Super günstiges Uran durch Berkeley Energia (Seite 84)

eröffnet am 20.01.16 15:19:16 von

neuester Beitrag 11.04.24 15:39:14 von

neuester Beitrag 11.04.24 15:39:14 von

Beiträge: 1.266

ID: 1.225.023

ID: 1.225.023

Aufrufe heute: 0

Gesamt: 112.901

Gesamt: 112.901

Aktive User: 0

ISIN: AU000000BKY0 · WKN: 911733 · Symbol: B5R

0,2220

EUR

+3,98 %

+0,0085 EUR

Letzter Kurs 25.04.24 Tradegate

Neuigkeiten

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7950 | +30,33 | |

| 5,1500 | +21,75 | |

| 15,715 | +20,33 | |

| 0,6000 | +20,00 | |

| 0,9000 | +16,13 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,6050 | -6,20 | |

| 0,5180 | -7,09 | |

| 10,040 | -7,89 | |

| 0,5400 | -8,47 | |

| 46,88 | -97,99 |

Beitrag zu dieser Diskussion schreiben

Antwort auf Beitrag Nr.: 54.477.054 von OliKo am 06.03.17 17:33:05als es bis zum Abbau zu bringen (der natürlich noch viel mehr Geld verschlingen würde)

Aber doch auch ein klein wenig Kohle ins Haus oder.

Mann wäre doch blöde zu verkaufen wen die Kohle

sprudelt.....auf Jahre....

Aber doch auch ein klein wenig Kohle ins Haus oder.

Mann wäre doch blöde zu verkaufen wen die Kohle

sprudelt.....auf Jahre....

Antwort auf Beitrag Nr.: 54.468.051 von phobieeee am 05.03.17 11:14:14ich glaube nicht, dass man solange warten muss...

Berkeley Energia ist eine Investmentidee, die aktuell nur in die Erschließung investiert, da der Uranpreis noch am Boden ist...

die Chance ist größer vorher zu einem tollen Preis zu verkaufen, als es bis zum Abbau zu bringen (der natürlich noch viel mehr Geld verschlingen würde)

da wir in Europa soetwas weniger nachfragen, kommt irgendwann ein zahlungskräftiger Käufer der das Ding braucht und alles kauft (z.B. China :-) )

Berkeley Energia ist eine Investmentidee, die aktuell nur in die Erschließung investiert, da der Uranpreis noch am Boden ist...

die Chance ist größer vorher zu einem tollen Preis zu verkaufen, als es bis zum Abbau zu bringen (der natürlich noch viel mehr Geld verschlingen würde)

da wir in Europa soetwas weniger nachfragen, kommt irgendwann ein zahlungskräftiger Käufer der das Ding braucht und alles kauft (z.B. China :-) )

Antwort auf Beitrag Nr.: 54.466.722 von spezi1000 am 04.03.17 20:44:42Als Orientierung

Gruß phobieeee

Gruß phobieeee

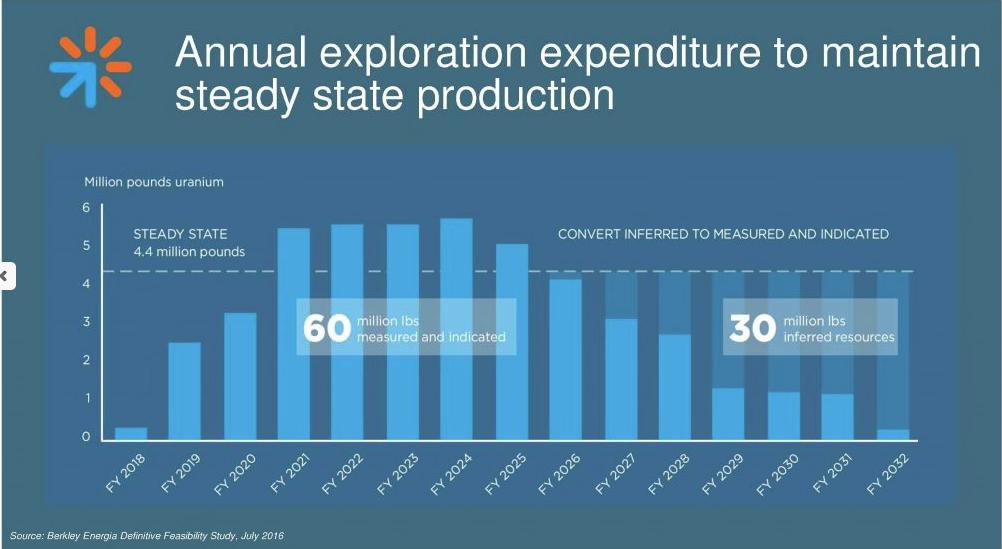

weiß jemand wann die Anlage genau fertig wird bzw. die Produktion genau losgeht und wieviel Uran Berkeley im ersten, zweiten, dritten Jahr abbauen will. Glaube kaum das sie im ersten Jahr 4 Mio Pfund schaffen.

Mittlerweile wird bky im vergleich zu den kanadisichen peers wieder billiger. 155 mil € MK im Vergleich zu efr 115 mil €. Vielleicht überlege ich es mir doch noch ;-)

Trading Spotlight

Antwort auf Beitrag Nr.: 54.432.029 von phobieeee am 28.02.17 17:56:41einigen wir uns auf den hier???

http://www.cmegroup.com/trading/metals/other/uranium.html

http://www.cmegroup.com/trading/metals/other/uranium.html

http://www.cmegroup.com/trading/metals/other/uranium.html

http://www.cmegroup.com/trading/metals/other/uranium.html

Antwort auf Beitrag Nr.: 54.431.804 von TraeidIngIdI0t am 28.02.17 17:38:28Hallo,

sehe ich nicht so kritisch. Sicherlich ist der Kurssrückgang nicht so schön, läd aber zur Positionsvergrößerung ein.

Dein Future Uranpreis ist mir suspekt, halte mich da lieber an den wöchentlichen Preis wie auf https://www.uxc.com/p/prices/UxCPrices.aspx" target="_blank" rel="nofollow ugc noopener">

https://www.uxc.com/p/prices/UxCPrices.aspx veröffentlicht. Neuste Zahlen dürften in Kürze eintreffen.

Weekly Spot Ux U3O8 Prices as of February 20, 2017 = $24.50

Ja der Uranpreis ist aktuell rückläufig, aber für BKY speziell nicht der Beinbruch aktuell, wohl aber für bestehende Produzenten. Eine weitere Marktbereinigung kann für BKY nur von Vorteil sein, PA sieht dies ähnlich und hat dies öfters betont.

Gruß phobieeee

sehe ich nicht so kritisch. Sicherlich ist der Kurssrückgang nicht so schön, läd aber zur Positionsvergrößerung ein.

Dein Future Uranpreis ist mir suspekt, halte mich da lieber an den wöchentlichen Preis wie auf https://www.uxc.com/p/prices/UxCPrices.aspx" target="_blank" rel="nofollow ugc noopener">

https://www.uxc.com/p/prices/UxCPrices.aspx veröffentlicht. Neuste Zahlen dürften in Kürze eintreffen.

Weekly Spot Ux U3O8 Prices as of February 20, 2017 = $24.50

Ja der Uranpreis ist aktuell rückläufig, aber für BKY speziell nicht der Beinbruch aktuell, wohl aber für bestehende Produzenten. Eine weitere Marktbereinigung kann für BKY nur von Vorteil sein, PA sieht dies ähnlich und hat dies öfters betont.

Gruß phobieeee

Spotmarkt

Tja, das (kurs)-entscheidende ist derzeit in Ermangelung von Unternehmensnachrichten der Uranpreis. Und da sieht`s momentan mal wieder mau aus:https://de.investing.com/commodities/uranium-futures

Berkeley present at our next London seminar on the 8th March

http://www.sharesoc.org/london-mar.html[/url]

Gruß phobieeee

http://www.sharesoc.org/london-mar.html[/url]

Gruß phobieeee

Three of the UK’s top mining analysts value Berkeley Energia (BKY.L) at over £1 per share

Three of London’s top mining analysts Paul Smith of WH Ireland, Michael Stoner of Peel Hunt and Ben Davies of Liberum have recently published updated research reports valuing the company well in excess of £1 per share.

Paul Smith reiterated his BUY recommendation with an increased target price of £1.28. His note highlights that the Salamanca mine is “a stand out project globally” and one of only a handful of uranium projects worldwide that is financially robust enough to proceed towards construction at currently depressed uranium prices.

Smith notes that the major catalysts to the share price are further exploration success at Zona 7 and additions to the recently signed long term offtake contracts.

Michael Stoner has an NAV of £1.18 per share and reiterates his BUY recommendation based on a risk weighted NAV of 90 pence per share. “We expect the company to deliver further offtake contracts, the start of construction, debt funding and the balance of the project funding through a strategic stake sell down. Each of these milestones de-risks the path to production and should yield individual re-ratings.”

Ben Davies has a Fair Value based on conservative NPV assumptions of £1.06 per share and a HOLD recommendation based on a share price of 60 pence per share. He highlights that the Company continues to deliver on its key aims on offtake contracts, initial financing and commencement of construction.

Despite forecasting a subdued uranium price outlook Davies demonstrates the project’s free cash flow of over US$150 million per year once in full production.

In light of the Company’s announcement that the cost of the recently ordered crushers has come in at 20% lower than estimates he has calculated that a reduction of 10% in capital and operating cost would increase his valuation to £1.18 per share.

Following an oversubscribed equity funding from London’s blue institutions the Company has over US$30 million in cash and is accelerating the development of the Salamanca project.

---

Kam gerade per Mail

Gruß phobieeee

Three of London’s top mining analysts Paul Smith of WH Ireland, Michael Stoner of Peel Hunt and Ben Davies of Liberum have recently published updated research reports valuing the company well in excess of £1 per share.

Paul Smith reiterated his BUY recommendation with an increased target price of £1.28. His note highlights that the Salamanca mine is “a stand out project globally” and one of only a handful of uranium projects worldwide that is financially robust enough to proceed towards construction at currently depressed uranium prices.

Smith notes that the major catalysts to the share price are further exploration success at Zona 7 and additions to the recently signed long term offtake contracts.

Michael Stoner has an NAV of £1.18 per share and reiterates his BUY recommendation based on a risk weighted NAV of 90 pence per share. “We expect the company to deliver further offtake contracts, the start of construction, debt funding and the balance of the project funding through a strategic stake sell down. Each of these milestones de-risks the path to production and should yield individual re-ratings.”

Ben Davies has a Fair Value based on conservative NPV assumptions of £1.06 per share and a HOLD recommendation based on a share price of 60 pence per share. He highlights that the Company continues to deliver on its key aims on offtake contracts, initial financing and commencement of construction.

Despite forecasting a subdued uranium price outlook Davies demonstrates the project’s free cash flow of over US$150 million per year once in full production.

In light of the Company’s announcement that the cost of the recently ordered crushers has come in at 20% lower than estimates he has calculated that a reduction of 10% in capital and operating cost would increase his valuation to £1.18 per share.

Following an oversubscribed equity funding from London’s blue institutions the Company has over US$30 million in cash and is accelerating the development of the Salamanca project.

---

Kam gerade per Mail

Gruß phobieeee