Cardero Resource Corp. (CDU) - It’s not only ore, it’s much more: Zahlen, Daten, Fakten und Diskussi - 500 Beiträge pro Seite (Seite 8)

eröffnet am 15.05.11 12:28:41 von

neuester Beitrag 31.03.22 17:25:22 von

neuester Beitrag 31.03.22 17:25:22 von

Beiträge: 4.628

ID: 1.166.193

ID: 1.166.193

Aufrufe heute: 0

Gesamt: 658.870

Gesamt: 658.870

Aktive User: 0

ISIN: CA14140U2048 · WKN: A142XA

0,1600

CAD

0,00 %

0,0000 CAD

Letzter Kurs 26.01.22 TSX Venture

dass ist ja nichts ... wenn selbst ich sowas stemmen könnte, dann zeigt das nur desinteresse

Antwort auf Beitrag Nr.: 43.723.571 von Sstocktrader am 17.10.12 19:24:21Nun, Carbon Creek hat einen Wert - ohne Zweifel. Ich bin derzeit aber auch etwas unentschlossen.

Price Size Orders

Ask

0.59 9,000 4

0.58 18,500 7

0.57 17,500 7

0.56 21,000 10

0.55 5,500 5

Bid

0.54 56,500 10

0.53 8,000 5

0.52 9,000 5

0.51 14,000 3

0.50 9,000 3

Price Size Orders

Ask

0.59 9,000 4

0.58 18,500 7

0.57 17,500 7

0.56 21,000 10

0.55 5,500 5

Bid

0.54 56,500 10

0.53 8,000 5

0.52 9,000 5

0.51 14,000 3

0.50 9,000 3

IDI, u.a. eine der Aktien in der Group, die mir im Moment Spass machen.

Indico Signs Binding MOU on the Maria Reyna Property

Indico Technologies Ltd

IDIFF | 10/17/2012 6:34:47 PM

Indico Signs Binding MOU on the Maria Reyna Property

http://www.stockhouse.com/news/usreleasesdetail.aspx?n=86425…

Indico Signs Binding MOU on the Maria Reyna Property

Indico Technologies Ltd

IDIFF | 10/17/2012 6:34:47 PM

Indico Signs Binding MOU on the Maria Reyna Property

http://www.stockhouse.com/news/usreleasesdetail.aspx?n=86425…

Moin,

solange nichts über die anstehende Finanzierung bekannt ist und generell keine Trendwende im Explorermarkt zu erkennen ist, werde ich auch zu den scheinbaren Schnäppchenkursen jetzt nicht "verbilligen". Im Zweifelsfall wirft man schlechtem Geld gutes hinterher und halbiert es wieder. Dann lieber die ersten paar Prozente der Erholung verpassen aber sicher sein dass es wirklich eine nennenswerte Erholung gibt. Damit meine ich nicht 50%, sondern mindestens 500% die jetzt nötig sind CDU nicht mehr als Totalversager dastehen zu lassen.

Stefan

solange nichts über die anstehende Finanzierung bekannt ist und generell keine Trendwende im Explorermarkt zu erkennen ist, werde ich auch zu den scheinbaren Schnäppchenkursen jetzt nicht "verbilligen". Im Zweifelsfall wirft man schlechtem Geld gutes hinterher und halbiert es wieder. Dann lieber die ersten paar Prozente der Erholung verpassen aber sicher sein dass es wirklich eine nennenswerte Erholung gibt. Damit meine ich nicht 50%, sondern mindestens 500% die jetzt nötig sind CDU nicht mehr als Totalversager dastehen zu lassen.

Stefan

Antwort auf Beitrag Nr.: 43.724.865 von Stefan0310 am 18.10.12 08:15:33"Coal Shares Are Still Underpriced

... we believe natural-gas price improvement, early predictions for a more normal winter, Gov. Romney's support for coal, higher iron ore and Chinese steel prices as a result of some Chinese restocking indications, hopes for more Chinese stimulus and beta-seeking investors have helped to aid valuation improvement. ..."

http://online.barrons.com/article/SB500014240531119040341045…

Geht das weiter, dann ziehen die Explorer nach - vor allen Dingen dann wenn sie guenstig produzieren können und eine geringe CAPEX haben. Cardero waere so ein Fall - eine sehr gute PFS mit praktisch kaum Schönheitsfehlern. Ich habe immer noch keinen geunstigeren Produzenten von met coal gefunden.

--

Ich setze mal eine Meinung rein (die ich reizvoll finde, aber nicht teile):

Big blocks on the BID a lot today

By bigmoneydave . Oct 17, 2012 4:16 PM . Permalink

This tells me this stock was probably walked down for accumulation to start.

Considering the amount of outstanding shares (90,000,000+), I doubt this company is in turmoil and drops this much over a few days with just a few 100K shares days.

http://finance.yahoo.com/mbview/threadview/;_ylt=AskYl0YYcB5…

... we believe natural-gas price improvement, early predictions for a more normal winter, Gov. Romney's support for coal, higher iron ore and Chinese steel prices as a result of some Chinese restocking indications, hopes for more Chinese stimulus and beta-seeking investors have helped to aid valuation improvement. ..."

http://online.barrons.com/article/SB500014240531119040341045…

Geht das weiter, dann ziehen die Explorer nach - vor allen Dingen dann wenn sie guenstig produzieren können und eine geringe CAPEX haben. Cardero waere so ein Fall - eine sehr gute PFS mit praktisch kaum Schönheitsfehlern. Ich habe immer noch keinen geunstigeren Produzenten von met coal gefunden.

--

Ich setze mal eine Meinung rein (die ich reizvoll finde, aber nicht teile):

Big blocks on the BID a lot today

By bigmoneydave . Oct 17, 2012 4:16 PM . Permalink

This tells me this stock was probably walked down for accumulation to start.

Considering the amount of outstanding shares (90,000,000+), I doubt this company is in turmoil and drops this much over a few days with just a few 100K shares days.

http://finance.yahoo.com/mbview/threadview/;_ylt=AskYl0YYcB5…

Trading Spotlight

Ich sehe hier noch keinen Boden. Warum sollte irgendjemand ins fallende Messer hinein investieren?

Falls wir mal einen Boden sehen, wüsste ich auch nicht, warum denn bitteschön ein schneller Anstieg erfolgen sollte.

Zählen wir doch mal die Fakten zusammen:

CDU hat ein schönes Kohleprojekt in Kanada, für das auch eine PFS vorliegt, die das Projekt wirtschaftlich sinnvoll erscheinen lassen.

CDU möchte Stand jetzt das Projekt allein stemmen.

Geld ist nicht genug da, um es ohne Finanzierung stemmen zu können.

Obendrein gibt es in Ghana ein Eisenprojekt, welches auch eher Geld verschlingt, als etwas bringt. Im Moment ist dies auch nicht verkäuflich.

Die Beteiligungen bringen nicht wirklich viel ein, würden eine Finanzierung des Kohleprojektes auch nicht zulassen.

Investoren wagen sich im Moment nirgends aus der Deckung.

Eine Finanzierung über ein Darlehen würde aufgrund der hohen Zinsbelastung keinen Sinn machen.

Ein PP zu diesen Schleuderpreisen erscheint auch nicht sinnvoll.

Ergo:

Sollte einer Interesse an CDU haben, Kurs runterprügeln, einen gehörigen Anteil kaufen, und ggf. ein Übernahmeangebot zu "geprügelten" Preisen machen. Läuft doch überall so.

Was hätte ein Investor bei dieser Vorgehensweise zu verlieren? Auf lange Sicht nichts!

Also ich gehe hier nicht von kurzfristig steigenden Kursen aus. Das ist alles zu vage.

Falls wir mal einen Boden sehen, wüsste ich auch nicht, warum denn bitteschön ein schneller Anstieg erfolgen sollte.

Zählen wir doch mal die Fakten zusammen:

CDU hat ein schönes Kohleprojekt in Kanada, für das auch eine PFS vorliegt, die das Projekt wirtschaftlich sinnvoll erscheinen lassen.

CDU möchte Stand jetzt das Projekt allein stemmen.

Geld ist nicht genug da, um es ohne Finanzierung stemmen zu können.

Obendrein gibt es in Ghana ein Eisenprojekt, welches auch eher Geld verschlingt, als etwas bringt. Im Moment ist dies auch nicht verkäuflich.

Die Beteiligungen bringen nicht wirklich viel ein, würden eine Finanzierung des Kohleprojektes auch nicht zulassen.

Investoren wagen sich im Moment nirgends aus der Deckung.

Eine Finanzierung über ein Darlehen würde aufgrund der hohen Zinsbelastung keinen Sinn machen.

Ein PP zu diesen Schleuderpreisen erscheint auch nicht sinnvoll.

Ergo:

Sollte einer Interesse an CDU haben, Kurs runterprügeln, einen gehörigen Anteil kaufen, und ggf. ein Übernahmeangebot zu "geprügelten" Preisen machen. Läuft doch überall so.

Was hätte ein Investor bei dieser Vorgehensweise zu verlieren? Auf lange Sicht nichts!

Also ich gehe hier nicht von kurzfristig steigenden Kursen aus. Das ist alles zu vage.

Sollte einer Interesse an CDU haben, Kurs runterprügeln, einen gehörigen Anteil kaufen, und ggf. ein Übernahmeangebot zu "geprügelten" Preisen machen. Läuft doch überall so.

Ask

0.60 5,000 1

0.59 10,000 2

0.58 16,500 9

0.57 8,500 8

0.56 4,500 3

Bid

0.55 12,000 4

0.54 49,000 10

0.53 7,000 4

0.52 15,500 5

0.51 16,000 2

Ask

0.60 5,000 1

0.59 10,000 2

0.58 16,500 9

0.57 8,500 8

0.56 4,500 3

Bid

0.55 12,000 4

0.54 49,000 10

0.53 7,000 4

0.52 15,500 5

0.51 16,000 2

...das Gute ist, wenn CDU bei einem Cent steht, reicht schon 1 Cent aus, um die Aktie um 100% steigen zu lassen...

Antwort auf Beitrag Nr.: 43.727.834 von gustel66 am 18.10.12 18:19:25So wie ich das sehe, zieht das OB gerade mit.

CDU: 0.62 CAD +0.07 +12.7% 139.6k

Antwort auf Beitrag Nr.: 43.728.861 von gustel66 am 18.10.12 22:44:46Sie bringen sich wieder als Uebernahmeziel ins Spiel und das ist ist gut und angemessen.

Cormark Securities:

Advancing Forward: Post the PFS, Management is looking to quickly advance Carbon Creek through feasibility and permitting. A bankable feasibility study has been slated for Q2/13, which will investigate various options proposed in the PFS and serve to further derisk the economics of the project. Concurrently over the near term, the Company will continue to collect baseline data for the Carbon Creek Environmental Assessment (EA) process. The main submission for the EA certificate is expected in Q2/13, which will allow the EA office about 180 days for review and approval by Q4/13. In addition to the EA process, environmental and associated permits must be obtained before full-scale mining. With approval expected in Q1/14, the Company believes construction can begin immediately with first production in late 2014. As we indicated previously, the Carbon Creek project does exhibit certain characteristics which should make it more amenable to a timely permit issuance. In addition to a large component of production being sourced via underground mining, the surface mining methods are designed to minimize waste rock mining, processing will not require groundwater or a tailings impoundment, and the use of a barge system eliminates the need for a haul road, tunnel or overland conveyors. As such, Management is confident in the permitting schedule laid out, which should allow all approvals in hand in H1/14. That said, meeting this timeline will be key to delivering the value presented.

Representing a potential risk to Cardero’s plans, we note the Company currently has port allocation at Ridley Terminals for 0.5MMtpa through 2014, increasing to 0.9MMtpa in 2015. The agreement has a 15 year term until December 31, 2008, which is extendable by 3 years. While these allocations are enough for the initial years, it is insufficient thereafter. Management is confident in its ability to acquire the needed port allocation as it expects several regional projects with significant port allocations to become delayed or cancelled. Recall, the deal is subject to Ridley receiving the Federal Government approval for addition of a fourth stacker/reclaimer that will increase capacity from 24MMtpa to 30MMtpa when sufficient capacity should be available.

Carbon Creek Scoped For A Major?

By increasing the production rate, the Company has also raised the upfront capital costs significantly for the project. This would normally make financing the mine even more difficult for the junior developer, especially given that the project economics (IRR, NPV) did not increase drastically from the PEA case. That said with its larger scale at a reasonable cost, we believe the Company has made the project more attractive and palatable for a regional producer. Recall that Carbon Creek is located on the Peace River coal trend, a district which hosts several major met coal operators, including Xstrata, Anglo American, and Walter Energy. We would especially note Xstrata, which has been an active consolidator in the area (most recently with the Sukunka coal deposit). In Figure 3, we present a regional concession map highlighting Carbon Creek’s position relative to other major operators in Peace River.

Maintaining Buy (S) Recommendation, Raising Target To C$2.50: Cardero continues to aggressively develop Carbon Creek, a met coal project which is sure to receive strong consideration by regional players in the near term. We see the potential for a rerating in the event a partner is brought in on the project or the coking coal market recovers materially. While interest in the met coal space is subdued due to near-term issues, we continue to see long-term potential and note that high-quality, low-risk assets are always in demand. With a pre-feasibility in hand, we recommend CDU to investors seeking exposure to metallurgical coal in the Peace River coalfield in a high-quality development asset. Having updated our model for the PFS findings, we reiterate our Buy (S) recommendation, and increase our target to C$2.50 from C$2.40 (based on 0.50x NAV plus cash and investments). As further development hurdles are overcome, our discount would be expected to narrow.

Quelle: http://finance.yahoo.com/mbview/threadview/?&bn=ae7ec2b4-5be…

Cormark Securities:

Advancing Forward: Post the PFS, Management is looking to quickly advance Carbon Creek through feasibility and permitting. A bankable feasibility study has been slated for Q2/13, which will investigate various options proposed in the PFS and serve to further derisk the economics of the project. Concurrently over the near term, the Company will continue to collect baseline data for the Carbon Creek Environmental Assessment (EA) process. The main submission for the EA certificate is expected in Q2/13, which will allow the EA office about 180 days for review and approval by Q4/13. In addition to the EA process, environmental and associated permits must be obtained before full-scale mining. With approval expected in Q1/14, the Company believes construction can begin immediately with first production in late 2014. As we indicated previously, the Carbon Creek project does exhibit certain characteristics which should make it more amenable to a timely permit issuance. In addition to a large component of production being sourced via underground mining, the surface mining methods are designed to minimize waste rock mining, processing will not require groundwater or a tailings impoundment, and the use of a barge system eliminates the need for a haul road, tunnel or overland conveyors. As such, Management is confident in the permitting schedule laid out, which should allow all approvals in hand in H1/14. That said, meeting this timeline will be key to delivering the value presented.

Representing a potential risk to Cardero’s plans, we note the Company currently has port allocation at Ridley Terminals for 0.5MMtpa through 2014, increasing to 0.9MMtpa in 2015. The agreement has a 15 year term until December 31, 2008, which is extendable by 3 years. While these allocations are enough for the initial years, it is insufficient thereafter. Management is confident in its ability to acquire the needed port allocation as it expects several regional projects with significant port allocations to become delayed or cancelled. Recall, the deal is subject to Ridley receiving the Federal Government approval for addition of a fourth stacker/reclaimer that will increase capacity from 24MMtpa to 30MMtpa when sufficient capacity should be available.

Carbon Creek Scoped For A Major?

By increasing the production rate, the Company has also raised the upfront capital costs significantly for the project. This would normally make financing the mine even more difficult for the junior developer, especially given that the project economics (IRR, NPV) did not increase drastically from the PEA case. That said with its larger scale at a reasonable cost, we believe the Company has made the project more attractive and palatable for a regional producer. Recall that Carbon Creek is located on the Peace River coal trend, a district which hosts several major met coal operators, including Xstrata, Anglo American, and Walter Energy. We would especially note Xstrata, which has been an active consolidator in the area (most recently with the Sukunka coal deposit). In Figure 3, we present a regional concession map highlighting Carbon Creek’s position relative to other major operators in Peace River.

Maintaining Buy (S) Recommendation, Raising Target To C$2.50: Cardero continues to aggressively develop Carbon Creek, a met coal project which is sure to receive strong consideration by regional players in the near term. We see the potential for a rerating in the event a partner is brought in on the project or the coking coal market recovers materially. While interest in the met coal space is subdued due to near-term issues, we continue to see long-term potential and note that high-quality, low-risk assets are always in demand. With a pre-feasibility in hand, we recommend CDU to investors seeking exposure to metallurgical coal in the Peace River coalfield in a high-quality development asset. Having updated our model for the PFS findings, we reiterate our Buy (S) recommendation, and increase our target to C$2.50 from C$2.40 (based on 0.50x NAV plus cash and investments). As further development hurdles are overcome, our discount would be expected to narrow.

Quelle: http://finance.yahoo.com/mbview/threadview/?&bn=ae7ec2b4-5be…

Antwort auf Beitrag Nr.: 43.729.519 von boersenbrieflemming am 19.10.12 09:09:00..ich wuerde mir nichts sehnlicher wuenschen, als endlich mal eines dieser Target Kurse zu sehen, aber kritisch bemerkt: wie haeufig wurde jemals so ein Zielkurs bisher erreicht? Und solche Ausblicke gab es schon so oft, dass ich es gar nicht mehr zaehlen kann...

Antwort auf Beitrag Nr.: 43.728.861 von gustel66 am 18.10.12 22:44:46Nabend carderos

Wehmütigkeit macht sich bei mir breit, wenn man hier liest, wie treu die Fans geblieben sind...

Obwohl der Kurs in Regionen tümpelt, die ich nie für möglich halten wollte , liest man

, liest man

12% plus gab es schon lange nicht mehr an einem Tag.

------------------------------------------------------------

Alles Gute noch für die Zukunft.

Wehmütigkeit macht sich bei mir breit, wenn man hier liest, wie treu die Fans geblieben sind...

Obwohl der Kurs in Regionen tümpelt, die ich nie für möglich halten wollte

, liest man

, liest man12% plus gab es schon lange nicht mehr an einem Tag.

------------------------------------------------------------

Alles Gute noch für die Zukunft.

Antwort auf Beitrag Nr.: 43.730.783 von gustel66 am 19.10.12 13:47:34wie haeufig wurde jemals so ein Zielkurs bisher erreicht

Ich glaube, da gibt es keine Statistik.

Ich glaube, da gibt es keine Statistik.

Antwort auf Beitrag Nr.: 43.732.285 von boersenbrieflemming am 19.10.12 19:37:34...ist wohl auch besser so, da dies sehr sehr sehr enttaeuschend waere...

Da wird gerade gekaempft. ;-)

Ask

0.66 14,000 4

0.65 15,000 6

0.64 23,000 4

0.63 12,500 11

0.61 9,500 2

Bid

0.60 37,500 4

0.59 14,000 4

0.58 28,500 11

0.57 5,000 7

0.56 8,000 5

--

Iron ore has room to rise to $125/tonne -trader

http://www.reuters.com/article/2012/10/19/markets-ironore-id…

Ask

0.66 14,000 4

0.65 15,000 6

0.64 23,000 4

0.63 12,500 11

0.61 9,500 2

Bid

0.60 37,500 4

0.59 14,000 4

0.58 28,500 11

0.57 5,000 7

0.56 8,000 5

--

Iron ore has room to rise to $125/tonne -trader

http://www.reuters.com/article/2012/10/19/markets-ironore-id…

Antwort auf Beitrag Nr.: 43.732.748 von gustel66 am 19.10.12 21:51:29Nun, die Analysten (bzw. deren Häuser) verdienen bei Finanzierungen. Cardero hat schon lange keine Financierung (mir ist da nur eine "non brokered") getätigt. Das hier nun in relativ kurzer Zeit Geld fliessen muss - das ist dem Markt bekannt.

Bei meinem "Liebling" TV sieht man ganz gut, wie positiv sich ein vernuenftiges Coverage auswirken kann. Da wurde die Aktie in Grund und Boden gelabert und dann schoss sie von 0,7x CAD auf knapp 1,30 CAD wieder hoch - auch wenn das Umfeld alles andere als optimal war/ist.

Es gibt genug Argumente Cardero jetzt als guenstigen Kauf zu sehen, aber auch Argumente dagegen. Wie immer.

Bei meinem "Liebling" TV sieht man ganz gut, wie positiv sich ein vernuenftiges Coverage auswirken kann. Da wurde die Aktie in Grund und Boden gelabert und dann schoss sie von 0,7x CAD auf knapp 1,30 CAD wieder hoch - auch wenn das Umfeld alles andere als optimal war/ist.

Es gibt genug Argumente Cardero jetzt als guenstigen Kauf zu sehen, aber auch Argumente dagegen. Wie immer.

Das geht schon in die richtige Richtung. Cardero mit seiner Kohlegrube ist auch erwähnt:

Coal to Rise on Seasonal Buying

After months of declining prices, coking coal producers are struggling to remain optimistic that demand support will return soon.

.... Company news

Cardero Resource (TSX:CDU,AMEX:CDY) announced late last month that it has increased its measured and indicated resource at its Carbon Creek property in Northeast British Columbia from 166 MT to 468 MT. It also established that its initial proven and probable reserves now top 121 MT with an initial 20-year mine life.

Angus Christie, Cardero’s COO, stated, “I believed when I joined the Company that we had an opportunity to turn the Carbon Creek asset into one of the largest producing, lowest cost operators in the region. This report demonstrates that we are in position to turn our expectations into reality and establish this asset as the benchmark against which other developments in the region will be evaluated.”

http://resourceinvestingnews.com/44397-coal-to-rise-on-seaso…

Coal to Rise on Seasonal Buying

After months of declining prices, coking coal producers are struggling to remain optimistic that demand support will return soon.

.... Company news

Cardero Resource (TSX:CDU,AMEX:CDY) announced late last month that it has increased its measured and indicated resource at its Carbon Creek property in Northeast British Columbia from 166 MT to 468 MT. It also established that its initial proven and probable reserves now top 121 MT with an initial 20-year mine life.

Angus Christie, Cardero’s COO, stated, “I believed when I joined the Company that we had an opportunity to turn the Carbon Creek asset into one of the largest producing, lowest cost operators in the region. This report demonstrates that we are in position to turn our expectations into reality and establish this asset as the benchmark against which other developments in the region will be evaluated.”

http://resourceinvestingnews.com/44397-coal-to-rise-on-seaso…

Antwort auf Beitrag Nr.: 43.736.964 von boersenbrieflemming am 22.10.12 12:21:36im Uebrigen habe ich immer noch keinen Explorer gefunden, der guenstiger produzieren kann. ... Das nur zum Thema Benchmark.

Die ist wieder auf dem Radar:

Indico Announces Granting of Stock Options

VANCOUVER, BRITISH COLUMBIA, Oct 22, 2012 (Menafn - Marketwire via COMTEX) --Indico Resources Ltd. ("Indico" or the "Company") (otcqx:IDIFF) announces the granting of incentive stock options to certain of its directors, officers and consultants to purchase up to an aggregate of 2,750,000 common shares in its capital stock at a price of 0.24 per share, exercisable for a period of two years.

http://www.menafn.com/menafn/37f3676a-10db-45d7-b8d6-eac752b…

Indico Announces Granting of Stock Options

VANCOUVER, BRITISH COLUMBIA, Oct 22, 2012 (Menafn - Marketwire via COMTEX) --Indico Resources Ltd. ("Indico" or the "Company") (otcqx:IDIFF) announces the granting of incentive stock options to certain of its directors, officers and consultants to purchase up to an aggregate of 2,750,000 common shares in its capital stock at a price of 0.24 per share, exercisable for a period of two years.

http://www.menafn.com/menafn/37f3676a-10db-45d7-b8d6-eac752b…

Es ist ganz interessant etwas ueber Peabody's Quartalsbericht zu lesen:

Regarding Peabody's Australia platform, the company is settling its available fourth quarter metallurgical coal contracts largely in line with benchmark settlements of $170 per tonne for high quality hard coking coal and $125 per tonne for low-vol PCI. The company continues to target 2012 metallurgical coal sales of 13 to 14 million tons and seaborne thermal coal sales of 11 to 12 million tons. Peabody now targets 2012 Australia sales of 31 to 33 million tons compared with 2011 sales of 25 million tons.

Read more here: http://www.sacbee.com/2012/10/22/4928842/peabody-energy-anno…

Regarding Peabody's Australia platform, the company is settling its available fourth quarter metallurgical coal contracts largely in line with benchmark settlements of $170 per tonne for high quality hard coking coal and $125 per tonne for low-vol PCI. The company continues to target 2012 metallurgical coal sales of 13 to 14 million tons and seaborne thermal coal sales of 11 to 12 million tons. Peabody now targets 2012 Australia sales of 31 to 33 million tons compared with 2011 sales of 25 million tons.

Read more here: http://www.sacbee.com/2012/10/22/4928842/peabody-energy-anno…

Das Thema Financing hat sich erst einmal erledigt.Sie machen es halb/halb und hängt am Haken von Sprott.

---

Cardero to raise $10-million, borrow $10-million

Cardero Resource Corp (C:CDU)

Shares Issued 93,353,454

Last Close 10/22/2012 $0.59

Tuesday October 23 2012 - News Release

Mr. Michael Hunter reports

CARDERO ANNOUNCES NON-BROKERED PRIVATE PLACEMENT AND DEBT FINANCING

Cardero Resource Corp. has arranged a non-brokered private placement for gross proceeds of up to $10-million. The Company has also arranged a CAD 10,000,000 bridge-loan credit facility with Sprott Resource Lending Partnership ("Sprott").

Non-brokered Private Placement

The Company has arranged a non-brokered private placement of up to 18,181,818 common shares at a price of CAD 0.55 per share for gross proceeds of up to CAD 10,000,000 (the "Offering"). All common shares issued in the Offering will have a hold period in Canada of four months from the closing of the Offering. All common shares issued in the United States will be subject to resale restrictions under U.S. federal and state securities laws. The Company may pay a finder's fee in connection with a portion of the Offering equal to 5% in cash plus warrants to purchase up to 5% of the common shares placed at a price of CAD 0.60 for one year. Certain insiders of the Company will participate in the Offering. The Company has determined that there are exemptions available from the various requirements of Multilateral Instrument 61-101 for the issuance of any common shares issued to insiders. There will not be any change of control as a result of the Offering.

The net proceeds from the Offering are intended to be used to fund the preparation of the bankable feasibility study, coal quality analyses and environmental baseline work on the Carbon Creek metallurgical coal project, as well as ongoing work programs and property payments on the Sheini Hills iron ore project in Ghana and for general working capital.

Completion of the Offering is subject to the acceptance for filing thereof by the Toronto Stock Exchange ("TSX") and approval by the NYSE-MKT.

Bridge-loan Financing through Sprott

The Company also announces that it has executed a term sheet for a CAD 10,000,000 bridge-loan credit facility agreement with Sprott.

The term sheet provides for a facility in the principal amount of CAD 10,000,000 at an interest rate of 12 per cent per annum, compounded and payable monthly, and due and payable in full on or before the first anniversary of the closing of the loan financing. Provided that the loan is in good standing and that Sprott is satisfied with the value of the security, the repayment of the loan may be extended for an additional year for a cash fee of 3% of the outstanding amount if the loan balance is CAD 7,500,000 or more or 2% if less. In consideration of the facility, the Company will, on closing, pay to Sprott a bonus payment equal to 3% of the loan amount, such payment to be satisfied by the issuance of common shares at a deemed price of CAD 0.55. The bonus shares will be subject to a hold period of four months from the date of issuance. A structuring fee in the amount of CAD 100,000 has also been paid to Sprott. As security for the loan, Sprott will be granted a first charge over the Company's shares of Cardero Coal Ltd. ("Cardero Coal"). In addition, the loan will be guaranteed by Cardero Coal, which will pledge all of its interest in the Carbon Creek metallurgical coal project and related assets to secure such guarantee.

Proceeds of the facility will be applied towards the ongoing development of the Carbon Creek metallurgical coal project, including property payments and work related to the ongoing bankable feasibility study, and for working capital.

Closing of the facility is subject to the satisfactory completion of due diligence by Sprott, the settlement and execution of formal documentation by all parties, the acceptance for filing by the TSX and approval of the NYSE-MKT with respect to the issuance of the bonus shares, and the completion of the Offering.

---

Cardero to raise $10-million, borrow $10-million

Cardero Resource Corp (C:CDU)

Shares Issued 93,353,454

Last Close 10/22/2012 $0.59

Tuesday October 23 2012 - News Release

Mr. Michael Hunter reports

CARDERO ANNOUNCES NON-BROKERED PRIVATE PLACEMENT AND DEBT FINANCING

Cardero Resource Corp. has arranged a non-brokered private placement for gross proceeds of up to $10-million. The Company has also arranged a CAD 10,000,000 bridge-loan credit facility with Sprott Resource Lending Partnership ("Sprott").

Non-brokered Private Placement

The Company has arranged a non-brokered private placement of up to 18,181,818 common shares at a price of CAD 0.55 per share for gross proceeds of up to CAD 10,000,000 (the "Offering"). All common shares issued in the Offering will have a hold period in Canada of four months from the closing of the Offering. All common shares issued in the United States will be subject to resale restrictions under U.S. federal and state securities laws. The Company may pay a finder's fee in connection with a portion of the Offering equal to 5% in cash plus warrants to purchase up to 5% of the common shares placed at a price of CAD 0.60 for one year. Certain insiders of the Company will participate in the Offering. The Company has determined that there are exemptions available from the various requirements of Multilateral Instrument 61-101 for the issuance of any common shares issued to insiders. There will not be any change of control as a result of the Offering.

The net proceeds from the Offering are intended to be used to fund the preparation of the bankable feasibility study, coal quality analyses and environmental baseline work on the Carbon Creek metallurgical coal project, as well as ongoing work programs and property payments on the Sheini Hills iron ore project in Ghana and for general working capital.

Completion of the Offering is subject to the acceptance for filing thereof by the Toronto Stock Exchange ("TSX") and approval by the NYSE-MKT.

Bridge-loan Financing through Sprott

The Company also announces that it has executed a term sheet for a CAD 10,000,000 bridge-loan credit facility agreement with Sprott.

The term sheet provides for a facility in the principal amount of CAD 10,000,000 at an interest rate of 12 per cent per annum, compounded and payable monthly, and due and payable in full on or before the first anniversary of the closing of the loan financing. Provided that the loan is in good standing and that Sprott is satisfied with the value of the security, the repayment of the loan may be extended for an additional year for a cash fee of 3% of the outstanding amount if the loan balance is CAD 7,500,000 or more or 2% if less. In consideration of the facility, the Company will, on closing, pay to Sprott a bonus payment equal to 3% of the loan amount, such payment to be satisfied by the issuance of common shares at a deemed price of CAD 0.55. The bonus shares will be subject to a hold period of four months from the date of issuance. A structuring fee in the amount of CAD 100,000 has also been paid to Sprott. As security for the loan, Sprott will be granted a first charge over the Company's shares of Cardero Coal Ltd. ("Cardero Coal"). In addition, the loan will be guaranteed by Cardero Coal, which will pledge all of its interest in the Carbon Creek metallurgical coal project and related assets to secure such guarantee.

Proceeds of the facility will be applied towards the ongoing development of the Carbon Creek metallurgical coal project, including property payments and work related to the ongoing bankable feasibility study, and for working capital.

Closing of the facility is subject to the satisfactory completion of due diligence by Sprott, the settlement and execution of formal documentation by all parties, the acceptance for filing by the TSX and approval of the NYSE-MKT with respect to the issuance of the bonus shares, and the completion of the Offering.

dat gibbt neue tiefs

Antwort auf Beitrag Nr.: 43.742.080 von AMUN666 am 23.10.12 15:20:43Wahnsinn! Sprott holt sich die Verluste aus Aktienverlusten wieder rein!

12% bei der Zinslage... Spread bei gut 1100 bp! Respekt!

Weitere 18 Mio. Aktien. Glückwunsch!

12% bei der Zinslage... Spread bei gut 1100 bp! Respekt!

Weitere 18 Mio. Aktien. Glückwunsch!

Antwort auf Beitrag Nr.: 43.742.125 von Sugar2000 am 23.10.12 15:31:35Das einzig Positive ist, dass das Thema damit erst einmal durch ist.

Nur einmal zur Info:

Ask

0.60 14,500 5

0.59 16,000 4

0.58 12,500 5

0.57 8,500 4

0.56 4,000 3

Bid

0.55 18,500 7

0.54 13,500 10

0.53 26,500 6

0.52 32,100 6

0.51 10,000 4

Ask

0.60 14,500 5

0.59 16,000 4

0.58 12,500 5

0.57 8,500 4

0.56 4,000 3

Bid

0.55 18,500 7

0.54 13,500 10

0.53 26,500 6

0.52 32,100 6

0.51 10,000 4

Antwort auf Beitrag Nr.: 43.742.125 von Sugar2000 am 23.10.12 15:31:35Eigentlich bekommt Sprott sogar 15%, 12% + 3% Cash Fee (heftig)

Antwort auf Beitrag Nr.: 43.742.700 von Tomy_HH am 23.10.12 17:13:21Hätte schlimmer kommen können. Immerhin ist überhaupt jemand bereit diesen Artisten ohne jegliche Sicherheiten Geld zu leihen. Hoffen wir dass es bis Mitte nächsten Jahres reicht und die Weltuntergangsstimmung im Explorerbeich dann auch vorbei ist.

Stefan

Stefan

Antwort auf Beitrag Nr.: 43.743.031 von Stefan0310 am 23.10.12 18:10:09Nun, Cardero Coal ist die Sicherheit. Aber wie gesagt, jetzt ist erst einmal Ruhe.

Price Size Orders

Ask

0.61 18,500 4

0.60 14,500 5

0.59 10,500 4

0.58 10,000 6

0.57 8,000 5

Bid

0.56 21,000 2

0.55 56,500 12

0.54 13,000 10

0.53 16,500 5

0.52 22,100 5

Ask

0.61 18,500 4

0.60 14,500 5

0.59 10,500 4

0.58 10,000 6

0.57 8,000 5

Bid

0.56 21,000 2

0.55 56,500 12

0.54 13,000 10

0.53 16,500 5

0.52 22,100 5

SK:

CDU: 0.57 CAD -0.02 -3.4% 226.4k

CDY: 0.5708 USD -0.0292 -4.9% 185.5k

--

Das OB hat zumindest gut mitgezogen.

CDU: 0.57 CAD -0.02 -3.4% 226.4k

CDY: 0.5708 USD -0.0292 -4.9% 185.5k

--

Das OB hat zumindest gut mitgezogen.

Zum Nachschlag ....

Peabody Energy's Future Burns Bright

..

Peabody management sees early signs of optimism regarding global coal markets for 2013. China's steel production has begun to increase in October. Chinese mine closures have resulted in 150 million tons of annualized coal production cuts from small and inefficient mines.

Metallurgical-coal markets seem to have bottomed out as current weak pricing for hard coking and low-volume pulverized coal injection (PCI) met coal is generating output cuts. In the U.S., management believes we could see more Powder River Basin (PRB) output discipline if pricing does not move faster than demand.

..

http://online.barrons.com/article/SB500014240527487043779045…

--

Sollte das die Talsohle gewesen sein ...

Peabody Energy's Future Burns Bright

..

Peabody management sees early signs of optimism regarding global coal markets for 2013. China's steel production has begun to increase in October. Chinese mine closures have resulted in 150 million tons of annualized coal production cuts from small and inefficient mines.

Metallurgical-coal markets seem to have bottomed out as current weak pricing for hard coking and low-volume pulverized coal injection (PCI) met coal is generating output cuts. In the U.S., management believes we could see more Powder River Basin (PRB) output discipline if pricing does not move faster than demand.

..

http://online.barrons.com/article/SB500014240527487043779045…

--

Sollte das die Talsohle gewesen sein ...

BAR

15 Min Video auf YouTube

22.10.2012

Balmoral Resources Corporate Presentation with President & CEO Darin Wagner

http://www.youtube.com/watch?v=NPueO5Z27cg

15 Min Video auf YouTube

22.10.2012

Balmoral Resources Corporate Presentation with President & CEO Darin Wagner

http://www.youtube.com/watch?v=NPueO5Z27cg

Cardero Resource Moving Coal by Barge

Lynsey Kitching

A main focus of the Cardero Resource Corporation was how they were going to actually move their coal. The property will be developing 40 km west of Hudson’s Hope. Near the southern shore of Williston Lake, which is a big advantage for the project.

Although coal was first discovered there in the early twentieth century, the first significant exploration was done in the early 70s. Coincidentally, back then, all of the heavy equipment was brought in by barge and landing sites are still evident on the reservoir. Angus Chris, representative for Cardero said, “There has been an increase in resource base from the 100 million tonnes defined in 1975, to the now 700 million tonnes and counting.”

The products extracted will be hard-coking coal and a semi—soft or PCI product. This gives the company the ability to blend products, and have a consistent product profile. These types of coal will be extracted using three mining methods: Surface, Highwall and Contour mining. a Also included in this proposal is Room and Pillar mining, a form of underground mining. Chris said, “Surface mining will comprise about 55 percent of reserve base, and underground mining will be about 42 percent.”

The coal, after being mined will be loaded onto a barge containing about 15,000–17,000 tonnes of material and will travel 174 km to Mackenzie. The options to transport the coal were between trucking or barging the coal from the site. Chris said, “At first it didn’t seem practical to take coal from the Carbon Creek and barge it 173 km to Mackenzie, or economically feasible,” he continued, “However with a truck, it would be a 64 km road haul, as well as creating a tunnel through the mountain range, anywhere from one to four km in length. As far as capital is concerned, that just didn’t make sense.”

The company decided to go by water. A question that arose around barging is how well it can be done through the winter months. Chris said, “Yes it can be done year round. The max ice thickness is 36 inches on Carbon Creek. At first we will be barging about once a week, but in full production, we will be barging every one to one and a half days. We will be able to maintain an open channel throughout the year. The barge we are going to build will have ice-breaking capabilities.”

Chris continued, “Once we started getting into the barging option and the practicality of it, we found that it’s very standard technology worldwide. Coal will be put onto self discharging barges, and travel to Mackenzie, where it will be stockpiled or directly loaded onto CN trains to Prince George.”

The project will generate anywhere between 850–900 direct jobs at the mine site, and take about six years to get to full production. Formal consultations with First Nations and communities will commence very shortly. Chris said, “There will be plenty of opportunity for local recruitment. We will be developing the skills, and training people in that period.”

http://www.tumblerridgenews.com/index.php/news/9706-carderom…

Lynsey Kitching

A main focus of the Cardero Resource Corporation was how they were going to actually move their coal. The property will be developing 40 km west of Hudson’s Hope. Near the southern shore of Williston Lake, which is a big advantage for the project.

Although coal was first discovered there in the early twentieth century, the first significant exploration was done in the early 70s. Coincidentally, back then, all of the heavy equipment was brought in by barge and landing sites are still evident on the reservoir. Angus Chris, representative for Cardero said, “There has been an increase in resource base from the 100 million tonnes defined in 1975, to the now 700 million tonnes and counting.”

The products extracted will be hard-coking coal and a semi—soft or PCI product. This gives the company the ability to blend products, and have a consistent product profile. These types of coal will be extracted using three mining methods: Surface, Highwall and Contour mining. a Also included in this proposal is Room and Pillar mining, a form of underground mining. Chris said, “Surface mining will comprise about 55 percent of reserve base, and underground mining will be about 42 percent.”

The coal, after being mined will be loaded onto a barge containing about 15,000–17,000 tonnes of material and will travel 174 km to Mackenzie. The options to transport the coal were between trucking or barging the coal from the site. Chris said, “At first it didn’t seem practical to take coal from the Carbon Creek and barge it 173 km to Mackenzie, or economically feasible,” he continued, “However with a truck, it would be a 64 km road haul, as well as creating a tunnel through the mountain range, anywhere from one to four km in length. As far as capital is concerned, that just didn’t make sense.”

The company decided to go by water. A question that arose around barging is how well it can be done through the winter months. Chris said, “Yes it can be done year round. The max ice thickness is 36 inches on Carbon Creek. At first we will be barging about once a week, but in full production, we will be barging every one to one and a half days. We will be able to maintain an open channel throughout the year. The barge we are going to build will have ice-breaking capabilities.”

Chris continued, “Once we started getting into the barging option and the practicality of it, we found that it’s very standard technology worldwide. Coal will be put onto self discharging barges, and travel to Mackenzie, where it will be stockpiled or directly loaded onto CN trains to Prince George.”

The project will generate anywhere between 850–900 direct jobs at the mine site, and take about six years to get to full production. Formal consultations with First Nations and communities will commence very shortly. Chris said, “There will be plenty of opportunity for local recruitment. We will be developing the skills, and training people in that period.”

http://www.tumblerridgenews.com/index.php/news/9706-carderom…

Antwort auf Beitrag Nr.: 43.746.911 von boersenbrieflemming am 24.10.12 15:28:24700 million tonnes and counting

Solche Zahlen wuerde ich lieber woanders lesen und nicht nur in einer kleinen Provinzzeitung .... Naaaaancy .....

--

Mein groesstes Problem mit Carbon Creek (geplanter Tunnel) hat sich somit auch erledigt.

Solche Zahlen wuerde ich lieber woanders lesen und nicht nur in einer kleinen Provinzzeitung .... Naaaaancy .....

--

Mein groesstes Problem mit Carbon Creek (geplanter Tunnel) hat sich somit auch erledigt.

Ask

0.60 10,500 5

0.59 9,000 2

0.58 6,500 5

0.57 7,500 5

0.56 4,500 1

Bid

0.55 29,500 5

0.54 25,000 12

0.53 18,500 6

0.52 27,600 6

0.51 1,000 1

0.60 10,500 5

0.59 9,000 2

0.58 6,500 5

0.57 7,500 5

0.56 4,500 1

Bid

0.55 29,500 5

0.54 25,000 12

0.53 18,500 6

0.52 27,600 6

0.51 1,000 1

ABS

Oct. 24, 2012

Abzu Announces Closing of Non-Brokered Private Placement and Announces Shares for Debt Transaction

http://tmx.quotemedia.com/article.php?newsid=55276491&qm_sym…

Oct. 24, 2012

Abzu Announces Closing of Non-Brokered Private Placement and Announces Shares for Debt Transaction

http://tmx.quotemedia.com/article.php?newsid=55276491&qm_sym…

Auch bei den Analysten scheiden sich die Geister:

Desjardins Securities Cuts Price Target on Cardero Resources Corp. (CDY)

Posted by Seth Barnet on Oct 24th, 2012 // No Comments

Cardero Resources Corp. (NYSEAMEX: CDY) had its price target lowered by Desjardins Securities from $1.25 to $0.90 in a research note released on Wednesday morning. They currently have a hold rating on the stock.

Separately, analysts at Paradigm Research raised their price target on shares of Cardero Resources Corp. from $1.50 to $1.85 in a research note to investors on Tuesday, September 25th. They now have a speculative buy rating on the stock.

Cardero Resources Corp. traded down 1.89% on Wednesday, hitting $0.56. Cardero Resources Corp. has a 1-year low of $0.54 and a 1-year high of $1.56. The company’s market cap is $52.3 million.

Cardero Resource Corp. (Cardero) is an exploration-stage company. The Company holds, or has rights to acquire, interests in mineral properties in Argentina, Mexico, Peru, the United States, Ghana and Canada.

http://www.jagsreport.com/2012/10/desjardins-securities-cuts…

--

Ich sehe bein der CDU derzeit eher ein kommunikatives Problem - Carbon Creek fliegt noch zu weit unterhalb des Radars.

Desjardins Securities Cuts Price Target on Cardero Resources Corp. (CDY)

Posted by Seth Barnet on Oct 24th, 2012 // No Comments

Cardero Resources Corp. (NYSEAMEX: CDY) had its price target lowered by Desjardins Securities from $1.25 to $0.90 in a research note released on Wednesday morning. They currently have a hold rating on the stock.

Separately, analysts at Paradigm Research raised their price target on shares of Cardero Resources Corp. from $1.50 to $1.85 in a research note to investors on Tuesday, September 25th. They now have a speculative buy rating on the stock.

Cardero Resources Corp. traded down 1.89% on Wednesday, hitting $0.56. Cardero Resources Corp. has a 1-year low of $0.54 and a 1-year high of $1.56. The company’s market cap is $52.3 million.

Cardero Resource Corp. (Cardero) is an exploration-stage company. The Company holds, or has rights to acquire, interests in mineral properties in Argentina, Mexico, Peru, the United States, Ghana and Canada.

http://www.jagsreport.com/2012/10/desjardins-securities-cuts…

--

Ich sehe bein der CDU derzeit eher ein kommunikatives Problem - Carbon Creek fliegt noch zu weit unterhalb des Radars.

WML (gibt cash):

"Crosshair to Acquire 2,600 Square Miles of Prospective Uranium Properties in Argentina

.. The consideration for the acquisition of the properties is payments to Wealth Minerals of CDN$1.0 million in cash and issuances to Wealth Minerals of one million Crosshair common shares. The cash payments and share issuances will be done over a two year period. In addition, Wealth Minerals retains a 1% yellowcake royalty on all uranium production and a 1% NSR royalty on all other minerals. ..."

http://www.stockhouse.com/news/canadianreleasesdetail.aspx?n…

"Crosshair to Acquire 2,600 Square Miles of Prospective Uranium Properties in Argentina

.. The consideration for the acquisition of the properties is payments to Wealth Minerals of CDN$1.0 million in cash and issuances to Wealth Minerals of one million Crosshair common shares. The cash payments and share issuances will be done over a two year period. In addition, Wealth Minerals retains a 1% yellowcake royalty on all uranium production and a 1% NSR royalty on all other minerals. ..."

http://www.stockhouse.com/news/canadianreleasesdetail.aspx?n…

Corvus Gold JV Partner Completes 2012 Exploration Drilling Program, Awaits Gold Production Numbers, Terra Project, Alaska

http://www.marketwatch.com/story/corvus-gold-jv-partner-comp…

http://www.marketwatch.com/story/corvus-gold-jv-partner-comp…

Jennings landete gestern in meiner Mailbox - mit zwei zentralen Aussagen:

Considering recent comparable acquisition multiples in Peace River, we believe that under an M&A scenario, Cardero could be worth up to C$3.00 per share based on its 75% attributable interest of M&I resource.

..

We are reinitiating coverage on Cardero Resource Corp. with a SPECULATIVE BUY recommendation and 12-month target price of C$1.85 per share.

..

EMERGING PURE-PLAY IN A WELL-ESTABLISHED COAL DISTRICT: SOURCE OF STABLE SUPPLY

Large resource, long mine-life: Carbon Creek development offers a potential long-life beyond 30 years and relatively low-cost production, which could transform Cardero into a significant player in the metallurgical coal seaborne export market.

Infrastructure & logistics to market: Carbon Creek, by its location, is endowed with the necessary infrastructure and cost advantaged barge-rail-port access to competitively deliver quality product to customers on a consistent basis.

Upcoming key catalysts: Obtaining conditional off- take agreements and completing the bankable feasibility study (BFS), expected in 2Q 2013.

Project financing: With the BFS underway, we believe that Carbon Creek has robust economics and potentially low permitting risk, which are likely to be very attractive to potential investors including strategics, project lenders and financial buyers.

M&A potential: The Peace River coal basin has seen over $5 billion in M&A deals completed in the last two years, mostly by new entrants. Considering recent comparable acquisition multiples in Peace River, we believe that under an M&A scenario, Cardero could be worth up to C$3.00 per share based on its 75% attributable interest of M&I resource.

Key risks: In our view, the primary risks to the Carbon Creek development are the strength of the coal market and obtaining $475 million in project funding.

Valuation: We have valued Cardero based on 1x NAV, using the DCF of unlevered free cash flow from its 75% attributable interest in the Carbon Creek project. Cardero is currently undervalued, trading at $0.13/t compared to its peer group average at $0.40/t based on EV/M&I resource.

We are re-initiating coverage on Cardero Resource Corp. with a SPECULATIVE BUY recommendation and 12-month target price of C$1.85 per share.

INVESTMENT SUMMARY

Cardero Resource Corp. (“Cardero” or the “Company”), through its 75% interest in the flagship Carbon Creek metallurgical coal project, offers investors potential long mine-life and a large expandable resource base with leverage to the premium hard coking coal (HCC) export market. Carbon Creek, by its location, is endowed with the necessary infrastructure and a cost advantaged barge-rail-port access to competitively deliver quality product to customers on a consistent basis.

Carbon Creek’s recent pre-feasibility study highlighted the significant increase in M&I resource by 180%, to 468mt, and the established maiden proven and probable reserve of 121mt, forming the baseline for an initial 20-year mine plan. Also, of equal importance is the increase in HCC composition from 35% to 60%, giving the Company greater leverage to the premium coking coal market, making the project more attractive to potential off-takers, strategic partners and potential lenders.

We believe Carbon Creek has developed a profile with robust economics and a potentially low carbon footprint, making it attractive to potential investors and easing the pathway toward environmental approval.

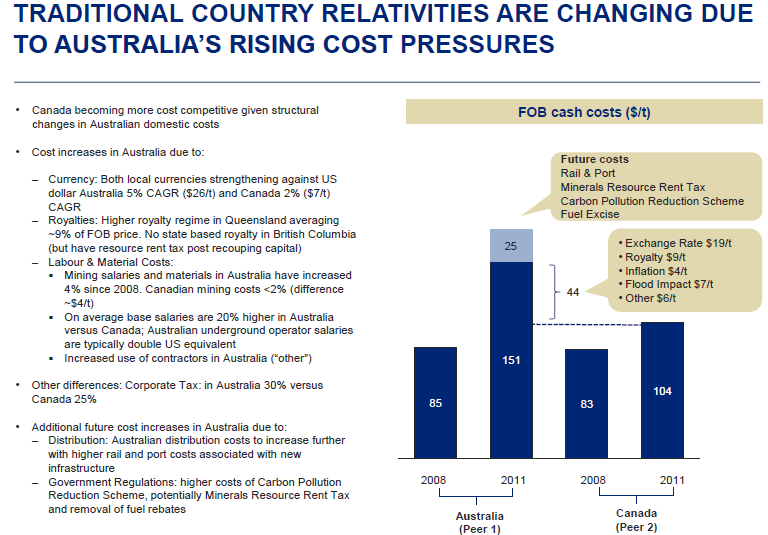

The metallurgical coal seaborne market is heavily concentrated in Australia, with control of over 50% of global export supply. However, recent events have caused a dramatic structural shift in the FOB cost structure in Australia (~$151/t in 2011), making Canada (FOB cost ~104/t) a lot more cost competitive. The Peace River Coalfield has seen a revitalization of interests, coming primarily from Anglo American and Teck Resources strategically looking to enhance their hard coking coal product offering to the seaborne market. The Peace River coal basin has also seen new entrants, by way of acquisitions, looking to grow market share of the export coal market with over $5 billion in M&A deal value completed in the last two years.

Considering recent comparable acquisition multiples in Peace River, we believe that under an M&A scenario, Cardero could be worth up to C$3.00 per share based on its 75% attributable interest of M&I resource.

We believe management has a proven track record and the necessary skillset to unlock value in the Carbon Creek project as they advance development. Key management personnel have been involved in several bulk mining deals such as the sale of First Coal, sale of an iron ore project in Brazil and the eventual Cardero/Coalhunter transaction, creating value along the way for shareholders.

In our view, the market has not ascribed much value to the upgraded M&I resource of 468mt and its underlying economically proven and probable reserve base. Based on its 75% attributable interest, Cardero is currently trading at $0.13/t compared to its peer group average of $0.40/t based on EV/M&I resource. We believe Cardero is likely to see a warranted market re-rating as it achieves key milestones such as the bankable feasibility study, which would enable the project to gain committed financing and put it on track toward completing its transformation into a coal producer, estimated in 2015.

We are reinitiating coverage on Cardero Resource Corp. with a SPECULATIVE BUY recommendation and 12-month target price of C$1.85 per share.

http://www.jenningscapital.com/reports/CDUReInitiatingCovera…

Considering recent comparable acquisition multiples in Peace River, we believe that under an M&A scenario, Cardero could be worth up to C$3.00 per share based on its 75% attributable interest of M&I resource.

..

We are reinitiating coverage on Cardero Resource Corp. with a SPECULATIVE BUY recommendation and 12-month target price of C$1.85 per share.

..

EMERGING PURE-PLAY IN A WELL-ESTABLISHED COAL DISTRICT: SOURCE OF STABLE SUPPLY

Large resource, long mine-life: Carbon Creek development offers a potential long-life beyond 30 years and relatively low-cost production, which could transform Cardero into a significant player in the metallurgical coal seaborne export market.

Infrastructure & logistics to market: Carbon Creek, by its location, is endowed with the necessary infrastructure and cost advantaged barge-rail-port access to competitively deliver quality product to customers on a consistent basis.

Upcoming key catalysts: Obtaining conditional off- take agreements and completing the bankable feasibility study (BFS), expected in 2Q 2013.

Project financing: With the BFS underway, we believe that Carbon Creek has robust economics and potentially low permitting risk, which are likely to be very attractive to potential investors including strategics, project lenders and financial buyers.

M&A potential: The Peace River coal basin has seen over $5 billion in M&A deals completed in the last two years, mostly by new entrants. Considering recent comparable acquisition multiples in Peace River, we believe that under an M&A scenario, Cardero could be worth up to C$3.00 per share based on its 75% attributable interest of M&I resource.

Key risks: In our view, the primary risks to the Carbon Creek development are the strength of the coal market and obtaining $475 million in project funding.

Valuation: We have valued Cardero based on 1x NAV, using the DCF of unlevered free cash flow from its 75% attributable interest in the Carbon Creek project. Cardero is currently undervalued, trading at $0.13/t compared to its peer group average at $0.40/t based on EV/M&I resource.

We are re-initiating coverage on Cardero Resource Corp. with a SPECULATIVE BUY recommendation and 12-month target price of C$1.85 per share.

INVESTMENT SUMMARY

Cardero Resource Corp. (“Cardero” or the “Company”), through its 75% interest in the flagship Carbon Creek metallurgical coal project, offers investors potential long mine-life and a large expandable resource base with leverage to the premium hard coking coal (HCC) export market. Carbon Creek, by its location, is endowed with the necessary infrastructure and a cost advantaged barge-rail-port access to competitively deliver quality product to customers on a consistent basis.

Carbon Creek’s recent pre-feasibility study highlighted the significant increase in M&I resource by 180%, to 468mt, and the established maiden proven and probable reserve of 121mt, forming the baseline for an initial 20-year mine plan. Also, of equal importance is the increase in HCC composition from 35% to 60%, giving the Company greater leverage to the premium coking coal market, making the project more attractive to potential off-takers, strategic partners and potential lenders.

We believe Carbon Creek has developed a profile with robust economics and a potentially low carbon footprint, making it attractive to potential investors and easing the pathway toward environmental approval.

The metallurgical coal seaborne market is heavily concentrated in Australia, with control of over 50% of global export supply. However, recent events have caused a dramatic structural shift in the FOB cost structure in Australia (~$151/t in 2011), making Canada (FOB cost ~104/t) a lot more cost competitive. The Peace River Coalfield has seen a revitalization of interests, coming primarily from Anglo American and Teck Resources strategically looking to enhance their hard coking coal product offering to the seaborne market. The Peace River coal basin has also seen new entrants, by way of acquisitions, looking to grow market share of the export coal market with over $5 billion in M&A deal value completed in the last two years.

Considering recent comparable acquisition multiples in Peace River, we believe that under an M&A scenario, Cardero could be worth up to C$3.00 per share based on its 75% attributable interest of M&I resource.

We believe management has a proven track record and the necessary skillset to unlock value in the Carbon Creek project as they advance development. Key management personnel have been involved in several bulk mining deals such as the sale of First Coal, sale of an iron ore project in Brazil and the eventual Cardero/Coalhunter transaction, creating value along the way for shareholders.

In our view, the market has not ascribed much value to the upgraded M&I resource of 468mt and its underlying economically proven and probable reserve base. Based on its 75% attributable interest, Cardero is currently trading at $0.13/t compared to its peer group average of $0.40/t based on EV/M&I resource. We believe Cardero is likely to see a warranted market re-rating as it achieves key milestones such as the bankable feasibility study, which would enable the project to gain committed financing and put it on track toward completing its transformation into a coal producer, estimated in 2015.

We are reinitiating coverage on Cardero Resource Corp. with a SPECULATIVE BUY recommendation and 12-month target price of C$1.85 per share.

http://www.jenningscapital.com/reports/CDUReInitiatingCovera…

Antwort auf Beitrag Nr.: 43.753.934 von boersenbrieflemming am 26.10.12 09:37:35Das wollte von der Jennings-Einschaetzung noch hervorheben:

"Carbon Creek development offers a potential long-life beyond 30 years" ... Das geht wieder in Richtung der 700 Mio. Tonnen, die seitens Cardero Coal in einem Provinzblatt geäußert worden sind - in der PFS wurde eine Minenlaufzeit von 20 Jahren dargestellt.

"Carbon Creek development offers a potential long-life beyond 30 years" ... Das geht wieder in Richtung der 700 Mio. Tonnen, die seitens Cardero Coal in einem Provinzblatt geäußert worden sind - in der PFS wurde eine Minenlaufzeit von 20 Jahren dargestellt.

Antwort auf Beitrag Nr.: 43.754.643 von boersenbrieflemming am 26.10.12 11:46:36Jaja, und was hat Cardero wieder an Jennings gezahlt, damit die das schreiben?

Antwort auf Beitrag Nr.: 43.754.797 von Sugar2000 am 26.10.12 12:23:42

http://www.cardero.com/s/contact.asp

Ich bin mit sicher Du bekommst da Auskunft, die kannst Du dann hier fuer alle einstellen.

http://www.cardero.com/s/contact.asp

Ich bin mit sicher Du bekommst da Auskunft, die kannst Du dann hier fuer alle einstellen.

Ask

0.63 2,000 2

0.61 9,500 2

0.59 10,000 2

0.58 6,000 4

0.57 20,000 7

Bid

0.54 18,000 7

0.53 34,000 5

0.52 26,600 5

0.51 5,000 2

0.50 42,500 3

0.63 2,000 2

0.61 9,500 2

0.59 10,000 2

0.58 6,000 4

0.57 20,000 7

Bid

0.54 18,000 7

0.53 34,000 5

0.52 26,600 5

0.51 5,000 2

0.50 42,500 3

Davon ein wenig mehr und Carderos Carbon Creek in Radarhoehe.

Is Coal Ready for Comeback?

http://resourceinvestingnews.com/44992-is-coal-ready-for-com…

SK

CDU: 0.56 CAD +0.01 1.8% 47.3k

CDY: 0.57 USD +0.02 3.6% 66.5k

Is Coal Ready for Comeback?

http://resourceinvestingnews.com/44992-is-coal-ready-for-com…

SK

CDU: 0.56 CAD +0.01 1.8% 47.3k

CDY: 0.57 USD +0.02 3.6% 66.5k

Antwort auf Beitrag Nr.: 43.758.104 von gustel66 am 27.10.12 13:40:30Empfehlungen mit irgendwelchen Kurszielen schreiben

Wenn Du immer zu ueber 60% richtig liegst, dann mache gleich einen kostenpflichtigen Newsletter draus.

Wenn Du immer zu ueber 60% richtig liegst, dann mache gleich einen kostenpflichtigen Newsletter draus.

Ich hatte gerde eine Zusammenstellung der unterschiedlichen Empfehlungen gefunden.

Jennings Capital Gives Speculative Buy Rating to Cardero Resources Corp. (CDY)

Posted by Scotty Dyson on Oct 26th, 2012 // No Comments

Jennings Capital reissued their speculative buy rating on shares of Cardero Resources Corp. (NYSEAMEX: CDY) in a research report released on Friday morning. Jennings Capital currently has a $1.85 price target on the stock.

Other equities research analysts have also recently issued reports about the stock. Analysts at Desjardins Securities cut their price target on shares of Cardero Resources Corp. from $1.25 to $0.90 in a research note to investors on Wednesday. They now have a hold rating on the stock. Separately, analysts at Paradigm Research raised their price target on shares of Cardero Resources Corp. from $1.50 to $1.85 in a research note to investors on Tuesday, September 25th. They now have a speculative buy rating on the stock.

Shares of Cardero Resources Corp. traded up 3.64% during mid-day trading on Friday, hitting $0.57. Cardero Resources Corp. has a 52 week low of $0.54 and a 52 week high of $1.56. The company’s market cap is $53.2 million.

Cardero Resource Corp. (Cardero) is an exploration-stage company. The Company holds, or has rights to acquire, interests in mineral properties in Argentina, Mexico, Peru, the United States, Ghana and Canada.

http://www.jagsreport.com/2012/10/jennings-capital-gives-spe…

Vieles wird auch davon abhängen, wie die Company nun weiter Carbon Creek und Sheini kommuniziert. Zu Sheini erwarte ich bald eine erste Ressourcenschaetzung und bei Carbon Creek scheinen sie ja die Resourcen schnell zu erweitern.

BL

Jennings Capital Gives Speculative Buy Rating to Cardero Resources Corp. (CDY)

Posted by Scotty Dyson on Oct 26th, 2012 // No Comments

Jennings Capital reissued their speculative buy rating on shares of Cardero Resources Corp. (NYSEAMEX: CDY) in a research report released on Friday morning. Jennings Capital currently has a $1.85 price target on the stock.

Other equities research analysts have also recently issued reports about the stock. Analysts at Desjardins Securities cut their price target on shares of Cardero Resources Corp. from $1.25 to $0.90 in a research note to investors on Wednesday. They now have a hold rating on the stock. Separately, analysts at Paradigm Research raised their price target on shares of Cardero Resources Corp. from $1.50 to $1.85 in a research note to investors on Tuesday, September 25th. They now have a speculative buy rating on the stock.

Shares of Cardero Resources Corp. traded up 3.64% during mid-day trading on Friday, hitting $0.57. Cardero Resources Corp. has a 52 week low of $0.54 and a 52 week high of $1.56. The company’s market cap is $53.2 million.

Cardero Resource Corp. (Cardero) is an exploration-stage company. The Company holds, or has rights to acquire, interests in mineral properties in Argentina, Mexico, Peru, the United States, Ghana and Canada.

http://www.jagsreport.com/2012/10/jennings-capital-gives-spe…

Vieles wird auch davon abhängen, wie die Company nun weiter Carbon Creek und Sheini kommuniziert. Zu Sheini erwarte ich bald eine erste Ressourcenschaetzung und bei Carbon Creek scheinen sie ja die Resourcen schnell zu erweitern.

BL

Statt nun endlich einmal die Maiden Resource von Sheini zu bekommen, haben die in Ghana längst bekanntes in einen Artikel gepackt.. :-)

Accra, Oct. 29, GNA - Cardero Resource Corporation and Emmaland Ghana Limited on Monday announced receipt of the final batch of high-grade drill results from Phase I drilling at the Company's Sheini Hills Iron Project in north eastern Ghana, which is positive and encouraging.

The Phase I drill programme was completed in August 2012 and all results have been received in full.

"We are delighted to have completed what was a very successful Phase I exploration and drill program at Sheini," Mr Michael Hunter, Cardero's President and CEO, stated in a statement to the Ghana News Agency in Accra.

http://www.ghananewsagency.org/details/Economics/Drill-resul…

Accra, Oct. 29, GNA - Cardero Resource Corporation and Emmaland Ghana Limited on Monday announced receipt of the final batch of high-grade drill results from Phase I drilling at the Company's Sheini Hills Iron Project in north eastern Ghana, which is positive and encouraging.

The Phase I drill programme was completed in August 2012 and all results have been received in full.

"We are delighted to have completed what was a very successful Phase I exploration and drill program at Sheini," Mr Michael Hunter, Cardero's President and CEO, stated in a statement to the Ghana News Agency in Accra.

http://www.ghananewsagency.org/details/Economics/Drill-resul…

Price Size Orders

Ask

0.64 10,500 2

0.63 1,500 1

0.61 9,500 2

0.59 6,500 3

0.58 7,000 2

Bid

0.57 3,500 2

0.56 15,500 3

0.55 14,000 2

0.54 8,500 2

0.53 21,500 2

Ask

0.64 10,500 2

0.63 1,500 1

0.61 9,500 2

0.59 6,500 3

0.58 7,000 2

Bid

0.57 3,500 2

0.56 15,500 3

0.55 14,000 2

0.54 8,500 2

0.53 21,500 2

Die neue Praesentation ist draussen (Basis war wohl Feb. 2011)

CARBON CREEK METALLURGICAL COAL DEPOSIT

Advanced Mine Development Project

Economically robust Prefeasibility Study

468Mt Measured & Indicated Resources

Including 121 Mt initial Reserve

Largest single resource in Peace River coalfield

Potentially largest single producer in coalfield

Potentially lowest cost producer

Existing infrastructure (power, port & rail)

Stable political environment

Cardero holds 100% working interest

• Subject to 25% NPI, payable to a private Alberta company

Auf Seite 6 werden 700 Mt kommuniziert (teilw. unclassified)

http://www.cardero.com/i/pdf/ppt/CorporatePresentation.pdf

CARBON CREEK METALLURGICAL COAL DEPOSIT

Advanced Mine Development Project

Economically robust Prefeasibility Study

468Mt Measured & Indicated Resources

Including 121 Mt initial Reserve

Largest single resource in Peace River coalfield

Potentially largest single producer in coalfield

Potentially lowest cost producer

Existing infrastructure (power, port & rail)

Stable political environment

Cardero holds 100% working interest

• Subject to 25% NPI, payable to a private Alberta company

Auf Seite 6 werden 700 Mt kommuniziert (teilw. unclassified)

http://www.cardero.com/i/pdf/ppt/CorporatePresentation.pdf

Aktien New York Ausblick

Weiter geschlossen wegen Hurrikan 'Sandy'

http://www.wallstreet-online.de/nachricht/5034732-aktien-new…

In Toronto weiter sehr zäh:

Ask

0.60 500 1

0.59 5,000 1

0.58 500 1

0.57 4,500 2

0.56 10,500 2

Bid

0.55 6,000 2

0.54 2,000 2

0.53 8,000 2

0.52 21,600 4

0.51 1,000 1

Weiter geschlossen wegen Hurrikan 'Sandy'

http://www.wallstreet-online.de/nachricht/5034732-aktien-new…

In Toronto weiter sehr zäh:

Ask

0.60 500 1

0.59 5,000 1

0.58 500 1

0.57 4,500 2

0.56 10,500 2

Bid

0.55 6,000 2

0.54 2,000 2

0.53 8,000 2

0.52 21,600 4

0.51 1,000 1

TABLE-Japan's Sept coking coal imports up 27.3 pct

30 (Reuters) - Following is a table of customs-cleared

coking coal imports for September released by Japan's Ministry

of Finance on Tuesday.

Figures are converted from yen to U.S. dollar using Japan

Customs' official conversion rate. Volumes are expressed in

tonnes.

http://af.reuters.com/article/commoditiesNews/idAFL3E8LU0QT2…

30 (Reuters) - Following is a table of customs-cleared

coking coal imports for September released by Japan's Ministry

of Finance on Tuesday.

Figures are converted from yen to U.S. dollar using Japan

Customs' official conversion rate. Volumes are expressed in

tonnes.

Country Sept Yr/Yr Sept YTD Yr/Yr

list Tonnes % $/Tonne Tonnes %

China 106,631 3,144.0 $169.61 477,255 -49.9

Mongolia - 19,105

Indonesia 1,810,808 56.8 $117.50 13,532,367 23.9

Russia 136,910 -47.2 $183.18 1,586,490 -19.5

Canada 760,463 72.5 $218.44 5,793,421 7.5

USA 384,992 69.3 $224.86 4,154,793 -3.4

Mexico - 101,545 34.0

Mozambique 21,416 $214.22 75,639

Australia 3,616,920 10.1 $187.50 28,732,081 5.5

New Zealand - 146,628 -42.0

Total 6,838,140 27.3 $174.23 54,619,324 6.8

http://af.reuters.com/article/commoditiesNews/idAFL3E8LU0QT2…

KOR

Oct. 30, 2012

Corvus Gold Discovers New 11 Kilometre Copper and Gold System at Gerfaut Project, Quebec

Highlights include: Rock samples with up to 23.6g/t Gold; and 3.9% Copper

http://tmx.quotemedia.com/article.php?newsid=55422415&qm_sym…

Oct. 30, 2012

Corvus Gold Discovers New 11 Kilometre Copper and Gold System at Gerfaut Project, Quebec

Highlights include: Rock samples with up to 23.6g/t Gold; and 3.9% Copper

http://tmx.quotemedia.com/article.php?newsid=55422415&qm_sym…

[18.02 Uhr] An US-Börsen wird Mittwoch wieder gehandelt

Die US-Börsen öffnen am Mittwoch wieder. Das teilten die Betreiber mit. Am Dienstag war der Handel ausgesetzt worden, weil die Händler wegen des stillstehenden Verkehrs nicht zur Arbeit kommen konnten. Zudem liegt die Wall Street in einer Gegend, die überflutungsgefährdet ist.

Die US-Börsen öffnen am Mittwoch wieder. Das teilten die Betreiber mit. Am Dienstag war der Handel ausgesetzt worden, weil die Händler wegen des stillstehenden Verkehrs nicht zur Arbeit kommen konnten. Zudem liegt die Wall Street in einer Gegend, die überflutungsgefährdet ist.

In Ghana werden die Sheini-Ergebnisse weiterhin abgefeiert - der Artikel ist von gestern, die Inhalte aber bekannt:

Drill results from Sheini Hills Iron Project in Ghana positive

News Date: 30th October 2012

http://www.businessghana.com/portal/news/index.php?op=getNew…

Drill results from Sheini Hills Iron Project in Ghana positive

News Date: 30th October 2012

http://www.businessghana.com/portal/news/index.php?op=getNew…

October 31, 2012

Balmoral Confirms and Expands Three High-Grade Gold Zones in Bug Lake Area, Martiniere Property, Quebec

http://news.balmoralresources.com/press-releases/balmoral-co…

Balmoral Confirms and Expands Three High-Grade Gold Zones in Bug Lake Area, Martiniere Property, Quebec

http://news.balmoralresources.com/press-releases/balmoral-co…

Price Size Orders

Ask

0.61 9,500 2

0.60 6,000 2

0.59 9,500 2

0.58 3,500 2

0.57 1,000 2

Bid

0.56 32,000 2

0.55 1,500 2

0.54 10,500 6

0.53 13,000 3

0.52 26,600 6

Ask

0.61 9,500 2

0.60 6,000 2

0.59 9,500 2

0.58 3,500 2

0.57 1,000 2

Bid

0.56 32,000 2

0.55 1,500 2

0.54 10,500 6

0.53 13,000 3

0.52 26,600 6

Das ist vom März ....

UPDATE 2-Xstrata expands Canadian coking coal operations

Thu Mar 8, 2012 9:24am GMT Print | Single Page [-] Text [+]

* Xstrata buys Sukunka deposit from Talisman

* Xstrata buys Sukunka deposit from Talisman

* To pay $500 million in cash

* Builds existing Peace River coalfield presenc

http://af.reuters.com/article/metalsNews/idAFL5E8E82KC201203…

--

Cardero hat jetzt 700 Mio. Tonnen in m&i,i - Sukunka waren 236 Mio. Tommen m&i.

Kurz darauf wurden die Japaner ins Boot geholt:

Xstrata sells 25% of its BC coal operations

http://www.canadianmanufacturing.com/fabrication/news/xstrat…

---

Wie die Zeit vergeht ...

UPDATE 2-Xstrata expands Canadian coking coal operations

Thu Mar 8, 2012 9:24am GMT Print | Single Page [-] Text [+]

* Xstrata buys Sukunka deposit from Talisman

* Xstrata buys Sukunka deposit from Talisman

* To pay $500 million in cash

* Builds existing Peace River coalfield presenc

http://af.reuters.com/article/metalsNews/idAFL5E8E82KC201203…

--

Cardero hat jetzt 700 Mio. Tonnen in m&i,i - Sukunka waren 236 Mio. Tommen m&i.

Kurz darauf wurden die Japaner ins Boot geholt:

Xstrata sells 25% of its BC coal operations

http://www.canadianmanufacturing.com/fabrication/news/xstrat…

---

Wie die Zeit vergeht ...

...und es werden nach dem Drilling wohl noch mehr Resourcen ... zudem eine gute/sehr gute PFS ..... und dann dieser Kurs ...

Ich setzte diese Meinung einmal rein, da im Basher-Thread sehr viel Unsinn, in ueblich unangenehmer Form ueber den User TMFSinchiruna verbreitet wird (der steht natuerlich Rede und Antwort) und zudem seine "Analyse" im weiteren Sinne meiner Meinung seit Veroeffentlichung der PFS (und teilw. noch weiter vorher) entspricht:

#2) On October 15, 2012 at 5:45 PM, TMFSinchiruna (94.99) wrote:

Ok... So 3 people asked me about Cardero today. I had a talk with CEO Michael Hunter last week. I became concerned after I discovered in the last quarter's filings that the company had divested the vast majority of its investment holdings in resource equities, and in the case of the Trevali shares at least at a price well beneath the recent breakout high. That was a tough pill for me to swallow, as I had viewed those holdings as a key aspect of the stock's value proposition. Because I did not see a corresponding jump in cash holdings, my next question was where on earth all that capital went to. He laid out the trailing expenditures, and with the exception of some unacceptably high G&A expenses, I chalk it up to just an expensive year of exploration and pre-feas work.

The PFS for Carbon Creek was excellent by any measure, but amid this spate of mine closures, dialed-back Capex projections, and persistently weak pricing, the market isn't giving any love to coal development projects. Same goes for Sheini, which Hunter hopes to monetize at his earliest opportunity. Please note Desjardins increased its price target on Cardero after the PFS, and I've seen a number of bullish analyst reports.

Some of the recent weakness likely attributable to technical selling after shares dropped through prior low, while the looming need to raise capital is likely spooking some.

http://caps.fool.com/Blogs/where-gold-and-silver-mines-go/76…

--

Etwas anderer Meinung bin ich bei Sheini (Eisenerz zum Aufsammeln) - hier sehe ich massives Potential (und warte auf die Maiden Resource), sehe aber keine schnelle (!) Monetarisierung des Projektes. Im Gegensatz zu ihm halte ich die G&A Expenses nicht fuer zu hoch und halte die PR bezueglich der CC PFS fuer weiterhin sehr unglücklich - das gilt auch fuer die aktuelle Unternehmensdarstellung. Die Kohlegrube halte ich fuer unterbewertet, die PFS fuer gut-sehr gut und laut Jennings waere im Fall eines M&A 3 Dollar pro Share drin, wie man auch am Beispiel Sukunka sieht - das wird aber den Markt nicht interessieren, solange der Pessimismus überwiegt. Kommt es zu einem weiter M&A in Peace River Coal Field, dann steht Cardero wieder im Focus und legt eine Rallye hin. Das hatten wir Anfang des Jahres waehrend der Xstrata-Kaeufe.

#2) On October 15, 2012 at 5:45 PM, TMFSinchiruna (94.99) wrote: