Gran Colombia Gold (Seite 390)

eröffnet am 02.11.10 14:47:21 von

neuester Beitrag 02.05.24 20:38:24 von

neuester Beitrag 02.05.24 20:38:24 von

Beiträge: 8.334

ID: 1.160.906

ID: 1.160.906

Aufrufe heute: 9

Gesamt: 703.512

Gesamt: 703.512

Aktive User: 0

ISIN: CA04040Y1097 · WKN: A3DTTG · Symbol: ZP1

3,8680

EUR

+1,52 %

+0,0580 EUR

Letzter Kurs 06.05.24 Tradegate

Neuigkeiten

01.08.23 · EQS Group AG |

26.07.23 · wO Chartvergleich |

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,5500 | +17,02 | |

| 2,0500 | +13,89 | |

| 35,60 | +8,50 | |

| 1,1500 | +8,49 | |

| 1,3000 | +8,33 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7340 | -12,62 | |

| 0,6000 | -18,37 | |

| 0,6601 | -26,22 | |

| 1,1600 | -46,79 | |

| 46,67 | -97,98 |

Beitrag zu dieser Diskussion schreiben

Antwort auf Beitrag Nr.: 60.828.446 von German2 am 18.06.19 07:48:20Also 900 USD all sustaining sollten auf jeden Fall machbar sein. Dort die doppelt so hohen Grades würden sich die Kosten nahezu halbieren, berücksichtigen muss man aber das das zukünftige Gestein weiter unten rausgeholt wird und die Kosten dadurch dezent steigen werden.

Wie du richtig sagst, kann man also komplett mit einem 50% Rückgang nicht 1:1 rechnen.

Sehr gute Zahlen heute mal wieder - trotz Minenunfall. Juni soll wieder komplett normal laufen.

Die Erhöhung des Jahresziels kommt dann nach den Halbjahres-Produktionszahlen und positiv ist auch das GCM bislang die maximale Anzahl an ausstehenden Warrants zurückgekauft hat.

Mit dem heutigen Goldpreisanstieg könnte das wieder ein super Tag werden.

Wie du richtig sagst, kann man also komplett mit einem 50% Rückgang nicht 1:1 rechnen.

Sehr gute Zahlen heute mal wieder - trotz Minenunfall. Juni soll wieder komplett normal laufen.

Die Erhöhung des Jahresziels kommt dann nach den Halbjahres-Produktionszahlen und positiv ist auch das GCM bislang die maximale Anzahl an ausstehenden Warrants zurückgekauft hat.

Mit dem heutigen Goldpreisanstieg könnte das wieder ein super Tag werden.

Gran Colombia Gold Provides May 2019 Gold Production Update

TORONTO, June 18, 2019 (GLOBE NEWSWIRE) -- Gran Colombia Gold Corp. (TSX: GCM; OTCQX: TPRFF) announced today that it produced a total of 18,528 ounces of gold in May bringing the total for the first five months of 2019 to 99,601 ounces, up 14% over the first five months of 2018. Gran Colombia’s trailing 12 months’ total gold production at the end of May 2019 of 230,136 ounces is up almost 6% over 2018’s annual production and remains above the top end of the Company’s guidance range for 2019 of between 210,000 and 225,000 ounces.

Lombardo Paredes, Chief Executive Officer of Gran Colombia, commenting on the Company’s latest production results, said, “We have gotten off to a stronger start in 2019 than in other years, setting us up to potentially exceed production guidance for the year. We will continue to monitor our operating performance and reassess our guidance when we report our mid-year production results. With our solid performance to-date and higher spot gold prices, we have the opportunity to use a portion of our free cash flow toward the recently announced NCIBs and have so far have been actively using our daily limit to purchase warrants for cancellation.”

The Segovia Operations continued to exceed expectations in May with gold production of 16,363 ounces bringing the total for the first five months of 2019 to 89,120 ounces, up 15% over the first five months of 2018. Gran Colombia processed an average of 1,144 tonnes per day (“tpd”) in May at its Segovia Operations, up slightly compared to the first four months of the year, with an average head grade of 16 g/t. In May, the Company began to see an expected increase in material from the small contract miners operating within its title, which grew from an average of 191 tpd in the first four months of 2019 to 267 tpd in May with an average grade of approximately 7 g/t. This helped to offset the impact on productivity in May at the Company’s mines following the accident at the Providencia mine which resulted in a temporary decline in tonnes processed from the Company mines in the month. The resultant shift in the mix of material processed in May with a greater contribution coming from the lower grade small contract miners resulted in the lower overall average grade reported for the month for the Segovia Operations. The Company expects to see performance at its own mines return to normal in June and continuation of the increased level of material sourced from the small contract miners going forward. Segovia’s trailing 12 months’ total gold production at the end of May 2019 stood at 204,713 ounces, up 6% over 2018’s annual production.

At the Marmato Operations, May’s gold production of 2,165 ounces brings total production for the first five months of 2019 to 10,481 ounces, up 5% over the first five months of 2018 driven by an increase in tonnes processed this year, and its trailing 12 months’ total gold production at the end of May 2019 to 25,423 ounces, up 2% over 2018’s annual production.

About Gran Colombia Gold Corp.

Gran Colombia is a Canadian-based mid-tier gold producer with its primary focus in Colombia where it is currently the largest underground gold and silver producer with several mines in operation at its Segovia and Marmato Operations. Gran Colombia is continuing to focus on exploration, expansion and modernization activities at its high-grade Segovia Operations.

Additional information on Gran Colombia can be found on its website at www.grancolombiagold.com and by reviewing its profile on SEDAR at www.sedar.com.

Cautionary Statement on Forward-Looking Information:

This news release contains "forward-looking information", which may include, but is not limited to, statements with respect to production guidance and anticipated business plans or strategies. Often, but not always, forward-looking statements can be identified by the use of words such as "plans", "expects", "is expected", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates", or "believes" or variations (including negative variations) of such words and phrases, or state that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Gran Colombia to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Factors that could cause actual results to differ materially from those anticipated in these forward-looking statements are described under the caption "Risk Factors" in the Company's Annual Information Form dated as of March 27, 2019 which is available for view on SEDAR at www.sedar.com. Forward-looking statements contained herein are made as of the date of this press release and Gran Colombia disclaims, other than as required by law, any obligation to update any forward-looking statements whether as a result of new information, results, future events, circumstances, or if management's estimates or opinions should change, or otherwise. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, the reader is cautioned not to place undue reliance on forward-looking statements.

For Further Information, Contact:

Mike Davies

Chief Financial Officer

(416) 360-4653

investorrelations@grancolombiagold.com

Gran Colombia Gold logo.jpg

Source: Gran Colombia Gold

TORONTO, June 18, 2019 (GLOBE NEWSWIRE) -- Gran Colombia Gold Corp. (TSX: GCM; OTCQX: TPRFF) announced today that it produced a total of 18,528 ounces of gold in May bringing the total for the first five months of 2019 to 99,601 ounces, up 14% over the first five months of 2018. Gran Colombia’s trailing 12 months’ total gold production at the end of May 2019 of 230,136 ounces is up almost 6% over 2018’s annual production and remains above the top end of the Company’s guidance range for 2019 of between 210,000 and 225,000 ounces.

Lombardo Paredes, Chief Executive Officer of Gran Colombia, commenting on the Company’s latest production results, said, “We have gotten off to a stronger start in 2019 than in other years, setting us up to potentially exceed production guidance for the year. We will continue to monitor our operating performance and reassess our guidance when we report our mid-year production results. With our solid performance to-date and higher spot gold prices, we have the opportunity to use a portion of our free cash flow toward the recently announced NCIBs and have so far have been actively using our daily limit to purchase warrants for cancellation.”

The Segovia Operations continued to exceed expectations in May with gold production of 16,363 ounces bringing the total for the first five months of 2019 to 89,120 ounces, up 15% over the first five months of 2018. Gran Colombia processed an average of 1,144 tonnes per day (“tpd”) in May at its Segovia Operations, up slightly compared to the first four months of the year, with an average head grade of 16 g/t. In May, the Company began to see an expected increase in material from the small contract miners operating within its title, which grew from an average of 191 tpd in the first four months of 2019 to 267 tpd in May with an average grade of approximately 7 g/t. This helped to offset the impact on productivity in May at the Company’s mines following the accident at the Providencia mine which resulted in a temporary decline in tonnes processed from the Company mines in the month. The resultant shift in the mix of material processed in May with a greater contribution coming from the lower grade small contract miners resulted in the lower overall average grade reported for the month for the Segovia Operations. The Company expects to see performance at its own mines return to normal in June and continuation of the increased level of material sourced from the small contract miners going forward. Segovia’s trailing 12 months’ total gold production at the end of May 2019 stood at 204,713 ounces, up 6% over 2018’s annual production.

At the Marmato Operations, May’s gold production of 2,165 ounces brings total production for the first five months of 2019 to 10,481 ounces, up 5% over the first five months of 2018 driven by an increase in tonnes processed this year, and its trailing 12 months’ total gold production at the end of May 2019 to 25,423 ounces, up 2% over 2018’s annual production.

About Gran Colombia Gold Corp.

Gran Colombia is a Canadian-based mid-tier gold producer with its primary focus in Colombia where it is currently the largest underground gold and silver producer with several mines in operation at its Segovia and Marmato Operations. Gran Colombia is continuing to focus on exploration, expansion and modernization activities at its high-grade Segovia Operations.

Additional information on Gran Colombia can be found on its website at www.grancolombiagold.com and by reviewing its profile on SEDAR at www.sedar.com.

Cautionary Statement on Forward-Looking Information:

This news release contains "forward-looking information", which may include, but is not limited to, statements with respect to production guidance and anticipated business plans or strategies. Often, but not always, forward-looking statements can be identified by the use of words such as "plans", "expects", "is expected", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates", or "believes" or variations (including negative variations) of such words and phrases, or state that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Gran Colombia to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Factors that could cause actual results to differ materially from those anticipated in these forward-looking statements are described under the caption "Risk Factors" in the Company's Annual Information Form dated as of March 27, 2019 which is available for view on SEDAR at www.sedar.com. Forward-looking statements contained herein are made as of the date of this press release and Gran Colombia disclaims, other than as required by law, any obligation to update any forward-looking statements whether as a result of new information, results, future events, circumstances, or if management's estimates or opinions should change, or otherwise. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, the reader is cautioned not to place undue reliance on forward-looking statements.

For Further Information, Contact:

Mike Davies

Chief Financial Officer

(416) 360-4653

investorrelations@grancolombiagold.com

Gran Colombia Gold logo.jpg

Source: Gran Colombia Gold

Antwort auf Beitrag Nr.: 60.828.011 von Popeye82 am 18.06.19 02:07:55also an Marmato und 600$ AISC glaube ich persönlich nicht ...aber so um die 900$ AISC sind da eventuell drin ... das man bei marmato jetzt auf Underground-Mining setzt kommt nicht daher das dies ursprünglich so gewollt war..es ist eher Plan B nacvh dem man die grosse-open-Pit Variante nicht durchbekommen hat wegern der illegalen miner und Proteste uswusw... man setzt daher auf Underground, da muss man sich wenigstens mit den Leute nicht rumärgern... viell eine werise Entscheidung...

warten wir die nächsten news ab ... jUNI/Juli erstmal Produktionszahlen Mai und eventuell news zu der Erweiterung der Anlage auf 1500 t/Tag Durchsatz ... wie du schon richtig feststelltest wird 2020/21 herum die Capex für Segovia heruntergehen da Filter-Pressen,Ventilation,Tasilings usw fertiggestellt sind..man kommt dann irgendwann an den Punkt das man nur noch Substaining-Kosten hat und weniger investieren muss.....

...was Toroparu angeht..we hier behaupter der Erwerb waere ein Griff ins Klo hat wohl die PEA nicht gelesen? die St udie legt doch eindeutig da das man ein recht grosses Projekt mit relativ geringer Capaex realisieren kann (wenn Wheaton nicht abspringt sogar sehr günstig)..dabei gibt es noch Aufwärtspotential was günstigen Strom usw angeht, sowie gebrauchtes Equipement... Toroparu ist eh noch paar Jahre hin...kann man locjker aus Segovia+Marmato-Cashflow + einem kelineren Kredit von 100-200 milo USD realisieren ... sehe da wenig Probleme

warten wir die nächsten news ab ... jUNI/Juli erstmal Produktionszahlen Mai und eventuell news zu der Erweiterung der Anlage auf 1500 t/Tag Durchsatz ... wie du schon richtig feststelltest wird 2020/21 herum die Capex für Segovia heruntergehen da Filter-Pressen,Ventilation,Tasilings usw fertiggestellt sind..man kommt dann irgendwann an den Punkt das man nur noch Substaining-Kosten hat und weniger investieren muss.....

...was Toroparu angeht..we hier behaupter der Erwerb waere ein Griff ins Klo hat wohl die PEA nicht gelesen? die St udie legt doch eindeutig da das man ein recht grosses Projekt mit relativ geringer Capaex realisieren kann (wenn Wheaton nicht abspringt sogar sehr günstig)..dabei gibt es noch Aufwärtspotential was günstigen Strom usw angeht, sowie gebrauchtes Equipement... Toroparu ist eh noch paar Jahre hin...kann man locjker aus Segovia+Marmato-Cashflow + einem kelineren Kredit von 100-200 milo USD realisieren ... sehe da wenig Probleme

Antwort auf Beitrag Nr.: 60.827.933 von Dubaianer am 18.06.19 00:29:33gute Zusammenfassung.. so sehe ich das auch....

Trading Spotlight

Antwort auf Beitrag Nr.: 60.827.960 von Dubaianer am 18.06.19 00:56:00Und wenn ich Mir Ihre Schreiben so ansehe:

Kann Es nicht beschwören, aber würde sagen JMF KÖNNTE zermatscht werden.

Muss Er EVT AUFPASSEN.

Kann Es nicht beschwören, aber würde sagen JMF KÖNNTE zermatscht werden.

Muss Er EVT AUFPASSEN.

Antwort auf Beitrag Nr.: 60.827.951 von Dubaianer am 18.06.19 00:42:35Mal ohne Wertung Der Aktie;

Das können Andere Viel besser;

aber Eure Diskussion Hier finde ich echt interessant.

Daumen HOCH!

Das können Andere Viel besser;

aber Eure Diskussion Hier finde ich echt interessant.

Daumen HOCH!

Antwort auf Beitrag Nr.: 60.827.930 von German2 am 18.06.19 00:27:28Genau, auch hier sollte man erst mal die PEA abwarten. Aktuell ist Marmato kaum gewinnträchtig, das ist absolut richtig.

Aber in 2-3 Jahren schaut auch hier alles ganz anders aus.

Genau wie man bei Segovia auf höhere Grades gesetzt hat, wird man das zukünftig bei Marmato machen. Startet ab dem vierten Quartal 2019 - alles anzuhören im letzten Konferenz-Call.

Die höheren Grades liegen aber weiter in der Tiefe. Deswegen wird man zukünftig von dort das Gestein rausholen.

Grob lässt sich sagen: Wenn zukünftig pro Tonne verarbeiteten Gestein 4 Gramm Gold hängen bleiben und nicht mehr nur 2 Gramm, dann wird man zu nahezu gleichen Produktionskosten die doppelte Menge Gold erhalten. Heißt die Produktionskosten je Unze werden sich fast halbieren! Und dann produziert man auf Marmato nicht mehr zu All-In-Cashkosten von ca. 1.200 USD, sondern etwas mehr als 600 USD.

Das ist in etwa von der PEA zu erwarten. Ist doch eigentlich logisch nachvollziehbar, oder?

Selbst wenn man konservativ von 800 oder 900 USD ausgeht, wird zukünftig hier eine ganze Menge an Geld hängen bleiben. Vor allem wenn man das ganze auf 180.000 Unzen pro Jahr ausweitet.

Das ganze ist kein Hexenwerk, sondern einfach nur 1:1 das gleiche was man auf Segovia schon erfolgreich gemacht hat und was die Mine so profitabel gemacht hat.

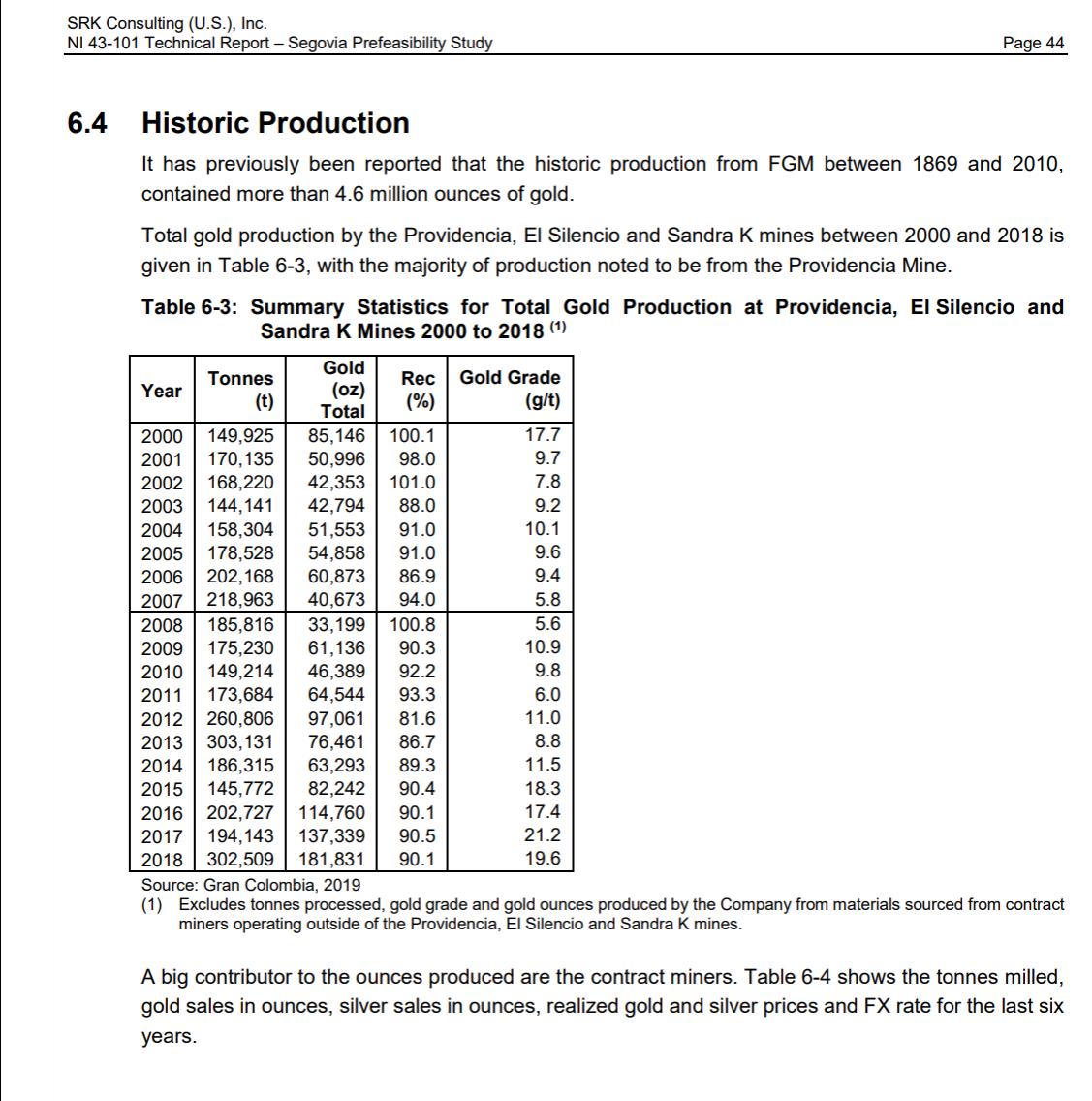

Ich habe hier explizit nochmal die Grafik eingefügt, damit jeder nochmal sehen kann, wie das Management seit dem Amtsantritt 2014 (als das Unternehmen faktisch fast Pleite war) die Grades hochgetrieben hat und dadurch die Mine hochprofitabel gemacht hat.

Nichts anderes wird in Zukunft auf Marmato gemacht werden!

Wenn man das versteht, dann wird man auch verstehen, warum die Aktie das Potential hat mittelfristig Kurse von 20, 30 oder gar 50 CAD zu erreichen! Natürlich nicht heute, aber spätestens 2023 wenn man hier 400.000 Unzen jährlich produzieren wird!

Aber in 2-3 Jahren schaut auch hier alles ganz anders aus.

Genau wie man bei Segovia auf höhere Grades gesetzt hat, wird man das zukünftig bei Marmato machen. Startet ab dem vierten Quartal 2019 - alles anzuhören im letzten Konferenz-Call.

Die höheren Grades liegen aber weiter in der Tiefe. Deswegen wird man zukünftig von dort das Gestein rausholen.

Grob lässt sich sagen: Wenn zukünftig pro Tonne verarbeiteten Gestein 4 Gramm Gold hängen bleiben und nicht mehr nur 2 Gramm, dann wird man zu nahezu gleichen Produktionskosten die doppelte Menge Gold erhalten. Heißt die Produktionskosten je Unze werden sich fast halbieren! Und dann produziert man auf Marmato nicht mehr zu All-In-Cashkosten von ca. 1.200 USD, sondern etwas mehr als 600 USD.

Das ist in etwa von der PEA zu erwarten. Ist doch eigentlich logisch nachvollziehbar, oder?

Selbst wenn man konservativ von 800 oder 900 USD ausgeht, wird zukünftig hier eine ganze Menge an Geld hängen bleiben. Vor allem wenn man das ganze auf 180.000 Unzen pro Jahr ausweitet.

Das ganze ist kein Hexenwerk, sondern einfach nur 1:1 das gleiche was man auf Segovia schon erfolgreich gemacht hat und was die Mine so profitabel gemacht hat.

Ich habe hier explizit nochmal die Grafik eingefügt, damit jeder nochmal sehen kann, wie das Management seit dem Amtsantritt 2014 (als das Unternehmen faktisch fast Pleite war) die Grades hochgetrieben hat und dadurch die Mine hochprofitabel gemacht hat.

Nichts anderes wird in Zukunft auf Marmato gemacht werden!

Wenn man das versteht, dann wird man auch verstehen, warum die Aktie das Potential hat mittelfristig Kurse von 20, 30 oder gar 50 CAD zu erreichen! Natürlich nicht heute, aber spätestens 2023 wenn man hier 400.000 Unzen jährlich produzieren wird!

Antwort auf Beitrag Nr.: 60.827.927 von German2 am 18.06.19 00:26:04Danke German2, du verstehst was ich meine.

Einfach mal die 600k Unzen vergessen. In 2-3 Jahren haben wir hier Millionen Unzen stehen. Zumindest bin ich davon 100% überzeugt und auch deshalb entsprechend stark investiert.

2012 hatte man eine Ressource von 113.000 Unzen und trotzdem war danach nicht Schicht im Schacht. Es wurden seitdem weitere 753.000 Unzen produziert und weitere 600.000 Unzen sind jetzt aktuell noch als Reserven(!) vorhanden.

Die Ressource ist nur deswegen so klein, weil GCM in der Vergangenheit kaum in die Exploration investiert hat bzw. finanziell nicht in der Lage war dies zu tun.

Das Blatt hat sich jetzt aber geändert die Verschuldung von 180 Millionen USD konnte heruntergefahren werden auf eine Nettoverschuldung (Schulden abzüglich Cashbestand) von mittlerweile nur noch ca. 20 Millionen USD. Spätestens Ende des Jahres wird man Netto-Schuldenfrei sein!

Das sind die knallharten Fakten. Jetzt ist mehr als ausreichend Geld da um die Ressource auszuweiten. Aber auch das wird noch 2 Jahre oder so dauern, bis das dann wirklich schwarz auf weiß nachlesbar sein wird.

Einfach mal die 600k Unzen vergessen. In 2-3 Jahren haben wir hier Millionen Unzen stehen. Zumindest bin ich davon 100% überzeugt und auch deshalb entsprechend stark investiert.

2012 hatte man eine Ressource von 113.000 Unzen und trotzdem war danach nicht Schicht im Schacht. Es wurden seitdem weitere 753.000 Unzen produziert und weitere 600.000 Unzen sind jetzt aktuell noch als Reserven(!) vorhanden.

Die Ressource ist nur deswegen so klein, weil GCM in der Vergangenheit kaum in die Exploration investiert hat bzw. finanziell nicht in der Lage war dies zu tun.

Das Blatt hat sich jetzt aber geändert die Verschuldung von 180 Millionen USD konnte heruntergefahren werden auf eine Nettoverschuldung (Schulden abzüglich Cashbestand) von mittlerweile nur noch ca. 20 Millionen USD. Spätestens Ende des Jahres wird man Netto-Schuldenfrei sein!

Das sind die knallharten Fakten. Jetzt ist mehr als ausreichend Geld da um die Ressource auszuweiten. Aber auch das wird noch 2 Jahre oder so dauern, bis das dann wirklich schwarz auf weiß nachlesbar sein wird.

Achja, noch ein Zusatz zu meinem letzten Post.

Auf Stockhouse hat jemand geschrieben, der auf der Hauptversammlung von GCM war. Ich war nicht vor Ort, aber angeblich wurde auf der Hauptversammlung gesagt, dass diese Woche die Produktionszahlen für den Monat Mai kommen sowie eine Anhebung der Produktionsprognose.

Also wird Mai wieder ein sehr gutes Quartal gewesen sein (übrigens 31 Produktionstage gegenüber 30 Tagen im April), sonst wäre man eher vorsichtiger mit einer Anhebung der Produktionsprognose.

Und Anfang Juli sollen dann die Produktionszahlen zum zweiten Quartal kommen - und ab Juni ist dann die tägliche Verarbeitungskapazität höher.

Auf Stockhouse hat jemand geschrieben, der auf der Hauptversammlung von GCM war. Ich war nicht vor Ort, aber angeblich wurde auf der Hauptversammlung gesagt, dass diese Woche die Produktionszahlen für den Monat Mai kommen sowie eine Anhebung der Produktionsprognose.

Also wird Mai wieder ein sehr gutes Quartal gewesen sein (übrigens 31 Produktionstage gegenüber 30 Tagen im April), sonst wäre man eher vorsichtiger mit einer Anhebung der Produktionsprognose.

Und Anfang Juli sollen dann die Produktionszahlen zum zweiten Quartal kommen - und ab Juni ist dann die tägliche Verarbeitungskapazität höher.

Gran Colombia Gold