Nebenprodukt des Eisenabbaus. In Gansu und Sichuan ist Bastnaesit die primäre Mineralie. Der US Geological Survey (USGS) berichtet, dass die Hauptproduktionsgebiete von Scandium ebenfalls in China sowie in Russland und der Ukraine liegen. Die weltweiten Reserven in “Seltenen Elementen“ werden heute auf etwa 100 Millionen Tonnen geschätzt. Zieht man von diesen jedoch die unwirtschaftlich abbaubaren und prozessbedingte Unwägbarkeiten ab, so dürften sich die abbaubaren Nettoreserven auf lediglich 6 bis 10 Millionen Tonnen REO betragen. Die weltweite Produktion von “Seltenen Elementen“ beträgt etwa 100,000 Tonnen Rare Earth Oxide (REO) pro Jahr. Seit den 90er Jahren wurde in Australien verstärkt nach REEs gesucht. Hierbei wurden vor allem die beiden Unternehmen Lynas Corporation und Arafura Resources fündig.

- Lynas ante portas

Eine besonders ergiebige Lagerstätte, welches vom Unternehmen Lynas Corporation (Ticker: LYC.AX) erschlossen wird, ist das Mt. Weld-Projekt in West-Australien. Lynas Corporation (Börsenkürzel: LYC.AX) ist in den letzten Zügen der Entwicklung der Mt Weld Mine, wird jedoch die Produktion nach Malaysien verlagern, um die aktuellen chinesischen Exportzölle von 10 % zu vermeiden. Da China mittlerweile die Produktion zurückgefahren hat, sind die durchschnittlichen Preisanstiege von über 60 % bei den “Seltenen Elementen“ kein Zufall. Das Mt Weld-Projekt von Lynas mit nachgewiesenen Reserven von über 2 Millionen Tonnen kann die Lücke zwischen Angebot und Nachfrage in den nächsten Jahren schliessen. Geht man von zukünftigen Preisen von zukünftig etwa 10 bis 15 USD/kg REO aus, so dürften die bisherigen Reserven von Lynas bei einem Reinheitsanteil von konservativ geschätzten 15 bis 20 % alleine 2 Milliarden USD wert sein. Bei noch höheren Reinheitsgraden und Preisen um 20 bis 25 USD könnten die Lynas-Reserven sogar bis zu 5 Milliarden USD wert sein. Dies allein würde Aktienkurse von etwa 3 bis 5 AUD (aktuell 0.6 AUD) in diesem Wert rechtfertigen. Wenn es keine Verzögerungen gibt, sollte Lynas bereits ab dem Jahr 2010 etwa 10.000 Tonnen pro Jahr, d.h. 10 % der weltweiten Nachfrage liefern können. Bis zum Jahr 2015 könnte diese Anteil auf über 15 % ansteigen. Die Mt. Weld Lagerstätten (ca 25 % Lanthanoxide, cac. 45 % Ceroxide sowie 20 % Neodymoxide) sind die weltweit grösste Fundstätte von “Seltenen Elementen“, wobei diese sogar in der Lage wären über einen Zeitraum von 30 Jahren 20 % der weltweiten Nachfrage zu decken. Somit dürfte Lynas in den nächsten Jahren in der Spitze etwa 75 bis 100 Millionen USD pro Jahr verdienen. Besonders interessant an der Strategie von Lynas ist, dass das Unternehmen die vertikale Integration vorantreibt. Es will nicht nur als einer der weltweit grössten Lieferanten, sondern auch als Weiterverarbeiter auftreten. Zur Absicherung dieser Strategie hat Lynas einen langfristigen Liefervertrag mit dem französischen Spezialchemieunternehmen Rhodia abgeschlossen. “Seltene Elemente“ werden oft als Nebenprodukt von schweren Sänden gefunden, die Titan beinhalten, was vor allem in Australien der Fall ist. Zusätzliches Potential dürfte Lynas deshalb das Crown Polymetallic Resource-Projekt im Mt. Welt-Abbaugebiet geben, enthält es doch grosse Ansammlungen von Niob (Legierungszusatz für rostfreie Stähle, Einsatz in der Nukleartechnik), Tantal (Einsatz in Kondensatoren), Zirkonium (Einsatz im Reaktorbau und bei Brennstoffzellen) sowie Titan (Einsatz im Flugzeugbau).

- Der zweite australische Player

Zu einem weiteren Schlüssel-Player in der australischen Rohstoffszene könnte sich hierbei Arafura Resources (Börsenkürzel: ARU.AX) mausern. Das Unternehmen weist ebenfalls sehr hohe Reserven an “Seltenen Elementen“ auf. So gab Arafura bereits im Jahr 2005 eine Verdreifachung seiner Reserven auf 18.6 Million Tonnen bei 3.1% REO, 14% P2O5 and 0.47 lb/Tonne U3O8 bekannt. Arafura has zahlreiche Abbauprojekte wie das Nolans Bore, das Lagoon Creek, das Lucy Creek-Projekt sowie das Aileron Basins-Projekt. Der Inground Value allein des im Nolans Bore Projekt liegenden Urans und Thoriums dürfte bei mindestens 3 Milliarden USD liegen, der Uranwert der übrigen Projekte bei etwa 1 Milliarde. Hinzu kommen noch einmal etwa 2 Milliarden USD Inground Value der übrigen Projekte im Bereich der “Seltenen Elemente“/Phosphate, dem Gold-Projekt Kurinelli Prospect sowie das Eisen-Projekts Frances Creek. Summa Summarum dürften sich somit die Inground-Resourcen von Arafura auf mindestens 6 Milliarden USD belaufen und dies bei einem Aktienkurs von aktuell etwa 0.9 AUD bzw. einer Börsenkapitalisierung von etwa 85 Millionen USD. Arafura hat den Abbau von Uran ausgegliedert. Der Demerger hat das neue Unternehmen NuPower Resources hervorgebracht. Das Bestreben der Regierungen die Treibhausgase deutlich zu reduzieren, dürfte sowohl Arafuras als auch NuPowers Kursrakete weiter zünden. Insbesondere könnte Thorium zukünftig für den Betrieb von Kernkraftwerken besonders interessant werden, weil dadurch weit weniger Plutonium als Abfallstoff anfällt. Die Abbaugebiete von Arafura sind darüber hinaus in den Northern Territories, welche minenfreundliche Rahmenbedingungen bieten.

- Fazit

Die Abhängigkeit vieler Industrieländer, vor allem den USA, von REEs aus China ist heute nahezu perfekt, insbesondere da die USA nur in Kalifornien (Mountain Pass) und vor allem jedoch in Wyoming (Bear Lodge) über nennenswerte Reserven verfügen, die dort vom Unternehmen Rare Element Resources (Börsenkürzel: RES.V) abgebaut werden. Während im Jahr 1990 die USA sich noch selbst mit “Seltenen Rohstoffen“ versorgen konnten, ist as Land heute zu 90 % von Importen aus China abhängig (Quelle: http://pubs.usgs.gov/fs/2002/fs087-02/). Sich vom chinesischen Quasi-Monopol zu befreien, ist deshalb nur möglich, wenn alternative Anbieter, die über nennenswerte Reserven verfügen, wie Lynas und Arafura, schnellstmöglich in die Abbauphase übergehen. Mit bisher nachgewiesenen Reserven von über 2 Millionen Tonnen kann Lynas zu einer ernsthaften Konkurrenz für die Chinesen avancieren. Wenn es keine Verzögerungen gibt, sollte Lynas Corporation bereits ab dem Jahr 2010 etwa 10.000 Tonnen pro Jahr, d.h. 10 % der weltweiten Nachfrage liefern können. Der andere Key Player Arafura Resources verfügt ebenfalls über erheblichen Reserven an “Seltenen Elementen“. Beide Aktien sind trotz ihres spekulativen Charakters aufgrund ihres zukünftigen Ertragspotentials als “strong buy“ einzustufen und in Schwächephasen zu akkumulieren.

Zur Person: Dr. Artur P. Schmidt ist Fondsmanager des MARIS GLOBAL COCKPIT FUND (www.cockpit.li) und Herausgeber des Finanzportals www.unternehmercockpit.com.

Aktuelle boerse-express.com News

Die neuste Investor Presentation - June 2007 wurde von LYNAS veröffentlicht:

und nicht nur die Kostenstruktur auf Seite 28 zum Mt Weld Projekt zeigt das gewaltige Potential von LYNAS auf.

http://www.asx.com.au/asx/research/CompanyInfoSearchResults.…http://www.asx.com.au/asxpdf/20070604/pdf/312sd4jlfwtl4v.pdf

http://www.lynascorp.com/

http://www.lynascorp.com/content/upload/files/press_releases…

http://www.tradingroom.com.au/apps/qt/quote.ac;jsessionid=07…

Gruß JoJo

und nicht nur die Kostenstruktur auf Seite 28 zum Mt Weld Projekt zeigt das gewaltige Potential von LYNAS auf.

http://www.asx.com.au/asx/research/CompanyInfoSearchResults.…http://www.asx.com.au/asxpdf/20070604/pdf/312sd4jlfwtl4v.pdf

http://www.lynascorp.com/

http://www.lynascorp.com/content/upload/files/press_releases…

http://www.tradingroom.com.au/apps/qt/quote.ac;jsessionid=07…

Gruß JoJo

Antwort auf Beitrag Nr.: 29.627.470 von JoJo49 am 04.06.07 12:07:04Hallo JoJo,

würdest du bitte die Fakten zu den Kosten mal im Einzelnen posten? Ich kann leider das PDF zur Zeit nicht herunterladen und bin aufgrund des Postings von Noch-n-Zocker im Hauptthread etwas irritiert.

Auch wäre es nett, wenn du die wichtigsten Infos bitte in Kürze zusammenfassen könntest. Danke dir.

würdest du bitte die Fakten zu den Kosten mal im Einzelnen posten? Ich kann leider das PDF zur Zeit nicht herunterladen und bin aufgrund des Postings von Noch-n-Zocker im Hauptthread etwas irritiert.

Auch wäre es nett, wenn du die wichtigsten Infos bitte in Kürze zusammenfassen könntest. Danke dir.

Immer auf dem neusten Stand:

1. - Kurse

http://stocknessmonster.com/

2. - News

http://stocknessmonster.com/news-history?S=LYC&E=ASX

Gruß JoJo

1. - Kurse

http://stocknessmonster.com/

2. - News

http://stocknessmonster.com/news-history?S=LYC&E=ASX

Gruß JoJo

Die immer weiter stark steigenden Nachfrage zeigt wie wichtig eine schnelle Produktinsaufnahme ist...

Südkorea versucht sich am Hybridauto

Da stellt sich mir nicht mehr die Frage: "warum die Chinesen Exportsteuern und Förderquote auf REO eingeführt haben" und m.E. ist da noch lange nicht das letzte Wort gesprochen.

http://www.handelsblatt.com/news/Unternehmen/Aussenwirtschaf…

Toyota meldet zwar einen Absatzrekord nach dem anderen bezogen auf Hybridautos/Batterien muss Toyota allerdings auch schon Probleme eingestehen.

(mehr als 1 Mill. Fahrzeuge verkauft)

Thema: die kleinere Lithium-Ionbatterie, soll die Nickel-Metallhydridbatterien Toyota ablösen, Problem es werden größere Mengen an Lanthan (Lanthanum oxide bei Mt Weld über 25%) benötigt.

http://seattletimes.nwsource.com/html/businesstechnology/200…

Nur ein Aspekt von REO-Anwendungen der allerdings immer wichtiger wird, siehe dazu die letzte Präsentation von LYNAS:

http://www.asx.com.au/asxpdf/20070604/pdf/312sd4jlfwtl4v.pdf

Gruß JoJo

Südkorea versucht sich am Hybridauto

Da stellt sich mir nicht mehr die Frage: "warum die Chinesen Exportsteuern und Förderquote auf REO eingeführt haben" und m.E. ist da noch lange nicht das letzte Wort gesprochen.

http://www.handelsblatt.com/news/Unternehmen/Aussenwirtschaf…

Toyota meldet zwar einen Absatzrekord nach dem anderen bezogen auf Hybridautos/Batterien muss Toyota allerdings auch schon Probleme eingestehen.

(mehr als 1 Mill. Fahrzeuge verkauft)

Thema: die kleinere Lithium-Ionbatterie, soll die Nickel-Metallhydridbatterien Toyota ablösen, Problem es werden größere Mengen an Lanthan (Lanthanum oxide bei Mt Weld über 25%) benötigt.

http://seattletimes.nwsource.com/html/businesstechnology/200…

Nur ein Aspekt von REO-Anwendungen der allerdings immer wichtiger wird, siehe dazu die letzte Präsentation von LYNAS:

http://www.asx.com.au/asxpdf/20070604/pdf/312sd4jlfwtl4v.pdf

Gruß JoJo

Seltenerdenmetalle

Seltene Erden (englisch: Rare Earth Elements, REE, RR.EE.)

Zu den Metallen der Seltenen Erden gehören die chemischen Elemente der 3. Nebengruppe des Periodensystems und die Lanthanoide.