Marvel Gold ehemals Graphex Mining - After Tax NPV 480 Mio AUD bei 16 Mio Börsenwert - world leadin (Seite 211)

eröffnet am 20.09.18 11:00:04 von

neuester Beitrag 28.02.23 09:04:40 von

neuester Beitrag 28.02.23 09:04:40 von

Beiträge: 3.976

ID: 1.288.876

ID: 1.288.876

Aufrufe heute: 0

Gesamt: 207.244

Gesamt: 207.244

Aktive User: 0

ISIN: AU0000102154 · WKN: A2QB8V · Symbol: GR2

0,0055

EUR

0,00 %

0,0000 EUR

Letzter Kurs 10.05.24 Tradegate

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,0000 | +809,09 | |

| 8,0000 | +45,45 | |

| 11,000 | +19,57 | |

| 1,6640 | +16,04 | |

| 527,60 | +15,68 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 6,6800 | -8,94 | |

| 0,7000 | -10,26 | |

| 324,70 | -10,30 | |

| 0,6601 | -26,22 | |

| 47,33 | -97,99 |

Beitrag zu dieser Diskussion schreiben

Syrah heute mit schlechten Nachrichten.

... Spot natural flake graphite (“graphite”) prices in China have suddenly and materially decreased across all flake sizes impacting existing contract price re-negotiations and contract renewal discussions.

Ab Q4/2019 wollen sie die Produktion auf 5kT/month runterfahren.

Quelle: http://www.syrahresources.com.au/investors/downloads/750

... Spot natural flake graphite (“graphite”) prices in China have suddenly and materially decreased across all flake sizes impacting existing contract price re-negotiations and contract renewal discussions.

Ab Q4/2019 wollen sie die Produktion auf 5kT/month runterfahren.

Quelle: http://www.syrahresources.com.au/investors/downloads/750

Übrigens hat Geologist Dr Chris Baker, der Graphex ein Kursziel von 1,63 AUD bescheinigt, im Januar 2019 Liontown bei 2,4c ein Kursziel von 12c benannt.

Es ging auf 15c hoch, aktuell 9c

https://resourcesrisingstars.com.au/news-article/former-top-…

Wollen wir mal hoffen, daß Dr Chris Baker bei Graphex genau so gut liegt.

Es ging auf 15c hoch, aktuell 9c

https://resourcesrisingstars.com.au/news-article/former-top-…

Wollen wir mal hoffen, daß Dr Chris Baker bei Graphex genau so gut liegt.

Antwort auf Beitrag Nr.: 61.405.160 von Reiners am 04.09.19 08:10:53Update on Tanzania

• As we detailed in our recent report, GPX has been working well to advance permitting of its Chilalo

graphite project. Despite all the issues attached to recent changes to the Tanzanian Mining Act, GPX

appears to have been highly successful in navigating a reasonable outcome. This will, of course,

involve a 16% free carried interest to the GoT. This is incorporated in our GPX valuation.

• A merger of Barrick and Acacia – now virtually fait accompli -should allow payment of the outstanding

tax liability following completion of the takeover, likely in 4Q19. This should then open the doors for

Tanzanian mining projects.

• Of the five graphite pre-development companies in Tanzania, GPX is by far the most advanced, with

a financing solution at hand. As far as we are aware, none of the other graphite ‘hopefuls’ have been

able to secure project debt facilities.

Our investment thoughts on GPX

• Based on our assumptions GPX is remarkably inexpensive. Even if we assume our valuation is wrong

by a factor of 2, or even 3, the stock is still dramatically underpriced.

• We understand that Tanzanian resources exposures should trade at a discount. But with an imminent

resolution of the Acacia situation, we believe the country is open for business. Our country visit

earlier in the year confirmed this view.

• Our recent experience in the graphite sector suggests investors still do not understand the graphite

sector. It is a small industrial mineral sector, and commodity supply/demand dynamics are far from

clear. To use Syrah Resources as a benchmark is simply comparing apples and oranges. GPX is not

trying to participate in the small flake graphite market.

• Without wishing to make the point too strongly, IT IS NOT POSSIBLE FOR SYRAH RESOURCES TO

PARTICIPATE MATERIALLY IN THE LARGE FLAKE GRAPHITE MARKET. It is simply not possible. The

characteristics of the Balama orebody does not allow it. Oversupply of fine flake graphite is unlikely

to impact the large flake producers.

• As we understand it the supply/demand dynamics for large flake graphite is very strong. Pricing

remains robust, and seems likely to remain so for some time.

• As we detailed in our recent report, GPX has been working well to advance permitting of its Chilalo

graphite project. Despite all the issues attached to recent changes to the Tanzanian Mining Act, GPX

appears to have been highly successful in navigating a reasonable outcome. This will, of course,

involve a 16% free carried interest to the GoT. This is incorporated in our GPX valuation.

• A merger of Barrick and Acacia – now virtually fait accompli -should allow payment of the outstanding

tax liability following completion of the takeover, likely in 4Q19. This should then open the doors for

Tanzanian mining projects.

• Of the five graphite pre-development companies in Tanzania, GPX is by far the most advanced, with

a financing solution at hand. As far as we are aware, none of the other graphite ‘hopefuls’ have been

able to secure project debt facilities.

Our investment thoughts on GPX

• Based on our assumptions GPX is remarkably inexpensive. Even if we assume our valuation is wrong

by a factor of 2, or even 3, the stock is still dramatically underpriced.

• We understand that Tanzanian resources exposures should trade at a discount. But with an imminent

resolution of the Acacia situation, we believe the country is open for business. Our country visit

earlier in the year confirmed this view.

• Our recent experience in the graphite sector suggests investors still do not understand the graphite

sector. It is a small industrial mineral sector, and commodity supply/demand dynamics are far from

clear. To use Syrah Resources as a benchmark is simply comparing apples and oranges. GPX is not

trying to participate in the small flake graphite market.

• Without wishing to make the point too strongly, IT IS NOT POSSIBLE FOR SYRAH RESOURCES TO

PARTICIPATE MATERIALLY IN THE LARGE FLAKE GRAPHITE MARKET. It is simply not possible. The

characteristics of the Balama orebody does not allow it. Oversupply of fine flake graphite is unlikely

to impact the large flake producers.

• As we understand it the supply/demand dynamics for large flake graphite is very strong. Pricing

remains robust, and seems likely to remain so for some time.

Graphex Mining (GPX AU, market cap A$19m)

Update: Significant resource upgrade confirms a +15 year mine life is achievable

Bridge Street sieht Minelife von über 15 Jahre für möglich.

Kursziel bleibt bei 1,63 AUD.

Das ist mehr als eine Verachtfachung vom jetzigen Niveau.

http://www.graphexmining.com.au/wp-content/uploads/2019/09/2…

Update: Significant resource upgrade confirms a +15 year mine life is achievable

Bridge Street sieht Minelife von über 15 Jahre für möglich.

Kursziel bleibt bei 1,63 AUD.

Das ist mehr als eine Verachtfachung vom jetzigen Niveau.

http://www.graphexmining.com.au/wp-content/uploads/2019/09/2…

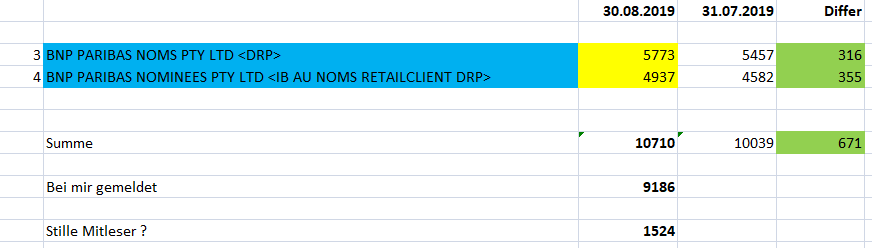

Naja, die "Deutschen" scheinen im August um 671.000 Stücke erhöht zu haben. Davon waren 157.000 von mir für ein Familienmitglied.

-----

Stille Mitleser demnach ca. 1,5 Mio Stücke, wenn in den beiden BNP Positionen nicht noch Anleger von anderen Ländern drin sein sollten, wovon ich kaum ausgehe und zweites, Deutsche nicht noch in anderen Top 50 Postionen enthalten sind, wovon ich auch nicht unbedingt ausgehe.

Ausnahme Leute wie Wilhelm Schröder oder Peter David Koller, die schon immer separat gemeldet waren und ich in meinen 9,2 Mio Stücke sowieso nie drin hatte.

-----

Stille Mitleser demnach ca. 1,5 Mio Stücke, wenn in den beiden BNP Positionen nicht noch Anleger von anderen Ländern drin sein sollten, wovon ich kaum ausgehe und zweites, Deutsche nicht noch in anderen Top 50 Postionen enthalten sind, wovon ich auch nicht unbedingt ausgehe.

Ausnahme Leute wie Wilhelm Schröder oder Peter David Koller, die schon immer separat gemeldet waren und ich in meinen 9,2 Mio Stücke sowieso nie drin hatte.

Trading Spotlight

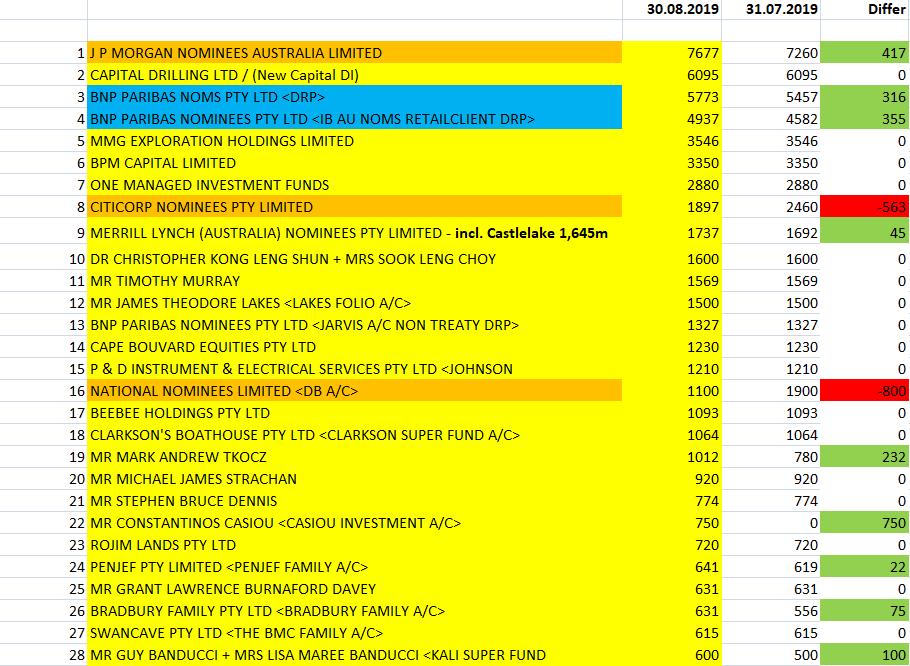

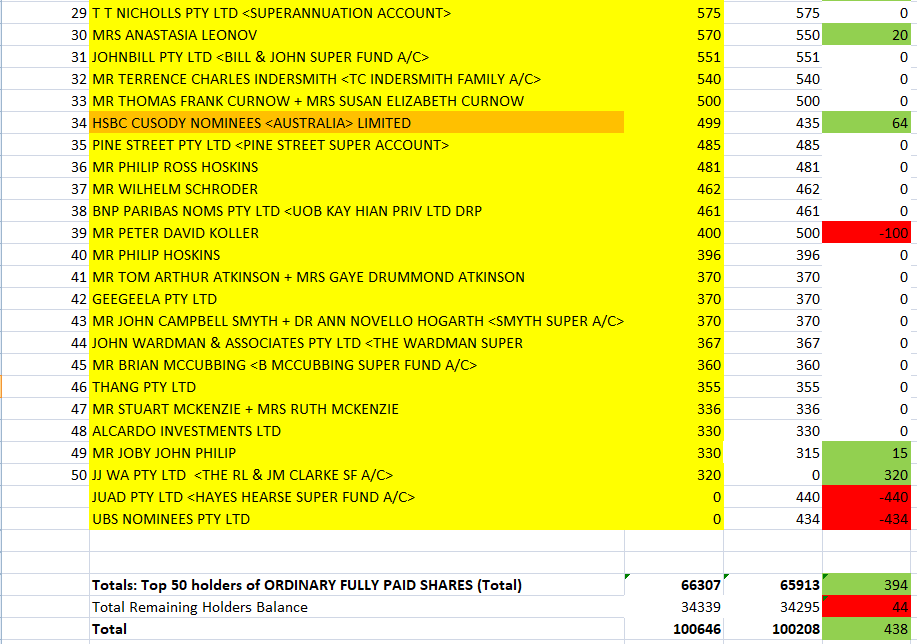

Top 50, kleinere Verschiebungen, weiter sehr stabil.

Antwort auf Beitrag Nr.: 61.385.252 von NoFriPri am 31.08.19 19:02:50Klar liegt es zum einen das die Milestones bei Graphex noch nicht erreicht sind und erst vor uns liegen. Klar liegt es zum zweiten daran, das Graphex noch nicht seine Story erzählt.

Hauptgrund liegt aber am Rohstoff Grafit.

Die ca. 50 bis 60 Grafitwerte weltweit die ich kenne, bzw die an der Börse notiert sind, keiner aber wirklich auch keiner hat die letzten 2 Jahre wirklich performt.

Ausnahme vielleicht Walkabout, aber das war professionelles Gepusche, das viel stupid money reingezogen hat.

Bestes Beispiel Syrah, von über 6,00 Aud auf unter 70 Cent jetzt.

Wann die Grafit Karte mal wieder gespielt wird, keine Ahnung. Vielleicht wenn Syrah irgendwann Geld verdienen sollte oder eine Graphex, Walkabout oder Triton in Produktion kommt und richtig Geld verdient.

Die economics von Graphex sind outstanding und wenn Graphex in Produktion kommt und halbwegs die Mengen und Margen erreicht die geplant sind, kommt eine ganz andere Käufergruppe und spätestens dann geht der Kurs hoch.

Hauptgrund liegt aber am Rohstoff Grafit.

Die ca. 50 bis 60 Grafitwerte weltweit die ich kenne, bzw die an der Börse notiert sind, keiner aber wirklich auch keiner hat die letzten 2 Jahre wirklich performt.

Ausnahme vielleicht Walkabout, aber das war professionelles Gepusche, das viel stupid money reingezogen hat.

Bestes Beispiel Syrah, von über 6,00 Aud auf unter 70 Cent jetzt.

Wann die Grafit Karte mal wieder gespielt wird, keine Ahnung. Vielleicht wenn Syrah irgendwann Geld verdienen sollte oder eine Graphex, Walkabout oder Triton in Produktion kommt und richtig Geld verdient.

Die economics von Graphex sind outstanding und wenn Graphex in Produktion kommt und halbwegs die Mengen und Margen erreicht die geplant sind, kommt eine ganz andere Käufergruppe und spätestens dann geht der Kurs hoch.

Antwort auf Beitrag Nr.: 61.385.252 von NoFriPri am 31.08.19 19:02:5031.07.2019 waren bei mir 8,3 Mio gemeldet.

Die beiden BNP Paribas Positionen waren zum gleichen Zeitpunkt zusammen 10,0Mio Stücke.

Stille Mitleser sollten also maximal 1,7 Mio Stücke haben.

Weiß nicht in welcher Top 50 sonst noch Deutsche stecken sollten.

Die beiden BNP Paribas Positionen waren zum gleichen Zeitpunkt zusammen 10,0Mio Stücke.

Stille Mitleser sollten also maximal 1,7 Mio Stücke haben.

Weiß nicht in welcher Top 50 sonst noch Deutsche stecken sollten.

Antwort auf Beitrag Nr.: 61.368.253 von Reiners am 29.08.19 11:12:15

Ich glaube nicht, dass diese Zahl unbedingt realistisch ist. Ich schätze, dass die Gesamtzahl um Einiges höher sein wird.

Es gibt sehr viele "stille Mitleser" wie mich, die sich aus unterschiedlichen Gründen zurückhalten und ihre Aktivitäten weder im Forum, oder über Bordmails bekannt geben.

Leider zeigt sich die Kursentwicklung bisher nicht zufriedenstellend und der eine oder andere

User wird zwischenzeitlich seine Bestände mit mehr oder weniger hohen Verlusten reduziert haben.

Die Gründe sind hier ausreichend erläutert.

Realistisch gesehen, habe ich mit dem Kauf meiner Graphex-Aktien (die ich nach wie vor halte) und die einen Teil meines Kapitals momentan "blockieren", im Vergleich mit meinem Wheaton Zerti MF5R5Y, (gleicher Kauftermin) das mir bis dato fast einen "Tenbagger" beschert hat, keinen Glücksgriff getätigt.

Ich hoffe, die Zukunft wird mich ein wenig entschädigen. Viel Erfolg bei unserer Graphex-Anlage. Sicher auch im Namen einiger "stiller" Mitleser.

Glückauf NoFriPri

Hallo Reiners,

63 Deutsche halten aktuell 9.186.400 shares, also knapp 9,2% von Graphex.Ich glaube nicht, dass diese Zahl unbedingt realistisch ist. Ich schätze, dass die Gesamtzahl um Einiges höher sein wird.

Es gibt sehr viele "stille Mitleser" wie mich, die sich aus unterschiedlichen Gründen zurückhalten und ihre Aktivitäten weder im Forum, oder über Bordmails bekannt geben.

Leider zeigt sich die Kursentwicklung bisher nicht zufriedenstellend und der eine oder andere

User wird zwischenzeitlich seine Bestände mit mehr oder weniger hohen Verlusten reduziert haben.

Die Gründe sind hier ausreichend erläutert.

Realistisch gesehen, habe ich mit dem Kauf meiner Graphex-Aktien (die ich nach wie vor halte) und die einen Teil meines Kapitals momentan "blockieren", im Vergleich mit meinem Wheaton Zerti MF5R5Y, (gleicher Kauftermin) das mir bis dato fast einen "Tenbagger" beschert hat, keinen Glücksgriff getätigt.

Ich hoffe, die Zukunft wird mich ein wenig entschädigen. Viel Erfolg bei unserer Graphex-Anlage. Sicher auch im Namen einiger "stiller" Mitleser.

Glückauf NoFriPri

Antwort auf Beitrag Nr.: 61.356.088 von 132427 am 28.08.19 02:56:40http://www.mining-journal.com/energy-minerals-news/news/1370…