Clarkson - Infodienstleister Schiffbranche - 500 Beiträge pro Seite

eröffnet am 04.03.11 14:59:28 von

neuester Beitrag 23.09.19 12:26:28 von

neuester Beitrag 23.09.19 12:26:28 von

Beiträge: 13

ID: 1.164.319

ID: 1.164.319

Aufrufe heute: 0

Gesamt: 1.518

Gesamt: 1.518

Aktive User: 0

ISIN: GB0002018363 · WKN: 872503

46,30

EUR

0,00 %

0,00 EUR

Letzter Kurs 08:15:59 Lang & Schwarz

Neuigkeiten

Werte aus der Branche Dienstleistungen

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,0000 | +99.999,00 | |

| 0,6197 | +138,36 | |

| 0,6000 | +50,00 | |

| 5,3000 | +42,47 | |

| 89,00 | +34,83 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,6201 | -13,59 | |

| 12,000 | -17,24 | |

| 14,000 | -26,32 | |

| 1,0300 | -30,87 | |

| 0,5500 | -57,69 |

...mit derzeit rund 4% Dividendenrendite.

Wie bei solchen Firmen üblich, schlanke Bilanz und gute Kapitalrendite.

Bewertung noch im Rahmen, allerdings ist Kurs in der Nähe des all-time high

Watchlist...

Wie bei solchen Firmen üblich, schlanke Bilanz und gute Kapitalrendite.

Bewertung noch im Rahmen, allerdings ist Kurs in der Nähe des all-time high

Watchlist...

nicht viel passiert seitdem;

H1-12 ungefähr gleich wie H1-2011

aktuell 4,3% Divi

H1-12 ungefähr gleich wie H1-2011

aktuell 4,3% Divi

Antwort auf Beitrag Nr.: 43.943.584 von R-BgO am 19.12.12 11:45:22na ja, nicht ganz identisch:

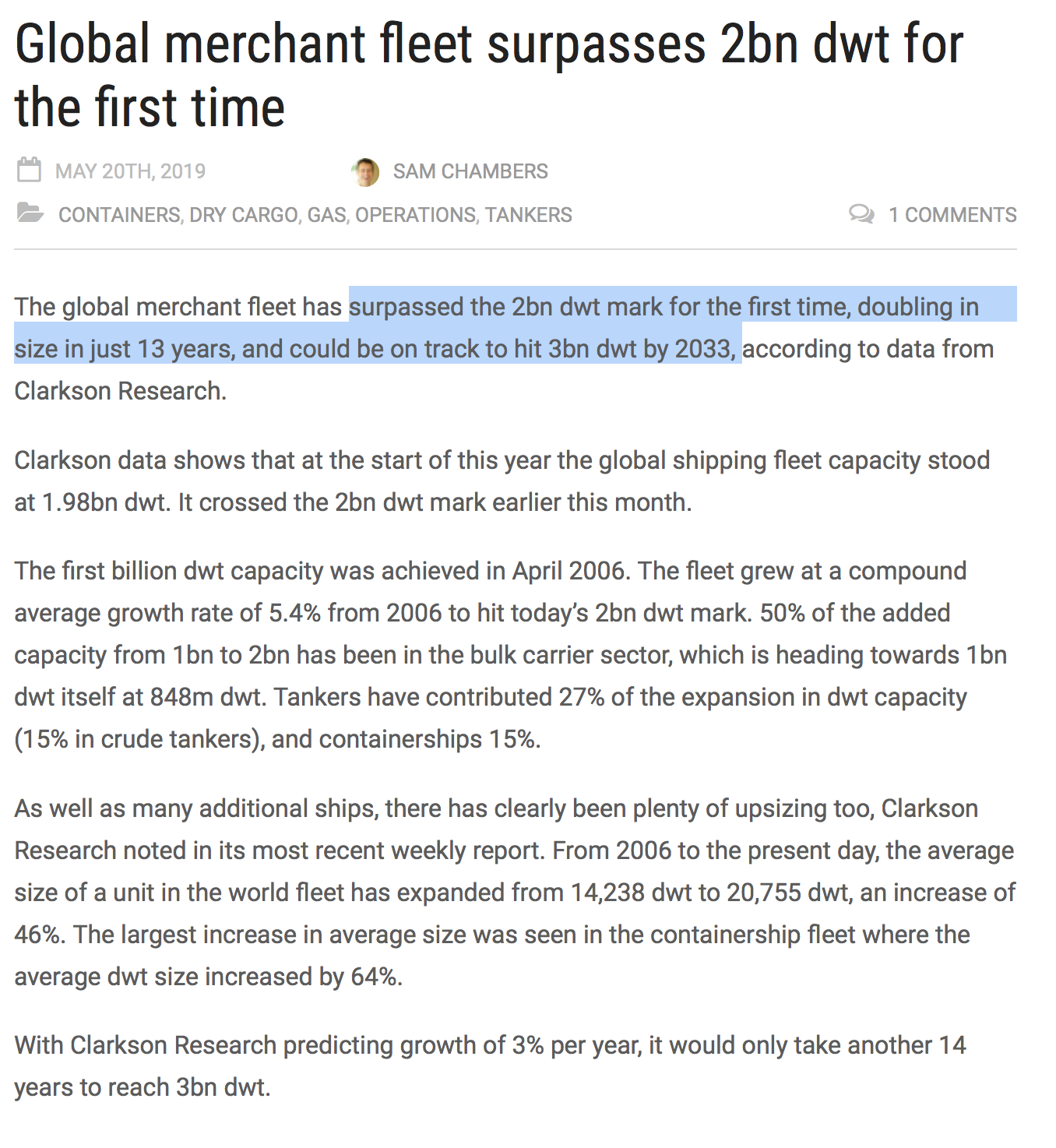

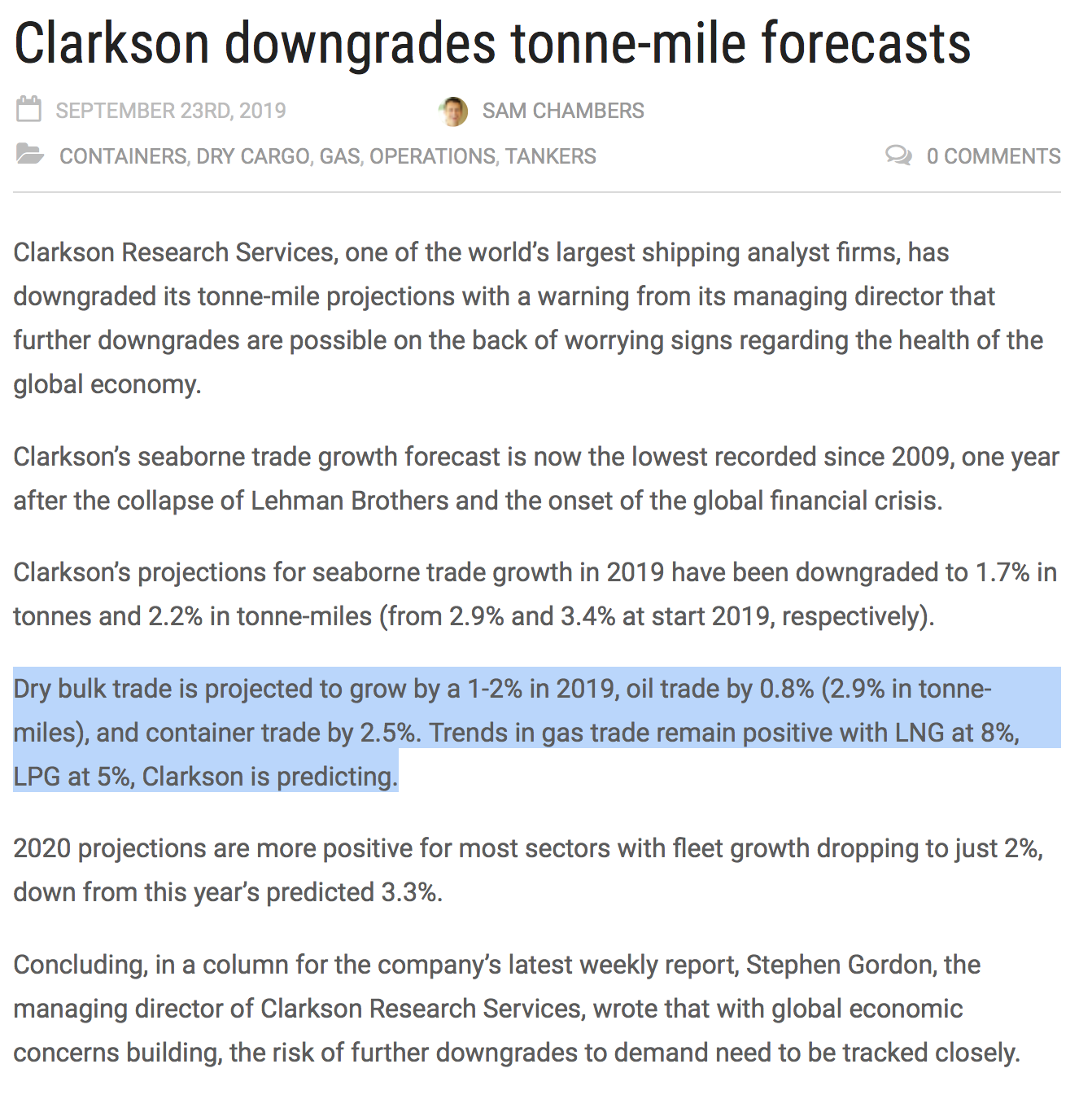

Clarkson sails into stormy seas

Wed 07 Nov 2012

LONDON (SHARECAST) - Ship broker Clarkson fell on Wednesday morning following a profits warning, which it blamed on global economic uncertainty reflected in reduced freight rates and lower asset prices.

In a trading update, the company commented: “The short-term outlook for rates and values is uncertain, with demand/supply imbalance a brake on recovery and continued weakness in capital markets. Lower than anticipated activity in the second half, particularly in broking and financial, has resulted in a reduction in the board's expectations for the full year results. Nevertheless Clarksons remains well placed to cope with current conditions and gain from recovery when it arrives”.

Its ship broking operation has been hard hit by the continued cyclical downturn in the shipping industry, with freight rates falling and downward pressure on asset prices across a number of sectors. Tightness in the debt market, especially for second hand tonnage, has further reduced the volume of sales and the value of the vessels hitting its revenues.

As if this weren’t enough, the weakening of the dollar against sterling has put further pressure on reported revenues.

All this has only been partially mitigated by increased transaction volumes through its general broking operations.

Its boutique investment banking operation for the shipping industry, Clarkson Capital Markets has suffered from very low levels of transactions, and the downsizing of its Dubai operations are well advanced.

One silver cloud is the strength of its research division that has delivered sound growth, while its port and agency services are trading in line.

Broker comment

Gert Zonneveld, analyst at house broker Panmure Gordon, retained his ‘hold’ recommendation with a price target of 1500p.

He commented: “Trading activity in the second half of the year to date has been weaker than expected, particularly in broking and financial, which has resulted in a reduction in the board’s expectations for the full year results.

"We have reduced our earnings forecasts to reflect the difficult market conditions in the shipping markets. Even though we remain bullish on the longer term prospects for Clarksons, we recognise the short term challenges. We expect the company to maintain its progressive dividend policy.”

Zonneveld has cut his adjusted earnings per share (EPS) estimate to 76.46p from 90.3p for 2012, with a reduction in 2013 to 92.27p from 112.4p. However, he expects the company to maintain its progressive dividend policy.

Clarkson sails into stormy seas

Wed 07 Nov 2012

LONDON (SHARECAST) - Ship broker Clarkson fell on Wednesday morning following a profits warning, which it blamed on global economic uncertainty reflected in reduced freight rates and lower asset prices.

In a trading update, the company commented: “The short-term outlook for rates and values is uncertain, with demand/supply imbalance a brake on recovery and continued weakness in capital markets. Lower than anticipated activity in the second half, particularly in broking and financial, has resulted in a reduction in the board's expectations for the full year results. Nevertheless Clarksons remains well placed to cope with current conditions and gain from recovery when it arrives”.

Its ship broking operation has been hard hit by the continued cyclical downturn in the shipping industry, with freight rates falling and downward pressure on asset prices across a number of sectors. Tightness in the debt market, especially for second hand tonnage, has further reduced the volume of sales and the value of the vessels hitting its revenues.

As if this weren’t enough, the weakening of the dollar against sterling has put further pressure on reported revenues.

All this has only been partially mitigated by increased transaction volumes through its general broking operations.

Its boutique investment banking operation for the shipping industry, Clarkson Capital Markets has suffered from very low levels of transactions, and the downsizing of its Dubai operations are well advanced.

One silver cloud is the strength of its research division that has delivered sound growth, while its port and agency services are trading in line.

Broker comment

Gert Zonneveld, analyst at house broker Panmure Gordon, retained his ‘hold’ recommendation with a price target of 1500p.

He commented: “Trading activity in the second half of the year to date has been weaker than expected, particularly in broking and financial, which has resulted in a reduction in the board’s expectations for the full year results.

"We have reduced our earnings forecasts to reflect the difficult market conditions in the shipping markets. Even though we remain bullish on the longer term prospects for Clarksons, we recognise the short term challenges. We expect the company to maintain its progressive dividend policy.”

Zonneveld has cut his adjusted earnings per share (EPS) estimate to 76.46p from 90.3p for 2012, with a reduction in 2013 to 92.27p from 112.4p. However, he expects the company to maintain its progressive dividend policy.

Antwort auf Beitrag Nr.: 43.943.618 von R-BgO am 19.12.12 11:53:15nett weitergelaufen

aus Bewertungsgründen bis auf ein Erinnerungsstück verkauft

Trading Spotlight

Antwort auf Beitrag Nr.: 48.310.354 von R-BgO am 13.11.14 14:34:28

Aktie weiter teuer.

Aber die Präsentationen sind Pflichtlektüre: http://www.clarksons.com/media/1086625/Preliminary%20Results…

Seitdem Fusion mit Platou,

und solides Jahresergebnis 2015;Aktie weiter teuer.

Aber die Präsentationen sind Pflichtlektüre: http://www.clarksons.com/media/1086625/Preliminary%20Results…

Antwort auf Beitrag Nr.: 52.223.977 von R-BgO am 19.04.16 14:24:18

wie eh' und je

dem ist nichts hinzuzufügen ein Wettbewerber

Thread: Braemar Shipping Services

still too expensive

Beitrag zu dieser Diskussion schreiben

Zu dieser Diskussion können keine Beiträge mehr verfasst werden, da der letzte Beitrag vor mehr als zwei Jahren verfasst wurde und die Diskussion daraufhin archiviert wurde.

Bitte wenden Sie sich an feedback@wallstreet-online.de und erfragen Sie die Reaktivierung der Diskussion oder starten Sie eine neue Diskussion.

Investoren beobachten auch:

| Wertpapier | Perf. % |

|---|---|

| +0,29 | |

| +0,22 | |

| +0,23 | |

| -0,41 | |

| +0,64 | |

| +1,83 | |

| +0,29 | |

| +0,21 | |

| +0,30 | |

| +0,78 |

Meistdiskutiert

| Wertpapier | Beiträge | |

|---|---|---|

| 80 | ||

| 48 | ||

| 28 | ||

| 24 | ||

| 23 | ||

| 21 | ||

| 16 | ||

| 14 | ||

| 13 | ||

| 10 |