Metals X - spannendes Investment bei steigendem Zinnpreis? - 500 Beiträge pro Seite

eröffnet am 18.01.13 10:23:12 von

neuester Beitrag 18.06.13 09:07:52 von

neuester Beitrag 18.06.13 09:07:52 von

Beiträge: 29

ID: 1.178.920

ID: 1.178.920

Aufrufe heute: 0

Gesamt: 3.871

Gesamt: 3.871

Aktive User: 0

ISIN: AU000000MLX7 · WKN: A0LG1C · Symbol: FG5

0,2605

EUR

-5,27 %

-0,0145 EUR

Letzter Kurs 10:33:46 Stuttgart

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7950 | +30,33 | |

| 5,1500 | +21,75 | |

| 15,715 | +20,33 | |

| 0,9000 | +16,13 | |

| 15.699,00 | +15,27 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,5180 | -7,09 | |

| 3,8000 | -7,54 | |

| 10,040 | -7,89 | |

| 0,5400 | -8,47 | |

| 0,5500 | -21,43 |

Metals X Limited

ISIN: AU000000MLX7 | WKN: A0LG1C

Homepage: http://www.metalsx.com.au/

Share Structure:

Issued & Outstanding Common shares: 1,652 Mio

Options: 38,2 Mio

Market Capitalisation (Jan. 2013): ca. AUD §250 Mio

Cash & Working Capital: ca. AUD $95

Schulden: AUD $0

Guter und ausführlicher Researchbericht von Green Leader (Dez. 2012): Homepage von Metals X Verlinkung unten in der Mitte

Projekte:

Renison Tin (Beteiligung von 50%):

Die Mine produziert aktuell in Tasmanien 1800 Tonnen Zinn pro Quartal zu Kosten von etwa $13000. Sollte der Zinnpreis durchschnittlich $25000 in 2013 betragen (wovon ich ausgehe) könnten etwa

1800t x $12000 Gewinn x 50% = 10 Mio

pro Quartal für Metals X übrig bleiben.

Die Ressource der Liegenschaft in nach unten und mehreren Seiten offen und wird weiter erbohrt.

Spannend für die Gewinnentwicklung von Metals X ist es, dass die volle Produktionskapazität erst im Dezember erreicht wurde. Dadurch sollte die Gewinnentwicklung zu den Vorjahren rapide ansteigen.

In der Nähe der Mine befindet sich mit Rentails eine weitere Zinnliegenschaft im Besitz von Metals X, die gerade erschlossen wird.

Wingellina (30% MLX free carried to commercial production)

Gemeinsam mit dem strategischen Partner Samsung C&T (also ein finanziell sehr potenter Partner) entwickelt Metals X eine gigantische Nickelliegenschaft in australischen Outback. Bisher sind 183Mt @ 1% Ni; 0,08% Co nachgewiesen.

Eine Feasibility Study liegt vor und geht von einem Minenleben von 40 Jahren aus.

Central Murchison Gold Projekt (100% MLX)

Seit letzter Woche liegt eine Feasibility Study vor:

http://www.metalsx.com.au/investors/asx-announcements/Ob Metals X selber produziert oder die Liegenschaft verkauft, werden die nächsten Monate zeigen.

Rover Projekt (100% MLX)

Die Liegenschaft befindet sich im Northern Territory im Tennant Creek gold field. Eine JORC Ressource von 1,2Moz AuEq liegt vor.

Außerdem besitzt MLX mehrere kleinere Investments.

Green Leader berechnen in ihrem Bericht einen fairen Wert für alle Liegenschaften von MLX von AUD $0,42. Wertsteigernd könnte sich 2013 eine positive Entwicklung des Zinnpreises auswirken. Ebenso würden positive Nachrichten von den Goldprojekten und vor allem zu Wingellina den Kurs nach Norden treiben.

Ich sehe hier eine Aktie mit einem enormen Potential, die aktuell weit unter Wert ihrer Liegenschaften gehandelt wird, da zu wenig transparent ist, wann welches Projekt wie weitergeführt wird. Geld ist jedoch da und wird weiter verdient. Für mich ist es nur eine Frage der Zeit bis uns weitere Nägel mit Köpfen präsentiert werden.

Daher bin ich diese Woche zu AUD $0,15 eingestiegen.

ISIN: AU000000MLX7 | WKN: A0LG1C

Homepage: http://www.metalsx.com.au/

Share Structure:

Issued & Outstanding Common shares: 1,652 Mio

Options: 38,2 Mio

Market Capitalisation (Jan. 2013): ca. AUD §250 Mio

Cash & Working Capital: ca. AUD $95

Schulden: AUD $0

Guter und ausführlicher Researchbericht von Green Leader (Dez. 2012): Homepage von Metals X Verlinkung unten in der Mitte

Projekte:

Renison Tin (Beteiligung von 50%):

Die Mine produziert aktuell in Tasmanien 1800 Tonnen Zinn pro Quartal zu Kosten von etwa $13000. Sollte der Zinnpreis durchschnittlich $25000 in 2013 betragen (wovon ich ausgehe) könnten etwa

1800t x $12000 Gewinn x 50% = 10 Mio

pro Quartal für Metals X übrig bleiben.

Die Ressource der Liegenschaft in nach unten und mehreren Seiten offen und wird weiter erbohrt.

Spannend für die Gewinnentwicklung von Metals X ist es, dass die volle Produktionskapazität erst im Dezember erreicht wurde. Dadurch sollte die Gewinnentwicklung zu den Vorjahren rapide ansteigen.

In der Nähe der Mine befindet sich mit Rentails eine weitere Zinnliegenschaft im Besitz von Metals X, die gerade erschlossen wird.

Wingellina (30% MLX free carried to commercial production)

Gemeinsam mit dem strategischen Partner Samsung C&T (also ein finanziell sehr potenter Partner) entwickelt Metals X eine gigantische Nickelliegenschaft in australischen Outback. Bisher sind 183Mt @ 1% Ni; 0,08% Co nachgewiesen.

Eine Feasibility Study liegt vor und geht von einem Minenleben von 40 Jahren aus.

Central Murchison Gold Projekt (100% MLX)

Seit letzter Woche liegt eine Feasibility Study vor:

http://www.metalsx.com.au/investors/asx-announcements/Ob Metals X selber produziert oder die Liegenschaft verkauft, werden die nächsten Monate zeigen.

Rover Projekt (100% MLX)

Die Liegenschaft befindet sich im Northern Territory im Tennant Creek gold field. Eine JORC Ressource von 1,2Moz AuEq liegt vor.

Außerdem besitzt MLX mehrere kleinere Investments.

Green Leader berechnen in ihrem Bericht einen fairen Wert für alle Liegenschaften von MLX von AUD $0,42. Wertsteigernd könnte sich 2013 eine positive Entwicklung des Zinnpreises auswirken. Ebenso würden positive Nachrichten von den Goldprojekten und vor allem zu Wingellina den Kurs nach Norden treiben.

Ich sehe hier eine Aktie mit einem enormen Potential, die aktuell weit unter Wert ihrer Liegenschaften gehandelt wird, da zu wenig transparent ist, wann welches Projekt wie weitergeführt wird. Geld ist jedoch da und wird weiter verdient. Für mich ist es nur eine Frage der Zeit bis uns weitere Nägel mit Köpfen präsentiert werden.

Daher bin ich diese Woche zu AUD $0,15 eingestiegen.

Hallo tpnl,

ein Thema zu diesem Wert sollte genügen, bitte nicht Spam-artig streuen.

Herzlichen Dank und beste Grüße,

a.mueller

ein Thema zu diesem Wert sollte genügen, bitte nicht Spam-artig streuen.

Herzlichen Dank und beste Grüße,

a.mueller

Hier einige Links zum Zinnmarkt:

Ein interessantes Interwiev zum Zinnmarkt (ca. 11 Minuten):http://www.brrmedia.com/event/107487/james-marlay-brr-media-…

Eine Präsentation vom Sept. 2012 zur "Zinn - Angebot/Nachfrage": http://de.slideshare.net/JohnSykes/supply-shortages-in-tin-m…

Ein weiterer differenzierter Hintergrundbericht zum Zinnmarkt:

http://https//www.itri.co.uk/index.php?option=com_zoo&task=i…

LONDON, Dec 11 (Reuters) - Companies seeking to build new tin mines are struggling to finance the projects, which could deepen shortages in a market that is already in deficit and exacerbate price moves that are already volatile.

Financing any new mine has become difficult following the global financial crisis, but the situation in the tin sector is even worse. Many banks shun lending to tin projects due to its thin market after the collapse of a cartel in the 1980s.

Prices may have to double to attract enough investment in new mines. But if the price soars out of control, consumers could be forced to find substitutes, leading to a boom-bust situation.

Companies are looking at a range of creative options to fund the next generation of mines to extract the metal, which is mainly used for solder in the electronics industry and in coatings for cans and other packaging.

Some are seeking money based on other products mined in the same project such as tungsten or iron ore, while others are trying to obtain financing from end-users who want to lock in a stream of supply.

"It's very tough for tin producers," said Peter Cook, chairman of Australia's biggest tin producer, Metals X.

"The real problem is tin is a commodity that has a very volatile price ... Any bank that finances a project likes to secure the cash flow," he said in an interview during a recent tin conference sponsored by industry group ITRI.

Banks often require mining firms to hedge output to lock in future prices, but long-term hedging is impossible for tin, because futures for the metal on the London Metal Exchange (LME) only extend 15 months forward, compared with 123 months for copper and aluminium.

Another difficulty is weak share markets and low valuations of mining shares, which makes it difficult to raise money through equity issues.

"Some projects can actually get project finance from the banks, but the project won't go because they can't raise the equity component," Kasbah Resources Managing Director Wayne Bramwell said.

END USERS

Australia's Venture Minerals, which is developing the Mt. Lindsay tin/tungsten mine in Tasmania, expects tungsten to be the main driver for financing and may sell U.S. bonds.

"There are more creative ways of getting funding through off-take around tungsten, but tin I have less confidence in," Andrew Radonjic, its technical director, said.

Kerry Heywood, chief executive of Tin International, a private company working on projects in eastern Germany, has been holding talks with European tin smelters that use scrap supplies but are interested in more stable feedstock from mines.

Kasbah Resources also has been holding talks with end-users. Most consumers have not been prepared to be the main sources of cash, but they probably hold the key to future funding, Bramwell said.

"We can see this security-of-supply issue already happening. The change will be driven by the end-users, reaching through the smelters and down into companies like our own to secure supply."

Korea's Daewoo International has already made an investment in a tin project in Cameroon, Bramwell added.

DEEPER DEFICITS

The tin market is the only one of the six main industrial metals on the LME with a deficit forecast for 2013.

According to a poll of analysts by Reuters, its deficit is estimated to be 2,970 tonnes this year and widen to 4,189 tonnes in 2013.

The shortfall could get deeper, because small-scale mining in locales such as China, Indonesia and Bolivia, which accounts for nearly 40 per cent of global mine output, is expected to decline in coming years as easily accessible deposits run out.

At the same time, few new bigger mines are due to launch production.

"There are many deposits but few real projects with economics that seem viable," John Sykes, director of Greenfields Research, said.

Many new mines have low grades of ore, which hikes costs. At a grade of 0.5 percent, a typical open pit mine would need a price of $25,000 a tonne to just break even, and an underground operation would need about $40,000, ITRI said.

Three-month tin on the LME has gained 18 per cent since late October to around $23,000 a tonne but is still down about a third from a peak of $33,600 touched in April 2011.

Peter Kettle of ITRI expects prices to reach $35,000 to $40,000 by 2015, a gain of 50 to 75 per cent.

A more bullish view comes from Mark Thompson, executive chairman of private firm Treliver Minerals, which is seeking to revive tin mining in Britain. He said prices would go as high as $100,000 per tonne due to the funding difficulties and resulting shortages, before settling at $40,000 to $60,000.

"Very few projects I look at, and I'm also on the board of Eurotin so I'm talking about our projects as well - none of these things work at $20,000, none of them are financeable," said Thompson, who co-founded Galena, the hedge fund arm of commodity trader Trafigura.

Warren Hallam, managing director of Metals X, warned that the tin market could behave like the rare earths market, where prices skyrocketed on supply fears when China imposed export controls and then later tumbled.

"It'll always be subject to manipulation because it (tin) is the tiniest of all those markets. It's a miniscule market compared to the copper market," Hallam said.

A spike in prices, however, could curb demand in the long run by spurring consumers to find alternatives, Kettle said.

"This is all still dependent on a continual growth in consumption of a couple per cent a year. If the price does go to $100,000 a tonne, then you will get a lot of substitution."

Ein interessantes Interwiev zum Zinnmarkt (ca. 11 Minuten):http://www.brrmedia.com/event/107487/james-marlay-brr-media-…

Eine Präsentation vom Sept. 2012 zur "Zinn - Angebot/Nachfrage": http://de.slideshare.net/JohnSykes/supply-shortages-in-tin-m…

Ein weiterer differenzierter Hintergrundbericht zum Zinnmarkt:

http://https//www.itri.co.uk/index.php?option=com_zoo&task=i…

LONDON, Dec 11 (Reuters) - Companies seeking to build new tin mines are struggling to finance the projects, which could deepen shortages in a market that is already in deficit and exacerbate price moves that are already volatile.

Financing any new mine has become difficult following the global financial crisis, but the situation in the tin sector is even worse. Many banks shun lending to tin projects due to its thin market after the collapse of a cartel in the 1980s.

Prices may have to double to attract enough investment in new mines. But if the price soars out of control, consumers could be forced to find substitutes, leading to a boom-bust situation.

Companies are looking at a range of creative options to fund the next generation of mines to extract the metal, which is mainly used for solder in the electronics industry and in coatings for cans and other packaging.

Some are seeking money based on other products mined in the same project such as tungsten or iron ore, while others are trying to obtain financing from end-users who want to lock in a stream of supply.

"It's very tough for tin producers," said Peter Cook, chairman of Australia's biggest tin producer, Metals X.

"The real problem is tin is a commodity that has a very volatile price ... Any bank that finances a project likes to secure the cash flow," he said in an interview during a recent tin conference sponsored by industry group ITRI.

Banks often require mining firms to hedge output to lock in future prices, but long-term hedging is impossible for tin, because futures for the metal on the London Metal Exchange (LME) only extend 15 months forward, compared with 123 months for copper and aluminium.

Another difficulty is weak share markets and low valuations of mining shares, which makes it difficult to raise money through equity issues.

"Some projects can actually get project finance from the banks, but the project won't go because they can't raise the equity component," Kasbah Resources Managing Director Wayne Bramwell said.

END USERS

Australia's Venture Minerals, which is developing the Mt. Lindsay tin/tungsten mine in Tasmania, expects tungsten to be the main driver for financing and may sell U.S. bonds.

"There are more creative ways of getting funding through off-take around tungsten, but tin I have less confidence in," Andrew Radonjic, its technical director, said.

Kerry Heywood, chief executive of Tin International, a private company working on projects in eastern Germany, has been holding talks with European tin smelters that use scrap supplies but are interested in more stable feedstock from mines.

Kasbah Resources also has been holding talks with end-users. Most consumers have not been prepared to be the main sources of cash, but they probably hold the key to future funding, Bramwell said.

"We can see this security-of-supply issue already happening. The change will be driven by the end-users, reaching through the smelters and down into companies like our own to secure supply."

Korea's Daewoo International has already made an investment in a tin project in Cameroon, Bramwell added.

DEEPER DEFICITS

The tin market is the only one of the six main industrial metals on the LME with a deficit forecast for 2013.

According to a poll of analysts by Reuters, its deficit is estimated to be 2,970 tonnes this year and widen to 4,189 tonnes in 2013.

The shortfall could get deeper, because small-scale mining in locales such as China, Indonesia and Bolivia, which accounts for nearly 40 per cent of global mine output, is expected to decline in coming years as easily accessible deposits run out.

At the same time, few new bigger mines are due to launch production.

"There are many deposits but few real projects with economics that seem viable," John Sykes, director of Greenfields Research, said.

Many new mines have low grades of ore, which hikes costs. At a grade of 0.5 percent, a typical open pit mine would need a price of $25,000 a tonne to just break even, and an underground operation would need about $40,000, ITRI said.

Three-month tin on the LME has gained 18 per cent since late October to around $23,000 a tonne but is still down about a third from a peak of $33,600 touched in April 2011.

Peter Kettle of ITRI expects prices to reach $35,000 to $40,000 by 2015, a gain of 50 to 75 per cent.

A more bullish view comes from Mark Thompson, executive chairman of private firm Treliver Minerals, which is seeking to revive tin mining in Britain. He said prices would go as high as $100,000 per tonne due to the funding difficulties and resulting shortages, before settling at $40,000 to $60,000.

"Very few projects I look at, and I'm also on the board of Eurotin so I'm talking about our projects as well - none of these things work at $20,000, none of them are financeable," said Thompson, who co-founded Galena, the hedge fund arm of commodity trader Trafigura.

Warren Hallam, managing director of Metals X, warned that the tin market could behave like the rare earths market, where prices skyrocketed on supply fears when China imposed export controls and then later tumbled.

"It'll always be subject to manipulation because it (tin) is the tiniest of all those markets. It's a miniscule market compared to the copper market," Hallam said.

A spike in prices, however, could curb demand in the long run by spurring consumers to find alternatives, Kettle said.

"This is all still dependent on a continual growth in consumption of a couple per cent a year. If the price does go to $100,000 a tonne, then you will get a lot of substitution."

Antwort auf Beitrag Nr.: 44.036.355 von a.mueller am 18.01.13 10:30:42Hallo a.mueller von w.o.,

mein Fehler. Ich würde mich freuen, wenn Sie den anderen Thread wieder rausnehmen könnten.

Vielen Dank

tpnl

mein Fehler. Ich würde mich freuen, wenn Sie den anderen Thread wieder rausnehmen könnten.

Vielen Dank

tpnl

Antwort auf Beitrag Nr.: 44.036.355 von a.mueller am 18.01.13 10:30:42Hier noch die letzten ASX Announcements:

CMGP Feasibility Study:

http://www.asx.com.au/asxpdf/20130111/pdf/42cczpyl80pdly.pdf

Renison Quarterly Results Update:

http://www.asx.com.au/asxpdf/20130111/pdf/42ccwnwcqr9fyf.pdf

High Grade Tin Results Extend Renison Ore System:

http://www.asx.com.au/asxpdf/20130110/pdf/42ccc97r7wb19r.pdf

GPG: Investment Portfolio Update:

http://www.asx.com.au/asxpdf/20130102/pdf/42c7g418ryhwtb.pdf

CMGP Feasibility Study:

http://www.asx.com.au/asxpdf/20130111/pdf/42cczpyl80pdly.pdf

Renison Quarterly Results Update:

http://www.asx.com.au/asxpdf/20130111/pdf/42ccwnwcqr9fyf.pdf

High Grade Tin Results Extend Renison Ore System:

http://www.asx.com.au/asxpdf/20130110/pdf/42ccc97r7wb19r.pdf

GPG: Investment Portfolio Update:

http://www.asx.com.au/asxpdf/20130102/pdf/42c7g418ryhwtb.pdf

Trading Spotlight

Antwort auf Beitrag Nr.: 44.036.322 von tpnl am 18.01.13 10:23:12Hallo,

werde mal hier mitlesen und mich informieren, danke für die Threaderöffnung!

Hier ein paar Charts:

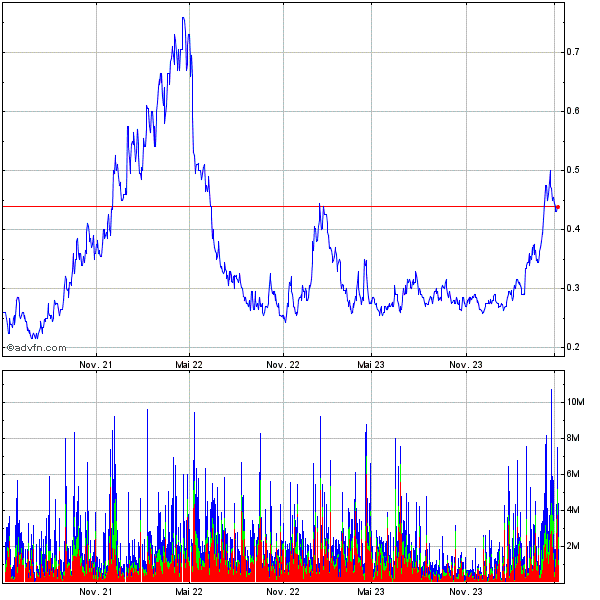

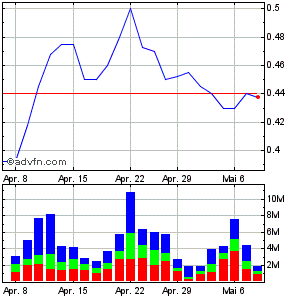

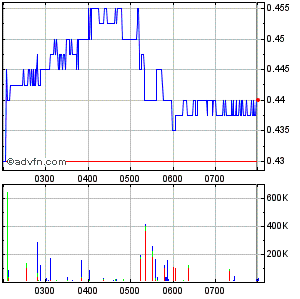

Metals X Chart (MLX)

Historischer Metals X Chart - 1 Monat

Intraday

Gruß

Stefan

werde mal hier mitlesen und mich informieren, danke für die Threaderöffnung!

Hier ein paar Charts:

Metals X Chart (MLX)

Historischer Metals X Chart - 1 Monat

Intraday

Gruß

Stefan

Zinn Chart in Dollar

Hier noch eine Info zu den Major Shareholdern:

APAC Resources: 24,1%

Jinchuan Group (weltweit größter Zinnproduzent): 10,7%

Blackrock: 5,3%

Board and Management: 8,5%

APAC Resources: 24,1%

Jinchuan Group (weltweit größter Zinnproduzent): 10,7%

Blackrock: 5,3%

Board and Management: 8,5%

Hallo tpnl,

Super Einleitung, sehr informativ - mein Kompliment!

Bei Deiner Aussage "Sollte der Zinnpreis durchschnittlich $25000 in 2013 betragen (wovon ich ausgehe) könnten etwa 1800t x $12000 Gewinn x 50% = 10 Mio pro Quartal für Metals X übrig bleiben." meinst Du sicherlich den operativen Gewinn, und nicht den Unternehmensgewinn. Das sind zwei unterschiedliche Aspekte.

Ich will demnächst selbst mal das Potenzial von Metals X ausloten.

Gruß

Tommy

Super Einleitung, sehr informativ - mein Kompliment!

Bei Deiner Aussage "Sollte der Zinnpreis durchschnittlich $25000 in 2013 betragen (wovon ich ausgehe) könnten etwa 1800t x $12000 Gewinn x 50% = 10 Mio pro Quartal für Metals X übrig bleiben." meinst Du sicherlich den operativen Gewinn, und nicht den Unternehmensgewinn. Das sind zwei unterschiedliche Aspekte.

Ich will demnächst selbst mal das Potenzial von Metals X ausloten.

Gruß

Tommy

Antwort auf Beitrag Nr.: 44.040.693 von tommy-hl am 19.01.13 14:08:20Hallo tommy-hl,

danke für das Lob und für die Ergänzung. Du hast Recht, ich war zu ungenau und damit zu optimistisch.

danke für das Lob und für die Ergänzung. Du hast Recht, ich war zu ungenau und damit zu optimistisch.

Hallo,

es wäre m.M.n. interessant, das Kurs-Potenzial mit versch. Preisen auszuloten. Z. B.: 25.000, 30.000, 35.000 $/t. Dann könnte man sich ein grobes Bild ausgehend von versch. Szenarien machen. Ist natürlich mit ein bisschen mehr Arbeit verbunden ...

Gruß

Tommy

es wäre m.M.n. interessant, das Kurs-Potenzial mit versch. Preisen auszuloten. Z. B.: 25.000, 30.000, 35.000 $/t. Dann könnte man sich ein grobes Bild ausgehend von versch. Szenarien machen. Ist natürlich mit ein bisschen mehr Arbeit verbunden ...

Gruß

Tommy

Hallo tommy-hl,

ich glaube nicht, dass der Zinnpreis alleine den Kurs vom Metals X bestimmen wird. Mindestens genauso wichtig wird sein, was sich bei den anderen Liegenschaften tut. Wie schnell entwickelt Samsung Wingellina weiter und was passiert mit den Goldliegenschaften. Werden sie verkauft, werden sie zur Produktion gebracht und wenn, dann in welchem Zeitraum?

Für eine Annäherung an der operativen Gewinn von Renison hatte ich vereinfachend folgende Formel verwendet:

Die Mine produziert aktuell in Tasmanien 1800 Tonnen Zinn pro Quartal zu Kosten von etwa $13000. Sollte der Zinnpreis durchschnittlich $25000/ $30000/ §35000 in 2013 betragen könnten etwa

1800t x $12000 x 50% = $10 Mio

1800t x $17000 x 50% = $15 Mio

1800t x $22000 x 50% = $20 Mio

je Quartal herausspringen. Bei 4 Quartalen könnte je nach Zinnpreis einiges zusammenkommen.

Ich möchte aber deutlich darauf hinweisen, dass diese Rechnung stark vereinfacht ist und maximal zu Näherungswerten führen kann.

ich glaube nicht, dass der Zinnpreis alleine den Kurs vom Metals X bestimmen wird. Mindestens genauso wichtig wird sein, was sich bei den anderen Liegenschaften tut. Wie schnell entwickelt Samsung Wingellina weiter und was passiert mit den Goldliegenschaften. Werden sie verkauft, werden sie zur Produktion gebracht und wenn, dann in welchem Zeitraum?

Für eine Annäherung an der operativen Gewinn von Renison hatte ich vereinfachend folgende Formel verwendet:

Die Mine produziert aktuell in Tasmanien 1800 Tonnen Zinn pro Quartal zu Kosten von etwa $13000. Sollte der Zinnpreis durchschnittlich $25000/ $30000/ §35000 in 2013 betragen könnten etwa

1800t x $12000 x 50% = $10 Mio

1800t x $17000 x 50% = $15 Mio

1800t x $22000 x 50% = $20 Mio

je Quartal herausspringen. Bei 4 Quartalen könnte je nach Zinnpreis einiges zusammenkommen.

Ich möchte aber deutlich darauf hinweisen, dass diese Rechnung stark vereinfacht ist und maximal zu Näherungswerten führen kann.

So weit so gut, aber vermutlich wolltest du, tommy-hl, auf einen anderen Faktor hinweisen, nämlich die große Aktienmenge.

Also noch einmal:

Wenn der Zinnpreis durchschnittlich $25000/ $30000/ §35000 in 2013 betragen sollte, könnte etwa folgendes für die einzene Aktie herauskommen:

Zinpreis $25000 (+0%) entspricht $40 Mio operativen Gewinn entspricht 2,5 Ct je Aktie (bei 1600 Mio Aktien)

Zinpreis $30000 (+20%) entspricht $60 Mio operativen Gewinn entspricht 3,75 Ct je Aktie (bei 1600 Mio), Minus den bisherigen 2,5 Ct entspricht dies einer Wertsteigerung zum Aktienkurs (aktuell bei 15Ct) von ca. 12%.

Zinpreis $35000 (+40%) entspricht $80 Mio operativen Gewinn entspricht 5 Ct je Aktie (bei 1600 Mio), Minus den bisherigen 2,5 Ct entspricht dies einer Wertsteigerung zum Aktienkurs (aktuell bei 15Ct) von ca. 17%.

Wenn ich keinen Rechenfehler gemacht habe, was gut sein kann, da ich es eilig habe, zeigt dies, das ich mit einem Zertikat auf den Zinnpreis besser fahre, wenn ich diese Aktie nur kaufe, da ich auf einen steigenden Zinnpreis spekuliere.

Interessant bleibt für mich jedoch, dass Metals X das verdiente Geld nicht

nutzen wird, um eine Dividende an uns Aktionäre zahlen, sondern vermutlich um ihre anderen Liegenschaften weiterzuentwickeln, wodurch sich der Gewinn auf dauern potentieren sollte.

Also noch einmal:

Wenn der Zinnpreis durchschnittlich $25000/ $30000/ §35000 in 2013 betragen sollte, könnte etwa folgendes für die einzene Aktie herauskommen:

Zinpreis $25000 (+0%) entspricht $40 Mio operativen Gewinn entspricht 2,5 Ct je Aktie (bei 1600 Mio Aktien)

Zinpreis $30000 (+20%) entspricht $60 Mio operativen Gewinn entspricht 3,75 Ct je Aktie (bei 1600 Mio), Minus den bisherigen 2,5 Ct entspricht dies einer Wertsteigerung zum Aktienkurs (aktuell bei 15Ct) von ca. 12%.

Zinpreis $35000 (+40%) entspricht $80 Mio operativen Gewinn entspricht 5 Ct je Aktie (bei 1600 Mio), Minus den bisherigen 2,5 Ct entspricht dies einer Wertsteigerung zum Aktienkurs (aktuell bei 15Ct) von ca. 17%.

Wenn ich keinen Rechenfehler gemacht habe, was gut sein kann, da ich es eilig habe, zeigt dies, das ich mit einem Zertikat auf den Zinnpreis besser fahre, wenn ich diese Aktie nur kaufe, da ich auf einen steigenden Zinnpreis spekuliere.

Interessant bleibt für mich jedoch, dass Metals X das verdiente Geld nicht

nutzen wird, um eine Dividende an uns Aktionäre zahlen, sondern vermutlich um ihre anderen Liegenschaften weiterzuentwickeln, wodurch sich der Gewinn auf dauern potentieren sollte.

Antwort auf Beitrag Nr.: 44.042.266 von tpnl am 20.01.13 14:34:58Danke für Deine Aufstellung über den oper. Gewinn

Gibt es eigentlich einen Business Plan, der die Wachstumstrategie aufzeigt?

Ich meine damit die geplanten Tonnen Zinn p. a. in den nä. Jahren, dann Zink und/oder Gold pro Jahr usw.

Die letzte Präsi ist ja schon ein bisschen alt ...

Gibt es eigentlich einen Business Plan, der die Wachstumstrategie aufzeigt?

Ich meine damit die geplanten Tonnen Zinn p. a. in den nä. Jahren, dann Zink und/oder Gold pro Jahr usw.

Die letzte Präsi ist ja schon ein bisschen alt ...

Einen Business Plan habe ich bisher ebenfalls vergeblich gesucht.

Auf der einen Seite wäre es für uns Anleger mit Plan leichter, eigene Erwartungen und Prognosen auf realistischere Beine zu stellen, auf der anderen Seite ist das Unternehmen ohne veröffentlichten Plan flexibler, wenn es darum geht, die eigene Entwicklung dem Geschehen auf den Rohstoffmärkten anzupassen.

Ich glaube nicht, dass Metal X all ihre Projekte gleichzeitig vorantreiben können. Sie werden Schwerpunkte setzen müssen und hier kann eine gewisse Flexibilität hilfreich sein.

Auf der einen Seite wäre es für uns Anleger mit Plan leichter, eigene Erwartungen und Prognosen auf realistischere Beine zu stellen, auf der anderen Seite ist das Unternehmen ohne veröffentlichten Plan flexibler, wenn es darum geht, die eigene Entwicklung dem Geschehen auf den Rohstoffmärkten anzupassen.

Ich glaube nicht, dass Metal X all ihre Projekte gleichzeitig vorantreiben können. Sie werden Schwerpunkte setzen müssen und hier kann eine gewisse Flexibilität hilfreich sein.

Link zu einer interessanten Umfrage von Reuters bei verschiedenen Investmenthäusern zu den Aussichten der Basismetalle für 2013 und 2014 (Danke tommy-hl für den Hinweis in deinem Thread!).

Zinn schneidet am besten ab.

http://uk.finance.yahoo.com/news/column-analysts-poll-only-w…

WINNERS

No surprise to see which metals analysts have picked out for upside price potential.

Tin is the favourite, an obvious choice given the soldering and plating metal's still-strong bull narrative of stretched supply.

Eight analysts offered a supply-demand balance forecast for tin and not one of them is expecting anything other than deficit for either this year or next.

The median forecast is for the tin price to average $23,800 per tonne this year and almost $25,000 per tonne in 2014.

Bei der Preisentwicklung erhoffe ich mir jedoch durchaus einen höheren Anstieg...

Zinn schneidet am besten ab.

http://uk.finance.yahoo.com/news/column-analysts-poll-only-w…

WINNERS

No surprise to see which metals analysts have picked out for upside price potential.

Tin is the favourite, an obvious choice given the soldering and plating metal's still-strong bull narrative of stretched supply.

Eight analysts offered a supply-demand balance forecast for tin and not one of them is expecting anything other than deficit for either this year or next.

The median forecast is for the tin price to average $23,800 per tonne this year and almost $25,000 per tonne in 2014.

Bei der Preisentwicklung erhoffe ich mir jedoch durchaus einen höheren Anstieg...

habe ich hier von der Webseite kopiert.

Das Renison Tin Projekt ist ja riesig, allerdings gehört MetalsX nur 50 % davon. 300 Mio $ replacement costs klingt gut, allerdings weiß man aus den Zahlen noch nicht welche Investitionen noch nötig sind.

Australia's Largest Tin Producer

Metals X is a globally significant tin producer through its 50% ownership of the Bluestone Mines Tasmania Joint Venture. The key assets of the Joint Venture are the world class Renison Tin Mine, a 700,000 tonne per annum tin concentrator plant and the Renison Expansion Project (Rentails).

Renison Tin Project

The Renison Project is located on the west coast of Tasmania and is a world class hard rock tin deposit with mining spanning three centuries. The current Resource is 245,000 tonnes of tin metal, 78% of which is JORC measured and indicated category. Renison is held as part of a 50/50 joint venture with the largest tin producer in the world, Yunnan Tin Group. The project is targeting annualised tin production of 7-8,000 tonnes at an operating cash cost of approximately A$12-13,000/t, comparing favourably with current tin prices.

The current mining reserve estimate is 45,700 tonnes of contained tin with a resource of 153,000 tonnes of contained tin. In 2012, Metals X increased the mining reserve estimate by 23% and the mineral resource estimate by 13%.

Renison remains the only major tin project in production in Australia and one of the few publicly held tin projects in the world.

Renison Tin Concentrator

Over the past few years the joint venture has invested considerable capital into exploration and increase of the resource base at Renison. Continued underground exploration activity has defined new zones of high-grade tin mineralisation beyond the boundaries of the current resource, and has also highlighted significant opportunities above existing development which were unrecognised by previous operators and now provides the opportunity for rapid conversion to reserve.

The mine is currently in the best shape it has been for many years. Replacement capital for the mine and processing infrastructure is estimated at over $300M.

Renison Expansion Project (Rentails)

Rentails Proposed Infrastructure

The Renison Expansion Project is a development project to reprocess the large historic tailings deposits generated at Renison since 1968 using modern technology. The estimated size of the project is 19.25M tonnes at 0.45% tin and 0.21% copper. The Renison Expansion Project represents one of the largest single resources of tin available in Australia today. A DFS was completed in 2009 and Metals X is currently working with its joint venture partners to prepare the project for development.

Other Tin Projects

Mt Bischoff Open Pit

Mt Bischoff is located 80km from Renison and is a significant deposit in its own right producing in excess of 55,000 tonnes of tin metal since the late 1800’s. The total footprint of historical production significantly exceeds the current open pit operations and the project has significant upside potential for additional tin mineralisation. The company continues to explore for further open pit and possible underground targets to continue to supplement ore supply to the Renison concentrator.

Collingwood Tin Project

The Collingwood Tin Project is located near the town of Cooktown in Far North Queensland. Metals X operated the Collingwood Tin Project until 2008 when it was placed on care and maintenance. The Collingwood Tin Project has a estimated mineral resource of 702,000 tonnes at 1.28% Sn.

Das Renison Tin Projekt ist ja riesig, allerdings gehört MetalsX nur 50 % davon. 300 Mio $ replacement costs klingt gut, allerdings weiß man aus den Zahlen noch nicht welche Investitionen noch nötig sind.

Australia's Largest Tin Producer

Metals X is a globally significant tin producer through its 50% ownership of the Bluestone Mines Tasmania Joint Venture. The key assets of the Joint Venture are the world class Renison Tin Mine, a 700,000 tonne per annum tin concentrator plant and the Renison Expansion Project (Rentails).

Renison Tin Project

The Renison Project is located on the west coast of Tasmania and is a world class hard rock tin deposit with mining spanning three centuries. The current Resource is 245,000 tonnes of tin metal, 78% of which is JORC measured and indicated category. Renison is held as part of a 50/50 joint venture with the largest tin producer in the world, Yunnan Tin Group. The project is targeting annualised tin production of 7-8,000 tonnes at an operating cash cost of approximately A$12-13,000/t, comparing favourably with current tin prices.

The current mining reserve estimate is 45,700 tonnes of contained tin with a resource of 153,000 tonnes of contained tin. In 2012, Metals X increased the mining reserve estimate by 23% and the mineral resource estimate by 13%.

Renison remains the only major tin project in production in Australia and one of the few publicly held tin projects in the world.

Renison Tin Concentrator

Over the past few years the joint venture has invested considerable capital into exploration and increase of the resource base at Renison. Continued underground exploration activity has defined new zones of high-grade tin mineralisation beyond the boundaries of the current resource, and has also highlighted significant opportunities above existing development which were unrecognised by previous operators and now provides the opportunity for rapid conversion to reserve.

The mine is currently in the best shape it has been for many years. Replacement capital for the mine and processing infrastructure is estimated at over $300M.

Renison Expansion Project (Rentails)

Rentails Proposed Infrastructure

The Renison Expansion Project is a development project to reprocess the large historic tailings deposits generated at Renison since 1968 using modern technology. The estimated size of the project is 19.25M tonnes at 0.45% tin and 0.21% copper. The Renison Expansion Project represents one of the largest single resources of tin available in Australia today. A DFS was completed in 2009 and Metals X is currently working with its joint venture partners to prepare the project for development.

Other Tin Projects

Mt Bischoff Open Pit

Mt Bischoff is located 80km from Renison and is a significant deposit in its own right producing in excess of 55,000 tonnes of tin metal since the late 1800’s. The total footprint of historical production significantly exceeds the current open pit operations and the project has significant upside potential for additional tin mineralisation. The company continues to explore for further open pit and possible underground targets to continue to supplement ore supply to the Renison concentrator.

Collingwood Tin Project

The Collingwood Tin Project is located near the town of Cooktown in Far North Queensland. Metals X operated the Collingwood Tin Project until 2008 when it was placed on care and maintenance. The Collingwood Tin Project has a estimated mineral resource of 702,000 tonnes at 1.28% Sn.

Hier der Link zu einem interessanten und aktuellen Researchbericht:

https://docs.google.com/viewer?a=v&q=cache:owoYegsaOhoJ:www.…

https://docs.google.com/viewer?a=v&q=cache:owoYegsaOhoJ:www.…

Habe mich auch mal ein wenig eingelesen. Unter 10 Eurocent werde ich mal eine kleine Position aufbauen. Mal sehen ob der Kurs in nächster Zeit mal dort hin schwankt.

Hallo Szween,

na dann viel Erfolg! Ich würde jedoch eher in Sydney handeln, da hier die Umsätze einfach größer sind nd du im "Notfall" die Aktien auch schnell wieder verkaufen kannst.

na dann viel Erfolg! Ich würde jedoch eher in Sydney handeln, da hier die Umsätze einfach größer sind nd du im "Notfall" die Aktien auch schnell wieder verkaufen kannst.

Antwort auf Beitrag Nr.: 44.070.222 von tpnl am 27.01.13 18:55:59Ich muss mir nur noch einen Broker suchen für Australien. Das geht bei DIBA nicht. Ist wohl leider unvermeidbar , da die Kurse da doch meist besser sind.

News: Der Quaterly Report ist da.

http://www.asx.com.au/mwg-internal/de5fs23hu73ds/progress?id…

Leider gelingt es mir nicht, einige relevante Auszüge zu kopieren und hier reinzustellen. Also, selber lesen. Die erste Seite gibt aber einen guten Überblick.

http://www.asx.com.au/mwg-internal/de5fs23hu73ds/progress?id…

Leider gelingt es mir nicht, einige relevante Auszüge zu kopieren und hier reinzustellen. Also, selber lesen. Die erste Seite gibt aber einen guten Überblick.

Der Fairness halber:

Habe meine Position von Metals X heute erstmal verkauft (für $AUD 0,16). Bei genauerem Nachrechnen erscheint mir der Quarterly Report eher negativ zu sein.

Werde den Wert jedoch weiterverfolgen und mein Glück vielleicht zu einem späteren Zeitpunkt noch einmal versuchen.

Habe meine Position von Metals X heute erstmal verkauft (für $AUD 0,16). Bei genauerem Nachrechnen erscheint mir der Quarterly Report eher negativ zu sein.

Werde den Wert jedoch weiterverfolgen und mein Glück vielleicht zu einem späteren Zeitpunkt noch einmal versuchen.

News:

Half Yearly Mineral Resource & Reserve Update

Download the Announcement:

http://www.metalsx.com.au/system/announcements/499/Half_Year…

Metals X is pleased to announce the half yearly update to its Mineral Resource and Ore Reserve Statements.

Highlights are:

• 20 % Increase in Tin Ore Reserves at the Renison Mine

• 83% Increase in Gold Mineral Resources at the Central Murchison Gold Project

• 37% Increase in Gold Reserves at the Central Murchison Gold Project

Metals X's CEO, Mr Peter Cook said:

“The outcomes of this half-yearly update clearly show the commodity diversity of the Metals X Group and in particular, the globally significant resource inventory we hold in Tin, Nickel, Cobalt and Gold.”

“ The growth in the Ore Reserves at the Renison Tin Project is an excellent outcome and testament to aggressive exploration, investment and belief in the future of the Renison mine over the past year. We have substantially increased both the size and quality of our Mineral Resources and Ore Reserves and we have again re-affirmed Renison as one of the great tin districts of the world. The size and quality of its tin inventory, including the Renison Expansion (“Rentails”) Project and the large amount of in-place capital plant infrastructure leaves it few peers as a Western world publicly listed tin company.”

“The growth in total Mineral Resource and Ore Reserves at the Central Murchison Project is beginning to reflect the potential of the three prolific gold mining centres that make up the project. What sets this area apart from others in the Murchison region is its core being three dominant higher grade underground mines that provide a platform for high-grade, higher margin, sustainable production as the down plunge continuity of these prolific past producers is re-established and exploited."

Half Yearly Mineral Resource & Reserve Update

Download the Announcement:

http://www.metalsx.com.au/system/announcements/499/Half_Year…

Metals X is pleased to announce the half yearly update to its Mineral Resource and Ore Reserve Statements.

Highlights are:

• 20 % Increase in Tin Ore Reserves at the Renison Mine

• 83% Increase in Gold Mineral Resources at the Central Murchison Gold Project

• 37% Increase in Gold Reserves at the Central Murchison Gold Project

Metals X's CEO, Mr Peter Cook said:

“The outcomes of this half-yearly update clearly show the commodity diversity of the Metals X Group and in particular, the globally significant resource inventory we hold in Tin, Nickel, Cobalt and Gold.”

“ The growth in the Ore Reserves at the Renison Tin Project is an excellent outcome and testament to aggressive exploration, investment and belief in the future of the Renison mine over the past year. We have substantially increased both the size and quality of our Mineral Resources and Ore Reserves and we have again re-affirmed Renison as one of the great tin districts of the world. The size and quality of its tin inventory, including the Renison Expansion (“Rentails”) Project and the large amount of in-place capital plant infrastructure leaves it few peers as a Western world publicly listed tin company.”

“The growth in total Mineral Resource and Ore Reserves at the Central Murchison Project is beginning to reflect the potential of the three prolific gold mining centres that make up the project. What sets this area apart from others in the Murchison region is its core being three dominant higher grade underground mines that provide a platform for high-grade, higher margin, sustainable production as the down plunge continuity of these prolific past producers is re-established and exploited."

Es ist ein neuer Report zu Metals X erschienen. Diesmal äußert sich Euroz Securities Limites (Kursziel: $ 0,27 - ungefähr 80% Kurssteigerung):

http://metalsx.us1.list-manage2.com/track/click?u=20720d1612…

http://metalsx.us1.list-manage2.com/track/click?u=20720d1612…

News:

Metals X Limited (MLX:ASX) is pleased to advise it has reached agreement with Crosslands Resources Ltd (Crosslands), to acquire its fully equipped 48 person accommodation facility located in Cue, adjacent to Metals X’s Central Murchison Gold Project (CMGP). Crosslands will also transfer Miscellaneous Lease L20/52, located on Metals X’s granted mining leases at Cuddingwarra, containing Crosslands’s surplus Stage 1 haulage laydown area which includes a weighbridge and associated infrastructure (See Figure 1 overleaf).

The agreement has been made subject to associated regulatory approvals.

Metals X has previously advised its intent to quickly bring the CMGP to fruition and the purchase is complimentary to that strategy whether Metals X elects to build a new plant or utilise ore processing opportunities in existing projects in the region. It provides the Company with the flexibility to consider a rapid start to open pit mining, including the Great Fingall pit which is the precursor to underground development of the high-grade Great Fingall and Golden Crown ore systems.

http://www.metalsx.com.au/system/announcements/503/20130222_…

Metals X Limited (MLX:ASX) is pleased to advise it has reached agreement with Crosslands Resources Ltd (Crosslands), to acquire its fully equipped 48 person accommodation facility located in Cue, adjacent to Metals X’s Central Murchison Gold Project (CMGP). Crosslands will also transfer Miscellaneous Lease L20/52, located on Metals X’s granted mining leases at Cuddingwarra, containing Crosslands’s surplus Stage 1 haulage laydown area which includes a weighbridge and associated infrastructure (See Figure 1 overleaf).

The agreement has been made subject to associated regulatory approvals.

Metals X has previously advised its intent to quickly bring the CMGP to fruition and the purchase is complimentary to that strategy whether Metals X elects to build a new plant or utilise ore processing opportunities in existing projects in the region. It provides the Company with the flexibility to consider a rapid start to open pit mining, including the Great Fingall pit which is the precursor to underground development of the high-grade Great Fingall and Golden Crown ore systems.

http://www.metalsx.com.au/system/announcements/503/20130222_…

Metals X Half Year Accounts:

http://www.metalsx.com.au/system/announcements/505/Half_Year…

und Renison Production Update:

http://www.metalsx.com.au/system/announcements/504/20130305_…

http://www.metalsx.com.au/system/announcements/505/Half_Year…

und Renison Production Update:

http://www.metalsx.com.au/system/announcements/504/20130305_…

News zu Wingellina:

http://www.asx.com.au/asx/statistics/displayAnnouncement.do?…

Der gesunkene Goldpreis wirkt sich natürlich fatal auf die Goldliegenschaften von Metals X aus, da deren Capex eh recht hoch ist. Der Kurs ist entsprechend gesunken.

http://www.asx.com.au/asx/statistics/displayAnnouncement.do?…

Der gesunkene Goldpreis wirkt sich natürlich fatal auf die Goldliegenschaften von Metals X aus, da deren Capex eh recht hoch ist. Der Kurs ist entsprechend gesunken.

Oh, Oh... Metals X legt das Nickel/Kobalt-Projekt auf Halde:

MetalsX to suspend WInGellIna DFS works

The Board of Metals X Limited advise that they have moved to postpone engineering works on the Definitive Feasibility Study (“DFS”) on its 100% owned Wingellina Nickel-Cobalt Project.

Metals X CEO and Executive Director, Peter Cook said “After due onsideration

of the current depressed equity and resource market and cyclical low in nickel prices, the Board has concluded that a deferral of expenditure is prudent.

Wingellina remains as one of the largest economically viable undeveloped nickel limonite projects in the world today and a short deferral of expenditure and/or feasibility works does not change this fact, nor will it impact the reflected valuation of the asset by the market for our shareholders”.

The Board has reviewed all aspects of the proposed study and the current market and believes that the previous Pre-feasibility Study completed in 2008 to a deemed +/- 25% confidence level remains sufficient to continue with the progression of the Wingellina Project in the interim.

Metals X is in a strong position with a healthy balance sheet (over $85M in cash and working capital and no debt) with positive cash flow from its Tasmanian tin operations. Mr Cook said “At this time it is prudent to preserve existing cash and build on the strong operating position the Company has with its tin business.

http://www.metalsx.com.au/system/announcements/514/2013061…

MetalsX to suspend WInGellIna DFS works

The Board of Metals X Limited advise that they have moved to postpone engineering works on the Definitive Feasibility Study (“DFS”) on its 100% owned Wingellina Nickel-Cobalt Project.

Metals X CEO and Executive Director, Peter Cook said “After due onsideration

of the current depressed equity and resource market and cyclical low in nickel prices, the Board has concluded that a deferral of expenditure is prudent.

Wingellina remains as one of the largest economically viable undeveloped nickel limonite projects in the world today and a short deferral of expenditure and/or feasibility works does not change this fact, nor will it impact the reflected valuation of the asset by the market for our shareholders”.

The Board has reviewed all aspects of the proposed study and the current market and believes that the previous Pre-feasibility Study completed in 2008 to a deemed +/- 25% confidence level remains sufficient to continue with the progression of the Wingellina Project in the interim.

Metals X is in a strong position with a healthy balance sheet (over $85M in cash and working capital and no debt) with positive cash flow from its Tasmanian tin operations. Mr Cook said “At this time it is prudent to preserve existing cash and build on the strong operating position the Company has with its tin business.

http://www.metalsx.com.au/system/announcements/514/2013061…

Beitrag zu dieser Diskussion schreiben

Zu dieser Diskussion können keine Beiträge mehr verfasst werden, da der letzte Beitrag vor mehr als zwei Jahren verfasst wurde und die Diskussion daraufhin archiviert wurde.

Bitte wenden Sie sich an feedback@wallstreet-online.de und erfragen Sie die Reaktivierung der Diskussion oder starten Sie eine neue Diskussion.

Investoren beobachten auch:

| Wertpapier | Perf. % |

|---|---|

| +3,09 | |

| -2,59 | |

| +0,37 | |

| +0,47 | |

| +0,22 | |

| 0,00 | |

| +1,72 | |

| +9,52 | |

| +3,23 | |

| -10,65 |

Meistdiskutiert

| Wertpapier | Beiträge | |

|---|---|---|

| 236 | ||

| 97 | ||

| 96 | ||

| 63 | ||

| 57 | ||

| 40 | ||

| 34 | ||

| 32 | ||

| 30 | ||

| 24 |