Rohstoff-Explorer: Research oder Neuvorstellung (Seite 1955)

eröffnet am 13.03.08 13:14:32 von

neuester Beitrag 01.05.24 21:08:23 von

neuester Beitrag 01.05.24 21:08:23 von

Beiträge: 29.536

ID: 1.139.490

ID: 1.139.490

Aufrufe heute: 16

Gesamt: 2.701.546

Gesamt: 2.701.546

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| vor 25 Minuten | 3339 | |

| 01.05.24, 18:36 | 2275 | |

| vor 53 Minuten | 2110 | |

| gestern 19:24 | 1735 | |

| vor 26 Minuten | 1366 | |

| vor 1 Stunde | 1339 | |

| gestern 18:35 | 1304 | |

| vor 13 Minuten | 1072 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 1. | 18.001,60 | +0,59 | 240 | |||

| 2. | 2. | 168,20 | +0,08 | 87 | |||

| 3. | 3. | 9,7000 | +12,27 | 75 | |||

| 4. | 14. | 6,1400 | -1,35 | 69 | |||

| 5. | 11. | 0,1865 | 0,00 | 52 | |||

| 6. | 7. | 0,8750 | -12,50 | 47 | |||

| 7. | 12. | 0,1561 | +2,97 | 38 | |||

| 8. | 6. | 2.302,50 | 0,00 | 36 |

Beitrag zu dieser Diskussion schreiben

Antwort auf Beitrag Nr.: 45.541.069 von tommy-hl am 30.09.13 16:45:29Danke, also 20-40 Dollar Gewinn Pro Tonne Erz bleiben übrig.

Beim Frac Sand sind die Kosten übrigens um die 15-17 Dollar die Tonne und der Preis geht so ab 60 Dollar los, Tendenz steigend.

Beim Frac Sand sind die Kosten übrigens um die 15-17 Dollar die Tonne und der Preis geht so ab 60 Dollar los, Tendenz steigend.

Antwort auf Beitrag Nr.: 45.536.807 von XIO am 29.09.13 21:37:50

XIO,

Die hier 'wollen(?)' wohl auch noch so Stück 'Frac Sand Land' Übernehmen, kannst Dir ja vielleicht mal anschauen. Ich hab davon keine Ahnung, vermutlich nur 'ne Bruchbude mit 'genialer Idee', Du kennst Dich da ja besser aus:

http://finance.yahoo.com/q?s=CPS.V&ql=1

Gruß

P.

XIO,

Die hier 'wollen(?)' wohl auch noch so Stück 'Frac Sand Land' Übernehmen, kannst Dir ja vielleicht mal anschauen. Ich hab davon keine Ahnung, vermutlich nur 'ne Bruchbude mit 'genialer Idee', Du kennst Dich da ja besser aus:

http://finance.yahoo.com/q?s=CPS.V&ql=1

Gruß

P.

Zitat von XIO: wie teuer ist es (ungefähres mittelmass), eine Tonne Eisenerz zu fördern ?

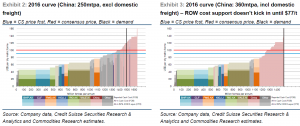

Hier eine Tabelle von Credit Suisse. In der Waagerechten ist das Produktionsvolumen pro Jahr, in der Senkrechten die Kosten dazu. Beispiel: 1.250 Mio. t p. a. sind bis zu 90 $/t zu produzieren. Wird ein größeres Volumen vom Markt verlangt, steigen die Kosten für das über 1.250 mtpa hinausgehende Eisenerz. Bei z. B. 1.400 mtpa müssen Kosten von 122 $/t für die Produktionsspitze berücksichtigt werden.

Bei dem Billig-Volumen der ersten rund 1.000 mtpa handelt es sich größtenteils um alte, sehr große Minen, die noch zu sehr niedrigen Kosten zu erschließen waren, schon lange abgeschrieben sind und sich durch niedrige Kosten ausweisen. Neue Lagerstätten sind viel teurer zu erschließen und zu betreiben:

Gesamtkosten ohne Steuer: Cash cost (C1) FOB plus C2+C3 plus Durchschnittsgrad 62% Fe plus CFR-China Kosten

Antwort auf Beitrag Nr.: 45.540.269 von tommy-hl am 30.09.13 15:08:10wie teuer ist es (ungefähres mittelmass), eine Tonne Eisenerz zu fördern ?

Trading Spotlight

Hier etwas für die "iron men" ...

Der Eisenerz-Preis hält sich um die 130 $/t:

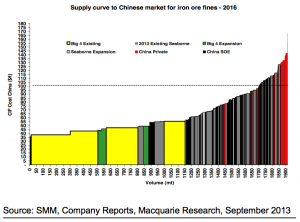

MacQuarie Bank geht in einer neuen Studie davon aus, dass Eisenerz für die nächsten 2 Jahre über 115 $/t notieren wird. Das wäre für die Produzenten natürlich gut:

We expect $100/t plus iron ore prices into the medium term

We have undertaken a detailed run-through of the iron ore demand and supply dynamics, focusing on a bottom-up approach to forecasting steel demand in China and a thorough investigation of inflation, expansions and depletions in both the Chinese domestic iron ore industry and the seaborne market. We conclude that iron ore prices will remain above $115/t over the next two years and will remain above $100/t out to 2020, based on an assessment of the competitive cost curve structure. As such, we have raised our long-run iron ore forecast to $90/t CFR China (62% basis, real $2013) from $80/t previously.

Taking a detailed look at the Chinese domestic ore curve

This work incorporates a detailed study of the Chinese domestic iron ore industry, focusing on cost inflation, capacity expansion and depletion. Based on our projections of the Chinese and seaborne supply curve, we find that nearly 40% of Chinese capacity, largely in the hands of private operators, will be uneconomic by 2018 under our base case forecasts. We believe the Chinese iron ore industry will behave in an economically rational way, as the financial and political incentives to support a loss making sector are no longer present.

The decision-making window closes quickly in a displacement cycle

Our project by project analysis of the potential seaborne expansions finds that half of the proposed projects will require a long-run price of over $100/t to generate a decent IRR and subsequently, depending on their timing to market, many look at risk. Meanwhile, we feel there is just a two-year decision making (and funding) window left for proposed assets before the shadow cast from Vale‟s 90mtpa S11D project prevents further approvals. As a result, we expect base case seaborne supply additions of 380mt through 2020, well below market expectations, as many prospective additions are not progressed, assuming rational decision making.

Moving into an environment of lower volatility

One of the key takeaways from our analysis is that the expected range of iron ore prices within any given year is set to be substantially reduced. With a 200mtpa annualised swing from peak to trough iron ore demand within any given year being common, the steep gradient of the cost curve drives “efficient volatility”, through the need to incentivise and displace marginal tonnes at various points in the cycle. Into the medium term, we see the upper end of the curve flattening, resulting in lower levels of volatility over time and as such, there should be increasing confidence in terms of the range iron ore will trade between in any given year. Certainly, potential for overshoot and undershoot will remain; however, the lower volatility could potentially be the catalyst for positive equity rerating. We note also that $85-90/t represents a floor in cyclical price swings throughout the forecast period. This scenario plays into the hands of the major producers, whose top tier assets allow them to avoid the competitive scrap their smaller peers will be engaged in, while having greater confidence around medium-term investment plans.

Der Eisenerz-Preis hält sich um die 130 $/t:

MacQuarie Bank geht in einer neuen Studie davon aus, dass Eisenerz für die nächsten 2 Jahre über 115 $/t notieren wird. Das wäre für die Produzenten natürlich gut:

We expect $100/t plus iron ore prices into the medium term

We have undertaken a detailed run-through of the iron ore demand and supply dynamics, focusing on a bottom-up approach to forecasting steel demand in China and a thorough investigation of inflation, expansions and depletions in both the Chinese domestic iron ore industry and the seaborne market. We conclude that iron ore prices will remain above $115/t over the next two years and will remain above $100/t out to 2020, based on an assessment of the competitive cost curve structure. As such, we have raised our long-run iron ore forecast to $90/t CFR China (62% basis, real $2013) from $80/t previously.

Taking a detailed look at the Chinese domestic ore curve

This work incorporates a detailed study of the Chinese domestic iron ore industry, focusing on cost inflation, capacity expansion and depletion. Based on our projections of the Chinese and seaborne supply curve, we find that nearly 40% of Chinese capacity, largely in the hands of private operators, will be uneconomic by 2018 under our base case forecasts. We believe the Chinese iron ore industry will behave in an economically rational way, as the financial and political incentives to support a loss making sector are no longer present.

The decision-making window closes quickly in a displacement cycle

Our project by project analysis of the potential seaborne expansions finds that half of the proposed projects will require a long-run price of over $100/t to generate a decent IRR and subsequently, depending on their timing to market, many look at risk. Meanwhile, we feel there is just a two-year decision making (and funding) window left for proposed assets before the shadow cast from Vale‟s 90mtpa S11D project prevents further approvals. As a result, we expect base case seaborne supply additions of 380mt through 2020, well below market expectations, as many prospective additions are not progressed, assuming rational decision making.

Moving into an environment of lower volatility

One of the key takeaways from our analysis is that the expected range of iron ore prices within any given year is set to be substantially reduced. With a 200mtpa annualised swing from peak to trough iron ore demand within any given year being common, the steep gradient of the cost curve drives “efficient volatility”, through the need to incentivise and displace marginal tonnes at various points in the cycle. Into the medium term, we see the upper end of the curve flattening, resulting in lower levels of volatility over time and as such, there should be increasing confidence in terms of the range iron ore will trade between in any given year. Certainly, potential for overshoot and undershoot will remain; however, the lower volatility could potentially be the catalyst for positive equity rerating. We note also that $85-90/t represents a floor in cyclical price swings throughout the forecast period. This scenario plays into the hands of the major producers, whose top tier assets allow them to avoid the competitive scrap their smaller peers will be engaged in, while having greater confidence around medium-term investment plans.

Antwort auf Beitrag Nr.: 45.539.159 von likeshares am 30.09.13 12:24:33Null Risk = null Chance

-----------------------

Nur bestes Management!

-----------------------

Nur geringstes Risiko!

-----------------------

Nur qualitativ hochwertige Resourcen!

-----------------------

Nur qualitativ hochwertige Studien!

-----------------------

Nur höchste Margen!

-----------------------

Nur längste Laufzeit!

-----------------------

Nur so funktioniert das NICHT!

Nur bestes Management!

-----------------------

Nur geringstes Risiko!

-----------------------

Nur qualitativ hochwertige Resourcen!

-----------------------

Nur qualitativ hochwertige Studien!

-----------------------

Nur höchste Margen!

-----------------------

Nur längste Laufzeit!

-----------------------

Nur so funktioniert das NICHT!

1929 ging es erst nach dem Dow Crash für die Minen mit dem Dow gemeinsAm aber viel steiler aufwärts. Sollte wer also einen Börsencrash erwarten, kann man auch aufsammeln. Allerdings verloren die Kurse der Minen wenig 1929. Seitwärt wäre also bis zur Gegenmassnahme nahc einem Crash auch möglcih.

Antwort auf Beitrag Nr.: 45.537.229 von prallhans am 30.09.13 01:30:00erinnert stark an 2000... aber vielleicht sind wir auch erst bei 1999.

jedenfalls wird die rohstoffbranche drehen... vermutlich wird alles wieder viel impulsiver als man es sich erdenken kann. 70% down from here und dann 5000% up oder so

ist man ja gewohnt in der extremen form seit die börsenwelt wie im zeitraffer durchgehandelt wird... auch eine folge des internets.

jedenfalls wird die rohstoffbranche drehen... vermutlich wird alles wieder viel impulsiver als man es sich erdenken kann. 70% down from here und dann 5000% up oder so

ist man ja gewohnt in der extremen form seit die börsenwelt wie im zeitraffer durchgehandelt wird... auch eine folge des internets.