LYNAS - Faktenthread, Analysen, Querverweise u. Meldungen zum Unternehmen (Seite 258)

eröffnet am 25.04.07 13:15:18 von

neuester Beitrag 29.04.24 12:08:30 von

neuester Beitrag 29.04.24 12:08:30 von

Beiträge: 3.528

ID: 1.126.458

ID: 1.126.458

Aufrufe heute: 12

Gesamt: 784.855

Gesamt: 784.855

Aktive User: 0

ISIN: AU000000LYC6 · WKN: 871899 · Symbol: LYI

3,9570

EUR

-0,25 %

-0,0100 EUR

Letzter Kurs 18:39:39 Tradegate

Neuigkeiten

18.04.24 · Der Aktionär TV |

23.01.24 · kapitalerhoehungen.de |

22.01.24 · wallstreetONLINE Redaktion |

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,0000 | +16,28 | |

| 2,5950 | +15,33 | |

| 0,5340 | +12,90 | |

| 0,8947 | +11,85 | |

| 0,8000 | +11,03 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 183,20 | -19,30 | |

| 0,7500 | -21,05 | |

| 1,1367 | -22,67 | |

| 12,000 | -25,00 | |

| 8,3600 | -39,81 |

Beitrag zu dieser Diskussion schreiben

!

Dieser Beitrag wurde vom System automatisch gesperrt. Bei Fragen wenden Sie sich bitte an feedback@wallstreet-online.de!

Dieser Beitrag wurde vom System automatisch gesperrt. Bei Fragen wenden Sie sich bitte an feedback@wallstreet-online.de

Antwort auf Beitrag Nr.: 40.505.361 von Optimist_ am 11.11.10 19:32:31 -  - Stimmt genau!

- Stimmt genau!

http://www.rohstoff-welt.de/news/artikel.php?sid=22723

Seltene Erden: Drohen Versorgungsengpässe?

12.11.2010 | 9:00 Uhr | Weinberg, Eugen, Commerzbank AG

Die Welt sorgt sich aktuell um die Verfügbarkeit sog. "Seltener Erden". Diese Metalle sind essentielle Bestandteile in der Herstellung vieler industrieller Produkte. China, das fast ein Monopol bei der Produktion von Seltenen Erden hat, hat die Exportquoten für diese Rohstoffe drastisch gekürzt und dreht der Welt quasi den Hahn zu. Angesichts des sich abzeichnenden Nachfrageüberschusses werden zumindest die Preise deutlich steigen, wenn es nicht sogar zu Versorgungsengpässen kommt.

Unter dem Begriff "Seltene Erden" wird die chemische Gruppe der Lanthanoide zusammengefasst. Diese besteht aus den folgenden 17 Elementen des Periodensystems: Lanthan, Cer, Praseodym, Neodym, Promethium, Samarium, Europium, Gadolinium, Terbium, Dysprosium, Holmium, Erbium, Thulium, Ytterbium, Lutetium, Yttrium und Scandium. In der Industrie werden sie zum Beispiel in der Unterhaltungselektronik (iPod, Plasmabildschirme), Kommunikationstechnologie (BlackBerrys), Automobilindustrie (Hybridmotoren) und alternativen Energiegewinnung (Windturbinen) eingesetzt. Daneben kommen sie in der Rüstungsindustrie und hier vor allem in Radar- und Raketenlenksystemen zur Verwendung. Die Seltenen Erden machen zwar nur einen Promilleanteil in der Herstellung vieler industrieller Produkte aus, sind aber essentiell und können kaum ersetzt werden.

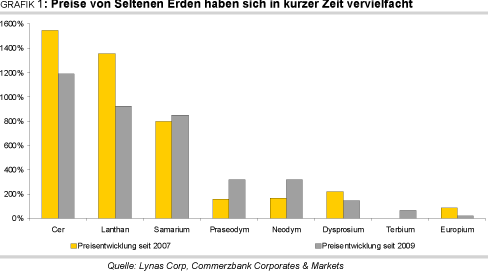

Die Preise Seltener Erden haben sich in den letzten Jahren und insbesondere in diesem Jahr rasant nach oben entwickelt. Cer beispielsweise stieg von durchschnittlich 3,88 USD je kg 2009 auf 50 USD je kg Anfang November. Lanthan hat sich, ebenfalls verglichen zum Durchschnittspreis von 2009, bis heute verzehnfacht. Terbium und Europium sehen da in diesem Vergleich mit Preiszuwächsen von 70% bzw. 23% relativ "schwach" aus (Grafik 1). Im Gegensatz zu den gängigen Metallen gibt es für Seltene Erden keinen Börsenhandel. Somit ist die Preisgestaltung sehr intransparent und weder Verbraucher noch Produzenten haben die Möglichkeit, Preise abzusichern.

Seltene Erden sind jedoch keineswegs so selten wie der Name vermuten lässt. So steht beispielsweise Cer bezüglich der Häufigkeit an 26. Stelle unter den Elementen. Es kommt fünfmal häufiger vor als Blei. Thulium, das seltenste Element der Seltenen Erden, ist immer noch häufiger vorhanden als Gold oder Platin. Aufgrund ihrer ähnlichen Eigenschaften treten die Seltenen Erden überwiegend gemeinsam auf, allerdings nur in geringen Konzentrationen und Qualität, so dass sich ein wirtschaftlicher Abbau bislang kaum gelohnt hat. Zur kommerziellen Nutzung müssen sie zumeist aufwendig voneinander getrennt werden. Sie zeichnen sich durch eine ausgeprägte Immobilität (Stabilität/Unlöslichkeit) im Verwitterungskreislauf aus, das heißt in neutralem und alkalischem Wasser sind sie nur schwer zu lösen.

Gemäß Angaben von U.S. Geological Survey betrugen die weltweiten bekannten ReservenEnde 2009 rund 99 Mio. Tonnen. Beim derzeitigen Produktionsniveau von ungefähr 124 Tsd.Tonnen reichen sie rund 800 Jahre. Die aktuelle globale Produktion liegt damit gut 9% unterdem bisherigen Spitzenwert von 137 Tsd. Tonnen im Jahr 2006. Das Produktionswachstum hatsich auf jährlich rund 4% in der Zeit von 2000 bis 2009 abgeschwächt, nach knapp 7% p.a. inden Jahren 1965 bis 2000. China besitzt mit einem Anteil von 37% die höchsten Reserven, gefolgt von den Staaten der ehemaligen Sowjetunion (19%), den USA (13%) und Australien (5%). Weitere Vorkommen an Seltenen Erden gibt es auch andernorts auf der Welt. Geprüft wird der Abbau unter anderem in Kanada und Grönland. In Afrika zum Beispiel wurde bislang wegen ihrer zuvor geringen wirtschaftlichen Bedeutung und der geringen Menge noch gar nicht nach Seltenen Erden gesucht.

Mit 97% der globalen Produktion ist China das größte Produzentenland für Seltene Erden. Das Reich der Mitte hat damit ein Quasi-Monopol am Weltmarkt (Grafiken 2 und 3). Dieses wird auch konsequent weiter ausgebaut. China verfügt zurzeit über das beste Know-how im Bereich der Gewinnung von Seltenen Erden und weist darüber hinaus die notwendigen Förderkapazitäten, Infrastruktur und Vertriebskanäle auf. Zudem herrschen dort relativ laxe Umwelt- und Arbeitsschutzstandards und die Arbeitskosten sind gering.

China, bislang ein relativ zuverlässiger Lieferant von Seltenen Erden, hat im Frühjahr dieses Jahres mit dem Aufbau strategischer Reserven für diese Rohstoffe begonnen. Darüber hinaus hat das Land in den letzten Jahren bereits die Exportquoten kontinuierlich gekürzt und eine Exportsteuer auf diese Metalle eingeführt (Grafik 4, S. 3). Im Juli hat China schließlich die Welt geschockt, indem es die Exportquoten für das zweite Halbjahr 2010 im Vergleich zum Vorjahr nochmals deutlich um 72% gekürzt hat, um die heimische Nachfrage zu befriedigen. Eine weitere Reduzierung der Exportquoten für das nächste Jahr ist möglich. Darüber hinaus plant die chinesische Regierung, bis 2015 die Anzahl der produzierenden Unternehmen von Seltenen Erden deutlich auf nur noch 20 zu reduzieren, was zu einer höheren Konzentration und Marktmacht auf der Anbieterseite führen wird.

Seitdem sieht sich China jedoch einem hohen internationalen Druck ausgesetzt und riskiert einen Handelsstreit sowohl mit Japan als auch den USA. Laut japanischen und US-amerikanischen Medienberichten hat China als politisches Druckmittel die Exporte von Seltenen Erden nach Japan gestoppt. Dies wird von chinesischer Seite jedoch dementiert. Pressemeldungen zufolge prüft zudem die USA die Einreichung einer Klage gegen China vor der Welthandelsorganisation (WTO). Beide Länder sind stark auf Importe von Seltenen Erden angewiesen, wobei Japan der weltweit größte Importeur dieser Metalle ist.

Im Oktober hat das chinesische Handelsministerium überraschend verkündet, dass die bekannten Reserven Chinas auf Basis der aktuellen Produktionsraten nur noch für 15-20 Jahre reichen würden. Das Ministerium schließt nicht aus, in einigen Jahren sogar Seltene Erden importieren zu müssen. Dies würde das ohnehin schon extrem knappe Angebot am Weltmarkt weiter einengen und wäre wohl als Super-GAU für die Abnehmerländer zu bezeichnen. Diese Aussagen dürften aber eher in einem politischen Zusammenhang stehen.

usw. Seiten: 1 | 2 | 3 »

@ ein schönes WE

Grüsse JoJo

- Stimmt genau!

- Stimmt genau!http://www.rohstoff-welt.de/news/artikel.php?sid=22723

Seltene Erden: Drohen Versorgungsengpässe?

12.11.2010 | 9:00 Uhr | Weinberg, Eugen, Commerzbank AG

Die Welt sorgt sich aktuell um die Verfügbarkeit sog. "Seltener Erden". Diese Metalle sind essentielle Bestandteile in der Herstellung vieler industrieller Produkte. China, das fast ein Monopol bei der Produktion von Seltenen Erden hat, hat die Exportquoten für diese Rohstoffe drastisch gekürzt und dreht der Welt quasi den Hahn zu. Angesichts des sich abzeichnenden Nachfrageüberschusses werden zumindest die Preise deutlich steigen, wenn es nicht sogar zu Versorgungsengpässen kommt.

Unter dem Begriff "Seltene Erden" wird die chemische Gruppe der Lanthanoide zusammengefasst. Diese besteht aus den folgenden 17 Elementen des Periodensystems: Lanthan, Cer, Praseodym, Neodym, Promethium, Samarium, Europium, Gadolinium, Terbium, Dysprosium, Holmium, Erbium, Thulium, Ytterbium, Lutetium, Yttrium und Scandium. In der Industrie werden sie zum Beispiel in der Unterhaltungselektronik (iPod, Plasmabildschirme), Kommunikationstechnologie (BlackBerrys), Automobilindustrie (Hybridmotoren) und alternativen Energiegewinnung (Windturbinen) eingesetzt. Daneben kommen sie in der Rüstungsindustrie und hier vor allem in Radar- und Raketenlenksystemen zur Verwendung. Die Seltenen Erden machen zwar nur einen Promilleanteil in der Herstellung vieler industrieller Produkte aus, sind aber essentiell und können kaum ersetzt werden.

Die Preise Seltener Erden haben sich in den letzten Jahren und insbesondere in diesem Jahr rasant nach oben entwickelt. Cer beispielsweise stieg von durchschnittlich 3,88 USD je kg 2009 auf 50 USD je kg Anfang November. Lanthan hat sich, ebenfalls verglichen zum Durchschnittspreis von 2009, bis heute verzehnfacht. Terbium und Europium sehen da in diesem Vergleich mit Preiszuwächsen von 70% bzw. 23% relativ "schwach" aus (Grafik 1). Im Gegensatz zu den gängigen Metallen gibt es für Seltene Erden keinen Börsenhandel. Somit ist die Preisgestaltung sehr intransparent und weder Verbraucher noch Produzenten haben die Möglichkeit, Preise abzusichern.

Seltene Erden sind jedoch keineswegs so selten wie der Name vermuten lässt. So steht beispielsweise Cer bezüglich der Häufigkeit an 26. Stelle unter den Elementen. Es kommt fünfmal häufiger vor als Blei. Thulium, das seltenste Element der Seltenen Erden, ist immer noch häufiger vorhanden als Gold oder Platin. Aufgrund ihrer ähnlichen Eigenschaften treten die Seltenen Erden überwiegend gemeinsam auf, allerdings nur in geringen Konzentrationen und Qualität, so dass sich ein wirtschaftlicher Abbau bislang kaum gelohnt hat. Zur kommerziellen Nutzung müssen sie zumeist aufwendig voneinander getrennt werden. Sie zeichnen sich durch eine ausgeprägte Immobilität (Stabilität/Unlöslichkeit) im Verwitterungskreislauf aus, das heißt in neutralem und alkalischem Wasser sind sie nur schwer zu lösen.

Gemäß Angaben von U.S. Geological Survey betrugen die weltweiten bekannten ReservenEnde 2009 rund 99 Mio. Tonnen. Beim derzeitigen Produktionsniveau von ungefähr 124 Tsd.Tonnen reichen sie rund 800 Jahre. Die aktuelle globale Produktion liegt damit gut 9% unterdem bisherigen Spitzenwert von 137 Tsd. Tonnen im Jahr 2006. Das Produktionswachstum hatsich auf jährlich rund 4% in der Zeit von 2000 bis 2009 abgeschwächt, nach knapp 7% p.a. inden Jahren 1965 bis 2000. China besitzt mit einem Anteil von 37% die höchsten Reserven, gefolgt von den Staaten der ehemaligen Sowjetunion (19%), den USA (13%) und Australien (5%). Weitere Vorkommen an Seltenen Erden gibt es auch andernorts auf der Welt. Geprüft wird der Abbau unter anderem in Kanada und Grönland. In Afrika zum Beispiel wurde bislang wegen ihrer zuvor geringen wirtschaftlichen Bedeutung und der geringen Menge noch gar nicht nach Seltenen Erden gesucht.

Mit 97% der globalen Produktion ist China das größte Produzentenland für Seltene Erden. Das Reich der Mitte hat damit ein Quasi-Monopol am Weltmarkt (Grafiken 2 und 3). Dieses wird auch konsequent weiter ausgebaut. China verfügt zurzeit über das beste Know-how im Bereich der Gewinnung von Seltenen Erden und weist darüber hinaus die notwendigen Förderkapazitäten, Infrastruktur und Vertriebskanäle auf. Zudem herrschen dort relativ laxe Umwelt- und Arbeitsschutzstandards und die Arbeitskosten sind gering.

China, bislang ein relativ zuverlässiger Lieferant von Seltenen Erden, hat im Frühjahr dieses Jahres mit dem Aufbau strategischer Reserven für diese Rohstoffe begonnen. Darüber hinaus hat das Land in den letzten Jahren bereits die Exportquoten kontinuierlich gekürzt und eine Exportsteuer auf diese Metalle eingeführt (Grafik 4, S. 3). Im Juli hat China schließlich die Welt geschockt, indem es die Exportquoten für das zweite Halbjahr 2010 im Vergleich zum Vorjahr nochmals deutlich um 72% gekürzt hat, um die heimische Nachfrage zu befriedigen. Eine weitere Reduzierung der Exportquoten für das nächste Jahr ist möglich. Darüber hinaus plant die chinesische Regierung, bis 2015 die Anzahl der produzierenden Unternehmen von Seltenen Erden deutlich auf nur noch 20 zu reduzieren, was zu einer höheren Konzentration und Marktmacht auf der Anbieterseite führen wird.

Seitdem sieht sich China jedoch einem hohen internationalen Druck ausgesetzt und riskiert einen Handelsstreit sowohl mit Japan als auch den USA. Laut japanischen und US-amerikanischen Medienberichten hat China als politisches Druckmittel die Exporte von Seltenen Erden nach Japan gestoppt. Dies wird von chinesischer Seite jedoch dementiert. Pressemeldungen zufolge prüft zudem die USA die Einreichung einer Klage gegen China vor der Welthandelsorganisation (WTO). Beide Länder sind stark auf Importe von Seltenen Erden angewiesen, wobei Japan der weltweit größte Importeur dieser Metalle ist.

Im Oktober hat das chinesische Handelsministerium überraschend verkündet, dass die bekannten Reserven Chinas auf Basis der aktuellen Produktionsraten nur noch für 15-20 Jahre reichen würden. Das Ministerium schließt nicht aus, in einigen Jahren sogar Seltene Erden importieren zu müssen. Dies würde das ohnehin schon extrem knappe Angebot am Weltmarkt weiter einengen und wäre wohl als Super-GAU für die Abnehmerländer zu bezeichnen. Diese Aussagen dürften aber eher in einem politischen Zusammenhang stehen.

usw. Seiten: 1 | 2 | 3 »

@ ein schönes WE

Grüsse JoJo

!

Dieser Beitrag wurde vom System automatisch gesperrt. Bei Fragen wenden Sie sich bitte an feedback@wallstreet-online.de!

Dieser Beitrag wurde vom System automatisch gesperrt. Bei Fragen wenden Sie sich bitte an feedback@wallstreet-online.deTrading Spotlight

Sehr schön hinsichtlich des Unterhaltungswerts fand' ich diesen FAZ Beitrag:

http://www.faz.net/s/Rub58BA8E456DE64F1890E34F4803239F4D/Doc…

Direktinvestments in Seltene Erden sind nicht nur mit Umständen verbunden, sondern auch mit hohen Kosten. Der Investor muss nicht nur An- und Verkauf sowie den Transport organisieren. Er braucht auch große Lagerräume. Und muss zudem die gesundheitsschädliche Wirkung mit in Betracht ziehen.

Schade, ich war gerade kurz davor mir 5 Tonnen Cer in der Speisekammer einzulagern... ...den Ford Transit hatte ich schon ausgeliehen und die Wegbeschreibung zur Baotou Mine hab ich hier gefunden.

...den Ford Transit hatte ich schon ausgeliehen und die Wegbeschreibung zur Baotou Mine hab ich hier gefunden.

http://www.bing.com/maps/?wip=2&v=2&style=r&rtp=~&&msnurl=ho…

Berlin-Baotou Strecke:8680.0 km, 103 Std. 53 Min.

...oder diese Stilblüte gefällt mir auch...

Fonds und Zertifikate für Seltene Erden hingegen sind derzeit noch rar, wie die Banken bestätigen.

..aber die Grafiken sind nun wirklich toll ausgesucht.

Ein schönes Wochenende schon mal!

http://www.faz.net/s/Rub58BA8E456DE64F1890E34F4803239F4D/Doc…

Direktinvestments in Seltene Erden sind nicht nur mit Umständen verbunden, sondern auch mit hohen Kosten. Der Investor muss nicht nur An- und Verkauf sowie den Transport organisieren. Er braucht auch große Lagerräume. Und muss zudem die gesundheitsschädliche Wirkung mit in Betracht ziehen.

Schade, ich war gerade kurz davor mir 5 Tonnen Cer in der Speisekammer einzulagern...

...den Ford Transit hatte ich schon ausgeliehen und die Wegbeschreibung zur Baotou Mine hab ich hier gefunden.

...den Ford Transit hatte ich schon ausgeliehen und die Wegbeschreibung zur Baotou Mine hab ich hier gefunden.http://www.bing.com/maps/?wip=2&v=2&style=r&rtp=~&&msnurl=ho…

Berlin-Baotou Strecke:8680.0 km, 103 Std. 53 Min.

...oder diese Stilblüte gefällt mir auch...

Fonds und Zertifikate für Seltene Erden hingegen sind derzeit noch rar, wie die Banken bestätigen.

..aber die Grafiken sind nun wirklich toll ausgesucht.

Ein schönes Wochenende schon mal!

Antwort auf Beitrag Nr.: 40.498.766 von slig am 11.11.10 09:37:10Aber klar doch, wird hier u.a. schon auf den ersten Seiten in diesm Thread behandelt.

Poste für dich nochmal einige Auszüge die ich hier schon im März 2008 eingestellt habe:

Weitere Standbeine sind die Phosphat Ressource und die IMHO gegenüber der REE Ressorurce noch höher zu bewertene Crown Polymetallic Ressource auf dem Mt Weld Feld.

Crown Polymetallic Resource

http://www.lynascorp.com/page.asp?category_id=2&page_id=5

Zusätzlich zu dieser Weltklasse-Seltene Erden Oxide (REO) Mine besitzt Lynas ganz in der Nähe eine umfangreiche polymetallischer Ressource innerhalb der "Crown Deposit" das Niob, Tantal, Zirkonium, Titan, und Seltene Erden einschließt.

Dazu erstellte Dr. Phillip Hellman von Hellman & Schofield Pty Ltd, Sydney, eine Studie, diese JORC-konforme Multi-Metall-geostatistische Ressource Schätzung , indizierte eine Inferred Ressources von 37,7 Millionen Tonnen.

Die Erz Zusammensetzung in Tabelle aufgeführt.(siehe Homepage von Lynas)

Die Mehrheit der Erz liegt zwischen 30m und 60m Tiefe und ist damit für den offenen Tagebau geeignet.

Die Scoping-Studie im Jahr 2005 stellt eine offene Schnitt-Mine und einen Prozess Route auf der Grundlage der bestehenden Technologie zum produzieren vor, eine Suite von Metall-Verbindungen und Produkten. Die starke wirtschaftliche und technische Ergebnisse der Scoping-Studie wurden als „sehr ermutigend“ eingestuft.

Weitere mineralogische Proben für die Beurteilung und die metallurgischen Tests wurden in diesem Jahr durchgeführt.

Eine externes Forschungsinstitut hat weitere Untersuchungen auf die mineralogische vorläufige Bewertung und Entwicklung der Prozess vom polymetallischem Erz durchgeführt um damit dieses Projekt weiterzuführen damit die Mitarbeiter von Lynas sich weiterhin zu 100% auf die Entwicklung vom Seltene Erden-Projekt konzentrieren können.

Der nächste Schritt zur Erschließung vom Polymetallic Projekt wird der Testbeginn der auf der Grundlage der vorläufigen Mineralogie und Prozessentwicklung sein.

Zu Niobium Niob:

Damit ist diese Mt. Weld möglicherweise der weltweit zweitgrößte Nb 2 O 5-Ressource (bezogen auf das Metall Niob) im Vergleich zu den Ressourcen der bestehenden kommerziellen Produzenten, dazu zählen:

· CBMM's Araxa in Brasilien, mit 460 Millionen Tonnen Einstufung von 2,5% Nb 2 O 5 liefert mehr als 80% des weltweiten Marktes Niob,

· Mineracao Catalao de Goias Ltd (Anglo American plc) in Brasilien in Höhe von rund 18 Millionen Tonnen zu einem Durchschnittskurs von 1,34% Nb 2 O 5,

· Niobec Inc's kanadisches Unternehmen mit 24 Millionen Tonnen auf 0,65% Nb 2 O 5

Zu Titanium Titan:

Titan-Metall-und Ti-ferroalloy Produkte werden in der Luft-und Raumfahrtindustrie, für spezielle Apparate und Energietechnik, chemische Verarbeitung und Sportgeräte, vor allem Gold-Clubs.

Zu Rare Earths and Scandium Seltene Erden und Scandium:

Das Mt. Weld Rare Metals Vorkommen enthält auch beträchtliche Anteile in hoher Qualitäten von Seltene Erden (HREE) die stark angereichert sind mit den wertvollen schweren Lanthaniden, die letztlich dazu beitragen könnten zur erheblichen Wertsteigerung. Ebenfalls vorhanden ist Scandium, wird für die hoher Festigkeit von Aluminiumlegierungen gebraucht.

Investor Presentation

http://www.lynascorp.com/page.asp?category_id=2&page_id=5

6 September 2007

Lynas Acquires New Rare Earths Resource in Malawi

http://www.lynascorp.com/content/upload/files/Announcements/…

http://translate.googleusercontent.com/translate_c?hl=de&ie=…

Link wird immer wieder aktualisiert:

http://treo.typepad.com/raremetalblog/lynas-corporation-ltd/…

Lynas Corporation Ltd.

...

...

übersetzt: http://translate.googleusercontent.com/translate_c?hl=de&ie=…

http://www.stocknessmonster.com/news-item?S=LYC&E=ASX&N=6048…

6 September 2010

Increase in Resource Estimate for Deposit with Elevated Heavy Rare Earths

Highlights

• The Rare Earths Mineral Resource at Mount Weld has been divided into two deposits

• The Mineral Resource estimate for the deposit with a higher distribution of Heavy Rare Earths has increased threefold to 7.62 million tonnes at a grade of 4.8% REO for a total of 366,000 tonnes REO, and has been renamed the Duncan Deposit

• The Central Lanthanide Deposit which includes the area of the current mine plan remains essentially unchanged

• The combined Rare Earths Mineral Resource estimate for Mount Weld increased to 17.49 million tonnes at 8.1% REO, giving a new Resource of 1.416 million tonnes of REO, a 19.4% increase in contained REO compared to the previous Resource estimate.

...

übersetzt: http://translate.google.de/translate?js=n&prev=_t&hl=de&ie=U…

http://stocknessmonster.com/news-item?S=LYC&E=ASX&N=605682

13 September 2010

Working Capital Facility – OCBC Bank (Malaysia) Berhad

Lynas Corporation Limited (ASX:LYC, OTC:LYSDY) is pleased to announce that the Lynas group of companies have accepted a letter of offer for the following working capital facilities from OCBC Bank (Malaysia) Berhad, which is equivalent to approximately A$30,000,000:

...

übersetzt: http://translate.google.de/translate?js=n&prev=_t&hl=de&ie=U…

http://www.lynascorp.com/page.asp?category_id=2&page_id=4

Grüsse JoJo

Poste für dich nochmal einige Auszüge die ich hier schon im März 2008 eingestellt habe:

Weitere Standbeine sind die Phosphat Ressource und die IMHO gegenüber der REE Ressorurce noch höher zu bewertene Crown Polymetallic Ressource auf dem Mt Weld Feld.

Crown Polymetallic Resource

http://www.lynascorp.com/page.asp?category_id=2&page_id=5

Zusätzlich zu dieser Weltklasse-Seltene Erden Oxide (REO) Mine besitzt Lynas ganz in der Nähe eine umfangreiche polymetallischer Ressource innerhalb der "Crown Deposit" das Niob, Tantal, Zirkonium, Titan, und Seltene Erden einschließt.

Dazu erstellte Dr. Phillip Hellman von Hellman & Schofield Pty Ltd, Sydney, eine Studie, diese JORC-konforme Multi-Metall-geostatistische Ressource Schätzung , indizierte eine Inferred Ressources von 37,7 Millionen Tonnen.

Die Erz Zusammensetzung in Tabelle aufgeführt.(siehe Homepage von Lynas)

Die Mehrheit der Erz liegt zwischen 30m und 60m Tiefe und ist damit für den offenen Tagebau geeignet.

Die Scoping-Studie im Jahr 2005 stellt eine offene Schnitt-Mine und einen Prozess Route auf der Grundlage der bestehenden Technologie zum produzieren vor, eine Suite von Metall-Verbindungen und Produkten. Die starke wirtschaftliche und technische Ergebnisse der Scoping-Studie wurden als „sehr ermutigend“ eingestuft.

Weitere mineralogische Proben für die Beurteilung und die metallurgischen Tests wurden in diesem Jahr durchgeführt.

Eine externes Forschungsinstitut hat weitere Untersuchungen auf die mineralogische vorläufige Bewertung und Entwicklung der Prozess vom polymetallischem Erz durchgeführt um damit dieses Projekt weiterzuführen damit die Mitarbeiter von Lynas sich weiterhin zu 100% auf die Entwicklung vom Seltene Erden-Projekt konzentrieren können.

Der nächste Schritt zur Erschließung vom Polymetallic Projekt wird der Testbeginn der auf der Grundlage der vorläufigen Mineralogie und Prozessentwicklung sein.

Zu Niobium Niob:

Damit ist diese Mt. Weld möglicherweise der weltweit zweitgrößte Nb 2 O 5-Ressource (bezogen auf das Metall Niob) im Vergleich zu den Ressourcen der bestehenden kommerziellen Produzenten, dazu zählen:

· CBMM's Araxa in Brasilien, mit 460 Millionen Tonnen Einstufung von 2,5% Nb 2 O 5 liefert mehr als 80% des weltweiten Marktes Niob,

· Mineracao Catalao de Goias Ltd (Anglo American plc) in Brasilien in Höhe von rund 18 Millionen Tonnen zu einem Durchschnittskurs von 1,34% Nb 2 O 5,

· Niobec Inc's kanadisches Unternehmen mit 24 Millionen Tonnen auf 0,65% Nb 2 O 5

Zu Titanium Titan:

Titan-Metall-und Ti-ferroalloy Produkte werden in der Luft-und Raumfahrtindustrie, für spezielle Apparate und Energietechnik, chemische Verarbeitung und Sportgeräte, vor allem Gold-Clubs.

Zu Rare Earths and Scandium Seltene Erden und Scandium:

Das Mt. Weld Rare Metals Vorkommen enthält auch beträchtliche Anteile in hoher Qualitäten von Seltene Erden (HREE) die stark angereichert sind mit den wertvollen schweren Lanthaniden, die letztlich dazu beitragen könnten zur erheblichen Wertsteigerung. Ebenfalls vorhanden ist Scandium, wird für die hoher Festigkeit von Aluminiumlegierungen gebraucht.

Investor Presentation

http://www.lynascorp.com/page.asp?category_id=2&page_id=5

6 September 2007

Lynas Acquires New Rare Earths Resource in Malawi

http://www.lynascorp.com/content/upload/files/Announcements/…

http://translate.googleusercontent.com/translate_c?hl=de&ie=…

Link wird immer wieder aktualisiert:

http://treo.typepad.com/raremetalblog/lynas-corporation-ltd/…

Lynas Corporation Ltd.

...

...

übersetzt: http://translate.googleusercontent.com/translate_c?hl=de&ie=…

http://www.stocknessmonster.com/news-item?S=LYC&E=ASX&N=6048…

6 September 2010

Increase in Resource Estimate for Deposit with Elevated Heavy Rare Earths

Highlights

• The Rare Earths Mineral Resource at Mount Weld has been divided into two deposits

• The Mineral Resource estimate for the deposit with a higher distribution of Heavy Rare Earths has increased threefold to 7.62 million tonnes at a grade of 4.8% REO for a total of 366,000 tonnes REO, and has been renamed the Duncan Deposit

• The Central Lanthanide Deposit which includes the area of the current mine plan remains essentially unchanged

• The combined Rare Earths Mineral Resource estimate for Mount Weld increased to 17.49 million tonnes at 8.1% REO, giving a new Resource of 1.416 million tonnes of REO, a 19.4% increase in contained REO compared to the previous Resource estimate.

...

übersetzt: http://translate.google.de/translate?js=n&prev=_t&hl=de&ie=U…

http://stocknessmonster.com/news-item?S=LYC&E=ASX&N=605682

13 September 2010

Working Capital Facility – OCBC Bank (Malaysia) Berhad

Lynas Corporation Limited (ASX:LYC, OTC:LYSDY) is pleased to announce that the Lynas group of companies have accepted a letter of offer for the following working capital facilities from OCBC Bank (Malaysia) Berhad, which is equivalent to approximately A$30,000,000:

...

übersetzt: http://translate.google.de/translate?js=n&prev=_t&hl=de&ie=U…

http://www.lynascorp.com/page.asp?category_id=2&page_id=4

Grüsse JoJo

Ein Musterbeispiel für einen schlecht recherchierten Artikel zum Thema voller Wiedersprüche und falscher bzw. unvollständiger Annahmen und Angaben wie man sie in letzter Zeit immer häufiger lesen muss.

Grüsse JoJo

http://www.fondsdiscount.de/nachrichten/artikel/2779/maerkte…

Rohstofffirmen | 02.11.2010 07:28:02

Die schwere Last der hohen Kurse

Die Preise von Seltenen Erden gehen durch die Decke. Das gilt auch für die Aktienkurse der Rohstofffirmen. Anleger sollten sehr vorsichtig agieren.

Eigentlich hätte der Molycorp-Chef Mark Smith Grund zum Feiern. Der Aktienkurs seines Unternehmens hat sich seit dem Börsengang im Sommer mehr als verdoppelt. Doch der Rummel stimmt Smith bedenklich. Der Hype um Seltene Erden, die für Hightechprodukte wie Hybridfahrzeuge, Mobiltelefone oder Katalysatoren gebraucht werden, könne zu einer Blase führen, so Smith in einem Interview mit dem US-Fernsehsender CNBC.

„Die Zeichen für eine Überhitzung nehmen langsam zu“, bestätigt auch Eckart Keil, Rohstoffexperte und Geschäftsführer von Premium Investments. Die Marktkapitalisierung der Branche wuchs in diesem Jahr um mehr als 300 Prozent von zwei auf über acht Milliarden US-Dollar. Zum Vergleich: Die jährliche Produktion Seltener Erden ist knapp zwei Milliarden Dollar wert. Der Preis für die 17 Elemente, die zu dieser Gruppe gezählt werden, stieg in den vergangenen drei Monaten um etwa 200 Prozent. Die Metalloxide mit exotischen Namen wie Lanthan, Neodym oder Yttrium werden für Hightechprodukte wie Elektro- und Hybridantriebe, Windräder oder Computerteile gebraucht.

Im Fokus stehen sie, seit China offenbar keine Seltenen Erden mehr nach Japan ausführt. „Über 95 Prozent der Seltenen Erden werden zurzeit in China gewonnen“, erklärt Maren Liedtke von der Bundesanstalt für Geowissenschaften und Rohstoffe (BGR) die Abhängigkeit von chinesischen Ausfuhren. Doch ob die deutsche oder die japanische Industrie, wie oft behauptet, unter Rohstoffknappheit leiden wird, ist keineswegs ausgemacht.

„Die Herausforderung für Anleger ist, sich aus den Angebots- und Nachfrageschätzungen eine klare Meinung zu bilden, ob es einen Angebotsüberschuss oder ein Defizit

geben wird“, sagt Charles Fawcett, Minenanalyst der Earth Resource Investment Group in London. Denn die Statistiken bieten kein einheitliches Bild. So geht der US-Kongress auf Datengrundlage von Molycorp davon aus, dass 2014 global 40 000 Tonnen an Seltenen Erden fehlen werden. Die Industrial Mineral Company of Australia schätzt das Defizit auf nur 1500 Tonnen weltweit. Klar ist dagegen, dass die Nachfrage in den vergangenen Jahren deutlich gestiegen ist: 2004 wurden noch 90 000 Tonnen in Batterien, Mag-neten und Katalysatoren verarbeitet. 2010 waren es bereits über 120 000 Tonnen. Und bis 2014 könnten mehr als 200 000 Tonnen in Endprodukten wie iPhones, satellitengestützten Kommunikationssystemen oder Hybridantrieben ihre Verwendung finden – mehr als doppelt so viel wie im Jahr 2004. Voraussetzung dafür ist aber, dass sich erwartete Nachfragetreiber wie der Markt für Fahrzeuge mit alternativen Antrieben so gut entwickeln werden, wie erwartet.

Aber nicht nur die Nachfrage, auch die chinesische Wirtschaftspolitik beeinflusst die Preisentwicklung. „China will nicht mehr nur Rohstoffexporteur sein, sondern zunehmend die gesamte Wertschöpfungskette abdecken“, erklärt Rohstoffexperte Keil die aktuelle Politik in Peking. Deshalb reduziert China die Rohstoffausfuhren und verarbeitet mehr im eigenen Land. „Zum anderen verwendet China die Rohstoffexporte aber auch als wirtschaftliche und politische Waffe.“ Doch das könnte sich wegen der hohen Preise schnell ändern. „Ein Politikwechsel in China könnte das Angebot erhöhen, sodass die globale Nachfrage von chinesischen Herstellern gedeckt wird. Außerdem könnten alternative Technologien die Abhängigkeit von Seltenen Erden mindern.“ Dann könnten sich die Ängste vor Versorgungsengpässen als Hysterie entpuppen.

In den USA will man sich darauf aber nicht verlassen. Besonders, da Seltene Erden auch für die Rüstungsproduktion relevant sind. So plant man, sich mit eigenen Förder- und Produktionsstätten von den chinesischen Lieferanten unabhängiger zu machen. Denn Seltene Erden gibt es häufiger, als ihr Name nahelegt. „Sie sind geologisch gesehen keineswegs selten und die bekannten Vorräte sind noch auf lange Sicht ausreichend“, so Maren Liedtke von der BGR. Von den rund 100 Millionen Tonnen an bisher entdeckten Reserven liegen etwa 63 Prozent außerhalb Chinas, davon 13 Prozent in den USA. Dort befand sich bis in die 80er-Jahre die größte Fördereinrichtung der Welt: die Mine am Mountain Pass in Kalifornien. Erst in den 90ern verlagerte sich der Abbau wegen geringerer Kosten und laxerer Umwelt- und Sicherheitsauflagen nach China. Molycorp trifft nun bereits Vorbereitungen, um die Produktion am Mountain Pass 2012 wieder aufzunehmen. In Australien erschließt der Minenkonzern Lynas im Moment eine Produktionsstätte am Mount Weld. Der australische Konkurrent Arafura hat eine Pilotanlage in Nolans eingerichtet, der Betrieb soll 2014 starten.

Jede dieser Minen soll jährlich 20 000 Tonnen Seltene Erden fördern. Doch noch wurde nichts aus dem Boden geholt. Trotzdem haben sich die Aktienkurse der Unternehmen seit Mitte des Jahres mindestens verdoppelt. Und auch Firmen, die zwar nach Vorkommen suchen, allerdings noch weit von der Förderung entfernt sind, sind an den Börsen gefragt. Die Aktien einiger kleiner Explorer haben sich in den vergangenen Monaten sogar vervierfacht. Die Fantasie der Anleger, die durch Medienberichte, exotische Namen und Zukunftstechnologien beflügelt wurde, hat die Kurse vieler Seltener-Erden-Konzerne schon sehr weit getragen. Sollte sich das Angebot von Lanthan oder Yttrium künftig besser darstellen als momentan erwartet, wird sich schnell Enttäuschung bei den Anlegern breitmachen. „Sinken die Preise, könnten die Aktienkurse einiger kleiner Unternehmen unter Druck geraten, die bisher über keine Ressourcen verfügen oder die hohe Rohstoffpreise brauchen, um wirtschaftlich zu sein“, glaubt Charles Fawcett. „Nicht jedes Unternehmen wird Geld verdienen. Und damit auch nicht jeder Anleger“, bestätigt auch Rohstoffexperte Keil.Ähnlich scheint es auch Molycorp-Chef Mark Smith zu sehen. Er legt seinen Konkurrenten nahe, ihren Geschäftsplan nicht auf Grundlage der aktuell hohen Preise für Seltene Erden aufzustellen. Vielleicht ein Rat, den auch Anleger berücksichtigen sollten.

Quelle: EamS

Grüsse JoJo

http://www.fondsdiscount.de/nachrichten/artikel/2779/maerkte…

Rohstofffirmen | 02.11.2010 07:28:02

Die schwere Last der hohen Kurse

Die Preise von Seltenen Erden gehen durch die Decke. Das gilt auch für die Aktienkurse der Rohstofffirmen. Anleger sollten sehr vorsichtig agieren.

Eigentlich hätte der Molycorp-Chef Mark Smith Grund zum Feiern. Der Aktienkurs seines Unternehmens hat sich seit dem Börsengang im Sommer mehr als verdoppelt. Doch der Rummel stimmt Smith bedenklich. Der Hype um Seltene Erden, die für Hightechprodukte wie Hybridfahrzeuge, Mobiltelefone oder Katalysatoren gebraucht werden, könne zu einer Blase führen, so Smith in einem Interview mit dem US-Fernsehsender CNBC.

„Die Zeichen für eine Überhitzung nehmen langsam zu“, bestätigt auch Eckart Keil, Rohstoffexperte und Geschäftsführer von Premium Investments. Die Marktkapitalisierung der Branche wuchs in diesem Jahr um mehr als 300 Prozent von zwei auf über acht Milliarden US-Dollar. Zum Vergleich: Die jährliche Produktion Seltener Erden ist knapp zwei Milliarden Dollar wert. Der Preis für die 17 Elemente, die zu dieser Gruppe gezählt werden, stieg in den vergangenen drei Monaten um etwa 200 Prozent. Die Metalloxide mit exotischen Namen wie Lanthan, Neodym oder Yttrium werden für Hightechprodukte wie Elektro- und Hybridantriebe, Windräder oder Computerteile gebraucht.

Im Fokus stehen sie, seit China offenbar keine Seltenen Erden mehr nach Japan ausführt. „Über 95 Prozent der Seltenen Erden werden zurzeit in China gewonnen“, erklärt Maren Liedtke von der Bundesanstalt für Geowissenschaften und Rohstoffe (BGR) die Abhängigkeit von chinesischen Ausfuhren. Doch ob die deutsche oder die japanische Industrie, wie oft behauptet, unter Rohstoffknappheit leiden wird, ist keineswegs ausgemacht.

„Die Herausforderung für Anleger ist, sich aus den Angebots- und Nachfrageschätzungen eine klare Meinung zu bilden, ob es einen Angebotsüberschuss oder ein Defizit

geben wird“, sagt Charles Fawcett, Minenanalyst der Earth Resource Investment Group in London. Denn die Statistiken bieten kein einheitliches Bild. So geht der US-Kongress auf Datengrundlage von Molycorp davon aus, dass 2014 global 40 000 Tonnen an Seltenen Erden fehlen werden. Die Industrial Mineral Company of Australia schätzt das Defizit auf nur 1500 Tonnen weltweit. Klar ist dagegen, dass die Nachfrage in den vergangenen Jahren deutlich gestiegen ist: 2004 wurden noch 90 000 Tonnen in Batterien, Mag-neten und Katalysatoren verarbeitet. 2010 waren es bereits über 120 000 Tonnen. Und bis 2014 könnten mehr als 200 000 Tonnen in Endprodukten wie iPhones, satellitengestützten Kommunikationssystemen oder Hybridantrieben ihre Verwendung finden – mehr als doppelt so viel wie im Jahr 2004. Voraussetzung dafür ist aber, dass sich erwartete Nachfragetreiber wie der Markt für Fahrzeuge mit alternativen Antrieben so gut entwickeln werden, wie erwartet.

Aber nicht nur die Nachfrage, auch die chinesische Wirtschaftspolitik beeinflusst die Preisentwicklung. „China will nicht mehr nur Rohstoffexporteur sein, sondern zunehmend die gesamte Wertschöpfungskette abdecken“, erklärt Rohstoffexperte Keil die aktuelle Politik in Peking. Deshalb reduziert China die Rohstoffausfuhren und verarbeitet mehr im eigenen Land. „Zum anderen verwendet China die Rohstoffexporte aber auch als wirtschaftliche und politische Waffe.“ Doch das könnte sich wegen der hohen Preise schnell ändern. „Ein Politikwechsel in China könnte das Angebot erhöhen, sodass die globale Nachfrage von chinesischen Herstellern gedeckt wird. Außerdem könnten alternative Technologien die Abhängigkeit von Seltenen Erden mindern.“ Dann könnten sich die Ängste vor Versorgungsengpässen als Hysterie entpuppen.

In den USA will man sich darauf aber nicht verlassen. Besonders, da Seltene Erden auch für die Rüstungsproduktion relevant sind. So plant man, sich mit eigenen Förder- und Produktionsstätten von den chinesischen Lieferanten unabhängiger zu machen. Denn Seltene Erden gibt es häufiger, als ihr Name nahelegt. „Sie sind geologisch gesehen keineswegs selten und die bekannten Vorräte sind noch auf lange Sicht ausreichend“, so Maren Liedtke von der BGR. Von den rund 100 Millionen Tonnen an bisher entdeckten Reserven liegen etwa 63 Prozent außerhalb Chinas, davon 13 Prozent in den USA. Dort befand sich bis in die 80er-Jahre die größte Fördereinrichtung der Welt: die Mine am Mountain Pass in Kalifornien. Erst in den 90ern verlagerte sich der Abbau wegen geringerer Kosten und laxerer Umwelt- und Sicherheitsauflagen nach China. Molycorp trifft nun bereits Vorbereitungen, um die Produktion am Mountain Pass 2012 wieder aufzunehmen. In Australien erschließt der Minenkonzern Lynas im Moment eine Produktionsstätte am Mount Weld. Der australische Konkurrent Arafura hat eine Pilotanlage in Nolans eingerichtet, der Betrieb soll 2014 starten.

Jede dieser Minen soll jährlich 20 000 Tonnen Seltene Erden fördern. Doch noch wurde nichts aus dem Boden geholt. Trotzdem haben sich die Aktienkurse der Unternehmen seit Mitte des Jahres mindestens verdoppelt. Und auch Firmen, die zwar nach Vorkommen suchen, allerdings noch weit von der Förderung entfernt sind, sind an den Börsen gefragt. Die Aktien einiger kleiner Explorer haben sich in den vergangenen Monaten sogar vervierfacht. Die Fantasie der Anleger, die durch Medienberichte, exotische Namen und Zukunftstechnologien beflügelt wurde, hat die Kurse vieler Seltener-Erden-Konzerne schon sehr weit getragen. Sollte sich das Angebot von Lanthan oder Yttrium künftig besser darstellen als momentan erwartet, wird sich schnell Enttäuschung bei den Anlegern breitmachen. „Sinken die Preise, könnten die Aktienkurse einiger kleiner Unternehmen unter Druck geraten, die bisher über keine Ressourcen verfügen oder die hohe Rohstoffpreise brauchen, um wirtschaftlich zu sein“, glaubt Charles Fawcett. „Nicht jedes Unternehmen wird Geld verdienen. Und damit auch nicht jeder Anleger“, bestätigt auch Rohstoffexperte Keil.Ähnlich scheint es auch Molycorp-Chef Mark Smith zu sehen. Er legt seinen Konkurrenten nahe, ihren Geschäftsplan nicht auf Grundlage der aktuell hohen Preise für Seltene Erden aufzustellen. Vielleicht ein Rat, den auch Anleger berücksichtigen sollten.

Quelle: EamS

Antwort auf Beitrag Nr.: 40.498.364 von JoJo49 am 11.11.10 08:53:52Guten Morgen JoJo!

Am Ende des von Dir angebrachten Artikels steht zum Theme HREE folgendes:

He sees one or two deals happening from within the industry, with Molycorp and Lynas circling the juniors looking for the best heavy rare earth asset. Once those deals have happened, there won’t be any suitors left

Ist damit jetzt beim Lynas ausdrücklich nur die NTU-Beteiligung gemeint

oder gibt es auch noch was anderes in Australien worauf wir "scharf" sind?

Am Ende des von Dir angebrachten Artikels steht zum Theme HREE folgendes:

He sees one or two deals happening from within the industry, with Molycorp and Lynas circling the juniors looking for the best heavy rare earth asset. Once those deals have happened, there won’t be any suitors left

Ist damit jetzt beim Lynas ausdrücklich nur die NTU-Beteiligung gemeint

oder gibt es auch noch was anderes in Australien worauf wir "scharf" sind?

Ist zwar ein sehr nordamerikanischlastiger Artikel aber IMHO sehr informativ in Bezug auf die Zahlenangaben von Verbräuchen/Bedarf für die einzelnen Produkte sowie der sich dabei ergebene zukünftig weiterhin steigende Bedarf für die westlichen Industrienationen, wobei ich die Annahme/Befürchtung das China die Exportbeschränkungen aufheben bzw. lockern könnte für mich nicht nachvollziehbar ist, weil z.B. auch wirtschaftliche Ressourcen/Lagerstätte der Seltene Erden/Metalle endlich sind und für die zukünftige weltweite wirtschaftliche Entwicklung unentbehrlich sind.

Grüsse JoJo

http://www.montrealgazette.com/technology/Abandoned+Canadian…

Abandoned Canadian mine a lesson for rare earth investors

By Julie Gordon, Reuters November 9, 2010

TORONTO – Rows of moss-covered concrete bricks block the opening of the Monmouth rare earth mine in Canada, keeping curious hikers from entering the long-abandoned shaft.

From the early 1940s to the late 1970s, a now-defunct company called Amalgamated Rare Earth Mines explored the site for uranium and a then-obscure cluster of 17 elements known as rare earths.

The mine, 340 kilometres north of Toronto, never went into commercial production and by the early 1980s the company abandoned the project, scared off by an aggressive Chinese campaign to corner the rare earth market.

Two decades after the Monmouth mine shut, China accounts for 97 per cent of the world’s rare earth ore production, empowering Beijing in a way that was unimaginable in the 1980s.

Rare earths have become crucial components for some of the world’s consumer and industrial icons: the Toyota Prius, General Electric wind turbines, the Apple iPhone and hundreds of other devices.

Until recently, the global dependency on China for rare earths was a well-kept secret. But word started to spread fast after Beijing cut export quotas by 70 per cent for the second half of 2010, sending prices of some oxides – the purified form of rare earth elements – up as much as 850 per cent. The need for alternative supplies from outside China suddenly became obvious.

Dozens of companies all around the world are now aiming to fill the coming void in supplies, and investors have poured billions of dollars into their projects.

Rare Element Resources, which owns a promising rare earth deposit in Wyoming, is a good example. Its shares have risen almost 400 per cent in less than 90 days, and over 2,000 per cent since April 2009. In that time, the 495,000 shares belonging to one director have jumped in value to more than $5.4 million from $247,500.

But the bricks that seal the entrance to Amalgamated’s long-abandoned Canadian mine should serve as a cautionary tale to rare earth investors.

Current Chinese policies, which are driving up prices of oxides as well as company share prices, could shift, leading to a big industry shakeout. Holdings worth millions of dollars could turn worthless overnight, leaving burned investors with a painful sense of déjà vu.

“There’s a dot-com aspect to a few of these mines,” said Christopher Ecclestone, a strategist with Hallgarten and Co. in New York. “These stocks are going up because the products are going up in price, but none of these companies have any products to sell.”

The common refrain in interviews with industry executives, analysts and mineral experts is that only about a half-dozen non-Chinese producers will emerge from the rubble.

“Some of these stocks will be found to be nothing more than a pile of dirt,” Ecclestone said. “And it’s not because the product isn’t there; it’s just going to be that they’re never going to be developed.”

While the odds of emerging as a successful producer are long, the winners are likely to be those with the right mix of specific rare earths in their deposits, the downstream processing know-how and the contacts to make it in a demanding industry.

With literally hundreds of exploration companies and junior miners to chose from, the challenge for investors is separating the real players from the pretenders playing the rare earth buzz to make a quick profit on the stock market.

The speculative nature of rare earth stocks, coupled with the intense investor demand to own them, has prompted fund manager Van Eck Global to launch an exchange-traded fund focused on rare earths and minor metals.

But even the buffer of trading a group of rare earth miners instead of just one doesn’t guarantee a safe ride for investors.

“Everybody’s standing up, waving the flag, and shrieking it’s rare earths, because that pushes the valuation up,” said Byron Capital Market analyst Jon Hykawy. “When the Chinese change their quota system, we will see the bubble rupture.”

That bubble, which has seen the average share price of the top juniors in the sector rise 145 per cent in six months, is one of the main risks facing investors.

Even BlackRock, the world’s largest money manager, says the “jury is still out” when it comes to the long-term investment potential for rare earth mines outside China.

“The ability to bring on production quickly in the higher-price environment means that the longer-term sustainability of those prices are questionable,” Catherine Raw, a fund manager in BlackRock’s natural-resources division, told Reuters.

Regardless of the red flags, analysts and industry observers agree more suppliers are needed, no matter what policy China pursues.

“Whether the Chinese are restricting supply or not, there’s going to be a need for new deposits,” Ecclestone said. “The Chinese do not have a boundless supply of rare earths.”

If new supplies of rare earths do not come online within the next 10 years, a global shortage would likely develop with far-reaching consequences: wind turbines will not be built, electric vehicle production will grind to a halt, and mobile phones would have to triple in size.

The issue even carries national security implications because of the rare earth content in many advanced military weapons, not to mention the economic threat that shortages would present. The problem is, getting new sources of supply into production is not that easy.

Rare earths, despite their name, are not that rare. In Canada alone, there are at least 26 publicly traded companies that have rare earth projects in some stage of exploration.

Not all rare earth deposits are created equal, and good quality, economically feasible deposits are scarce – a risk factor that some investors may have overlooked.

“People just don’t fully understand what’s involved in going from having a few holes in the ground to actually being a producer,” said industry expert Dudley Kingsnorth from a rare earth industry event in Perth, Australia. “You’ve got to build it, and you’ve got to start it up, and the expertise outside China to do that is limited.”

Every rare earth mine contains all 17 elements locked into a mineral that needs to be broken down, or cracked, usually using acid. The cracked rare earth concentrate then needs to be processed again, to separate the individual rare earths, which are then purified into oxides.

With the current quota system, China does not distinguish between the individual rare earth oxides but limits the total tonnage of exports across the board. That has led to Chinese companies exporting as much as possible of the high-value heavy rare earths like dysprosium, instead of low-value light rare earths like cerium.

Because no one is exporting cerium, the prices for the oxide, which is used in catalysts and glass polishing, has jumped to about $53 a kilogram this month from $4 a kg in 2008, according to Asian Metal, a firm that tracks industry prices.

“The price fluctuations recently have been the lights,” said Asian Metal analyst Phil Arnheim. “I think, as long as we have the export quota system in place, there’s going to be a premium on those materials.”

With prices for light rare earths soaring, projects like Molycorp Inc’s Mountain Pass mine in California are looking very attractive to investors.

But most analysts believe China will eventually change its quota system to restrict the rare earths individually. Because China has an abundance of light rare earths available through the Bayan Obo project in Mongolia, changing the quota system would likely trigger a sudden flood of cerium and lanthanum on to the market.

That’s a big risk for Molycorp. If the price of lanthanum oxide were to drop back down to around $7 per kg, the value of a five-year contract the company recently announced with W.R. Grace would tumble from more than $750 million to about $100 million.

Molycorp Chief Executive Mark Smith, speaking at an industry event in Washington, D.C., said he is confident the price at which his company could sell the oxides will stay up across the board, based on supply and demand.

“The entire world outside of China needs about 50,000 tonnes of product a year. … All that China is exporting right now is about 30,000,” he said, adding the oxide prices “are real and we think that they are very sustainable as we move forward.”

While the long-term price of the light rare earths remains open for debate, it is a given in the industry that quotas will continue to tighten the supply of heavy rare earths like terbium and dysprosium, sending prices soaring.

Dysprosium oxide, used in hybrid vehicles, lasers and nuclear reactors, is already selling for $284 a kg and that is projected to rise to over $400 in the next couple of years, according to Asian Metals.

The already tight supply will only get tighter, as analysts anticipate that the heavy rare earths mined in southern China’s ionic clays could run out within 15 to 20 years, which could lead to even higher oxide prices.

While this is good news for miners with deposits rich in heavy rare earths, having valuable minerals in the ground doesn’t necessarily mean big benefits for investors.

Even if the non-Chinese mines were to go into production today, the miners would not receive hundreds of dollars per kilogram of material they produce.

“Eighty to 90 percent of the value is in the processing and that is the great secret of the rare earth space,” Ecclestone said. “Basically, when you pull it out of the ground, it’s not worth a damn.”

It is the processors, who separate the rare earth concentrate into refined oxides, and build relationships with end users, who are making all the money.

A life-size terracotta Warrior watches over the vast lobby at the Neo Material Technologies head office in Toronto. That’s where chief executive Constantine Karayannopoulos has spent the last 17 years building up a rare earth empire.

His company buys rare earth concentrate and separates it into individual oxides in China. Then it transforms those oxides into highly specialized rare earth alloys and magnetic powders, using facilities around the world.

Neo Material is one of just a handful of companies that work closely with technology companies like Samsung and Canon to make rare earth products specific to their needs. The qualification process for working with a new client usually takes one to three years, Karayannopoulos said.

“It’s not as simple as digging it out of the ground and putting it on a truck and out it goes,” Karayannopoulos said. “The basis of what we do is our ability to separate rare earth elements from one another and then to add a lot of value using material technology skills.”

Taking rare earths from minerals in the ground to a separated oxide to a powerful magnet used to rotate a wind turbine is a long and complicated process. To get terbium oxide, worth about $615 a kg, it takes over 30 days of processing.

“I think the markets are completely unaware of what it takes not only to bring a rare earth mine into production,” Karayannopoulos said, “but also to achieve levels of production, and quality of production, that will allow you to sell your products to people who are willing to pay for them.”

In the second quarter of 2010, Neo Material sold just over 3,100 tonnes of separated rare earth oxides, rare earth compounds and magnetic powders. The company posted a quarterly profit of $16 million on revenue of $79.2 million.

Revenue for the 12 months to the end of the second quarter was $261.2 million on 11,719 tonnes of high-value rare earth product and magnetic powders – that is about $22.29 per kg for highly processed rare earth products, which usually sell at a 7-per-cent premium over concentrate.

Contrast that to junior miner Avalon Rare Metal Inc., which plans to sell unprocessed rare earth concentrate for $21.94 a kg, according to its prefeasibility report.

Rare earth concentrate sells for about $4 a kg in China, and while analysts estimate it could be worth between $10 and $20 in the United States or Europe, there are currently no facilities outside China to process it.

Neo Material is investigating building a separation plant in Latin America, Karayannopoulos said, adding his company would look to non-Chinese sources of concentrate to supply it.

“Ultimately, it is in the best interest of our company to be able to get raw materials from other folks, not just our Chinese suppliers,” he said. “So, to us, this global diversification of the supply chain is good.”

In 2008, global demand for rare earths was about 123,000 tonnes. By 2015, demand is forecast to be about 200,000 tonnes a year. This expected growth, coupled with the recent export cuts from China, has end users of rare earths scrambling for supplies, according to Jim Engdahl, CEO of Canada’s Great Western Minerals Group Ltd.

Clients “are exceptionally anxious – I guess the word could be just about in panic mode,” he said. “We’re getting calls daily from non-clients who want product from us.”

Great Western buys rare earth oxides from China and sells rare earth-based metals and alloys to major magnet manufacturers around the world.

The Saskatoon, Saskatchewan-based company also owns numerous rare earth properties in Canada, and is developing the Steenkampskraal mine in South Africa.

It plans to double production of rare earth products at its processing facility in Britain by 2013, when Steenkampskraal is projected to come online.

That expansion will start to relieve some of the tension in the multibillion-dollar industries that rare earths support, like the permanent magnets used in electric cars.

“Now we’re probably talking about $100 billion worth of products built off the back of the capabilities and properties of these rare earths,” Hykawy said.

He estimates the motor in the average Prius hybrid uses about 193 grams, or about 7 ounces, of neodymium and 24 grams of dysprosium, while the fully electric Nissan Leaf uses about 421 grams of neodymium and 56 grams of dysprosium.

“We believe that the electric vehicle is going to be a dominant form of transportation in decades to come,” Byron Capital’s Hykawy said, adding demand for the magnetic rare earths is set to jump almost 800 per cent by 2015.

Even with new mines coming online within the next five years, analysts are forecasting a shortage of heavy rare earths terbium and dysprosium by 2015, and a very tight supply of light rare earths neodymium and praseodymium.

The impending shortage has Bart Gordon, chairman of the U.S. House of Representatives Committee on Science and Technology, and other politicians calling for the U.S. government to fast-track domestic rare earth production.

Since rare earths are used in many U.S. military applications, from the tiny motors in guided missiles to night-vision goggles and lasers, Gordon calls China’s dominance of the industry “a real problem.”

Legislation has been introduced in both the Senate and the House to increase investment in, and boost the production of, rare earths in the United States, a move that has sent valuations surging for miners with U.S. projects.

Over the past three months, Molycorp has risen over 200 per cent to a high of $40.90 a share. It has a market cap of almost $3 billion, despite operating at a loss since launching in June 2008.

Using consensus analyst estimates, Molycorp is currently trading at 70 times above its expected 2010 revenue of $31.9 million. By comparison, a composite group of mining companies currently trades at an average of 2.5 times above expected 2010 revenue.

While the numbers are shocking, Neo Material’s Karayannopoulos sees Molycorp in a different class from the hundreds of junior miners who dot the landscape. His company has signed an agreement with the Colorado-based giant to buy rare earth concentrates once its massive California mine comes online.

“If Molycorp gets up to their design … they’ll be producing 40,000 tonnes of light rare earths at Mountain Pass,” Karayannopoulos said. “At a 40,000 tonne output, they could be producing 1,000 tonnes plus or minus of heavy rare earths.”

“It could be enough to supply the United States, which is not a big buyer of heavy rare earths.

China is home to only about one-third to one-half of global rare earth reserves, but it produces 97 per cent of the world’s supply.

“Over time, the percentage could shrink to less than 50 per cent,” said Michael Komesaroff, an analyst with Australian-based Urandaline Investments, pointing to the new mines coming online outside of China.

The first project out of the gate is likely to be the Mount Weld mine operated by Australia’s Lynas. It is set to start producing up to 22,000 tonnes of rare earths annually by the end of 2011.

Like Molycorp’s Mountain Pass, Mount Weld is a high-grade, light rare earth project. And like Molycorp, Lynas has a huge market cap, about $2.4 billion, despite not having any revenue at all.

While basic economics suggest both companies are overvalued, Byron’s Hykawy is maintaining a “speculative buy” rating on the stocks for now.

“It’s a freight train. I mean, people are investing in it right now who don’t know mining from a hole in the ground,” he said. “Do you want to jump in front of that speeding train?”

The big risk going forward is that if China releases its quotas for 2011 and removes restrictions on the sale of cerium and lanthanum – a scenario that Hykawy sees as a virtual certainty – “the light deposits like Molycorp and Lynas are going to be impacted.”

The other big concern is that neither Lynas nor Molycorp has substantial deposits of terbium and dysprosium, two of the heavy rare earths that are in high demand. This has created a supply hole that many of the exploration companies are focusing on filling.

“A lot of these Canadian companies are focusing entirely on heavy rare earths,” said Asian Metal’s Arnheim, who manages the Beijing-based company’s Pittsburgh bureau. “I think that makes sense.”

To address the growing market for heavies, Neo Material is moving forward on its Pitinga project in Brazil, which will recover heavy rare earths from the tailings of a tin mine in the Amazon basin.

The project, with Brazilian miner Mineracao Taboca, will cost about $100 million to bring to market. Mitsubishi Corp. is a partner in the development of the project.

Great Western’s Steenkampskraal mine, which is projected to come online in early 2013, will cost just $30 million, including the construction of a separation facility in South Africa.

That compares with the $729 million Avalon needs to bring its massive Nechalacho mine into production in Northern Canada.

Nechalacho, like Quest Rare Minerals Ltd’s Strange Lake project in northern Quebec, is a heavy rare earth deposit with a higher than normal concentration of dysprosium and terbium.

The implied value of a heavy rare earth deposit has boosted Avalon’s market cap to $350 million and Quest’s market cap up to almost $250 million.

But both projects are located in remote regions of Canada, with no infrastructure in place. The deposits also are very low grade and locked in syenite, an unproved mineral for rare earth extraction.

Analysts say the price tag of developing such a project is too steep for a junior miner, suggesting the only way projects like Nechalacho or Strange Lake will make it to market is if a major end user like Toyota Motor Corp. were to buy out the company and develop the mine at a loss.

Ecclestone doesn’t see that happening.

“We have to brush away a delusion here,” Ecclestone said. “Most of these companies think that they’re going to get taken over, but most of them won’t be.”

He sees one or two deals happening from within the industry, with Molycorp and Lynas circling the juniors looking for the best heavy rare earth asset. Once those deals have happened, there won’t be any suitors left.

As for the rest, just like Amalgamated and its Monmouth Mine back in the 1980s, “the dance may be over.”

And once the dust settles, many of these “promising” rare earth properties will end up being nothing more than a moss-covered reminder of the promise of the next mining gold rush.

© Copyright (c) The Montreal Gazette

übersetzt: http://translate.googleusercontent.com/translate_c?hl=de&ie=…

Grüsse JoJo

http://www.montrealgazette.com/technology/Abandoned+Canadian…

Abandoned Canadian mine a lesson for rare earth investors

By Julie Gordon, Reuters November 9, 2010

TORONTO – Rows of moss-covered concrete bricks block the opening of the Monmouth rare earth mine in Canada, keeping curious hikers from entering the long-abandoned shaft.

From the early 1940s to the late 1970s, a now-defunct company called Amalgamated Rare Earth Mines explored the site for uranium and a then-obscure cluster of 17 elements known as rare earths.

The mine, 340 kilometres north of Toronto, never went into commercial production and by the early 1980s the company abandoned the project, scared off by an aggressive Chinese campaign to corner the rare earth market.

Two decades after the Monmouth mine shut, China accounts for 97 per cent of the world’s rare earth ore production, empowering Beijing in a way that was unimaginable in the 1980s.

Rare earths have become crucial components for some of the world’s consumer and industrial icons: the Toyota Prius, General Electric wind turbines, the Apple iPhone and hundreds of other devices.

Until recently, the global dependency on China for rare earths was a well-kept secret. But word started to spread fast after Beijing cut export quotas by 70 per cent for the second half of 2010, sending prices of some oxides – the purified form of rare earth elements – up as much as 850 per cent. The need for alternative supplies from outside China suddenly became obvious.

Dozens of companies all around the world are now aiming to fill the coming void in supplies, and investors have poured billions of dollars into their projects.

Rare Element Resources, which owns a promising rare earth deposit in Wyoming, is a good example. Its shares have risen almost 400 per cent in less than 90 days, and over 2,000 per cent since April 2009. In that time, the 495,000 shares belonging to one director have jumped in value to more than $5.4 million from $247,500.

But the bricks that seal the entrance to Amalgamated’s long-abandoned Canadian mine should serve as a cautionary tale to rare earth investors.

Current Chinese policies, which are driving up prices of oxides as well as company share prices, could shift, leading to a big industry shakeout. Holdings worth millions of dollars could turn worthless overnight, leaving burned investors with a painful sense of déjà vu.

“There’s a dot-com aspect to a few of these mines,” said Christopher Ecclestone, a strategist with Hallgarten and Co. in New York. “These stocks are going up because the products are going up in price, but none of these companies have any products to sell.”

The common refrain in interviews with industry executives, analysts and mineral experts is that only about a half-dozen non-Chinese producers will emerge from the rubble.

“Some of these stocks will be found to be nothing more than a pile of dirt,” Ecclestone said. “And it’s not because the product isn’t there; it’s just going to be that they’re never going to be developed.”

While the odds of emerging as a successful producer are long, the winners are likely to be those with the right mix of specific rare earths in their deposits, the downstream processing know-how and the contacts to make it in a demanding industry.

With literally hundreds of exploration companies and junior miners to chose from, the challenge for investors is separating the real players from the pretenders playing the rare earth buzz to make a quick profit on the stock market.

The speculative nature of rare earth stocks, coupled with the intense investor demand to own them, has prompted fund manager Van Eck Global to launch an exchange-traded fund focused on rare earths and minor metals.

But even the buffer of trading a group of rare earth miners instead of just one doesn’t guarantee a safe ride for investors.

“Everybody’s standing up, waving the flag, and shrieking it’s rare earths, because that pushes the valuation up,” said Byron Capital Market analyst Jon Hykawy. “When the Chinese change their quota system, we will see the bubble rupture.”

That bubble, which has seen the average share price of the top juniors in the sector rise 145 per cent in six months, is one of the main risks facing investors.

Even BlackRock, the world’s largest money manager, says the “jury is still out” when it comes to the long-term investment potential for rare earth mines outside China.

“The ability to bring on production quickly in the higher-price environment means that the longer-term sustainability of those prices are questionable,” Catherine Raw, a fund manager in BlackRock’s natural-resources division, told Reuters.

Regardless of the red flags, analysts and industry observers agree more suppliers are needed, no matter what policy China pursues.

“Whether the Chinese are restricting supply or not, there’s going to be a need for new deposits,” Ecclestone said. “The Chinese do not have a boundless supply of rare earths.”

If new supplies of rare earths do not come online within the next 10 years, a global shortage would likely develop with far-reaching consequences: wind turbines will not be built, electric vehicle production will grind to a halt, and mobile phones would have to triple in size.

The issue even carries national security implications because of the rare earth content in many advanced military weapons, not to mention the economic threat that shortages would present. The problem is, getting new sources of supply into production is not that easy.

Rare earths, despite their name, are not that rare. In Canada alone, there are at least 26 publicly traded companies that have rare earth projects in some stage of exploration.

Not all rare earth deposits are created equal, and good quality, economically feasible deposits are scarce – a risk factor that some investors may have overlooked.

“People just don’t fully understand what’s involved in going from having a few holes in the ground to actually being a producer,” said industry expert Dudley Kingsnorth from a rare earth industry event in Perth, Australia. “You’ve got to build it, and you’ve got to start it up, and the expertise outside China to do that is limited.”

Every rare earth mine contains all 17 elements locked into a mineral that needs to be broken down, or cracked, usually using acid. The cracked rare earth concentrate then needs to be processed again, to separate the individual rare earths, which are then purified into oxides.

With the current quota system, China does not distinguish between the individual rare earth oxides but limits the total tonnage of exports across the board. That has led to Chinese companies exporting as much as possible of the high-value heavy rare earths like dysprosium, instead of low-value light rare earths like cerium.

Because no one is exporting cerium, the prices for the oxide, which is used in catalysts and glass polishing, has jumped to about $53 a kilogram this month from $4 a kg in 2008, according to Asian Metal, a firm that tracks industry prices.

“The price fluctuations recently have been the lights,” said Asian Metal analyst Phil Arnheim. “I think, as long as we have the export quota system in place, there’s going to be a premium on those materials.”

With prices for light rare earths soaring, projects like Molycorp Inc’s Mountain Pass mine in California are looking very attractive to investors.

But most analysts believe China will eventually change its quota system to restrict the rare earths individually. Because China has an abundance of light rare earths available through the Bayan Obo project in Mongolia, changing the quota system would likely trigger a sudden flood of cerium and lanthanum on to the market.

That’s a big risk for Molycorp. If the price of lanthanum oxide were to drop back down to around $7 per kg, the value of a five-year contract the company recently announced with W.R. Grace would tumble from more than $750 million to about $100 million.

Molycorp Chief Executive Mark Smith, speaking at an industry event in Washington, D.C., said he is confident the price at which his company could sell the oxides will stay up across the board, based on supply and demand.

“The entire world outside of China needs about 50,000 tonnes of product a year. … All that China is exporting right now is about 30,000,” he said, adding the oxide prices “are real and we think that they are very sustainable as we move forward.”

While the long-term price of the light rare earths remains open for debate, it is a given in the industry that quotas will continue to tighten the supply of heavy rare earths like terbium and dysprosium, sending prices soaring.

Dysprosium oxide, used in hybrid vehicles, lasers and nuclear reactors, is already selling for $284 a kg and that is projected to rise to over $400 in the next couple of years, according to Asian Metals.

The already tight supply will only get tighter, as analysts anticipate that the heavy rare earths mined in southern China’s ionic clays could run out within 15 to 20 years, which could lead to even higher oxide prices.

While this is good news for miners with deposits rich in heavy rare earths, having valuable minerals in the ground doesn’t necessarily mean big benefits for investors.

Even if the non-Chinese mines were to go into production today, the miners would not receive hundreds of dollars per kilogram of material they produce.

“Eighty to 90 percent of the value is in the processing and that is the great secret of the rare earth space,” Ecclestone said. “Basically, when you pull it out of the ground, it’s not worth a damn.”

It is the processors, who separate the rare earth concentrate into refined oxides, and build relationships with end users, who are making all the money.

A life-size terracotta Warrior watches over the vast lobby at the Neo Material Technologies head office in Toronto. That’s where chief executive Constantine Karayannopoulos has spent the last 17 years building up a rare earth empire.

His company buys rare earth concentrate and separates it into individual oxides in China. Then it transforms those oxides into highly specialized rare earth alloys and magnetic powders, using facilities around the world.

Neo Material is one of just a handful of companies that work closely with technology companies like Samsung and Canon to make rare earth products specific to their needs. The qualification process for working with a new client usually takes one to three years, Karayannopoulos said.

“It’s not as simple as digging it out of the ground and putting it on a truck and out it goes,” Karayannopoulos said. “The basis of what we do is our ability to separate rare earth elements from one another and then to add a lot of value using material technology skills.”

Taking rare earths from minerals in the ground to a separated oxide to a powerful magnet used to rotate a wind turbine is a long and complicated process. To get terbium oxide, worth about $615 a kg, it takes over 30 days of processing.

“I think the markets are completely unaware of what it takes not only to bring a rare earth mine into production,” Karayannopoulos said, “but also to achieve levels of production, and quality of production, that will allow you to sell your products to people who are willing to pay for them.”

In the second quarter of 2010, Neo Material sold just over 3,100 tonnes of separated rare earth oxides, rare earth compounds and magnetic powders. The company posted a quarterly profit of $16 million on revenue of $79.2 million.

Revenue for the 12 months to the end of the second quarter was $261.2 million on 11,719 tonnes of high-value rare earth product and magnetic powders – that is about $22.29 per kg for highly processed rare earth products, which usually sell at a 7-per-cent premium over concentrate.

Contrast that to junior miner Avalon Rare Metal Inc., which plans to sell unprocessed rare earth concentrate for $21.94 a kg, according to its prefeasibility report.

Rare earth concentrate sells for about $4 a kg in China, and while analysts estimate it could be worth between $10 and $20 in the United States or Europe, there are currently no facilities outside China to process it.

Neo Material is investigating building a separation plant in Latin America, Karayannopoulos said, adding his company would look to non-Chinese sources of concentrate to supply it.

“Ultimately, it is in the best interest of our company to be able to get raw materials from other folks, not just our Chinese suppliers,” he said. “So, to us, this global diversification of the supply chain is good.”

In 2008, global demand for rare earths was about 123,000 tonnes. By 2015, demand is forecast to be about 200,000 tonnes a year. This expected growth, coupled with the recent export cuts from China, has end users of rare earths scrambling for supplies, according to Jim Engdahl, CEO of Canada’s Great Western Minerals Group Ltd.

Clients “are exceptionally anxious – I guess the word could be just about in panic mode,” he said. “We’re getting calls daily from non-clients who want product from us.”

Great Western buys rare earth oxides from China and sells rare earth-based metals and alloys to major magnet manufacturers around the world.

The Saskatoon, Saskatchewan-based company also owns numerous rare earth properties in Canada, and is developing the Steenkampskraal mine in South Africa.

It plans to double production of rare earth products at its processing facility in Britain by 2013, when Steenkampskraal is projected to come online.

That expansion will start to relieve some of the tension in the multibillion-dollar industries that rare earths support, like the permanent magnets used in electric cars.

“Now we’re probably talking about $100 billion worth of products built off the back of the capabilities and properties of these rare earths,” Hykawy said.

He estimates the motor in the average Prius hybrid uses about 193 grams, or about 7 ounces, of neodymium and 24 grams of dysprosium, while the fully electric Nissan Leaf uses about 421 grams of neodymium and 56 grams of dysprosium.

“We believe that the electric vehicle is going to be a dominant form of transportation in decades to come,” Byron Capital’s Hykawy said, adding demand for the magnetic rare earths is set to jump almost 800 per cent by 2015.

Even with new mines coming online within the next five years, analysts are forecasting a shortage of heavy rare earths terbium and dysprosium by 2015, and a very tight supply of light rare earths neodymium and praseodymium.

The impending shortage has Bart Gordon, chairman of the U.S. House of Representatives Committee on Science and Technology, and other politicians calling for the U.S. government to fast-track domestic rare earth production.

Since rare earths are used in many U.S. military applications, from the tiny motors in guided missiles to night-vision goggles and lasers, Gordon calls China’s dominance of the industry “a real problem.”

Legislation has been introduced in both the Senate and the House to increase investment in, and boost the production of, rare earths in the United States, a move that has sent valuations surging for miners with U.S. projects.

Over the past three months, Molycorp has risen over 200 per cent to a high of $40.90 a share. It has a market cap of almost $3 billion, despite operating at a loss since launching in June 2008.

Using consensus analyst estimates, Molycorp is currently trading at 70 times above its expected 2010 revenue of $31.9 million. By comparison, a composite group of mining companies currently trades at an average of 2.5 times above expected 2010 revenue.

While the numbers are shocking, Neo Material’s Karayannopoulos sees Molycorp in a different class from the hundreds of junior miners who dot the landscape. His company has signed an agreement with the Colorado-based giant to buy rare earth concentrates once its massive California mine comes online.

“If Molycorp gets up to their design … they’ll be producing 40,000 tonnes of light rare earths at Mountain Pass,” Karayannopoulos said. “At a 40,000 tonne output, they could be producing 1,000 tonnes plus or minus of heavy rare earths.”

“It could be enough to supply the United States, which is not a big buyer of heavy rare earths.