Oroco - kleiner Explorer (Gold) mit zukünftig sehr niedrigen Produktionskosten - 500 Beiträge pro Seite

eröffnet am 10.06.09 10:12:01 von

neuester Beitrag 04.05.24 18:09:34 von

neuester Beitrag 04.05.24 18:09:34 von

Beiträge: 2.394

ID: 1.150.999

ID: 1.150.999

Aufrufe heute: 6

Gesamt: 175.832

Gesamt: 175.832

Aktive User: 0

ISIN: CA6870331007 · WKN: A0Q2HB

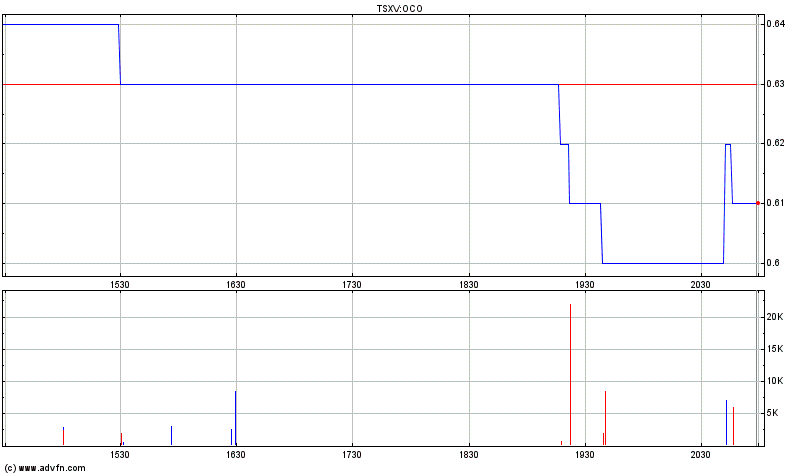

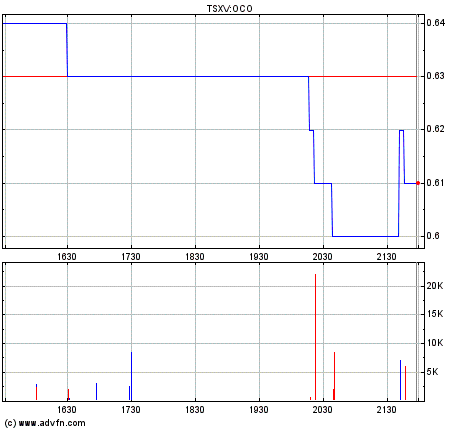

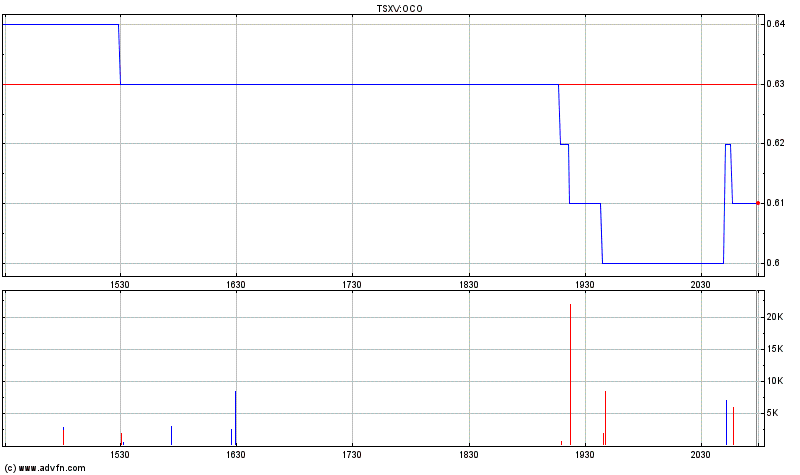

0,3940

EUR

+9,14 %

+0,0330 EUR

Letzter Kurs 10.05.24 Lang & Schwarz

Meistbewertete Beiträge

| Datum | Beiträge | Bewertungen |

|---|---|---|

| 03.05.24 | ||

| 04.05.24 | ||

| 02.05.24 |

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,0000 | +809,09 | |

| 8,0000 | +45,45 | |

| 11,000 | +19,57 | |

| 1,6640 | +16,04 | |

| 527,60 | +15,68 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 6,6800 | -8,94 | |

| 0,7000 | -10,26 | |

| 324,70 | -10,30 | |

| 0,6601 | -26,22 | |

| 47,33 | -97,99 |

Vor ca. 2 Wochen habe ich das Managementteam von Oroco in Zürich getroffen. Gerade machen Sie eine kleine Kapitalerhöhung zu 0.15 CAD, die wie es scheint natürlich total überzeichnet ist und fast niemand etwas bekommt, da die Firma sehr interessant ist und der Kurs bei um die 0,20 CAD liegt. Das jetzt schon vorhandene Gold rechtfertig allein schon mehr als den heutigen Aktienkurs und man bohrt ja weiter... Die Infrastruktur aussen rum ist bezüglich Strassen und Strom recht gut, d.h. hier fallen keine grossen Kosten an. Um den Laden am Schluss in Produktion zu bringen sind rund 20 Mio $ notwendig und davon bekommt man noch rund 75 % ja von entsprechenden Banken geliehen... Die Produktionskosten werden auch sehr niedrig sein, da die einen Berg / Hügel abtragen und man voll beladen eher nach unten fährt....

Was meint Ihr dazu. Die Marktkapitalisierung ist lächerlich niedrig und bei erfolgreichem Projektverlauf ist eine Vervielfachung wahrscheinlich.

Was meint Ihr dazu. Die Marktkapitalisierung ist lächerlich niedrig und bei erfolgreichem Projektverlauf ist eine Vervielfachung wahrscheinlich.

Antwort auf Beitrag Nr.: 37.360.333 von Smallcappicker am 10.06.09 10:12:01Na, dann schau Dir mal die Beiträge über Ascot Mining an: A0Q0G8,

da bin ich vor ca. 6 Monaten mit 20K eingestiegen, zumindest bis

jetzt totes Kapital. Einmal und NIE wieder. Es gibt immer noch viele

Möglichkeiten kurz- und mittelfristig richtig Geld zu verdienen, was

also soll der Quatsch???

da bin ich vor ca. 6 Monaten mit 20K eingestiegen, zumindest bis

jetzt totes Kapital. Einmal und NIE wieder. Es gibt immer noch viele

Möglichkeiten kurz- und mittelfristig richtig Geld zu verdienen, was

also soll der Quatsch???

Das dauert noch bis zur Produktion....

Seite 16

http://www.orocoresourcecorp.com/graphics/images/Oroco%20Res…

Hab auf die Schnelle keine Zahlen gefunden bzgl. kosten!

Auch keine bilanz!

Aber wenn jetzt schon ein PP gemacht wird ist auch nicht viel Geld in der Kasse!

Ergo weitere KE´s werden folgen!

Seeeeehr risikoreich...

Seite 16

http://www.orocoresourcecorp.com/graphics/images/Oroco%20Res…

Hab auf die Schnelle keine Zahlen gefunden bzgl. kosten!

Auch keine bilanz!

Aber wenn jetzt schon ein PP gemacht wird ist auch nicht viel Geld in der Kasse!

Ergo weitere KE´s werden folgen!

Seeeeehr risikoreich...

Antwort auf Beitrag Nr.: 37.362.469 von c77k am 10.06.09 13:12:11Vielen Dank für Eure Meinungen. Das mit den weiteren aber sehr kleinen PP's ist schon bekannt. Ein Freund von mir, der bei Oroco mitmacht und sich sehr gut auskennt, war bei Ascot sehr skeptisch....

Antwort auf Beitrag Nr.: 37.373.738 von Smallcappicker am 11.06.09 17:05:03Insgesamt machen 3 gute Bekannte von mir mit, die sich wirklich gut auskennen und oft auch die Liegenschaften von solchen Firmen persönlich in Mexiko, Kanada, Kolumbien, Ghana usw. anschauen.

Trading Spotlight

Der Betafaktor hat nun auch ganz knapp aus der Gerüchteküche von Oroco etwas geschrieben. Wenn da an sehr guten Bohrergebnissen etwas dran sein sollte, dann könnte das dem Kurs einen Schub geben. Jetzt heisst es abwarten. Selbst das ursprünglich erwartete wäre ja schon nicht schlecht, wenn es eintrifft

OROCO SECOND PHASE DRILLING VERIFIES 2.0 KILOMETER MINERALIZED STRUCTURE

VANCOUVER, British Columbia – (September 17, 2009) Oroco Resource Corp. (TSX-V:

OCO) (“Oroco” or “the Company”) is pleased to announce the progress on and results from

its Cerro Prieto Project in Sonora State, Mexico.

Since beginning the Phase 2 drill program on August 9th, 2009, the two drills have completed

approximately 2000 meters of drilling in ten holes. Six of the holes have been drilled

immediately to the north of the 2008 Phase 1 drill locations at 100 meter intervals along strike

and to depth with the intent of adding resources in the oxide zone. The remaining four drill

holes have been completed on the claims optioned from Yamana Gold Inc. further north along

strike with the objective of extending the overall length of the Cerro Prieto mineralized

structure.

Drill hole locations plotted on a longitudinal section of Cerro Prieto may be viewed at

orocoresourcecorp.com/projects-Cerro-Prieto-Project-Maps-and-Sections.html.

Highlights of the Phase 2 drilling to date include:

All holes completed to their target depth have intersected a strongly mineralized zone,

therefore establishing a drilled strike length of two kilometers;

CP025 intersected 53.1 meters of mineralization with greater than 1% zinc and

anomalous gold, silver and lead values;

CP026 intersected 15.6 meters with 0.324 g/t Au and 65.2 g/t Ag including a 6.2 meter

section with 0.686 g/t Au, and 156.2 g/t Ag;

CP027 intersected a 13.5 m section averaging 0.826 g/t Au and 10.2 g/t Ag including a

3.1 meter section with 2.777 g/t Au and 26.2 g/t Ag; and

CP029 intersected 7.0 meters averaging 1.464 g/t Au including 1 meter that assays

9.070 g/t Au.

CP025 was drilled under 2008 holes CP020 and CP021 which both intersected sections of

highly anomalous mineralization. The paucity of gold and silver and abundance of base metals

points to the vertical zoning of the deposit.

CP026 was drilled 100 meters north along strike of the section with CP025 and intersected the

zone approximately 100 meters below surface.

CP029 was drilled to intersect the mineralized zone 100 meters below CP026.

CP027 was drilled 100 meters north along strike of CP026 and also intersected the zone

approximately 100 meters below surface.

CP028 was drilled under very high surface samples on the Yamana option as outlined in

Oroco’s press release dated August 11, 2009. The hole failed to intersect the target because of

poor drilling conditions and was redrilled as CP030.

Assays have been received for four holes and the highlights are presented in the following table.

Significant Intersections from Cerro Prieto Phase 2 Drill Results

Hole No.

From (m)

To (m) Apparent Thickness True Thickness Au (g/t)

Ag (g/t)

Pb (%)

Zn (%)

CP025

219.0 272.1 53.1 34.5 0.126 4.2 0.19 1.01

222.0 266.5 44.5 28.9 0.137 4.9 0.22 1.16

223.5 253.0 29.5 19.2 0.149 7.1 0.29 1.45

CP026 131.0 146.6 15.6 14.0 0.324 65.2 0.10 0.28

incl 140.4 146.6 6.2 6.0 0.686 156.2 0.11 0.25

and 139.0 143.5 4.5 4.3 1.030 82.9 0.11 0.24

CP027 82.5 96.0 13.5 12.2 0.826 10.2 0.09 0.22

incl 87.0 93.5 6.5 5.9 1.663 19.1 0.14 0.25

incl 87.9 91.0 3.1 2.9 2.777 26.2 0.20 0.25

CP028 NO ASSAYS

CP029 187.0 194.0 7.0 7.0 1.464 2.5 0.18 0.48

incl 188.5 189.5 1.0 1.0 9.070 5.3 0.25 0.64

Oroco is pleased that the results verify that the mineralized zone extends to the north and

maintains a significant thickness. The drilling completed in 2008 enabled the company to

complete a resource estimate from line 150N to line 750N (a distance of 600 meters) and

identified the mineralized zone in drilling as far north as line 1050N in step out hole CP023.

Visual results from the holes drilled on the ground optioned from Yamana also indicate that the

faulting, shearing and brecciation that characterize the zone are all present through line 2150N.

The mineralized zone has now been identified in drilling over a total distance of two kilometers

and is still open, within a 17.5 kilometer strike length, in both directions.

About Oroco

Oroco is a Canadian-based mineral exploration company with its primary focus on the

accelerated development of the gold bearing oxide zones of its Cerro Prieto project, a

polymetallic (Au-Ag-Pb-Zn) project in Sonora State, Mexico.

The Cerro Prieto project consists of the 100% owned, 2,723 ha, San Felix, San Francisco and

Cerro Prieto concessions and the 4,120 ha of the connecting Argonauta 5 Fraccion 1 concession

to which the Company holds an option to purchase (see May 14, 2009 news release). During

the first field season in 2008, the Company drilled 5,975 meters of core and tabled a NI 43-101

compliant resource estimate together with the results of a preliminary metallurgical study (See

May 11, 2009 news release). The Company is moving the Cerro Prieto project forward with the

rapid development of mineral resources, further metallurgy studies and the development of a

preliminary assessment by an independent mining engineering firm.

Qualified Person

Kenneth R. Thorsen, B.Sc., P. Geo., is a director of the company and is a 'qualified person' for

the purposes of National Instrument 43-101 Standards of Disclosure for Mineral Properties of

the Canadian Securities Administrators. He has verified the data (including sampling, analytical

and test data) and prepared or supervised the preparation of the information contained in this

news release.

Quality Assurance & Control

The Company has implemented a quality assurance and control (QA/QC) program to ensure

sampling and analysis of all exploration work is conducted in accordance with the best possible

practices. Split core is transported to the ALS Chemex laboratory in Hermosillo where it is

crushed and pulverized, with pulps sent to the ALS Chemex laboratory in Vancouver, B.C. for

assaying. The other half of the core is retained for future assay verification. The QA/QC policy

includes the chain of custody monitoring, insertion of blanks, standards and duplicates in the

initial samples submitted. The laboratory provides an additional internal control program.

OROCO RESOURCE CORP.

789-999 West Hastings Street, Vancouver, BV V6C 2W2

T: 604.688.6200 F: 604.688.6260

www.orocoresourcecorp.com

For further information, please contact:

Mr. Craig Dalziel, President and CEO

Oroco Resource Corp.

Tel: 604-688-6200

www.orocoresourcecorp.com

VANCOUVER, British Columbia – (September 17, 2009) Oroco Resource Corp. (TSX-V:

OCO) (“Oroco” or “the Company”) is pleased to announce the progress on and results from

its Cerro Prieto Project in Sonora State, Mexico.

Since beginning the Phase 2 drill program on August 9th, 2009, the two drills have completed

approximately 2000 meters of drilling in ten holes. Six of the holes have been drilled

immediately to the north of the 2008 Phase 1 drill locations at 100 meter intervals along strike

and to depth with the intent of adding resources in the oxide zone. The remaining four drill

holes have been completed on the claims optioned from Yamana Gold Inc. further north along

strike with the objective of extending the overall length of the Cerro Prieto mineralized

structure.

Drill hole locations plotted on a longitudinal section of Cerro Prieto may be viewed at

orocoresourcecorp.com/projects-Cerro-Prieto-Project-Maps-and-Sections.html.

Highlights of the Phase 2 drilling to date include:

All holes completed to their target depth have intersected a strongly mineralized zone,

therefore establishing a drilled strike length of two kilometers;

CP025 intersected 53.1 meters of mineralization with greater than 1% zinc and

anomalous gold, silver and lead values;

CP026 intersected 15.6 meters with 0.324 g/t Au and 65.2 g/t Ag including a 6.2 meter

section with 0.686 g/t Au, and 156.2 g/t Ag;

CP027 intersected a 13.5 m section averaging 0.826 g/t Au and 10.2 g/t Ag including a

3.1 meter section with 2.777 g/t Au and 26.2 g/t Ag; and

CP029 intersected 7.0 meters averaging 1.464 g/t Au including 1 meter that assays

9.070 g/t Au.

CP025 was drilled under 2008 holes CP020 and CP021 which both intersected sections of

highly anomalous mineralization. The paucity of gold and silver and abundance of base metals

points to the vertical zoning of the deposit.

CP026 was drilled 100 meters north along strike of the section with CP025 and intersected the

zone approximately 100 meters below surface.

CP029 was drilled to intersect the mineralized zone 100 meters below CP026.

CP027 was drilled 100 meters north along strike of CP026 and also intersected the zone

approximately 100 meters below surface.

CP028 was drilled under very high surface samples on the Yamana option as outlined in

Oroco’s press release dated August 11, 2009. The hole failed to intersect the target because of

poor drilling conditions and was redrilled as CP030.

Assays have been received for four holes and the highlights are presented in the following table.

Significant Intersections from Cerro Prieto Phase 2 Drill Results

Hole No.

From (m)

To (m) Apparent Thickness True Thickness Au (g/t)

Ag (g/t)

Pb (%)

Zn (%)

CP025

219.0 272.1 53.1 34.5 0.126 4.2 0.19 1.01

222.0 266.5 44.5 28.9 0.137 4.9 0.22 1.16

223.5 253.0 29.5 19.2 0.149 7.1 0.29 1.45

CP026 131.0 146.6 15.6 14.0 0.324 65.2 0.10 0.28

incl 140.4 146.6 6.2 6.0 0.686 156.2 0.11 0.25

and 139.0 143.5 4.5 4.3 1.030 82.9 0.11 0.24

CP027 82.5 96.0 13.5 12.2 0.826 10.2 0.09 0.22

incl 87.0 93.5 6.5 5.9 1.663 19.1 0.14 0.25

incl 87.9 91.0 3.1 2.9 2.777 26.2 0.20 0.25

CP028 NO ASSAYS

CP029 187.0 194.0 7.0 7.0 1.464 2.5 0.18 0.48

incl 188.5 189.5 1.0 1.0 9.070 5.3 0.25 0.64

Oroco is pleased that the results verify that the mineralized zone extends to the north and

maintains a significant thickness. The drilling completed in 2008 enabled the company to

complete a resource estimate from line 150N to line 750N (a distance of 600 meters) and

identified the mineralized zone in drilling as far north as line 1050N in step out hole CP023.

Visual results from the holes drilled on the ground optioned from Yamana also indicate that the

faulting, shearing and brecciation that characterize the zone are all present through line 2150N.

The mineralized zone has now been identified in drilling over a total distance of two kilometers

and is still open, within a 17.5 kilometer strike length, in both directions.

About Oroco

Oroco is a Canadian-based mineral exploration company with its primary focus on the

accelerated development of the gold bearing oxide zones of its Cerro Prieto project, a

polymetallic (Au-Ag-Pb-Zn) project in Sonora State, Mexico.

The Cerro Prieto project consists of the 100% owned, 2,723 ha, San Felix, San Francisco and

Cerro Prieto concessions and the 4,120 ha of the connecting Argonauta 5 Fraccion 1 concession

to which the Company holds an option to purchase (see May 14, 2009 news release). During

the first field season in 2008, the Company drilled 5,975 meters of core and tabled a NI 43-101

compliant resource estimate together with the results of a preliminary metallurgical study (See

May 11, 2009 news release). The Company is moving the Cerro Prieto project forward with the

rapid development of mineral resources, further metallurgy studies and the development of a

preliminary assessment by an independent mining engineering firm.

Qualified Person

Kenneth R. Thorsen, B.Sc., P. Geo., is a director of the company and is a 'qualified person' for

the purposes of National Instrument 43-101 Standards of Disclosure for Mineral Properties of

the Canadian Securities Administrators. He has verified the data (including sampling, analytical

and test data) and prepared or supervised the preparation of the information contained in this

news release.

Quality Assurance & Control

The Company has implemented a quality assurance and control (QA/QC) program to ensure

sampling and analysis of all exploration work is conducted in accordance with the best possible

practices. Split core is transported to the ALS Chemex laboratory in Hermosillo where it is

crushed and pulverized, with pulps sent to the ALS Chemex laboratory in Vancouver, B.C. for

assaying. The other half of the core is retained for future assay verification. The QA/QC policy

includes the chain of custody monitoring, insertion of blanks, standards and duplicates in the

initial samples submitted. The laboratory provides an additional internal control program.

OROCO RESOURCE CORP.

789-999 West Hastings Street, Vancouver, BV V6C 2W2

T: 604.688.6200 F: 604.688.6260

www.orocoresourcecorp.com

For further information, please contact:

Mr. Craig Dalziel, President and CEO

Oroco Resource Corp.

Tel: 604-688-6200

www.orocoresourcecorp.com

Antwort auf Beitrag Nr.: 37.362.047 von chinagerd am 10.06.09 12:30:20Na, herzlichen Glückwunsch zu Ascot?!

Oder nich...

Oder nich...

06.10.2009 14:58

IRW-PRESS: Oroco Resource Corp.: Oroco Resource Corp.: Beginn von metallurgischen Phase-II-Tests

Oroco Resource Corp.: Beginn von metallurgischen Phase-II-Tests

VANCOUVER, British Columbia (6. Oktober 2009) Oroco Resource Corp. (TSX-V: OCO) (Oroco oder das Unternehmen) freut sich, ein Update seines Projektes Cerro Prieto im mexikanischen Bundesstaat Sonora bekannt zu geben.

Nach dem Erhalt der Ergebnisse des Bohrprogramms 2008 und angesichts der positiven Resultate des aktuellen Bohrprogramms hat Oroco seine vorläufige Minenplanung und metallurgische Phase-II-Tests begonnen und wird in Kürze eine Umweltstudie starten.

Die ersten metallurgischen Studien, die gleichzeitig mit dem Phase-I-Explorationsprogramm 2008 durchgeführt wurden, ergaben bei Bottle-Roll-Tests eine Goldgewinnung von 85 bis 92 %. Das Unternehmen beauftragte Kappes, Cassidy&Associates aus Reno (Nevada) mit der Durchführung von weiteren Tests während der nächsten Phase der metallurgischen Untersuchungen. In der vergangenen Woche hat das Unternehmen zwei metallurgische 250-Kilogramm-Proben von zwei im Jahr 2008 gebohrten Bohrlöchern der Oxidzone Cerro Prieto entnommen. Diese sind die ersten von sechs Testproben, die entlang des zwei Kilometer langen Streichens der mineralisierten Zone entnommen werden, welche mittels Schürfungen und Bohrungen beschrieben wurde.

Die ersten beiden entnommenen Proben stammen aus Bohrlöchern zwischen den Abschnitten 150N und 650N, die 2008 gebohrt wurden. Eine Probe umfasst die Zone zwischen der Oberfläche und einer Tiefe von 150 Metern, wo im Allgemeinen höhere Goldgehalte vorhanden sind, während die zweite Probe die Zone zwischen einer Tiefe von 150 Metern und dem Ende der Oxidzone etwa 300 Meter unterhalb der Oberfläche umfasst. Die restlichen vier Proben werden nach dem Abschluss des aktuellen Bohrprogramms entnommen. Zwei Proben werden in ähnlichen Tiefen zwischen den Abschnitten 750N und 1.350N entnommen werden, zwei weitere Proben zwischen dem Abschnitt 1.350N und dem nördlichen Ende der mineralisierten Zone.

Die ersten beiden Proben wurden an Kappes, Cassidy gesendet, wo eine Reihe von Tests zur Bestimmung der Laugungsqualitäten des Materials durchgeführt wird. Jede Probe wird einem grobkörnigen Bottle-Roll-Laugungstest sowie zwei 120-Tage-Säulenlaugungstests mit Brechgrößen von -25 bzw. -12,5 Millimeter unterzogen. Bei den Proben werden nötigenfalls auch Agglomerationstests durchgeführt. Nach den ersten Agglomerationstests werden bei Haufenhöhen von 40 und 60 Metern Durchlässigkeitstests durchgeführt.

Die Erprobung aller Proben wird etwa vier Monate nach dem Einreichen der letzten Proben erfolgen. Da die Bohrungen am nördlichen Ende der mineralisierten Zone vermutlich im November oder Dezember abgeschlossen werden, geht man davon aus, dass die letzten Ergebnisse der Tests im ersten oder zweiten Quartal 2010 eintreffen werden.

Das Unternehmen begann auch metallurgische Tests, um herauszufinden, ob der Kern für die Laugung von Zink, Silber und Blei mittels der AmmLeach-Technologie geeignet ist. AmmLeach ist ein eigenes ammoniakbasiertes Verfahren, das von MetalLeach aus Western Australia entwickelt wurde. AmmLeach sandte zunächst den Teil einer Erzprobe für Kopfuntersuchungen und zur mineralogischen Identifizierung ein. Danach wurden Bodenproben (75 Mikron) mittels AmmLeach-Lösungen gelaugt und die Extraktionsrate sowie der Extraktionsgehalt gemessen. Die ersten Ergebnisse, die in Kürze eintreffen sollen, werden Auskunft darüber geben, ob weitere umfassende Erprobungen gerechtfertigt sind.

Moose Mountain Technical Services, das vom Unternehmen mit der Durchführung von technischen Dienstleistungen beauftragt wurde, absolvierte in der vergangenen Woche eine Standortbesichtigung des Projektes Cerro Prieto, um dessen Beschaffenheit zu überprüfen und die erforderlichen Informationen für die Entwicklung einer vorläufigen Evaluierung zu erhalten. Der vorläufige Bericht von Moose Mountain, der auf den Daten des Phase-I-Explorationsprogramms und auf der jüngsten Standortbesichtigung basiert, soll in den kommenden Wochen eintreffen. Ein aktualisierter Endbericht wird erstellt, sobald alle Untersuchungen der Phase-II-Explorationen eingetroffen sind.

Das Unternehmen überprüft auch Vorschläge hinsichtlich der Durchführung von Umweltstudien. Das Unternehmen geht davon aus, dass noch in diesem Monat ein entsprechender Auftrag erteilt werden wird.

Craig Dalziel, President von Oroco, sagte bezüglich der Fortschritte des Unternehmens: Einer positiven Produktionsentscheidung bei Orocos Projekt Cerro Prieto scheint nichts mehr im Wege zu stehen. Die vorläufige Minenbewertung, die metallurgischen Phase-II-Erprobungen und die Umweltstudien sollen das Projekt weiterentwickeln, sodass eine entsprechende Entscheidung gefällt werden kann. Wir sind zuversichtlicher denn je, dass Oroco dieses Ziel erreichen kann.

Über Oroco

Oroco ist ein kanadisches Mineralexplorationsunternehmen, dessen Hauptaugenmerk auf der raschen Erschließung der goldhaltigen Oxidzonen auf seinem Projekt Cerro Prieto, einem polymetallischen (Au-Ag-Pb-Zn) Projekt im mexikanischen Bundesstaat Sonora, liegt.

Das Projekt Cerro Prieto besteht aus den zu 100 % unternehmenseigenen Konzessionen San Felix, San Francisco und Cerro Prieto (insgesamt 2.723 ha) und aus der Konzession Argonauta 5 Fracción 1 (4.120 ha), auf die das Unternehmen eine Kaufoption hat (siehe Pressemitteilung vom 14. Mai 2009). Im Laufe der ersten Feldsaison 2008 bohrte das Unternehmen 5.975 Meter und erstellte eine Ressourcenschätzung gemäß NI 43-101 sowie die Ergebnisse einer vorläufigen metallurgischen Studie (siehe Pressemitteilung vom 11. Mai 2009). Das Phase-II-Bohrprogramm, das geplante Diamantbohrungen auf 8.000 Metern beinhaltet, hat im Juli dieses Jahres begonnen.

Qualifizierte Person

Kenneth R. Thorsen, B. Sc., P. Geo., ist ein Director des Unternehmens und eine qualifizierte Person gemäß den Bestimmungen von National Instrument 43-101, Standards of Disclosure for Mineral Properties of the Canadian Securities Administrators. Er hat die Erstellung der technischen Informationen in dieser Pressemitteilung beaufsichtigt.

Für weitere Informationen kontaktieren Sie bitte:

Mr. Craig Dalziel, President und CEO

www.orocoresourcecorp.com

Quelle: http://www.finanznachrichten.de/nachrichten-2009-10/15131046…

IRW-PRESS: Oroco Resource Corp.: Oroco Resource Corp.: Beginn von metallurgischen Phase-II-Tests

Oroco Resource Corp.: Beginn von metallurgischen Phase-II-Tests

VANCOUVER, British Columbia (6. Oktober 2009) Oroco Resource Corp. (TSX-V: OCO) (Oroco oder das Unternehmen) freut sich, ein Update seines Projektes Cerro Prieto im mexikanischen Bundesstaat Sonora bekannt zu geben.

Nach dem Erhalt der Ergebnisse des Bohrprogramms 2008 und angesichts der positiven Resultate des aktuellen Bohrprogramms hat Oroco seine vorläufige Minenplanung und metallurgische Phase-II-Tests begonnen und wird in Kürze eine Umweltstudie starten.

Die ersten metallurgischen Studien, die gleichzeitig mit dem Phase-I-Explorationsprogramm 2008 durchgeführt wurden, ergaben bei Bottle-Roll-Tests eine Goldgewinnung von 85 bis 92 %. Das Unternehmen beauftragte Kappes, Cassidy&Associates aus Reno (Nevada) mit der Durchführung von weiteren Tests während der nächsten Phase der metallurgischen Untersuchungen. In der vergangenen Woche hat das Unternehmen zwei metallurgische 250-Kilogramm-Proben von zwei im Jahr 2008 gebohrten Bohrlöchern der Oxidzone Cerro Prieto entnommen. Diese sind die ersten von sechs Testproben, die entlang des zwei Kilometer langen Streichens der mineralisierten Zone entnommen werden, welche mittels Schürfungen und Bohrungen beschrieben wurde.

Die ersten beiden entnommenen Proben stammen aus Bohrlöchern zwischen den Abschnitten 150N und 650N, die 2008 gebohrt wurden. Eine Probe umfasst die Zone zwischen der Oberfläche und einer Tiefe von 150 Metern, wo im Allgemeinen höhere Goldgehalte vorhanden sind, während die zweite Probe die Zone zwischen einer Tiefe von 150 Metern und dem Ende der Oxidzone etwa 300 Meter unterhalb der Oberfläche umfasst. Die restlichen vier Proben werden nach dem Abschluss des aktuellen Bohrprogramms entnommen. Zwei Proben werden in ähnlichen Tiefen zwischen den Abschnitten 750N und 1.350N entnommen werden, zwei weitere Proben zwischen dem Abschnitt 1.350N und dem nördlichen Ende der mineralisierten Zone.

Die ersten beiden Proben wurden an Kappes, Cassidy gesendet, wo eine Reihe von Tests zur Bestimmung der Laugungsqualitäten des Materials durchgeführt wird. Jede Probe wird einem grobkörnigen Bottle-Roll-Laugungstest sowie zwei 120-Tage-Säulenlaugungstests mit Brechgrößen von -25 bzw. -12,5 Millimeter unterzogen. Bei den Proben werden nötigenfalls auch Agglomerationstests durchgeführt. Nach den ersten Agglomerationstests werden bei Haufenhöhen von 40 und 60 Metern Durchlässigkeitstests durchgeführt.

Die Erprobung aller Proben wird etwa vier Monate nach dem Einreichen der letzten Proben erfolgen. Da die Bohrungen am nördlichen Ende der mineralisierten Zone vermutlich im November oder Dezember abgeschlossen werden, geht man davon aus, dass die letzten Ergebnisse der Tests im ersten oder zweiten Quartal 2010 eintreffen werden.

Das Unternehmen begann auch metallurgische Tests, um herauszufinden, ob der Kern für die Laugung von Zink, Silber und Blei mittels der AmmLeach-Technologie geeignet ist. AmmLeach ist ein eigenes ammoniakbasiertes Verfahren, das von MetalLeach aus Western Australia entwickelt wurde. AmmLeach sandte zunächst den Teil einer Erzprobe für Kopfuntersuchungen und zur mineralogischen Identifizierung ein. Danach wurden Bodenproben (75 Mikron) mittels AmmLeach-Lösungen gelaugt und die Extraktionsrate sowie der Extraktionsgehalt gemessen. Die ersten Ergebnisse, die in Kürze eintreffen sollen, werden Auskunft darüber geben, ob weitere umfassende Erprobungen gerechtfertigt sind.

Moose Mountain Technical Services, das vom Unternehmen mit der Durchführung von technischen Dienstleistungen beauftragt wurde, absolvierte in der vergangenen Woche eine Standortbesichtigung des Projektes Cerro Prieto, um dessen Beschaffenheit zu überprüfen und die erforderlichen Informationen für die Entwicklung einer vorläufigen Evaluierung zu erhalten. Der vorläufige Bericht von Moose Mountain, der auf den Daten des Phase-I-Explorationsprogramms und auf der jüngsten Standortbesichtigung basiert, soll in den kommenden Wochen eintreffen. Ein aktualisierter Endbericht wird erstellt, sobald alle Untersuchungen der Phase-II-Explorationen eingetroffen sind.

Das Unternehmen überprüft auch Vorschläge hinsichtlich der Durchführung von Umweltstudien. Das Unternehmen geht davon aus, dass noch in diesem Monat ein entsprechender Auftrag erteilt werden wird.

Craig Dalziel, President von Oroco, sagte bezüglich der Fortschritte des Unternehmens: Einer positiven Produktionsentscheidung bei Orocos Projekt Cerro Prieto scheint nichts mehr im Wege zu stehen. Die vorläufige Minenbewertung, die metallurgischen Phase-II-Erprobungen und die Umweltstudien sollen das Projekt weiterentwickeln, sodass eine entsprechende Entscheidung gefällt werden kann. Wir sind zuversichtlicher denn je, dass Oroco dieses Ziel erreichen kann.

Über Oroco

Oroco ist ein kanadisches Mineralexplorationsunternehmen, dessen Hauptaugenmerk auf der raschen Erschließung der goldhaltigen Oxidzonen auf seinem Projekt Cerro Prieto, einem polymetallischen (Au-Ag-Pb-Zn) Projekt im mexikanischen Bundesstaat Sonora, liegt.

Das Projekt Cerro Prieto besteht aus den zu 100 % unternehmenseigenen Konzessionen San Felix, San Francisco und Cerro Prieto (insgesamt 2.723 ha) und aus der Konzession Argonauta 5 Fracción 1 (4.120 ha), auf die das Unternehmen eine Kaufoption hat (siehe Pressemitteilung vom 14. Mai 2009). Im Laufe der ersten Feldsaison 2008 bohrte das Unternehmen 5.975 Meter und erstellte eine Ressourcenschätzung gemäß NI 43-101 sowie die Ergebnisse einer vorläufigen metallurgischen Studie (siehe Pressemitteilung vom 11. Mai 2009). Das Phase-II-Bohrprogramm, das geplante Diamantbohrungen auf 8.000 Metern beinhaltet, hat im Juli dieses Jahres begonnen.

Qualifizierte Person

Kenneth R. Thorsen, B. Sc., P. Geo., ist ein Director des Unternehmens und eine qualifizierte Person gemäß den Bestimmungen von National Instrument 43-101, Standards of Disclosure for Mineral Properties of the Canadian Securities Administrators. Er hat die Erstellung der technischen Informationen in dieser Pressemitteilung beaufsichtigt.

Für weitere Informationen kontaktieren Sie bitte:

Mr. Craig Dalziel, President und CEO

www.orocoresourcecorp.com

Quelle: http://www.finanznachrichten.de/nachrichten-2009-10/15131046…

Antwort auf Beitrag Nr.: 38.264.995 von kockar am 27.10.09 20:28:33Volumen 835'100

Sieht aus als wurde hier ausserbörslich kräftig eingekauft!

Der Kursgewinn heute von mehr als 11% war ja auch nicht schlecht!

Sieht aus als wurde hier ausserbörslich kräftig eingekauft!

Der Kursgewinn heute von mehr als 11% war ja auch nicht schlecht!

Heute in Frankfurt +52,71% - ausserdem sollen grossartige News folgen!!!! Hier könnte es bald sehr munter nach Oben gehen!

Zum jetzigen Preis ist die Aktie noch immer ein Geschenk.

Schauen wir mal.....

Zum jetzigen Preis ist die Aktie noch immer ein Geschenk.

Schauen wir mal.....

Was meint ihr zum Titel? Der Wert wurde ja mit "Strong Buy" eingestuft!

Oroco drills 22.5 m of 4.36 g/t Au at Cerro Prietro

2010-01-12 06:25 ET - News Release

Mr. Craig Dalziel reports

OROCO ANNOUNCES CERRO PRIETO PHASE TWO DRILL RESULTS

Oroco Resource Corp. has released the following results from the 2009 phase 2 drill program at its Cerro Prieto project in northern Sonora state, Mexico.

Highlights of the results from the infill drilling include:

22.5 metres of 4.36 grams per tonne (g/t) Au in CP053 including nine metres of 8.62 g/t Au;

26 metres of 2.96 g/t Au in CP064 including 3.5 metres of 7.80 g/t Au;

19 metres of 2.99 g/t Au in CP065 including 8.1 metres of 6.42 g/t Au.

In 2009, the company completed a total of 8,575.9 metres in 42 diamond drill holes. Fifteen holes tested the extension of the oxide zone that contains the resource calculated from the 2008 drill program, three holes tested the deeper sulphide mineralization, eight holes tested the Argonauta claim optioned from Yamana Gold Inc., the results of which have been previously reported, and most significantly, 16 holes were recently drilled to infill an area from which the company anticipates the initial ore production at Cerro Prieto.

2010-01-12 06:25 ET - News Release

Mr. Craig Dalziel reports

OROCO ANNOUNCES CERRO PRIETO PHASE TWO DRILL RESULTS

Oroco Resource Corp. has released the following results from the 2009 phase 2 drill program at its Cerro Prieto project in northern Sonora state, Mexico.

Highlights of the results from the infill drilling include:

22.5 metres of 4.36 grams per tonne (g/t) Au in CP053 including nine metres of 8.62 g/t Au;

26 metres of 2.96 g/t Au in CP064 including 3.5 metres of 7.80 g/t Au;

19 metres of 2.99 g/t Au in CP065 including 8.1 metres of 6.42 g/t Au.

In 2009, the company completed a total of 8,575.9 metres in 42 diamond drill holes. Fifteen holes tested the extension of the oxide zone that contains the resource calculated from the 2008 drill program, three holes tested the deeper sulphide mineralization, eight holes tested the Argonauta claim optioned from Yamana Gold Inc., the results of which have been previously reported, and most significantly, 16 holes were recently drilled to infill an area from which the company anticipates the initial ore production at Cerro Prieto.

neben der Goldresource finde ich die Zinkgeschichte fast noch mehr interssant!!!

beim aktuellen Zinkkurs iss das ein Schatz!

alleine das Zink hat einen Marktwert von ca. 800 Mio $

CERRO PRIETO PROJECT HIGHLIGHTS

• Gold resource: 300,000 ounce indicated oxide gold resource with 85% extraction in preliminary

leach tests.

• Zinc resource : +500,000,000 pound zinc resource with 85.3% extraction in preliminary leach tests.

• Updated resource to incorporate Phase Two drill program data.

• Recent expansion of landholdings through property option agreement with Yamana Gold Inc. gives

Oroco 100% ownership of 7,000 ha of concessions with no additional cash payments.

• Concessions contain 17.5 km of strike length of structure being tested at Cerro Prieto.

• Thickness of zone, topography and grade indicate potential for very low cost initial open pit

operation focused on mining the oxide gold resource.

• Premier logistics include water source, paved highway and national power grid within 10 kilometers,

and good mining work force within one hour of project.

• Mining friendly Mexico gives the opportunity to put project into production within a short time frame.

• 8,500 meter Phase Two drill program initiated July 2009: Testing 1,500 meters strike length of oxide

mineralization, as well as infill drilling in area of indicated resource. 42 holes completed December

2010.

• Phase Two metallurgy studies initiated October 2009.

• Preliminary assessment by an independent mining engineering firm underway.

beim aktuellen Zinkkurs iss das ein Schatz!

alleine das Zink hat einen Marktwert von ca. 800 Mio $

CERRO PRIETO PROJECT HIGHLIGHTS

• Gold resource: 300,000 ounce indicated oxide gold resource with 85% extraction in preliminary

leach tests.

• Zinc resource : +500,000,000 pound zinc resource with 85.3% extraction in preliminary leach tests.

• Updated resource to incorporate Phase Two drill program data.

• Recent expansion of landholdings through property option agreement with Yamana Gold Inc. gives

Oroco 100% ownership of 7,000 ha of concessions with no additional cash payments.

• Concessions contain 17.5 km of strike length of structure being tested at Cerro Prieto.

• Thickness of zone, topography and grade indicate potential for very low cost initial open pit

operation focused on mining the oxide gold resource.

• Premier logistics include water source, paved highway and national power grid within 10 kilometers,

and good mining work force within one hour of project.

• Mining friendly Mexico gives the opportunity to put project into production within a short time frame.

• 8,500 meter Phase Two drill program initiated July 2009: Testing 1,500 meters strike length of oxide

mineralization, as well as infill drilling in area of indicated resource. 42 holes completed December

2010.

• Phase Two metallurgy studies initiated October 2009.

• Preliminary assessment by an independent mining engineering firm underway.

DRILL, DEFINE, MINE: CRITICAL PATH TO MINING

Jan 2009 Complete resource estimate, begin metallurgical studies

July 2009 Commence infill and extension drilling

Oct 2009 Commence pre-feasibility study, phase two

metallurgical study and environmental study

Dec 2009 Complete Phase Two drilling

Complete preliminary environmental studies

Q1 2010 est. Complete updated resource calculation

Q2 2010 est. Complete Phase Two metallurgical study

Q2 2010 est. Complete prefeasibility Study

da steht einiges an.............

Jan 2009 Complete resource estimate, begin metallurgical studies

July 2009 Commence infill and extension drilling

Oct 2009 Commence pre-feasibility study, phase two

metallurgical study and environmental study

Dec 2009 Complete Phase Two drilling

Complete preliminary environmental studies

Q1 2010 est. Complete updated resource calculation

Q2 2010 est. Complete Phase Two metallurgical study

Q2 2010 est. Complete prefeasibility Study

da steht einiges an.............

CERRO PRIETO PROJECT

Highlights

300,000 OUNCE OXIDE GOLD RESOURCE OPEN ALONG STRIKE

100% OWNERSHIP INTEREST IN 70 SQ. KM (7,000 ha) OF CONCESSIONS CONTAINING UP TO 17.5 KM OF STRIKE LENGTH OF GEOLOGICAL STRUCTURE

CERRO PRIETO PURCHASE PRICE OF US $2.5 MILLION FULLY PAID

FAVOURABLE LOCATION AND MINING LAWS

OXIDE MINERALIZATION FROM SURFACE TO MAXIMUM DEPTH OF 350 METERS

PRELIMINARY METALURGY COMPLETE INDICATING GOOD RECOVERIES

POTENTIAL FOR LOW COST OPEN PIT MINE: PRELIMINARY MINING PLAN UNDERWAY

Summary

Concessions: San Francisco (15 hectares), San Felix (200 hectares), and Cerro Prieto North (2,508 hectares)

Ownership: Oroco owns a 100% interest in each of the three properties. The San Francisco and San Felix properties are subject to a 2% NSR. The Argonauta concession was optioned from Yamana Gold Inc. on May 11, 2009. The Option terms include the issuance of 500,000 common shares to Yamana upon signing of a formal option agreement, the completion of at least 1,500 meters of drilling on the Optioned Property before January 1, 2011, and the issuance of an additional 500,000 common shares to Yamana on or before January 1, 2011.Thereafter the property is 100% owned by Oroco, subject to a 2% net smelter return royalty payable to Yamana.

Location: Sonora State, Mexico, 135 kilometers north of state capital Hermosillo. The concessions cover land that is a privately owned cattle range land with no communities or residents. Access to the property is secured by agreement with the landowner. The nearest community of Cucurpe is 12 kilometres south. The regional center of Magdalena de Kino (population 40,000) is 27 kilometres northwest and is a one hour drive on mostly paved road.

Infrastructure: National Grid power lines and a paved road leading to the State’s major highway are each less than five kilometres from the property. Ground water is available on site and a river flows year round four kilometers south of the property. There are numerous nearby road and rail links to ports in the state of Sonora.

NI 43-101 Compliant Resource: The results of an independently calculated mineral resource estimate based on data from the Phase 1 exploration program were announced on January 27, 2009. With the completion of preliminary metallurgical testing demonstrating high percentage recoveries of gold and zinc the resource estimate was redefined and a restated resource estimate was issued on May 12, 2009.

The San Francisco and San Felix concessions were optioned in November of 2006 and the acquisition completed in March of 2008 with the payment of the full purchase price. Exploration commenced in April 2008 immediately following Oroco’s initial public offering. The objective of the Phase I exploration program was to confirm the historical resource reported in 1999 (which was based on a 23 hole reverse circulation drill program and an underground and surface sampling program, and to test for the potential to expand that resource. The historic, non-NI43-101 compliant resource was considered important as a guide to the potential of the property but the objective of the Phase I exploration program was to both confirm the historical resource and test the potential for the presence of a larger, bulk mineable zone of economic mineralization along strike, and at depth, where mineralization remained open and where the previous operator had not drilled nor reported a sampling program. That Phase I program was completed in October of 2008 with excellent results. The program consisted of a total of 5,975.1 meters of diamond drilling in twenty-four holes, trenching and sampling across the mineralized shear zone at 50 meter intervals, and mapping on surface. Twenty-two of the holes drilled intersected the mineralized zone with a true thickness ranging from ten meters to greater than fifty meters, with an average true thickness of approximately forty meters, while two drill holes were abandoned due to poor ground conditions before hitting the structure. Drilling has now been completed at 100 meter spacing along 600 meters of strike length to a maximum depth of 400 meters, allowing for an initial indicated resource and inferred resource to be calculated. In addition, a single drill hole drilled 300 meters along strike of intensive drilling intersected a strongly mineralized zone. Drilling, trenching, and mapping have now traced the mineralized structure for 1250 meters on surface to a maximum depth of 400 meters.

YAMANA OPTION

The 4,200 ha Argonauta concession was optioned from Yamana Gold Inc. on May 11, 2009. The Option terms include the issuance of 500,000 common shares to Yamana upon signing of a formal option agreement, the completion of at least 1,500 meters of drilling on the Optioned Property before January 1, 2011, and the issuance of an additional 500,000 common shares to Yamana on or before January 1, 2011.Thereafter the property is 100% owned by Oroco, subject to a 2% net smelter return royalty payable to Yamana.

The Optioned Property covers projected extensions to the north and south of the mineralized shear zone on the Company’s 100% owned Cerro Prieto project claims (“Cerro Prieto”) which host the recently announced estimated resource. The extensions total 9.2 kilometres and include 1.7 kilometres of projected strike length between Cerro Prieto and the Company’s 100% owned Cerro Prieto North claim (“CPN Claim”) and 7.5 kilometres to the south of Cerro Prieto.

To the north of the estimated resource, the Company has established the continuation of the Cerro Prieto mineralized zone to its northern boundary with the Optioned Property. In addition, the Company established what it believes to be the continuation of the mineralized zone on the CPN Claim with highly anomalous assays from samples taken over a series of outcrops of the mineralized zone along 400 metres of strike length (see the Company’s April 30, 2008 news release). Furthermore, Mexican government geologic maps identify the historical gold and silver La Tinaja mine on the projected mineralized zone on the Optioned Property approximately 450 metres north of CP023, the Company’s northernmost drill hole on Cerro Prieto. Consequently, the Company is of the opinion that the mineralized zone continues to the north on to the Optioned Property and possibly strikes to and through the CPN Claim.

To the south of Cerro Prieto, the Optioned Property covers a previously unexplored potential 7.5 kilometre extension of the mineralized shear zone. In total, Cerro Prieto, the CPN Claim and the Optioned Property cover a total potential strike length of the mineralized shear zone of 17.5 kilometres.

Diamond Drill Results – Table – Cross Sections

Trenching and Sampling Results – Plan View

At the completion of Oroco's Phase 1 exploration program at Cerro Prieto, Giroux Consultants Ltd. of Vancouver, an independent consulting firm specializing in resource and reserve calculations completed a resource calculation using information from 23 of the 24 holes completed by Oroco in 2008 (Drill hole CP023, considered a step out hole, was drilled on strike, 300 meters north of the area of drilling at 100 meter intervals, and intercepted a broad zone of well mineralized rock but data from this hole was not included in the resource calculation).

The results of an independently calculated mineral resource estimate based on data from the Phase 1 exploration program were announced on January 27, 2009. With the completion of preliminary metallurgical demonstrating high percentage recoveries of gold and zinc the resource estimate was redefined and a restated resource estimate was issued on May 12, 2009.

A Phase 2 drill program is planned for 2009 which will include drilling the strike length between this hole and the area of the initial resource calculation, where mineralization has also been confirmed by trenching and sampling on the outcropping structure, as well as drilling on strike north of this hole to the property boundary, as well as a detailed metallurgical study, an environmental study, underground cleaning, mapping, and sampling. Following this program the Company intends to undertake a prefeasibility study on the project.

The Cerro Prieto North concession was acquired through direct application and lottery with the Department of Mines in July 2007. Oroco targeted this area as it was considered prospective for additional strike length of the regional structure hosting the Cerro Prieto Mine. This was confirmed through a limited exploration and sampling program in 2008 which returned channel sample assays as high as 2.8 g/t Au, 200 g/t Ag, 2.26 % Pb, and 3.17% Zn, from samples taken on a 300 meter outcrop of the structure on surface.

NI 43-101 Compliant Resource

The results of an independently calculated mineral resource estimate based on data from the Phase 1 exploration program were announced on January 27, 2009. With the completion of preliminary metallurgical testing demonstrating high percentage recoveries of gold and zinc the resource estimate was redefined and a restated resource estimate was issued on May 12, 2009.

Table 1. Cerro Prieto: Mineral Resource in Oxide Zone Using a 0.5 g/t Gold Cut-Off

Category

Tonnes

> Cut-Off

Au (g/t)

Ag (g/t)

Pb (%)

Zn (%)

Indicated

7,450,000

1.24

12.8

0.41

1.04

Inferred

140,000

0.99

11.2

0.73

1.98

The following table shows gross contained metal within the estimated resources from the tables above:

Table 2. Cerro Prieto: Contained Metal in Resource Oxide Zone Using a 0.5 g/t Gold Cut-off

Category Tonnes

Gold (ounces)

Silver (ounces)

Zinc (Million lbs)

Indicated

7,450,000

297,000

3,066,320

170.8

Inferred

140,000

4,500

50,400

6.1

Correlation coefficients and plots for the various elements indicate that, while overlapping, the higher grade gold and zinc zones are not completely correlated. As a result, the resource estimates using a gold cut-off do not include all higher grade zinc blocks. Therefore, Giroux has calculated separate resource estimates using a zinc cut-off as set out in the following tables As the zinc cut-off resource estimates contain many of the same blocks as included in the gold cut-off estimates, the zinc cut-off estimates should not be added to the gold cut-off resource estimates.

Table 3. Cerro Prieto: Mineral Resource Using a 0.5% Zinc Cut-off

Category

Tonnes > Cut-Off

Au (g/t)

Ag (g/t)

Pb (%)

Zn (%)

Indicated

20,440,000

0.43

8.7

0.38

1.2

Inferred

6,290,000

0.13

14.5

0.30

1.04

The following table shows gross contained metal within the estimated resources from the tables above.

Table 4. Cerro Prieto: Contained Metal in Resource Using a 0.5% Zinc Cut-off

Category

Tonnes

Gold (ounces)

Silver (ounces)

Zinc (Million lbs)

Indicated

20,440,000

282,600

5,717,400

540,597,100

Inferred

6,290,000

26,300

2,932,000

144,176,900

METALLURGY

The Company retained SGS de Mexico, S.A. de C.V. (“SGS”), under the direction of the Company’s consultant, Mr. Art Winckers of Arthur H. Winckers and Associates (“Winkers”) to conduct a preliminary metallurgical study on sample rejects from drill holes CP009 and CP019, two holes that are considered to be representative of the deposit.

SGS was asked to deliver results for precious metal extraction using a cyanide leach and for zinc extraction using a sulphuric acid leach. Highlights of the results of the tests include

Gold – using a grind size of 80% minus 200 mesh and a NaCN concentration of 3 g/l extracted an average of 91.5% of the gold and 35% of the silver over 6 tests in a 96 hour leach.

Gold – using the minus 10 mesh fraction and a 0.25 g/l sodium cyanide concentration on an overall composite sample resulted in 85% gold extraction and 19.7% silver extraction within less than 48 hours.

Zinc – using a grind size of 80% minus 200 mesh, and a sulphuric acid addition of 31 kg/t extracted an average of 64% of the zinc and 13% of the silver in a 6 hour leach. Winckers noted that the relatively low recovery was probably a result of the short leach time.

Zinc – using the minus 10 mesh fraction on an overall composite sample and a sulphuric acid addition of 35.8 kg/t resulted in an 85.3% zinc extraction and a 13.0% silver extraction within less than 72 hours.

Lead – lead was not recoverable above 10% in any of the tests attempted.

Winckers concluded that: “The results of these very preliminary leach tests are viewed as promising considering that high zinc and gold extractions were obtained with low lixiviant additions that are not considered to be optimized.”

The 85.3% zinc recovery using only 35.8 kg/t of sulphuric acid indicates the lack of problematic carbonate rock and silicate minerals in the Cerro Prieto Project. Most producing zinc oxide deposits are in carbonate hosts and many also contain zinc silicate minerals. As zinc is extracted using sulphuric acid, and carbonate rock neutralizes sulphuric acid, extraction of zinc in carbonate hosts requires either a very high amount of sulphuric acid (up to 200 kg/t) to digest both the carbonate and the zinc or a very costly alternative method to reduce the carbonate rock prior to extraction of the zinc. Zinc silicates are also difficult to extract requiring either very high rates of acid use or other, very costly, alternate techniques. The preliminary zinc extraction rates achieved indicate that zinc silicates are also not a problem in the Cerro Prieto mineralization.

Cerro Prieto Project: Mineralization

Polymetallic mineralization (consisting of gold, silver, lead, and zinc with strong indications of copper and molybdenum mineralization in the deepest holes) at the historical Cerro Prieto Mine is contained within a major regional shear zone traceable for a total strike length in excess of 10 kilometers, with approximately 6.5 km of strike length contained on Oroco’s concessions. This shear zone cuts all geological units from Jurassic to Lower Tertiary in age. Within this shear zone are contained hanging wall and footwall veins, secondary veins, breccia zones and stringer zones, which, where tested, produce continuous mineralized zone from approximately 10 m to in excess of 50 m thick.

At the mine site the geological structure strikes north 350° and dips from vertical to 80° to the east. Mineralization outcrops on surface across the entire length of the San Francisco and San Felix concessions, a distance of approximately 1.7 kilometers, and extends to below the lowest levels yet drill tested, over 400 meters below. It remains open at depth, to the north and to the south.

The Project is interpreted to be a strong epithermal mineralizing system, no older than Tertiary in age, signifying considerable additional depth potential below the deepest drill intercept.

Oxide mineralization has been intersected from surface to a depth of 400 meters with significant sulphide mineralization only intersected in hole CP011, the deepest drilled to date.

History

The Cerro Prieto Mine operated from 1906 with production reportedly between 500 and 720 tpd of gold and silver ore grading 3 to 15 g/ton Au and 50 to 60 g/ton Ag. Mining operations ceased in 1912 at the time of the Mexican Revolution and were never resumed. A number of factors, including the 1966 mining law requiring 51% Mexican ownership, prevented further mining in the 20th century. Companies conducting exploration programs from 1969 to 1999 issued consistent reports of mineralization at Cerro Prieto. In 1998 Morgain Minerals Inc. conducted a reverse circulation drill program of 23 holes and based on this drill program Morgain management estimated that within the area of drilling and detailed work there is a bulk underground resource* of 7,061,129 tons at an average gold equivalent grade of 4.40 g/ton and an open pit resource* of 1,391,000 with an average gold equivalent grade of 2.47 g/ton. (* any resource estimates referred to in this section are historical and as such, in accordance with NI 43-101, section 2.4 should be used only as an indicator of the potential of the property.

Highlights

300,000 OUNCE OXIDE GOLD RESOURCE OPEN ALONG STRIKE

100% OWNERSHIP INTEREST IN 70 SQ. KM (7,000 ha) OF CONCESSIONS CONTAINING UP TO 17.5 KM OF STRIKE LENGTH OF GEOLOGICAL STRUCTURE

CERRO PRIETO PURCHASE PRICE OF US $2.5 MILLION FULLY PAID

FAVOURABLE LOCATION AND MINING LAWS

OXIDE MINERALIZATION FROM SURFACE TO MAXIMUM DEPTH OF 350 METERS

PRELIMINARY METALURGY COMPLETE INDICATING GOOD RECOVERIES

POTENTIAL FOR LOW COST OPEN PIT MINE: PRELIMINARY MINING PLAN UNDERWAY

Summary

Concessions: San Francisco (15 hectares), San Felix (200 hectares), and Cerro Prieto North (2,508 hectares)

Ownership: Oroco owns a 100% interest in each of the three properties. The San Francisco and San Felix properties are subject to a 2% NSR. The Argonauta concession was optioned from Yamana Gold Inc. on May 11, 2009. The Option terms include the issuance of 500,000 common shares to Yamana upon signing of a formal option agreement, the completion of at least 1,500 meters of drilling on the Optioned Property before January 1, 2011, and the issuance of an additional 500,000 common shares to Yamana on or before January 1, 2011.Thereafter the property is 100% owned by Oroco, subject to a 2% net smelter return royalty payable to Yamana.

Location: Sonora State, Mexico, 135 kilometers north of state capital Hermosillo. The concessions cover land that is a privately owned cattle range land with no communities or residents. Access to the property is secured by agreement with the landowner. The nearest community of Cucurpe is 12 kilometres south. The regional center of Magdalena de Kino (population 40,000) is 27 kilometres northwest and is a one hour drive on mostly paved road.

Infrastructure: National Grid power lines and a paved road leading to the State’s major highway are each less than five kilometres from the property. Ground water is available on site and a river flows year round four kilometers south of the property. There are numerous nearby road and rail links to ports in the state of Sonora.

NI 43-101 Compliant Resource: The results of an independently calculated mineral resource estimate based on data from the Phase 1 exploration program were announced on January 27, 2009. With the completion of preliminary metallurgical testing demonstrating high percentage recoveries of gold and zinc the resource estimate was redefined and a restated resource estimate was issued on May 12, 2009.

The San Francisco and San Felix concessions were optioned in November of 2006 and the acquisition completed in March of 2008 with the payment of the full purchase price. Exploration commenced in April 2008 immediately following Oroco’s initial public offering. The objective of the Phase I exploration program was to confirm the historical resource reported in 1999 (which was based on a 23 hole reverse circulation drill program and an underground and surface sampling program, and to test for the potential to expand that resource. The historic, non-NI43-101 compliant resource was considered important as a guide to the potential of the property but the objective of the Phase I exploration program was to both confirm the historical resource and test the potential for the presence of a larger, bulk mineable zone of economic mineralization along strike, and at depth, where mineralization remained open and where the previous operator had not drilled nor reported a sampling program. That Phase I program was completed in October of 2008 with excellent results. The program consisted of a total of 5,975.1 meters of diamond drilling in twenty-four holes, trenching and sampling across the mineralized shear zone at 50 meter intervals, and mapping on surface. Twenty-two of the holes drilled intersected the mineralized zone with a true thickness ranging from ten meters to greater than fifty meters, with an average true thickness of approximately forty meters, while two drill holes were abandoned due to poor ground conditions before hitting the structure. Drilling has now been completed at 100 meter spacing along 600 meters of strike length to a maximum depth of 400 meters, allowing for an initial indicated resource and inferred resource to be calculated. In addition, a single drill hole drilled 300 meters along strike of intensive drilling intersected a strongly mineralized zone. Drilling, trenching, and mapping have now traced the mineralized structure for 1250 meters on surface to a maximum depth of 400 meters.

YAMANA OPTION

The 4,200 ha Argonauta concession was optioned from Yamana Gold Inc. on May 11, 2009. The Option terms include the issuance of 500,000 common shares to Yamana upon signing of a formal option agreement, the completion of at least 1,500 meters of drilling on the Optioned Property before January 1, 2011, and the issuance of an additional 500,000 common shares to Yamana on or before January 1, 2011.Thereafter the property is 100% owned by Oroco, subject to a 2% net smelter return royalty payable to Yamana.

The Optioned Property covers projected extensions to the north and south of the mineralized shear zone on the Company’s 100% owned Cerro Prieto project claims (“Cerro Prieto”) which host the recently announced estimated resource. The extensions total 9.2 kilometres and include 1.7 kilometres of projected strike length between Cerro Prieto and the Company’s 100% owned Cerro Prieto North claim (“CPN Claim”) and 7.5 kilometres to the south of Cerro Prieto.

To the north of the estimated resource, the Company has established the continuation of the Cerro Prieto mineralized zone to its northern boundary with the Optioned Property. In addition, the Company established what it believes to be the continuation of the mineralized zone on the CPN Claim with highly anomalous assays from samples taken over a series of outcrops of the mineralized zone along 400 metres of strike length (see the Company’s April 30, 2008 news release). Furthermore, Mexican government geologic maps identify the historical gold and silver La Tinaja mine on the projected mineralized zone on the Optioned Property approximately 450 metres north of CP023, the Company’s northernmost drill hole on Cerro Prieto. Consequently, the Company is of the opinion that the mineralized zone continues to the north on to the Optioned Property and possibly strikes to and through the CPN Claim.

To the south of Cerro Prieto, the Optioned Property covers a previously unexplored potential 7.5 kilometre extension of the mineralized shear zone. In total, Cerro Prieto, the CPN Claim and the Optioned Property cover a total potential strike length of the mineralized shear zone of 17.5 kilometres.

Diamond Drill Results – Table – Cross Sections

Trenching and Sampling Results – Plan View

At the completion of Oroco's Phase 1 exploration program at Cerro Prieto, Giroux Consultants Ltd. of Vancouver, an independent consulting firm specializing in resource and reserve calculations completed a resource calculation using information from 23 of the 24 holes completed by Oroco in 2008 (Drill hole CP023, considered a step out hole, was drilled on strike, 300 meters north of the area of drilling at 100 meter intervals, and intercepted a broad zone of well mineralized rock but data from this hole was not included in the resource calculation).

The results of an independently calculated mineral resource estimate based on data from the Phase 1 exploration program were announced on January 27, 2009. With the completion of preliminary metallurgical demonstrating high percentage recoveries of gold and zinc the resource estimate was redefined and a restated resource estimate was issued on May 12, 2009.

A Phase 2 drill program is planned for 2009 which will include drilling the strike length between this hole and the area of the initial resource calculation, where mineralization has also been confirmed by trenching and sampling on the outcropping structure, as well as drilling on strike north of this hole to the property boundary, as well as a detailed metallurgical study, an environmental study, underground cleaning, mapping, and sampling. Following this program the Company intends to undertake a prefeasibility study on the project.

The Cerro Prieto North concession was acquired through direct application and lottery with the Department of Mines in July 2007. Oroco targeted this area as it was considered prospective for additional strike length of the regional structure hosting the Cerro Prieto Mine. This was confirmed through a limited exploration and sampling program in 2008 which returned channel sample assays as high as 2.8 g/t Au, 200 g/t Ag, 2.26 % Pb, and 3.17% Zn, from samples taken on a 300 meter outcrop of the structure on surface.

NI 43-101 Compliant Resource

The results of an independently calculated mineral resource estimate based on data from the Phase 1 exploration program were announced on January 27, 2009. With the completion of preliminary metallurgical testing demonstrating high percentage recoveries of gold and zinc the resource estimate was redefined and a restated resource estimate was issued on May 12, 2009.

Table 1. Cerro Prieto: Mineral Resource in Oxide Zone Using a 0.5 g/t Gold Cut-Off

Category

Tonnes

> Cut-Off

Au (g/t)

Ag (g/t)

Pb (%)

Zn (%)

Indicated

7,450,000

1.24

12.8

0.41

1.04

Inferred

140,000

0.99

11.2

0.73

1.98

The following table shows gross contained metal within the estimated resources from the tables above:

Table 2. Cerro Prieto: Contained Metal in Resource Oxide Zone Using a 0.5 g/t Gold Cut-off

Category Tonnes

Gold (ounces)

Silver (ounces)

Zinc (Million lbs)

Indicated

7,450,000

297,000

3,066,320

170.8

Inferred

140,000

4,500

50,400

6.1

Correlation coefficients and plots for the various elements indicate that, while overlapping, the higher grade gold and zinc zones are not completely correlated. As a result, the resource estimates using a gold cut-off do not include all higher grade zinc blocks. Therefore, Giroux has calculated separate resource estimates using a zinc cut-off as set out in the following tables As the zinc cut-off resource estimates contain many of the same blocks as included in the gold cut-off estimates, the zinc cut-off estimates should not be added to the gold cut-off resource estimates.

Table 3. Cerro Prieto: Mineral Resource Using a 0.5% Zinc Cut-off

Category

Tonnes > Cut-Off

Au (g/t)

Ag (g/t)

Pb (%)

Zn (%)

Indicated

20,440,000

0.43

8.7

0.38

1.2

Inferred

6,290,000

0.13

14.5

0.30

1.04

The following table shows gross contained metal within the estimated resources from the tables above.

Table 4. Cerro Prieto: Contained Metal in Resource Using a 0.5% Zinc Cut-off

Category

Tonnes

Gold (ounces)

Silver (ounces)

Zinc (Million lbs)

Indicated

20,440,000

282,600

5,717,400

540,597,100

Inferred

6,290,000

26,300

2,932,000

144,176,900

METALLURGY

The Company retained SGS de Mexico, S.A. de C.V. (“SGS”), under the direction of the Company’s consultant, Mr. Art Winckers of Arthur H. Winckers and Associates (“Winkers”) to conduct a preliminary metallurgical study on sample rejects from drill holes CP009 and CP019, two holes that are considered to be representative of the deposit.

SGS was asked to deliver results for precious metal extraction using a cyanide leach and for zinc extraction using a sulphuric acid leach. Highlights of the results of the tests include

Gold – using a grind size of 80% minus 200 mesh and a NaCN concentration of 3 g/l extracted an average of 91.5% of the gold and 35% of the silver over 6 tests in a 96 hour leach.

Gold – using the minus 10 mesh fraction and a 0.25 g/l sodium cyanide concentration on an overall composite sample resulted in 85% gold extraction and 19.7% silver extraction within less than 48 hours.

Zinc – using a grind size of 80% minus 200 mesh, and a sulphuric acid addition of 31 kg/t extracted an average of 64% of the zinc and 13% of the silver in a 6 hour leach. Winckers noted that the relatively low recovery was probably a result of the short leach time.

Zinc – using the minus 10 mesh fraction on an overall composite sample and a sulphuric acid addition of 35.8 kg/t resulted in an 85.3% zinc extraction and a 13.0% silver extraction within less than 72 hours.

Lead – lead was not recoverable above 10% in any of the tests attempted.

Winckers concluded that: “The results of these very preliminary leach tests are viewed as promising considering that high zinc and gold extractions were obtained with low lixiviant additions that are not considered to be optimized.”

The 85.3% zinc recovery using only 35.8 kg/t of sulphuric acid indicates the lack of problematic carbonate rock and silicate minerals in the Cerro Prieto Project. Most producing zinc oxide deposits are in carbonate hosts and many also contain zinc silicate minerals. As zinc is extracted using sulphuric acid, and carbonate rock neutralizes sulphuric acid, extraction of zinc in carbonate hosts requires either a very high amount of sulphuric acid (up to 200 kg/t) to digest both the carbonate and the zinc or a very costly alternative method to reduce the carbonate rock prior to extraction of the zinc. Zinc silicates are also difficult to extract requiring either very high rates of acid use or other, very costly, alternate techniques. The preliminary zinc extraction rates achieved indicate that zinc silicates are also not a problem in the Cerro Prieto mineralization.

Cerro Prieto Project: Mineralization

Polymetallic mineralization (consisting of gold, silver, lead, and zinc with strong indications of copper and molybdenum mineralization in the deepest holes) at the historical Cerro Prieto Mine is contained within a major regional shear zone traceable for a total strike length in excess of 10 kilometers, with approximately 6.5 km of strike length contained on Oroco’s concessions. This shear zone cuts all geological units from Jurassic to Lower Tertiary in age. Within this shear zone are contained hanging wall and footwall veins, secondary veins, breccia zones and stringer zones, which, where tested, produce continuous mineralized zone from approximately 10 m to in excess of 50 m thick.

At the mine site the geological structure strikes north 350° and dips from vertical to 80° to the east. Mineralization outcrops on surface across the entire length of the San Francisco and San Felix concessions, a distance of approximately 1.7 kilometers, and extends to below the lowest levels yet drill tested, over 400 meters below. It remains open at depth, to the north and to the south.

The Project is interpreted to be a strong epithermal mineralizing system, no older than Tertiary in age, signifying considerable additional depth potential below the deepest drill intercept.

Oxide mineralization has been intersected from surface to a depth of 400 meters with significant sulphide mineralization only intersected in hole CP011, the deepest drilled to date.

History

The Cerro Prieto Mine operated from 1906 with production reportedly between 500 and 720 tpd of gold and silver ore grading 3 to 15 g/ton Au and 50 to 60 g/ton Ag. Mining operations ceased in 1912 at the time of the Mexican Revolution and were never resumed. A number of factors, including the 1966 mining law requiring 51% Mexican ownership, prevented further mining in the 20th century. Companies conducting exploration programs from 1969 to 1999 issued consistent reports of mineralization at Cerro Prieto. In 1998 Morgain Minerals Inc. conducted a reverse circulation drill program of 23 holes and based on this drill program Morgain management estimated that within the area of drilling and detailed work there is a bulk underground resource* of 7,061,129 tons at an average gold equivalent grade of 4.40 g/ton and an open pit resource* of 1,391,000 with an average gold equivalent grade of 2.47 g/ton. (* any resource estimates referred to in this section are historical and as such, in accordance with NI 43-101, section 2.4 should be used only as an indicator of the potential of the property.

Oroco Cerro Prieto Project Concession Map September 2009

CERRO PRIETO Drill Area Plan September 2009

Cerro Prieto Long Section Updated January 11, 2010

Cerro Prieto Long Section (infill Drilling) Jan. 2010 Oroco Rescource Corp

%20Jan.%202010%20Oroco%20Rescource%20Corp.jpg)

die Unternehmenspräsentation ist Topaktuell vom Januar 2010 !!!

http://www.orocoresourcecorp.com/pdf/Oroco%20Resource%20Corp…

http://www.orocoresourcecorp.com/pdf/Oroco%20Resource%20Corp…

zwar vom letzten Jahr aber ein guter Überblick!

Oroco Resources Compressed Timeline to Production

By James West

MidasLetter.com

Wednesday, June 24, 2009

We've seen a lot of junior mining companies come and go, but its seldom that we see one as focused as Oroco Resources Corp (TSX.V:OCO) when it comes to moving a prospective deposit quickly along the exploration process. Oroco has gone from Initial Public Offering in March last year to 43-101 resource calculation in just under a year and is aiming towards a production decision and the completion of a pre-feasibility study in under a year from now.

The National Instrument 43-101 compliant study concludes that work to date on the property has outlined an indicated resource of 7,450,000 tonnes with an average grade of 1,25 grams per tonne gold, 12.8 grams per tonne silver, and 1.02% zinc (297,000 ounces of gold) contained within a larger indicated resource of 25,250,000 tonnes with an average grade of 0.52 grams per tonne gold, 8.6 grams per tonne silver, 0.34% lead and 1.02% Zn and, in addition, a total inferred resource of 4,690,000 tonnes with an average grade of 0.17 grams per tonne gold, 19.4 grams per tonne silver, 0.37% lead and 1.20% Zn. Within the larger resource is contained 445,000 ounces of gold, 9.9 million ounces of silver, 742 million pounds of zinc, and 244 million pounds of lead.[/green]

The company drilled 22 holes on its 100% owned Cerro Prieto project in northern Sonora State, Mexico, and every single hole penetrated the target mineralized zone.

"We are excited about the success of the phase one exploration program and the rapid development of the resource at Cerro Prieto, said company president Ken Thorsen. "Given the geological modeling completed to date, we expect to drill more of the same during phase two."

In all, Oroco completed 5,975.1 meters of diamond drilling in 22 drill holes during Phase One exploration in 2008. Average drill hole spacing was approximately 100 meters and 600 meters of strike length were drilled at this spacing. Phase Two drilling will test an additional 1600 meters of strike where continuity of mineralization has been confirmed by a step out hole and trenching and strongly indicated by the presence of historical mining.

Oroco starts Phase 2 drilling this month, and has doubled the land position at Cerro Prieto through the acquisition of an additional 4,200 hectare block from Yaman Gold Inc. (TSX:YRI) The additional ground covers projected extensions to the north and south of the mineralized shear zone on Cerro Prieto, and total 9.2 kilometres and include 1.7 kilometres of projected strike length between Cerro Prieto and the Company's 100% owned Cerro Prieto North claim ("CPN Claim") and 7.5 kilometres to the south of Cerro Prieto. This brings the entire strike length to a potential18 kilometers.

Its no surprise to industry observers that the project is moving along so rapidly. The management team under the leadership of Ken Thorsen reads like a who's who of the mining industry, and not so much in terms of exploration as in experience putting mines into production.

Thorsen himself has 40 years experience in the mining business including 15 years as a student and field geologist with Selection Trust, three years with Saskatchewan Mining and Development Corporation (Cameco), 21 years with Teck Corporation (TSX, NYSE:TCK) and six years as a consultant. During this period, Thorsen was directly involved at the field level with the discovery of three ore bodies and at the management level with the discovery and development of three additional ore bodies. Prior to becoming a consultant in 2002, Thorsen worked in senior exploration management at Teck, including a two year period managing its world wide exploration as President of Teck Exploration Ltd.

The company's chairman, Stephen Leahy, doubles as CEO of TSX Venture Exchange-listed North American Tungsten, one of the world's largest producers of tungsten concentrate, a strategic industrial metal required in a wide variety of products ranging from jet turbine engines and high-speed cutting tools to electronic circuitry and surgical instruments.

Mexico is the world's second largest silver producer, and ranks 11th in terms of global copper production. The country's biggest gold mine, La Herradura in Sonora state is owned and operated as a joint venture between Newmont Mining (NYSE: NEM) and Mexican mining conglomerate Industrias Penoles.

Sonora State accounted for 24% of all mineral production in Mexico in 2006, and the proliferation of exploration and mining companies with offices in the state capital of Hermosillo are testimony to the prolific mineral potential of that part of the country. Oroco's Cerro Prieto lies 135 km north of Hermosillo.

National Grid power lines and a paved road leading to the State's major highway are each less than five kilometres from the property. Ground water is available on site and a river flows year round four kilometers south of the property. There are numerous nearby road and rail links to ports in the state of Sonora. The project is being modeled as an open pit, heap leach gold producer, with significant silver and zinc credits. Mining costs at comparable operations in Sonora run well under $5 per tonne and Oroco's average grade of 1.24 grams per tonne gold put it at the high end of the range when compared to other resources being mined or slated to be mined in the region.

Oroco is currently closing a recently announced private placement financing of CA$1.2 million, and so the company is well capitalized to execute the phase 2 drill program now underway.

Although currently focused intently on advancing the Cerro Prieto deposit, the company also holds a 100% stake in two contiguous mineral concessions in Guerrero, Mexico; Celia Generosa and Celia Gene, totaling 193 hectares and together called the Xochipala Project.

According to a report issued in 1997 by geologist Tawn Albinson, "The Xochipala claims cover ground in the Guerrero Gold Belt sufficient to potentially generate reserves greater than 1 million ounces gold in ore bodies similar to the productive high-grade ore bodies that have been discovered in the past within the region."

The Xochipala Project is located in the southeast extreme of the original Morelos National Mining Reserve, a 49,400 ha federal mineral reserve which includes the most promising and expanding gold reserves in Mexico. This region encompasses a northwest trend of intrusions with associated gold bearing iron skarn deposits and is part of a wider area which has come to be known as the Guerrero Gold Belt (the "GGB").

The GGB is currently the focus of aggressive exploration, delineation, development, and mining by Canadian and Mexican majors. Teck Cominco, Goldcorp and Grupo Mexico are exploring and delineating gold reserves in the GGB and to date have discovered in excess of 12 million ounces of gold.

Oroco currently has just over 27 million shares outstanding. Follow the company's progress at www.orocoresourcecorp.com.

SOURCE: http://www.midasletter.com/news/09062406_Oroco-resources-com…

Oroco Resources Compressed Timeline to Production

By James West

MidasLetter.com

Wednesday, June 24, 2009