Marvel Gold ehemals Graphex Mining - After Tax NPV 480 Mio AUD bei 16 Mio Börsenwert - world leadin (Seite 203)

eröffnet am 20.09.18 11:00:04 von

neuester Beitrag 28.02.23 09:04:40 von

neuester Beitrag 28.02.23 09:04:40 von

Beiträge: 3.976

ID: 1.288.876

ID: 1.288.876

Aufrufe heute: 0

Gesamt: 207.236

Gesamt: 207.236

Aktive User: 0

ISIN: AU0000102154 · WKN: A2QB8V · Symbol: GR2

0,0060

EUR

0,00 %

0,0000 EUR

Letzter Kurs 30.04.24 Tradegate

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7750 | +17,42 | |

| 0,7200 | +12,50 | |

| 0,8947 | +11,85 | |

| 0,5700 | +11,76 | |

| 205,00 | +10,81 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,3400 | -10,07 | |

| 183,20 | -19,30 | |

| 1,1367 | -22,67 | |

| 12,000 | -25,00 | |

| 46,06 | -98,04 |

Beitrag zu dieser Diskussion schreiben

Antwort auf Beitrag Nr.: 61.519.331 von Chancen1904 am 19.09.19 11:11:23meine Aussage bezog sich eindeutig auf die von WKT zur Verfügung gestellten Angaben.

Habe ich eine negative Marge auf mein Produkt, dann generiere ich Verluste. Verkaufe ich von dem Produkt noch mehr, sind die Verluste größer. Ganz unabhängig ob ich statt 200USD dann nur noch 170USD pro Tonne Verlust einfahre....

bei dieser völlig willkürlichen "Rechnung" hast du natürlich Recht. Aber ich habe ohnehin nicht behauptet, dass diese Aussage überhaupt nicht zutrifft, sondern dass die Pauschalisierung falsch ist. Es gibt sehr wohl auch im Rohstoffbereich Skaleneffekte. Und hätte SYR die angestrebten Produktionskosten (C1) von <U$330 bereits erreicht, stünden sie ganz anders da. Dann sprächen wir nämlich beispielsweise für Q2 nicht mehr über Cashoutflow, sondern (moderaten) Cashinflow. Versteht sich hoffentlich von selbst, dass Skaleneffekte nur dann eine Wirkung entfalten können, wenn der Verkaufspreis nicht im selben Umfang nachgibt. Da liegt eben auch das Hauptproblem von SYR - dass sie sich ihren Markt selbst zerstör(t)en. Daher trifft die Aussage des HC-Users aktuell für SYR zu, ist aber nicht allgemein gültig. Nur ein Gegenbeispiel: GXY.AX

Q4/18: Produktion knapp 34k t, Cashkosten $560/t

Q1/19: Produktion knapp 42k t, Cashkosten $453/t

Q2/19: Produktion über 56k t, Cashkosten $337/t

bei den aktuell niedrigen Verkaufspreisen für Spodumene wäre der op. Cashflow in Q4 klar negativ, aber in Q2 positiv. Skalenffekte wirken!

Habe ich eine negative Marge auf mein Produkt, dann generiere ich Verluste. Verkaufe ich von dem Produkt noch mehr, sind die Verluste größer. Ganz unabhängig ob ich statt 200USD dann nur noch 170USD pro Tonne Verlust einfahre....

bei dieser völlig willkürlichen "Rechnung" hast du natürlich Recht. Aber ich habe ohnehin nicht behauptet, dass diese Aussage überhaupt nicht zutrifft, sondern dass die Pauschalisierung falsch ist. Es gibt sehr wohl auch im Rohstoffbereich Skaleneffekte. Und hätte SYR die angestrebten Produktionskosten (C1) von <U$330 bereits erreicht, stünden sie ganz anders da. Dann sprächen wir nämlich beispielsweise für Q2 nicht mehr über Cashoutflow, sondern (moderaten) Cashinflow. Versteht sich hoffentlich von selbst, dass Skaleneffekte nur dann eine Wirkung entfalten können, wenn der Verkaufspreis nicht im selben Umfang nachgibt. Da liegt eben auch das Hauptproblem von SYR - dass sie sich ihren Markt selbst zerstör(t)en. Daher trifft die Aussage des HC-Users aktuell für SYR zu, ist aber nicht allgemein gültig. Nur ein Gegenbeispiel: GXY.AX

Q4/18: Produktion knapp 34k t, Cashkosten $560/t

Q1/19: Produktion knapp 42k t, Cashkosten $453/t

Q2/19: Produktion über 56k t, Cashkosten $337/t

bei den aktuell niedrigen Verkaufspreisen für Spodumene wäre der op. Cashflow in Q4 klar negativ, aber in Q2 positiv. Skalenffekte wirken!

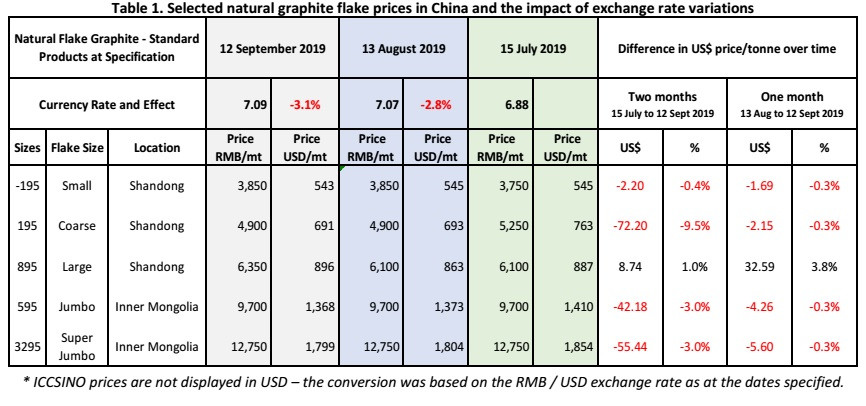

Coarse steht in der Tabelle wohl für Medium

Antwort auf Beitrag Nr.: 61.519.250 von IllePille am 19.09.19 11:02:48Wenn man sich die Preise für Jumbos und Super Jumbos anschaut, sind die in Yuan sogar gleich geblieben.

Antwort auf Beitrag Nr.: 61.519.250 von IllePille am 19.09.19 11:02:48Ja das ist richtig. Wir zählen aber alles unter large zu fines.... Aufpassen müssen wir da beim wording.

Und @illepille

EoS wird bei solchen Operationen offenbar föllig überschätzt und das Urteil, was du als zu pauschal kritisierst und ihm die Kompetenz in Folge absprichst trifft den Nagel imho auf den Kopf. Natürlich hast du geringfügig skaleneffekte. Aber auch nicht jede Operation ist sensibel für skeleneffekte. Eine Mining operation halte ich nicht wirklich für sensibel. Aber das kann man jetzt breit ausdiskutieren und hängt an zu vielen Rahmenbedingungen.... Fakt ist naturlich: Habe ich eine negative Marge auf mein Produkt, dann generiere ich Verluste. Verkaufe ich von dem Produkt noch mehr, sind die Verluste größer. Ganz unabhängig ob ich statt 200USD dann nur noch 170USD pro Tonne Verlust einfahre....

Und @illepille

EoS wird bei solchen Operationen offenbar föllig überschätzt und das Urteil, was du als zu pauschal kritisierst und ihm die Kompetenz in Folge absprichst trifft den Nagel imho auf den Kopf. Natürlich hast du geringfügig skaleneffekte. Aber auch nicht jede Operation ist sensibel für skeleneffekte. Eine Mining operation halte ich nicht wirklich für sensibel. Aber das kann man jetzt breit ausdiskutieren und hängt an zu vielen Rahmenbedingungen.... Fakt ist naturlich: Habe ich eine negative Marge auf mein Produkt, dann generiere ich Verluste. Verkaufe ich von dem Produkt noch mehr, sind die Verluste größer. Ganz unabhängig ob ich statt 200USD dann nur noch 170USD pro Tonne Verlust einfahre....

Antwort auf Beitrag Nr.: 61.518.383 von Reiners am 19.09.19 09:49:51"Coarse" zwei Monate -9,5% vs. Fines -0,4%

Trading Spotlight

Antwort auf Beitrag Nr.: 61.517.303 von IllePille am 19.09.19 07:53:17genau das Gegenteil von dem, was WKT jüngst berichtet hat. Demzufolge musste "Coarse" mit Abstand die grössten Preisrückgänge hinnehmen,

Ich weiss nicht wovon du sprichst.

Wenn du in die WKT Tabelle schaust, ist der Rückgang bei den großen Flocken nur marginal.

Ich weiss nicht wovon du sprichst.

Wenn du in die WKT Tabelle schaust, ist der Rückgang bei den großen Flocken nur marginal.

Antwort auf Beitrag Nr.: 61.517.084 von Reiners am 19.09.19 06:52:07Investors were asking questions and pushing management for an increase in production... Management could be blamed for lots of things but for this, investors should also be questioned themselves. They should be asking at least some of the right questions.

jetzt sollen die Investoren schuld sein an einer verfehlten Outputstrategie? Lächerlich. Von einem guten Management kann man erwarten, dass sie sich nicht an etwaigen unsinnigen Forderungen irgendwelcher Investoren, sondern am Markt orientieren. Fakt ist, sie haben viel zu spät reagiert auf eine Marktentwicklung, die deutlich hinter den (wie so oft) optimistischen Prognosen zurück geblieben ist. Was sich die Investoren allerdings fragen sollten: warum sie diesen Leuten immer wieder beträchtliche Summen zu Mondpreisen zukommen liessen, selbst dann noch, als die grundlegenden Probleme ganz offensichtlich zu Tage traten.

If you are selling for a loss, increasing sales will only increase your losses.

so ein - falsches - Pauschalurteil wirft die Frage auf, wie kompetent der Schreiber tatsächlich ist. Stichwort Skaleneffekte.

jetzt sollen die Investoren schuld sein an einer verfehlten Outputstrategie? Lächerlich. Von einem guten Management kann man erwarten, dass sie sich nicht an etwaigen unsinnigen Forderungen irgendwelcher Investoren, sondern am Markt orientieren. Fakt ist, sie haben viel zu spät reagiert auf eine Marktentwicklung, die deutlich hinter den (wie so oft) optimistischen Prognosen zurück geblieben ist. Was sich die Investoren allerdings fragen sollten: warum sie diesen Leuten immer wieder beträchtliche Summen zu Mondpreisen zukommen liessen, selbst dann noch, als die grundlegenden Probleme ganz offensichtlich zu Tage traten.

If you are selling for a loss, increasing sales will only increase your losses.

so ein - falsches - Pauschalurteil wirft die Frage auf, wie kompetent der Schreiber tatsächlich ist. Stichwort Skaleneffekte.

Antwort auf Beitrag Nr.: 61.517.063 von Reiners am 19.09.19 06:42:47Coarse flake graphite pricing remains strong.

genau das Gegenteil von dem, was WKT jüngst berichtet hat. Demzufolge musste "Coarse" mit Abstand die grössten Preisrückgänge hinnehmen, obwohl SYR den Markt bekanntlich ganz überwiegend mit "Fines" geflutet hat (deren Preis lt. WKT überraschenderweise am stabilsten war).

genau das Gegenteil von dem, was WKT jüngst berichtet hat. Demzufolge musste "Coarse" mit Abstand die grössten Preisrückgänge hinnehmen, obwohl SYR den Markt bekanntlich ganz überwiegend mit "Fines" geflutet hat (deren Preis lt. WKT überraschenderweise am stabilsten war).

I have worked for Syrah for more than 6 years and early last year (2018) I have resigned and left the company. From just a scratch – a resource in the ground- and transition to a giant graphite producer, I was there as a part of a good team. Spherical graphite, recarburizers even graphite electrodes, aluminium anodes and lots of other ideas were developed by us, and we spent a considerable amount of time to develop those markets. Old good days, water under the bridge. I was a bad performer, some of us were redundant for the new management, and old team left the company.

Now, this giant has been knocked down, but this didn’t happen in a day. I must say I think I am emotionally attached to Syrah and really hoped to see it, as the world biggest graphite producer with profit and positive cash flow. I feel deeply sorry when I see it like this. When I have resigned, I have been seriously warned – maybe kind of being threatened – not to tell anything to anyone about what I know or what was happening in Syrah, especially related the issues or actions of management that I have been strongly opposing. I still can’t tell most of this, but I feel I need to tell something.

But I am not a pessimist, I can say that giant still could be saved. You need the right strategies based on the realities of today. A decrease in production; to be honest a bit late but not a bad move. Then it is also important to diagnose the problem, and in order to do this what had happened should be known and lessons should be derived.

Blaming the management is the easiest way, probably I will do or am doing the same thing. But on the other hand, maybe also investors should ask themselves that; “Did they ask the right questions to the management?” Investors were asking questions and pushing management for an increase in production, signing more sales contracts with considerable sizes/quantities. Later average sales prices and costs were announced. It was obvious that Syrah selling products for loss, yet still everybody was chasing for increasing production, asking when they will reach production targets and more sales contract. But it was obvious that demand wasn’t good enough to absorb additional supply increase. If you are selling for a loss, increasing sales will only increase your losses. Management could be blamed for lots of things but for this, investors should also be questioned themselves. They should be asking at least some of the right questions.

Increase in production wouldn’t have been that problematic, because we really worked hard to develop a marketing strategy and solid business for Syrah. As this was a couple of time told to the public, I think I can say this, as you probably remember, initial strategy was having BAM plant up and running almost just after the flotation plant started production. BAM plant will be ramped up parallel to flotation plant ramp-up. This was a known business strategy that has been told to the market several times under the former management. BAM plant would be pulling the majority of the production of the flotation plant. And this wasn’t just a fancy announcement or story we were telling; it was a solid business case that we have developed over the years and spent years working on it. As you know Syrah used to have pilot plants, for concentrate and spherical graphite production. Those pilot plants weren’t for showing off, they well served for what they were built for. As a team, we did everything to make “Syrah dream” a reality, and it was a reality till some strategic decisions have been made, but when that was done, “The old team” was either just an ordinary employee with no words or has been told they were redundant or forced to leave. Can you imagine that the key engineer who developed your spherical graphite and vanadium pentoxide process and was the main party in preparation of the vanadium and spherical graphite scoping study as well as technical development of the project, and on top of this he was the key personnel in Qualification process of spherical graphite, has been told that he was redundant and fired.

There are lots of other things I want to write. I hope this would be the start of a storm and I can continue to write and tell the real Syrah story.

To be continued ………..

Now, this giant has been knocked down, but this didn’t happen in a day. I must say I think I am emotionally attached to Syrah and really hoped to see it, as the world biggest graphite producer with profit and positive cash flow. I feel deeply sorry when I see it like this. When I have resigned, I have been seriously warned – maybe kind of being threatened – not to tell anything to anyone about what I know or what was happening in Syrah, especially related the issues or actions of management that I have been strongly opposing. I still can’t tell most of this, but I feel I need to tell something.

But I am not a pessimist, I can say that giant still could be saved. You need the right strategies based on the realities of today. A decrease in production; to be honest a bit late but not a bad move. Then it is also important to diagnose the problem, and in order to do this what had happened should be known and lessons should be derived.

Blaming the management is the easiest way, probably I will do or am doing the same thing. But on the other hand, maybe also investors should ask themselves that; “Did they ask the right questions to the management?” Investors were asking questions and pushing management for an increase in production, signing more sales contracts with considerable sizes/quantities. Later average sales prices and costs were announced. It was obvious that Syrah selling products for loss, yet still everybody was chasing for increasing production, asking when they will reach production targets and more sales contract. But it was obvious that demand wasn’t good enough to absorb additional supply increase. If you are selling for a loss, increasing sales will only increase your losses. Management could be blamed for lots of things but for this, investors should also be questioned themselves. They should be asking at least some of the right questions.

Increase in production wouldn’t have been that problematic, because we really worked hard to develop a marketing strategy and solid business for Syrah. As this was a couple of time told to the public, I think I can say this, as you probably remember, initial strategy was having BAM plant up and running almost just after the flotation plant started production. BAM plant will be ramped up parallel to flotation plant ramp-up. This was a known business strategy that has been told to the market several times under the former management. BAM plant would be pulling the majority of the production of the flotation plant. And this wasn’t just a fancy announcement or story we were telling; it was a solid business case that we have developed over the years and spent years working on it. As you know Syrah used to have pilot plants, for concentrate and spherical graphite production. Those pilot plants weren’t for showing off, they well served for what they were built for. As a team, we did everything to make “Syrah dream” a reality, and it was a reality till some strategic decisions have been made, but when that was done, “The old team” was either just an ordinary employee with no words or has been told they were redundant or forced to leave. Can you imagine that the key engineer who developed your spherical graphite and vanadium pentoxide process and was the main party in preparation of the vanadium and spherical graphite scoping study as well as technical development of the project, and on top of this he was the key personnel in Qualification process of spherical graphite, has been told that he was redundant and fired.

There are lots of other things I want to write. I hope this would be the start of a storm and I can continue to write and tell the real Syrah story.

To be continued ………..

Following Syrah Resources recent announcement of a production downgrade and its related commentary on the state of the graphite market, Bridge Street Capital and Patersons Securities have released new research notes:

Bridge Street Capital - SYR/Balama fails, proving a large volume fine flake graphite strategy is flawed. Coarse flake graphite pricing remains strong.

https://graphexmininglimited.emlnk1.com/lt.php?s=2c8f9a9031e…

Patersons Securities - Market read-through from Syrah update

https://graphexmininglimited.emlnk1.com/lt.php?s=2c8f9a9031e…

Response from Managing Director Phil Hoskins:

"The Bridge Street and Patersons research notes provide two differing, some would argue divergent views on the state of the natural graphite market. While we strongly disagree with the underlying assumption made by the Patersons note as it pertains to pricing for large flake (expandable) graphite, we nonetheless provide both pieces of research without fear or favour.

Graphex was the first ASX-listed company to identify and articulate the compelling opportunity for potential graphite producers in the Chinese expandable graphite market, we remain committed and unwavering in the pursuit of the strategy we identified a long time ago.

...........

Vor allem den Bridge Street Report würde ich an eurer Stelle mal lesen.

Bridge Street Capital - SYR/Balama fails, proving a large volume fine flake graphite strategy is flawed. Coarse flake graphite pricing remains strong.

https://graphexmininglimited.emlnk1.com/lt.php?s=2c8f9a9031e…

Patersons Securities - Market read-through from Syrah update

https://graphexmininglimited.emlnk1.com/lt.php?s=2c8f9a9031e…

Response from Managing Director Phil Hoskins:

"The Bridge Street and Patersons research notes provide two differing, some would argue divergent views on the state of the natural graphite market. While we strongly disagree with the underlying assumption made by the Patersons note as it pertains to pricing for large flake (expandable) graphite, we nonetheless provide both pieces of research without fear or favour.

Graphex was the first ASX-listed company to identify and articulate the compelling opportunity for potential graphite producers in the Chinese expandable graphite market, we remain committed and unwavering in the pursuit of the strategy we identified a long time ago.

...........

Vor allem den Bridge Street Report würde ich an eurer Stelle mal lesen.