Cardero Resource Corp. (CDU) - It’s not only ore, it’s much more: Zahlen, Daten, Fakten und Diskussi - 500 Beiträge pro Seite (Seite 9)

eröffnet am 15.05.11 12:28:41 von

neuester Beitrag 31.03.22 17:25:22 von

neuester Beitrag 31.03.22 17:25:22 von

Beiträge: 4.628

ID: 1.166.193

ID: 1.166.193

Aufrufe heute: 0

Gesamt: 658.864

Gesamt: 658.864

Aktive User: 0

ISIN: CA14140U2048 · WKN: A142XA

0,1600

CAD

0,00 %

0,0000 CAD

Letzter Kurs 26.01.22 TSX Venture

Antwort auf Beitrag Nr.: 44.245.918 von GulOcram am 13.03.13 12:04:04Bonjour ,

,

Dich hat man hier aber lange nicht mehr gesehen, was? Der Anzug ist schick, der steht Dir gut. Mit Abzu bist Du auf dem fALSCHEN dAMPFER: cdu hängt seit Coalhunter nicht public ging, spätestens aber mit dem Prinzen Kosie Kwaku auf sheini hills am Hungerhaken.

Aber das ist alles halb so wild. Der uny wird noch was draus machen. Er ist sogar schon seit Anfang Februar kräftig dabei.

@King,

Du hast doch Humor, verkaufst da die ollen Kamellen von coalinvestingnews der Oma als neu und bekommst wohl von der Maultasche ein schwäbsches Fingerli. Übrigens "Finger" ist 'ne Type, der wird auch dem Schneekönig gefallen, wetten?

,

,Dich hat man hier aber lange nicht mehr gesehen, was? Der Anzug ist schick, der steht Dir gut. Mit Abzu bist Du auf dem fALSCHEN dAMPFER: cdu hängt seit Coalhunter nicht public ging, spätestens aber mit dem Prinzen Kosie Kwaku auf sheini hills am Hungerhaken.

Aber das ist alles halb so wild. Der uny wird noch was draus machen. Er ist sogar schon seit Anfang Februar kräftig dabei.

@King,

Du hast doch Humor, verkaufst da die ollen Kamellen von coalinvestingnews der Oma als neu und bekommst wohl von der Maultasche ein schwäbsches Fingerli. Übrigens "Finger" ist 'ne Type, der wird auch dem Schneekönig gefallen, wetten?

Antwort auf Beitrag Nr.: 44.246.012 von uny1989 am 13.03.13 12:21:25Mensch, zu schnell gekommen, wie so oft. Eigentlich wollte unser Ronny dem GulOcram zum Runden gratulieren!

Antwort auf Beitrag Nr.: 44.245.883 von Stefan0310 am 13.03.13 11:59:03Ich könnte mir jeden Tag selbst in den Arsch treten trotz meiner richtigen Einschätzung des CH Deals nicht die Konsequenzen gezogen zu haben.

Da bist Du nicht der einzige - ich hatte lediglich wegen der einseitigen Kohleausrictungreduziert und das Explorerdepot angepasst. Aber gut ... Blick nach vorne!

Sie liegt aber bei denjenigen die sich von ihm übers Ohr hauen ließen.

Das mag sein - ich kenne die Gruende dafuer nicht.

Da bist Du nicht der einzige - ich hatte lediglich wegen der einseitigen Kohleausrictungreduziert und das Explorerdepot angepasst. Aber gut ... Blick nach vorne!

Sie liegt aber bei denjenigen die sich von ihm übers Ohr hauen ließen.

Das mag sein - ich kenne die Gruende dafuer nicht.

Ich mache mich hier auch lieber unsichtbar. Gelegentlich schaue ich mir die kümmerlichen Reste meines Carderodepots an und beiß mir in den A. Dann binn ich auch schon wieder weg und mach was Schöneres.

Antwort auf Beitrag Nr.: 44.246.869 von boersenbrieflemming am 13.03.13 15:01:20So, so, der King hat den Coalhunter Deal also beizeiten richtig eingeschätzt. Genau wie die Liquiditätsplanung.

Schätzer kommt im Vereinigten Königreich wohl von Schwätzer.

Was man unter einer Schneesaat genau zu verstehen hat, wird Ihre Majestät in nicht all zu ferner Zukunft nachlesen können.

Bis dahin sollte sie vielleicht einmal darüber nachdenken, ihren Thread einzustampfen, zumindest ihren Lesern hier die Botschaften ihres Outperformancethreads nahe bringen.

Schätzer kommt im Vereinigten Königreich wohl von Schwätzer.

Was man unter einer Schneesaat genau zu verstehen hat, wird Ihre Majestät in nicht all zu ferner Zukunft nachlesen können.

Bis dahin sollte sie vielleicht einmal darüber nachdenken, ihren Thread einzustampfen, zumindest ihren Lesern hier die Botschaften ihres Outperformancethreads nahe bringen.

Trading Spotlight

Antwort auf Beitrag Nr.: 44.248.377 von uny1989 am 13.03.13 19:26:30Habemus Papam, der Countdown hat nicht ganz hingehauen, Spannung Ghana Turkson?

Antwort auf Beitrag Nr.: 44.248.377 von uny1989 am 13.03.13 19:26:30 der King hat den Coalhunter Deal also beizeiten richtig eingeschätzt.

Nein, ich haette nicht gedacht das der Kohlepreis so stark zurück geht. Ich haette mit Spottpreisen um 190-200 USD gerechnet - frueher liefen die Preise halbwegs konform mit der Iron Öre Entwicklung uahc das ist derzeit etwas anders.

Nein, ich haette nicht gedacht das der Kohlepreis so stark zurück geht. Ich haette mit Spottpreisen um 190-200 USD gerechnet - frueher liefen die Preise halbwegs konform mit der Iron Öre Entwicklung uahc das ist derzeit etwas anders.

Antwort auf Beitrag Nr.: 44.248.861 von boersenbrieflemming am 13.03.13 20:58:29jetzt hoere einfach mal mit de "Nibelungentreue " auf oder warst du auch in der Neono GmbH?

Es reicht- obwohl du bei Seabridge recht hast-das wird niemals finanziert...

Ich habe von beiden Firmen keine Aktie -nur Watchlist , und das seit Jahren.

Es reicht- obwohl du bei Seabridge recht hast-das wird niemals finanziert...

Ich habe von beiden Firmen keine Aktie -nur Watchlist , und das seit Jahren.

Zitat von maurer_35: jetzt hoere einfach mal mit de "Nibelungentreue " auf oder warst du auch in der Neono GmbH?

Es reicht- obwohl du bei Seabridge recht hast-das wird niemals finanziert...

Ich habe von beiden Firmen keine Aktie -nur Watchlist , und das seit Jahren.

Denkst du denn, dass man ITH "finanziert bekommt"?

Antwort auf Beitrag Nr.: 44.248.902 von maurer_35 am 13.03.13 21:05:52Spottpreise ...

@maurer_35

Ich fand den Report von BMO im Februar ganz interessant - hier werden beide Werte, die ich immer miteiander verglichen habe, gegeneiander gestellt: CAD und CDU.

http://research-ca.bmocapitalmarkets.com/documents/2C815E32-…

--

Die Bewertung ist derzeit immer aehnlich: Niedriger Sharepreis, Projektkosten finanziert durch 50% Dilution und 50% Debt. Das nur am Rande, wesentlich fand ich folgende Aussage:

"Carbon Creek is a joint venture between Cardero (75% interest and operator) and Carbon Creek Partnership (CCP, 225% interest). CCP, a private company controlled by the Burns family, is thought to be an unwilling seller."

Soetwas liest man in Analysen selten.

"GmbH"

Ich brauche keine weiteren Gesellschaften oder Beteiligungen. :-)

@maurer_35

Ich fand den Report von BMO im Februar ganz interessant - hier werden beide Werte, die ich immer miteiander verglichen habe, gegeneiander gestellt: CAD und CDU.

http://research-ca.bmocapitalmarkets.com/documents/2C815E32-…

--

Die Bewertung ist derzeit immer aehnlich: Niedriger Sharepreis, Projektkosten finanziert durch 50% Dilution und 50% Debt. Das nur am Rande, wesentlich fand ich folgende Aussage:

"Carbon Creek is a joint venture between Cardero (75% interest and operator) and Carbon Creek Partnership (CCP, 225% interest). CCP, a private company controlled by the Burns family, is thought to be an unwilling seller."

Soetwas liest man in Analysen selten.

"GmbH"

Ich brauche keine weiteren Gesellschaften oder Beteiligungen. :-)

Antwort auf Beitrag Nr.: 44.248.939 von 666-2004 am 13.03.13 21:11:14Denkst du denn, dass man ITH "finanziert bekommt"?

Nein, mit einer Capex von ca. 2 Mrd. sehr schwierig. Aber: Mit einer guten FS ist ITH ein Uebernahmekandidat

- jedenfalls sollten dann die Risiken sehr deutlich minimiert sein. Eine Machbarkeitsstudie ist Koenigsklasse.

Nein, mit einer Capex von ca. 2 Mrd. sehr schwierig. Aber: Mit einer guten FS ist ITH ein Uebernahmekandidat

- jedenfalls sollten dann die Risiken sehr deutlich minimiert sein. Eine Machbarkeitsstudie ist Koenigsklasse.

Antwort auf Beitrag Nr.: 44.249.289 von boersenbrieflemming am 13.03.13 22:40:12... zudem finde ich BAR und KOR derzeit weitaus interessanter als WML und IDI.

Antwort auf Beitrag Nr.: 44.249.798 von 666-2004 am 14.03.13 07:24:01Fuer die Frage habe ich Dir eben einen Daumen gegeben. Nach meiner Einschaetzung sieht es etwas besser als bei Werder aus. Schau doch bitte einmal unter Sedar.com nach, ich bin mir sicher Du schaffst das und kannst dann die Ergebnisse hier teilen..

---

Das wird zunaechst wenig Auswirkungen auf die Preisgestaltung haben - ist aber ein interessanter Ansatz:

Coking coal futures approved. ...

"The new financial product will be popular among investors. For one thing, the entry threshold for investment is low and also the price for coking coal has a lot of room to move because it is a raw material," Liu explained, adding that investors may be able to purchase a contract for as little as 6,000 yuan ($965)."

http://english.peopledaily.com.cn/90778/8166616.html

---

Das wird zunaechst wenig Auswirkungen auf die Preisgestaltung haben - ist aber ein interessanter Ansatz:

Coking coal futures approved. ...

"The new financial product will be popular among investors. For one thing, the entry threshold for investment is low and also the price for coking coal has a lot of room to move because it is a raw material," Liu explained, adding that investors may be able to purchase a contract for as little as 6,000 yuan ($965)."

http://english.peopledaily.com.cn/90778/8166616.html

!

Dieser Beitrag wurde von MadMod moderiert. Grund: Provokation!

Dieser Beitrag wurde von MadMod moderiert. Grund: Korrespondierendes Posting wurde entfernt

outube]http://m.youtube.com/#/watch?v=JEo03T80MZw&desktop_uri=%2Fwa…[/youtube]

Es waere fuer Carbon Creek sicherlich förderlich, wenn die Hochzeit nun bald Realitaet wuerde. Zumindest waere dann in der direkten Nachbarschaft eine 56 Mrd. Company. Probleme ueberall ...

Der Markt scheint wohl davon auszugehen, dass Cardero Carbon Creek verliert. Realistisch betrachtet gib es dazu mit Sicherheit in den naechsten 4 Wochen News, da dann die Verlaengerungsoption der Lizenzen ausläuft.

--

In diesem Thread war immer Platz fuer andere mit Cardero assoziierte Unternehmungen und warum soll hier nur die extrem schlecht performenden Werte wie etwa IDI, ABS oder WML erwähnen, wenn es Werte gibt die ich persoenlich fuer aussichtsreich in diesem fast toten Markt halte?

Es waere fuer Carbon Creek sicherlich förderlich, wenn die Hochzeit nun bald Realitaet wuerde. Zumindest waere dann in der direkten Nachbarschaft eine 56 Mrd. Company. Probleme ueberall ...

Der Markt scheint wohl davon auszugehen, dass Cardero Carbon Creek verliert. Realistisch betrachtet gib es dazu mit Sicherheit in den naechsten 4 Wochen News, da dann die Verlaengerungsoption der Lizenzen ausläuft.

--

In diesem Thread war immer Platz fuer andere mit Cardero assoziierte Unternehmungen und warum soll hier nur die extrem schlecht performenden Werte wie etwa IDI, ABS oder WML erwähnen, wenn es Werte gibt die ich persoenlich fuer aussichtsreich in diesem fast toten Markt halte?

Selbst wenn der Sprott Geldhahn zu bleibt sollten ja wohl noch 4 Mio. übrig sein und die Lizenzen zu verlängern. Falls Cardero dieses 130 Mio. teure Asset wegen so einem lächerlichen Betrag verliert, kann sich Hunter auf eine Klagewelle wegen Betruges gefasst machen...

Stefan

Stefan

Antwort auf Beitrag Nr.: 44.257.340 von Stefan0310 am 15.03.13 13:53:08Ich denke auch nicht das es soweit kommt, aber die Schiebetaktik ist dem Kurs nicht förderlich und leider gehen 50% nicht wieder automatisch wieder rauf, wenn die Zweifel (Lizenzen, Finanzierung) ausgeraeumt sind - ich hatte vor ein paar Tagen ein Link zur BMO-Analyse hier eingebracht. Man kann am Beispiel CAD deutlich sehen, dass der Markt Verkaufsabsichten derzeit eher goutiert.

Ein Trauerspiel.

BL

Ein Trauerspiel.

BL

Price Size Orders

Ask

0.27 6,500 4

0.265 7,000 3

0.26 3,000 4

0.255 2,000 2

0.25 1,000 1

Bid

0.24 66,100 5

0.235 1,000 1

0.23 31,000 6

0.22 500 1

0.21 1,700 2

Ask

0.27 6,500 4

0.265 7,000 3

0.26 3,000 4

0.255 2,000 2

0.25 1,000 1

Bid

0.24 66,100 5

0.235 1,000 1

0.23 31,000 6

0.22 500 1

0.21 1,700 2

Antwort auf Beitrag Nr.: 44.258.068 von boersenbrieflemming am 15.03.13 16:03:14Kopf hoch, nicht jmmern!

we have been able to raise 4.6billion dollars from Canada which are bringing to invest here.

Das wird schon, wenn alleine Hoffman 200.000 im Quartal bekommt, die Jungs in Ghana über 10.000 Arbeitsplätze schaffen und dort Eisenbahnlinien und Häfen bauen, dann werden die Paar Mille nicht weiter ins Gewicht fallen.

Selbst von einem Stehbierhallenbetreiber würde man erwarten, dass er einen Liquiditätsplan hat. Was meinst'n Du, welche Entwürfe erst uns're hochbezahlten Direktoren aus den Schubladen ziehen. Iss 'n Teller Buchstabensuppe, das gibt Dir Kraft. Der uny schreibt aus Erfahrung!

we have been able to raise 4.6billion dollars from Canada which are bringing to invest here.

Das wird schon, wenn alleine Hoffman 200.000 im Quartal bekommt, die Jungs in Ghana über 10.000 Arbeitsplätze schaffen und dort Eisenbahnlinien und Häfen bauen, dann werden die Paar Mille nicht weiter ins Gewicht fallen.

Selbst von einem Stehbierhallenbetreiber würde man erwarten, dass er einen Liquiditätsplan hat. Was meinst'n Du, welche Entwürfe erst uns're hochbezahlten Direktoren aus den Schubladen ziehen. Iss 'n Teller Buchstabensuppe, das gibt Dir Kraft. Der uny schreibt aus Erfahrung!

Antwort auf Beitrag Nr.: 44.257.340 von Stefan0310 am 15.03.13 13:53:08Das aktuelle FS, sowie MD&A liegen nun vor (spaeter dann auch via Sedar.com)

Auszug aus dem MD&A: The Company does not have sufficient funds in place to carry out all of the planned work at Carbon Creek, and so its ability to carry out the planned activities is subject to raising the required funding.

Das Statement ist mehr oder weniger eine Standardformulierung, trifft aber den Kern, wenn man sich die FS anschaut. Ohne Fund Raising wird es schwierig mit der abschliessenden Lizenz, auch wenn ich davon ausgehe, dass Carbon Creek eine Mine wird. Die finanzielle Situation und die noch fehlende Perspektive einer Minenfinazierung, werden exakt im Kurs dargestellt, hinzu kommen fehlende Uebernahmephantasien, die u.a. der aktuellen Lage geschuldet sind.

---

SEDAR MD & A

Cardero Resource Corp (C:CDU)

Shares Issued 107,624,048

Last Close 3/15/2013 $0.25

Friday March 15 2013 - SEDAR MD & A

This filing is available at:

http://www.stockwatch.com/nocomp/newsit/newsit_sedardoc.aspx…

SEDAR Interim Financial Statements

Cardero Resource Corp (C:CDU)

Shares Issued 107,624,048

Last Close 3/15/2013 $0.25

Friday March 15 2013 - SEDAR Interim Financial Statements

This filing is available at:

http://www.stockwatch.com/nocomp/newsit/newsit_sedardoc.aspx…

Auszug aus dem MD&A: The Company does not have sufficient funds in place to carry out all of the planned work at Carbon Creek, and so its ability to carry out the planned activities is subject to raising the required funding.

Das Statement ist mehr oder weniger eine Standardformulierung, trifft aber den Kern, wenn man sich die FS anschaut. Ohne Fund Raising wird es schwierig mit der abschliessenden Lizenz, auch wenn ich davon ausgehe, dass Carbon Creek eine Mine wird. Die finanzielle Situation und die noch fehlende Perspektive einer Minenfinazierung, werden exakt im Kurs dargestellt, hinzu kommen fehlende Uebernahmephantasien, die u.a. der aktuellen Lage geschuldet sind.

---

SEDAR MD & A

Cardero Resource Corp (C:CDU)

Shares Issued 107,624,048

Last Close 3/15/2013 $0.25

Friday March 15 2013 - SEDAR MD & A

This filing is available at:

http://www.stockwatch.com/nocomp/newsit/newsit_sedardoc.aspx…

SEDAR Interim Financial Statements

Cardero Resource Corp (C:CDU)

Shares Issued 107,624,048

Last Close 3/15/2013 $0.25

Friday March 15 2013 - SEDAR Interim Financial Statements

This filing is available at:

http://www.stockwatch.com/nocomp/newsit/newsit_sedardoc.aspx…

alleine Hoffman 200.000 im Quartal bekommt,

Kannst Du mir mal einen Beleg erbringen, dass Hoffmann 800k im Jahr als Salär bekommt?

Kannst Du mir mal einen Beleg erbringen, dass Hoffmann 800k im Jahr als Salär bekommt?

Antwort auf Beitrag Nr.: 44.260.643 von boersenbrieflemming am 16.03.13 11:22:27Ne Hawebraddler, hat der uny auch nicht geschrieben. Hast Du die Hochrechnung auf Grund der 200.000 im vorletzten Quartal ohne Taschenrechner geschafft?

W§enn Du 'n Kerl wärst, würdest Du den Kern dessen, wAS dIR DER uny geschrieben hat in Deinem Thread ansprechen. In der MD&A steht im Grunde klipp und klar, dass Ende Gelände ist. Esw reicht eigentlich, sich auf die Aussagen zur Liquidität ab Seite 25 zu beschränken. Wie oft hat der uny darauf hingewiesen, dass die Jungs an viel zu vieln Fronten gleichzeitig kämpfen. Das haben schon andere erfahren müssen, dass das in die Hose geht.

#

Du hast hier jahrelang von Liquiditätsplanung gefaselt und hast von Tuten und Blasen keine Ahnung. Statt dass Du Deinen Lesern die volle Wahrheit sagst, hast Du seit geraumer langsam damit begonnen den Rückwärtsgang einzulegen. Bei Neono konnte man vestehen, dass er sich einfach so verdrückte, weil er wußte, was wohl passieren wird, wenn er seine mittlerweile wohl gewonnenen Ansichten klar äußert.

Aber so ein Dreikäsehoch wie Du kann ruhig mit offenen Karten spielen, das wird dem Kurs nicht mehr schaden können.

Siehste King, der uny macht den Steinbrück. Du verträgst doch Klartext? Oder? Steelball? Und solltest Du Dich durch den ein oder anderen Ausdruck beleidigt fühlen, tuts dem uny jetzt schon Leid. Das ist nämlich nicht seine Absicht.

Jetzt kannste wieder den Mod bemühen, oder bei Seabridge Deinen Käse ablassen.

Der uny jedenfalls hat besseres zu tun, als sich auf das einzulassen, was Du mit Deiner Fragestellung beabsichtigt hast.

Wenn Du mal offen zugeben würdest, dass Du einfach nur versagt hast mit Deinen Prognosen zu Cardero, könnte man Dich gegebenenfalls für voll nehmen.

Sei es wie es sei, der uny wünscht Fir ein angenehmes Wochenende, möglichst mal ohne Online-Präsenz. Das würde Dir bestimmt gut tun. Kannst j amal über diese Worte nachdenken.

W§enn Du 'n Kerl wärst, würdest Du den Kern dessen, wAS dIR DER uny geschrieben hat in Deinem Thread ansprechen. In der MD&A steht im Grunde klipp und klar, dass Ende Gelände ist. Esw reicht eigentlich, sich auf die Aussagen zur Liquidität ab Seite 25 zu beschränken. Wie oft hat der uny darauf hingewiesen, dass die Jungs an viel zu vieln Fronten gleichzeitig kämpfen. Das haben schon andere erfahren müssen, dass das in die Hose geht.

#

Du hast hier jahrelang von Liquiditätsplanung gefaselt und hast von Tuten und Blasen keine Ahnung. Statt dass Du Deinen Lesern die volle Wahrheit sagst, hast Du seit geraumer langsam damit begonnen den Rückwärtsgang einzulegen. Bei Neono konnte man vestehen, dass er sich einfach so verdrückte, weil er wußte, was wohl passieren wird, wenn er seine mittlerweile wohl gewonnenen Ansichten klar äußert.

Aber so ein Dreikäsehoch wie Du kann ruhig mit offenen Karten spielen, das wird dem Kurs nicht mehr schaden können.

Siehste King, der uny macht den Steinbrück. Du verträgst doch Klartext? Oder? Steelball? Und solltest Du Dich durch den ein oder anderen Ausdruck beleidigt fühlen, tuts dem uny jetzt schon Leid. Das ist nämlich nicht seine Absicht.

Jetzt kannste wieder den Mod bemühen, oder bei Seabridge Deinen Käse ablassen.

Der uny jedenfalls hat besseres zu tun, als sich auf das einzulassen, was Du mit Deiner Fragestellung beabsichtigt hast.

Wenn Du mal offen zugeben würdest, dass Du einfach nur versagt hast mit Deinen Prognosen zu Cardero, könnte man Dich gegebenenfalls für voll nehmen.

Sei es wie es sei, der uny wünscht Fir ein angenehmes Wochenende, möglichst mal ohne Online-Präsenz. Das würde Dir bestimmt gut tun. Kannst j amal über diese Worte nachdenken.

Antwort auf Beitrag Nr.: 44.261.136 von uny1989 am 16.03.13 15:44:21Gut gesprochen Uny! Ich muss Dir leider zustimmen, dass die Filings keinen anderen Schluss zulassen, als dass CDU fertig hat und aus 80% Verlust demnächst 100 werden. Ich habe zwar frisches Geld beseitegelegt um bei besseren Aussichten zu verbilligen aber dafür mach ich wohl lieber mal ne Reise nach Kanada und verclicker den Herrschaften persönlich was ich von ihrem Shareholdervalue-Verständnis halte.

Für den Fall der Fälle sollten sich alle Geschädigten überlegen, eine Sammelklage gegen dieses Verbrecherpack einzureichen. Geld genug muss ja da sein wenn man sich die großzügigen Vergütungen anschaut.

Stefan

Für den Fall der Fälle sollten sich alle Geschädigten überlegen, eine Sammelklage gegen dieses Verbrecherpack einzureichen. Geld genug muss ja da sein wenn man sich die großzügigen Vergütungen anschaut.

Stefan

Antwort auf Beitrag Nr.: 44.261.194 von Stefan0310 am 16.03.13 16:15:52Hab grade noch mal drüber gelesen. Man kann auch der Anaicht sein, der uny hat sich im Ton vergriffen. Lemming hat gelesen, dass Hoffman im letzten Quartal "nur" 125.000 oder 120.000, weiß jetzt nicht genau, vderdient hat. Ungefähr das Doppelte als die anderen Hrrschaften. Für was? Labrador iron sands?

Statt das offen und ehrlich anzusprechen, oder diesen Offenbarungseid in der MD&A macht er hier Andeutungen, aber kaum mehr. In seinem Performancethread verkauft er CDU.

Wäre er ein Kerl, würde er seinen Thread mit den entsprechenden Worten abschliessen. Schwamm drüber un dgut wärs.

Er tut mir la leid. Diese ständige Präsenz hier macht einen bestimmt kirre.

Ich sag jetzt mal wieder Tschüss. Ob's ein Wiedersehen geben wird, steht in den Sternen. Seit Februar hab ich wirklich ernsthaft mit dem Schreiben begonnen. Wird noch ein Weilchen dauern bis das Buch fertig ist. Damit ich keine kostbare Zeit hier investiere, klinke ich mich aus mit Hinweis:

Sorry für die besser nicht geschriebenen Worte und Köpfe hoch. Es gibt wahrlich Schöneres als zu zocken.

uny1989, "Mit Klose in der Hose und Gomez an der Hand"

Statt das offen und ehrlich anzusprechen, oder diesen Offenbarungseid in der MD&A macht er hier Andeutungen, aber kaum mehr. In seinem Performancethread verkauft er CDU.

Wäre er ein Kerl, würde er seinen Thread mit den entsprechenden Worten abschliessen. Schwamm drüber un dgut wärs.

Er tut mir la leid. Diese ständige Präsenz hier macht einen bestimmt kirre.

Ich sag jetzt mal wieder Tschüss. Ob's ein Wiedersehen geben wird, steht in den Sternen. Seit Februar hab ich wirklich ernsthaft mit dem Schreiben begonnen. Wird noch ein Weilchen dauern bis das Buch fertig ist. Damit ich keine kostbare Zeit hier investiere, klinke ich mich aus mit Hinweis:

Sorry für die besser nicht geschriebenen Worte und Köpfe hoch. Es gibt wahrlich Schöneres als zu zocken.

uny1989, "Mit Klose in der Hose und Gomez an der Hand"

wAS dIR DER uny geschrieben

Das Liquiditaets-Problem ist aber kein Alleinstellungsmerkmal von Cardero, sondern betrifft eigentlich fast alle Explorer (mit sehr, sehr wenigen Ausnahmen). Der Markt ist derzeit tot.

Ich hatte dich eigentlich nur gebeten hier einmal Deine Behauptung das "alleine Hoffman 200.000 im Quartal bekommt zu belegen. Nach meinem Wissen entspricht das nicht der Wahrheit. Mehr wollte ich nicht und Deine Ausfälle interessieren mich nicht.

@stefan

Meine persönliche Meinung kennst Du. Sie haben einen Kollaps abgewendet, aber ohne die Perspektive der Minenfinanzierung und Klärung der Lizenzfrage (Wann wird gezahlt) ist die CDU in meinen Augen derzeit kein Kauf, schafft es das MM mir eine Perspektive aufzuzeigen (JV-Partner, Sprott oder Andere, Lizenz) ändert sich das ganz schnell.

Das Liquiditaets-Problem ist aber kein Alleinstellungsmerkmal von Cardero, sondern betrifft eigentlich fast alle Explorer (mit sehr, sehr wenigen Ausnahmen). Der Markt ist derzeit tot.

Ich hatte dich eigentlich nur gebeten hier einmal Deine Behauptung das "alleine Hoffman 200.000 im Quartal bekommt zu belegen. Nach meinem Wissen entspricht das nicht der Wahrheit. Mehr wollte ich nicht und Deine Ausfälle interessieren mich nicht.

@stefan

Meine persönliche Meinung kennst Du. Sie haben einen Kollaps abgewendet, aber ohne die Perspektive der Minenfinanzierung und Klärung der Lizenzfrage (Wann wird gezahlt) ist die CDU in meinen Augen derzeit kein Kauf, schafft es das MM mir eine Perspektive aufzuzeigen (JV-Partner, Sprott oder Andere, Lizenz) ändert sich das ganz schnell.

Antwort auf Beitrag Nr.: 44.261.436 von boersenbrieflemming am 16.03.13 18:01:30uny1989

abgemeldet

--

nachvollziehbar ...

abgemeldet

--

nachvollziehbar ...

Lemming, hast du dir das Dokument auf Sedar angeschaut?

Wenn ja, schreib hier so keinen Mist, wenn Arbeiter an der Maschine nichts leisten gibt's kein Geld, dieses Management steckt Dahrlehnsgeld ein, gibt eine Erklärung ab das alle Angaben korrekt sind und fahren das Drecksding in die Scheiße.

Auf dich haben einige gehört, wenn ich dich mal irgendwo treffe werde ich dich ganz lieb drücken, mein Held

Wenn ja, schreib hier so keinen Mist, wenn Arbeiter an der Maschine nichts leisten gibt's kein Geld, dieses Management steckt Dahrlehnsgeld ein, gibt eine Erklärung ab das alle Angaben korrekt sind und fahren das Drecksding in die Scheiße.

Auf dich haben einige gehört, wenn ich dich mal irgendwo treffe werde ich dich ganz lieb drücken, mein Held

In vier Wochen werden wir endgültig wissen, ob die Muppets 130 Mio. verzockt haben für eine Top-Property die CDU wegen lächerlichen 4 Mio. Lizenzkosten plötzlich nicht mehr gehört. Das Alleinstellungsmerkmal von Cardero ist nicht die Liquiditätskrise, sondern dass diese ohne jeglichen betriebswirtschaftlichen Verstand selbst herbeigeführt wurde. Wer so agiert und dabei noch großzügige Gehälter einstreicht muss bluten!!!

Stefan

Stefan

Antwort auf Beitrag Nr.: 44.261.476 von Birdy1960 am 16.03.13 18:16:11Lemming, hast du dir das Dokument auf Sedar angeschaut?

Welches? Das Financial Statement? Oder die MD&A?

dieses Management steckt Dahrlehnsgeld ein

Leider nein:

"As a consequence of the closing of the first and second tranche of the Offerings and of the FT Offering, the Company has raised gross proceeds of $7,697,957. Accordingly, the Company had estimated that that the Sprott loan, if completed, would be for approximately $7,700,000. However, the Company now believes that, due to current market conditions for the securities of junior resource companies, the Sprott loan will likely be for a lesser amount, possibly $5 million. However, this matter remains under negotiation. The Company is unable to predict the potential closing date for the Sprott loan, and there can be no certainty that the Sprott loan will, in fact, be closed"

MD&A (Seite 27)

wenn ich dich mal irgendwo treffe werde ich dich ganz lieb drücken, mein Held

Sage mir so etwas bitte lieber persoenlich - anonyme Drohungen sind eher unschön.

Welches? Das Financial Statement? Oder die MD&A?

dieses Management steckt Dahrlehnsgeld ein

Leider nein:

"As a consequence of the closing of the first and second tranche of the Offerings and of the FT Offering, the Company has raised gross proceeds of $7,697,957. Accordingly, the Company had estimated that that the Sprott loan, if completed, would be for approximately $7,700,000. However, the Company now believes that, due to current market conditions for the securities of junior resource companies, the Sprott loan will likely be for a lesser amount, possibly $5 million. However, this matter remains under negotiation. The Company is unable to predict the potential closing date for the Sprott loan, and there can be no certainty that the Sprott loan will, in fact, be closed"

MD&A (Seite 27)

wenn ich dich mal irgendwo treffe werde ich dich ganz lieb drücken, mein Held

Sage mir so etwas bitte lieber persoenlich - anonyme Drohungen sind eher unschön.

Antwort auf Beitrag Nr.: 44.261.560 von Stefan0310 am 16.03.13 18:53:45Nur zu den Gehältern. Das ist nicht das Problem (Salaries 12-125K), zudem sollte Hunter genug via First Coal und Carbon Creek sehr viel Geld eingenommen haben.

Falls sie es in die Grütze fahren sollten, wird Carbon Creek mit Sicherheit wieder irgendwo auftauchen und auch zur Mine entwickelt werden.

Falls sie es in die Grütze fahren sollten, wird Carbon Creek mit Sicherheit wieder irgendwo auftauchen und auch zur Mine entwickelt werden.

So, mal wieder nach vorne schauen:

Sukunka Coal Mine Project and Carbon Creek Metallurgical Coal Mine Project

Substitution requested under the Canadian Environmental Assessment Act, 2012

Public Comments Invited

OTTAWA, March 15, 2013 /CNW/ - As part of the strengthened and modernized Canadian Environmental Assessment Act, 2012 (CEAA 2012) put in place to support the government's Responsible Resource Development Initiative, the Canadian Environmental Assessment Agency is seeking comments from the public on substitution requests by British Columbia (B.C.) for the environmental assessment of the proposed Sukunka Coal Mine Project and of the Carbon Creek Metallurgical Coal Mine Project located in B.C.

CEAA 2012 enables cooperation between the federal government and other jurisdictions in the delivery of timely, high quality environmental assessments through a number of different means. One of these means is for the Minister of the Environment to substitute the environmental assessment process of another jurisdiction for the process that would otherwise be conducted by the Agency. This approach achieves the objective of "one project-one assessment" which has been endorsed by the Canadian Council of Ministers of the Environment.

The Minister of the Environment, the Honourable Peter Kent, must approve the substitution requests if he is satisfied that the conditions for substitution under CEAA 2012 are met and if he is of the opinion that the B.C. process would be an appropriate substitute for an environmental assessment by the Agency.

Written comments in that regard must be submitted by April 4, 2013 to the Canadian Environmental Assessment Agency:

...

http://www.newswire.ca/en/story/1130385/sukunka-coal-mine-pr…

...

Ein weiterer Schritt im Genehmigungsverfahren.

Sukunka Coal Mine Project and Carbon Creek Metallurgical Coal Mine Project

Substitution requested under the Canadian Environmental Assessment Act, 2012

Public Comments Invited

OTTAWA, March 15, 2013 /CNW/ - As part of the strengthened and modernized Canadian Environmental Assessment Act, 2012 (CEAA 2012) put in place to support the government's Responsible Resource Development Initiative, the Canadian Environmental Assessment Agency is seeking comments from the public on substitution requests by British Columbia (B.C.) for the environmental assessment of the proposed Sukunka Coal Mine Project and of the Carbon Creek Metallurgical Coal Mine Project located in B.C.

CEAA 2012 enables cooperation between the federal government and other jurisdictions in the delivery of timely, high quality environmental assessments through a number of different means. One of these means is for the Minister of the Environment to substitute the environmental assessment process of another jurisdiction for the process that would otherwise be conducted by the Agency. This approach achieves the objective of "one project-one assessment" which has been endorsed by the Canadian Council of Ministers of the Environment.

The Minister of the Environment, the Honourable Peter Kent, must approve the substitution requests if he is satisfied that the conditions for substitution under CEAA 2012 are met and if he is of the opinion that the B.C. process would be an appropriate substitute for an environmental assessment by the Agency.

Written comments in that regard must be submitted by April 4, 2013 to the Canadian Environmental Assessment Agency:

...

http://www.newswire.ca/en/story/1130385/sukunka-coal-mine-pr…

...

Ein weiterer Schritt im Genehmigungsverfahren.

Hier kurz der direkte Link zur "Canadian Environmental Assessment Agency" und dem Projekt Carbon Creek.

http://www.ceaa-acee.gc.ca/050/details-eng.cfm?evaluation=80…

Es waere sehr bedauerlich, wenn die FS nicht abgeschlossen werden kann (und die Einarbeitung der Drillings 2012 unvollstaendig bleibt) und fatal, wenn das neue MM es trotz hoher Explorations -und grenzwertiger Administrationskosten es nicht schafft Perspektiven aufzuzeigen und den notwendigen Teil der Explorationslizenzen zu sichern.

Da summiert sich einiges an Terminen im April: CEAA-Kommentare (4.), AGM (25.) und die Lizenzen (14.) und je mehr man sich damit beschaeftigt, desto sorgenvoller wird der Blick auf die Company und das neue MM (insbesondere Hunter und Bailey) - mir fehlt da ein wenig der Hunger und Wille Cardero (!) zum Erfolg zu bringen, während Carbon Creek immer noch gut aussieht und sich Produzenten (Bsp. ANR) schön erholen ...

http://www.ceaa-acee.gc.ca/050/details-eng.cfm?evaluation=80…

Es waere sehr bedauerlich, wenn die FS nicht abgeschlossen werden kann (und die Einarbeitung der Drillings 2012 unvollstaendig bleibt) und fatal, wenn das neue MM es trotz hoher Explorations -und grenzwertiger Administrationskosten es nicht schafft Perspektiven aufzuzeigen und den notwendigen Teil der Explorationslizenzen zu sichern.

Da summiert sich einiges an Terminen im April: CEAA-Kommentare (4.), AGM (25.) und die Lizenzen (14.) und je mehr man sich damit beschaeftigt, desto sorgenvoller wird der Blick auf die Company und das neue MM (insbesondere Hunter und Bailey) - mir fehlt da ein wenig der Hunger und Wille Cardero (!) zum Erfolg zu bringen, während Carbon Creek immer noch gut aussieht und sich Produzenten (Bsp. ANR) schön erholen ...

Coking coal price under pressure

Frik Els | March 15, 2013

http://www.mining.com/coking-coal-prices-under-pressure-3932…

---

Das macht es auch nicht einfacher - wie gesagt ein Trauerspiel.

Frik Els | March 15, 2013

http://www.mining.com/coking-coal-prices-under-pressure-3932…

---

Das macht es auch nicht einfacher - wie gesagt ein Trauerspiel.

... die andere Seite ..

• Ron Fernandes, CEO of Avatar Investment Management in Stamford, Conn., with $800 million in assets under management: Market Vectors Coal ETF (KOL).

Coal is an under-loved commodity within the energy sector. Low natural gas prices and a slowdown in China reduced demand and drove valuations down in 2012.

However, natural gas prices are rebounding, China has stabilized, India is showing signs of life. Commodities are powering up and emerging markets are poised for continued solid growth in 2013.

Four countries — China, India, Australia and Indonesia — generate more than 60% of the total world output. China alone produces 40%. The U.S., perceived by many as a leading producer, comes in at roughly 15% of total production.

Global demand is expected to grow at 5% annualized over the next decade, more than offsetting the cut in U.S.-based demand. That steady growth will make both China and India — the first- and second-largest global populations — net importers of coal and provide an opportunity for U.S.-headquartered producers to build a lucrative export-driven model. KOL has little downside risk with potential to deliver a 25% return in 2013.

Read More At Investor's Business Daily: http://news.investors.com/investing-etfs/122712-638483-stock…

Follow us: @IBDinvestors on Twitter | InvestorsBusinessDaily on Facebook

• Ron Fernandes, CEO of Avatar Investment Management in Stamford, Conn., with $800 million in assets under management: Market Vectors Coal ETF (KOL).

Coal is an under-loved commodity within the energy sector. Low natural gas prices and a slowdown in China reduced demand and drove valuations down in 2012.

However, natural gas prices are rebounding, China has stabilized, India is showing signs of life. Commodities are powering up and emerging markets are poised for continued solid growth in 2013.

Four countries — China, India, Australia and Indonesia — generate more than 60% of the total world output. China alone produces 40%. The U.S., perceived by many as a leading producer, comes in at roughly 15% of total production.

Global demand is expected to grow at 5% annualized over the next decade, more than offsetting the cut in U.S.-based demand. That steady growth will make both China and India — the first- and second-largest global populations — net importers of coal and provide an opportunity for U.S.-headquartered producers to build a lucrative export-driven model. KOL has little downside risk with potential to deliver a 25% return in 2013.

Read More At Investor's Business Daily: http://news.investors.com/investing-etfs/122712-638483-stock…

Follow us: @IBDinvestors on Twitter | InvestorsBusinessDaily on Facebook

So war das frueher mal:

Wobei Anlaufschwierigkeiten in der Produktion hier genauso wenig beruecksichtigt werden (ich denke da gerne an die haeufig postulierten 3monatigen Ramp Ups, die sich dann ueber Jahre hinziehen können), wie das Financing (Dilution, billige Warrants) oder gerade die aktuell uebergreifenden Liquiditätsprobleme und Kohlepreise.

Cardero befindet sich im Bereich kurz vor der der Markierung, die heute extremeren Marktbedingungen kennen wir und bemerken das in unseren Depots oder Watchlisten.

Wobei Anlaufschwierigkeiten in der Produktion hier genauso wenig beruecksichtigt werden (ich denke da gerne an die haeufig postulierten 3monatigen Ramp Ups, die sich dann ueber Jahre hinziehen können), wie das Financing (Dilution, billige Warrants) oder gerade die aktuell uebergreifenden Liquiditätsprobleme und Kohlepreise.

Cardero befindet sich im Bereich kurz vor der der Markierung, die heute extremeren Marktbedingungen kennen wir und bemerken das in unseren Depots oder Watchlisten.

Zitat von boersenbrieflemming: So war das frueher mal:

(..)

Cardero befindet sich im Bereich kurz vor der der Markierung, die heute extremeren Marktbedingungen kennen wir und bemerken das in unseren Depots oder Watchlisten.

Wen genau meinst du denn mit "wir"?

Und welche Markierung ist gemeint, die "Reality sets in"?

Zitat von boersenbrieflemming: So war das frueher mal:

![]()

Wobei Anlaufschwierigkeiten in der Produktion hier genauso wenig beruecksichtigt werden (ich denke da gerne an die haeufig postulierten 3monatigen Ramp Ups, die sich dann ueber Jahre hinziehen können), wie das Financing (Dilution, billige Warrants) oder gerade die aktuell uebergreifenden Liquiditätsprobleme und Kohlepreise.

Cardero befindet sich im Bereich kurz vor der der Markierung, die heute extremeren Marktbedingungen kennen wir und bemerken das in unseren Depots oder Watchlisten.

Wie ist es denn heute anders? Hast du dazu auch eine Grafik?

Ausserdem was für "extremere" Marktbedingungen sind gemeint? Rohstoffe und Edelmetalle notieren sehr solide .. oder meinst du den Kurs eine Cardero-Aktie?

Du scheinst verunsichert

Antwort auf Beitrag Nr.: 44.263.403 von euroztar am 17.03.13 16:53:31 denn mit "wir"

Die, die Interesse an der Aktie oder Explorerbuden haben - ob nun im Depot oder auf der WL.

Markierung ist gemeint

Lower Risk - nach Abschluss einer FS (wobei ich da eher nur hoffe das sie es noch hinbekommen).

Die, die Interesse an der Aktie oder Explorerbuden haben - ob nun im Depot oder auf der WL.

Markierung ist gemeint

Lower Risk - nach Abschluss einer FS (wobei ich da eher nur hoffe das sie es noch hinbekommen).

Zitat von boersenbrieflemming: (..)

Wobei Anlaufschwierigkeiten in der Produktion hier genauso wenig beruecksichtigt werden (ich denke da gerne an die haeufig postulierten 3monatigen Ramp Ups, die sich dann ueber Jahre hinziehen können), wie das Financing (Dilution, billige Warrants) oder gerade die aktuell uebergreifenden Liquiditätsprobleme und Kohlepreise.

Wieso denkst du da "gerne" dran, spielt dir das in die Karten?

Zitat von boersenbrieflemming: (..) wir und bemerken das in unseren Depots oder Watchlisten.

Oder an der dünnen Teilnahm im einst gut frequentierten thread.

Antwort auf Beitrag Nr.: 44.263.440 von euroztar am 17.03.13 17:02:54Ausserdem was für "extremere" Marktbedingungen sind gemeint? Rohstoffe und Edelmetalle notieren sehr solide .. oder meinst du den Kurs eine Cardero-Aktie?

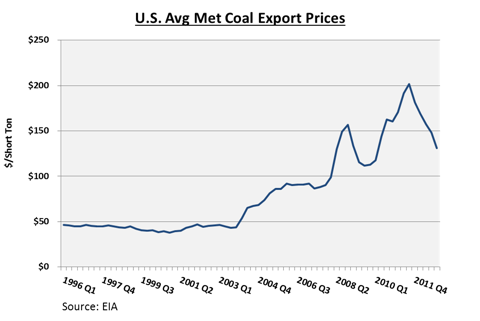

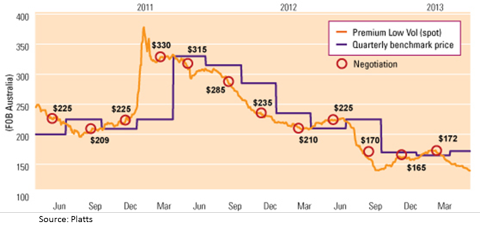

Du schreibst bei Northland Res. und kennst die grundsaetzliche Problematik. Der Explorerbereich ist derzeit fast tot, Financings finden auf niedrigstem Niveau statt und da die "sehr soliden" Rohstoffpreise erwähnst: Met Coal ist immer noch im Keller und rangiert knapp ueber den Produktionskosten in Australien.

Der Kurs der Cardero-Aktie performed unter dem Vergleichswert CAD, was mich im Moment nicht wirklich wundert.

Du schreibst bei Northland Res. und kennst die grundsaetzliche Problematik. Der Explorerbereich ist derzeit fast tot, Financings finden auf niedrigstem Niveau statt und da die "sehr soliden" Rohstoffpreise erwähnst: Met Coal ist immer noch im Keller und rangiert knapp ueber den Produktionskosten in Australien.

Der Kurs der Cardero-Aktie performed unter dem Vergleichswert CAD, was mich im Moment nicht wirklich wundert.

Einfaches Einfügen von wallstreetONLINE Charts: So funktionierts.

N.S. government expects Donkin coal mine to open

http://www.ipolitics.ca/2013/03/13/n-s-government-expects-do…

Interessant ist auch, dass Xstrata seine Donkin Mine (75% Interest) wiedereröffnet (nachdem sie es nicht verkauft haben) und das Prinzip des Kohletranportes dem von Carbon Creek entspricht.

http://www.cbc.ca/player/Shows/ID/2200745583/

Infos zu Donkin

http://www.erdene.com/projects40/donkin41b1.php

http://www.ipolitics.ca/2013/03/13/n-s-government-expects-do…

Interessant ist auch, dass Xstrata seine Donkin Mine (75% Interest) wiedereröffnet (nachdem sie es nicht verkauft haben) und das Prinzip des Kohletranportes dem von Carbon Creek entspricht.

http://www.cbc.ca/player/Shows/ID/2200745583/

Infos zu Donkin

http://www.erdene.com/projects40/donkin41b1.php

Interessanter Fund zum Thema Eisenerz in Afrika:

http://au.news.yahoo.com/thewest/business/a/-/national/16387…

Die Chance Sheini zu Geld zu machen dürfte gegen null tendieren - Emmaland hat da einen super Deal gemacht...

Stefan

http://au.news.yahoo.com/thewest/business/a/-/national/16387…

Die Chance Sheini zu Geld zu machen dürfte gegen null tendieren - Emmaland hat da einen super Deal gemacht...

Stefan

Antwort auf Beitrag Nr.: 44.265.297 von Stefan0310 am 18.03.13 09:50:06Nun, Guinea ist nicht Ghana. Auch wenn ich die Ecke etwas kenne (Mali), kann man da nicht generalisieren, da Ghana eher ein Minenland mit entsprechender Tradition und Strukturen ist. Tatsaechlich wird aber auch die Infrastruktur von Sheini im argen liegen, zumal ich u.a. nicht genau weiss was aus der entsprechenden Bahnlinie in den Norden geworden ist.

Sheini hat ein anderes Problem - ich haette mir etwas mehr Exploration gewuenscht, da die Aussicht auf oeberflaechliches Iron Ore mir guenstig erscheint. Ob die bisherigen Massnahmen Maiden Resource und Metallurgie fuer einen Verkauf oder Verpartnerung ausreichen, das bleibt in der Tat sehr fraglich. Etwas weniger administrative Kosten, etwas mehr Sheini ... ich erinnere mich noch gut daran, dass ich damals hoffte das sie Cardero in Cardero Coal und Cardero Iron auftreilen. Ich bin eher ein Steelball, als ein Koksbruder.

Sheini hat ein anderes Problem - ich haette mir etwas mehr Exploration gewuenscht, da die Aussicht auf oeberflaechliches Iron Ore mir guenstig erscheint. Ob die bisherigen Massnahmen Maiden Resource und Metallurgie fuer einen Verkauf oder Verpartnerung ausreichen, das bleibt in der Tat sehr fraglich. Etwas weniger administrative Kosten, etwas mehr Sheini ... ich erinnere mich noch gut daran, dass ich damals hoffte das sie Cardero in Cardero Coal und Cardero Iron auftreilen. Ich bin eher ein Steelball, als ein Koksbruder.

Cardero mit dem benachbarten Xstrata-Projekt ...

Sukunka Coal Mine Project and Carbon Creek Metallurgical Coal Mine Project

Monday, Mar 18, 2013

OTTAWA, March 15, 2013 /CNW/ - As part of the strengthened and modernized Canadian Environmental Assessment Act, 2012 (CEAA 2012) put in place to support the government's Responsible Resource Development Initiative, the Canadian Environmental Assessment Agency is seeking comments from the public on substitution requests by British Columbia (B.C.) for the environmental assessment of the proposed Sukunka Coal Mine Project and of the Carbon Creek Metallurgical Coal Mine Project located in B.C.

CEAA 2012 enables cooperation between the federal government and other jurisdictions in the delivery of timely, high quality environmental assessments through a number of different means. One of these means is for the Minister of the Environment to substitute the environmental assessment process of another jurisdiction for the process that would otherwise be conducted by the Agency.

This approach achieves the objective of "one project-one assessment" which has been endorsed by the Canadian Council of Ministers of the Environment.

The Minister of the Environment, the Honourable Peter Kent, must approve the substitution requests if he is satisfied that the conditions for substitution under CEAA 2012 are met and if he is of the opinion that the B.C. process would be an appropriate substitute for an environmental assessment by the Agency.

The Sukunka Coal Mine Project

Xstrata Coal Canada proposes to develop and operate an integrated surface and underground metallurgical coal mine located approximately 55 kilometres south of Chetwynd and 40 kilometres west of Tumbler Ridge, in northeast British Columbia.

The proposed project would initially produce 1.5 to 2.5 million tonnes per year increasing to 6 million tonnes per year when underground mining begins. The mine life is expected to exceed 20 years.

The Carbon Creek Metallurgical Coal Mine Project

Cardero Coal Ltd proposes to develop and operate an open pit metallurgical coal mine located approximately 60 kilometres northwest of Chetwynd and 40 kilometres west of Hudson's Hope, in northeast British Columbia. The proposed project would involve open pit surface mining followed by combined open pit and underground mining. The production rate would be 4.1 million metric tonnes of metallurgical coal per year, over a mine life of 20 years.

http://www.yourindustrynews.com/sukunka+coal+mine+project+an…

Sukunka Coal Mine Project and Carbon Creek Metallurgical Coal Mine Project

Monday, Mar 18, 2013

OTTAWA, March 15, 2013 /CNW/ - As part of the strengthened and modernized Canadian Environmental Assessment Act, 2012 (CEAA 2012) put in place to support the government's Responsible Resource Development Initiative, the Canadian Environmental Assessment Agency is seeking comments from the public on substitution requests by British Columbia (B.C.) for the environmental assessment of the proposed Sukunka Coal Mine Project and of the Carbon Creek Metallurgical Coal Mine Project located in B.C.

CEAA 2012 enables cooperation between the federal government and other jurisdictions in the delivery of timely, high quality environmental assessments through a number of different means. One of these means is for the Minister of the Environment to substitute the environmental assessment process of another jurisdiction for the process that would otherwise be conducted by the Agency.

This approach achieves the objective of "one project-one assessment" which has been endorsed by the Canadian Council of Ministers of the Environment.

The Minister of the Environment, the Honourable Peter Kent, must approve the substitution requests if he is satisfied that the conditions for substitution under CEAA 2012 are met and if he is of the opinion that the B.C. process would be an appropriate substitute for an environmental assessment by the Agency.

The Sukunka Coal Mine Project

Xstrata Coal Canada proposes to develop and operate an integrated surface and underground metallurgical coal mine located approximately 55 kilometres south of Chetwynd and 40 kilometres west of Tumbler Ridge, in northeast British Columbia.

The proposed project would initially produce 1.5 to 2.5 million tonnes per year increasing to 6 million tonnes per year when underground mining begins. The mine life is expected to exceed 20 years.

The Carbon Creek Metallurgical Coal Mine Project

Cardero Coal Ltd proposes to develop and operate an open pit metallurgical coal mine located approximately 60 kilometres northwest of Chetwynd and 40 kilometres west of Hudson's Hope, in northeast British Columbia. The proposed project would involve open pit surface mining followed by combined open pit and underground mining. The production rate would be 4.1 million metric tonnes of metallurgical coal per year, over a mine life of 20 years.

http://www.yourindustrynews.com/sukunka+coal+mine+project+an…

Coal still looks good (to some) for the future

http://www.canadianminingjournal.com/news/coal-still-looks-g…

--

Dann kann man ja nur hoffen, dass die Coalhunter-Crew hier etwas gebacken bekommt.

http://www.canadianminingjournal.com/news/coal-still-looks-g…

--

Dann kann man ja nur hoffen, dass die Coalhunter-Crew hier etwas gebacken bekommt.

So, das war es wohl mit dem Coalhunter-Team:

Cardero Announces Resignation of CEO

NR13-06 March 20, 2013.

Vancouver, British Columbia…Cardero Resource Corp. (“Cardero” or the “Company”) (TSX: CDU, NYSE-MKT: CDY) announces that Michael Hunter has resigned as the Chief Executive Officer and President, and as a director, of the Company, effective March 19, 2013. The Company would like to thank Michael for his service and significant contribution to the Company. The Board of Directors has appointed Hendrik van Alphen as the new Chief Executive Officer and President of the Company.

About Carbon Creek

The Company’s flagship asset is the Carbon Creek Metallurgical Coal Deposit. Carbon Creek is an advanced metallurgical coal development project located in the Peace River Coal District of northeast British Columbia, Canada. The project has a current reserve of 121 million tonnes, included within a 468 million tonne measured and indicated resource, of ASTM Coal Rank mvB coal. Having completed acquisition of the project in June 2011, the Company released results of an independent preliminary economic assessment in December 2011, followed by a Prefeasibility Study (“PFS”) in September 2012. The PFS estimates an undiscounted cash flow of $2.2 billion, an NPV8 of $633 million, and an IRR of 24% (all on a post-tax, 75% basis). The Company is currently undertaking a bankable feasibility study on the project.

For details with respect to the work done to date and the assumptions underlying the current resource and reserve estimates and prefeasibility study, see the technical report entitled “Technical Report, Prefeasibility Study of the Carbon Creek Coal Property, British Columbia, Canada” dated November 6, 2012 with an effective date of September 20, 2012 and available under the Company’s profile at www.sedar.com.

EurGeol Keith Henderson, PGeo, Cardero’s Executive Vice President and a qualified person as defined by National Instrument 43-101, has reviewed the scientific and technical information that forms the basis of this news release, and has approved the disclosure herein. Mr. Henderson is not independent of the Company, as he is an officer and shareholder.

About Cardero Resource Corp.

The common shares of the Company are currently listed on the Toronto Stock Exchange (symbol CDU), the NYSE-MKT (symbol CDY) and the Frankfurt Stock Exchange (symbol CR5). For further details on the Company readers are referred to the Company’s web site (www.cardero.com), Canadian regulatory filings on SEDAR at www.sedar.com and United States regulatory filings on EDGAR at www.sec.gov.

On Behalf of the Board of Directors of

CARDERO RESOURCE CORP.

“Henk van Alphen” (signed)

Hendrik van Alphen

Chief Executive Officer and President

Contact Information: Andrew Muir

Direct Tel: 604 638-3287

---

Mal schauen, ob Henk das rumreissen kann.

Cardero Announces Resignation of CEO

NR13-06 March 20, 2013.

Vancouver, British Columbia…Cardero Resource Corp. (“Cardero” or the “Company”) (TSX: CDU, NYSE-MKT: CDY) announces that Michael Hunter has resigned as the Chief Executive Officer and President, and as a director, of the Company, effective March 19, 2013. The Company would like to thank Michael for his service and significant contribution to the Company. The Board of Directors has appointed Hendrik van Alphen as the new Chief Executive Officer and President of the Company.

About Carbon Creek

The Company’s flagship asset is the Carbon Creek Metallurgical Coal Deposit. Carbon Creek is an advanced metallurgical coal development project located in the Peace River Coal District of northeast British Columbia, Canada. The project has a current reserve of 121 million tonnes, included within a 468 million tonne measured and indicated resource, of ASTM Coal Rank mvB coal. Having completed acquisition of the project in June 2011, the Company released results of an independent preliminary economic assessment in December 2011, followed by a Prefeasibility Study (“PFS”) in September 2012. The PFS estimates an undiscounted cash flow of $2.2 billion, an NPV8 of $633 million, and an IRR of 24% (all on a post-tax, 75% basis). The Company is currently undertaking a bankable feasibility study on the project.

For details with respect to the work done to date and the assumptions underlying the current resource and reserve estimates and prefeasibility study, see the technical report entitled “Technical Report, Prefeasibility Study of the Carbon Creek Coal Property, British Columbia, Canada” dated November 6, 2012 with an effective date of September 20, 2012 and available under the Company’s profile at www.sedar.com.

EurGeol Keith Henderson, PGeo, Cardero’s Executive Vice President and a qualified person as defined by National Instrument 43-101, has reviewed the scientific and technical information that forms the basis of this news release, and has approved the disclosure herein. Mr. Henderson is not independent of the Company, as he is an officer and shareholder.

About Cardero Resource Corp.

The common shares of the Company are currently listed on the Toronto Stock Exchange (symbol CDU), the NYSE-MKT (symbol CDY) and the Frankfurt Stock Exchange (symbol CR5). For further details on the Company readers are referred to the Company’s web site (www.cardero.com), Canadian regulatory filings on SEDAR at www.sedar.com and United States regulatory filings on EDGAR at www.sec.gov.

On Behalf of the Board of Directors of

CARDERO RESOURCE CORP.

“Henk van Alphen” (signed)

Hendrik van Alphen

Chief Executive Officer and President

Contact Information: Andrew Muir

Direct Tel: 604 638-3287

---

Mal schauen, ob Henk das rumreissen kann.

Das koennte neue Optionen ermöglichen. Hunter ist bei First Coal ausgestiegen, weil hier der Weg in Richtung Verkauf ging. First Coal wurde spaeter verkauft.

Da ist auch nix durchgesickert:

CDU: 0.26 +0.01 4.0 80.2k

CDU: 0.26 +0.01 4.0 80.2k

Was wohl aus dem >Rest den Coalhunter-Teams bei Cardero wird:

http://www.coalhunter.com/CMC-Presentation.pdf

http://www.coalhunter.com/CMC-Presentation.pdf

Zitat von boersenbrieflemming: Das koennte neue Optionen ermöglichen. Hunter ist bei First Coal ausgestiegen, weil hier der Weg in Richtung Verkauf ging. First Coal wurde spaeter verkauft.

Woher du immer deinen Optimismus hast. Der Michel hat das sinkende Schiff verlassen, nachdem er abkassiert hat und den Laden nun völlig an die Wand gefahren hat.

Welchen Grund sollte er denn haben, weiterhin bei Cardero zu bleiben, falls in nährerer Zukunft irgendwo ein Licht am Ende des Tunnels sein sollte.

Was für ein schei.... Laden!!!!!!!!!!!!!! Leider kann ich absolut nichts positives mehr über Cardero sagen.

Ich könnte mich so in den Arsch beissen, dass ich nicht rechtzeitig die Reissleine gezogen habe.

Zitat von boersenbrieflemming: So, das war es wohl mit dem Coalhunter-Team:

Cardero Announces Resignation of CEO

NR13-06 March 20, 2013.

Vancouver, British Columbia…Cardero Resource Corp. (“Cardero” or the “Company”) (TSX: CDU, NYSE-MKT: CDY) announces that Michael Hunter has resigned as the Chief Executive Officer and President, and as a director, of the Company, effective March 19, 2013. The Company would like to thank Michael for his service and significant contribution to the Company. The Board of Directors has appointed Hendrik van Alphen as the new Chief Executive Officer and President of the Company.

....

"...significant contribution to the Company."

dass ich nicht lache....

Antwort auf Beitrag Nr.: 44.279.370 von gustel66 am 21.03.13 00:54:20Woher du immer deinen Optimismus hast.

Das war gar nicht so optimistisch gemeint. Hunter hat extrem gut verdient (Verkauf First Coal,

Verkauf Carbon Creek) und konnte in Carbon Creek nur einen Anreiz fuer sich persoenlich sehen: die Produktion.

Das ist nunter den Marktbedingungen schwer machbar, stell Dir bitte einmal eine Finanzierung mittels Dilution (50% von ueber 400 Mio.)zum derzeitigen Sharepreis vor. Somit ist er folgerichtig zurückgetreten und überlaesst anderen den

Aufraeumdienst.

Das war gar nicht so optimistisch gemeint. Hunter hat extrem gut verdient (Verkauf First Coal,

Verkauf Carbon Creek) und konnte in Carbon Creek nur einen Anreiz fuer sich persoenlich sehen: die Produktion.

Das ist nunter den Marktbedingungen schwer machbar, stell Dir bitte einmal eine Finanzierung mittels Dilution (50% von ueber 400 Mio.)zum derzeitigen Sharepreis vor. Somit ist er folgerichtig zurückgetreten und überlaesst anderen den

Aufraeumdienst.

!

Dieser Beitrag wurde von CloudMOD moderiert. Grund: SPAM

Im Moment kann man nicht bewerten ob es positiv oder negativ ist. Beides ist möglich - wir müssen abwarten was mit CC passiert.

Wenn Hunter wirklich so clever war die über 100 Mio von Cardero für sein Projekt abzugreifen und es (unter dem Vorwand der nicht aufbringbaren Lizenzkosten) dann auch noch mit in seine nächste Company nimmt sollte er sich auf was gefasst machen. Ich werde mir das nicht gefallen lassen und die Leute die hier neulich noch fast 8 Mio. an frischem Kapital eingebracht haben sicher auch nicht.

Verbleibt Carbon Creek bei CDU, ist es eine positive Nachricht denn dann wird es einen Verkauf geben der wohl unmöglich billiger als die derzeitige MK sein kann.

Stefan

Wenn Hunter wirklich so clever war die über 100 Mio von Cardero für sein Projekt abzugreifen und es (unter dem Vorwand der nicht aufbringbaren Lizenzkosten) dann auch noch mit in seine nächste Company nimmt sollte er sich auf was gefasst machen. Ich werde mir das nicht gefallen lassen und die Leute die hier neulich noch fast 8 Mio. an frischem Kapital eingebracht haben sicher auch nicht.

Verbleibt Carbon Creek bei CDU, ist es eine positive Nachricht denn dann wird es einen Verkauf geben der wohl unmöglich billiger als die derzeitige MK sein kann.

Stefan

Antwort auf Beitrag Nr.: 44.279.912 von Stefan0310 am 21.03.13 09:04:24Sie brauchen Geld fuer Carbon Creek und es wird nicht einfach hier genug aufzutreiben, haetten sie Hunter vor einem Dreiviertiel Jahr gefeuert (vor der PFS), dann waere ich wesentlich optimistischer. Bei den duerren Abschiedsworten gehe ich von einem Feuern aus. Der Mann hat versagt und Cardero an den Rand des Kollaps geritten. Zu Sprott braucht man nicht mehr viel zu schreiben.

Sie haben nun mehrere Optionen und jeder der geschäftlich aktiv ist (und damit auch schwierige Situationen kennt) weiß, dass ein Gegenueber nie das Gefuehl haben darf, dass dem Verhandelnen das Wasser bis zum Hals steht. Das ist bei Public Companies schwer zu überspielen. Es gibt jetzt mehr Optionen, allerdings aus einer sehr ungünstigen Position heraus.

Ein weiteres Fakt ist nicht unbedeutend, Hunter haelt ca. 1 Mio. Shares, die er auf den Markt werden kann, Versager denken da sicherlich nicht an irgendein kursschonendes Verhalten, sondern brauchen Bestaetigung das der Laden ohne sie abraucht.

Sie haben nun mehrere Optionen und jeder der geschäftlich aktiv ist (und damit auch schwierige Situationen kennt) weiß, dass ein Gegenueber nie das Gefuehl haben darf, dass dem Verhandelnen das Wasser bis zum Hals steht. Das ist bei Public Companies schwer zu überspielen. Es gibt jetzt mehr Optionen, allerdings aus einer sehr ungünstigen Position heraus.

Ein weiteres Fakt ist nicht unbedeutend, Hunter haelt ca. 1 Mio. Shares, die er auf den Markt werden kann, Versager denken da sicherlich nicht an irgendein kursschonendes Verhalten, sondern brauchen Bestaetigung das der Laden ohne sie abraucht.

... andererseits sind das Dinge die Henk kann, beim Verkauf von PdP war die Situation vergleichbar.

Antwort auf Beitrag Nr.: 44.280.240 von boersenbrieflemming am 21.03.13 10:00:09Ich habe kurz nachgeschaut;

Hunter:

Direct Ownership Direct Ownership

Common Shares 1,717,462

Options 1,425,000

Warrants 262,870

Quelle: inkresearch.com

Zu den Optionen findet sich mehr in den MD&A (S. 30). Man kann da durchaus den 1. Juni im Blick haben.

Hunter:

Direct Ownership Direct Ownership

Common Shares 1,717,462

Options 1,425,000

Warrants 262,870

Quelle: inkresearch.com

Zu den Optionen findet sich mehr in den MD&A (S. 30). Man kann da durchaus den 1. Juni im Blick haben.

Nur 380k der Optionen sind im Geld, der große Rest wird vermutlich - wie bei CDU üblich - wertlos verfallen. Das mit den 1,7 Mio. Shares sehe ich so:

- sind wir Carbon Creek los wird das hier eh ein Totalverlust da ändern die 1,7 Mio Hunter Shares auch nix dran

- wird Carbon Creek verkauft wird auch Hunter mit dem Verkauf warten bis er die Shares teurer los wird

Entgegen Deiner Meinung halte ich ihn für cleverer als den Rest des CDU MMs zusammen. Sein scheinbares "Versagen" ist darauf zurückzufähren dass ihm die CDU Shareholder egal da - in dem Punkt sind sind sie sich alle einig.

Stefan

- sind wir Carbon Creek los wird das hier eh ein Totalverlust da ändern die 1,7 Mio Hunter Shares auch nix dran

- wird Carbon Creek verkauft wird auch Hunter mit dem Verkauf warten bis er die Shares teurer los wird

Entgegen Deiner Meinung halte ich ihn für cleverer als den Rest des CDU MMs zusammen. Sein scheinbares "Versagen" ist darauf zurückzufähren dass ihm die CDU Shareholder egal da - in dem Punkt sind sind sie sich alle einig.

Stefan

Ich habe nicht geschrieben, dass ich ihn fuer nicht clever halte. Ich habe, wie Du auch im Hinterkopf, dass hier durchaus eine Coalhunter II entstehen koennte. Kapital dürfte von seiner Seite vorhanden sein. Dann haette er tatsächlich alle gelinkt und koennte dann in ein zwei Jahren einen schicken Deal machen - wie man lesen konnte fasziniert in Carbon Creek schon seit Ewigkeiten., das wird nicht aus seinem Kopf sein.

----

Was mich gerade interessiert ist Donkin

Morien Resources Corp. interested in purchasing Donkin mine

...

. However, Istomin said it is only one mine and that in the past four or five years Xstrata has been combining three or four mines together in complexes.

http://www.capebretonpost.com/News/Local/2013-03-20/article-…

Fuer Carbon Creek sieht es nicht so uebel aus, vor allen dann nicht wenn Glencore und Xstata ihren Merger abschließen und in der Nachbarschaft eine ueber 50 Mrd. Company buddelt. Die Frage bleibt nur, ob Cardero davon etwas hat.

----

Was mich gerade interessiert ist Donkin

Morien Resources Corp. interested in purchasing Donkin mine

...

. However, Istomin said it is only one mine and that in the past four or five years Xstrata has been combining three or four mines together in complexes.

http://www.capebretonpost.com/News/Local/2013-03-20/article-…

Fuer Carbon Creek sieht es nicht so uebel aus, vor allen dann nicht wenn Glencore und Xstata ihren Merger abschließen und in der Nachbarschaft eine ueber 50 Mrd. Company buddelt. Die Frage bleibt nur, ob Cardero davon etwas hat.

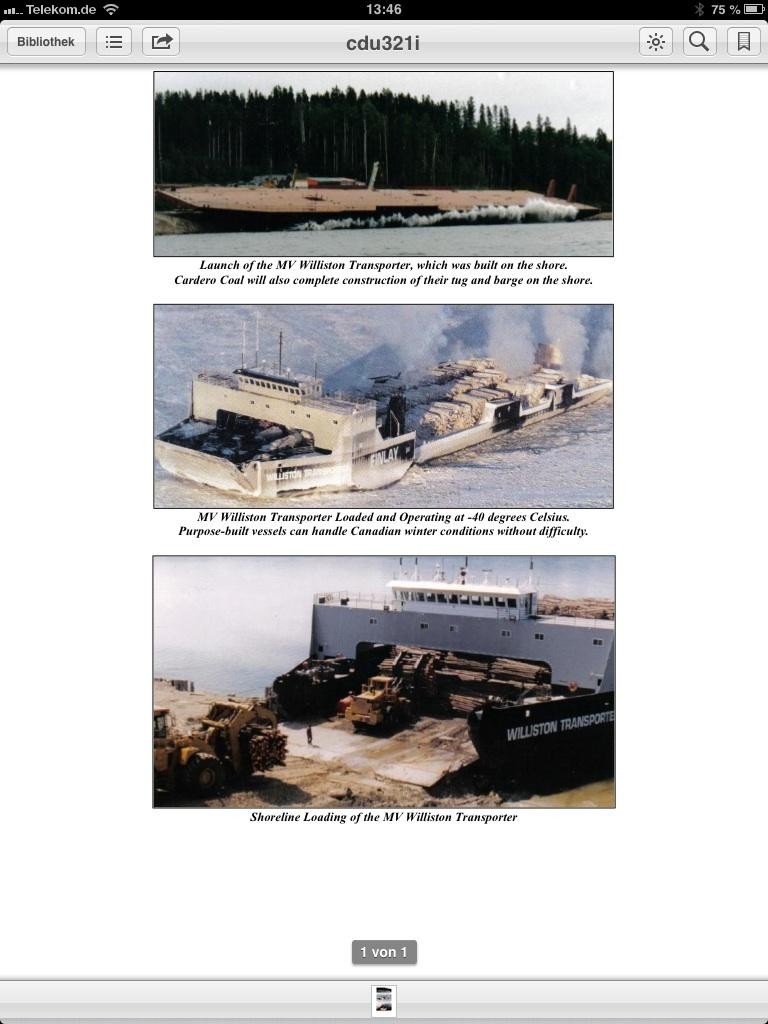

CARDERO SECURES ACCESS TO COAL TRANSPORTATION BARGE

Cardero Resource Corp.'s Cardero Coal Ltd. has signed a letter of intent with Canadian Forest Products Ltd. outlining the terms under which Cardero Coal will charter the Williston Transporter for transportation of metallurgical coal from Carbon Creek to the railhead at Mackenzie, B.C. This charter party arrangement will terminate at the end of 2015, at which time it is anticipated that Cardero Coal's purpose-built tug and barge will be commissioned to transport coal through the remainder of the currently proposed mine life.

Under the terms of the LOI, the Companies will enter into two definitive agreements, being a Charter Party relating to the MV Williston Transporter and a Timber Harvesting Agreement relating to mine site logging prior to mine construction. Cardero Coal will pay for the charter of the MV Williston Transporter, but anticipates receiving revenue from the logging of the mine site under the Timber Harvesting Agreement.

MV Williston Transporter

Cardero Coal intends to transport coal from the proposed Carbon Creek mine site to the railhead at Mackenzie via the Williston Reservoir, using a tug and barge system. It is anticipated that Cardero Coal's purpose-built tug and barge solution will be constructed on site at Mackenzie. A Request for Qualification has been circulated to engineering firms with marine experience and responses are currently under review. It is anticipated that the final design and tender process will begin in Q2 and will be completed in early Q3 2013.

Cardero Coal intends to use the MV Williston Transporter as an interim solution during construction, initial production and ramp-up at Carbon Creek. The MV Williston Transporter is a 360 foot, 7,400 horsepower, self-propelled ice-breaking barge with a deadweight capacity of 4,000 tonnes. The vessel was constructed for Canfor Mackenzie in 1994 by Findlay Navigation, who began operations in 1968 as a marine towing business, operating tugs and barges on Williston Reservoir.

The vessel was built on the shores of the Williston Reservoir and has been in service since 1995, providing year-round transportation services for forestry and mining industries located on the shores of the reservoir. The vessel will be chartered by Cardero Coal, on a bareboat basis, in July 2014 for 18 months and will initially assist with transportation of mine construction plant and materials from Mackenzie railhead to the mine site. Once initial coal has been produced, it is planned that the vessel will switch to metallurgical coal transportation from the mine site to Mackenzie. Since the vessel can be loaded directly from shore, it will not be necessary to complete construction of material handling systems prior to shipping the first product.

To view the photos accompanying this release, please visit the following link: http://media3.marketwire.com/docs/cdu321i.pdf

The foregoing arrangements are subject to, amongst other things, the settlement and execution of the definitive Charter Party and Timber Harvesting Agreement and receipt of all required approvals and consents.

EurGeol Keith Henderson, PGeo, Cardero's Executive Vice President and a qualified person as defined by National Instrument 43-101, has reviewed the scientific and technical information that forms the basis of this news release, and has approved the disclosure herein. Mr. Henderson is not independent of the Company, as he is an officer and shareholder.

Cardero Resource Corp.'s Cardero Coal Ltd. has signed a letter of intent with Canadian Forest Products Ltd. outlining the terms under which Cardero Coal will charter the Williston Transporter for transportation of metallurgical coal from Carbon Creek to the railhead at Mackenzie, B.C. This charter party arrangement will terminate at the end of 2015, at which time it is anticipated that Cardero Coal's purpose-built tug and barge will be commissioned to transport coal through the remainder of the currently proposed mine life.

Under the terms of the LOI, the Companies will enter into two definitive agreements, being a Charter Party relating to the MV Williston Transporter and a Timber Harvesting Agreement relating to mine site logging prior to mine construction. Cardero Coal will pay for the charter of the MV Williston Transporter, but anticipates receiving revenue from the logging of the mine site under the Timber Harvesting Agreement.

MV Williston Transporter

Cardero Coal intends to transport coal from the proposed Carbon Creek mine site to the railhead at Mackenzie via the Williston Reservoir, using a tug and barge system. It is anticipated that Cardero Coal's purpose-built tug and barge solution will be constructed on site at Mackenzie. A Request for Qualification has been circulated to engineering firms with marine experience and responses are currently under review. It is anticipated that the final design and tender process will begin in Q2 and will be completed in early Q3 2013.

Cardero Coal intends to use the MV Williston Transporter as an interim solution during construction, initial production and ramp-up at Carbon Creek. The MV Williston Transporter is a 360 foot, 7,400 horsepower, self-propelled ice-breaking barge with a deadweight capacity of 4,000 tonnes. The vessel was constructed for Canfor Mackenzie in 1994 by Findlay Navigation, who began operations in 1968 as a marine towing business, operating tugs and barges on Williston Reservoir.

The vessel was built on the shores of the Williston Reservoir and has been in service since 1995, providing year-round transportation services for forestry and mining industries located on the shores of the reservoir. The vessel will be chartered by Cardero Coal, on a bareboat basis, in July 2014 for 18 months and will initially assist with transportation of mine construction plant and materials from Mackenzie railhead to the mine site. Once initial coal has been produced, it is planned that the vessel will switch to metallurgical coal transportation from the mine site to Mackenzie. Since the vessel can be loaded directly from shore, it will not be necessary to complete construction of material handling systems prior to shipping the first product.

To view the photos accompanying this release, please visit the following link: http://media3.marketwire.com/docs/cdu321i.pdf

The foregoing arrangements are subject to, amongst other things, the settlement and execution of the definitive Charter Party and Timber Harvesting Agreement and receipt of all required approvals and consents.

EurGeol Keith Henderson, PGeo, Cardero's Executive Vice President and a qualified person as defined by National Instrument 43-101, has reviewed the scientific and technical information that forms the basis of this news release, and has approved the disclosure herein. Mr. Henderson is not independent of the Company, as he is an officer and shareholder.

So sieht das dann aus.

Die Börse weiß wohl auch nicht so recht was sie mit der Hunter News anfangen soll. Ich wage mal die Prognose dass sich der Kurs in den nächsten 4 Wochen um mindestens 15 Cent verändern wird. Da völlig unklar ist in welche Richtung ist CDU bestenfalls ein "Hold". Wer jetzt kauft geht besser ins Casino an den Roulettetisch und setzt auf rot oder schwarz. Die Chancen auf einen Verdoppler dürften dort besser sein und steuerfrei ist es noch dazu...

Ich für meinen Teil werde den Mist erstmal behalten und die anstehenden News zu Carbon Creek abwarten. Eine eventuelle kräftige Erholung nach einem Verkauf würde mich mehr ärgern als wenn die restlichen 20% auch noch Futsch sind.

Stefan

Ich für meinen Teil werde den Mist erstmal behalten und die anstehenden News zu Carbon Creek abwarten. Eine eventuelle kräftige Erholung nach einem Verkauf würde mich mehr ärgern als wenn die restlichen 20% auch noch Futsch sind.

Stefan

Antwort auf Beitrag Nr.: 44.283.249 von Stefan0310 am 21.03.13 18:08:25Das im Moment starke, bzw. staerkere OB liegt an zwei Analysten-Empfehlungen:

Macquarie: Outperform and $1.25 target for CDU

According to Macquarie Research:

Cardero Resource

Change at the top

Event

- New President and CEO. Yesterday after the close Cardero announced that President and CEO Michael Hunter resigned from the company. The Board of Directors has appointed Hendrik van Alphen as the new CEO and President of Cardero.

Impact

- Neutral – a familiar name taking the seat. Mr Van Alphen has over 27 years of experience in the mining industry and has been a director of the company since 1999. We also note that he was previously the CEO of Cardero from 2001 to 2011. With Executive Vice President Keith Henderson and COO Angus Christie

remaining in place Cardero retains two of the key technical people for Carbon Creek.

- Resetting expectations. With the change at the top we are taking the opportunity to reset our expectations on the timeline to first production. We continue to believe that Carbon Creek is a high quality metallurgical coal development project, but given the reality of the current financing market and the lack of a strategic partner we find it increasingly unlikely that first production will be achieved in late 2014. As a result we are pushing the start date out by one year to late 2015. We remain hopeful that Cardero can attract a strategic partner in the near term to assist with project financing to develop Carbon Creek.

Earnings and target price revision

- NAV down to $1.60/sh, target down to $1.25/sh. With the adjustment to our start date our NAV decreases to $1.60/sh from $2.25/sh previously and we are lowering our target price to $1.25 from $2.25 previously. Our target reflects a discount of 23% to our NAV. Our earnings and cashflow estimates are also adjusted to reflect our revised timeline.

Price catalyst

- 12-month price target: C$1.25 based on a discount to NAV methodology.

- Catalyst: A feasibility study on Carbon Creek in 2Q13. Ongoing permitting. A rail access agreement. Potential negotiation of an offtake / financing partnership. Monetization of its interest in Sheini Hills. Closing the Sprott debt facility.

Action and recommendation

- We maintain our Outperform rating. We continue to believe that the September 2012 pre-feasibility study on Carbon Creek highlights the potential for Cardero to develop a large scale metallurgical coal project in an established coal field in Canada. For patient investors, the stock offers compelling value at current levels trading at 0.16x our NAV estimate.

Read more at http://www.stockhouse.com/bullboards/messagedet…

und

According to Desjardins Securities:

Cardero Resource Corp. (CDU C$0.26, TSX)

CEO departure may stall Carbon Creek development; maintaining Hold rating but reducing target to C$0.65 from C$0.90

The Desjardins Takeaway

Michael Hunter has resigned as President, CEO and Director of Cardero Resource Corp. He will be replaced by Hendrik van Alphen, the company’s founder and former CEO (2001–11). We are cautious about the change as we believe it could result in delays to our expected project development timeline, given Mr Hunter was a strong supporter of the project. We continue to rate Cardero Hold–Speculative at this time; however, we have reduced our target price to C$0.65/share from C$0.90/share as a result of the delays to our expected project development timeline.

Highlights

Cardero Resource Corp. announced yesterday the departure of President, CEO and Director Michael Hunter, effective March 19, 2013. Hendrik (Henk) van Alphen has been named as the permanent replacement to Mr Hunter. Mr van Alphen founded Cardero in 1999 and served as CEO from 2001–11. He was also involved in the establishment of the Cardero Group of Companies.

We are cautious as the company could slow development of the company’s flagship Carbon Creek asset in light of Mr Hunter’s departure, given he was a strong supporter of the property. Cardero acquired the Carbon Creek metallurgical coal property though the acquisition of CoalHunter in 2011.

Mr Hunter founded CoalHunter in 2008 and was instrumental in securing the rights to Carbon Creek. Project development is likely behind our previous estimates. We had expected that significant capital spending on the Carbon Creek project would begin in early FY13 (November 2012–October 2013).

Given the low capex spending reported in 4Q FY12 (August–October 2012), we have pushed back our expected development of Carbon Creek by nine months. We now expect significant capital spending to begin in 4Q FY13 (August–October 2013), from 1Q FY13 previously.

Valuation

We continue to value Cardero based on a 0.3x target multiple to our primary asset NAV and a 1.0x multiple to our current working capital and corporate adjustments.

Recommendation

We continue to rate Cardero Hold–Speculative at this time; however, we have reduced our one-year target price to C$0.65/share from C$0.90/share previously as a result of the delays to our expected project development timeline and updates to our estimates for 1Q FY13 actual results.

Read more at http://www.stockhouse.com/bullboards/messagedetail.aspx?p=0&…

OB aktuell:

Ask

0.29 10,500 2

0.285 3,000 2

0.28 8,500 5

0.275 1,000 1

0.27 3,000 3

Bid

0.265 6,000 2

0.26 20,500 5

0.255 17,000 3

0.25 14,500 3

0.245 2,000 2

Macquarie: Outperform and $1.25 target for CDU

According to Macquarie Research:

Cardero Resource

Change at the top

Event