Marvel Gold ehemals Graphex Mining - After Tax NPV 480 Mio AUD bei 16 Mio Börsenwert - world leadin (Seite 258)

eröffnet am 20.09.18 11:00:04 von

neuester Beitrag 28.02.23 09:04:40 von

neuester Beitrag 28.02.23 09:04:40 von

Beiträge: 3.976

ID: 1.288.876

ID: 1.288.876

Aufrufe heute: 0

Gesamt: 207.238

Gesamt: 207.238

Aktive User: 0

ISIN: AU0000102154 · WKN: A2QB8V

0,0060

EUR

0,00 %

0,0000 EUR

Letzter Kurs 02.05.24 Lang & Schwarz

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 2,1200 | +17,78 | |

| 9,8360 | +17,66 | |

| 85.089,50 | +16,19 | |

| 2,5900 | +13,85 | |

| 0,5340 | +12,90 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,6865 | -6,92 | |

| 19,480 | -9,69 | |

| 183,20 | -19,30 | |

| 12,000 | -25,00 | |

| 46,60 | -97,97 |

Beitrag zu dieser Diskussion schreiben

Antwort auf Beitrag Nr.: 60.775.861 von Reiners am 11.06.19 07:27:06Wichtig das meine beiden Punkte bestätigt wurden. 15 years Minelife und DFS Q4/2019

final DFS by 4Q19

The DFS is targeting 15 years (at a 108ktpa production rate) and we know the resource potential is excellent.

final DFS by 4Q19

The DFS is targeting 15 years (at a 108ktpa production rate) and we know the resource potential is excellent.

Hier noch mal seine Kommentare:

------

Simon’s and Black Rock’s own comments on offtake make it sound like the offtake is rock solid. They’re not worth the paper they’re written on. I know the Chinese consultant who introduced them

-------

WKT have just signed “binding offtake agreements” (even though it is blatantly obvious from the announcement they lack all the key aspects of a binding agreement)

------

Simon’s and Black Rock’s own comments on offtake make it sound like the offtake is rock solid. They’re not worth the paper they’re written on. I know the Chinese consultant who introduced them

-------

WKT have just signed “binding offtake agreements” (even though it is blatantly obvious from the announcement they lack all the key aspects of a binding agreement)

Naja, ich rede von den binding offtakes wie sie bis jetzt, nicht nur von WKT, veröffentlicht worden sind.

Phil will es ja gleich richtig / konkret machen mit den Off takes, deshalb werden Sie auch nicht jetzt veröffentlicht, sondern kurz vor der Finanzierung.

Phil hatte ja sofort bemängelt, das bei den BKT / WKT off takes wesentliche Elemente fehlen.

Phil will es ja gleich richtig / konkret machen mit den Off takes, deshalb werden Sie auch nicht jetzt veröffentlicht, sondern kurz vor der Finanzierung.

Phil hatte ja sofort bemängelt, das bei den BKT / WKT off takes wesentliche Elemente fehlen.

Diese ganzen binding offtakes im Grafit Bereich sind nicht das Papier wert auf dem sie geschrieben sind.

das würde dann auch für GPX gelten.

Mir ist eine solche Aussage zu pauschal. Letztlich kommt es auf die genauen Bedingungen der OT-Vereinbarungen an

das würde dann auch für GPX gelten.

Mir ist eine solche Aussage zu pauschal. Letztlich kommt es auf die genauen Bedingungen der OT-Vereinbarungen an

user vooose haut ihnen gerade ihre ganzen falschen gedankengaenge um die ohren

Trading Spotlight

Antwort auf Beitrag Nr.: 60.776.722 von gast77 am 11.06.19 09:21:50Diese ganzen binding offtakes im Grafit Bereich sind nicht das Papier wert auf dem sie geschrieben sind.

Sie helfen den Börsenwert hoch zu bekommen siehe WKT oder BKT, aber so gut wie kaum bei der Finanzierung.

Viele werden noch ganz dumm gucken, wenn WKT in Sachen Finanzierung die nächsten Monate nix bringt.

Gerade eine schöne Diskussion im WKT Thread dazu.

Sie helfen den Börsenwert hoch zu bekommen siehe WKT oder BKT, aber so gut wie kaum bei der Finanzierung.

Viele werden noch ganz dumm gucken, wenn WKT in Sachen Finanzierung die nächsten Monate nix bringt.

Gerade eine schöne Diskussion im WKT Thread dazu.

Antwort auf Beitrag Nr.: 60.775.861 von Reiners am 11.06.19 07:27:06Reiners haben die von Dir abgeschrieben?

Aber ist doch schön für Dich wenn auch andere mal das gleiche sagen.

Aber ist doch schön für Dich wenn auch andere mal das gleiche sagen.

http://www.graphexmining.com.au/wp-content/uploads/2019/06/0…

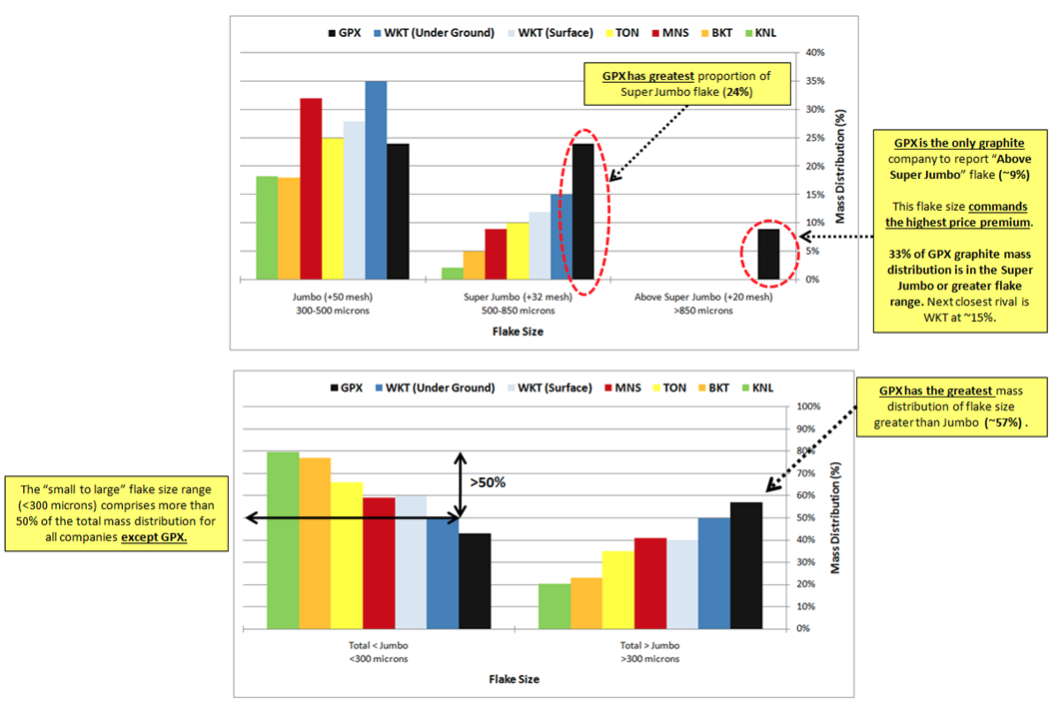

Graphex Mining (GPX AU, market cap A$25m)Commentary prior to a site visit to the Chilalo projectWe will be undertaking a site visit to the Graphex/Chilalo graphite project next week. All mining projects in Tanzania have stalled, pending a final review of the Tanzanian Mining Act. We get the feeling that an outcome is imminent, perhaps crystallised by the resolution of the dispute between Barrick Mining (and subsidiary Acacia) and the Government of Tanzania. We will be travelling to Dodoma, Tanzania’s capital, next Monday for discussions with senior bureaucrats and (hopefully) politicians. This week’s Government-led mining round table will undoubtedly see a strong push from the miners (and particularly devco’s) toward an early resolution of outstanding issues.

There is little doubt in our mind that Tanzania will ultimately become one of the leading producers of coarse flake graphite, with quality characteristics far surpassing deposits in other domiciles.Prior to our visit we have undertaken comparatives for GPX with its graphite peers in Tanzania. What stands out is that despite the high grade and high margins on GPX’s Chilalo project and the fact that GPX has a funding solution for the project, the company is one of the lowest valued by market capitalisation (at ca. A$22m). This seems far too cheap to us, and at sub A$0.30/share is trading at roughly 15% of our fully financed NPV per share (A$1.69).Importantly GPX is the only Tanzanian graphite devco which has a full funding solution. GPX is now working to complete a final DFS by 4Q19 one of the important conditions precedent for the Castlelake funding package. All other graphite devco’s have completed DFS, but there are few signs of final funding outcomes.

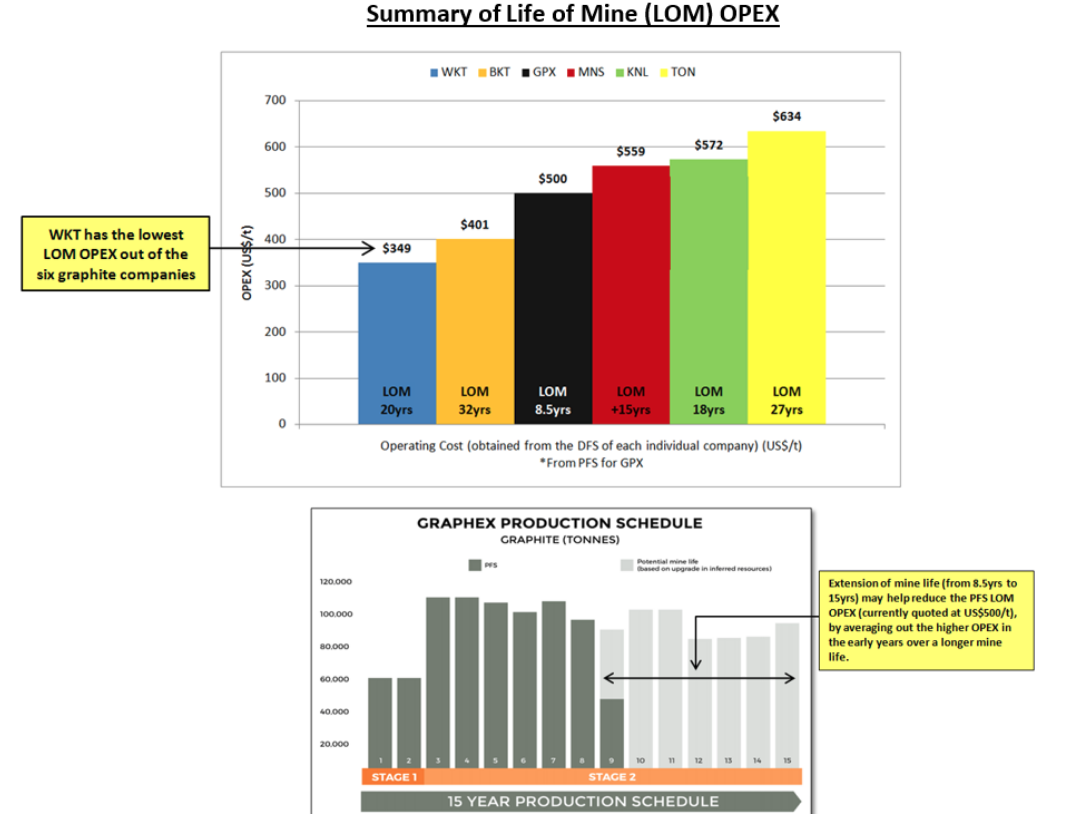

As reserves stand currently, GPX/Chilalo offers one of the shorter mine lives. The DFS is targeting 15 years (at a 108ktpa production rate) and we know the resource potential is excellent.

One area of concern within the sector relates to the quality of product offtake agreements. Several of the companies state they have “binding offtakes”. As Phil can discuss in more detail, many of these do not stand detailed scrutiny. Most offtakes quoted are condition on production, financing and often with 60 day termination notices. Surprisingly few (in fact none) have a negotiated offtake price for the product, which is normal for an offtake agreement. As we know, Phil Hoskins has been very careful not to overstate the security of Chilalo’s offtake.

Graphex Mining (GPX AU, market cap A$25m)Commentary prior to a site visit to the Chilalo projectWe will be undertaking a site visit to the Graphex/Chilalo graphite project next week. All mining projects in Tanzania have stalled, pending a final review of the Tanzanian Mining Act. We get the feeling that an outcome is imminent, perhaps crystallised by the resolution of the dispute between Barrick Mining (and subsidiary Acacia) and the Government of Tanzania. We will be travelling to Dodoma, Tanzania’s capital, next Monday for discussions with senior bureaucrats and (hopefully) politicians. This week’s Government-led mining round table will undoubtedly see a strong push from the miners (and particularly devco’s) toward an early resolution of outstanding issues.

There is little doubt in our mind that Tanzania will ultimately become one of the leading producers of coarse flake graphite, with quality characteristics far surpassing deposits in other domiciles.Prior to our visit we have undertaken comparatives for GPX with its graphite peers in Tanzania. What stands out is that despite the high grade and high margins on GPX’s Chilalo project and the fact that GPX has a funding solution for the project, the company is one of the lowest valued by market capitalisation (at ca. A$22m). This seems far too cheap to us, and at sub A$0.30/share is trading at roughly 15% of our fully financed NPV per share (A$1.69).Importantly GPX is the only Tanzanian graphite devco which has a full funding solution. GPX is now working to complete a final DFS by 4Q19 one of the important conditions precedent for the Castlelake funding package. All other graphite devco’s have completed DFS, but there are few signs of final funding outcomes.

As reserves stand currently, GPX/Chilalo offers one of the shorter mine lives. The DFS is targeting 15 years (at a 108ktpa production rate) and we know the resource potential is excellent.

One area of concern within the sector relates to the quality of product offtake agreements. Several of the companies state they have “binding offtakes”. As Phil can discuss in more detail, many of these do not stand detailed scrutiny. Most offtakes quoted are condition on production, financing and often with 60 day termination notices. Surprisingly few (in fact none) have a negotiated offtake price for the product, which is normal for an offtake agreement. As we know, Phil Hoskins has been very careful not to overstate the security of Chilalo’s offtake.

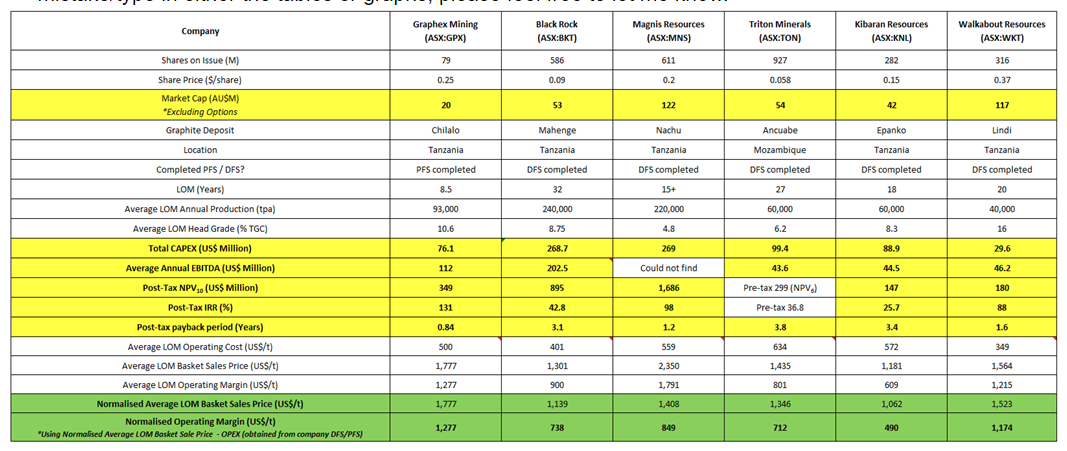

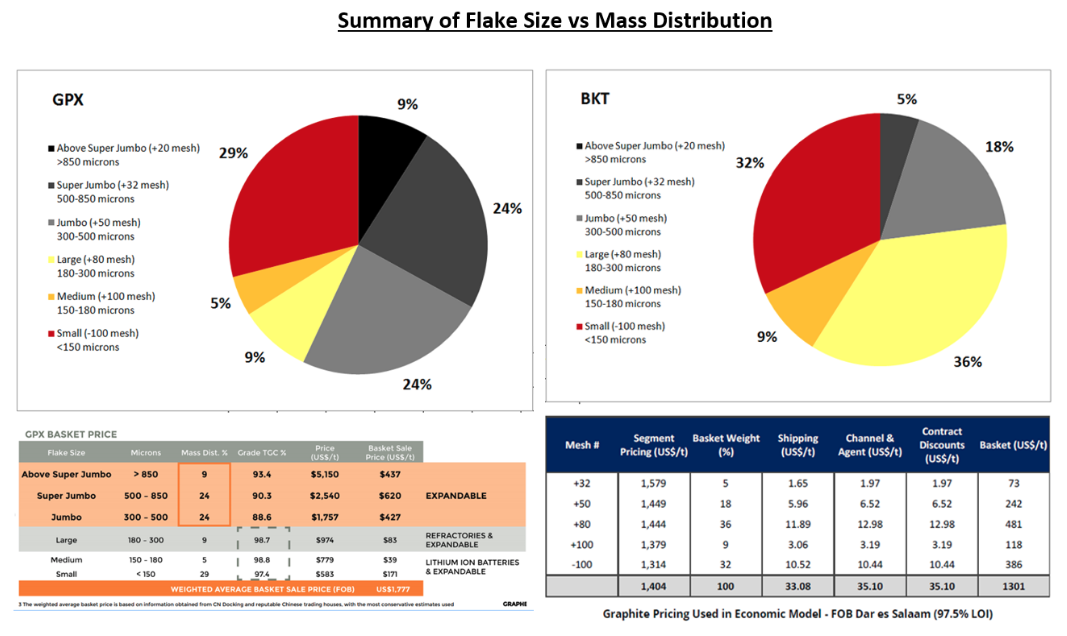

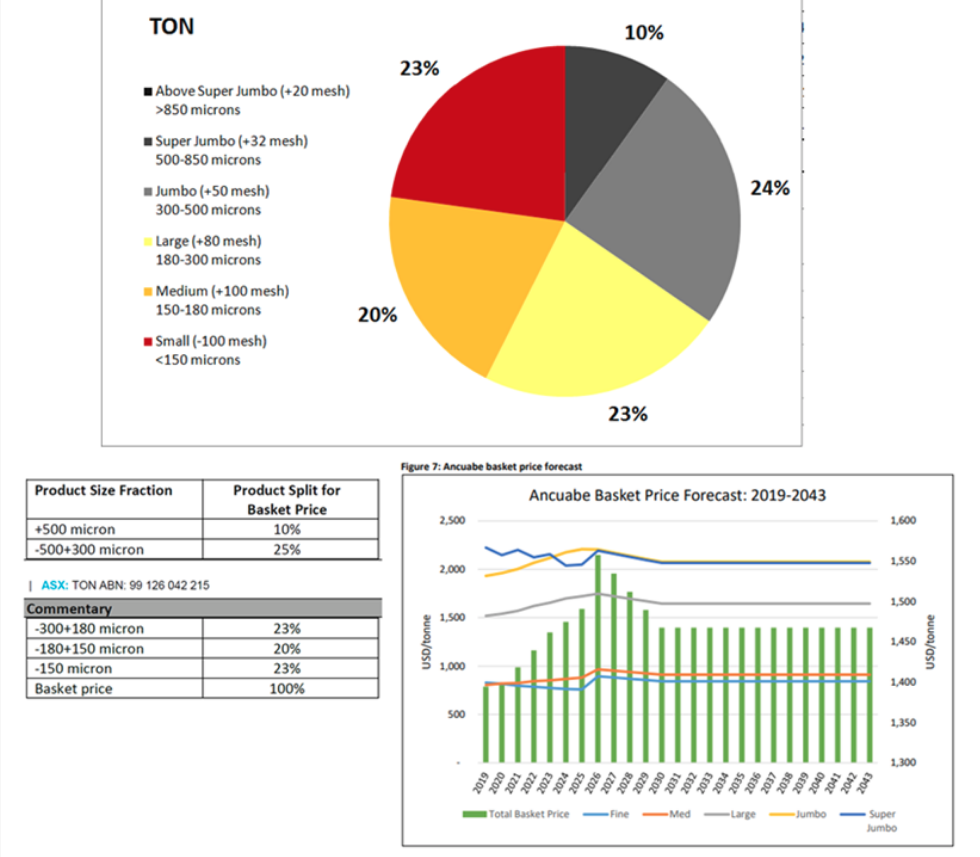

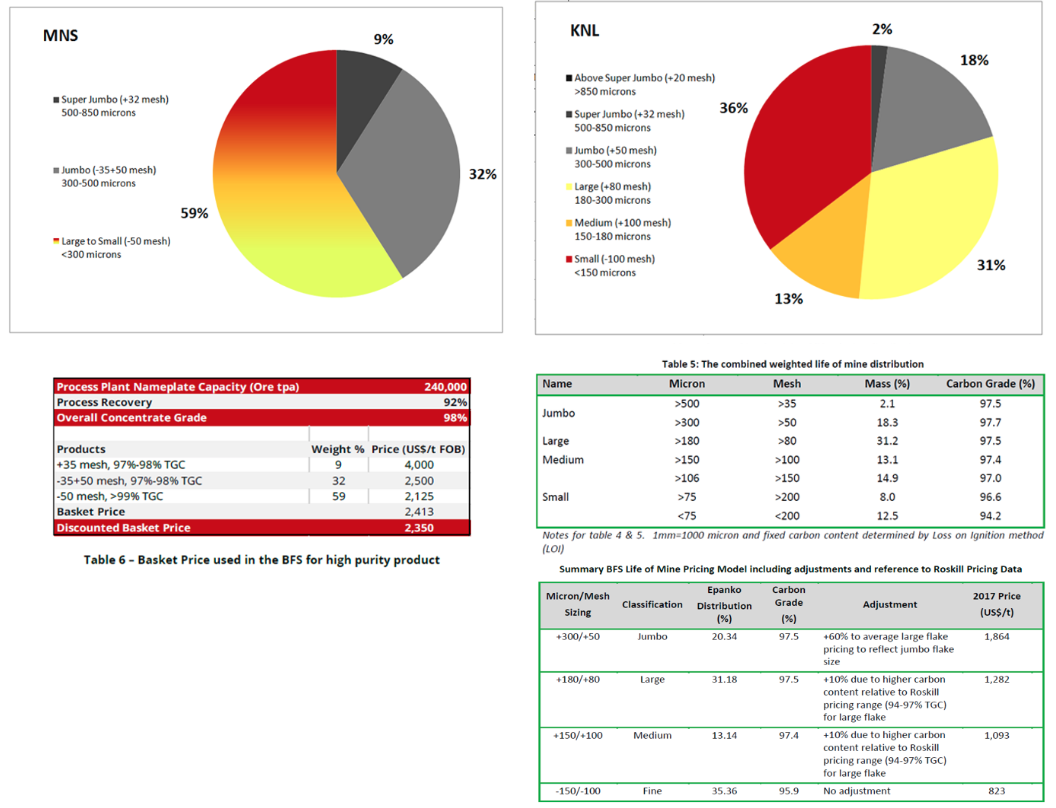

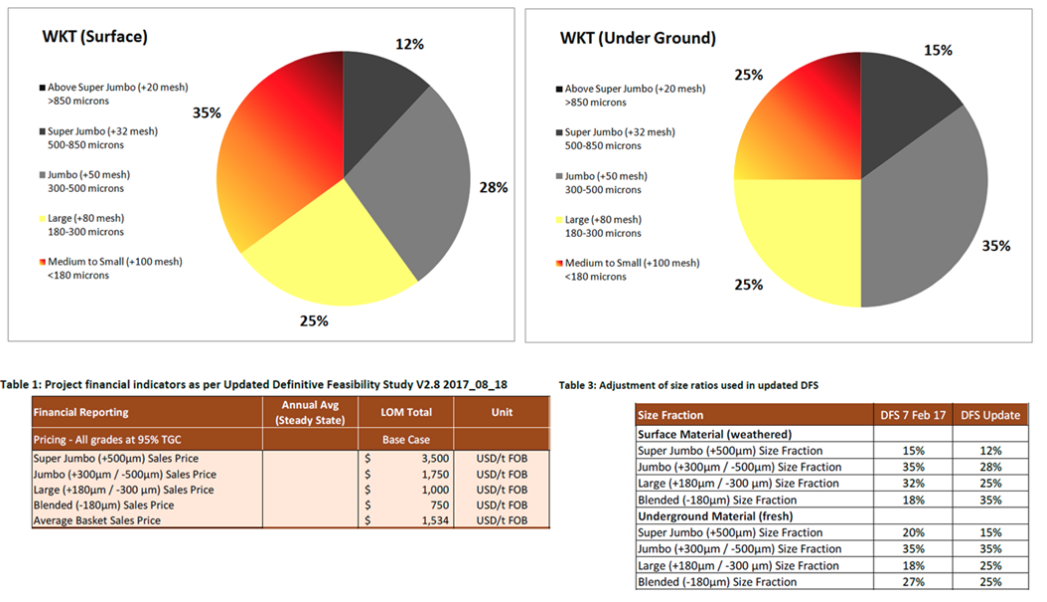

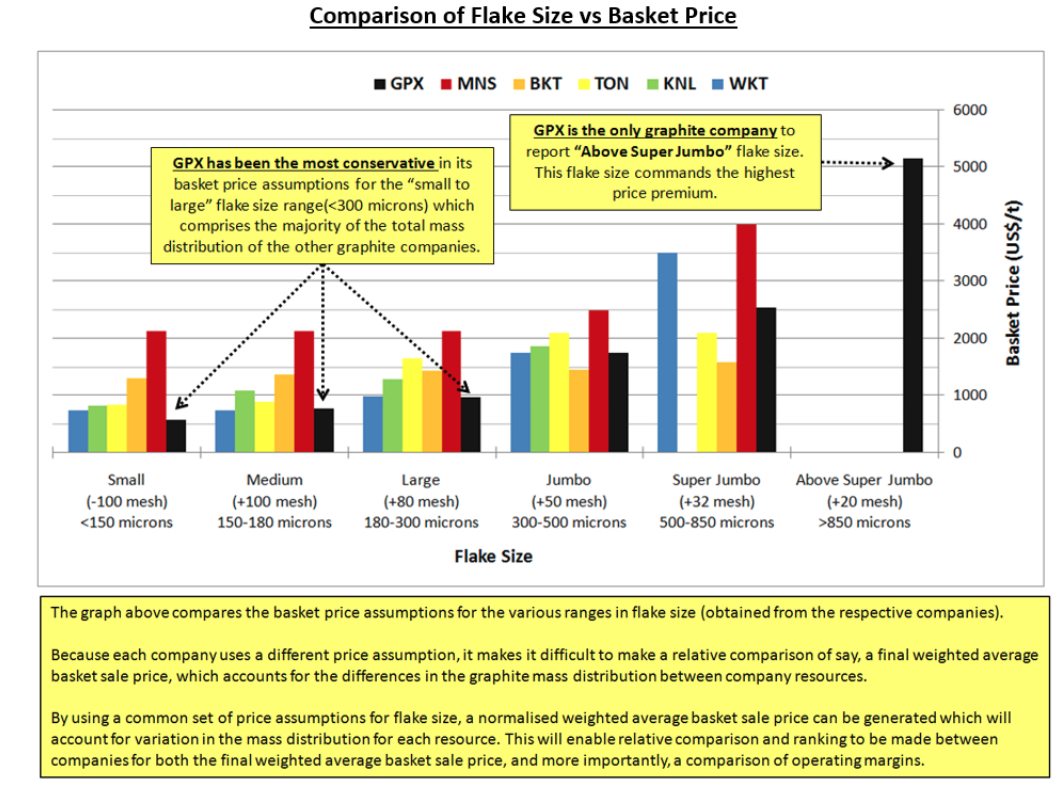

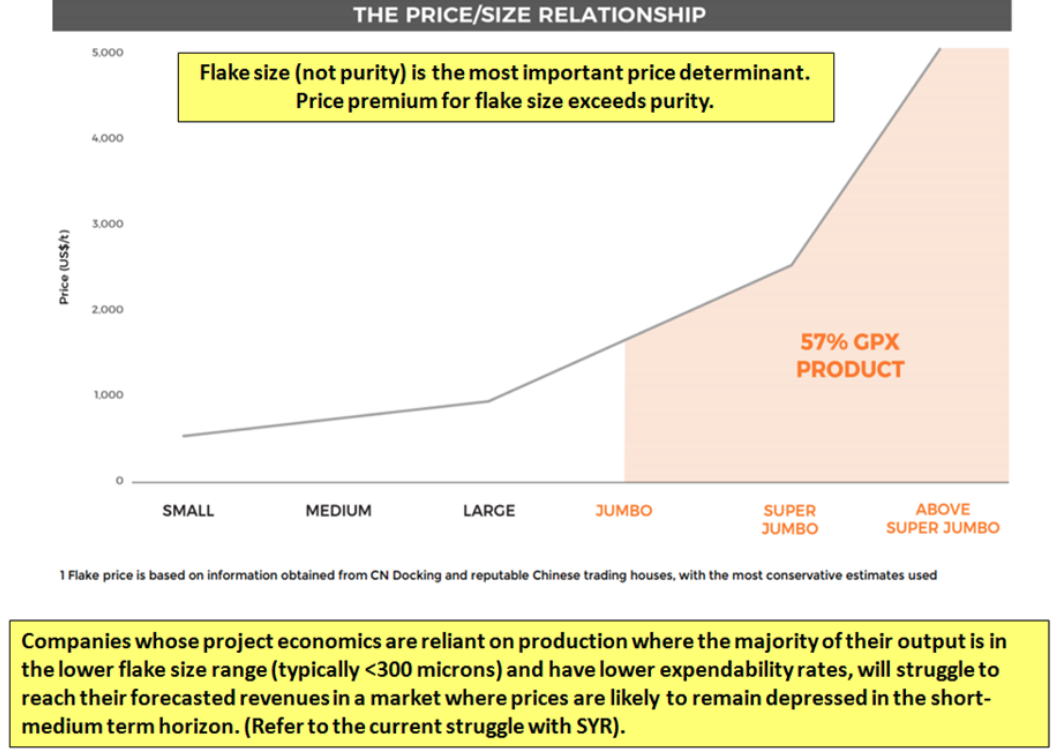

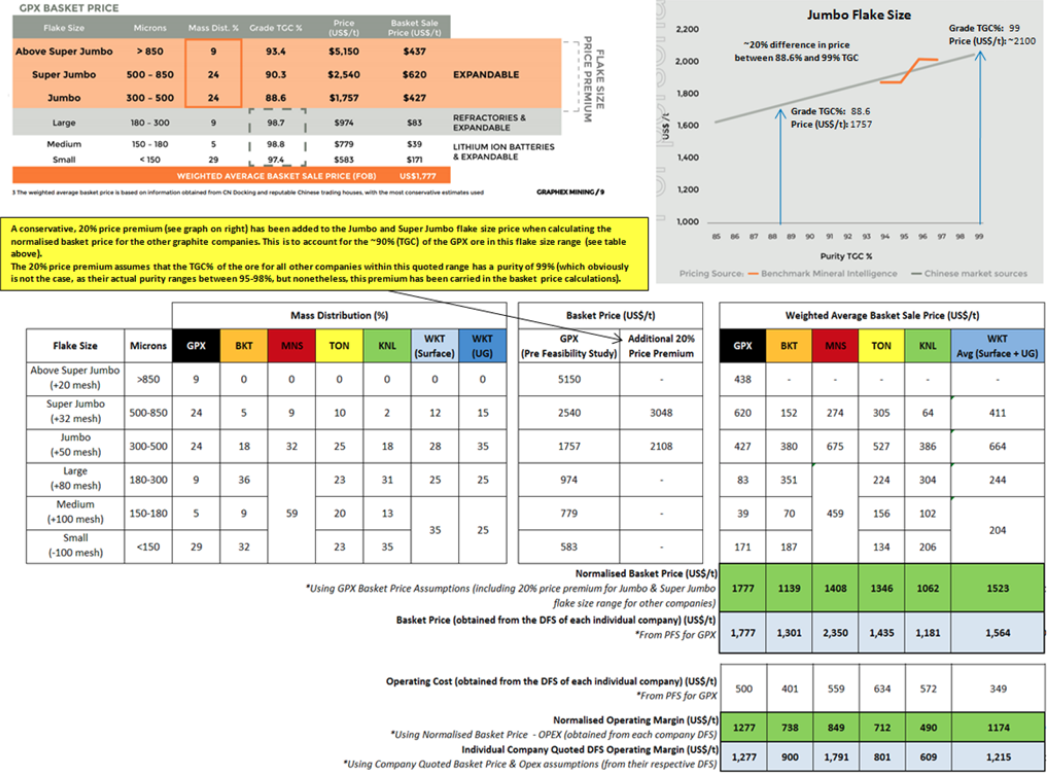

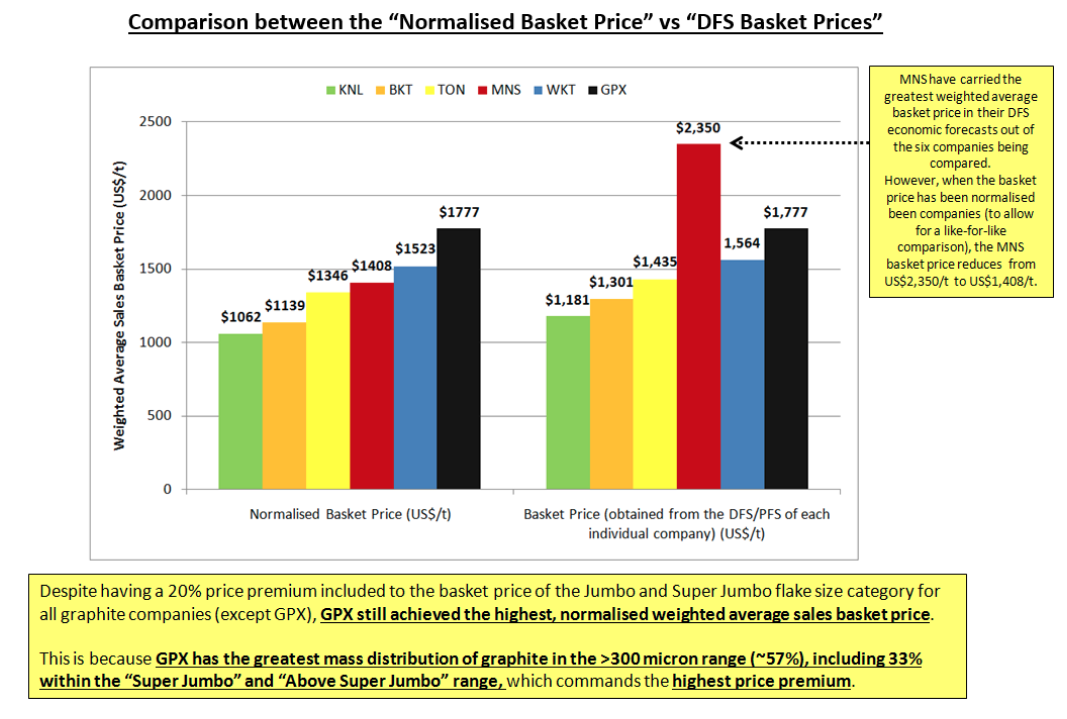

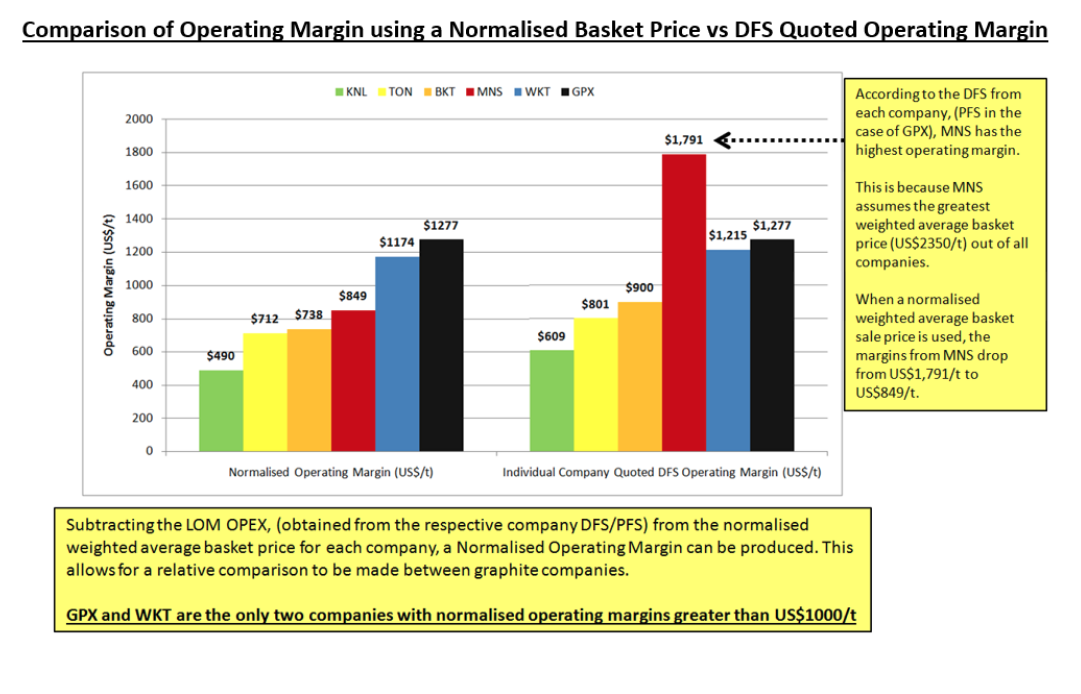

Da hat sich mal jemand viel Mühe gemacht, Fazit GPX ganz oben, WKT Platz 2

----------------------------------------

https://hotcopper.com.au/threads/gpx-comparison.4802847/

----------------------------------------

https://hotcopper.com.au/threads/gpx-comparison.4802847/

der User spectre888 hat einen sehr aufwändigen Überblick über die Graphit Player erstellt. Fazit: Wir sind hier ganz gut investiert.