Golar LNG Partners LP - LNG-MLP - 500 Beiträge pro Seite

eröffnet am 21.03.14 11:21:30 von

neuester Beitrag 21.04.21 20:31:46 von

neuester Beitrag 21.04.21 20:31:46 von

Beiträge: 88

ID: 1.192.701

ID: 1.192.701

Aufrufe heute: 0

Gesamt: 8.393

Gesamt: 8.393

Aktive User: 0

ISIN: MHY2745C1021 · WKN: A1H9DR

2,9540

EUR

+0,08 %

+0,0025 EUR

Letzter Kurs 16.04.21 Tradegate

Neuigkeiten

Werte aus der Branche Finanzdienstleistungen

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,9000 | +20,00 | |

| 2,1850 | +19,24 | |

| 4,5000 | +15,38 | |

| 6,3000 | +14,55 | |

| 3,4200 | +14,00 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,3500 | -10,60 | |

| 7,16 | -12,04 | |

| 12,60 | -21,93 | |

| 1,5000 | -23,08 | |

| 1,5000 | -40,00 |

...ist die Tochter von Thread: Golar neue Chancen durch verstärkte Umwandlung von Gas in LNG und wird deshalb -in üblicher MLP-Manier- immer auch ein bisschen ausgenommen;

andererseits derzeit rund 7% p.a. Ausschüttung

andererseits derzeit rund 7% p.a. Ausschüttung

Kurs seit März um knapp 20% gestiegen

heute von der Mutter in die Tochter getauscht....

aufgestockt

Trading Spotlight

im heutigen Reportgewitter vglw. schön ruhig geblieben hier...

drop-down:

Published: 22:28 CET 15-12-2014 /GlobeNewswire /Source: Golar LNG / : GOL /ISIN: BMG9456A1009

Sale of Golar Eskimo to Golar LNG Partners L.P.

Golar LNG Limited (the "Company") announced today that it has entered into an agreement to sell its ownership interests in the companies that will own and operate the floating storage and regasification unit ("FSRU") Golar Eskimo ("Eskimo") to Golar LNG Partners L.P. ("Golar Partners") for a price of USD 390 million. The transaction is subject to the satisfaction of certain closing conditions which is expected to be finalized in January 2015.

The Partnership will finance the purchase price with cash on hand, the proceeds of a $220.0 million loan from the Company and the assumption of outstanding bank debt in respect of the Golar Eskimo on the closing date of the acquisition (which is be approximately $162.8 million). The loan is for a term of 2 years with a rate of interest of LIBOR plus a blended margin of 2.84%.

Part of the agreement with Golar Partners is for the Company to retain the right to use the FSRU and to charter the vessel to a third party starting in January 2015 and ending in June 2015. Any hire received during this period will belong to the Company. In return for this, the Company will pay Golar Partners $22 million to be paid in equal monthly instalments starting in January 2015.

This transaction is the sixth dropdown of assets to Golar Partners since its IPO in April 2011.

Published: 22:28 CET 15-12-2014 /GlobeNewswire /Source: Golar LNG / : GOL /ISIN: BMG9456A1009

Sale of Golar Eskimo to Golar LNG Partners L.P.

Golar LNG Limited (the "Company") announced today that it has entered into an agreement to sell its ownership interests in the companies that will own and operate the floating storage and regasification unit ("FSRU") Golar Eskimo ("Eskimo") to Golar LNG Partners L.P. ("Golar Partners") for a price of USD 390 million. The transaction is subject to the satisfaction of certain closing conditions which is expected to be finalized in January 2015.

The Partnership will finance the purchase price with cash on hand, the proceeds of a $220.0 million loan from the Company and the assumption of outstanding bank debt in respect of the Golar Eskimo on the closing date of the acquisition (which is be approximately $162.8 million). The loan is for a term of 2 years with a rate of interest of LIBOR plus a blended margin of 2.84%.

Part of the agreement with Golar Partners is for the Company to retain the right to use the FSRU and to charter the vessel to a third party starting in January 2015 and ending in June 2015. Any hire received during this period will belong to the Company. In return for this, the Company will pay Golar Partners $22 million to be paid in equal monthly instalments starting in January 2015.

This transaction is the sixth dropdown of assets to Golar Partners since its IPO in April 2011.

Golar LNG Partners declare quarterly cash distribution

Golar LNG Partners said that its board of directors has declared a quarterly cash distribution with respect to the quarter ended December 31, 2014 of $0.5625 per unit.This represents an increase of $0.015 per unit, or approximately 2.7%, from the third quarter 2014 distribution.

This cash distribution will be paid on February 13, 2015 to all unitholders of record as of the close of business on February 5, 2015.

nachgelegt

Golar LNG Partners Unit Purchase Program

Published: 18:18 CEST 04-08-2015 /GlobeNewswire /Source: Golar LNG / : GOL /ISIN: BMG9456A1009Golar LNG Limited ("Golar" or the "Company") today announced that it has approved a unit purchase program under which the Company may purchase up to $25 million worth of Golar LNG Partners L.P. outstanding units over the next 12 months. The authorization is effective immediately. Given Golar LNG Partners' current yield of approximately 11%, the Company views this purchase program as an attractive investment opportunity.

The Company intends to purchase units from time to time for cash in open market transactions or in privately-negotiated transactions in accordance with applicable federal securities laws. The timing and the amount of any purchases will be determined by the Company's management based on its evaluation of market conditions, capital allocation alternatives, and other factors. The unit purchase program does not require the Company to acquire any specific number of units and may be modified, suspended, extended or terminated by the Company at any time without prior notice. Golar will execute purchases only during periods where the executive team and the Board of Directors are not aware of material inside information that would likely affect a seller's decision to sell.

Golar LNG Limited

Hamilton, Bermuda

4 August, 2015

Antwort auf Beitrag Nr.: 50.333.730 von R-BgO am 05.08.15 09:17:52

Aber, wenn ich einen Rohstoff nur transportiere, dann kann es doch nichts ausmachen, wie der Preis der Ware ist oder mache ich jetzt einen Denkfehler?

Warum leidet die Aktie so stark?

Hängt es mit dem Preisverfall für Erdgas zusammen?Aber, wenn ich einen Rohstoff nur transportiere, dann kann es doch nichts ausmachen, wie der Preis der Ware ist oder mache ich jetzt einen Denkfehler?

Antwort auf Beitrag Nr.: 50.778.018 von kainza am 05.10.15 15:49:06

habe -für mich- substantielle Positionen von Golar, Gaslog, Dynagas, Hoegh und Teekay aufgebaut, daneben in geringerem Umfang auch LPG-Transporteure mit BW LPG, Avance, Stealth, Dorian LPG, Exmar, ...

grundsätzlich denke ich, dass die Abstrafung zwar einerseits mit der Energy-Sippenhaft zu tun hat, aber andererseits auch -wie immer- das Risiko besteht, dass überinvestiert wird, was dann die Preise kaputtmacht

Fakt scheint zu sein, dass aktuell eher zu viele Schiffe im Angebot sind, während die projektierten LNG-Terminals etwas hinterher hängen; siehe dazu auch Thread: LNG, LPG etc. - Übersichtsthread

deswegen kaufe ich lieber die MLP-Töchter, die mit längeren Verträgen ausgestattet sind, als die Mütter, die das Risiko haben ihre newbuilds nicht loszuwerden...

die längsten Restlaufzeiten sehe ich bei Höegh LNG Partners und Teekay LNG Partners

zumindest denkst Du genauso wie ich,

deswegen habe ich im letzten Jahr munter Aktien der LNG-Transporteure akkumuliert;habe -für mich- substantielle Positionen von Golar, Gaslog, Dynagas, Hoegh und Teekay aufgebaut, daneben in geringerem Umfang auch LPG-Transporteure mit BW LPG, Avance, Stealth, Dorian LPG, Exmar, ...

grundsätzlich denke ich, dass die Abstrafung zwar einerseits mit der Energy-Sippenhaft zu tun hat, aber andererseits auch -wie immer- das Risiko besteht, dass überinvestiert wird, was dann die Preise kaputtmacht

Fakt scheint zu sein, dass aktuell eher zu viele Schiffe im Angebot sind, während die projektierten LNG-Terminals etwas hinterher hängen; siehe dazu auch Thread: LNG, LPG etc. - Übersichtsthread

deswegen kaufe ich lieber die MLP-Töchter, die mit längeren Verträgen ausgestattet sind, als die Mütter, die das Risiko haben ihre newbuilds nicht loszuwerden...

die längsten Restlaufzeiten sehe ich bei Höegh LNG Partners und Teekay LNG Partners

Antwort auf Beitrag Nr.: 50.778.201 von R-BgO am 05.10.15 16:03:58

Überkapazitäten tuen sich schnell auf. Erscheint ein Markt lukrativ, will jeder mitmischen. Das ist wie mit den Offshoredrillern, die vor einigen Jahren zusätzliche deepsea-Flotten in Auftrag gegeben haben. Dann kam der große Frackingboom und die Preise stürzten. Jetzt fallen die dayrates und Verträge werden nicht mehr verlängert.

Für Rohstoffe sieht es allgemein nicht gut aus. Habe dazu meine Meinung.

Die Rohstoffpreise fallen seit 2011 zunächst langsam und seit einem Jahr beschleunigt. 2011 war ein Minicrash an den Börsen, den die FED mit billigem Geld geheilt hat. Aber in der Weltwirtschaft läuft es wohl nicht mehr so richtig, wenn der Rohstoffindex jetzt tiefer steht als 2009.

Dazu kommen jetzt die High-Yields Anleihen der Energiebranche. Bleibt abzuwarten, wie viele noch frisches Geld auf dem Markt aufnehmen können.

Danke für deinen Hinweis!

Zitat von R-BgO: deswegen habe ich im letzten Jahr munter Aktien der LNG-Transporteure akkumuliert;

habe -für mich- substantielle Positionen von Golar, Gaslog, Dynagas, Hoegh und Teekay aufgebaut, daneben in geringerem Umfang auch LPG-Transporteure mit BW LPG, Avance, Stealth, Dorian LPG, Exmar, ...

grundsätzlich denke ich, dass die Abstrafung zwar einerseits mit der Energy-Sippenhaft zu tun hat, aber andererseits auch -wie immer- das Risiko besteht, dass überinvestiert wird, was dann die Preise kaputtmacht

Fakt scheint zu sein, dass aktuell eher zu viele Schiffe im Angebot sind, während die projektierten LNG-Terminals etwas hinterher hängen; siehe dazu auch Thread: LNG, LPG etc. - Übersichtsthread

deswegen kaufe ich lieber die MLP-Töchter, die mit längeren Verträgen ausgestattet sind, als die Mütter, die das Risiko haben ihre newbuilds nicht loszuwerden...

die längsten Restlaufzeiten sehe ich bei Höegh LNG Partners und Teekay LNG Partners

Überkapazitäten tuen sich schnell auf. Erscheint ein Markt lukrativ, will jeder mitmischen. Das ist wie mit den Offshoredrillern, die vor einigen Jahren zusätzliche deepsea-Flotten in Auftrag gegeben haben. Dann kam der große Frackingboom und die Preise stürzten. Jetzt fallen die dayrates und Verträge werden nicht mehr verlängert.

Für Rohstoffe sieht es allgemein nicht gut aus. Habe dazu meine Meinung.

Die Rohstoffpreise fallen seit 2011 zunächst langsam und seit einem Jahr beschleunigt. 2011 war ein Minicrash an den Börsen, den die FED mit billigem Geld geheilt hat. Aber in der Weltwirtschaft läuft es wohl nicht mehr so richtig, wenn der Rohstoffindex jetzt tiefer steht als 2009.

Dazu kommen jetzt die High-Yields Anleihen der Energiebranche. Bleibt abzuwarten, wie viele noch frisches Geld auf dem Markt aufnehmen können.

seadrill und Golar haben keine Gemeinsamkeiten

die Floating Technologie ist bei LNG deutlich günstiger als die landbasierten Lösungen

und bei Rohstoffprojekten geht es nur um die Produktionskosten

je niedriger der Preis für LNG,desto grösser die Vorteile für Golar

die Floating Technologie ist bei LNG deutlich günstiger als die landbasierten Lösungen

und bei Rohstoffprojekten geht es nur um die Produktionskosten

je niedriger der Preis für LNG,desto grösser die Vorteile für Golar

zudem unterscheidet sich Golar von dem Rest darin,dass sie sich in den nächsten Jahren zu einem integriertem LNG Dienstleistungsunternehmen mausern werden.

Die GoFLNG Schiffe sind mit vollwertigen Verflüssigungsanlagen ausgestattet.

Dasselbe macht Shell mit der Prelude.

Das erste FLNG Projekt hat Golar mit Cameroon vor wenigen Taegn unterzeichnet.Cameroon hat zusätzlich noch eine Kreditlinie zur Verfügung gestellt.

3 weitere FLNG Schiffe stehen in den nächsten Jahren in den Startlöchern.

Naheliegend ist,dass sie dann auch eigene Tanker einsetzen werden.

1)Marktvorsprung

2)Technologie ermöglicht die günstigsten Förderkosten im LNG Bereich(Katar mal aussen vor)

3)integrierter Anbieter

Klar,wenn sich herausstellen sollte,dass GoFLNG in der Realität nicht funktioniert,ist Golar LTD. platt.Dann wird man an Golar Partners auch keine Freude haben.

Das hat aber dann wenig bis gar nichts mit dem weltwirtschaftlichen Umfeld zu tun,und ist aus meiner Sicht zudem unwahrscheinlich.

Die GoFLNG Schiffe sind mit vollwertigen Verflüssigungsanlagen ausgestattet.

Dasselbe macht Shell mit der Prelude.

Das erste FLNG Projekt hat Golar mit Cameroon vor wenigen Taegn unterzeichnet.Cameroon hat zusätzlich noch eine Kreditlinie zur Verfügung gestellt.

3 weitere FLNG Schiffe stehen in den nächsten Jahren in den Startlöchern.

Naheliegend ist,dass sie dann auch eigene Tanker einsetzen werden.

1)Marktvorsprung

2)Technologie ermöglicht die günstigsten Förderkosten im LNG Bereich(Katar mal aussen vor)

3)integrierter Anbieter

Klar,wenn sich herausstellen sollte,dass GoFLNG in der Realität nicht funktioniert,ist Golar LTD. platt.Dann wird man an Golar Partners auch keine Freude haben.

Das hat aber dann wenig bis gar nichts mit dem weltwirtschaftlichen Umfeld zu tun,und ist aus meiner Sicht zudem unwahrscheinlich.

Report: Gazprom M&T books full capacity at Cameroon FLNG project

Gazprom Marketing & Trading has reportedly firmed up an agreement to offtake 1.2 mtpa from the Cameroon FLNG project being developed by Golar LNG, Perenco and Societe Nationale de Hydrocarbures.As reported by Interfax, the deal, priced between US$7-8 per mmBtu has no destination clause, meaning the cargoes from the project could end up being delivered to Latin America, North Africa or East Asia.

A final investment decision on the Cameroon FLNG project was reached at the end of September, with Golar stating that commissioning is targeted for the second quarter of 2017.

The project, based on the allocation of 500 Bcf of natural gas reserves from offshore Kribi fields, will have a production capacity of 1.2 million tons of LNG per year, meaning Gazprom Marketing & Trading booked the projects full output.

Keppel Shipyard in Singapore is currently working on a US$1.2 billion conversion of a Golar LNG carrier Hilli into an FLNG facility and is scheduled to complete works by February 2017.

Das sieht aber heute ganz böse aus, gibt es etwas neues?

Antwort auf Beitrag Nr.: 51.327.417 von 1erhart am 17.12.15 17:16:59

GasLog (GLOG -13.6%) and Golar LNG (GLNG -8.1%) are sharply lower in the wake of the Teekay dividend cuts, as the market focuses on GLOG and GLNG following Teekay's (TK -55.6%) announcement and Kinder Morgan's cut earlier this month.

Wells Fargo downgrades TK and GLOG to Market Perform from Outperform, saying pressure around dividend cuts is likely to continue weighing on the stocks.

The firm issues reduced price target ranges for the stocks, to $18-$20 from $35-$37 for TK and to $10-$12 from $21-$23 at GLNG.Also: TGP -45.8%, GMLP -34%, GLOP -8.4%, STNG -3.5%, NNA -3.2%, NAP -2.2%.

sieht nach Sippenhaft aus:

2015, 10:48 ET | About: GasLog (GLOG) | By: Carl Surran, SA News Editor Contact this editor with comments or a news tipGasLog (GLOG -13.6%) and Golar LNG (GLNG -8.1%) are sharply lower in the wake of the Teekay dividend cuts, as the market focuses on GLOG and GLNG following Teekay's (TK -55.6%) announcement and Kinder Morgan's cut earlier this month.

Wells Fargo downgrades TK and GLOG to Market Perform from Outperform, saying pressure around dividend cuts is likely to continue weighing on the stocks.

The firm issues reduced price target ranges for the stocks, to $18-$20 from $35-$37 for TK and to $10-$12 from $21-$23 at GLNG.Also: TGP -45.8%, GMLP -34%, GLOP -8.4%, STNG -3.5%, NNA -3.2%, NAP -2.2%.

Antwort auf Beitrag Nr.: 51.328.077 von R-BgO am 17.12.15 18:42:35Jo, Sippenhaft. Und Schnäppchenpreise.

Aber bitte beachten: Es ist durchaus möglich, wenn nicht wahrscheinlich, dass die Divs gekürzt werden (aktuell ja nördlich von 25%). Die Partnerships von Golar, Dynagas, Gaslog, etc können klassischerweise nur über Kredite oder die Ausgabe neuer Anteilsscheine das nötige Kapital aufbringen, das zum Wachstum nötig ist (Erwerb der Schiffe von der Mutter). Die aktuelle Stimmung am Bondmarkt bzw. Aktienpreise machen beides aber unmöglich. Daher ist die Verwendung von Cashflow eigentlich die einzige Möglichkeit zum Wachstum (statt den Cashflow fast komplett auszuschütten). Nach einem Div-Cut könnten sie auch wieder über die Ausgabe neuer Anteile nachdenken (hoffentlich nicht, wg. Verwässerung). Wenn der Div-cut kommen sollte, wird der Preis wohl noch einmal kräftig nachgeben, siehe TGP heute. Es wären dann aber erst recht Kaufkurse, denn das Geschäftsmodell ist ja gut! (üppig Cashflow, gute Wachstumsaussichten, gefragter Nischenmarkt).

Ich habe heute ein wenig gekauft, und warte (hoffe) auf einen Div-Cut bis zum richtigen Einstieg.

Vor allem GMLP wegen einzigartigem Geschäftsmodell gefällt mir (nur Hoegh kommt da auch mit) und GLOP scheinen mir gut (noch relativ wenige Schulden, soweit ich weiß). Und DLNG-A ist auch ein heftiges Schnäppchen, wenn man an die Story glaubt. Aber die konnte ich über OnVista nicht bekommen

Aber bitte beachten: Es ist durchaus möglich, wenn nicht wahrscheinlich, dass die Divs gekürzt werden (aktuell ja nördlich von 25%). Die Partnerships von Golar, Dynagas, Gaslog, etc können klassischerweise nur über Kredite oder die Ausgabe neuer Anteilsscheine das nötige Kapital aufbringen, das zum Wachstum nötig ist (Erwerb der Schiffe von der Mutter). Die aktuelle Stimmung am Bondmarkt bzw. Aktienpreise machen beides aber unmöglich. Daher ist die Verwendung von Cashflow eigentlich die einzige Möglichkeit zum Wachstum (statt den Cashflow fast komplett auszuschütten). Nach einem Div-Cut könnten sie auch wieder über die Ausgabe neuer Anteile nachdenken (hoffentlich nicht, wg. Verwässerung). Wenn der Div-cut kommen sollte, wird der Preis wohl noch einmal kräftig nachgeben, siehe TGP heute. Es wären dann aber erst recht Kaufkurse, denn das Geschäftsmodell ist ja gut! (üppig Cashflow, gute Wachstumsaussichten, gefragter Nischenmarkt).

Ich habe heute ein wenig gekauft, und warte (hoffe) auf einen Div-Cut bis zum richtigen Einstieg.

Vor allem GMLP wegen einzigartigem Geschäftsmodell gefällt mir (nur Hoegh kommt da auch mit) und GLOP scheinen mir gut (noch relativ wenige Schulden, soweit ich weiß). Und DLNG-A ist auch ein heftiges Schnäppchen, wenn man an die Story glaubt. Aber die konnte ich über OnVista nicht bekommen

Antwort auf Beitrag Nr.: 51.329.505 von hannes2000 am 17.12.15 22:22:42

Na, da lag ich teilweise wohl falsch. Die Lage ist besser als ich angenommen hatte. Heute eine PM, u.a. mit folgendem Inhalt: (s. Firmen-Webseite)

"As at September 30, 2015 the Partnership had a total revenue backlog of $2.5 billion and a net debt to annualized third quarter 2015 EBITDA ratio of 3.4 and also does not have any newbuilding capital commitments."

D.h. von dieser Seite (capex Bedarf) besteht offenbar keine akute Notwendigkeit, die Divs zu kürzen. Was allerdings fehlt, ist ein zeitlicher Aspekt zu dieser Aussage... Vielmehr hat man hat aktuell offenbar sogar noch Geld für ein Rückkaufprogramm übrig:

"The Partnership also announced that the Board has authorized the repurchase by the Partnership of up to $25 million of its outstanding common units. "

Auch wenn der Betrag zunächst eher symbolisch erscheint, können damit immerhin >3% der Anteile zurückgekauft werden (wenn ich richtig rechne).

Ich habe heute also noch mehr eingekauft. Noch keine "volle" Position, aber für eine riskante, aber dafür aussichtsreiche Spekulation schon nicht schlecht. Der Kurs hat auch schon prompt und kräftig reagiert - aber erst nachdem in NY die Börsen aufgemacht haben.

GMLP

Na, da lag ich teilweise wohl falsch. Die Lage ist besser als ich angenommen hatte. Heute eine PM, u.a. mit folgendem Inhalt: (s. Firmen-Webseite)

"As at September 30, 2015 the Partnership had a total revenue backlog of $2.5 billion and a net debt to annualized third quarter 2015 EBITDA ratio of 3.4 and also does not have any newbuilding capital commitments."

D.h. von dieser Seite (capex Bedarf) besteht offenbar keine akute Notwendigkeit, die Divs zu kürzen. Was allerdings fehlt, ist ein zeitlicher Aspekt zu dieser Aussage... Vielmehr hat man hat aktuell offenbar sogar noch Geld für ein Rückkaufprogramm übrig:

"The Partnership also announced that the Board has authorized the repurchase by the Partnership of up to $25 million of its outstanding common units. "

Auch wenn der Betrag zunächst eher symbolisch erscheint, können damit immerhin >3% der Anteile zurückgekauft werden (wenn ich richtig rechne).

Ich habe heute also noch mehr eingekauft. Noch keine "volle" Position, aber für eine riskante, aber dafür aussichtsreiche Spekulation schon nicht schlecht. Der Kurs hat auch schon prompt und kräftig reagiert - aber erst nachdem in NY die Börsen aufgemacht haben.

Golar Ltd. braucht doch die Liquidität aus den Dividenden

Golar Partners wird erstmal ihren Spielraum auf der Fremdkapitalseite ausreizen

die werden 2016 keine Dividende kürzen

Golar Partners wird erstmal ihren Spielraum auf der Fremdkapitalseite ausreizen

die werden 2016 keine Dividende kürzen

drop-down:

...verstehe nur das Timing nicht so ganz:Published: 15:16 CET 10-02-2016 /GlobeNewswire /Source: Golar LNG / : GOL /ISIN: BMG9456A1009

Sale of FSRU Golar Tundra to Golar LNG Partners LP

Hamilton, Bermuda: Golar LNG Limited ("Golar") announced today that it has entered into a purchase agreement to sell the Golar Tundra, a floating storage and regasification unit, to Golar LNG Partners LP ("Golar Partners" or the "Partnership") for a sale price of $330.0 million.

In connection with the closing, the Partnership will receive a daily fee plus operating expenses, aggregating to approximately $2.6 million per month, for Golar's right to use the FSRU from the date of the closing until the date that the Golar Tundra commences operations under its time charter with West Africa Gas Limited. In return, the Partnership will remit to Golar any hire income received with respect to the Golar Tundra during this period. The sale is expected to close in March 2016 and the vessel is expected to commence operations under its time charter with West Africa Gas Limited at the end of the second quarter of 2016.

The sale of the Golar Tundra will strengthen Golar's liquidity by approximately $130 million. The sale has been arranged in accordance with the Omnibus Agreement which regulates Golar's obligation to offer any vessel on charter for more than five years to the Partnership.

Hier mal was neues zur Dividende schaut nicht schlecht aus

http://mydividends.de/content/golar-lng-partners-sch%C3%BCtt…

http://mydividends.de/content/golar-lng-partners-sch%C3%BCtt…

Die Anleihen notieren zu:

(2017er) 97,5% => 8,2% Rendite; http://www.wallstreet-online.de/anleihen/a1ha02-golar-lng-pa…(2020er) 86,2% => 9,8% Rendite; http://www.wallstreet-online.de/anleihen/211520740

beide nicht nachrangig

das hat mich auch nachdenklich gemacht

zudem dreht Golar LTD ein Riesenrad

und verliert derzeit massig Geld pro Quartal

China wird auch nicht jedes Quartal 1 Billion US-Dollar locker machen

Ich nutze die steigenden Kurse bei Golar Partners zum Verkauf

mein Depotanteil lag zum Kurstief aber auch über 50%

zudem dreht Golar LTD ein Riesenrad

und verliert derzeit massig Geld pro Quartal

China wird auch nicht jedes Quartal 1 Billion US-Dollar locker machen

Ich nutze die steigenden Kurse bei Golar Partners zum Verkauf

mein Depotanteil lag zum Kurstief aber auch über 50%

Antwort auf Beitrag Nr.: 52.529.150 von bernieschach am 02.06.16 19:19:50Ja, die 86% Anleihe ist ja aber von der Mutter GLNG, nicht von GMLP. Bei Golar hat man derzeit schon größere Probleme mit den geringen Spot-Preisen bei den LNG-Tankern, während gleichzeitig die Umbauten jede Menge cash brauchen.

GMLP ist im Kurs dagegen letzte Woche richtig nach oben gesprungen (10% am Donnerstag). Gabs da Neuigkeiten? Ich habe auf die Schnelle nix gefunden...

GMLP ist im Kurs dagegen letzte Woche richtig nach oben gesprungen (10% am Donnerstag). Gabs da Neuigkeiten? Ich habe auf die Schnelle nix gefunden...

Hab die Hälfte von GMLP verkauft. Ist in diesem Jahr seit den Tiefs ja auch mal gut gelaufen (Posi ist +50%). Eine hälfte bleibt im Depot für die üppige Div, der frei werdende Betrag wurde/wird in TGP investiert.

Antwort auf Beitrag Nr.: 53.398.716 von hannes2000 am 03.10.16 17:37:57Na, das nenne ich mal schlechtes Timing. Immerhin hab ich noch die Hälfte.

So hab ich die letzte Aktion zwischen Golar und GMLP verstanden:

GMLP hat die IDRs von Golar "zurückgekauft", d.h. der Anteil, der bei den common unit holders bleibt, ist nun höher, die Ansprüche (IDRs) des "General Partners" niedriger. Golar als "General Partner" bekommt also etwas weniger, bzw. erst wieder wenn GMLP die Divs deutlich erhöht hat. Nur durch den Deal wird es möglich, dass GMLP in der Zukunft weiter effektiv wachsen kann, und dass künftig die Divs auch weiter deutlich erhöht werden können. Erkaufen tut sich das GMLP durch die Ausgabe von common units an Golar. Diese neuen Units bringen nun natürlich erstmal keinen neuen Cashflow. Aber immerhin ist das Wachstumspotenzial nun besser und durch den höheren Kurs kann es künftig deutlich effektiver / leichter zu neuen Dropdowns und Div-Steigerungen kommen.

Soweit mein Verständnis des Ganzen - Ohne Gewähr. Wenn das eine falsche Darstellung war, bitte ich um Berichtigung.

So hab ich die letzte Aktion zwischen Golar und GMLP verstanden:

GMLP hat die IDRs von Golar "zurückgekauft", d.h. der Anteil, der bei den common unit holders bleibt, ist nun höher, die Ansprüche (IDRs) des "General Partners" niedriger. Golar als "General Partner" bekommt also etwas weniger, bzw. erst wieder wenn GMLP die Divs deutlich erhöht hat. Nur durch den Deal wird es möglich, dass GMLP in der Zukunft weiter effektiv wachsen kann, und dass künftig die Divs auch weiter deutlich erhöht werden können. Erkaufen tut sich das GMLP durch die Ausgabe von common units an Golar. Diese neuen Units bringen nun natürlich erstmal keinen neuen Cashflow. Aber immerhin ist das Wachstumspotenzial nun besser und durch den höheren Kurs kann es künftig deutlich effektiver / leichter zu neuen Dropdowns und Div-Steigerungen kommen.

Soweit mein Verständnis des Ganzen - Ohne Gewähr. Wenn das eine falsche Darstellung war, bitte ich um Berichtigung.

Antwort auf Beitrag Nr.: 53.505.981 von hannes2000 am 19.10.16 10:56:17

Immerhin bekommt Solar vorab was in die Flossen, was sie vielleicht auch direkt zu Geld machen können

ich hab's auch so verstanden;

allerdings ist mir nicht klar, wer dabei den besseren Deal gemacht hat.Immerhin bekommt Solar vorab was in die Flossen, was sie vielleicht auch direkt zu Geld machen können

Antwort auf Beitrag Nr.: 53.506.068 von R-BgO am 19.10.16 11:03:22

Jo, wer den besseren Deal gemacht hat, weiß ich auch nicht. Die tatsächlichen Zahlen durchzukauen und zu bewerten dazu sehe ich mich nicht in der Lage. Vom Kurs her haben haben beide in den letzten Tagen profitiert. Soweit ich das sehe, hat Golar scheinbar immer akuten Kapitalbedarf, von daher ist der Vorschuss und die Units vermutlich nicht schlecht (wohl kaum schlechter als die IDRs?). GMLP bekommt Wachstumspotenzial, und muss dafür erst mal nur blechen.

Zitat von R-BgO: allerdings ist mir nicht klar, wer dabei den besseren Deal gemacht hat.

Immerhin bekommt Solar vorab was in die Flossen, was sie vielleicht auch direkt zu Geld machen können

Jo, wer den besseren Deal gemacht hat, weiß ich auch nicht. Die tatsächlichen Zahlen durchzukauen und zu bewerten dazu sehe ich mich nicht in der Lage. Vom Kurs her haben haben beide in den letzten Tagen profitiert. Soweit ich das sehe, hat Golar scheinbar immer akuten Kapitalbedarf, von daher ist der Vorschuss und die Units vermutlich nicht schlecht (wohl kaum schlechter als die IDRs?). GMLP bekommt Wachstumspotenzial, und muss dafür erst mal nur blechen.

Golar LNG Partners L.P. - Successful Placement of New Unsecured Bonds

Golar LNG Partners L.P. has successfully completed the issuance of a USD 250 million senior unsecured bond in the Nordic bond market.

The bond issue was significantly oversubscribed.

Settlement is expected to be February 15, 2017 with final maturity date expected May 15, 2021. The new bond issue has a coupon of 3 month LIBOR + 6.25%. An application will be made for the bonds to be listed on the Oslo Stock Exchange.

The net proceeds from the bond issue will be used for part refinancing of existing bonds and for general corporate purposes.

Danske Bank Markets, DNB Markets, Nordea, SEB and Pareto Securities acted as Joint Lead Managers for the bond issuance.

This press release is neither an offer to sell nor a solicitation of an offer to buy any of the bonds or any other security of Golar LNG Partners LP. The bonds have not been and will not be registered under the Securities Act or any state securities laws. Unless so registered, the bonds may not be offered or sold in the United States except pursuant to an exemption from the registration requirements of the Securities Act and applicable state securities laws.

Hamilton, Bermuda

February 1, 2017

Golar LNG Partners L.P. has successfully completed the issuance of a USD 250 million senior unsecured bond in the Nordic bond market.

The bond issue was significantly oversubscribed.

Settlement is expected to be February 15, 2017 with final maturity date expected May 15, 2021. The new bond issue has a coupon of 3 month LIBOR + 6.25%. An application will be made for the bonds to be listed on the Oslo Stock Exchange.

The net proceeds from the bond issue will be used for part refinancing of existing bonds and for general corporate purposes.

Danske Bank Markets, DNB Markets, Nordea, SEB and Pareto Securities acted as Joint Lead Managers for the bond issuance.

This press release is neither an offer to sell nor a solicitation of an offer to buy any of the bonds or any other security of Golar LNG Partners LP. The bonds have not been and will not be registered under the Securities Act or any state securities laws. Unless so registered, the bonds may not be offered or sold in the United States except pursuant to an exemption from the registration requirements of the Securities Act and applicable state securities laws.

Hamilton, Bermuda

February 1, 2017

Antwort auf Beitrag Nr.: 54.229.759 von R-BgO am 03.02.17 09:33:20

Golar LNG Partners LP Announces Pricing of Public Offering

February 08, 2017 04:42 ET | Source: Golar LNG Partners LP

Golar LNG Partners LP ("Golar Partners" or the "Partnership") (NASDAQ: GMLP) announces that it has priced its previously announced underwritten public offering of 4,500,000 common units representing limited partner interests in the Partnership for total gross proceeds of approximately $103.5 million. The Partnership has granted the underwriters a 30-day option to purchase up to 675,000 additional common units from the Partnership. The underwriter intends to offer our common units in transactions on the Nasdaq Global Market, in the over-the-counter market or through negotiated transactions at market prices or at negotiated prices. The Partnership expects to close the sale of the common units on February 13, 2017.

The Partnership intends to use the net proceeds that it receives in the offering and the related capital contribution by its general partner to maintain its 2% general partner interest for general partnership purposes, which may include, among other things, repaying indebtedness and funding working capital, capital expenditures or acquisitions.

KE gibt's auch:

zu 23$Golar LNG Partners LP Announces Pricing of Public Offering

February 08, 2017 04:42 ET | Source: Golar LNG Partners LP

Golar LNG Partners LP ("Golar Partners" or the "Partnership") (NASDAQ: GMLP) announces that it has priced its previously announced underwritten public offering of 4,500,000 common units representing limited partner interests in the Partnership for total gross proceeds of approximately $103.5 million. The Partnership has granted the underwriters a 30-day option to purchase up to 675,000 additional common units from the Partnership. The underwriter intends to offer our common units in transactions on the Nasdaq Global Market, in the over-the-counter market or through negotiated transactions at market prices or at negotiated prices. The Partnership expects to close the sale of the common units on February 13, 2017.

The Partnership intends to use the net proceeds that it receives in the offering and the related capital contribution by its general partner to maintain its 2% general partner interest for general partnership purposes, which may include, among other things, repaying indebtedness and funding working capital, capital expenditures or acquisitions.

Tolle News...

Na, da habe ich mir ja gestern einen tollen Zeitpunkt zum Einstieg ausgesucht

Allerdings sehe ich die News auch positiv: Wenn man davon ausgeht - und dazu brauchts mMn beim aktuellen Marktausblick für 17/18 nicht viel Optimismus - dass man das gzum Juni gekündigte Golar Spirit direkt wieder zu möglichst ähnlichen Konditionen vermietet bekommt, dann hat man aufgrund der Strafzahlung für dieses Jahr schonmal einen sehr schönen Zusatzgewinn.

Einhergehend wurde auch der Abschluss der letzten Finanzierung verkündet. Cash haben sie jetzt also mehr als genug. Spannend wird jetzt die Verlängerung der auslaufenden und des gekündigten Vertrags...

M. E. ist der Kursrückgang heute eine gute Einstiegsgelegenheit. Hoffentlich vorerst die letzte

News:

http://seekingalpha.com/pr/16755755-golar-lng-partners-l-p-p…

Slides

http://seekingalpha.com/article/4050473-golar-lng-partners-l…

Antwort auf Beitrag Nr.: 54.431.942 von TraeidIngIdI0t am 28.02.17 17:50:21

http://seekingalpha.com/pr/16774374-golar-lng-partners-l-p-n…

Das mindert schon mal das Risiko und die Chance ist hoch, das man auch in den Gesprächen über den zweiten auslaufenden Vertrag, die Golar Maria bald Positives verkünden kann.

Und dann bleibt noch spannend, was nun im FSRU-Bereich weiter erreicht werden kann.

Stay tuned with GMLP! ;-)

Erste Vertragsverlängerung gesichert...

Sehr schöne News! Wie in der letzten Präsi angekündigt, hat man für einen der beiden Carrier (Golar Grand) mit auslaufendem Vertrag einen neuen Vertragspartner bekommen:http://seekingalpha.com/pr/16774374-golar-lng-partners-l-p-n…

Das mindert schon mal das Risiko und die Chance ist hoch, das man auch in den Gesprächen über den zweiten auslaufenden Vertrag, die Golar Maria bald Positives verkünden kann.

Und dann bleibt noch spannend, was nun im FSRU-Bereich weiter erreicht werden kann.

Stay tuned with GMLP! ;-)

Hier mal ein Update hoffentlich kann Golar LNG davon Profitieren

https://www.australianmining.com.au/news/australian-lng-expo…

https://www.australianmining.com.au/news/australian-lng-expo…

kompliziert...:

Golar LNG Limited - Sale of an Interest in the FLNG, Hilli Episeyo

Golar LNG Limited (NASDAQ: GLNG) ("Golar") announced today that it and affiliates of Keppel Shipyard Limited ("Keppel") and Black and Veatch ("B&V") have entered into a purchase and sale agreement (the "PSA") for the sale (the "Sale") of equity interests (the "Interests") in Golar Hilli LLC to Golar LNG Partners L.P. (the "Partnership"), which will, on the closing date of the Sale, indirectly own the Hilli Episeyo (the "Hilli"), a floating liquefied natural gas vessel.

The Acquired Interests represent the equivalent of 50% of the two liquefaction trains, out of a total of four, that have been contracted to Perenco Cameroon SA and Societe Nationale Des Hydrocarbures (together, the "Customer") for an eight-year term.

The sale price for the Interests, as described below, is $658 million less net lease obligations under the financing facility for the Hilli (the "Hilli Facility") that are expected to be between $468 and $480 million. Concurrent with the execution of the PSA, the Partnership paid a $70 million deposit to Golar, on which the Partnership will receive interest at a rate of 5% per annum.

The closing of the Sale (the "Closing") is subject to the satisfaction of certain closing conditions which include, among others, receiving the consent of the lenders under the Hilli Facility, the closing of the previously announced put-sale closing with respect to the Golar Tundra (the "Tundra Put Sale"), the delivery to and acceptance by the Customer of the Hilli, the commencement of commercial operations under the liquefaction tolling agreement (the "LTA") and the formation of Golar Hilli LLC and the related Pre-Closing Contributions as described further below.

Prior to the Closing, Golar, Keppel and B&V will contribute their equity interests in Golar Hilli Corporation ("Hilli Corp"), the entity that owns the Hilli, to the newly formed Golar Hilli LLC (the "Pre-Closing Contributions") in return for equity interests in Golar Hilli LLC.

Membership interests in Golar Hilli LLC will be represented by three classes of units:

*Common Units ("Common Units");

*Series A Special Units ("Series A Units"); and

*Series B Special Units ("Series B Units").

Common Units will be entitled to cash flows from the first 50% of contracted capacity, initially contracted to the Customer under the LTA. Common Units will not be exposed to the oil-linked pricing elements of the tolling fee under the LTA but will bear the operating costs of the Hilli, with only incremental costs ("Incremental Costs") accruing to the Series B Units and the interest costs of the Hilli Facility.

Series A Units will only be entitled to cash flows associated with oil price linked elements of the tolling fee under the LTA, net of incremental tax expenses and their pro rata portion of any costs that may arise as a result of the underperformance of the Hilli ("Underperformance Costs").

Holders of Series B Units will be entitled to the cash flows associated with any expansion of contracted capacity of the Hilli beyond the first 50%, net of Incremental Costs arising as a result of making available more than the first 50% of production capacity of the Hilli, Underperformance Costs and any reduction in revenue attributable to the first 50% of LNG production capacity as a result of making more than 50% of capacity available under the LTA.

Through the Sale, the Partnership will only acquire 50% of the Common Units and none of the Series A Units or Series B Units.

Upon the Closing, which is expected to occur on or before April 30, 2018, Golar, Keppel and B&V will sell 50% of the Common Units to the Partnership in return for the payment of the net purchase price of between approximately $178 and $190 million.

The Partnership will apply the $107 million deferred purchase price receivable from Golar in connection with the Tundra Put Sale and the $70 million deposit referred to above against the net purchase price and will pay the balance with cash on hand.

The Hilli conversion is nearing completion and no major issues have been identified. All equipment has been installed and pre-commissioning work is well underway. Golar is focused on doing as much testing as possible in the yard and at anchorage in order to minimise the risk of issues being encountered in Cameroon. The extra days spent in Singapore are expected to reduce the time required for commissioning on site. The Hilli is scheduled to leave Singapore for Cameroon at the end of September or beginning of October. LNG bunkering has been booked for mid-September. The mooring system has been installed in Cameroon and is ready for hook up of Hilli. All going well, the voyage between Singapore and Cameroon is expected to take 32 to 40 days allowing Golar to tender its notice of readiness during the first half of November. The Customer remains on track with its scope of works and the Hilli conversion currently remains materially under budget.

Golar will draw down the final tranche of the Hilli Facility upon Customer acceptance of the vessel. After settlement of all outstanding conversion costs, Golar currently expects to receive approximately $140 million, net of the Keppel and B&V minority interests, which is additional to the sale proceeds from the Partnership as described above.

Golar LNG Limited - Sale of an Interest in the FLNG, Hilli Episeyo

Golar LNG Limited (NASDAQ: GLNG) ("Golar") announced today that it and affiliates of Keppel Shipyard Limited ("Keppel") and Black and Veatch ("B&V") have entered into a purchase and sale agreement (the "PSA") for the sale (the "Sale") of equity interests (the "Interests") in Golar Hilli LLC to Golar LNG Partners L.P. (the "Partnership"), which will, on the closing date of the Sale, indirectly own the Hilli Episeyo (the "Hilli"), a floating liquefied natural gas vessel.

The Acquired Interests represent the equivalent of 50% of the two liquefaction trains, out of a total of four, that have been contracted to Perenco Cameroon SA and Societe Nationale Des Hydrocarbures (together, the "Customer") for an eight-year term.

The sale price for the Interests, as described below, is $658 million less net lease obligations under the financing facility for the Hilli (the "Hilli Facility") that are expected to be between $468 and $480 million. Concurrent with the execution of the PSA, the Partnership paid a $70 million deposit to Golar, on which the Partnership will receive interest at a rate of 5% per annum.

The closing of the Sale (the "Closing") is subject to the satisfaction of certain closing conditions which include, among others, receiving the consent of the lenders under the Hilli Facility, the closing of the previously announced put-sale closing with respect to the Golar Tundra (the "Tundra Put Sale"), the delivery to and acceptance by the Customer of the Hilli, the commencement of commercial operations under the liquefaction tolling agreement (the "LTA") and the formation of Golar Hilli LLC and the related Pre-Closing Contributions as described further below.

Prior to the Closing, Golar, Keppel and B&V will contribute their equity interests in Golar Hilli Corporation ("Hilli Corp"), the entity that owns the Hilli, to the newly formed Golar Hilli LLC (the "Pre-Closing Contributions") in return for equity interests in Golar Hilli LLC.

Membership interests in Golar Hilli LLC will be represented by three classes of units:

*Common Units ("Common Units");

*Series A Special Units ("Series A Units"); and

*Series B Special Units ("Series B Units").

Common Units will be entitled to cash flows from the first 50% of contracted capacity, initially contracted to the Customer under the LTA. Common Units will not be exposed to the oil-linked pricing elements of the tolling fee under the LTA but will bear the operating costs of the Hilli, with only incremental costs ("Incremental Costs") accruing to the Series B Units and the interest costs of the Hilli Facility.

Series A Units will only be entitled to cash flows associated with oil price linked elements of the tolling fee under the LTA, net of incremental tax expenses and their pro rata portion of any costs that may arise as a result of the underperformance of the Hilli ("Underperformance Costs").

Holders of Series B Units will be entitled to the cash flows associated with any expansion of contracted capacity of the Hilli beyond the first 50%, net of Incremental Costs arising as a result of making available more than the first 50% of production capacity of the Hilli, Underperformance Costs and any reduction in revenue attributable to the first 50% of LNG production capacity as a result of making more than 50% of capacity available under the LTA.

Through the Sale, the Partnership will only acquire 50% of the Common Units and none of the Series A Units or Series B Units.

Upon the Closing, which is expected to occur on or before April 30, 2018, Golar, Keppel and B&V will sell 50% of the Common Units to the Partnership in return for the payment of the net purchase price of between approximately $178 and $190 million.

The Partnership will apply the $107 million deferred purchase price receivable from Golar in connection with the Tundra Put Sale and the $70 million deposit referred to above against the net purchase price and will pay the balance with cash on hand.

The Hilli conversion is nearing completion and no major issues have been identified. All equipment has been installed and pre-commissioning work is well underway. Golar is focused on doing as much testing as possible in the yard and at anchorage in order to minimise the risk of issues being encountered in Cameroon. The extra days spent in Singapore are expected to reduce the time required for commissioning on site. The Hilli is scheduled to leave Singapore for Cameroon at the end of September or beginning of October. LNG bunkering has been booked for mid-September. The mooring system has been installed in Cameroon and is ready for hook up of Hilli. All going well, the voyage between Singapore and Cameroon is expected to take 32 to 40 days allowing Golar to tender its notice of readiness during the first half of November. The Customer remains on track with its scope of works and the Hilli conversion currently remains materially under budget.

Golar will draw down the final tranche of the Hilli Facility upon Customer acceptance of the vessel. After settlement of all outstanding conversion costs, Golar currently expects to receive approximately $140 million, net of the Keppel and B&V minority interests, which is additional to the sale proceeds from the Partnership as described above.

Antwort auf Beitrag Nr.: 55.537.992 von R-BgO am 16.08.17 18:09:25Eine nmM gute Zusammenfassung des Deals (Registrierung notwendig):

https://seekingalpha.com/article/4099921-golar-lng-partners-…

Bin auf den Q2-Report gespannt, da sollte ja die "Strafzahlung von Petrobras wegen der vorzeitigen Vertragsbeendigung rein...

Bin versucht hier nochmal aufzustocken. Die hohe Ausschüttung scheint nun auf lange Sicht sicher...

Wie wird die in Deutschland eigentlich steuerlich behandelt? Bei den bisherigen Ausschüttungen wurden mir weder Steuern abgezogen noch der EK verringert.

https://seekingalpha.com/article/4099921-golar-lng-partners-…

Bin auf den Q2-Report gespannt, da sollte ja die "Strafzahlung von Petrobras wegen der vorzeitigen Vertragsbeendigung rein...

Bin versucht hier nochmal aufzustocken. Die hohe Ausschüttung scheint nun auf lange Sicht sicher...

Wie wird die in Deutschland eigentlich steuerlich behandelt? Bei den bisherigen Ausschüttungen wurden mir weder Steuern abgezogen noch der EK verringert.

ich glaube, jetzt haben sie alle preferreds emittiert:

(Gaslog, Dynagas, Teekay, Hoegh)Golar LNG Partners L.P. Announces Pricing of Series A Preferred Unit Offering

Golar LNG Partners LP (NASDAQ: GMLP) (the "Partnership") announced today that it has priced its public offering of 4,800,000 of its 8.75% Series A Cumulative Redeemable Preferred Units ("Series A Preferred Units"), representing limited partner interests, at $25.00 per unit.

Distributions will be payable on the Series A Preferred Units at a rate of 8.75% per annum of the stated liquidation preference of $25.00. The offering is expected to close on October 31, 2017. The Partnership has granted the underwriters a 30-day option to purchase up to an additional 720,000 Series A Preferred Units.

The Partnership intends to use the net proceeds from the offering and any exercise of the underwriters' option to purchase additional Series A Preferred Units for general partnership purposes, which may include, among other things, repaying indebtedness and funding working capital, capital expenditures or acquisitions.

Morgan Stanley and BofA Merrill Lynch are acting as the joint bookrunners in connection with the offering.

Antwort auf Beitrag Nr.: 56.032.011 von R-BgO am 26.10.17 13:22:20

heute endlich

auch ein paar von diesen eingesammelt

Antwort auf Beitrag Nr.: 56.114.684 von R-BgO am 06.11.17 20:45:44Wieviel Dividende zählt denn GMLP ? Hab im Netz nur was von 5 Cents pro Quartal gelesen. Das wären nur 1 % pro Jahr....

Antwort auf Beitrag Nr.: 56.497.820 von Sargon8 am 20.12.17 01:10:28Das ist die letzte Dividendenzahlung gewesen

27.10.17 0,5775 USD

Ordentliche Dividende

Quartal

27.10.17 0,5775 USD

Ordentliche Dividende

Quartal

Hallo hier nochmal etwas zur Zukunft der LNG Verschiffung wenn das Stimmt sieht es bis 2025 nicht schlecht....

https://deutsche-wirtschafts-nachrichten.de/2017/12/27/china…

https://deutsche-wirtschafts-nachrichten.de/2017/12/27/china…

Antwort auf Beitrag Nr.: 56.497.820 von Sargon8 am 20.12.17 01:10:28

die 5c

werden bei der Mutter Golar LNG bezahlt

Golar LNG Partners L.P. Secures New Long-term FSRU Contract

January 19, 2018 -

Golar LNG Partners LP (NASDAQ: GMLP), (the "Partnership" or "Golar Partners") announces that it has executed a 15-year charter with an energy and logistics company for the provision of an FSRU (floating storage and regasification unit) and related services in the Atlantic Basin.

The charter provides the Partnership with the flexibility to nominate either the Golar Spirit or the Golar Freeze to service the contract provided that the nominated FSRU satisfies certain technical specifications ahead of project start-up, which is expected in the fourth quarter of 2018.

The vessel is expected to remain in service for up to 15 years without drydock and will therefore undergo drydocking as well as some minor modifications prior to service commencement. The capital element of the charter rate will vary according to demand for regasification throughput but includes a cap and a floor and so is expected to generate annual operating income before depreciation and amortisation of between approximately $18 and $22 million.

The charter includes an option after 3 years for the charterer to terminate the contract and seek an alternative regasification solution, but only in the event that certain throughput targets have not been met. Additionally, Golar Partners will have a matching right to provide such alternative solution. The charter also includes a 5-year extension option.

Golar Partners CEO Graham Robjohns commented: "securing this contract demonstrates the underlying value of the Partnership's existing assets, adds significant term and revenue backlog whilst simultaneously reducing re-contracting risk. It also reflects the growing interest in smaller, cost competitive FSRUs that can facilitate the opening of niche markets previously considered uneconomic for LNG".

January 19, 2018 -

Golar LNG Partners LP (NASDAQ: GMLP), (the "Partnership" or "Golar Partners") announces that it has executed a 15-year charter with an energy and logistics company for the provision of an FSRU (floating storage and regasification unit) and related services in the Atlantic Basin.

The charter provides the Partnership with the flexibility to nominate either the Golar Spirit or the Golar Freeze to service the contract provided that the nominated FSRU satisfies certain technical specifications ahead of project start-up, which is expected in the fourth quarter of 2018.

The vessel is expected to remain in service for up to 15 years without drydock and will therefore undergo drydocking as well as some minor modifications prior to service commencement. The capital element of the charter rate will vary according to demand for regasification throughput but includes a cap and a floor and so is expected to generate annual operating income before depreciation and amortisation of between approximately $18 and $22 million.

The charter includes an option after 3 years for the charterer to terminate the contract and seek an alternative regasification solution, but only in the event that certain throughput targets have not been met. Additionally, Golar Partners will have a matching right to provide such alternative solution. The charter also includes a 5-year extension option.

Golar Partners CEO Graham Robjohns commented: "securing this contract demonstrates the underlying value of the Partnership's existing assets, adds significant term and revenue backlog whilst simultaneously reducing re-contracting risk. It also reflects the growing interest in smaller, cost competitive FSRUs that can facilitate the opening of niche markets previously considered uneconomic for LNG".

Das hört sich alles sehr gut an finde es gut wenn man die Schiffe langfristig verchartern kann das schafft Planungssicherheit....

Wie seht ihr die Dividendenrendite denkt ihr die Dividende ist sicher ? ich meine das die Firma auch in schweren Zeiten weiter Dividende zahlt

Wie seht ihr die Dividendenrendite denkt ihr die Dividende ist sicher ? ich meine das die Firma auch in schweren Zeiten weiter Dividende zahlt

wie definierst Du "schwere Zeiten" ?

solange die Vertragspartner zahlen,wird die Dividende natürlich auch bezahlt.

ist zwar emerging markets,aber das ist mittlerweile die ganze Welt

Schiffe sind mobil,können schwerlich besteuert werden und mit der Stromerzeugung deckt LNG ein Grundbedürnis ab.

zudem kann Golar LNG mit den FLNG Schiffen nicht aus dem Markt gedrängt werden,da es bis auf wenige Ausnahmen die kostengünstigsten Projekte ermöglicht.

im Grunde für Rohstoffprojekte ideal,weil nicht die ganze Infrastruktur auf einmal hingestellt werden muss.

mit dem ersten Schiff Cashflow sichern und dann erweitern

machen die Banken vermutlich auch gerne mit

zudem werden bei Golar LNG und Golar Partners vermutlich die Fremdkapitalkosten noch fallen,weil das Unternehmen in 3 Jahren völlig neu aufgestellt sein wird.

bleibt mehr Geld für Ausschüttungen oder Investitionen

solange die Vertragspartner zahlen,wird die Dividende natürlich auch bezahlt.

ist zwar emerging markets,aber das ist mittlerweile die ganze Welt

Schiffe sind mobil,können schwerlich besteuert werden und mit der Stromerzeugung deckt LNG ein Grundbedürnis ab.

zudem kann Golar LNG mit den FLNG Schiffen nicht aus dem Markt gedrängt werden,da es bis auf wenige Ausnahmen die kostengünstigsten Projekte ermöglicht.

im Grunde für Rohstoffprojekte ideal,weil nicht die ganze Infrastruktur auf einmal hingestellt werden muss.

mit dem ersten Schiff Cashflow sichern und dann erweitern

machen die Banken vermutlich auch gerne mit

zudem werden bei Golar LNG und Golar Partners vermutlich die Fremdkapitalkosten noch fallen,weil das Unternehmen in 3 Jahren völlig neu aufgestellt sein wird.

bleibt mehr Geld für Ausschüttungen oder Investitionen

Antwort auf Beitrag Nr.: 56.869.934 von bernieschach am 30.01.18 08:58:23

mit dem Rest Deiner Anmerkungen bin ich zudem d'accor!

Die aktuellen Kurse sind attraktiv, drum habe ich hier mal reingesehen!

Zitat von bernieschach: ist zwar emerging markets,aber das ist mittlerweile die ganze Welt

mit dem Rest Deiner Anmerkungen bin ich zudem d'accor!

Die aktuellen Kurse sind attraktiv, drum habe ich hier mal reingesehen!

Die Dividende klingt sehr interessant also fallen bei Golar LNG Partners keine Quellensteuer usw an ?

Antwort auf Beitrag Nr.: 56.992.046 von freddy1989 am 10.02.18 11:04:44Richtig, aufgrund des Firmensitzes (Marshallinseln) werden auf die Ausschüttungen keine Quellensteuern abgeführt und bisher (bei Consors) auch keine dt. Abgeltungssteuer. Muss man also sicherlich dann über die Steuererklärung melden. Aber hab keine Ahnung, ob das dann besteuert wird oder lediglich über den Progressionsvorbehalt zu einer höheren Besteuerung führt. Ich beziehe mich auf die Situation eines in Deutschland steuerpflichtigen Anlegers...

Die langfristigen Aussichten dieses Unternehmens und insbesondere des General Partners sind m.E. hervorragend, daher die Dividende gesichert und die momentanen Kurse ein freundliches "Einsteigen bitte!".

Je nach Marktsituation kann es natürlich aber immer noch tiefer gehen...

Die langfristigen Aussichten dieses Unternehmens und insbesondere des General Partners sind m.E. hervorragend, daher die Dividende gesichert und die momentanen Kurse ein freundliches "Einsteigen bitte!".

Je nach Marktsituation kann es natürlich aber immer noch tiefer gehen...

das ist dann von Broker zu Broker unterschiedlich

bei flatex wurde bisher die dt.Abgeltungssteuer immer abgezogen

bei flatex wurde bisher die dt.Abgeltungssteuer immer abgezogen

weiter aufgestockt

C-CORP 1099 TAX FILER – NO FORM K‑1

aus: http://www.golarlngpartners.com/

hier gab's ein Crash:

wegen Q1-Earnings drop:

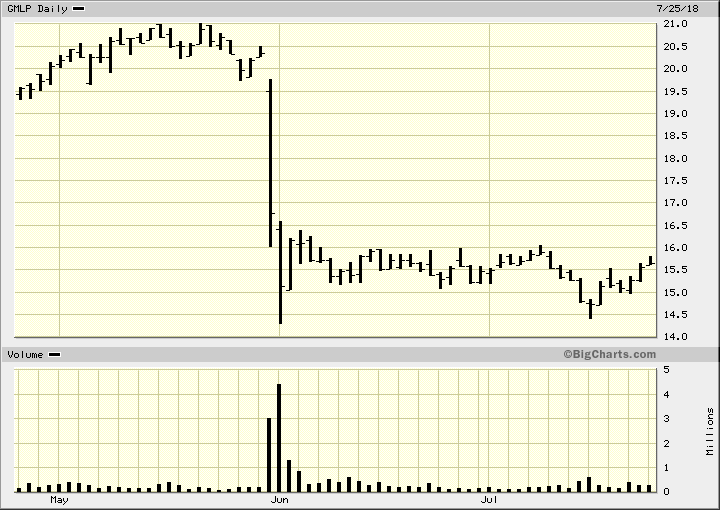

...With the release of its 2018 first quarter earnings report Golar LNG Partners LP (GMLP) dropped from over $20 down to $15. This pushed the yield up from about 11% to over 15%. Golar owns LNG transport ships and floating natural gas processing vessels. In that Q1 earnings, distributable cash flow was well short of the dividend. That scared investors and the stock dropped like a rock.

Golar management has been telegraphing for several quarters that there would be a cash flow shortfall in early 2018 as the company needed time to release some coming off lease vessels. New contracts and an acquisition will bring dividend coverage back above one times by the end of 2018.

Golar has said they plan to continue the current dividend through the two or three quarters of shortfall. This stock will be back in the $20’s when the distributable cash flow is again greater than the dividend...

aus: http://www.mydividends.de/news/golar-lng-partners-kuendigt-d…

aus: http://www.golarlngpartners.com/

hier gab's ein Crash:

wegen Q1-Earnings drop:

...With the release of its 2018 first quarter earnings report Golar LNG Partners LP (GMLP) dropped from over $20 down to $15. This pushed the yield up from about 11% to over 15%. Golar owns LNG transport ships and floating natural gas processing vessels. In that Q1 earnings, distributable cash flow was well short of the dividend. That scared investors and the stock dropped like a rock.

Golar management has been telegraphing for several quarters that there would be a cash flow shortfall in early 2018 as the company needed time to release some coming off lease vessels. New contracts and an acquisition will bring dividend coverage back above one times by the end of 2018.

Golar has said they plan to continue the current dividend through the two or three quarters of shortfall. This stock will be back in the $20’s when the distributable cash flow is again greater than the dividend...

aus: http://www.mydividends.de/news/golar-lng-partners-kuendigt-d…

Antwort auf Beitrag Nr.: 58.303.865 von faultcode am 26.07.18 01:37:54

=> gibt mittlerweile schon viele, global operierende LNG-Schiffe:

Europe will import more US natural gas, Trump and Juncker say after meeting

=> das mit dem "will" wird sich noch herausstellen:

• The United States and and European Union agreed to work towards facilitating more U.S. natural gas shipments to the Continent.

• EU Commission President Jean-Claude Juncker said the EU will build more terminals to import liquefied natural gas.

• LNG stocks and shares of U.S. natural gas producers popped after the announcement.

Trump + Juncker: LNG

daher hatte ich die Idee - und machte einer sehr kleine Rundschau:=> gibt mittlerweile schon viele, global operierende LNG-Schiffe:

Europe will import more US natural gas, Trump and Juncker say after meeting

=> das mit dem "will" wird sich noch herausstellen:

• The United States and and European Union agreed to work towards facilitating more U.S. natural gas shipments to the Continent.

• EU Commission President Jean-Claude Juncker said the EU will build more terminals to import liquefied natural gas.

• LNG stocks and shares of U.S. natural gas producers popped after the announcement.

Die prognostizierte LNG-Exportmenge aus den USA wird ständig nach oben revidiert.

da aus geologischen Gründen die Entfernungen weit sind,steigen auch die ton miles.

LNG ist eigentlich idiotensicher,solange in China das Kredit-Ponzisystem nicht zusammenbricht

Im Übrigen ist mir noch nie eine Aktie wie Golar Partners begegnet,bei der alle Welt fast ausschliesslich nur auf die Ausschüttung glotzt,ohne die strategische Ausrichtung zu beachten.

Es kann gut sein,dass sie in Zukunft einen grösseren Teil des Gewinns einbehalten müssen,um weiteres Wachstum zu ermöglichen.

gerade bei Öl und Gas können die Bewertungen sehr niedrig bleiben

trotzdem oder gerade deswegen eine gute Möglichkeit in deinem deflationären Umfeld Geld zu verdienen

da aus geologischen Gründen die Entfernungen weit sind,steigen auch die ton miles.

LNG ist eigentlich idiotensicher,solange in China das Kredit-Ponzisystem nicht zusammenbricht

Im Übrigen ist mir noch nie eine Aktie wie Golar Partners begegnet,bei der alle Welt fast ausschliesslich nur auf die Ausschüttung glotzt,ohne die strategische Ausrichtung zu beachten.

Es kann gut sein,dass sie in Zukunft einen grösseren Teil des Gewinns einbehalten müssen,um weiteres Wachstum zu ermöglichen.

gerade bei Öl und Gas können die Bewertungen sehr niedrig bleiben

trotzdem oder gerade deswegen eine gute Möglichkeit in deinem deflationären Umfeld Geld zu verdienen

naja, die letzten (gefühlt) Jahre hat GMLP immer über 100% des Gewinns ausgeschüttet. Das kann nicht ewig so weiter gehen. Das sollten auch die sehen, die nur auf die Ausschüttung "glotzen".

Die LNG Raten (160) sind jedenfalls gut angezogen.

Die LNG Raten (160) sind jedenfalls gut angezogen.

Zahlen gut, Divi stabil, der Kurs hupfte genau wie bei FRO im Vorfeld wild herum.

Antwort auf Beitrag Nr.: 58.520.493 von Mmmaulheld am 23.08.18 19:37:03

Antwort auf Beitrag Nr.: 58.524.204 von R-BgO am 24.08.18 09:37:03Das hört sich alles sehr gut an bleibt auch genug Gewinn über um die Dividenden weiterhin stabil zu bezahlen?

Ich meine wie ist es bei der Firma mit Krediten spielen die Banken da mit oder muss man sich sorgen machen das die Banken einmal nein sagen?

Ich meine wie ist es bei der Firma mit Krediten spielen die Banken da mit oder muss man sich sorgen machen das die Banken einmal nein sagen?

Antwort auf Beitrag Nr.: 58.537.628 von freddy1989 am 26.08.18 17:09:05

Hast Du #60 überhaupt nicht gelesen?

Divi ist sehr wohl in Gefahr; manche würden sagen, ein Cut ist sicher...

bei Golar Partners kann man derzeit mal wieder die Beliebigkeit von Unternehmensbewertung bestaunen.

welchen langfristigen Investor interessiert es schon,ob die Divi mal einige Monate 10-15% gekürzt wird?

Zudem ist bei vielen auch noch nicht angekommen,dass in einem Umfeld von Geldknappheit die preisgünstigste Alternative an Wert gewinnt.

Einzelwerte zu analysieren lohnt nur noch,um die Dummheit der Herde auszunutzen.

welchen langfristigen Investor interessiert es schon,ob die Divi mal einige Monate 10-15% gekürzt wird?

Zudem ist bei vielen auch noch nicht angekommen,dass in einem Umfeld von Geldknappheit die preisgünstigste Alternative an Wert gewinnt.

Einzelwerte zu analysieren lohnt nur noch,um die Dummheit der Herde auszunutzen.

Antwort auf Beitrag Nr.: 58.524.204 von R-BgO am 24.08.18 09:37:03

Golar LNG Partners LP Cash Distributions

Wed October 24, 2018 8:31 AM|GlobeNewswire|About: GMLP

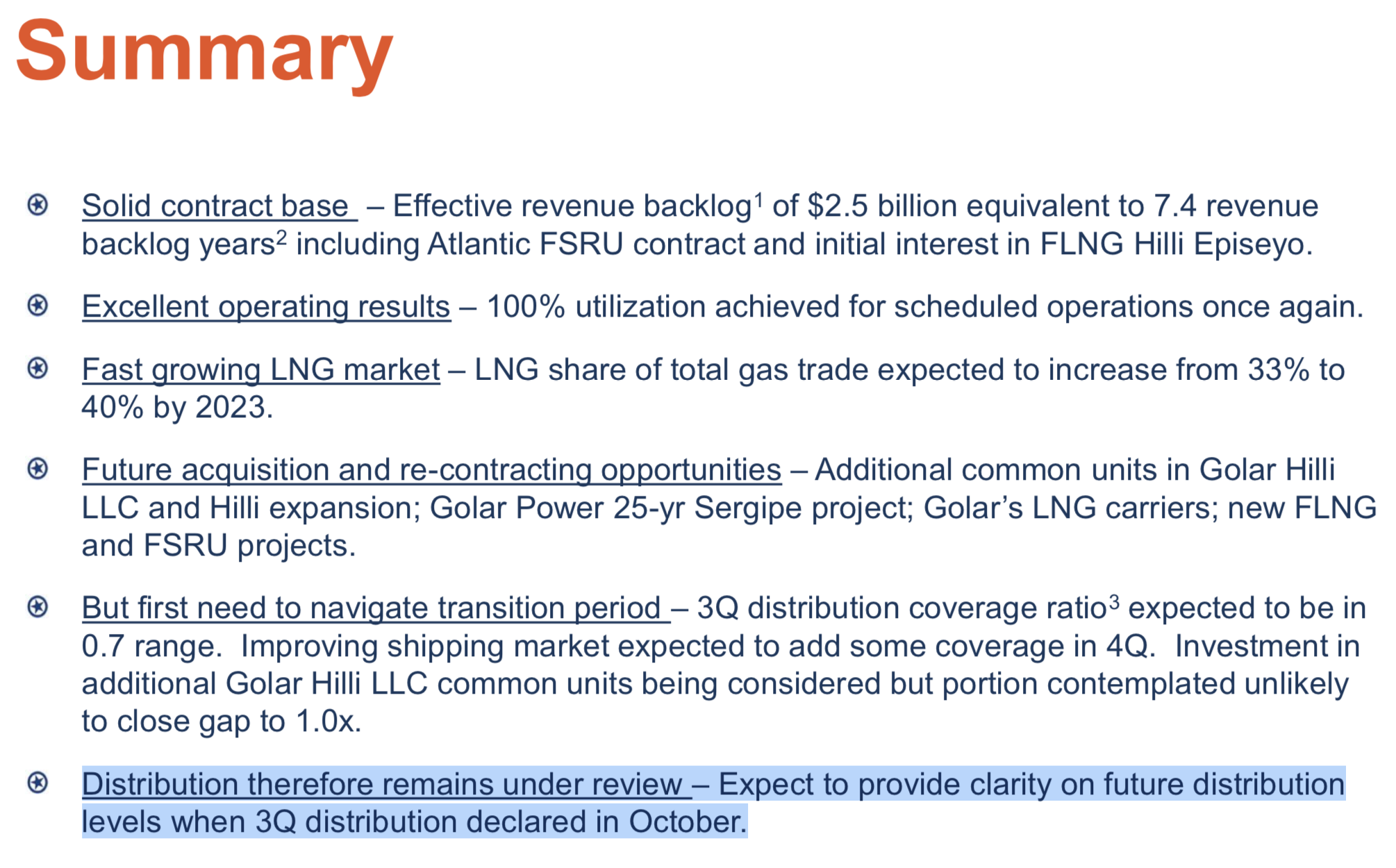

Management of Golar LNG Partners LP ("the Partnership" or "Golar Partners") (NASDAQ: GMLP) has completed its review of the Partnership's distribution capacity. After a thorough review the Partnership's board announced today that it has approved a quarterly cash distribution going forward of $0.4042 per common and general partner unit. Applicable in respect of the quarter ended September 30, 2018, this cash distribution will be paid on November 14, 2018 to all common and general partner unitholders of record as of the close of business on November 7, 2018.

It has been a target of the Board to set a distribution that is sustainable for the long-term.

Conservative assumptions have been applied to

-long-run rates achievable by the Partnership's three carriers currently exposed to the spot and short-term market. Similarly, a cautious stance has been taken on the

-contract status and future rates applicable in respect of the FSRU Golar Igloo.

-No future earnings are assumed in respect of the FSRU Golar Spirit or from the acquisition of additional common units in Golar Hilli LLC.

In light of these conservative assumptions and to maintain sustainable coverage levels for the foreseeable future, a distribution cut of 30% was therefore considered necessary.

Golar Partners is now well positioned financially. Distribution upside exists in the event that the shipping market outperforms assumptions or the Golar Spirit secures employment. Significant growth opportunities also exist including additional units in Golar Hilli LLC and the 25-year contracted FSRU Golar Nanook and associated Sergipe cash flows. These opportunities will however, to a large extent, be dependent on more effectively priced equity or realization of a flatter debt amortization profile.

A cash distribution of $0.546875 per Series A preferred unit (NASDAQ: GMLPP) for the period from August 15, 2018 through November 14, 2018 has also been declared. This will be payable on November 15, 2018 to all Series A preferred unitholders of record as at November 8, 2018.

Golar LNG Partners LP (GMLP)

Hamilton, Bermuda

October 24, 2018

wie zu erwarten war:

./.30%Golar LNG Partners LP Cash Distributions

Wed October 24, 2018 8:31 AM|GlobeNewswire|About: GMLP

Management of Golar LNG Partners LP ("the Partnership" or "Golar Partners") (NASDAQ: GMLP) has completed its review of the Partnership's distribution capacity. After a thorough review the Partnership's board announced today that it has approved a quarterly cash distribution going forward of $0.4042 per common and general partner unit. Applicable in respect of the quarter ended September 30, 2018, this cash distribution will be paid on November 14, 2018 to all common and general partner unitholders of record as of the close of business on November 7, 2018.

It has been a target of the Board to set a distribution that is sustainable for the long-term.

Conservative assumptions have been applied to

-long-run rates achievable by the Partnership's three carriers currently exposed to the spot and short-term market. Similarly, a cautious stance has been taken on the

-contract status and future rates applicable in respect of the FSRU Golar Igloo.

-No future earnings are assumed in respect of the FSRU Golar Spirit or from the acquisition of additional common units in Golar Hilli LLC.

In light of these conservative assumptions and to maintain sustainable coverage levels for the foreseeable future, a distribution cut of 30% was therefore considered necessary.

Golar Partners is now well positioned financially. Distribution upside exists in the event that the shipping market outperforms assumptions or the Golar Spirit secures employment. Significant growth opportunities also exist including additional units in Golar Hilli LLC and the 25-year contracted FSRU Golar Nanook and associated Sergipe cash flows. These opportunities will however, to a large extent, be dependent on more effectively priced equity or realization of a flatter debt amortization profile.

A cash distribution of $0.546875 per Series A preferred unit (NASDAQ: GMLPP) for the period from August 15, 2018 through November 14, 2018 has also been declared. This will be payable on November 15, 2018 to all Series A preferred unitholders of record as at November 8, 2018.

Golar LNG Partners LP (GMLP)

Hamilton, Bermuda

October 24, 2018

Warum kürzt man bei so guten (Q3) Zahlen die Dividende so drastisch - und vor allem dauerhaft?

Antwort auf Beitrag Nr.: 59.146.470 von Mmmaulheld am 06.11.18 10:12:10gutes Chance / Risiko bei den zurückgekommenen (gecrashten) Aktienpreisen (in der ganzen Schifffahrtsbranche)!

auch bei Dynagas, die geradezu auf "scrap value" notieren. Jeden Tag ein Stück günstiger. War das nicht der Werbespruch von REWE?

Antwort auf Beitrag Nr.: 59.092.109 von R-BgO am 30.10.18 10:44:10Golar LNG Partners L.P. Common Unit Repurchase Program

HAMILTON, BERMUDA-

Despite a positive initial response to the October 24, 2018 distribution cut, the Board of Golar LNG Partners L.P. (the "Partnership"; NASDAQ: GMLP) believes that the current unit price does not reflect the underlying value of the business, its prospects or the sustainability of the new distribution.

Given the current yield of approximately 13%, unit repurchases also represent an attractive rate of return on the Partnership's surplus cash. The Board has therefore authorized an increase to the common unit repurchase program announced in March 2018, from $25 million to $50 million. This facility will remain available until March 2020.

Under the terms of the repurchase program, the Partnership may repurchase common units from time to time, at the Partnership's discretion, on the open market or in privately negotiated transactions. Any repurchases are subject to market conditions, applicable legal requirements and other considerations. Common units will be purchased only during periods where the Partnership is not aware of material inside information that would likely affect a seller's decision to sell.

The Partnership is not obligated under the repurchase program to repurchase any specific dollar amount or number of common units, and the repurchase program may be modified, suspended or discontinued at any time. Any common units repurchased by the Partnership under the program will be cancelled.

HAMILTON, BERMUDA-

Despite a positive initial response to the October 24, 2018 distribution cut, the Board of Golar LNG Partners L.P. (the "Partnership"; NASDAQ: GMLP) believes that the current unit price does not reflect the underlying value of the business, its prospects or the sustainability of the new distribution.

Given the current yield of approximately 13%, unit repurchases also represent an attractive rate of return on the Partnership's surplus cash. The Board has therefore authorized an increase to the common unit repurchase program announced in March 2018, from $25 million to $50 million. This facility will remain available until March 2020.

Under the terms of the repurchase program, the Partnership may repurchase common units from time to time, at the Partnership's discretion, on the open market or in privately negotiated transactions. Any repurchases are subject to market conditions, applicable legal requirements and other considerations. Common units will be purchased only during periods where the Partnership is not aware of material inside information that would likely affect a seller's decision to sell.

The Partnership is not obligated under the repurchase program to repurchase any specific dollar amount or number of common units, and the repurchase program may be modified, suspended or discontinued at any time. Any common units repurchased by the Partnership under the program will be cancelled.

puh, heute wieder auf Tauchfahrt. Ich hoffe das Management hat noch Pulver trocken für weitere Rückkäufe, denn das wird hier wöchentlich noch billiger!

aufgestockt zu $10,79

Antwort auf Beitrag Nr.: 59.492.916 von R-BgO am 21.12.18 20:25:16mich juckt es auch!

Antwort auf Beitrag Nr.: 59.494.212 von Mmmaulheld am 21.12.18 23:17:43

Kommender Schiffsüberhang?

...???

Hast Du eine Theorie, warum die alle abrauschen?

Sippenhaft mit Öl?Kommender Schiffsüberhang?

...???

wer sich über den Aktienkurs Gedanken machen muss,hat sowieso kein Geld.

man kann es drehen und wenden,wie man will

billige,saubere Energie kann keine Blase sein

zu keinem Zeitpunkt,damit sind auch die Wertansätze in der Bilanz korrekt

vermutlich im Gegensatz zu 99,9% der sonstigen Aktien

Golar Partners kann mit den älteren FSRU Schiffen zu viel besseren Konditionen vermieten

das sind eher frontier markets,preissensitive Märkte

die hatten schon immer ein etwas höheres Risikoprofil

und,nachdem BP jetzt seinen Segen für die FLNG Schiffe gegeben hat,fühlt sich das noch besser an.

man kann es drehen und wenden,wie man will

billige,saubere Energie kann keine Blase sein

zu keinem Zeitpunkt,damit sind auch die Wertansätze in der Bilanz korrekt

vermutlich im Gegensatz zu 99,9% der sonstigen Aktien

Golar Partners kann mit den älteren FSRU Schiffen zu viel besseren Konditionen vermieten

das sind eher frontier markets,preissensitive Märkte

die hatten schon immer ein etwas höheres Risikoprofil

und,nachdem BP jetzt seinen Segen für die FLNG Schiffe gegeben hat,fühlt sich das noch besser an.

Seit 2 Jahren eine Richtung 🤯

hallo,

von der Auszahlung 0,4042 US-Dollar bleiben nach Steuern?

GMLP zahlen brutto für netto $? (wg. Marshall Islands -keine Steuern)

In D als Einkommensteuer oder Kap?

danke

von der Auszahlung 0,4042 US-Dollar bleiben nach Steuern?

GMLP zahlen brutto für netto $? (wg. Marshall Islands -keine Steuern)

In D als Einkommensteuer oder Kap?

danke

Antwort auf Beitrag Nr.: 60.970.396 von biviol1 am 07.07.19 10:57:55...hab mal eine kleine position aufgebaut

eigentlich tritt jetzt das Szenario ein,das ich erwartet habe.

billige LNG Preise,die nahe an die Cashkosten der Produzenten fallen

dadurch entsteht neue Nachfrage auf der Abnehmerseite,weil der Unterschied zu Kohle nicht mehr so gross ist

Golar Partners ist mit den älteren FSRU Schiffen für dieses Marktsegment gut aufgestellt

billige LNG Preise,die nahe an die Cashkosten der Produzenten fallen

dadurch entsteht neue Nachfrage auf der Abnehmerseite,weil der Unterschied zu Kohle nicht mehr so gross ist

Golar Partners ist mit den älteren FSRU Schiffen für dieses Marktsegment gut aufgestellt

ein artikel ohne pc

https://www.achgut.com/artikel/fluessiges_erdgas_die_usa_sta…

--

gestern div von 0,40$ erkärt, habe auch nachgekauft.

https://www.achgut.com/artikel/fluessiges_erdgas_die_usa_sta…

--

gestern div von 0,40$ erkärt, habe auch nachgekauft.

Hmmm, werde mal zupacken! Sieht so schlecht nicht aus. GMLP macht gerade einen Bullen-Bären-Kampf aus. Die Abwärtsbewegung ist vorbei. Zudem ist das Niveau einfach zu niedrig. Oversold!

Antwort auf Beitrag Nr.: 59.494.212 von Mmmaulheld am 21.12.18 23:17:43Hier juckt es mich auch in den Fingern man kann in der Schifffahrtsbranche richtig gutes Geld machen

https://www.wallstreet-online.de/nachricht/11887554-investor…

https://www.wallstreet-online.de/nachricht/11887554-investor…

wird ja immer billiger

Golar kann Golar Partners nicht einfach fallen lassen

die sind doch über das LNG schiffchen verbunden

aber irgendwie überzeugt den Markt das Konzept nicht

Golar kann Golar Partners nicht einfach fallen lassen

die sind doch über das LNG schiffchen verbunden

aber irgendwie überzeugt den Markt das Konzept nicht

und die älteren FSRU Schiffe kann man auch nicht reproduzieren,Neubauten sind teurer und können auch nicht viel mehr

ein grosser Unterschied zu LNG Tankern,da sind Neubauten deutlich besser

warum sollen sie die also nicht vermietet bekommen?

billiges LNG gibt es auch genug

der Aktienkurs erinnert mich an den Hindernislauf geistig verwirrter Menschen

ein grosser Unterschied zu LNG Tankern,da sind Neubauten deutlich besser

warum sollen sie die also nicht vermietet bekommen?

billiges LNG gibt es auch genug

der Aktienkurs erinnert mich an den Hindernislauf geistig verwirrter Menschen

Antwort auf Beitrag Nr.: 62.566.711 von bernieschach am 03.02.20 16:44:36

Zu dem Hindernislauf habe ich jetzt kein Bild im Kopf..🙄

Ich kann den Kursverlauf eher mit der Politik unserer Verbotspartei vergleichen, denen täglich ein neuer 🧀 einfällt.

Vielleicht hat bei GMLP der Markt Seadrill vor Augen? So lange ist das ja noch nicht her. Oder Int. Tankers?

Zitat von bernieschach: und die älteren FSRU Schiffe kann man auch nicht reproduzieren,Neubauten sind teurer und können auch nicht viel mehr

ein grosser Unterschied zu LNG Tankern,da sind Neubauten deutlich besser

warum sollen sie die also nicht vermietet bekommen?

billiges LNG gibt es auch genug

der Aktienkurs erinnert mich an den Hindernislauf geistig verwirrter Menschen

Zu dem Hindernislauf habe ich jetzt kein Bild im Kopf..🙄

Ich kann den Kursverlauf eher mit der Politik unserer Verbotspartei vergleichen, denen täglich ein neuer 🧀 einfällt.

Vielleicht hat bei GMLP der Markt Seadrill vor Augen? So lange ist das ja noch nicht her. Oder Int. Tankers?

wer auf Nummer sicher gehen will,muss warten,bis Perenco die Bohrungen in diesem Jahr durchführt.

Golar geht davon aus,dass die Ressource gross genug ist,damit das Schiff 25 Jahre dort produzieren kann.

dann können sie alle anderen Schiffe verschrotten,und die Aktie wäre nicht teuer

Golar geht davon aus,dass die Ressource gross genug ist,damit das Schiff 25 Jahre dort produzieren kann.

dann können sie alle anderen Schiffe verschrotten,und die Aktie wäre nicht teuer

Bondholder meeting 21.04.

Summons GOLP02 and GOLP03 1 April 2020