Super günstiges Uran durch Berkeley Energia (Seite 111)

eröffnet am 20.01.16 15:19:16 von

neuester Beitrag 11.04.24 15:39:14 von

neuester Beitrag 11.04.24 15:39:14 von

Beiträge: 1.266

ID: 1.225.023

ID: 1.225.023

Aufrufe heute: 0

Gesamt: 112.901

Gesamt: 112.901

Aktive User: 0

ISIN: AU000000BKY0 · WKN: 911733 · Symbol: B5R

0,2245

EUR

+1,13 %

+0,0025 EUR

Letzter Kurs 26.04.24 Tradegate

Neuigkeiten

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 2,6900 | +23,96 | |

| 5,1500 | +21,75 | |

| 15,890 | +21,67 | |

| 0,8900 | +17,11 | |

| 0,9000 | +16,13 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,5180 | -7,09 | |

| 10,040 | -7,89 | |

| 0,5700 | -8,06 | |

| 0,5400 | -8,47 | |

| 46,88 | -97,99 |

Beitrag zu dieser Diskussion schreiben

Antwort auf Beitrag Nr.: 52.832.836 von IllePille am 14.07.16 14:04:58Hallo,

ja das liegt an der mehrstufigen Entwicklung des Projektes. Die notwendigen Mittel sollen jedoch aus dem Cashflow generiert werden. Ggf. einfach noch mal etwas mehr mit dem Wert als solches Beschäftigen.

Gruß phobieeee

ja das liegt an der mehrstufigen Entwicklung des Projektes. Die notwendigen Mittel sollen jedoch aus dem Cashflow generiert werden. Ggf. einfach noch mal etwas mehr mit dem Wert als solches Beschäftigen.

Gruß phobieeee

Gewinne von ungefähr 110 Mio USD !

aber nur, wenn sich der Uranpreis so stark entwickelt wie in der DFS unterstellt.

jetzt muss BKY aber erstmal das Investitionskapital auftreiben. Und da fand ich erste Tabelle etwas irreführend. Dort liest man "upfront capital U$95,7 Mio. Taucht man tiefer ins Dokument ein, findet man dies (Beträge von mir gerundet):

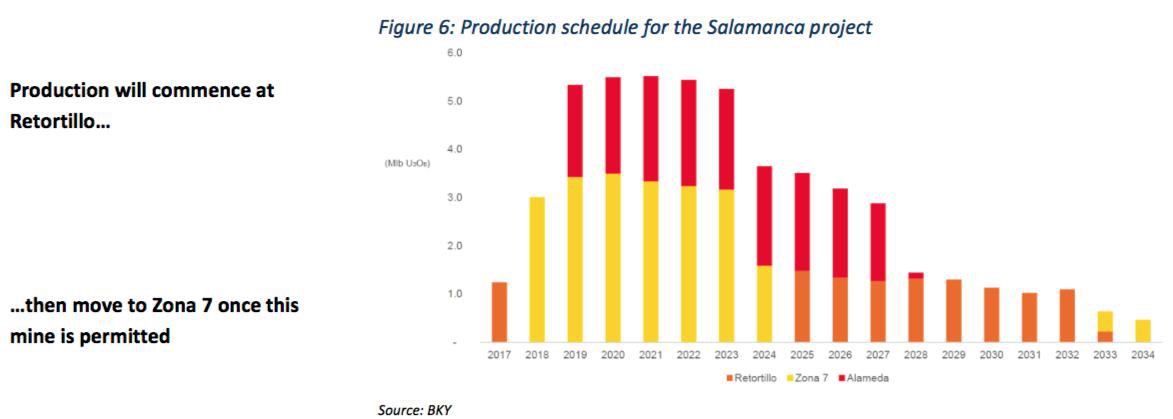

Initial CAPEX of all infrastructure and indirect costs required to develop and commence production at Retortillo is U$96 Mio.

Initial CAPEX for the mine, processing facilities and associated infrastructure for Zona 7 is U$59 Mio and will be incurred during 1.year of production.

Initial CAPEX for the mine, processing facilities and associated infrastructure for Alameda is U$80 Mio and will be incurred during 2.year of production.

aber nur, wenn sich der Uranpreis so stark entwickelt wie in der DFS unterstellt.

jetzt muss BKY aber erstmal das Investitionskapital auftreiben. Und da fand ich erste Tabelle etwas irreführend. Dort liest man "upfront capital U$95,7 Mio. Taucht man tiefer ins Dokument ein, findet man dies (Beträge von mir gerundet):

Initial CAPEX of all infrastructure and indirect costs required to develop and commence production at Retortillo is U$96 Mio.

Initial CAPEX for the mine, processing facilities and associated infrastructure for Zona 7 is U$59 Mio and will be incurred during 1.year of production.

Initial CAPEX for the mine, processing facilities and associated infrastructure for Alameda is U$80 Mio and will be incurred during 2.year of production.

Antwort auf Beitrag Nr.: 52.829.737 von Timesystem1002 am 14.07.16 08:42:05Stimme Dir zu, aktuell gibt es wenig Interesse im Sektor. Deshalb haben wir auch die Möglichkeit ein Weltklasseunternehmen wie Berkeley zu diesen niedrigen Preisen zu kaufen.

Berkeleys Projekt kann bei extrem niedrigen Uranpreisen fette Gewinne erwirtschaften, während Unternehmen wie Cameco hier keine Chance haben, mitzuhalten. Gewinne von ungefähr 110 Mio USD ! Nimmt man einen KGV von 6 oder 7 an, so haben wir locker ein MArketcap von 700 Mio.!

Berkeleys Projekt kann bei extrem niedrigen Uranpreisen fette Gewinne erwirtschaften, während Unternehmen wie Cameco hier keine Chance haben, mitzuhalten. Gewinne von ungefähr 110 Mio USD ! Nimmt man einen KGV von 6 oder 7 an, so haben wir locker ein MArketcap von 700 Mio.!

Antwort auf Beitrag Nr.: 52.829.647 von shamane am 14.07.16 08:35:14Da hast Du sicherlich Recht aber wer interessiert sich aktuell für Uran? Die Investmentgemeinde sicherlich nicht...wahrscheinlich dann die grossen Spieler...

Sieht eigentlich perfekt aus! Berkeley Energia ist das beste Uraninvestment!

An independent Study has confirmed the Salamanca project as one of the

world’s lowest cost producers capable of generating strong after tax cash flow

through the current

low point in the uranium price cycle.

A Definitive Feasibility Study has reported that over an initial ten

year period the project is capable of producing an average of 4.4 million pounds of

uranium per year at a cash cost of US$13.30 per pound and at a total cash

cost of US$15.06

per pound which compares with the current spot price of

US$26 per pound and term contract price of US$41 per

pound. During this ten year steady state period, based on the most recent UxC

forward curve of uranium prices, the project is expected to generate an

average annual net profit after tax

of US$ 116 million.

Trading Spotlight

DFS confirms Salamanca as one of the lowest cost producers

http://www.asx.com.au/asxpdf/20160714/pdf/438kgwz3q5rj72.pdf

http://www.asx.com.au/asxpdf/20160714/pdf/438kgwz3q5rj72.pdf

Antwort auf Beitrag Nr.: 52.826.347 von shamane am 13.07.16 17:47:42Hallo,

gut werden wird sie wohl, die Frage wird halt eher sein, ob die hohen Erwartungen an die DFS erfüllt werden. Es kann auch immer zu einem "sell on good news" kommen. Der heutige Entwicklung an der LSE würde ich nicht zuviel beimessen. Das dort heute weiter gehandelt wurde hängt auch nur damit zusammen, dass die Richtlinien der ASX strikter sind. Die Börsenplätze in DE wurden alle zeitig geschlossen und wer "zocken" wollte hat dies eben an der LSE gemacht. Der Umsatz war mit 544,593 Stücken auch nicht außergewöhnlich hoch. Das Groß wird sich vor der DFS positioniert haben, aus dem heiteren Himmel kommt die ja nicht.

Schauen wir mal.

Gruß phobieeee

gut werden wird sie wohl, die Frage wird halt eher sein, ob die hohen Erwartungen an die DFS erfüllt werden. Es kann auch immer zu einem "sell on good news" kommen. Der heutige Entwicklung an der LSE würde ich nicht zuviel beimessen. Das dort heute weiter gehandelt wurde hängt auch nur damit zusammen, dass die Richtlinien der ASX strikter sind. Die Börsenplätze in DE wurden alle zeitig geschlossen und wer "zocken" wollte hat dies eben an der LSE gemacht. Der Umsatz war mit 544,593 Stücken auch nicht außergewöhnlich hoch. Das Groß wird sich vor der DFS positioniert haben, aus dem heiteren Himmel kommt die ja nicht.

Schauen wir mal.

Gruß phobieeee

plus 10 % in London! DFS wird wohl gut werden.

das sieht sehr interessant aus . bin mal gespannt, was für Zahlen sie bringen werden.

In London kann man noch handeln!!!

In London kann man noch handeln!!!

DFS

13.07.16

Request for Trading Halt

Berkeley Energia Limited (ASX:BKY) requests an immediate voluntary trading halt to the Company’s securities, pending an announcement regarding a Definitive Feasibility Study at the Salamanca project.

The Company requests that the trading halt remain until the earlier of an announcement to the market regarding the above or the opening of trade on ASX on 15 July 2016.

The Company is not aware of any reason why the trading halt should not be granted.

http://www.stocknessmonster.com/news-item?S=BKY&E=ASX&N=7822…

13.07.16

Request for Trading Halt

Berkeley Energia Limited (ASX:BKY) requests an immediate voluntary trading halt to the Company’s securities, pending an announcement regarding a Definitive Feasibility Study at the Salamanca project.

The Company requests that the trading halt remain until the earlier of an announcement to the market regarding the above or the opening of trade on ASX on 15 July 2016.

The Company is not aware of any reason why the trading halt should not be granted.

http://www.stocknessmonster.com/news-item?S=BKY&E=ASX&N=7822…