BANNERMAN - jetzt auch in Frankfurt - 500 Beiträge pro Seite

eröffnet am 13.12.07 10:38:53 von

neuester Beitrag 11.03.14 08:55:29 von

neuester Beitrag 11.03.14 08:55:29 von

Beiträge: 383

ID: 1.136.308

ID: 1.136.308

Aufrufe heute: 0

Gesamt: 28.825

Gesamt: 28.825

Aktive User: 0

ISIN: AU000000BMN9 · WKN: A0EAC6

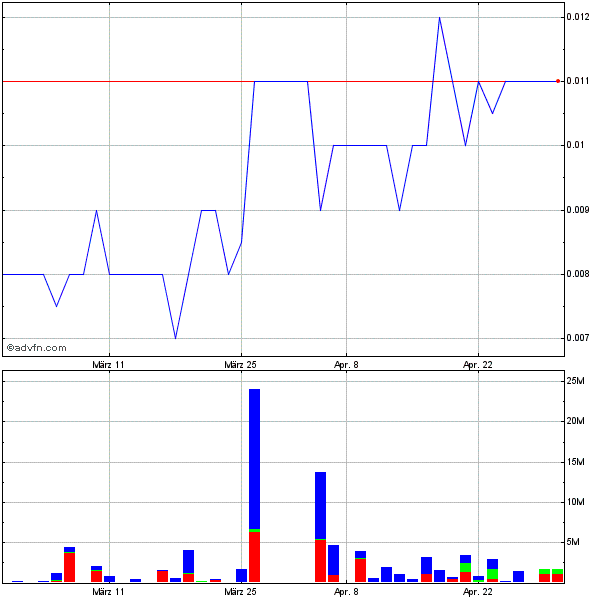

2,7450

EUR

-1,26 %

-0,0350 EUR

Letzter Kurs 07:53:10 Lang & Schwarz

Neuigkeiten

29.04.24 · Der Finanzinvestor |

12.02.24 · Der Finanzinvestor |

18.12.23 · Der Finanzinvestor |

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,0000 | +809,09 | |

| 8,0000 | +45,45 | |

| 11,000 | +19,57 | |

| 1,2000 | +18,05 | |

| 527,60 | +15,68 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 324,70 | -10,30 | |

| 9,8500 | -10,54 | |

| 12,070 | -18,99 | |

| 0,6166 | -19,12 | |

| 0,6601 | -26,22 |

ein sehr interessantes Unternehmen wie mir scheint

ASX: BMN

TSX: BAN

ASX: BMN

TSX: BAN

Bannerman vs Xemplar Energy ein interessanter Vergleich . . .

mit dem kleinen Unterschied, das bei Bannerman im Januar ein resource update

von 100 (+ X) mln lbs ansteht

Uramin wurde mit einer ähnlich großen resource (Trekkopje uranium project

in Namibia) von Areva für 2.5 Mrd übernommen

unter den Nachbarn von Bannerman befinden sich unter anderen:

Rio Tinto

Paladin

Forsys

von 100 (+ X) mln lbs ansteht

Uramin wurde mit einer ähnlich großen resource (Trekkopje uranium project

in Namibia) von Areva für 2.5 Mrd übernommen

unter den Nachbarn von Bannerman befinden sich unter anderen:

Rio Tinto

Paladin

Forsys

Antwort auf Beitrag Nr.: 32.817.514 von DaenischeSuedsee am 19.12.07 17:55:13ein paar andere Nachbarn sind XE, WME und Extract Resources

Trading Spotlight

Fat Prophets initially recommended buying Bannerman

08 Nov, 2006

"Bannerman Resources caught our attention as one of the most prospective

exploration plays that we have seen."

http://www.bannermanresources.com.au/docs/FatProphets08Nov20…

08 Nov, 2006

"Bannerman Resources caught our attention as one of the most prospective

exploration plays that we have seen."

http://www.bannermanresources.com.au/docs/FatProphets08Nov20…

This work has increased the strike length of identified uranium mineralisation

to more than 37km, with a feature known as the Goanikontes dome hosting

22km of this strike length. This works has also found another one of the 12

anomalies, known as Anomaly 11, to be much larger than expected, at 15km

in strike length.

What all of this means is that Bannerman's Welwitschia Project hosts large-scale

targets of outstanding potential. Ongoing drilling work is sure to provide enormous

excitement for Members, in our view.

to more than 37km, with a feature known as the Goanikontes dome hosting

22km of this strike length. This works has also found another one of the 12

anomalies, known as Anomaly 11, to be much larger than expected, at 15km

in strike length.

What all of this means is that Bannerman's Welwitschia Project hosts large-scale

targets of outstanding potential. Ongoing drilling work is sure to provide enormous

excitement for Members, in our view.

Bannerman's Swakop River project meanwhile is just as attractive and surrounds

another world-class uranium deposit, Paladin Resources' Langer Heinrich uranium

mine.

another world-class uranium deposit, Paladin Resources' Langer Heinrich uranium

mine.

. .  . . still flying under the radar ?? Hm, vielleicht auch besser so, Geduld wird

. . still flying under the radar ?? Hm, vielleicht auch besser so, Geduld wird

sich hier auszahlen, Ende Januar steht ein signifikantes resource update an und

durch Xemplar wird auch Bannerman in den Focus vieler Instis gelangen

große Aufregung bei Xemplar wegen Rio Tinto

http://www.news.com.au/dailytelegraph/story/0,22049,23016179…

Bannerman ist deutlich besser aufgestellt und mit weniger als der halben Mk bewertet

http://www.stockhouse.ca/bullboards/forum.asp?symbol=BAN&tab…

. . still flying under the radar ?? Hm, vielleicht auch besser so, Geduld wird

. . still flying under the radar ?? Hm, vielleicht auch besser so, Geduld wird sich hier auszahlen, Ende Januar steht ein signifikantes resource update an und

durch Xemplar wird auch Bannerman in den Focus vieler Instis gelangen

große Aufregung bei Xemplar wegen Rio Tinto

http://www.news.com.au/dailytelegraph/story/0,22049,23016179…

Bannerman ist deutlich besser aufgestellt und mit weniger als der halben Mk bewertet

http://www.stockhouse.ca/bullboards/forum.asp?symbol=BAN&tab…

A grand Namibian plan

When Bannerman Resources managing director

Peter Batten describes an open pit in Namibia

similar in size to that of Rossing, the world’s largest

open pit uranium mine, his vision seems ambitious

– but also achievable. By Kate Haycock

http://www.bannermanresources.com.au/docs/2007/BMN_Resources…

When Bannerman Resources managing director

Peter Batten describes an open pit in Namibia

similar in size to that of Rossing, the world’s largest

open pit uranium mine, his vision seems ambitious

– but also achievable. By Kate Haycock

http://www.bannermanresources.com.au/docs/2007/BMN_Resources…

.

"The current resource stands at 27 mlbs, with the company targeting

a resource upgrade of over 100 mlbs by mid-January 2008 followed

by a final resource estimate by March 2008 targeting over 160 mlbs

U308."

.

"The current resource stands at 27 mlbs, with the company targeting

a resource upgrade of over 100 mlbs by mid-January 2008 followed

by a final resource estimate by March 2008 targeting over 160 mlbs

U308."

.

BAN may be one of the very few bargains left!!!

Paladin now able to look for some bargains

Email Print Normal font Large font AdvertisementAdvertisementJamie Freed

January 15, 2008

oTHE uranium producer Paladin Energy is expected to resume its focus on acquisitions now that it has overcome production issues at its brand new Langer Heinrich mine in Namibia.

The mine, one of the first of a new breed of uranium mines since a recent increase in the price of the nuclear fuel, was unable to meet its original production forecast last year after a failure of its leach tank liners.

"We were in suspension [as a company]," said the managing director of Paladin, John Borshoff. "We couldn't do other things until we got our credibility back and our performance where we said we would be."

Paladin yesterday said it had met its second-half production target of 295 tonnes of uranium from Langer Heinrich.

The mine's production is expected to reach its nameplate capacity of 1179 tonnes this year before a planned expansion to 1678 tonnes.

Mr Borshoff said the board expected to approve the $US40 million ($44.7 million) to $US50 million expansion next month and to complete construction by the end of the year.

"When you look at the guidance of all the uranium companies around the world today, Paladin is one of the few that is maintaining its guidance for 2008," he said. "I think that's a tremendous achievement."

The construction of Paladin's second mine, Kayelekera in Malawi, should be completed by the end of the year. Mr Borshoff said Paladin should produce about 1723 tonnes of uranium from the two mines next year, rising to 2267 tonnes in 2010.

The company, which last year bought the Queensland uranium explorer Summit Resources, has renewed its focus on acquisitions after working through the teething problems at Langer Heinrich.

Since the uranium spot price has fallen from last year's record high of $US138 a pound, the value of many uranium stocks has dived. Mr Borshoff said the drop in the uranium price to its current level of $US90 a pound was "not one iota" of a concern, with the projected strong demand for nuclear power. But the fall in the share prices of uranium companies may help Paladin further its ambitions of buying more projects, particularly in North America.

On Friday Deutsche Bank analysts deemed Paladin their "preferred pick" within the uranium sector with an $8.25 target price.

The analysts said: "We forecast strong earnings growth from the company's stated production guidance and recognise that further upside opportunities are available to the company via production expansions at both Langer Heinrich and Kayelekera."

Paladin shares closed 6c lower at $5.95, after trading to $6.18.

Paladin now able to look for some bargains

Email Print Normal font Large font AdvertisementAdvertisementJamie Freed

January 15, 2008

oTHE uranium producer Paladin Energy is expected to resume its focus on acquisitions now that it has overcome production issues at its brand new Langer Heinrich mine in Namibia.

The mine, one of the first of a new breed of uranium mines since a recent increase in the price of the nuclear fuel, was unable to meet its original production forecast last year after a failure of its leach tank liners.

"We were in suspension [as a company]," said the managing director of Paladin, John Borshoff. "We couldn't do other things until we got our credibility back and our performance where we said we would be."

Paladin yesterday said it had met its second-half production target of 295 tonnes of uranium from Langer Heinrich.

The mine's production is expected to reach its nameplate capacity of 1179 tonnes this year before a planned expansion to 1678 tonnes.

Mr Borshoff said the board expected to approve the $US40 million ($44.7 million) to $US50 million expansion next month and to complete construction by the end of the year.

"When you look at the guidance of all the uranium companies around the world today, Paladin is one of the few that is maintaining its guidance for 2008," he said. "I think that's a tremendous achievement."

The construction of Paladin's second mine, Kayelekera in Malawi, should be completed by the end of the year. Mr Borshoff said Paladin should produce about 1723 tonnes of uranium from the two mines next year, rising to 2267 tonnes in 2010.

The company, which last year bought the Queensland uranium explorer Summit Resources, has renewed its focus on acquisitions after working through the teething problems at Langer Heinrich.

Since the uranium spot price has fallen from last year's record high of $US138 a pound, the value of many uranium stocks has dived. Mr Borshoff said the drop in the uranium price to its current level of $US90 a pound was "not one iota" of a concern, with the projected strong demand for nuclear power. But the fall in the share prices of uranium companies may help Paladin further its ambitions of buying more projects, particularly in North America.

On Friday Deutsche Bank analysts deemed Paladin their "preferred pick" within the uranium sector with an $8.25 target price.

The analysts said: "We forecast strong earnings growth from the company's stated production guidance and recognise that further upside opportunities are available to the company via production expansions at both Langer Heinrich and Kayelekera."

Paladin shares closed 6c lower at $5.95, after trading to $6.18.

Bannerman Resources Ltd. Reports Goanikontes Anomaly A Operational Cost Reductions

Friday January 18, 2:47 pm ET

http://biz.yahoo.com/iw/080118/0350400.html

Friday January 18, 2:47 pm ET

http://biz.yahoo.com/iw/080118/0350400.html

Bannerman sees Goanikontes A major uranium producer

Sunday, January 20, 2008; Posted: 05:32 PM

Sydney, Jan 21, 2008 (RWE via COMTEX) -- BNNLF | news | PowerRating | PR Charts -- (RWE Aust Business News) Bannerman Resources (ASX:BMN) has results from the scoping study at its Namibian project, Goanikontes Anomaly A, which shows the potential to be a major producer of uranium on the world scene.

The project is ideally located close to existing uranium mines and major infrastructure and the study has outlined the potential for an economic and robust project.

The case study for on site acid production is part of the ongoing work that is refining the details for the project economics in areas identified with the potential to reduce the operating costs in the proposed processing plant.

On site acid production not only reduces the project costs but includes the security of supply against third party acid procurement and produces a significant component of the overall project power requirements.

Further improvements to the operating costs may be achievable and the work required to assess these improvements will be included within the scope of the Bankable Feasibility Study scheduled to commence in February 2008.

Bannerman is continuing to progress the project towards development in line with the schedule.

A resource update for Goanikontes Anomaly A will be completed this month.

rweabn.com.au

http://www.tradingmarkets.com/.site/news/Stock%20News/100752…

Sunday, January 20, 2008; Posted: 05:32 PM

Sydney, Jan 21, 2008 (RWE via COMTEX) -- BNNLF | news | PowerRating | PR Charts -- (RWE Aust Business News) Bannerman Resources (ASX:BMN) has results from the scoping study at its Namibian project, Goanikontes Anomaly A, which shows the potential to be a major producer of uranium on the world scene.

The project is ideally located close to existing uranium mines and major infrastructure and the study has outlined the potential for an economic and robust project.

The case study for on site acid production is part of the ongoing work that is refining the details for the project economics in areas identified with the potential to reduce the operating costs in the proposed processing plant.

On site acid production not only reduces the project costs but includes the security of supply against third party acid procurement and produces a significant component of the overall project power requirements.

Further improvements to the operating costs may be achievable and the work required to assess these improvements will be included within the scope of the Bankable Feasibility Study scheduled to commence in February 2008.

Bannerman is continuing to progress the project towards development in line with the schedule.

A resource update for Goanikontes Anomaly A will be completed this month.

rweabn.com.au

http://www.tradingmarkets.com/.site/news/Stock%20News/100752…

A URANIUM EXPLORER MAKES EXCITING FIND BUT SHARES SLIDE

Sydney - Wednesday - January 23: (RWE Aust Business News)

*********************************************************

OVERVIEW

The market has certainly lost confidence when a miner announces that a new uranium discovery has the potential of a major producer but the shares buckle in the current selloff. Shares of Bannerman Resources Ltd (ASX:BMN) yesterday slumped 93c to $2.25 on what should have been a bullish report in any other period.

But the market has fallen 12 sessions in row and every company has been vulnerable to a downturn. On Monday, Bannerman Resources declared it sees its Namibian project, Goanikontes Anomaly A, as a major uranium producer based on results from a scoping study.

The project is ideally located close to existing uranium mines and major infrastructure and the study has outlined the potential for an economic and robust project. The case study for on-site acid production is part of the ongoing

work that is refining the details for the project economics in areas identified with the potential to reduce the operating costs in the proposed processing plant. On-site acid production not only reduces the project costs but includes the security of supply against third-party acid procurement and produces a significant component of the overall project power requirements.

Further improvements to the operating costs may be achievable and the work required to assess these improvements will be included within the scope of the Bankable Feasibility Study scheduled to commence in February.

Bannerman is continuing to progress the project towards development in line with the schedule. A resource update for Goanikontes Anomaly A will be completed this month.

SHARE PRICE MOVEMENTS

*********************

Shares of Bannerman Resources yesterday slumped 93c to $2.27. Rolling high for the year is $4.14 and low 1.30. The company has 132.5 million with a market cap of $298.2 million. But the weakness in the company may not all be due to current market conditions.

In December, Bannerman Resources reported that a company incorporated in Namibia, Savanna Marble Close Corporation, had commenced proceedings in the High Court of Namibia against the Namibian Minister of Mines and Energy, Bannerman's 80 per cent-owned subsidiary Bannerman Mining Resources (Namibia) (Proprietary) and an individual known as Robert D Wirtz who has no connection with Bannerman.

The proceedings sought to seek an order reviewing and correcting or setting aside the decision taken by the Minister of Mines and Energy in Namibia to grant Bannerman Namibia Licence EPL3345 with exclusive mineral rights for the nuclear fuel group of minerals over the area covered by Savanna's EPL3045, or alternatively, orders that the decision by the Minister of Mines and Energy to grant Bannerman Namibia EPL3345 be declared null and void.

Savanna is also seeking the costs of the application. Bannerman said EPL3045 held by Savanna only entitles it to mine stone known as "dimension stone". It is not entitled to explore for or mine any nuclear fuel minerals.

About three months ago Savanna applied to have nuclear fuels added to its licence. This application has not been dealt with and in Bannerman's view is unlikely to be granted. Savanna's EPL3045 is situated north of the Swakop River not near the company's Goanikontes Anomaly A deposit. The area which is the subject of the notice does not overlap on the current drilling program and will not have an impact on the exploration and development work planned by Bannerman Namibia.

Bannerman is not expecting any delays to the current schedule from this action. Savanna has applied for a mining licence indicating the area of economic interest for dimension stone sits on the northern boundary of the company's licence EPL3345.

The mining licence application does not cover any uranium targets currently in the company's inventory. Prior to the commencement of the proceedings Bannerman Namibia had taken advice in relation to many of the matters that are the subject of the proceedings, has formed the view that the proceedings have no proper foundation and are unlikely to succeed. The proceedings will be vigorously defended. Bannerman pointed out that under Namibian law it is possible, and quite common, to have overlapping mining permits for different minerals.

Apart from the Savanna dimension stone prospecting licence there is also a mining licence for copper, a prospecting licence for limestone and an application for mica. Bannerman Namibia does not expect that Savanna's right to mine dimension stone will affect Bannerman's ability to explore for and mine uranium in the overlapping parts of its licences.

Sydney - Wednesday - January 23: (RWE Aust Business News)

*********************************************************

OVERVIEW

The market has certainly lost confidence when a miner announces that a new uranium discovery has the potential of a major producer but the shares buckle in the current selloff. Shares of Bannerman Resources Ltd (ASX:BMN) yesterday slumped 93c to $2.25 on what should have been a bullish report in any other period.

But the market has fallen 12 sessions in row and every company has been vulnerable to a downturn. On Monday, Bannerman Resources declared it sees its Namibian project, Goanikontes Anomaly A, as a major uranium producer based on results from a scoping study.

The project is ideally located close to existing uranium mines and major infrastructure and the study has outlined the potential for an economic and robust project. The case study for on-site acid production is part of the ongoing

work that is refining the details for the project economics in areas identified with the potential to reduce the operating costs in the proposed processing plant. On-site acid production not only reduces the project costs but includes the security of supply against third-party acid procurement and produces a significant component of the overall project power requirements.

Further improvements to the operating costs may be achievable and the work required to assess these improvements will be included within the scope of the Bankable Feasibility Study scheduled to commence in February.

Bannerman is continuing to progress the project towards development in line with the schedule. A resource update for Goanikontes Anomaly A will be completed this month.

SHARE PRICE MOVEMENTS

*********************

Shares of Bannerman Resources yesterday slumped 93c to $2.27. Rolling high for the year is $4.14 and low 1.30. The company has 132.5 million with a market cap of $298.2 million. But the weakness in the company may not all be due to current market conditions.

In December, Bannerman Resources reported that a company incorporated in Namibia, Savanna Marble Close Corporation, had commenced proceedings in the High Court of Namibia against the Namibian Minister of Mines and Energy, Bannerman's 80 per cent-owned subsidiary Bannerman Mining Resources (Namibia) (Proprietary) and an individual known as Robert D Wirtz who has no connection with Bannerman.

The proceedings sought to seek an order reviewing and correcting or setting aside the decision taken by the Minister of Mines and Energy in Namibia to grant Bannerman Namibia Licence EPL3345 with exclusive mineral rights for the nuclear fuel group of minerals over the area covered by Savanna's EPL3045, or alternatively, orders that the decision by the Minister of Mines and Energy to grant Bannerman Namibia EPL3345 be declared null and void.

Savanna is also seeking the costs of the application. Bannerman said EPL3045 held by Savanna only entitles it to mine stone known as "dimension stone". It is not entitled to explore for or mine any nuclear fuel minerals.

About three months ago Savanna applied to have nuclear fuels added to its licence. This application has not been dealt with and in Bannerman's view is unlikely to be granted. Savanna's EPL3045 is situated north of the Swakop River not near the company's Goanikontes Anomaly A deposit. The area which is the subject of the notice does not overlap on the current drilling program and will not have an impact on the exploration and development work planned by Bannerman Namibia.

Bannerman is not expecting any delays to the current schedule from this action. Savanna has applied for a mining licence indicating the area of economic interest for dimension stone sits on the northern boundary of the company's licence EPL3345.

The mining licence application does not cover any uranium targets currently in the company's inventory. Prior to the commencement of the proceedings Bannerman Namibia had taken advice in relation to many of the matters that are the subject of the proceedings, has formed the view that the proceedings have no proper foundation and are unlikely to succeed. The proceedings will be vigorously defended. Bannerman pointed out that under Namibian law it is possible, and quite common, to have overlapping mining permits for different minerals.

Apart from the Savanna dimension stone prospecting licence there is also a mining licence for copper, a prospecting licence for limestone and an application for mica. Bannerman Namibia does not expect that Savanna's right to mine dimension stone will affect Bannerman's ability to explore for and mine uranium in the overlapping parts of its licences.

29/01/2008 ! Trading Halt 2 PDF

29/01/2008 ! Quarterly Cashflow Report 5 PDF

29/01/2008 ! Quarterly Activities Report 16 PDF

http://www.asx.com.au/asx/research/CompanyInfoSearchResults.…

29/01/2008 ! Quarterly Cashflow Report 5 PDF

29/01/2008 ! Quarterly Activities Report 16 PDF

http://www.asx.com.au/asx/research/CompanyInfoSearchResults.…

oh- jetzt gibt auch einen thread

hatte vor paar monaten schonmal geschaut

da gabs noch keinen

ein interessanter wert

reserven etc sehen gut aus

produktion ja erst ab 2011

von daher kann man das ganze in der nächsten zeit noch von der seitenlinie aus betrachten

mal schauen was der u308 preis noch so veranstaltet

hatte vor paar monaten schonmal geschaut

da gabs noch keinen

ein interessanter wert

reserven etc sehen gut aus

produktion ja erst ab 2011

von daher kann man das ganze in der nächsten zeit noch von der seitenlinie aus betrachten

mal schauen was der u308 preis noch so veranstaltet

Haywood gives a $4.50 taget

Haywood have just started covering BMN.

The report below is worth a read

http://www.haywood.com/pdffiles/BANFeb122008.pdf

Haywood have just started covering BMN.

The report below is worth a read

http://www.haywood.com/pdffiles/BANFeb122008.pdf

Mar 03, 2008 16:14 ET

Bannerman Resources Announces Equity Financing

TORONTO, ONTARIO--(Marketwire - March 3, 2008) -

http://www.marketwirecanada.com/mw/rel_ca.jsp?id=828079

Bannerman Resources Announces Equity Financing

TORONTO, ONTARIO--(Marketwire - March 3, 2008) -

http://www.marketwirecanada.com/mw/rel_ca.jsp?id=828079

Bannerman Resources Ltd. (TSX:BAN)(ASX:BMN) ("Bannerman" or the "Company") announced today that it has filed a preliminary short form prospectus with securities regulatory authorities in Ontario, British Columbia, Alberta, Saskatchewan and Manitoba in respect of a public offering of ordinary shares (the "Offering"). The Offering will be conducted through a syndicate of underwriters, led by Haywood Securities Inc., and including GMP Securities L.P., Cormark Securities Inc. and Thomas Weisel Partners Canada Inc.

The Offering will be priced in the context of the market with final terms of the Offering to be determined at the time of pricing. Bannerman plans to use the net proceeds from the financing to develop its Goanikontes uranium project in Namibia, other exploration costs and for working capital and general corporate purposes.

Trading in Bannerman's shares will be temporarily suspended on the Australian Stock Exchange pending finalization of the terms of the proposed Offering.

The Offering is subject to certain conditions including, but not limited to, the entering into by Bannerman and the underwriters of an underwriting agreement and the receipt of all necessary approvals, including the approval of the Toronto Stock Exchange and the Australian Stock Exchange.

The Offering is expected to close on or about March 27, 2008.

These securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the "U.S. Securities Act"), or the securities laws of any state of the United States and these securities may not be offered or sold, directly or indirectly, within the United States or to or for the account or benefit of a U.S. person (as defined in Regulation S under the U.S. Securities Act) without registration under the U.S. Securities Act and any applicable state securities laws unless an exemption from registration is available. This news release is not an offer to sell or the solicitation of an offer to buy the securities in any jurisdiction.

About Bannerman

Bannerman Resources Limited is an emerging international uranium producer with projects in Namibia and Botswana and an interest in a license in Australia. The Company's major focus is on the exploration and development of a uranium project in Namibia.

Bannerman is currently focused on accelerating the development of its primary asset, the Goanikontes uranium project located in the world-class uranium country of Namibia and situated on a trend southwest of the Rio Tinto Rossing mine. A bankable feasibility study is planned for 2008 with production planned to commence in 2011.

The Offering will be priced in the context of the market with final terms of the Offering to be determined at the time of pricing. Bannerman plans to use the net proceeds from the financing to develop its Goanikontes uranium project in Namibia, other exploration costs and for working capital and general corporate purposes.

Trading in Bannerman's shares will be temporarily suspended on the Australian Stock Exchange pending finalization of the terms of the proposed Offering.

The Offering is subject to certain conditions including, but not limited to, the entering into by Bannerman and the underwriters of an underwriting agreement and the receipt of all necessary approvals, including the approval of the Toronto Stock Exchange and the Australian Stock Exchange.

The Offering is expected to close on or about March 27, 2008.

These securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the "U.S. Securities Act"), or the securities laws of any state of the United States and these securities may not be offered or sold, directly or indirectly, within the United States or to or for the account or benefit of a U.S. person (as defined in Regulation S under the U.S. Securities Act) without registration under the U.S. Securities Act and any applicable state securities laws unless an exemption from registration is available. This news release is not an offer to sell or the solicitation of an offer to buy the securities in any jurisdiction.

About Bannerman

Bannerman Resources Limited is an emerging international uranium producer with projects in Namibia and Botswana and an interest in a license in Australia. The Company's major focus is on the exploration and development of a uranium project in Namibia.

Bannerman is currently focused on accelerating the development of its primary asset, the Goanikontes uranium project located in the world-class uranium country of Namibia and situated on a trend southwest of the Rio Tinto Rossing mine. A bankable feasibility study is planned for 2008 with production planned to commence in 2011.

West Australian Metals in Stuttgart! (während der „Invest“)

----------------------------------------------------------------------------

------------------------------------

Die interessanteste Uranstory des Jahres! West Australian Metals, einer der

größten Uranexplorer in Namibia, stellt das dortige „Marencia Projekt“

vor. „Marencia“ erstreckt sich über 700 km² mit hohem Potential für

sekundäre und primäre Uranvorkommen. Hier werden über 100 Millionen Pfund

Uranoxid vermutet, davon sind bereits 15 Mio. per JORC Studie nachgewiesen.

Neben australischen Experten arbeiten an dem Projekt auch deutsche Geologen.

Das Gebiet grenzt unmittelbar an Areva / Uramin. Infrastruktur und

verkehrsmäßige Anbindung gelten als optimal.

Also: Informationen aus erster Hand! Chairman, Technischer Direktor und ein

deutscher Geologe stellen das Projekt vor und beantworten Ihre Fragen.

Wann: 12.April 2008, 17 Uhr

Wo: Hotel Mövenpick, 70629 Stuttgart Airport, Flughafenstrasse 50, (Nähe

Messe und Flughafen) Im Anschluss Imbiss und Möglichkeit des persönlichen

Gesprächs.

Weitere Informationen: http://www.wametals.de – dort können Sie auch

Infos per Mail anfordern. Oder direkt unter: westaustralianmetals@web.de

West Australian Metals ist in Frankfurt, Berlin und Sydney gelistet.

Frankfurter Börse: WTT / ISIN:AU000000WME4 - Sydney ASX.com: WME

interessant . . . Bannerman hat bereits 70 Mio pfd JORC, in der direkten

Nachbarschaft der Rossing Mine von Rio Tinto und wird noch in diesem

Jahr 100 Mio pfd + x nachweisen und hat schon die Bankable Feasibility

Study in Arbeit . . .

.

----------------------------------------------------------------------------

------------------------------------

Die interessanteste Uranstory des Jahres! West Australian Metals, einer der

größten Uranexplorer in Namibia, stellt das dortige „Marencia Projekt“

vor. „Marencia“ erstreckt sich über 700 km² mit hohem Potential für

sekundäre und primäre Uranvorkommen. Hier werden über 100 Millionen Pfund

Uranoxid vermutet, davon sind bereits 15 Mio. per JORC Studie nachgewiesen.

Neben australischen Experten arbeiten an dem Projekt auch deutsche Geologen.

Das Gebiet grenzt unmittelbar an Areva / Uramin. Infrastruktur und

verkehrsmäßige Anbindung gelten als optimal.

Also: Informationen aus erster Hand! Chairman, Technischer Direktor und ein

deutscher Geologe stellen das Projekt vor und beantworten Ihre Fragen.

Wann: 12.April 2008, 17 Uhr

Wo: Hotel Mövenpick, 70629 Stuttgart Airport, Flughafenstrasse 50, (Nähe

Messe und Flughafen) Im Anschluss Imbiss und Möglichkeit des persönlichen

Gesprächs.

Weitere Informationen: http://www.wametals.de – dort können Sie auch

Infos per Mail anfordern. Oder direkt unter: westaustralianmetals@web.de

West Australian Metals ist in Frankfurt, Berlin und Sydney gelistet.

Frankfurter Börse: WTT / ISIN:AU000000WME4 - Sydney ASX.com: WME

interessant . . . Bannerman hat bereits 70 Mio pfd JORC, in der direkten

Nachbarschaft der Rossing Mine von Rio Tinto und wird noch in diesem

Jahr 100 Mio pfd + x nachweisen und hat schon die Bankable Feasibility

Study in Arbeit . . .

.

Sydney - Wednesday - April 2:

(RWE Aust Business News) -

Bannerman Resources (ASX:BMN) has been advised by director Nathan McMahon

and other shareholders that a portion of their shareholdings are subject

to an equity finance contract with Opes Prime, in receivership by the ANZ

Bank (ASX:ANZ).

The company cannot provide surety of the total number of the

securities affected by the Opes margin lending, however, following an

analysis of the register, identified two holdings which it believes may

be potentially linked to the Opes facilities.

These shares represent 10.3pc of the issued capital.

Mr McMahon has informed the company that entities associated with

him have margin lending arrangements with Opes under which 14,722,097

ordinary shares representing 10.2pc of the issued capital are pledged as

collateral which are held in these ANZ Nominees accounts.

The key terms of the Opes facilities as understood by Mr McMahon

were that of a standard margin loan facility, whereby equity securities

were given as collateral for funds advanced to clients and a security

value for the collateral was determined by Opes.

The current status of the ownership and control of the securities

is unclear at this time.

No other directors or executives have any margin loan

arrangements secured by the company's shares.

(RWE Aust Business News) -

Bannerman Resources (ASX:BMN) has been advised by director Nathan McMahon

and other shareholders that a portion of their shareholdings are subject

to an equity finance contract with Opes Prime, in receivership by the ANZ

Bank (ASX:ANZ).

The company cannot provide surety of the total number of the

securities affected by the Opes margin lending, however, following an

analysis of the register, identified two holdings which it believes may

be potentially linked to the Opes facilities.

These shares represent 10.3pc of the issued capital.

Mr McMahon has informed the company that entities associated with

him have margin lending arrangements with Opes under which 14,722,097

ordinary shares representing 10.2pc of the issued capital are pledged as

collateral which are held in these ANZ Nominees accounts.

The key terms of the Opes facilities as understood by Mr McMahon

were that of a standard margin loan facility, whereby equity securities

were given as collateral for funds advanced to clients and a security

value for the collateral was determined by Opes.

The current status of the ownership and control of the securities

is unclear at this time.

No other directors or executives have any margin loan

arrangements secured by the company's shares.

wallstreet-team

kriegt Ihr das mit dem Seitenumbruch noch mal hin ?? oder soll man sich hier 'nen Wolf scrollen ??

kriegt Ihr das mit dem Seitenumbruch noch mal hin ?? oder soll man sich hier 'nen Wolf scrollen ??

Antwort auf Beitrag Nr.: 33.855.236 von DaenischeSuedsee am 10.04.08 11:33:10Korrektur: HAYWOOD Research Report

Antwort auf Beitrag Nr.: 33.855.303 von DaenischeSuedsee am 10.04.08 11:38:20Namibia: Work On Desalination Plant to Start

(Windhoek)

4 April 2008

Posted to the web 4 April 2008

Petronella Sibeene

Windhoek

NamWater has announced that the construction of a second plant to desalinate salty seawater for domestic and industrial use in a project worth overa billion Namibian dollars in the Erongo region will commence in October.

The desalination plant will supply water to about 12 new uranium mines expected to start operating in 2010.

Managing Director of NamWater, Dr Vaino Shivute,yesterday said the unprecedented increase in uranium demand globally since 2000, has aroused interest among companies to explore uraniummining in Namibia.

Mines in the pipeline such as Valencia, Goanikontes, Husab, Marenica, Tubas and Tumas and fiveothers are expected to open in the Erongo region starting 2010. Rössing and Langer Heinrich mines are expected to increase their production in the coming few years and will also get water supply from the desalination plant.

They will consume about 53million cubic metres per annum exceeding the utility's nationwide supply of 67 million cubic metres per annum.

This will be the second desalination plant in that region.

In November last year, NamWater and UraMin announced a joint undertaking to construct a seawater intake and brine disposal system.

The plant to be commissioned end 2009 will supply about 20 million cubic metres per year to Trekkopje Mine.

The capital cost for the project announced yesterday is estimated at N$1.48 billion.

Considering the huge financial outlay involved, Shivute said NamWater is likely to go the market to borrow. A financial consultant has already been appointed.

NamWater will recover the money from the mining companies either as capital payment upfront or water tariffs.

The funds will be used for putting up a system for seawater intake,building the plant itself, pipes, pump station, reservoirs and also for power supply.

"It is not true that NamWater is subsidising water to the mines. They are prepared top pay," he said.

Upcoming mines guaranteed they will buy water from NamWater and recover thecosts within the shortest period of the mine's lifespan, NamWater said.

Last year, NamWater appointed a desalination consultant and prequalification bidders have already been completed.

The tender documents were completed and preferred bidders were presented with the documents last month.

The commissioning date for the desalination plant is early 2010.

While the mining industry depends heavily on energy supply in order to operate big machines, Shivute said an inter-ministerial committee comprising of members of NamPower and NamWater was established to coordinate requirements from the ministries and parastatals. NamPower assured it would by the third-quarter of next year have enough electricity for the mines.

The desalinationproject will facilitate enormous growth in uranium mining in the country resulting in economic growth, said Shivute.

It is estimated that about 3000 Namibians will secure jobs in the industry.

Shivute also indicated that the design of themuch-anticipated desalination plant will be in such a way that itminimises the brine discharge into the sea.

"A stringent environmental management plan will be imposed by NamWater onall the engineering contractors that will be employed on the project,"Shivute added.

Meanwhile, coastal water demands will still be met from the Kuiseb and Omdel aquifers.

http://www.newera.com.na/

(Windhoek)

4 April 2008

Posted to the web 4 April 2008

Petronella Sibeene

Windhoek

NamWater has announced that the construction of a second plant to desalinate salty seawater for domestic and industrial use in a project worth overa billion Namibian dollars in the Erongo region will commence in October.

The desalination plant will supply water to about 12 new uranium mines expected to start operating in 2010.

Managing Director of NamWater, Dr Vaino Shivute,yesterday said the unprecedented increase in uranium demand globally since 2000, has aroused interest among companies to explore uraniummining in Namibia.

Mines in the pipeline such as Valencia, Goanikontes, Husab, Marenica, Tubas and Tumas and fiveothers are expected to open in the Erongo region starting 2010. Rössing and Langer Heinrich mines are expected to increase their production in the coming few years and will also get water supply from the desalination plant.

They will consume about 53million cubic metres per annum exceeding the utility's nationwide supply of 67 million cubic metres per annum.

This will be the second desalination plant in that region.

In November last year, NamWater and UraMin announced a joint undertaking to construct a seawater intake and brine disposal system.

The plant to be commissioned end 2009 will supply about 20 million cubic metres per year to Trekkopje Mine.

The capital cost for the project announced yesterday is estimated at N$1.48 billion.

Considering the huge financial outlay involved, Shivute said NamWater is likely to go the market to borrow. A financial consultant has already been appointed.

NamWater will recover the money from the mining companies either as capital payment upfront or water tariffs.

The funds will be used for putting up a system for seawater intake,building the plant itself, pipes, pump station, reservoirs and also for power supply.

"It is not true that NamWater is subsidising water to the mines. They are prepared top pay," he said.

Upcoming mines guaranteed they will buy water from NamWater and recover thecosts within the shortest period of the mine's lifespan, NamWater said.

Last year, NamWater appointed a desalination consultant and prequalification bidders have already been completed.

The tender documents were completed and preferred bidders were presented with the documents last month.

The commissioning date for the desalination plant is early 2010.

While the mining industry depends heavily on energy supply in order to operate big machines, Shivute said an inter-ministerial committee comprising of members of NamPower and NamWater was established to coordinate requirements from the ministries and parastatals. NamPower assured it would by the third-quarter of next year have enough electricity for the mines.

The desalinationproject will facilitate enormous growth in uranium mining in the country resulting in economic growth, said Shivute.

It is estimated that about 3000 Namibians will secure jobs in the industry.

Shivute also indicated that the design of themuch-anticipated desalination plant will be in such a way that itminimises the brine discharge into the sea.

"A stringent environmental management plan will be imposed by NamWater onall the engineering contractors that will be employed on the project,"Shivute added.

Meanwhile, coastal water demands will still be met from the Kuiseb and Omdel aquifers.

http://www.newera.com.na/

zur info...

Vom 15.05.2008

Daumen hoch für Bannerman Resources

Das australische Explorationsunternehmen Bannerman Resources Ltd hat nach jüngsten erfolgsversprechenden Untersuchungsergebnissen für das Goanikontes-Uranprojekt 41 Kilometer südlich von Swakopmund eine positive Resonanz von internationalen Analysten bekommen.

Die Uranförderung in Namibia, hier bei der Rössing-Mine, bleibt trotz des gesunkenen Weltmarktpreises weiterhin interessant und lukrativ.

Wir stufen Goanikontes als eines der wichtigsten Uranprojekte weltweit ein”, so die Meinung eines renommierten kanadischen Brokers. Bannerman ist an der Börse von Toronto notiert, einer der beliebtesten Kapitalsammelstellen für Explorationsfirmen weltweit. „Die Untersuchungsergebnisse von Goanikontes A haben bislang erhebliche Uranablagerungen gezeigt. Wir gehen davon aus, dass der bislang geschätzte Umfang der U3O8-Ablagerungen von 72,2 Millionen Pfund demnächst deutlich nach oben revidiert wird”, fuhr er fort. Triuranoctoxid (U3O8) ist das erste Zwischenprodukt, das beim Abbau von Uranerzen gewonnen wird.

Das Goanikontes-Projekt ist das derzeit wichtigste Projekt von Bannerman Resources, einschließlich Explorationsaktivitäten in Australien und Botswana. Bannerman hat nach aktuellen Daten hier bislang 333 Probebohrungen durchgeführt und ist dabei, seine Untersuchungen auszuweiten. So hat das Unternehmen nach eigenen Angaben damit begonnen, auch beim Rössingberg Probebohrungen durchzuführen.

Im Zuge des enorm gestiegenen Uranpreises, der im Juli 2007 bei über 130 US-Dollar je Pfund seinen vorläufigen Höchststand erreicht hat, inzwischen allerdings auf rund 70 US-Dollar gefallen ist, hat sich das Gebiet südlich von Swakopmund in der Nähe des größten Urantagebaus der Welt, Rössing Uranium von Rio Tinto, zu einem Mekka für Uranexplorationsgesellschaften aus aller Welt entwickelt. Obwohl dies zu starken Protesten von Umweltschützern geführt hat, sind inzwischen eine Reihe Explorationsprojekte erfolgreich abgeschlossen und der Minenbetrieb aufgenommen worden, wie im Falle der Mine Langer Heinrich vom ebenfalls australischen Unternehmen Paladin Resources.

Auch das Goanikontes-Projekt ist bislang auf wenig Gegenliebe bei Umweltschützern gestoßen. Zudem ist es zu einer gerichtlichen Auseinandersetzung mit einem hiesigen Minenbetrieb über den Grenzverlauf der Welwitschia-Prospektierlizenz (EPL 3345) gekommen, die das Goanikontes-Projekt umfasst. Die EPL 3345 deckt eine Oberfläche von rund 500 Quadratkilometer ab. Im Rahmen dieser Prospektierlizenz will Bannerman insgesamt zehn potenzielle Lagerstätten untersuchen. Die Regierung hat sich trotz aller Kontroversen bislang konsequent für die Interessen der ausländischen Explorationsfirmen eingesetzt.

In einer Projektübersicht auf seiner Internetseite geht Bannerman Resources davon aus, dass es rund 70 Prozent seines Elektrizitätsbedarfs selbst decken und daher von der regionalen Stromnotlage nicht stark betroffen sein werde. Zudem wird angedeutet, dass die von NamWater gebaute Meerwasserentsalzungsanlage nördlich von Wlotzkasbaken eine entscheidende Rolle in der Wasserversorgung der Bannermann-Projekte spielen soll.

Neben Kanada und Australien ist Bannerman Resources Ltd seit dem 2. April dieses Jahres auch in Namibia an der Börse notiert. An diesem Tag ging die Bannerman-Aktie (Kürzel: BMN) bei fast 14 Namibia-Dollar aus dem Handel. Inzwischen hat sie auf 11,32 Namibia-Dollar (13. Mai 2008) abgespeckt. Die Aktie sei relativ illiquide, werde also wenig gehandelt, ergab gestern eine Nachfrage bei einem hiesigen Broker. Anlagen in Explorationsgesellschaften seien gemeinhin höchst spekulativ, auch wenn sie von Marktbeobachtern mit dem positiven Prädikat „sector ourperform” – wie im Falle von Bannerman Resources – bewertet werden.

Von Sven Heussen

http://www.az.com.na/wirtschaft/daumen-hoch-fr-bannerman-res…

Vom 15.05.2008

Daumen hoch für Bannerman Resources

Das australische Explorationsunternehmen Bannerman Resources Ltd hat nach jüngsten erfolgsversprechenden Untersuchungsergebnissen für das Goanikontes-Uranprojekt 41 Kilometer südlich von Swakopmund eine positive Resonanz von internationalen Analysten bekommen.

Die Uranförderung in Namibia, hier bei der Rössing-Mine, bleibt trotz des gesunkenen Weltmarktpreises weiterhin interessant und lukrativ.

Wir stufen Goanikontes als eines der wichtigsten Uranprojekte weltweit ein”, so die Meinung eines renommierten kanadischen Brokers. Bannerman ist an der Börse von Toronto notiert, einer der beliebtesten Kapitalsammelstellen für Explorationsfirmen weltweit. „Die Untersuchungsergebnisse von Goanikontes A haben bislang erhebliche Uranablagerungen gezeigt. Wir gehen davon aus, dass der bislang geschätzte Umfang der U3O8-Ablagerungen von 72,2 Millionen Pfund demnächst deutlich nach oben revidiert wird”, fuhr er fort. Triuranoctoxid (U3O8) ist das erste Zwischenprodukt, das beim Abbau von Uranerzen gewonnen wird.

Das Goanikontes-Projekt ist das derzeit wichtigste Projekt von Bannerman Resources, einschließlich Explorationsaktivitäten in Australien und Botswana. Bannerman hat nach aktuellen Daten hier bislang 333 Probebohrungen durchgeführt und ist dabei, seine Untersuchungen auszuweiten. So hat das Unternehmen nach eigenen Angaben damit begonnen, auch beim Rössingberg Probebohrungen durchzuführen.

Im Zuge des enorm gestiegenen Uranpreises, der im Juli 2007 bei über 130 US-Dollar je Pfund seinen vorläufigen Höchststand erreicht hat, inzwischen allerdings auf rund 70 US-Dollar gefallen ist, hat sich das Gebiet südlich von Swakopmund in der Nähe des größten Urantagebaus der Welt, Rössing Uranium von Rio Tinto, zu einem Mekka für Uranexplorationsgesellschaften aus aller Welt entwickelt. Obwohl dies zu starken Protesten von Umweltschützern geführt hat, sind inzwischen eine Reihe Explorationsprojekte erfolgreich abgeschlossen und der Minenbetrieb aufgenommen worden, wie im Falle der Mine Langer Heinrich vom ebenfalls australischen Unternehmen Paladin Resources.

Auch das Goanikontes-Projekt ist bislang auf wenig Gegenliebe bei Umweltschützern gestoßen. Zudem ist es zu einer gerichtlichen Auseinandersetzung mit einem hiesigen Minenbetrieb über den Grenzverlauf der Welwitschia-Prospektierlizenz (EPL 3345) gekommen, die das Goanikontes-Projekt umfasst. Die EPL 3345 deckt eine Oberfläche von rund 500 Quadratkilometer ab. Im Rahmen dieser Prospektierlizenz will Bannerman insgesamt zehn potenzielle Lagerstätten untersuchen. Die Regierung hat sich trotz aller Kontroversen bislang konsequent für die Interessen der ausländischen Explorationsfirmen eingesetzt.

In einer Projektübersicht auf seiner Internetseite geht Bannerman Resources davon aus, dass es rund 70 Prozent seines Elektrizitätsbedarfs selbst decken und daher von der regionalen Stromnotlage nicht stark betroffen sein werde. Zudem wird angedeutet, dass die von NamWater gebaute Meerwasserentsalzungsanlage nördlich von Wlotzkasbaken eine entscheidende Rolle in der Wasserversorgung der Bannermann-Projekte spielen soll.

Neben Kanada und Australien ist Bannerman Resources Ltd seit dem 2. April dieses Jahres auch in Namibia an der Börse notiert. An diesem Tag ging die Bannerman-Aktie (Kürzel: BMN) bei fast 14 Namibia-Dollar aus dem Handel. Inzwischen hat sie auf 11,32 Namibia-Dollar (13. Mai 2008) abgespeckt. Die Aktie sei relativ illiquide, werde also wenig gehandelt, ergab gestern eine Nachfrage bei einem hiesigen Broker. Anlagen in Explorationsgesellschaften seien gemeinhin höchst spekulativ, auch wenn sie von Marktbeobachtern mit dem positiven Prädikat „sector ourperform” – wie im Falle von Bannerman Resources – bewertet werden.

Von Sven Heussen

http://www.az.com.na/wirtschaft/daumen-hoch-fr-bannerman-res…

Broker_Haywood May 21

Downloaded 119 times

File: Broker_Haywood May 21.pdf

Size: 171.57 KB

Download: Click Here

http://www.datafilehost.com/download-ae4c78b6.html

.

Downloaded 119 times

File: Broker_Haywood May 21.pdf

Size: 171.57 KB

Download: Click Here

http://www.datafilehost.com/download-ae4c78b6.html

.

=======================================================================

Re: News Releases - Tuesday, June 24, 2008

Bannerman Resources' Resource Drilling Finalised at Anomaly A

Exploration Commences for Additional Production Capacity

=======================================================================

Perth, Australia -- June 24, 2008 -- Bannerman Resources Ltd (ASX: BMN, TSX: BAN) ("Bannerman" or the "Company"), a uranium exploration and mine development company focused on projects in Namibia, is pleased to report that resource drilling has now been completed at Goanikontes' Anomaly A and that senior geological staff have mobilised to the Perth Company office to begin final resource estimation work.

Drill rigs have now been mobilised to explore prospects which have been identified beyond the principle uranium deposit at Goanikontes' Anomaly A. In all, fifteen prospects have been identified to date with targets prioritised based on historic drill results (where available), ground and airborne radiometric surveys and geological mapping. This marks the commencement of an exciting new exploration phase for the Company. It is the Company's intention to define additional significant uranium resources with proximity to the Anomaly A deposit.

Additional Uranium deposits could provide for;

-Enhanced and additional ore to supplement the Anomaly A project, -Additional resources to underpin a possible Stage 2 expansion beyond the envisaged 15Mt p.a. mining and milling operation at Anomaly A, -A much larger resource base for an additional stand alone plant elsewhere on the lease, utilising shared infrastructure and management capabilities.

Drilling at Anomaly A totalled 441 RC holes for 117,198 metres and 47 Diamond Core holes for 18,123 metres over the 2.3 kilometre strike that has been defined for the resource estimate. This represents the culmination of over 18 months of continuous drilling and has identified one of the world's largest known uranium deposits.

The Company expects to announce an updated resource estimate in Q3 2008. To this end, the completion of resource drilling and the mobilisation of senior geological staff to the Perth office to work with RSG Coffey Mining are major milestones.

The final resource will mostly comprise chemical assay data, including results from significant width and depth extensions that were not included in the interim resource estimate announced in January, 2008 and will also include core and RC drill hole results from infill drilling completed on a 50 metre by 50 metre grid.

This new resource estimate will be the basis of the definitive feasibility study being completed by GRD Minproc, however, mineralisation at Anomaly A remains open to the North, South, West and at depth. One diamond core rig will remain in the area testing these extensions and collecting samples for geotechnical and metallurgical test work for the feasibility study currently under commission.

Peter Batten, Managing Director says, "It is important to recognise that the Anomaly A project is in fact a single pit that does not yet include all the known mineralisation. The geological sequence hosting the Anomaly A Project is known to continue and in some cases repeat itself along strike and down dip. It would be more accurate to describe Anomaly A as the first open pit in the Project area."

Bannerman is currently establishing a sample preparation laboratory, to be run by an independent commercial laboratory firm, in Swakopmund for the exclusive use of the Company. It is expected that this facility will greatly expedite the processing of drill samples.

Exploration drilling on the other prospects has now commenced with drilling being conducted at Oshivelli, Rossingberg and at Ombuga South.

About Bannerman

Bannerman Resources Limited is an emerging uranium producer with interests in two properties in Namibia, an African country considered to be a premier mining jurisdiction. Its principal and most significant asset is its 80% interest in the Goanikontes project situated on a trend southwest of the Rio Tinto Rössing uranium mine.

Bannerman is focused on accelerating the development of one of a very large uranium deposit at Goanikontes, Namibia. A mine plan is contemplating low cost uranium production using proven processing techniques. The scoping study completed in December 2007 describes robust project economics using conservative uranium prices. A definitive feasibility study is currently underway by GRD Minproc. The company expects to bring its starter asset at the Goanikontes deposit into production by 2011.

As well, the area offers tremendous exploration potential. Exploration of an initial fifteen identified targets has commenced and will continue through the development stages of the Goanikontes starter asset.

Please visit the Company website at www.bannermanresources.com

For further information please contact:

Peter Batten

Managing Director

Bannerman Resources Ltd.

Ph: +61 (08) 9381 1436

Em: peter@bannermanresources.com.au

North America

Ann Gibbs

Investor Relations

Bannerman Resources Ltd

Tel: 1 416 388 7247

E: ann@bannermanresources.com

The information in this report that relates to the Exploration Results, Mineral Resources or Ore Reserves of the projects owned by Bannerman Resources Ltd is based on information compiled by Mr Peter Batten, who is a Member of The Australasian Institute of Mining and Metallurgy and who has sufficient experience relevant to the style of mineralisation and types of deposits under consideration and to the activity which is being undertaken to qualify as Competent Person as defined in the 2004 Edition of the "Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves" and as a Qualified Person for purposes of National Instrument 43-101 of the Canadian Securities Administrators.. Mr Batten consents to the inclusion in the report of the matters based on his information in the form and context in which it appears.

=======================================================================

Copyright (c) 2008 BANNERMAN RESOURCES LIMITED (BAN) All rights reserved. For more information visit our website at http://www.bannermanresources.com/ or send mailto:questions@bannermanresources.com

=======================================================================

das hatte ja die Wirkung eines Treibsatzes, sieht so aus als wird bei Bannerman

alles wieder in's Lot kommen . . .

Re: News Releases - Tuesday, June 24, 2008

Bannerman Resources' Resource Drilling Finalised at Anomaly A

Exploration Commences for Additional Production Capacity

=======================================================================

Perth, Australia -- June 24, 2008 -- Bannerman Resources Ltd (ASX: BMN, TSX: BAN) ("Bannerman" or the "Company"), a uranium exploration and mine development company focused on projects in Namibia, is pleased to report that resource drilling has now been completed at Goanikontes' Anomaly A and that senior geological staff have mobilised to the Perth Company office to begin final resource estimation work.

Drill rigs have now been mobilised to explore prospects which have been identified beyond the principle uranium deposit at Goanikontes' Anomaly A. In all, fifteen prospects have been identified to date with targets prioritised based on historic drill results (where available), ground and airborne radiometric surveys and geological mapping. This marks the commencement of an exciting new exploration phase for the Company. It is the Company's intention to define additional significant uranium resources with proximity to the Anomaly A deposit.

Additional Uranium deposits could provide for;

-Enhanced and additional ore to supplement the Anomaly A project, -Additional resources to underpin a possible Stage 2 expansion beyond the envisaged 15Mt p.a. mining and milling operation at Anomaly A, -A much larger resource base for an additional stand alone plant elsewhere on the lease, utilising shared infrastructure and management capabilities.

Drilling at Anomaly A totalled 441 RC holes for 117,198 metres and 47 Diamond Core holes for 18,123 metres over the 2.3 kilometre strike that has been defined for the resource estimate. This represents the culmination of over 18 months of continuous drilling and has identified one of the world's largest known uranium deposits.

The Company expects to announce an updated resource estimate in Q3 2008. To this end, the completion of resource drilling and the mobilisation of senior geological staff to the Perth office to work with RSG Coffey Mining are major milestones.

The final resource will mostly comprise chemical assay data, including results from significant width and depth extensions that were not included in the interim resource estimate announced in January, 2008 and will also include core and RC drill hole results from infill drilling completed on a 50 metre by 50 metre grid.

This new resource estimate will be the basis of the definitive feasibility study being completed by GRD Minproc, however, mineralisation at Anomaly A remains open to the North, South, West and at depth. One diamond core rig will remain in the area testing these extensions and collecting samples for geotechnical and metallurgical test work for the feasibility study currently under commission.

Peter Batten, Managing Director says, "It is important to recognise that the Anomaly A project is in fact a single pit that does not yet include all the known mineralisation. The geological sequence hosting the Anomaly A Project is known to continue and in some cases repeat itself along strike and down dip. It would be more accurate to describe Anomaly A as the first open pit in the Project area."

Bannerman is currently establishing a sample preparation laboratory, to be run by an independent commercial laboratory firm, in Swakopmund for the exclusive use of the Company. It is expected that this facility will greatly expedite the processing of drill samples.

Exploration drilling on the other prospects has now commenced with drilling being conducted at Oshivelli, Rossingberg and at Ombuga South.

About Bannerman

Bannerman Resources Limited is an emerging uranium producer with interests in two properties in Namibia, an African country considered to be a premier mining jurisdiction. Its principal and most significant asset is its 80% interest in the Goanikontes project situated on a trend southwest of the Rio Tinto Rössing uranium mine.

Bannerman is focused on accelerating the development of one of a very large uranium deposit at Goanikontes, Namibia. A mine plan is contemplating low cost uranium production using proven processing techniques. The scoping study completed in December 2007 describes robust project economics using conservative uranium prices. A definitive feasibility study is currently underway by GRD Minproc. The company expects to bring its starter asset at the Goanikontes deposit into production by 2011.

As well, the area offers tremendous exploration potential. Exploration of an initial fifteen identified targets has commenced and will continue through the development stages of the Goanikontes starter asset.

Please visit the Company website at www.bannermanresources.com

For further information please contact:

Peter Batten

Managing Director

Bannerman Resources Ltd.

Ph: +61 (08) 9381 1436

Em: peter@bannermanresources.com.au

North America

Ann Gibbs

Investor Relations

Bannerman Resources Ltd

Tel: 1 416 388 7247

E: ann@bannermanresources.com

The information in this report that relates to the Exploration Results, Mineral Resources or Ore Reserves of the projects owned by Bannerman Resources Ltd is based on information compiled by Mr Peter Batten, who is a Member of The Australasian Institute of Mining and Metallurgy and who has sufficient experience relevant to the style of mineralisation and types of deposits under consideration and to the activity which is being undertaken to qualify as Competent Person as defined in the 2004 Edition of the "Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves" and as a Qualified Person for purposes of National Instrument 43-101 of the Canadian Securities Administrators.. Mr Batten consents to the inclusion in the report of the matters based on his information in the form and context in which it appears.

=======================================================================

Copyright (c) 2008 BANNERMAN RESOURCES LIMITED (BAN) All rights reserved. For more information visit our website at http://www.bannermanresources.com/ or send mailto:questions@bannermanresources.com

=======================================================================

das hatte ja die Wirkung eines Treibsatzes, sieht so aus als wird bei Bannerman

alles wieder in's Lot kommen . . .

super wert

ein ver10facher ist hier drin

kennzahlen sehen super aus

wenn der uran preis mitspielt

ein ver10facher ist hier drin

kennzahlen sehen super aus

wenn der uran preis mitspielt

This article may assist all those on-lookers, in deciding a position in Bannerman.

___________________________________________________________

Battle for uranium resource hots up.

WINDHOEK - The battle for uranium oxide or yellow cake is heating up after the Ministry of Mines and Energy's decision to issue a mining licence to Bannerman Mining Resources Namibia.

In December 2007, another mine, Savanna Marble CC filed a lawsuit against the Minister of Mines and Energy and Bannerman Resources Limited, challenging the validity of a licence given to Bannerman to mine uranium.

The bone of contention is that the area in which Bannerman is licensed to mine uranium, overlaps the area in which Savanna is licensed to mine dimension stones.

In its lawsuit, Savanna Marble is seeking an order to declare the granting of the licence given to Bannerman null and void.

International stock market company Tradingmarkets.com reported recently that Savanna Marble is challenging the granting of this licence because it wants to mine uranium in that very same area itself.

The area in question is situated in the Erongo region, just outside Swakopmund.

Bannerman's mine is situated at Goanikontes towards the Namib Naukluft Park.

The chairman of Bannerman, Geoff Stanley, stated in an update on this matter on his company's website last week that even Namibian Minister of Mines and Energy Erkki Nghimtina is strongly opposed to Savanna's claim.

He said both his company and the Minister of Mines and Energy agree that Savanna's claim should be rejected prior to any substantive hearing of the case, on the grounds that Savanna is guilty of serious and unacceptable delays in waiting for two years to bring proceedings against the respondents.

"The application is without merit and will fail," he stressed.

In an effort to reassure shareholders, Stanley said: "Currently, the company has no debt and sufficient cash to fund the ongoing feasibility study into the development of the project."

"The company has continued to achieve its targets at the Goanikontes Uranium Project in the Erongo Region.

The company believes the resources at Goanikontes Anomaly has the potential to underpin one of the largest uranium-producing operations in the world," he added.n in Bannerman.

___________________________________________________________

Here's a Link to the Company in mention Savanna.

http://www.savannamarble.com/

___________________________________________________________

Battle for uranium resource hots up.

WINDHOEK - The battle for uranium oxide or yellow cake is heating up after the Ministry of Mines and Energy's decision to issue a mining licence to Bannerman Mining Resources Namibia.

In December 2007, another mine, Savanna Marble CC filed a lawsuit against the Minister of Mines and Energy and Bannerman Resources Limited, challenging the validity of a licence given to Bannerman to mine uranium.

The bone of contention is that the area in which Bannerman is licensed to mine uranium, overlaps the area in which Savanna is licensed to mine dimension stones.

In its lawsuit, Savanna Marble is seeking an order to declare the granting of the licence given to Bannerman null and void.

International stock market company Tradingmarkets.com reported recently that Savanna Marble is challenging the granting of this licence because it wants to mine uranium in that very same area itself.

The area in question is situated in the Erongo region, just outside Swakopmund.

Bannerman's mine is situated at Goanikontes towards the Namib Naukluft Park.

The chairman of Bannerman, Geoff Stanley, stated in an update on this matter on his company's website last week that even Namibian Minister of Mines and Energy Erkki Nghimtina is strongly opposed to Savanna's claim.

He said both his company and the Minister of Mines and Energy agree that Savanna's claim should be rejected prior to any substantive hearing of the case, on the grounds that Savanna is guilty of serious and unacceptable delays in waiting for two years to bring proceedings against the respondents.

"The application is without merit and will fail," he stressed.

In an effort to reassure shareholders, Stanley said: "Currently, the company has no debt and sufficient cash to fund the ongoing feasibility study into the development of the project."

"The company has continued to achieve its targets at the Goanikontes Uranium Project in the Erongo Region.

The company believes the resources at Goanikontes Anomaly has the potential to underpin one of the largest uranium-producing operations in the world," he added.n in Bannerman.

___________________________________________________________

Here's a Link to the Company in mention Savanna.

http://www.savannamarble.com/

LETTER TO SHAREHOLDER vom neuen CEO unter nachfolg. link...

http://stocknessmonster.com/news-item?S=BMN&E=ASX&N=429997

...da kommt wieder musik rein....IMO !!!

...MIR scheint, wir haben grad phantastische

KAUF- kurse !!!!

KAUF- kurse !!!!

Antwort auf Beitrag Nr.: 36.053.774 von hbg55 am 24.11.08 17:34:12

...mit heutiger vorlage aus USA/ CAN wirds MORGEN

auch bei den AUSSIS krachen - drum HEUTE noch REIN !!!

...mit heutiger vorlage aus USA/ CAN wirds MORGEN

auch bei den AUSSIS krachen - drum HEUTE noch REIN !!!

....auch charttech. stehen die zeichen auf erholung....IMO !!!

Antwort auf Beitrag Nr.: 36.053.871 von hbg55 am 24.11.08 17:42:04

......und SO starten wir dann auch FEST in den neuen tag mit

nem sprung über den aud 0,50- widerstand.....

Trade

Number (s) Time

Last Traded Price Volume Change Value Number

of Trades

35 - 37 10:11:27 am 52 91,000 0.5 $47,320 3

33 - 34 10:10:47 am 51.5 567 0.5 $292 2

31 - 32 10:08:22 am 52 9,000 3 $4,680 2

28 - 30 10:00:29 am 55 5,794 0.5 $3,187 3

27 10:00:29 am 54.5 86 0.5 $47 1

25 - 26 10:00:29 am 54 4,120 0.5 $2,225 2

1 - 24 10:00:25 am 54.5 155,000 $84,475 24

......und SO starten wir dann auch FEST in den neuen tag mit

nem sprung über den aud 0,50- widerstand.....

Trade

Number (s) Time

Last Traded Price Volume Change Value Number

of Trades

35 - 37 10:11:27 am 52 91,000 0.5 $47,320 3

33 - 34 10:10:47 am 51.5 567 0.5 $292 2

31 - 32 10:08:22 am 52 9,000 3 $4,680 2

28 - 30 10:00:29 am 55 5,794 0.5 $3,187 3

27 10:00:29 am 54.5 86 0.5 $47 1

25 - 26 10:00:29 am 54 4,120 0.5 $2,225 2

1 - 24 10:00:25 am 54.5 155,000 $84,475 24

...allen interessierten an BMN sei auch die brandakt.

pres. zum annual general meeting unter nachfolg. link

zu empfehlen........

http://stocknessmonster.com/news-item?S=BMN&E=ASX&N=430559

mit dem heutigen tag mit SK von 0,58 sollte uns

endgültig der sprung ÜBER die aud 0,50 gelungen sein.....

Trade

Number (s) Time

Last Traded Price Volume Change Value Number

of Trades

119 - 121 5:07:14 pm 58 10,725 1 $6,220 3

118 3:58:07 pm 59 8,650 0.5 $5,104 1

115 - 117 3:58:07 pm 58.5 40,000 1 $23,400 3

112 - 114 3:53:23 pm 57.5 11,350 0.5 $6,526 3

111 3:52:35 pm 57 9,100 0.5 $5,187 1

106 - 110 3:52:07 pm 56.5 14,100 0.5 $7,967 5

105 3:48:04 pm 57 900 0.5 $513 1

104 3:46:04 pm 56.5 2,816 1.5 $1,591 1

103 3:44:17 pm 55 9,357 1 $5,146 1

102 3:44:17 pm 56 2,695 1 $1,509 1

99 - 101 3:44:17 pm 57 50,000 1 $28,500 3

endgültig der sprung ÜBER die aud 0,50 gelungen sein.....

Trade

Number (s) Time

Last Traded Price Volume Change Value Number

of Trades

119 - 121 5:07:14 pm 58 10,725 1 $6,220 3

118 3:58:07 pm 59 8,650 0.5 $5,104 1

115 - 117 3:58:07 pm 58.5 40,000 1 $23,400 3

112 - 114 3:53:23 pm 57.5 11,350 0.5 $6,526 3

111 3:52:35 pm 57 9,100 0.5 $5,187 1

106 - 110 3:52:07 pm 56.5 14,100 0.5 $7,967 5

105 3:48:04 pm 57 900 0.5 $513 1

104 3:46:04 pm 56.5 2,816 1.5 $1,591 1

103 3:44:17 pm 55 9,357 1 $5,146 1

102 3:44:17 pm 56 2,695 1 $1,509 1

99 - 101 3:44:17 pm 57 50,000 1 $28,500 3

....´bevors´ die GLOBAL player machen, bietet sich hier

akt. eine TOP- chance....IMO !!!

so seihts auch ein HC- veteran......siehe nachfolg. auszug...

As to a takeover ... man, BMN must be looking juicy ATM!

Every time I see the Swakop River EPL surrounding PDN's Langer H .... I just smile!! That must be such a temptation to PDN, because the extension of LH, and the host alaskite to their resource is all on BMN land!!

Any attempt at a takeover would have to be initiated at around $1 per share at the moment. That would be nowhere enough, as sufficient shares are held by directors and friendly hands to hold out for higher prices.

One year ago, I would have said $5-$7 would get you BMN ... Today its a different story. I would say that a $3 - $4 final offer might make it!

But each day that the world market recovers, each day that BMN recovers, and advances the project will improve that. A removal of Savannah, will change the landscape altogether.

akt. eine TOP- chance....IMO !!!

so seihts auch ein HC- veteran......siehe nachfolg. auszug...

As to a takeover ... man, BMN must be looking juicy ATM!

Every time I see the Swakop River EPL surrounding PDN's Langer H .... I just smile!! That must be such a temptation to PDN, because the extension of LH, and the host alaskite to their resource is all on BMN land!!

Any attempt at a takeover would have to be initiated at around $1 per share at the moment. That would be nowhere enough, as sufficient shares are held by directors and friendly hands to hold out for higher prices.

One year ago, I would have said $5-$7 would get you BMN ... Today its a different story. I would say that a $3 - $4 final offer might make it!

But each day that the world market recovers, each day that BMN recovers, and advances the project will improve that. A removal of Savannah, will change the landscape altogether.

Antwort auf Beitrag Nr.: 36.071.999 von hbg55 am 26.11.08 10:51:14zum besseren verständnis nachfolg. aussage mal die

entsprechende praghik !!!

......Every time I see the Swakop River EPL surrounding PDN's Langer H .... I just smile!! That must be such a temptation to PDN, because the extension of LH, and the host alaskite to their resource is all on BMN land!!.....

entsprechende praghik !!!

......Every time I see the Swakop River EPL surrounding PDN's Langer H .... I just smile!! That must be such a temptation to PDN, because the extension of LH, and the host alaskite to their resource is all on BMN land!!.....

ASX RELEASE

17 December 2008

Settlement of Savanna Litigation

Perth, Australia – 17 December 2008 – Bannerman Resources Ltd (ASX: BMN, TSX:

BAN) ("Bannerman" or the "Company") advises that its subsidiary Bannerman Mining

Resources (Namibia) Pty Ltd (“Bannerman Namibia”) has entered into an agreement to

settle the litigation against Bannerman and others brought by Savanna Marble CC

(“Savanna”) and certain associated parties (the “Savanna Parties”).

Under the terms of the settlement agreement, Savanna has agreed to discontinue the

review application in Notice of Motion A338 of 2007 in the High Court of Namibia. As

previously announced to the market, Savanna had sought a declaration that the grant by

the Minister of Mines and Energy of Namibia of the Company’s Exclusive Prospective

Licence (“EPL”) 3345, on which the Etango Project is situated, was void.

This settlement removes a very real threat to the Company’s timetable for the

development of the Etango Project and any possibility of losing the licence.

Bannerman CEO Mr Len Jubber said that the Bannerman board of directors was

unanimously of the view that settlement of the Savanna litigation represented a much

better outcome for Bannerman than proceeding to trial.

“While we were very confident in our legal position, we could not ignore the reality that the

delay in finalising the litigation was going to significantly complicate our ability to advance

our development plans for the Etango Project and our other interests in Namibia.

“Apart from the time, effort and expense associated with the litigation we were also

cognisant of the risk, no matter how small, of an adverse outcome from the proceedings”.

“The settlement of this litigation removes a significant potential roadblock for us and will

allow us to progress discussions with all stakeholders – including various arms of the

Namibian government and potential investors and partners – free of the impediments that

the litigation created.”

Details of settlement agreement